epistar corporation

TRANSCRIPT

~2~

【【【【Translation】】】】

Stock code: 2448 EPISTAR CORPORATION

2019 Annual General Shareholders’ Meeting

Meeting Agenda

Meeting Time: 9:00 a.m. on Thursday, June 20, 2019

Place: Conference Room 101, Association of Industries in Hsinchu Science

Park (No.2, Zhanye 1st

Rd., Hsinchu City, Taiwan) 2019 Annual General Shareholders’ Meeting check website:

1. MOPS website: http://mops.twse.com.tw

2. EPISTAR CORPORATION website: http://www.epistar.com.tw

Table of Contents

ⅠⅠⅠⅠ.Procedures for the 2019 Annual General Shareholders’ Meeting………....................... 1

ⅡⅡⅡⅡ. Agenda of the 2019 Annual General Shareholders’ Meeting………………..................... 2

1. Report Items……………………………………………………………………………………................... 3

2. Approval Items………………………………………………………………………............................. 5

3. Election Item………………………………………………………................................................ 6

4. Discussion Items………………………………………………………........................................... 7

5. Extemporary Motions……………………………………………………………………….................. 14

6. Adjournment………………………………………………………………………………………………………. 14

ⅢⅢⅢⅢ. Attachments

Attachment 1: 2018 Business Report……………………………………………………………………… 15

Attachment 2: Audit Committees’ Review Report………………………………………………….. 17

Attachment 3: Rules for the Repurchase of Shares and Transfer to Employees……… 18

Attachment 4: Amendments to the Rules and Procedures for the Board of

Directors' Meeting………………………………………………………………………….. 20

Attachment 5: 2018 Report of Independent Accountants and Financial Statements 30

Attachment 6: 2018 Deficit Compensation Statement…………………………………………… 58

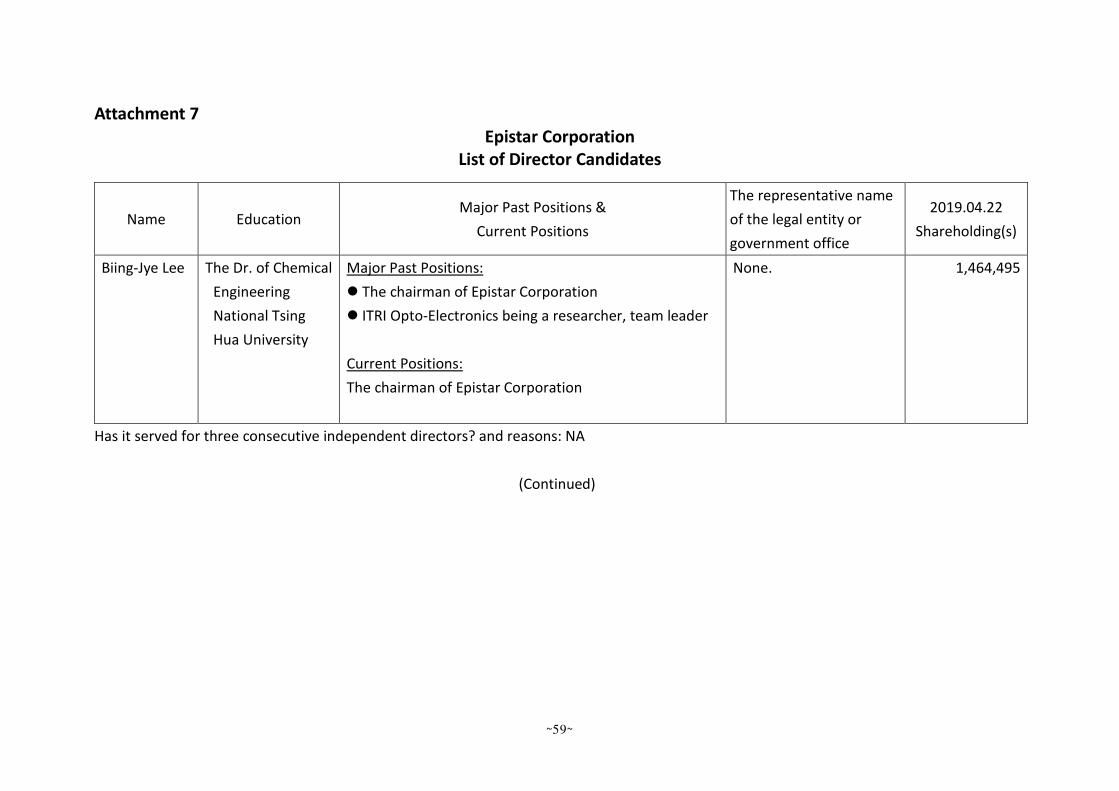

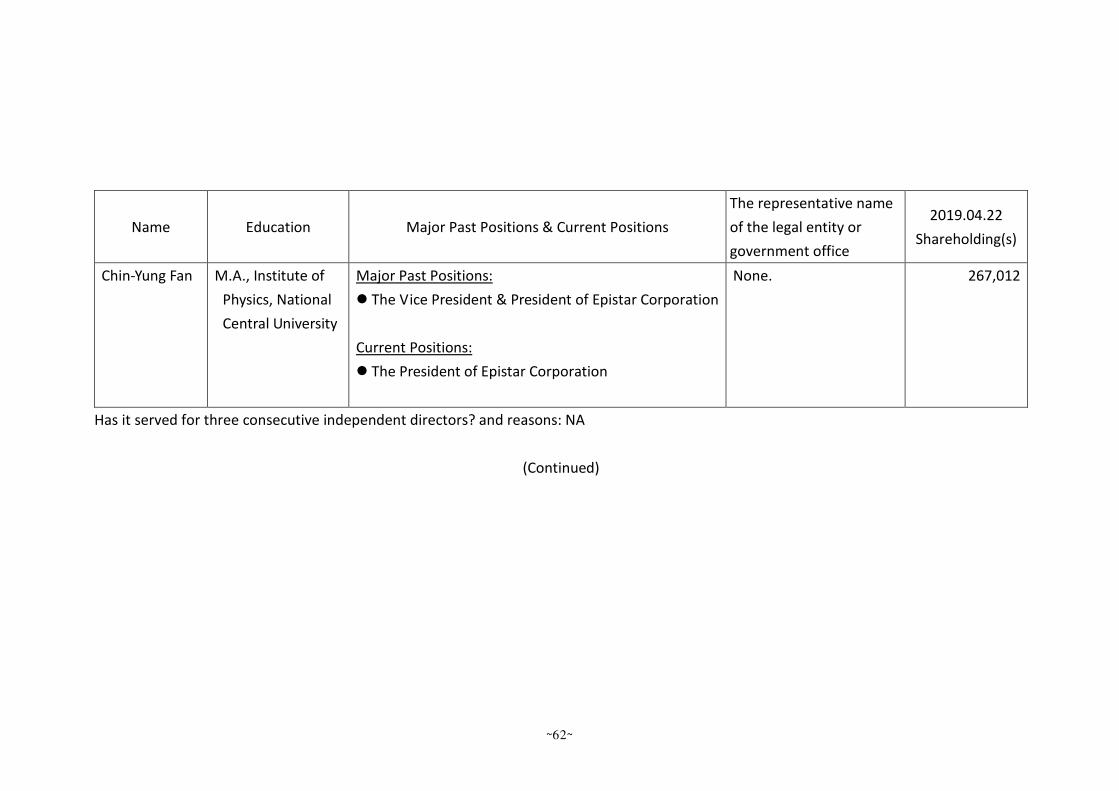

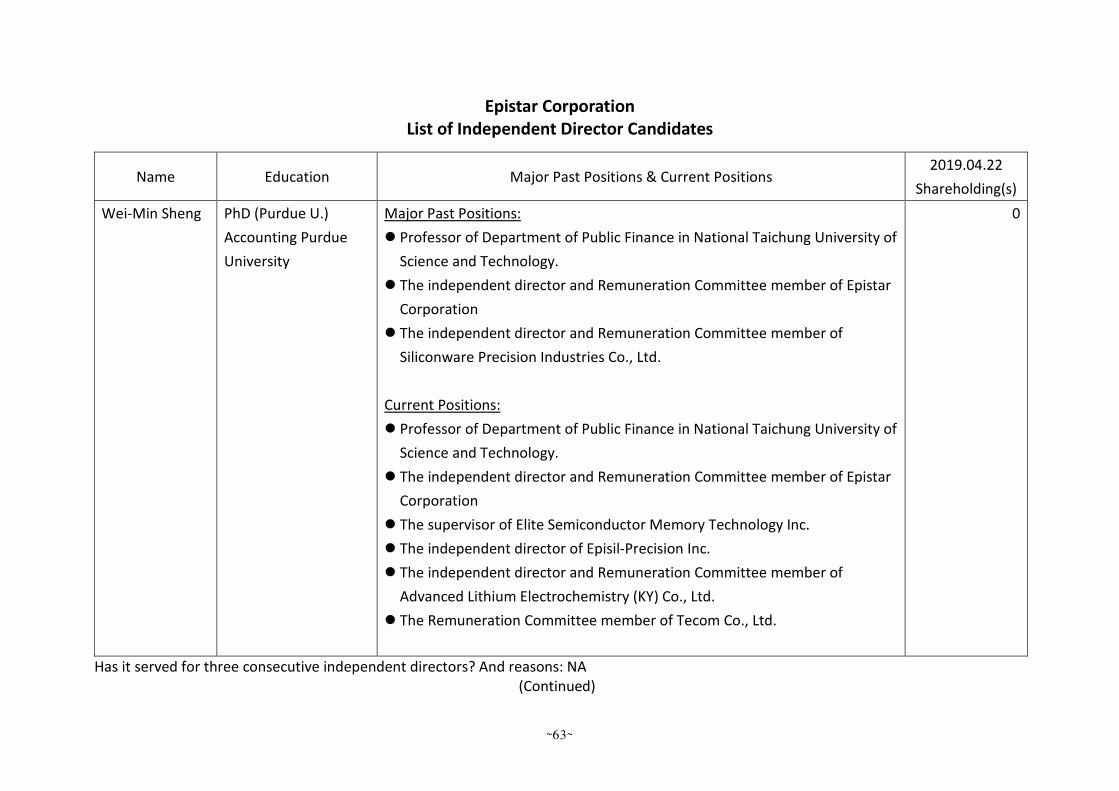

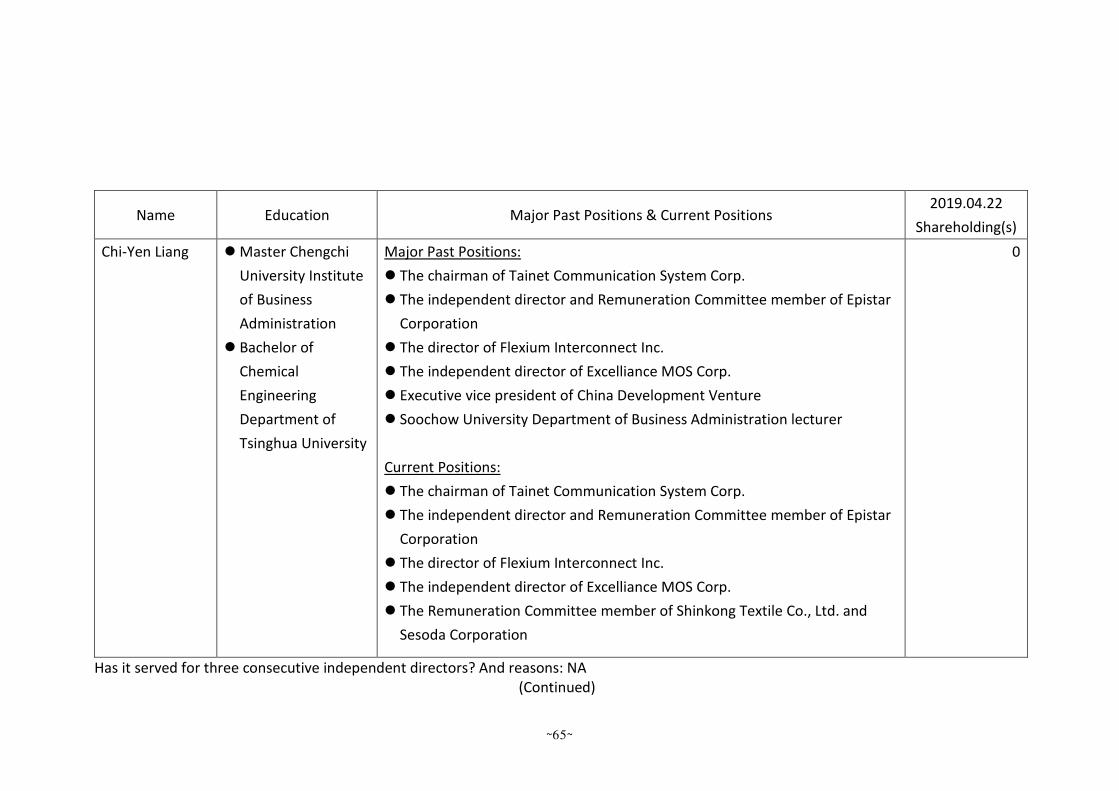

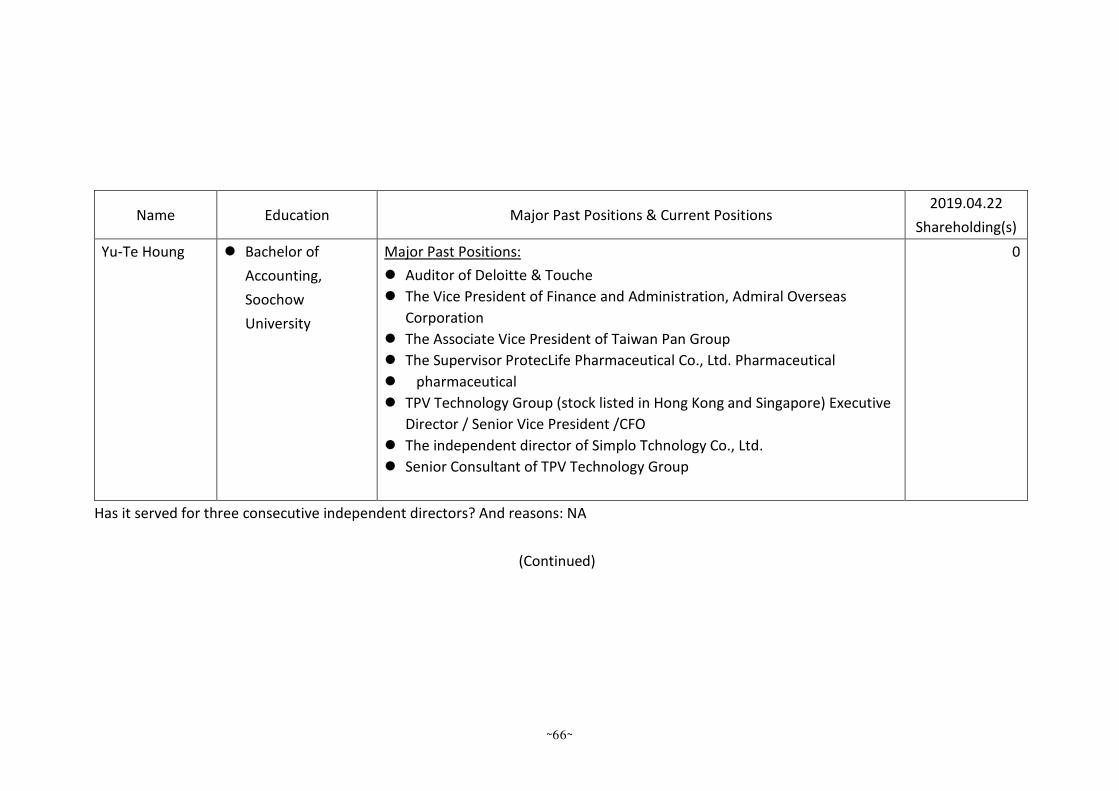

Attachment 7: List of Director (Including independent Director) Candidates………… 59

Attachment 8: Amendments to the Articles of Incorporation………………………………… 68

Attachment 9: Amendments to the Acquisition or Disposal Procedures of Assets.… 80

Attachment 10: Amendments to the Procedures for Loaning Funds to Other Parties. 117

Attachment 11: Amendments to the Procedures for Endorsements and Guarantees.. 124

Attachment 12: List of releasing the directors from non-competition restrictions…….. 131

ⅣⅣⅣⅣ. Appendixes

Appendix 1: Articles of Incorporation………………………………………………………………… 135

Appendix 2: Rules for the Procedure of the Shareholders’ Meeting..................... 141

Appendix 3: Rules for Elections of Directors and Supervisors…………………………….. 145

Appendix 4: Related Information on Remuneration to Directors and Employees. 147

Appendix 5: The Impact of Stock Dividend Issuance on Business Performance,

EPS, and Shareholder Return Rate………………………………………………….. 147

Appendix 6: Related Information on Proposals and Nominations from

Shareholders owning 1% or more of the issued shares of the

Company………………………………………………………………………………………… 147

Appendix 7: Current Shareholding of Directors…………….…………………………………… 148

~1~

EPISTAR CORPORATION

Procedures for the 2019 Annual General Shareholders’ Meeting

1 . Call the Meeting to Order

2 . Chairman’s Address

3 . Report Items

4 . Approval Items

5 . Election Item

6 . Discussion Items

7 . Extemporary Motions

8 . Adjournment

~2~

EPISTAR CORPORATION

Agenda of the 2019 Annual General Shareholders’ Meeting

i. Time: 9:00 a.m., Thursday, June 20, 2019 ii. Place: Conference Room 101, Association of Industries in Hsinchu Science Park (No.2, Zhanye

1st Rd., Hsinchu City, Taiwan (R.O.C.)). iii. Call the Meeting to Order iv. Chairman’s Address v. Meeting Items

1. Report Items

(1) The 2018 Business Report.

(2) Audit Committee's report of 2018 audited financial report.

(3) Implementation Report on the Issuance of the Common Stocks through Private

Placement which approved by the 2018 Annual General Shareholders' Meeting.

(4) Implementation Report on the repurchase of the Company’s common stocks.

(5) Amendments to the Rules for the Conduct of the Board of Directors' Meeting.

(6) Status of Endorsements and Guarantees as of the End of 2018.

2. Approval Items

(1) 2018 Business Report and Financial Statements.

(2) Proposal for 2018 Deficit Compensation.

3. Election Item

(1) To elect 9 directors of the 10th term of the Board of Directors.( including 5

independent directors)

4. Discussion Items

(1) Cash Distribution of the Capital Surplus to Shareholders.

(2) Amendments to the Articles of Incorporation.

(3) To amend "Acquisition or Disposal Procedures of Asset".

(4) To amend "Procedures for Loaning Funds to Other Parties".

(5) To amend "Procedures of Endorsement and Guarantee".

(6) To approve issuance of new common shares for cash to sponsor issuance of the global

depositary receipt and/or issuance of new common shares for cash in private

placement.

(7) To release the newly elected directors from non-competition restrictions.

5. Extemporary Motions

6. Adjournment

The Chairman may rule to vote on the case or to vote on the whole or part of the proposal before

the extemporary motion proceeds.

~3~

1. Report Items

(1) The 2018 Business Report.

(Proposed by the Board of Directors)

Explanation:

The 2018 Business Report is attached hereto as Attachment 1 (pages 15-16).

(2) Audit Committee's report of 2018 audited financial report.

(Proposed by the Board of Directors)

Explanation:

The Audit Committee’s Review Report is attached hereto as Attachment 2 (page 17).

(3) Implementation Report on the Issuance of the Common Stocks through Private Placement

which approved by the 2018 Annual General Shareholders' Meeting.

