equipment - local site visit aug 2006 - iis windows...

TRANSCRIPT

• Introduction

• Southern Africa

• Northern Cape

• Siberia

Barloworld Equipment team

� Lester Day

� Chris Gibb

� Wayne Witherspoon

� Gerhard Vorster

� Peter Tapson

Agenda

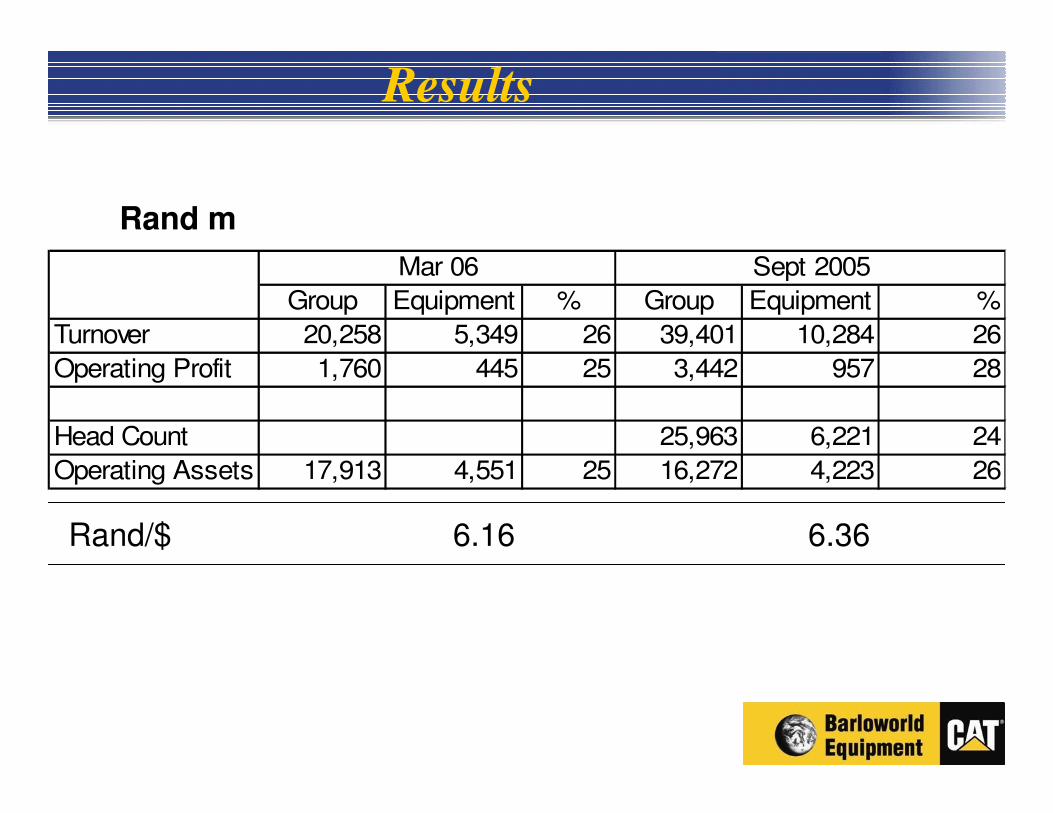

Group Equipment % Group Equipment %

Turnover 20,258 5,349 26 39,401 10,284 26

Operating Profit 1,760 445 25 3,442 957 28

Head Count 25,963 6,221 24

Operating Assets 17,913 4,551 25 16,272 4,223 26

Mar 06 Sept 2005

Rand m

Rand/$ 6.16 6.36

Results

Closing rateAverage monthly rate

Closing Rate

Average RateClosing rate

Daily QZAR= [Bar, Line]2004/10/01 - 2006/06/30 (GMT)[Standard]

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun2004 2005 2006

Price/USD

5.6

5.7

5.8

5.9

6.1

6.2

6.3

6.4

6.5

6.6

6.7

6.8

6.9

7.1

7.2

7.3

7.4

6

7

QZAR=, Bid, Bar2006/08/22 7.0149 7.1355 7.0040 7.0900QZAR=, Close(Ask), Line2006/08/22 7.1400

