factors effecting estimation of working capital

TRANSCRIPT

1

Factors Affecting Estimation of Working Capital

INDEX

Sr. No. Particulars Page No.

1. Introduction and Meaning 2-7

2. Factors affecting working capital or determinants of

working capital

8-13

3. Methods for estimating working capital requirement 14-23

4. Estimation of working capital calculation 24-30

5. Bibliography 31

2

INTRODUCTION AND MEANING:

What is 'Working Capital'

Working capital is a measure of both a company's efficiency and its short-term financial health.

Working capital is calculated as:

Working Capital = Current Assets - Current Liabilities

The working capital ratio (Current Assets/Current Liabilities) indicates whether a company has

enough short term assets to cover its short-term debt. Anything below 1 indicates negative W/C

(working capital). While anything over 2 means that the company is not investing excess assets.

Most believe that a ratio between 1.2 and 2.0 is sufficient. Also, known as "net working capital".

If a company's current assets do not exceed its current liabilities, then it may run into trouble

paying back creditors in the short term. The worst-case scenario is bankruptcy. A declining

working capital ratio over a longer time period could also be a red flag that warrants further

analysis. For example, it could be that the company's sales volumes are decreasing and, as a result,

its accounts receivables number continues to get smaller and smaller.Working capital also gives

investors an idea of the company's underlying operational efficiency. Money that is tied up in

inventory or money that customers still owe to the company cannot be used to pay off any of the

company's obligations. So, if a company is not operating in the most efficient manner (slow

collection), it will show up as an increase in the working capital. This can be seen by comparing

the working capital from one period to another; slow collection may signal an underlying problem

in the company's operations.

• If the ratio is less than one then they have negative working capital.

• A high working capital ratio isn't always a good thing, it could indicate that they have too

much inventory or they are not investing their excess cash

Working capital (abbreviated WC) is a financial metric which represents operating

liquidity available to a business, organization or other entity, including governmental entity.

Along with fixed assets such as plant and equipment, working capital is considered a part of

3

operating capital. Gross working capital equals to current assets. Working capital is calculated

as current assets minus current liabilities.[1] If current assets are less than current liabilities,

an entity has a working capital deficiency, also called a working capital deficit.

A company can be endowed with assets and profitability but short of liquidity if its assets

cannot readily be converted into cash. Positive working capital is required to ensure that a firm

is able to continue its operations and that it has sufficient funds to satisfy both maturing short-

term debt and upcoming operational expenses. The management of working capital involves

managing inventories, accounts receivable and payable, and cash.

Working capital is the difference between the current assets and the current liabilities.

The basic calculation of the working capital is done on the basis of the gross current assets of

the firm.

Current assets and current liabilities include three accounts which are of special importance. These

accounts represent the areas of the business where managers have the most direct impact:

• Accounts receivable (current asset)

• Inventory (current assets), and

• Accounts payable (current liability)

The current portion of debt (payable within 12 months) is critical, because it represents a short-

term claim to current assets and is often secured by long-term assets. Common types of short-term

debt are bank loans and lines of credit.

An increase in net working capital indicates that the business has either increased current

assets (that it has increased its receivables, or other current assets) or has decreased current

liabilities—for example has paid off some short-term creditors, or a combination of both.

4

Working capital is that amount of funds which is required to carry out the day-to-day operations

of an enterprise-whether big or small. It may also be regarded as that portion of an enterprise’s

total capital which is employed in its short-term operations.

These operations consist of primarily such items as raw materials, semi-processed goods, sundry

debtors, finished products, short-term investments, etc. Thus, working capital also refers to all the

short-term assets known as current assets used in day-to-day operations of an enterprise.

The Accounting Principles Board of the American Institute of Certified Public Accountants,

U.S.A. has defined working capital as follows:

“Working capital, sometimes called net working capital, is represented by the excess of current

assets over current liabilities and identifies the relatively liquid portion of total enterprise capital

which constitutes a margin of buffer for maturing obligations within the ordinary operating cycle

of the business.”

What is an Operating Cycle:

Working capital is also called a circulating capital or revolving capital. That is the money/capital

which circulates in various forms of current assets in a continued manner. For example, at a point

of time, funds may be tied up in raw materials, then later converted into semi-finished products,

then into finished/ final products and when these finished products are sold, it is converted either

into account receivables or cash.

This cash is reinvested in current assets. Thus, the amount always keeps on circulating or revolving

from cash to current assets and back again to cash. That is why some people prefer to use the term

liquidity management instead of working capital management. Although this circulation takes

place at short intervals, the money is required again and again.

The American Institute of Certified Public Accountants defined the operating cycle as: “the

average time intervening between the acquisition of material or services entering the process and

the final cash realisation.”

5

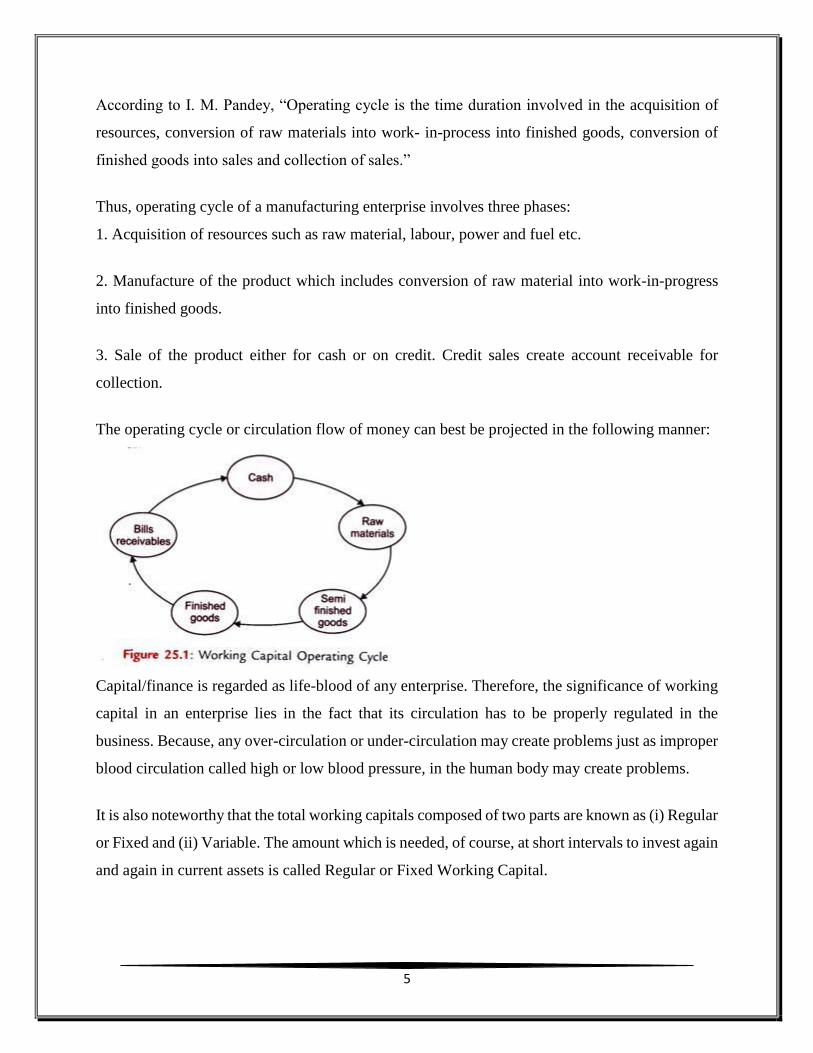

According to I. M. Pandey, “Operating cycle is the time duration involved in the acquisition of

resources, conversion of raw materials into work- in-process into finished goods, conversion of

finished goods into sales and collection of sales.”

Thus, operating cycle of a manufacturing enterprise involves three phases:

1. Acquisition of resources such as raw material, labour, power and fuel etc.

2. Manufacture of the product which includes conversion of raw material into work-in-progress

into finished goods.