(Proposed by the Board of Directors)

Explanation:

Capital injection by issuance of 160 million shares of common stocks through private

placement had been terminated by the resolution of the Board of Directors meeting on

March 14th, 2019 due to lack of qualified strategic investor can be found before the expiry

date on June 20th, 2019.

(4) Implementation Report on the repurchase of the Company’s common stocks.

(Proposed by the Board of Directors)

Explanation:

A. In order to encourage its employees, the Board of Directors meeting on November 12,

2018 resolved the share repurchase and transfer to employees. The Rules for the

Repurchase of Shares and Transfer to Employees is attached hereto as Attachment 3

(page 18-19).

B. Status of repurchases are listed below:

The period November 13, 2018 ~ January 12, 2019

Repurchased price range NT$25~NT$40. When the Company's stock price

is below the set floor price, the Company will

continue its exercise plan.

The actual number of shares

repurchased

7,800,000 shares.

Ratio of the shares to be repurchased to total

issued shares of the Company is 0.72%

The actual total monetary

amount of the share repurchased

NT$ 190,327,325

Average repurchase price NT$ 24.4

The status of transferred 0 share.

~4~

(5) Amendments to the Rules for the Conduct of the Board of Directors' Meeting.

(Proposed by the Board of Directors)

Explanation:

A. It is resolved by the Board of Directors to revise part of the articles of 「the Rules for the

Conduct of the Board of Directors' Meeting」of the Company to comply with the

amendment of Company Act and the amendment of Article 15 and Article 20 of Taiwan

Stock Exchange Corporation Operation Directions for Compliance with the Establishment

of Board of Directors by TWSE Listed Companies and the Board’s Exercise of Powers.

B. The Company hereby proposes to amend the Rules for the Conduct of the Board of

Directors' Meeting. Comparison Table for Amendments is attached hereto as

Attachment 4 (page 20-29).

(6) Status of Endorsements and Guarantees as of the End of 2018.

(Proposed by the Board of Directors)

Explanation:

A. The Company provided endorsements and guarantees for the finance of its wholly

owned subsidiary, Episky Corporation (Xiamen) Ltd. The balance of endorsements and

guarantees amounted to US$83,000,000 and RMB$72,000,000 as of December 31st,

2018.

B. The Company provided endorsements and guarantees for the finance of its 86.97%

owned subsidiary, Jiangsu Canyang Optoelectronics Ltd. The balance of endorsements

and guarantees amounted to US$13,000,000 as of December 31st, 2018.

~5~

2. Approval Items

(1) 2018 Business Report and Financial Statements.

(Proposed by the Board of Directors)

Explanation:

A. The 2018 Business Report and Financial Statements were approved by the Board of

Directors’ Meeting on March 14, 2019 and reviewed by the Audit Committee. The Audit

Committee’s report was issued accordingly.

B. The 2018 Business Report, Audit Report from the Certified Public Accountant (CPA) and

Financial Statements are attached hereto as Attachments 1 and 5 (pages 15-16 and

pages 30-57).

Resolution:

(2) Proposal for 2018 Deficit Compensation.

(Proposed by the Board of Directors)

Explanation:

A. The 2018 net loss after tax was approximately NT$ 456,146 thousand.

B. The Deficit Compensation Statement is attached hereto as Attachment 6 (page 58).

Resolution:

~6~

3. Election Item

(1) To elect 9 directors of the 10th term of the Board of Directors.( including 5 independent

directors)

(Proposed by the Board of Directors)

Explanation:

A. The Company will elect the 10th term of Directors during the 2019 Annual General

Shareholders’ Meeting. Nine directors will be considered for the Board. The term for

elected Directors is three years, starting from June 20th, 2019 to June 19th, 2022.

B. The Company have established an Audit Committee pursuant to the R.O.C. Securities and

Exchange Act. The Audit Committee is composed of all independent directors.

C. Please refer to Attachment 7 (page 59-67) for personal information of Director

Candidates.

Resolution:

~7~

4. Discussion Items

(1) Cash Distribution of the Capital Surplus to Shareholders.

(Proposed by the Board of Directors)

Explanation:

A. Pursuant to Article 241 of the Company Act, the Company plans to distribute

NT$324,270,423 as dividend in cash. It shall be allocated from the capital surplus derived

from the capital increase in which the new shares were issued with the amount

exceeding the par value. It shall be distributed in accordance with the share amounts

held by the shareholders as registered in the roster of shareholders on the record date of

the dividend distribution. The distribution calculation shall be rounded up to the nearest

NT dollar.

B. As calculated on the basis of the number of shares issued by the Company as of March

6th, 2019, eligible share for distribution was 1,080,901,410 in total, the cash dividend

shall be NT$0.3 per share.

C. It is proposed that shareholders’ meeting resolve to authorize chairman to set up the

date of ex-dividends and other relevant issues. If the dividend ratio is affected by the

change of the numbers of outstanding shares of the company, the chairman of the

Board of Directors is fully authorized to conduct necessary process.

Resolution:

(2) Amendments to the Articles of Incorporation.

(Proposed by the Board of Directors)

Explanation:

A. To comply with the amendments of the Company Act amended by the Republic of China

on August 1st, 2018 and operational requirements of the Company, the Company hereby

proposes to amend the Articles of Incorporation.

