fa4e sm ch06

DESCRIPTION

awdTRANSCRIPT

Chapter 6

Reporting and Analyzing Revenues and Receivables

Learning Objectives – coverage by questionMini-

ExercisesExercises Problems

Cases and Projects

LO1 – Describe and apply the criteria for determining when revenue is recognized.

14, 15, 17 26, 27,32, 39

47 - 49

LO2 – Illustrate revenue and expense recognition when the transaction involves future deliverables.

17, 24, 25 30, 39, 40 46 47, 48

LO3 – Illustrate revenue and expense recognition for long-term projects.

13, 16 28 - 30 42

LO4 – Estimate and account for uncollectible accounts receivable.

18 - 21, 23 33 - 37 45 49

LO5 – Calculate return on capital employed, net operating profit after taxes, net operating profit margin, accounts receivable turnover, and average collection period.

22 31, 34, 38 44 49

LO6 –Discuss earnings management and explain how it affects analysis and interpretation of financial statements.

27, 32, 34 43, 44 48

LO7 Appendix 6A – Describe and illustrate the reporting for

41

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-1

nonrecurring items.

©Cambridge Business Publishers, 2014

6-2 Financial Accounting, 4th Edition

DISCUSSION QUESTIONS

Q6-1. Revenue must be realized or realizable and earned before it can be reported in the income statement. Realized or realizable means that the company’s net assets have increased, that is, the company has received an asset (for example, cash or accounts receivable) or satisfied a liability as a result of the transaction. Earned means that the company has done everything it must do under the terms of the sale.

For retailers, like Abercrombie & Fitch, revenue is generally earned when title to the merchandise passes to the buyer (e.g., when the buyer takes possession of the merchandise), because returns can be estimated. For companies operating under long-term contracts, the earning process is typically measured using the percentage-of-completion method, that is, by the percentage of costs incurred relative to total expected costs.

Q6-2. Financial statement analysis is usually conducted for purposes of forecasting future financial performance of the company. Discontinued operations are, by definition, not expected to continue to affect the profits and cash flows of the company. Accordingly, the financial statements separately report discontinued operations from continuing operations to provide more useful measures of financial performance and financial income. For example, yielding an income measure that is more likely to persist into the future, and a net assets measure absent discontinued items.

Q6-3. In order for an event to be classified as an extraordinary item, its occurrence must be both unusual and infrequent. Items that are considered to be both unusual and infrequent might be the destruction of property by natural disaster or the expropriation of assets by a foreign government in which the company operates. Gains and losses on early retirement of long-term bonds, once comprising the majority of extraordinary items, are no longer considered as such unless they meet the tests outlined above. Other events not likely to be included as extraordinary items include asset write-downs, gains and losses on the sales of assets, and costs related to an employee strike.

Q6-4. Restructuring costs typically consist of two general categories: asset write-downs and accruals of liabilities. Asset write-downs reduce assets and are recognized in the income statement as an expense that reduces income and, thus, equity. Liability accruals create a liability, such as for anticipated severance costs and exit costs, and yield a corresponding expense that reduces income and equity.

Big bath refers to an event in which a company records a nonrecurring loss in a period of already depressed income. By deliberately reducing current period earnings, the company removes future costs from the balance sheet or creates ‘reserves’ that can be used to increase future period earnings.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-3

Q6-5. Earnings management may be motivated by a desire to reach or exceed previously stated earnings targets, to meet analysts’ expectations, or to maintain steady growth in earnings from year to year. This desire to achieve income goals may be motivated by the need to avoid violating covenants in loan indentures or to maximize incentive-based compensation.

The tactics used to manage income involve transaction timing (recognizing a gain or loss) and estimations that increase (or decrease) income to achieve a target.

Q6-6. Pro forma income adjusts GAAP income to eliminate (and sometimes add) various items that the company believes do not reflect its core operations. Such pro forma disclosures are only reported in earnings and press releases and are not part of the published 10-Ks or other annual reports provided for shareholders. The SEC requires that GAAP income be reported together with pro forma income. Yet, companies often report their GAAP income at the very end of the earnings or press release, thus obfuscating their comparison and focusing attention on the pro forma income.

It is because of this potential to confuse the reader about the true financial performance of the company that the SEC has become concerned. Also, pro forma numbers are not subject to accepted standards (and, thus, we observe differing definitions across companies), are not subject to usual audit tests, and are subject to considerable management latitude in what is and is not included and how items are measured.

Q6-7. Estimates are necessary in order to accurately measure and report income on a timely basis. For example, in order to record periodic depreciation of long-lived assets, one must estimate the useful life of the asset. Estimates allow accountants to match revenues and expenses incurred in different periods. For example, accountants estimate warranty costs so that the warranty expense is matched against the corresponding sales revenue. If the accounting process waited until no estimates were necessary, there would be a significant delay in the reporting of financial results.

Q6-8. When analysts publish earnings forecasts, these forecasts become a benchmark against which some investors evaluate the company’s performance. A company that fails to meet analysts’ forecasts may suffer a stock price decline, even though earnings are higher than previous years’ earnings and overall performance is good. Consequently, management may feel pressure to meet or slightly exceed analysts’ forecasts of earnings.

©Cambridge Business Publishers, 2014

6-4 Financial Accounting, 4th Edition

Q6-9. Bad debts expense is recorded in the income statement when the allowance for uncollectible accounts is increased. If a company overestimates the allowance account, net income will be understated on the income statement and accounts receivable (net of the allowance account) will be underestimated on the balance sheet. In future periods, such a company will not need to add as much to its allowance account since it is already overestimated from that prior period (or, it can reverse the existing excess allowance balance). As a result, future net income will be higher.

On the other hand, if a company underestimates its allowance account, then current net income will be overstated. In future periods, however, net income will be understated as the company must add to the allowance account and report higher bad debts expense.

Q6-10. There are several possible explanations for a decrease in the allowance account. First, after an aging of accounts receivable, Wallace Company may have determined that a smaller percentage of its receivables are past due. Wallace Company may have changed its credit policy such that it is attracting lower-risk customers than in the past. Second, experience may have indicated that the percentages used to estimate uncollectibles was too high in previous years. By correcting the estimated percentage of defaults, the estimated uncollectibles would end up lower than in past years. Third, Wallace Company may be managing earnings. By lowering estimated uncollectibles, the company can increase current earnings, but may end up reporting a loss in a future year when write-offs exceed the balance in the allowance account.

Q6-11. Minimizing uncollectible accounts is not necessarily the best objective for managing accounts receivable. That objective could be accomplished by not offering to sell to customers on credit. The purpose of offering credit to customers is to increase sales and profits. Losses from uncollectible accounts are a cost of doing business. As long as the benefit (greater contribution to profits due to increased sales) exceeds the cost (increased losses due to uncollectibles) then a higher-risk credit policy which increases the amount of uncollectible accounts would be a more profitable policy.

Q6-12. The number of defaults tends to rise and fall with the economy. For example, in a recession, customers are more likely to default and companies take longer, on average, to pay their bills than during a healthy economy. This would result in higher estimated uncollectibles if the estimates are based on an aging of accounts receivable.

For many companies, sales revenue also tends to decline during a recession. If estimated uncollectibles are estimated as a percentage of sales, then the estimate would tend to fall in a recession. This is contrary to the increase in the number of defaults that occurs during a recession. Therefore, the percentage of sales approach is not as sensitive to changing economic conditions as is accounts receivable aging.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-5

