fashioning a winning trail - how to build sustainable business models in indian apparel retail

TRANSCRIPT

1

FASHIONING A WINNING TRAIL How to build sustainable business models in Indian apparel retail

2

Kanvic is a management consulting firm helping businesses develop winning strategies, drive profitable growth and achieve operational excellence to reap long lasting rewards in the fast growing Indian economy.

We work with C-level executives to develop innovative solutions for the business challenges of 21st century India by bringing in leading edge management thinking informed by in-depth research and sound analysis.

FASHIONING A WINNING TRAIL How to build sustainable business models in Indian apparel retail

Deepak Sharma

Ravindra Beleyur

Gehan Wanduragala

Shiv Kumar Sharma

kanvic.com

November 2013

About the Authors Deepak Sharma is a partner and co-founder at Kanvic where he leads the strategy practice. Ravindra Beleyur is a partner and co-founder at Kanvic where he leads the corporate finance practice. Gehan Wanduragala is an associate consultant in India and the UK and works closely with international companies tapping the Indian market. Shiv Kumar Sharma is an associate consultant in the strategy practice.

Acknowledgements Kanvic would like to acknowledge the contribution of the team behind the report. We would especially like to thank Sagnik Dasgupta for his extensive research in the sector to build and test initial hypotheses. Clement Rougeron contributed in conducting substantial analysis for the report. Vlad Flamind gave editorial inputs.

Further information We welcome your questions and comments on this report. For further information, please contact us at:

Email: [email protected]

Phone: +91 99283 77800

Contents

Foreword 9

Executive Summary 11

Evolution of Indian apparel retail 17

The elusive success of apparel retail in India 23

The root cause of failure High risk growth A crisis of leadership The weakness of surviving business models

Emerging as a winner in apparel retail 41

Improve business economics Get the growth strategy right Stress test the business model Make the right entry decisions Demonstrate boldness in exiting Look at the right metrics

Conclusion 59

Foreword

On the surface, apparel retail seems to be the standout success story in India’s journey towards modern retail. Organised players represent a larger share of the total organised retail market than any other retail category. What is more, they have achieved this status with little of the political controversy that has blighted the modernisation of other categories. However, despite this rapid rise and the seemingly huge market potential, business success has been elusive for India’s apparel retailers.

At Kanvic we were both intrigued by this apparent paradox and unsatisfied by the consensus explanations that largely blame the high cost of rentals in India. As a result, we set about identifying the real issues, with a view to charting a sustainable and profitable way forward for Indian retailers.

As a first step we built a comprehensive database of Indian apparel retailers and tracked the growth of the retail space they occupied over the last decade. We then segmented the retailers into distinct groups according to their strategies and their reasons for failure. From each of these groups we studied a representative sample of players in detail by reviewing their annual reports, the interviews of their leaders, and their financial performance. We then benchmarked these retailers against the top global players to understand the differences in their profit model. As we continued our analysis we validated our findings with industry players and against our own experience of the on-the-ground realities in the sector.

Finally (and most importantly), on the basis of our extensive analysis and experience, we identified and developed six key steps players can take to build sustainable business models and fashion a winning trail in Indian apparel retail.

We hope the resulting report will be of real interest and practical value to your organisation. We welcome your comments and we look forward to beginning a conversation about how the report’s findings and recommendations relate to your business context.

Deepak SharmaDirector and co-founder

Executive Summary

The elusive nature of success in India’s apparel retail industry has left many of its incumbents struggling, while still many more have fallen by the wayside during the economic turbulence of recent years. This report looks at the root causes of failure in the sector and highlights the persistent weakness of the surviving players. It then moves on to address the six key areas where Indian apparel retailers need to take action if they are to build the sustainable business models that will win in the future.

The emergence of organised apparel retail in India has been rapid, outstripping that of other categories and attracting significant investment from private equity. It has also seen rapid evolution as retailers sought to attract customers away from the unorganised sector through greater convenience, improved experience, and lower prices. However, by tracking the performance of leading retailers from 2008 to 2013, we have observed how the sector has been marred by a high number of failures. Kanvic analysis shows that players representing over 30% of the total apparel retail space in 2008 have either closed down or sold their business. Retailers representing a further 22% of the space are currently struggling i.e. reducing the size of their business or actively looking to sell. Whereas retailers accounting for less than half of the retail space in 2008 have been able to improve their business performance over the last 5 years.

Struck by this high failure rate in a rapidly expanding sector, Kanvic looked to identify the root causes. Our analysis found that the high risk growth strategies of retailers and a crisis of leadership within their organisations were the critical factors in bringing about failure. Firstly, the drive for rapid top-line growth and a massive expansion in store numbers led many retailers to take on unsustainable levels of debt, leaving them dangerously overextended when the slowdown hit.

These high risk growth strategies were closely related to the second cause of failure: a crisis of leadership. First and foremost, many retail leaders fell into the trap of making linear growth assumptions based on the heady economic sentiment of the mid 2000’s. Seeing uninterrupted growth ahead, they perceived ‘execution risk’ as the most serious threat to their success. This meant opening more stores than their competitors in a race to lock down the best locations in a real estate market where quality, availability, and rentals posed significant challenges. These overly optimistic growth assumptions were exacerbated by a prevailing state of hubris among many retail leaders, as they took early success to be an indication of the unique strength of their business models and their own capabilities. With such overconfidence in their

own abilities, retail leaders failed to expand the management bandwidth in their organisations. They concentrated control in a small group of promoters and relied on micromanagement, leaving them unable to manage the increased risks that came with growing business complexity.

Explaining why many Indian apparel retailers failed is only half the story though. Perhaps even more important for the industry is to understand why those who survived have yet to develop the kind of robust business models that are necessary to win in the sector. By benchmarking the top Indian retailers against the global leaders, Kanvic found that their average profit margin (as measured by EBITDA) is less than half that of their international peers.

The consensus explanation for this low profitability has been the high cost of rentals in India. However, Kanvic analysis has categorically found that high rentals are not the main cause of poor performance by apparel retailers. As a percentage of total sales, average rentals for Indian retailers are slightly lower than those of their international peers. In fact, operating costs overall are lower for Indian retailers thanks to substantially lower employee costs. The real culprit for poor profitability is the low gross margins of Indian retailers.

Kanvic analysis shows that these low gross margins are the result of two prevailing factors among Indian apparel retailers: poor supply side economics and low price realisation.

On the supply side, Indian retailers are being squeezed by an inefficient and fragmented garment industry and their weak bargaining power relative to apparel brands. With Indian garment manufacturing characterised by small scale producers using relatively low levels of technology, inefficiencies are passed on to retailers in a higher cost of goods. Furthermore, as brands and manufacturers pursue forward integration by opening their own Exclusive Brand Outlets (EBO’s), they reduce their dependence on retailers, allowing them to demand high margins.

On the demand side, retailers’ margins are being squeezed by their weak bargaining power with customers and the high level of mark-downs. Most of the basic innovations of organised retail such as air conditioned stores and a wide selection of brands have now become generic. With a lack of clear differentiation between many apparel retailers both in product and experience, the highly value conscious Indian consumer is unwilling to pay a premium and aggressively seeks out discounts. This tendency combined with a lack of effective mark-down management is destroying value across the sector.

With a scenario of low gross margins and a highly uncertain domestic and global economic climate, the clear imperative for Indian apparel retailers is to take decisive

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

12

action to strengthen their business models. Through extensive research and on-the-ground experience in the sector, Kanvic has identified six key steps they should follow to get on the winning trail:

1. Improve the Business Economics

First and foremost, retailers need to improve their business economics by reducing the cost of goods sold and increasing sales. The former requires the right sourcing decisions, including carefully considering the potential advantages of imported garments from lower cost manufacturing countries. Whether sourcing abroad or at home, retailers will need to make substantial investments in their supply chain to reduce lead times, improve quality and continually reduce costs over the long-term. Additionally, retailers will need to increase the share of private label products in their stores.

In order to increase sales, retailers must first clearly differentiate themselves. This requires identifying their target segment, getting a deep understanding of customer needs and consistently delivering a unique customer experience. At present retailers’ catch-all approach is failing to satisfy an increasingly fragmented Indian consumer market. In delivering a differentiated experience, improved customer interaction with the store staff is critical - and this is a major area of weakness for Indian retailers.

Secondly, retailers need to shift away from today’s largely push based supply model that involves placing an ‘all in’ bet on the next season, and towards a push and pull model that gives them the flexibility to supply according to actual customer demand. This can be achieved through shorter planning cycles and by breaking down the product range according to the predictability of demand.

Thirdly, retailers must implement effective mark-down management. By setting the level of possible mark-downs for each product line ahead of the season and integrating it in their financial planning, retailers will have a clear picture of the implications of price reductions on profitability. Furthermore, by closely tracking throughput of a line, minor price reductions can be made in-season to avoid the need for deep end-of-season sales.

Lastly, retailers can reduce the price elasticity of their customers by employing loyalty tools to segment and target consumers, as well as complementing it with the all important personal touch of in-store staff.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

13

2. Get the growth strategy right

While Indian retailers have focussed on store expansion as the main driver of revenues, sustainable growth demands finding the optimal balance between new store openings and increased sales productivity. Kanvic has developed a proprietary model for retail growth strategy that captures these critical aspects. The model’s key inputs in determining the future growth strategy for a retailer are their current profit levels and the degree of financial leverage in the business. Different growth strategies can be played out under a range of future scenarios to see how they fare in varying market conditions. This modelling exercise can practically help retailers re-calibrate their growth strategy to ensure its sustainability.

