new fatca reporting and withholding and ongoing...

TRANSCRIPT

Presenting a live 110‐minute webinar with interactive Q&A

New FATCA Reporting and Withholding Requirements and Ongoing FBAR Requirements and Ongoing FBAR Compliance ChallengesNavigating Complex Requirements for Reporting Foreign Assets

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, JANUARY 24, 2012

Today s faculty features:

Daniel L. Gottfried, Partner, Rogin Nassau, Hartford, Conn.

Michael J. Miller, Partner, Roberts & Holland, New York

Attendees seeking CPE credit must listen to the audio over the telephone.

Pl f h i i il d i f di l i i f i A d Please refer to the instructions emailed to registrants for dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE credits, please let us know how many people are listening online by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

For CPE credits, attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online.

Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityFor this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problemwe can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

New FATCA Reporting and hh ld dWithholding Requirements and

Ongoing FBAR Compliance ChallengesOngoing FBAR Compliance Challenges

T d J 24 2012Tuesday, January 24, 2012Strafford Publications, Inc.

These materials are provided for educational and informational purposes only,d i d d d h ld b d l l d iand are not intended and should not be construed as legal advice.

5

IntroductionI. Foreign Account Tax Compliance Act (FATCA) overview

II. FATCA information reporting

Section 6038D- Section 6038D

- T.D. 9567

- Form 8938 and instructions

l d- Unresolved Issues

III. FATCA withholding

- Sections 1471-1474

- Withholding requirements

- Reporting requirement

- IRS Notices, effective dates

IV. Report of Foreign Bank and Financial Accounts (FBAR)

- Comparison with FATCA reporting

- Unresolved issues

6

FATCA OVERVIEW

Foreign Account Tax Compliance Act (FATCA)

March 18, 2010 – Hiring Incentives to Restore Employment Act (HIRE Act).Act (HIRE Act).

Enacted Foreign Account Tax Compliance Act (FATCA) as an element of the HIRE Act.

FATCA greatly increases disclosure requirements and penalties on taxpayers with foreign accounts and assets.

FATCA reporting is in addition to the FBAR requirements.p g q

FATCA also imposes new withholding regime.

New rules for U.S. payors

New burdens on foreign financial institutions (FFI) and non-financial foreign entities (NFFE).

8

FATCA INFORMATION REPORTING

In General

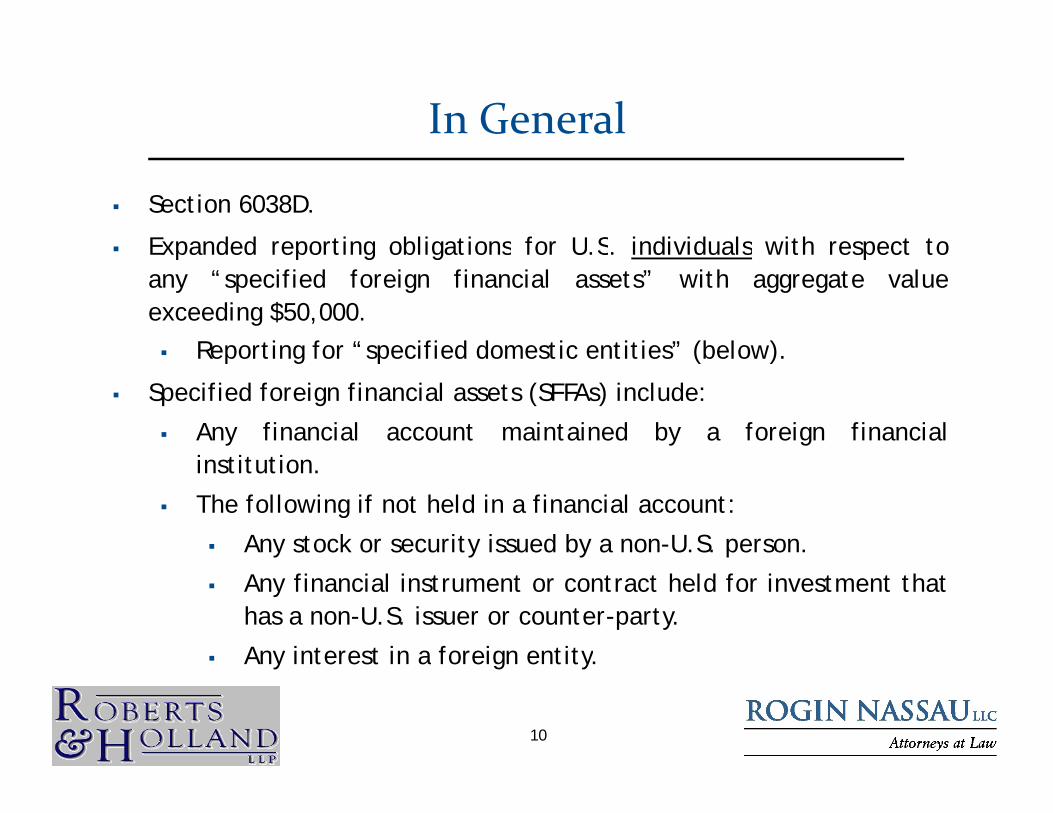

Section 6038D.

Expanded reporting obligations for U.S. individuals with respect toExpanded reporting obligations for U.S. individuals with respect toany “specified foreign financial assets” with aggregate valueexceeding $50,000.

Reporting for “specified domestic entities” (below).Reporting for specified domestic entities (below).

Specified foreign financial assets (SFFAs) include:

Any financial account maintained by a foreign financiali tit tiinstitution.

The following if not held in a financial account:

Any stock or security issued by a non-U.S. person.

Any financial instrument or contract held for investment thathas a non-U.S. issuer or counter-party.

Any interest in a foreign entity.Any interest in a foreign entity.

10

Specified Foreign Financial Assets

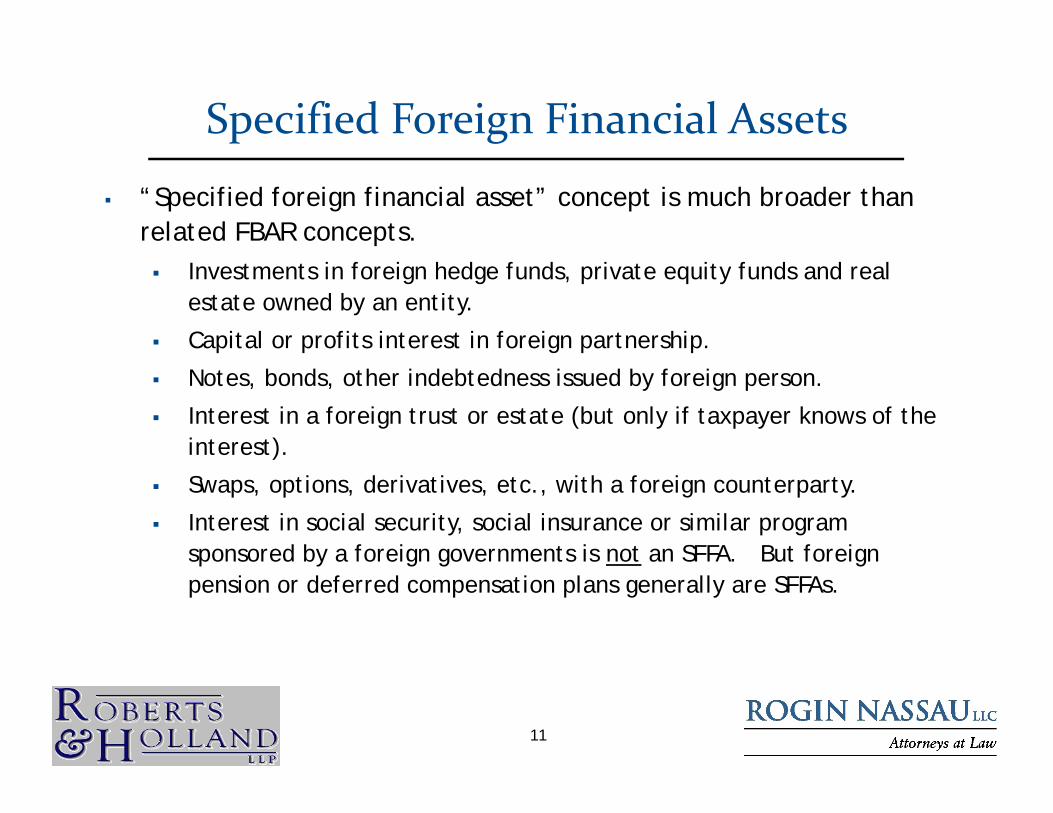

“Specified foreign financial asset” concept is much broader than related FBAR concepts. Investments in foreign hedge funds, private equity funds and real

estate owned by an entity.

