f–2414 sub. code 7bco1c1

TRANSCRIPT

sp5

F–2414

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

First Semester

Commerce

ADVANCED ACCOUNTANCY – I

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all the questions.

1. Define in the term Accounting.

PnUQ¯À Áøμ°»UPn® u¸P.

2. What is Double Entry System?

Cμmøh £vÄ •øÓ GßÓõÀ GßÚ?

3. What is Suspense Account?

AÚõ©zx PnUS GßÓõÀ GßÚ?

4. What is compensating Error?

\›UPmk® ¤øÇ GßÓõÀ GßÚ?

5. Define in the term Depreciation.

÷u´©õÚ® Áøμ¯ÖUP.

6. What is Sinking Fund method?

Dk {v GßÓõÀ GßÚ?

Sub. Code 7BCO1C1

F–2414

2

sp5 7. What is meant by sole trading?

uÛ¯õÒ ÁoP® GßÓõÀ GßÚ?

8. What is Adjusting Entry?

\›Pmk £vÄ GßÓõÀ GßÚ?

9. What is meant by Average due date?

\μõ\› uÁøÚ |õÒ GßÓõÀ GßÚ?

10. What is Red ink Interest?

]Á¨¦ ø© Ámi GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all the questions.

11. (a) What are the advantages of double entry system?

Cμmøh £vÄ •øÓ°ß |ßø©PÒ ¯õøÁ?

Or

(b) Give Journal entries for the following transactions.

2018 July 1

Cheque received from kumar Rs.10,000

3 Deposited the above cheque into Bank

6 Received cheque from kumar and deposited into bank on the same day Rs.5,000

15 Paid Arun by cheque Rs.2,500

F–2414

3

sp5 R÷Ç öPõkUP¨£mh |hÁiUøPPÐUS SÔ¨÷£mk

£vÄ GÊxP.

2018áúø»

1

S©õ›h® C¸¢x Põ÷\õø» ö£ØÓx ¹.10,000

3 ÷©÷» öPõkUP¨£mh Põ÷\õø» Á[Q°À

÷£õh¨£mhx

6 Põ÷\õø» ö£Ó¨£mh Aß÷Ó S©õº Á[Q

PnUQÀ ÷£õh¨£mhx ¹.5,000

15 A¸qUS Põ÷\õø» öPõkzux ¹.2500

12. (a) What are the types of errors?

¤øÇPÎß ÁøPPÒ ¯õøÁ?

Or

(b) Give the rectification entries for following error.

(i) Payment of Rs.500 to R.Mohan was wrongly debited to P.Mohan account.

(ii) Sale of furniture for Rs.750 was credited to sales account

(iii) Purchases from mani Rs.2,100 was wrongly passed through sales day book.

(iv) Wages Rs.1000 paid on erection of machinery was debited to wages account.

RÌPõq® |hÁiUøPPÐUS ¤øÇz v¸zu¨£vÄ

u¸P.

(i) R.÷©õPß US ¹.500 ö\¾zv¯x uÁÖu»õP

P.÷©õPß PnUQÀ £ØÖ øÁUP¨£mkÒÍx

(ii) AøÓP»ß ÂØÓx ¹.750 uÁÖu»õP ÂØ£øÚ

PnUQÀ ÁμÄ øÁUP¨£mkÒÍx

F–2414

4

sp5 (iii) ©o°hª¸¢x öPõÒ•uÀ ö\´ux ¹.2,100

uÁÖu»õP ÂØ£øÚ £v÷ÁmiÀ

£v¯¨£mkÒÍx

(iv) T¼ ÁÇ[Q¯x ¹.1,000 C¯¢vμzvØS

ö\¾zv¯uõP ö\¾zv¯uõP uÁÖu»õP £ØÖ

øÁUP¨£mkÒÍx. T¼ PnUQÀ.

13. (a) What are the objectives of providing Depreciation?

÷u´©õÚ® PnUQkÁvß ÷|õUP[PÒ ¯õøÁ?

Or

(b) Calculate the depreciation under straight line method.

Rs.

Purchase price of machine 2,00,000

Expenses for installation 50,000

Estimated residual value 25,000

Expected useful life 5 years

÷u´©õÚzøu ÷|º÷Põmk •øÓ°À PnUQkP

¹.

C¯¢vμ® Áõ[Q¯x 2,00,000

{ÖÄøP ö\»ÄPÒ 50,000

«u ©v¨¤mk öuõøP 25,000

£¯nΨ¦ Põ»® 5 BskPÒ

14. (a) What are the difference between Trial Balance and Balance sheet?

C¸¨£õ´Ä ©ØÖ® C¸¨¦ {ø» SÔ¨¦US

Cøh÷¯¯õÚ ÷ÁÖ£õkPÒ ¯õøÁ?

Or

F–2414

5

sp5 (b) Prepare Trading Account of Shri. Vijay for the year

ending 31st March 2017 from the following figures.

Rs.

Purchases 3,00,000

Sales 5,00,000

Stock (April 1, 2016) 40,000

Wages 30,000

Carriage inwards 4,000

Return outwards 3,000

Return outwards 2,500

Freight and clearing charges 5,000

Closing stock 42,000

RÌUPsh £vÄPøÍ öPõsk v¸.Âá´ AÁºPÎß 31

©õºa 2017® BskS›¯ ¯õ£õμ PnUøP u¯õ›UP.

¹.

öPõÒ•uÀ 3,00,000

ÂØ£øÚ 5,00,000

C¸¨¦ (H¨μÀ 1, 2016) 40,000

T¼ 30,000

EÒ yUS T¼ 4,000

öPõÒ•uÀ v¸¨£® 3,000

ÂØ£øÚ v¸¨£® 2,500

G›¨ö£õ¸Ò ©ØÖ® Pmk©õÚ ö\»Ä 5,000

CÖv C¸¨¦ 42,000

F–2414

6

sp5 15. (a) What are the uses of Average Due Date?

\μõ\› uÁøn |õÎß |øh•øÓ £¯ß£õkPÒ ¯õøÁ?

Or

(b) Kannan purchased goods from Raman. The due data for payment in cash being as follows:

Rs.

March 15 1,000 Due on 18th April

April 21 1,500 Due on 24th May

April 27 500 Due on 30th June

May 15 600 Due on 18th July

Raman agreed to draw a bill for the total amount due on the Average Due data. Calculate Average due data.

Psnß Cμõ©Ûhª¸¢x ö£õ¸mPøÍ Áõ[QÚõº

AÁº £n® ö\¾zu ÷Ási¯ uÁøn •iÁøμ²®

|õmPÒ ¤ßÁ¸©õÖ.

¹.

©õºa 15 1,000 •vºÄ |õÒ H¨μÀ 18

H¨μÀ 21 1,500 •vºÄ |õÒ ÷© 24

H¨μÀ 27 500 •vºÄ |õÒ áúß 30

÷© 15 600 •vºÄ |õÒ áúø» 18

Cμõ©ß AøÚzx öuõøPUS® ©õØÖ^mk GÊv \μõ\›

uÁøn |õÎÀ £n® ö\¾zvÂkÁuõP EhߣiQÓõº

GÚ öPõsk \μõ\› uÁøn |õÎøÚ PnUQkP.

F–2414

7

sp5 Part C (3 10 = 30)

Answer any three questions.

16. Prepare a Trial Balance from the following details. Rs. Rs.

Capital 16,800 Opening stock 21,000

Drawings 5,000 Purchases 36,000

Sales 72,000 Purchase return 2,000

Sales returns 3,000 Debtors 4,500

Creditors 2,500 Furniture 900

Bills Receivable 2,300 Bills payable 4,200

Wages 1,200 Advertisement 600

Discount allowed 100 Commission Received 600

Machinery 20,000 Cash 3,500

RÌPsh ÂÁμ[PøÍU öPõsk C¸¨£õ´Ä u¯õ›UP.

¹. ¹.

•uÀ 16,800 öuõhUP \μUQ¸¨¦ 21,000

Gk¨¦PÒ 5,000 öPõÒ•uÀ 36,000

ÂØ£øÚ 72,000 öPõÒ•uÀ v¸¨£® 2,000

ÂØ£øÚ v¸¨£® 3,000 PhÚõÎPÒ 4,500

PhÜ¢÷uõº 2,500 AøÓP»ß 900

ö£ÖuØSÔ¯

©õØÖ^mk

2,300 ö\¾zxuØS›¯

©õØÖ^mk

4,200

T¼ 1,200 ÂÍ®£μ ö\»Ä 600

AÎzu uÒУi 100 PÈĨö£ØÓx 600

C¯¢vμ® 20,000 öμõUP® 3,500

F–2414

8

sp5 17. Rectify the following errors:-

(a) Sales returns by a customer mohamed even though taken into stock Rs.600 not entered in the books.

(b) Sales book overcast by Rs.500

(c) The total of discount column on the debit side of cash book for Rs.75 not posted in discount account.

(d) Repairs to machinery Rs.630 debited to machinery account.

¤ßÁ¸® ¤øÇPøÍ v¸zu® ö\´P.

(A) •P©x GßÓ ÁõiUøP¯õͺ v¸¨¤ Aݨ¤¯

ÂØ£øÚ v¸¨£©õÚ ¹.600. \μU÷PmiÀ £vÄ

ö\´¯¨£hÂÀø».

(B) ÂØ£øÚ Hk ¹.500 AvP©õP Põmh¨£mkÒÍx.

(C) öμõUP Hmiß £ØÖ £Sv°¾ÒÍ ö©õzu uÒУi¯õÚ

¹.75 uÁøn uÒУi PnUQÀ £vÄ

ö\´¯¨£hÂÀø».

(D) C¯¢vμ £Êx£õº¨¦ ö\»Ä ¹.630 øÚ C¯¢vμ

PnUQÀ £ØÖ øÁUP¨£mkÒÍx.

18. A second hand machinery was purchased on 1.1.2010 for Rs.30,000 and Rs.6,000 and Rs.4,000 were spent on it’s repairs and erection respectively. On 1.7.2011, another machine was purchased for Rs.26,000. On 1.7.2012, the first machine was sold for Rs.30,000. On the same day one more machine was bought for Rs.25,000 On 31.12.2012 the machine bought on 1.7.2011 was sold for Rs.23,000 Accounts are closed on 31st December every year.

Depreciation is written of at 15% per annum written Down value method. Prepare Machinery account for 3 years.

F–2414

9

sp5 1.1.2010 AßÖ •ß÷ÚÓ £¯ß£kzv¯ C¯¢vμzvøÚ

¹.30,000 US Áõ[Q ¹.6,000 ©ØÖ® ¹.4,000 zuøÚ •øÓ÷¯

£Êx£õº¨¦ ©ØÖ® {ÖÄÁuØPõP ö\»ÁõP ö\´¯¨£mhx.

1.7.2011 À ©ØöÓõ¸ C¯¢vμ® ¹.26,000 US Áõ[P¨£mhx.

1.7.2012 À •u»õP C¯¢vμ® ¹.30,000US ÂØUP¨£mhx.

A÷u |õÒ ©ØöÓõ¸ C¯¢vμ® ¹.25,000US

Áõ[P¨£mkÒÍx. 31.12.2012 À 1.7.2011 À Áõ[Q¯

C¯¢vμ® ¹.23,000 US ÂØ£øÚ ö\´¯¨£mhx. JÆöÁõ¸

Bsk® 31 i\®£º ©õuzvÀ PnUS •iUP¨£kQÓx.

15% ÷u´©õÚ©õÚx SøÓ¢u ö\À C¸¨¦{ø» •øÓ°À

PnUQh¨£kQÓx GÚU öPõsk ‰ßÓõskPÐUS C¯¢vμ

PnUQøÚ u¯õ›UP.

19. From the following Trial Balance as on 31.12.2018. Prepare Trading and Profit and Loss a/c for the year ending 31.12.2018 and Balance sheet as on 31.12.2018.

Particulars Dr

(Rs.)

Particulars Cr

(Rs.)

Sundry Debtors 70,000 Sundry Creditors

50,000

Drawings 25,000 Capital 3,00,000

Insurance 50,000 Return outwards

5,000

General expenses 3,000 Sales 3,95,000

Salaries 6,000

Goodwill 40,000

Machinery 1,00,000

Freehold land building

50,000

Stock (opening) Building

10,000

2,00,000

F–2414

10

sp5

Particulars Dr

(Rs.)

Particulars Cr

(Rs.)

Carriage on purchase

5,000

Carriage on sales 2,000

Fuel and power 5,000

Wages 2,000

Return inwards 3,000

Purchases 1,50,000

Cash at Bank 13,000

Cash in hand 16,000

Adjustments:-

(a) Closing stock as on 31.12.2018 was Rs.30,000

(b) Goods worth Rs.1000 was taken for personal use by the proprietor.

(c) Provide 5% Interest on capital.

(d) Create 5% provision for doubtful debts.

(e) Loss of stock by Fire was Rs.10,000 and the Insurance company has agreed to pay the full money as compensation.

RÌPsh £vÄPøÍ öPõsk 31.12.2018 Bsiß Â¯õ£õμ,

C»õ£ |mh PnUS ©ØÖ® A¢|õøͯ C¸¨¦{ø»

SÔ¨¤øÚ²® u¯õ›UP.

ÂÁμ® £ØÖ

(¹.)

ÂÁμ® ÁμÄ

(¹.)

£Ø£» PhÚõÎPÒ 70,000 £Ø£»

PhÜ¢÷uõº

50,000

Gk¨¦ 25,000 •uÀ 3,00,000

F–2414

11

sp5

ÂÁμ® £ØÖ

(¹.)

ÂÁμ® ÁμÄ

(¹.)

Põ¨¥k 50,000 öPõÒ•uÀ

v¸¨£®

5,000

ö£õx ö\»ÄPÒ 3,000 ÂØ£øÚ 3,95,000

\®£Í® 6,000

|Øö£¯º 40,000

C¯¢vμ® 1,00,000

C»Á\ {» Pmih® 50,000

\μUQ¸¨¦

(öuõhUP®)

10,000

Pmih® 2,00,000

Ási öPõÒ•uÀ 5,000

Ási ÂØ£øÚ 2,000

G›ö£õ¸Ò ©ØÖ®

G›\Uv

5,000

T¼ 2,000

ÂØ£øÚ v¸¨£® 3,000

öPõÒ•uÀ 1,50,000

Á[Q öμõUP® 13,000

øP°¸¨¦ 16,000

\›PmkuÀPÒ

(A) 31.12.2018 ß £i CÖv \μUQ¸¨¦ ¹.30,000

(B) ¹.1000 ©v¨¦øh¯ ö£õ¸mPøÍ E›ø©¯õͺ ö\õ¢u

÷uøÁUS GkzxÒÍõº.

(C) 5% •uÀ «x Ámi PnUQkP.

(D) 5% I¯Phß JxUS E¸ÁõUP

(E) w°ÚõÀ ÷\u•ØÓ ¹.10,000 ©v¨¦øh¯

ö£õ¸ÒPÐUPõÚ CǨ¥miøÚ Põ¨¥mi {ÖÁÚ®

u¸ÁuõP EhߣmkÒÍx.

F–2414

12

sp5 20. Explain the different methods of calculation of interest

with its advantages.

£À÷ÁÖ ÁøP¯õÚ Ámi PnUQk® •øÓ°øÚ Auß

|ßø©PÐhß ÂÍUSP.

————————

Sp 5

F–2415

B.Com DEGREE EXAMINATION, NOVEMBER 2019

First Semester

Commerce

BUSINESS ORGANISATION

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. What is meant by trade?

Áõo£® GßÓõÀ GßÚ?

2. Define business.

¯õ£õμzvøÚ Áøμ¯ÖUP.

3. Who is sole proprietor?

uÛ¯õÒ ÁõoPº GߣÁº ¯õº?

4. State the definition of partnership.

Tmhõsø©°ß Áøμ»UPÚ® u¸P.

5. What do you know about representative firm?

¤μv{v {ÖÁÚ® £ØÔ }º AÔÁx ¯õx?