3. Stress test the business model

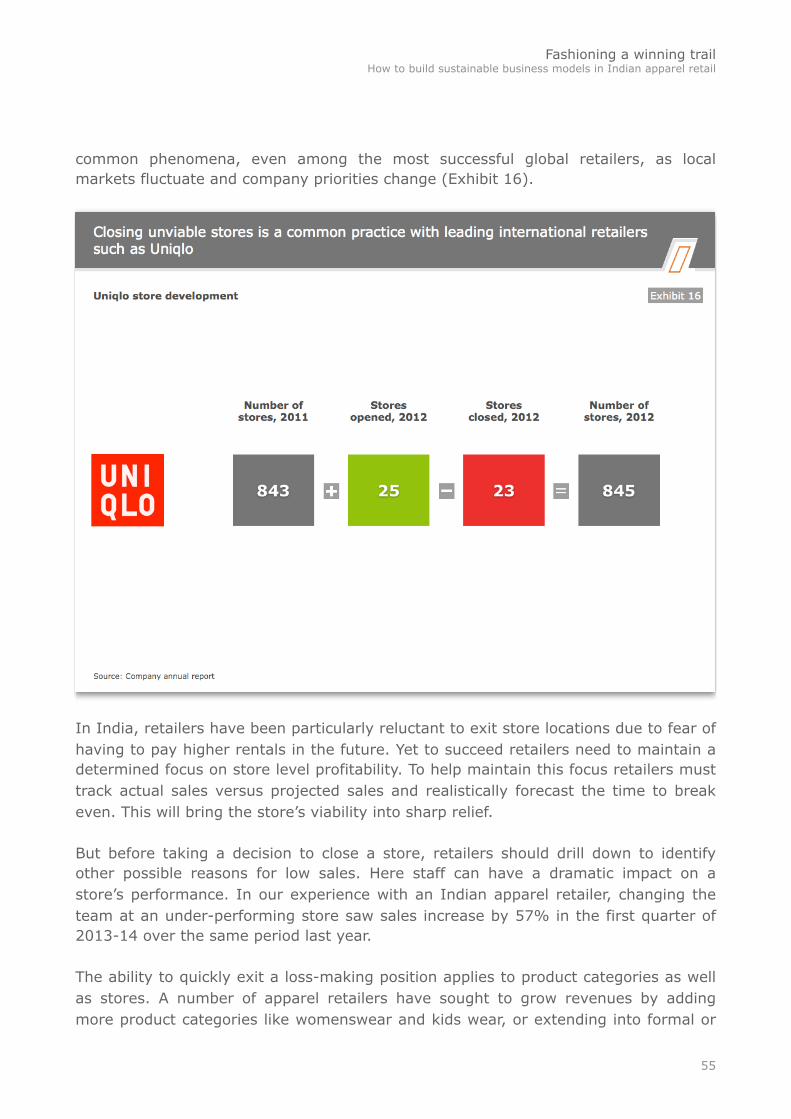

In order to build resilience to future crises, retailers need to stress test their business models under different economic scenarios. This can reduce the risk of being blindsided by future shocks in demand or supply. The first step is to prepare a baseline business plan with the current assumptions, and then assess its performance under optimistic and pessimistic scenarios. These must be extreme but still probable.

Testing the business model against these extreme but probable scenarios - rather than incrementally tweaking the key variables - puts it under real stress, and reveals the performance outcomes in such situations. However, it is important that this activity is conducted by someone emotionally detached from the strategy and can take an ‘outside-in’ approach to reveal potential blind spots. On the basis of this stress testing retailers can take action to mitigate the potential risks by, for example, reducing their leverage, increasing cash reserves or altering the future plans.

4. Make the right entry decisions

Choosing when and where to open new stores is critical to retail success. However, many Indian players have fallen into the trap of entering unviable locations to meet ambitious expansion targets or, as a speculative hedge against future trends in the real estate market - such as a rise in rentals or a shortage of supply. The result is that ill-thought out market entries have undermined the overall sustainability of their business.

Instead, before opening a new store retailers need to assess the overall demand and supply situation in the given geography to fully understand its potential. In India this can vary dramatically between for example, a developed market like Pune in Maharashtra and an undeveloped market like Bikaner in Rajasthan. Once they have decided on the target cities, retailers must drill down and assess the attractiveness of

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

14

the market according to the presence of their target customer segment and the level of competition from retailers in the same strategic group. This detailed analysis can reveal profitable micro markets which can help determine the exact store location.

Furthermore, the fit of a new store location with the existing or planned network is very important. Increasing store density in one area rather than leaping to new regions can produce greater economies in distribution, market knowledge, personnel and advertising spend.

5. Demonstrate boldness in exiting

Being able to objectively assess the viability of a store location or product category and make a prompt exit is a necessary discipline for retailers. Although store closures are a common phenomenon among top global retailers, we have seen great reluctance by leaders in India to exit loss-making positions. This reluctance comes from our human nature to be loss averse. In fact research has shown that we value a loss at as much as two-and-a-half times that of a gain of the same magnitude. To help maintain an objective focus, retailers need to closely track actual performance versus projected sales and regularly review the time to break-even. A quick exit can stem losses early and allow resources to be focussed on more profitable parts of the business.

6. Look at the right metrics

As the saying goes “revenue is vanity, profit is sanity, cash is reality”, but for too long Indian retailers have been too focussed on top line growth. To avoid being distracted from the most important indicators of success, retailers need to develop a performance dashboard that incorporates all three aspects of performance and continually monitor it. The retail performance dashboard developed by Kanvic incorporates key lagging indicators like sales, profitability and cash flow, as well as leading indicators that can give an early warning on future performance. These leading indicators can include customer and employee satisfaction levels as they have a direct relationship with sales.

In conclusion, given the current scenario of low gross margins and the combined threat of economic uncertainty and new market entrants, Indian apparel retailers must take immediate action to strengthen their business models. They can do this by improving the business economics, getting the growth strategy right, stress testing the business model, making the right entry decisions, demonstrating boldness in exiting non viable stores and product categories and looking at the right performance metrics.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

15

EVOLUTION OF INDIAN APPAREL RETAIL

Evolution of Indian apparel retail

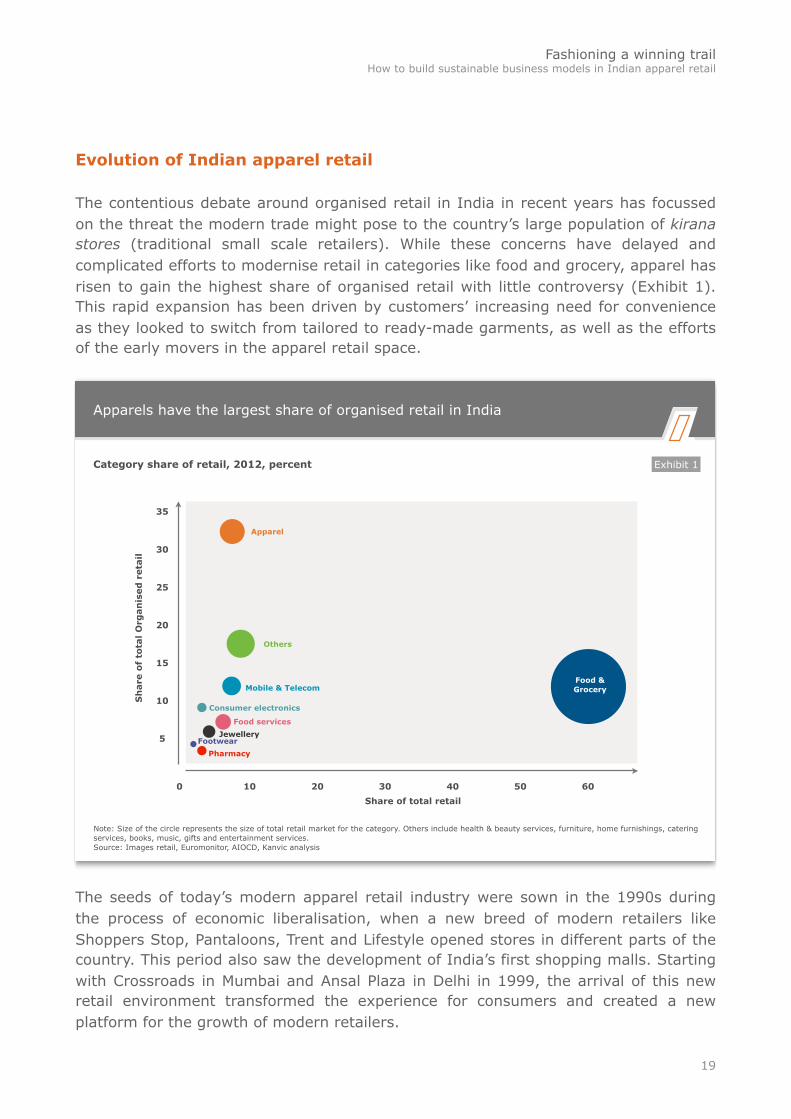

The contentious debate around organised retail in India in recent years has focussed on the threat the modern trade might pose to the country’s large population of kirana stores (traditional small scale retailers). While these concerns have delayed and complicated efforts to modernise retail in categories like food and grocery, apparel has risen to gain the highest share of organised retail with little controversy (Exhibit 1). This rapid expansion has been driven by customers’ increasing need for convenience as they looked to switch from tailored to ready-made garments, as well as the efforts of the early movers in the apparel retail space.

