encana cenovus financial analysis

DESCRIPTION

This is Encana Cenovus Financial Analysis and a comparison of both the companies Advanced Corporate FinanceTRANSCRIPT

i

FINE6150: Forecasting Assignment

Analysis of the Encana Corporation Spin-off of Cenovus Energy

Prepared for: Prof. Karen Chiykowski

2

Table of Contents

Executive Summary...................................................................................................................................... iIndustry Overview.......................................................................................................................................1EnCana Corporation: Company Overview...................................................................................................2EnCana Corp: Capital Structure, Dividend Policy, Share Structure..............................................................2EV/EBITDA Comparison...............................................................................................................................2Cenovus Spin-off Time Line.........................................................................................................................3Rationale for Spinoff....................................................................................................................................3Reorganization............................................................................................................................................5

Assets to EnCana (GasCo)........................................................................................................................5Assets to Cenovus (IOCo).........................................................................................................................5

Balance Sheet......................................................................................................................................6Deal Structure..............................................................................................................................................6

Share value..............................................................................................................................................7Announcement – May 2008....................................................................................................................7Proceeding with Spin off – September 10, 2009......................................................................................7Shareholder value estimates – September 10, 2009...............................................................................7

Multiples..............................................................................................................................................7Discounted Cash Flow..........................................................................................................................8

Actual Trading post split up – Dec 3, 2009...............................................................................................8Post Spin-off Performance...........................................................................................................................8Share price performance after Spin-off.......................................................................................................9Conclusion – did it create value.................................................................................................................10Appendices................................................................................................................................................11

Appendix A: Porter 5 Forces and Industry Risk Assessment..................................................................11Appendix B: Encana Corporation Capital Structure Summary...............................................................12Appendix C: EnCana and Cenovus Dividend Policy Review....................................................................12Appendix D: Share Ownership at Announcement.................................................................................13Appendix E: EnCana Valuation Analysis.................................................................................................15Appendix F: Benefits of the Spin-off......................................................................................................16Appendix G: Location of assets to EnCana (GasCo)...............................................................................17Appendix H: EnCana (Pre-Spin-off) Value chain.....................................................................................18Appendix I: Location of assets to Cenovus (IOCo)..................................................................................19Appendix I: Location of assets to Cenovus (IOCo)..................................................................................19Appendix J: Breakup of Encana balance sheet into Encana and Cenovus..............................................20Appendix K: Breakdown of shareholder value in May 2008..................................................................21Appendix L: Proceeding with Spin-off in September 10, 2009...............................................................22Appendix M: Shareholder value estimates – September 10, 2009........................................................23

Multiples Approach...........................................................................................................................23DCF Approach....................................................................................................................................27

Appendix X: Actual Trading post split up - Dec 3, 2009.........................................................................30Appendix X: Encana business unit performance....................................................................................31Appendix X: Cenovus business unit performance..................................................................................31Appendix X: Consolidated Financial Performance Post Split.................................................................32

3

Appendix X: Combined post-split firm trading values does not demonstrate much change in shareholder value..................................................................................................................................33Appendix X: The TSX has outperformed the combined firms since the split in 2009.............................34Appendix X: Monthly total returns of the independent firms are less volatile THIS IS MARGINAL, remove/restate.....................................................................................................................................35

References.................................................................................................................................................36

i

Executive Summary

EXEC SUMMARY HERE

1

Industry Overview

The Oil & Gas Industry in North America in 2008 was riding an all-time high, driven by soaring

commodity prices. (1) In addition, all indications are that the industry will continue to grow based on

international demand for oil and domestic demand for natural gas. (1) These high commodity prices are

driving producers to consider previously commercially unviable reserves, such as shale gas. In the

natural gas market, it is expected (in 2009) that the growing demand will outplace the massive reserves

that shale gas represents.

Given the intense capital investment nature of the industry, the sector is dominated by large

international firms. In North America, a small group of large scale producers lead the market including:

EnCana, Exxon Mobile and Imperial Oil. (1) In addition to the large leaders, the market is populated by

second tier players. Despite the varying size of the firms in the industry, there is one truth in the

industry that profitability is tied back to reserves quality and production rates. (1)

The industry structure is described via a Porter 5 forces in Appendix A. However, the highlights

of this analysis show that there is a high degree of rivalry within the industry (due to the fact that firms

must constantly seek out new reserves) and a low threat of new entrants (due to the intense capital

investments required).

Lastly, a high-level industry risk assessment is presented in Appendix A. Although the industry is

rife with potential risks, the single biggest external determinant of risk is commodity pricing. (1) Swings

in commodity prices can have massive impacts on the profitability of the firms within the industry. This

is an especially concerning issue, as the firms have little to no ability to offset this risk, given the massive

capital outlays required to get reserves to the production phase. Firms are typically required to run

production when a site reaches maturity, independent of commodity pricing, with output only being

controlled. (1)

EnCana Corporation: Company Overview

Company details – Sean

2

EnCana Corp: Capital Structure, Dividend Policy, Share Structure

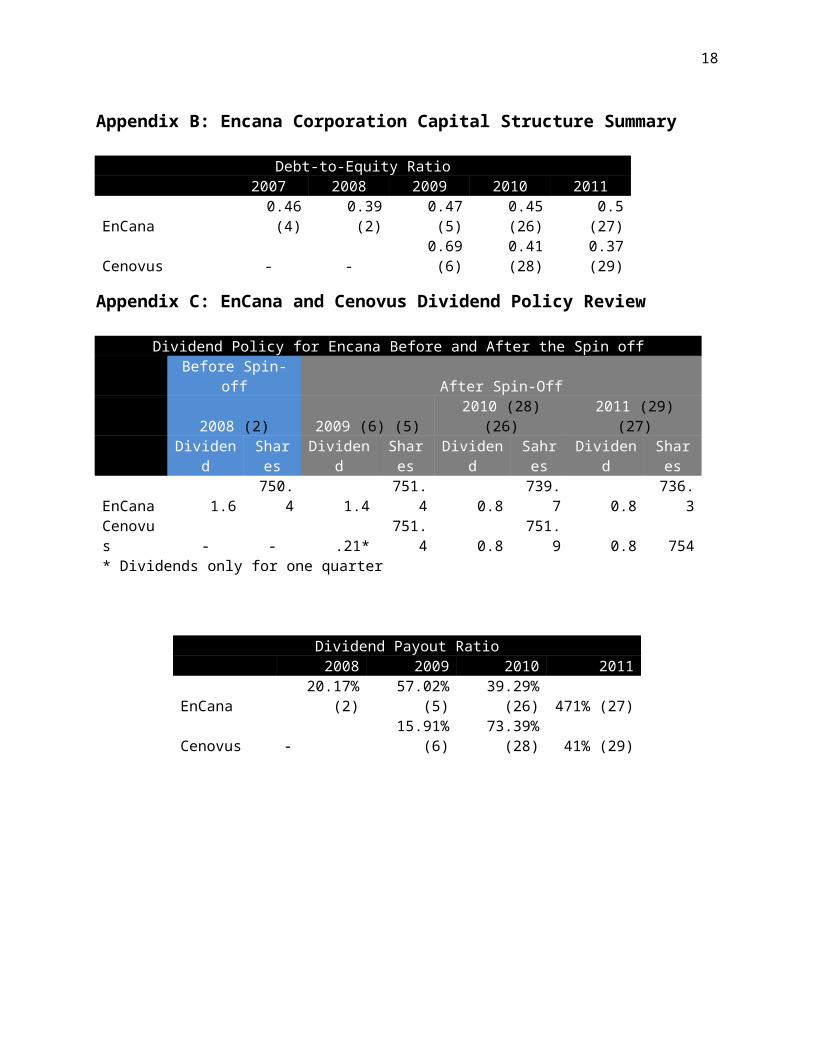

Prior to the spin-off Encana Corp. had a debt-to-equity ratio of 0.46 (2)and a targeted net debt-

to-capitalization ratio of between 30 and 40 percent and a net debt to adjusted EBITDA of 1.0 to 2.0

times at the time of the announcement of the spin-off. (3)

In 2008, prior to the Cenovus spin-off Encana paid a dividend of $1.60/share. (4) This was in-

line with the dividend payout for 2007 (4), however EnCana has stated consistently that it would flex

dividends to maintain the desired capital structure (5). Reviewing the Dividend ratio (Appendix B), it

appears that despite the statements in the annual reports to the contrary, EnCana was trying to

maintain a consistent dividend/share.

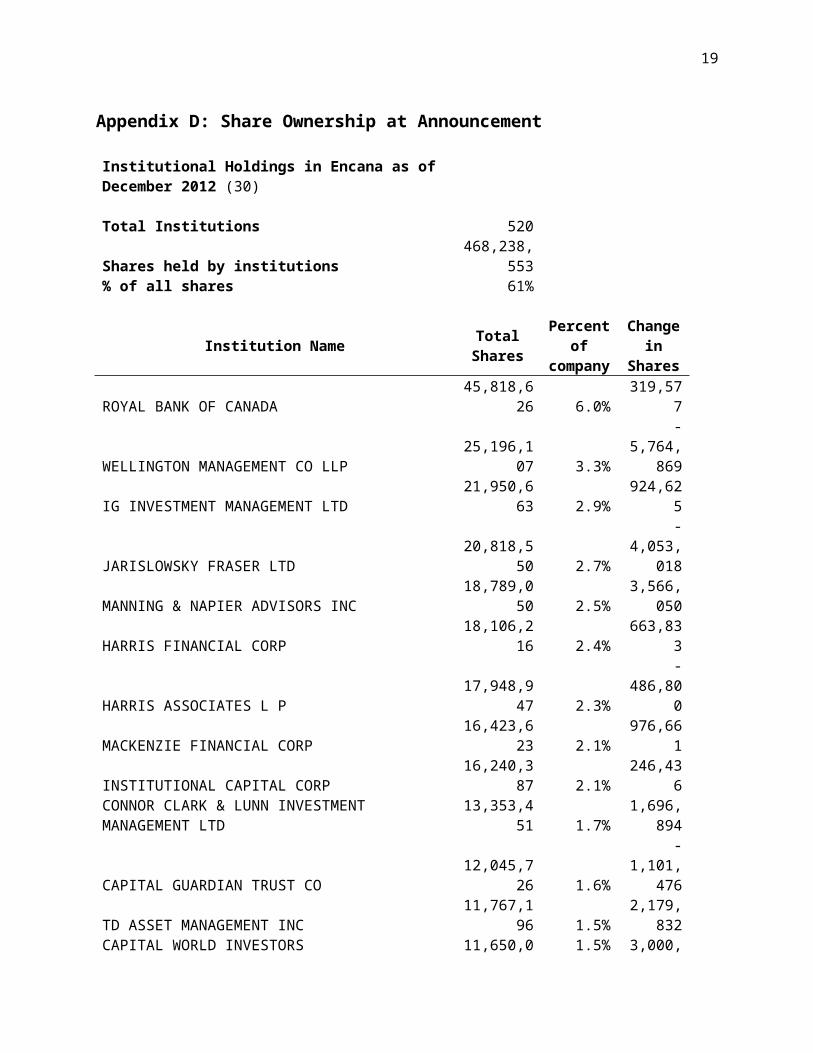

At the time the spin-off was announced, EnCana only had a single share class and hence all

shares were voting shares. (6) No information is available regarding who owned shares at the time of

the transaction, but as the issue was never raised in the press, it is assumed that it was widely held, as it

was in 2012 and 2010 (Appendix D). In addition, in reviewing the notes of the 2008 and 2007 annual

report, no risks associated with a majority shareholder or controlling interest was highlighted. (2) (4)

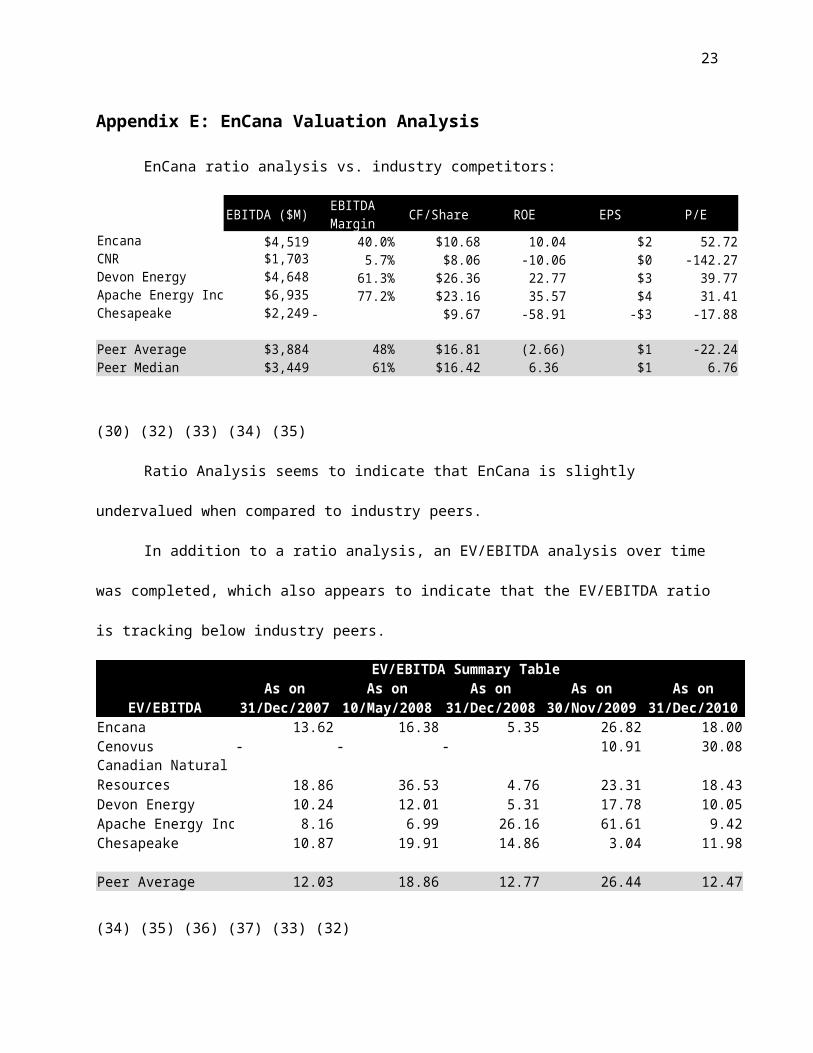

EV/EBITDA Comparison

NEEDS WORK

At the time of the announcement of the deal the Encana shares were underpriced with a

EV/EBITDA valuation of 16.38 as compared to 18.86 for its peers. And the multiple further plummeted to

5.35 as compared to its peers multiple of 1.277 as of Dec-2008. We calculated the EV/EBITDA multiple

for 2009 till 2011 and found that significant value was realized for both the new entities. The Encana,

had a EV/EBITDA multiple of 91.69 in 2011 (but this was primarily due to an impairment of $1 billion in

the year 2011, but even if we consider the impairment into consideration the multiple stands at 21.91)

and Cenovus had the EV/EBITDA multiple of 18.99. The EV/EBITDA multiple for the peers was 8.55 for

the year 2011.

