estate buy-back strategy lending limitations may 26, 2015 1

TRANSCRIPT

1

Estate Buy-Back StrategyLending Limitations

May 26, 2015

2

2012 Time Machine

Full Transfer at Death – 2012 Taxable Estate $ 15,000,000 Exemption $ 7,000,000 Net Estate $ 8,000,000 Transfer Tax Rate 35% CA Capital Gains Tax 0% Federal Capital Gains Tax 0% Total Tax $2,800,000

H&W have a $15M gross estate (assume a 25% basis). None of H&W’s assets are Crown Jewels (all assets will be sold upon their death). Were H&W to have passed away in 2012, the tax affect would have looked somewhat as follows:

3

The belief was that come January 2013 the highest marginal transfer tax rate was going to increase to 55% and the Exemption was going to drop to $1M. Without lifetime gifting, the belief was that H&W’s estate (should they pass away in 2013) would suffer somewhat the following results:

Full Transfer at Death – 2013 Taxable Estate $ 15,000,000 Exemption $ 2,000,000 Net Estate $ 13,000,000 Transfer Tax Rate 55% CA Income Tax 0% Federal Capital Gains Tax 0% Total Tax $7,150,000

The difference between using your exemption and not using your exemption was $4,350,000 if the Exemption had, in fact, dropped to $1M and if the rates had,

in fact, increased.

4

The Rush Was On

2012 Inter-Vivos Gifts, Death in 2013 Taxable Estate $ 15,000,000 Exemption Used $ 7,000,000 Net Taxable Estate $ 8,000,000 Transfer Tax Rate 55% Step-Up Assets $ 8,000,000 Non-Step-up Assets $ 7,000,000 Basis of Non Step-up Assets $ 1,750,000 Assets Subject to CG & Income Tax $ 5,250,000 CA Income Tax Rate 9.3% CA Income Tax $ 488,250 Federal CG Rate 15% Federal CG Tax $ 1,837,500 Total CG & Income Tax $ 2,325,750 Transfer Tax $ 4,400,000 Total Tax $ 6,725,750

At the end of 2012, there was a rush to transfer low-basis/highly-appreciating assets to intentionally defective grantor trusts (IDGTs). Many spousal lifetime access trusts (SLATs) were also created as a safety measure.

Setting aside cash-flow analyses to the contrary, assume that H&W’s estate planning attorney recommended that they transfer their maximum allowable then-existing Exemption amount ($3.5M per person for a total transfer to an IDGT of $7M). Assume H&W were to pass away in 2013, the tax affect would have been something akin to the following:

Assumptions* Assume payment of estate tax from outside source, such as an irrevocable life trust (ILIT)

** Real purpose was to permit the $7M transferred to grow outside of the Grantors’ estates. This illustration, for sake of simplicity, assumes death in early 2013 almost immediately following 2012 gifting.

Assumed savings v. no 2012 Gifting = $424,250

5

Now, assume H&W were to pass away in 2015. The tax affect might look something like the following:

2012 Inter-Vivos Gifts, Death in 2015 Taxable Estate $ 15,000,000 Lifetime Exemption Used $ 7,000,000 Gross Estate $ 8,000,000 Remaining Exemption $ 3,860,000 Net Taxable Estate $ 4,140,000 Transfer Tax Rate 40% Step-Up Assets $ 8,000,000 Non-Step-up Assets $ 7,000,000 Basis $ 1,750,000 Assets Subject to CG & Income Tax $ 5,250,000 CA Income Tax Rate 13.30% CA Income Tax $ 698,250 Federal CG Rate 20% Federal CG Tax $ 2,079,000 Obamacare 3.80% Obamacare Tax $ 199,500 Total CG & Income Tax $ 2,976,750 Transfer Tax $ 1,656,000 Total Tax $ 4,632,750

6

The 2012 Fiscal Cliff Negotiations

In Q4 2012, Congress and the President negotiated an end to the “Fiscal Cliff.” In part, the negotiations resulted in an Exemption at the TRA 2010 level of $5M adjusted upwards annually for inflation, portability was made permanent, and the highest marginal transfer tax bracket increased to 40%.

Significantly, since the 2012 changes, income taxes (including the Obamacare increases and the CA state income tax rate increases) are almost identical to the transfer tax rate.

