fatca:investment reporting and … reporting and the...i. fatca purposes impacts of fatca (1) •...

TRANSCRIPT

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN

FINANCIAL INSTITUTIONS

Barbados International Business Association Conference

October 26, 2012

Bruce Zagaris

Partner Berliner, Corcoran, & Rowe LLP

1101 17th St. NW, Ste. 1100 Washington D.C. 20036 (202)293-2371 (phone)

(202)293-9035 (fax)

1

I. FATCA Purposes

• The purpose of FATCA is to guarantee U.S. persons with financial assets

outside the U.S. declare their income and assets.

• U.S. Withholding Agents and Participating Foreign Financial

Institutions must withhold 30% on U.S. sourced payments and

payments subject to Pass Thru withholding to foreign

institutions/entities that don’t comply.

• FATCA is effective January 2013. However, in most cases, withholding

will generally begin on or after January 1, 2014.

2

I. FATCA Purposes Impacts of FATCA (1)

• U.S. Withholding Agents: U.S. person that has control, receipt, custody disposal or payment of any withholdable payment.

• U.S. Financial Institutions (FIs): U.S. entity that accepts deposits, holds financial assets for the account of others as a substantial part of its business, or engages (or holds itself out as being engaged) primarily in the business of investing or trading securities, commodities, partnerships, or any interests in such positions.

• Foreign Financial Institutions (FFIs): Non-U.S. entity that accepts deposits, holds financial assets for the account of others as a substantial part of its business, or engages (or holds itself out as being engaged) primarily in the business of investing or trading securities, commodities, partnerships, or any interests in such positions

3

I. FATCA Purposes Impacts of FATCA (2)

• Non Financial Foreign Entities: Includes any foreign entity that is not a FFI or is not one of the following specifically EXCEPTED entities:

•Any publicly traded corporation and its corporate affiliates (more than 50% of vote and value)

•Any entity organized under the laws of a possession of the U.S.

•Any foreign government, or any wholly owned agency thereof

•Any international organization or any wholly owned agency or instrumentality of such

•Any foreign central bank (unless acting as intermediary for clients)

•Any other class of persons identified by the Secretary as posing a low risk of tax evasion.

• U.S. individuals: U.S. citizens, U.S. residents (e.g., Green cardholder) and nonresident aliens who meet the substantial presence test

4

I. FATCA Purposes Key Requirements (1)

• Registration: The IRS has proposed that participating FFIs or deemed-compliant FFIs can register online with the IRS before 30 June 2013 to avoid withholding from 1 January 2014.

• Remediation: Organizations will need to search electronic information on pre-existing accounts maintained or executed by the withholding agent as of 1 January 2013 or executed by the FFI prior to the effective date of the FFI agreement.

• Withholding: Participating FFIs are still required to withhold on payments made to non-participating FFIs beginning on 1 Jan 2014.

• Withholding on gross proceeds begins in 2017.

5

I. FATCA Purposes Key Requirements (2)

• Reporting: For calendar years 2013 and 2014, participating FFIs are required to report only name, address, TIN, account number, and account balance with respect to US accounts (as well as data on recalcitrant accounts).

• Income received will be reported in 2015, and full reporting is effective in 2016.

• Client/Investor: The proposed regulations generally do not require an FFI to make significant modifications to the information collected on customer intake, and existing KYC processes can generally be used, except in specific cases.

6

I. FATCA Purposes FATCA Implications (1)

• USFI Requirements:

• Identify all account holders that are foreign entities;

• Determine FATCA taxonomy status (e.g. FFI, NFFE) of foreign entity accounts;

• Obtain required documentation and certifications from foreign entity accounts;

• Maintain scanned documents associated with each account to support the decisions made; and

• Establish a process for FATCA withholding and reporting for non-compliant foreign entity accounts (non-participating FFIs and NFFEs that do not provide appropriate certification).

7

I. FATCA Purposes FATCA Implications (2)

• FFI Requirements:

• Enter into an FFI agreement with the IRS

• Obtain information to determine which account holders and beneficiaries are U.S. accounts;

• Comply with verification and due diligence procedures on such accounts as required by the IRS;

• Report information regarding “specified” U.S. accounts to the IRS on an annual basis (where foreign law would prevent such reporting, obtain a waiver, and if unable to obtain a waiver, close the account);

• Deduct and withhold the 30% tax on payments to recalcitrant account holders, non-compliant NFFEs, electing FFIs, and FFIs that did not enter into an FFI agreement with the IRS; and

• Comply with requests from the IRS for any additional information.

8

I. FATCA Purposes Key FATCA preparation activities

Key elements for FATCA preparations are: • Analyze an entity’s existing investor information within the current share

registry and new FATCA requirements • Define policies and procedures for incorporating FATCA data requirements

within the new customer intake procedure and KYC/AML process • Submit required information to the U.S. Treasury to obtain FFI status, and

communicate FFI compliance number to trading counterparties and custodians (for U.S. and non-U.S. assets)

• Establish methodology and reporting policies and procedures for maintaining Pass Thru Payment Percentage (PPP)

• Identify systematic enhancements or service provider oversight programs to track:

• FFI status

• PPP

• Withholding amounts

• Adjustments to investor capital balances for FATCA withholdings

• Tracking of amounts paid to the U.S. Treasury

• Post-FATCA investor reporting. 9

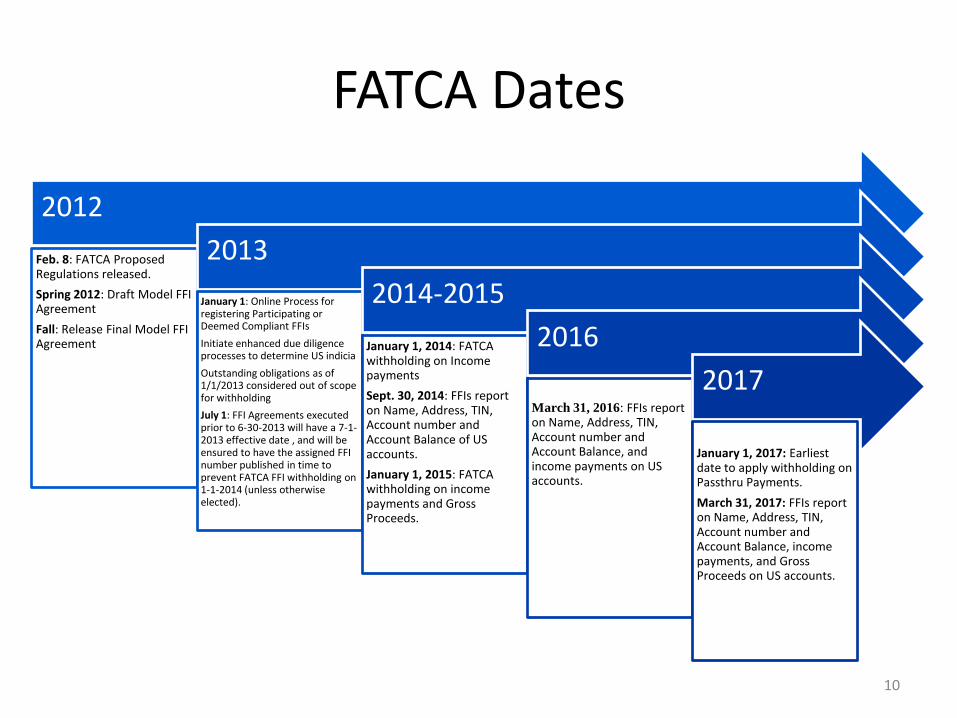

FATCA Dates

2012

Feb. 8: FATCA Proposed Regulations released.

