executive summary india solar market update q2...

TRANSCRIPT

Executive Summary India Solar Market Update – Q2 2017

www.mercomindia.com

India Solar Demand Forecast

• The Indian solar industry is witnessing its best year, with nearly

4.8 GW installed during first six months of 2017, more than all

of the solar installed in 2016.

• Cumulative installed solar capacity now stands at nearly 14.7

GW.

• Mercom forecasts nearly 10.5 GW of solar installations in

calendar year 2017, due to robust project development pipeline

slated to be commissioned by year end.

• Andhra Pradesh became the first Indian state to reach an

installed solar capacity of over 2 GW, closely followed by

Rajasthan with 1.9 GW.

• In Q2 2017, an all time low solar tariff of ₹2.44 (~$0.038) per

kWh was discovered at Bhadla Phase III solar auction in

Rajasthan.

• The lowest bid in solar reverse auctions declined by about 26

percent from Q1 to Q2 2017

• Solar now accounts for nearly 4.4 percent of total installed

electricity generation capacity, and provided nearly one percent

of the total power generated during FY2016-17.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Cu

mu

lati

ve In

stal

lati

on

s (M

W)

An

nu

al In

stal

lati

on

s (M

W)

Annual Rooftop Solar Installations (MW)

Annual Utility-scale Solar Installations (MW)

Cumulative Solar Installations (MW)

Source: Mercom India (Jun 2017)

India Solar Demand Forecast (MW)

www.mercomindia.com

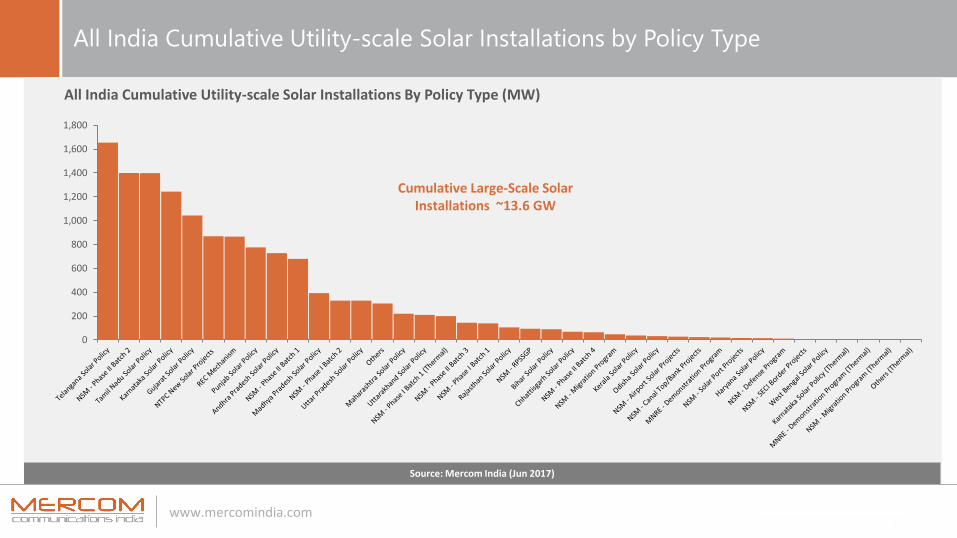

All India Cumulative Utility-scale Solar Installations by Policy Type

1,6

55

1,4

00

1,3

99

1,2

43

1,0

44

870

867

777

729

680

393

330

330

306

220

211

200

145

140

106

94 90 69 65 48 38 33 29 24 21 16 15 11 5 5 3 3 3 1

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

All India Cumulative Utility-scale Solar Installations By Policy Type (MW)

Cumulative Large-Scale Solar Installations ~13.6 GW

Source: Mercom Capital Group (Dec 2016)Source: Mercom India (Jun 2017)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

All India Cumulative Utility-scale Solar Installations By Policy Type (MW)