USD / ZAR movement

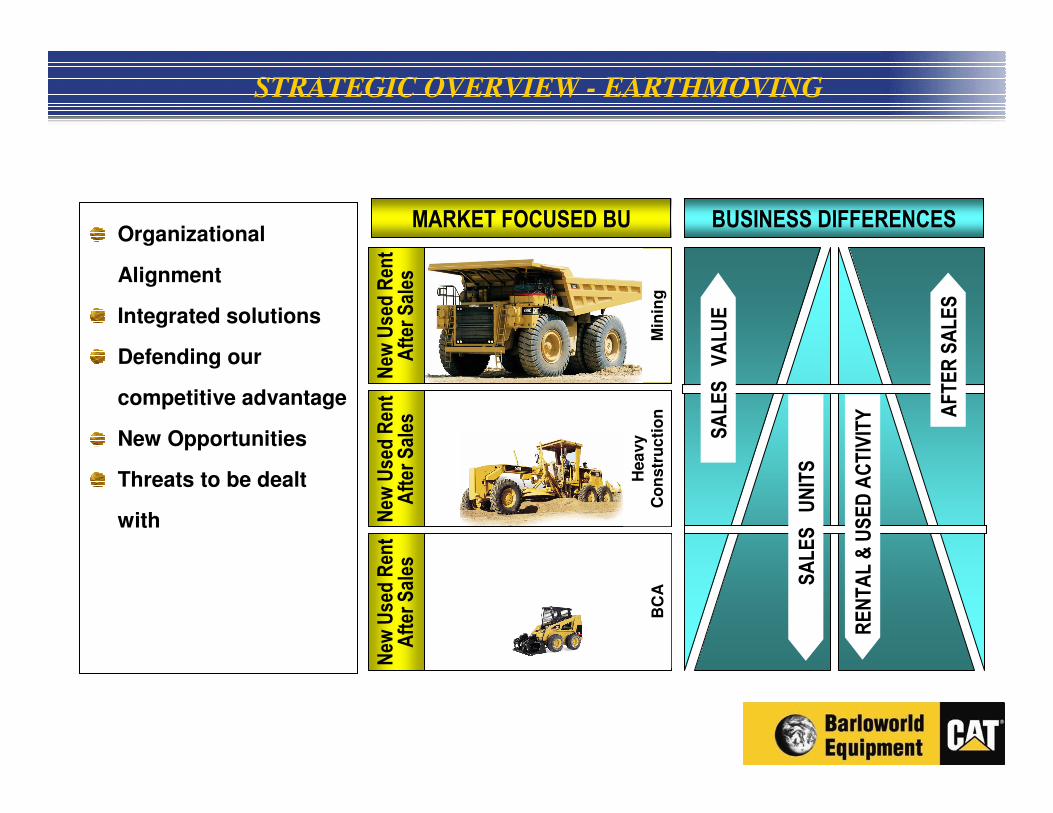

STRATEGIC OVERVIEW - EARTHMOVING

New

Use

d Ren

tAfter Sales

New

Use

d Ren

tAfter Sales

New

Use

d Ren

tAfter Sales

SALES VALUE

SALES UNITS

RENTAL & USED ACTIVITY AFTER SALES

MARKET FOCUSED BU BUSINESS DIFFERENCES

Min

ing

Hea

vy

Co

ns

tru

cti

on

BC

A

Organizational

Alignment

Integrated solutions

Defending our

competitive advantage

New Opportunities

Threats to be dealt

with

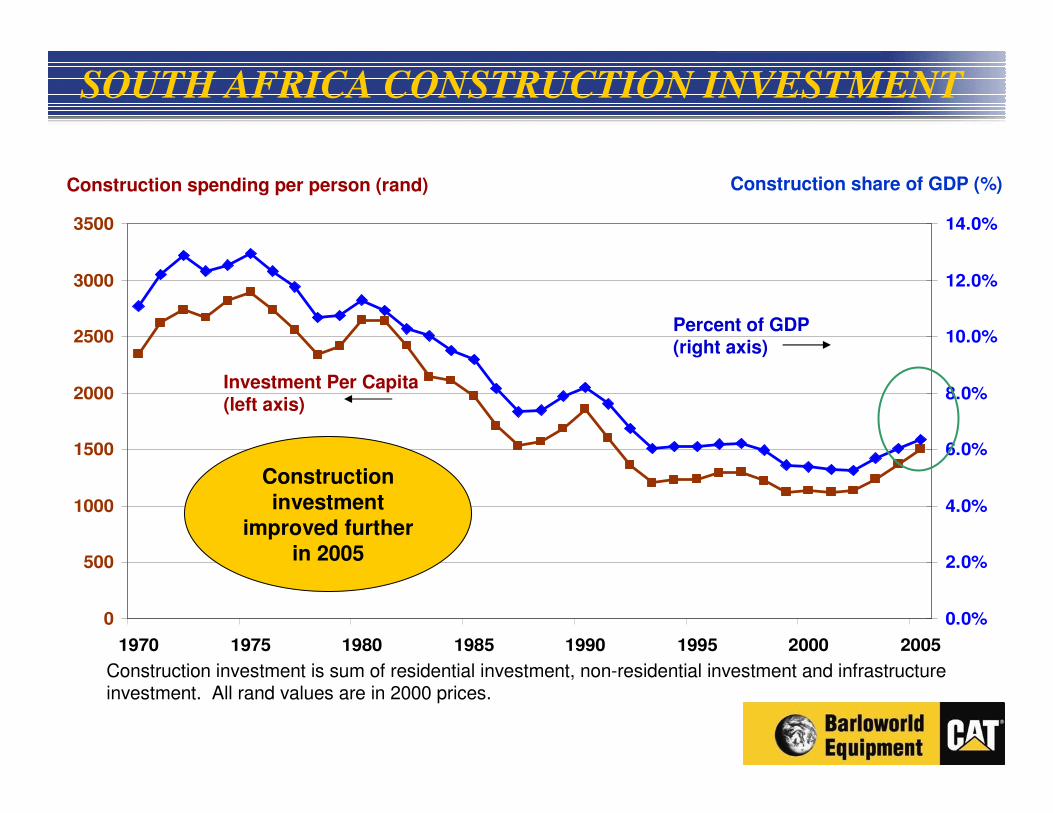

South African growth good over short and medium term

Bullish construction prospects

Higher government infrastructure spending

Higher commercial/industrial building construction

Housing sector has highest risks

Mining outlook strong on high average prices

Drives continuing mining investment

Risks:

Oil prices

Global economy / terrorismBoom time for

machine industry in Southern Africa

MARKET OUTLOOK AND MAJOR PROJECTS

ECONOMIC OUTLOOK 2007-2011

0

500

1000

1500

2000

2500

3000

3500

1970 1975 1980 1985 1990 1995 2000 2005

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Construction spending per person (rand) Construction share of GDP (%)

Investment Per Capita(left axis)

Percent of GDP(right axis)

Construction investment

improved further in 2005

Construction investment is sum of residential investment, non-residential investment and infrastructure investment. All rand values are in 2000 prices.