MINI EXERCISES

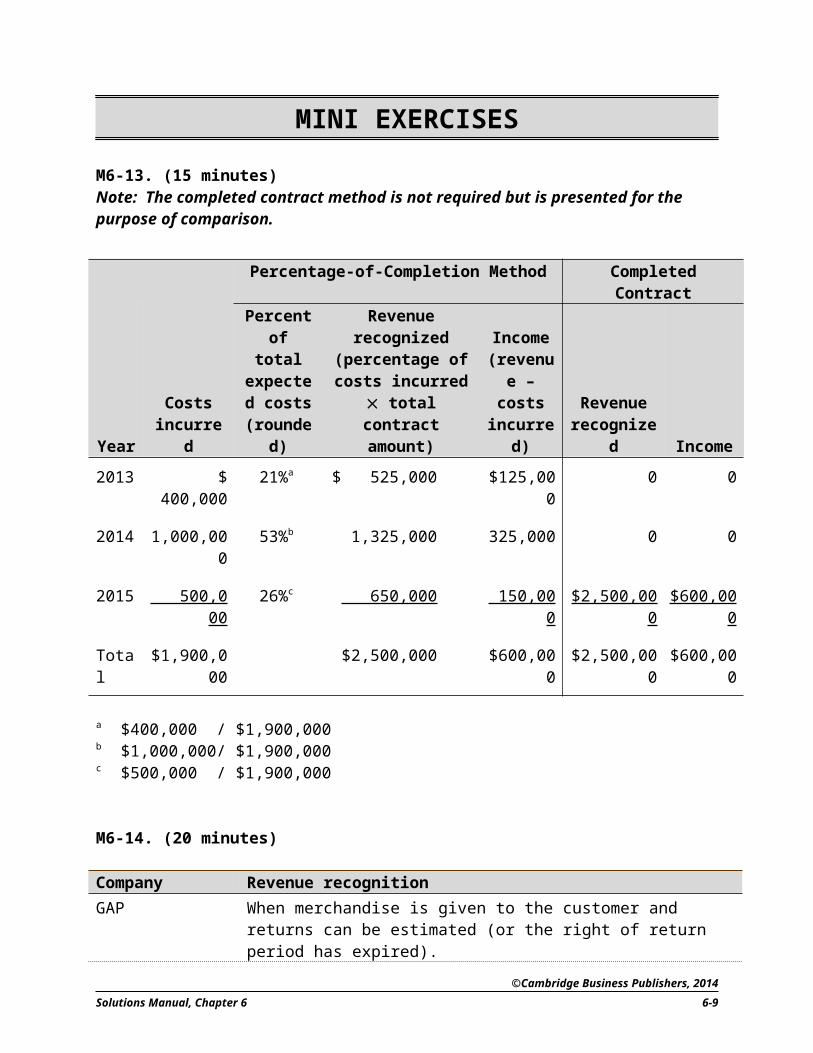

M6-13. (15 minutes)Note: The completed contract method is not required but is presented for the purpose of comparison.

Percentage-of-Completion Method Completed Contract

YearCosts

incurred

Percent of total

expected costs

(rounded)

Revenue recognized

(percentage of costs incurred

total contract amount)

Income (revenue – costs

incurred)Revenue

recognized Income

2013 $ 400,000 21%a $ 525,000 $125,000 0 0

2014 1,000,000 53%b 1,325,000 325,000 0 0

2015 500,000 26%c 650,000 150,000 $2,500,000 $600,000

Total $1,900,000 $2,500,000 $600,000 $2,500,000 $600,000

a $400,000 / $1,900,000b $1,000,000/ $1,900,000c $500,000 / $1,900,000

M6-14. (20 minutes)

Company Revenue recognitionGAP When merchandise is given to the customer and returns can be

estimated (or the right of return period has expired).Merck When merchandise is given to the customer and returns can be

estimated (or the right of return period has expired). The company will also establish a reserve and recognize expense relating to uncollectible accounts receivable at the time the sale is recorded.

Deere When merchandise is given to the customer and the right of return period, if any, has expired. The company will also establish a reserve and recognize expense for uncollectible accounts receivable and anticipated warranty costs at the time the sale is recorded.

Bank of America Interest is earned by the passage of time. Each period, Bank of America accrues income on each of its loans and establishes a receivable on its balance sheet.

Johnson Controls Revenue is recognized under long-term contracts under the percentage-of-completion method.

©Cambridge Business Publishers, 2014

6-6 Financial Accounting, 4th Edition

M6-15. (15 minutes)

The Unlimited can only recognize revenues once they have been earned and the amount of returns can be estimated with sufficient accuracy. Assuming that happens at the time of sale, it must estimate the proportion of product that is likely to be returned and deduct that amount from gross sales for the period. In this case, it would report $4.9 million in net revenue (98% of $5 million) for the period. If The Unlimited does not have sufficient experience to estimate returns, then it should wait to recognize revenue until the right of return period has elapsed.

M6-16. (20 minutes)

a. Percentage-of-completion method:

Year 2013 2014 2015 Total

Percent completed 30% 50% 20%

Revenue $12,000,000 $20,000,000 $8,000,000 $40,000,000

Construction costs 9,000,000 15,000,000 6,000,000 30,000,000

Gross profit $3,000,000 $5,000,000 $2,000,000 $10,000,000

b. Completed contract method:

Year 2013 2014 2015 Total

Revenue $40,000,000 $40,000,000

Construction costs 30,000,000 30,000,000

Gross profit $10,000,000 $10,000,000

M6-17. (20 minutes)

a. A.J. Smith should recognize the warranty revenue as it is earned. Since the warranties provide coverage for three years beginning in 2014, one-third of the revenue should be recognized in 2014, one-third in 2015, and the remaining third in 2016.

b.Year 2014 2015 2016 TotalRevenue $566,666 $566,667 $566,667 $1,700,000Warranty expenses 166,666 166,667 166,667 500,000Gross profit $400,000 $400,000 $400,000 $1,200,000

continued next page

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-7

M6-17. concluded

c. Total revenue from sales of the camera packages is $79,800 ($399 x 200). The revenue is allocated among the three elements of the sale (camera, printer and warranty) as follows:

Element Retail Price Proportion of TotalCamera $300 60% ($300/$500)Printer 125 25% ($125/$500)Warranty 75 15% ($75/$500)Total $500 100%

Using these proportions, the revenue is allocated among the three elements and recognized for each element as it is earned. In this case, the portion of the revenue allocated to the camera and printer are recognized immediately, while the revenue allocated to the warranty is deferred and recognized over the three-year warranty coverage period.

Year Revenue2014 $67,830 ($79,800 x .6 + $79,800 x .25)2015 3,990 ($79,800 x .15 / 3)2016 3,9902017 3,990Total $79,800

M6-18. (15 minutes)

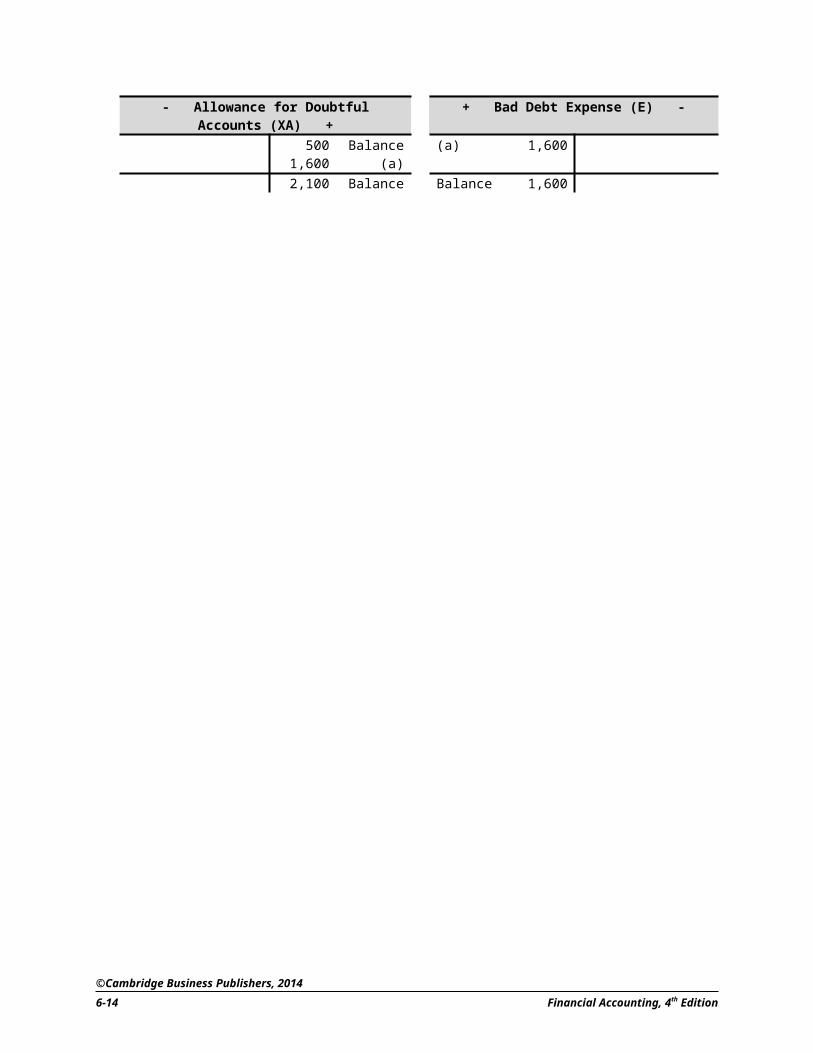

a. To bring the allowance to the desired balance of $2,100, the company will need to increase the allowance account by $1,600, resulting in bad debt expense of that same amount.

b. The net amount of Accounts Receivable is calculated as follows: $98,000 $2,100 = $95,900.

c.- Allowance for Doubtful Accounts (XA) + + Bad Debt Expense (E) -

500 Balance (a) 1,6001,600 (a)2,100 Balance Balance 1,600

©Cambridge Business Publishers, 2014

6-8 Financial Accounting, 4th Edition

M6-19. (15 minutes)

a. Credit losses are incurred in the process of generating sales revenue. Specific losses may not be known until many months after the sale. A company sets up an allowance for uncollectible accounts to place the expense of uncollectible accounts in the same accounting period as the sale and to report accounts receivable at its estimated realizable value at the end of the accounting period.

b. The balance sheet presentation shows the gross amount of accounts receivable, the allowance amount, and the difference between the two, the estimated net realizable value. The balance sheet, thus, reports the net amount that we expect to collect. That is the amount that is the most relevant to financial statement users.

c. The matching concept requires that expenses (credit losses) related to a given revenue be matched with, and deducted from, the revenue in the determination of net income. This dictates the use of the allowance method. Recognition of expense only upon the write-off of the account would delay the reporting of our knowledge that losses are likely and, thereby, reduce the informativeness of the income statement. Accountants believe that providing more timely information justifies the use of estimates that may not be as precise as we would like.