Spring 2012: Draft Model FFI Agreement

Fall: Release Final Model FFI Agreement

2013

January 1: Online Process for registering Participating or Deemed Compliant FFIs

Initiate enhanced due diligence processes to determine US indicia

Outstanding obligations as of 1/1/2013 considered out of scope for withholding

July 1: FFI Agreements executed prior to 6-30-2013 will have a 7-1-2013 effective date , and will be ensured to have the assigned FFI number published in time to prevent FATCA FFI withholding on 1-1-2014 (unless otherwise elected).

2014-2015

January 1, 2014: FATCA withholding on Income payments

Sept. 30, 2014: FFIs report on Name, Address, TIN, Account number and Account Balance of US accounts.

January 1, 2015: FATCA withholding on income payments and Gross Proceeds.

2016

March 31, 2016: FFIs report on Name, Address, TIN, Account number and Account Balance, and income payments on US accounts.

2017

January 1, 2017: Earliest date to apply withholding on Passthru Payments.

March 31, 2017: FFIs report on Name, Address, TIN, Account number and Account Balance, income payments, and Gross Proceeds on US accounts.

10

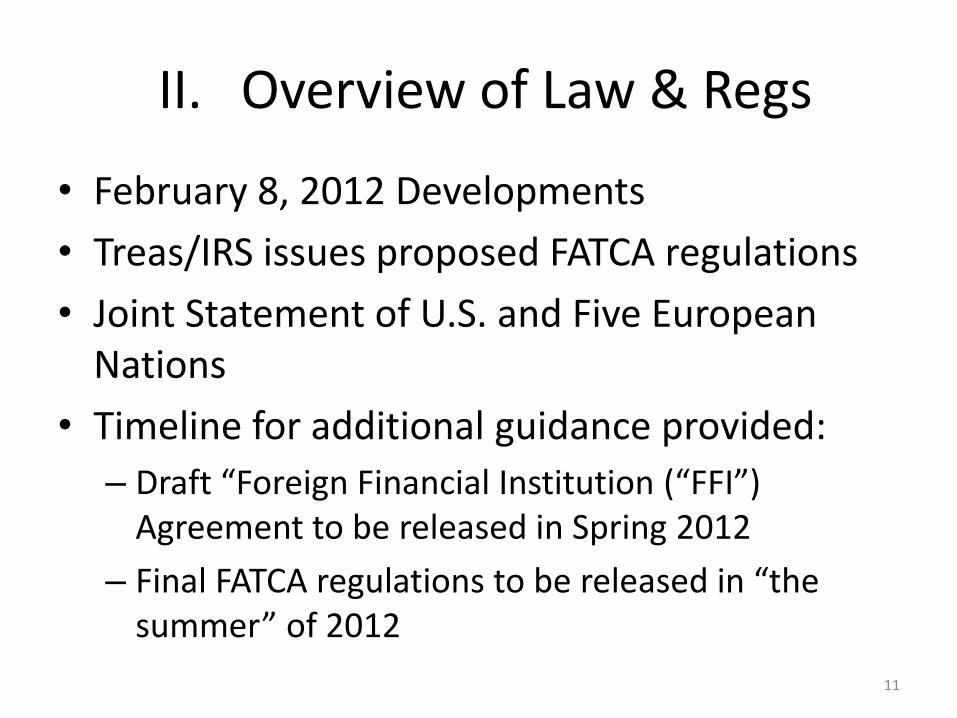

II. Overview of Law & Regs

• February 8, 2012 Developments

• Treas/IRS issues proposed FATCA regulations

• Joint Statement of U.S. and Five European Nations

• Timeline for additional guidance provided:

– Draft “Foreign Financial Institution (“FFI”) Agreement to be released in Spring 2012

– Final FATCA regulations to be released in “the summer” of 2012

11

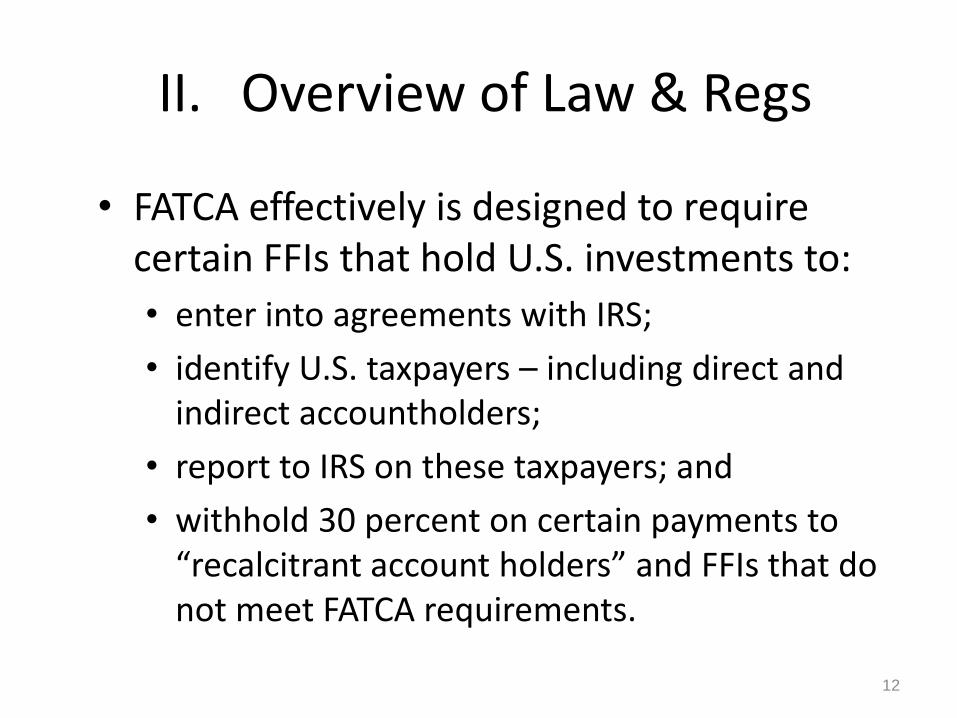

II. Overview of Law & Regs

• FATCA effectively is designed to require certain FFIs that hold U.S. investments to:

• enter into agreements with IRS;

• identify U.S. taxpayers – including direct and indirect accountholders;

• report to IRS on these taxpayers; and

• withhold 30 percent on certain payments to “recalcitrant account holders” and FFIs that do not meet FATCA requirements.