SOUTH AFRICA CONSTRUCTION INVESTMENT

CONSTRUCTION PROJECTS

GautrainR20 B

Jun-2006

Sishen-SaldhanaRailway Line

R4.4 BComplete 2010

Pebble BedModular Reactor

Construction starts2007

Waterfall CityR11 B

2,200 ha

Hydro ElectricVan Reenens

PassR4.5 B

COEGAStainless SteelPrecision Mill

R1.6 B

Fuel PipelineR1.8 B

2007/2008

Richards Bay Coal

TerminalR1 B2006

Airports UpgradeJhb – Dbn - CT

Pre 2010R5.2 B

World Cup Soccer 2010

MARKET OUTLOOK – MAJOR PROJECTS

(GOVERNMENT INFRASTRUCTURE SPENDING – 2006 TO 2009)

Provincial - R109bn

(26%)

Municipal - R82bn

(22%)

Public Enterprise -

R123bn

(33%)

National - R 32bn

(9%)

Other public - 26bn

(7%)

R372 billion

Source: ASGISA

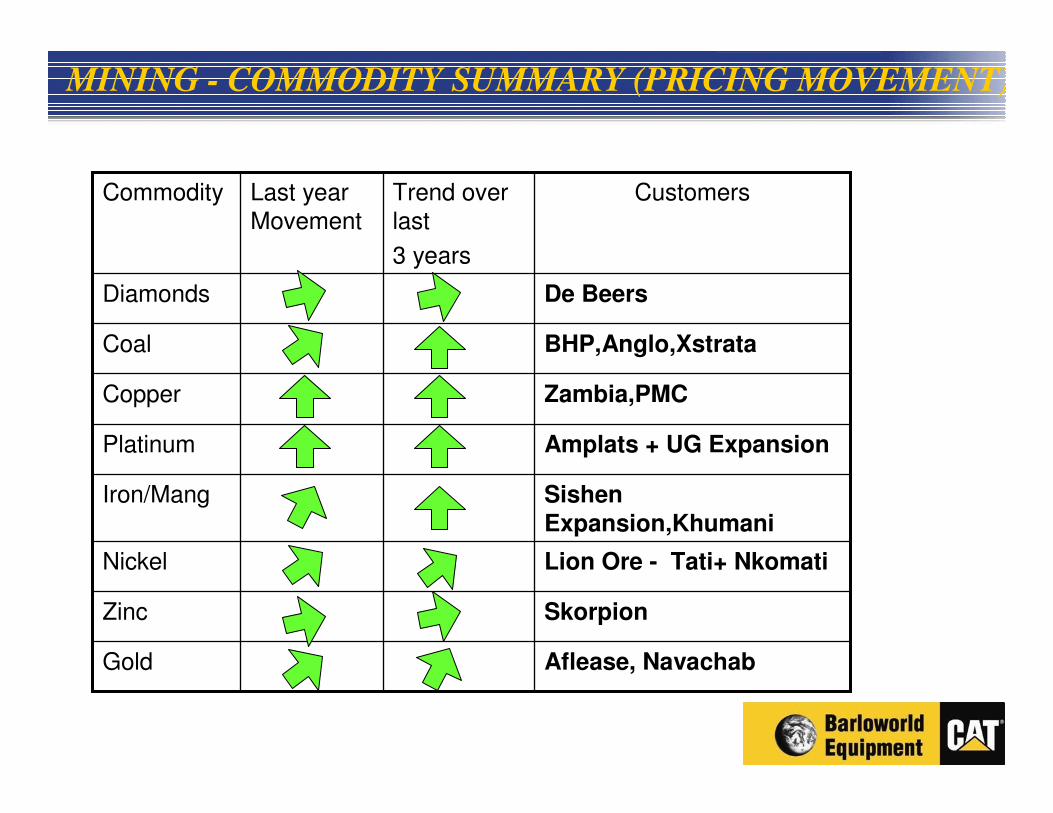

MINING - COMMODITY SUMMARY (PRICING MOVEMENT)