Capital or profits interest in foreign partnership.

Notes, bonds, other indebtedness issued by foreign person.

Interest in a foreign trust or estate (but only if taxpayer knows of the interest).)

Swaps, options, derivatives, etc., with a foreign counterparty.

Interest in social security, social insurance or similar program sponsored by a foreign governments is not an SFFA. But foreign sponsored by a foreign governments is not an SFFA. But foreign pension or deferred compensation plans generally are SFFAs.

11

Source of Rules

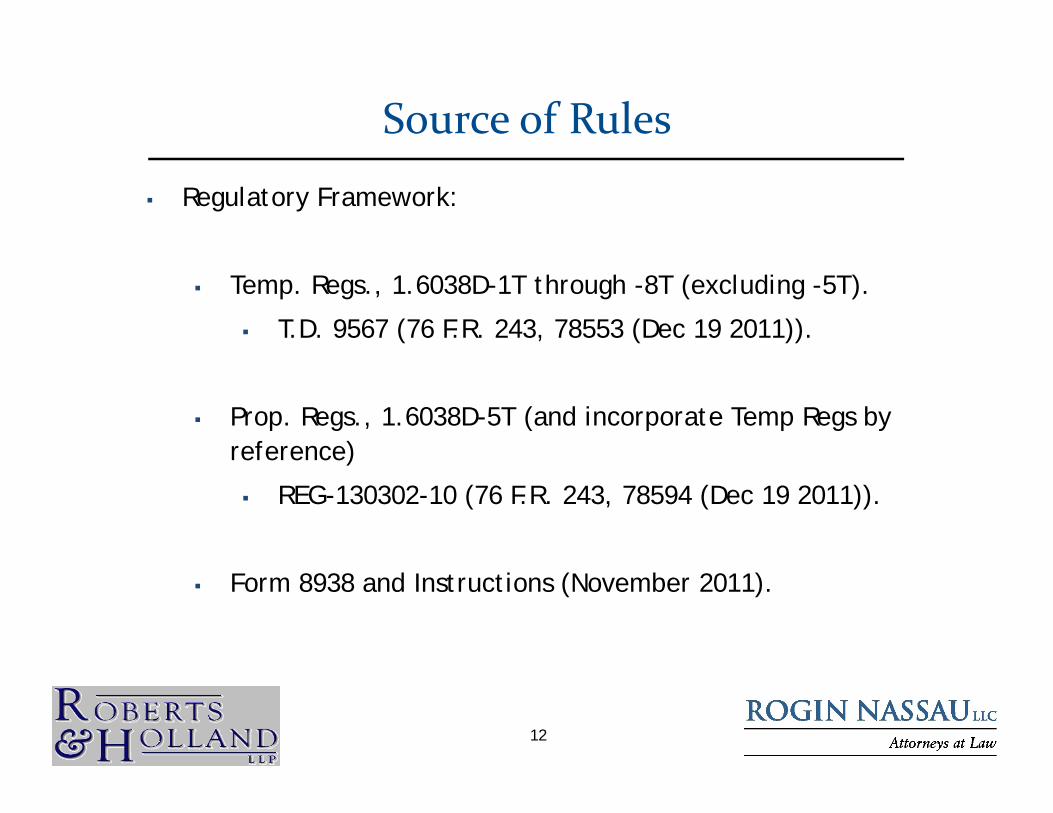

Regulatory Framework:

Temp. Regs., 1.6038D-1T through -8T (excluding -5T).

T.D. 9567 (76 F.R. 243, 78553 (Dec 19 2011)).

Prop. Regs., 1.6038D-5T (and incorporate Temp Regs by reference) reference)

REG-130302-10 (76 F.R. 243, 78594 (Dec 19 2011)).

Form 8938 and Instructions (November 2011).

12

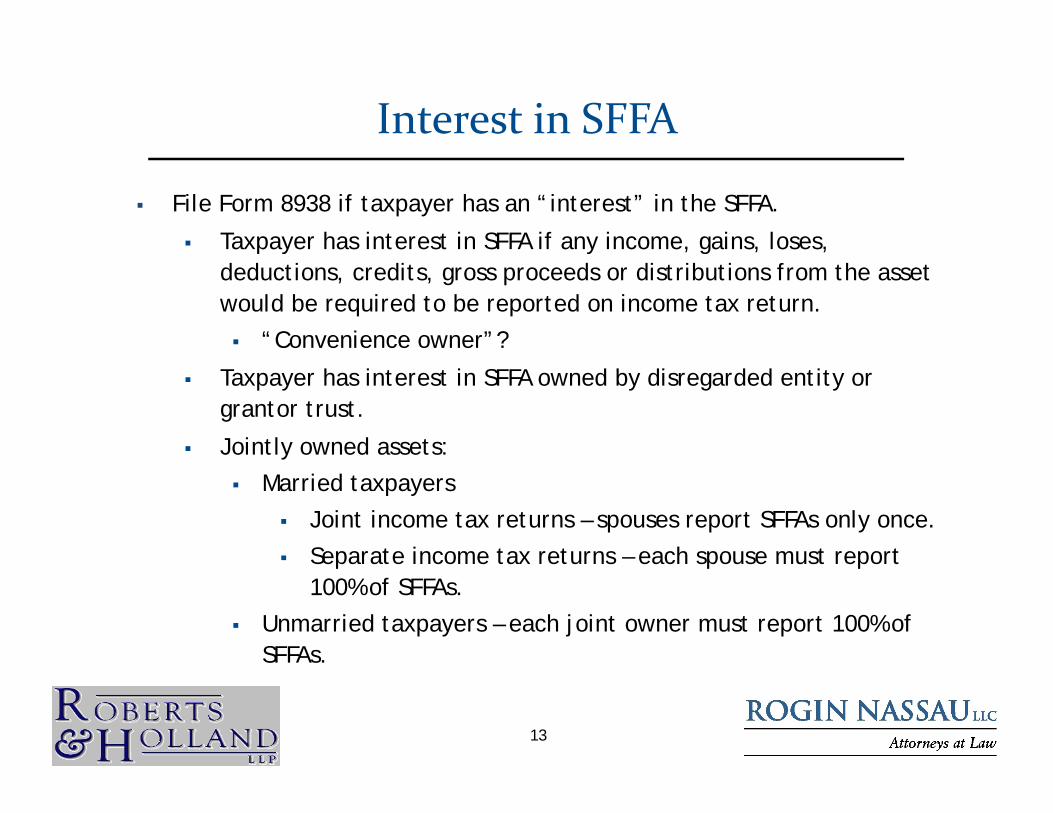

Interest in SFFA

File Form 8938 if taxpayer has an “interest” in the SFFA.

Taxpayer has interest in SFFA if any income, gains, loses, p y y , g , ,deductions, credits, gross proceeds or distributions from the asset would be required to be reported on income tax return.

“Convenience owner”?

Taxpayer has interest in SFFA owned by disregarded entity or grantor trust.

Jointly owned assets:y

Married taxpayers

Joint income tax returns – spouses report SFFAs only once.

Separate income tax returns – each spouse must report Separate income tax returns each spouse must report 100% of SFFAs.

Unmarried taxpayers – each joint owner must report 100% of SFFAs.

