epa’s new environmental s new environmental requirements: how will they impact the power...

TRANSCRIPT

EPA’s New Environmental Requirements: How Will They Impact the Power Sector?

National Conference of State Legislatures Webinar

November 3, 2011

Daniel Chartier

Director, Environmental Markets & Air Quality Programs

Electric Companies Use a Diverse Mix

Of Fuels to Generate Electricity

*Includes generation by agricultural waste, landfill gas

recovery, municipal solid waste, wood, geothermal,

non-wood waste, wind, and solar.

** Includes generation by tires, batteries, chemicals, hydrogen,

pitch, purchased steam, sulfur, and miscellaneous

technologies.

Source: U.S. Department of Energy, Energy Information

Administration, Power Plant Operations Report (EIA-923); 2010

preliminary generation data.

July 2011

© 2011 by the Edison Electric Institute. All rights reserved.

2010

National Fuel Mix

2

*Includes generation by

agricultural waste, landfill gas

recovery, municipal solid waste,

wood, geothermal, non-wood

waste, wind, and solar.

** Includes generation by tires,

batteries, chemicals, hydrogen,

pitch, purchased steam, sulfur,

and miscellaneous technologies.

Sum of components may not add

to 100% due to independent

rounding.

Source: U.S. Department of

Energy, Energy Information

Administration, Power Plant

Operations Report (EIA-923);

2010 preliminary generation data.

July 2011

© 2011 by the Edison Electric

Institute. All rights reserved.

Different Regions of the Country Use

Different Fuel Mixes to Generate Electricity

3

Coal Units by Age, Capacity and Emissions U.S. Generating Units, 10 Year Increments

4

Age of Units*

Generating Units

Total Nameplate Capacity

Total Net Generation Year 2008

Total CO2 Emissions Year 2008

Total SO2 Emissions Year 2008

Total NOX

Emissions Year 2008

# Percent of Total

GW Percent of Total

GWH Percent of Total

MTons Percent of Total

Tons Percent of Total

Tons Percent of Total

0-10 Years 16 1.4% 5.3 1.6% 19,788 1.1% 28.7 1.4% 18,083 0.2% 13,779 0.5%

11-20 Years 64 5.8% 14.9 4.5% 78,261 4.2% 78.1 3.8% 137,803 1.9% 108,115 3.8%

21-30 Years 186 16.7% 86.1 26.1% 541,408 29.0% 615.0 29.6% 1,336,033 18.0% 763,207 26.9%

31-40 Years 238 21.4% 122.5 37.1% 724,206 38.8% 780.7 37.6% 2,750,025 37.1% 1,053,259 37.1%

41-50 Years 270 24.3% 60.8 18.4% 316,029 16.9% 352.2 16.9% 1,879,152 25.4% 533,038 18.8%

51-60 Years 304 27.3% 39.3 11.9% 187,473 10.0% 220.7 10.6% 1,265,388 17.1% 356,902 12.6%

61-70 Years 30 2.7% 0.9 0.3% 1,166 0.1% 2.5 0.1% 19,223 0.3% 6,554 0.2%

> 70 Years 4 0.4% 0.0 0.01% 5 0.0003% 0.1 0.004% 87 0.001% 484 0.02%

Coal Unit Totals

1,112 100.0% 329.95 100.0% 1,868,336 100.0% 2077.9 100.0% 7,405,794 100.0% 2,835,339 100.0%

Source: Ventyx, Inc.—EV Suite MTon = million tons * Does not include units that came online in 2009

Location of Coal- and Oil-Based Plants

Source: National Electric Energy Data

System (NEEDS 4.10) (EPA, December 2010) 5

Possible Timeline for Environmental Regulatory

Requirements for the Utility Industry

Ozone (O3)

PM/PM2.5

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17

Begin CAIR

Phase I

Seasonal

NOx Cap

HAPs MACT

Proposed

Rule

Revised

Ozone

NAAQS

Begin CAIR

Phase I

Annual SO2

Cap

Adapted from Wegman (EPA 2003 Updated 09-12-2011

Proposed

PM-2.5

NAAQS

Revision

PM

Transport

Rule

SO2 Primary

NAAQS

SOX/NOx

Secondary

NAAQS

NOx

Primary

NAAQS

SOx/NOx/Visibility

CAMR &

Delisting

Rule

vacated

Hg/HAPS

Transport Rule

Proposal Issued (CAIR Replacement)

HAPs MACT

Final Rule

Expected

CAIR

Vacated

HAPS MACT

Compliance

3 yrs After

Final Rule

CAIR

Remanded

CAIR/Transport

Begin CAIR

Phase I

Annual NOx

Cap

316(b)

Proposed

Rule

316(b) Final

Rule

Expected

316(b)

Compliance

1-8 yrs After

Final rule

Effluent

Guidelines

Proposed Rule

Expected

Water

Effluent Guidelines

Final Rule Expected

Effluent Guidelines

Compliance 0-5+ yrs

After Final Rule

Begin Compliance

Requirements

Under Final CCB

Rule (ground

water monitoring,

double liners,

closure, dry ash

conversion)