Aflease, NavachabGold

SkorpionZinc

Lion Ore - Tati+ NkomatiNickel

SishenExpansion,Khumani

Iron/Mang

Amplats + UG ExpansionPlatinum

Zambia,PMCCopper

BHP,Anglo,XstrataCoal

De BeersDiamonds

CustomersTrend over last

3 years

Last year Movement

Commodity

MINING PROJECTS - New machine expansion prospects

Coal

R 2436m

Moatise

R 900m

Diamonds

R 750m

Copper

R 600m

Diamonds

R 840m

Platinum

R 982mIron/Manganese

R 750m

Uranium

R 250m

Projects R 7,8b

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

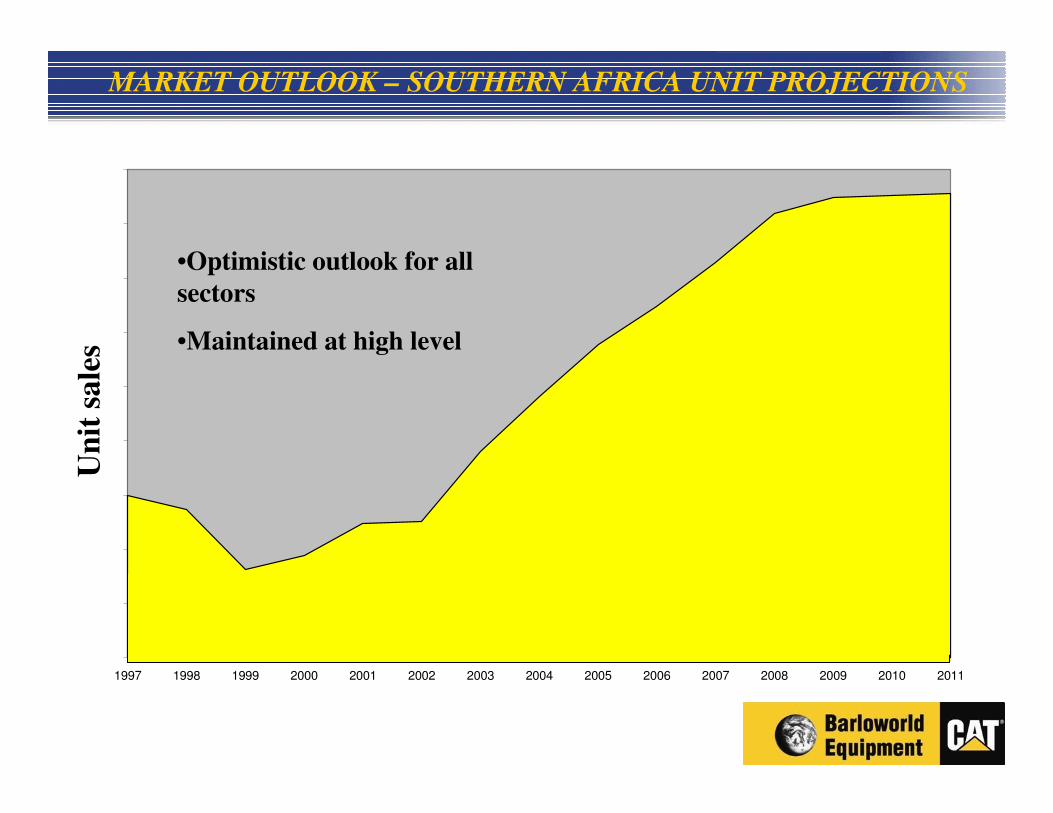

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

MARKET OUTLOOK – SOUTHERN AFRICA UNIT PROJECTIONS

•Optimistic outlook for all

sectors

•Maintained at high level

Un

it s

ale

s

KEY ISSUES

• Emergence of China as an opportunity/threat

• Significant growth in all territories/markets

• Challenge of up-skilling to meet growth

– Retention of BEE staff

– Remote sites

• Currency volatility

• Impact of CAT delivery constraints

– Equipment

– Tyres

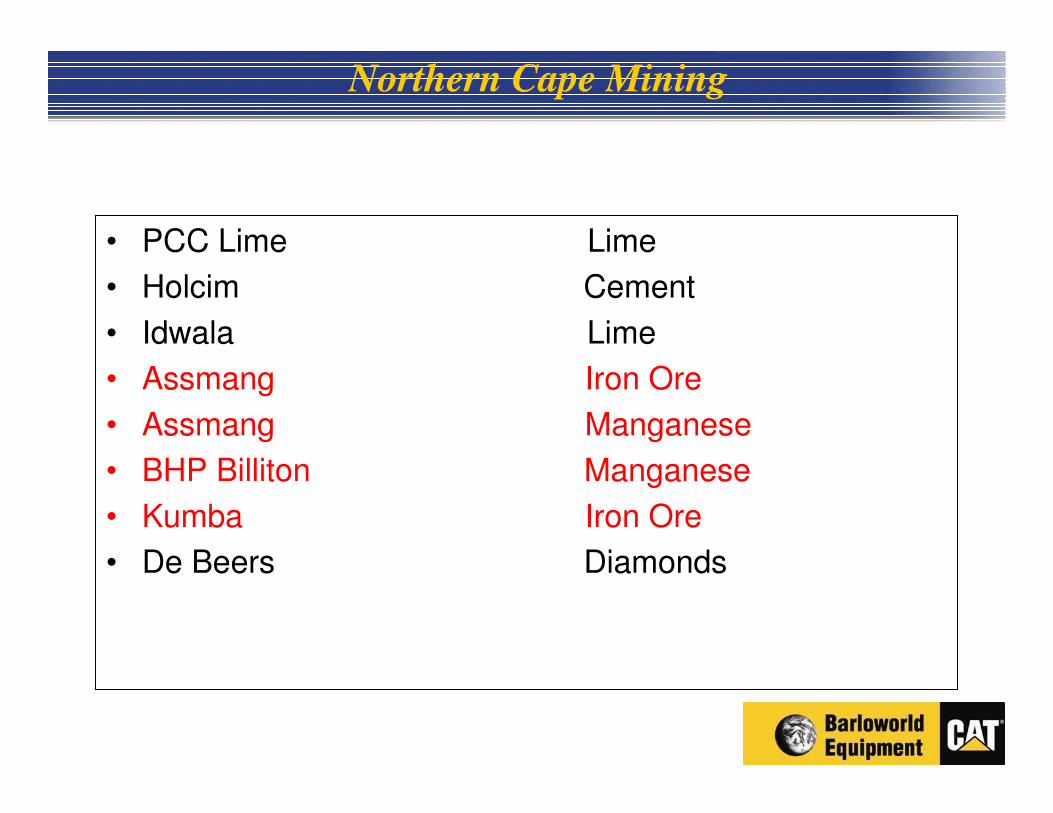

Northern Cape Mining

• PCC Lime Lime