13

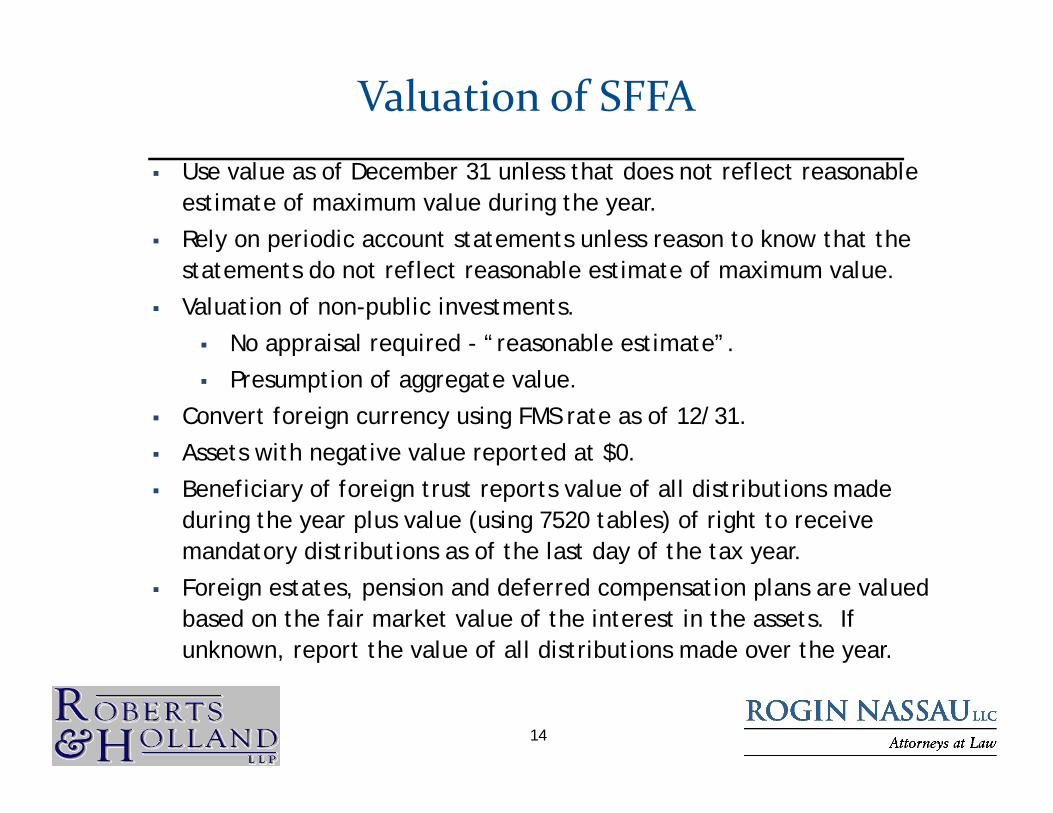

Valuation of SFFA Use value as of December 31 unless that does not reflect reasonable

estimate of maximum value during the year.

Rely on periodic account statements unless reason to know that the statements do not reflect reasonable estimate of maximum value.

Valuation of non-public investments.

No appraisal required - “reasonable estimate”.pp q

Presumption of aggregate value.

Convert foreign currency using FMS rate as of 12/31.

Assets with negative value reported at $0.Assets with negative value reported at $0.

Beneficiary of foreign trust reports value of all distributions made during the year plus value (using 7520 tables) of right to receive mandatory distributions as of the last day of the tax year.y y y

Foreign estates, pension and deferred compensation plans are valued based on the fair market value of the interest in the assets. If unknown, report the value of all distributions made over the year.

14

Reporting Thresholds

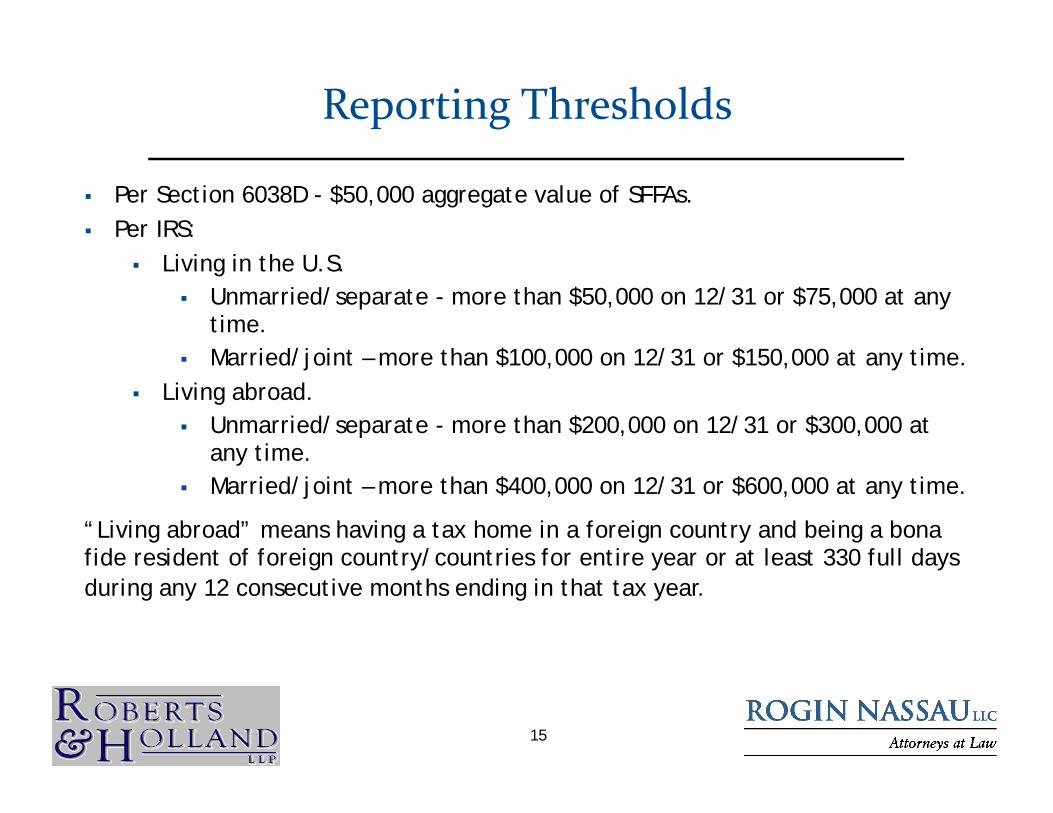

Per Section 6038D - $50,000 aggregate value of SFFAs. Per IRS:

Living in the U.S. Unmarried/separate - more than $50,000 on 12/31 or $75,000 at any

time.Married/joint more than $100 000 on 12/31 or $150 000 at any time Married/joint – more than $100,000 on 12/31 or $150,000 at any time.

Living abroad. Unmarried/separate - more than $200,000 on 12/31 or $300,000 at

any time.any time. Married/joint – more than $400,000 on 12/31 or $600,000 at any time.

“Living abroad” means having a tax home in a foreign country and being a bona fide resident of foreign country/countries for entire year or at least 330 full days fide resident of foreign country/countries for entire year or at least 330 full days during any 12 consecutive months ending in that tax year.

15

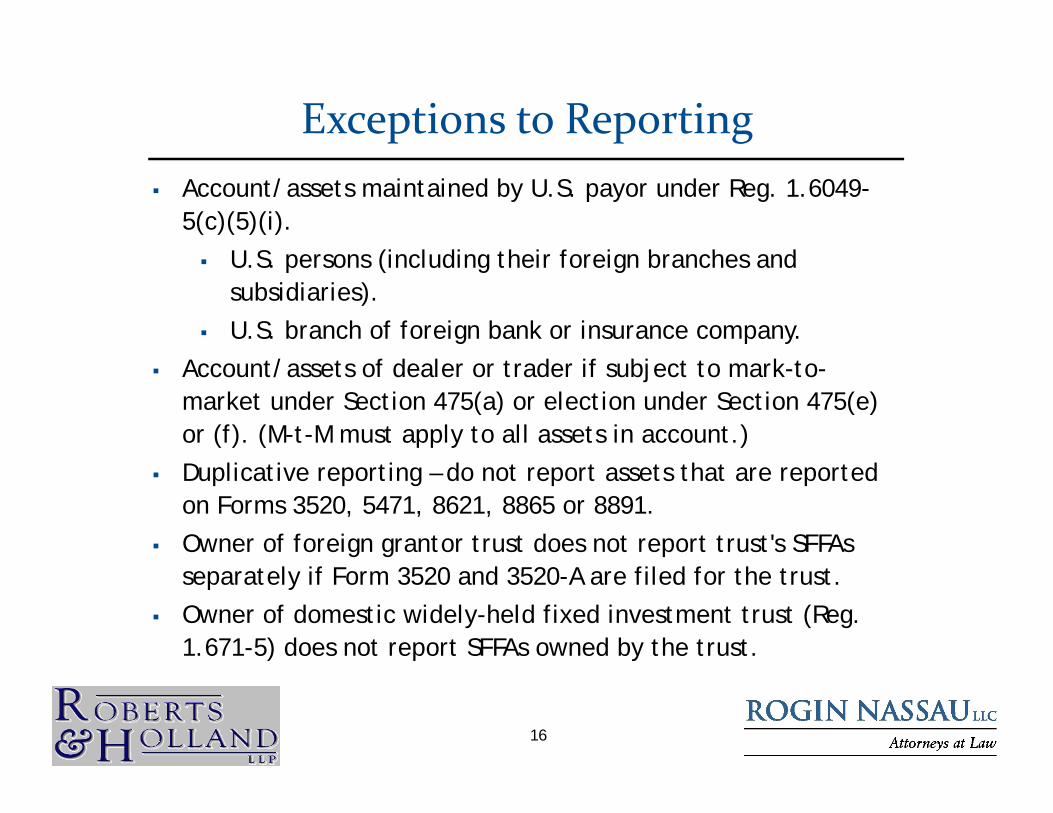

Exceptions to Reporting Account/assets maintained by U.S. payor under Reg. 1.6049-

5(c)(5)(i).