3

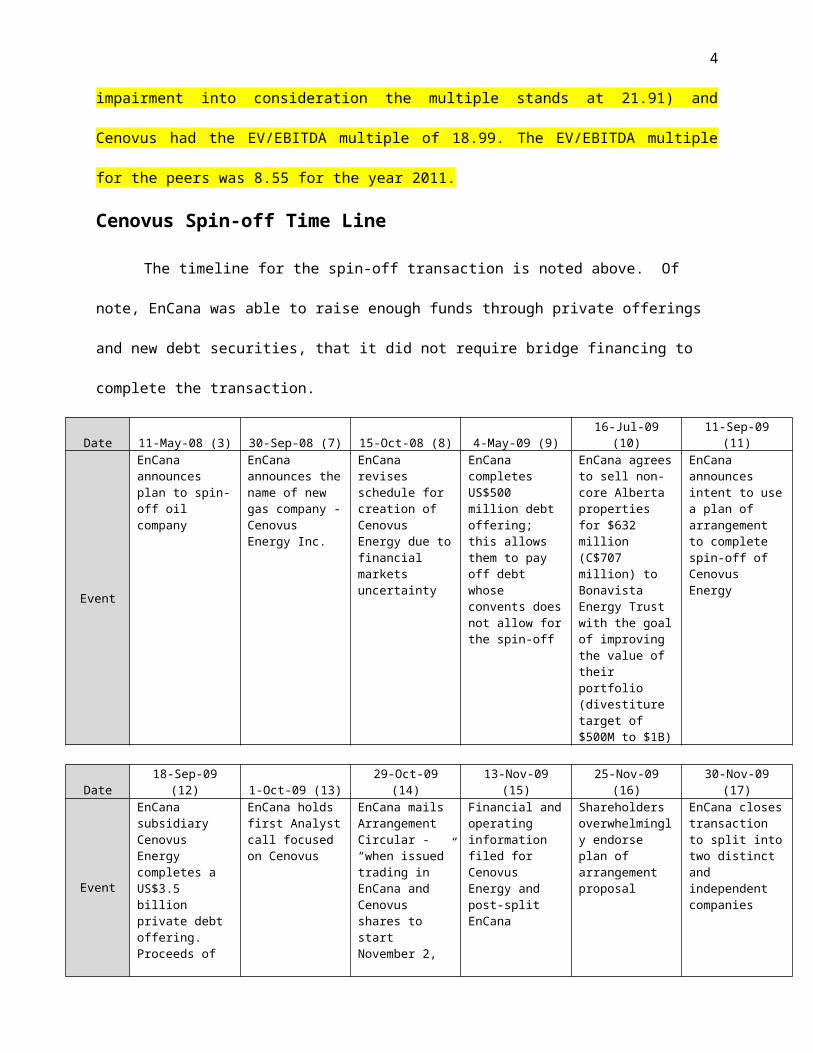

Cenovus Spin-off Time Line

The timeline for the spin-off transaction is noted above. Of note, EnCana was able to raise

enough funds through private offerings and new debt securities, that it did not require bridge financing

to complete the transaction.

Date 11-May-08 (3) 30-Sep-08 (7) 15-Oct-08 (8) 4-May-09 (9) 16-Jul-09 (10) 11-Sep-09 (11)

Event

EnCana announces plan to spin-off oil company

EnCana announces the name of new gas company - Cenovus Energy Inc.

EnCana revises schedule for creation of Cenovus Energy due to financial markets uncertainty

EnCana completes US$500 million debt offering; this allows them to pay off debt whose convents does not allow for the spin-off

EnCana agrees to sell non-core Alberta properties for $632 million (C$707 million) to Bonavista Energy Trust with the goal of improving the value of their portfolio (divestiture target of $500M to $1B)

EnCana announces intent to use a plan of arrangement to complete spin-off of Cenovus Energy

Date 18-Sep-09 (12) 1-Oct-09 (13) 29-Oct-09 (14) 13-Nov-09 (15) 25-Nov-09 (16) 30-Nov-09 (17)

Event

EnCana subsidiary Cenovus Energy completes a US$3.5 billion private debt offering. Proceeds of the private offering will eliminate the need for the US$3 billion bridge credit facility.

EnCana holds first Analyst call focused on Cenovus

EnCana mails Arrangement Circular - “when issued” trading in EnCana and Cenovus shares to start November 2, 2009

Financial and operating information filed for Cenovus Energy and post-split EnCana

Shareholders overwhelmingly endorse plan of arrangement proposal

EnCana closes transaction to split into two distinct and independent companies

Rationale for Spinoff

EnCana spun-off Cenovus with the goal of creating value of shareholders. By creating two

independent companies, each with its own management and strategies best suited for its operations,

the ability to increase the shareholder value was maximized (3). The general thesis behind this value

creation relates to the underlying assets of the firm, specifically the properties. When the spin-off was

proposed, EnCana owned two distinct set of assets: 1) unconventional gas reserves, such as shale

reserves, which are much harder to develop into production capable sites 2) Conventional gas and oil

4

(both on shore and offshore) reserves and oil refineries (18). The basic logic behind the spin-off was that

in order to maximize the return on these assets, there needed to be different operating practices,

different capital management practices and focus from management. This rationale is supported by the

fact Natural gas is a North American continental market business, with limited shipments overseas. (19)

There is considerable price volatility in the business as unconventional sources of North American gas

may be realized in the near future, driving down prices. (20) In contrast, the Canadian oil sands are a

relatively stable resource with well defined reserves. Price is also a major point of uncertainty, but unlike

with gas there is no source of oil that may enter the market at a lower price point – price is primarily a

factor of demand. (21) The oil sands also have a better established international distribution network. It

was felt that the only way to achieve this result was through a spin-off (more akin to a split) of the

company.

The spin-off would result in EnCana focusing on unconventional Natural gas reserve

development, while a new firm (eventually named Cenovus) would focus on oil (offshore as well as oil

sands) and traditional gas reserves. These two firms would be lead by EnCana’s existing CEO and CFO

respectively. (3)

Lastly, the spin-off would offer Encana stakeholders several advantages. First, shareholders

could elect to own the business and the risks that suited them, instead of accepting both the business

model risks at once. The division also removed transfer pricing issues, as the oil sands are a major user

of natural gas in the production process.

Based on the general rationale that the EnCana assets had a lot of value and that the firm was

somewhat undervalued, when compared to industry peers, the most logical course of action was a spin-

off or to stay the course. Selling off any assets, when management believed the firm was undervalued,

would not result in a fair valuation from management’s perspective.

Lastly, a series of additional supporting arguments for a spin-off are presented in Appendix F.

5

Reorganization

The parent EnCana was divided along the operational lines to have minimal impact to the

employees, suppliers, stakeholders and day-to-day operations. Under the proposed transaction,

EnCana’s Integrated Oil Division and Canadian Plains Division will become IOCo. GasCo will contain the

Canadian Foothills Division, the USA Division, the Offshore & International Division and the midstream

assets. (3)

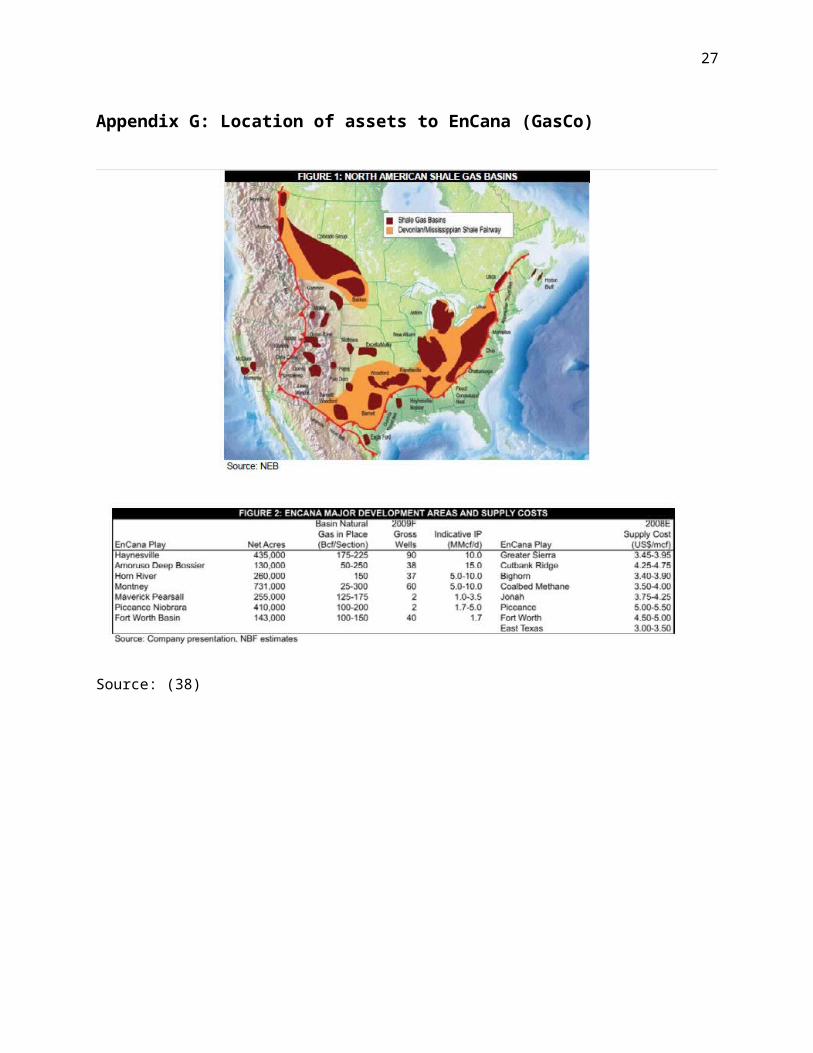

Assets to EnCana (GasCo)

GasCo will represent about two-thirds of parent EnCana’s current production and proved

reserves (11). Parent EnCana’s major operating divisions, Canadian Foothills and USA, were retained to

form a pure-play natural gas company, aimed at growing existing high-potential resource plays in

Canada and the United States (3). GasCo has a portfolio of current and emerging resource plays in key

basins in Alberta, British Columbia, Wyoming, Colorado, Texas, Louisiana and offshore Nova Scotia

(Appendix X). GasCo will hold the company’s portfolio of prolific gas resource plays: CBM (coalbed

methane) and Bighorn in Alberta, Cutbank Ridge and Greater Sierra in British Columbia, Jonah in

Wyoming, Piceance in Colorado and Fort Worth and East Texas in Texas (3). GasCo also achieved some

promising exploration results in a number of North American shale plays, such as Horn River in British

Columbia and the Haynesville shale in Louisiana, plus the Mannville CBM play in central Alberta, and

these plays have the potential to add significant depth to the company’s strong portfolio of natural gas

assets (3).

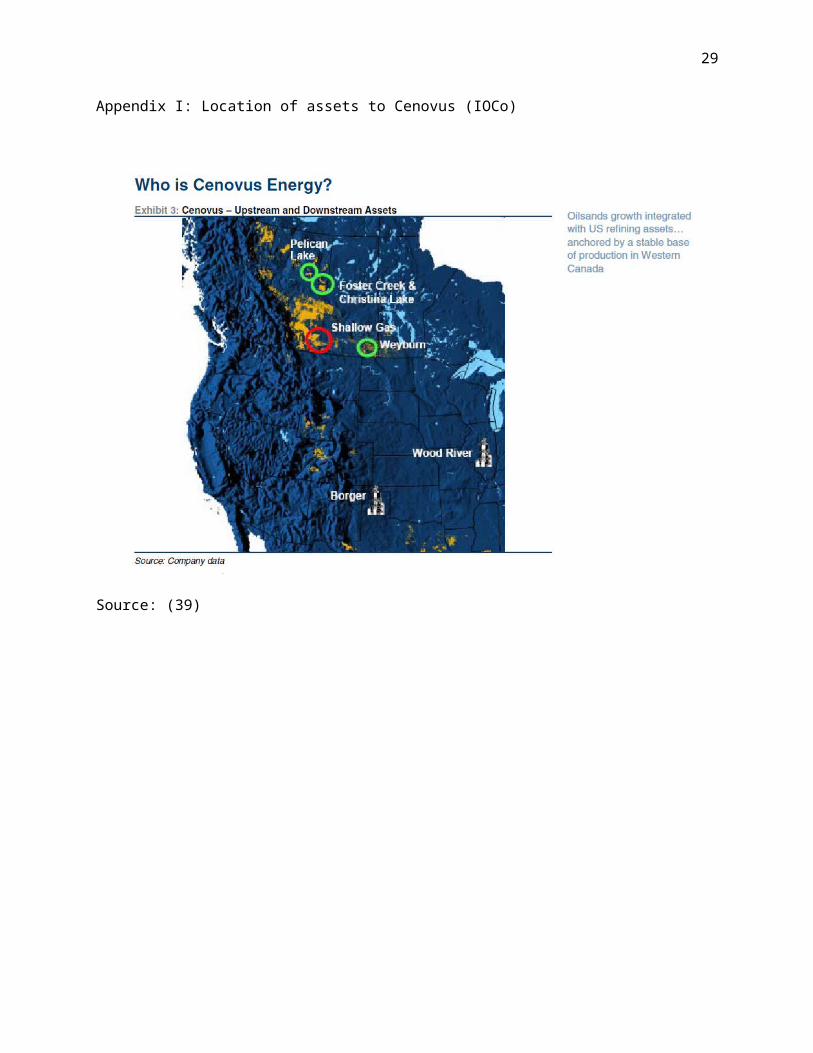

Assets to Cenovus (IOCo)

Cenovus’s assets contain parent EnCana’s Integrated Oil and Canadian Plains divisions and represent about

one third of EnCana’s current production and proved reserves (11). Assets were transferred to Cenovus with a

focus on the development of parent EnCana’s Canadian oil sands assets and refinery interests in the United

States, supported by a natural gas and oil production base in Alberta and Saskatchewan. Cenovus will also

capture the benefits of the full value chain (Appendix X) through EnCana’s integration of two producing

upstream Alberta oil sands assets – Foster Creek and Christina Lake, and two top-performing refineries at

6

Wood River in Illinois and Borger in Texas (Appendix X) (11). Cenovus’s assets will also include successful

enhanced oil developments at Pelican Lake in northern Alberta (3).

