exemption to educational institutions

TRANSCRIPT

―EXEMPTION TO EDUCATIONAL INSTITUTIONS‖

BY GSTCORNOR®

CONTACT US

Website :- www.gstcornor.com

Email Id :- [email protected]/ [email protected]

We are Socially Active (Follow us #gstcornor)

!! Twitter !! LinkedIn !! Quora !! Facebook !! Instagram !!

JOIN GSTCORNOR E-SUBSCRIPTION PACKAGE

(Click Here)

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

2 | P a g e w w w . G S T C O R N O R . c o m

Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 is as below:

Heading Description of Service GST Effective

Date

Heading

9992 or

Heading

9963**

(Entry

No.66)

Services provided –

a) By an educational institution to its students, faculty

and staff;

b) To an educational institution, by way of,-

i. Transportation of students, faculty and staff;

ii. Catering, including any mid-day meals scheme

sponsored by the Central Government, State Government or Union territory;

iii. Security or cleaning or house-keeping services performed in such educational institution;

iv. Services relating to admission to, or conduct of examination by, such institution; upto higher

secondary

Provided that nothing contained in entry (b) shall apply to

an educational institution other than an institution providing services by way of pre-school education and

education up to higher secondary school or equivalent.

Nil 01.07.2017

Heading

9992

(Entry

No.67)

Services provided by the Indian Institutes of Management, as per the guidelines of the Central Government, to their

students, by way of the following educational programmes, except Executive Development Programme: -

(a) two year full time Post Graduate Programmes in Management for the Post Graduate Diploma in

Management, to which admissions are made on the basis of Common Admission Test (CAT) conducted by the Indian

Institute of Management;

(b) fellow programme in Management;

(c) five year integrated programme in Management.