U S (i l di th i f i b h d U.S. persons (including their foreign branches and subsidiaries).

U.S. branch of foreign bank or insurance company.

Account/assets of dealer or trader if subject to mark-to-market under Section 475(a) or election under Section 475(e) or (f). (M-t-M must apply to all assets in account.)

Duplicative reporting – do not report assets that are reported on Forms 3520, 5471, 8621, 8865 or 8891.

Owner of foreign grantor trust does not report trust's SFFAs separately if Form 3520 and 3520-A are filed for the trust.

Owner of domestic widely-held fixed investment trust (Reg. 1.671-5) does not report SFFAs owned by the trust.

16

Exceptions to Reporting (cont’d)

Owner of domestic liquidating trust (Reg. 301-7701-4(d)) created under Bankruptcy Code (Chapt. 7 or 11) does not report created under Bankruptcy Code (Chapt. 7 or 11) does not report SFFAs owned by the trust.

Bona fide resident of U.S. possession (American Samoa, Guam, Northern Mariana Islands, Puerto Rico or U.S. Virgin Islands) Northern Mariana Islands, Puerto Rico or U.S. Virgin Islands) generally does not report SFFAs issued or maintained by organizations in that possession.

17

Information Provided on Form 8938

Basic identification of the account/asset.

Name/address of financial institution where account is held (if Name/address of financial institution where account is held (if applicable).

Name/address of issuer or counterparty of stock, securities or financial instruments (if applicable).financial instruments (if applicable).

Information regarding whether account/asset was acquired (opened) or disposed of (closed) during the year.

The amount of income gain or other tax attributes recognized The amount of income, gain or other tax attributes recognized during the year and schedule, form or return on which reported to IRS.

Currency exchange rate (and source of rate if not FMS)Currency exchange rate (and source of rate, if not FMS).

If SFFA reported on other form (3520, 5471, etc.) report type and number of such other forms.

18

Specified Domestic Entities (SDEs)

6038D(f): “To the extent provided by the Secretary in regulations or other guidance, the provisions of this section shall apply to any g , p pp y ydomestic entity which is formed or availed of for purposes of holding, directly or indirectly, specified foreign financial assets, in the same manner as if such entity were an individual.”

Temporary and proposed regulations issued on December 14, 2011 provide for reporting by SDEs commencing for taxable years beginning after December 31, 2011.

See Prop. Reg. 1.6038D-6 (Specified domestic entities).

SDE includes certain domestic corporations, partnerships or trusts.

Estates are not SDEs.

SDE qualification is tested annually.

19

SDEs; Corporations and Partnerships

Domestic corporations and partnerships:

Have interest in SFFAs with aggregate value in excess of $50,000.

Closely held by specified individual.

Individual owns at least 80% of stock (by vote or value) or capital or profits interest, as of the last day of SDE's taxable year.

Direct, indirect and constructive ownership rules apply.

One of the following two conditions is satisfied:

At least 50% of gross income is passive, or at least 50% of assets At least 50% of gross income is passive, or at least 50% of assets are held for the production of passive income; or

At least 10% of gross income is passive, or at least 10% of assets are held for the production of passive income, and the SDE was are held for the production of passive income, and the SDE was formed with the principal purpose of avoiding reporting under Section 6038D.

Valuation?

20

SDEs; Corporations and Partnerships (cont’d)

Passive income includes dividends, interest, rents, royalties, annuities, capital gains, income from investments contracts.

Rents and royalties not included to extent derived in active trade or business.

No similar exception for dividends/interest.

Capital gains included only when related to sale or exchange of passive assets.

Futures, forwards and similar contracts not included if “commodity , yhedging transactions” under Section 954(c)(5)(A) (generally relating to hedging risk of price or currency fluctuations with respect to business property).

21

SDEs; Corporations and Partnerships (cont’d 2)

Aggregation rules:

To determine whether the SDE meets the reporting threshold, all p g ,domestic corporations and partnerships owned by the same specified individual are treated as a single entity.

To determine whether the SDE meets the passive income or asset threshold, domestic corporations and partnerships that are closely held by the same individual and connected through ownership with a common parent entity are treated as a single entity.

Blessing and a curse.

Constructive ownership:

Apply Section 267(c) and (e)(3), except that Section 267(c)(4) is pp y ( ) ( )( ) p ( )( )expanded to include spouses of family members.

22

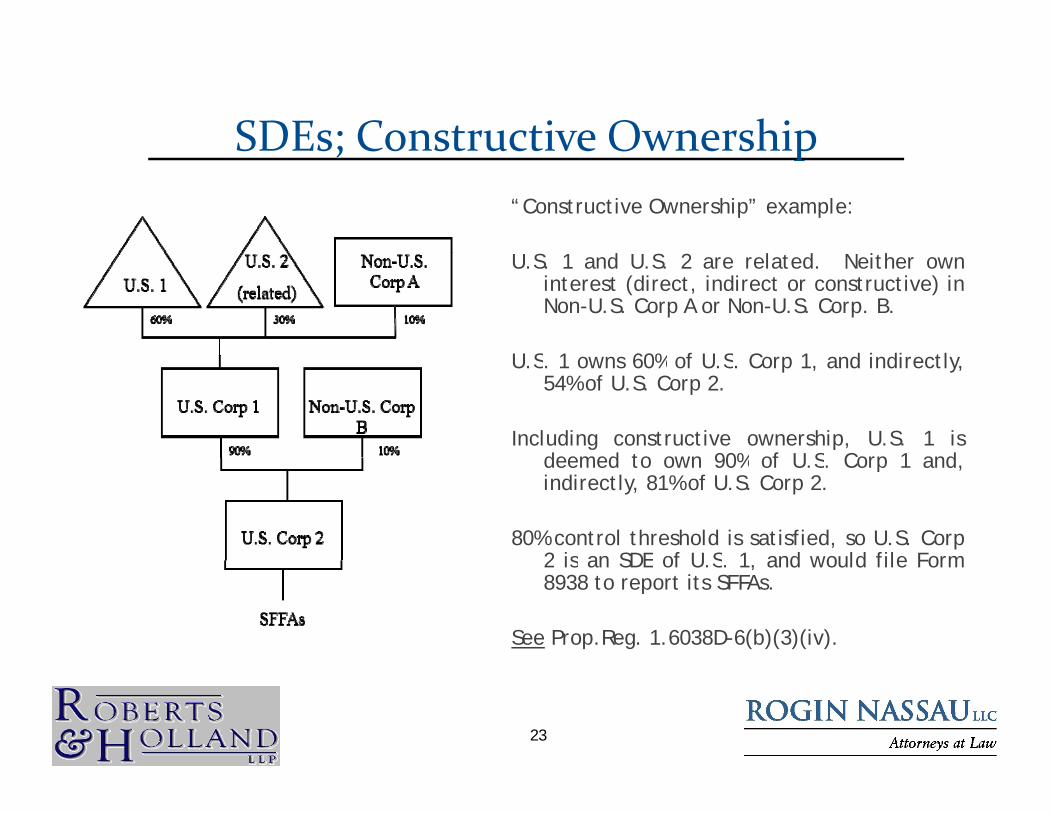

SDEs; Constructive OwnershipSDEs; Constructive Ownership“Constructive Ownership” example:

d l d hU.S. 1 and U.S. 2 are related. Neither owninterest (direct, indirect or constructive) inNon-U.S. Corp A or Non-U.S. Corp. B.

U S 1 60% f U S C 1 d i di tlU.S. 1 owns 60% of U.S. Corp 1, and indirectly,54% of U.S. Corp 2.

Including constructive ownership, U.S. 1 isdeemed to own 90% of U S Corp 1 anddeemed to own 90% of U.S. Corp 1 and,indirectly, 81% of U.S. Corp 2.

80% control threshold is satisfied, so U.S. Corp2 is an SDE of U S 1 and would file Form2 is an SDE of U.S. 1, and would file Form8938 to report its SFFAs.

See Prop.Reg. 1.6038D-6(b)(3)(iv).

23

SDEs; Domestic Trusts

Domestic trusts is an SDE if

Has interest in SFFAs with aggregate value in excess of $50,000.gg g ,

One or more specified persons is a “current beneficiary”.

Current beneficiary is any person who may (whether by entitlement or exercise of discretion) receive a distribution entitlement or exercise of discretion) receive a distribution from principal or income from the trust.

Without regard to powers of appointment that remain unexercised as of the end of the taxable year.y

24

SDEs; Exceptions Domestic entity is not SDE if it is described in Section 1473(3) as excepted from

definition of specified United States person:

Company traded on exchange or affiliate.p y g

Organization exempt under Section 501(a) or IRA.

U.S., state, subdivision, agency, etc.

Bank REIT RIC etc Bank, REIT, RIC, etc.