Cumulative Large-Scale Solar Installations ~13.6 GW

Source: Mercom Capital Group (Dec 2016)Source: Mercom India (Jun 2017)

www.mercomindia.com

Policy Updates

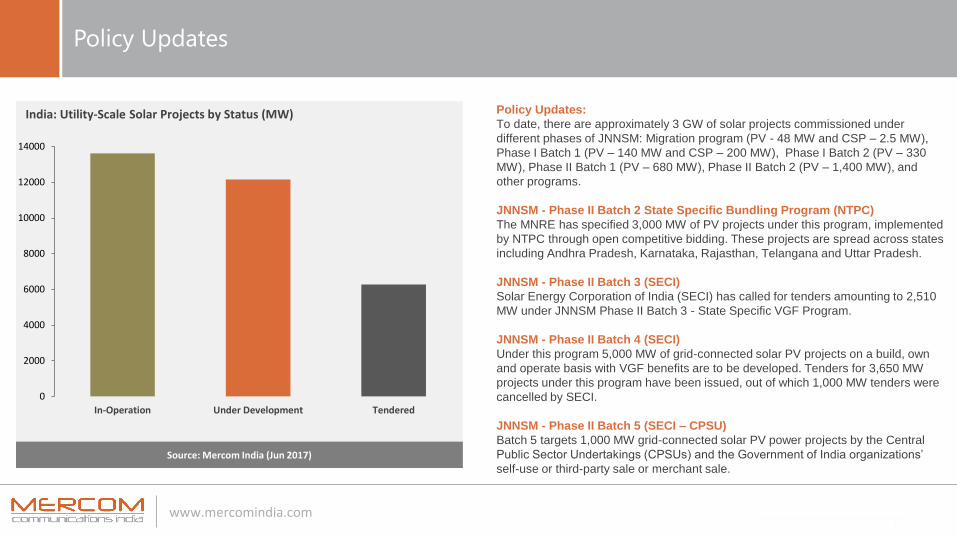

Policy Updates:

To date, there are approximately 3 GW of solar projects commissioned under

different phases of JNNSM: Migration program (PV - 48 MW and CSP – 2.5 MW),

Phase I Batch 1 (PV – 140 MW and CSP – 200 MW), Phase I Batch 2 (PV – 330

MW), Phase II Batch 1 (PV – 680 MW), Phase II Batch 2 (PV – 1,400 MW), and

other programs.

JNNSM - Phase II Batch 2 State Specific Bundling Program (NTPC)

The MNRE has specified 3,000 MW of PV projects under this program, implemented

by NTPC through open competitive bidding. These projects are spread across states

including Andhra Pradesh, Karnataka, Rajasthan, Telangana and Uttar Pradesh.

JNNSM - Phase II Batch 3 (SECI)

Solar Energy Corporation of India (SECI) has called for tenders amounting to 2,510

MW under JNNSM Phase II Batch 3 - State Specific VGF Program.

JNNSM - Phase II Batch 4 (SECI)

Under this program 5,000 MW of grid-connected solar PV projects on a build, own

and operate basis with VGF benefits are to be developed. Tenders for 3,650 MW

projects under this program have been issued, out of which 1,000 MW tenders were

cancelled by SECI.

JNNSM - Phase II Batch 5 (SECI – CPSU)

Batch 5 targets 1,000 MW grid-connected solar PV power projects by the Central

Public Sector Undertakings (CPSUs) and the Government of India organizations’

self-use or third-party sale or merchant sale.

0

2000

4000

6000

8000

10000

12000

14000

In-Operation Under Development Tendered

India: Utility-Scale Solar Projects by Status (MW)

Source: Mercom India (Jun 2017)

www.mercomindia.com

Solar Tenders and Auctions

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q3 2016 Q4 2016 Q1 2017 Q2 2017

India Solar Tenders and Auctions by Quarter (MW)

Tenders Auctions

Source: Mercom India

Q3’16 - Out of the total 555 MW, 300 MW tender was cancelled by SECI, due to recently discovered low bids in Rajasthan

Q1’17 - Of the total 1,856 MW, 1,000 MW is a re-tender by NTPC which was earlier tendered in 2016

www.mercomindia.com

Historical Average Module Spot Price Trends in China

• Chinese module prices in India fell by approximately 5% in the

second quarter of 2017.

• Price quotes for Chinese modules in India ranged from $0.28

(~₹18.03)/W to $0.34 (~₹21.9)/W based on size of the orders and

other parameters.

• According to our channel checks, price drop in Q3 could be less

than Q3 of last year as demand in China is a lot stronger due to Top

Runner, Poverty Alleviation programs and increased demand from

the U.S. in anticipation of antidumping ruling in the Suniva case.