• Holcim Cement

• Idwala Lime

• Assmang Iron Ore

• Assmang Manganese

• BHP Billiton Manganese

• Kumba Iron Ore

• De Beers Diamonds

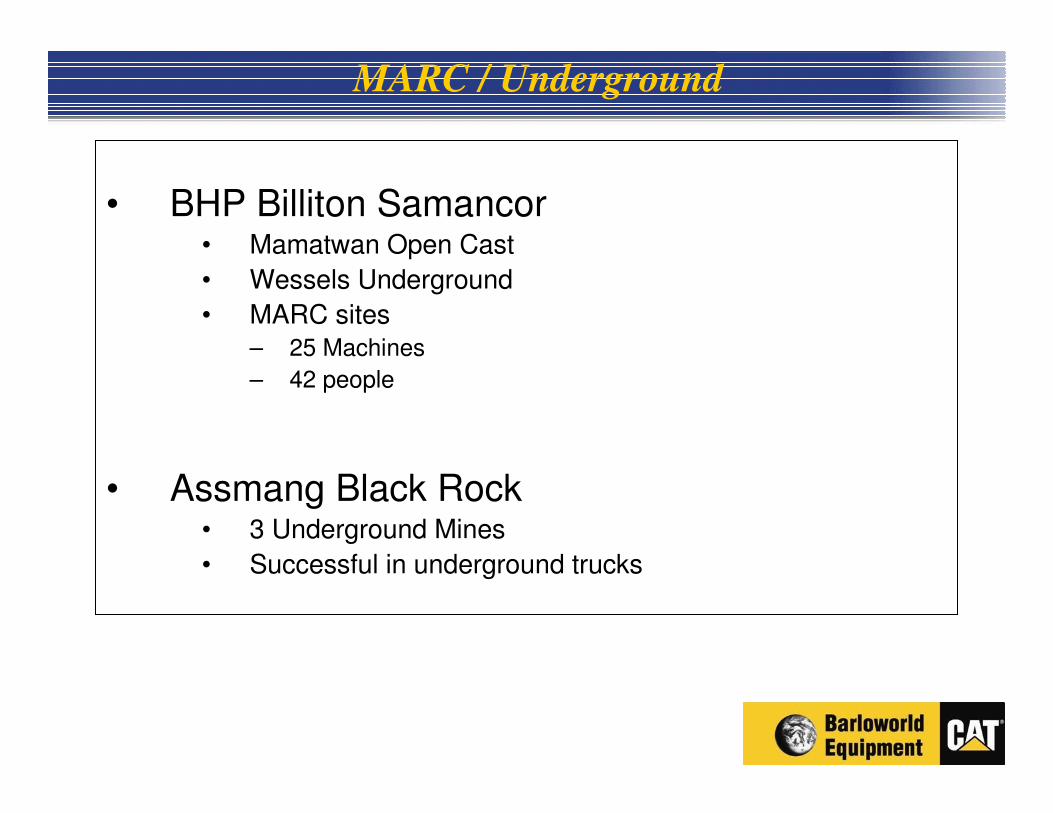

MARC / Underground

• BHP Billiton Samancor• Mamatwan Open Cast

• Wessels Underground

• MARC sites– 25 Machines

– 42 people

• Assmang Black Rock• 3 Underground Mines

• Successful in underground trucks

Assmang Beeshoek

• 24 Cat Machines and 3 Loco Engines

– 92% market share on new machines (PINS)

• Policy of using OEM parts

– 92% market share on Parts (DCAL)

• Tend to do own servicing

– Own capability

• Caterpillar oil well accepted

• Presence of contract miners

– 12 Caterpillar 100t trucks

Assmang Khumani

• New Iron ore mine starting Feb 2007

• Equipment awarded for phase 1• 100% Caterpillar

Equipment• Expect 95 % parts DCAL• On Site Dealer Support

• Blast Hole Drills• 100% PINS• Expect 95% parts DCAL• Aquila Technology (Drill

Monitoring and Navigation)

• Caterpillar Lubricants• Fluid Link• In Pit Service• On Site Support

–

Kumba Sishen

• Expansion• SEP (Sishen Expansion

Project)