7

Had H&W not done 2012 transfers and died in 2015, the result might look as follows:

No 2012 Inter-Vivos Gifts, Death in 2015 Taxable Estate $ 15,000,000 Estate Tax Exemption $ 10,860,000 Net Estate $ 4,140,000 Transfer Tax Rate 40% Step-Up Assets $ 15,000,000 Non-Step-up Assets $ - Basis $ - Assets Subject to CG & Income Tax $ - CA Income Tax Rate 13.30% CA Income Tax $ - Federal CG Rate 20% Federal CG Tax $ - Obamacare 3.80% Obamacare Tax $ - Total CG & Income Tax $ - Transfer Tax $ 1,656,000 Total Tax $ 1,656,000

Difference between 2012 Transfers and Death in 2015 v. Death in 2015

with NO 2012 Transfers = $2,976,750

* Assume payment of estate tax from outside source, such as an ILIT

8

It’s All About IRC §1014

It is the cumulative effect of Federal Capital Gains Taxes, CA State income taxes, and the Obamacare 3.8% tax that have led to the understanding that many of the low-basis asset transfers made in 2012, although done for the right reasons, have turned out to be less effective that originally hoped.

Federal CG Taxes + CA Income Taxes + Obamacare = 37.1%

Federal Estate Tax = 40%

Nearly identical

26 U.S. C. §1014 (a) In general Except as otherwise provided in this section, the basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall, if not sold, exchanged, or otherwise disposed of before the decedent’s death by such person, be— (1) the fair market value of the property at the date of the decedent’s death,

9

Grantor TrustsMost of the trusts funded in 2012 were Grantor Trusts containing an IRC §675(4)(C) “power of substitution.” Also, many transfers were of discounted closely held stock and real estate. These types of transfers in trust are subject to the “carryover-basis” rules [IRC §1015].

Rev. Rul. 85-13 – A grantor of an irrevocable trust may be treated as owner of the trust assets for income tax purposes but not estate tax purposes.

Rev. Rul. 2004-64 – Grantor’s payment of income taxes on investment income of assets held in an irrevocable trust was not a taxable gift.

Rev. Rul. 2007-13 – A transfer of a life insurance policy from one irrevocable grantor trust to another irrevocable grantor trust does not (1) violate the “transfer for value” rule and (2) the death proceeds remained income-tax free [IRC §101].

Rev. Rul. 2008-22 – Exercising a “power of substitution” [IRC §675(4)(C)] would not lead to inclusion of the substituted assets in the grantor’s taxable estate under either IRC Section 2036(a) (a retained life interest) or IRC Section 2038 (a power to alter, amend, or revoke).

26 U.S. C. §675 The grantor shall be treated as the owner of any portion of a trust in respect of which—…(4) General powers of administration A power of administration is exercisable in a nonfiduciary capacity by any person without the approval or consent of any person in a fiduciary capacity. For purposes of this paragraph, the term “power of administration” means any one or more of the following powers: …(C) a power to reacquire the trust corpus by substituting other property of an equivalent value.

10

Grantor Trusts

26 U.S.C. §2038 (a) In general The value of the gross estate shall include the value of all property — (1) Transfers after June 22, 1936 To the extent of any interest therein of which the decedent has at any time made a transfer (except in case of a bona fide sale for an adequate and full consideration in money or money’s worth), by trust or otherwise, where the enjoyment thereof was subject at the date of his death to any change through the exercise of a power (in whatever capacity exercisable) by the decedent alone or by the decedent in conjunction with any other person (without regard to when or from what source the decedent acquired such power), to alter, amend, revoke, or terminate, or where any such power is relinquished during the 3 year period ending on the date of the decedent’s death.