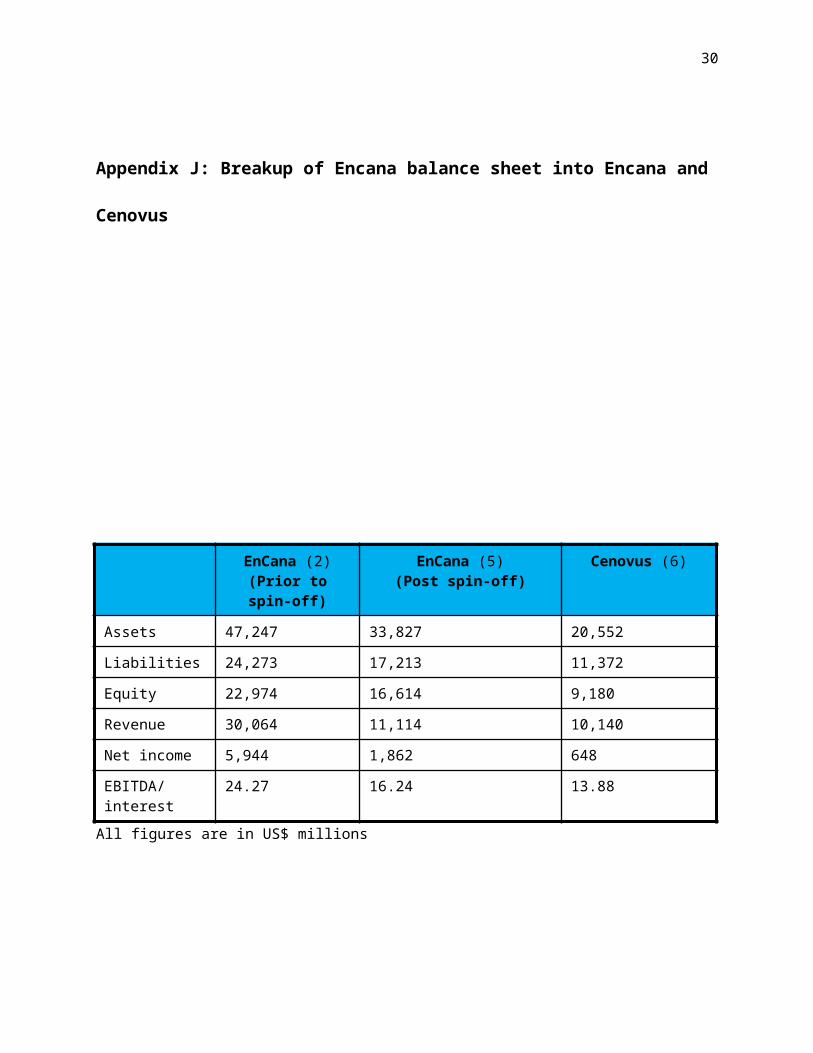

Balance Sheet

Depicting the above asset transfer in dollar values indicate that the parent company prior to transfer

had total assets worth $47.25B (2). Post split up EnCana retained $33.8B (5) worth of assets and $20.6B

(6) was transferred to Cenovus (Appendix X). The slight increase in the values of the assets for EnCana

was due to the cash ($3.5B) (11) received from the sale of its oil sands asset to Cenovus while a portion

of the goodwill was transferred from EnCana to Cenovus. The increase in asset base for Cenovus was

due to the step up in upstream and downstream refineries cost ($2.3B) (6).

Deal Structure

Under the Split Transaction, EnCana shareholders received one new EnCana Common Share and one

EnCana Special Share in exchange for each EnCana Common Share previously held (5). The book value of

EnCana's outstanding Common Shares immediately prior to the Split Transaction was attributed to the

new EnCana Common Shares and the EnCana Special Shares in direct proportion to the weighted

average trading price of the shares on a "when issued" basis. The value attributed to the new EnCana

Common Shares and the EnCana Special Shares was $2,360 million and $2,222 million, respectively (5).

The EnCana Special Shares were subsequently exchanged by EnCana shareholders for Common Shares

of Cenovus, thereby effecting the Split Transaction (5). Also, a committed and fully underwritten $3

billion non-revolving, 364-day, bridge financing was obtained from RBC Capital Markets to partially fund

the approximately $3.5 billion amount to be paid by Cenovus to EnCana to acquire the Cenovus assets

under the transaction (18). The Split Transaction reduced EnCana’s total Shareholders’ Equity due to a

reduction in Share capital of $2,222 million, a reduction in Retained earnings of $4,902 million and a

reduction in Accumulated other comprehensive income of $2,096 million. However, EnCana received

amounts due from Cenovus and invested the net proceeds of approximately $3.75 billion in short-term

marketable securities (5).

7

Share value

Announcement – May 2008

At the time of announcement in May, 2008, the closing share price of EnCana was $85.93. Owing to the

uncertainty and volatility of the global financial markets, EnCana decided to delay the spin off until clear

signs of stabilization returned to financial markets (8).

Proceeding with Spin off – September 10, 2009

Prior to the split up in September 2009, each shareholder who owned a share of parent EnCana would

have received $55.03 per share based on the closing share price of EnCana on Sept 10, 2009 ( Appendix

X). The drop in price was primarily due to the depressed state of the financial markets.

Shareholder value estimates – September 10, 2009

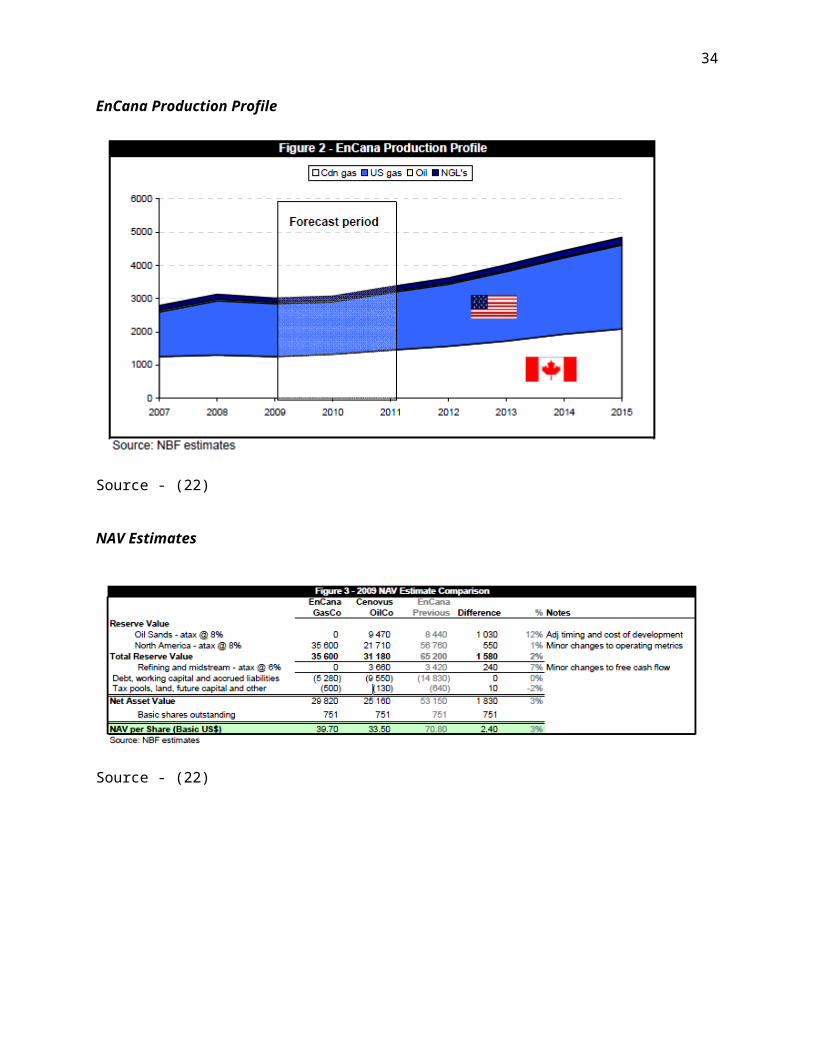

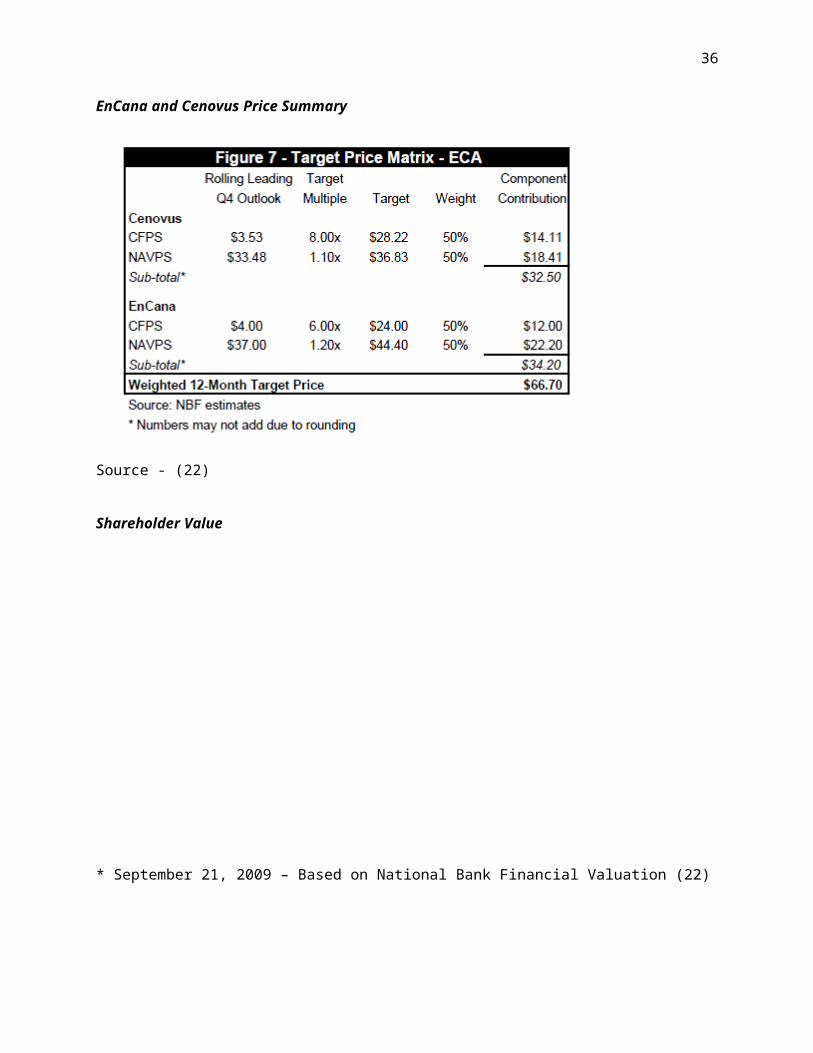

Multiples

National Bank Financial (22) estimated the share value of Cenovus and EnCana based on the Cash flow

method and the NAV method. An Equal weight of 50% was used and per share value was determined

based on comparable multiples. EnCana was valued at 6.0x Cash Flows and a P/NAV multiple of 1.2x was

used. Based on the two multiples, the par share price of EnCana was estimated to be $34.20. To further

account for valuation uncertainty, an additional discount of 0.7xNAV was factored and hence EnCana’s

share price was determined to be $27.54/share (Appendix X). Cenovus was valued using a P/CF multiple

of 8x and a P/NAV multiple of 1.10x. After accounting for valuation uncertainty (additional discount of

0.9xNAV), per share value of Cenovus was determined to be $30/share (Appendix X).