• Sishen South

• We supply support equipment• 76 Machines

• 55% PINS

• 85% parts DCAL

• 100% of large haul trucks are electric drive

• Caterpillar have announced electric drive truck development

Northern Cape Logistics

• Staff compliment 72

• Limited infrastructure

– On site presence

– Parts satellite stores

• Field service capability

– Local learnership program

• Parts deliver to mines

– Daily run from Isando to Kuruman

• Receive parts 6 am in Kuruman

• Dispatch to mines at 7am

– Emergency parts can be supplied within 6 hours from Isando

Microsoft PowerPoint

PresentationMicrosoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Isando

SishenMicrosoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Saldanha

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

Microsoft PowerPoint

Presentation

KurumanMicrosoft PowerPoint

Presentation

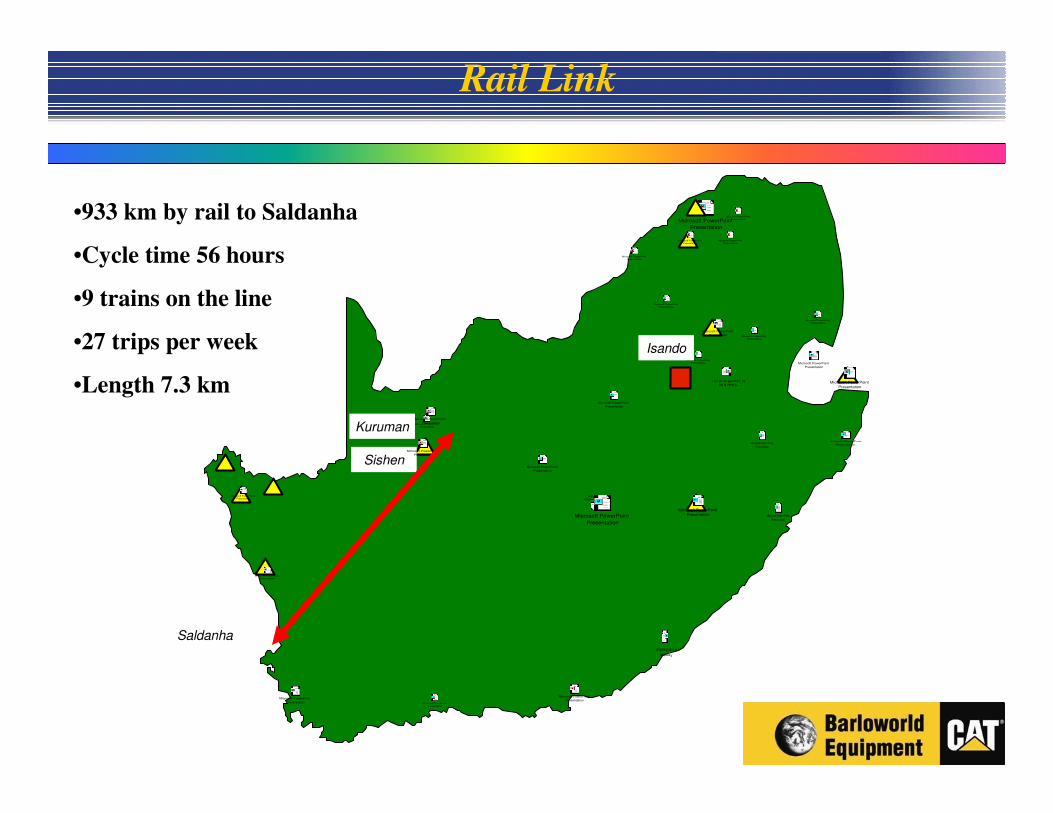

•933 km by rail to Saldanha

•Cycle time 56 hours

•9 trains on the line

•27 trips per week

•Length 7.3 km

Rail Link

Rail Link cont.

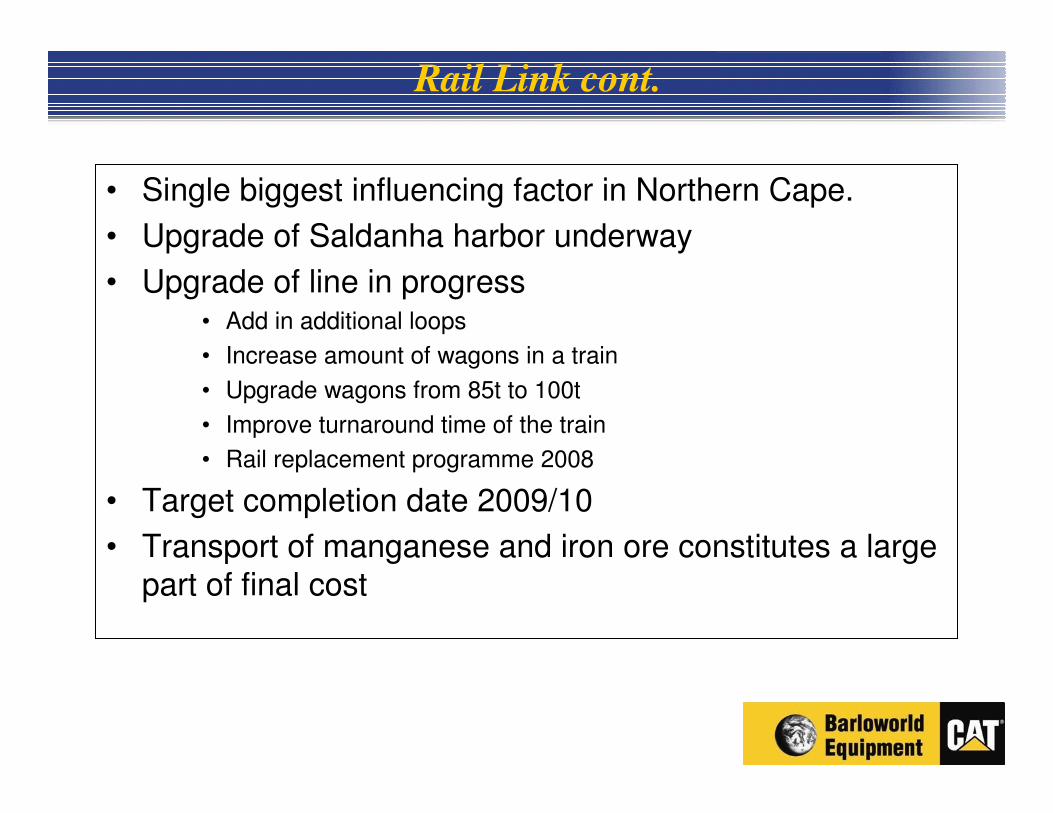

• Single biggest influencing factor in Northern Cape.

