evaluating the infrastructure for crisis management

TRANSCRIPT

Evaluating the Infrastructure for Crisis Management 1Nairobi, May 15-17, 2006

World Bank Seminar on Financial Stability and Development

EVALUATING THE INFRASTRUCTURE FOR CRISIS

MANAGEMENT

Yira MascaróSenior Financial Economist

World Bank

Evaluating the Infrastructure for Crisis Management 2Nairobi, May 15-17, 2006

Structure Of PresentationI. Introduction Importance of crisis management infrastructure Banking safety net: definition

II. Elements of a banking safety net Prompt corrective regime Lender of last resort facilities Explicit deposit insurance Intervention Bank Resolution

III. Bank resolution (BR) Framework Pillars Bank resolution schemes: List and selection criteria

IV. Systemic crisis management 17. Containing the crisis18. Asset management and corporate restructuring

Evaluating the Infrastructure for Crisis Management 3Nairobi, May 15-17, 2006

Importance of crisis management infrastructure: minimize occurrence, costs, and risks of banking crises

• Relatively frequent events:– From late 1970s to 1999 113 systemic crises in 93 countries and 50 non-

systemic crises in 44 countries (Caprio and Klingebiel 2000)

• High costs: banking crises generally imply large costs (e.g. Gross cost above 30 % in Indonesia, Chile, Thailand, turkey, Korea, Jamaica)

– Costs tend to vary not only depending on severity of crises, but on the way and speed these events are handled

• High risks: contagion risk particularly important for developing countries

Danger for stability and health of financial system

I. Introduction

Evaluating the Infrastructure for Crisis Management 4Nairobi, May 15-17, 2006

Banking safety net

• Definition (de la Torre 2006) : Integrated and interrelated functions to manage individual and systemic banking crises, while striking a balance to limit:

– contagion risk– scope for self-fulfilling runs– moral hazard

• Goal: Increase readiness to increase speed and reduce costs, while enabling better handling of constraints (including political)

– infrastructure in place, which can be assessed and should be kept updated– training – clarity of roles (time is of the essence)

I. Introduction (cont.)

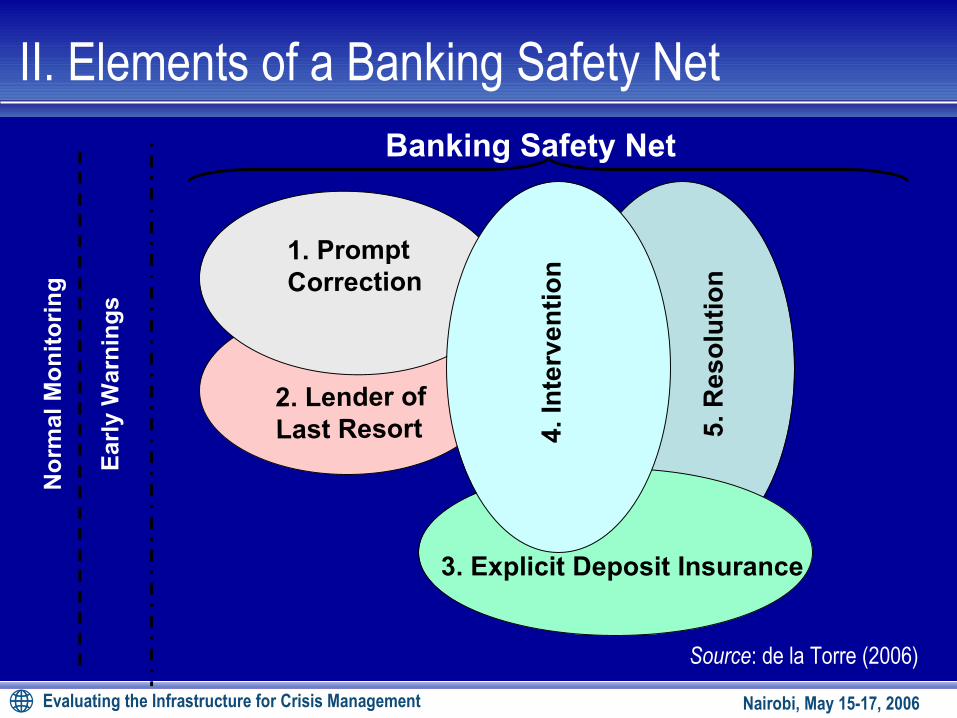

Evaluating the Infrastructure for Crisis Management 5Nairobi, May 15-17, 20065

. Re

so

luti

on

3. Explicit Deposit Insurance

1. Prompt Correction

4. In

terv

en

tio

n

2. Lender ofLast Resort

No

rmal

Mo

nit

ori

ng

Ear

ly W

arn

ing

s

Banking Safety Net

Source: de la Torre (2006)

