enron collapse

DESCRIPTION

Riska ManegementTRANSCRIPT

MM 6029

CORPORATE RISK MANAGEMENT

THE ENRON COLLAPSE

A R. Sofyandi Sedar (29111144)

Debby Sugithio (29111330)

Ferdinand Throedu (29111343)

Yunus Arie Wiratama (29111322)

MASTER OF BUSINESS ADMINISTRATION

SCHOOL OF BUSINESS AND MANAGEMENT

INSTITUT TEKNOLOGI BANDUNG

2012

THE ENRON COLLAPSE

Background

Enron was the seventh largest company by revenues in the United States. It employed 25,000 people worldwide. It had been voted as one of the most admired companies in United States. Its performance of the transformation of a conservative, domestic energy company into a global player had been lauded in the media and business school cases. As more and more facts emerged, it became clear that Enron had many elements of a “Ponzi” scheme. The drive to maintain reported earnings groth led to the extensive use of “aggresive” accounting policies to accelerate earnings.

Enron was found in 1985 (merger between Houston Natural Gas and InterNorth) by Kenneth Lay and he became chairman and CEO of the new entity. This combination created the largest company-owned natural gas pipeline system in the United States of some 37,000 miles stretching from the border of Canada to Mexico and from the Arizona-California border to Florida.

Richard Kinder was the chief operating officer (COO) and set about building up Enron through a series of new ventures and acquisitions. Many of these were financed by debt and by the end of 1987, Enron’s debt was 75% of its market capitalisation.

During its operation, Enron entered many huge contracts for example; Enter a 20-year deal with Sithe Energies to supply all the natural gas for a 1,000 megawatt electricity.Total deal estimation around US$3.5 billion. They also entered contract with Dabhol power project in Maharashtra State in India (US$ 3billion). Enron introduced Volumetric Production Payments, in this agreement, Enron provided liquidity by prepaying for long-term fixed-price gas supplies, with the payment secured on the gas itself and not on the assets of the producer.

On this case we will eveluate each Enron strategies which contained many high risk strategies or deals. We also analyze main thing that makes Enron collapse in 2 December 2001.

Risk Identification:

Hazard Peril Loss Risk Type

The complexity of

transactions that

Enron did with all of

the counterparties.

Poor Controls of

Management and

Board levels in the

implementation

Big loss of Enron’s

profit.

ACCOUNTING

RISK

The creation of

Limited Liability

Partnership of LJM

from Andrew

Fastow.

CEO’s role: the

failure of the system

of internal control to

mitigate the risk

inherent in the

relationship between

Enron and the LJM

partnerships.

Big loss of Enron’s

profit.