3. Sale of the product either for cash or on credit. Credit sales create account receivable for

collection.

The operating cycle or circulation flow of money can best be projected in the following manner:

Capital/finance is regarded as life-blood of any enterprise. Therefore, the significance of working

capital in an enterprise lies in the fact that its circulation has to be properly regulated in the

business. Because, any over-circulation or under-circulation may create problems just as improper

blood circulation called high or low blood pressure, in the human body may create problems.

It is also noteworthy that the total working capitals composed of two parts are known as (i) Regular

or Fixed and (ii) Variable. The amount which is needed, of course, at short intervals to invest again

and again in current assets is called Regular or Fixed Working Capital.

6

In fact, this investment is irreducible minimum and remains permanently sunk in the enterprise.

The other part of the working capital may vary due to the fluctuations {i.e. Rise or fall) in the

volume of business. Hence, it is called as the ‘Variable Working Capital.’

The two parts of working capital are shown in the Figure 25.2.

Figure 25.2 clearly illustrates the difference between fixed and variable working capital. However,

the fixed working capital line need not be horizontal if the firm’s requirement for fixed working

capital is increasing or decreasing over the period.

For a growing enterprise, the difference between fixed and variable working capital can be

depicted through the following Figure 25.3.

What is Net Operating Cycle:

The net operating cycle, also called the cash conversion cycle, is the number of days it takes a

company to generate revenues with assets.

How it works (example):

Analysts can calculate the length of the cycle with the following formula:

7

Net Operating Cycle = Days Inventory Outstanding + Days Sales Outstanding + Days Payables

Outstanding

Note that DPO is a negative number.

The net operating cycle involves determining how long it takes to create inventory, sell inventory

and collect on invoices to customers. For example, let's say Company XYZ makes widgets, which

typically sit in the warehouse for 10 days. Let's also assume that it typically takes 15 days to collect

on the sale of each widget, and that it takes 14 days to pay invoices to Company XYZ's vendors.

Using the formula above, Company XYZ's net operating cycle is:

Net Operating Cycle = 10 + 15 + -14 = 11 days

This means that Company XYZ generates cash from its assets within 11 days.

Why it matters:

The net operating cycle is a measure of how long an investment is locked up in production before

turning into cash.

Changes in net operating cycle can be very telling. For example, when companies take a long time

to collect on outstanding bills, or they overproduce and fill up the warehouse because they can't

figure out what sells, their net operating cycles lengthen. For small businesses especially, long net

operating cycles can be the difference between profit and bankruptcy. After all, companies can

only pay for things with cash, not profits. In turn, the net operating cycle is a measure of managerial

competency as well as operational efficiency.

It is important to note that different industries have different capital requirements and standards,

and determining whether a company has a long or short net operating cycle should be made within

that context.

8

FACTORS AFFECTING WORKING CAPITAL OR DETERMINANTS OF

WORKING CAPITAL

Requirements Of working capital depend upon various factors such as nature of business, size of

business, the flow of business activities. However, small organization relatively needs lesser

working capital than the big business organization. Following are the factors which affect the

working capital of a firm:

1. Size of business

The requirement of working capital depends on the nature of business. The nature of business is

usually of two types: Manufacturing Business and Trading Business. In the case of manufacturing

business, it takes a lot of time in converting raw material into finished goods. Therefore, capital

remains invested for a long time in raw material, semi-finished goods and the stocking of the

finished goods. Working capital requirement of a firm is directly influenced by the size of its

business operation. Big business organizations require more working capital than the small

business organization. Therefore, the size of organization is one of the major determinants of

working capital. Consequently, more working capital is required. On the contrary, in case of

trading business the goods are sold immediately after purchasing or sometimes the sale is affected

even before the purchase itself. Therefore, very little working capital is required. Moreover, in

case of service businesses, the working capital is almost nil since there is nothing in stock.

2. Nature of Business

Working capital requirement depends upon the nature of business carried by the firm. Normally,

manufacturing industries and trading organizations need more working capital than in the service

business organizations. A service sector does not require any amount of stock of goods. In service

enterprises, there are less credit transactions. But in the manufacturing or trading firm, credit sales

and advance related transactions are in large amount. So, they need more working capital.

9

3.Storage time or processing period

Time needed for keeping the stock in store is called storage period. The amount of working capital

is influenced by the storage period. If storage period is high, a firm should keep more quantity of

goods in store and hence requires more working capital. Similarly, if the processing time is more,

then more stock of goods must be held in store as work-in-progress.

4.Credit Period

Credit period allowed to customers is also one of the major factors which influence the requirement

of working capital. Longer credit period requires more investment in debtors and hence more

working capital is needed. But, the firm which allows less credit period to customers’ needs less

working capital.

5.Seasonal requirement

In certain business, raw material is not available throughout the year. Such business organizations

have to buy raw material in bulk during the season to ensure an uninterrupted flow and process

them during the entire year. Thus, a huge amount is blocked in the form of raw material inventories

which gives rise to more working capital requirements.

6.Potential growth or expansion of business

If the business is to be extended in future, more working capital is required. More amount of

Working capital is required to meet the expansion need of business.

7.Changes in price level

Change in price level also affects the working capital requirements. Generally, the rise in price

will require the firm to maintain large amount of working capital as more funds will be required

to maintain the sale level of current assets.

10

8.Dividend Policy

The dividend policy of the firm is an important determinant of working capital. The need for

working capital can be met with the retained earnings. If a firm retains more profit and distributes

lower amount of dividend, it needs less working capital.

9.Access to money market

If a firm has good access to capital market, it can raise loan from bank and financial institutions.

It results in minimization of need of working capital.

10.Working capital cycle

When the working capital cycle of a firm is long, it will require larger amount of working capital.

But, if working capital cycle is short, it will need less working capital.

11.Operating efficiency

The operating efficiency of a firm also affects the firm's need of working capital. The operating

efficiency of the firm results in optimum utilization of assets. The optimum utilization of assets in

turn results in more fund release for working capital.

12. Scale of Operation

There is a direct link between the working capital and the scale of operations. In other words, more

working capital is required in case of big organisations while less working capital is needed in case

of small organizations.

11

13. Business Cycle

The need for the working capital is affected by various stages of the business cycle. During the

boom period, the demand of a product increases and sales also increase. Therefore, more working

capital is needed. On the contrary, during the period of depression, the demand declines and it

affects both the production and sales of goods. Therefore, in such a situation less working capital

is required.

14. Seasonal Factors

Some goods are demanded throughout the year while others have seasonal demand. Goods which

have uniform demand the whole year their production and sale are continuous. Consequently, such

enterprises need little working capital. On the other hand, some goods have seasonal demand but

the same are produced almost the whole year so that their supply is available readily when

demanded. Such enterprises have to maintain large stocks of raw material and finished products

and so they need large amount of working capital for this purpose. Woolen mills are a good

example of it.

15. Production Cycle

Production cycle means the time involved in converting raw material into finished product. The

longer this period, the more will be the time for which the capital remains blocked in raw material

and semi-manufactured products. Thus, more working capital will be needed. On the contrary,

where period of production cycle is little, less working capital will be needed.

16. Credit Allowed

Those enterprises which sell goods on cash payment basis need little working capital but those

who provide credit facilities to the customers need more working capital.

12

17. Credit Availed

If raw material and other inputs are easily available on credit, less working capital is needed. On

the contrary, if these things are not available on credit then to make cash payment quickly large

amount of working capital will be needed.

18. Operating Efficiency

Operating efficiency means efficiently completing the various business operations. Operating

efficiency of every organization happens to be different. Some such examples are:

(i) converting raw material into finished goods at the earliest, (ii) selling the finished goods

quickly, and

(ii) (iii) quickly getting payments from the debtors. A company which has a better

operating efficiency has to invest less in stock and the debtors. Therefore, it requires

less working capital, while the case is different in respect of companies with less

operating efficiency.