• Currently, record-low bids in India are mostly driven by extremely

low Chinese module prices which have enabled developers to be

aggressive in reverse auctions in anticipation of falling Chinese

module prices.0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

0.65

Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17

Indian Modules ($/W)

Chinese Modules ($/W)

Chinese and Indian Module ASPs Q2 2017

Source: Mercom India (Q2 2017)

www.mercomindia.com

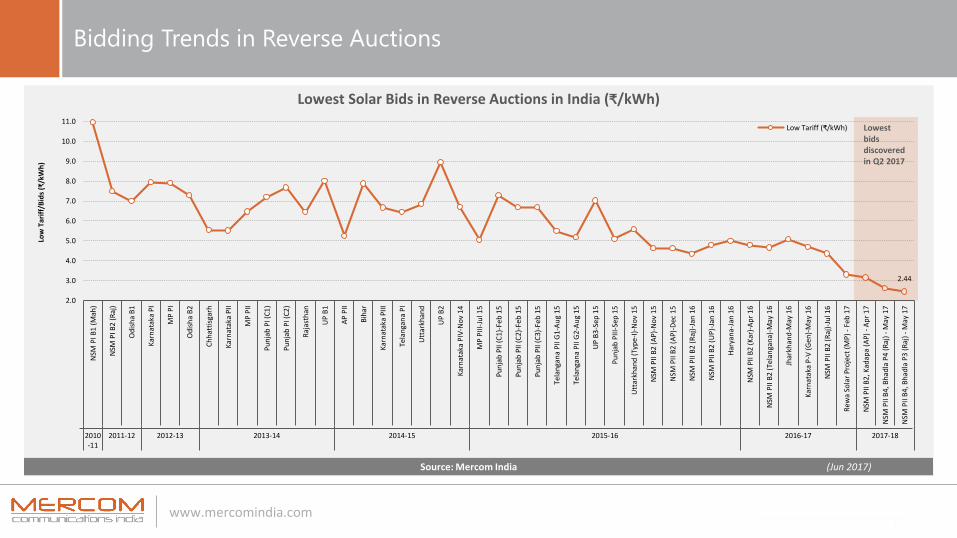

Bidding Trends in Reverse Auctions

2.44

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

NSM

PI B

1 (

Mah

)

NSM

PI B

2 (

Raj

)

Od

ish

a B

1

Kar

nat

aka

PI

MP

PI

Od

ish

a B

2

Ch

hat

tisg

arh

Kar

nat

aka

PII

MP

PII

Pu

nja

b P

I (C

1)

Pu

nja

b P

I (C

2)

Raj

asth

an

UP

B1

AP

PII

Bih

ar

Kar

nat

aka

PII

I

Tela

nga

na

PI

Utt

arkh

and

UP

B2

Kar

nat

aka

PIV

-No

v 14

MP

PII

I-Ju

l 15

Pu

nja

b P

II (

C1)

-Feb

15

Pu

nja

b P

II (

C2)

-Feb

15

Pu

nja

b P

II (

C3)

-Feb

15

Tela

nga

na

PII

G1-

Au

g 1

5

Tela

nga

na

PII

G2-

Au

g 1

5

UP

B3

-Sep

15

Pu

nja

b P

III-

Sep

15

Utt

arkh

and

(Ty

pe-

I)-N

ov

15

NSM

PII

B2

(AP

)-N

ov

15

NSM

PII

B2

(AP

)-D

ec 1

5

NSM

PII

B2

(Raj

)-Ja

n 1

6

NSM

PII

B2

(UP

)-Ja

n 1

6

Har

yan

a-Ja

n 1

6

NSM

PII

B2

(Kar

)-A

pr

16

NSM

PII

B2

(Tel

anga

na)

-May

16

Jhar

khan

d-M

ay 1

6

Kar

nat

aka

P-V

(G

en)-

May

16

NSM

PII

B2

(Raj

)-Ju

l 16

Rew

a So

lar

Pro

ject

(M

P)

- Fe

b 1

7

NSM

PII

B2,

Kad

apa

(AP)

- A

pr

17

NSM

PII

B4,

Bh

adla

P4

(R

aj)

- M

ay 1

7

NSM

PII

B4,

Bh

adla

P3

(R

aj)

- M

ay 1

7

2010-11

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

Low

Tar

iff/

Bid

s (₹

/kW

h)

Low Tariff (₹/kWh) Lowest bids discovered in Q2 2017

Source: Mercom India (Jun 2017)