12

II. Overview of Law & Regs

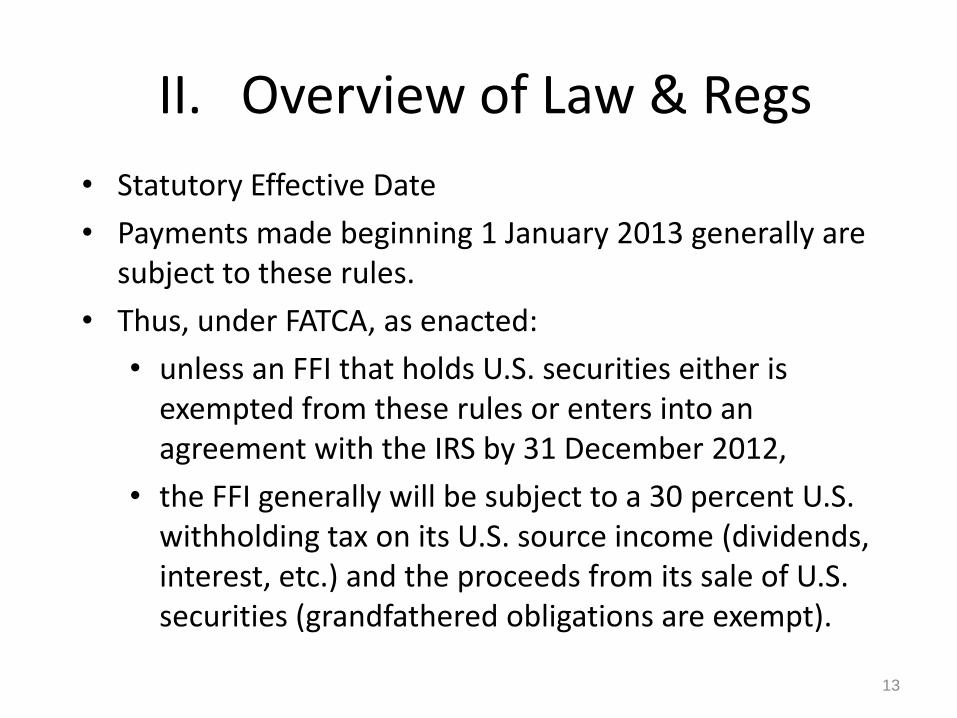

• Statutory Effective Date

• Payments made beginning 1 January 2013 generally are subject to these rules.

• Thus, under FATCA, as enacted:

• unless an FFI that holds U.S. securities either is exempted from these rules or enters into an agreement with the IRS by 31 December 2012,

• the FFI generally will be subject to a 30 percent U.S. withholding tax on its U.S. source income (dividends, interest, etc.) and the proceeds from its sale of U.S. securities (grandfathered obligations are exempt).

13

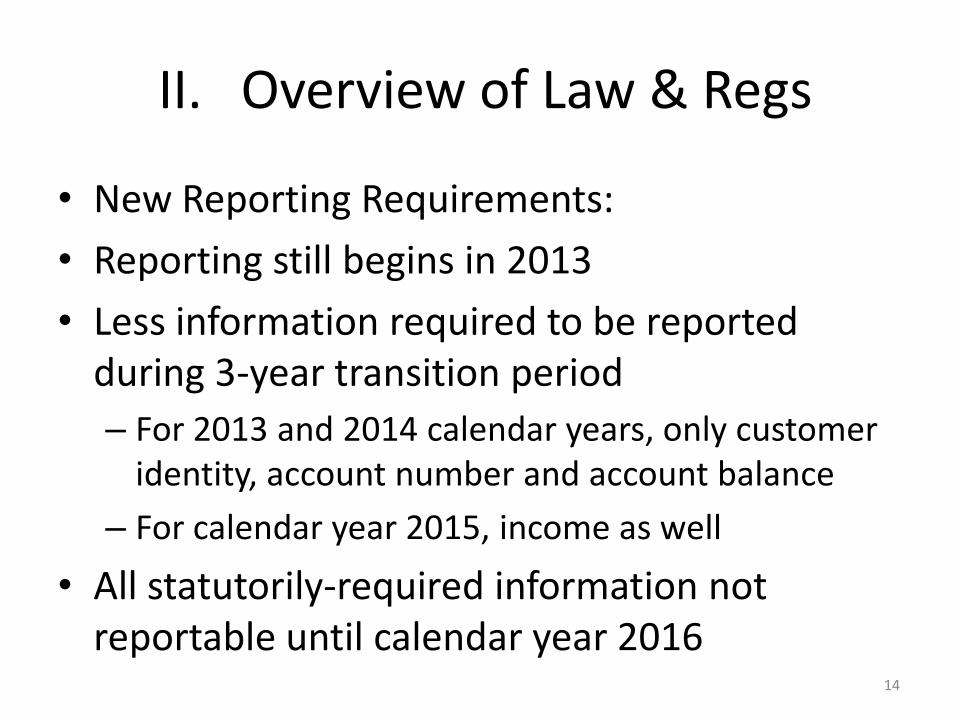

II. Overview of Law & Regs

• New Reporting Requirements:

• Reporting still begins in 2013

• Less information required to be reported during 3-year transition period

– For 2013 and 2014 calendar years, only customer identity, account number and account balance