6. How the size of business will be measured?

¯õ£õμzvß AÍÂøÚ GÆÁõÖ AÍÂkÁõ´?

Sub. Code 7BCO1C2

F–2415

2

Sp 5

7. What do you know about democratization?

áÚ|õ¯P©õ¯©õUPÀ £ØÔ }º AÔÁx ¯õx?

8. State the meaning of oligarchy.

ußÚ»USÊÂß ö£õ¸Ò u¸P.

9. What is meant by price policy?

Âø»U öPõÒøP GßÓõÀ GßÚ?

10. What do you know about public enterprise?

ö£õx {ÖÁÚzøu¨ £ØÔ }º AÔÁx ¯õx?

Part B (5 5 = 25)

Answer all questions. choosing either (a) or (b)

11. (a) Elucidate the objectives of business.

ÁoP ÷|õUP[PøÍ öuÎÄ£kzxÄ®.

Or

(b) Briefly explain the qualities of good businessman.

|À» öuõÈ»v£›ß Sn[PøÍ _¸UP©õP ÂÍUSP.

12. (a) Interpret about ideal form of organization.

Aø©¨¤ß ]Ó¢u ÁiÁ® £ØÔ _¸UP©õP ÂÍUSP.

Or

(b) State the merits and demerits of joint stock company.

Tmk¨ £[S {ÖÁÚzvß |ßø©PÒ ©ØÖ®

SøÓ£õkPøÍ TÖP.

F–2415

3

Sp 5

13. (a) Focus the evils of big business.

ö£¸ÁoPzvß wø©PøÍ TÖP.

Or

(b) Generalize the factors affecting optimum size of business.

¯õ£õμzvß AvP£m\ AÍøÁ £õvUS®

PõμoPøͨ ö£õxø©¨£kzxP.

14. (a) Enumerate the powers and duties of chief executives.

uø»ø© {ºÁõQPÎß AvPõμ[PøͲ® ©ØÖ®

Phø©PøͲ® ÂÁ›UPÄ®.

Or

(b) Describe the functions of Board of Directors.

C¯US|ºPÒ Áõ›¯zvß ö\¯À£õkPøÍ _¸UP©õP

ÂÁ›UPÄ®.

15. (a) Indicate the rationale of public enterprises.

ö£õx {ÖÁÚ[PÎß •UQ¯zxÁzøu _miUPõmkP.

Or

(b) Summarize the characteristics of public utilities.

ö£õx £¯ß£õkPÎß £s¦PøÍ _¸UP©õP TÖP.

Part C (3 10 = 30)

Answer any three questions.

16. Predict the requisites for success in modern business.

|ÃÚ Â¯õ£õμzvÀ öÁØÔUPõÚ ÷uøÁPøÍ ÂÁ›UPÄ®.

17. Distinguish between various forms of business.

£À÷ÁÖ ÁøP¯õÚ ÁoP[PÐUS Cøh÷¯ EÒÍ

÷ÁÖ£õmiøÚ ÂÁ›UPÄ®.

F–2415

4

Sp 5

18. Critique the reasons for survival of small units.

]Ô¯ ÁoP A»SPÎß ÁõÌÄ öuõhºÁuß Põμn[PøÍ

ÂÁ›UPÄ®.

19. Illustrate the problems faced by company management.

{ÖÁÚzvß ÷©»õsø© GvºöPõÒЮ ¤μa]øÚPøÍ

ÂÍUSP.

20. Sketch the industrial policy in India including industrial policy resolutions.

öuõÈÀxøÓ öPõÒøP wºÄPÒ Em£h C¢v¯õÂß

öuõÈÀxøÓ öPõÒøPø¯ ÂÍUSP.

————————

Wk 3

F–2416

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Second Semester

Commerce

ADVANCED ACCOUNTANCY – II

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. What is meant by bill of exchange?

©õØÖa ^mk GßÓõÀ GßÚ?

2. What do you know about promissory note?

Phß £zvμ® £ØÔ }º AÔÁx ¯õx?

3. What is meant by fire insurance?

wUPõ¨¥k GßÓõÀ GßÚ?

4. What do you know about memorandum trading account?

SÔ¨£õøÚ Â¯õ£õμ PnUS £ØÔ }º AÔÁx ¯õx?

5. What is cost price?

AhUP Âø» GßÓõÀ GßÚ?

6. What is consignment account?

Aq¨¥k PnUS GßÓõÀ GßÚ?

Sub. Code 7BCO2C1

F–2416

2

Wk 37. Write the name of the methods of keeping Joint venture.

CønÂøÚ øÁzxU öPõÒÍ £¯ß£k® •øÓPøÍ GÊxP.

8. Why joint bank account is maintained in Joint venture?

Cøn ÂøÚ°À Hß Cøn Á[Q P/S £μõ©›UP¨£kQÓx?

9. What is meant by single entry system?

JØøÓ¨ £vÄ •øÓ GßÓõÀ GßÚ?

10. What is meant by bills payable?

ö\¾zuØS›¯ ©õØÖa ^m GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Describe the features of bill of exchange.

©õØÖa ^miß C¯À¦PøÍ _¸UP©õP ÂÁ›.

Or

(b) On March 10th, Mr. A. Sold goods to Mr. B and draw

a bill for Rs.800 which B accepts immediately and

returns it to Mr. A. The bill is honoured on the due

date. Pass entries in the books of A and B.

©õºa 10® ÷uv v¸. A GߣÁº BUS ö£õ¸Ò ÂØ£øÚ

ö\´x, ^mk JßÖ ¹.800 US Áøμ¢uõº. Ehß B Aøu

HØÖUöPõsk A&ÂØS v¸¨¤ Aݨ¤Úõº. SÔ¨¤mh

÷uv°À ^mkUS £n® ö\¾zu¨£mhx GÛÀ A ©ØÖ®

Bß PnUQÀ £vÄPøÍ GÊxP.

F–2416

3

Wk 312. (a) Describe the significance of memorandum trading

account.

SÔ¨£õøÚ Â¯õ£õμ PnUQß •UQ¯zxÁzøu

_¸UP©õP ÂÁ›.

Or

(b) A fire occurred on 15th September, 2017 in the business premises. From the following figures ascertain the claim to be lodged.

Rs. Stock on 1st April, 2017 1,05,300Purchases from 1st April 2017 to the date of fire

3,50,000

Manufacturing expenses 2,60,000Sales from 1st April 2017 to the date of fire

6,76,000

Goods used by the partners privately (cost)

10,500

The rate of gross profit is 30% on cost

The stock salvaged is Rs. 36,000.

15.9.17À ¯õ£õμ {ÖÁÚzvÀ w £zx HØ£mhx.

¤ßÁ¸® £μ[Pμ¸¢x w Põ¨¥mk öuõøP°øÚ

Psk¤iUP. ¹.

1.4.2017À \μUS 1,05,300

1.4.17 •uÀ w HØ£mh Põ»® Áøμ

öPõÒ•uÀ 3,50,000

EØ£zv ö\»Ä 2,60,000

1.4.17 •uÀ w HØ£mh Põ»® Áøμ

ÂØ£øÚ 6,76,000

E›ø©¯õͺ AhUP Âø»°À

£¯ß£kzv¯øÁ

10,500

AhUPÂø»°À 30% ö©õzu »õ£ ÂQu®

Põ¨£õØÓ¨£mh \μUS ¹. 36,000.

F–2416

4

Wk 313. (a) Describe the procedure for calculating unsold stock.

ÂØPõu ö£õ¸mPøÍ PnUQkÁuØPõÚ |øh•øÓø¯

_¸UP©õP ÂÁ›.

Or

(b) Sri Krishna & Co. of Chennai consigned 100, Mp3

players to Venkatram & Co of Hyderabad. The cost

of each MP3 player was Rs.500 The consignor paid

insurance Rs.500 and freight Rs.800 Venkatram &

co. sold 80 units of MP3 players at Rs.600 each. It

incurred the following expenses. Carriage Rs.20

establishment expenses Rs.130 and commission @

5% is Rs.2,400. Calculate the value of consignment

stock.

Q¸èn & Co. 100, Mp3 J¼¨£õøÚ, íuõμõ£õz

öÁ[Pm μõ® & Co ØS Aݨ¥k ö\´uõº.

JÆöÁõßÖ® AhUPÂø» ¹.500. Põ¨¥k ¹.500

©ØÖ® ÷£õUSÁμzx ¹.800 I Aݨ¥k ö\´uÁº

ö\¾zvÚõº. JÆöÁõßÖ® MP3 ¹.600 Ãu® 80

J¼¨£õßPøÍ öÁ[Pmμõ® & {ÖÁÚ® ÂØ£øÚ

ö\´ux ©ØÖ® Ási ÁõhøP ¹.20 Aø©¨¦ ö\»Ä

¹.130 ©ØÖ® 5% uμS ¹.2,400 BQ¯ÁØøÓ

ö\¾zv¯x. Aݨ¥k \μUS ©v¨¦ Psk¤iUP.

14. (a) Distinguish between joint venture and sale.

CønÂøÚ ©ØÖ® ÂØ£øÚ CÁØøÓ ÷ÁÖ£kzxP.

Or

F–2416

5

Wk 3 (b) X and Y entered into a joint venture for purchase

and sales of some household items. They agreed to share profit and losses in the ratio of their respective contribution. X contribute Rs.10,000 in cash and Y Rs.13,000. The whole amount was placed in a joint bank account. Goods were purchased by X for Rs.10,000 and expenses paid by Y Rs.2,000. They also purchased goods for Rs.15,000 through the Joint Bank Account. The expenses on purchase and sale of the articles amounted to Rs.6,000 (including those met by Y). Goods costing Rs.20,000 were sold for Rs.45,000 and the balance was lost by fire.

Prepare Joint Venture Account, Joint Bank Account and the Venturers’ Accounts for closing the venture.

Ãmk E£÷¯õP ö£õ¸mPøÍ Áõ[Q ÂØP X ©ØÖ® Y CønÂøÚ HØ£kzvÚº. AÁºPÒ »õ£ |mhzøu

£[PΨ¦ ÂQuzvÀ ¤›UP •iÄ ö\´uÚº. öμõUP©õP

X ¹.10,000, Y ¹.13,000 £[PÎzuÚº. AøÁ

CønÁ[Q PnUQÀ ÷£õh¨£mhx. X ¹.10,000US

öPõÒ•uÀ ©ØÖ® Y ö\»ÂØPõP ¹.2,000 ö\»Ä

ö\´uÚº. Cøn Á[Q ‰»® ¹.15,000 öPõÒ•uÀ.

öPõÒ•uÀ ÂØ£øÚ°À ö\»Ä ¹.6,000 (Y ö\´u

ö\»Ä ÷\º¢x) ¹.20,000 AhUPÂø»¨ ö£õ¸Ò

¹.45,000 ØS ÂØ£øÚ BQ¯Ú «u•ÒÍøÁ w°À

÷\u•ØÓx GÚU öPõsk CønÂøÚ PnUS, Cøn

Á[Q PnUS ©ØÖ® CønÂøÚbºPÎß PnUSPøÍ

CønÂøÚ •iÄØÓx GÚU öPõsk u¯õ›UP.

15. (a) What are the advantages of single entry system?

JØøÓ£vÄ •øÓ°ß |ßø©PÒ ¯õøÁ?

Or

F–2416

6

Wk 3 (b) From the following information, calculate the

profit/loss earned by Ms. Kamila a small trader during the year 2018

Rs.

Capital as on 31.12.2018 66,000

Capital as on 1.1.2018 65,000

Drawings during 2018 12,000

Additional capital introduced during 2018 7,000

¤ßÁ¸® £μ[PøÍU öPõsk ]Ö öuõÈÀ ¯õ£õ›

v¸©v Põª»õÂß 2018 Bsk »õ£ |mhzøu

PnUQkP

¹.

‰»uÚ® 31.12.2018À 66,000

‰»õuÚ® 1.1.2018 À 65,000

2018 Á¸hzvÀ Gk¨¦ 12,000

2018À TkuÀ ‰»uÚ® AÔ•P¨£mhx 7,000

Part C (3 10 = 30)

Answer any three questions.

16. Raj draws a bill on Murugan at 3 months for Rs.4,00,000 on 1.7.2016 and on acceptance, immediately discounts the bill at 7% p.a. and sends half the proceeds to Murugan. On the same date, Murugan draws a 3 months bill on Raj for Rs.2,00,000 and remits half of the proceeds to Raj after discounting the bill, at 8% p,a. Murugan is declared as Insolvent on 31.8.2016 and a First and Final dividend of 25% is received on 15.10.2016. Pass Journal Entries in the Books of Raj and Murugan.

F–2416

7

Wk 3 1.7.2016 AßÖ ¹.4,00,000 ØS μõä •¸Pß «x 3 ©õu ^mk

HØ£kzv, AuøÚ HØÓÄhß 7% uÒУi°À Ámh®

ö\´uõº. AvÀ £õvø¯ •¸PÝUS Aݨ¤Úõº. A÷u

÷uv°À •¸Pß ¹.2,00,000 ØS 3 ©õu ^mk u¯õº ö\´x

AuøÚ μõä HØÓ ¤ß 8% uÒУi ö\´x öuõøP°À

£õvø¯ μõáúUS Aݨ¤Úõº. 31.8.2016 À •¸Pß ö|õi¨¦

{ø» Aøh¢uõº. 15.10.2016 À •uÀ ©ØÖ® CÖv £[PõP

25% Qøhzux. μõä ©ØÖ® •¸Pß PnUQß •uØSÔ¨÷£k

£vÄPÒ u¸P.

17. A fire occurred on the premises of a merchant on 18th September, 2016 and a considerable part of the stock was destroyed. The value of the stock saved was Rs.8,200. The books disclosed that on 1st April 2016 the stock was valued at Rs.66,850, the purchases to the line of fire amounted to Rs.1,85,000 and the sales to Rs.2,82,500. Goods costing Rs. 500 were taken for personal use and goods sold for Rs.2,500 were returned to the merchant. On investigation it is found that during the past five years the average gross profit on the cost was 25%.

You are required to prepare statement showing the amount the merchant should claim from the insurance company in respect of stock destroyed by fire.

18.9.2016À w £zx HØ£mk ö£õ¸Ò ÷\u©øh¢ux.

¹.8,200 ©v¨¦ ö£õ¸Ò «mP¨£mhÚ. 1.4.2016 \μUS ©v¨¦

¹.66,850, £zx HØ£mh |õÒ Áøμ öPõÒ•uÀ ¹.1,85,000,

©ØÖ® ÂØ£øÚ ¹.2,82,500 ö\õ¢u E£÷¯õPzvØS Gkzx

ö\À»¨£mh ö£õ¸Ò ¹.500 ©ØÖ® ¯õ£õ›US

v¸¨£¨£mh ö£õ¸Ò ¹.2,500 Ph¢u 5 BskPÎÀ \μõ\›

ö©õzu »õ£ ÂQu® AhUP Âø»°À 25%.

w°ÚõÀ HØ£mh |mh Dk Põ¨¥k {ÖÁÚzvh® C¸¢x ö£Ó

÷Ási¯ öuõøPø¯ PnUQkP.

F–2416

8

Wk 318. Arun of Madras consigned 100 sewing machine to Sanjay

of Jaipur. Cost price of a machine Rs.1,500. Invoice Price Rs.2,000. Arun paid Rs.6,000 as railway charges and Rs.2,000 as insurance. Sanjay remitted Rs.1,00,000 to Arun by Bank draft. 80 sewing machines were sold @ Rs.2,200 each. Sanjay’s expenses : carriage inwards Rs.250; Octori Rs.750; Godown rent Rs.5,000; Advertisement Rs.3,000. Sanjay is entitled to 5% commission on sales. Prepare a consignment and consignees account.