Nil 01.07.2017

** Notification No. 28/2018-Central Tax (Rate) dated 31.12.2018

Series of Amendment in Exemptions to Educational institutions

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

3 | P a g e w w w . G S T C O R N O R . c o m

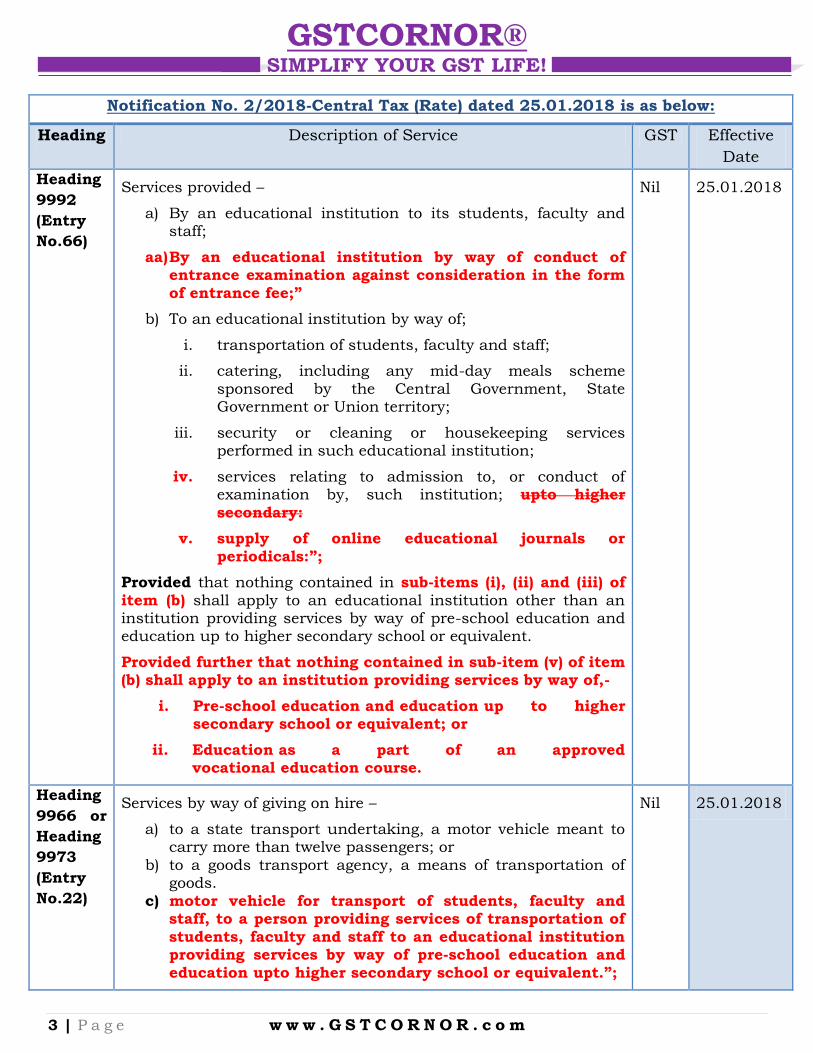

Notification No. 2/2018-Central Tax (Rate) dated 25.01.2018 is as below:

Heading Description of Service GST Effective

Date

Heading

9992

(Entry

No.66)

Services provided –

a) By an educational institution to its students, faculty and staff;

aa) By an educational institution by way of conduct of entrance examination against consideration in the form

of entrance fee;‖

b) To an educational institution by way of;

i. transportation of students, faculty and staff;

ii. catering, including any mid-day meals scheme

sponsored by the Central Government, State Government or Union territory;

iii. security or cleaning or housekeeping services performed in such educational institution;

iv. services relating to admission to, or conduct of examination by, such institution; upto higher

secondary:

v. supply of online educational journals or

periodicals:‖;

Provided that nothing contained in sub-items (i), (ii) and (iii) of

item (b) shall apply to an educational institution other than an institution providing services by way of pre-school education and education up to higher secondary school or equivalent.

Provided further that nothing contained in sub-item (v) of item (b) shall apply to an institution providing services by way of,-

i. Pre-school education and education up to higher secondary school or equivalent; or

ii. Education as a part of an approved vocational education course.

Nil 25.01.2018

Heading

9966 or

Heading

9973

(Entry

No.22)

Services by way of giving on hire –

a) to a state transport undertaking, a motor vehicle meant to carry more than twelve passengers; or

b) to a goods transport agency, a means of transportation of goods.

c) motor vehicle for transport of students, faculty and staff, to a person providing services of transportation of

students, faculty and staff to an educational institution providing services by way of pre-school education and

education upto higher secondary school or equivalent.‖;

Nil 25.01.2018

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

4 | P a g e w w w . G S T C O R N O R . c o m

Notification No. 28/2018-Central Tax (Rate) dated 31.12.2018 is as below:

Heading Description of Service GST Effective

Date

Heading

9992

(Entry

No.67)

Services provided by the Indian Institutes of

Management, as per the guidelines of the Central Government, to their students, by way of the following

educational programmes, except Executive Development Programme: -

(a) two year full time Post Graduate Programmes in Management for the Post Graduate Diploma in

Management, to which admissions are made on the basis of Common Admission Test (CAT) conducted by

the Indian Institute of Management;

(b) fellow programme in Management;

(c) five year integrated programme in Management.

Nil 01.01.2019

Clarifications regarding Exemption to IIM’s

Circular No. 82/01/2019 – GST ( F. No. 354/428/2018 )

With effect from 31st January, 2018, all the IIMs are “educational institutions” as defined under notification No. 12/ 2017- Central Tax (Rate) dated 28.06.2017 as they provide education as a part of a curriculum for obtaining a qualification recognized by law for the time being in force.

For the period from 1st July, 2017 to 30th January, 2018, IIMs were not covered by the definition of educational institutions as given in notification No. 12/ 2017 Central Tax (Rate) dated 28.06.2017. Thus, they were not entitled to exemption under Sl. No. 66 of the said notification. However, there was specific exemption to following three programs of IIMs under Sl. No. 67 of notification No. 12/2017- Central Tax (Rate):

a. two year full time Post Graduate Programmes in Management for the Post Graduate

Diploma in Management, to which admissions are made on the basis of Common Admission Test (CAT) conducted by the Indian Institute of Management;

b. fellow programme in Management;

c. Five year integrated programme in Management.

Therefore, for the period from 1st July, 2017 to 30th January, 2018, GST exemption would be available only to three long duration programs specified above.