Common trust fund for bank's custodial/fiduciary funds under Section 584.

Although included under Section 1473(3), this exception does not apply to trust that is exempt from tax under Section 664(c) i e charitable trust that is exempt from tax under Section 664(c), i.e., charitable remainder annuity trust or a charitable remainder unitrust.

Domestic trust is not SDE if trustee is bank, financial institution or certain corporations subject to financial oversight, if the trustee timely files annual p j g yreturns and informational returns for the trust.

Grantor trust under Sections 671-679 is not an SDE.

The “grantor” may need to file Form 8938 directly, if applicable.

25

Form 8938; Penalties

Penalties for failure to file or failure to report an asset:

$10 000 minimum increased for noncompliance 90 $10,000 minimum, increased for noncompliance 90days after IRS notice up to $50,000 maximum. No stacking – See Temp. Reg. 1.6038D-8T(a).

Penalties joint and several for joint filers.

Reasonable cause exception may apply, but you must“affirmatively show the facts that support a reasonableaffirmatively show the facts that support a reasonablecause claim.”

Section 6662 penalties increased from 20% up to 40%for underpayments involving undisclosed SFFAs. Section6662(j).

26

Form 8938; Statute of Limitations

Statute of limitations remains open until 3 years after all information is receivedall information is received.

Six year statute of limitations if matter involves omission of gross income more than $5 000 related to omission of gross income more than $5,000 related to foreign financial asset.

Does not require substantial understatement.Does not require substantial understatement.

New statute of limitations applies to open years as of March 18, 2010.,

27

FATCA WITHHOLDING

CURRENT WITHHOLDING REGIME

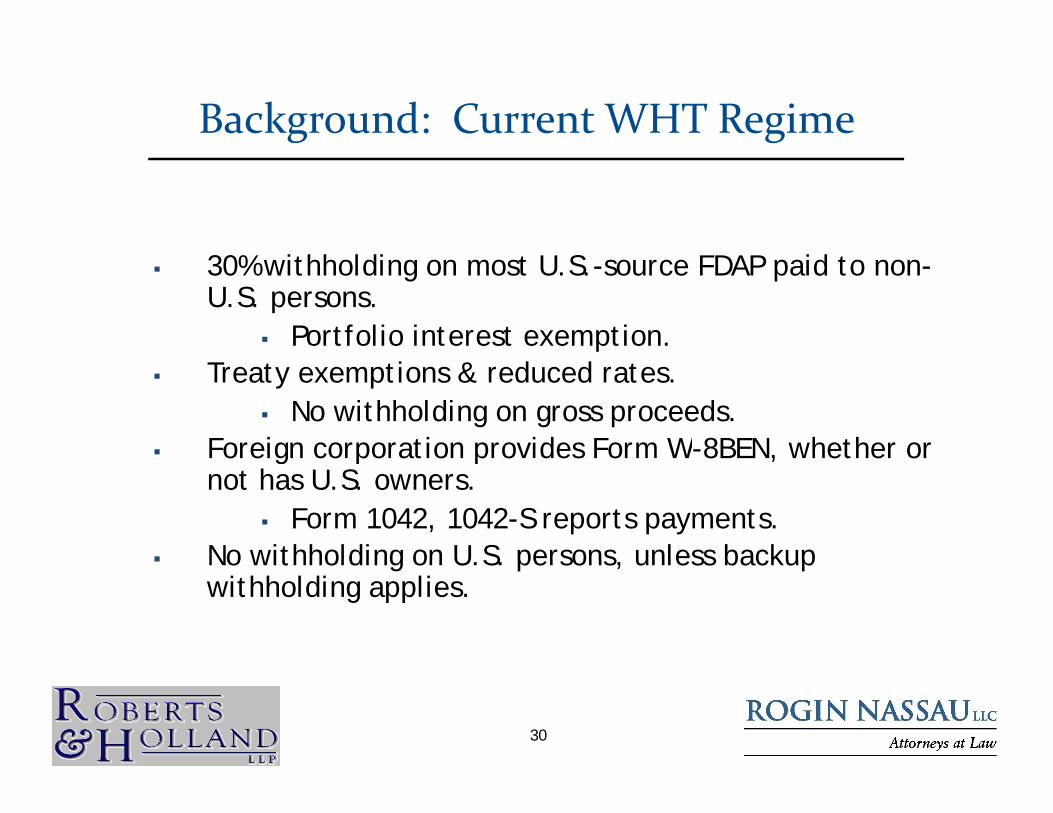

Background: Current WHT Regime

30% withholding on most U.S.-source FDAP paid to non-U.S. persons.

Portfolio interest exemption. Treaty exemptions & reduced rates.

No withholding on gross proceeds. Foreign corporation provides Form W-8BEN, whether or Foreign corporation provides Form W 8BEN, whether or

not has U.S. owners. Form 1042, 1042-S reports payments.

No withholding on U S persons unless backup No withholding on U.S. persons, unless backup withholding applies.

30

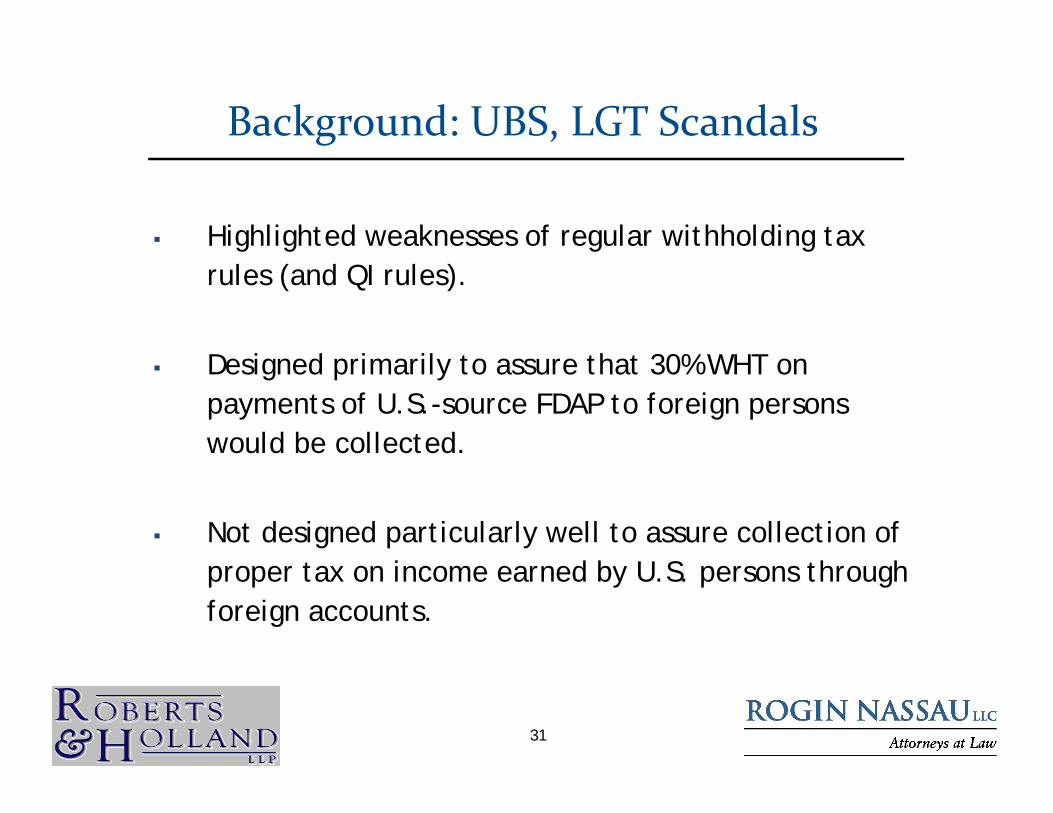

Background: UBS, LGT Scandals

Highlighted weaknesses of regular withholding tax rules (and QI rules).

D i d i il t th t 30% WHT Designed primarily to assure that 30% WHT on payments of U.S.-source FDAP to foreign persons would be collected.

Not designed particularly well to assure collection of i d b S h h proper tax on income earned by U.S. persons through

foreign accounts.