M6-20. (20 minutes)

a. ($ millions) 2011 2010

Accounts receivable (net) $6,361 $6,539

Allowance for uncollectible accounts 143 246

Gross accounts receivable $6,504 $6,785

Percentage of uncollectible accounts to gross accounts receivable

2.2%($143/$6,504)

3.6%($246/$6,785)

b. The decrease in the allowance for uncollectible accounts as a percentage of gross accounts receivable may indicate that the quality of the accounts receivable has improved, perhaps because the economy has improved, the company is selling to a more creditworthy class of customers, or the company’s management of accounts receivable is more effective. It may also indicate, however, that the receivables were over-reserved (e.g., allowance account was too high in 2010). This would result in higher reported profits in 2011 because past profits were too low.

c. $54,365/[($6,361+$6,539)/2] = 8.43 times

365/8.43 = 43.3 days

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-9

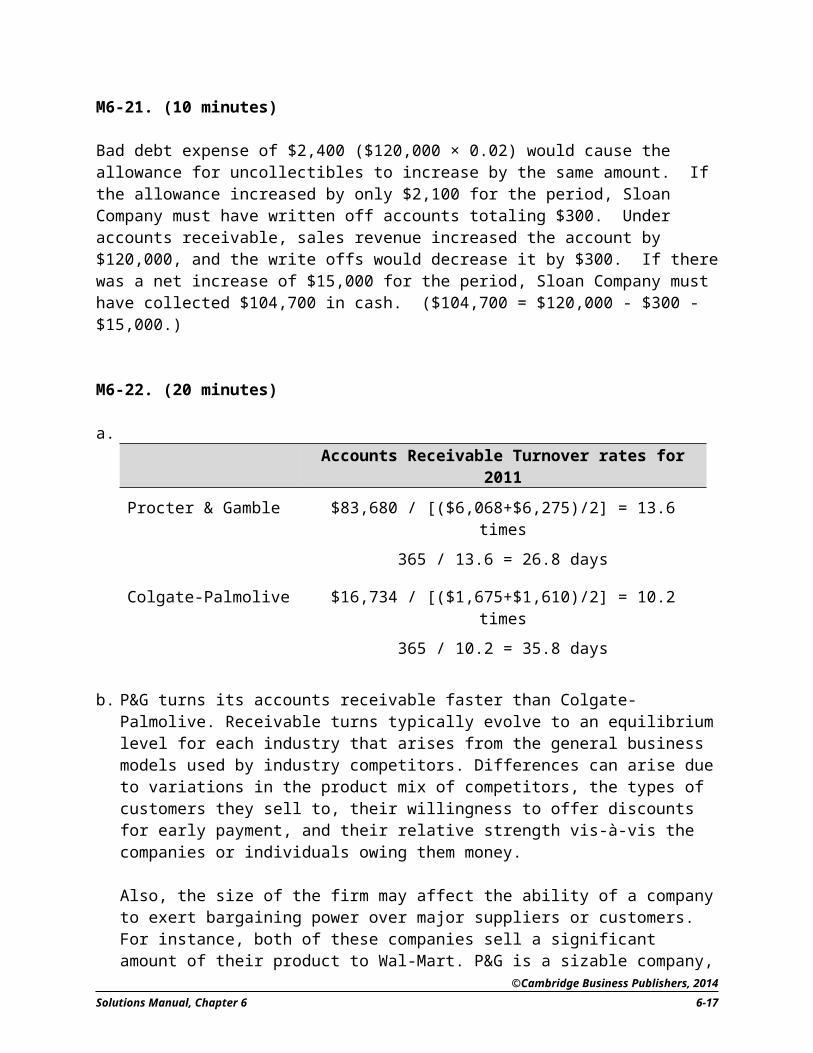

M6-21. (10 minutes)

Bad debt expense of $2,400 ($120,000 × 0.02) would cause the allowance for uncollectibles to increase by the same amount. If the allowance increased by only $2,100 for the period, Sloan Company must have written off accounts totaling $300. Under accounts receivable, sales revenue increased the account by $120,000, and the write offs would decrease it by $300. If there was a net increase of $15,000 for the period, Sloan Company must have collected $104,700 in cash. ($104,700 = $120,000 - $300 - $15,000.)

M6-22. (20 minutes)

a. Accounts Receivable Turnover rates for 2011

Procter & Gamble $83,680 / [($6,068+$6,275)/2] = 13.6 times

365 / 13.6 = 26.8 days

Colgate-Palmolive $16,734 / [($1,675+$1,610)/2] = 10.2 times

365 / 10.2 = 35.8 days

b. P&G turns its accounts receivable faster than Colgate-Palmolive. Receivable turns typically evolve to an equilibrium level for each industry that arises from the general business models used by industry competitors. Differences can arise due to variations in the product mix of competitors, the types of customers they sell to, their willingness to offer discounts for early payment, and their relative strength vis-à-vis the companies or individuals owing them money.

Also, the size of the firm may affect the ability of a company to exert bargaining power over major suppliers or customers. For instance, both of these companies sell a significant amount of their product to Wal-Mart. P&G is a sizable company, and may have greater bargaining power over Wal-Mart than does the smaller Colgate-Palmolive.

One other possibility is that the difference is due to the companies’ differing fiscal year-ends. If the receivable balance is not constant during the year due to some seasonality, then the receivable turnover ratio will depend on the choice of fiscal year.

©Cambridge Business Publishers, 2014

6-10 Financial Accounting, 4th Edition

M6-23. (20 minutes)

a.i. Accounts receivable (+A) ……………………………………… 3,200,000

Sales revenue (+R, +SE) …………………………..…… 3,200,000

ii. Bad debts expense (+E, -SE) …………………………………

42,000

Allowance for uncollectible accounts (+XA, -A)……. 42,000

iii. Allowance for uncollectible accounts (-XA, +A) ………. 39,000Accounts receivable (-A) ………………………………….. 39,000

iv. Accounts receivable (+A) ……………………………………… 12,000Allowance for uncollectible accounts (+XA, -A) 12,000

Cash (+A) …..……………………………………………………… 12,000Accounts receivable (-A) ………………………………… 12,000

The recovered receivable is reinstated, so that its payment may be properly recorded.

b. Besides the $12,000 in recovery, the collections from customers can be summarized in the following entry:

v. Cash (+A) 2,926,000Accounts receivable (-A) 2,926,000

(This amount includes payment of the recovered receivable for $12,000. The allowance increases by $15,000 over the period, so the fact that net receivables increased by $220,000 means that gross receivables must have increased by $235,000. That fact allows us to “back out” the cash received.)

c.+ Cash (A) - - Sales Revenue (R) +

(iv) 12,000 3,200,000 (i)(v) 2,926,000

2,938,000+ Accounts Receivable (A) - + Bad Debts Expense (E) -

(i) 3,200,000 (ii) 42,000(iv) 12,000 39,000 (iii)

12,000 (iv)2,926,000 (v)

235,000- Allowance for Uncollectibles (XA) +

42,000 (ii)(iii) 39,000

12,000 (iv)15,000

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-11

continued next page

©Cambridge Business Publishers, 2014

6-12 Financial Accounting, 4th Edition

M6-23. concluded

d.Balance Sheet Income Statement

TransactionCash Asset +

Noncash Assets - Contra

Assets = Liabil-ities + Contrib.

Capital + Earned Capital Revenues - Expenses = Net Income

i. Sales on account.

+3,200,000Accounts

Receivable- =

+3,200,000Retained Earnings

+3,200,000Sales

Revenue- = +3,200,000

ii. Bad debt expense.

-+42,000

Allowance for Uncollectible

Accounts

=-42,000

Retained Earnings

-+42,000Bad Debt Expense

= -42,000

iii. Write-off of uncollectible accounts.