A¸ß, ö\ßøÚ°¼¸¢x 100 øu¯À C¯¢vμ® \g\´

öá´§¸US Aݨ¤Úõº. JßÔß AhUP Âø» ¹.1,500. Chõ¨¦ Âø» ¹.2,000. μ°À÷Á ö\»ÂPÒ ¹.6,000 ©ØÖ®

Põ¨¥k ¹.2,000 A¸s ö\¾zvÚõº Á[Q ‰»©õP \g\´

¹.1,00,000 A¸qUS ÁÇ[QÚõº. JÆöÁõßÖ® ¹.2,200 Ãu® 80 C¯¢vμ® ÂØ£øÚ¯õÚx. \g\´ ö\»ÄPÒ : Ási

ö\»Ä ¹.250; Aμ_ •zvøμ ¹.750; ÁõhøP ¹.5,000; ÂÍ®£μ® ¹.3,000. ÂØ£øÚ uμS 5%. \g\õ´US QøhUS®

GÚU öPõsk Aݨ¥k ©ØÖ® ö£Ö|º PnUS u¯õ›UP.

19. Banerjee and Mukherjee agreed to import Russian timber into India. On 1st July, 2016, they opened a joint bank account with Rs.25,000, towards which Banerjee contributed Rs.15,000 and Mukherjee contributed Rs.10,000. They agreed to share profits and lossed in proportion to their cash contributions.

They remitted to their agent, in Russia Rs.20,000 to pay for timber purchased, and later Rs.2,100 in settlement of his account, Freight, insurance, and clock charges amounted to Rs.3,900. On Dec. 31, 2016 the sales amounted to Rs.28,740 which enabled them to repay themselves with cost originally advanced (no account to he taken of interest). They then decided to close the venture and Mukherjee agreed to take over the timber unsold for Rs.1,260, which is to be deducted from his share of profit.

Prepare the necessary accounts.

F–2416

9

Wk 3 μè¯ ©μzuiPøÍ C¢v¯õÄUS CÓUS©v ö\´¯ £õÚºâ

©ØÖ® •Pºâ \®©vzuÚº. 1.7.2016 ¹.25,000 öPõsk

Cøn Á[QU P/S öuõhUP®. AvÀ £õں⠹.15,000 ©ØÖ®

•Pºâ ¹.10,000. öμõUP £[PΨ¤ß £i »õ£ |mh ¤›¨¦

|øhö£Ö®.

öPõÒ•uÀ ¦v¯ μè¯ •PÁ¸US ¹.20,000 Aݨ£¨£mk

¤ß ¹.2,100 ö\¾zv PnUS •iUP¨£mhx. Ási ÁõhøP,

Põ¨¥k ©ØÖ® PiPõμ Âø» ¹.3,900. 31.12.2016 À ÂØ£øÚ

¹.28,740. Cuß ‰»® •ß £n©õP ö\¾zu¨£mh

öuõøPø¯ (Ámi ÷\ºUPõ©À) öPõkUP •i¢ux. ¤ß Cøn

ÂøÚø¯ •iÄUS öPõsk Á¢x, ÂØ£øÚ BPõu

ö£õ¸øÍ •Pºâ ¹.1,260 GÚ Gkzx öPõshõº. CzöuõøP

AÁμx £[S »õ£zvÀ SøÓUP¨£k® GÚU öPõsk •UQ¯

PnUSPøÍ u¯õ›UP.

20. Mr Xavier has maintained his books by single entry method. From the following details, calculate profit for the year and a statement of affairs at the end of the year. Rs.1,000 (Cost) furniture was sold for Rs.5,000 on 1.1.2016. 10% depreciation is to be charged on furniture. Mr. Xavier has drawn Rs.1,000 p.m. Rs.2,000 was invested further capital.

1.1.2016 31.12.2016

Rs. Rs.

Stock 40,000 60,000

Debtors 30,000 40,000

Cash 2,000 1,000

Bank 10,000 5,000

Creditors 15,000 25,000

Outstanding expenses 5,000 8,000

Furniture (cost) 3,000 2,000

Bank balance on 1.1.2016 is as per cash book but the bank overdraft an 31.12.2016 is as bank statement. Rs.2,000 cheques drawing in Dec. 2016 have not been encashed within the year.

F–2416

10

Wk 3 v¸ ÷\¯º JØøÓ £vÄ •øÓ°À PnUS £μõ©›UQÓõº.

RÌPõq® £μzv¼¸¢x Bsk CÖvUPõÚ »õ£zøu

Psk¤izx {ø» AÔUøP u¯õ›UP. 1.1.2016À ¹.1,000

AhUPÂø»²ÒÍ AøÓP»ß ¹.5,000ØS ÂØÓx. CuØS 10%

÷u´©õÚ® PnUQh¨£mkÒÍx. AÁº ©õu® ¹.1,000 Gk¨¦

ö\´uõº. TkuÀ •u»õP ¹.2,000 •u½k ö\´¯¨£mhx.

1.1.2016 31.12.2016

¹. ¹.

\μUS 40,000 60,000

PhÚõÎPÒ 30,000 40,000

öμõUP® 2,000 1,000

Á[Q 10,000 5,000

PhÜ¢÷uõº 15,000 25,000

öPõk£hõu ö\»Ä 5,000 8,000

©øÚzxøn¨ ö£õ¸Ò 3,000 2,000

1.1.2016 öμõUP ¦zuP¨£i Á[Q C¸¨¦ BÚõÀ Á[Q

AÔUøP £i 31.12.2016 À Á[Q ÷©À Áø쨣ØÖ i\®£º

2016 GkUP¨£mh Põ÷\õø» ¹.2,000 A¢u BsiØSÒ

£n©õUP¨£hÂÀø».

————————

sp4

F–2417

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Second Semester

Commerce

MARKETING

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all the questions.

1. What is marketing?

\¢øu°kuÀ GßÓõÀ GßÚ?

2. Define the term of marketing mix.

\¢øu°ku¼ß P»øÁ GßÚ?

3. What is product policy?

u¯õ›¨¦ öPõÒøP GßÓõÀ GßÚ?

4. Write a short note an product life cycle.

u¯õ›¨¦ ÁõÌUøP _ÇØ] ]ÖU SÔ¨¦ ÁøμP.

5. What is financing?

{v°¯À GßÓõÀ GßÚ?

6. What is risk bearing?

B£zx uõ[Q GßÓõÀ GßÚ?

Sub. Code 7BCO2C2

F–2417

2

sp 47. What is pricing policy?

Âø» öPõÒøP GßÓõÀ GßÚ?

8. What are the pricing strategies?

Âø» EzvPÒ GßÓõÀ GßÚ?

9. What is promotion policy?

FUS¨¦ öPõÒøP GßÓõÀ GßÚ?

10. Write a short note an sales promotion.

ÂØ£øÚ FUS¨¦ J¸ ]ÖU SÔ¨¦ ÁøμP.

Part B (5 5 = 25)

Answer all the questions, choosing eigther (a) or (b).

11. (a) Write the needs of marketing segmentation.

\¢øu°kuÀ ¤›Âß ÷uøÁPøÍ GÊxP.

Or

(b) List out the evolution of marketing.

\¢øu°ku¼ß £›nõ©zvøÚ £mi¯¼kP.

12. (a) What are the classifications of consumer goods?

~Pº÷Áõº ö£õ¸mPÎß ÁøP¨£õkPÒ ¯õøÁ?

Or

(b) Write the features of product policy.

u¯õ›¨¦ öPõÒøP°ß A®\[PøÍ GÊxP.

F–2417

3

sp 413. (a) What are the functions of marketing?

\¢øu°ku¼ß ö\¯À£õkPÒ ¯õx?

Or

(b) List out the types of transportation.

÷£õUSÁμzvß ÁøPPÒ £ØÔ £mi¯¼kP.

14. (a) What are objectives of pricing policy?

Âø»U öPõÒøP°ß ÷|õUP[PÒ ¯õøÁ?

Or

(b) Discuss the factors influencing price decisions.

Âø»•iÄPøÍ £õvUS® PõμoPøÍ ÂÁõv.

15. (a) What are the various media of advertisement?

ÂÍ®£μzvß £À÷ÁÖ FhP® ¯õøÁ?

Or

(b) Discuss the qualities of a successful salesman.

öÁØÔPμ©õÚ ÂØ£øÚ¯õÍ›ß Sn[Pøͨ £ØÔ

ÂÁõv.

Part C (3 10 = 30)

Answer any three questions.

16. Briefly explain the criteria for segmentation.

£S¨£õ´ÄUPõÚ AÍÄ÷PõÀPøÍ _¸UP©õP ÂÍUSP.

17. Discuss the stages of product life cycle.

u¯õ›¨¦ ÁõÌUøP _ÇØ]°ß {ø»PøÍ ÂÁõv.

F–2417

4

sp 418. Distinguish between the grindings and standardization.

uμ® ©ØÖ® uμ{ø»US Cøh÷¯ EÒÍ ÷ÁÖ£õkPøÍ TÖP.

19. Explain the various methods of promotion policy.

÷©®£õmkU öPõÒøP°ß £» ÁÈ•øÓPøÍ ÂÍUSP.

20. Explain the significance of Personal selling.

uÛ¨£mh ÂØ£øÚ°ß CßÔ¯ø©¯õø© £ØÔ ÂÁ›.

–––––––––

Wk 6

F–2418

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Third Semester

Commerce

PRINCIPLES OF INSURANCE

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. Define in the term of risk.

uøh GߣuøÚ Áøμ¯Ö.

2. What is insurance?

Põ¨¥k GßÓõÀ GßÚ?

3. What is investment of fund?

•u½mk {v GßÓõÀ GßÚ?

4. What is the life insurance?

B²Ò Põ¨¥k GßÓõÀ GßÚ?

5. What is report?

AÔUøP GßÓõÀ GßÚ?

6. Define in the term of life policy.

ÁõÌUøP öPõÒøP Áøμ¯Ö.

Sub. Code 7BCO3C1

F–2418

2

Wk 67. What is issue of premiums?

•øÚ©zvÀ öÁΰkuÀ GßÓõÀ GßÚ?

8. What are policy conditions?

öPõÒøP {£¢uøÚPÒ GßÓõÀ GßÚ?

9. What are marine policies?

PhÀ öPõÒøPPÒ GßÓõÀ GßÚ?

10. What is payment of claim?

E›ø© ÷Põ¸Áx GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Explain the various methods of treating risk.

B£zvß ]Qaø\°ß £À÷ÁÖ •øÓPÒ ¯õøÁ?

Or

(b) What are the functions of insurance?

Põ¨¥miß ö\¯À£õkPÒ GßöÚßÚ?

12. (a) Explain the importance of investment of fund.

•u½mk {v°ß •UQ¯zxÁzøu ÂÁ›.

Or

(b) Explain the fundamentals of life contract.

ÁõÌUøP J¨£¢uzvß Ai¨£øhPøÍ ÂÍUSP.

F–2418

3

Wk 613. (a) Write a short note on the financial positions.

{v {ø»PøÍ £ØÔ ]ÖU SÔ¨¦ ÁøμP.

Or

(b) List out about medical examinations.

©¸zxÁ £›÷\õuøÚ £ØÔ GkzxøμUP.

14. (a) Explain the role of LIC in human life.

©Ûu ÁõÌÂØS B²Ò Põ¨¥mk {ÖÁÚzvß £[QøÚ

ÂÁ›.

Or

(b) Write a short on the commencement of risk.

B£zx E¸ÁõSÁvøÚ £ØÔ SÔ¨¦ ÁøμP.

15. (a) Explain the nature of marine insurance contract.

PhÀ Põ¨¥k J¨£¢uzvß ußø©ø¯ ÂÍUSP.

Or

(b) Put out the methods of payments of claim.

÷Põ›UøP ö\¾zxuÀ •øÓPÒ £ØÔ ÂÁ›UP.

Part C (3 10 = 30)

Answer any three questions.

16. What are the types of insurance? Explain in detail.

Põ¨¥k ÁøPPÒ GßöÚßÚ? ›ÁõP ÂÁ›.

17. Briefly explain the various types of investment.

£À÷ÁÖ ÁøP¯õÚ •u½kPøÍ £ØÔ _¸UP©õP ÂÁ›UP.

18. Describe the various methods of reports.

£À÷ÁÖ ÁøP¯õÚ AÔUøPPøÍ £ØÔ ÂÁ›UP.

F–2418

4

Wk 619. Write a short note on the surrender value and paid up

value.

J¨£øh¨¦ ©v¨¦ ©ØÖ® Fv¯ ©v¨¦ £ØÔ ]Ö SÔ¨¦

ÁøμP.

20. Discuss the classification of marine policies.

PhÀ öPõÒøPPÎß ÁøP¨£õkPøÍ £ØÔ ÂÁõvUP.

————————

Ws9

F–2419

B.Com DEGREE EXAMINATION, NOVEMBER 2019

Third Semester

Commerce

BANKING THEORY

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. What is banking?

Á[Q°¯À GßÓõÀ GßÚ?

2. Define unit banking.

AÍÄ Á[Q Áøμ»UPn® u¸P.

3. What is commercial bank?

ÁºzuP Á[Q GßÓõÀ GßÚ?

4. What is merchant banking?

ÁoP Á[Q GßÓõÀ GßÚ?

5. What are the terms of credit creation?

Phß E¸ÁõUP® GßÓõÀ GßÚ?

6. What is money market?

£n\¢øu GßÓõÀ GßÚ?

Sub. Code 7BCO3C2

F–2419

2

Ws9

7. Define in the term central bank

©zv¯ Á[Q Áøμ»UPn® u¸P.

8. What is Co-operative sector?

TmkÓÄ xøÓ GßÓõÀ GßÚ?

9. What are called as banking sector reform?

Á[Qz xøÓ°ß ^ºv¸zu® GßÓõÀ GßÚ?

10. Define E-banking.

C–Á[Q Áøμ»UPn® u¸P.

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Briefly explain the organizational structure of banks.

Á[Q {ÖÁÚ Pmhø©¨¦PøÍ _¸UP©õP ÂÍUSP.

Or

(b) Write about Unit Banking, Branch Banking.

A»S Á[Q, QøÍ Á[QPøÍ £ØÔ GÊxP.

12. (a) List out the role of bank in economic development.

Á[Q°ÚõÀ HØ£k® ö£õ¸Íõuõμ Áͺa]ø¯

£mi¯¼kP.

Or

(b) Explain about merchant banking.

ÁoP Á[Q £ØÔ ÂÁ›.

F–2419

3

Ws9

13. (a) What are the importances of money market?

£na \¢øu°ß •UQ¯zxÁ[PÒ GßÚ?

Or

(b) Explain the investment policy of bank

Á[Q°ß •u½mk öPõÒøPø¯ ÂÍUSP.

14. (a) Discuss about SBI and Co-operative sector.

SBI ©ØÖ® TmkÓÄ xøÓ £ØÔ ÂÁõv.

Or

(b) State the functions of RBI.

C¢v¯ ›\ºÆ Á[Q°ß £oPøÍ TÖP.

15. (a) List out the provision requirements.

ÁÇ[PÀ ÷uøÁPøÍ £mi¯¼kP.

Or

(b) Briefly explain the recent developments in banking.

\«£zvß Á[Q°¯À Áͺa]ø¯ ÂÍUSP.

Part C (3 10 = 30)

Answer any three questions.

16. What are the classifications of banking structure?

Á[Q Aø©¨¤ß ÁøP¨£õkPÒ GßöÚßÚ?

17. Briefly explain the various types of merchant banking.

£À÷ÁÖ ÁøP¯õÚ ÁoP Á[QPøÍ _¸UP©õP ÂÍUSP.

18. Explain the importance of money market.

£n® \¢øu°ß •UQ¯zxÁzøu ÂÍUSP.

F–2419

4

Ws9

19. Briefly explain about small scale industries.

]Ô¯ AÍ»õÚ öuõÈØ\õø»PøÍ _¸UP©õP ÂÍUSP.

20. Discuss the various products of e-Banking.

Cøn¯uÍ Á[Q°ß £À÷ÁÖ ÷\øÁPøÍ ÂÁõvUP.

————————

Wk ser

F–2420

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Third Semester

Commerce

BUSINESS STATISTICS

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all the questions.