B. Comparison Table for Amendments is attached hereto as Attachment 8 (page 68-79).

Resolution:

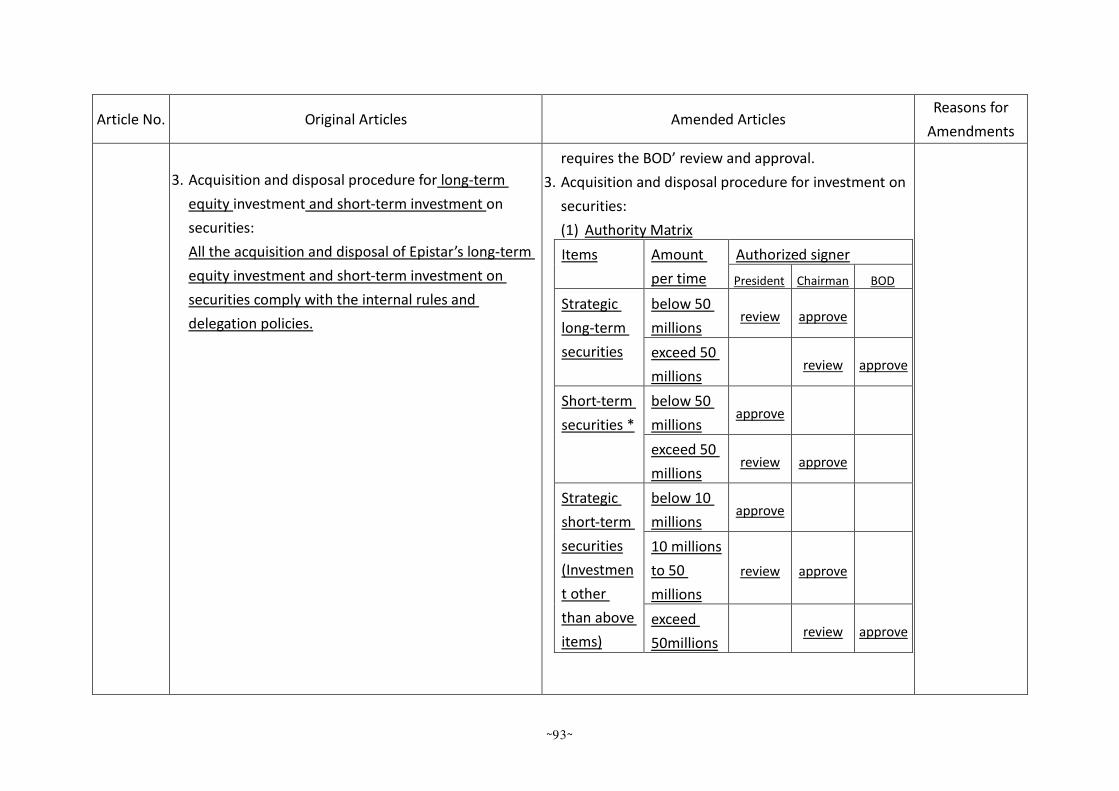

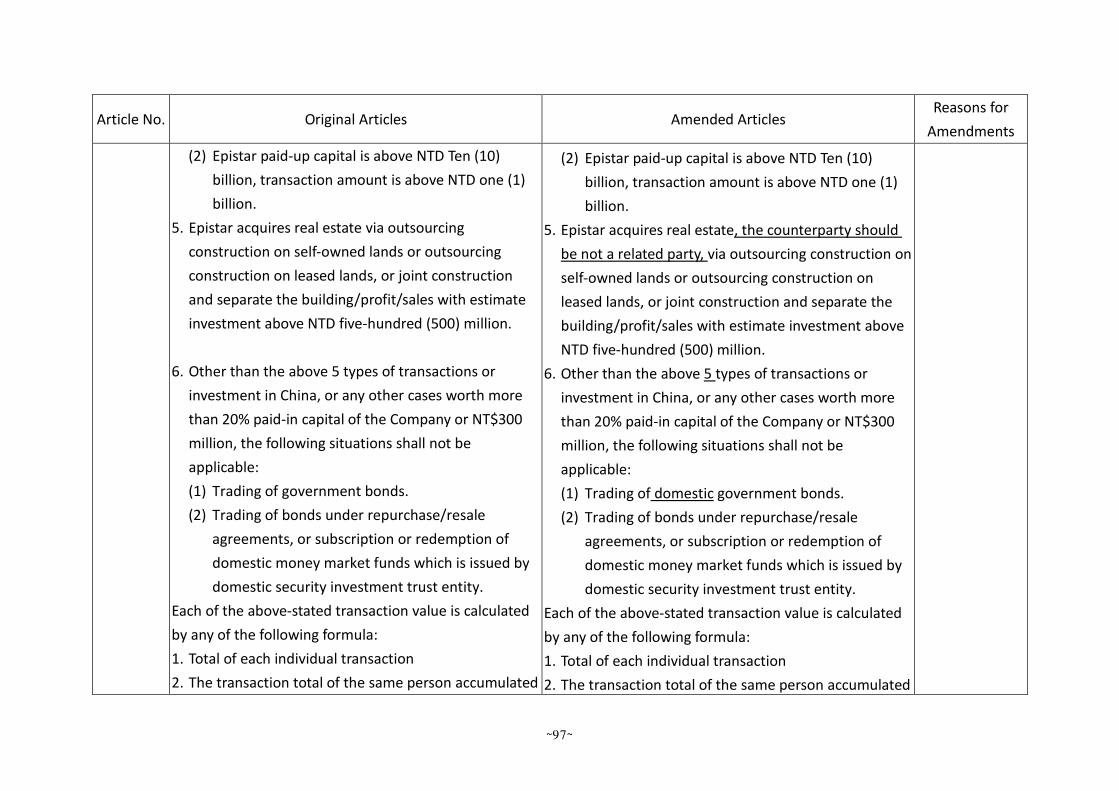

(3) To amend "Acquisition or Disposal Procedures of Asset".

(Proposed by the Board of Directors)

Explanation:

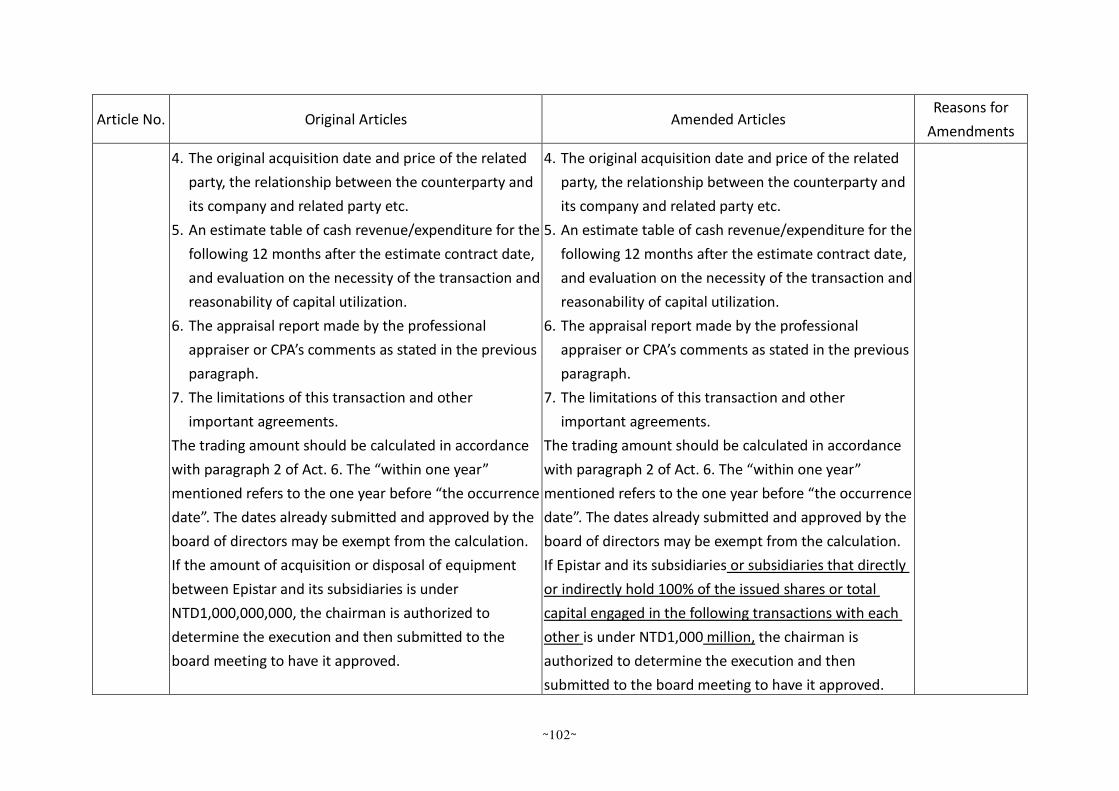

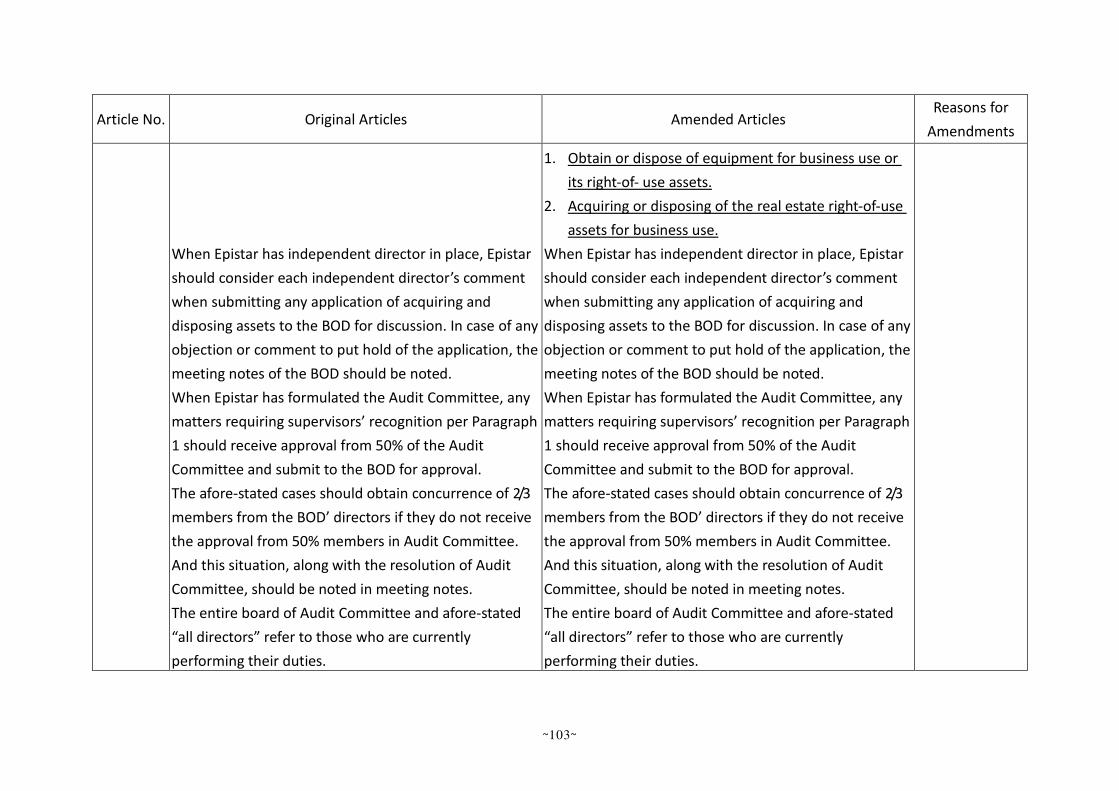

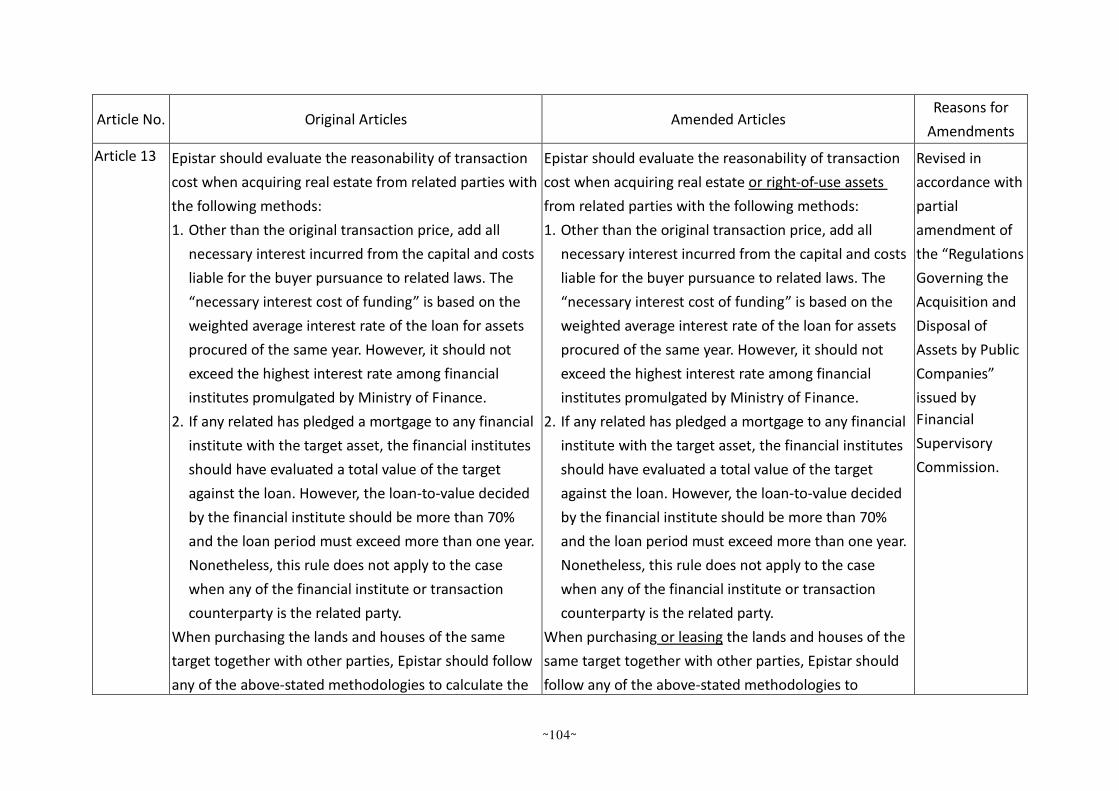

A. Pursuant to the amendments of Regulations Governing the Acquisition and Disposal of

Assets by Public Companies issued per the Order No. 10703410725 of The Financial

Supervisory Commission dated on November 26th, 2018, and to slightly revise crossing

check Investment quota, authorization level and an execution unit in the “management

procedure of the long-term and short-term investment of the company” according to

business operation situation and merge into “Acquisition or Disposal Procedures of

Asset”, then the “management procedure of the long-term and short-term investment of

the company” is abolished.