31

NEW FATCA WITHHOLDING REGIME

Overview of New FATCA Regime

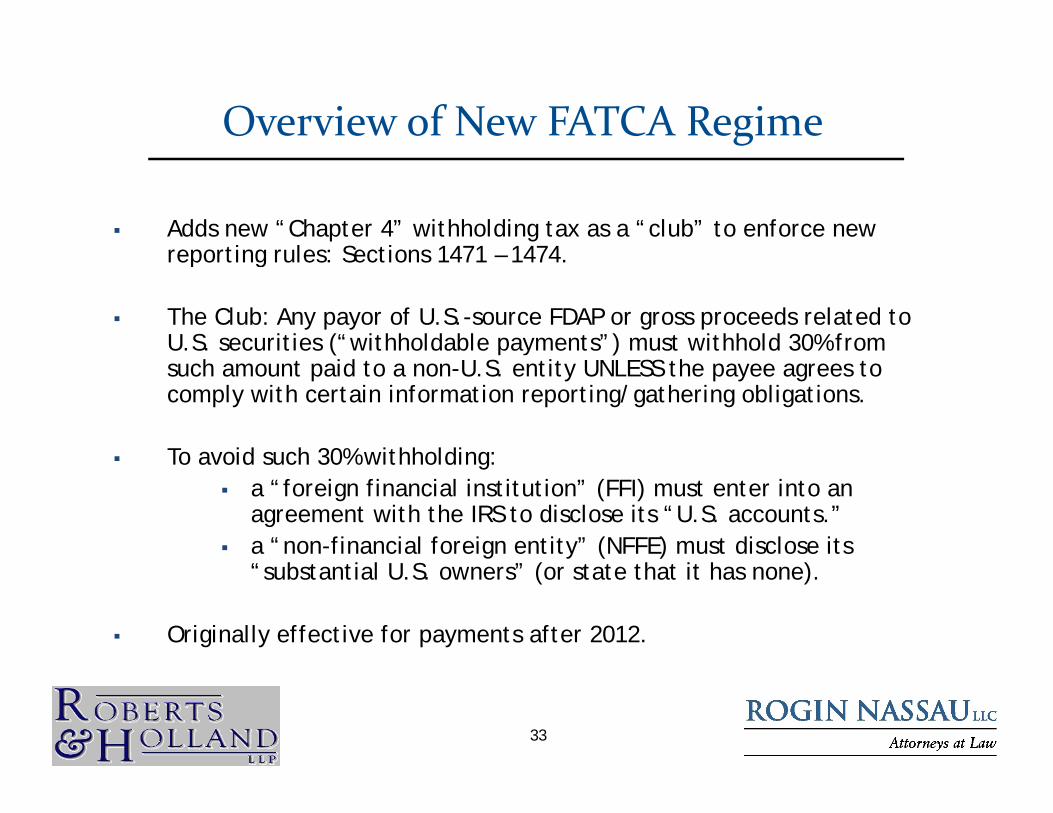

Adds new “Chapter 4” withholding tax as a “club” to enforce new reporting rules: Sections 1471 1474reporting rules: Sections 1471 – 1474.

The Club: Any payor of U.S.-source FDAP or gross proceeds related to U.S. securities (“withholdable payments”) must withhold 30% from ( )such amount paid to a non-U.S. entity UNLESS the payee agrees to comply with certain information reporting/gathering obligations.

To avoid such 30% withholding: To avoid such 30% withholding: a “foreign financial institution” (FFI) must enter into an

agreement with the IRS to disclose its “U.S. accounts.” a “non-financial foreign entity” (NFFE) must disclose its

“substantial U.S. owners” (or state that it has none).

Originally effective for payments after 2012.

33

FFI Obligations Under Agreement with IRS

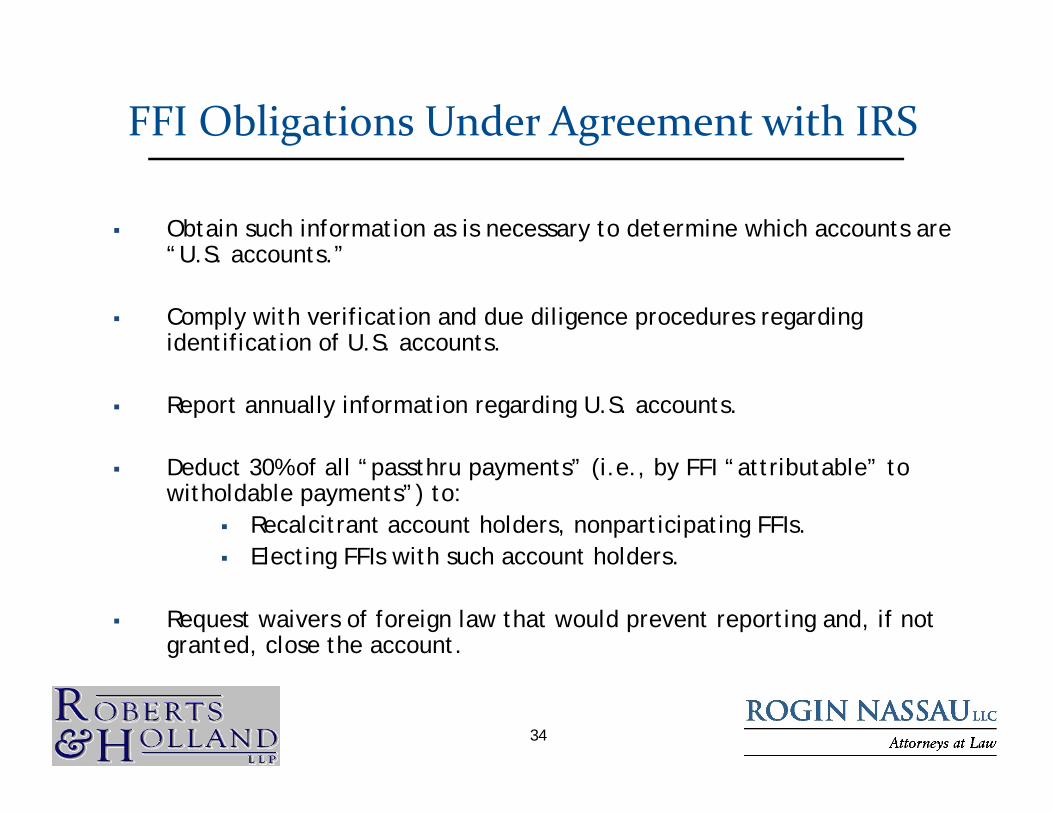

Obtain such information as is necessary to determine which accounts are “U S accounts ”U.S. accounts.

Comply with verification and due diligence procedures regarding identification of U.S. accounts.

Report annually information regarding U.S. accounts.

D d 30% f ll “ h ” (i b “ ib bl ” Deduct 30% of all “passthru payments” (i.e., by FFI “attributable” to witholdable payments”) to:

Recalcitrant account holders, nonparticipating FFIs. Electing FFIs with such account holders Electing FFIs with such account holders.

Request waivers of foreign law that would prevent reporting and, if not granted, close the account.

34

Broad Definition of FFI

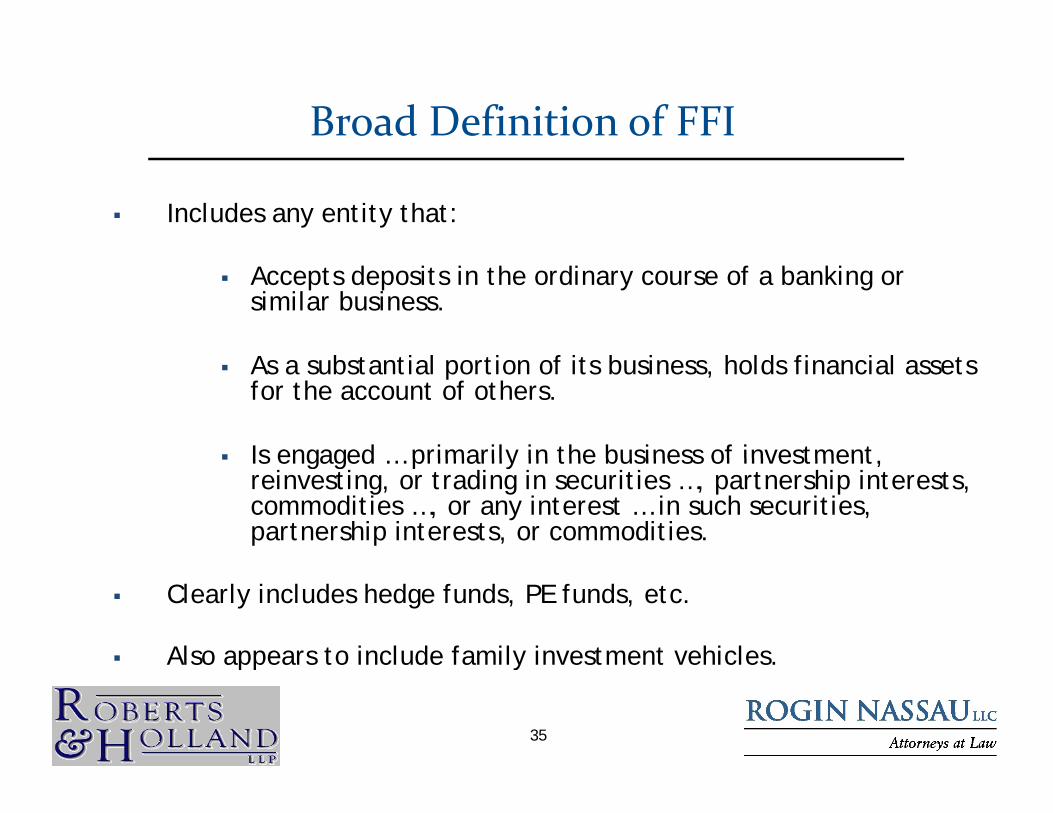

Includes any entity that:

Accepts deposits in the ordinary course of a banking or similar business.