It is further, clarified that with effect from 31st January, 2018, all IIMs have become eligible for exemption benefit under Sl. No. 66 of notification No. 12/ 2017- Central Tax (Rate) dated 28.06.2017. As such, specific exemption granted to IIMs vide Sl. No. 67 has become redundant. The same has been deleted vide notification No. 28/2018- Central Tax (Rate) dated, 31st December, 2018 w.e.f. 1st January 2019

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

5 | P a g e w w w . G S T C O R N O R . c o m

Following summary table may be referred to while determining eligibility of various programs conducted by Indian Institutes of Managements for exemption from GST.

Sl. No

Periods Programmes offered by IIMs Whether Exempt from GST or not

1 1st July, 2017 to 30th January, 2018

i. two-year full time Post Graduate Programmes in Management for the Post Graduate Diploma in Management, to which admissions are made on the basis of Common Admission Test (CAT) conducted by the Indian Institute of Management,

ii. fellow programme in Management, iii. Five years integrated programme in

Management.

Exempt

i. One- year Post Graduate Programs for Executives,

ii. Any programs other than those mentioned at Sl. No. 67 of notification No. 12/2017- Central Tax (Rate), dated 28.06.2017.

iii. All short duration executive development programs or need based specially designed programs (less than one year).

Not exempt from GST

2 31st January, 2018 onwards**

All long duration programs (one year or more) conferring degree/ diploma as recommended by Board of Governors as per the power vested in them under the IIM Act, 2017 including one- year Post Graduate Programs for Executives.

Exempt

All short duration executive development programs or need based specially designed programs (less than one year) which are not a qualification recognized by law.

Not exempt from GST

** For the period from 31st January, 2018 to 31st December, 2018, two exemptions, i.e. under Sl. No. 66 and under Sl. No. 67 of notification No. 12/ 2017- Central Tax (Rate), dated 28.06.2017 are available to the IIMs. The legal position in such situation has been clarified by Hon’ble Supreme Court in many cases that if there are two or more exemption notifications available to an assessee, the assesse can claim the one that is more beneficial to him. Therefore, from 31st January, 2018 to 31st December, 2018, IIMs can avail exemption either under Sl. No 66 or Sl. No. 67 of the said notification for the eligible programme

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

6 | P a g e w w w . G S T C O R N O R . c o m

Heading Description of Service GST

Heading

9992 or

Heading

9963

(Entry

No.66)

Services provided –

a) By an educational institution to its students, faculty and staff;

(aa) By an educational institution by way of conduct of entrance examination

against consideration in the form of entrance fee;

b) To an educational institution, by way of,-

i. Transportation of students, faculty and staff;

ii. Catering, including any mid-day meals scheme sponsored by the

Central Government, State Government or Union territory;

iii. Security or cleaning or house-keeping services performed in

such educational institution;

iv. Services relating to admission to, or conduct of examination by,

such institution;

v. Supply of online educational journals or periodicals:

Provided that nothing contained in sub-items (i), (ii) and (iii) of item (b) shall apply to an educational institution other than an institution

providing services by way of pre-school education and education up to higher secondary school or equivalent.

Provided further that nothing contained in sub-item (v) of item (b) shall apply to an institution providing services by way of,-

i. Pre-school education and education up to higher secondary school or equivalent; or

ii. Education as a part of an approved vocational education course.

Nil

As per Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017,

Clause 2(y):- Educational Institution means an institution providing services by way of:

1. Pre-school education and education up to higher secondary school or equivalent;

2. Education as a part of a curriculum for obtaining a qualification recognized by any law for the time being in force;

3. Education as a part of an approved vocational education course

Clause 2(h):- An “approved vocational education course” means, –

i. A course run by an industrial training institute or an industrial training centre affiliated to the National Council for Vocational Training or State Council for Vocational Training offering courses in designated trades notified under the Apprentices Act, 1961 (52 of 1961); or

ii. A Modular Employable Skill Course, approved by the National Council of Vocational Training, run by a person registered with the Directorate General of Training, Ministry of Skill Development and Entrepreneurship.