Apparels have the largest share of organised retail in India

10 20 30 40 50 600

5

10

15

20

25

30

35

Share of total retail

Sh

are

of t

otal

Org

anis

ed r

etai

l

Food & Grocery

Apparel

Mobile & Telecom

Food servicesJewellery

Consumer electronics

FootwearPharmacy

Exhibit 1Category share of retail, 2012, percent

Note: Size of the circle represents the size of total retail market for the category. Others include health & beauty services, furniture, home furnishings, catering services, books, music, gifts and entertainment services. Source: Images retail, Euromonitor, AIOCD, Kanvic analysis

Others

The seeds of today’s modern apparel retail industry were sown in the 1990s during the process of economic liberalisation, when a new breed of modern retailers like Shoppers Stop, Pantaloons, Trent and Lifestyle opened stores in different parts of the country. This period also saw the development of India’s first shopping malls. Starting with Crossroads in Mumbai and Ansal Plaza in Delhi in 1999, the arrival of this new retail environment transformed the experience for consumers and created a new platform for the growth of modern retailers.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

19

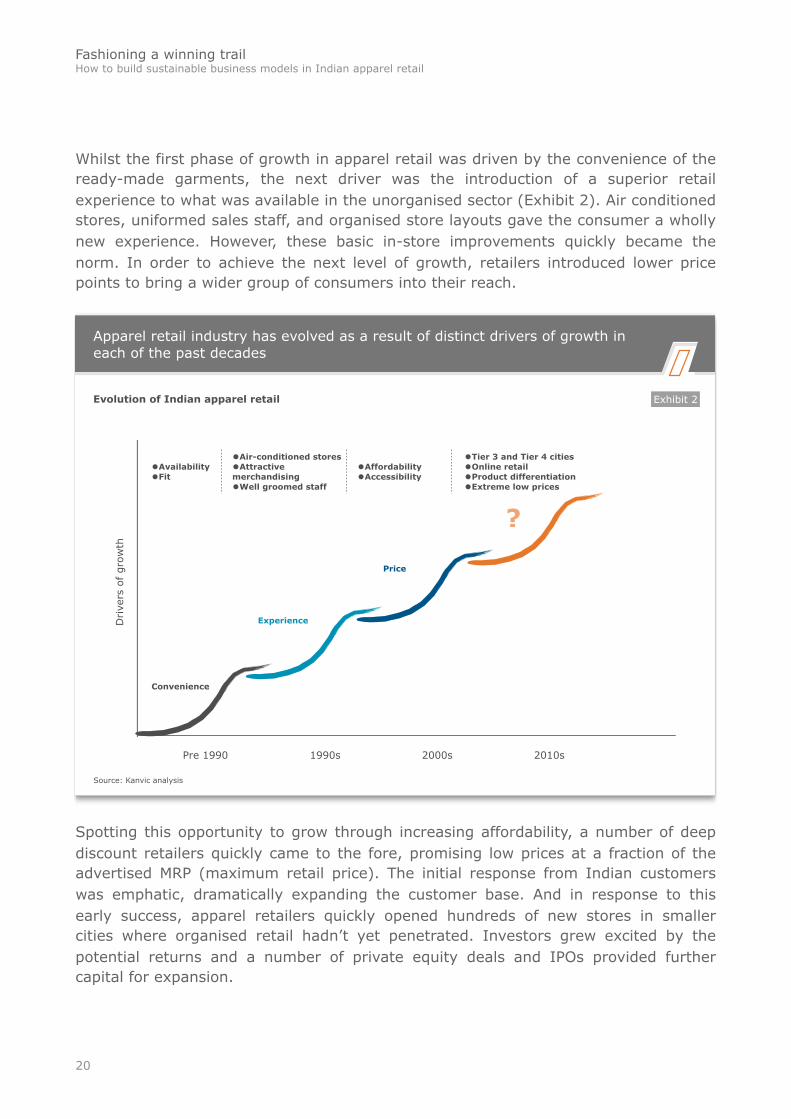

Whilst the first phase of growth in apparel retail was driven by the convenience of the ready-made garments, the next driver was the introduction of a superior retail experience to what was available in the unorganised sector (Exhibit 2). Air conditioned stores, uniformed sales staff, and organised store layouts gave the consumer a wholly new experience. However, these basic in-store improvements quickly became the norm. In order to achieve the next level of growth, retailers introduced lower price points to bring a wider group of consumers into their reach.

Apparel retail industry has evolved as a result of distinct drivers of growth in each of the past decades

Pre 1990 1990s

Convenience

Experience

Price

2000s

•Tier 3 and Tier 4 cities •Online retail •Product differentiation •Extreme low prices

•Availability •Fit

•Air-conditioned stores •Attractive merchandising •Well groomed staff

•Affordability •Accessibility

2010s

Drive

rs o

f gr

owth

Source: Kanvic analysis

?

Exhibit 2Evolution of Indian apparel retail

Spotting this opportunity to grow through increasing affordability, a number of deep discount retailers quickly came to the fore, promising low prices at a fraction of the advertised MRP (maximum retail price). The initial response from Indian customers was emphatic, dramatically expanding the customer base. And in response to this early success, apparel retailers quickly opened hundreds of new stores in smaller cities where organised retail hadn’t yet penetrated. Investors grew excited by the potential returns and a number of private equity deals and IPOs provided further capital for expansion.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

20

Kanvic analysis of private equity activity in retail shows that apparel received more than half of the total number of deals in the sector between 2000 and 2009, a period of high growth for Indian retail (Exhibit 3). It also accounted for 60% of the total number of deals across the textile and apparel value chain during the same period.

Apparel retailers have received a majority share of the private equity deals in both the retail industry as well as in the textile value chain

47

53

42

58Apparels

Non apparels

Apparel retail

Textile manufacturing

Note: Deals included are those which concluded between 2000 and 2009, a period of high growth for apparel retailers Source: VCCEdge, Venture intelligence, Kanvic analysis

Exhibit 3Private equity deals in retail industry, percent

Private equity deals in textile value chain, percent

100% = 100% =129 117

After a period of investment and rapid growth in the early 2000s, India’s apparel retail industry hit severe turbulence in late 2008 with the onset of the global economic crisis. The slowdown that followed exposed clear weaknesses in the business models of apparel retailers as many players sold their business, closed down or scaled back their operations.

In the next chapter we analyse the reasons for the failures in apparel retail during the crisis and then dig deeper and ask why weaknesses still persist among many of the survivors.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

21

THE ELUSIVE SUCCESS OF APPAREL RETAIL IN INDIA

Successful business models remain elusive

The first decade of the twenty-first century was a turbulent one for India’s apparel retail industry. In a few short years many of the industry’s brightest stars rose and quickly faded into oblivion, while others were dimmed under the burden of heavy debts.

Although India’s organised apparel retail was worth some $11.3 billion in 2012 and has grown at over 12% CAGR over the last 5 years (Exhibit 4), players are still looking for a winning formula to establish a successful and robust business model.

As a starting point for this report we looked back at the pre-crisis point of 2008 and identified the top 40 Indian apparel retailers ranked by the retail space they occupied at the time. We then tracked their fortunes through the crisis to 2013 to see how they have fared.

Our analysis (Exhibit 5) shows that retailers controlling over 30% of the total apparel retail space in 2008 were forced to either close down or sell their business.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

25

Furthermore, retailers accounting for another 22.4% of retail space in 2008 can be classified as struggling. That means they are either suffering losses, scaling down their operations, or actively looking for an exit.

From the pre-crisis peak, retailers representing less than half of the total retail space in 2008 have survived and been able to improve their business performance over the last 5 years, on major indicators such as like-to-like sales, EBITDA1 and inventory turn.

However, even among these survivors, we have found that the business models of a majority of players are not sufficiently robust to withstand future crises or deliver sustained profits in an increasingly competitive environment.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

26

1 EBITDA - Earnings before Interest, Tax, Depreciation and Amortisation

The causes of failure

We first focussed on the root causes of the high failure rate during the period until 2013. Our analysis found that it was the result of two inter-related factors: the pursuit of high risk growth strategies and a crisis of leadership at apparel retailers.

High risk growth

Enthusiastic entrepreneurs rushed into apparel retail in the first years of the new millennium, inspired by the clear market opportunity and a motivation to establish themselves as leaders in the game. At the same time the availability of private equity cash in the industry and a number of high profile IPOs created an appealing prospect of substantial short-term rewards. And looming ever larger on the horizon was the seemingly inevitable arrival of Foreign Direct Investment (FDI) from global retailers, promising an even bigger pay day.

In such a climate the ‘animal spirits’ of entrepreneurs took hold, as they sought to match or outstrip the growth of their peers to emerge as leaders. Any doubts about the risks of such rapid growth were dispelled by a belief that the deep well of untapped Indian consumers and the deep pockets of investors would see them through to a profitable outcome. As a result, many apparel retailers developed business models that would deliver the fastest top-line growth and capture the largest market share, for which they believed investors would reward them handsomely.

Such fast growth demanded rapid new store openings and accelerated conversion of consumers from the unorganised sector. In response to this need, the phenomena of deep discounting gained popularity among a key group of fast growing apparel retailers. Their approach elicited early success as shoppers flocked to buy aggressively priced products in the new modern retail stores. At one of the largest deep discount retailers, newly opened stores had to temporarily close their doors to control the inflow of customers.

This initial success was seen as a validation of the business model and other players were quick to join the fray as valuations and investor interest grew. The arrival of new entrants further accelerated the push for store expansion as it brought the importance of location to the fore. With a scarcity of space in India’s cities, retailers saw a direct relationship between future market share and control of prime retail real estate. Thus, securing the best locations sooner rather than later became the priority, as retailers sought to lock in lower rentals today as well as block future competition.

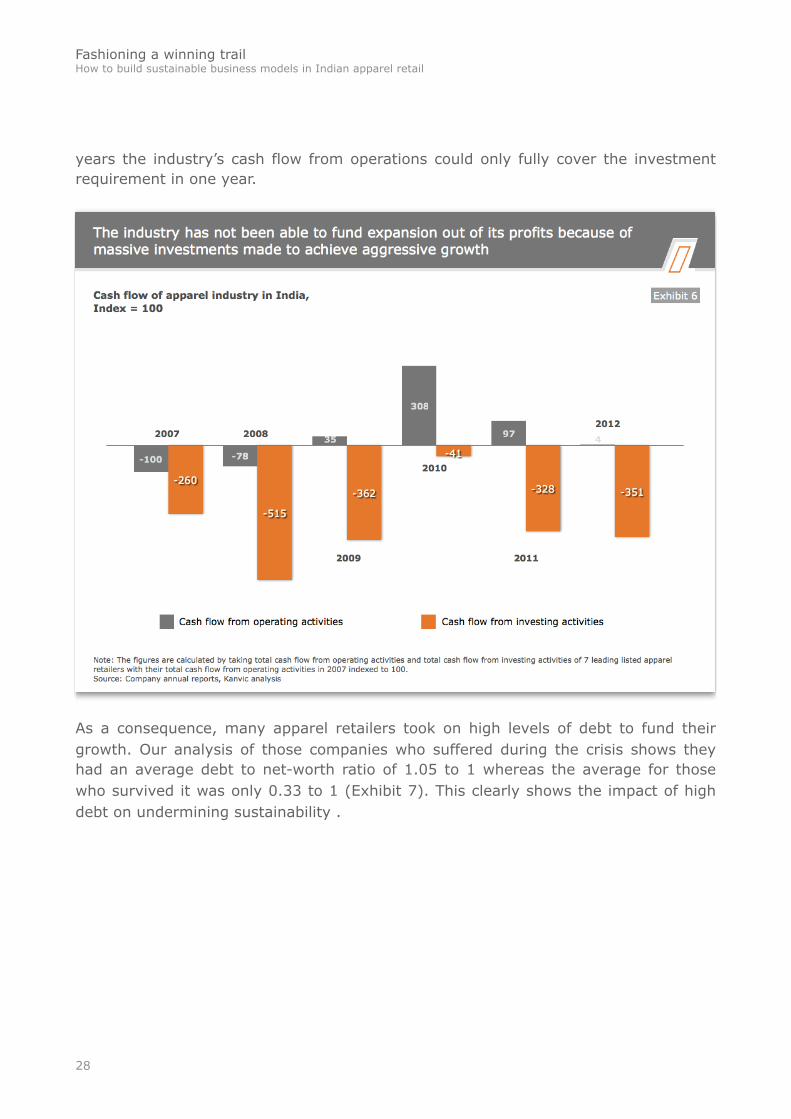

However, funding such rapid growth required additional funds as retailers could not generate the necessary cash flow from operating activities (Exhibit 6). In the last six

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

27

years the industry’s cash flow from operations could only fully cover the investment requirement in one year.