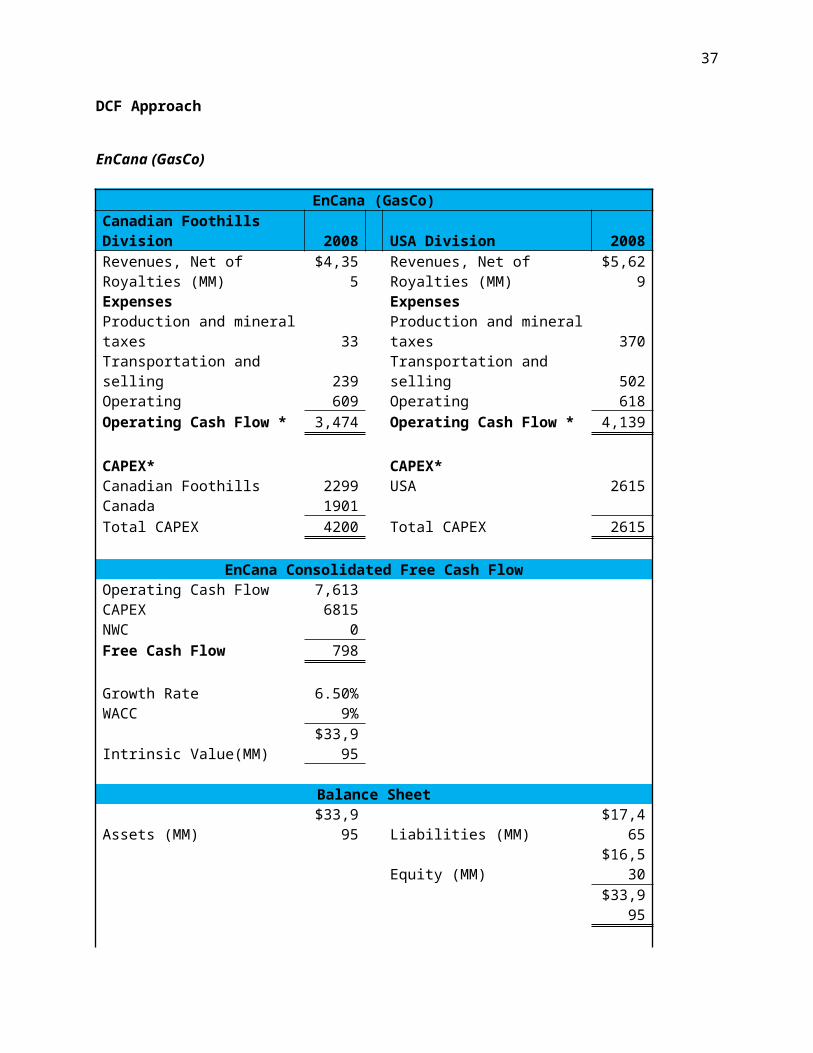

Discounted Cash Flow

A DCF analysis was performed based on the cash flows generated by operations transferred to Cenovus

and the operations retained by EnCana. The consolidated Free Cash flow based on operating cash flows

and necessary CAPEX for the Canadian Foothills division and USA division, both parts of EnCana (GasCo)

was $798MM (Appendix X). At an adjusted estimated growth rate of 6.50% (11) and WACC of 9% (23),

8

the intrinsic value was determined to be $33,395MM. After accounting for liabilities ($17,465MM), the

per share price of EnCana was determined to be $22 (Appendix X).

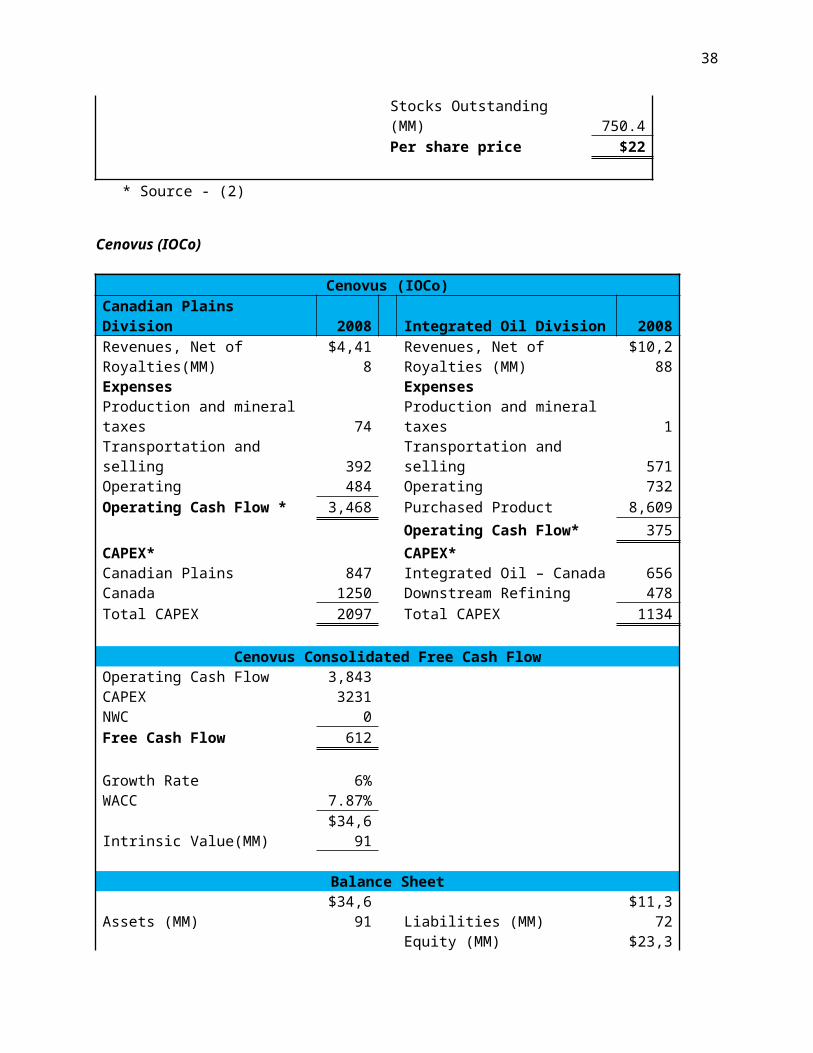

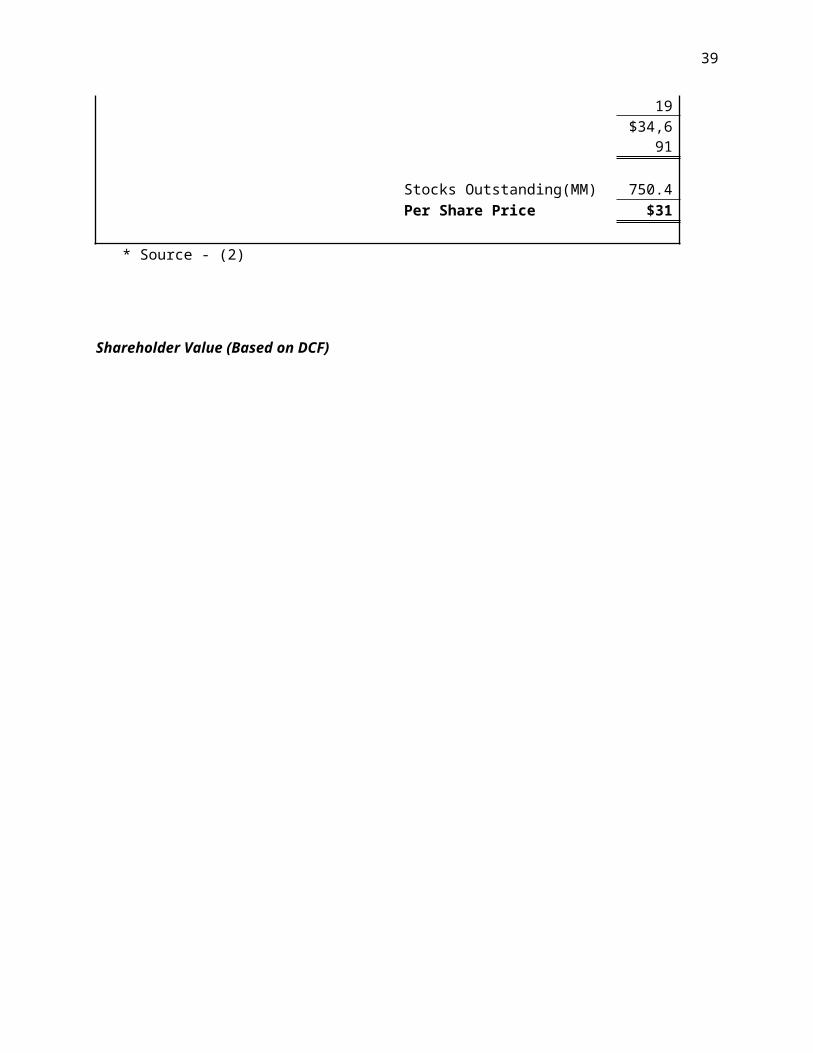

The consolidated Free Cash flow based on operating cash flows and necessary CAPEX for the Canadian

Plains division and Integrated Oil division, both parts of Cenovus (IOCo) was $612MM (Appendix X). At

an adjusted estimated growth rate of 6% (11) and WACC of 7.87% (24), the intrinsic value was

determined to be $34,691MM. After accounting for liabilities ($11,372MM), the per share price of

EnCana was determined to be $31 (Appendix X).

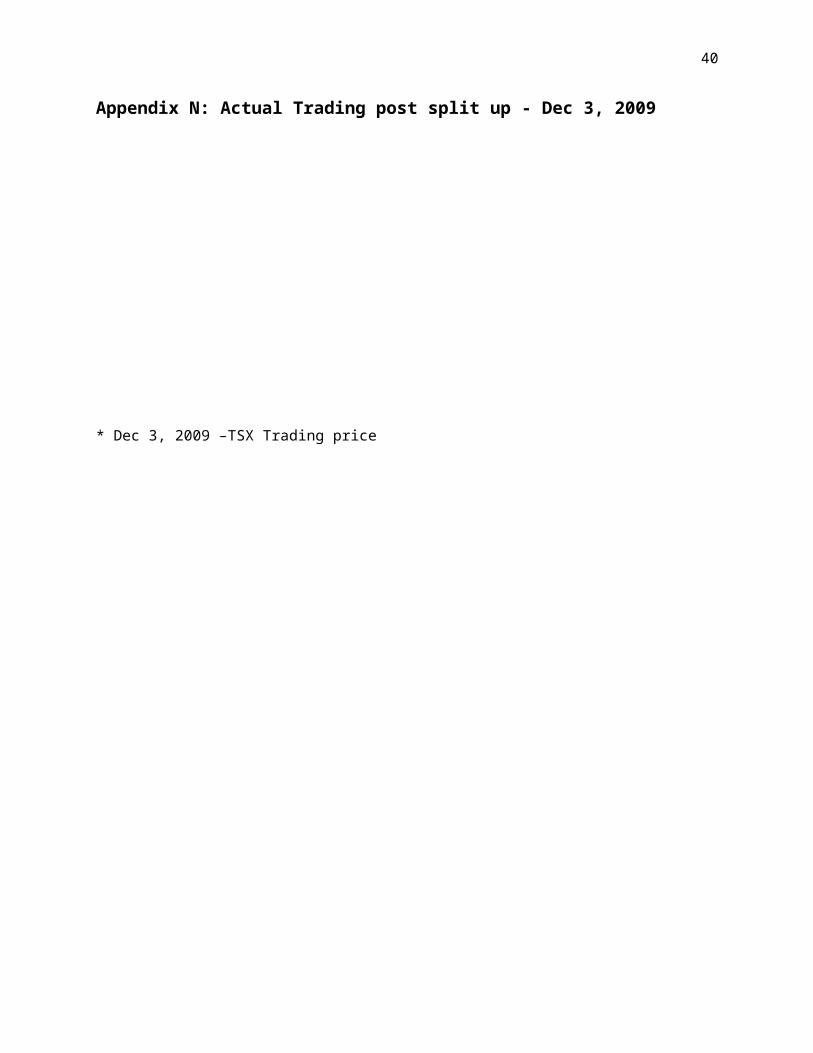

Actual Trading post split up – Dec 3, 2009

The stock price of the spun off companies did not appreciate much and the share price of EnCana was

$29.40/share and the share price of Cenovus was $26.75/share (Appendix X). The aggregated value to

share holder was $56.15 which was a meager 1.02% increase from $55.03 (as of September 10, 2009),

indicating that the market was expecting the split up for quite some time and factored in the price

already.

Post Spin-off Performance

On December 1, 2009 EnCana split into two companies. Post split, the two new companies appear to be

on different business trajectories. After a significant decline from 2008-2009, Encana revenues have not

made a major recovery, stalling at $8,467 in 2011, a 37% decline since 2008. Net income has also

dropped, with a corresponding decrease in profit margin. (Appendix X)

In contrast, Cenovus has experienced a faster revenue rebound, with 2011 revenue nearly back up to

levels that were experienced in 2008 for the operating units that would be spun off into Cenovus in

2009. Net income has also shown positive growth, although profit margin is lower than before.

(Appendix X)

Operational improvements from divesting unrelated businesses, such as Encana and Canovus, are often

cited as reasons for a divestiture. Based on a consolidated view of the two resulting companies, there is

9

little evidence of operational improvements from the split outweighing overall economic effects that

have occurred over time.

Revenue, driven by gains in the Cenovus component of the consolidated performance of the two firms,

is approaching the high water revenue mark set by the old Encana in 2008, indicating increased

performance as well as a potentially improving economic climate. However, expenses associated with

recovering resources and selling them have risen faster. Profit margin for the consolidated reports of

Encana and Canovus are still well below those reported before the 2009 split.

Balance sheet performance appears stable, with the two separate firms not making significant changes

to operating components of the business now that they have parted ways. Long term debt to equity or

long term asset ratios are both stable, indicating that capital structure, on the aggregate, has not

significantly changed. (Appendix X)

A loan payable of $3,750 payable to Encana was placed on Cenovus’ balance sheet upon separation. This

was paid in the same year, 2009. (6) There appears to be no ongoing relationship between the two

companies. Not 100% why this was done

Share price performance after Spin-off

The Encana – Cenovus split was handled by exchanging each share of Old Encana for one share each of

New Encana and Cenovus. This had the effect of significantly decreasing the share price of Encana, from

about $60 per share, which kept its ticker symbol, to about $30 per share. Cenovus began trading at

about $28 dollars per share, valuing the combined entities at approximately $58, similar to the

combined company’s previous level.