Present Scenario for Exemptions to Educational institutions

Definitions

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

7 | P a g e w w w . G S T C O R N O R . c o m

POINTS TO BE NOTED

It is important to understand that ―education as a part of curriculum‖ is only exempt in this list. Services provided by way of education as a part of a prescribed curriculum for

obtaining a qualification recognized by a law of a foreign country are also not exempted because the course / degree not recognized by Indian Law.

Training given by private coaching institutes or other unrecognized institution or self-styled educational institution would not be exempted as such training does not lead to grant of a

recognized qualification since private institute does not have any specific curriculum.

Services provided by an Educational Institution are exempt from GST, but, when services

are supplied to an Educational Institution, exemption is restricted only for specified services (transportation of student‟s faculty staff, catering, security, cleaning ) and that to

only for pre-school and higher secondary.

Education services (such as transportation of students faculty staff, catering, security,

cleaning ) entry no 66 of Notification No. 12/2017 dated 28.06.2017, if provided to educational institutions providing degree or higher education, the same would not be

exempt from GST.

For removal of doubts, it is clarified that the Central and State Educational Boards shall be

treated as Educational Institution for the limited purpose of providing services by way of conduct of examination to the students.

There are some instances which don’t fall in the above exemption list as:

Advertisement Services provided to educational institutions

Placement services for students provided to educational institutions

Summer Camp for Other School Students

Educational Institutions rents premises for organizing any function

Campus Interview

Clarifications regarding GST on College Hostel Mess Fees

Circular No.28/02/2018-GST [F.NO.354/03/2018], dated 8-1-2018, as corrected by

Corrigendum to circular No.28/02/2018-GST, has clarified as under:

The educational institutions have mess facility for providing food to their students and staff.

Such facility is either run by the institution/ students themselves or is outsourced to a third person. Supply of food or drink provided by a mess or canteen is taxable at 5% without

Input Tax Credit [Serial No. 7(i) of notification No. 11/2017-CT (Rate) as amended vide notification No. 46/2017-CT (Rate) dated 14.11.2017 refers]. It is immaterial whether the

service is provided by the educational institution itself or the institution outsources the activity to an outside contractor.

If the catering services is one of the services provided by an educational institution to its

students, faculty and staff and the said educational institution is covered by the definition given under Para 2(y) of notification No. 12/2017- Central Tax (Rate), then the same is

exempt. [Sl. No. 66(a) of Notification No. 12/2017-Central Tax (Rate) refers]

If the catering services, i.e., supply of food or drink in a mess or canteen, is provided by

anyone other than the educational institution, then it is a supply of service at entry 7(i) of notification No. 11/2017-CT to the concerned educational institution and attracts GST of

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

8 | P a g e w w w . G S T C O R N O R . c o m

5% provided that credit of input tax charged on goods and services used in supplying the

service has not been taken, effective from 15.11.2017.

Hostel Services provided to students

In the press release dated 13-7-2017, the Board has clarified that Services of lodging/boarding in hostels provided by such educational institutions which are providing

pre-school education and education up to higher secondary school or equivalent or education leading to a qualification recognized by law, are fully exempt from GST. Annual

subscription/fees charged as lodging/boarding charges by such educational institutions from its students for hostel accommodation shall not attract GST.

I. GST ADVANCE RULING ON ―IIM COURSES‖

Applicant IIM, BANGALORE

Ruling Sought On

The applicant offers Executive Development Programme as:

Post Graduate Programme in Public Policy and Management

Post Graduate Programme in Enterprise Management

Post Graduate Programme in Management

The courses offered above by the applicant that if above course are not covered

under entry no. 67 of the said notification; are covered under entry no. 66 of the said notification and are also exempt.

AAR Decision AAR held that both Serial no. 66 and 67 are related to all educational services covered under the same Heading 9992. It is held that Serial Number 67 has been carved out specifically and only for the educational services provided

by the IIM.

In other words the IIM have been segregated from all other educational institutes

and the educational services provided by them are subject to different treatment in terms of exemptions. Therefore in so far as educational services provided by

IIM are concerned, the provisions contained in Serial no. 67 only shall apply not Serial no 66. Hence the courses offered in the Para 2 are taxable i.e. any supply

made by/to IIMB under Serial No.66 are also taxable.