~8~

B. Comparison Table for Amendments is attached hereto as Attachment 9 (page 80-116).

Resolution:

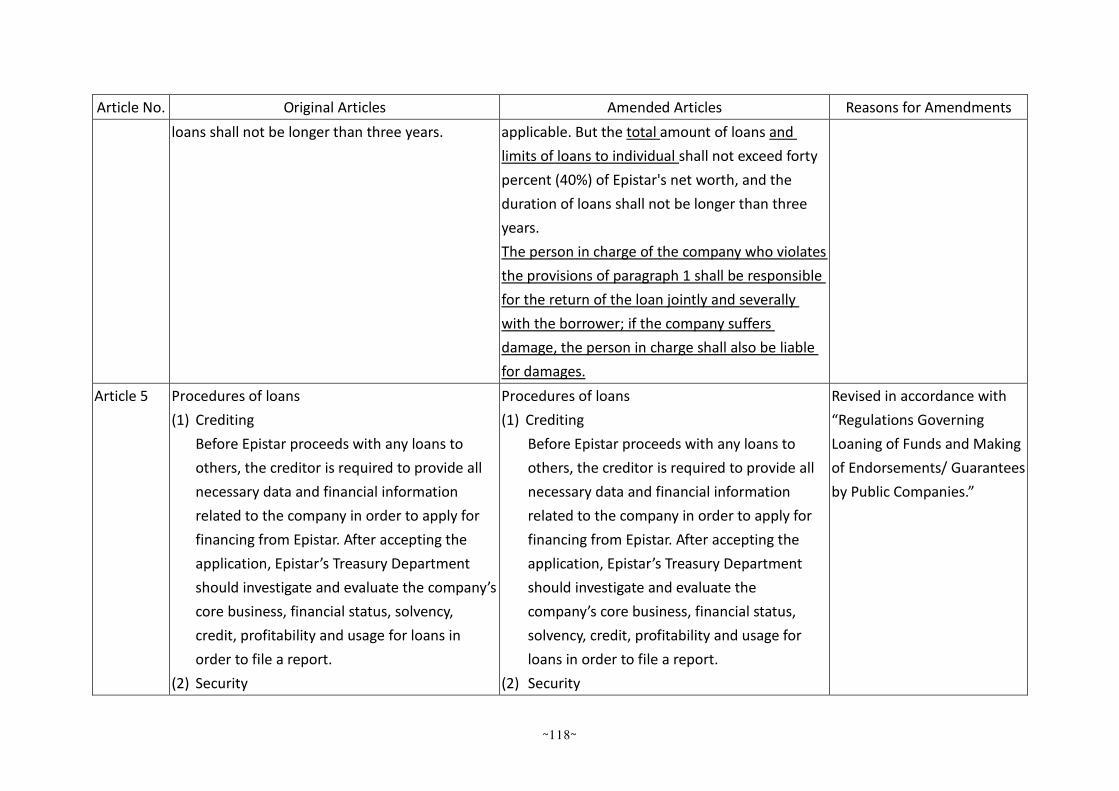

(4) To amend "Procedures for Loaning Funds to Other Parties".

(Proposed by the Board of Directors)

Explanation:

A. The amendment is based on the amendments of the Regulations Governing Loaning of

Funds and Making of Endorsements/Guarantees by Public Companies promulgated by

Financial Supervisory Commission on March 7th, 2019 (Ref. 1080304826)

B. Comparison Table for Amendments is attached hereto as Attachment 10 (page 117-123).

Resolution:

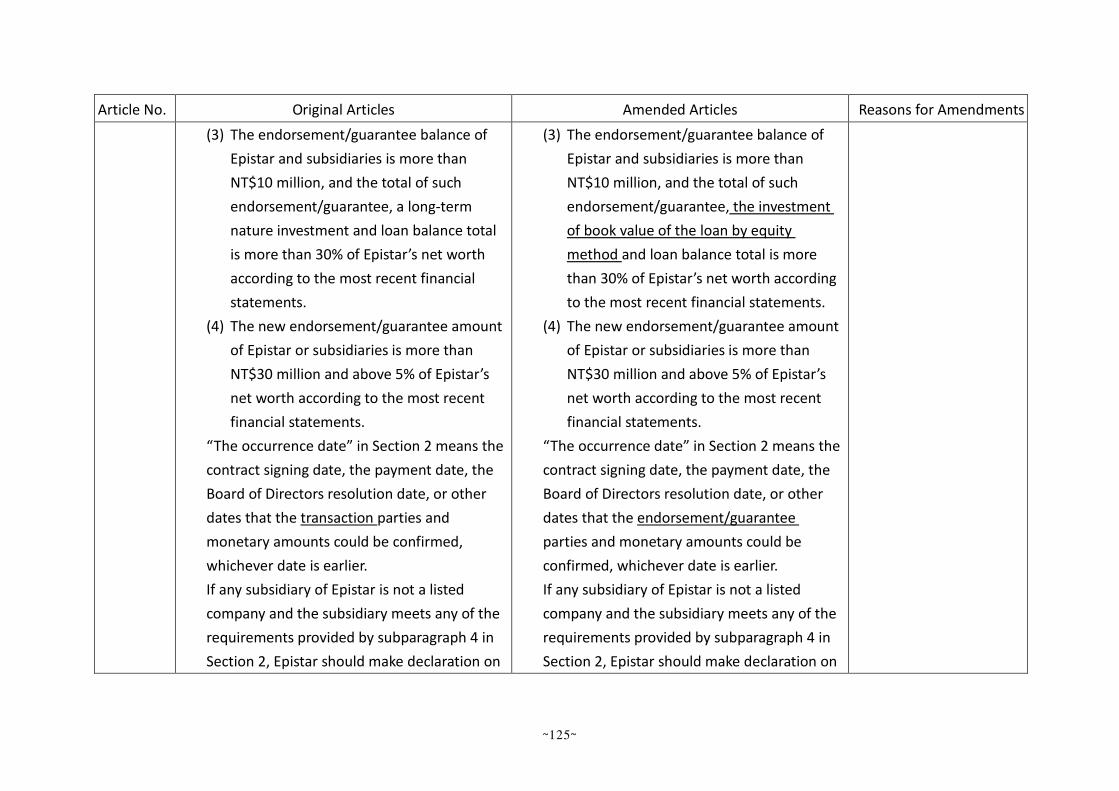

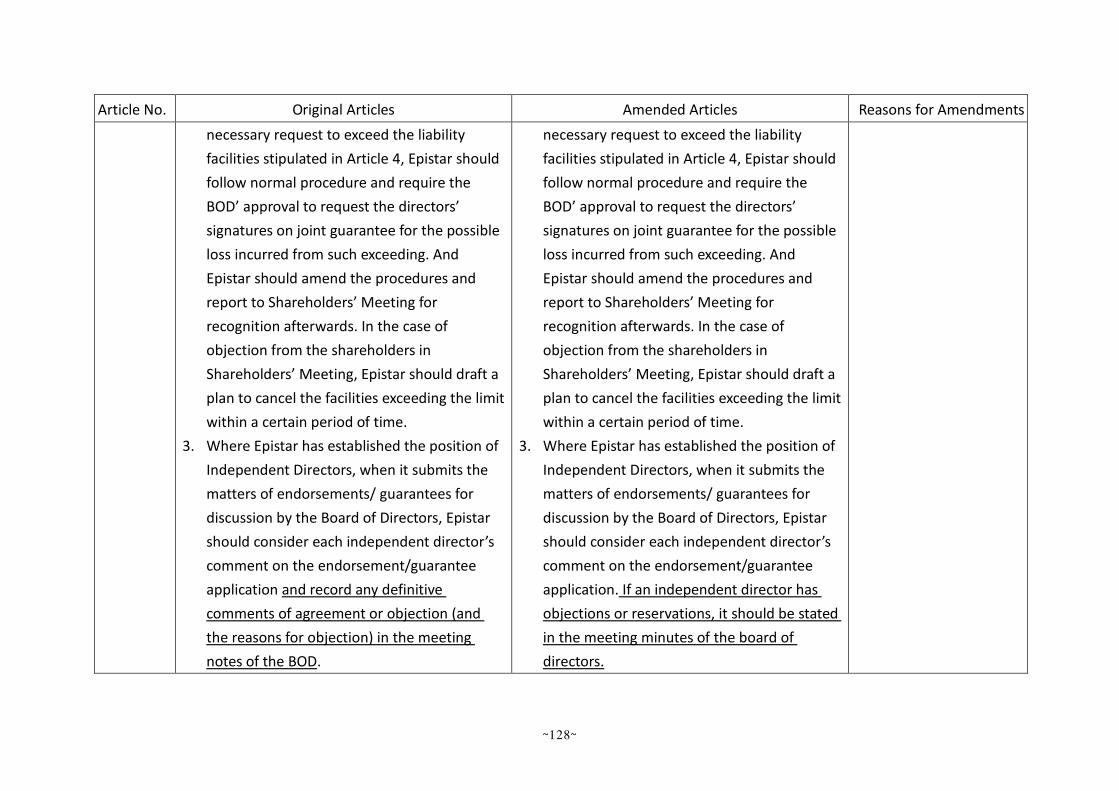

(5) To amend "Procedures of Endorsement and Guarantee".

(Proposed by the Board of Directors)

Explanation:

A. The amendment is based on the amendments of the Regulations Governing Loaning of

Funds and Making of Endorsements/Guarantees by Public Companies promulgated by

Financial Supervisory Commission on March 7th, 2019 (Ref. 1080304826)

B. Comparison Table for Amendments is attached hereto as Attachment 11 (page 124-130).

Resolution:

(6) To approve issuance of new common shares for cash to sponsor issuance of the global

depositary receipt and/or issuance of new common shares for cash in private placement.

(Proposed by the Board of Directors)

Explanation:

A. Because the issuance of new common shares for cash to sponsor DR Offering and/or

Issue Private Placement Shares which are approved by Annual General Shareholders’

Meeting convened on June 21st, 2018 are not executed within 12 months from the date

of approval on the last Annual General Shareholders’ Meeting, the plan of fundraising is

canceled. The Company proposes the plan of fundraising to be approved at Annual

General Shareholders’ Meeting in 2019.

B. In order to purchase machines and equipment, repay bank loans, enrich working capital,

have sound financial structure and/or finance the Company's long term development

plans, the Company plans to introduce strategic investors and diversify its fund-raising

channels so as to achieve financial flexibility, by taking into account the capital market

condition, timeliness and feasibility of fundraising, issuance cost, and/or the

development of the Company. It is hereby proposed at the shareholders’ meeting to

authorize the Board of Directors ("Board"), within the limit of 120,000,000 common

shares in total, depending on the market conditions and the Company’s capital needs, to

choose appropriate timing and fund raising method(s):

~9~

Ⅰ. To issue new common shares for cash to sponsor DR Offering and/or

Ⅱ. To issue Private Placement Shares

The number of 120,000,000 common shares represents 11.02% of the total issued shares

and 9.93% of the enlarged share capital.

C. If the method of issuing new common shares for cash to sponsor DR Offering is adopted:

Ⅰ. It will be proposed at the shareholders’ meeting to authorize the Board, within the

limit of 120,000,000 common shares, depending on the market conditions, to choose

appropriate timing and fund raising method(s), to issue new commons shares for

cash to sponsor DR Offering and/or issue Private Placement Shares.

Ⅱ. Except for 10% of the new common shares which shall be allocated for the

employees' subscription in accordance with the applicable law, it is proposed at the

shareholders’ meeting to approve the waiver of current shareholders’ rights on

subscribing the remaining shares and such remaining shares will be offered to the

public under Article 28-1 of the Securities and Exchange Act as the underlying shares

of the global depositary shares to be sold in the DR Offering. Any new common

shares not subscribed by employees of the Company shall be determined by the

Chairman, depending on the market needs, to be allocated as underlying shares of

the global depositary shares or to be subscribed by the designated person(s).

Ⅲ. The actual issue price of the new common shares for cash to sponsor DR Offering

will be decided in accordance with the relevant provisions of the Taiwan Securities

Association Regulations Governing Underwriters’ assistance in Offering and Issuance

of Securities by Issuing Companies. The price shall not be less than 90% of the

reference price (The average of the closing price of the Company’s common shares

for either 1, 3 or 5 consecutive trading days prior to the pricing date after

adjustment for bonus shares issued as stock dividends, shares cancelled in

connection with capital reduction and the cash dividends). If the relevant domestic

laws and regulations are changed, the pricing mechanism will be adjusted

accordingly. In view of the fluctuant share prices in the domestic stock market, the

actual issue price of the common shares in accordance with the preceding set mode,

will be determined by the chairman by taking reference to international practice,

international capital markets, the domestic market price and the purchase situation

summary circle etc., and by discussion with the underwriters.

Ⅳ. The common stock issuance through new commons shares for cash to sponsor DR

Offering and/or Private Placement Shares are planned to be no more than

120,000,000 shares. If the new common share issuance for cash to sponsor DR

Offering and/or Private Placement Shares is conducted, the maximum of issued

shares will amount for 9.93% of the enlarged share capital. The share issuance is

expected to improve the Company's competitiveness which will then increase

shareholders' value. Because the issue price of the new common shares will be

decided with reference to fair market value of the common shares in the form of

~10~

centralized domestic market as the basis, the existing shareholders will be able to

purchase common shares in the domestic stock market with the price close to the

issue price of the GDR without bearing exchange rate risk and liquidity risk. It should

not cause a significant impact on the existing shareholders' value.