1. Define statistics.

¦Òΰ¯À – Áøμ»UPn® u¸P.

2. What is primary data?

•ußø© uPÁÀ GßÓõÀ GßÚ?

3. Define the term mode.

•Pk Áøμ»UPn® u¸P.

4. What is Range?

Á쮦 GßÓõÀ GßÚ?

5. What is correlation?

Cø¯¦ GßÓõÀ GßÚ?

6. Define regression analysis.

¤ßÚøhÄ £S¨£õ´Ä Áøμ¯Ö.

Sub. Code 7BCO3C3

F–2420

2

Wk ser7. Define Index Number.

SÔ±mk Gs Áøμ»UPn® u¸P.

8. What is Base Shifting?

Ai¨£øh ©õØÓ® GßÓõÀ GßÚ?

9. What is a time series?

÷|μ öuõhº GßÓõÀ GßÚ?

10. What is moving average method?

\μõ\› |PºÄ •øÓ GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all the questions, choosing either (a) or (b).

11. (a) What are the objectives of samples?

©õv›PÎß ÷|õUP[PÒ ¯õøÁ?

Or

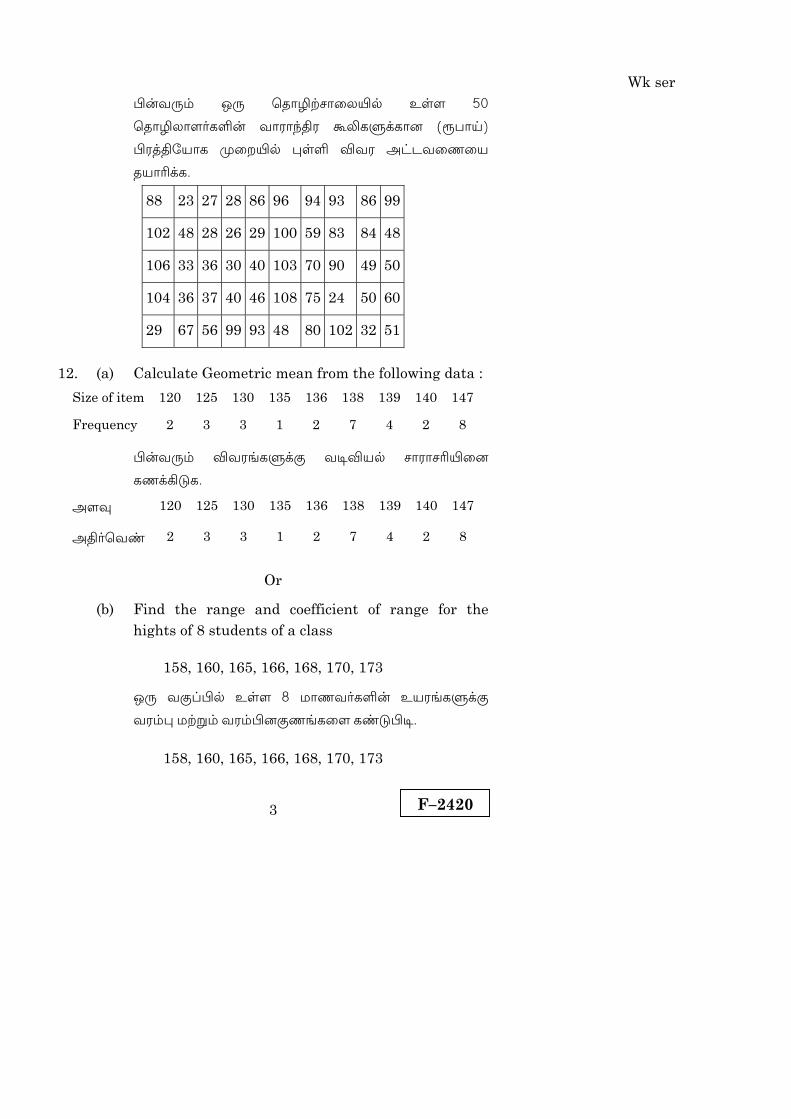

(b) Prepare a statistical table from the following weekly wages of 50 workers (in Rupees) of a Factory. Use the exclusive method of classification.

88 23 27 28 86 96 94 93 86 99

102 48 28 26 29 100 59 83 84 48

106 33 36 30 40 103 70 90 49 50

104 36 37 40 46 108 75 24 50 60

29 67 56 99 93 48 80 102 32 51

F–2420

3

Wk ser ¤ßÁ¸® J¸ öuõÈØ\õø»°À EÒÍ 50

öuõÈ»õͺPÎß Áõμõ¢vμ T¼PÐUPõÚ (¹£õ´)

¤μzv÷¯õP •øÓ°À ¦ÒÎ ÂÁμ AmhÁønø¯

u¯õ›UP.

88 23 27 28 86 96 94 93 86 99

102 48 28 26 29 100 59 83 84 48

106 33 36 30 40 103 70 90 49 50

104 36 37 40 46 108 75 24 50 60

29 67 56 99 93 48 80 102 32 51

12. (a) Calculate Geometric mean from the following data :

Size of item 120 125 130 135 136 138 139 140 147

Frequency 2 3 3 1 2 7 4 2 8

¤ßÁ¸® ÂÁμ[PÐUS Ái¯À \õμõ\›°øÚ

PnUQkP.

AÍÄ 120 125 130 135 136 138 139 140 147

AvºöÁs 2 3 3 1 2 7 4 2 8

Or

(b) Find the range and coefficient of range for the hights of 8 students of a class

158, 160, 165, 166, 168, 170, 173

J¸ ÁS¨¤À EÒÍ 8 ©õnÁºPÎß E¯μ[PÐUS

Á쮦 ©ØÖ® Á쮤ÚSn[PøÍ Psk¤i.

158, 160, 165, 166, 168, 170, 173

F–2420

4

Wk ser13. (a) Find the Karl Pearson’s co-efficient of correlation

X 6 2 10 4 8

Y 9 11 5 8 7

PõμÀ ¤¯õº\Ûß öuõhº¦PõÚ öPÊÂøÚ Psk¤i.

X 6 2 10 4 8

Y 9 11 5 8 7

Or

(b) Ten competitors in a beauty contest are ranked by two judges in the following order : calculate rank correlation

X 1 6 5 10 3 2 4 9 7 8

Y 6 4 9 8 1 2 3 10 5 7

¤ßÁ¸® C¸ }v£vPÎß AÇS ÷£õmiUPõÚ 10

÷£õmi¯õͺPÎß Á›ø\°¼¸¢x Á›ø\

öuõhº¤øÚ Psk¤i.

X 1 6 5 10 3 2 4 9 7 8

Y 6 4 9 8 1 2 3 10 5 7

14. (a) Calculate the Laspeyre’s Index : Types Price Quantity

2010 2014 2010 2014X 9 15 5 5 Y 4 12 10 11 Z 1 5 6 6

»õU줯º SÔ±mk GsønU Psk¤i.

ÁøP Âø» A»S

2010 2014 2010 2014X 9 15 5 5 Y 4 12 10 11 Z 1 5 6 6

Or

F–2420

5

Wk ser (b) Construct chain index numbers from the Link

relatives given below : Year 2010 2011 2012 2013 2014

Link Index 100 105 95 115 102

\[Q¼ öuõhº SÔ±mk Gs ‰»® Cøn¨¦ EÓÂøÚ

ÁiÁø©.

Bsk 2010 2011 2012 2013 2014

öuõhº¦ SÔ±k 100 105 95 115 102

15. (a) Calculate three yearly moving average of the following data :

Year 2005 2006 2007 2008 2009 2010 2011 2012

No.of students 15 16 17 20 23 25 29 33

‰ßÖ BskPÐUPõP \μõ\› |PºÂøÚ PnUQkP.

Bsk 2005 2006 2007 2008 2009 2010 2011 2012

©õnÁºPÎß

GsoUøP

15 16 17 20 23 25 29 33

Or

(b) State the components of time series.

÷|μz öuõhº¤ß TÖPøÍ TÖP.

Part C (3 10 = 30)

Answer any three questions.

16. Calculate the lower and upper quartiles from the following data :

Central Value 2.5 7.5 12.5 17.5 22.5

Frequency 7 18 25 30 20

F–2420

6

Wk ser ¤ßÁ¸® ÂÁμ[Pμ¸¢x RÌ÷©À PõÀ©õÚ[PøÍ

PnUQkP.

©zv¯ ©v¨¦ 2.5 7.5 12.5 17.5 22.5

AvºöÁs 7 18 25 30 20

17. Represent the following data. in a pie diagram. Items Expenditure (in Rupees)

Food 87

Clothing 24

Recreation 11

Education 13

Rent 25

Miscellaneous 20

ø£ Áøμ£hzøu ÁøμP.

ÁøPPÒ ö\»ÂÚ[PÒ (¹£õ°À)

EnÄ 87

xo 24

©Ú©QÌ 11

PÀÂ 13

ÁõhøP 25

£ÀÁøP 20

18. Find regression Lines by using assumed mean :

X 40 38 35 42 30

Y 30 28 25 35 18

P¸xÁx \μõ\› ‰»® ¤ßÚøhÄ Á›PøÍ Psk¤i.

X 40 38 35 42 30

Y 30 28 25 35 18

F–2420

7

Wk ser19. Calculate Index number using

(a) Paache’s method

(b) Laspeyre’s method Products P0 Q0 P1 Q1

A 12 100 20 120

B 4 200 4 240

C 8 120 12 150

D 20 60 24 50

SÔ±mk Gsøn

(A) £õa]ì •øÓ ©ØÖ®

(B) »õU줯º •øÓPÎÀ PnUQkP.

ö£õ¸ÒPÒ P0 Q0 P1 Q1

A 12 100 20 120

B 4 200 4 240

C 8 120 12 150

D 20 60 24 50

20. Calculate trend values by the method of least square from the data given below and estimate sales for 2016,

Year 2009 2010 2011 2012 2013

Sales 70 74 80 86 90

¤ßÁ¸® ÂÁμ[Pμ¸¢x 2016 ® BskUPõÚ ÂØ£øÚ

÷£õUS ©v¨¤øÚ SøÓ¢u \xμ •øÓ°À PnUQkP.

Âø» 2009 2010 2011 2012 2013

ÂØ£øÚ 70 74 80 86 90

_____________

Wk 4

F–2421

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Third Semester

Commerce

ADVANCED ACCOUNTANCY — III

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. Define ‘Partnership’.

Tmhõsø© Áøμ¯Ö.

2. What is fixed capital?

{ø» •uÀ GßÓõÀ GßÚ?

3. What is meant by ‘gaining ratio’?

Buõ¯ ÂQu® GßÓõÀ GßÚ?

4. Define ‘Goodwill’.

|Øö£¯º Áøμ¯Ö.

5. What is ‘Realisation account’?

wºÄU PnUSPÒ GßÓõÀ GßÚ?

6. What is meant by life insurance policy?

B²Ò Põ¨¥mk vmh® GßÓõÀ GßÚ?

Sub. Code 7BCO3C4

F–2421

2

Wk 47. What is ‘dissolution of partnership firm’?

Tmk £[S {ÖÁÚ Pø»¨¦ GßÓõÀ GßÚ?

8. What is meant by ‘insolvency’?

ö|õi¨¦ {ø» GßÓõÀ GßÚ?

9. What is ‘Purchase consideration’?

öPõÒ•uÀ ©Ö£¯ß GßÓõÀ GßÚ?

10. What is ‘Maximum Loss method’?

AvP£m\ CǨ¦ •øÓ GßÓõÀ GßÚ?

Section B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) ‘A’ and ‘B’ are partners in a firm ‘A’ draws Rs. 900

regularly in the middle of each month during the

year 2016. ‘B’ draws Rs. 5,400 at the end of each

half year. Calculate interest on their drawings at

5% p.a.

‘A’ ©ØÖ® ‘B’ C¸Á¸® J¸ {ÖÁÚzvß TmhõÎPÒ

‘A’ 2016&® BsiÀ JÆöÁõ¸ ©õu Cøh°¾®

öuõhº¢x ¹. 900 GkzxU öPõÒQÓõº. ‘B’ JÆöÁõ¸

Aøμ¯õsk CÖv°¾® ¹. 5,400 GkzxU öPõÒQÓõº.

BskUS 5% Gk¨¦PÒ «uõÚ Ámi PnUQhÄ®.

Or

F–2421

3

Wk 4 (b) Prepare fluctuating capital account of Babu and

Gopu from the following details. Babu Gopu

Capital on 1.1.16 8,00,000 7,00,000

Drawing during 2016 1,60,000 1,40,000

Interest on drawings 4,000 2,000

Share of profit for 2016 84,000 66,000

Interest on capital 48,000 42,000

Salary 72,000 Nil

RÌPõq® £μ[PøÍU öPõsk £õ¦ ©ØÖ® ÷Põ¦Âß

©õÖ£k® •uÀ PnUøP u¯õ›UPÄ®.

£õ¦ ÷Põ¦

•uÀ 1.1.16 8,00,000 7,00,000

Gk¨¦ 2016&À 1,60,000 1,40,000

Gk¨¦ «uõÚ Ámi 4,000 2,000

2016&® BsiØPõÚ »õ£ £[S 84,000 66,000

•uÀ «uõÚ Ámi 48,000 42,000

\®£Í® 72,000 Nil

12. (a) The goodwill is to be valued at 3 years purchase of last 5 years average profit. The profit were Rs. 9,600 Rs. 14,400, Rs. 20,000, Rs. 6,000 and Rs. 10,000. Find out the value of goodwill.

{ÖÁÚzvß |Øö£¯º Ph¢u 5 BskPÎß \μõ\›

C»õ£zvÀ 3 Bsk öPõÒ•uÀ GÚ

©v¨¤h¨£kQÓx. 5 BskPÎß C»õ£[PÒ •øÓ÷¯

¹. 9,600, ¹. 14,400, ¹. 20,000, ¹. 6,000 ©ØÖ®

¹. 10,000. |Øö£¯›ß ©v¨ø£ PnUQkP.

Or

F–2421

4

Wk 4 (b) ‘X’ and ‘Y’ are partners shared profit in the ratio of

7 : 3 partners ‘Z’ was admitted as a New partner ‘X’ surrendered 2/7th of his share and Y 1/7th of his share in favour of ‘Z’. Calculate new ratio.

‘X’ ©ØÖ® ‘Y’ GßÓ TmhõÎPÒ •øÓ÷¯ 7 : 3 GßÓ

ÂQuzvÀ C»õ£® £Qº¢x öPõÒQßÓÚº. AÁºPÒ ‘Z’ GßÓ ¦v¯ TmhõÎUS ‘X’ öPõkUS® £[S 2/7 ©ØÖ®

‘Y’ GߣÁº öPõkUS® £[S 1/7 BS®. AÁºPÐøh¯

ÂQu® GßÚ?

13. (a) Explain the various methods of treatment of goodwill.

|ß©v¨ø£U PnUSPÎÀ øP¯õÐÁuØPõÚ £À÷ÁÖ

•øÓPøÍ ÂÍUSP.

Or

(b) A, B, C, D and E were partners in a firm sharing profits and losses in the ratio of 5 : 4 : 3 : 2 : 1 respectively. Unfortunately D and E met with an accident in which both of them died.

The goodwill of the firm was valued at Rs. 75,000 and ‘A’ ‘B’ and ‘C’ decided to share the future profit and losses in the ratio of 4 : 6 : 5 respectively. Pass journal entries.

A, B, C, D ©ØÖ® E BQ¯ TmhõÎPÒ •øÓ÷¯

5 : 4 : 3 : 2 : 1 GßÓ ÂQuzvÀ C»õ£® £Qº¢x Á¢uÚº.

Gvº£õμõu Âu©õP D ©ØÖ® E J¸ £zvÀ

©μn©øh¢uÚº.

Tmhõsø©°ß |ß©v¨¦ ¹. 75,000 GÚ

©v¨¤h¨£kQÓx. ÷©¾® ‘A’ ‘B’ ©ØÖ® ‘C’ •øÓ÷¯

4 : 6 : 5 GßÓ ÂQuzvÀ GvºPõ» C»õ£ |mhzøu £Qμ

•iöÁkzuÚº. SÔ¨÷£mk¨ £vÄPøÍ u¸P.