11

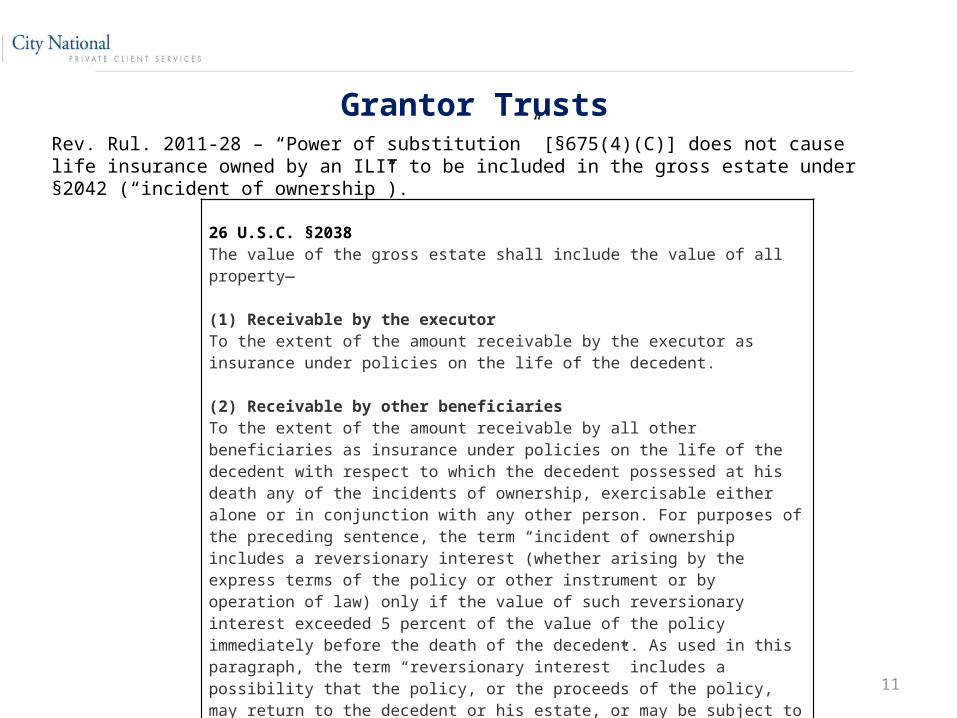

Grantor TrustsRev. Rul. 2011-28 – “Power of substitution” [§675(4)(C)] does not cause life insurance owned by an ILIT to be included in the gross estate under §2042 (“incident of ownership”).

26 U.S.C. §2038The value of the gross estate shall include the value of all property— (1) Receivable by the executor To the extent of the amount receivable by the executor as insurance under policies on the life of the decedent. (2) Receivable by other beneficiaries To the extent of the amount receivable by all other beneficiaries as insurance under policies on the life of the decedent with respect to which the decedent possessed at his death any of the incidents of ownership, exercisable either alone or in conjunction with any other person. For purposes of the preceding sentence, the term “incident of ownership” includes a reversionary interest (whether arising by the express terms of the policy or other instrument or by operation of law) only if the value of such reversionary interest exceeded 5 percent of the value of the policy immediately before the death of the decedent. As used in this paragraph, the term “reversionary interest” includes a possibility that the policy, or the proceeds of the policy, may return to the decedent or his estate, or may be subject to a power of disposition by him. The value of a reversionary interest at any time shall be determined (without regard to the fact of the decedent’s death) by usual methods of valuation, including the use of tables of mortality and actuarial principles, pursuant to regulations prescribed by the Secretary. In determining the value of a possibility that the policy or proceeds thereof may be subject to a power of disposition by the decedent, such possibility shall be valued as if it were a possibility that such policy or proceeds may return to the decedent or his estate.

12

Planning Concept

Exercise the Grantor’s power of substitution by substituting high-basis assets equal to the appraised FMV of the trust’s low-basis assets.

OR

Substitute cash equal to the appraised FMV of the trust’s low-basis assets.

Low-basis assets returned to Grantor.

Trust steps-up its basis to cash.

Trust invests the cash. Typical investments are a managed accounts with tailored investment policy statements. An alternative is to acquire an SUL policy meeting the 7-pay test (MEC consideration).

Grantor holds the low-basis assets until death and uses Grantor’s then remaining Exemption (and its inflation adjustment) at death (and not during life) in order to obtain a step-up.

Restrict lifetime gifting to high-basis assets.