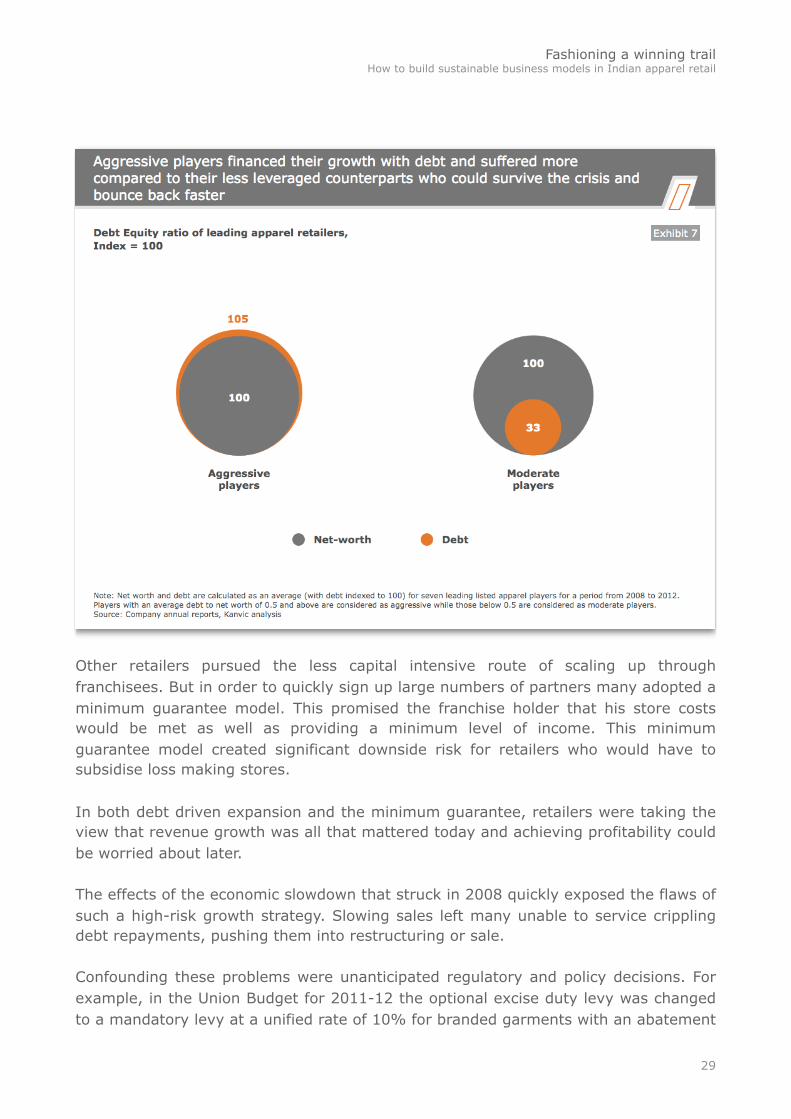

As a consequence, many apparel retailers took on high levels of debt to fund their growth. Our analysis of those companies who suffered during the crisis shows they had an average debt to net-worth ratio of 1.05 to 1 whereas the average for those who survived it was only 0.33 to 1 (Exhibit 7). This clearly shows the impact of high debt on undermining sustainability .

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

28

Other retailers pursued the less capital intensive route of scaling up through franchisees. But in order to quickly sign up large numbers of partners many adopted a minimum guarantee model. This promised the franchise holder that his store costs would be met as well as providing a minimum level of income. This minimum guarantee model created significant downside risk for retailers who would have to subsidise loss making stores.

In both debt driven expansion and the minimum guarantee, retailers were taking the view that revenue growth was all that mattered today and achieving profitability could be worried about later.

The effects of the economic slowdown that struck in 2008 quickly exposed the flaws of such a high-risk growth strategy. Slowing sales left many unable to service crippling debt repayments, pushing them into restructuring or sale.

Confounding these problems were unanticipated regulatory and policy decisions. For example, in the Union Budget for 2011-12 the optional excise duty levy was changed to a mandatory levy at a unified rate of 10% for branded garments with an abatement

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

29

of 55%. This hit the retailers offering year round discount of 50% to 90% the hardest, because of the large difference between their Maximum Retail Price (MRP) and actual sale price, effectively rendering the deep discount model unviable.

A Crisis of Leadership

The second major contributor to failure in the apparel retail industry was the crisis of leadership at the top of many organisations. This was crystallised in three critical shortcomings: linear growth assumptions, overconfidence, and a lack of management bandwidth.

i) Linear growth assumptions

The working assumption of many leaders in the apparel retail industry was one of uninterrupted linear growth, a seemingly inevitable consequence of the long-term Indian consumption story. However, in assuming uninterrupted growth retail leaders had succumbed to the availability bias in their outlook. The availability bias is human beings’ tendency to give preference to the most recent and widely available information. This is often the information that is most highlighted in the media or discussed by our peers.

In the case of apparel retailers they based assumptions on the recent successes in the industry, using a tiny data set from the very early stages of the sector’s birth to extrapolate high growth rates far into the future. Their assumptions on industry growth rates were also based on the very recent performance of the Indian economy, which had grown at an average of 8.7% per annum from 2004 to 2008.

Assuming non-stop growth, the only perceived challenge, and the one most regularly cited by retailers, was ‘execution risk’, i.e. how to open as many stores as quickly as possible and gain a pan-India presence. Therefore, the most important metric of success became the number and speed of new store openings. As part of our work in the sector we came across one retailer who mentioned in their initial discussions that they wanted to grow to 1,000 stores across India in a few years. This was without having a clear plan or a detailed understanding of the business model for the new venture.

By assuming uninterrupted linear growth, retail leaders failed to consider alternative scenarios where growth could decline and then factor this risk into their business models.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

30

ii) Overconfidence

The second shortcoming among leaders in apparel retail was their overconfidence in their own capabilities to run the business as well as their ability to predict external events.

The rapid early growth of many apparel retailers created a positive feedback to their assumptions and fed a growing state of hubris. Initial success was seen as a vindication not only of their bet on the sector, but also of their business model and leadership capabilities.

Studies have shown that executive hubris often manifests itself in business decisions relating to growth for its own sake, acquisitions, and the disregard for rules2. In the case of Indian apparel retail, leaders further raised their goals for store openings and accelerated the speed of expansion, entering into an increasingly incredible contest to announce more ambitious plans than their competitors. In our analysis of an annual report of one large retailer, we found that the term “aggressive” was used in relation to their strategy seven times in 2007-08 while it was not used at all in 2011-12.

Furthermore, apparel retailers made similarly overconfident predictions about the imminence of major foreign direct investment (FDI) in the sector (Exhibit 8). Yet this was dependent on important policy decisions by the Government of India, a policy process over which they had little or no influence and which has a long history of stop-start activity. Flowing from this was an equally overconfident belief that international retailers would pay a large premium to acquire immediate scale in the Indian market. Further assuming that they would have little concern for the underlying profitability, operational efficiency, or risk profile of the business.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

31

2 Kroll, M.J., Toombs, L.A. and Wright, P. (2000), “Napoleon’s tragic march home from Moscow: lessons in hubris”, Academy of Management Executive, Vol. 14 No. 1, pp. 117-28

These displays of executive hubris should have been seen as a warning signal that the organisation’s leadership was losing touch with reality. In recent research on the subject, the language of a chief executive at a European bank that went from boom to bust was analysed to track his rising hubris. During the boom years it was found that he attributed an increasing amount of the good news about the firm to himself personally, less to the company and very little to external factors. By contrast no bad news was attributed to himself or the company.3

In reality, the early successes of many Indian retailers had little to do with the strength or uniqueness of their business models - which were often value destroying - and more to do with a short-lived first mover advantage.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

32

3 Brennan, Niamh M., Conroy John P.; “Executive hubris: the case of a bank CEO”, Accounting, Auditing& Accountability Journal, Vol. 26 No. 2, 2013, pp. 172-195

iii) Management bandwidth

As Indian apparel retailers began to achieve significant scale, the organisational complexity multiplied, but many retailers lacked the management bandwidth to effectively run their companies. With control often concentrated in a small group of promoters, there was an absence of professional managers at the head office and at the store level. As a result, the companies’ leadership struggled to get a handle on the growing risks to the business.

Many of the Indian promoters running apparel retail businesses tended to rely on gut to power their organisation. Retail leaders believed that they alone could manage a large-scale operation, which in turn resulted in a lack of appropriate hiring and a strong degree of micromanagement. Furthermore, the habit of depending on informal networks of advisers with ambiguous roles was characteristic of the traditional way of retailing. Practices like this served to undermine the process of professionalisation, which is an essential element in the modernisation of retail.

Often it was only after pressure from external investors or the realities of a crisis that promoters moved to hire professionals. However, without the appropriate management structures and systems in place these individuals were not able to perform to their potential.