F–2421

5

Wk 414. (a) Explain the rule of Garner vs Murray.

PõºÚº öÁì •÷μ ÂvPøÍ ÂÁ›.

Or

(b) ‘A’ ‘B’ and ‘C’ are partners, their balance sheet as on 31.12.2016.

Liabilities Rs. Assets Rs. Capital a/c : Land and buildings 5,500A 4,000 Stock in trade 2,000B 2,000 Debtors 1,000C 500 Cash in hand 1,500Creditors 3,500 10,000 10,000

They decided to dissolve partnership on the above date. ‘A’ agrees to take over the stock at a valuation of Rs. 1,500 and the debtors at a valuation of Rs. 700 the land and building is sold at Rs. 2,700, prepare realisation account.

31.12.2016 AßÖ •iÁøh²® ‘A’ ‘B’ ©ØÖ® ‘C’ C¸¨¦ {ø» SÔ¨¦ R÷Ç öPõkUP¨£mkÒÍx.

ö£õÖ¨¦PÒ ¹ ö\õzxUPÒ ¹.

•uÀ PnUS {»® ©ØÖ® Pmih® 5,500A 4,000 \μUQ¸¨¦ 2,000B 2,000 PhÚõÎPÒ 1,000C 500 öμõUP øP°¸¨¦ 1,500PhÜ¢÷uõº 3,500 10,000 10,000

÷©ØSÔ¨¤mh |õÎÀ AÁºPÒ Tmhõsø© Pø»UP

•iÁkzuÚº. ‘A’ GßÓ TmhõÎ \μUQ¸¨ø£ ¹. 1,500

©v¨¤ØS® ©ØÖ® PhÚõÎPøÍ ¹. 700 ©v¨¤ØS®

GkUP •iöÁkzuÚº. {»® ©ØÖ® Pmih®

¹. 2,700US ÂØP¨£kQÓx, wºÄ PnUS u¯õ›UPÄ®.

F–2421

6

Wk 415. (a) Explain the methods of calculation of purchase

consideration.

öPõÒ•uÀ ©Ö£¯øÚ PnUQk® •øÓPøÍ ÂÁ›.

Or

(b) A, B, C share profits in the ratio of 4 : 3 : 2. They have decided to sell their firm to a limited company on June 30th 2016, their balance sheet on that date.

Liabilities Rs. Assets Rs.

Creditors 12,000 Machinery 30,000

Capital : Debtors 15,000

A 20,000 Stock 13,000

B 15,000 Cash 2,000

C 13,000

60,000 60,000

Purchase consideration agreed upon was Rs. 50,000 of this the company has paid Rs. 32,000 in its own shares and the balance in cash. Dissolution expenses of the firm Rs. 600 was paid by the company. Prepare realisation a/c.

A, B ©ØÖ® C GßÓ TmhõÎPÒ •øÓ÷¯ 4 : 3 : 2 GßÓ

ÂQuzvÀ C»õ£zøu £Qº¢x Á¢uÚº. AÁºPÒ

Tmhõsø©ø¯ Áøμ¯ÖUP¨£mh {Ö©zvØS 30

áüß 2016 AßÖ GÚ •iöÁkzuÚº. AßøÓ¯

C¸¨¦ {ø»U SÔ¨¦. ö£õÖ¨¦PÒ ¹. ö\õzxUPÒ ¹.

PhÜ¢÷uõº 12,000 C¯¢vμ® 30,000

•uÀ : PhÚõÎPÒ 15,000

A 20,000 \μUQ¸¨¦ 13,000

B 15,000 öμõUP® 2,000

C 13,000

60,000 60,000

F–2421

7

Wk 4 öPõÒ•uÀ ©Ö£¯ÚõP ¹. 50,000 HØÖU

öPõÒͨ£mhx. AvÀ uÚx ö\õ¢u £[SPøÍ

¹. 32,000 ©v¨¤¾® «uz öuõøP°øÚ öμõUP©õPÄ®

{Ö©® ö\¾zv¯x. {ÖÁÚ Pø»¨¦a ö\»Ä ¹. 600 I

A¢{Ö©® ö\¾zv¯x.

Tmhõsø© {ÖÁÚzvß wºÄ C»õ£zvøÚ

PnUQkP.

Part C (3 10 = 30)

Answer any three questions.

16. On 31st Dec 2016, after close of the account, the capital account of A, B and C stood in the books of the firm at Rs. 80,000, Rs. 60,000, Rs. 40,000 respectively. It was subsequently discovered that interest at 5% on partners capital as at the beginning of the year and interest on drawing of partners were not considered. The interest on drawing of ‘A’ ‘B’ and ‘C’ stood as Rs. 500, Rs. 360 and Rs. 200 respectively. The profit for the year in arriving at the above figures of capital amounted to Rs. 1,20,000 and partners drawings had been ‘A’ Rs. 20,000, ‘B’ Rs. 15,000 and ‘C’ Rs. 9,000. The partners shared profit and losses in the ratio of 3 : 2 : 1 pass necessary journal entries.

i\®£º 31, 2016À PnUøP •izu ¤ß ‘A’ ‘B’ ©ØÖ® ‘C’ ß

•uÀ •øÓ÷¯ ¹. 80,000, ¹. 60,000 ©ØÖ® ¹. 40,000 BS®.

¤ßÚº Psk¤izuÀ B쮣 •uÀ «uõÚ Ámi 5% ©ØÖ®

Gk¨¦ «uõÚ Ámi. ‘A’ ‘B’ ©ØÖ® ‘C’ •øÓ÷¯ ¹. 500, ¹. 360

©ØÖ® ¹. 200 BS®. A¢u Bsiß C»õ£® ÷©ØTÔ¯ •uÀ

PnUQk® ö£õÊx ¹. 1,20,000 BS®. ©ØÖ® TmhõÎPÒ

A, B ©ØÖ® Cß Gk¨¦ •øÓ÷¯ ¹. 20,000, ¹. 15,000 ©ØÖ®

¹. 90,000 BS®. TmhõÎPÒ C»õ£ |mhzøu 3 : 2 : 1 GßÓ

ÂQuzvÀ £Qº¢x Á¸QßÓÚº. ÷uøÁ¯õÚ SÔ¨÷£mk¨

£vÄPøÍ u¸P.

F–2421

8

Wk 417. ‘A’ and ‘B’ are partner sharing profit in proportion to

capital their balance sheet as on 31st March 2017 is as under

Liabilities Rs. Assets Rs.

Sundry creditors 60,000 Bank 12,000

Bills payable 40,000 Debtors 40,000

Capital accounts : Stock 40,000

A 60,000 Building 90,000

B 40,000 Furniture 18,000

2,00,000 2,00,000

They decided to admit ‘C’ into partnership with effect from 1st April 2017 on the following terms.

(a) ‘C’ share bring in a capital of Rs 50,000 for 1/5th share of profits.

(b) Goodwill is to be valued at Rs. 40,000

(c) Building and furniture was to be depreciated by 5%

(d) Provision for doubtful debts credited at 1 21 % on

Sunday debtors.

Show revaluation a/c, capital a/c and balance sheet of the reconstructed partnership.

‘A’, ‘B’ GßÓ TmhõÎPÒ •øÓ÷¯ •uÀ ÂQuzvÀ C»õ£®

£Qº¢x Á¸QßÓÚº. AÁºPÒ 31.3.2017® |õøͯ C¸¨¦

{ø»U SÔ¨¦ ¤ßÁ¸©õÖ.

ö£õÖ¨¦PÒ ¹. ö\õzxPÒ ¹.

£Ø£» PhÜ¢÷uõº 60,000 Á[Q 12,000

ö\¾zuØS›¯ ©õØÖ ^mk 40,000 PhÚõÎPÒ 40,000

•uÀ PnUSPÒ : \μUQ¸¨¦ 40,000

A 60,000 Pmih® 90,000

B 40,000 AøÓP»ß 18,000

2,00,000 2,00,000

F–2421

9

Wk 4 AÁºPÒ ¤ßÁ¸® CÚ[PøÍU P¸zvÀ öPõsk ‘C’

GߣÁøμ 2017 H¨μÀ 1. AßÖ Tmhõsø©°À ÷\ºzxU

öPõÒÍ •iÄ GkzuÚº.

(A) ‘C’ uß 1/5 £[SUS ¹. 50,000 •uÀ öPõsk Á¸Áx

(B) |Øö£¯º ¹. 40,000 GÚ ©v¨¤kÁx

(C) Pmih® ©ØÖ® AøÓP»ß «x 5% ÷u´©õÚ® }USÁx

(D) £Ø£» PhÚõÎPÒ «x 1 21 % ÁμõUPhß JxUS

E¸ÁõUSP.

©Ö©v¨¥mkU PnUS, •uÀ PnUSPÒ ©ØÖ® C¸¨¦

{ø»U SÔ¨¦ u¯õº ö\´P.

18. M, N and O are partners of a firm sharing profit bases in the ratio of 6 : 2 : 2 their balance sheet as on 30.06.2016.

Liabilities Rs. Assets Rs.

Sundry creditors 8,000 Cash in hand 3,000

Reserve fund 30,000 Cash at bank 5,000

Capital a/c : Debtors 45,000

M 70,000 Stock 35,000

N 50,000 Machinery 30,000

O 30,000 Building 70,000

1,88,000 1,88,000

On that date ‘O’ retires from the business. It is agreed to adjust the value of the assets as follows :

(a) To provide a reserve of 5% on Sundry debtors

(b) Depreciate stock by 5% and machinery by 10%

(c) Building to be revalued at Rs. 75,000.

Prepare revaluation a/c, capital a/c and balance sheet.

F–2421

10

Wk 4 M, N ©ØÖ® O GßÓ TmhõÎPÒ 6 : 2 : 2 GÝ® ÂQuzvÀ

C»õ£ |mh[PÒ £Qº¢x AÁºPÐøh¯ 30.6.2016® |õøͯ

C¸¨¦ {ø»U SÔ¨¦ ¤ßÁ¸©õÖ :

ö£õÖ¨¦PÒ ¹. ö\õzxPÒ ¹.

£Ø£» PhÜ¢÷uõº 8,000 øP°¸¨¦ öμõUP® 3,000

Põ¨¦ {v 30,000 Á[Q°¸¨¦ öμõUP® 5,000

•uÀ : PhÚõÎPÒ 45,000

M 70,000 \μUQ¸¨¦ 35,000

N 50,000 C¯¢vμ® 30,000

O 30,000 Pmih® 70,000

1,88,000 1,88,000

¤ßÁ¸® £QºÄPÐUS Ehß £mk {ÖÁÚzv¼¸¢x ‘O’ »QÚõº.

(A) £Ø£» PhÚõÎPÒ «x 5% JxUS E¸ÁõUSP.

(B) \μUQ¸¨¦ «x 5% C¯¢vμzvß «x 10% ÷u´©õÚ®

}USP.

(C) Pmihzvß ©v¨¦ ¹. 75,000 BP ©v¨¤kP.

©Ö©v¨¥mk P/S, •uÀ P/S ©ØÖ® C¸¨¦{ø»

SÔ¨¦ u¯õº ö\´P.

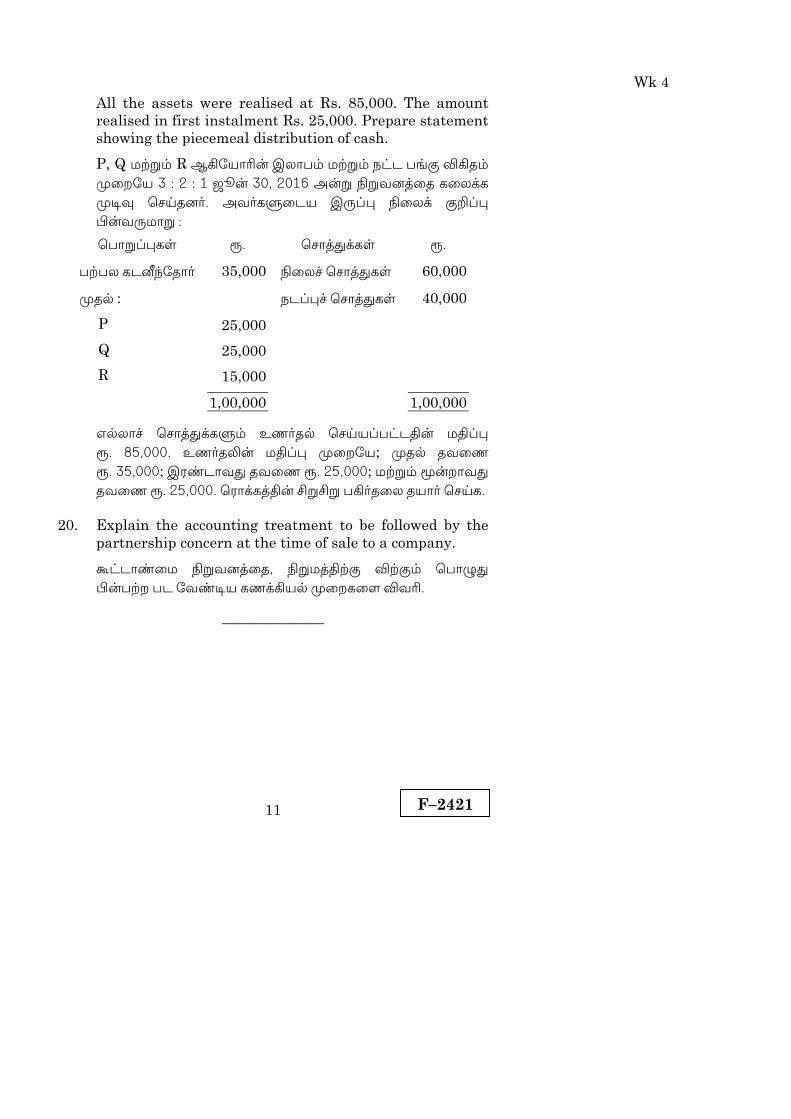

19. P, Q and R were partners sharing profit and losses in the ratio of 3 : 2 : 1 respectively. They decided to dissolve the firm on 30th June 2016. Their balance sheet as on that date was as under

Liabilities Rs. Assets Rs.

Sundry creditors 35,000 Fixed assets 60,000

Capital : Current assets 40,000

P 25,000

Q 25,000

R 15,000

1,00,000 1,00,000

F–2421

11

Wk 4 All the assets were realised at Rs. 85,000. The amount

realised in first instalment Rs. 25,000. Prepare statement showing the piecemeal distribution of cash.

P, Q ©ØÖ® R BQ÷¯õ›ß C»õ£® ©ØÖ® |mh £[S ÂQu®

•øÓ÷¯ 3 : 2 : 1 áüß 30, 2016 AßÖ {ÖÁÚzøu Pø»UP

•iÄ ö\´uÚº. AÁºPÐøh¯ C¸¨¦ {ø»U SÔ¨¦

¤ßÁ¸©õÖ :

ö£õÖ¨¦PÒ ¹. ö\õzxUPÒ ¹.

£Ø£» PhÜ¢÷uõº 35,000 {ø»a ö\õzxPÒ 60,000

•uÀ : |h¨¦a ö\õzxPÒ 40,000

P 25,000

Q 25,000

R 15,000

1,00,000 1,00,000

GÀ»õa ö\õzxUPЮ EnºuÀ ö\´¯¨£mhvß ©v¨¦

¹. 85,000. Enºu¼ß ©v¨¦ •øÓ÷¯; •uÀ uÁøn

¹. 35,000; CμshõÁx uÁøn ¹. 25,000; ©ØÖ® ‰ßÓõÁx

uÁøn ¹. 25,000. öμõUPzvß ]Ö]Ö £Qºuø» u¯õº ö\´P.