– For calendar year 2015, income as well

• All statutorily-required information not reportable until calendar year 2016

14

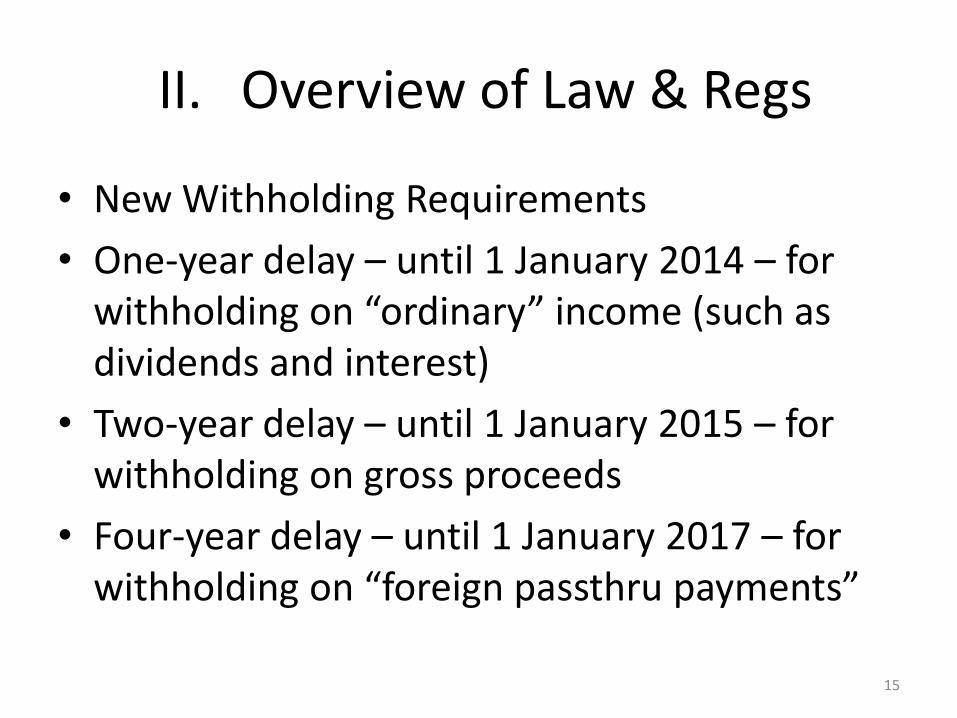

II. Overview of Law & Regs

• New Withholding Requirements

• One-year delay – until 1 January 2014 – for withholding on “ordinary” income (such as dividends and interest)

• Two-year delay – until 1 January 2015 – for withholding on gross proceeds

• Four-year delay – until 1 January 2017 – for withholding on “foreign passthru payments”

15

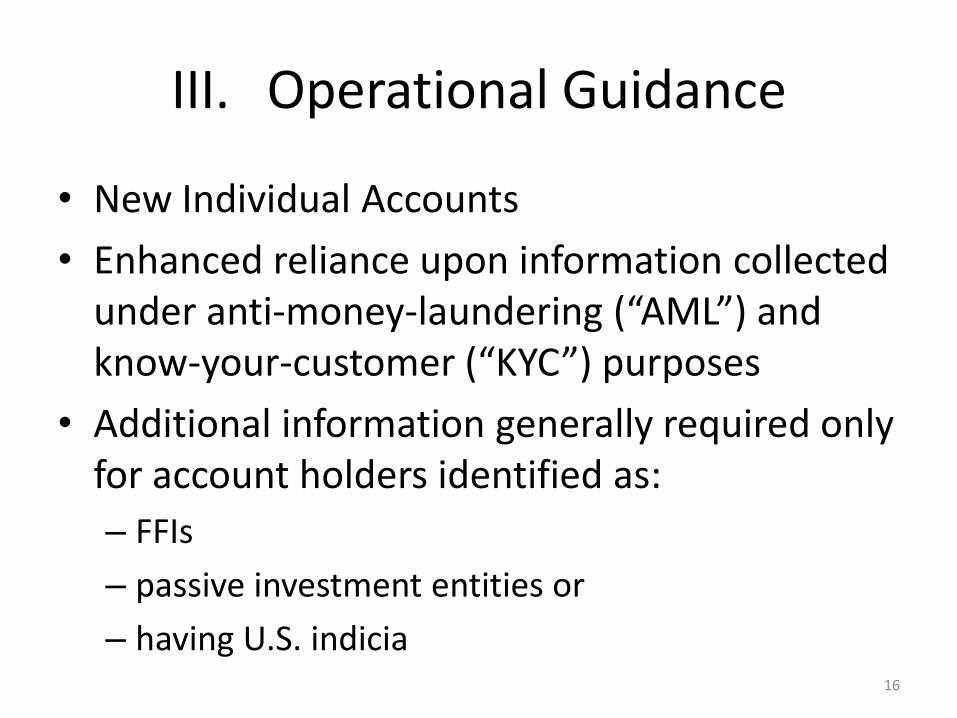

III. Operational Guidance

• New Individual Accounts

• Enhanced reliance upon information collected under anti-money-laundering (“AML”) and know-your-customer (“KYC”) purposes

• Additional information generally required only for account holders identified as:

– FFIs

– passive investment entities or

– having U.S. indicia 16

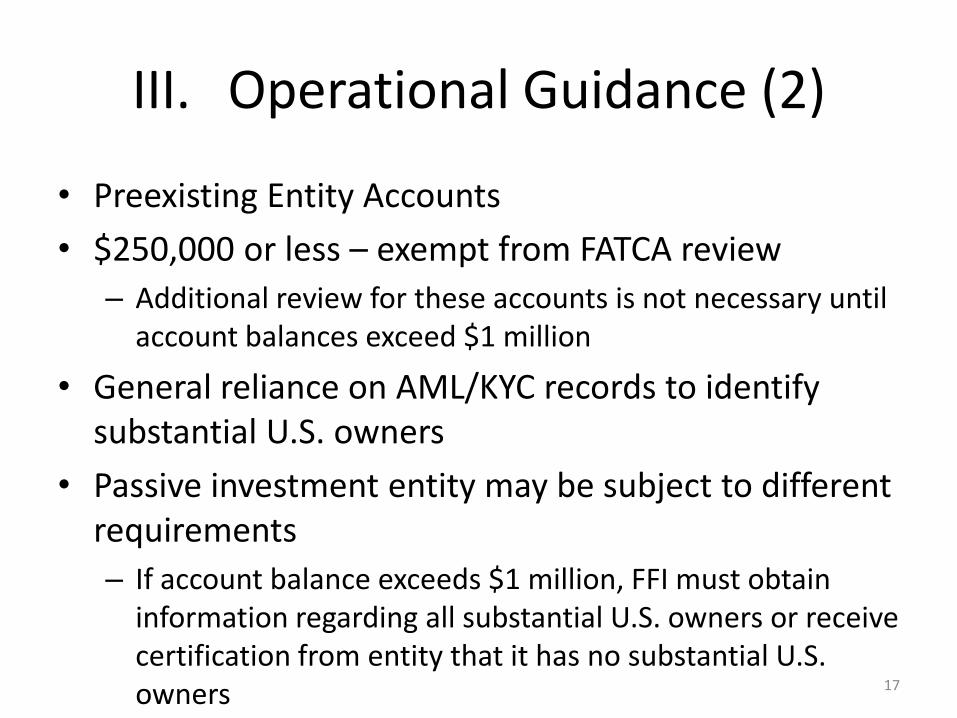

III. Operational Guidance (2)

• Preexisting Entity Accounts

• $250,000 or less – exempt from FATCA review

– Additional review for these accounts is not necessary until account balances exceed $1 million

• General reliance on AML/KYC records to identify substantial U.S. owners

• Passive investment entity may be subject to different requirements

– If account balance exceeds $1 million, FFI must obtain information regarding all substantial U.S. owners or receive certification from entity that it has no substantial U.S. owners 17

III. Operational Guidance (3)

• If entity is “active” nonfinancial foreign entity (an “active NFFE”), NO requirement to determine whether entity has U.S. owners

– Active NFFE defined as any NFFE with

• less than 50 percent of income for calendar year from passive sources and

• less than 50 percent of assets produce passive income

• Determination of substantial U.S. owners will be required only for “passive” NFFE

18

III. Operational Guidance (4)

• FFI Agreement Certifications

• “Responsible officer” of FFI must certify that :

– written compliance policies and procedures adopted;

– periodic internal compliance reviews will be conducted; and

– certifications and other information will be provided periodically to allow IRS to determine whether FFI has met its obligations

19

III. Operational Guidance (5)

• Deemed Compliant Categories

• One change in the proposed regulations that will be considered a major improvement over prior guidance is the expansion of the categories of deemed-compliant entities, which are another term of art.