Ⅴ. After the shareholders meeting approves the resolution of issuance of new common

shares to sponsor the DR Offering, it is proposed at the shareholders’ meeting to

authorize the Board to determine and amend, at the Board’s sole discretion, the

terms and condition of the new common shares to be issued for the DR Offering, the

plan for the use of proceeds, the schedule and projected benefits and all matters in

connection therewith, in accordance with the Company’s actual needs, market

conditions and relevant regulations and if any amendment thereto is required by the

regulatory changes or required by the regulator’s instruction or based on the

Company’s operation evaluation or change of the market conditions, the Board is

authorized to make the required amendments at the Board’s sole discretion.

Ⅵ. To complete the fund raising, the Chairman or the Chairman's designee is authorized,

on behalf of the Company, to handle all matters relating to, and sign all agreements

and documents in connection with, issuance of the new common shares to sponsor

the DR Offering.

Ⅶ. The Board is authorized to handle all matters which are not addressed herein in

accordance with the applicable laws and regulations.

D. If the method of issuing Private Placement Shares is adopted:

Ⅰ. In accordance with Article 43-6 of the Securities and Exchange Act, the Company

proposes to process capital increase in cash to issue common stocks through private

placement at appropriate timing. On the basis of the following principles and the

actual fundraising status, the Board of Directors requests to be authorized to

process the common stock issuance through private placement. The issuance shall

be processed in one or two installments within twelve months after the resolution is

approved at the Annual General Shareholders’ Meeting. The Board of Directors will

be authorized to determine the issuance amounts in each installment.

Ⅱ. The upper limit of the common share issuance through Private Placement

a. Shares issued through new commons shares for cash to sponsor DR Offering

and/or Private Placement: The number of issued shares shall not exceed

120,000,000 shares.

b. Par value per share: NT$10.

c. Total private placement amounts: To be calculated according to the final share

issue price.

Ⅲ. The Pricing Basis of Private Placement and its Reasonableness

The private placement price of the Company shall be no less than 80% of the higher

of the following two calculation bases prior to the price determination date:

a. The simple average closing price of the common stock of either the one, three or

~11~

five consecutive business day period immediately before the price

determination date, after adjustment for any distribution of stock dividends,

cash dividends, or capital reduction.

b. The simple average closing price of the common stock of the thirty consecutive

business day period immediately before the price determination date, after

adjustment for any distribution of stock dividends, cash dividends, or capital

reduction.

The determination of the actual price determination date and common stock prices

through private placement is to be authorized to the Board of Directors. The actual

price shall be no less than the price set by the resolution proposed at the Annual

General Shareholders' Meeting, and in accordance with the future market status.

The determination of the price is to be reasonable, and have no significant influence

on the value of shareholders' equities.

Ⅳ. Selection of Specific Investors

The Board of Directors proposes to be authorized the sole discretion to handle the

selection process by the Annual General Shareholders’ Meeting.

a. Selection Method

The premise of the selection of common share subscribers is to be in compliance

with Article 43-6 of the Securities and Exchange Act and related letter issued by

the Financial Supervisory Commission, R.O.C., and the share issuance will not

cause significant changes on the management control of the company. The

common share subscriber shall meet the abovementioned criteria and shall be a

strategic investor who is able to benefit the Company on business development.

b. Selection Purpose

The selection purpose is in order to upgrade technology, expand the Company's

business as its main purpose.

c. Necessity and Effects

To enhance competitiveness and develop long-term operation capacities, it is

necessary for the Company to adopt strategic investors. The Company expects to

expand its product marketing channel and benefit its business growth by

introducing strategic investors.

The Company will select the strategic investors who could bring synergies to the

company.

Ⅴ. Reasons for the Necessity of the Private Placement

The LED upstream industry chip market suffered from oversupply and it has affected

revenue and profitability, the Company will launch foundry business such as VCSEL,

GaN on Si and new product line Mini-LED this year and will consider forming strategic

cooperation with downstream strategy partners industry players. As such, the

Company requests shareholders’ approval on the mandate of issuing shares by

private placement so as to introduce strategic investors who can bring synergies to

~12~

our technology and product development and overall corporate growth.

In addition, the Company expects to expand its product marketing channel and

benefit its business growth by introducing strategic investors.

The purpose of each share issuance is to finance the collaboration on patent,

technology, and business strategy, and strengthen working capital to meet the

requirement of the Company’s operation needs.

The strategic plan will support the Company to develop new business and eventually

improve the Company’s profitability and competitive position.

We believe that it is in the best interest of the shareholders of the Company.

a. Reasons for Conducting Non-public Offerings

The company will take into account the capital market condition, timeliness and

feasibility of fundraising, issuance cost, and/or the development of the Company

when introducing strategic investors. Because the lock-up limitation of

transferring privately placed shares can ensure the long-term cooperation

between the Company and the strategic investors, and strengthen the stability

of the Company’s operation, the method of fundraising is proposed by private

placement.

b. Purposes of the Private Placement Capital and Estimated Effects

Common stock issuance through private placement is planned to be processed

in one or two installments. The purpose of each issuance is to finance the

collaboration on patent, technology, and business strategy, and strengthen

working capital to meet the requirement of the Company’s operation needs. The

proceeds of the fund will be used within three years after the completion of

fundraising. The purpose of each installment is to achieve the business growth of

the Company, lower the risk of running the Company, and increase the value of

the shareholders' equities.

Ⅵ. The Company believes that the corporate governance structure of the Board is

sufficient and comprehensive for overseeing the Company’s substantial actions and

protecting shareholders’ value. The Company has established the Audit Committee

which is exclusive for independent directors and the number of committee member

should not be less than three. The Audit Committee is currently consisted of three

independent directors. The independent directors have reviewed and agreed every

resolution to be proposed at the upcoming Annual General Shareholders’ Meeting,

including the share issue resolution. Annual General Shareholders' Meeting of 2019

will elect five(5) independent directors who constituted more than half of the seats

of the Board. The independent rate of the Board of the Company is 55.6%. We

believe the Company has sufficient independence to reduce the potential risk of

abuse of share issuance mandate by insiders to benefit themselves. The Audit

Committee will review the qualifications of potential strategic investors and assess

their capacities of creating synergies to the Company.

~13~

Ⅶ.Whether any material change in the Company’s management control occurs after

introducing strategic investors

The common stock issuance through new commons shares for cash to sponsor DR

Offering and/or Private Placement Shares are planned to be no more than

120,000,000 shares. If the new common share issuance for cash to sponsor DR

Offering and/or Private Placement Shares is conducted, the maximum of issued

shares will amount for 9.93% of the enlarged share capital. In order to enhance the

possibility of introducing diversified strategic investors, the Company plans to issue

common stocks through private placement in two installments. The diversification of

investors through this private placement will reduce the possibility of changing the

management control and protect current shareholders’ interests.

The Company will communicate with the potential share subscribers while seeking

strategic investors in accordance with the principle of not causing significant

changes in the Company’s management control.

Ⅷ. Rights and obligations of the common stock through this private placement

Rights and obligations of common stocks through private placement are generally

the same with common stocks issued by the Company. However, pursuant to Article

43-8 of the Securities and Exchange Act, with the exception of special conditions,

common stocks issued through private placement will not be freely transferred until

three years after the settlement date. An application for the public offering of

common stocks through private placement and listing on the Taiwan Stock Exchange

shall be made at least three years after the settlement date under related laws and

regulations.

Ⅸ. Should any revision to major matters regarding common stocks through private

placement be made due to a competent authority or a change of the objective

circumstance, excluding the price determination ratio, but including the issuance

terms and conditions, the issuance price, the issuance shares, the total raising capital,

the project items and progress, the expected use of funds, the expected efficacy and

any other related matters, it shall be fully authorized to the Board of Directors to

deal with.

ⅩPursuant to the letter No. 1080001050 dated on March 26, 2019, from Securities and

Futures Investors Protection Center, the Company explains as below: The main purpose of this private placement is that because of the fierce

competition in the global LED industry and the rapidly change of the overall

operating environment, the use of the core technologies of the Company to develop

existing LEDs and other III-V semiconductor products will enable the Company to

expand in different fields then to enhance profitability of the Company. Adopting

the private placement to introducing strategic investors is not only because the need

of funds, it will also enhance the Company's competitiveness and maintaining the

Company's stable growth to achieve a sustainable business by cooperating with the

~14~

Company's product-related application customers from the perspectives of

patenting, technical or strategic cooperation and enriching working capital of the

Company, it also accelerate the virtual vertical integration of the industry and

expanding product marketing channels through jointly develop products and

markets. After the private placement has been approved by the shareholders'

meeting to authorize the Board, the board of directors will assess the introduction

of strategic investors at an appropriate time and in a synergistic manner, thereby

increasing the return on equity.

Resolution:

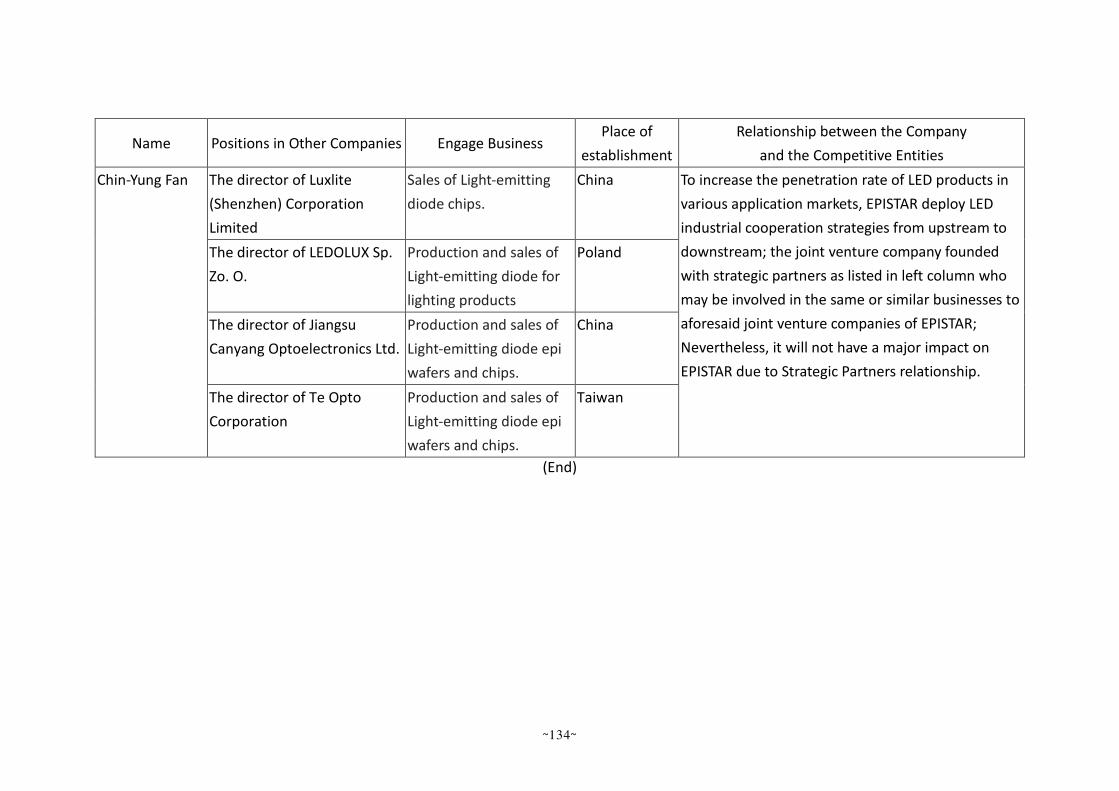

(7) To release the newly elected directors from non-competition restrictions.

(Proposed by the Board of Directors)

Explanation:

A. According to Article 209, Company Act.

B. Propose to approve to release the list of Company’s directors from non-competition

restrictions as attached hereto as Attachment 12 (page 131-134).

Resolution:

5. Extemporary Motions

6. Adjournment

~15~

Attachment 1

EPISTAR Corporation

2018 Business Report In 2018, other companies in the LED business have completed expansion of their production

capacity, resulting in fierce competition and overcapacity of the global nitride-based LED business.

Although our entire staff and workforce has dedicated all our effort into lowering operating

costs and increasing product mix optimization, our product prices continue to decrease rapidly.

In 2018, the Company’s individual net Sales was about NTD 17.19 billion, decreased 21.7%

from 2017. Our Net Operating Loss was NTD 0.407 billion and Net Loss after tax was NTD 0.456

billion.

In order to accommodate the launch of new products, upgrade product specification and

improve competitiveness, we acquired new process equipment, clean room, RD equipment, and

equipment upgrades. We also invested in increasing environmental protection and work safety

facilities; therefore this year’s capital expenditure is around NTD 2.746 billion.

Our company continues to invest in research and development. In 2018 our research and

development cost was NTD 1.828 billion, which were primarily invested to develop new products

and increase cost-performance ratio, all with good results. Asides from winning the 2018 Taiwan

International Lighting Show (TILS) Innovative Product award, we also have considerable progress in

acquiring of patents. We acquired 265 patents last year and now have a total of 4,017 patents. Our

company has earned recognition in implementation of corporate social responsibility. In addition

to “The British Standards Association CSR certification statement” issued to us, we also obtained

the 2018 Taiwan Enterprise Sustainability Report Award and BSI Award.