Favorable/ Unfavorable

Unfavorable

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

9 | P a g e w w w . G S T C O R N O R . c o m

II. GST ADVANCE RULING ON ―PRINTING QUESTION PAPERS‖

Applicant Ashok Kumar

Ruling Sought On

The Applicant is stated supplier of printed question papers for various examinations conducted by the Government/Government aided Educational

Boards/ Councils/ Universities etc

The Councils/Boards/Universities/ Institutions are supplying the matter to be printed to the Applicant, who is providing the paper, ink, other inputs,

manpower, machinery, etc to print the given matter in appropriate question paper format as provided by the Councils/Boards/Universities/Institutions

supplying the matter.

How should the service of printing question papers for educational institutions be classified???

AAR Decision It is necessary to determine whether the Question Papers supplied by the Applicant are “goods” or “services”.

Section 9 of the GST Tariff-Services deals with Community, Social and Personal

Services and other miscellaneous services which include Education Services (covering services related to admission to or conduct of examination by

Educational Institutions) under Heading 9992. Since the Applicant has specified the printing of question papers for Educational Institutions,

supply of service under Section 9 of the GST Tariff is found to be appropriate.

Serial No. 66(b)(iv) of Notification No. 12/2017 dated 28/06/2017, as amended

from time to time, as applicable, wholly exempts services provided to an Educational Institution relating to conduct of examination. The phrase „relating

to‟ expands the scope of this entry to include such support services without which conduct of the examination is not possible.

Question papers can have no use other than in conducting a specific

examination, and the supply of service of printing such question papers is a supply related to conduct of that examination.

Explanation (iv) to Notification No. 12/2017 dated 28/06/2017, inserted vide

Notification No. 14/2018 dated 26/07/2018, clarifies that the Central and State Educational Boards shall be treated as Educational Institution for the limited

purpose of services by way of conducting examinations. Serial No. 66(b)(iv) above, therefore, includes services provided to such Boards relating to the

conduct of examinations.

The Applicant is, therefore, not liable to pay tax on the service of printing

question papers provided to the Educational Boards/ Councils/ Universities/ Institutions relating to the conduct of examination

Favorable/ Unfavorable

Favorable

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

10 | P a g e w w w . G S T C O R N O R . c o m

III. GST ADVANCE RULING ON ―ACTIVITY OF COLLECTING EXAM FEES‖

Applicant Arivu Educational Consultants Pvt. ltd

Ruling Sought On

The Applicant is engaged in the providing coaching, learning and training services in relation to undergraduate, graduate and post graduate degree,

diploma and professional courses on standalone bases to students or for any institution, corporate, company, institutes, universities and colleges in the subject and branches of all types of disciplines.

In this process, the applicant collects certain amount as exam fee from the students and remits the same to the respective institute or college or

universities without any profit element. This payment is separately indicated in the invoice issued to the respective students.

Does the activity of collecting exam fee (charged by any university or

institution) from the students and remitting to that particular university or institution without any value addition to it, amount to taxable services???

AAR Decision The applicant is educational consultant and a professional in the field of education. It doesn’t satisfy the definition of educational institution as defined in Para 2(y) of the Notification No. 12/2017 dated 28.06.2017.

The applicant collects fee for coaching or training classes they conduct from the students which attracts 18% GST. Apart from this the applicant also collects

certain amount as exam fee from the students and remits the same to the respective intuition without any addition to it.

The applicant is collecting the exact amount payable to the institute or college or

universities exam fee from the students (Service recipient) and remits the same amount to the respective institute (third party) without any profit element or

additions, on authorization of students. This payment is separately indicated in invoice. The applicant providing this kind of services to the students in addition

to the services as training and coaching institute

Hence, the applicant satisfies all the conditions of the pure agent as narrated in the Rule 33 of the CGST Rules, 2017. Therefore amount of fee

collected by the applicant from the student as exam fee which is remitted to the respective institute or college is excluded from the value of supply.

Favorable/ Unfavorable

Unfavorable

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

11 | P a g e w w w . G S T C O R N O R . c o m

IV. GST ADVANCE RULING ON ―AFFILIATION TO SEPECIFIED UNIVERSITES‖

Applicant Emerge Vocational Skills Pvt. Ltd

Ruling Sought On

The Applicant is engaged in providing specified educational services in the field of Hotel Management.