-39,000Accounts

Receivable-

-39,000Allowance for Uncollectible

Accounts

= - =

iv. Reinstate account previously written off.

+12,000Accounts

Receivable-

+12,000Allowance for Uncollectible

Accounts

- =

Collect reinstated account.

+12,000Cash

-12,000Accounts

Receivable- - =

v. Collect cash on sales. +2,926,000

Cash

-2,926,000Accounts

Receivable- = - =

M6-24. (20 minutes)

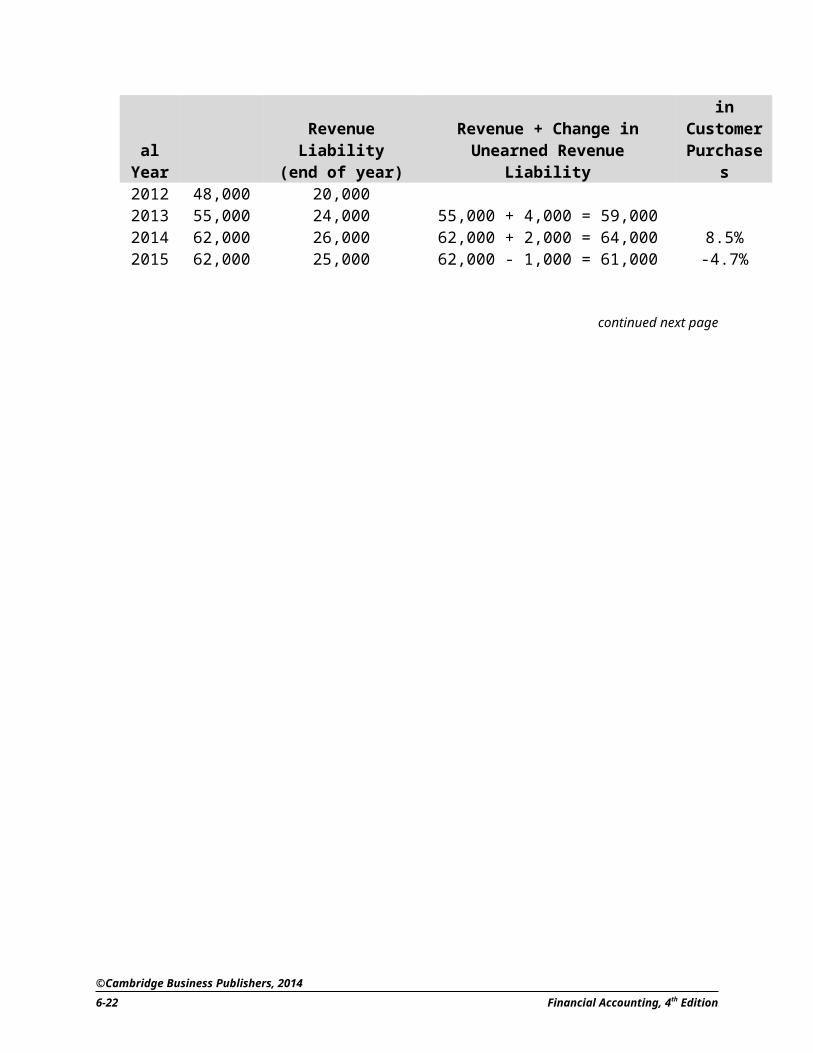

a.Fiscal Year Revenue Revenue Growth2012 48,0002013 55,000 14.6%2014 62,000 12.7%20150 62,000 0.0%

b.

Fiscal Year Revenue

Unearned Revenue Liability

(end of year)

Customer Purchases = Revenue + Change in Unearned

Revenue Liability

Growth in Customer Purchases

2012 48,000 20,0002013 55,000 24,000 55,000 + 4,000 = 59,0002014 62,000 26,000 62,000 + 2,000 = 64,000 8.5%2015 62,000 25,000 62,000 - 1,000 = 61,000 -4.7%

continued next page

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-13

M6-24. concluded

c. In both fiscal year 2014 and 2015, the growth in customer purchases is lower than the growth in reported revenues. The practice of deferring revenue recognition implies that reported revenues in a given period are the result of customer purchases over many periods, resulting in a smoothing of revenues. In the case of Finn Publishing, revenues in any given year are the result of newsstand and bookstore purchases during that year, plus part of the subscriptions from that year, plus part of the subscriptions from the previous year. That means that growth in annual revenues is a composite of growth in customer purchases over an even longer period of time.

For 2014 and 2015, Finn’s growth in revenues exceeds the growth in customer purchases because the revenues are still reflecting growth from prior periods. Purchases are a “leading indicator” of revenues, and thus, calculating customer purchase behavior can be useful in forecasting future revenue and identifying changes in customers’ attitudes about a company’s current offerings.

M6-25. (15 minutes)

This question is based on an actual situation, in which the accounting rules were influencing the product decisions. The rules for revenue deferral when there are multiple deliverables deterred the company from providing enhancements and upgrades that were available. If Commtech’s customers (the wireless companies) had been willing to pay for the upgrades to its customer’s phones, that would have been allowed. (It’s not clear what the wireless companies’ incentives would be, because they may want to encourage users to purchase new phones – with a new service contract – rather than improving their existing phones.)

The question can generate a discussion about whether accounting should drive decisions. Whether it should or not, it does, so the question should evolve into what top management should do about this type of situation. Does the situation described in the problem require some managerial action, or not. Is the company foregoing sales because of its accounting? Within Commtech, the finance staff was skeptical of marketing’s predictions that the upgrades and enhancements would increase the sales of existing phone models. If the upgrades and enhancements are delivered, Commtech will have to change its accounting for revenue, with a resulting decrease in near-term profitability. How might the company communicate that change in a way that the investing public will understand as a net benefit to the company?

©Cambridge Business Publishers, 2014

6-14 Financial Accounting, 4th Edition

EXERCISES

E6-26. (20 minutes)

Company Revenue Recognition

The Limited When merchandise is given to the customer and returns can be estimated (or the right of return period has expired).

Boeing Corporation

Revenue is recognized under long-term contracts under the percentage-of-completion method.

SUPERVALU When merchandise is given to the customer and cash is received.

MTV When the content is aired by the TV stations.

Real estate developer

When title to the houses is transferred to the buyers.

Wells Fargo Interest is earned by the passage of time. Each period, Wells Fargo accrues income on each of its loans and establishes an account receivable on its balance sheet.

Harley-Davidson When title to the motorcycles is transferred to the buyer. Harley will also set up a reserve for anticipated warranty costs and recognize the expected warranty cost expense when it recognizes the sales revenue.

Time-Warner When the magazines are sent to subscribers.

E6-27. (20 minutes)

Company Revenue Recognition

Real Money Recognize revenue ratably over the period of time that customers can access its Web site, not when the cash is received. The recognition of revenue is dependent upon Real Money providing updates.

Oracle The fee to purchase the right to use the software can be recorded as revenue when the software is installed, unless that fee includes future deliverables like upgrades and support. (If such post-sale services are included in the fee, some portion must be deferred and recognized over the appropriate period.) Service revenue can only be recognized ratably over the period of time covered by the service contract.

Intuit Recognize revenue when the software is sent to customers. The company must estimate potential warranty claims and establish a reserve for them when revenue is recorded.

Computer game developer

Record revenue after the 10-day right of return period has elapsed.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-15