Lowest Solar Bids in Reverse Auctions in India (₹/kWh)

www.mercomindia.com

Market Leaders

Source: Mercom India (Jun 2017)

Top 5 Indian Solar Module

Manufacturers

ADANI

VIKRAM SOLAR

EMMVEE

WAAREE ENERGIES

TATA POWER

1

2

3

3

4

Source: Mercom India (Jun 2017)

Top 5 Solar EPC

Players

STERLING & WILSON

MAHINDRA SUSTEN

L&T SOLAR

HARTEK SOLAR

VIKRAM SOLAR

1

2

3

4

5

Our quarterly report includes market share information for:

• Top Utility-scale Project Developers with Installed Capacity (MW)

• Top Utility-scale Project Developers with Under-development Pipeline (MW)

• Top Solar Inverter Suppliers in India (Cumulative Shipments in MW)

• Top Solar Rooftop Developers and EPC Companies in India (MW)

• Top Solar Module Manufacturers in India

• Top Solar Cell Manufacturers in India

• Top Utility-scale EPC Players with Commissioned Capacity (MW)

• Top Utility-scale Third Party EPC Players with Commissioned Capacity (MW)

• Top Solar Module Suppliers in India (Cumulative Shipments in MW)

www.mercomindia.com

State Policies

Updates: The Uttar Pradesh New and

Renewable Energy Development Agency

(UPNEDA) has issued the ‘Draft Solar Power

Policy-2017’ for Uttar Pradesh. The

Government of Uttar Pradesh has set a target

of 10,700 MW for solar power, including 4,300

MW from rooftop solar projects, by FY 2022.

Updates: TANGEDCO has proposed

adopting a revised accounting methodology to

cut back on tariffs for the existing net-

metering program in the state. TANGEDCO

has cited various reasons for the cut,

including recent record low tariffs and losses

incurred in wheeling and banking of wind

energy.

Updates: In Q2 2017, Bihar came up with a

new renewable energy policy with an aim to

harness 3,433 MW of clean energy over the

next five years. The policy specifically aims at

development of 2,969 MW for solar, 244 MW

for biomass and bagasse cogeneration and

220 MW for small hydro power by 2022. The

policy also targets installation of 1,000 MW

rooftop solar using both net-metering and

gross metering mechanisms.

Updates: The state government of Gujarat

has removed the capacity restriction of 50

percent of the approved load or contracted

demand by small residential rooftop owners.

Now, residential consumers can install rooftop

solar systems of capacity of their choice,

irrespective of the approved or contracted

load.

Uttar Pradesh

Tamil Nadu

Bihar

Gujarat

Complete state by state updates are covered in our full report

Top Seven states which now have over 1 GW of installed solar capacity represent approximately 82 percent of the total installed capacity

1

Total Installations - 2,130 MW Total Installations - 1,921 MW Total Installations - 1,867 MW Total Installations - 1,608 MW Total Installations - 1,271 MW

Total Installations - 1,171 MW Total Installations - 1,165 MW Total Installations - 792 MW Total Installations - 551 MW Total Installations - 479 MW

Top 10 Solar States in IndiaState Ranking Based on Total Installed Utility-scale Solar as of Jun 2017