A b i l i f i b i h ld fi i l As a substantial portion of its business, holds financial assets for the account of others.

Is engaged primarily in the business of investment Is engaged … primarily in the business of investment, reinvesting, or trading in securities …, partnership interests, commodities …, or any interest … in such securities, partnership interests, or commodities.

Clearly includes hedge funds, PE funds, etc.

Also appears to include family investment vehicles.Also appears to include family investment vehicles.

35

Definition of U.S. Account

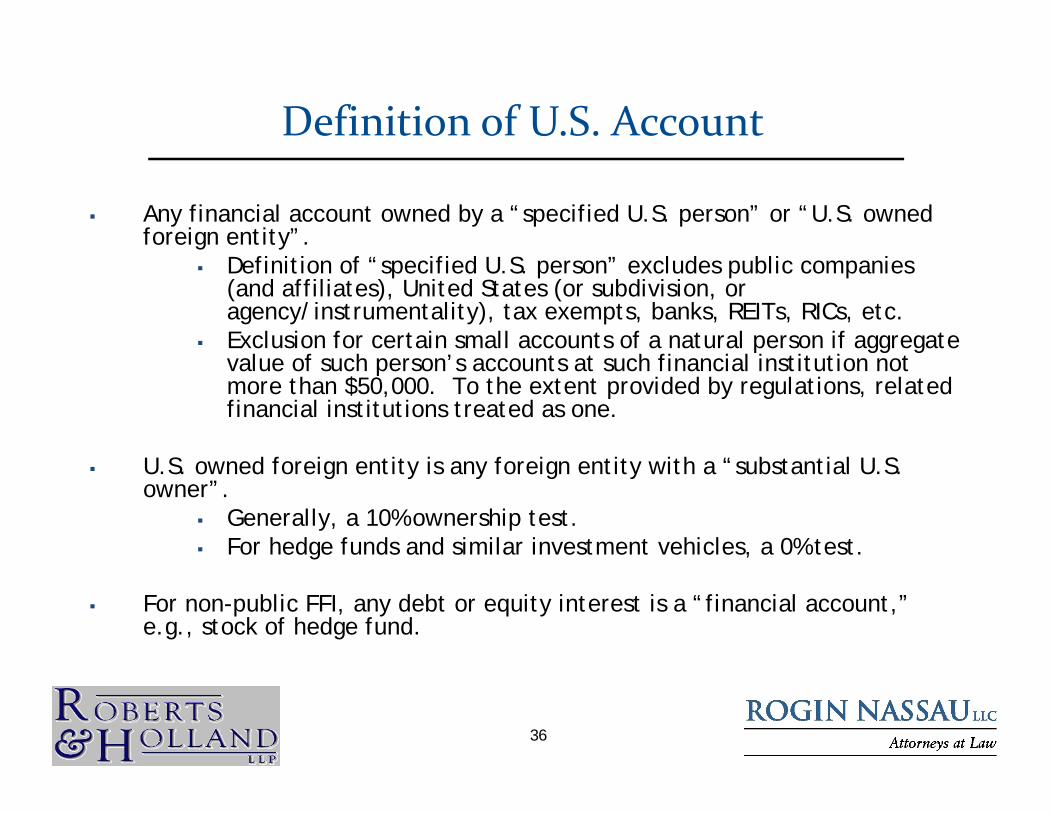

Any financial account owned by a “specified U.S. person” or “U.S. owned foreign entity”.

Definition of “specified U.S. person” excludes public companies (and affiliates), United States (or subdivision, or agency/instrumentality), tax exempts, banks, REITs, RICs, etc.

Exclusion for certain small accounts of a natural person if aggregate l f h ’ t t h fi i l i tit ti t value of such person’s accounts at such financial institution not

more than $50,000. To the extent provided by regulations, related financial institutions treated as one.

U S d f i i i f i i i h “ b i l U S U.S. owned foreign entity is any foreign entity with a “substantial U.S. owner”.

Generally, a 10% ownership test. For hedge funds and similar investment vehicles, a 0% test.

For non-public FFI, any debt or equity interest is a “financial account,” e.g., stock of hedge fund.

36

Identification of U.S. Accounts

FFI must prove negative proposition – that account holder is not a specified U.S. person or U.S. owned foreign entity.

Existing FFIs with many accounts have lots of records to comb through, and those records may not g , yeven have the necessary information.

C / A d i il d KYC / AML documentation not necessarily adequate.

37

Credits & Refunds

Determination of overpayment generally made as if FATCA tax had been withheld under chapter 3FATCA tax had been withheld under chapter 3.

Thus, generally refundable.

No credit or refund however for “specified financial No credit or refund, however, for specified financial institution payment,” i.e., any payment if a FFI is the beneficial owner.

Except to extent exemption or reduced rate p pavailable under a treaty, provided that FFI identifies its substantial U.S. owners.

Increased reporting requirement may violate t ttreaty.

Thus, if hedge fund an FFI, shareholders may be ineligible.

38

Notice 2010‐60, 2010‐37 IRB 329 Grandfathered obligations. Definition of FFI / NFFE.

E g confirms that family trust generally an FFI E.g., confirms that family trust generally an FFI. FFI exclusions, special rules for:

Holding, startup companies not FFI.Certain insurance companies not FFI Certain insurance companies not FFI.

Certain “small” FFIs deemed compliant. Certain retirement plans deemed compliant.

narrow: e g no U S participants permitted narrow: e.g., no U.S. participants permitted. Identification of accounts by FFIs & USFIs.

Pre-existing vs. new.Individual vs entity Individual vs. entity.

Reporting by FFI on U.S. accounts. Reporting by FFIs re: recalcitrant account holders.

Number and aggregate value of such accounts Number and aggregate value of such accounts.

39

Notice 2011‐34, 2011‐19 IRB 765

Revised procedures for FFIs to Identify pre-existing U.S. accounts.

Look for accounts documented as U.S.Look for accounts documented as U.S. Disregard other accounts of $50,000 or less. Higher standard of diligence for private banking & accounts of $500,000 or more.

Definition of passthru payment.

See next slide. Deemed-compliant FFIs.

Certain funds if all holders participating and deemed-compliant FFIs. ETFs and other funds where all interests publicly-traded ETFs and other funds where all interests publicly traded. Certain retirement plans.

Reporting on U.S. accounts by FFIs.

Rules for qualified intermediaries and affiliated groups.

Long-term recalcitrant account holders.

Withholding. Other measures possible, depending on number, aggregate value of such accounts.