13

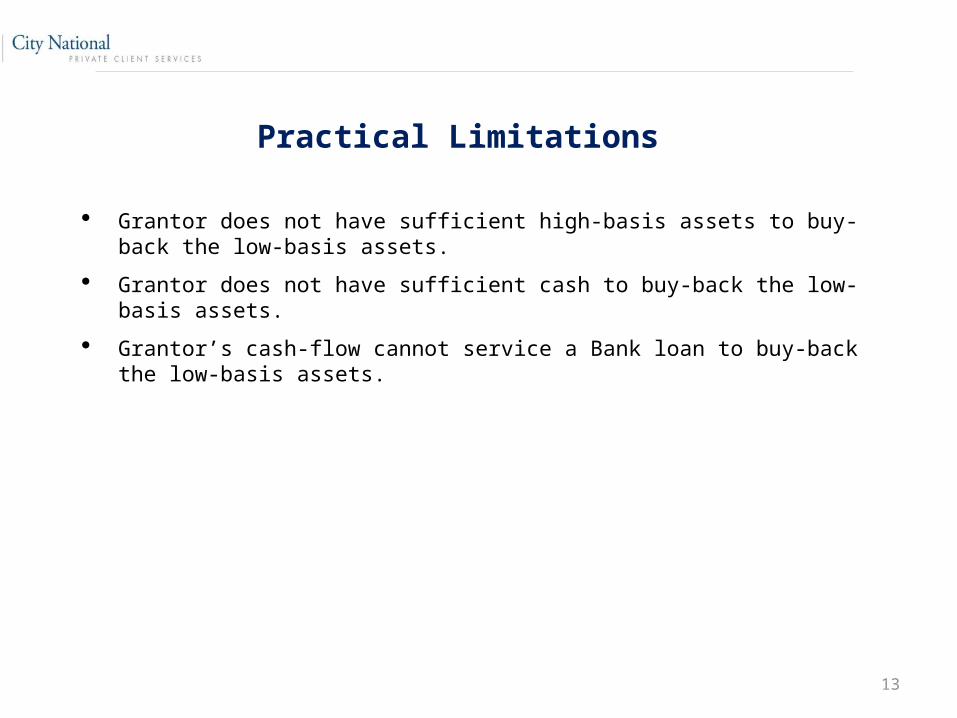

Practical Limitations

Grantor does not have sufficient high-basis assets to buy-back the low-basis assets.

Grantor does not have sufficient cash to buy-back the low-basis assets.

Grantor’s cash-flow cannot service a Bank loan to buy-back the low-basis assets.

14

Solution Being Proposed Grantor enters into a fee relationship with a lender.

Lender underwrites an uncommitted, unfunded stand-by line of credit (“SLOC”).

When Grantor is on death-bed, Grantor (or Grantor’s Agent) completes loan docs and the loan funds. However, this could be problematic and subject all parties to Elder Abuse allegations. Banks typically do not accept death bed loan documents.

Grantor (or Grantor’s Agent) then buys-back the low-basis assets from the IDGT.

IDGT basis now stepped-up to cash.

Grantor dies holding low-basis assets.

Low-basis assets passed to heirs up to remaining Exemption.

Estate then sells the (formerly) low basis assets (which now have a high-basis) to the IDIT for no gain and retrieves the cash which is used to pay-off the loan.

15

Bank Perspective

Staffing – The underwriting of these types of loans is time consuming due to the technical nature and regulatory demands.

Source of Repayment – A client might be cash constrained if the bulk of a client’s estate was

transferred into a trust. Given the client’s cash crunch, obtaining a commercial loan to buy back the assets can be difficult.

Solution: Have the IDGT guarantee the loan, parent pays the IDGT a guarantee fee (e.g., 1.5%), leading to an additional estate tax savings (equal to 40% of the cash used to pay the guarantee fee).

Sarbanes Oxley – This type of SLOC request may create a commitment to lend. A bank must account for all commitments and hold-back working capital against that commitment. There is no method for accounting for, pricing, or holding reserves against a phantom loan.

Sound Mind Considerations –Due to the timing of the signatures a bank will have legal questions

about the loan and need to demonstrate that the decedent executed loan documents with a sound mind. Additional legal concerns may arise regarding authority to disburse funds and act on behalf of the estate. Banks will need to determine their own appetite for risk regarding these types of transactions.

Solution: Durable Power of Attorney will permit Agent to enter into the agreement.