Prospecting the upcoming year of 2019 in the LED industry, the market is still over supplied

and competition is intense. However due to global issues on energy-saving and emphasis on

environmental protection, as well as luminous efficiency has improved over the years and

miniaturization of LED chips, many more new applications of LED are emerging and the LED market

has potential to continue to grow. For example, the applications and demand of Mini LED in

various kinds of display has increased, LED High efficiency tube and filament LED light bulb demand

has grown over the years, and LED application in lighting and automobile and other applications

has continued to permeate throughout other fields of applications. LED application in Horticulture

has gradually gained importance and IR LED in security control, smart phone sensor, and so on.

~16~

In 2019, our expected shipment of LED chip is estimated at 626,221 million pcs.

In response to market promotion of our VCSEL foundry business, in addition to significant

increase in sales of data transfer VCESL epitaxy wafer, we set up the subsidiary Unikorn

Semiconductor Corporation in Oct., 2018 so as to start to promote the foundry business and

development of VCSEL in sensor device products and the 5G application this year.

In reaction to the demands toward intelligentization and digitalization of applications and

price–performance ratio in the upcoming future, we still need to constantly put our effort in

research and development, improve our technique and lower our costs. Our company will continue

to launch new products, improve efficiency of resource operations, increase product’s additional

value and product mix optimization and compete for more high quality orders in order to achieve

the goal of out of the red in this year.

Chairman Biing-Jye Lee

President Chin-Yung Fan

Accounting Personnel Shih-Shien Chang

~17~

Attachment 2

Audit Committee’s Review Report

To: EPISTAR Corporation Annual General Shareholders’ Meeting of 2019

The board of directors has prepared and submitted the Company’s 2018 Business Report, Financial

Statements and Proposal for 2018 Deficit Compensation. Ya-Huei Cheng CPA and Chin-Cheng Hsieh

CPA of PricewaterhouseCoopers have also audited the financial statements and issued the

auditors’ report. The Business Report, Financial Statements and Proposal for 2018 Deficit

Compensation have been reviewed and determined to be correct and accurate by the Audit

Committee members of Epistar Corporation. According to article 14-4 of the Securities and

Exchange Act and Article 219 of the Company Act, we hereby submit the report.

EPISTAR Corporation

Chairman of the Audit Committee: Mr. Wei-Min Sheng

Date: March 14th, 2019

~18~

Attachment 3

Epistar Corporation

Rules for the Repurchase of Shares and Transfer to Employees at the first round of

Year 2018

Article 1

In order to care for and encourage its employees, Epistar adopts these Rules for the

Repurchase of Shares and Transfer to Employees in accordance with Article 28-2,

paragraph 1, subparagraph 1 of the Securities and Exchange Act and the provisions

of the Regulations Governing Share Repurchase by Exchange-Listed and OTC-Listed

Companies issued by the Financial Supervisory Commission, Executive Yuan. Any

repurchase of shares and transfer to employees by Epistar, in addition to complying

with related laws and regulations, will be carried out in accordance with these Rules.

Article 2 Type of shares to be transferred, a description of the rights attaching thereto, and

any restrictions on such rights.

The shares in the present transfer of shares to employees will be common shares,

and the rights and obligations associated with those shares, unless otherwise

provided by applicable laws and regulations or these Rules, will be the same as other

outstanding common shares of Epistar.

Article 3 Transfer period.

In accordance with these Rules, the shares in the present share repurchase may be

transferred to employees in a single transfer or multiple transfers within three years

from the date of the share repurchase.

Article 4 Eligibility requirements for transferees.

All regular employees of Epistar and employees of subsidiaries owed over 50% by

Epistar directly or indirectly.

Article 5 Transfer allocation

1. The number of shares to which employees may subscribe will be determined

based on their salary, seniority, and performance evaluations with further

considering factors such as, at the base date of shares purchasing, the total

number of shares bought back by the company and the upper limit of the single

employee's subscription.

2. Other than the number of shares that can be subscribed in Article 5.1, the

chairman is authorized to allocate additional share subscriptions to employees

with special contributions to the company based on their respective contribution

levels. As to the managers, additional share subscriptions should be first

proposed by the salary & compensation committee and then be submitted for

Board's discussion and approval.

3. The chairman is authorized to approve the number of shares, record date,

payment deadline and related matters in accordance with related regulation. A

list of employees and the number of shares to which they may subscribe will be

drawn up according to the approval of the chairman of the board.

4. Employees who have not subscribed and completed payment at the conclusion

of the designated subscription and payment period will be deemed to have

waived their subscription rights. In the event of an insufficient number of

subscriptions, the chairman may contact other employees regarding subscription

to the remaining shares.

~19~

Article 6 Repurchase and Procedures for transfer of shares.

Procedures for the present repurchase of shares and transfer to employees:

1. The repurchase of Epistar shares will be publicly announced, reported, and

carried out during the implementation period in accordance with a resolution of

the board of directors.

2. To publicly announce operating procedures relating to the record date for

employee subscriptions, the standards for numbers of shares to which

employees may subscribe, the period for payment for subscriptions, and the

rights associated with share subscriptions.

3. Statistics will be compiled on the numbers of shares actually subscribed and paid

for, and the registration of share transfers will be carried out.

Article 7 Agreed transfer price per share

The share transfer price for the present repurchase of shares and transfer to

employees will be the average of the actual share repurchase prices, (The transfer

price is calculated round up to one decimal place.) provided that if, prior to the

transfer, there is either an increase in the number of issued shares of Epistar

common stock, the transfer price may be adjusted within a range proportional to the

increase.

Transfer price adjustment formula:

Adjusted transfer prices (Note 1)=

Actual Average repurchase price (Note 2) x (The total number of ordinary shares on

the date which repurchase completion(Note 3) ÷The total number of ordinary shares

before the record date which transfer to employees (Note 3))

Note 1:

The adjusted transfer price is calculated round up to one decimal place.

Note 2:

Actual average repurchase price is calculated round up to one decimal place.

Note 3:

The total number of ordinary shares is determined according to the registration of

the Ministry of Economy of the total issued shares.

Article 8 Except otherwise provided, the rights and obligations associated with the

transferred shares, following the transfer of shares in the present share repurchase

to employees and registration of share transfer, will be the same as those originally

associated with the shares.

Article 9 When Epistar transfers to employees treasury stock it has repurchased, the related

tax should be paid. But in the future, in case of any amendment to the relevant tax

laws and regulations of the ROC, all tax matters shall be construed in accordance

with the then prevailing laws.

Article 10 These Rules will be adopted and take effect following a resolution of the board of

directors, and may be amended by submission to the board of directors for a

resolution.

Article 11 These Rules, and any amendments hereto, shall be reported to the shareholders

meeting.

~20~

Attachment 4

Epistar Corporation

Rules for the Procedures of the Board of Directors’ Meeting

Comparison Table for Amendments

Article No. Original Articles Amended Articles Reasons for Amendments

Article 4 Agenda

The Treasury Department and Financial

Management Division of the Company (the “TFM

Division”) is appointed by the BOD of the Company

to act as the secretariat of the meeting (the

“Secretariat”).

The Secretariat shall draft the agenda items to be

discussed in a meeting prior to the commencement

of BOD meeting, prepare sufficient materials for

the meeting, and deliver them to the members of

the BOD together with the meeting notice.

If any director of the BOD deems materials for a

discussion item insufficient, they may request for

supplements. If more than 50% of the directors

share the same view, such discussion item may be

postponed to another meeting subject to the

respective resolution adopted by the BOD.

Agenda and related document

The financial and accounting center of the

Company is appointed by the BOD of the Company

to act as the secretariat of the meeting (the

“Secretariat”).

The Secretariat shall draft the agenda items to be

discussed in a meeting prior to the commencement

of BOD meeting, prepare sufficient materials for

the meeting, and deliver them to the members of

the BOD together with the meeting notice.

If any director of the BOD deems materials for a

discussion item insufficient, they may request for

supplements then the financial and accounting

center should provide it within three working days.

If more than 50% of the directors share the same

view, such discussion item may be postponed to

another meeting subject to the respective

resolution adopted by the BOD.

To add the new title and

amend the content by

complying with the

amendment of article 15

of Taiwan Stock Exchange

Corporation Operation

Directions for the

Appointment of

Independent Directors by

TWSE Listed Companies.

~21~

Article No. Original Articles Amended Articles Reasons for Amendments

Article 4-1 (New item) Set up Corporate Governance Director

The company shall set up a specific (part-time) unit

and a corporate governance supervisor of the

company to be the supreme director in charge of

corporate governance related matters. The

authority scope, qualifications and training for the

director shall be set and exercised by following the

provisions of “Taiwan Stock Exchange Corporation

Operation Directions for the Appointment of

Independent Directors by TWSE Listed Companies”.

All directors of the company should be able to

obtain the assistance of the corporate governance

supervisor to ensure that the board procedures and

all applicable laws and regulations are followed,

and to ensure good information exchange between

board members and between the directors and the

manager.

The corporate governance supervisor is responsible

for handling the requirements of the directors. The

principle of promptly and effectively assisting the

directors in performing their duties should be

handled within three working days, unless

otherwise required by the law. If the processing

time may exceed three working days, the directors

shall negotiate with the directors as soon as

To add by complying with

the amendment article 20

of Taiwan Stock Exchange

Corporation Operation

Directions for the

Appointment of

Independent Directors by

TWSE Listed Companies.

~22~

Article No. Original Articles Amended Articles Reasons for Amendments

possible.

Article 7 Chairman and proxy of the chair for BOD

The Chairman of the BOD of the Company shall call

and preside over the meeting. Nevertheless, the

director who receives votes representing the

largest portion of voting rights at the shareholders’

meeting of the Company shall call and chair the

first meeting of each newly elected BOD of the

Company. If there are 2 or more directors who are

entitled to convene the above-mentioned initial

meeting, theses directors shall elect one person by

and from among themselves to call and preside

over the first meeting.

If the Chairman is on leave, or cannot execute his

or her authority of office for any reason, the vice

Chairman shall preside over the meeting. If the

vice Chairman is also on leave, or cannot execute

his or her authority of office for any reason, the

Chairman shall designate one of the directors to

preside over the meeting. If the Chairman does not

Chairman and proxy of the chair for BOD

The Chairman of the BOD of the Company shall call

and preside over the meeting. Nevertheless, the

director who receives votes representing the

largest portion of voting rights at the shareholders’

meeting of the Company shall call and chair the

first meeting of each newly elected BOD of the

Company. If there are 2 or more directors who are

entitled to convene the above-mentioned initial

meeting, theses directors shall elect one person by

and from among themselves to call and preside

over the first meeting.

In case the meeting is convened by half or more

directors according to Article 203 (4) or Article

203-1 (1) of Company Act, the directors shall elect a

chairman of the meeting from among the directors

to preside the meeting.

If the Chairman is on leave, or cannot execute his

or her authority of office for any reason, the vice

Chairman shall preside over the meeting. If the

vice Chairman is also on leave, or cannot execute

his or her authority of office for any reason, the

Chairman shall designate one of the directors to

preside over the meeting. If the Chairman does not

To amend by comply with

the amendment of Article

203 and Article 203-1 of

the company Act

published at Nov. 1st 2018.

~23~

Article No. Original Articles Amended Articles Reasons for Amendments

designate any proxy to preside over the meeting on

his or her behalf, the directors shall elect one from

among themselves to preside over the meeting.

designate any proxy to preside over the meeting on

his or her behalf, the directors shall elect one from

among themselves to preside over the meeting.

Article 8 Meeting materials, participants and meeting

commencement

Before and during a meeting, the designated

division shall prepare relevant materials for the

directors present at the meeting to review at any

time.

While convening a meeting, subject to the contents

of the discussion items, the Company may request

the staff of the relevant departments or

subsidiaries to attend the meeting. The Company

may also invite its accountants, lawyers or other

relevant specialists to attend the meeting and

make a statement, if necessary. But such attendees

shall leave the meeting when the discussion items

are being conducted and resolved.

The chairman of a meeting shall call the meeting

according to the schedule, provided that 50% of

Meeting materials, participants and meeting

commencement

Before and during a meeting, the designated

division shall prepare relevant materials for the

directors present at the meeting to review at any

time.

While convening a meeting, subject to the contents

of the discussion items, the Company may request

the staff of the relevant departments or

subsidiaries to attend the meeting.

The Company may also invite its accountants,

lawyers or other relevant specialists to attend the

meeting and make a statement, if necessary. But

such attendees shall leave the meeting when the

discussion items are being conducted and resolved.

The chairman of a meeting shall call the meeting

according to the schedule, provided that 50% of

Separate the second half

of the original second

paragraph into the third

paragraph. The original

third paragraph was

moved to the fourth

paragraph, and the

original fourth paragraph

was moved to the fifth

paragraph.

~24~

Article No. Original Articles Amended Articles Reasons for Amendments

the total directors are present. If at the scheduled

starting time of the meeting, the number of

directors present at the meeting has not yet

reached 50% of the total directors, the chairman

may postpone the starting time of the meeting.

The postponements shall be limited to twice at

most. The chairman shall reconvene the meeting,

according to the procedures set forth in Paragraph

2 of Article 3 of the Rules, if the number of

directors present at the meeting has still not yet

reached 50% of the total directors after the

meeting has been postponed twice.