PEOPLE RISK

The request from

Enron’s board that

not to publish the

audited financial

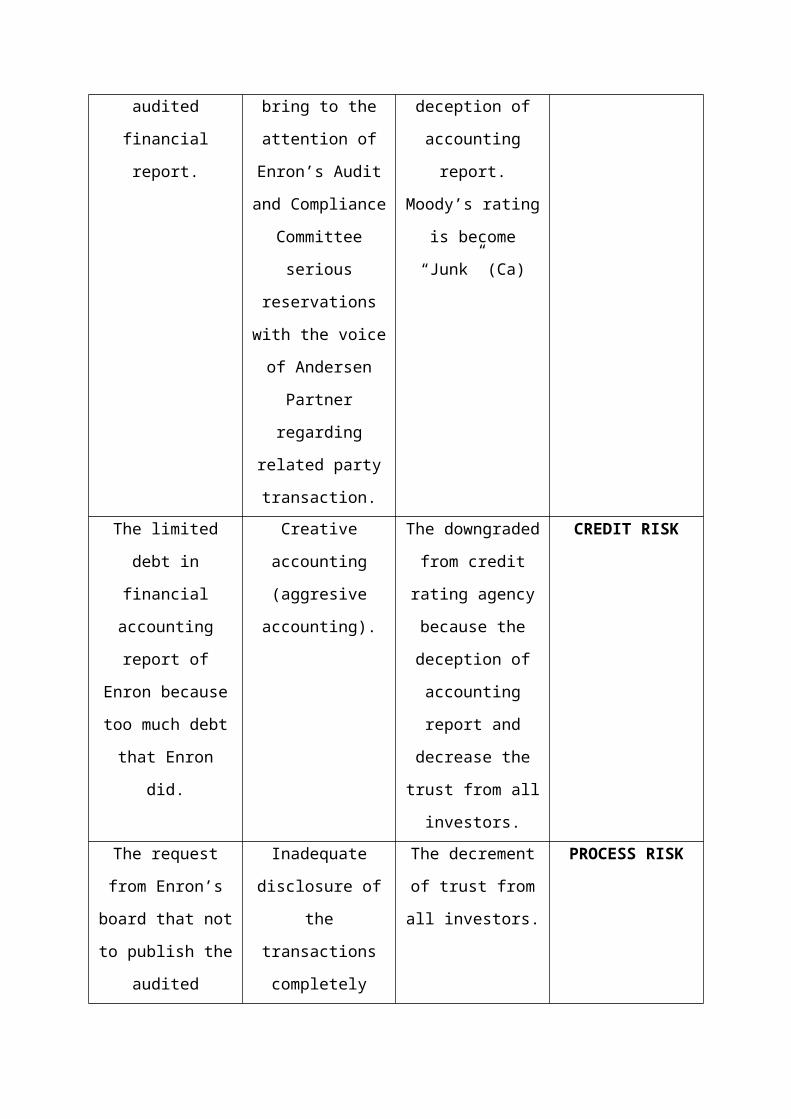

report.

Auditor’s role: The

Andersen failed to

bring to the attention

of Enron’s Audit and

Compliance

Committee serious

reservations with the

voice of Andersen

Partner regarding

related party

transaction.

The downgraded

from credit rating

agency because the

deception of

accounting report.

Moody’s rating is

become “Junk” (Ca)

SYSTEM RISK

The limited debt in

financial accounting

report of Enron

because too much

debt that Enron did.

Creative accounting

(aggresive

accounting).

The downgraded

from credit rating

agency because the

deception of

accounting report and

decrease the trust

from all investors.

CREDIT RISK

The request from

Enron’s board that

not to publish the

audited financial

report.

Inadequate disclosure

of the transactions

completely

The decrement of

trust from all

investors.

PROCESS RISK

The board members

want to seek the

highest profit as

much as possible.

Lack of

understanding of the

board members.

Big loss of Enron’s

profit.

PEOPLE RISK

Enron wants to seek

the highest profit and

the lowest cost.

Make many Special

Purpose Entities

(SPEs).

Make a complex

problems in Enron so

that if the situation

fail, Enron will

receive big loss from

this SPEs.

LEVERAGE

OPERATIONAL

RISK

Enron didn’t have

cash money to

finance their debt.

Borrow the money

from the bank like

Credit Suisse First

Boston and NatWest.

Too much of debt

will make Enron fall

someday.

LIQUIDITY RISK

Devaluation of local

currency in Brazil,

the Azurix venture

had already resulted

in write downs of

$326 Million relating

to assets in

Argentina, the

Wessex Water

business in England

was experiencing

both financial and

operational

difficulties.

Some hedge funds

had become short

sellers of Enron

stock.

Enron’s share price

continue to slide.

MARKET RISK

There are several risks in Enron:

1. People Risk

2. Process Risk

3. Leverage Operational Risk

4. Accounting Risk

5. System Risk

6. Credit Risk

7. Market Risk

8. Liquidity Risk

Severity Corporate HR Finance

Catastrophic Objective can not be

achieved, may have

financial problems,

incompetent, selling

of SBU, even

liquidation

Loss of key

personnel bring

losses to corporate

competitiveness

Long Term Negative

ROI and ROE,

Credit Rating

Downgrade,

Stock Price

Deterioration

Significant Objective may not be

achieved, must

modify strategy with

big investment

Extra effort to

maintain key

personnel

Short term stock

price decline for one

year

Moderate Corporate

restructuring with

moderate/low

investment

Modify process

business and review

key personnel

Decline ROI and

ROE but price of

stock relative stable

Minor Operation objectives

can not be achieved

Low motivation in

key personnel

Decline of ROI and

ROE compare with

average industry

Insignificant Minor problems in

operational

objectives

Key personnel only

have minor problems

ROI and ROE Still

positive

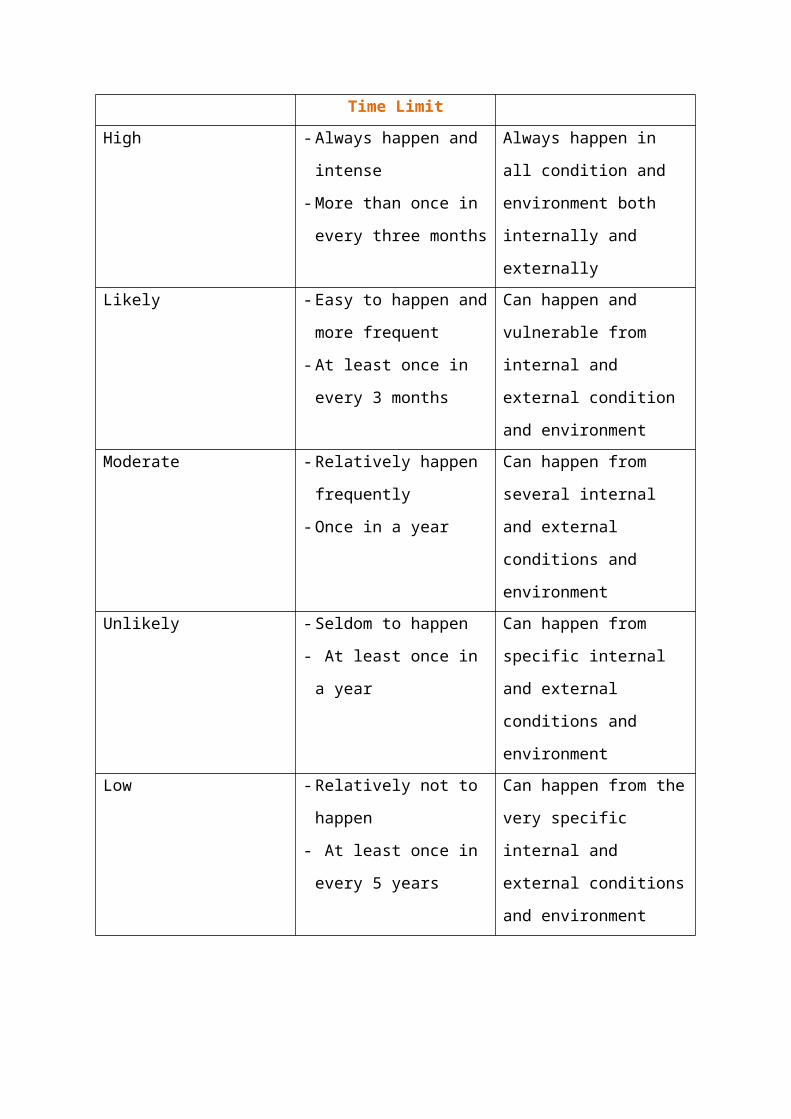

Probability General Criteria Time

Limit

Specific Criteria

High - Always happen and

intense

- More than once in every

three months

Always happen in all

condition and environment

both internally and

externally

Likely - Easy to happen and more

frequent

- At least once in every 3

months

Can happen and vulnerable

from internal and external

condition and environment

Moderate - Relatively happen

frequently

- Once in a year

Can happen from several

internal and external

conditions and environment

Unlikely - Seldom to happen

- At least once in a year

Can happen from specific

internal and external

conditions and environment

Low - Relatively not to happen

- At least once in every 5

years

Can happen from the very

specific internal and external

conditions and environment

Then we measured each risk based on descriptions above and plot into risk metrix :

Catastrophic 8 3 5 1,4,6Very

Low

Major 7 2 Low

Moderate Tolerabl

e

Minor High

Insignificant Very

High

Low Unlikely

Moderat

e Likely High

Risk Exposure Calculators

GROWTH SCOREPressure for performance + Rate of expansion +

Inexperience key employees = 11

5 5 1CULTURE

Rewards for entrepreneurial risk

taking +Executive resistance

to bad news + Level of competition = 155 5 5

INFORMATION MANAGEMENT

Transaction complexity +Gaps in diagnostic

performance measures +

Degree of decentralized

decision making = 115 4 2

Total Score 37

Pressure for Performance

At Enron, Skilling had introduced a rigorous employee performance assessment process that

became known as “rank or yank”. Under this system the bottom 10% in performance were

fired. There was heavy pressure to meet targets and remuneration linked to the deals done and

profits booked in the previous quarter.