16

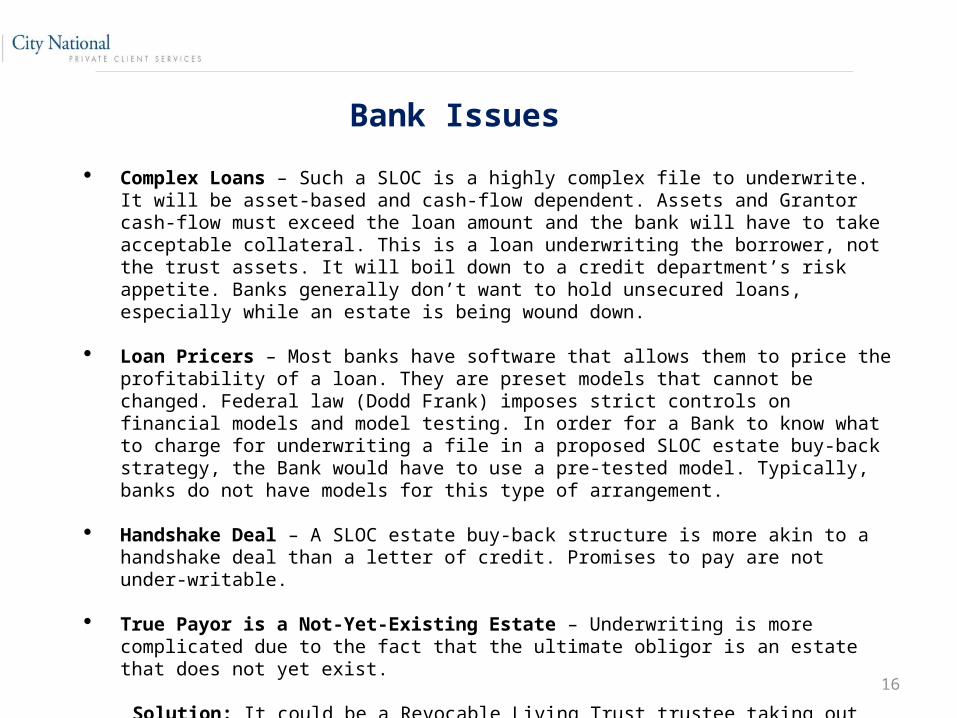

Bank Issues Complex Loans – Such a SLOC is a highly complex file to underwrite. It will be asset-based and cash-

flow dependent. Assets and Grantor cash-flow must exceed the loan amount and the bank will have to take acceptable collateral. This is a loan underwriting the borrower, not the trust assets. It will boil down to a credit department’s risk appetite. Banks generally don’t want to hold unsecured loans, especially while an estate is being wound down.

Loan Pricers – Most banks have software that allows them to price the profitability of a loan. They are

preset models that cannot be changed. Federal law (Dodd Frank) imposes strict controls on financial models and model testing. In order for a Bank to know what to charge for underwriting a file in a proposed SLOC estate buy-back strategy, the Bank would have to use a pre-tested model. Typically, banks do not have models for this type of arrangement.

Handshake Deal – A SLOC estate buy-back structure is more akin to a handshake deal than a letter of

credit. Promises to pay are not under-writable.

True Payor is a Not-Yet-Existing Estate – Underwriting is more complicated due to the fact that the ultimate obligor is an estate that does not yet exist.

Solution: It could be a Revocable Living Trust trustee taking out the loan (not a person), which is an existing and continuing obligor.

17

Bank Issues

Time Considerations – When underwriting a loan, a bank must project the time-horizon for its

commitment. In this case, time-horizon is unknown, therefore it is difficult to determine when the a triggering event will occur.

Excess Prior Gifting – A client who transferred the bulk of their estate to an IDGT may never be

able to qualify. Solution: IDGT Trustee guarantees the loan.

Per Capita Loan Thresholds – Most banks have a per capita lending restriction. Loans to any single person/estate at or above that amount are prohibited to them (e.g., $50M) and would have to be syndicated.

Elder Abuse Concerns – “Deathbed” signatures are problematic and subject to challenge by

courts and heirs.

Solution: Negotiate the arrangement long before such an issue arises (not a deathbed signature) or do it with a POA.

18

Bank Issues

Global Cash Flow – Buying-back closely-held assets will be very complicated due to the nature of

underwriting such assets in general.

Finite Duration – A SLOC is a commitment for a finite amount of time, typically 364 days, which minimizes required reserve capital. The underwriting process would have to be undertaken on an annual basis. The concept of just updating a file is not as simple as it sounds.