20. Explain the accounting treatment to be followed by the partnership concern at the time of sale to a company.

Tmhõsø© {ÖÁÚzøu, {Ö©zvØS ÂØS® ö£õÊx

¤ß£ØÓ £h ÷Ási¯ PnUQ¯À •øÓPøÍ ÂÁ›.

———————

wk 10

F–2422

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Fourth Semester

Commerce

PRINCIPLES OF MANAGEMENT

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. Define the term management.

÷©»õsø©°øÚ Áøμ¯ÖUP.

2. Who is the father of scientific management?

AÔ¯À ÷©»õsø©°ß u¢øu GߣÁº ¯õº?

3. State the definition of planning.

vmhªh¼øÚ Áøμ¯ÖUP.

4. What do you know about decision-making?

•iöÁkzuÀ £ØÔ }º AÔÁx ¯õx?

5. State the meaning of decentralization of authority.

AvPõμzøu ›ģkzxÁuØPõÚ ö£õ¸Ò u¸P.

6. What do you know about performance appraisal?

ö\¯ÀvÓß ©v¨¥k £ØÔ }º AÔÁx ¯õx?

Sub. Code 7BCO4C1

F–2422

2

Wk 107. Define communication.

uPÁÀ öuõhº¤øÚ Áøμ¯ÖUP.

8. What is meant by motivation?

FUP‰mhÀ GßÓõÀ GßÚ?

9. What do you know about controlling?

Pmk¨£kzxuÀ £ØÔ }º AÔÁx ¯õx?

10. What is meant by span of control?

Pmk¨£õmk vÓ® GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Elucidate the functions of management.

÷©»õsø© ö\¯À£õkPøÍ öuÎÄ£kzxP.

Or

(b) Trace the evolution of management thought.

÷©»õsø© ]¢uøÚ°ß £›nõ©zøu ÁøμP.

12. (a) Demonstrate the importance of planning.

vmhªh¼ß •UQ¯zxÁzøu {¹¤.

Or

(b) Categorize the steps in planning.

vmhªh¼ß £i{ø»PøÍ ÁøP¨£kzxP.

13. (a) Describe the factors governing the span of management.

÷©»õsø© vÓÛøÚ BЮ PõμoPøÍ _¸UP©õP

ÂÁ›.

Or

F–2422

3

Wk 10 (b) Briefly explain the objectives of organizing.

J¸[Qønzu¼ß ÷|õUP[PøÍ _¸UP©õP ÂÁ›.

14. (a) Clarify the principles of effective communication.

£¯ÝÒÍ uPÁÀ öuõhº¤ß öPõÒøPPøÍ

öuÎÄ£kzxP.

Or

(b) Enumerate the barriers of communication.

uPÁÀöuõhº¤À HØ£k® uøhPøÍ _¸UP©õP ÂÁ›.

15. (a) Generalize the significance of controlling.

Pmk¨£kzu¼ß •UQ¯zxÁzøu ö£õxø©¨£kzxP.

Or

(b) Indicate the techniques of controlling in management.

{ºÁõPzvÀ Pmk¨£kzx® ~m£[PøÍU SÔ¨¤kP.

Part C (3 10 = 30)

Answer any three questions.

16. Who proposed the four principles of scientific management? Discuss in detail.

ÂgbõÚ §ºÁ ÷©»õsø©°ß |õßS öPõÒøPPøÍ

•ßøÁzuÁº ¯õº? ›ÁõP ÂÁõvUPÄ®.

17. Illustrate the guidelines for effective planning.

£¯ÝÒÍ vmhªh¼ß ÁÈPõmkuÀPøÍ ÂÍUSP.

18. Critically examine the essential steps involved in the process of staffing.

£o¯©ºzuÀ £o°À Dk£mkÒÍ Azv¯õÁ]¯

|hÁiUøPPøÍ wÂμ©õP Bμõ´P.

F–2422

4

Wk 1019. Infer a logical conclusion about Herzberg’s two factors

theory.

öíºìö£ºUQß Cμsk PõμoPÒ ÷Põm£õk £ØÔ uºUP

Ÿv¯õÚ •iøÁU PõsP.

20. Interpret the steps involved in control process.

Pmk¨£õmk ÁÈ•øÓPÎÀ EÒÍ £iPÒ SÔzx ÂÍUPÄ®.

——————

WK11

F–2423

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Fourth Semester

Commerce

BANKING LAW AND PRACTICE

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. Define the term banking.

Á[Q°¯À SÔzu Áøμ»UPÚ® u¸P.

2. Who are called as customer?

ÁõiUøP¯õͺ GߣÁº ¯õº?

3. What is a garnishee order in banking?

Á[Q°À øP¯P¨£kzx® EzuμÄ GßÓõÀ GßÚ?

4. Who are called as special types of customers?

]Ó¨¦ ÁõiUøP¯õͺPÍõP ¯õº AøÇUP¨£kQÓõºPÒ?

5. What do you know about crossing of a cheque?

Põ÷\õø»°À Rμ¼hÀ £ØÔ }º AÔÁx ¯õx?

6. What is the meaning of material alteration in a cheque?

J¸ Põ÷\õø»°À ö£õ¸Ò ©õØÔ¯ø©¨¤ß ö£õ¸Ò GßÚ?

Sub. Code 7BCO4C2

F–2423

2

WK117. What is meant by endorsement?

J¨¦uÀ ‰»® GßÓõÀ GßÚ?

8. What do you know about paying banker?

ö\¾zx® Á[Q¯õÍøμ £ØÔ }º AÔÁx ¯õx?

9. What is meant by FDR?

FDR GßÓõÀ GßÚ?

10. What is meant by letter of credit?

Phß Piu® GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Critique the rights of a banker.

J¸ Á[Q¯õÍ›ß E›ø©PøÍ öuÎÄ£kzuÄ®.

Or

(b) What is the rule in Clayton’s Case? Explain in brief.

U÷ÍhÛß ÁÇUQß ÂvPÒ GßÚ? _¸UP©õP

ÂÍUSP.

12. (a) Express about fixed deposit receipt and state its legal implications.

{ø»¯õÚ øÁ¨¦ μ^x £ØÔ öÁΨ£kzuÄ® ©ØÖ®

Auß \mhŸv¯õÚ uõUP[PøÍU SÔ¨¤hÄ®.

Or

(b) Describe the perspectives related to effects of wrong entries.

uÁÓõÚ EÒÏkPÎß ÂøÍÄPÒ öuõhº£õÚ

•ß÷ÚõUSPøÍ ÂÁ›.

F–2423

3

WK1113. (a) Distinguish between Cheque Vs Bill of Exchange.

Põ÷\õø» ©ØÖ® ©õØÖa^mk CÁØÔß ÷ÁÖ£õmiøÚ

ÂÁ›.

Or

(b) Outline the types and significance of crossing.

Rμ¼h¼ß ÁøPPÒ ©ØÖ® •UQ¯zxÁzøu

öÁΨ£kzxP.

14. (a) Elucidate the consequences of wrongful dishonour of cheques.

Põ÷\õø»°ß uÁÓõÚ AÁ©v¨¤ß ÂøÍÄPøÍ

öuÎÄ£kzxP.

Or

(b) Briefly explain the various kinds of endorsement.

£» ÁøP¯õÚ J¨¦uÀ ‰»zvøÚ _¸UP©õ ÂÁ›.

15. (a) State the concept of negligence.

¦ÓUPo¨¦ GßÓ P¸zvøÚ öuÎÄ£kzxP.

Or

(b) List the features of traveller’s cheque.

£¯oPÐUPõÚ Põ÷\õø»°ß A®\[PøÍ

£mi¯¼kP.

Part C (3 10 = 30)

Answer any three questions.

16. Clarify the relationship between a banker and a customer.

Á[Q¯õͺ ©ØÖ® ÁõiUøP¯õͺ BQ÷¯õº Cøh÷¯ EÒÍ

EÓÄPøÍ öuÎÄ£kzxP.

F–2423

4

WK1117. Critically examine the general procedure for opening and

closing an account.

Á[QU PnUøPz xÁ[Q ©ØÖ® ‰kÁuØPõÚ ö£õx

ÁÈ•øÓPøÍ wÂμ©õP Bμõ´P.

18. Discuss the consequences of drawing up of a cheque without sufficient balance.

÷£õx©õÚ C¸¨¦ CÀ»õ©À J¸ Põ÷\õø» Áøμu¼ß

ÂøÍÄPøÍ £ØÔ ÂÁõv.

19. Clearly explain the circumstances for dishonour of cheques.

Põ÷\õø»PøÍ AÁ©vUS® `Ì{ø»PøÍ öuÎÄ£kzxP.

20. Discuss the statutory protection regarding collecting banker.

Á`À Á[Q¯›ß \mhŸv¯õÚ £õxPõ¨ø£ £ØÔ ÂÁõv.

————————

Wk 4

F–2424

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Fourth Semester

Commerce

BUSINESS MATHEMATICS

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Section A (10 2 = 20)

Answer all questions.

1. Find the simple interest on Rs. 5,000 at 10% for 3 years.

¹. 5,000&ØS 10% Ámi ÃuzvÀ 3 Á¸hzvØPõÚ uÛ

Ámiø¯ PnUQkP.

2. Write the two kinds of bill.

μ^vß Cμsk ÁøPPøÍ GÊxP.

3. Write the product and quotient rules in logarithm.

©hUøP°ß ö£¸UPÀ ©ØÖ® ÁSzuÀ Âvø¯ GÊxP.

4. Find m if 3log3 m .

3log3 m GÛÀ m &ß ©v¨¤øÚ PõsP.

Sub. Code 7BCO4C3

F–2424

2

Wk 45. State Demorgan’s law.

j©õºPß Âv°øÚ GÊxP.

6. If A = [1,2,3] and B = [1,3,5] then find BA .

A = [1,2,3] ©ØÖ® B = [1,3,5] GÛÀ BA ø¯ PõsP.

7. Write about Bayes Theorem.

÷£´ì ÷uØÓzvøÚ GÊxP.

8. A perfect die is rolled twice. Find the probability of getting a total of 9.

C¸ £PøhPÒ Ã\¨£k®÷£õx TkuÀ 9 Qøh¨£uØPõÚ

{PÌuPÄ ¯õx?

9. State any two properties of normal distribution.

C¯À{ø»¨ £μÁ¼À H÷uÝ® C¸ £s¦PøÍU TÖP.

10. Write the formula for finding binomial distribution.

D¸Ö¨¦ £μÁ¼ß \μõ\›UPõÚ `zvμzøu GÊxP.

Section B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Compute the interest on Rs. 1000 for 10 years at 4% per annum the interest being paid annually.

J¸ Á¸hzvØPõÚ 4% Ámi ÂQuzvÀ ¹£õ´

1000zvØS 10 Á¸hzvØPõÚ Ámi°øÚ PõsP.

Or

F–2424

3

Wk 4 (b) Find the term of a bill of Rs. 18,450 whose true

discount at 5% per annum is Rs. 450.

¹. 18,450 öuõøP öPõsh ¤À¼ß J¸ Á¸hzvØPõÚ

Esø© uÒУi 5% Ãu® 450 GÛÀ Auß

Esø©¯õÚ öuõøPø¯ PnUQkP.

12. (a) Prove that 0logloglog 5546

6569

2633 .

0logloglog 5546

6569

2633 GÚ {¹¤.

Or

(b) If ,/log/log)/(log bczacycbx show that

1xyz .

bczacycbx /log/log)/(log GÛÀ, 1xyz

GÚ {¹¤.

13. (a) Using Venn diagram prove that )()()( CABACBA .

öÁs£hzvøÚ £¯ß£kzv

)()()( CABACBA GÚ {¹¤.

Or

(b) Given U = [1, 2, 3, 4, 5, 6, 7], A [1, 2, 3, 4, 5] B = [1, 3, 5, 7], C = [2, 5, 6, 7], Find.

(i) CA

(ii) AB

(iii) BC

(iv) AC

(v) BA

F–2424

4

Wk 4 U = [1, 2, 3, 4, 5, 6, 7], A [1, 2, 3, 4, 5]

B = [1, 3, 5, 7], C = [2, 5, 6, 7] BQ¯øÁ

öPõkUP¨£mkÒÍ CÁØÔØS

(i) CA

(ii) AB

(iii) BC

(iv) AC

(v) BA BQ¯ÁØøÓU PõsP.

14. (a) State and prove addition theorem of probability.

{PÌuPÂØPõÚ TmhÀ – ÷uØÓzvøÚ TÔ {ÖÄP.

Or

(b) The probability of success of an event is P and that of failure is q. Find the expected number of trials to get a success.

J¸ {PÌa]°ß öÁØÔUPõÚ {PÌuPÄ P Auß

÷uõÀÂUPõÚ {PÌuPÄ q GÚ C¸¢uõÀ öÁØÔ

AøhÁuØPõÚ •¯Ø]PÎß GsoUøP°ß

Gvº£õºzuÀ GßÚ?

15. (a) Obtain the mode of normal distribution.

C¯À{ø»¨ £μÁ¼ß •PmøhU PõsP.

Or

(b) Find the mean and standard deviation of a Binomial distribution.

D¸Ö¨¦ £μÁ¼ß \μõ\› ©ØÖ® vmh »UQøÚ

PõsP.

F–2424

5

Wk 4 Part C (3 10 = 30)

Answer any three questions.

16. The simple interest on a certain principal for 5 years is

Rs. 360 and the interest is 9/25 of the Principal. Find the

principal and the interest rate.

SÔ¨¤mh öuõøP°ß 5 Á¸hzvØPõÚ uÛ Ámi 360 ©ØÖ®

Ámi¯õÚx 9/25 À A\À öuõøP GÛÀ A\À öuõøPø¯²®,

Ámi ÂQuzøu²® PõsP.

17. If bcax log1 , ,log1 ca

ay abcz log1 show that

1/1/1/1 zyx .

bcax log1 , ,log1 ca

ay abcz log1 GÛÀ

1/1/1/1 zyx GÚ {¹¤.

18. In a survey of 5000 persons, it was found that 2800 read

Indian express and 2,300 read Statesman while 400 read

both papers. How many read neither Indian Express nor

statesman.

5000 ©ÛuºPøÍ PnUöPkzu÷£õx 2800 ÷£º C¢v¯ß

GUì¤μì ö\´vuõЮ, 2300 ÷£º ì÷hm÷©ß

ö\´vuõЮ, 400 ÷£º Cμsk uõÒPøͲ® £iUQÓõºPÒ.

C¢v¯ß GUì¤μì ©ØÖ® ì÷hm÷©ß ö\´vuõÒ

CμsiøÚ²® £iUPõuÁºPÎß GsoUøP GzuøÚ?

19. State and prove Baye’s theorem.

÷£°ì ÷uØÓzøu TÔ ÂÍUSP.

F–2424

6

Wk 420. Write down any five properties of normal distribution and

find the mode of the normal distributions.

C¯À {ø» £μÁ¼ß £¯ß£õkPÒ I¢vøÚ GÊxP. ©ØÖ®

C¯À{ø»¨ £μÁ¼ß •PmiøÚ PõsP.

———————

Sp6

F–2425

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Fourth Semester

Commerce

ADVANCED ACCOUNTANCY – IV

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. What is meant by contract account?

J¨£¢u PnUS GßÓõÀ GßÚ?

2. What do you know about notional profit?

¦»ÚõPõ »õ£® £ØÔ }º AÔÁx ¯õx?

3. What is meant by royalties?

Buõ¯ E›ø©PÒ GßÓõÀ GßÚ?

4. What do you know about lease?

SzuøP £ØÔ }º AÔÁx ¯õx?

5. What is meant by hire purchase?

ÁõhøP öPõÒ•uÀ GßÓõÀ GßÚ?

6. What is meant by re-possession?

©Ö Á\® GßÓõÀ GßÚ?

Sub. Code 7BCO4C4

F – 2425

2

Sp6 7. What do you know about insolvency?

ö|õi¨¦ {ø» £ØÔ }º AÔÁx ¯õx?

8. What is meant by deficiency account?

£ØÓUSøÓ PnUS GßÓõÀ GßÚ?