19. Availability of Raw Material

Availability of raw material also influences the amount of working capital. If the enterprise makes

use of such raw material which is available easily throughout the year, then less working capital

will be required, because there will be no need to stock it in large quantity. On the contrary, if the

enterprise makes use of such raw material which is available only in some particular months of the

year whereas for continuous production it is needed all the year round, then large quantity of it

will be stocked. Under the circumstances, more working capital will be required.

20. Growth Prospects

Growth means the development of the scale of business operations (production, sales, etc.). The

organisations which have sufficient possibilities of growth require more working capital, while the

case is different in respect of companies with less growth prospects.

13

21. Level of Competition

High level of competition increases the need for more working capital. In order to face

competition, more stock is required for quick delivery and credit facility for a long period has to

be made available.

22. Inflation

Inflation means rise in prices. In such a situation, more capital is required than before in order to

maintain the previous scale of production and sales. Therefore, with the increasing rate of inflation,

there is a corresponding increase in the working capital.

14

METHODS FOR ESTIMATING WORKING CAPITAL REQUIREMENT

There are broadly three methods of estimating or analyzing the requirement of working capital of

a company viz. Percentage of revenue or sales, regression analysis, and operating cycle method.

Estimating working capital means calculating future working capital. It should be as accurate as

possible because the planning of working capital would be based on these estimates and bank and

other financial institutes finance the working capital needs to be based on such estimates only.

PERCENTAGE OF SALES METHOD:

In this method, level of working capital requirements is decided on the basis of past experience.

The past relationship between sales and working capital is taken as a base for determining the size

of working capital requirements for future. It is, however, presumed that relationship between sales

and working capital, as existed in the past, has been stable.

It is the easiest of the methods for calculating the working capital requirement of a company. This

method is based on the principle of ‘history repeats itself’. For estimating, a relationship of sales

and working capital is worked out for say last 5 years. If it is constantly coming near say 40% i.e.

Working capital level is 40% of sales, the next year estimation is done based on this estimate. If

the expected sales are 500 million dollars, 200 million dollars would be required as working

capital.

The advantage of this method is that it is very simple to understand and calculate also.

Disadvantage includes its assumption which is difficult to be true for many organizations. So,

where there is no linear relationship between the revenue and working capital, this method is not

useful. In new startup projects, also, this method is not applicable because there is no past.

Advantages and Disadvantages of Percentage of Sales Method

Advantages of this method are that it is easy to understand and simple to calculate. There is not

rocket science in calculating the working capital based on this method.

The biggest disadvantage is its assumption which is not very practical in all situations. This method

is useful only where the relation between the revenue and working capital is linear. Elsewhere this

15

method is not suggested. Another drawback is that it is highly dependent on sales forecast. If the

sales forecast is faulty, a whole calculation will be faulty. Higher working capital would attract

higher interest cost and low profitability and lower working capital would pose a problem to the

smoothness of the operating cycle.

Illustration:

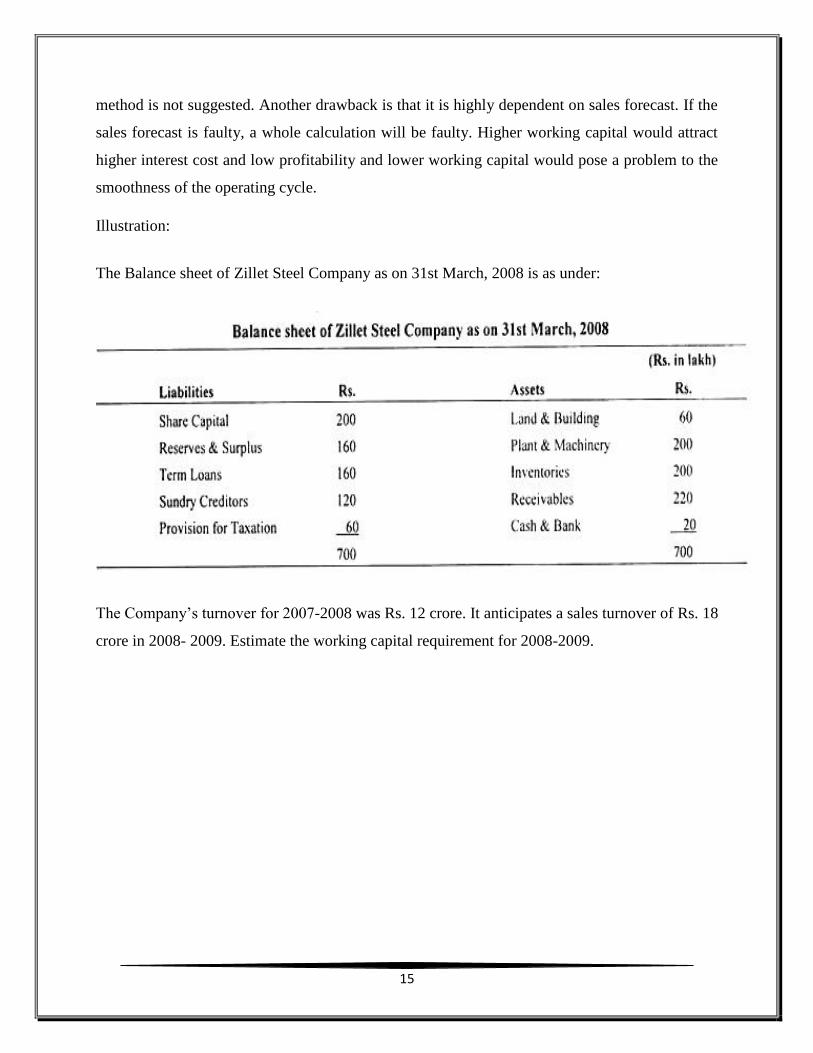

The Balance sheet of Zillet Steel Company as on 31st March, 2008 is as under:

The Company’s turnover for 2007-2008 was Rs. 12 crore. It anticipates a sales turnover of Rs. 18

crore in 2008- 2009. Estimate the working capital requirement for 2008-2009.

16

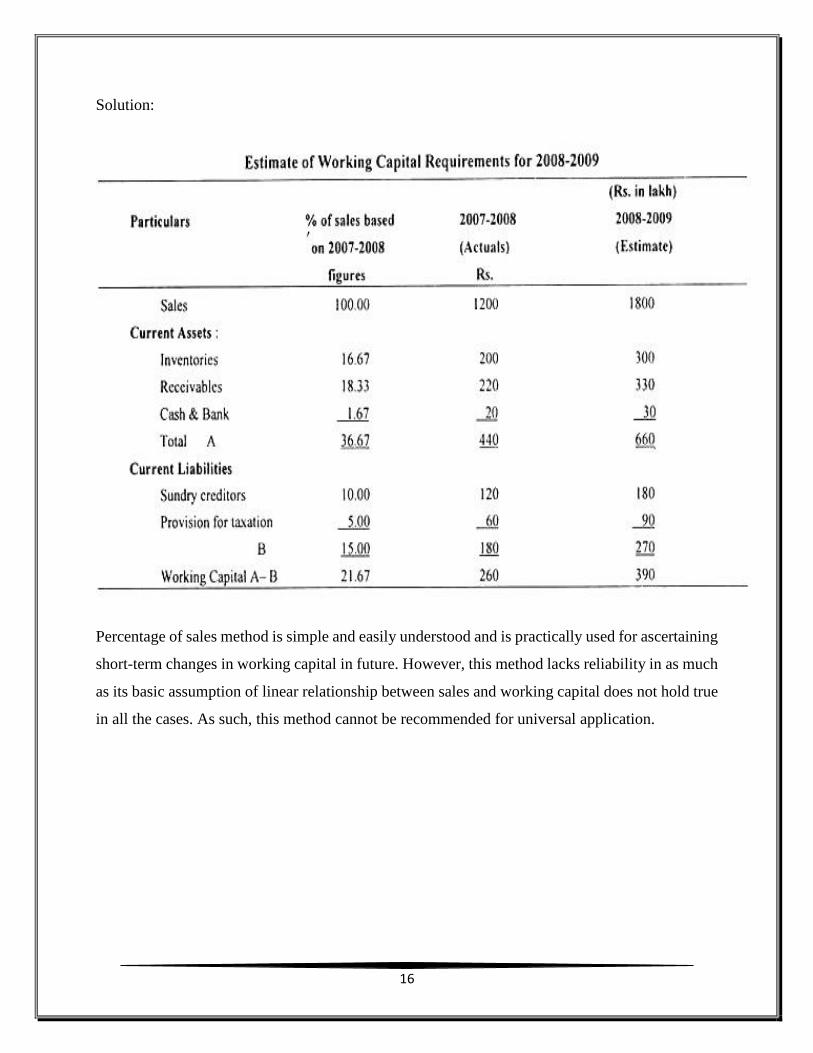

Solution:

Percentage of sales method is simple and easily understood and is practically used for ascertaining

short-term changes in working capital in future. However, this method lacks reliability in as much

as its basic assumption of linear relationship between sales and working capital does not hold true

in all the cases. As such, this method cannot be recommended for universal application.

17

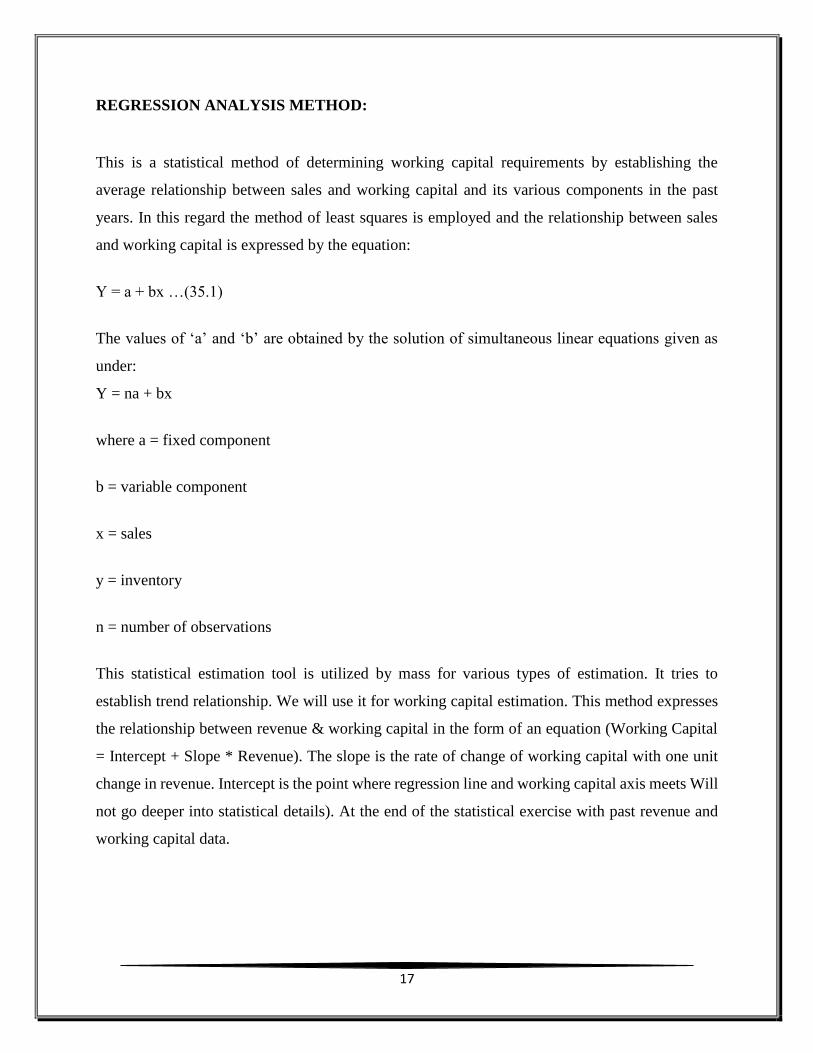

REGRESSION ANALYSIS METHOD:

This is a statistical method of determining working capital requirements by establishing the

average relationship between sales and working capital and its various components in the past

years. In this regard the method of least squares is employed and the relationship between sales

and working capital is expressed by the equation:

Y = a + bx …(35.1)

The values of ‘a’ and ‘b’ are obtained by the solution of simultaneous linear equations given as

under:

Y = na + bx

where a = fixed component

b = variable component

x = sales

y = inventory

n = number of observations

This statistical estimation tool is utilized by mass for various types of estimation. It tries to

establish trend relationship. We will use it for working capital estimation. This method expresses

the relationship between revenue & working capital in the form of an equation (Working Capital

= Intercept + Slope * Revenue). The slope is the rate of change of working capital with one unit

change in revenue. Intercept is the point where regression line and working capital axis meets Will

not go deeper into statistical details). At the end of the statistical exercise with past revenue and

working capital data.

18

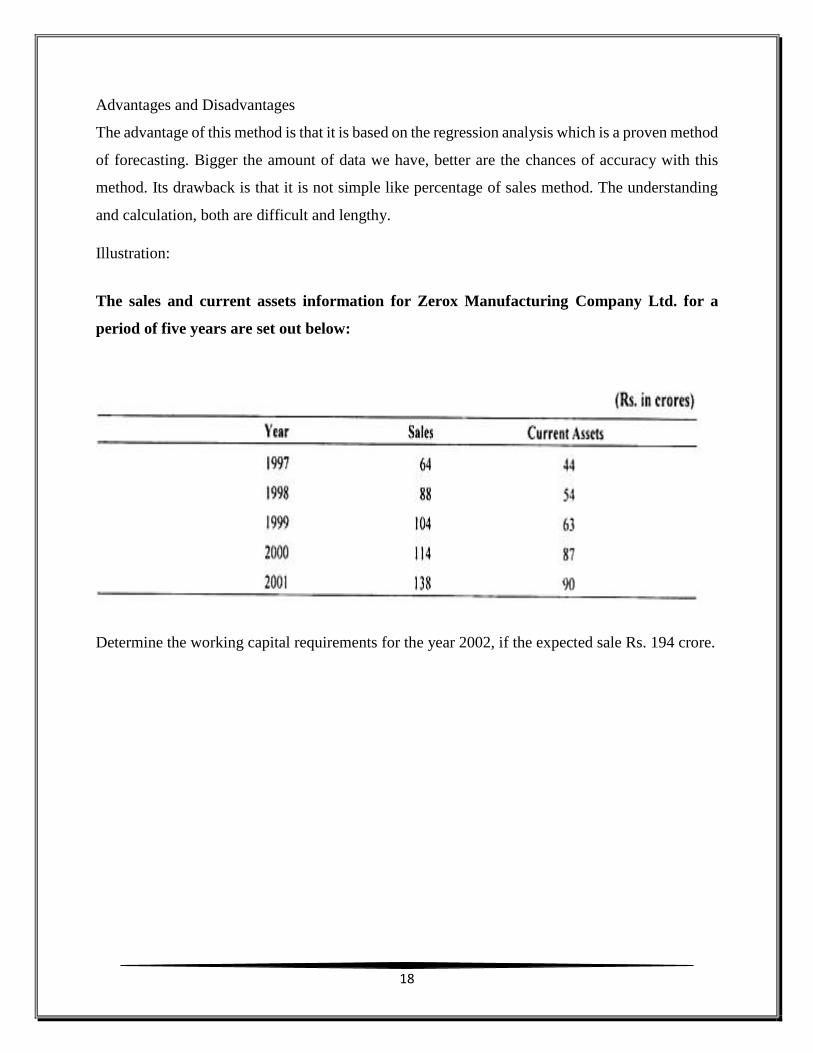

Advantages and Disadvantages

The advantage of this method is that it is based on the regression analysis which is a proven method

of forecasting. Bigger the amount of data we have, better are the chances of accuracy with this

method. Its drawback is that it is not simple like percentage of sales method. The understanding

and calculation, both are difficult and lengthy.