Andhra Pradesh Rajasthan Telangana

Data from Mercom's India Solar Project Tracker

Karnataka

Gujarat Madhya Pradeh Punjab Maharashtra Uttar Pradesh

Tamil Nadu1 2 3 4 5

6 7 8 9

13.6 GWCumulat ive Solar Capacity

1.6 GWSolar Installat ions Q2 2017

www.mercomindia.com

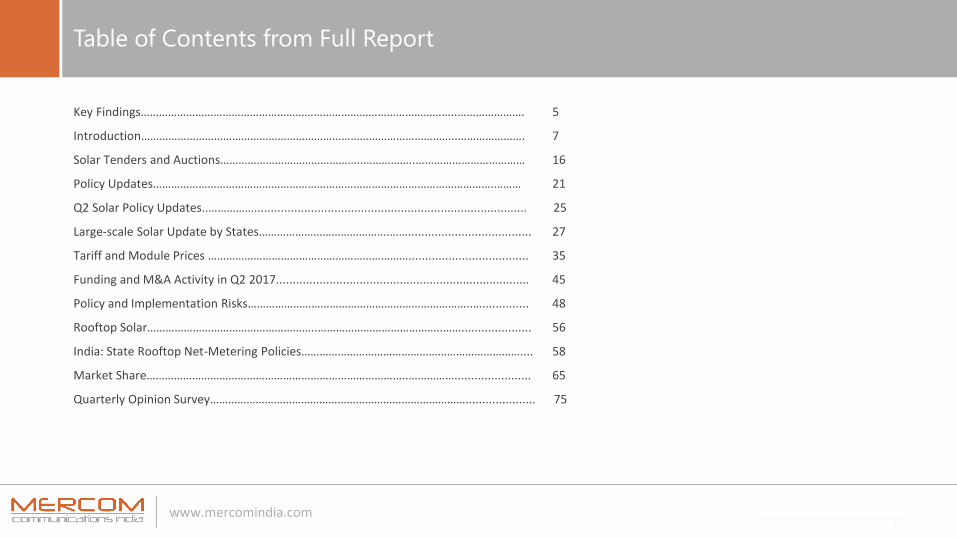

Table of Contents from Full Report

Key Findings…………………………………………………………………………………………..…………………. 5

Introduction…………………………………………………………………………………………..…………………. 7

Solar Tenders and Auctions………………………………………..……………..……………………………… 16

Policy Updates………………………………………………………………………………………………….……… 21

Q2 Solar Policy Updates..…………….................................................................................. 25

Large-scale Solar Update by States…………………………………….……..................................... 27

Tariff and Module Prices ………………………………………………………….................................... 35

Funding and M&A Activity in Q2 2017............................................................................ 45

Policy and Implementation Risks………………………………………………………………..….............. 48

Rooftop Solar………………………………………………..…………………………………..……..................... 56

India: State Rooftop Net-Metering Policies……………………………………………………………….... 58

Market Share…………………………………………………………………………..……………....................... 65

Quarterly Opinion Survey…………………………………………………………………………..................... 75

www.mercomindia.com

List of Charts/Tables from Full Report

India Solar Demand Forecast (MW)……………………….………………………………..…………..…….. 7Installation and Forecast by Market Segment (MW)……………………..…………………..………. 8Solar Installations in 2017 by Quarter (MW) ..……………………………………...……………..……. 9Quarterly Utility-scale Solar Installations in India (MW) ..………………………..………..………. 10Share of New Power Generating Capacity Additions in India ..……………..….………..………. 10All India Cumulative Utility-scale Solar Installations by Policy Type (MW)……..……….…… 11India Utility-scale Solar Project Pipeline (MW) ………………………………............................... 11All India Cumulative Large-Scale Solar Installations By Policy Type................................. 12India Utility-scale Solar Project Pipeline by Policy (MW) …………………............................. 13State-wise Utility-scale Solar Installations in Q2 2017 (MW) ……………….......................... 14India Utility-scale Cumulative Solar Installations by States (MW) …………........................ 15Solar Project Development Pipeline by State (MW)………………………………………………........ 16State-Wise Solar Project Development Pipeline………..………………………………………........... 17India Solar Tenders and Auctions by Quarter (MW) …..................................................... 18Solar Auctions in Q2 2017 ………........................................................................................ 19New Solar Tenders Announced in Q2 2017…………………………………………..…...................... 20Utility-scale Solar Projects by Status (MW)………………………………….……..……..................... 21Status of Projects Under JNNSM Phase-II, Batch-5, CPSU Program………………................ 23Targets for Solar Projects to be Developed by the Ministry of Defense…………………....... 2350 MW Solar Projects Under Canal Top Program…………………..………….………................... 2450 MW Solar Projects Under Canal Bank Program……………………………….……………………… 24Chinese and Indian Module ASPs Q2 2017………………………………….................................... 35Average Solar Project Cost per MW…………………………..……….………………………….....…….….. 37Breakdown of Solar Project Cost per MW in India (₹ Lakh) Q2 2017....……………………..….. 37