Clearly hindsight offers advantages when explaining the failures in Indian apparel retail, but identifying the root cause is an essential exercise in addressing the weaknesses that still persist in the industry, as we will address next in the report.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

33

The weakness of surviving business models

Although a large number of players in Indian apparel retail sold out, shut shop or are still struggling, a significant group have survived with their ambitions humbled but their businesses largely intact. Whilst their survival indicates a relative degree of strength, a closer analysis of these companies shows a prevailing weakness in their business models that raises questions about their long-term profitability - and ultimately their viability.

By benchmarking the top listed Indian apparel retailers against global leaders, Kanvic has found that after over 20 years of organised apparel retail, none of the existing business models have been able to achieve margins on a par with the international leaders. On the key benchmark of EBITDA, which allows comparison of operating performance across companies irrespective of their financial leverage and investment intensity, India’s top apparel retailers achieve less than half the figure of the top global players (Exhibit 9).

Indian apparel retailers have weak business models as a result of higher cost of sales compared to successful global players

24.015.6

7.9

9.413.7

10.9

9.99.9

8.3

16.112.3

5.4

40.548.4

67.5

Note: For Indian retailers, figures are averages from 2010 to 2012 for seven leading apparel retailers listed on the stock market. For Uniqlo and ZARA, the figures are averages for the same period. Source: Companies annual report, Kanvic analysis

Exhibit 9Benchmarking of Indian retailers’ profit model with leading International players, % of sales

Cost of goods sold

Employee cost

Rent

Other costs

EBITDA

Indian retailers ZARAUniqlo

Gross margin 32.5 59.551.6

While rents are projected as the main cause of retailers’ woes, our benchmarking of leading listed apparel retailers with the global leaders shows their average rents as well as overheads are much lower than the global leaders

Our analysis clearly shows that lower gross margin (as a result of higher cost of goods sold) is the root cause for Indian players’ weak and unsustainable business model

As a result of higher gross margins, global players have 2-3 times the EBITDA margins compared to Indian players in spite of higher overheads

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

34

A common explanation for the underperformance of the Indian retail sector is that rentals in India account for a higher percentage of total sales. While indeed rent as a percentage of sales has more than doubled over the last 7-10 years for some leading apparel retailers, Kanvic analysis shows that rentals for Indian retailers account for a lower percentage of revenues than more profitable international players like Zara and Uniqlo.

Certainly, the combination of rising rentals with increasing employee and energy costs has negated some of the economies of scale Indian retailers may have expected to benefit from with expansion. But, despite these factors, overall operating expenses for the leading Indian players are still lower than the most successful international retailers. Most notably due to the substantially higher employee costs in other countries.

What all of this clearly shows is that operating costs - and rent more specifically - are not the cause of the low margins and weak business models in Indian apparel retail. The real cause of their weakness is low gross margins.

The root causes of low margins

Having established low gross margins as the critical issue in Indian apparel retail, we then focussed our analysis on identifying the root causes. Our findings show that these root causes come down to poor supply side economics and retailers’ weak position relative to customers.

i) Poor supply side economics

On the supply side, the margins of Indian apparel retailers are being squeezed by the fragmented and inefficient nature of the Indian garment industry and retailers’ weak bargaining position relative to fashion brands. A critical success factor for the leaders in global apparel retail has been their relentless focus on and command of their supply chain. This has enabled them to get the latest trends to market faster and at a lower cost.

In Indian apparel retail the first point of inefficiency we identified is in sourcing. The majority of players are sourcing product domestically. Here, in terms of labour, power, construction, and land transportation, India is a more expensive manufacturing centre than many of its competitors in the global apparel trade. By comparison, leading international apparel brands seek out and source their products from the lowest cost suppliers globally, including Bangladesh and China (Exhibit 10).

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

35

Indian retailers by contrast are burdened by the inefficiencies of a highly fragmented domestic supplier base. There are over 100,000 garment units in India4 but most of them are small and using low levels of technology. Their inefficiency is then passed on to the retailers in higher prices.

The fragmented supplier scenario in India also results in lower economies in the purchase of fabrics and other raw materials, further increasing the cost of goods sold. By contrast, global brands achieve supply chain efficiency through their scale, placing large standardised orders with large organised suppliers.

Finally, India’s small and often loss-making garment manufacturers have little ability to invest in the modern machinery that can reduce time to market and drive down costs in the long-run. By comparison, the top global apparel brands invest substantial time and resources in developing and integrating their suppliers, allowing

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

36

4 Source: Confederation of Indian Textile Industry (CITI)

them to cut lead times, lower costs, and improve quality. Thus their supply chain becomes an integral part of their competitive advantage.

In addition to the inefficiencies in supply chain, apparel retailers must also deal with the higher bargaining power of both manufacturers and brand owners. On an average, domestic manufacturer’s operating margin is 5% higher than exporting firms5, showing their ability to take a larger piece of the pie from Indian retailers. At the same time, the pursuit of forward integration by fashion brands - through the expansion of their own exclusive brand outlets (EBOs) - is reducing their dependence on multi-brand apparel retailers, including large retail formats. The resulting high bargaining power of the brand owners was evident following the reduction in excise duty in 2013, when brands did not pass on the lower costs to customers while some retailers went ahead and reduced the prices.

ii) Low price realisation

The second cause of poor gross margins among Indian apparel retailers is their inability to realise higher prices. This is the result of a low level of bargaining power with their customers and a high level of mark-downs.

Firstly, retailers have little bargaining power with their customers due to a lack of differentiation between the competing apparel retailers and high price elasticity among consumers.

In India, both organised and unorganised multi-brand outlets (MBOs) are usually selling the same range of branded apparel at similar price points in a barely distinguishable retail environment. When organised apparel retailers first entered the Indian market they focussed on differentiating themselves from the unorganised sector. However, the basic steps like air conditioned stores and a wide range of products have now become generic - an expected minimum by India’s urban shoppers. Without a clear differentiation between retailers, customers are unwilling to pay a premium to that of the lowest priced competitor.

Given the highly value conscious nature of the Indian consumer, high price elasticity is common as customers actively seek out bargains and discounts. Retailers can combat this by creating a loyalty system and tracking their loyal customers. However, today only 20% of Indian apparel retailers get more than 25% of their sales from loyal customers and a majority (60%) are not even measuring sales from loyal customers at all (Exhibit 11).

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

37

5 Source: CRISIL

Sixty percent of retailers do not have a system to measure sales from loyal customers

Not measured

< 25%

25% - 50% 20%

20%

60%

Source: Retailers Association of India

Exhibit 11Sales form loyal customers, percent of respondents

60%

Globally, players have created differentiation and brand loyalty through delivering a distinctive style, quality or customer experience that is difficult to find elsewhere. For example, Zara’s in-house production system continually delivers versions of the latest fashion to their stores faster than their peers, with the added incentive for customers that when it’s gone, it’s gone! Uniqlo delivers a less fashion centric offering but with a quality of fabric that is impossible to find at a better price elsewhere, due to its huge scale in sourcing and its massive investment in production and textile technology. Finally, new experience led stores like Hollister’s make large investments in store fit-outs to draw customers in and increase the likelihood of conversion, in their case creating an experience that is more like a nightclub than a retail store!

Compounding retailers’ weak bargaining power with customers is the high level of mark-downs in the sector. This is the product of poor demand management and weak mark-down management. Poor systems for merchandise planning result in large build-ups of unwanted stock, necessitating heavy discounting at the end of the season. This distorts customer expectations on price as well as eroding the retailers’ brand image, making it even more difficult to command higher prices in the future. Even where Indian retailers are not suffering from high levels of slow moving stock, they are often

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

38

forced into mark-downs by their competitors who launch their sale early or extend it for longer.

By comparison, leading international apparel retailers like Next and Nordstrom leverage their customer loyalty to make their main sale a recognised retail event. The dates are fixed from year to year, building a sense of customer anticipation that often results in queues outside the stores and huge traffic to their web portals.

In today’s scenario Indian apparel retailers are competing increasingly against other organised players as well as the unorganised sector. As such, the lack of differentiation in retail experience leaves apparel retailers particularly vulnerable to both the threat of new entrants and the emergence of low touch channels like online retail.

With Indian apparel retailers hampered by low gross margins, the imperative of the moment is to take decisive action to strengthen their business models. In an uncertain domestic and global economic climate, muddling through with the status quo is not a sustainable option. In the next chapter, we present six steps Indian apparel retailers can follow to get on the winning track.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

39

EMERGING AS A WINNER IN APPAREL RETAIL

Emerging as a winner in apparel retail

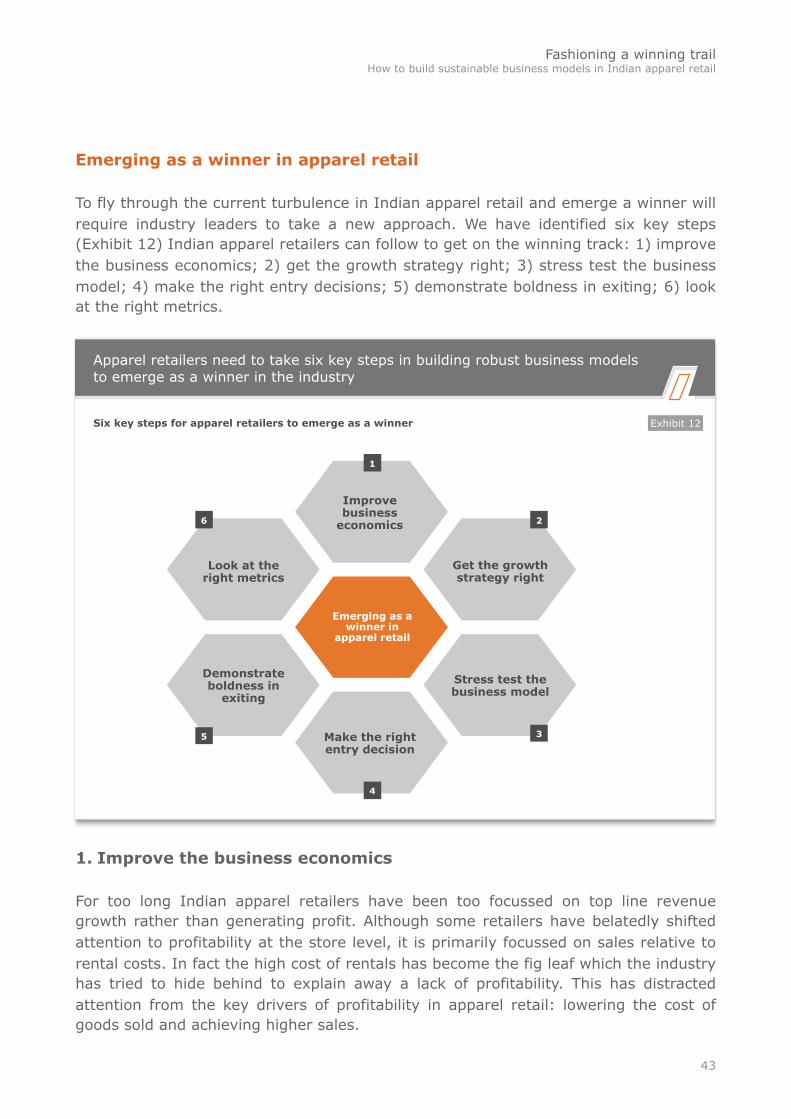

To fly through the current turbulence in Indian apparel retail and emerge a winner will require industry leaders to take a new approach. We have identified six key steps (Exhibit 12) Indian apparel retailers can follow to get on the winning track: 1) improve the business economics; 2) get the growth strategy right; 3) stress test the business model; 4) make the right entry decisions; 5) demonstrate boldness in exiting; 6) look at the right metrics.