Illustration:

The sales and current assets information for Zerox Manufacturing Company Ltd. for a

period of five years are set out below:

Determine the working capital requirements for the year 2002, if the expected sale Rs. 194 crore.

19

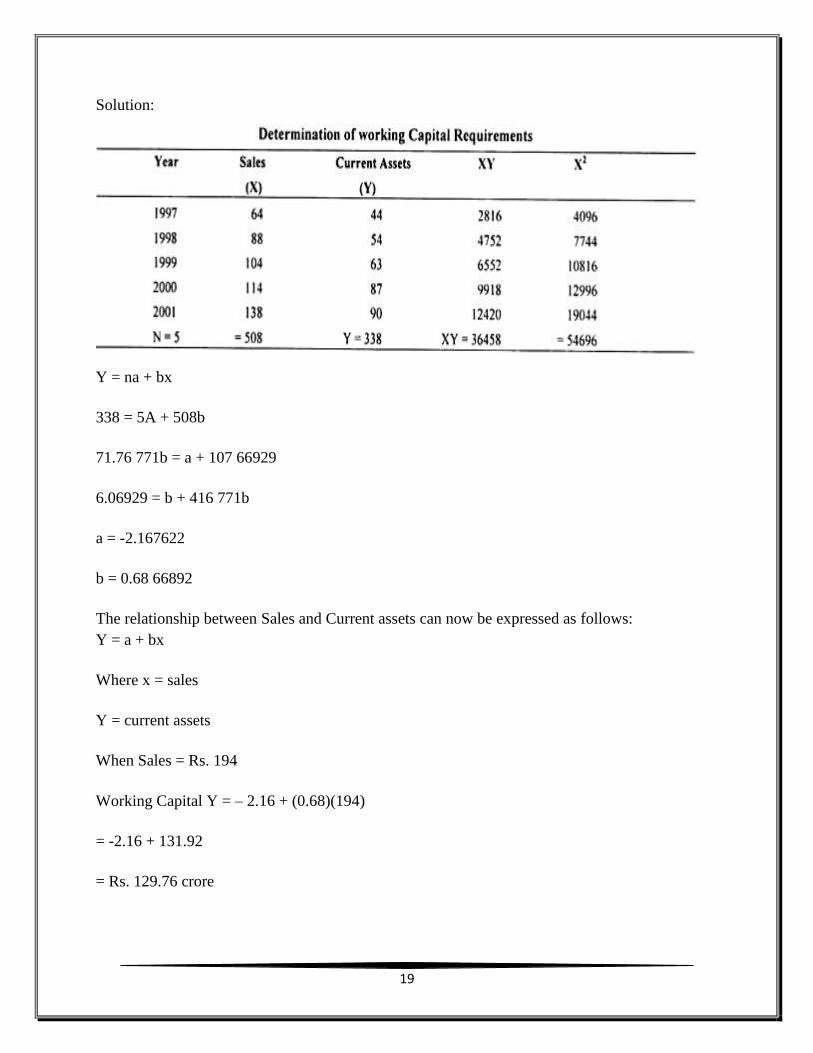

Solution:

Y = na + bx

338 = 5A + 508b

71.76 771b = a + 107 66929

6.06929 = b + 416 771b

a = -2.167622

b = 0.68 66892

The relationship between Sales and Current assets can now be expressed as follows:

Y = a + bx

Where x = sales

Y = current assets

When Sales = Rs. 194

Working Capital Y = – 2.16 + (0.68)(194)

= -2.16 + 131.92

= Rs. 129.76 crore

20

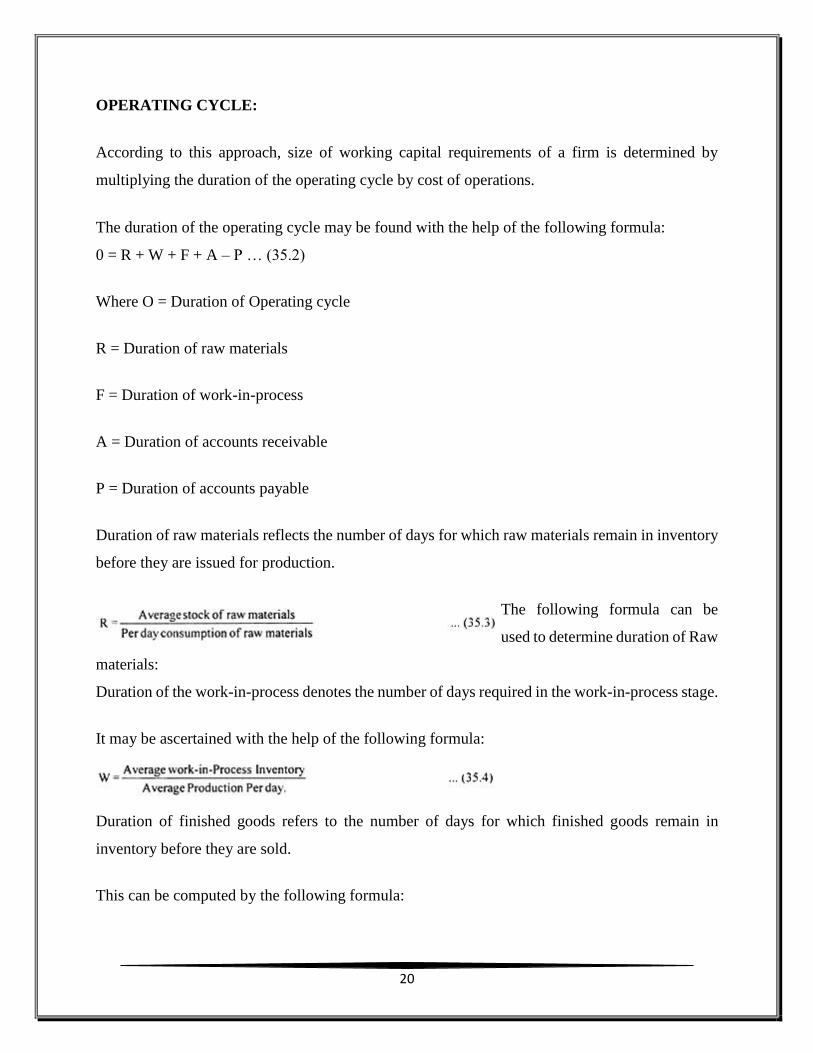

OPERATING CYCLE:

According to this approach, size of working capital requirements of a firm is determined by

multiplying the duration of the operating cycle by cost of operations.

The duration of the operating cycle may be found with the help of the following formula:

0 = R + W + F + A – P … (35.2)

Where O = Duration of Operating cycle

R = Duration of raw materials

F = Duration of work-in-process

A = Duration of accounts receivable

P = Duration of accounts payable

Duration of raw materials reflects the number of days for which raw materials remain in inventory

before they are issued for production.

The following formula can be

used to determine duration of Raw

materials:

Duration of the work-in-process denotes the number of days required in the work-in-process stage.

It may be ascertained with the help of the following formula:

Duration of finished goods refers to the number of days for which finished goods remain in

inventory before they are sold.