Ash

Proposed

Rule for

CCBs

Management

Final Rule

for CCBs

Mgmt

CSAPR Issued (CAIR/Transport

Rule Replacement)

CO2

CO2

Regulation

(PSD/BACT)

Ozone

NAAQS

Revision

CSAPR

Phase I

Reductions

CSAPR

Phase II

Reductions

Ozone

Transport

Rule

GHG NSPS

Proposal

GHG

NSPS

Final

Expected

Final PM-2.5

NAAQS

Revision

PCB Phase-out

PCB

ANPR

PCB

Proposed

Rule

Expected

PCB Final Rule

Expected (start

of phase-out

period)

EPA Notice -

Regional Haze

SIPS Overdue

BART

(Visibility)

Deadline at

Some Plants

EPA Action

on Regional

Haze/BART

GHG NSPS

Implementation

(existing sources)

6

Congressional Landscape

EPA regulations a primary focus of activity

Republicans using 3-pronged strategy to target EPA regulations:

Increase oversight – numerous hearings on EPA authority, timing and cost of rules

Decrease funding

Eliminate EPA authority

House has passed several bills (TRAIN Act, Upton bill, appropriations bills)

House has announced schedule of activity through the winter targeting individual, major rulemakings

Unlikely any major environmental legislation passes in current Congress

Republican House opposes GHG caps, additional environmental legislation

Efforts to reform environmental statutes would not survive Presidential veto even if passed by both Houses

Memories of failed effort on cap-and-trade in last Congress

7

Role of States

States have a critical role to play in environmental regulations – the feds may regulate but the states have to implement

Have to develop the specific policies and rules to implement the regulations

Have to balance the views of various interests within the state while also being one of the calmer stakeholders in the federal process

Exercise oversight in implementation

States have to provide the necessary funding for permitting and enforcement of the regulations

Slow economy and state budget issues are impacting level of resources and personnel available to implement some standards (e.g., NAAQS)

“The fiscal impact has been deep and prolonged, with fiscal year 2012 marking the fourth consecutive year that states face significant mismatches between revenue and spending” – State Budget Update: Summer 2011 (NCSL)

Loss of ARRA funds; PUC budget cuts

8

Power Sector Objectives

Minimize economic impacts to consumers

Continue environmental improvements

Maintain system reliability

Maintain fuel diversity options

Develop and deploy new technologies

Obtain access to capital and cost recovery

Negotiate myriad political landscapes

9

Power Sector Objectives (2)

Power sector has been proactive in addressing these regulations

Have tried to carry a positive message – want to comply with regulations and make necessary reductions

Important that it be done cost-effectively and minimize economic impacts to consumers

Diversity of views within industry

CEOs have taken active role in development of EEI positions

10

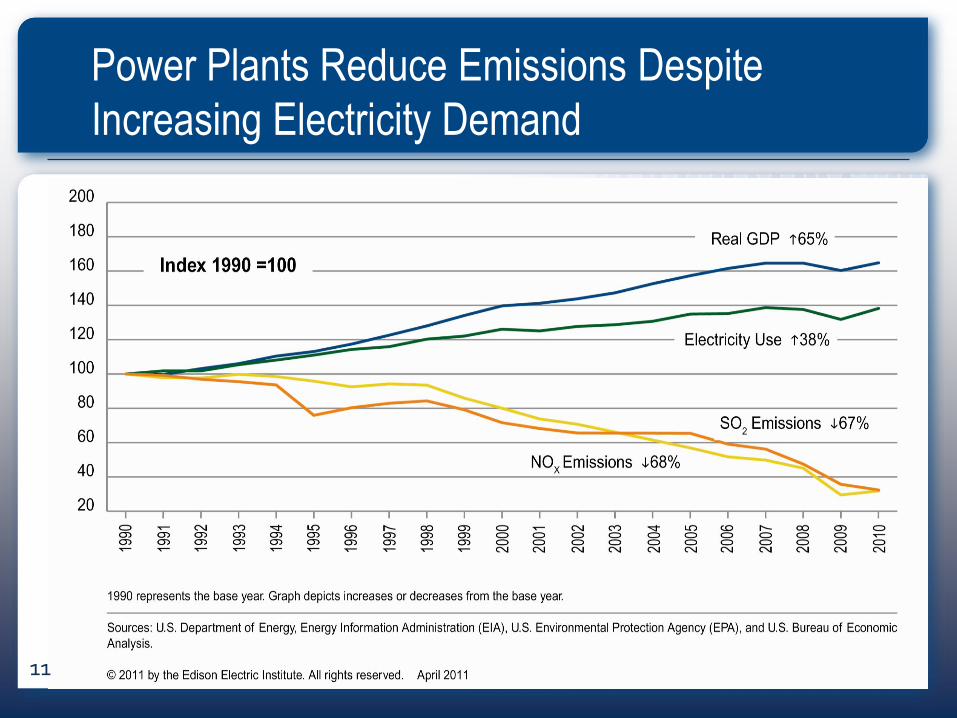

Power Plants Reduce Emissions Despite

Increasing Electricity Demand

11

Utility MACT Regulation

Proposed in March 2011; final rule due by December 16, 2011

3-yr compliance timeline after final rule; states/EPA have authority to grant 1-yr extension under limited circumstances