The total number of directors referred to in the

preceding paragraph shall mean the directors who

are currently assuming their duties as directors.

the total directors are present. If at the scheduled

starting time of the meeting, the number of

directors present at the meeting has not yet

reached 50% of the total directors, the chairman

may postpone the starting time of the meeting.

The postponements shall be limited to twice at

most. The chairman shall reconvene the meeting,

according to the procedures set forth in Paragraph

2 of Article 3 of the Rules, if the number of

directors present at the meeting has still not yet

reached 50% of the total directors after the

meeting has been postponed twice.

The total number of directors referred to in the

preceding paragraph shall mean the directors who

are currently assuming their duties as directors.

Article 11 Procedure of meeting

A meeting shall proceed in accordance with the

agenda, unless otherwise resolved by the BOD of

the Company with affirmative vote of at least 50%

of all directors present at the meeting.

Unless otherwise resolved by the BOD of the

Company with affirmative vote of at least 50% of all

directors present at the meeting, the chairman

shall not adjourn the meeting.

During a meeting, the chairman of the meeting

Procedure of meeting

A meeting shall proceed in accordance with the

agenda, unless otherwise resolved by the BOD of

the Company with affirmative vote of at least 50%

of all directors present at the meeting.

Unless otherwise resolved by the BOD of the

Company with affirmative vote of at least 50% of all

directors present at the meeting, the chairman

shall not adjourn the meeting.

During a meeting, the chairman of the meeting

To amend the paragraph 4.

~25~

Article No. Original Articles Amended Articles Reasons for Amendments

shall suspend the meeting if a motion is brought up

by a director, in the event that the number of the

directors present in the meeting is less than 50% of

the directors present at the meeting. Under such

circumstance, Paragraph 3 of Article 8 of the Rules

shall apply.

shall suspend the meeting if a motion is brought up

by a director, in the event that the number of the

directors present in the meeting is less than 50% of

the directors present at the meeting. Under such

circumstance, Paragraph 4 of Article 8 of the Rules

shall apply.

Article 15 Withdrawal from discussion as an interested party

At a meeting in which a director or the juristic

person that the director represents is an interested

party and his or her participation is likely to

prejudice the interest of the Company, such

director shall state significant respects regarding

the conflict of interest at said Board of Directors’

meeting. This director is prohibited from

participating in discussion of or voting on a matter,

and shall physically withdraw himself or herself

from participating in the discussion or voting on

such matter, and likewise is prohibited from voting

on such matter as a proxy of another director.

Withdrawal from discussion as an interested party

At a meeting in which a director or the juristic

person that the director represents is an interested

party and his or her participation is likely to

prejudice the interest of the Company, such

director shall state significant respects regarding

the conflict of interest at said Board of Directors’

meeting. This director is prohibited from

participating in discussion of or voting on a matter,

and shall physically withdraw himself or herself

from participating in the discussion or voting on

such matter, and likewise is prohibited from voting

on such matter as a proxy of another director.

Where the spouse, a blood relative within the

second degree of kinship of a director, or any

company which has a controlling or subordinate

relation with a director has interests in the matters

under discussion in the meeting of the preceding

paragraph, such director shall be deemed to have a

To amend by comply with

the amendment of article

206 of the company Act

published at Nov. 1st 2018.

~26~

Article No. Original Articles Amended Articles Reasons for Amendments

Under the circumstance set forth in the preceding

paragraph of this Article, pursuant to Paragraph 3

of Article 206 of the Company Act, Paragraph 2 of

Article 180 of the Company Act shall apply to the

resolution adopted by the BOD of the Company.

personal interest in the matter.

Under the circumstance set forth in the preceding

two paragraphs of this Article, pursuant to

Paragraph 4 of Article 206 of the Company Act,

Paragraph 2 of Article 180 of the Company Act shall

apply to the resolution adopted by the BOD of the

Company.

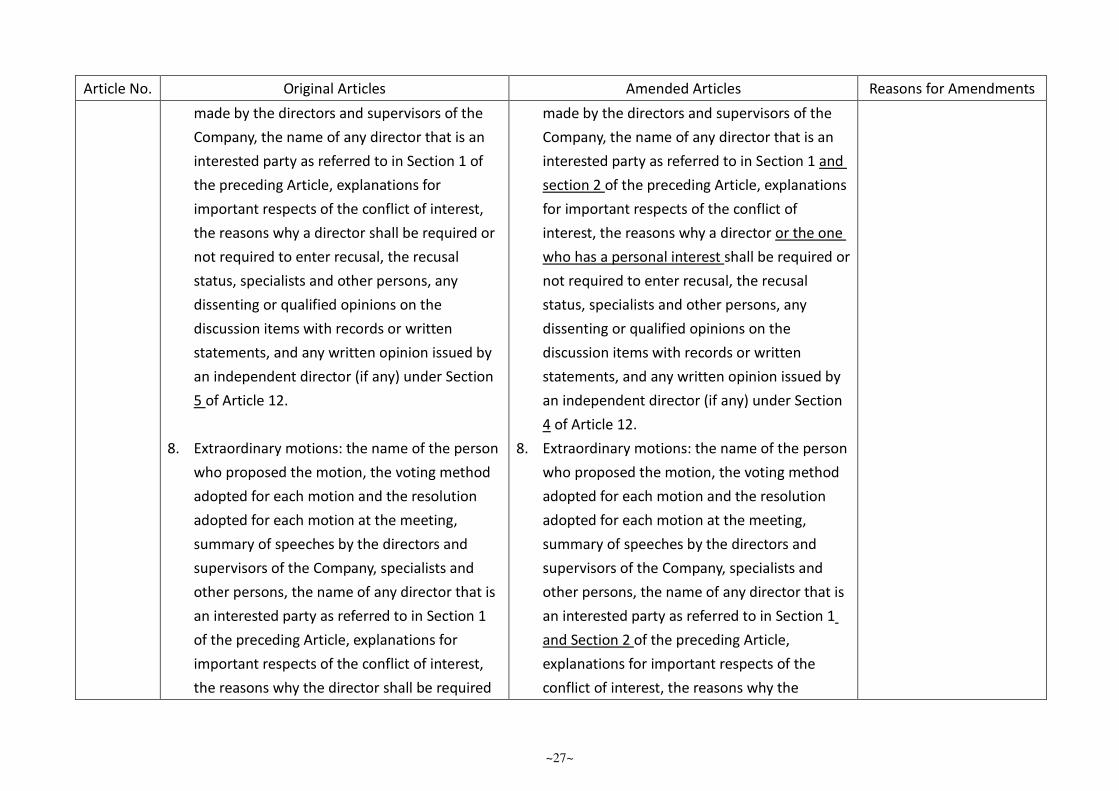

Article 16 Meeting minutes

Resolutions adopted at the meeting shall be

recorded in the meeting minutes. The meeting

minutes shall fully and accurately record the items

as follows:

1. The identification number of the meeting (or

the year), meeting time and venue;

2. The name of the chairman of the meeting;

3. Attendance status, including the names and

number of the directors who were present, on

a leave and absent, respectively;

4. The names and positions of the persons

present as guest at the meeting;

5. The name of the secretary of the meeting;

6. Reporting items;

7. Discussion items: the voting method adopted

for each resolution and each resolution

adopted at the meeting, summary of speeches

Meeting minutes

Resolutions adopted at the meeting shall be

recorded in the meeting minutes. The meeting

minutes shall fully and accurately record the items

as follows:

1. The identification number of the meeting (or

the year), meeting time and venue;

2. The name of the chairman of the meeting;

3. Attendance status, including the names and

number of the directors who were present, on

a leave and absent, respectively;

4. The names and positions of the persons

present as guest at the meeting;

5. The name of the secretary of the meeting;

6. Reporting items;

7. Discussion items: the voting method adopted

for each resolution and each resolution

adopted at the meeting, summary of speeches

To amend by comply with

the amendment of Article

206 of the Company Act

published at Nov. 1st 2018,

and Article 14-3 and

Article 14-5 of Securities

and Exchange Act.

~27~

Article No. Original Articles Amended Articles Reasons for Amendments

made by the directors and supervisors of the

Company, the name of any director that is an

interested party as referred to in Section 1 of

the preceding Article, explanations for

important respects of the conflict of interest,

the reasons why a director shall be required or

not required to enter recusal, the recusal

status, specialists and other persons, any

dissenting or qualified opinions on the

discussion items with records or written

statements, and any written opinion issued by

an independent director (if any) under Section

5 of Article 12.

8. Extraordinary motions: the name of the person

who proposed the motion, the voting method

adopted for each motion and the resolution

adopted for each motion at the meeting,

summary of speeches by the directors and

supervisors of the Company, specialists and

other persons, the name of any director that is

an interested party as referred to in Section 1

of the preceding Article, explanations for

important respects of the conflict of interest,

the reasons why the director shall be required

made by the directors and supervisors of the

Company, the name of any director that is an

interested party as referred to in Section 1 and

section 2 of the preceding Article, explanations

for important respects of the conflict of

interest, the reasons why a director or the one

who has a personal interest shall be required or

not required to enter recusal, the recusal

status, specialists and other persons, any

dissenting or qualified opinions on the

discussion items with records or written

statements, and any written opinion issued by

an independent director (if any) under Section

4 of Article 12.

8. Extraordinary motions: the name of the person

who proposed the motion, the voting method

adopted for each motion and the resolution

adopted for each motion at the meeting,

summary of speeches by the directors and

supervisors of the Company, specialists and

other persons, the name of any director that is

an interested party as referred to in Section 1

and Section 2 of the preceding Article,

explanations for important respects of the

conflict of interest, the reasons why the

~28~

Article No. Original Articles Amended Articles Reasons for Amendments

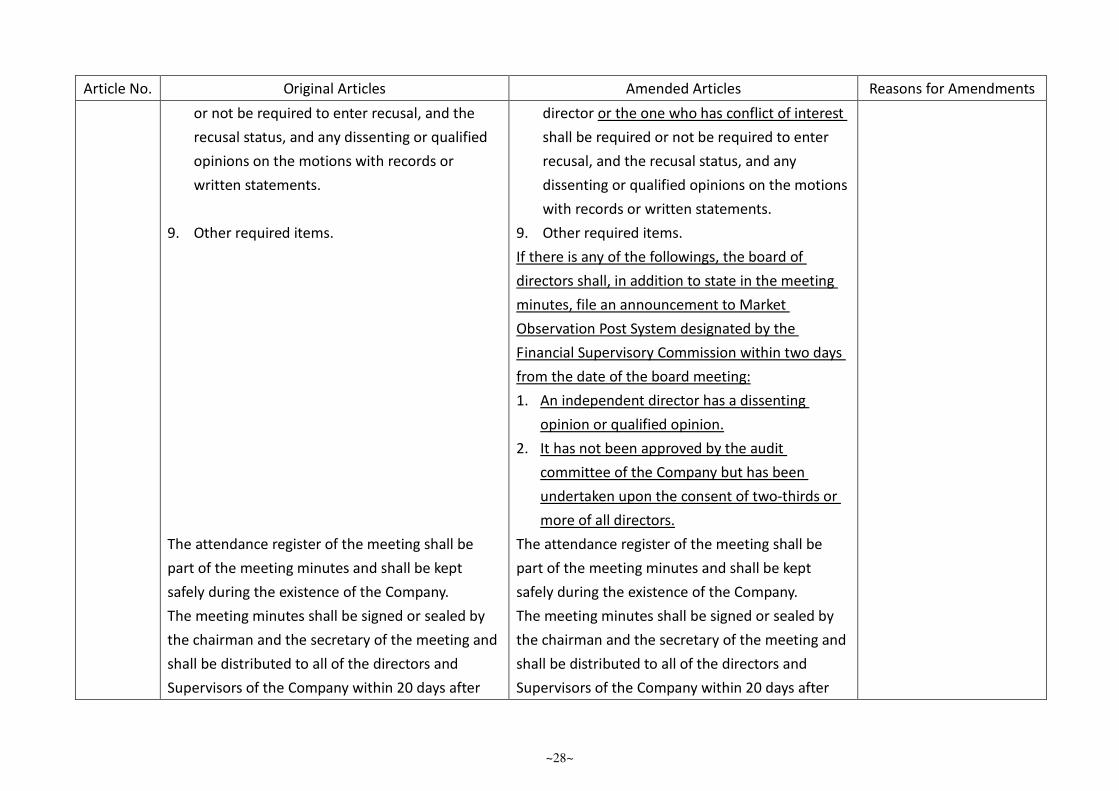

or not be required to enter recusal, and the

recusal status, and any dissenting or qualified

opinions on the motions with records or

written statements.

9. Other required items.

The attendance register of the meeting shall be

part of the meeting minutes and shall be kept

safely during the existence of the Company.

The meeting minutes shall be signed or sealed by

the chairman and the secretary of the meeting and

shall be distributed to all of the directors and

Supervisors of the Company within 20 days after

director or the one who has conflict of interest

shall be required or not be required to enter

recusal, and the recusal status, and any

dissenting or qualified opinions on the motions

with records or written statements.

9. Other required items.

If there is any of the followings, the board of

directors shall, in addition to state in the meeting

minutes, file an announcement to Market

Observation Post System designated by the

Financial Supervisory Commission within two days

from the date of the board meeting:

1. An independent director has a dissenting

opinion or qualified opinion.

2. It has not been approved by the audit

committee of the Company but has been

undertaken upon the consent of two-thirds or

more of all directors.