• Notice 2011-34 gave initial guidance on categories of FFIs that would be considered deemed compliant.

• They would not have to enter into a FFI Agreement with the IRS in order to be relieved from FATCA withholding.

20

III. Operational Guidance (6) Deemed Compliant Categories (2)

• The proposed regulations include broader categories of deemed-compliant entities than were in the earlier guidance and permit some types of FFIs, such as retirement plans, to self-certify that they meet the requirements to be a deemed-compliant entity.

• Registered Deemed-Compliant FFI

• Certified Deemed-Compliant FFI

• Owner-Documented FFIs

21

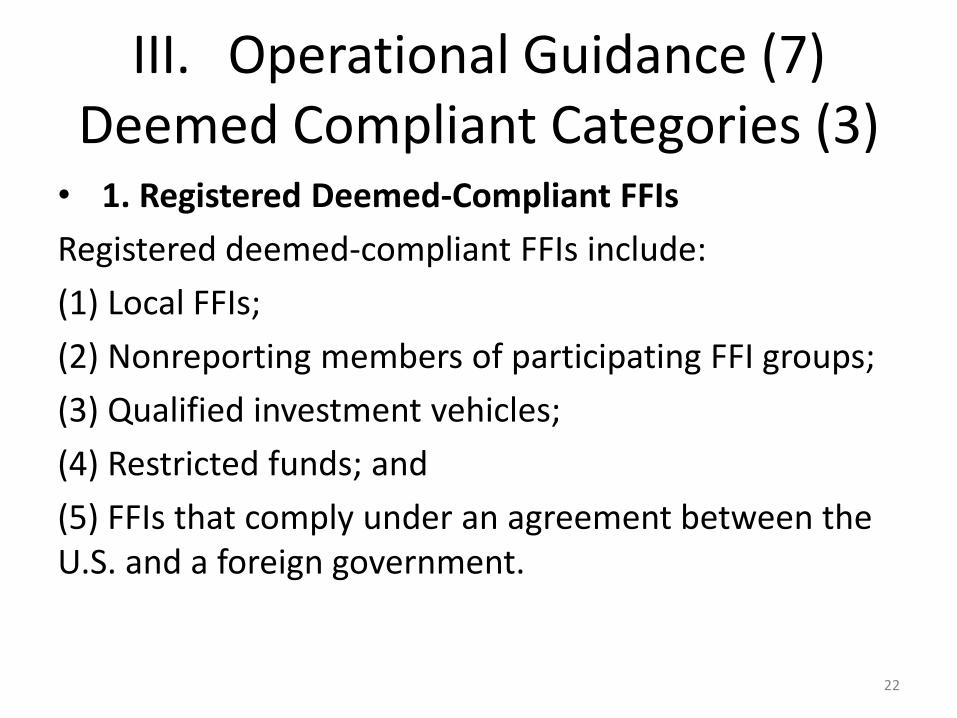

III. Operational Guidance (7) Deemed Compliant Categories (3)

• 1. Registered Deemed-Compliant FFIs

Registered deemed-compliant FFIs include:

(1) Local FFIs;

(2) Nonreporting members of participating FFI groups;

(3) Qualified investment vehicles;

(4) Restricted funds; and

(5) FFIs that comply under an agreement between the U.S. and a foreign government.

22

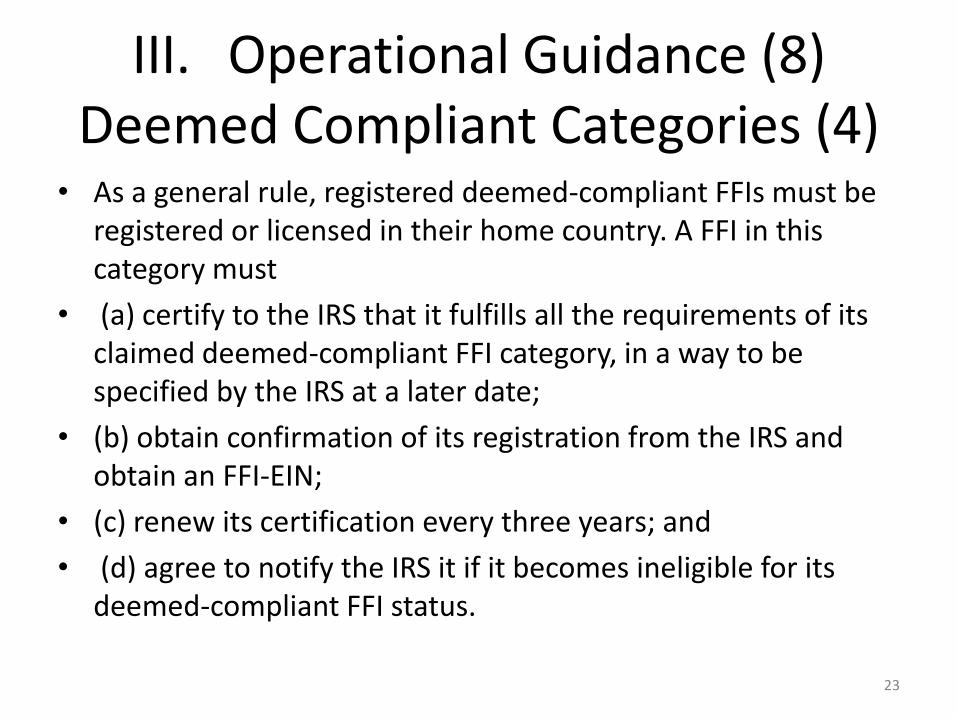

III. Operational Guidance (8) Deemed Compliant Categories (4)

• As a general rule, registered deemed-compliant FFIs must be registered or licensed in their home country. A FFI in this category must

• (a) certify to the IRS that it fulfills all the requirements of its claimed deemed-compliant FFI category, in a way to be specified by the IRS at a later date;

• (b) obtain confirmation of its registration from the IRS and obtain an FFI-EIN;

• (c) renew its certification every three years; and

• (d) agree to notify the IRS it if it becomes ineligible for its deemed-compliant FFI status.