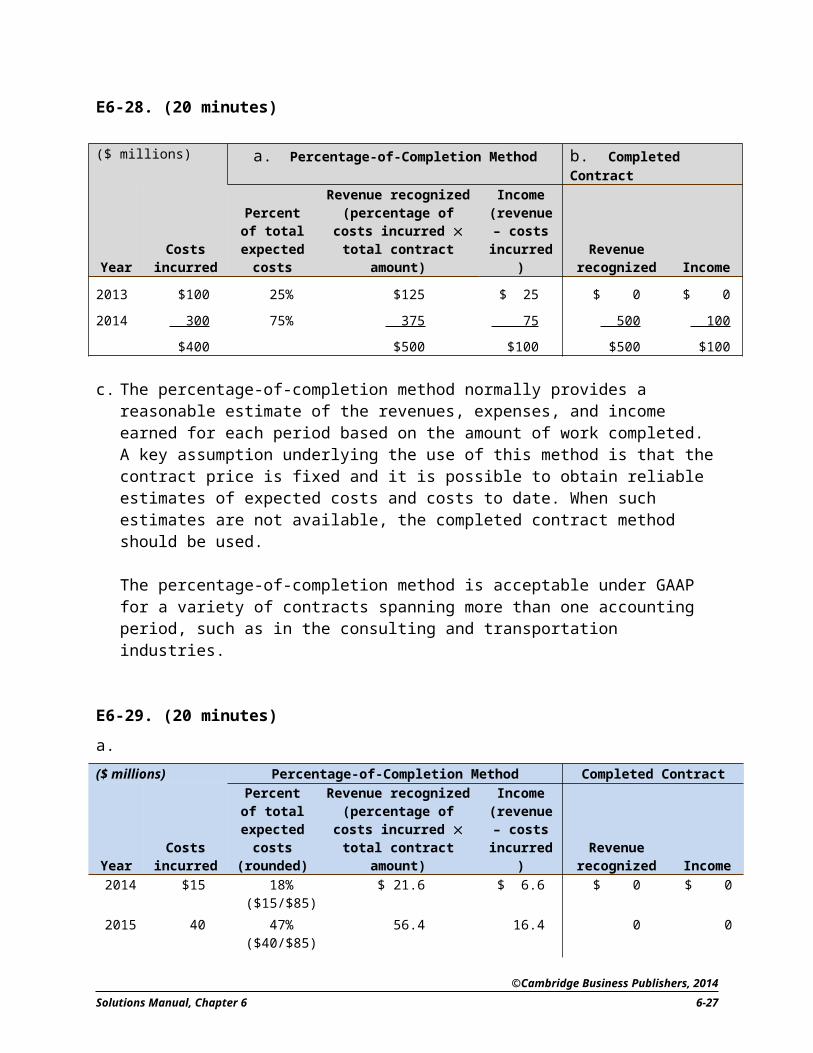

E6-28. (20 minutes)

($ millions) a. Percentage-of-Completion Method b. Completed Contract

YearCosts

incurred

Percent of total

expected costs

Revenue recognized (percentage of costs

incurred total contract amount)

Income (revenue –

costs incurred)

Revenue recognized Income

2013 $100 25% $125 $ 25 $ 0 $ 0

2014 300 75% 375 75 500 100

$400 $500 $100 $500 $100

c. The percentage-of-completion method normally provides a reasonable estimate of the revenues, expenses, and income earned for each period based on the amount of work completed. A key assumption underlying the use of this method is that the contract price is fixed and it is possible to obtain reliable estimates of expected costs and costs to date. When such estimates are not available, the completed contract method should be used.

The percentage-of-completion method is acceptable under GAAP for a variety of contracts spanning more than one accounting period, such as in the consulting and transportation industries.

E6-29. (20 minutes)

a.

($ millions) Percentage-of-Completion Method Completed Contract

YearCosts

incurred

Percent of total

expected costs

(rounded)

Revenue recognized (percentage of costs

incurred total contract amount)

Income (revenue –

costs incurred)

Revenue recognized Income

2014 $15 18%($15/$85)

$ 21.6 $ 6.6 $ 0 $ 0

2015 40 47%($40/$85)

56.4 16.4 0 0

2016 30 35%($30/$85)

42.0 12.0 120 35

$85 $120.0 $35.0 $120 $ 35

b. The percentage-of-completion method provides a good estimate of the revenue and income earned in each period. This method is also acceptable under GAAP for contracts spanning more than one accounting period. Recognition of revenue and income is not affected by the cash received, but the percentage-of-completion method more closely approximates cash flows than the completed contract method.

©Cambridge Business Publishers, 2014

6-16 Financial Accounting, 4th Edition

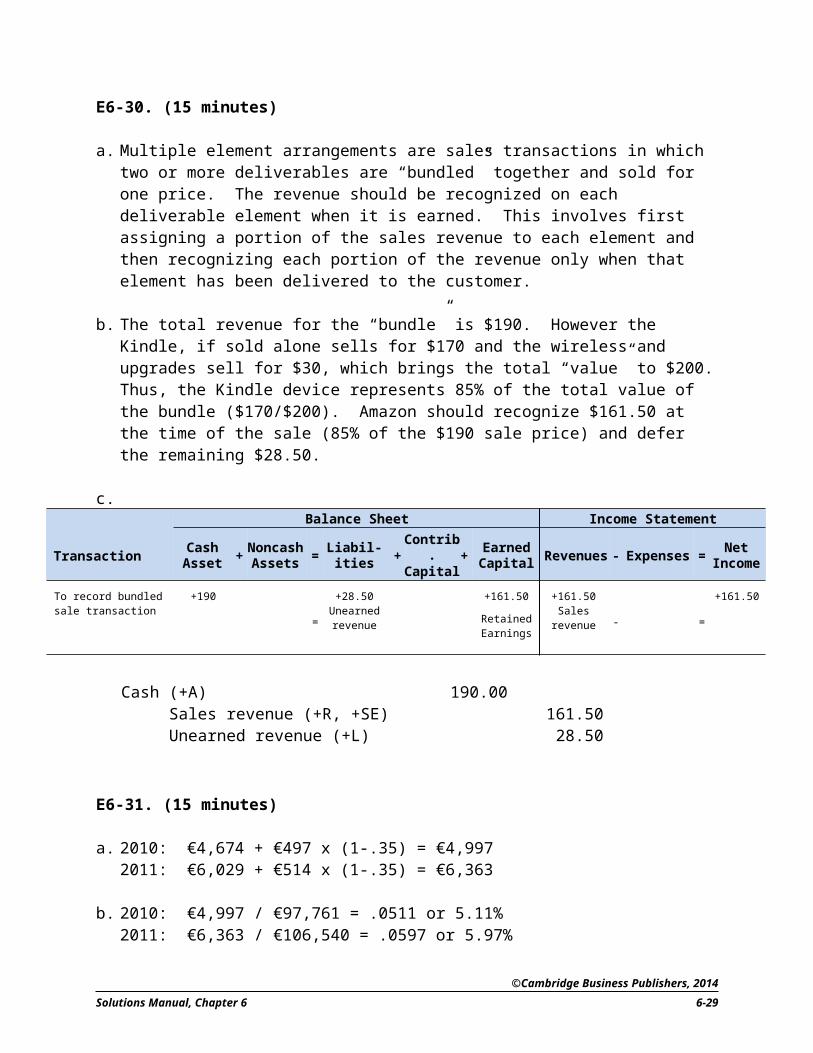

E6-30. (15 minutes)

a. Multiple element arrangements are sales transactions in which two or more deliverables are “bundled” together and sold for one price. The revenue should be recognized on each deliverable element when it is earned. This involves first assigning a portion of the sales revenue to each element and then recognizing each portion of the revenue only when that element has been delivered to the customer.

b. The total revenue for the “bundle” is $190. However the Kindle, if sold alone sells for $170 and the wireless and upgrades sell for $30, which brings the total “value” to $200. Thus, the Kindle device represents 85% of the total value of the bundle ($170/$200). Amazon should recognize $161.50 at the time of the sale (85% of the $190 sale price) and defer the remaining $28.50.

c.Balance Sheet Income Statement

TransactionCash Asset + Noncash

Assets = Liabil-ities + Contrib. Capital + Earned

Capital Revenues - Expenses = Net Income

To record bundled sale transaction

+190

=

+28.50 Unearned revenue

+161.50

Retained Earnings

+161.50 Sales

revenue - =

+161.50

Cash (+A) 190.00Sales revenue (+R, +SE) 161.50Unearned revenue (+L) 28.50

E6-31. (15 minutes)

a. 2010: €4,674 + €497 x (1-.35) = €4,9972011: €6,029 + €514 x (1-.35) = €6,363

b. 2010: €4,997 / €97,761 = .0511 or 5.11%2011: €6,363 / €106,540 = .0597 or 5.97%

c. €6,363 / [(€143,844 - €23,571 + €131,487 - €21,191) / 2] = .0552 or 5.52%

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-17

E6-32. (15 minutes)

In none of these cases should Simpyl Technologies recognize revenue. Each of the four settings touches on one of the four conditions for revenue recognition listed by the SEC. In part a, “persuasive evidence of an exchange agreement” does not yet exist, because the company’s policies have defined a contract with authorized signatures to constitute persuasive evidence. In part b, delivery has not occurred. The product has been shipped, but not to the customer and not with the specified customizations that are required by the customer. In part c, the price is not yet fixed or determinable, because the negotiations over volume discounts have not been concluded. Finally, the distributor in part d does not have the means to pay for the items delivered, so collectibility cannot be reasonably assured (until the distributor sells the product to an end customer). The delivery should be viewed as a consignment arrangement, in which Simpyl recognizes revenue when the distributor sells the items to a third party.