The attendance register of the meeting shall be

part of the meeting minutes and shall be kept

safely during the existence of the Company.

The meeting minutes shall be signed or sealed by

the chairman and the secretary of the meeting and

shall be distributed to all of the directors and

Supervisors of the Company within 20 days after

~29~

Article No. Original Articles Amended Articles Reasons for Amendments

the date on which the meeting is held. The meeting

minutes shall be categorized as one of the material

records or files of the Company and shall be safely

kept during the existence of the Company.

Preparation and distribution of the meeting

minutes mentioned in Paragraph 1 of this Article

may be made by electronic form.

the date on which the meeting is held. The meeting

minutes shall be categorized as one of the material

records or files of the Company and shall be safely

kept during the existence of the Company.

Preparation and distribution of the meeting

minutes mentioned in Paragraph 1 of this Article

may be made by electronic form.

~30~

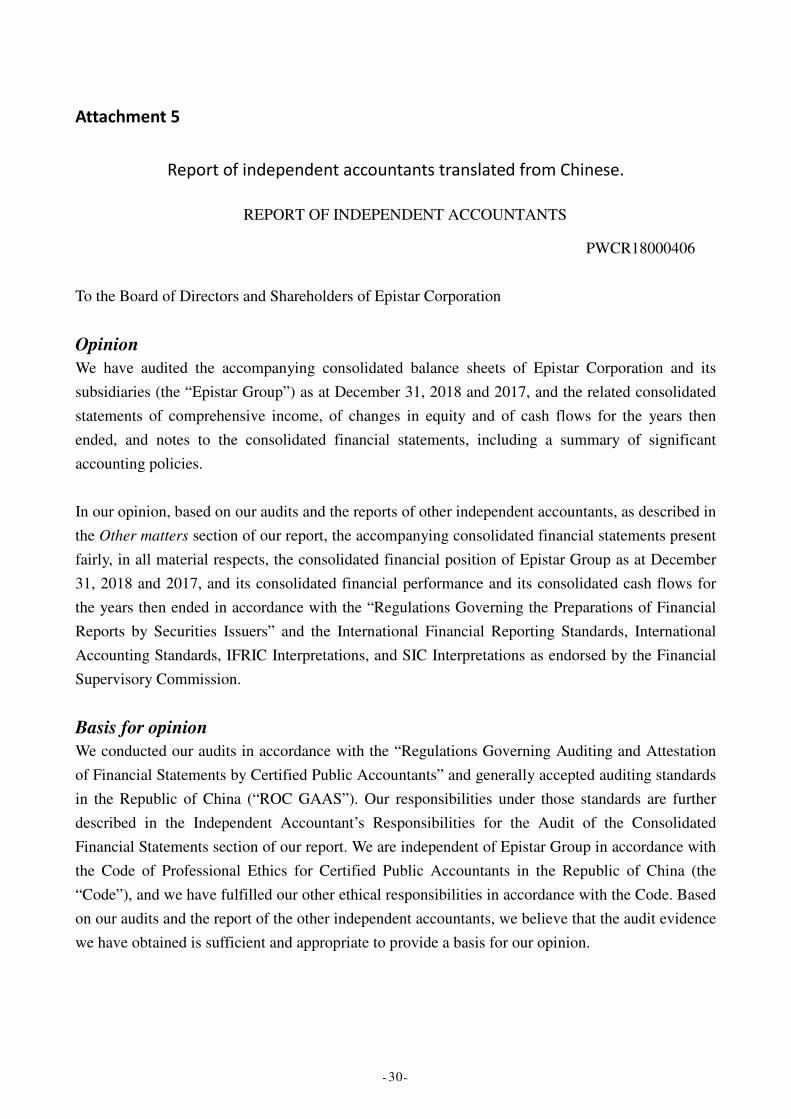

Attachment 5

Report of independent accountants translated from Chinese.

REPORT OF INDEPENDENT ACCOUNTANTS

PWCR18000406

To the Board of Directors and Shareholders of Epistar Corporation

Opinion

We have audited the accompanying consolidated balance sheets of Epistar Corporation and its

subsidiaries (the “Epistar Group”) as at December 31, 2018 and 2017, and the related consolidated

statements of comprehensive income, of changes in equity and of cash flows for the years then

ended, and notes to the consolidated financial statements, including a summary of significant

accounting policies.

In our opinion, based on our audits and the reports of other independent accountants, as described in

the Other matters section of our report, the accompanying consolidated financial statements present

fairly, in all material respects, the consolidated financial position of Epistar Group as at December

31, 2018 and 2017, and its consolidated financial performance and its consolidated cash flows for

the years then ended in accordance with the “Regulations Governing the Preparations of Financial

Reports by Securities Issuers” and the International Financial Reporting Standards, International

Accounting Standards, IFRIC Interpretations, and SIC Interpretations as endorsed by the Financial

Supervisory Commission.

Basis for opinion

We conducted our audits in accordance with the “Regulations Governing Auditing and Attestation

of Financial Statements by Certified Public Accountants” and generally accepted auditing standards

in the Republic of China (“ROC GAAS”). Our responsibilities under those standards are further

described in the Independent Accountant’s Responsibilities for the Audit of the Consolidated

Financial Statements section of our report. We are independent of Epistar Group in accordance with

the Code of Professional Ethics for Certified Public Accountants in the Republic of China (the

“Code”), and we have fulfilled our other ethical responsibilities in accordance with the Code. Based

on our audits and the report of the other independent accountants, we believe that the audit evidence

we have obtained is sufficient and appropriate to provide a basis for our opinion.

~31~

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in

our audit of the consolidated financial statements of the current period. These matters were

addressed in the context of our audit of the consolidated financial statements as a whole and, in

forming our opinion thereon, we do not provide a separate opinion on these matters.

The key audit matters in relation to consolidated financial statements for the year ended December

31, 2018 are outlined as follows:

Evaluation of Impairment Losses of Property, Plant and Equipment, and Goodwill

Description

Please refer to Note 4(18) of the consolidated financial statement for the accounting policy on

impairment losses on non-financial assets, Note 5(2) for the accounting estimates and assumptions

in relation to impairment losses on non-financial assets, Note 6(10) for the explanations regarding

impairment losses on non-financial assets. As of December 31, 2018, the balances of property, plant

and equipment, and goodwill were NT$22,435,949 thousand and NT$6,324,659 thousand,

respectively.

Epistar Group evaluates the recoverable amounts of idle property, plant and equipment through

assessing the fair values after deducting the disposal costs, and of property, plant and equipment,

and intangible assets through value in use. Epistar Group evaluates whether impairment losses will

be provided for property, plant and equipment, and goodwill utilizing the aforementioned

recoverable amounts. The evaluation of value in use for operational property, plant and equipment

and intangible assets consists of the estimation of future cash flows and the determination of

discount rates. Since the assumptions adopted in the estimation of future cash flows and the results

of the estimation would have significant impact on value in use of operational property, plant, and

equipment, and intangible assets, it was identified as one of the key audit matters.

How our audit addressed the matter

We have obtained the appraisal report of idle property, plant and equipment prepared by

independent valuers from Epistar Group and assessed the reasonableness of evaluation methods and

fair values utilized. For value in use of operational property, plant and equipment, and goodwill, the

following procedures were conducted:

~32~

1. Interviewed with management and obtained an understanding of Epistar Group’s operational

procedures in estimating future cash flows and verified the consistency to operation plans

approved by the Board of Directors.

2. Discussed operation plans with management to understand the product strategies and their

respective executions status.

3. Assessed the reasonableness for assumptions utilized in estimating future cash flows, including

projected sales volumes, unit prices and unit costs. Assessed the parameters adopted in

determining discount rates, including calculating and comparing the weighted average cost of

capital at risk-free rates, the industrial risk premium and the long-term rates of returns.

Evaluation of Inventories

Description

Please refer to Note 4(12) of the consolidated financial statement for the accounting policy on

inventory valuation, Note 5(2) for the accounting estimates and assumptions in relation to inventory

valuation, Note 6(5) for the explanations regarding inventory valuation. As of December 31, 2018,

the balances of inventories and the allowance for valuation loss were NT$5,631,815 thousand and

NT$926,624 thousand, respectively.

Epistar Group is primarily engaged in manufacturing and sales of LED wafers and chips. Due to

rapid technological developments, short product lifespans and frequent fluctuations of market prices,

the risk of decline in market value and obsolescence for inventories is high. Epistar Group evaluates

net realized values for inventories which aged over a specific period of time and specific obsolete

inventories in order to provide allowance for valuation loss. Since the identification of the above

obsolete inventories and their respective net realizable values are subject to management’s judgment,

it was identified as one of the key audit matters.

How our audit addressed the matter

Our key audit procedures performed in respect of the above included the following:

1. Obtained an understanding of Epistar Group’s operations and the nature of its industry and

interviewed with management to understand the probability of future sales for those out-of-date

inventories and to evaluate the reasonableness of allowance for valuation loss.

~33~

2. Obtained and validated the accuracy of the detailed listings of inventories aged over a specific

period of time and specific obsolete inventories. Validated information of historical sales and

discounts for those obsolete inventories to assess the reasonableness of policies in providing

allowance for inventory valuation loss.

Other matter – Audited by other Independent Accountants

We did not audit the financial statements of certain consolidated subsidiaries. Those financial

statements were audited by other independent accountants, whose reports thereon have been

furnished to us, and our opinion expressed herein, insofar as it relates to the amounts included in the

financial statements and the information on the consolidated subsidiaries disclosed in Note 13 was

based solely on the reports of other independent accountants. Total assets of those consolidated

subsidiaries amounted to NT$812,777 thousand and NT$1,045,560 thousand, constituting 1.29%

and 1.56% of the consolidated total assets as at December 31, 2018 and 2017, respectively, and total

operating revenues of NT$0 thousand and NT$0 thousand, constituting 0% and 0% of the

consolidated total operating revenues for the years then ended. Furthermore, we did not audit the

2018 and 2017 financial statements of certain equity investments accounted for under the equity

method. Those financial statements were audited by other independent accountants whose reports

thereon were furnished to us and our opinion expressed herein, insofar as it relates to the amounts

included in the consolidated financial statements and certain information disclosed in Note 13

relative to these investments, is based solely on the reports of the other independent accountants.

These equity investments amounted to NT$849,968 thousand and NT$802,377 thousand,

representing 1.35% and 1.19% of the consolidated total assets as of December 31, 2018 and 2017,

respectively, and their comprehensive income (loss) (including share of loss of associates and joint

ventures accounted for under equity method and share of other comprehensive income/(loss) of

associates and joint ventures accounted for under equity method) amounted to NT$78,078 thousand

and (NT$485,632) thousand, representing (7.08%) and (33.58%) of the consolidated comprehensive

income for the years then ended.

Other matter – Parent company only financial reports

We have also and expressed an unmodified opinion on the parent company only financial

statements of Epistar Corporation as of and for the years ended December 31, 2018 and 2017.

~34~

Responsibilities of management and those charged with governance for the

consolidated financial statements

Management is responsible for the preparation and fair presentation of the consolidated financial

statements in accordance with the “Regulations Governing the Preparations of Financial Reports by

Securities Issuers” and the International Financial Reporting Standards, International Accounting

Standards, IFRIC Interpretations, and SIC Interpretations as endorsed by the Financial Supervisory

Commission, and for such internal control as management determines is necessary to enable the

preparation of consolidated financial statements that are free from material misstatement, whether

due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the

Epistar Group’s ability to continue as a going concern, disclosing, as applicable, matters related to

going concern and using the going concern basis of accounting unless management either intends to

liquidate the Epistar Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance, including audit committee, are responsible for overseeing the

Epistar Group’s financial reporting process.

Independent accountant’s responsibilities for the audit of the consolidated financial

statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial

statements as a whole are free from material misstatement, whether due to fraud or error, and to

issue a report that includes our opinion. Reasonable assurance is a high level of assurance, but is not

a guarantee that an audit conducted in accordance with ROC GAAS will always detect a material

misstatement when it exists. Misstatements can arise from fraud or error and are considered

material if, individually or in the aggregate, they could reasonably be expected to influence the

economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with ROC GAAS, we exercise professional judgment and

maintain professional skepticism throughout the audit. We also:

~35~

1. Identify and assess the risks of material misstatement of the consolidated financial statements,

whether due to fraud or error, design and perform audit procedures responsive to those risks,

and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.

The risk of not detecting a material misstatement resulting from fraud is higher than for one

resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

2. Obtain an understanding of internal control relevant to the audit in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of expressing an

opinion on the effectiveness of Epistar Group’s internal control.

3. Evaluate the appropriateness of accounting policies used and the reasonableness of accounting

estimates and related disclosures made by management.

4. Conclude on the appropriateness of management’s use of the going concern basis of

accounting and, based on the audit evidence obtained, whether a material uncertainty exists

related to events or conditions that may cast significant doubt on Epistar Group’s ability to

continue as a going concern. If we conclude that a material uncertainty exists, we are required

to draw attention in our report to the related disclosures in the consolidated financial

statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are

based on the audit evidence obtained up to the date of our report. However, future events or

conditions may cause Epistar Group to cease to continue as a going concern.

5. Evaluate the overall presentation, structure and content of the consolidated financial statements,

including the disclosures, and whether the consolidated financial statements represent the

underlying transactions and events in a manner that achieves fair presentation.