23

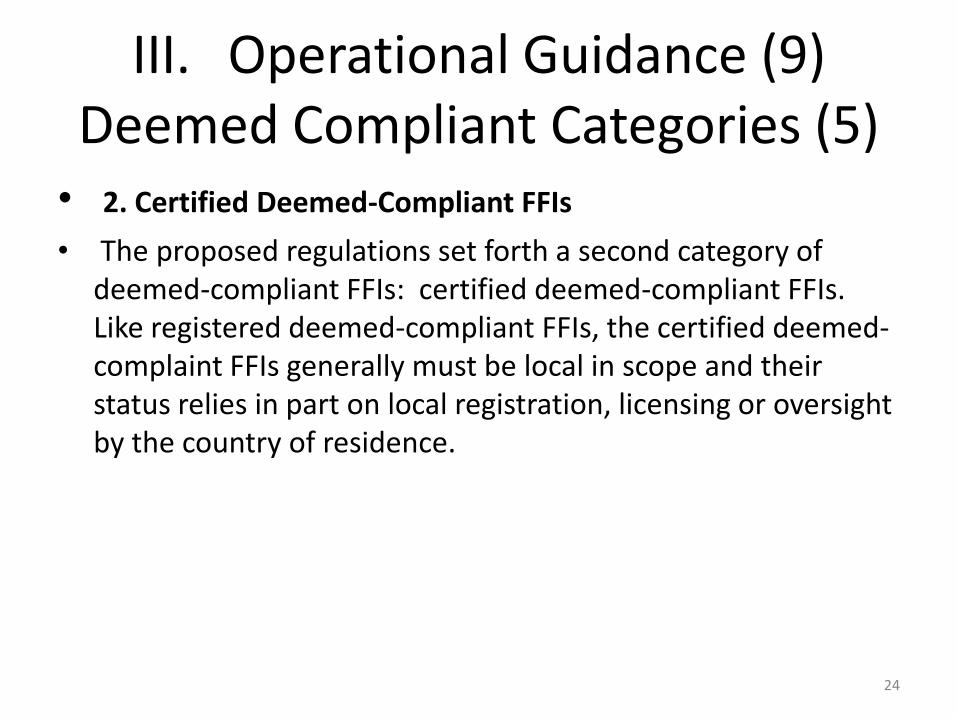

III. Operational Guidance (9) Deemed Compliant Categories (5)

• 2. Certified Deemed-Compliant FFIs

• The proposed regulations set forth a second category of deemed-compliant FFIs: certified deemed-compliant FFIs. Like registered deemed-compliant FFIs, the certified deemed-complaint FFIs generally must be local in scope and their status relies in part on local registration, licensing or oversight by the country of residence.

24

III. Operational Guidance (10) Deemed Compliant Categories (6)

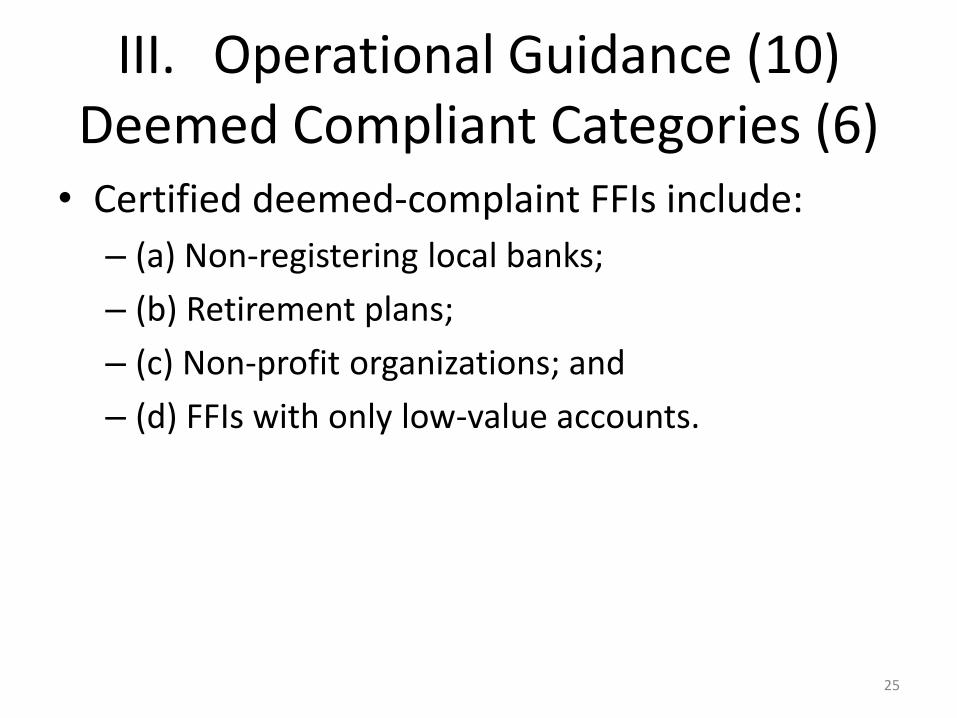

• Certified deemed-complaint FFIs include:

– (a) Non-registering local banks;

– (b) Retirement plans;

– (c) Non-profit organizations; and

– (d) FFIs with only low-value accounts.

25

III. Operational Guidance (11) Deemed Compliant Categories (7)

• 3. Owner-Documented FFIs -- Owner-documented FFIs are deemed-compliant only with respect to payments received by or accounts held with a withholding agent. They must provide certain documentation of their status to withholding agents and they may not act as intermediaries.

26

III. Operational Guidance (12) Deemed Compliant Categories (8)

• Certified deemed-compliant FFIs must provide a withholding agent with certain documentation (including withholding certificates and financial statements), certifying their status as to the relevant deemed-complaint category.

27

III. Operational Guidance (13)

Pass-thru Payments • The proposed regulations delay withholding on pass-thru

payments until January 1, 2017.

• To reduce incentives for nonparticipating FFIs to use participating FFIs to block the FATCA rules, the proposed regulations require that participating FFIs report annually to the IRS the aggregate amount of certain payments made to each nonparticipating FFI until withholding applies.

• The proposed regulations request comments on how to implement the pass-thru payment rules.

28

III. Operational Guidance (14) Pass-thru Payments (2)

• The proposed regulations indicate that Treasury and the IRS are seeking to develop alternative approaches to implementing the policy objectives of the pass-thru payment rules with foreign governments.

• At present no pass-thru payment withholding is required on foreign pass-thru payments. According to the preamble to the FATCA proposed regulations, withholding on foreign pass-thru payments will be required starting in 2017.

• However, for 2015 and 2016, PFFIs must report the aggregate amount of certain payments to NPFFIs.

29

III. Operational Guidance (15) Due Diligence Requirements

• The proposed regulations would revise due diligence requirements for preexisting accounts to permit for primarily electronic reviews.