This problem is based on the restatements of Symbol Technologies, Inc.’s 10-K filing for fiscal year 2002, in which they detail the errors and irregularities in financial statements dating back to 1998. Symbol had made accounting entries that violated each of the SEC’s four criteria for revenue recognition. An article by Steve Lohr describing the incoming CEO’s experiences at Symbol Technologies can be found in the New York Times, June 21, 2004. The title of the article is “Day 2: I Learn the Books are Cooked.” (Motorola, Inc., acquired Symbol Technologies in January 2007 for a price of $3.9 billion.)

E6-33. (20 minutes)

a. Prior to the aging of accounts, the balance in the Allowance for Uncollectible Accounts would be a credit of $520 (the opening balance of $4,350 less the amounts written off of $3,830).

2013 bad debt expense computation$250,000 0.5% = $1,250

$ 90,000 1% = 900 20,000 2% = 400 11,000 5% = 550 6,000 10% = 600 4,000 25% = 1,000

4,700 Less: Unused balance before adjustment 520 Bad debt expense for 2013 $4,180

continued next page

©Cambridge Business Publishers, 2014

6-18 Financial Accounting, 4th Edition

E6-33. concluded

b. Accounts receivable, net = $381,000 - $4,700 = $376,300

Reported in the balance sheet as follows:Accounts receivable, net of $4,700 in allowances.................................... $376,300

c.+ Bad Debts Expense (E) - - Allowance for Uncollectible Accounts (XA) +

(a) 4,180 4,350 BalanceWrite-offs 3,830

4,180 (a)

4,700 Balance

E6-34. (25 minutes)

a. Allowance for doubtful accounts (-XA) 70Accounts receivable (-A) 70

Provision for doubtful accounts (+E,-SE) 9Allowance for doubtful accounts (+XA) 9

The provision for doubtful accounts (bad debt expense) has a credit entry that has the effect of decreasing Ethan Allen’s reported income by $9 thousand for the year. The write-off of $70 thousand of uncollectible accounts has no effect on income.

b.2012 2011

Accounts receivable, net 14,919 15,036Allowance for doubtful accounts 1,250 1,171

Gross receivables (net plus allowance) $16,169 $16,207

Allowance as a % of gross receivables 7.7% 7.2%

c. $729,373 / [($14,919 + $15,036) / 2] = 48.7 times. The very fast ART is probably due to the custom furniture aspect of Ethan Allen’s business. Many of their products are not produced until a customer places an order and payment occurs upon delivery or very soon thereafter.

d. $729,373 + ($65,465 - $62,649) – ($14,919 - $15,036) – $9 = $723,297.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-19

E6-35. (15 minutes)

Accounts receivable $138,100Less Allowance for uncollectible accounts 10,384 $127,716

ComputationsAccounts Allowance for

Receivable Uncollectible Accounts

Beginning balance $ 122,000 $ 7,900Sales 1,173,000Collections (1,150,000)Write-offs ($3,600 + $2,400 +$900) (6,900) (6,900)Provision for uncollectibles ($1,173,000 0.8%) _________ 9,384

$ 138,100 $ 10,384

E6-36. (20 minutes)

a. Aging schedule at December 31, 2013 Current $304,000 1% = $ 3,0400–60 days past due 44,000 5% = 2,20061–180 days past due 18,000 15% = 2,700Over 180 days past due 9,000 40% = 3,600Amount required 11,540

Balance of allowance 4,200 Provision $ 7,340 = 2010 bad debt expense

b. Current Assets Accounts receivable $375,000Less: Allowance for uncollectible accounts 11,540 $363,460

c.+ Bad Debts Expense (E) - - Allowance for Uncollectible Accounts (XA) +

(a) 7,340 4,200 Balance 7,340 (a)

11,540 Balance

©Cambridge Business Publishers, 2014

6-20 Financial Accounting, 4th Edition

E6-37. (30 minutes)

a.Year Sales Collections Accounts Written Off2012 $ 751,000 $ 733,000 $ 5,3002013 876,000 864,000 5,8002014 972,000 938,000 6,500Total $2,599,000 $2,535,000 $17,600

Accounts Receivable at the end of 2014 is $46,400, computed as:($2,599,000 - $2,535,000 - $17,600).

Bad Debts Expense is:2012 $ 7,510 computed as 1% $751,0002013 8,760 computed as 1% $876,0002014 9,720 computed as 1% $972,0002012-2014 $25,990 computed as 1% $2,599,000

Allowance for Uncollectible Accounts is $8,390 computed as:$25,990 total bad debts expense less $17,600 in total write-offs.

b.Accounts Receivable (A) Allowance for Uncollectibles (XA)

Beg Bal 0 0 Beg BalSales 751,000 5,300 Write offs Write offs 5,300 7,510 Bad debts exp.

733,000 Collections2012 Bal 12,700 2,210 2012 BalSales 876,000 5,800 Write offs Write offs 5,800 8,760 Bad debts exp.

864,000 Collections2013 Bal 18,900 5,170 2013 BalSales 972,000 6,500 Write offs Write offs 6,500 9,720 Bad debts exp.

938,000 Collections2014 Bal 46,400 8,390 2014 Bal

There isn’t any indication that the 1% rate is incorrect. If the rate is too high, we would expect the allowance to grow at a faster rate than receivables. If the rate is too low, the opposite would occur. In this case, the allowance percentage of receivables is 17%, 27% and 18% at the end of 2012, 2013 and 2014, respectively. So, there is no clear direction that would indicate an inappropriate estimate.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-21

E6-38. (20 minutes)

a.Earnings

from Operations

End. Assets

Beg. Assets

Avg. Assets

Return on Capital

Employed

Personal Systems Group $ 2,350 $ 15,781 $ 16,548 $16,164.5 14.5%

Services 5,149 40,614 41,989 41,301.5 12.5%

Imaging and Printing Group 3,973 11,939 12,514 12,226.5 32.5%

Enterprise Servers, Storage and Network

3,026 17,539 18,262 17,900.5 16.9%

HP Software 698 21,028 9,979 15,503.5 4.5%

HP Financial Services 348 13,543 12,123 12,833.0 2.7%

b. The most profitable group seems to be the Imaging and Printing Group, which represents HP’s traditional strength. However, it is not growing very quickly (based on sales percentage increases). The Enterprise Servers, Storage and Networking Group and the Personal Systems Group (commercial and personal PCs, workstations, etc.) also have good return on capital employed. The HP Software Group has a low return on capital employed but that group appears to have had a major investment in assets during the year, which can distort this measure, depending on the timing of the capital expenditures.

c. Restructuring charges are reported “above the line,” as part of income from continuing operations before income taxes. They are listed as a charge against operating income in the income statement, and thus would reduce our calculation of return on capital employed. Restructuring charges are nonrecurring, however, and should be considered separately when evaluating profitability of a business segment.

©Cambridge Business Publishers, 2014

6-22 Financial Accounting, 4th Edition

E6-39. (20 minutes)

a. Just like for-profit organizations, not-for-profit organizations cannot recognize revenue until it has been earned. In the case of The Lyric Opera, it cannot recognize the ticket revenue until the performances occur. (The Lyric does not issue quarterly reports, so we cannot observe how much of the revenue has been earned by six months through its fiscal year.)

b. This entry is simplified by the fact the fiscal year-end is after the end of the current season and by assuming that all of The Lyric’s deferred revenue relates to the following season (and none to any years after the following season).

To record revenue for the fiscal year 2012 season:

Deferred ticket and other revenue (-L) 12,711Cash or Accounts receivable (+A) 12,319

Ticket sales (+R, +NA) 25,030

(As a not-for-profit, The Lyric Opera does not have shareholders’ equity, but rather “net assets.” Therefore, the recognition of revenue increases net assets (NA) on the balance sheet.)

To record advance purchases for the fiscal year 2012 season:Cash or Accounts receivable (+A) 12,638

Deferred ticket and other revenue (+L) 12,638

c. It’s likely that the downturn in the economy caused some subscribers not to renew (or to wait until after April 30 to renew) in 2009 and it would appear that three years later, the advanced ticket sales have not recovered from the 2009 decline. It’s possible that the decline in advance purchases is a statement about the opera selections. However, the loyal subscriber base (and the desire to keep one’s assigned seating) makes the economy a more likely cause.

d. The Lyric Opera usually operates at close to seating capacity. And, in a typical year, approximately more than one-half of its seats are sold by the April 30th preceding the season. So, the quantity of unsold seats will affect The Lyric’s marketing efforts for subscribers who have not yet renewed, outreach to new potential subscribers and promotions for individual tickets which go on sale shortly before the season. Those efforts can be scaled up or down depending on the experience with advance sales.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-23

E6-40. (20 minutes)

a. Membership fees are initially recorded as a liability (deferred membership fee revenue) and recognized over a period of one year. Member rewards are similarly deferred, but the offsetting debit is recorded as a reduction to sales revenue.

b.Cash (+A) 2.203

Deferred membership fees (+L) 2,203

Deferred membership fees (-L) 2,075Membership fee revenue (+R, +SE) 2,075

c.Sales revenue (-R, -SE) 900

Accrued member rewards (+L) 900

Accrued member rewards (-L) 841Merchandise inventory (-A)* 841

*The Costco note does not say how the membership rewards are redeemed. The entry above assumes that the rewards are redeemed for merchandise, as is the case in many such situations. If, instead, the rewards are redeemed for cash, the credit entry would be to cash and not merchandise inventory.