Apparel retailers need to take six key steps in building robust business models to emerge as a winner in the industry

Emerging as a winner in

apparel retail

Improve business

economics

Stress test the business model

Get the growth strategy right

Make the right entry decision

Demonstrate boldness in

exiting

Look at the right metrics

1

2

3

4

5

6

Exhibit 12Six key steps for apparel retailers to emerge as a winner

1. Improve the business economics

For too long Indian apparel retailers have been too focussed on top line revenue growth rather than generating profit. Although some retailers have belatedly shifted attention to profitability at the store level, it is primarily focussed on sales relative to rental costs. In fact the high cost of rentals has become the fig leaf which the industry has tried to hide behind to explain away a lack of profitability. This has distracted attention from the key drivers of profitability in apparel retail: lowering the cost of goods sold and achieving higher sales.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

43

The most profitable global apparel retailers have created superior business economics by driving cost out of the supply chain at the same time as delivering a clearly differentiated customer experience. Such successes have yet to be achieved by Indian apparel retailers but, by taking action on a number of levers (Exhibit 13) they can get on the path to improved profitability.

Indian apparel retailers can their improve business economics by acting on both sales and cost levers

Sales

Cost of goods sold

•Increasing differentiation •Shifting from simple push to push and pull supply model

•Employing better mark down management

•Improving customer engagement

•Right sourcing strategy •Investing in and integrating the supply chain

•Increasing the share of private label

Source: Kanvic analysis

Margin expansion

Expanding margins through both increased sales and cost reduction

Exhibit 13

Reducing the cost of goods sold (COGS)

The first front for improving the business economics in Indian apparel retail is reducing the cost of goods sold. This will be achieved through i) the right sourcing strategy, ii) investing in and integrating the supply chain, and iii) increasing the share of private label.

Firstly, Indian apparel retailers need to get their sourcing strategy right. This involves identifying the best value suppliers whether in India or abroad. For example, manufacturing costs in neighbouring Bangladesh are 20 percent lower compared to

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

44

India6. In 2012 Bangladesh’s total apparel export was $22.2 billion compared to India’s $12.9 billion7, resulting in larger scale manufacturers more attuned to international requirements. In recent years steadily rising garment imports from both Bangladesh and Sri Lanka show the increasing competitiveness of imported products versus locally manufactured garments. Imports from Bangladesh and Sri Lanka grew at a CAGR of 90% and 61% respectively between 2008 and 2012, compared to 23% growth of total apparel imports during the same period8.

In addition to making the right sourcing decisions, retailers need to make substantial investments in their supply chain to improve the speed and quality of production, which will further lower the costs of goods over time. At present the lead time for many Indian suppliers is 4-6 months - far too long to respond to changing consumer trends. But to make the necessary investment in machinery, technology, and systems requires long-term strategic collaboration with suppliers. These kind of partnerships will demand commitment, substantial financial investment and a collaborative approach from the retailer.

Finally, increasing the share of private label products is a critical step to reducing the cost of goods sold. The most profitable global retailers such as Zara, Uniqlo and H&M are almost exclusively private label retailers. In a highly competitive market, paying higher prices to brands is margin eroding and the indirect investment in their brand dilutes the retailers’ standalone brand equity. Globally, multi-brand apparel retail is the domain of premium department stores, online retailers or local boutique stores. The first can maintain margins due to the high price of the product as well as commanding rentals for shop-in-shop concessions. Secondly, lower infrastructure costs allow e-retailers to preserve profit margins. While smaller stores serve niche local markets and lack the scale to source their own product.

Indian apparel retailers need to develop a clear plan for building a capability in private label, from developing an integrated supply chain through to better understanding their customers’ needs.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

45

6 Source: Fashion United

7 Source: International Trade Centre

8 Source: International Trade Centre

Increasing Sales

The second front for improving the business economics is increasing sales. Apparel retailers can increase sales on a like-to-like basis by: increasing their sales density (sales per square foot); protecting their MRP price; and gaining a capacity to increase prices without a reduction in volumes. To achieve these objectives Indian apparel retailers need to focus on four key areas for improvement: i) increasing their differentiation, ii) switching from a simple push to a push and pull supply model iii) employing better mark-down management and iv) improving customer engagement.

i) Increasing differentiation

When the product and experience are weakly differentiated from other players competing in the same segment, the customer will only compare in terms of price. Thus when one player discounts to shift slow moving stock or increase sales, the other players are forced to follow suit, destroying value across the sector. This is the prevailing scenario in Indian apparel retail.

To effectively differentiate, retailers need to deliver a unique combination of product offering, price point, and customer experience. But to do this they first need to decide in which customer segment they want to play, and then develop the proposition that will be most highly valued by these customers. Today Indian retailers have yet to effectively target discrete customer groups, with most offering a largely generic range of mens western casuals and formals. But as the Indian consumer market becomes increasingly fragmented, customers are looking to express themselves in distinct ways. In such a scenario continuing to try and be all things to all people is a recipe for failure.

For example, an older customer that buys according to quality and customer service is likely to be unsatisfied by a store that promotes fashionable items on young models and is staffed by young attendants. Alternatively teenagers and students looking for casual wear will be put off by extensive floor space dedicated to office wear and older attendants dressed in formals.

But being targeted doesn’t mean that the retailer remains small. Zara is a multi-billion dollar enterprise but clearly focusses on a younger fashion conscious consumer with its core format, developing other concepts like Kids or distinct brands like Massimo Dutti (luxury) for other segments. Similarly Uniqlo’s single format model ignores the highly fashion conscious consumer and focusses on those who value great functionality and affordability in their garments.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

46

Critical to achieving a differentiated positioning is its consistency across every aspect of the customer experience; from the look and feel of the stores, to the level and type of customer service and the convenience of the channel.

However, in transforming a unique strategic positioning into a truly differentiated experience, the moment of truth is the customer interaction with the retailer’s staff on the shop floor. Store staff are vital to converting walk-ins to customers, cross-selling new products and upgrading them to higher value purchases. What is more, they acquire numerous insights on customer behaviour and feedback that are invaluable to the organisation. All of this is critical to the achievement of higher sales.

The quality of the customer interaction is a persistent area of weakness for Indian apparel retailers and a great opportunity for players to achieve differentiation. With staff representing a low percentage of total expenditure and the high availability of low skilled labour in India, this critical component of a retail organisation is treated on a commodity-like basis. The inevitable result is low employee engagement and high attrition rates, with retail managers and store staff trapped in a cycle of mutual dissatisfaction. The net effect are false economies in operating costs that actually mask a mountain of lost sales and unhappy customers.

Tackling this weakness requires appropriate organisational design, proper internal communication and decision-making systems, incentive programmes that recognise success beyond simple financial rewards, and meritocratic models for promotion that reward loyalty to the organisation over the long-term. These systems and processes need to be transparent and supplemented by ongoing training and development at the store and head office level.

ii) switching from a simple push to a push and pull supply model

Apparel retailers need to move away from the current practice of push based supply to a more intelligent system of push and pull. Today many retailers are waging an ‘all in’ bet on the next season by placing their complete orders in advance. The impossibility of accurately predicting the next season’s fashion trends, weather, or consumer confidence, inevitably results in slow or non-moving stock that must be sold at discount, bringing down the gross margins.

Instead, retailers should break the season down into shorter periods and break the product range down into different categories according to their predictability. For example, by breaking the season down into shorter planning cycles, retailers can continually test the customer response to say a style or colour and place further orders accordingly for the next ‘mini’ season. As a result the downside of a bad call in merchandise planning is limited to a much smaller amount of stock.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

47

These shorter planning cycles should be supported by a clear break-down of the product range according to their fashion quotient. For example, a simple segmentation could be into basic, basic fashion and fashion items. These categories are defined by whether their predictability of demand is high, medium or low. For example, basic items like simple white shirts, t-shirts and inner wear might see very little variation in demand from season-to-season. These items can be ordered further in advance and in larger quantities. As the fashion quotient increases, the more fickle the customer response will be. Therefore more fashion oriented items should be ordered in smaller quantities with shorter lead times, giving planners sufficient wiggle room to adjust their orders.

To implement shorter and more agile planning cycles retailers must create dedicated internal planning teams that are constantly monitoring the latest global and Indian trends. There also need to be systems in place to regularly communicate information back from store staff and customers to inform these planning decisions.

iii) employing better mark-down management

Even when inventory is under control, Indian retailers can fall into the trap of marking down prices due to pressure from competitors, producing a negative impact on income. Whilst a strongly differentiated value proposition will help persuade customers of a brand’s superior value, retailers need to maintain discipline in mark-downs to protect their margins.

Key to mark-down management is having a proper mark-down plan in place ahead of the season. Retailers should consider in advance which products they are willing to discount and by how much. This should be integrated with their financial planning for the season, so they are fully aware of the implications of mark-downs on their profitability at both the chain and category level.