9. What is meant by departmental accounting?

xøÓÁõ› PnUQ¯À GßÓõÀ GßÚ?

10. What is meant by branch accounting?

QøÍU PnUQ¯À GßÓõÀ GßÚ?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Contract price – Rs. 10,00,000

Work certified – Rs. 5,00,000

Notional Profit – Rs. 2,40,000

Cash received is 80% of work certified

Calculate the amount to be transferred to the profit and loss account.

J¨£¢u Âø» – ¹.10,00,000

\õßÓÎUP¨£mh ÷Áø» – ¹. 5,00,000

¦»ÚõPõ C»õ£® – ¹.2,40,000

80% \õßÓÎUP¨£mh ÷Áø»US öuõøP ö£Ó¨£mhx.

C»õ£ |mh PnUQÀ Põmh¨£h ÷Ási¯ öuõøPø¯

PõsP.

Or

(b) Clarify the features of notional profit.

¦»ÚõPõ »õ£zvß C¯À¦PøÍ öuÎĨ£kzxP.

F – 2425

3

Sp6 12. (a) On 1st January 2011, the Gudur Mines leased some

land for a minimum rent of Rs. 3,000 for the first year, Rs. 5,000 in the second years and thereafter Rs. 10,000 per annum merging into a royalty of 50 paise per ton with power to recoup Short working over two years after occurring of short workings. The outputs were as follows:

2011 – 3,000 tons

2012 – 8,600 tons

2013 – 22,000 tons

2014 – 50,000 tons

Show how the accounts would appear in the books of the Gudur Mines.

áÚÁ› 1, 2011 AßÖ “Skº” _μ[P® SøÓ¢u AÍÄ

ÁõhøP¯õP •uÀ BsiØS ¹.3,000. Cμshõ®

BsiØS ¹.5,000 ÷©¾® Auß ¤ÓS BsiØS

¹.10,000 GÚÄ® Aøu Põ¨¦›ø©z öuõøP²hß J¸

hßÛØS 50 ø£\õ GÚ Cønzx ö£Ö©õÖ SzuøPUS

J¨¦U öPõskÒÍx. ÷©¾® {øÓÄö£Óõu ÷Áø»ø¯

Cμsk BsiØS¨¤ß ö£Ö©õÖ® J¨¦U

öPõÒͨ£mhx :

EØ£zv ¤ßÁ¸©õÖ :

2011 – 3,000 hßPÒ

2012 – 8,600 hßPÒ

2013 – 22,000 hßPÒ

2014 – 50,000 hßPÒ

Skº _μ[P PnUS HkPÎÀ Cx GÆÁõÖ ÷uõßÖ®

Gߣøu PshÔP.

Or

F – 2425

4

Sp6 (b) A Company had two departments A and B.

A department supplies the goods to B department at its usual Selling price. From the following figures prepare departmental Trading Profit and loss account for the year 2016.

A B

(Rs.) (Rs.)

Opening stock 1.1.2016 30,000 –

Purchases 2,10,000 –

Transfer to B 50,000 50,000

Sales 2,00,000 60,000

Closing stock (31.12.2016) 40,000 10,000

J¸ {ÖÁÚzvÀ A, B GßÝ® Cμsk xøÓPÒ

C¸UQßÓÚ. B xøÓUS ÷Ási¯øu xøÓ A

AuÝøh¯ ÂØ£øÚ Âø»°À u¸QÓx. RÌPsh

£μ[Pμ¸¢x 2016 ® BskUPõÚ xøÓÁõ›

¯õ£õμ C»õ£ |èh PnUSPøÍ u¯õ›UPÄ®.

A B

(¹.) (¹.)

B쮣 \μUQ¸¨¦ 1.1.2016 30,000 –

öPõÒ•uÀ 2,10,000 –

B US ©õØÓ¨£mh \μUS 50,000 50,000

ÂØ£øÚ 2,00,000 60,000

CÖva \μUS (31.12.2016) 40,000 10,000

F – 2425

5

Sp6 13. (a) X Ltd. had purchased a machinery on hire purchase

system from Y Ltd. The terms are that X Ltd. would pay Rs. 20,000 down on signing the agreement and annual instalments of Rs, 11,000 each commencing from the beginning of the next year. X Ltd. charged depreciation at 10% per annum under diminishing balance system. Y Ltd. charged interest at 10% per annum, Prepare machinery account and Y Ltd. a/c in the books of X Ltd.

X {ÖÁÚ® Y {ÖÁÚzvhª¸¢x ÁõhøPU öPõÒ•uÀ

•øÓ°À J¸ C¯¢vμzøu öPõÒ•uÀ ö\´ux.

X {ÖÁÚ® J¨£¢uzvÀ øPö¯õ¨£ªk® ÷£õx

¹.20,000 •uÀ öuõøP¯õPÄ® «v öuõøPø¯

¹.11,000 Ãu® Akzu Bsk B쮣® •uÀ

uμ÷Áskö©Ú {£¢uøÚ EÒÍx. BsiØS 10%

SøÓ¢xö\À C¸¨¦ •øÓ ÷u´©õÚzøu X {Ö©®

_©zxQÓx. BsiØS 10% Ámiø¯ Y {ÖÁÚ®

_©zxQÓx. X {ÖÁÚ HkPÎÀ

Y {ÖÁÚ PnUøP²® ÷©¾® C¯¢vμU PnUøP²®

u¯õº ö\´P.

Or

(b) Describe the nature of hire purchase accounts.

ÁõhøP öPõÒ•uÀ PnUQß C¯À¤øÚ _¸UP©õP

ÂÁ›.

14. (a) What is the need for insolvency accounting? Explain in brief.

ö|õi¨¦ {ø» PnUQ¯¼ß ÷uøÁ ¯õx? _¸UP©õP

ÂÁ›.

Or

F – 2425

6

Sp6 (b) The assets of Ramaswamy of Bombay on 31.6.2000

as shown by his books were Rs. 28,000 and his liabilities Rs. 22,000. He estimated his deficiency Rs. 15,000. He found the following were not taken into account.

(i) Interest at 6% on his capital from 1.1 .2000.

(ii) A contingent liability of Rs. 1,250 on bills discounted by his for Rs. 5,000.

(iii) Amount due as wages Rs. 300, Rent Rs. 100, Taxes – Rs. 150. Prepare statement of affairs and deficiency account.

v¸ £®£õ´ Cμõ©\õª°ß ö\õzxUPÒ, ö£õÖ¨¦PÒ

31.6.2000 ß £i •øÓ÷¯ ¹.28,000, ¹. 22,000, AÁº

PnUQߣi £ØÓõUSøÓ ¹.15,000 ¤ÓS

RÌPshøÁPøÍ PnUQÀ GkzxUöPõÒÍÂÀø»

GßÖ AÔ¢uõÀ.

(i) •uÀ «x Ámi 6% (1.1.2000 ¼¸¢x)

(ii) {a\¯©ØÓ ö£õÖ¨¦ ¹.1,250, Ámhg ö\´u

Esi¯¼ß «x ¹.5,000.

(iii) öPõk£h ÷Ási¯øÁ T¼ ¹.300, ÁõhøP

¹. 100, Á› ¹.150, {ø» AÔUøP¯²®

£ØÓõUSøÓ PnUøP²® u¯õº ö\´P.

15. (a) The Bombay Textiles Ltd. Opened a branch at Delhi on 1st April, 2013.

From the following particulars, prepare all the accounts effected for 2013 – 2014 and 2014 – 2015 in the books of the head office :

F – 2425

7

Sp6 2013 – 2014 2014 – 15 (Rs.) (Rs.)

Goods sent to Delhi 45,000 1,35,000Cash sent to Branch for : Rent 6,000 6,000 Salaries 4,800 6,800Other Expenses 2,000 3,000Cash received from Branch 70,000 1,60,000Stock on 31st March 7,000 26,000Petty cash in hand on 31st March 120 260

£®£õ´ {ÖÁÚ® 1.4.2013 öhÀ¼°À QøÍ

öuõh[Q¯x. uø»ø© {ÖÁÚ ¦zuPzvÀ 2013 – 14

©ØÖ® 2014 – 15 –ØPõÚ AøÚzx PnUSPøͲ®

u¯õ›UP.

2013 – 2014 2014 – 15

(¹.) (¹.)

öhÀ¼US Aݨ£¨£mh ö£õ¸Ò 45,000 1,35,000

QøÍ ö\»ÂØS Aݨ£¨£mh £n® :

ÁõhøP 6,000 6,000

\®£Í® 4,800 6,800

©ØÓ ö\»ÄPÒ 2,000 3,000

QøÍ°¼¸¢x ö£Ó¨£mh £n® 70,000 1,60,000

31 ©õºa]À \μUQ¸¨¦ 7,000 26,000

31 ©õºa]À ]Ö öuõøP C¸¨¦ 120 260

Or

(b) Briefly explain the procedure for Allocation of expenses for departments.

xøÓ ö\»ÂÚ[PÐUPõÚ JxURk SÔzx _¸UP©õP

ÂÍUPÄ®.

F – 2425

8

Sp6 Part C (3 10 = 30)

Answer any three questions.

16. A firm of builders, carrying out large contracts kept in a contract ledger separate accounts for each contract. The following particulars relate to a certain contract carried out during the year ended 30th June.

Rs.

Work certified by Architects 1,43,000

Cash received from the contractee 1,30,000

Materials sent to site 64,500

Labour engaged on site 54,800

Plant installed at site 11,300

Value of plant at 30th June (closing) 8,200

Cost of work not yet certified 3,400

Establishment charges 3,250

Direct Expenditure 2,400

Wages accrued due 1,800

Materials, closing balance 1,400

Materials returned to store 400

Direct expenses accrued due 200

Contract price 2,00,000

You are required to prepare an account, showing the profit on the contract to 30th June.

F – 2425

9

Sp6 J¸ ö£›¯ Pmih {Ö©®, ö£›¯ AÍ»õÚ J¨£¢u[PøÍ

uÛuÛ ÷£÷μmkU PnUSPÎÀ ÷©ØöPõskÒÍx.

¤ßÁ¸® ÂÁμ[PÒ áúß 30 –À •iÄÖ® BsiØPõÚ J¸

J¨£¢u® öuõhº¦øh¯uõS®.

¹.

Pmih {¦nºPÍõÀ \õßÓÎUP¨£mh ÷Áø»°ß

AÍÄ

1,43,000

J¨£¢uuõμ›hª¸¢x ö£Ó¨£mh öμõUP® 1,30,000

£o°hzvØS Aݨ£¨£mh \μUQß ©v¨¦ 64,500

£o°hzvÀ £o¦›÷Áõº ©v¨¦ 54,800

£o°hzvÀ {ÖÁ¨£mh uÍÁõh[PÒ 11,300

áúß 30 |õÍßøÓ¯ uÍÁõh[PÎß ©v¨¦ (CÖv

©v¨¦)

8,200

\õßÓÎUP¨£hõu £o°ß ©v¨¦ 3,400

{ÖÄu¾UPõÚ ö\»ÄPÒ 3,250

÷|μi ö\»ÄPÒ 2,400

öPõk£h ÷Ási¯ T¼ 1,800

\μUSPÎß CÖv ©v¨¦ 1,400

£shP\õø»US v¸¨¤ Aݨ£¨£mh \μUSPÒ 400

÷|μi ö\»ÄPÒ öPõk£h ÷Ási¯x 200

J¨£¢u Âø» 2,00,000

30 áúß |õÍßøÓ¯ J¨£¢u® «uõÚ C»õ£zøu Põmk®

PnUS JßøÓ u¯õº ö\´¯ {ú ÷Põ쨣kQÕº.

F – 2425

10

Sp6 17. N. Traders purchased two machines costing Rs. 1,60,000

each from Delhi Motors on 1st January 2012 on Hire Purchase System. The terms were:

Payment on delivery Rs. 40,000 for each machine and balance in three equal instalement together with interest at 10% p.a. to be paid at the end of each year.

N Traders write off 25% depreciation each on the Diminishing Balance Method.

N Traders paid the instalment due on 31st Dec. 2012 and on 31st Dec. 2013 but could not pay the final instalment.

Delhi motors repossessed one machine adjusting its value to the amount due. The repossession was done on the basis of 30% depreciation on Diminishing Balance Method.

Write up the ledger a/c in the books of N. Traders showing the above transactions.

áÚÁ› 1, 2012 – ® Á¸h® N i÷μhºì JÆöÁõßÖ®

¹. 1,60,000 ©v¨¤»õÚ Cμsk C¯¢vμ[PøÍ öhÀ¼

÷©õmhõºì {ÖÁÚzvh® uÁøn öPõÒ•uÀ •øÓ°À

Áõ[Q²ÒÍx.

{£¢uøÚPÒ :

JÆöÁõ¸ C¯¢vμzvØS® ¹.40,000 EhÚi¯õP £n®

ö\¾zv «u•ÒÍ ‰ßÖ uÁøn¯õP 10% Ámi²hß

ö\¾zxÁuõP J¨¦ öPõÒͨ£mhx.

N i÷μhºì 25% SøÓ¢u ö\À ©v¨¤À ÷u´©õÚ® JxURk

ö\´QßÓx.

N i÷μhºì 31 i\®£º, 2012 ©ØÖ® 31 i\®£º 2013 –S›¯

uÁøn ©mk® ö\¾zv EÒÍx. Pøh] uÁøn

ö\¾zuÂÀø».

öhÀ¼ ÷©õmhõºì {¾øÁ öuõøPUPõP J¸ C¯¢vμzøu

v¸®£ øP¯P¨£kzv²ÒÍx. ©ÖøP¯P¨£kzuÀ 30%.

SøÓ¢u ö\À ©v¨¤À PnUQh¨£mkÒÍx.

N i÷μhºì Hmiß PnUSPøÍ ÷©ØPsh |hÁiUøP ‰»®

u¯õº ö\´P.

F – 2425

11

Sp6 18. Mr. Gupta purchased a machine under hire purchase

agreement from Mr. Pankaj. The cash price of the machine was Rs, 15,500. The payment for the purchase is to be made us under.

On Signing the agreement Rs. 3,000 End of the first year Rs. 5,000 End of the second year Rs. 5,000 End of the third year Rs. 5,000 Make necessary journal entries in the books of both the parties. Charge depreciation at the rate of 10% diminishing balance method.

v¸. S¨uõ GߣÁº v¸. £[Pä GߣÁ›hª¸¢x J¸

C¯¢vμzøu ÁõhøP öPõÒ•uÀ J¨£¢u£i öPõÒ•uÀ

ö\´xÒÍõº. C¯¢vμzvß öμõUP {ø» ¹. 15,500.

öPõÒ•u¾UPõÚ Âø» ¤ßÁ¸©õÖ ö\¾zu¨£mhx. J¨£¢u® øPö¯ÊzuõS® ÷£õx ¹. 3,000 •u»õsk

CÖv°À ¹.5,000 Cμshõ©õsk CÖv°À ¹.5,000

‰ßÓõ©õsk CÖv°À ¹.5,000 Cμsk |£ºPÎß

HkPξ® ÷uøÁ¯õÚ SÔ¨÷£mk¨ £vÄPøÍU u¸P.