©Cambridge Business Publishers, 2014

6-24 Financial Accounting, 4th Edition

PROBLEMS

P6-41.A (20 minutes)

a. The following items might be considered to be operating:

1. Net Sales, cost of sales, R&D expenses, and SG&A expenses are typically designated as operating.

2. Amortization of intangible assets and restructuring charges would usually be considered to be operating under the assumptions that the acquisition that gave rise to the intangible assets is included as part of operations, and that the restructuring did not involve discontinuation of distinct parts of the business.

3. The asbestos-related credit, restructuring charges and goodwill impairment losses would be considered to be operating since they are related to Dow Chemical’s operating activities. (These items are both operating and nonrecurring – see b.)

4. Purchased in-process research and development charges and Acquisition-related expenses are caused by the company’s investing activities, and would be considered nonoperating.

5. Equity in earnings of nonconsolidated affiliates would be considered operating under the assumption that the affiliates are related to Dow’s core operations, which is typically the case.

6. Sundry income would generally be considered nonoperating in the absence of a footnote clearly indicating its connection to the operating activities of the company.

7. Interest income is considered nonoperating

8. Interest expense and amortization of debt discount is nonoperating.

continued next page

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-25

P6-41.A concluded

b. The following items might be identified as nonrecurring items:

1. Purchased in-process research and development and Acquisition-related expenses – these are one-time (e.g., nonrecurring) costs incurred in connection with the acquisition of another company and can properly be expensed under GAAP.

2. Asbestos-related credit – this is a reversal of a previous accrual for litigation in connection with asbestos-related lawsuits. GAAP requires such an accrual if the loss is probable and can be reasonably estimated. Since it is a one-time occurrence, it can be considered to be a transitory item.

3. Goodwill impairment losses – this loss results from changes in expectations of the performance of past acquisitions. It would be considered operating, but transitory.

4. Restructuring charges – these relate to the company’s actions due to the economic decline in 2008 and the expectations that future performance will not meet prior expectations. Restructuring costs are considered “special items,” meaning that individually they are transitory, but as a category, they happen frequently.

5. The charge for discontinued operations would be considered nonrecurring.

We would need to examine prior years’ income statements to discern if the other categories in Dow’s income statement are to be considered transitory.

c. 2010: $2,321 + ($1,473 + $143 - $125 - $37) x (1-.35) = $3,266.1

$3,266.1 / $53,674 = 6.1%

2009: $676 + ($1,571 + $7 + $166 - $891 - $39) x (1-.35) = $1,205.1

$1,205.1 / $44,875 = 2.7%

©Cambridge Business Publishers, 2014

6-26 Financial Accounting, 4th Edition

P6-42. (20 minutes)

a. 1. Percentage-of-completion based on number of employees trainedYear 2013 2014 2015 TotalNumber of employees trained 125 200 75 400Revenues (# trained x $1,200) $150,000.00 $240,000.00 $90,000.00 $480,000.00Expenses (# trained x $437.50)* 54,687.50 87,500.00 32,812.50 175,000.00Gross Profit $95,312.50 $152,500.00 $57,187.50 $305,000.00

* $437.50 = $175,000 / 400

2. Percentage-of-completion based on costs incurredYear 2013 2014 2015 TotalCosts incurred $60,000 $75,000 $40,000 $175,000Percentage completed 34.29% 42.86% 22.86% 100.00%Revenues (% x $480,000) $164,571.43 $205,714.29 $109,714.29 $480,000.00Expenses 60,000.00 75,000.00 40,000.00 175,000.00Gross Profit $104,571.43 $130,714.29 $69,714.29 $305,000.00

3. Completed contract methodYear 2013 2014 2015 TotalRevenues $0 $0 $480,000 $480,000Expenses 0 0 175,000 175,000Gross Profit $0 $0 $305,000 $305,000

b. Assuming that (1) Philbrick has a noncancelable contract that specifies the price at $1,200 per employee, (2) the number of employees and the costs of training can be estimated with a reasonable degree of accuracy, and (3) Elliot Company is a reasonable credit risk, the best method would be to recognize revenues using the percentage-of-completion method based on the number of employees trained. The completed contract method should only be used if either of the first two conditions is not met.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-27

P6-43. (15 minutes)

a. Management would have an incentive to shift $1 million of income from the current period into next. This might be accomplished by delaying revenue recognition or accelerating expenses. This would increase their bonus by $100,000 next year without decreasing the current bonus.

b. Management would have an incentive to shift $3 million of income from next year into income reported this year. This would increase the current year bonus by $300,000 without reducing next year’s bonus.

c. Management would have an incentive to shift income from the current year into next year. Even though this would reduce earnings this year, earnings are already so low that management does not expect to receive a bonus. Shifting earnings into a future period increases the bonus in that period.

d. These incentives for earnings management would be mitigated if the “kinks” in the bonus formula were removed. Alternatively, some companies pay bonuses based on a three-year moving average of earnings to minimize the impact of earnings management.

This problem can provide an opportunity to discuss the “slippery slope” of earnings management. For example, management’s optimism about next year in part b may not turn out to be warranted. Suppose next year’s “natural” earnings turns out to be $20 million instead of $24 million. Management’s action in the first year will have reduced next year’s $20 million to $17 million, and earnings management would again be required to meet the target. And, if meeting the target in one year causes the next year’s target to increase, things can get out of control very quickly.

©Cambridge Business Publishers, 2014

6-28 Financial Accounting, 4th Edition

P6-44. (40 minutes)(all in $ millions)

a. Net receivables as of January 28, 2012 were $2,033.Net receivables as of January 29, 2011 were $2,026.

b. Bad debts expense (+E, -SE) 101

Allowance for credit losses (+XA) 101

Allowance for credit losses (-XA) 153Accounts receivable (-A) 153

Cash (+A) 22Allowance for credit losses (+XA) 22

c. Estimated credit losses to gross credit card receivables are:

5.5% ($115/$2,074) in 20116.9% ($145/$2,103) in 2010

The decrease in the allowance for credit losses as a percent of credit card receivables is reflected in the aging of Nordstrom’s receivables. The percentage of receivables that are 30 or more days past due has decreased from 3.0% on January 29, 2011 to 2.6% at January 28, 2012. This could be caused by (1) a general improvement in economic conditions (fewer customers are late or defaulting on their obligations), (2) tighter credit policies (credit is denied to risky customers) and/or (3) more rigorous collection practices.

d. The receivables turnover rate is $10,497 / [($2,033 + $2,026)/2] = 5.17Days sales in accounts receivable is $365/5.17 = 70.6 days

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-29

P6-45. (25 minutes)

For the instructor: This problem covers the accounting for product returns, which is not covered in the chapter. The description of The Gap’s practices should allow students to answer parts a and b. Part c is a bit of a stretch, because it requires that the allowance for returns, which is in gross profit terms, be “grossed-up” to revenue terms.

a. Beginning balance + $634 million - $635 million = $21 million, so Beginning balance = $22 million.

b. Sale and expected returns:(1) Record revenue. Cash (+A) 5,000

Revenue (+R,+SE) 5,000(2) Record COGS. Cost of goods sold (+E,-SE) 3,000

Inventory (-A) 3,000(3) Recognize

expected returns.Revenue contra, returns (+XR, -SE) 500

COGS contra, returns (+XE, +SE) 300Sales returns allowance (+L) 200

The sales returns allowance is equal to Gross sales ($5,000) times the probability of return (10%) times the gross profit margin (40%), or $200. For these ten units, the cost of goods was $300.

Returns:(4) Process return

transactions.Inventory (+A) 300Sales returns allowance (-L) 200

Cash (-A) 500

At the conclusion of this transaction, the customers have their cash, the inventory costs have been adjusted to include the returned items, and the sales returns allowance liability has a balance of zero because the actual returns coincided with the expected returns.

continued next page

©Cambridge Business Publishers, 2014

6-30 Financial Accounting, 4th Edition

P6-45. concluded

c. The Gap’s reported gross profit is 36.2% of its net sales ($5,274million/$14,549 million). So, if The Gap expects returns of items with gross profit of $634 million, those items must have had sales prices of $1,751 million ($634 million/0.362) and cost of goods sold of $1,117 million ($1,751 million - $634 million). The entry that would have reflected The Gap’s accounting for these expected returns is the following:

Recognize expected returns.