Secondly, retailers need to be proactive in their use of mark-downs to avoid having to clear large amounts of stock at the end of the season. If a line is selling slowly, incremental price reductions in-season can help clear inventory, without the need for aggressive sales across all products lines at the end of the season.

Finally, planning the dates for your major yearly or twice yearly sales and building a marketing plan around them will help optimise the mark-down process. Retailers can project the amount of discounts and the likely uptick in sales volume and thus estimate an appropriate marketing budget to invest during the sales period. Well-planned and executed sales can actually drive profitability through dramatically increasing volumes at key points of the year. By combining effective marketing communication about the sale with attractive discounts targeted at loyal shoppers,

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

48

sales can also become a valued element of your proposition to your most profitable customers.

By employing these techniques sales are no longer a necessary evil but an integral part of the retail strategy, contributing to both profitability and customer excitement about the brand.

iv) Improving customer engagement

While a clear differentiation will attract customers to the brand, retaining and upgrading them requires retailers to engage them in a targeted way. Here measuring customer loyalty is an essential first step which many Indian retailers have yet to take. But managing loyal customers must go beyond simply issuing cards and giving points. Loyalty programmes need to be used to identify and segment the most loyal - and profitable - customers. They then need to be given interesting targeted offers and services. As retailers grow their capabilities in loyalty management, analytics become a powerful tool, enabling them to send highly personalised offers to individual customers according to their recent purchase behaviour.

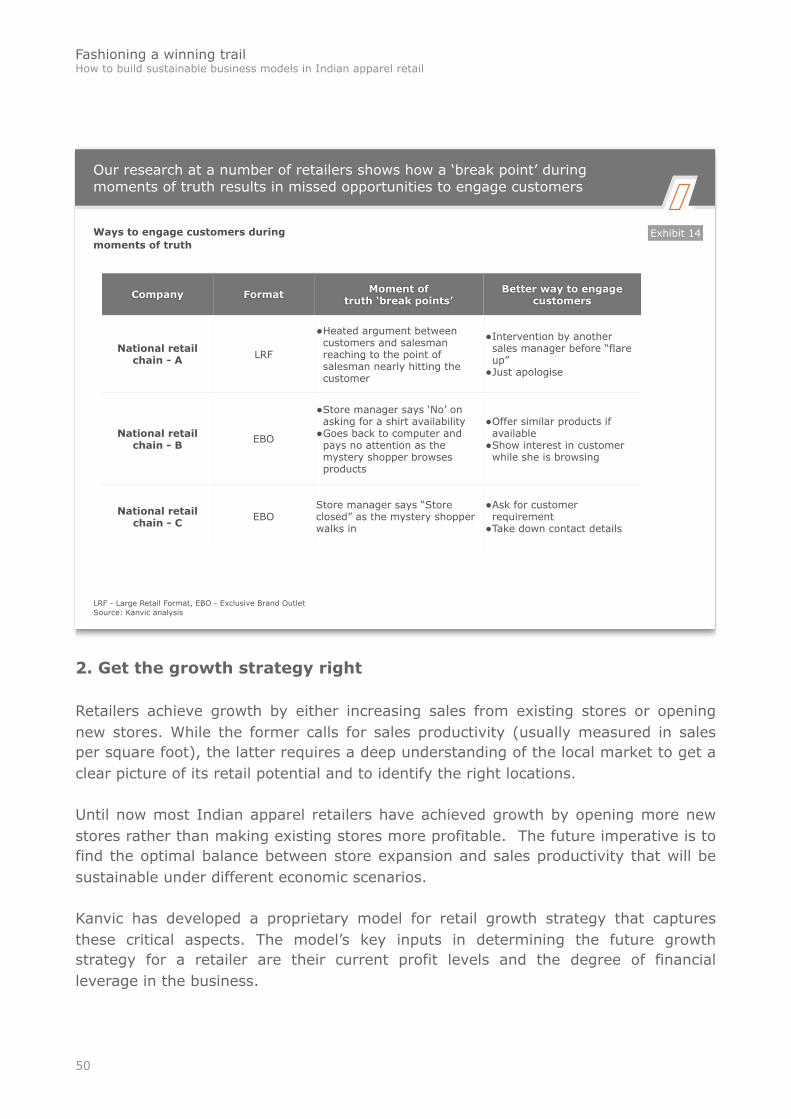

These technology based loyalty tools are insufficient though, if they are not supported by the right actions of store staff at the critical moment of truth. In our research conducted at a number of national retailers (Exhibit 14), we witnessed how store staff regularly missed opportunities to engage customers and convert walk-ins into billings, and how in some cases they even alienated and offended their clientele. Addressing these ‘break points’ by training staff in the correct techniques for customer engagement will significantly increase conversions and customer satisfaction.

Furthermore, the most loyal customers must receive enhanced service by store staff and managers or else they will remain underwhelmed. In this regard lessons from the hospitality and travel industry are particularly valid, where top airlines and hotels ensure their staff are fully briefed about the personal preferences and requirements of their most loyal customers, enabling them to give them special recognition and treatment.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

49

Our research at a number of retailers shows how a ‘break point’ during moments of truth results in missed opportunities to engage customers

Company Format Moment of truth ‘break points’

Better way to engage customers

National retail chain - A LRF

•Heated argument between customers and salesman reaching to the point of salesman nearly hitting the customer

•Intervention by another sales manager before “flare up”

•Just apologise

National retail chain - B EBO

•Store manager says ‘No’ on asking for a shirt availability

•Goes back to computer and pays no attention as the mystery shopper browses products

•Offer similar products if available

•Show interest in customer while she is browsing

National retail chain - C EBO

Store manager says “Store closed” as the mystery shopper walks in

•Ask for customer requirement

•Take down contact details

LRF - Large Retail Format, EBO - Exclusive Brand Outlet Source: Kanvic analysis

Exhibit 14Ways to engage customers during moments of truth

2. Get the growth strategy right

Retailers achieve growth by either increasing sales from existing stores or opening new stores. While the former calls for sales productivity (usually measured in sales per square foot), the latter requires a deep understanding of the local market to get a clear picture of its retail potential and to identify the right locations.

Until now most Indian apparel retailers have achieved growth by opening more new stores rather than making existing stores more profitable. The future imperative is to find the optimal balance between store expansion and sales productivity that will be sustainable under different economic scenarios.

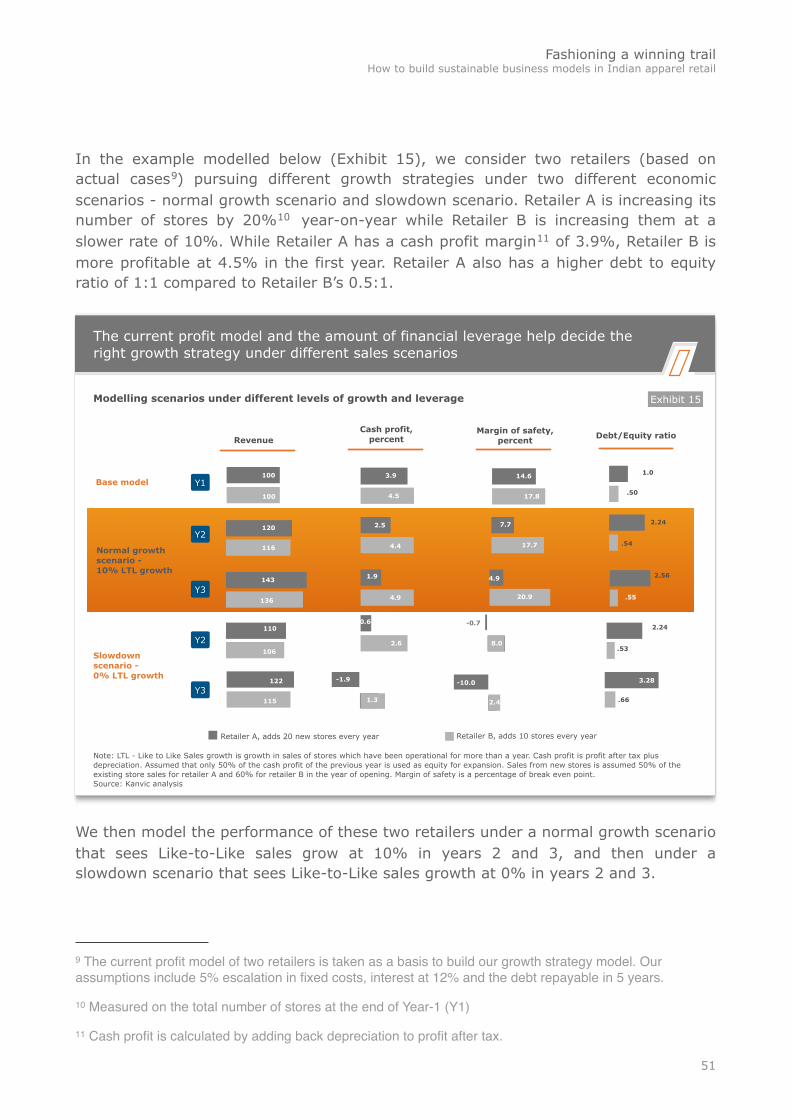

Kanvic has developed a proprietary model for retail growth strategy that captures these critical aspects. The model’s key inputs in determining the future growth strategy for a retailer are their current profit levels and the degree of financial leverage in the business.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

50

In the example modelled below (Exhibit 15), we consider two retailers (based on actual cases9) pursuing different growth strategies under two different economic scenarios - normal growth scenario and slowdown scenario. Retailer A is increasing its number of stores by 20%10 year-on-year while Retailer B is increasing them at a slower rate of 10%. While Retailer A has a cash profit margin11 of 3.9%, Retailer B is more profitable at 4.5% in the first year. Retailer A also has a higher debt to equity ratio of 1:1 compared to Retailer B’s 0.5:1.