Lowest Solar Bids in Reverse Auctions in India (₹/kWh)………………..………………….…….….. 38Indian Solar PV Imports and Exports………………………..………………….…….……………………..…. 40Country-wise Breakdown of Indian Solar Imports (%) FY2016-17……………………….…….…. 41Country-wise Breakdown of Indian Solar Exports (%) FY2016-17…………………………….…. 41India: Solar Electricity Generation (MU)………………..………………………………………………….…. 42Electricity Generation by Source in FY2016-17………………………………………….……………….…. 43India: Installed Power Capacity Mix (%)…………………………………………………..…..………….…. 43India Solar Funding and M&A Transactions (1H 2016 – 1H 2017)……………….…………….…. 45Comparison of Solar Park Charges Across Various Indian States……………………………….…. 48Detailed Analysis of Solar Park Fees in India….……………………………..………………………….…. 50Fifth Integrated Rating for State DISCOMs: Utility-wise Grades………………………………..…. 53India: Solar Cell and PV Module Manufacturing Capacity as of June 2017 (MW)..…….…. 55Amendment in Tariff for SECI 500 MW Phase-I Rooftop Tender……………….……………...…. 56Rooftop Net-Metering Policies by States and UTs………………............................................ 60Top 10 Utility-scale Project Developers with Installed Capacity (MW)……………………….…. 65Top 10 Utility-scale Project Developers with Under-development Pipeline (MW)…….…. 66Top 10 Solar Inverter Suppliers in India (Cumulative Shipments in MW)………..………….… 67Top 10 Solar Rooftop Developers and EPC Companies in India (MW)……………………….…. 68Top 10 Solar Module Manufacturers in India…………………………………………………………….…. 69Top 10 Solar Cell Manufacturers in India…………………………………..………………………..…….…. 70Top 10 Utility-scale EPC Players with Commissioned Capacity (MW)……..………………….…. 71Top 10 Utility-scale Third Party EPC Players with Commissioned Capacity (MW)……….…. 72Top 10 Solar Module Suppliers in India (Cumulative Shipments in MW)…………………….…. 73Capacity of Solar Projects Financed by Different Banks/FIs (MW)……….…………………….…. 74

www.mercomindia.com

Disclaimer/Copyright

- 13 -

© 2017 by Mercom Capital Group, llc. All rights reserved.

Ownership Rights: This report is owned by Mercom Capital Group, llc. (Mercom) and is protected by United States copyright and trademark laws and

international copyright/intellectual property laws under applicable treaties and/or conventions.

Grant of License Rights: Mercom hereby grants user a non-exclusive, non-refundable, non-transferable license to use the report or its data for research

purposes only. Mercom retains exclusive and sole ownership of the report and its data disseminated under this license agreement. User agrees not to

permit any unauthorized use, reproduction, distribution, publication or electronic transmission of any report or the information/data therein without the

express written permission of Mercom. By purchasing this report, user is prohibited from distributing the report or the data to anyone person or entity not

covered by the license agreement.

Disclaimer of Warranty and Liability: Disclaimer of Warranty and Liability: Mercom has used best efforts in collecting and preparing each report and

compiling data. Mercom owners, their employees, affiliates, agents, subsidiaries and licensors do not warrant the accuracy, completeness, correctness,

non-infringement, merchantability, or fitness for a particular purpose of reports or data. Owners, their employees, affiliates, agents, subsidiaries, or licensors

shall not be liable to User or any third party for losses or injury caused in whole or part by our negligence or contingencies beyond Mercom’s control in

compiling, preparing or disseminating Reports or Data or for any decision made or action taken by User or any third party in reliance on such information or

for any consequential, special, indirect or similar damages, even if one or more employee, owner, affiliate, agent, subsidiary, and licensor at Mercom were

advised of the possibility of the same. User agrees that the liability of Mercom, their employees, affiliates, agents, subsidiaries and licensors, if any, arising

out of any kind of legal claim (whether in contract, tort or otherwise) in connection with its goods/services under this license and sale shall not exceed the

amount User paid to Mercom for use of its reports and data. A copy of the full Terms and Conditions that you agreed to can be found at:

http://mercomcapital.com/termsandconditions.php.

www.mercomindia.com

Pricing Information

Mercom Communications India, Pvt. Ltd.S-3, Harshita Arcade No.138, First Main Road SheshadripuramBangalore- 560020t | +91.80.23560436

USA:Mercom Capital Group, llc4611 Bee Caves Road, Suite 303Austin, Texas 78746t | +1.512.215.4452

w | www.mercomindia.come | [email protected]

Purchase your copy of the report here!

Full Quarterly Report: $1,499

Annual Subscription: $3,499

Full Quarterly Report – Mercom Clients: $999

Annual Subscription – Mercom Clients: $2,499

- all reports come with an Enterprise License.