• Upgrade of Saldanha harbor underway

• Upgrade of line in progress• Add in additional loops

• Increase amount of wagons in a train

• Upgrade wagons from 85t to 100t

• Improve turnaround time of the train

• Rail replacement programme 2008

• Target completion date 2009/10

• Transport of manganese and iron ore constitutes a large part of final cost

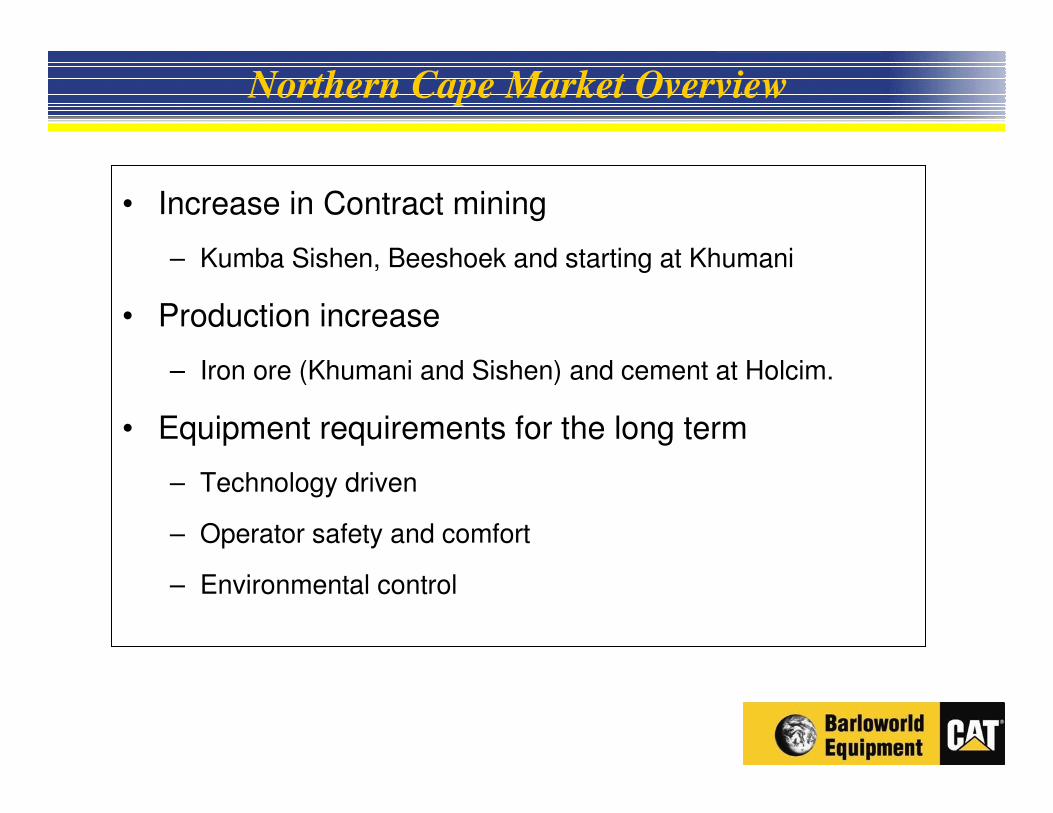

Northern Cape Market Overview

• Increase in Contract mining

– Kumba Sishen, Beeshoek and starting at Khumani

• Production increase

– Iron ore (Khumani and Sishen) and cement at Holcim.