The current profit model and the amount of financial leverage help decide the right growth strategy under different sales scenarios

RevenueCash profit,

percentMargin of safety,

percent Debt/Equity ratio

Base model100

100

1.0

.50

Normal growth scenario - 10% LTL growth

2.24

.54

2.56

.55

Slowdown scenario - 0% LTL growth

110

106

-0.7 2.24

.53

122

115

-1.9

1.3

-10.0

2.4 .66

Note: LTL - Like to Like Sales growth is growth in sales of stores which have been operational for more than a year. Cash profit is profit after tax plus depreciation. Assumed that only 50% of the cash profit of the previous year is used as equity for expansion. Sales from new stores is assumed 50% of the existing store sales for retailer A and 60% for retailer B in the year of opening. Margin of safety is a percentage of break even point. Source: Kanvic analysis

Retailer A, adds 20 new stores every year Retailer B, adds 10 stores every year

Exhibit 15Modelling scenarios under different levels of growth and leverage

Y1

Y2

Y3

Y2

Y3

120

116

143

136

3.9

4.5

2.5

4.4

1.9

4.9

0.6

2.6

14.6

17.8

17.7

7.7

4.9

20.9

3.28

8.0

We then model the performance of these two retailers under a normal growth scenario that sees Like-to-Like sales grow at 10% in years 2 and 3, and then under a slowdown scenario that sees Like-to-Like sales growth at 0% in years 2 and 3.

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

51

9 The current profit model of two retailers is taken as a basis to build our growth strategy model. Our assumptions include 5% escalation in fixed costs, interest at 12% and the debt repayable in 5 years.

10 Measured on the total number of stores at the end of Year-1 (Y1)

11 Cash profit is calculated by adding back depreciation to profit after tax.

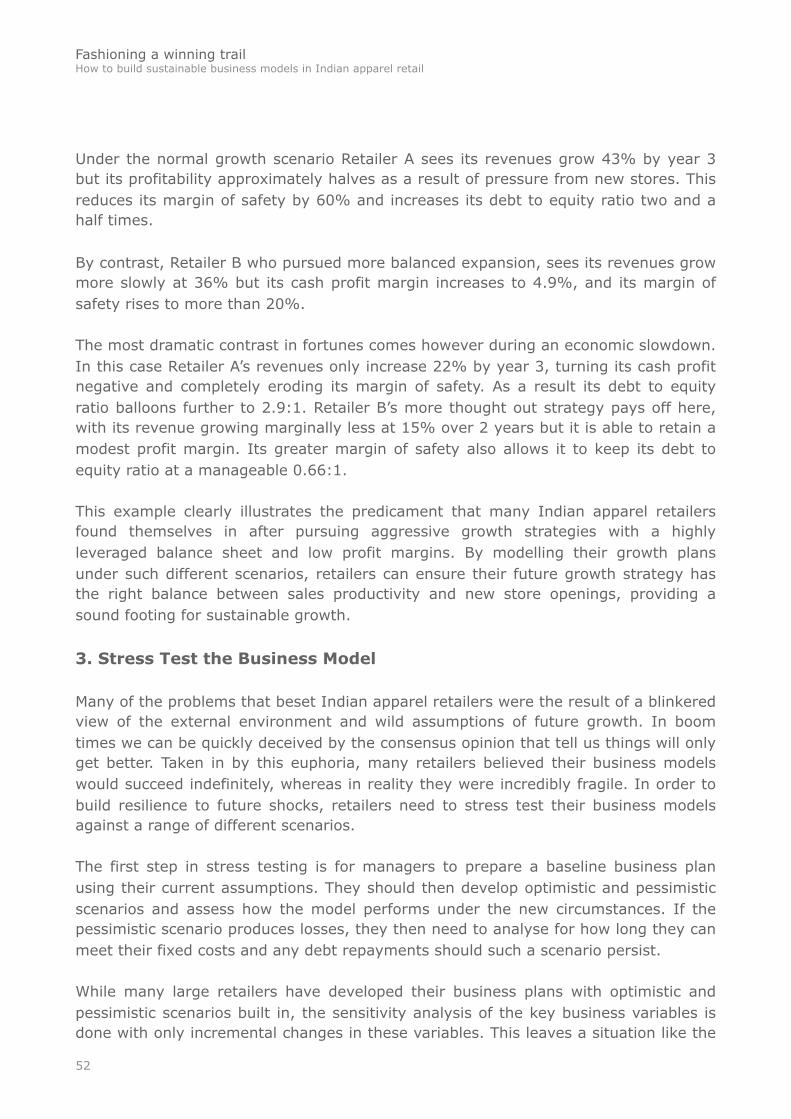

Under the normal growth scenario Retailer A sees its revenues grow 43% by year 3 but its profitability approximately halves as a result of pressure from new stores. This reduces its margin of safety by 60% and increases its debt to equity ratio two and a half times.

By contrast, Retailer B who pursued more balanced expansion, sees its revenues grow more slowly at 36% but its cash profit margin increases to 4.9%, and its margin of safety rises to more than 20%.

The most dramatic contrast in fortunes comes however during an economic slowdown. In this case Retailer A’s revenues only increase 22% by year 3, turning its cash profit negative and completely eroding its margin of safety. As a result its debt to equity ratio balloons further to 2.9:1. Retailer B’s more thought out strategy pays off here, with its revenue growing marginally less at 15% over 2 years but it is able to retain a modest profit margin. Its greater margin of safety also allows it to keep its debt to equity ratio at a manageable 0.66:1.

This example clearly illustrates the predicament that many Indian apparel retailers found themselves in after pursuing aggressive growth strategies with a highly leveraged balance sheet and low profit margins. By modelling their growth plans under such different scenarios, retailers can ensure their future growth strategy has the right balance between sales productivity and new store openings, providing a sound footing for sustainable growth.

3. Stress Test the Business Model

Many of the problems that beset Indian apparel retailers were the result of a blinkered view of the external environment and wild assumptions of future growth. In boom times we can be quickly deceived by the consensus opinion that tell us things will only get better. Taken in by this euphoria, many retailers believed their business models would succeed indefinitely, whereas in reality they were incredibly fragile. In order to build resilience to future shocks, retailers need to stress test their business models against a range of different scenarios.

The first step in stress testing is for managers to prepare a baseline business plan using their current assumptions. They should then develop optimistic and pessimistic scenarios and assess how the model performs under the new circumstances. If the pessimistic scenario produces losses, they then need to analyse for how long they can meet their fixed costs and any debt repayments should such a scenario persist.

While many large retailers have developed their business plans with optimistic and pessimistic scenarios built in, the sensitivity analysis of the key business variables is done with only incremental changes in these variables. This leaves a situation like the

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

52

2008 global financial crisis out of sight. To really prepare themselves for future uncertainties, retailers need to stress test their business models under ‘extreme’ but probable scenarios, not with a series of minor or incremental tweaks. Such testing may involve inputs such as like-to-like sales ending in a negative territory or the key costs spiralling over a short period of time. In addition to internal business variables, retailers also need to test their business models for key external assumptions e.g. policy decisions getting delayed in unanticipated ways.

Furthermore, it is important that such stress testing is conducted by people who are emotionally detached from the current business strategy and are able to factor in future scenarios more objectively. This ‘outside in’ approach helps in revealing the potential blind spots and testing the business model for future shocks in the economy.

This kind of stress testing is particularly critical before adopting major strategic changes such as changing the store format or switching to a new business model. It is important to note that the real value of stress testing is much more in going through the process than in trying to predict the future.

Once the performance of the business model has been assessed and the key risks identified, the company then needs to decide what measures it can take to mitigate them. For example, given the future performance under ‘extreme’ scenarios, retailers could take a more measured approach to growth or they might improve their risk profile by altering their leverage.

It is also possible to run with the same business model but build in risk mitigation to deal with future downturns in the business. For example, one mid-sized Indian apparel retailer has created a ‘business fund’ of Rs. 10 Crores that can be deployed in case of a serious downturn.

4. Make the right entry decisions

Choosing when and where to enter a new market is critical to retail success. A large number of retailers have tied themselves into undesirable locations and unsustainable rentals on the basis of aggressive expansion targets and speculation about future trends in the real estate market. However, by ignoring the market realities of specific locations retailers have put their sustainability at risk.

Before committing to a new store location retailers need to first assess the overall demand and supply scenario in the given geography to understand its broad potential. As retailers opened their first stores in the metros and large Indian cities, these locations have reached various levels of saturation in supply across different product categories. For example, Pune has an oversupply of retail space, creating tough competition among incumbents. Any new entrant will face major resistance in this

Fashioning a winning trail How to build sustainable business models in Indian apparel retail

53

market and will find it difficult to generate the expected sales until the retailer offers a really unique value proposition. On the other hand, the attention to new growth markets in tier 2 and tier 3 cities has not delivered the expected results. Bikaner, a smaller city in Rajasthan is under-penetrated and under served for apparels but the existing players seem to have a complete disconnect with the local customers and their preferences. This leaves the opportunity wide open to nimble regional players and local MBOs.

After deciding on the city, retailers must then drill down and assess the attractiveness of the new market, in terms of the availability of their target customer segment and the level of competition from retailers in the same strategic group. This will reveal the micro markets within the city and help decide the right locations. While retailers may mention ‘location, location, location’ as a key factor for success, they sometimes overlook the basics in a rush to open stores and have their presence in ‘hip’ locations. In our work, we came across a large International retailer with over 2,000 stores that was making location decisions based on a ‘flying visit’ to the city’s latest trendy spots, without thinking through its target segments and the competition. Such passing attention to choosing store locations will not help retailers in making stores profitable.

Retailers also need to test the fit of any new location with their existing or planned store network. Having sufficient knowledge of a particular market and its customer base and being able to efficiently manage and stock a store is critical to its profitability.

Here, increasing store density in a specific city or region rather than rapidly jumping to new part of the country retailers can reap a number of benefits. Firstly, it delivers greater economies in warehousing and transportation of goods, particularly given India’s challenging infrastructure scenario. Furthermore, as we have found in our client work, a close proximity of stores makes it easier to transfer experienced staff to support new outlets, helping to share knowledge and instil the company culture at the new location. Finally, achieving higher store density can deliver greater economies in advertising spend as a single media campaign benefits multiple locations. This is highly pertinent in India’s strongly regional media market.

Finally, when a retailer is operating a number of outlets serving similar customer profiles they are able to cluster stores. Clustering allows them to replicate product mix, pricing, staffing and store design across multiple stores rather than going to the added complexity and cost of individual plans.

5. Demonstrate boldness in exiting