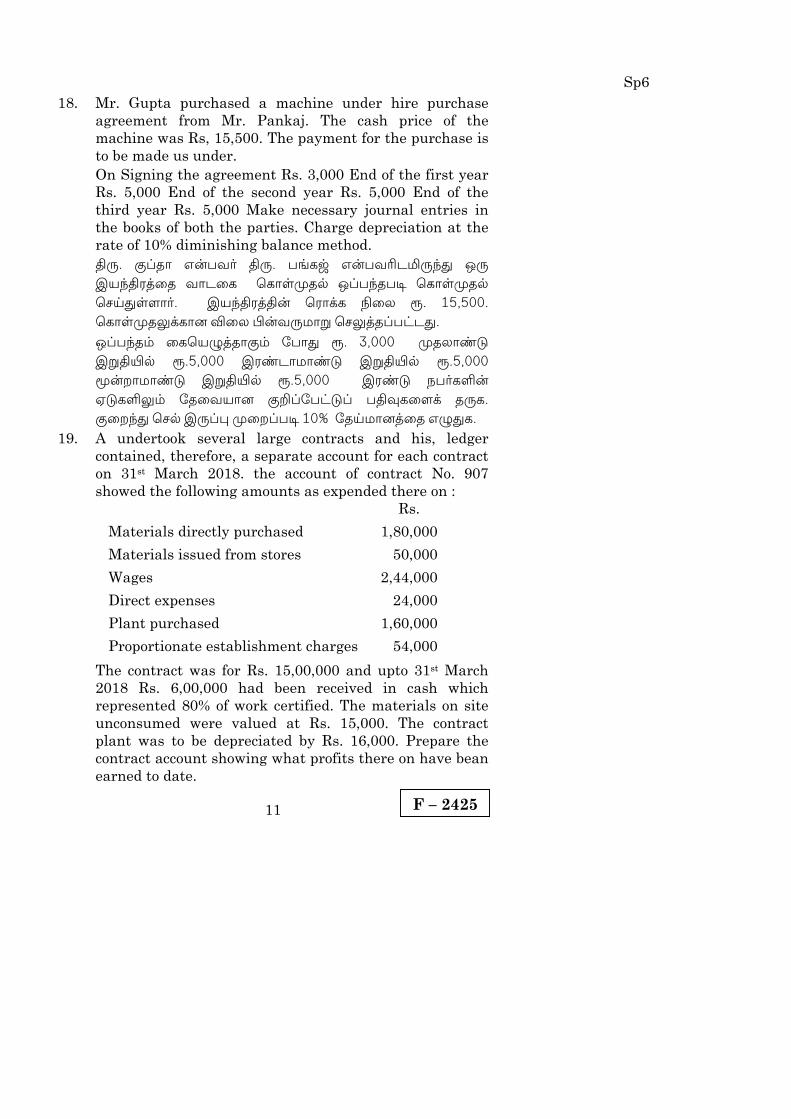

SøÓ¢x ö\À C¸¨¦ •øÓ¨£i 10% ÷u´©õÚzøu GÊxP. 19. A undertook several large contracts and his, ledger

contained, therefore, a separate account for each contract on 31st March 2018. the account of contract No. 907 showed the following amounts as expended there on :

Rs.

Materials directly purchased 1,80,000

Materials issued from stores 50,000

Wages 2,44,000

Direct expenses 24,000

Plant purchased 1,60,000

Proportionate establishment charges 54,000

The contract was for Rs. 15,00,000 and upto 31st March 2018 Rs. 6,00,000 had been received in cash which represented 80% of work certified. The materials on site unconsumed were valued at Rs. 15,000. The contract plant was to be depreciated by Rs. 16,000. Prepare the contract account showing what profits there on have bean earned to date.

F – 2425

12

Sp6 A GߣÁº £À÷ÁÖ ÷ÁÖ ÷£μÍÄ J¨£¢u[PøÍ

HØÖUöPõshõº. JÆöÁõ¸ J¨£¢uzvØS® uÛzuÛ¯õP

PnUSPÒ ÷£÷μmiÀ Ch® ö£ØÓÚ. 2018 ©õºa_ ©õu® 31,

AßÖ Gs. 907 GßÓ J¨£¢uzvß «uõÚ ö\»ÄPÒ R÷Ç

öPõkUP¨£mkÒÍÚ :

¹.

‰»¨ö£õ¸mPÒ ÷|μiU öPõÒ•uÀ ö\´ux 1,80,000

£shP C¸¨¤¼¸¢x öPõkzu ö£õ¸ÒPÒ 50,000

T¼ 2,44,000

÷|μia ö\»ÄPÒ 24,000

G¢vμ® Áõ[Q¯x 1,60,000

{¸ÁõP Ãu¨£i ¤›zu ö\»ÄPÒ 54,000

J¨£¢u® 2018, ©õºa_ 31 – À •iÁøhø¯U Ti¯x®

¹. 15,00,000 US BS®. ¹. 6,00,000 öμõUP©õP¨

ö£Ó¨£mhx. Cx \õßÓÎUP¨£mh •i¢u ÷Áø»°À

80 \uÃu©õS®. öuõȼhzvÀ ~PμõP ‰»¨ö£õ¸Îß

©v¨¦ ¹. 15,000. J¨£¢u G¢vμzvß «x ¹.16,000

÷u´©õÚ©õS®. A¢|õÎÀ ö£Ó¨£mh C»õ£zvøÚU

Põmk® J¨£¢uU PnUQøÚz u¯õ›UPÄ®.

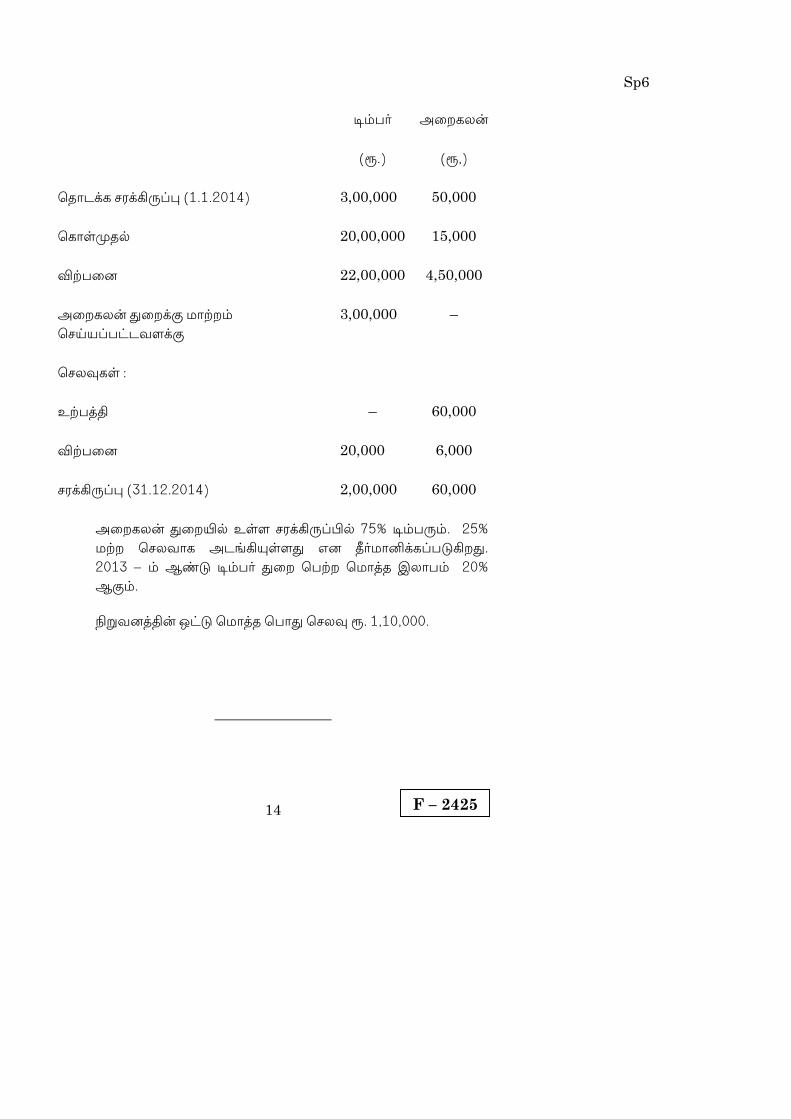

20. A firm has two departments, Timber and Furniture. Furniture was made by the firm itself out of timber supplied by the Timber department at its usual selling price. From the following figures prepare Departmental Trading and profit and loss a/c fm the year 2014.

F – 2425

13

Sp6

Timber Furniture

(Rs.) (Rs.)

Opening stock (1.1.2014) 3,00,000 50,000

Purchases 20,00,000 15,000

Sales 22,00,000 4,50,000

Transfer to Furniture Department 3,00,000 –

Expenses :

Manufacturing – 60,000

Selling 20,000 6,000

Stock 31.12.2014 2,00,000 60,000

The stock in the furniture department may be considered as consisting of 75% of Timber and 25% other expenses. Timber department earned Gross Profit at the rate of 20% in 2013. General expenses come to Rs. 1,10,000.

J¸ {ÖÁÚzvØS i®£º ©ØÖ® AøÓP»ß GÚ Cμsk

xøÓPÒ EÒÍÚ. AøÓP»ß xøÓUS ÷uøÁ¯õÚ

AøÓP»ÝUS›¯ ©μÁøPPøÍ i®£º xøÓ ÁÇUP©õÚ

ÂØ£øÚ Âø»°À ©μÁøPPøÍ AÎzx Á¸QßÓx.

¤ßÁ¸® uPÁ¼ß£i 2014 & ® BskUS›¯ xøÓÁõ›¯õÚ

¯õ£õμ® ©ØÖ® C»õ£ |mh PnUS u¯õº ö\´P.

F – 2425

14

Sp6

i®£º AøÓP»ß

(¹.) (¹,)

öuõhUP \μUQ¸¨¦ (1.1.2014) 3,00,000 50,000

öPõÒ•uÀ 20,00,000 15,000

ÂØ£øÚ 22,00,000 4,50,000

AøÓP»ß xøÓUS ©õØÓ®

ö\´¯¨£mhÁÍUS

3,00,000 –

ö\»ÄPÒ :

EØ£zv – 60,000

ÂØ£øÚ 20,000 6,000

\μUQ¸¨¦ (31.12.2014) 2,00,000 60,000

AøÓP»ß xøÓ°À EÒÍ \μUQ¸¨¤À 75% i®£¸®. 25%

©ØÓ ö\»ÁõP Ah[Q²ÒÍx GÚ wº©õÛUP¨£kQÓx.

2013 – ® Bsk i®£º xøÓ ö£ØÓ ö©õzu C»õ£® 20%

BS®.

{ÖÁÚzvß Jmk ö©õzu ö£õx ö\»Ä ¹. 1,10,000.

————————

WK11

F–2426

B.Com. DEGREE EXAMINATION, NOVEMBER 2019

Fifth Semester

Commerce

CORPORATE ACCOUNTING

(CBCS – 2017 onwards)

Time : 3 Hours Maximum : 75 Marks

Part A (10 2 = 20)

Answer all questions.

1. What is share capital?

£[S ‰»uÚ® GßÓõÀ GßÚ?

2. What is maturity?

•vºÄ GßÓõÀ GßÚ?

3. What is incorporation?

Cøn¨¦ GßÓõÀ GßÚ?

4. What is time ratio?

÷|μ ÂQu® GßÓõÀ GßÚ?

5. Define in the term final account.

CÖv PnUS Áøμ¯øÓ ö\´P.

6. What is interim dividend?

CøhUPõ» £[Põuõ¯® GßÓõÀ GßÚ?

Sub. Code 7BCO5C1

F–2426

2

WK117. What is amalgamation?

J¸[Qøn¨¦ GßÓõÀ GßÚ?

8. What is purchase consideration?

öPõÒ•uÀ ©Ö£¯ß GßÓõÀ GßÚ?

9. Define in the term Good will.

|Øö£¯º Áøμ»UPn® ¯õx?

10. Who is liquidater?

Pø»¨£õͺ Gߣõº ¯õº?

Part B (5 5 = 25)

Answer all questions, choosing either (a) or (b).

11. (a) Sri Siva Ltd. invited applications for 5,000 shares of Rs. 10 each, payable as : on application - Rs. 5, on allotment Rs. 5, the entire is she was applied for and the amount was received in full. Pass Journal entries in the books of the company.

ÿ. ]Áõ ¼m 5000 £[SPøÍ ¹. 10 Ãu® öÁΰmhx.

¹. 5 Cøn Âsn¨£zv¾® ¹. 5 vøÚ

JxURmØPõÄ® ö£Ó ÷Ási¯x. öÁΰmh AøÚzx

£[SPÐUS® £n® ö£Ó¨£mhuõP öPõsk.

A¢{ÖÁÚzvß SÔ¨÷£mk £vÄPøÍ u¸P.

Or

(b) Pass Journal entries for the following issues of debentures.

(i) Issue of 500, 10% debentures of Rs. 100 each

(ii) Issue of 500, 10% debentures of Rs. 100 each at a premium of 10%

(iii) Issue of 500, 10% debentures of Rs. 100 each at a discount of 10%

F–2426

3

WK11 ¤ßÁ¸® PhÜmk£zvμ® öÁαmiØPõÚ SÔ¨÷£mk

£vÄPøÍ u¸P.

(i) 500, 10% PhÜmk £zvμ[PøÍ ¹. 100 Ãu®

öÁΰmhx

(ii) 500, 10% PhÜmk £zvμ[PøÍ ¹. 100 Ãu® 10%

•øÚ©zvÀ öÁΰmhx

(iii) 500, 10% PhÜmk £zvμ[PøÍ ¹. 100 Ãu® 10%

ÁmhzuõÀ öÁ°mhx.

12. (a) How do you calculate sales ratio?

ÂØ£øÚ ÂQuzvøÚ }º GÆÁõÖ PnUQkÁõ´?

Or

(b) What are the objectives of axquistion of Business?

¯õ£õμ {ÖÁÚ øP¯P¨£kzxu¼ß ÷|õUP[PÒ

¯õøÁ?

13. (a) The following in the trial balance of Anitha Ltd. as 30th June 2018. Prepare trading account

Rs.

Stock, 30th June 2017 75,000

Sales 3,50,000

Purchases 2,45,000

Wages 50,000

Discount received 5,000

Share capital 1,00,000

Stock, 30th June 2018 83,000

F–2426

4

WK11 30 áúß 2018 ® |õøͯ AÛuõ Áøμ¯ÖUP¨£mh

{ÖÁÚzvß C¸¨£õ°¼¸¢x ¯õ£õμ PnUQøÚ

u¯õ›UP

¹.

\μUQ¸¨¦ 30 áúß 2017 ß £i 75,000

ÂØ£øÚ 3,50,000

öPõÒ•uÀ 2,45,000

T¼ 50,000

uÒУi ö£ØÓx 5,000

£[S ‰»uÚ® 1,00,000

\μUQ¸¨¦ 30 áúß 2018 ß £i 83,000

Or

(b) From the following informations, prepare a balance sheet of Mr. Fun Ltd as on 31, March 2018

Share capital Rs. 3,92,500

Reserve and surplus Rs. 55,000

Long term borrowings Rs. 3,00,000

Trade payable Rs. 77,350

Short term provisions Rs. 35,750

Short term advances Rs. 31,000

Trade receivable Rs. 82,650

Closing stock Rs. 95,000

Tangible assets Rs. 6,16,950

Intangible assets Rs. 35,000

F–2426

5

WK11 ¤ßÁ¸® ÂÁμ[Pμ¸¢x v¸. £ß Áøμ¯ÖUP¨£mh

{ÖÁÚzvß 31 ©õºa 2018 ® |õøͯ C¸¨¦ {ø»

SÔ¨¤øÚ u¯õ›UP.

£[S ‰»uÚ® ¹. 3,92,500

Põ¨¦® JxUS® ¹. 55,000

}sh Põ» Phß ¹. 3,00,000

¯õ£õμ ö\¾zxuÀPÒ ¹. 77,350

SÖQ¯ Põ» JxUS ¹. 35,750

SÖQ¯ Põ» ö£¸uÀPÒ ¹. 31,000

¯õ£õμ ö£ÖuÀPÒ ¹. 82,650

CÖv \μUQ¸¨¦ ¹. 95,000

¦»ÚõS® ö\õzxUPÒ ¹. 6,16,950

¦»ÚõPõu ö\õzxUPÒ ¹. 35,000.

14. (a) A Ltd agrees to take over B Ltd on the following terms:

(i) The share holders of B Ltd are to be paid Rs. 50 in cash and issues 4 shares of Rs. 10 each in A Ltd for every share of B Ltd. B Ltd has 50,000 equity shares.

(ii) 5000 debentures of Rs. 100 each of B Ltd. are to be redeemed of a premium of 10%