Whether the services provided by the applicant in affiliation to specified universities and providing degree courses to students under related curriculums are exempt from GST vide entry no. 66 of the Notification No.

12/ 2017 – Central Tax dated 28.06.2017???

AAR Decision The applicant has submitted that he proposes to obtain an affiliation with a University in the State of Karnataka and shall thereafter be engaged in provision

of education in affiliation with the said university in the State of Karnataka.

The applicant also undertakes that the courses would be conducted as per the

curriculum of the university concerned in affiliation with them and the examination would be conducted by the University and degrees shall be granted

to the successful candidates of the institution.

As per the contention of the applicant, he is getting the institution affiliated to a

University in the State of Karnataka and is also proposing to impart education as a part of a curriculum provided by the University and the examination would

be conducted by the University and qualifications which are recognized by law would be issued to the successful candidates. Hence the institution would

qualify as an ―educational institution‖ for the purposes of such courses only which lead to a qualification recognized by any law for the time being

in force.

Favorable/ Unfavorable

Favorable

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

12 | P a g e w w w . G S T C O R N O R . c o m

V. GST ADVANCE RULING ON ―ONLIBE EDUCATIONAL JOURNALS‖

Applicant Informatics Publishing limited

Ruling Sought On

The Applicant states that they are a company engaged in the supply of online journals. They import various online journals from the foreign suppliers and

supply them mainly to the educational institutions.

The applicant states that as per the Notification No. 2/2018- Central Tax (Rate) dated 25.02.2018, supply of online journals and periodicals to the educational

institutions is not liable for GST. Generally, as per Section 17(1), 17(2) read with Rule 42 of the CGST Act, ITC attributable to exempt supply is not available.

Whether the input tax credit is available when the online educational journals and periodicals are supplied to the Educational Institutions other

than to preschool and higher secondary school or equivalent, which is exempt by virtue of Notification No. 2/2018 – Central Tax (Rate) dated

25.01.2018???

AAR Decision Notification No. 2/2018- Central tax (Rate) dated 25.01.2018, has been issued under Section 11 of the Act and as per the notification, the exemption is subject

to the condition that the supply of online journal and periodicals to an educational institution other than pre-school and higher secondary educational

institution is exempt from GST. It means the exemption is not “wholly” exempt under Section 11.

It is a conditional exemption. The conditions attached to the notification are as under:

a) The supply should be to an educational institution b) Supply should be only online educational journal or periodicals c) Educational Institution excludes

primary and higher secondary educational institutions

The applicant is only providing access to the articles published in various

journals and papers to its subscribers. It itself is not publishing any online journal, but only maintaining a database of links to all the journals

The transaction of the applicant is covered under the Heading 9984 Telecommunications, broadcasting and information supply services under

the Group 99843 and SAC of 998631,

Favorable/

Unfavorable

Unfavorable

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

13 | P a g e w w w . G S T C O R N O R . c o m

VI. GST ADVANCE RULING ON ―ENTRY 66 ANALYSIS‖

Applicant Emrald Heights International School

Ruling Sought On

The School is an Educational Institution and inter-alia, engaged in the providing world class education to its student‟s upto Higher Secondary only. Amongst

various organizations the „school is also member school of an association namely “Round Square”.

The Applicant and the Association intend to enter into an agreement (Proposed agreement) for hosting and managing the conference/gathering. The Proposed

agreement clearly mentions that the school shall act as Host of the Conference in its own right as Principal and shall not be deemed to be acting as an Agent of the

Association.

As per the Proposed agreement, the applicant is responsible to hold the

conference engaging appropriately skilled, trained and experienced personnel and sufficient financial and material resources. This shall include planning the

conference, inviting the participants, arranging the accommodation, food etc., organizing and managing the events in the „conference etc.

Will the consideration received by the school from the participant school(s) for participation of their students and staff in the conference would be exempted under entry No. 66 or entry No. 1 or entry No. 80 or any other

entry of the Notification No.12/2017 — Central Tax (Rate) or will be chargeable to GST under CGST Act, 2017 & MP’ GST Act, 2017 or IGST Act,

2017?