• Under the proposed regulations manual reviews would be limited to accounts with a balance or value of over $1 million, and would exclude individual accounts with a balance or value of $50,000 or less, and some case value insurance contracts with a value of $250,000 or less, from the due diligence

procedure.

30

III. Operational Guidance (16) Due Diligence Requirements (2)

• In response to comments from many financial institutions, the new due diligence requirements also would eliminate the private banking test from Notice 2011-34 that would have required banks to do paper searches for many more accounts in order to identify U.S. indicia and would have put more emphasis on information known by relationship managers.

• The new $1 million threshold would reduce the instances where financial institutions must perform the due diligence searches.

• Banks can rely on electronic searches for accounts under the $1 million threshold.

31

III. Operational Guidance (17) Due Diligence Requirements (3)

• The proposed regulations provide more to the list of indicia of U.S. status, such as a U.S. telephone number and a U.S. place of birth as another reason to know that a withholding certificate establishing foreign status is unreliable.

• Detailed due diligence requirements must be performed for account holders that are entities. They are intended to provide maximum flexibility, so that in some cases the burden on the FFIs and U.S. withholding agents could be reduced.

• The proposed regulations have an exception from withholding for nonfinancial foreign entities (NFFEs) that are not passive. For pre-existing accounts held by some NFFEs, FFIs can rely on AML inquiries already performed.

32

III. Operational Guidance (18) Coordination with Other U.S. Tax

Withholding Rules

• If a payment is subject to regular income withholding, the amount withheld receives a credit against any FATCA withholding taxes that must be withheld. If a payment is subject to withholding under the Foreign Investment in Real Property Tax Act (FIRPTA), it is not subject to FATCA withholding.

• Amounts subject to withholding on a partnership allocation of income effectively connected with the conduct of a trade or business in the U.S. under IRC Section 1446 are not subject to FATCA withholding.

33

III. Operational Guidance (19) Transition Rules for Affiliated Groups

• Notice 2011-34 provided that the IRS will require that each FFI be a member of an expanded affiliated group (“EAG”) that is a PFFI or a deemed-compliant FFI in order for any FFI in the expanded affiliated group to become a PFFI.

• The proposed regulations recognize the legal, political, and economic issues in countries that presently impose prohibitions that do not permit fulfillment of the requires and have a two-year transition, until January 1, 2016, to

implement this requirement.

34

III. Operational Guidance (20) Transition Rules for Affiliated Groups (2)

• The proposed regulations state that during the transition period a branch or affiliate of an FFI in a jurisdiction that forbids the reporting or withholding required by FATCA will not preclude the other FFIs within the same EAG from concluding a FFI Agreement.

• Notwithstanding any local law prohibition, on or before January 1, 2016, all members of an EAG must have concluded a FFI Agreement. Otherwise, no member of the EAG will be treated as a PFFI.

• The FFI must also meet various requirements to qualify for the transition rule for a limited branch.

35

III. Operational Guidance (21) Verification Procedures

• The proposed regulations modify prior guidance concerning

procedures through which FFIs could verify their compliance with FATCA.

• The new rules provide that some officers of a participating FFI will certify under penalties of perjury that the FFI has complied with the terms of its FFI agreement.

• The proposed regulations require a participating FFI to show compliance with its FFI Agreement. The IRS will provide for a model FFI Agreement in a future Revenue Procedure. The proposed regulations state that

36

III. Operational Guidance (22) Verification Procedures (2)

• (i) the FFI will adopt written policies and procedures to comply with its obligations;

• (ii) the FFI will conduct periodic internal reviews of its compliance; and

• (iii) the FFI will periodically provide certification of its compliance by its responsible officers.

• The proposed regulations state that no third-party audits will occur, a welcome development to the financial community. However, if the IRS has concerns about the PFFI’s compliance based on its reporting and certification, or if the PFFI repeatedly fails to comply, the IRS may impose additional verification requirements, such as external audits of the PFFI’s compliance by IRS-approved third-party auditors 37

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (1) • The proposed framework would allow the U.S. and a

partner country to conclude an agreement in which the foreign country would agree to collect information required by FATCA and transfer that information to the IRS.

• As a result, FFIs in the foreign country could avoid having to conclude directly a FFI agreement with the IRS and would eliminate U.S. withholding on payments to FFIs established in the foreign country.

38

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (2) • The agreement would also obligate the U.S. to reciprocate

regarding automatic collecting and reporting on the U.S. accounts of residents of the FATCA partner.

• To reciprocate, the U.S. has issued final bank interest reporting regulations (REG-146097-09) under section 6049.

• Those proposed rules would extend information reporting to include bank deposit interest paid to nonresident alien individuals who are residents of any foreign country. At present the U.S. reports only on interest paid to U.S. persons and Canadian residents.

39

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (3) • In the Joint Statement the six countries commit to "working

with other FATCA partners, the OECD, and where appropriate, the EU, on adapting FATCA in the medium term to a common model for automatic exchange of information.“

• The U.S. and a FATCA partner would conclude an agreement pursuant to which, subject to certain terms and conditions, the FATCA partner would agree to:

40

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (4) • (1) pursue the necessary implementing

legislation to require FFIs in its jurisdiction to collect and report to the authorities of the FTCA partner the required information;

• (2) enable FFIs established in the FATCA partner (other than FFIs that are excepted pursuant to the agreement or in U.S. guidance) to apply the necessary diligence to identify U.S. accounts; and

• (3) transfer to the U.S., on an automatic basis, the information reported by the FFIs.

41

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (5)

• The bilateral agreement would require the U.S. to:

• (1) eliminate the obligation for each FFI in the FATCA partner to enter into a separate comprehensive FFI agreement directly with the IRS, provided that each FFI is registered with the IRS or is excepted from registration pursuant to the agreement or IRS guidance;

• (2) allow FFIs in the FATCA partner to comply with their reporting obligations under FATCA by reporting information to the FATCA partner rather than reporting it directly to the IRS;

• (3) eliminate U.S. withholding under FATCA on payments to FFIs in the FATCA partner (i.e., by identifying all FFIs in the FATCA partner as participating FFIs or deemed-complaint FFIs, as appropriate);

42

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (6) • (4) identify in the agreement specific categories of FFIs

established in the FATCA partner that would be treated, consistent with the IRS guidelines, as deemed compliant or presenting a low risk of tax evasion; and

• (5) commit to reciprocity with respect to collecting and reporting on an automatic basis to the authorities of the FATCA partner information on the U.S. accounts of residents of the FATCA partner.

43

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (7) • Additionally, pursuant to the agreement, FFIs in the FATCA

partner would not have to:

• (6) terminate the account of a recalcitrant account holder; impose pass-thru payment withholding in payments to recalcitrant account holders; and

• (7) impose pass-thru payment withholding on payments to other FFIs organized in the FATCA treaty partner or in another jurisdiction with which the U.S. has a FATCA implementing agreement.