Based on the evolution of the companies’ share price since the split, the split of the two firms does not

appear to have increased shareholder value. On March 1st, 2013, the combined value of an Encana and

Cenovus share was $51.06, a decline of nearly $10 since just before the split.

10

Since the split, Encana has trended downwards, falling to a share price of $18.32 on March 1 st, 2013 and

significantly underperforming the TSX Index. Cenovus, on the other hand, has improved in value, rising

to $32.74 on March 1st, 2013.

On a consolidated basis, a shareholder of Encana just before the split would have slightly

underperformed the TSX as of March 1st, 2013. Indexed to 100 as of December 2nd, 2009, the TSX would

stand at 108.4 on March 1st while the pre-split Encana shareholder would hold an indexed value of 90.5.

This represents a loss over the period of 14.9% percent. Inclusive of dividends, representing a total

return perspective, the loss falls to 6.0%.

Is there a relative valuation story?

Conclusion – did it create value

text

11

Appendices

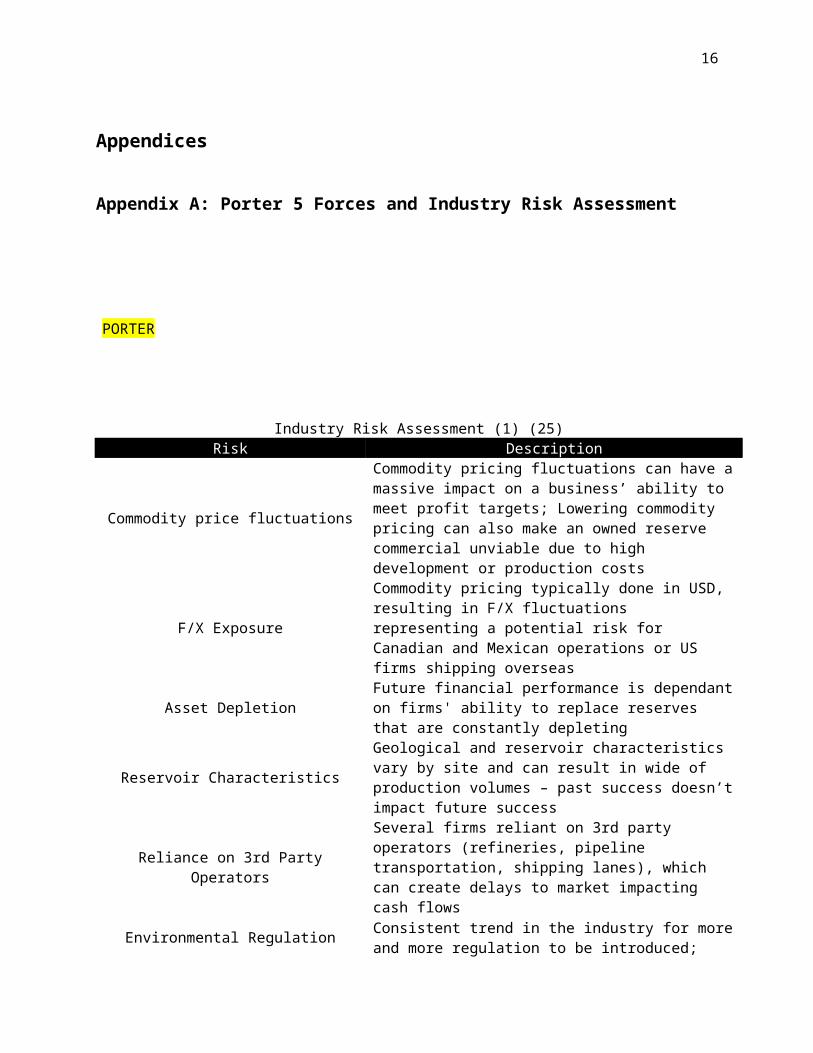

Appendix A: Porter 5 Forces and Industry Risk Assessment

PORTER

Industry Risk Assessment (1) (25)Risk Description

Commodity price fluctuations

Commodity pricing fluctuations can have a massive impact on a business’ ability to meet profit targets; Lowering commodity pricing can also make an owned reserve commercial unviable due to high development or production costs

F/X ExposureCommodity pricing typically done in USD, resulting in F/X fluctuations representing a potential risk for Canadian and Mexican operations or US firms shipping overseas

Asset Depletion Future financial performance is dependant on firms' ability to replace reserves that are constantly depleting

Reservoir CharacteristicsGeological and reservoir characteristics vary by site and can result in wide of production volumes – past success doesn’t impact future success

Reliance on 3rd Party OperatorsSeveral firms reliant on 3rd party operators (refineries, pipeline transportation, shipping lanes), which can create delays to market impacting cash flows

Environmental Regulation

Consistent trend in the industry for more and more regulation to be introduced; this increases production costs and can potentially make owned reserves not commercially viable (ex, risk of anti-fraking regulations)

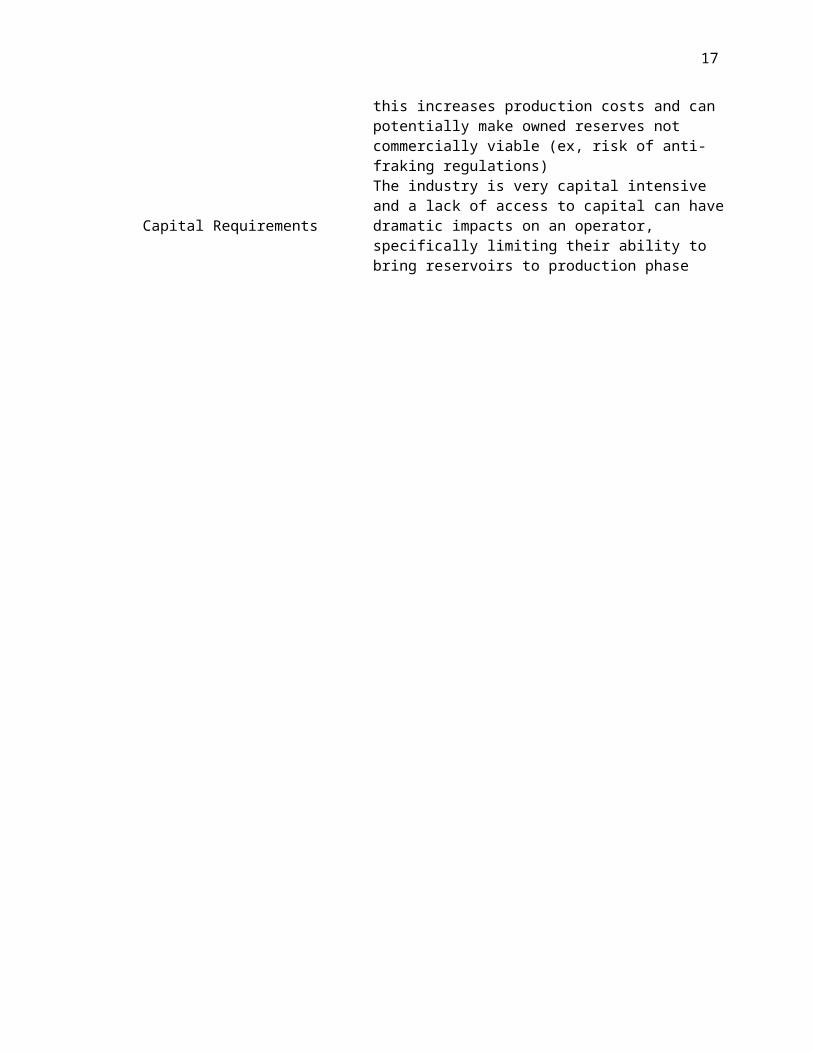

Capital Requirements

The industry is very capital intensive and a lack of access to capital can have dramatic impacts on an operator, specifically limiting their ability to bring reservoirs to production phase

12

Appendix B: Encana Corporation Capital Structure Summary

Debt-to-Equity Ratio 2007 2008 2009 2010 2011EnCana 0.46 (4) 0.39 (2) 0.47 (5) 0.45 (26) 0.5 (27)Cenovus - - 0.69 (6) 0.41 (28) 0.37 (29)

Appendix C: EnCana and Cenovus Dividend Policy Review

Dividend Policy for Encana Before and After the Spin off Before Spin-off After Spin-Off 2008 (2) 2009 (6) (5) 2010 (28) (26) 2011 (29) (27) Dividend Shares Dividend Shares Dividend Sahres Dividend Shares

EnCana 1.6 750.4 1.4 751.4 0.8 739.7 0.8 736.3Cenovus - - .21* 751.4 0.8 751.9 0.8 754* Dividends only for one quarter

Dividend Payout Ratio 2008 2009 2010 2011EnCana 20.17% (2) 57.02% (5) 39.29% (26) 471% (27)Cenovus - 15.91% (6) 73.39% (28) 41% (29)

13

Appendix D: Share Ownership at Announcement

Institutional Holdings in Encana as of December 2012 (30)

Total Institutions 520

Shares held by institutions468,238,55

3% of all shares 61%

Institution NameTotal

Shares

Percent of

company

Change in Shares

ROYAL BANK OF CANADA 45,818,626 6.0% 319,577

WELLINGTON MANAGEMENT CO LLP 25,196,107 3.3%

-5,764,86

9IG INVESTMENT MANAGEMENT LTD 21,950,663 2.9% 924,625

JARISLOWSKY FRASER LTD 20,818,550 2.7%

-4,053,01

8

MANNING & NAPIER ADVISORS INC 18,789,050 2.5%3,566,05

0HARRIS FINANCIAL CORP 18,106,216 2.4% 663,833HARRIS ASSOCIATES L P 17,948,947 2.3% -486,800MACKENZIE FINANCIAL CORP 16,423,623 2.1% 976,661INSTITUTIONAL CAPITAL CORP 16,240,387 2.1% 246,436CONNOR CLARK & LUNN INVESTMENT MANAGEMENT LTD 13,353,451 1.7%

1,696,894

CAPITAL GUARDIAN TRUST CO 12,045,726 1.6%

-1,101,47

6

TD ASSET MANAGEMENT INC 11,767,196 1.5%2,179,83

2

CAPITAL WORLD INVESTORS 11,650,000 1.5%3,000,00

0CIBC WORLD MARKETS INC. 11,589,154 1.5% -128,738INVESCO LTD 10,676,594 1.4% -329,787

BANK OF NOVA SCOTIA 10,190,361 1.3%1,091,71

2TORONTO DOMINION BANK 10,081,114 1.3% 324,872

CAPITAL RESEARCH GLOBAL INVESTORS 8,540,000 1.1%1,035,00

0BEUTEL GOODMAN & CO LTD 7,875,032 1.0% 648,344PRIMECAP MANAGEMENT CO 7,605,302 1.0% -500

14

SAC CAPITAL ADVISORS LP 5,100,984 0.7% -158,632AGF FUNDS INC 4,928,844 0.6% 62,034MERCATOR ASSET MANAGEMENT L P 4,486,700 0.6% -147,700RUSSELL FRANK CO 4,301,619 0.6% 935,754TETREM CAPITAL MANAGEMENT LTD. 3,733,482 0.5% -459,497

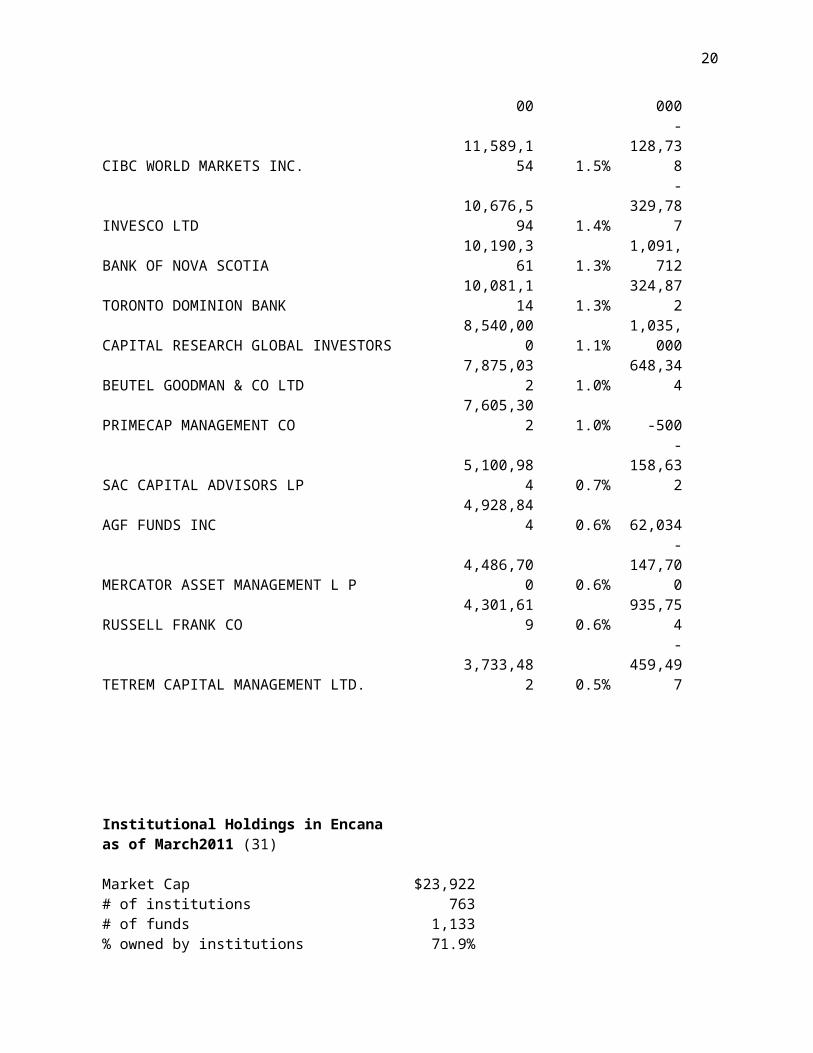

Institutional Holdings in Encana as of March2011 (31)