Rate of Expansion

Enron ambition to expand its business made the company took action in several numbers of

big projects overseas some of them are the Dabhol power project in India which the value of

the contract around $3 billion in 1992, Enron purchased Wessex Water in UK and formed

Azurix in July 1998 to develop and operate water and wastewater assets including

distribution systems and treatment facilities and related infrastructures, Enron bought energy

plants in Brazil and Bolivia, and bought 4,000 mile Argentinean pipeline system that

delivered two-thirds of that country’s gas. In 1993 Enron also built a gas turbine power plant

on Teesside, England. By 1994, Enron was operating power and pipeline projects in 15

countries and developing a similar number in several others.

Inexperience Key Employees

Enron hired several key employees with good background such as graduated MBA and good

experiences. Such as, Enron hired Jeffrey Skilling a Harvard MBA and ex-employee of

McKinsey, to be head of Enron Finance later became COO. As Enron increased its trading

activities, the company hired its own traders from the investment banking and brokerage

industries.

Rewards for Entrepreneurial Risk Taking

Jeffrey Skilling advised Ken Lay on how to take advantage of gas deregulation and

established so called “gas bank”. Jeff Skilling suggested the idea of making money by trading

in energy rather than generating and supplying it and this practice became Enron main source

of income, later on Jeff Skilling were appointed as president and COO of Enron. Another

event was when Andrew Fastow gave a proposal to raise $15 million from two limited

partners, through an SPE, which would purchase from Enron certain assets and associated

liabilities that the company wished to remove from its balance sheet by forming LJM1. Later

on Fastow through Enron establishing LJM2 to raise $200 million of institutional private

equity in order to purchase assets that Enron wanted to syndicate. This resulting Enron’s

president, Skilling, promoted Fastow to CFO.

Executive Resistance to Bad News

Enron’s executives in Enron were resisted to bad news. This proved by the event when

internal auditor of Andersen gave memos that revealed concerns being expressed by technical

partners. One of them, Carl Bass, was removed from the engagement after Enron complained

that he was being deliberately obstructive.

Level of Competition

As Skilling had introduced a rigorous employee performance assessment process that became

known as “rank or yank”. Under this system the bottom 10% in performance were fired.

These policies created high level of competition between employees, there no employees that

wanted to be fired from their job.

Transaction Complexity

The deals Enron entered with the so-called Raptors, the purpose was the hedging of Enron’s

own investments, were complicated. Most of the deals appeared to be predicted to Enron’s

share price being maintained as Enron shares had been used to fund the vehicles. The

existence of these entities had been disclosed but the financial exposure had not been made

clear.

Gaps in Diagnostic Performance Measures

Enron only used its shares value without looked at the growth of the company and balanced

score card. The rapid growth of expansion caused the increasing complexity and the

difficulties in measuring real performances.

Degree of Decentralization Decision Making

The key decision in Enron as well as in its all subsidiaries is made by the chief officer of

Enron itself especially Jeff Skilling as president and COO and Enron’s board. Although in the

trading floor the decision in making deals laid at the hand of each trader.

Risk Mitigation:

To manage all of the risks in Enron and to prevent so that the risks will not happen

again, Enron needs mitigation like this:

- People

Risk:

hire new

trust

people

Type Of Risk Risk Mitigation

Market Risk Transfer

Liquidity Risk Control

Credit Risk Transfer

Leverage Operational

Risk

Avoid

Process Risk Control

Accounting Risk Avoid

System Risk Avoid

People Risk Control

to execute every problems that will face the company. Create a strong monitoring

system by giving every employee trust when they see something wrong, they can

directly go to board members.

- Process Risk: Create the system of transparency and implied good corporate

governance (GCG) by implement opennes culture and embarce their auditors to do

their role (which is not tolerate on creative accounting).

- Liquidity Risk: don’t make an obligation or borrow money too much because the

debt levels of Enron was so high and had reached the limits.