If not exempted then what would be the appropriate category of the service

and the appropriate Tax Rate?

What would be the Place of Supply for such services?

Whether exemption provided to service providers of catering, security, cleaning, house-keeping, transportation etc. to an educational institution

upto higher secondary be available to the Service Providers of the Applicant for services related to such conference.

Whether ITC would be eligible of all the input services availed for the purpose of the above conference?

AAR Decision Mier going through the provisions of Act/Rules/notification it is clear that

Supply of all services to an Educational Institution are not exempt. Only the specified services are exempt.

Similarly, supply of services pertaining to transportation of students, faculty and staff is exempt only because of eligibility of an Educational Institution for

exemption for educational services for pre-school education and education up to higher secondary „School or equivalent.

Supply of such services to an Educational Institution for any other purpose, say for education beyond higher secondary level, shall not be exempt.

GSTCORNOR® SIMPLIFY YOUR GST LIFE!

14 | P a g e w w w . G S T C O R N O R . c o m

Clause (a) of Entry 80 is not applicable to the proposed activities to be carried on

by the applicant, as the said clause is applicable to services by way of training or coaching in recreational activities relating to arts or culture.

The activities of holding educational conference / gathering of students. Faculty and staff of other Schools, cannot be said to be training or coaching in

recreational activities relating to arts or culture.

Clause (b) of Entry 80 is also not applicable, as the said clause is applicable to

services by way of training or coaching in recreational activities relating to sports by charitable entities registered u/s 12AA of I.T. Act.

Clause (a) of Entry 66 is pertaining to services provided by an educational institution to its students, faculty and staff.

The activities of holding educational conference / gathering of students, faculty and staff of other Schools, cannot be treated as services provided by an

educational institution to its students, faculty and staff;

Clause (aa) of Entry 66 is pertaining to conduct of entrance examination.

Therefore, this clause is not applicable to the activities of holding educational conference / gathering of students and staff of other Schools;

Clause (b)(i) of Entry 66 is pertaining to transportation of students, faculty and staff. This clause is not applicable to holding of educational conference /

gathering of students and staff of other Schools. This is also because such other Schools may or may not be providing educational services for pre-school

education or education up to higher secondary school or equivalent.

Clause (b)(ii) of Entry 66 is pertaining to the services provided to an educational

institution by way of catering. This clause shall not be applicable to catering services provided to an educational institution for holding of educational

conference / gathering of students and staff of other Schools, because the activities of organising an educational conference / gathering of students and staff of other Schools, itself is not eligible for exemption in any of the

Entries of Notification No. 12/2017-Central Tax (Rate).

Favorable/ Unfavorable

Unfavorable

DISCLAIMER

The information cited in this publication has been drawn from various provisions of The CGST Act, Rules, Circulars and other various sources. This material and the information contained herein prepared by Team GSTCORNOR® is intended for the citizens and professionals in GST to provide updates under GST and is not an exhaustive treatment of such subject. The above information‟s are not intended, and must not be taken, as legal advice on any particular set of facts or circumstances. While every effort has been made to keep, the information cited in this publication error free, Team GSTCORNOR® does not take any responsibility for any typographical or clerical error which may have crept in while compiling the information provided in this publication.

GSTCORNOR® disclaims all liability in respect to actions taken or not taken based on any or all the contents of this publication to the fullest extent permitted by law. Do not act or refrain from acting upon this information without seeking professional legal counsel

Monthly-Rs.149/-

Quarterly-Rs.399/-

Half Yearly-Rs.749/-

Yearly-Rs.1499/-

MONTHLY E-MAGAZINE

Note:- Please send screenshot of payment on ourwhatsapp no. 8989077616

MORNING DAILY E-NEWS LETTERONE PAGER BRIEFING ON GST RULING'SGST INSIGHTS ON COMPLEX TOPICS

JOIN GST E- SUBSCRIPTION PACKAGE

+91-8989077616

Paytm/BHIM/GooglePay At 8989077616IDBI A/c No. 0345102000007269 (IFSC: IBKL0000345)

WWW.GSTCORNOR.COM

READ. LEARN. SUCCEED IN GST...!!!

(Offer)

UPDATES +

LEARNING+

EXPERTISE