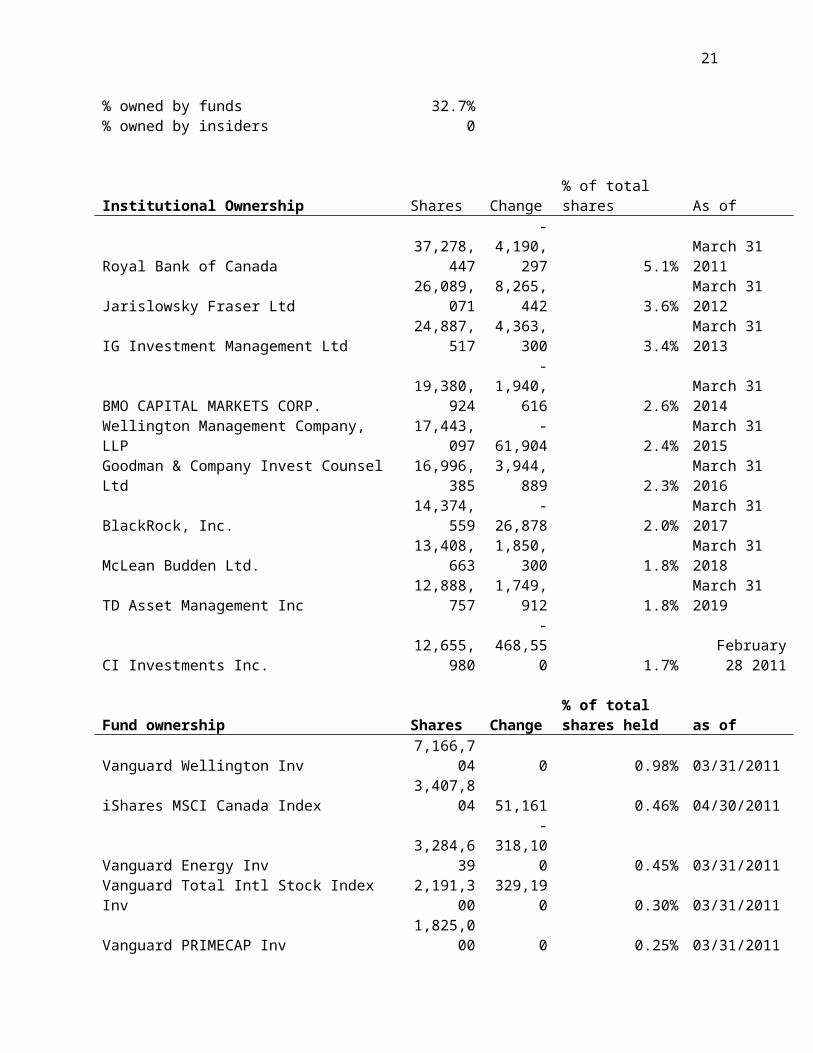

Market Cap $23,922# of institutions 763# of funds 1,133% owned by institutions 71.9%% owned by funds 32.7%% owned by insiders 0

Institutional Ownership Shares Change % of total shares As of

Royal Bank of Canada37,278,44

7

-4,190,29

7 5.1% March 31 2011

Jarislowsky Fraser Ltd26,089,07

18,265,44

2 3.6% March 31 2012

IG Investment Management Ltd24,887,51

74,363,30

0 3.4% March 31 2013

BMO CAPITAL MARKETS CORP.19,380,92

4

-1,940,61

6 2.6% March 31 2014

Wellington Management Company, LLP17,443,09

7 -61,904 2.4% March 31 2015

Goodman & Company Invest Counsel Ltd16,996,38

53,944,88

9 2.3% March 31 2016

BlackRock, Inc.14,374,55

9 -26,878 2.0% March 31 2017

McLean Budden Ltd.13,408,66

31,850,30

0 1.8% March 31 2018

TD Asset Management Inc12,888,75

71,749,91

2 1.8% March 31 2019

CI Investments Inc.12,655,98

0 -468,550 1.7%February 28

2011

15

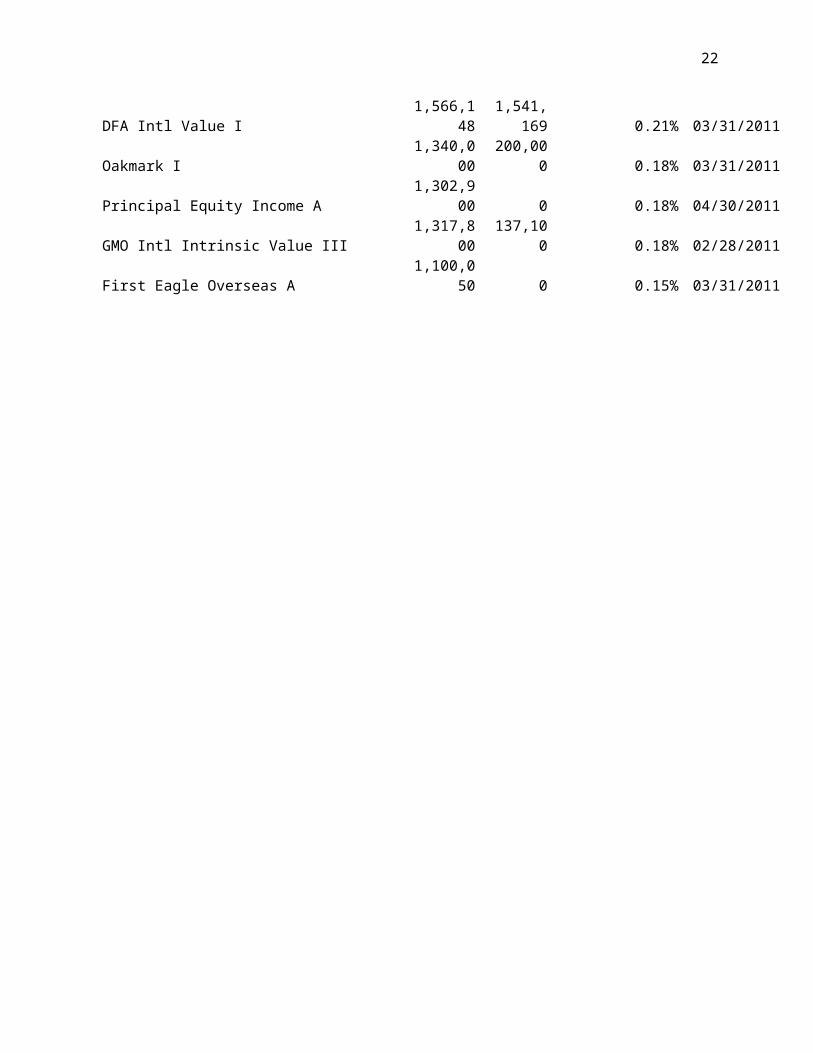

Fund ownership Shares Change% of total shares held as of

Vanguard Wellington Inv 7,166,704 0 0.98% 03/31/2011iShares MSCI Canada Index 3,407,804 51,161 0.46% 04/30/2011Vanguard Energy Inv 3,284,639 -318,100 0.45% 03/31/2011Vanguard Total Intl Stock Index Inv 2,191,300 329,190 0.30% 03/31/2011Vanguard PRIMECAP Inv 1,825,000 0 0.25% 03/31/2011

DFA Intl Value I 1,566,1481,541,16

9 0.21% 03/31/2011Oakmark I 1,340,000 200,000 0.18% 03/31/2011Principal Equity Income A 1,302,900 0 0.18% 04/30/2011GMO Intl Intrinsic Value III 1,317,800 137,100 0.18% 02/28/2011First Eagle Overseas A 1,100,050 0 0.15% 03/31/2011

16

Appendix E: EnCana Valuation Analysis

EnCana ratio analysis vs. industry competitors:

EBITDA ($M) CF/Share ROE EPS P/E EV/EBITDA

Encana $4,519 40.0% $10.68 10.04 $2 52.72 16.38CNR $1,703 5.7% $8.06 -10.06 $0 -142.27 36.53Devon Energy $4,648 61.3% $26.36 22.77 $3 39.77 12.01Apache Energy Inc $6,935 77.2% $23.16 35.57 $4 31.41 6.99Chesapeake $2,249 - $9.67 -58.91 -$3 -17.88 19.91

Peer Average $3,884 48% $16.81 (2.66) $1 -22.24 18.86Peer Median $3,449 61% $16.42 6.35 $1 6.76 15.96

As on 10/May/2008

EBITDA Margin

(30) (32) (33) (34) (35)

Ratio Analysis seems to indicate that EnCana is slightly undervalued when compared to industry

peers.

In addition to a ratio analysis, an EV/EBITDA analysis over time was completed, which also

appears to indicate that the EV/EBITDA ratio is tracking below industry peers.

EV/EBITDA Summary Table

EV/EBITDAEncana 13.62 16.38 5.35 26.82 18.00 91.69Cenovus - - - 10.91 30.08 18.99

18.86 36.53 4.76 23.31 18.43 13.88Devon Energy 10.24 12.01 5.31 17.78 10.05 5.60Apache Energy Inc 8.16 6.99 26.16 61.61 9.42 5.20Chesapeake 10.87 19.91 14.86 3.04 11.98 9.50

Peer Average 12.03 18.86 12.77 26.44 12.47 8.55Peer Median 10.55 15.96 10.09 20.54 11.01 7.55

As on 31/Dec/2007

As on 10/May/2008

As on 31/Dec/2008

As on 30/Nov/2009

As on 31/Dec/2010

As on 31/Dec/2011

Canadian Natural Resources

(34) (35) (36) (37) (33) (32)

17

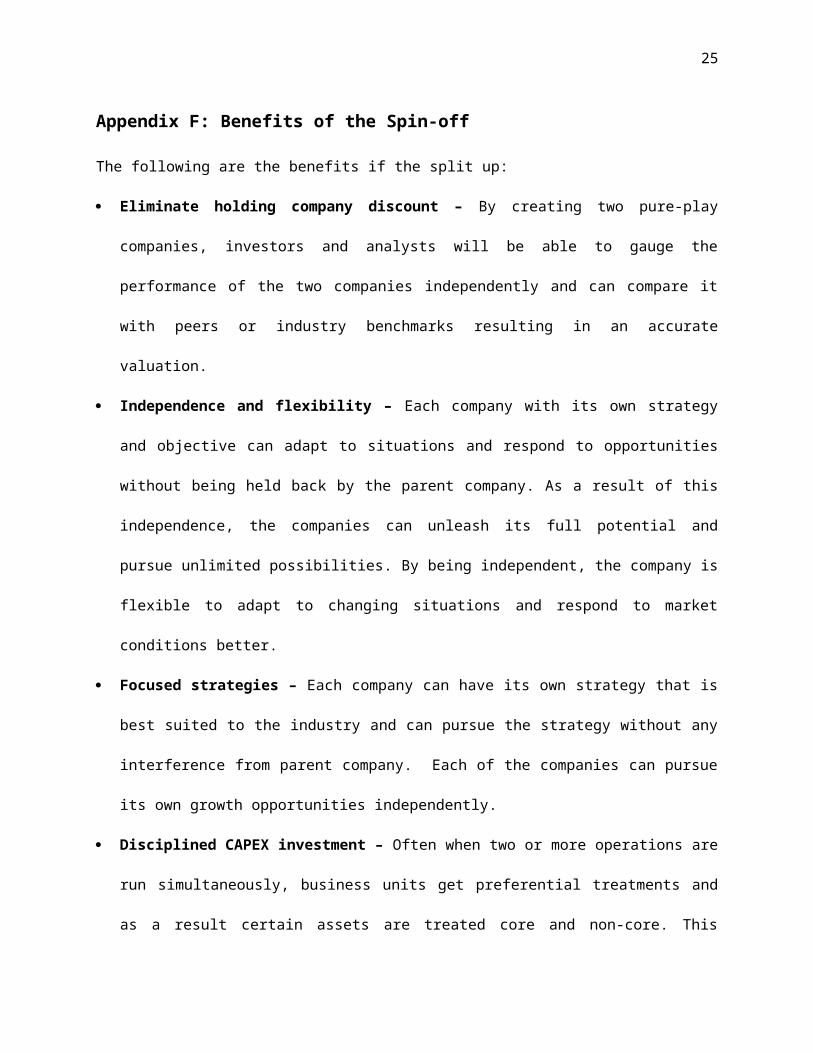

Appendix F: Benefits of the Spin-off

The following are the benefits if the split up:

Eliminate holding company discount – By creating two pure-play companies, investors and analysts

will be able to gauge the performance of the two companies independently and can compare it with

peers or industry benchmarks resulting in an accurate valuation.

Independence and flexibility – Each company with its own strategy and objective can adapt to

situations and respond to opportunities without being held back by the parent company. As a result

of this independence, the companies can unleash its full potential and pursue unlimited possibilities.

By being independent, the company is flexible to adapt to changing situations and respond to

market conditions better.

Focused strategies – Each company can have its own strategy that is best suited to the industry and

can pursue the strategy without any interference from parent company. Each of the companies can

pursue its own growth opportunities independently.

Disciplined CAPEX investment – Often when two or more operations are run simultaneously,

business units get preferential treatments and as a result certain assets are treated core and non-

core. This results in under investment of non-core assets. By splitting the 2 companies this partiality

in investment is eliminated and each of the two companies can invest effectively in CAPEX and

operational improvements.