Revenue contra, returns (+XR, -SE) 1,751COGS contra, returns (+XE, +SE) 1,117Sales returns allowance (+L) 634

The Gap’s gross sales revenue would have been $16,300 million ($14,549 million + $1,751 million), and its expected returns as a percentage of sales would be 10.7% ($1,751 million/$16,300 million).

The size of the allowance for 2011 ($634 million) relative to the end-of-year return liability ($21 million) means that the vast majority of these product returns occurred during the 2011 fiscal year, so it is more a reflection of actual experience than of management’s estimates of future events.

d. Under these circumstances, The Gap doesn’t have to worry about accounting for expected returns, because it has not satisfied the requirements for revenue recognition. If the amount to be received (or in this case, the amount to be kept) is not yet “fixed or determinable,” the revenue should not be recognized until it is.

P6-46. (25 minutes)

a.Fiscal year

ending March 31 Net revenueGrowth

rate2005 3,129 –2006 2,951 -5.7%2007 3,091 4.7%2008 3,665 18.6%2009 4,212 14.9%2010 3,654 -13.2%2011 3,589 -1.8%2012 4,143 15.4%

continued next page

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-31

P6-46. concluded

b.Fiscal year

ending March 31

Net revenue

Deferred net revenue (liability)

Purchases = Net revenue + Change in Deferred net revenue

Growthrate

2005 3,129 0 3,129 –2006 2,951 9 2,960 -5.4%2007 3,091 32 3,114 5.2%2008 3,665 387 4,020 29.1%2009 4,212 261 4,086 1.6%2010 3,654 766 4,159 1.8%2011 3,589 1,005 3,828 -8.0%2012 4,143 1,048 4,186 9.4%

When companies defer revenue, there is a lag between customers’ purchases and the recognition of revenue on the income statement. When purchases grow significantly (as they did in 2008) revenues grow in subsequent years. When purchases fall off, we would expect revenues to fall off in subsequent years (see 2009 and 2010). 2012 appears to be an anomaly. Purchases declined in 2011 but revenue grew significantly in 2012.

c. If customer purchases in 2012 are a leading indicator of revenue in 2013, we would predict a substantial revenue growth for 2013.

©Cambridge Business Publishers, 2014

6-32 Financial Accounting, 4th Edition

CASES and PROJECTS

C6-47. (40 minutes)

a.Cash (+A) 120,000

Sales revenue (+R, +SE) 60,000Payable to merchant partners (+L) 60,000

b. Revenues were previously recorded at the full amount of the Groupon sale ($120,000 in a above) and the amount payable to the merchant partner was recorded as an expense. This was changed in 2011 to record the sale of the Groupon, net of the amount due to the merchant partner as revenue. The effect of this change was that revenues and expenses were reduced by the amount paid to the merchant partner. This did not alter the bottom line as net income does not change. The NOPM ratio would increase due to the decrease in revenue without a corresponding decrease in operating income.

c.Sales revenue contra (-R, -SE) 6,000

Allowance for returns (+L) 6,000

Allowance for returns (-L) 6,000Payable to merchant partners (-L) 6,000

Cash (-A) 12,000

d.Cost of revenue (+E, -SE) 6,000

Allowance for returns (+L) 6,000

Allowance for returns (-L) 6,000Cash (-A) 6,000

e. Groupon could wait to recognize revenue until the 60-day period to pay the merchant partner has expired. By doing so, there would be no need to estimate refunds that would involve reducing the payable or recovering a refund from the merchant partner. Groupon would still need to estimate refunds for any cancelation that might occur after the end of the 60-day period when the merchant partner has been paid. This is when Groupon’s risk is greatest, since it cannot recover any part of the refund from the merchant. However, by waiting 60 days before recognizing the revenue (and estimating the refunds) Groupon would likely have a better idea about the amount of refunds that will likely occur.

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-33

C6-48. (30 minutes)

a. When Dell sells other companies’ software products, it is often as part of a multiple-element sales agreement. For example, the customer may purchase hardware, software, and customer support for one price. This is an example of a bundled sale. Dell must allocate the sales price based on the relative fair market value of each element. Revenue is recognized for each specific element when it is clear that the element has been delivered and the revenue is earned.

There are at least two possibilities for earnings management here. First, Dell could misallocate the sales price. By allocating more of the price to hardware and less to software, Dell may be able to manage when earnings are reported. Second, Dell may be aggressive in applying the “earned and realizable” criteria to each element, thereby prematurely recognizing revenue.

From the information provided, it appears that Dell was recognizing revenue on software “resales” at the time of sale. However, most software is not truly sold. Instead, the customer purchases a license to use the software. As a result, Dell should have deferred part of the revenue and recognized it ratably over the license period.

b. Extended warranties are typically sold separately from other products. Therefore, the revenue should be deferred and recognized ratably over the warranty contract period. Dell employees were apparently recording revenue at the time of sale, or were recognizing the revenue over a shorter time period than the contract period. As a result, revenues and income were overstated.

c. It is common for managers to have performance targets based on revenues and earnings. This provides an incentive for these employees to take actions to accelerate revenue recognition when it appears that targets may not be met. On the other hand, in periods when revenues and earnings exceed the targets, managers may delay revenue recognition until a future period. In this way, they can “store up” revenues and earnings to meet future targets.

The key to preventing this type of abuse is the periodic audit of divisional revenues and earnings. In addition, businesses spend a large amount of resources trying to design incentive compensation plans that do not encourage this type of abuse.

©Cambridge Business Publishers, 2014

6-34 Financial Accounting, 4th Edition

C6-49. (45 minutes)

a. 2011:i. Bad debt expense (+E, -SE) 13,989

Allowance for doubtful accounts (+XA, -A) 13,989

ii. Allowance for doubtful accounts (-XA, +A) 1,206Accounts receivable (-A) 1,206

2012:iii. Bad debt expense (+E, -SE) 2,111

Allowance for doubtful accounts (+XA, -A) 2,111

iv. Allowance for doubtful accounts (-XA, +A) 14,903Accounts receivable (-A) 14,903

- Allowance for Doubtful Accounts (XA) ($000) +Balance 6,859 2010 BalanceSales 13,989 (i)

(ii) 1,206Balance 19,642 2011 Balance

2,111 (iii)(iv) 14,903

6,850 2012 Balance

b. 2011: $19,642 / ($168,310 + $19,642 + $65,664) = 7.7%2010: $6,850 / ($171,561 + $6,850 + $48,612) = 3.0%The extra provision for the Borders account significantly increased Wiley’s allowance account for 2011.

c. If sales returns are material in amount and can be estimated with a reasonable degree of accuracy, they should be estimated just as bad debts are estimated. Sales revenue is debited for the estimated returns while an allowance for returns is credited. One important difference is that with sales returns (unlike bad debts) the customer returns the product to the company and it is often returned to inventory. Hence, the amount of allowance for returns is a net amount equal to the estimated gross profit on expected returns.

continued next page

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-35

C6-49. concluded

d. To record estimated returns:

Sales revenue (est. sales returns) (-R, -SE) 112,948Allowance for returns – A/R (+XA) 112,948

Allowance for returns – Inventory (+A) 17,761Cost of sales (-E, +SE) 17,761

Allowance for returns – royalties payable (+XL) 12,286Royalty expense (-E, +SE) 12,286

To record actual returns:

Allowance for returns – A/R (-XA, +A) 130,000Accounts receivable (-A) 130,000

Inventory (+A) 20,000Allowance for returns – Inventory (-A) 20,000

Royalties payable (-L) 13,963Allowance for returns – Royalties payable (-XL) 13,963

The net amount reported in the allowance for returns consists of three separate amounts – one offsetting accounts receivable (a contra asset) an amount added to inventory (an adjunct asset) and a third amount offsetting royalties payable (a contra liability):

Allowance for returns – A/R: $65,664 + $112,948 - $130,000 = $48,612

Allowance for returns – Inventory: $9,485 + $17,761 - $20,000 = $7,246

Allowance for returns – Royalties: $7,270 + $12,286 - $13,963 = $5,593

Note that $130,000 - $20,000 - $13,963 = $96,037, and $112,948 - $17,761 - $12,286 = $82,901.

When these three accounts are combined, we get the net amount reported in the allowance for returns each year.

e. Accounts receivable turnover: $1,782,742 / [($171,561 + $168,310)/2] = 10.5 times.

Average collection period: 365 / 10.5 = 34.8 days.

©Cambridge Business Publishers, 2014

6-36 Financial Accounting, 4th Edition

©Cambridge Business Publishers, 2014

Solutions Manual, Chapter 6 6-37