This can be computed by the following formula:

21

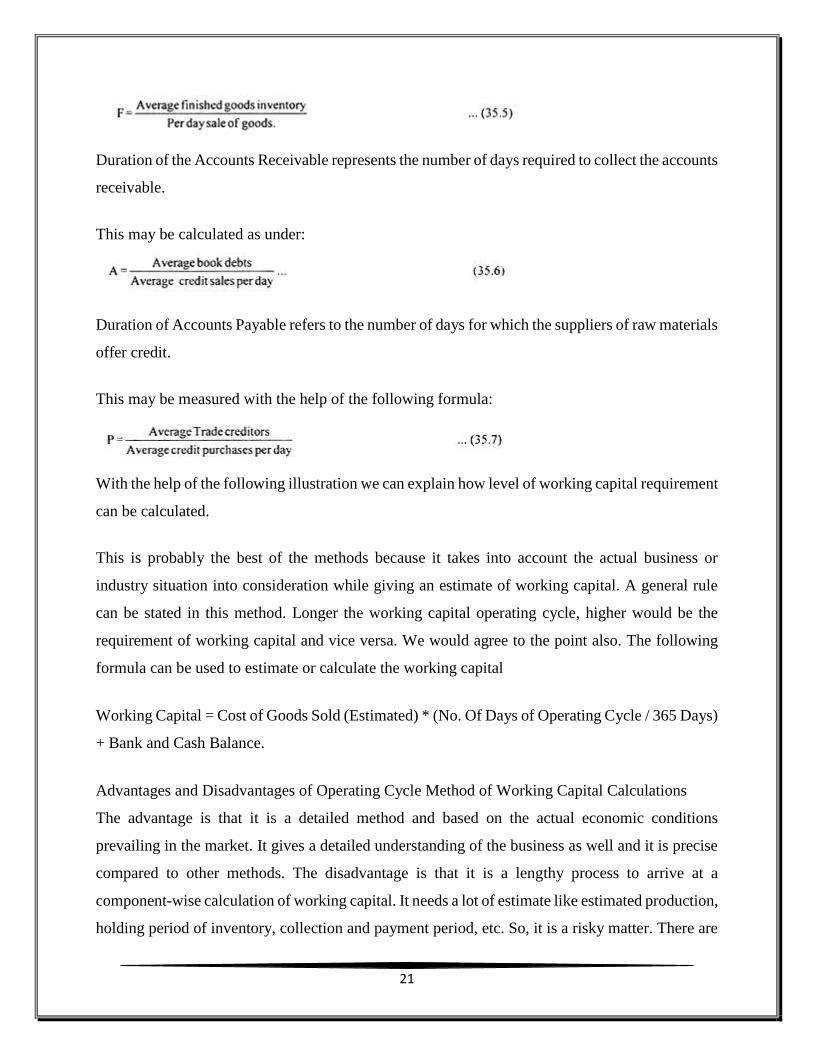

Duration of the Accounts Receivable represents the number of days required to collect the accounts

receivable.

This may be calculated as under:

Duration of Accounts Payable refers to the number of days for which the suppliers of raw materials

offer credit.

This may be measured with the help of the following formula:

With the help of the following illustration we can explain how level of working capital requirement

can be calculated.

This is probably the best of the methods because it takes into account the actual business or

industry situation into consideration while giving an estimate of working capital. A general rule

can be stated in this method. Longer the working capital operating cycle, higher would be the

requirement of working capital and vice versa. We would agree to the point also. The following

formula can be used to estimate or calculate the working capital

Working Capital = Cost of Goods Sold (Estimated) * (No. Of Days of Operating Cycle / 365 Days)

+ Bank and Cash Balance.

Advantages and Disadvantages of Operating Cycle Method of Working Capital Calculations

The advantage is that it is a detailed method and based on the actual economic conditions

prevailing in the market. It gives a detailed understanding of the business as well and it is precise

compared to other methods. The disadvantage is that it is a lengthy process to arrive at a

component-wise calculation of working capital. It needs a lot of estimate like estimated production,

holding period of inventory, collection and payment period, etc. So, it is a risky matter. There are

22

probable chances of going wrong in estimating these data and that may hurt the whole process. It

is advisable to keep a cushion while estimating things on the darker side.

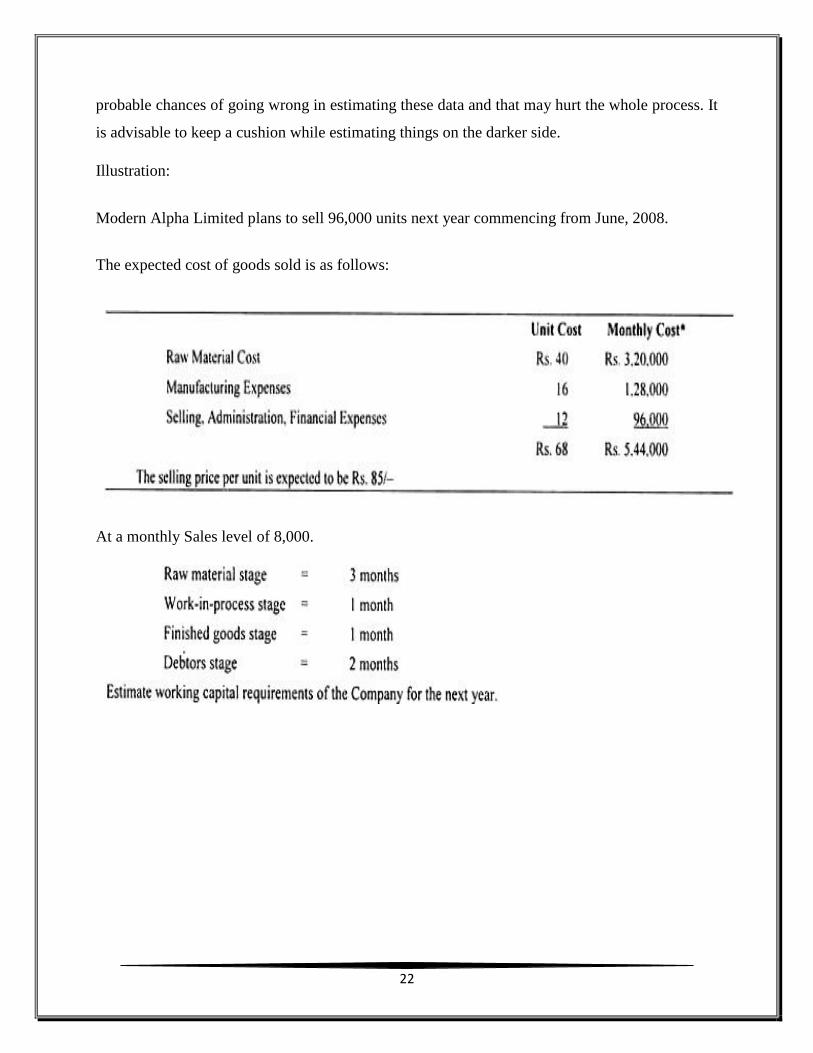

Illustration:

Modern Alpha Limited plans to sell 96,000 units next year commencing from June, 2008.

The expected cost of goods sold is as follows:

At a monthly Sales level of 8,000.