44

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (8) • In return, the FATCA partner would commit to developing a

practical and effective alternative approach to achieve the policy objectives of pass-thru payment withholding that minimizes burden; and

• commit to working with other FATCA partners, the OECD, and where appropriate the EU, on adapting FATCA in the medium term to a common model for automatic exchange of information, including the development of reporting and due diligence standards.

45

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA (9) • The one burden imposed on other governments concluding

a Joint Statement with the U.S. is that it does require them to receive the FATCA reports and forward them to the U.S. Hence, there would be additional cost and human resource burden on the tax authority of the FATCA partner.

• Future Questions:

– Will jurisdictions prioritizing financial privacy want to conclude new arrangements?

46

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA

(10) – Will the U.S. legislative and executive branches be able to

reciprocate in terms of furnishing information on FATCA “withholdable payments” since they include not only U.S.-source payments such as dividends, interest and other types of U.S.-source payments, but also gross proceeds from the sale of assets that can produce U.S. source interest or dividends?

47

IV. Joint Statement Regarding an Intergov’tal Approach to FATCA

(11) • If the U.S. financial institutions must look

through corporate and pass-thru entities to determine the ultimate beneficial owner and provide gross amounts of transactions to the IRS for transmission to foreign governments, the U.S. financial community and the IRS will have to do much more work.

• The details and timing of the U.S. changes are not known at present.

48

IV. Joint Statement Regarding an Intergovernmental Approach

Intergov’tal Approach to FATCA (12)

• It appears that the so called FATCA-5 will not insist on detailed FATCA reciprocity, but only general reciprocity.

• The US hopes that FATCA partners would simply refer to the US legislation in their own tax codes – effectively bringing it into their own legislation.

49

V. UK-US SIGN FIRST FATCA IGA

• Sept. 12, 2012

• Annex II lists exempt UK beneficial owners are: U.K. gov’tal orgs, the U.K. office of int’l organizations, and retirement funds.

• list of Deemed-Compliant FIs:

• non-profit organizations

• FIs with a local client base & exempt products (e.g., certain retirement products, certain other tax-favored accounts or products, such as Individual Savings Accounts (ISAs). 50

V. UK-US SIGN FIRST FATCA IGA (2) • Art 7 has a most-favored-nation provision.

• Art. 7(2) requires the U.S. to notify the U.K. of any such favorable terms and applying such favorable terms automatically.

• Sept. 18, 2012, the HMRC starts a consultation process w 24 questions and seeks to establish “the costs associated with the introduction of FATCA.”

• HMRC will publish draft legislation “by the end of the year”.

51

VI. SWISS-JAPAN MODEL FATCA IGA

• June 21, 2012 US & Swiss & Japan announce 2d model FATCA IGA.

• Swiss & Japan gov’ts would direct all their FIs, not otherwise except or deemed compliant, to conclude a FFI Agrm’t with the IRS.

• Such FIs would receive exempt from criminal provisions prohibiting sharing such information.

52

VI. SWISS-JAPAN FATCA IGA (2)

• The Swiss gov’t would accept and promptly honor, as foreseeably relevant without regard to any other condition, a group request for additional information about U.S. accounts identified as recalcitrant and reported by Swiss FIs on an aggregate basis.

• The U.S. would eliminate U.S. withholding under FATCA on payments to Swiss financial institutions.

53

VI. SWISS-JAPAN FATCA IGA (3)

• The U.S. and Japan model agrmt states they are willing to work with other FATCA partners and the OECD in the medium term on developing a common model for automatic exchange of information, including the development of reporting and due diligence standards.

54

VII. CARIBBEAN FI IMPLICATIONS • Caribbean FIs will either have to enter into FFI

agreements with the IRS comply with FATCA reporting requirements or they will suffer a 30% withholding on most payments from the U.S.

• If they are not FATCA compliant, they will have difficulty accessing payments from other FATCA-compliant institutions & jurisdictions.

• Current bills in Congress further disadvantage US persons dealing with FIs that are not FATCA compliant. 55

VII. CARIBBEAN FI IMPLICATIONS (2)

• Jurisdictions that have a FATCA IGA can apply to exempt those FIs and products whose clients and transactions do not pose a threat of tax evasion.

• For countries wanting the benefits of the exclusions of entities and products and exemptions from the pass-thru payment requirements, but that do not have an Inland Revenue Commission or believe the costs of involving its tax authority are not cost-effective, FATCA Model II may be best.

56

VII. CARIBBEAN FI IMPLICATIONS (3)

• In any case Caribbean countries wanting to prepare for a potential FATCA IGA will want to initiate a consultative process with the financial sector and the broader constituency.

• The U.K. HMRC has initiated such a process in the context of its FATCA IGA with an eye to preparing legislation in its 2013 Budget.

57

VIII. FUTURE WORK

• In 2012 Treasury and the IRS will issue draft forms concerning

FATCA reporting. They still need to revise the QI agreement.

• The IRS will also have to amend the W-8 forms, Form 1042 (Annual Withholding Tax Return for U.S. Source Income of Foreign Persons), and Form 1042-S (Foreign Person's U.S. Source Income Subject to Withholding).

• The draft model FFI Agreement will have more information with respect to the periodic internal review and certification a PFFI must perform in order for the IRS to ascertain whether the PFFI has fulfilled its requirements under the FFI Agreement.

58

VIII. FUTURE WORK (2)

• The proposed regulations do not define comprehensively pass-thru payments, which is any withholdable payment and any foreign pass-thru payment.

• The scope of withholding by both a U.S. withholding agent and an FFI awaits the final definition of the definition of foreign pass-thru payment.

• The statutory withholding rules are different for U.S. financial institutions and FFIs.

• Whereas U.S. financial institutions must withhold only on U.S.-source income, FFIs must withhold on gross proceeds and pass-thru payments as well.

59

VIII. FUTURE WORK (3)

• The Preamble states that future guidance will prevent U.S. financial institutions from acting as blockers for foreign pass-thru payment reporting and withholding.

• For instance, a U.S. person paying foreign-source income to an NPFFI would not have to withhold on a foreign pass-thru payment (that has allocated U.S.-source income).

• A potential for future regulations is further expansion of the deemed-compliant categories. Insurance is an area in which the government especially needs comments on expanding the

categories of deemed-compliant FFIs.

60

VIII. FUTURE WORK (4)

• Future guidance will allow online PFFI registration prior to 2013 procedures for permitting a PFFI to designate an entity that will be the “lead PFFI” for affiliated entities, the provision of PFFI identification numbers (FATCA Identifications), and amendments to qualified intermediary agreements to contain

FATCA representations. • In the future U.S. taxpayers in the Caribbean will be pressed

to respond to the increased compliance and enforcement measures of the U.S. income tax law.

• The U.S. government is likely to make requests for exchange of information and evidence gathering in some cases.

61