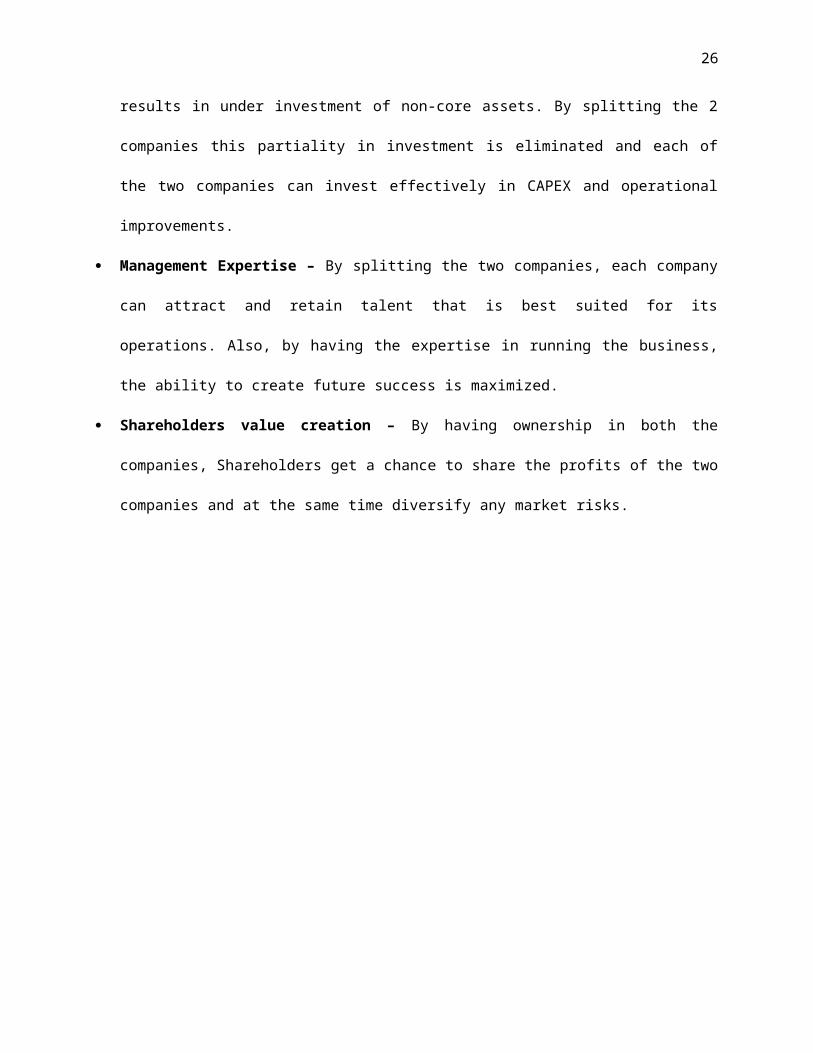

Management Expertise – By splitting the two companies, each company can attract and retain

talent that is best suited for its operations. Also, by having the expertise in running the business, the

ability to create future success is maximized.

Shareholders value creation – By having ownership in both the companies, Shareholders get a

chance to share the profits of the two companies and at the same time diversify any market risks.

18

Appendix G: Location of assets to EnCana (GasCo)

Source: (38)

19

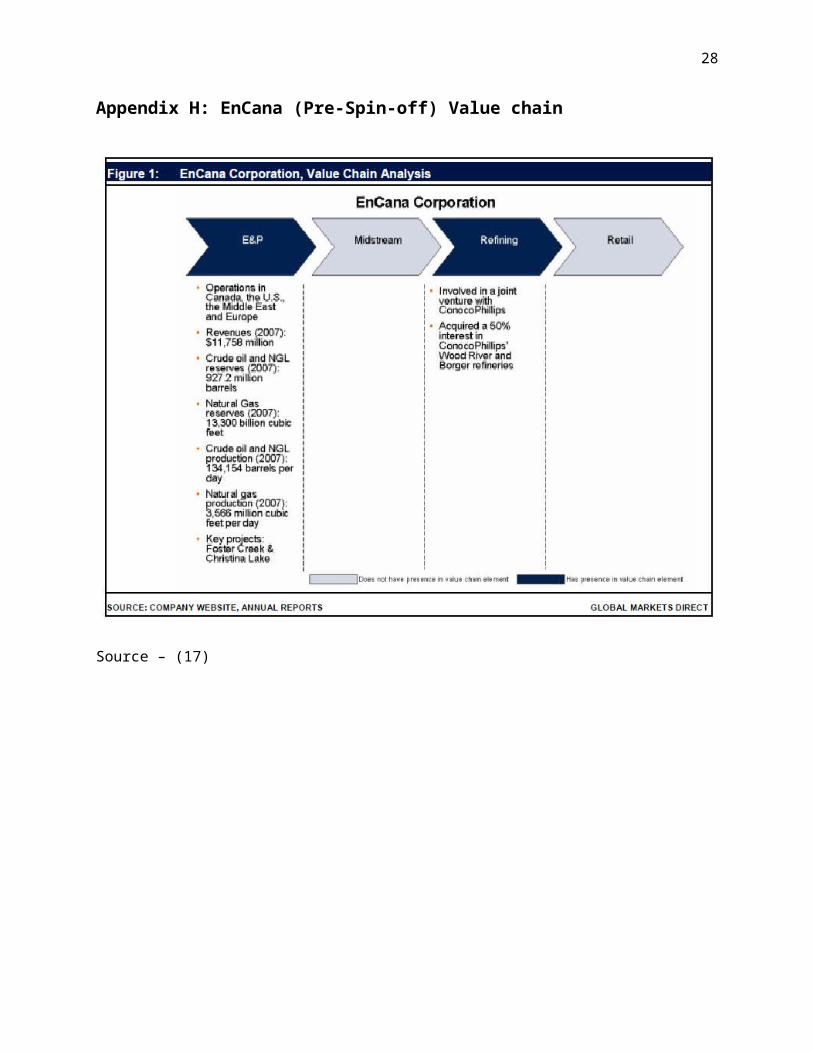

Appendix H: EnCana (Pre-Spin-off) Value chain

Source – (17)

20

Appendix I: Location of assets to Cenovus (IOCo)

Source: (39)

21

Appendix J: Breakup of Encana balance sheet into Encana and Cenovus

EnCana (2)(Prior to spin-off)

EnCana (5)(Post spin-off)

Cenovus (6)

Assets 47,247 33,827 20,552

Liabilities 24,273 17,213 11,372

Equity 22,974 16,614 9,180

Revenue 30,064 11,114 10,140

Net income 5,944 1,862 648

EBITDA/interest 24.27 16.24 13.88

All figures are in US$ millions

Shareholders

EnCana

Shareholders

IOCo(later to become

Cenovus)EnCana(GasCo)

Cenovus(IOCo)

$47.25B

$33.8B

$20.6B

22

Appendix K: Breakdown of shareholder value in May 2008

Shareholder Value

EncanaShare holder

Encana($85.93/share*)

GasCo(Pure play natural gas company

– later to retain EnCana)

IOCo(Integrated Oil Company – later

to become Cenovus)

23

Appendix L: Proceeding with Spin-off in September 10, 2009

Shareholder Value

* Sept 10, 2009 (Date of proceeding with divestiture) – TSX Closing share price

EncanaShare holder

Encana($55.03/share*)

GasCo(Pure play natural gas company

– later to retain EnCana)

IOCo(Integrated Oil Company – later

to become Cenovus)

24

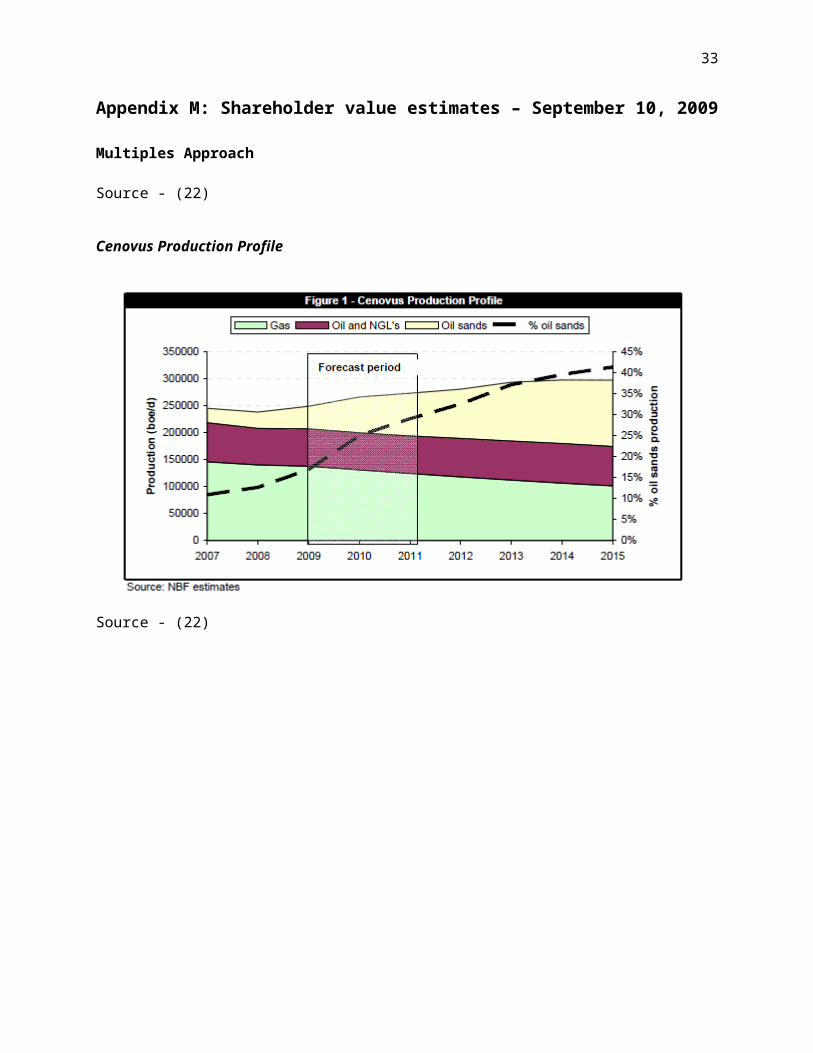

Appendix M: Shareholder value estimates – September 10, 2009

Multiples Approach

Source - (22)

Cenovus Production Profile

Source - (22)

25

EnCana Production Profile

Source - (22)

NAV Estimates

Source - (22)

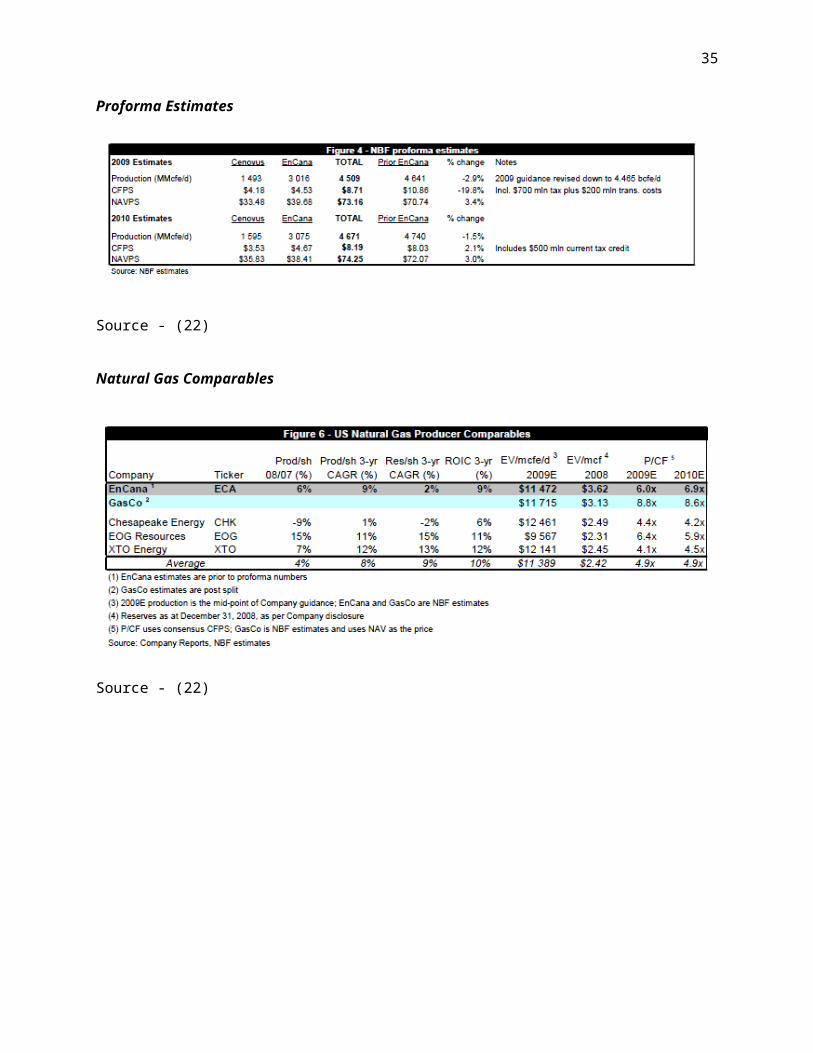

26

Proforma Estimates

Source - (22)

Natural Gas Comparables

Source - (22)

27

EnCana and Cenovus Price Summary

Source - (22)

Shareholder Value

* September 21, 2009 – Based on National Bank Financial Valuation (22)

Share holder($57/Share)

Encana($27/share*)

Cenovus($30/share*)

28

DCF Approach

EnCana (GasCo)

EnCana (GasCo)Canadian Foothills Division 2008 USA Division 2008Revenues, Net of Royalties (MM) $4,355

Revenues, Net of Royalties (MM) $5,629

Expenses Expenses Production and mineral taxes 33 Production and mineral taxes 370Transportation and selling 239 Transportation and selling 502Operating 609 Operating 618Operating Cash Flow * 3,474 Operating Cash Flow * 4,139 CAPEX* CAPEX* Canadian Foothills 2299 USA 2615Canada 1901 Total CAPEX 4200 Total CAPEX 2615

EnCana Consolidated Free Cash FlowOperating Cash Flow 7,613 CAPEX 6815 NWC 0 Free Cash Flow 798 Growth Rate 6.50% WACC 9%