19

Successful Candidates

Clients who are very credit worthy (especially with IDGT guarantee). Proposed loan must be under the bank’s per capital lending threshold. Assets in trust should represent a small percent of the client’s overall estate (but not necessarily if the

IDGT guarantees the loan) or loan could be guaranteed by the IDGT. Client would have to have a large relationship with the bank or a significant prospective client.

20

Alternatives for Consideration

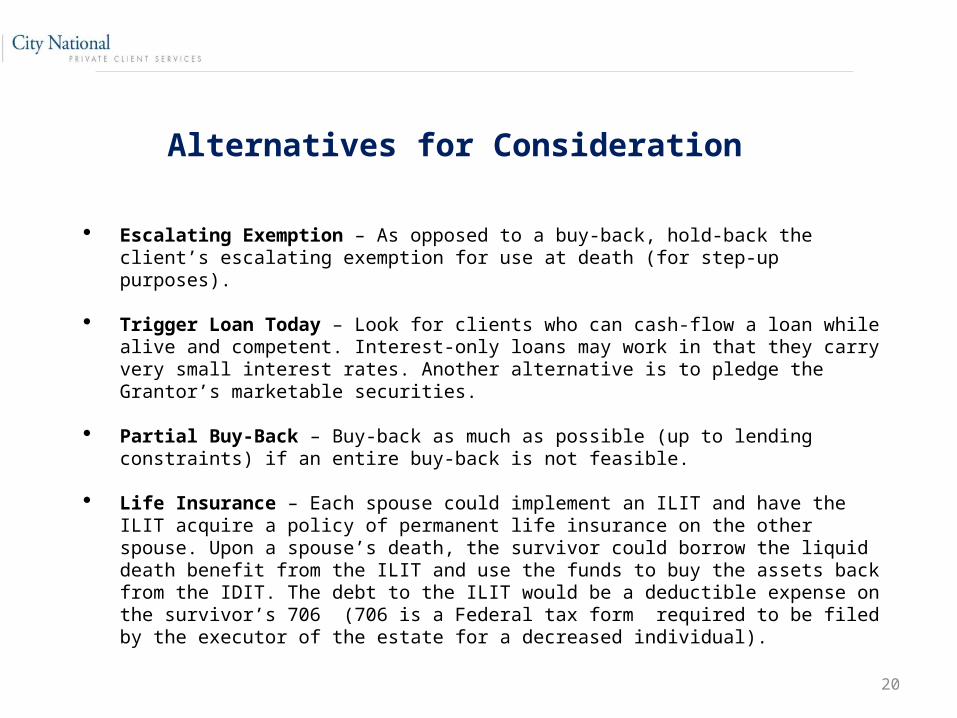

Escalating Exemption – As opposed to a buy-back, hold-back the client’s escalating exemption for use

at death (for step-up purposes). Trigger Loan Today – Look for clients who can cash-flow a loan while alive and competent. Interest-

only loans may work in that they carry very small interest rates. Another alternative is to pledge the Grantor’s marketable securities.

Partial Buy-Back – Buy-back as much as possible (up to lending constraints) if an entire buy-back is

not feasible.

Life Insurance – Each spouse could implement an ILIT and have the ILIT acquire a policy of permanent life insurance on the other spouse. Upon a spouse’s death, the survivor could borrow the liquid death benefit from the ILIT and use the funds to buy the assets back from the IDIT. The debt to the ILIT would be a deductible expense on the survivor’s 706 (706 is a Federal tax form required to be filed by the executor of the estate for a decreased individual).

21

Conclusion

Reacquiring low-basis assets from a Grantor Trust via a bank loan facility is complex. Familiarize yourself with the bank’s lending policy and appetite for risk prior to entering into a

negotiation. Credit lenders may not understand the estate buy-back concept, so be patient. You may not understand the underwriting process, so be patient!

¹City National Bank, as a matter of policy, does not give tax, accounting, regulatory or legal advice. The effectiveness of the strategies presented in this document will depend on the unique characteristics of your situation and on a number of complex factors. Rules in the areas of law, tax, and accounting are subject to change and open to varying interpretations. The strategies presented in this document were not intended to be used, and cannot be used for the purpose of avoiding any tax penalties that may be imposed. The strategies were not written to support the promotion or marketing to another person of any transaction or matter addressed. Before implementation, you should consult with your other advisors on the tax, accounting and legal implications of the proposed strategies based on your particular circumstances.