Key Issues

Compliance timeline

Use of filterable PM as surrogate for non-mercury metals

DSI may not be viable option for all coal units

Mercury standard should be based on best 12% average

Monitoring and verification requirements should be streamlined

Work practice standards for limited use oil-based units, and for startup and shutdown

New unit standards should be based on technology at existing sources

Allow broad emissions averaging as alternative compliance mechanism

12

Utility MACT Regulation (2)

Annualized compliance costs to power industry estimated at $10.9 billion (2007$) in 2015, and ~$10 billion in 2020 and 2030

EPA projects ~10 GW of coal-based generation may retire by 2015

EPA projects the installation of:

81 GW of dry scrubbing controls

93 GW of activated carbon injection

166 GW of fabric filters (baghouses)

EPA projects this rule will yield annual monetized benefits of $59-140 billion (2007$) using a 3-percent discount rate

CEO-level activity having an impact on rulemaking:

Develop consensus on EEI issues

Extensive discussion on advocacy; extensive state and beltway-focused strategies in play

13

Transport Rule

Final Transport Rule signed July 6, 2011

Proposal affects power companies in 31 eastern states

Emission budgets for NOx and/or SO2 (both for most states)

Supplemental proposal (July 11) to add NOX ozone season requirements for IA, KS, MI, MO, OK, WI (OK = 28th state)

Some EEI members can meet requirements, others have concerns:

Must be met only 6 and 30 months after rule is finalized

Provides little long-term certainty – requirements will be superseded by subsequent Transport Rules addressing potential changes to PM and ozone standards

Constraints on emissions trading

Numerous legal challenges have been filed 14

Cross-State Air Pollution Rule

15

Cooling Water Intake Structures 316(b)

Proposed rule signed March 28, 2011; EPA is required to finalize the rule by July 27, 2012

In general, the rule sets separate standards for impingement mortality and entrainment mortality for units with design intake rates above 2 million gallons per day (MGD)

The proposed rule leaves much to the discretion of the permit writer (and the EPA Region that reviews the permit)

EPA estimates the total annualized cost of the rule at $384.8 million; benefits = $18 million; cost-benefit ratio ~21:1

EEI and its allies having positive impact on rulemaking

16

Cooling Water Intake Structures – 316(b) Rule

17

Coal Combustion Residuals (CCR)

Co-proposal of two options in June 2010 (75 Fed. Reg. 35128):

Subtitle C, “Special” hazardous waste listing; Subtitle D regulations

Beneficial use exempt from regulation

Comments submitted Nov. 2010; Final Rule expected 2012

Subtitle C option would reverse 1993 & 2000 Regulatory Determinations

Majority of states, ash recyclers, industry groups, large number in Congress oppose hazardous waste regulations

Will significantly impact operations: closure of ash ponds, construction of additional disposal capacity, reductions in beneficial use

EEI and its allies having positive impact on rulemaking

18

GHG Regulation

Motor vehicle GHG regulation forced stationary source GHG regulation

EPA Tailoring Rule modified permitting rules to exclude small sources (at least for several years)

Legal basis uncertain – numerous lawsuits because CAA reinterpreted by EPA

Affected sources subject to Best Available Control Technology (BACT) reviews as of January 2011

Inherent uncertainty; states issue permits on case-by-case basis

GHG NSPS being developed for fossil power generators and refineries, including for existing sources

Draft rule due in July, now likely out in December 2011

19

National Ambient Air Quality

Standards (NAAQS)

1-hour NO2 and SO2 standards revised in 2010

EPA expected to tighten PM and ozone standards in 2012 and 2013, respectively:

New PM and ozone standards will drive additional new Transport Rules

Ozone review delayed until 2013 by President (September 2)

NAAQS continually ratcheted down over time:

Ozone – 1994, 2008, 2011

PM2.5 – 1997, 2006, 2012

State Implementation Plans: EGUs in bulls-eye due to perceived cost-effectiveness

20

Industry Next Steps

Have to retrofit, retire or repower virtually every coal plant Estimates of retirements vary widely

Impacts on reserve margins

~48 GW of coal-fired generation retirements have been announced already; ceiling may be ~60-80 GW Take place between 2010 and 2022

Most will be 50-60 years old upon retirement

Due to fuel and/or compliance costs, consent decrees, age, etc.

Some will be replaced with natural gas

Will require significant amount of investment; potential impacts on power prices

Continued active oversight and engagement by CEOs

21

Utility Power Plants Closing Coal Units Between 2010 -2022

22

Contact Information

Daniel Chartier

Director, Environmental Markets & Air Quality Programs

202-508-55710

23