Intrinsic Value(MM)$33,99

5

Balance Sheet

Assets (MM)$33,99

5 Liabilities (MM)$17,46

5

Equity (MM)$16,53

0

$33,99

5 Stocks Outstanding (MM) 750.4 Per share price $22

* Source - (2)

29

Cenovus (IOCo)

Cenovus (IOCo)Canadian Plains Division 2008 Integrated Oil Division 2008Revenues, Net of Royalties(MM) $4,418 Revenues, Net of Royalties (MM) $10,288Expenses Expenses Production and mineral taxes 74 Production and mineral taxes 1Transportation and selling 392 Transportation and selling 571Operating 484 Operating 732Operating Cash Flow * 3,468 Purchased Product 8,609 Operating Cash Flow* 375CAPEX* CAPEX* Canadian Plains 847 Integrated Oil – Canada 656Canada 1250 Downstream Refining 478Total CAPEX 2097 Total CAPEX 1134

Cenovus Consolidated Free Cash FlowOperating Cash Flow 3,843 CAPEX 3231 NWC 0 Free Cash Flow 612 Growth Rate 6% WACC 7.87%

Intrinsic Value(MM)$34,69

1

Balance Sheet

Assets (MM)$34,69

1 Liabilities (MM) $11,372 Equity (MM) $23,319 $34,691 Stocks Outstanding(MM) 750.4 Per Share Price $31

* Source - (2)

30

Shareholder Value (Based on DCF)

Share holder($53/Share)

Encana($22/share)

Cenovus($31/share)

31

Appendix N: Actual Trading post split up - Dec 3, 2009

* Dec 3, 2009 –TSX Trading price

Share holder($56.15/Share)

Encana($29.4/share*)

Cenovus($26.75/share*)

32

Appendix O: Encana business unit performance

EnCana Performance 2008PF 2009PF 2010 2011

Revenue $ 13,505 $ 6,732 $ 8,870 $ 8,467

Net income $ 3,405 $ 749 $ 1,499 $ 128

Profit margin 25% 11% 17% 2%

SOURCE?

Appendix P: Cenovus business unit performance

Cenovus Performance 2008PF 2009PF 2010 2011

Revenue $ 16,559 $ 10,140 $ 12,973 $ 15,696

Net income $ 2,368 $ 648 $ 993 $ 1,478

Profit margin 14% 6% 8% 9%

SOURCE?

33

Appendix Q: Consolidated Financial Performance Post Split

Source?

Consolidated Performance 2007 2008 2010 2011

Revenue $ 21,700 $ 30,064 $ 21,843 $ 24,163

Expenses $ 16,879 $ 21,487 $ 18,620 $ 21,954

Earnings before taxes $ 4,821 $ 8,577 $ 3,223 $ 2,209

Net Income $ 3,959 $ 5,944 $ 2,492 $ 1,606

Long Term Assets $ 42,530 $ 41,645 $ 50,486 $ 47,274

Long Term Liabilities $ 19,940 $ 20,379 $ 23,505 $ 24,174

Equity $ 20,704 $ 22,974 $ 27,349 $ 25,730

Profit Margin 22% 29% 15% 9%

LT Liabilities / Equity 0.96 0.89 0.86 0.94

LT Liabilities / LT Assets 0.47 0.49 0.47 0.51

ROA 11% 13% n/a 3%

ROE 23% 29% n/a 6%

34

Appendix R: Combined post-split firm trading values does not demonstrate

much change in shareholder value

7/24/1998 4/19/2001 1/14/2004 10/10/2006 7/6/2009 4/1/2012 12/27/2014$0

$20

$40

$60

$80

$100

$120

Encana Closing PriceCenovus Closing PriceCombined Closing Price

Share price,C$

Source: Yahoo Finance (2012)

Adjusted for Splits

SOURCE

35

Appendix S: The TSX has outperformed the combined firms since the split in

2009.

7/6/2009 8/10/2010 9/14/2011 10/18/2012 11/22/20130

20

40

60

80

100

120

140

160

Encana Index

Cenovus Index

TSX Index

Consolidated Firm Index

Index,Dec 2 2009 = 100

Source: Yahoo Finance (2012)

SOURCE

36

References

1. MarketLine. MarketLine Industry Profile: Oil & Gas North America. [Online] june 2012. [Cited: 03 26,

2013.] http://advantage.marketline.com.ezproxy.library.yorku.ca/Product?pid=MLIP0559-0024.

2. EnCana . EnCana 2008 Annual Report. [Online] 2009. [Cited: 03 20, 2013.]

http://www.encana.com/pdf/investors/financial/annual-reports/2009/annual-report-2009.pdf.

3. Encana. EnCana plans to split along distinct business lines to create two Calgary-headquartered

energy companies. Encana. [Online] May 11, 2008. [Cited: March 16, 2013.]

http://www.encana.com/news-stories/news-releases/details.html?release=609419.

4. EnCana. EnCana 2007 Annual Report. [Online] 2008. [Cited: 03 22, 2013.]

http://www.encana.com/pdf/investors/financial/annual-reports/2007/2007-annual-report.pdf.

5. —. EnCana 2009 Annual Report. [Online] 2010. [Cited: 03 18, 2013.]

http://www.encana.com/pdf/investors/financial/annual-reports/2009/annual-report-2009.pdf.

6. Cenovus 2009 Annual Report. Cenovus 2009 Annual Report. [Online] 2010. [Cited: 03 18, 2013.]

http://www.cenovus.com/invest/docs/2010/2009-annual.pdf.

7. Encana. Cenovus Energy Inc. to be North America’s newest integrated oil company. Encana. [Online]

September 30, 2008. [Cited: March 16, 2013.]

http://www.encana.com/news-stories/news-releases/details.html?release=609377.

8. —. EnCana revises schedule for creation of Cenovus Energy due to financial markets uncertainty.

Encana. [Online] October 15, 2008. [Cited: March 16, 2013.]

http://www.encana.com/news-stories/news-releases/details.html?release=609363.

9. —. EnCana completes US$500 million debt offering. Encana. [Online] May 04, 2009. [Cited: March 16,

2013.] http://www.encana.com/news-stories/news-releases/details.html?release=609296.

37

10. —. EnCana agrees to sell non-core Alberta properties for $632 million (C$707 million) to Bonavista

Energy Trust. Encana. [Online] July 16, 2009. [Cited: March 16, 2013.] http://www.encana.com/news-

stories/news-releases/details.html?release=609318.

11. —. EnCana proceeds with plan to split into two distinct and independent energy companies. Encana.

[Online] September 10, 2009. [Cited: March 16, 2013.] http://www.encana.com/news-stories/news-

releases/details.html?release=609273.

12. —. EnCana subsidiary Cenovus Energy completes a US$3.5 billion private debt offering. Encana.

[Online] Spetember 18, 2009. [Cited: March 16, 2013.] http://www.encana.com/news-stories/news-

releases/details.html?release=609266.

13. —. EnCana to hold conference call and webcast on Integrated Oil Division. Encana. [Online] October

01, 2009. [Cited: March 16, 2013.] http://www.encana.com/news-stories/news-releases/details.html?

release=609255.

14. —. EnCana mails Arrangement Circular - “when issued” trading in EnCana and Cenovus shares to

start November 2, 2009. Encana. [Online] October 29, 2009. [Cited: March 16, 2013.]

http://www.encana.com/news-stories/news-releases/details.html?release=609247.

15. —. Financial and operating information filed for Cenovus Energy and post-split EnCana. Encana.

[Online] November 13, 2009. [Cited: March 16, 2013.] http://www.encana.com/news-stories/news-

releases/details.html?release=609230.

16. —. Shareholders overwhelmingly endorse split of EnCana into two distinct and independent

companies - Cenovus Energy and EnCana. Encana. [Online] November 25, 2009. [Cited: March 16, 2013.]

http://www.encana.com/news-stories/news-releases/details.html?release=609227.

17. Global Markets Direct. EnCana Corporation Financial Profile. s.l. : Global Markets Direct, 2008.

18. Encana . EnCana closes transaction to split into two distinct and independent companies – Cenovus

Energy and EnCana. Encana. [Online] November 30, 2009. [Cited: March 16, 2013.]

38

http://www.encana.com/news-stories/news-releases/details.html?release=609226.

19. The Economist. America’s Cheap Gas: Bonanza or Bane? [Online] March 2, 2013. [Cited: 03 20,

2013.] http://www.economist.com/news/finance-and-economics/21572815-natural-gas-prices-are-

sure-riseeventually-bonanza-or-bane.

20. KPMG Global Energy Institute. KPMG (2011). Shale Gas, a Global Perspective. [Online] KPMG, 2011.

[Cited: 03 26, 2013.] www.gses.com/images/documents/shale-gas-global-perspective.pdf.

21. Bennet Jones. Bennet Jones (2012). The Canadian Oil Sands: A Backgrounder. [Online] 2012. [Cited:

03 19, 2013.] http://www.bennettjones.com/uploadedFiles/Publications/Guides/The%20Canadian

%20Oil%20Sands%202012-Web.pdf.

22. National Bank Financial . EnCana Corp. - Taking another look as we split the forecast. Toronto : The

NBF Daily Bulletin, 2009.

23. Wiki Wealth. EnCana WACC. Wiki Wealth Collaborative Research. [Online] 2012. [Cited: March 23,

2013.] http://www.wikiwealth.com/wacc-analysis:eca.

24. Henry Fund Research. Cenovus Energy. Tippie School of Management. [Online] September 18, 2012.

[Cited: March 23, 2013.] http://tippie.uiowa.edu/henry/reports12/cve_f12.pdf.

25. TriStone Capital Inc. TriStone Capital Inc. Research Report: EnCana 2009. [Online] May 29, 2009.

[Cited: 03 26, 2013.] Bloomberg Terminal.

26. EnCana. EnCana 2010 Annual Report. [Online] 2011. [Cited: 03 20, 2013.]

http://www.encana.com/pdf/investors/financial/annual-reports/2010/annual-report-2010.pdf.

27. —. EnCana 2011 Annual Report. [Online] 2012. [Cited: 03 22, 2013.]

http://www.encana.com/pdf/investors/financial/annual-reports/2011/annual-report-2011.pdf.

28. Cenovus. Cenovus 2010 Annual Report. [Online] 2011. [Cited: 03 18, 2013.]

http://www.cenovus.com/invest/docs/2010-annual-report/cenovus-AR-2010.pdf.

39

29. —. Cenovus 2011 Annual Report. [Online] 2012. [Cited: 03 17, 2013.]

http://www.cenovus.com/invest/docs/2011-annual-report/cenovus-AR-2011.pdf.

30. Mergent. Mergent Online EnCana Company Profile (2013). [Online] [Cited: 03 26, 2013.]

http://www.mergentonline.com.

31. Morningstar. Morningstar, Encana Corp via The Internet Archive Wayback Machine (2013). [Online]

2011. [Cited: 03 26, 2013.]

http://web.archive.org/web/20110611012255/http://investors.morningstar.com/ownership/

shareholders-overview.html?t=ECA®ion=USA&culture=en-US.

32. Mergent Online. Chesapeake Energy Corp. Mergent Online . [Online] March 20, 2013. [Cited: March

20, 2013.] http://www.mergentonline.com/companyfinancials.php?

pagetype=asreported&compnumber=75886&period=Annuals&dataarea=PL&range=5¤cy=AsRep

&scale=AsRep&Submit=Refresh.

33. —. Devon Energy Corp. Mergent Online. [Online] March 20, 2013. [Cited: March 20, 2013.]

http://www.mergentonline.com/companyfinancials.php?

pagetype=asreported&compnumber=98163&period=Annuals&dataarea=PL&range=5¤cy=AsRep

&scale=AsRep&Submit=Refresh.

34. Mergen Online. Apache Corp. Mergent Online. [Online] March 20, 2013. [Cited: March 20, 2013.]

http://www.mergentonline.com/companyfinancials.php?

pagetype=asreported&compnumber=525&period=Annuals&dataarea=PL&range=5¤cy=AsRep&sc

ale=AsRep&Submit=Refresh.

35. Mergent Online. CNR. Mergent Online. [Online] March 20, 2013. [Cited: March 20, 2013.]

http://www.mergentonline.com/companyfinancials.php?

pagetype=asreported&compnumber=6434&period=Annuals&dataarea=PL&range=5¤cy=AsRep&

scale=AsRep&Submit=Refresh.

40

36. —. Cenovus Energy Inc. Mergent Online. [Online] March 20, 2013. [Cited: March 20, 2013.]

http://www.mergentonline.com/companyfinancials.php?

pagetype=asreported&compnumber=128343&period=Annuals&dataarea=PL&range=5¤cy=AsRe

p&scale=AsRep&Submit=Refresh.

37. —. Encana Corp. Mergent Online . [Online] March 18, 2013. [Cited: March 18, 2013.]

http://www.mergentonline.com/companyfinancials.php?

pagetype=ratios&compnumber=6434&period=AnnualsIFRS&dataarea=BS&range=7¤cy=AsRep&s

cale=AsRep.

38. National Bank Financial. EnCana Corporation - Initiating Coverage. Toronto : The NBF Daily Bulletin,

2009.

39. Credit Suisse. Cenovus Energy Inc. s.l. : Credit Suisse Equity Research, 2009.

40. Market Watch. Historical Quotes. Market Watch. [Online] March 20, 2013. [Cited: March 20, 2013.]

http://www.marketwatch.com/investing/stock/CVE/historical.

41. Investopedia. Integrated Oil & Gas Company . Investopedia . [Online] [Cited: March 16, 2013.]

http://www.investopedia.com/terms/i/integrated-oil-gas-company.asp#axzz2NjV9lBZP.

42. Morgan Stanley Research. EnCana Corporation- Split Announced; Committed to Shareholder Value.

North America : Morgan Sanley Research, 2009.