II. Elements of a Banking Safety Net

Evaluating the Infrastructure for Crisis Management 6Nairobi, May 15-17, 2006

1. Prompt corrective regime

• Importance: sizeable costs when failing to intervene early

• Goal: early identification of weaknesses leading to preventive and corrective measures that may avoid crisis or reduce costs

• Guideline: corrective actions proportional to seriousness of problem

• Key elements: clear triggers for intervention, regularization plans to be submitted by banks, and legal background with necessary authority and protection for governmental officials

II. Elements of a Banking Safety Net

Evaluating the Infrastructure for Crisis Management 7Nairobi, May 15-17, 2006

1. Lender of last resort facilities• Concept: discretionary provision of liquidity for solvent banks

• Goal: avoid disruptions to payment system, contagion, and fire-sale insolvency (emerging from occasional liquidity problems)

• To enable cost and risk minimization:– Well-collateralized, high interest rates etc.– Occasional, once market sources are exhausted (e.g., due to shocks - Bolivia)– Set pre-established internal guidelines, including inter-institutional coordination

• Risk of abuse or misuse:– Increase moral hazard (informed dep.) - Mask hard-to-determine insolvency– Delay bank resolution - weaken choice of collateral – May enable further asset stripping - insufficient sterilization (postponed costs)

II. Elements of a Banking Safety Net (cont.)

Evaluating the Infrastructure for Crisis Management 8Nairobi, May 15-17, 2006

3. Explicit deposit insurance

• Benefits: allow rapid deposit payout to avoid contagion, facilitate bank resolution, limit government responsibility to cover insolvent banks, protect small and unsophisticated depositors

• Costs: administration costs and risks (e.g., Moral hazard, reduced market discipline )

Need adequate design to minimize costs (ample literature)

II. Elements of a Banking Safety Net (cont.)

Evaluating the Infrastructure for Crisis Management 9Nairobi, May 15-17, 2006

3. Explicit deposit insurance - key design features:• Defined by law and supported by regulation; Compulsory membership

• Limited coverage per account and depositor (and coinsurance)

• Appropriate funding features: ex-ante system, mixed funding (mostly private), risk-sensitive premiums (mixed) and adequate solvency

• Clear monitoring function

• Ability to participate in bank resolution

• Adapted to institutional environment in place

• Independence and accountability

II. Elements of a Banking Safety Net (cont.)

Evaluating the Infrastructure for Crisis Management 10Nairobi, May 15-17, 2006

II. Elements of a Bank Safety Net (cont.)

1. Intervention

• Concept: discretionary official authority takes direct managerial control of bank to (i) protect its assets; (ii) assess its financial condition and; (iii) bring the bank back to compliance or resolve it (WB and IMF 2005).

• Most efficient if: – short-lived: intervention without resolution is an unstable (and costly) equilibrium

– authorities adequately empowered to: (i) take action; (ii) balance among market discipline, financial stability, and property rights) and (iii) enable sufficient flexibility (especially for systemic cases)

• Typical legal triggers for suspension of operations: (i) “insolvency”; (ii) failure to meet prompt corrective requirements; (iii) failure to honor payments; (iv) chronic and irreversible illiquidity; and (v) unsound and fraudulent management

Evaluating the Infrastructure for Crisis Management 11Nairobi, May 15-17, 2006

Bank Resolution Definition

Component of a banking safety net consisting of procedures and measures taken by the authorities to solve the situation of an unviable bank (Bolzico, et.al., 2004).

Pillars

Preconditions for the institutional framework to facilitate an efficient bank resolution process

Efficient: minimizes costs, preserves assets and banking services, reduces moral hazard, market-friendly

II. Elements of a Bank Safety Net (cont.)

Evaluating the Infrastructure for Crisis Management 12Nairobi, May 15-17, 2006

DepositInsurance

Agency

Formalprocedures

Implemen-tation

Capability

Properlegislation

EnhancedSupervision

BankCapitalization

Fund

Pillars (source: Bolzico et. al, 2004):

III. Bank Resolution Framework

Pillars for an Efficient Bank Resolution Scheme

Evaluating the Infrastructure for Crisis Management 13Nairobi, May 15-17, 2006

1.1. Proper legislation• Establish clear and consistent assignment of roles and responsibilities• Grant legal capabilities to the supervisor• Provide adequate protection to the authorities• Define clear priority of claims• Specify a worst case scenario solution (liquidation)• Provide legal certainty