23

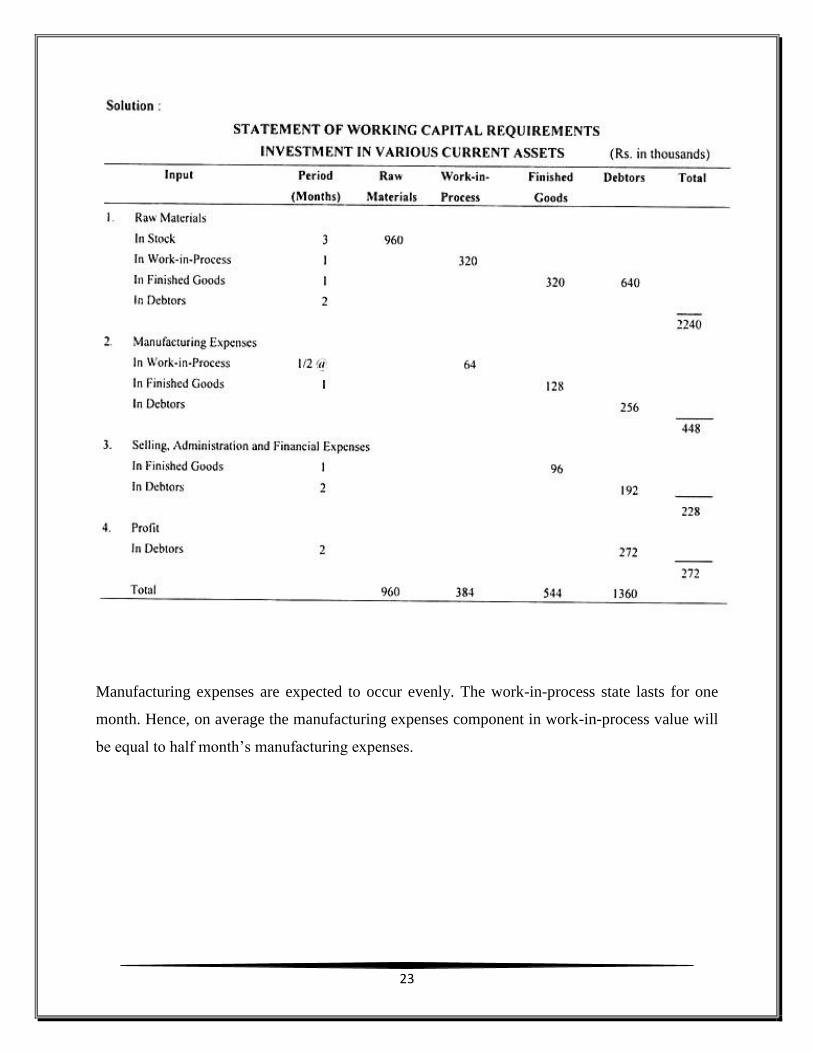

Manufacturing expenses are expected to occur evenly. The work-in-process state lasts for one

month. Hence, on average the manufacturing expenses component in work-in-process value will

be equal to half month’s manufacturing expenses.

24

ESTIMATION OF WORKING CAPITAL CALCULATION

PERCENTAGE OF SALES METHOD

Percentage of sales method is a working capital forecasting method which is based on past

relationship between sales and working capital. Just like technical analysis in the stock market, it

assumes that the history will repeat itself and thus the ratio of working capital to sales will remain

constant. In other words, it assumes that the whole business will move in tandem with sales.

How to Calculate Working Capital Using Percentage of Sales Method?

Percentage of sales method is the simplest and easiest way of finding future working capital. First,

each component of working capital as a percentage of sales is calculated. Like, accounts payable

are 20 million, and sales are 100 million, accounts payable as a percentage of sales would be 20%.

Secondly, the coming year sales forecast is taken as a base and the component is calculated as per

the percentage. In our instant example, if forecasted sales are 150 million, accounts payable should

be 30 million. This is as simple as that. Let us see a practical example with formula and example.

Percentage of Sales Method Formula = Component of Working Capital * 100 / Sales of the Year

Percentage of Sales Method Example

Consider following balance sheet for the year 2014 as an example. The sales for 2014 are $400.

The forecasted sales figure for the year 2015 is $600.

25

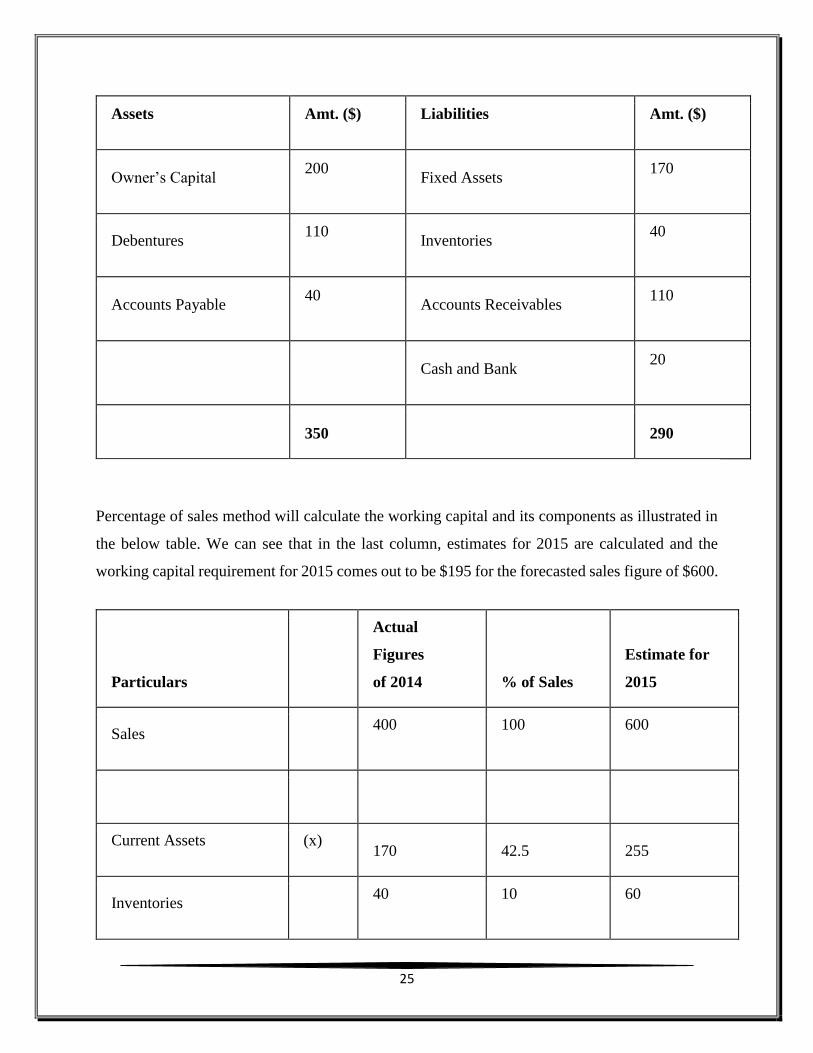

Assets Amt. ($) Liabilities Amt. ($)

Owner’s Capital 200

Fixed Assets 170

Debentures 110

Inventories 40

Accounts Payable 40

Accounts Receivables 110

Cash and Bank 20

350

290

Percentage of sales method will calculate the working capital and its components as illustrated in

the below table. We can see that in the last column, estimates for 2015 are calculated and the

working capital requirement for 2015 comes out to be $195 for the forecasted sales figure of $600.

Particulars

Actual

Figures

of 2014 % of Sales

Estimate for

2015

Sales

400 100 600

Current Assets (x) 170 42.5 255

Inventories

40 10 60

26

Accounts Receivables

110 27.5 165

Cash and Bank

20 5 20

Current Liabilities (y) 40 10 60

Accounts Payable

40 10 60

Working Capital (x-y) 130 32.5 195

REGRESSION ANALYSIS

The Regression analysis, a statistical tool, is used to estimate the working capital and its

components. It establishes an equation relationship between revenue and working capital. It can

also be called trend analysis because the relation is carved out based on past trend. Without going

into technical details, this method says ‘Working Capital = Intercept + Slope * Revenue’.

The standard equation is stated as below:

y = a + bx

In our case, y represents the working capital because that is to be forecasted. x represents sales as

it is the base for finding out the working capital. a & b are intercept and slope. A slope is the rate

of change of working capital with one unit change in revenue. Intercept is the point where

regression line and working capital axis meets. At the end of the statistical exercise with past

revenue and working capital data, we will get an equation as explained above with real values of

a and b. Then we will be able to find out y (working capital) for a given x (forecasted sales).

27

How to Calculate Working Capital using Regression Analysis with Formula and Example

Let us try to understand what we have to do for getting our estimates rather than understanding too

much technical statistics. See the following table. The first column is a year, a second is sales and

third is working capital. As we required the past data for future forecasting, here we have our past

data. The fourth column is the product of sales and working capital and a fifth is the square of

sales.