Risk Monitoring:

From the case, we found Enron trying to do sell or transfer risk by creating SPVs and Raptor

mechanism, this is not uncommon in business world. However, to do that Enron need some

prequisite before go and dump the debt using this method. Companies desire to buy and sell

risk has increased in recent years and has extended to a much wider range of risk than in the

past. There are increasing opportinities to sell risk but at the time that companies are looking

to lay off risk the prices rises and the number of potential buyer’s declines.

The prequisites Enron’s need are:

The risk must be clearly defined; corporate bonds or mortgage backed securities.

Riskiness must be quantifieable; Triple A rated bonds or junk bonds.

Legal documentation must be in place – in order to ensure rights and obligations are

well defined.

The price is right – the buyer must pay a price that leaves the seller with a profit

(unless the seller expect the risk to deteriorate and wants to cut his losses).

Now, as we know Enron’s prequisites we found management actions regarding risk

monitoring is quite reckless and endanger company position by doing:

Not defined risk clearly – Enron has a large risk assesment and control group, headed

by chief risk officer (CRO), however sometimes the level of activity was such that it

had time to do little more than check arithmethic rather than to question the

underlying assumptions.

Unquantifieable riskiness – The Enron solution regarding the investment grade is by

using getting off the assets and related debt from balance sheet. This process created

by using SPEs and because of its complexity, it become difficult to quantified its

riskiness.

Do not have legal document in the place – The comitte investigate Enron case stated

that they were denied to access to Andersen personnel and papers. This is a problem

since Andersen is public auditor, and Power’s comitte have a rights to understand

about Enron cases.

The price has become a junk – Dynergy Inc., Enron’s rival, has try to become the

White Knight by bid to acquire Enron. But withdrew it after doing some due

diligence. Most financial analyst still think that the Enron’s stock still worth “hold”

or “buy” position, however a rating agency already stamp Enron’s debt to “Junk”

(Ca).

By seeing the unfulfilled prequisite above we can see that Enron’s case is not applying good

monitoring procees. Froot, Scharfstein, and Stein (1994) stated that there are three basic

premises of risk management, which are:

The key to creating corporate value is making good investments

The key to making good investments is generating enough cash internally to fund

those investments. When companies do not generate enough cash, they tend to cut

investment more drastically than their competitors do.

Cash flow – so crucial to the investment process – can often be disrupted by

movements in external factors such as exchange rates, commodity prices, and interest

rates, potentially compromising a company’s ability to invest.

The change condition that derived

from external factor such as market

demand, government regulation, and

environmental effect could change the

way of company manages the risk. So it

is important for company to do evaluation

and monitoring to ensure the

sustainability of managing the risk itself. Review process and feedback loop

This review process could use time framework as shown in figure above. The company

monitors the result from tactical plan and review the decision outcome of it. When the risk

exposure is increase or the mitigation process has not effective, the risk holder as the person

who burden the risk would introspect the risk loop to made better decision until satisfy the

KRI (Key Risk Indicator) board member’s demanded.

Conclusion and Recommendation

1. Our recommendation Enron should mitigate the risk:

2. With the

risk

calculator method show that Enron have 37 point, it means Enron in DANGER

ZONE. Enron must prepare any risks created by pressure due to growth, pressure due

to culture and pressure due to information management. In fact this company declared

bankruptcy in December 2001.

3. The problem for Enron was that those who had invested had been promised and

expected to get more money from selling gas and electricity and this was not

happening. In this position it sought to hide the truth from the public and borrow more

money to fill the hole. A blatant fraud was concocted to create the illusion of real

money, but those involved did not see it as fraudulent. They were shielded by the

Type Of Risk Risk Mitigation

Market Risk Transfer

Liquidity Risk Control

Credit Risk Transfer

Leverage Operational

Risk

Avoid

Process Risk Avoid

Accounting Risk Avoid

System Risk Avoid

People Risk Control

legitimacy given to the arrangements by the marketplace and by the complicity of

Enron's partners, the banks and the accountants. They designed and implemented the

fraud on Enron's behalf.

References

Olsson, Carl. Risk Management in Emerging Markets: How to Survive and Prosper, Prentice

Hall, 2002

Simmons, Robert. How Risky Is Your Company. Harvard Business Review, 1999

Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein, 1994. A Framework for Risk

Management. Harvard Business School Publishing, Boston.