1.2. Deposit insurance agency• Provides flexibility to implement a wider variety of BR schemes (especially

important for purchase-and-assumption -P&A) • Reduces resolution delays: depositors and public more likely supportive

III. Bank Resolution Framework (cont.)

Evaluating the Infrastructure for Crisis Management 14Nairobi, May 15-17, 2006

1.3. Enhanced supervision• Reduces moral hazard:– Minimizes the number of banks to be resolved– Facilitates efficient bank resolution with reliable information and early intervention

• But, it entails: – Compliance with Basel committee’s core principles (BCPs) for effective banking

supervision– Early intervention to decrease unviable banks and decrease costs of resolution– Move towards risk-based supervision

III. Bank Resolution Framework (cont.)

Evaluating the Infrastructure for Crisis Management 15Nairobi, May 15-17, 2006

1.4. Formal procedures

• Benefits:– Increase speed and transparency of BR process– Enhance efficiency by avoiding improvisation and promoting early intervention

• Basic elements:– Triggers for commencing BR process– BR manual specifying all necessary actions for BR– Pro-forma contracts– Pre-designed models for separation procedures– Central bank regulations

III. Bank Resolution Framework (cont.)

Evaluating the Infrastructure for Crisis Management 16Nairobi, May 15-17, 2006

1.5. Implementation capabilities• For adequate implementation of BR procedures

• BR calls for qualified individuals with wide variety of skills

• To attract and retain personnel: selection process, career development, competitive compensation, constant training

1.6. Bank capitalization fund• Useful tool for BR (e.g., LAC)

• Benefits: – Encourages the participation of potential buyers– Strengthens operation with capital injection

III. Bank Resolution Framework (cont.)

Evaluating the Infrastructure for Crisis Management 17Nairobi, May 15-17, 2006

2. Bank resolution schemes2.1. List (Basle Committee):• Radical restructuring– Concept: Intervention of key areas of unviable bank

– Advantage: most suitable for big banks (difficult to apply other schemes) – Disadvantages: can be very costly (e.g., in weak institutional environments

with mismanagement of public companies) and increases moral hazard

• Mergers and Acquisitions (M&A)– Concept: M&A of unviable banks by private banks

– Pre-requirements: (i) failing bank should have positive net worth; and (ii) acquiring bank should be healthy and operation should not harm it

III. Bank Resolution Framework (cont.)

Evaluating the Infrastructure for Crisis Management 18Nairobi, May 15-17, 2006

2.1. List (cont.)• P&A– Concept: Private institution(s) or investor(s) purchase some or all the assets of

the failing bank and assume some or all of its liabilities

– Requirements: Financially attractive; intensive role (and skills) of supervisory authorities

Good Bank – Bad Bank (GB-BB): successful P&A scheme with

failing bank separated in two

• Bridge bank– Concept: Failed bank is administered by government or banks and receives

external financial support– Advantages: (i) time for the gov. to evaluate and market bank and for buyers to

assess it and submit offers; and (ii) uninterrupted service to customers

– Disadvantages: (i) postponing permanent solution with loss of value; and (ii) moral hazard increase in weak institutional environments