• Equipment requirements for the long term

– Technology driven

– Operator safety and comfort

– Environmental control

The land of opportunity

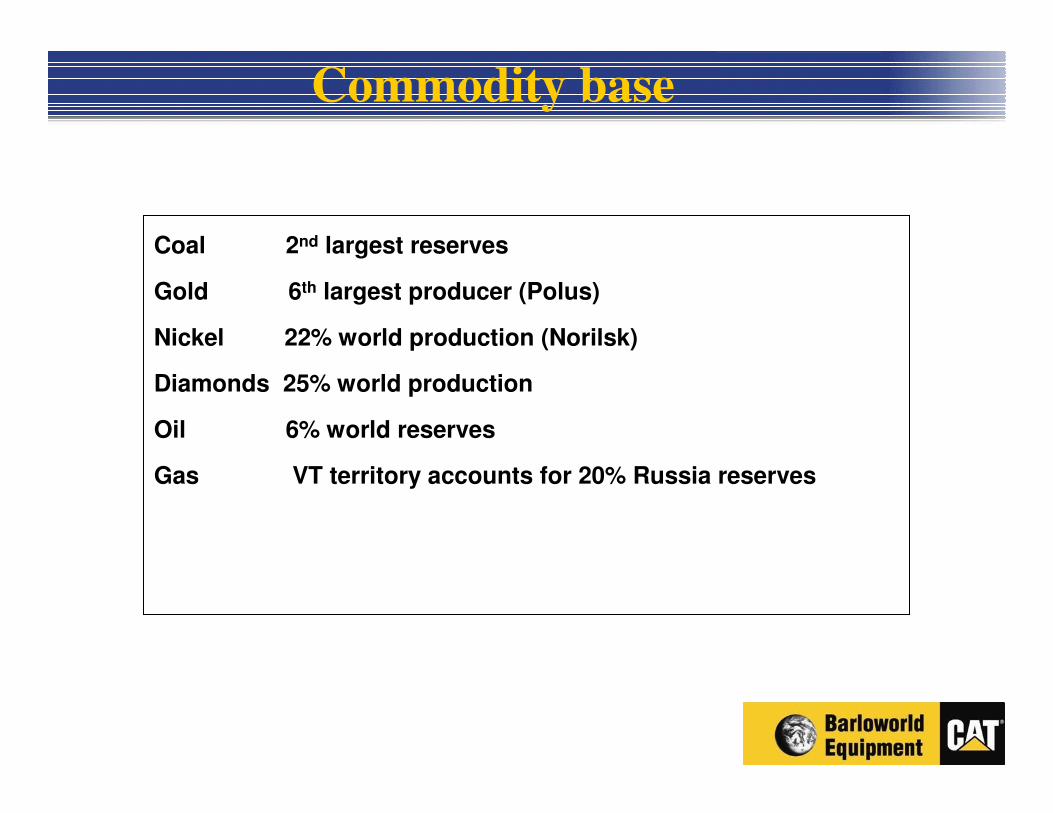

Coal 2nd largest reserves

Gold 6th largest producer (Polus)

Nickel 22% world production (Norilsk)

Diamonds 25% world production

Oil 6% world reserves

Gas VT territory accounts for 20% Russia reserves

Commodity base

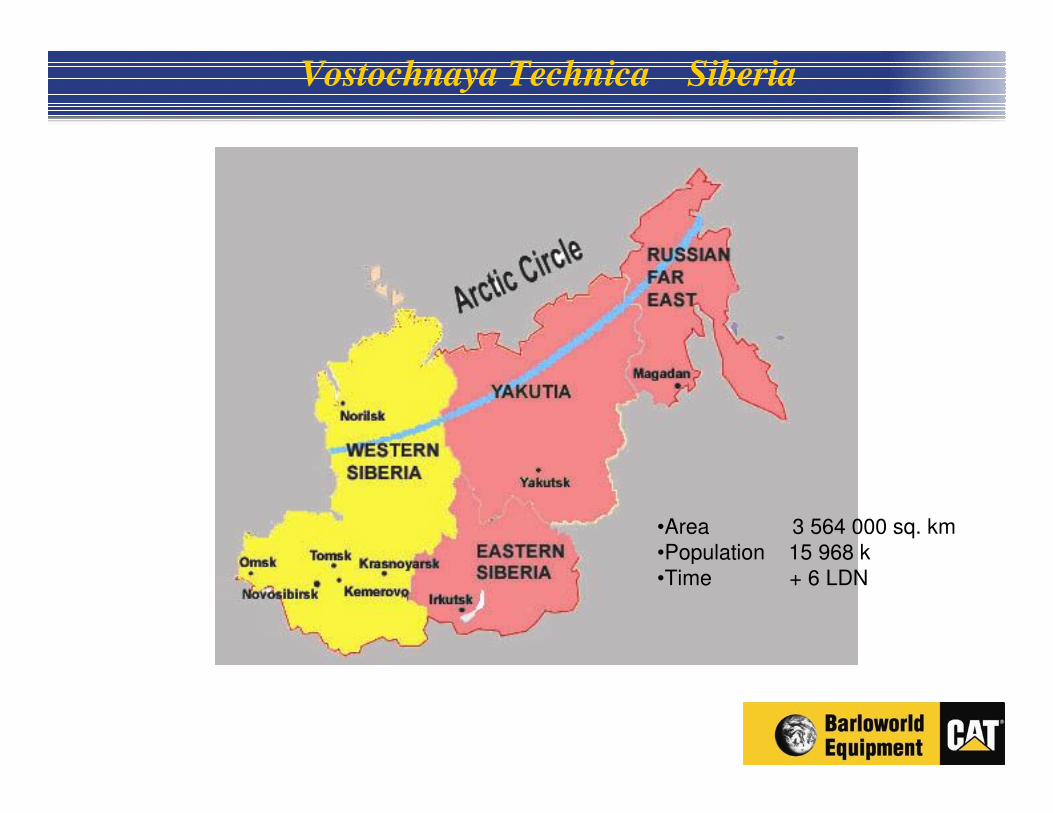

Vostochnaya Technica Siberia

•Area 3 564 000 sq. km•Population 15 968 k•Time + 6 LDN

East Siberia Pacific Oil

Route: Taishet – Skovorodino – PerevoznayaLength – 4130 km, pipe diameter – 1220 mm

Capital investment – $11 billion

On track for $100m target

Conclusion

• Machine Cycle from Replacement to Expansion

• Customer Backorder at R4,3bn (6/06) R 3bn (3/06)

• Truck availability constrained by tyre shortages

• Demand for quality people