Sr.

No. Year

Sales

(x)

Working

Capital

(y)

Product of

Sales (x)

and

Working

Capital (y)

x*y

Square of

Sales (x)

x2

1 2001

100 55 5,500 10,000

2 2002

110 64 7,040 12,100

3 2003

121 80 9,680 14,641

4 2004

130 70 9,100 16,900

5 2005

150 90 13,500 22,500

6 2006

180 120 21,600 32,400

7 2007

181 100 18,100 32,761

8 2008

190 140 26,600 36,100

28

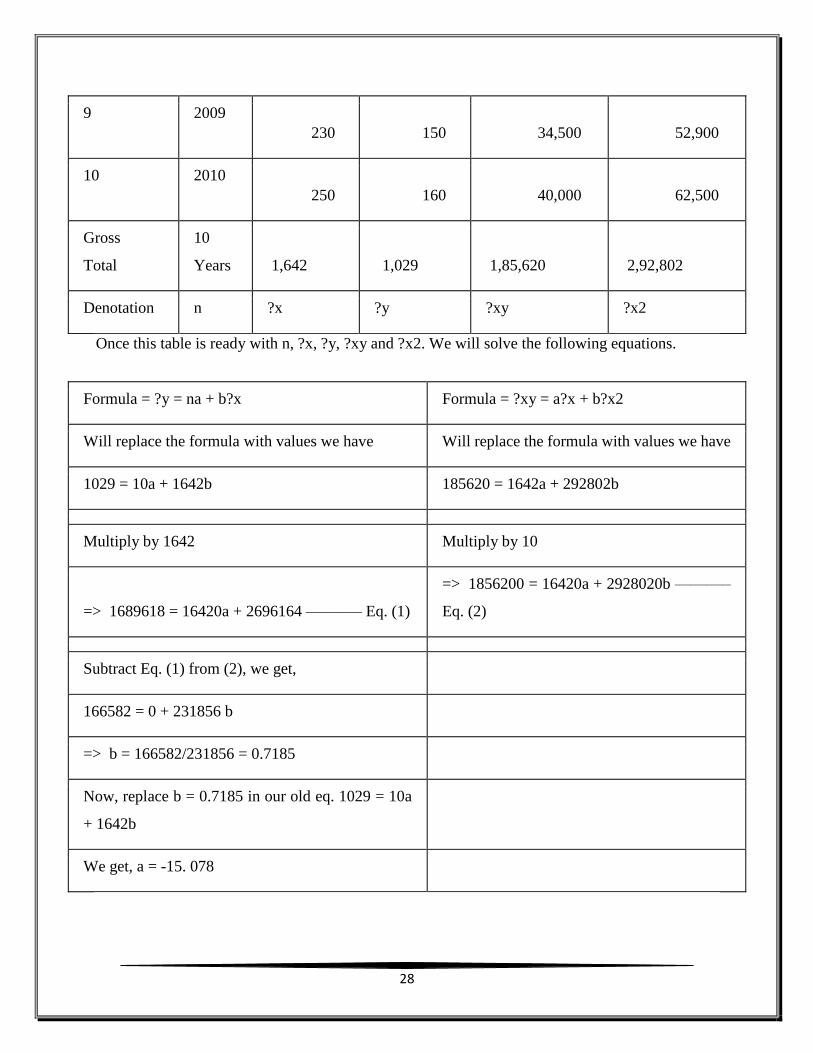

9 2009

230 150 34,500 52,900

10 2010

250 160 40,000 62,500

Gross

Total

10

Years 1,642 1,029 1,85,620 2,92,802

Denotation n ?x ?y ?xy ?x2

Once this table is ready with n, ?x, ?y, ?xy and ?x2. We will solve the following equations.

Formula = ?y = na + b?x Formula = ?xy = a?x + b?x2

Will replace the formula with values we have Will replace the formula with values we have

1029 = 10a + 1642b 185620 = 1642a + 292802b

Multiply by 1642 Multiply by 10

=> 1689618 = 16420a + 2696164 ———– Eq. (1)

=> 1856200 = 16420a + 2928020b ———–

Eq. (2)

Subtract Eq. (1) from (2), we get,

166582 = 0 + 231856 b

=> b = 166582/231856 = 0.7185

Now, replace b = 0.7185 in our old eq. 1029 = 10a

+ 1642b

We get, a = -15. 078

29

After all this exercise, we get the following equation,

Working Capital (x) = -15.078 + 0.7185 Sales (b)

Now, if the forecasted sales for the year 2015 are 300, the working capital as per this method would

be 200.472. (Working Capital = -15.078 + 0.7185 * 300 = 200.472). In the similar fashion, all the

components can be calculated.

OPERATING CYCLE METHOD

Operating cycle method of working capital estimation is based on the duration of operating cycle.

Longer the period of the cycle, bigger will be the working capital requirements. Operating cycle

means the cycle of raw material to work in progress to finished goods to accounts payable and

finally to cash. Operating cycle time is the time taken starting from raw material purchases to its

conversion into cash.

How to calculate or estimate working capital using this method?

For calculating the working capital, we would need 3 important things and they have estimated

cost of goods sold, operating cycle time, and desired cash levels. The time of cycle can be

calculated using operating cycle formula.

Formula for calculating working capital requirement directly is as follows:

Working Capital = {Estimated Cost of Goods Sold * (Operating Cycle/ 365)} +Desired Cash and

Bank Balance

Calculating the total working capital will not suffice the purpose. How this working capital is

formed is also important. It means each component of working capital will have to be known. For

that, we would first need the activity level of the company under review. Let us see how to calculate

each item of working capital below:

Raw Material (RM) Stock: The formula for determining the RM stock is mentioned below. RM

and many other calculations are based on estimated production units and therefore it should be

calculated with utmost accuracy.

Estimated Production Units * Per Unit Cost of RM * (RM Holding Period / 365 Days)

30

Work In Progress (WIP): In calculating the WIP, special care has to be taken of the percentage of

labor and overheads. These may vary depending on the stage of the product and completion

percentage. We have taken the percentage for an example.

Estimated Production * {Per Unit Cost of — RM (100%) + Labor (50%) + Overheads (50%)} *

(Work In Progress Period / 365 Days)

Finished Goods Stock: In Finished Goods workings, we have to know the cost of production with

the help of the previous year cost sheets or budgeted cost sheets of the company’s products.

Estimated Production * Per Unit Cost of Goods Produced * (Finished Goods Holding Period / 365

Days)

Accounts Receivables: This calculation is simple and we just need to put the estimates and average

collection period right.

Estimated Production * Selling Price * (Collection Period / 365 Days)

Accounts Payables: The calculation of accounts payable is similar but the major difference is of

raw material cost. We take finished goods selling price in accounts receivable calculation whereas

raw material cost in case of accounts payable.

Estimated Production * Per Unit RM Cost * (Payment Period / 365 Days)

31

BIBLIOGRAPHY

✓ http://www.investopedia.com/terms/w/workingcapital.asp

✓ https://en.wikipedia.org/wiki/Working_capital

✓ http://accountlearning.blogspot.in/2011/07/factors-affecting-working-capital-or.html

✓ https://efinancemanagement.com/working-capital-financing/methods-for-estimating-

working-capital-requirement

✓ https://efinancemanagement.com/working-capital-financing/working-capital-calculation-

percentage-of-sales-method

✓ https://efinancemanagement.com/working-capital-financing/working-capital-estimation-

operating-cycle-method

✓ https://efinancemanagement.com/working-capital-financing/working-capital-calculation-

regression-analysis-method

✓ http://www.yourarticlelibrary.com/economics/capital-formation/working-capital-

definition-and-operating-cycle-explained-with-diagram/41043/

✓ http://www.investinganswers.com/financial-dictionary/businesses-corporations/net-

operating-cycle-2538