III. Bank Resolution

Evaluating the Infrastructure for Crisis Management 19Nairobi, May 15-17, 2006

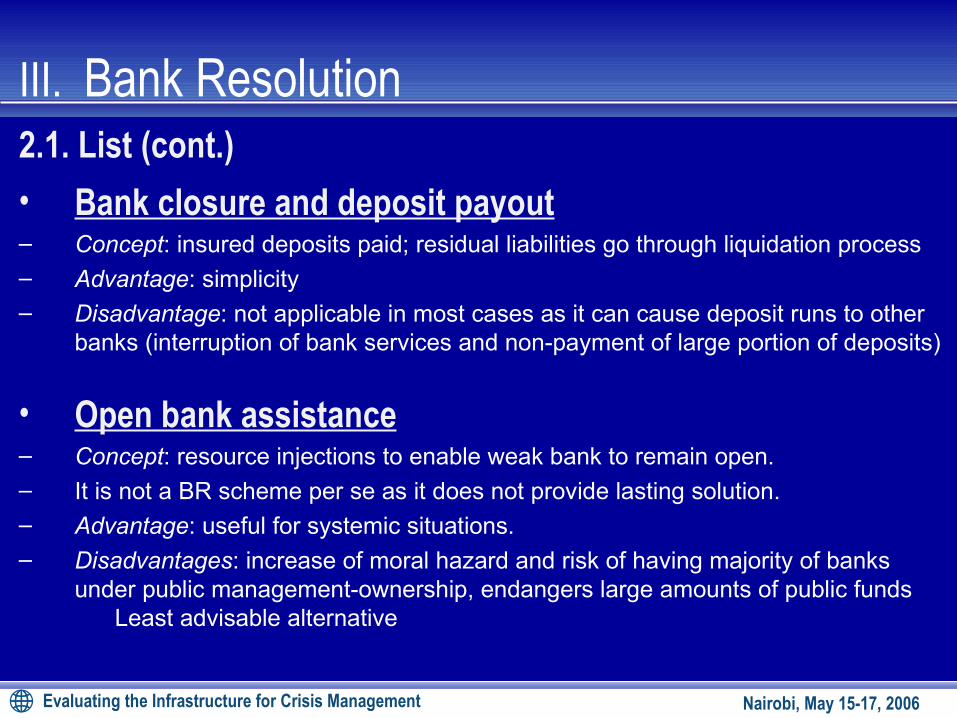

2.1. List (cont.)

• Bank closure and deposit payout– Concept: insured deposits paid; residual liabilities go through liquidation process

– Advantage: simplicity

– Disadvantage: not applicable in most cases as it can cause deposit runs to other banks (interruption of bank services and non-payment of large portion of deposits)

• Open bank assistance– Concept: resource injections to enable weak bank to remain open.

– It is not a BR scheme per se as it does not provide lasting solution.

– Advantage: useful for systemic situations.– Disadvantages: increase of moral hazard and risk of having majority of banks

under public management-ownership, endangers large amounts of public funds Least advisable alternative

III. Bank Resolution

Evaluating the Infrastructure for Crisis Management 20Nairobi, May 15-17, 2006

3.2. Selection criteria for bank resolution schemes ( Bolzico and Mascaró, mimeo)

• Enables minimization of total contagion risk: – Direct Contagion Risk: increases with coverage of deposits– Indirect Contagion Risk: Decreases with coverage of deposits

• Enables minimization of social cost

• Entails minimum protection level to depositors

• Avoids of shareholders bail out

• Ensures adequate transparency

• Enhances timely response and speedy resolution

• Considers available capacity and resources

III. Bank Resolution

Evaluating the Infrastructure for Crisis Management 21Nairobi, May 15-17, 2006

1. Containing the crisis

• systemic liquidity provision, timely bank intervention

• Important to have effective safety net in place to:– Lower occurrence of systemic crises, by adequately managing individual crisis– Enhance readiness, when crises do arise– Open bank resolution with “Accordion technique”: a la good bank-bad bank, but with

resolution agency “mimicking” the role of the market

• Crisis management infrastructure needs “structured flexibility”:– Exceptions to the rule (systemic or too big to fail cases)– High threshold of authority– Government bears costs or through surcharges on banking industry in the future– Administrative measures for uninsured depositors?

IV. Systemic Crisis Management

Evaluating the Infrastructure for Crisis Management 22Nairobi, May 15-17, 2006

1. Asset Management and corporate Restructuring:– Extensive literature on AMC with mixed results at best– Challenge is to avoid very high costs and lengthy processes– Importance of aligning expectations both regarding loan recovery and successful

corporate restructuring– Importance of bankruptcy and corporate restructuring laws

IV. Systemic Crisis Management

Evaluating the Infrastructure for Crisis Management 23Nairobi, May 15-17, 2006

Bolzico, Javier, Alberto Figueroa, Yira Mascaró, and Ricardo Tappatá (2004). “ Bank Resolution Workshop”. The World Bank. Washington, DC (December)

Bolzico, Javier and Yira Mascaró. “ A Conceptual Framework for Contagion Risks in the Context of Bank Resolution”. Washington, DC (Mimeo, work in progress)

Caprio, Gerard and Daniela Klingebiel (2000). “Episodes of Systemic and Borderline Banking Crises”. Managing the Real and Fiscal Effects of Banking Crises, Klingebiel Daniela and Luc Laeven. WB Discussion Paper No. 428. Washington, D.C.: WB

De la Torre, Augusto (2006). “Financial Safety Net: Components, Functions, Institutional Design”. Presented at Seminar on Financial Stability. Dalian, China

Kane and Demirguc-Kunt (2001): Deposit Insurance Around the Globe: Where Does it Work?, NBER Working paper Series, No. 8493

World Bank and IMF (2005). “Global Bank Insolvency Initiative: Legal, Institutional, and Regulatory Framework to Deal with Banking Resolution and Insolvency”

References