40

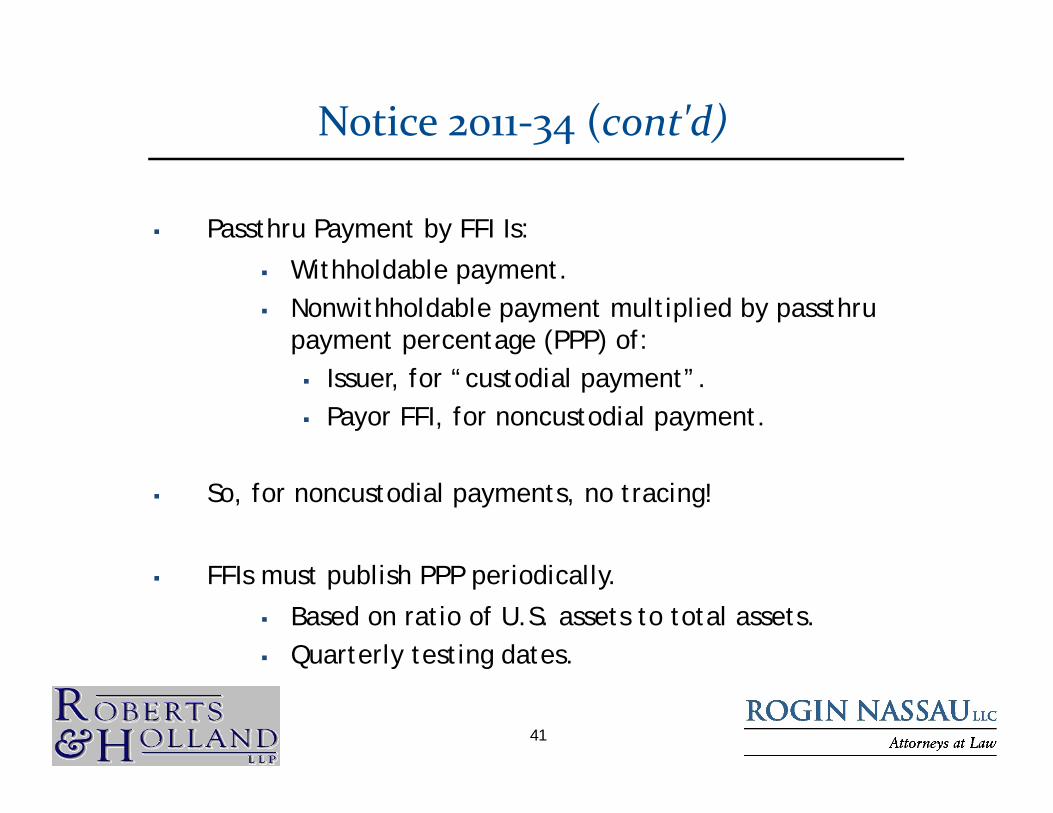

Notice 2011‐34 (cont'd)

Passthru Payment by FFI Is:

Withholdable payment. Nonwithholdable payment multiplied by passthru

payment percentage (PPP) of: Issuer, for “custodial payment”. Payor FFI, for noncustodial payment.

So, for noncustodial payments, no tracing!

FFIs must publish PPP periodically.

Based on ratio of U.S. assets to total assets. Quarterly testing dates.Quarterly testing dates.

41

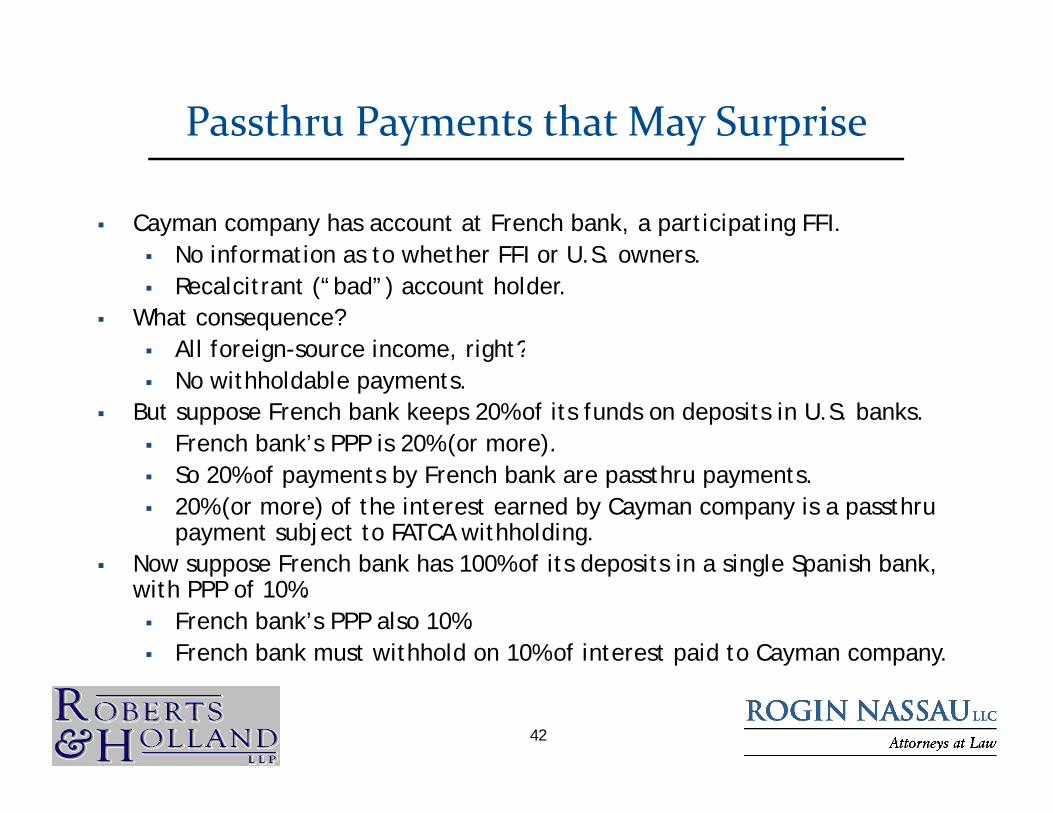

Passthru Payments that May Surprise

Cayman company has account at French bank, a participating FFI.No information as to whether FFI or U S owners No information as to whether FFI or U.S. owners.

Recalcitrant (“bad”) account holder. What consequence?

All foreign-source income, right?All foreign source income, right? No withholdable payments.

But suppose French bank keeps 20% of its funds on deposits in U.S. banks. French bank’s PPP is 20% (or more). So 20% of payments by French bank are passthru payments. 20% (or more) of the interest earned by Cayman company is a passthru

payment subject to FATCA withholding.Now suppose French bank has 100% of its deposits in a single Spanish bank Now suppose French bank has 100% of its deposits in a single Spanish bank, with PPP of 10%. French bank’s PPP also 10%. French bank must withhold on 10% of interest paid to Cayman company.p y p y

42

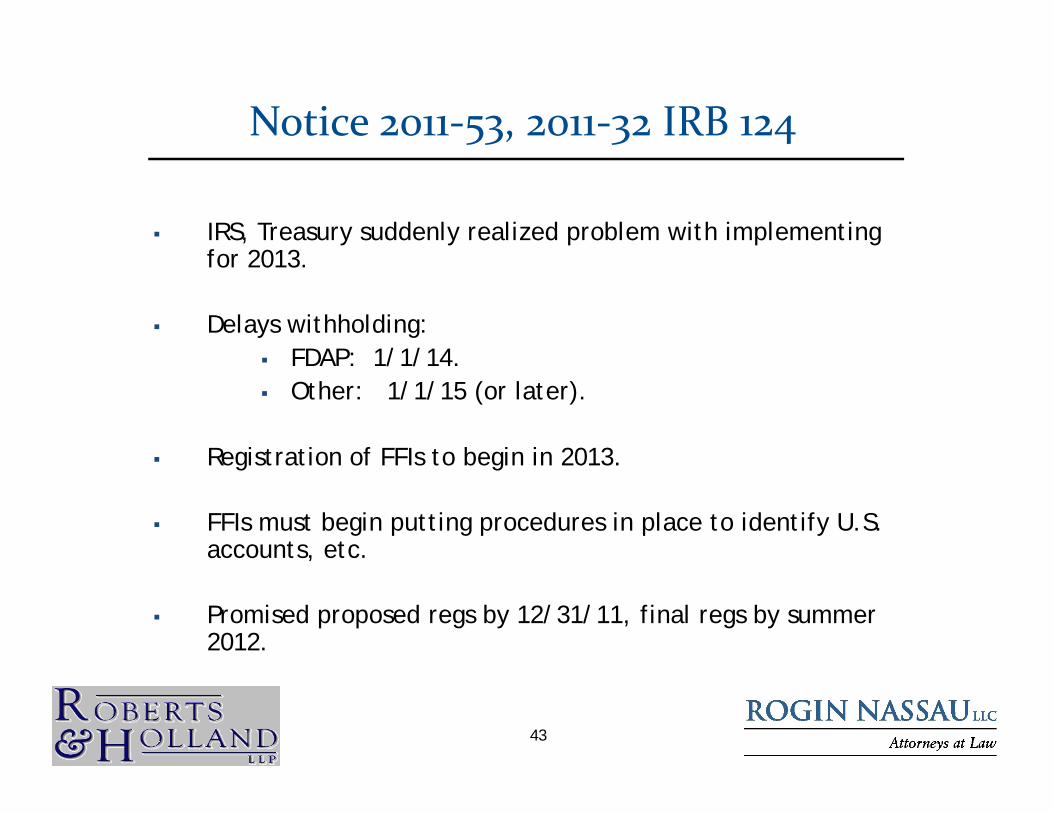

Notice 2011‐53, 2011‐32 IRB 124

IRS, Treasury suddenly realized problem with implementing f 2013for 2013.

Delays withholding:FDAP: 1/1/14 FDAP: 1/1/14.

Other: 1/1/15 (or later).

Registration of FFIs to begin in 2013 Registration of FFIs to begin in 2013.

FFIs must begin putting procedures in place to identify U.S. accounts, etc.,

Promised proposed regs by 12/31/11, final regs by summer 2012.

43

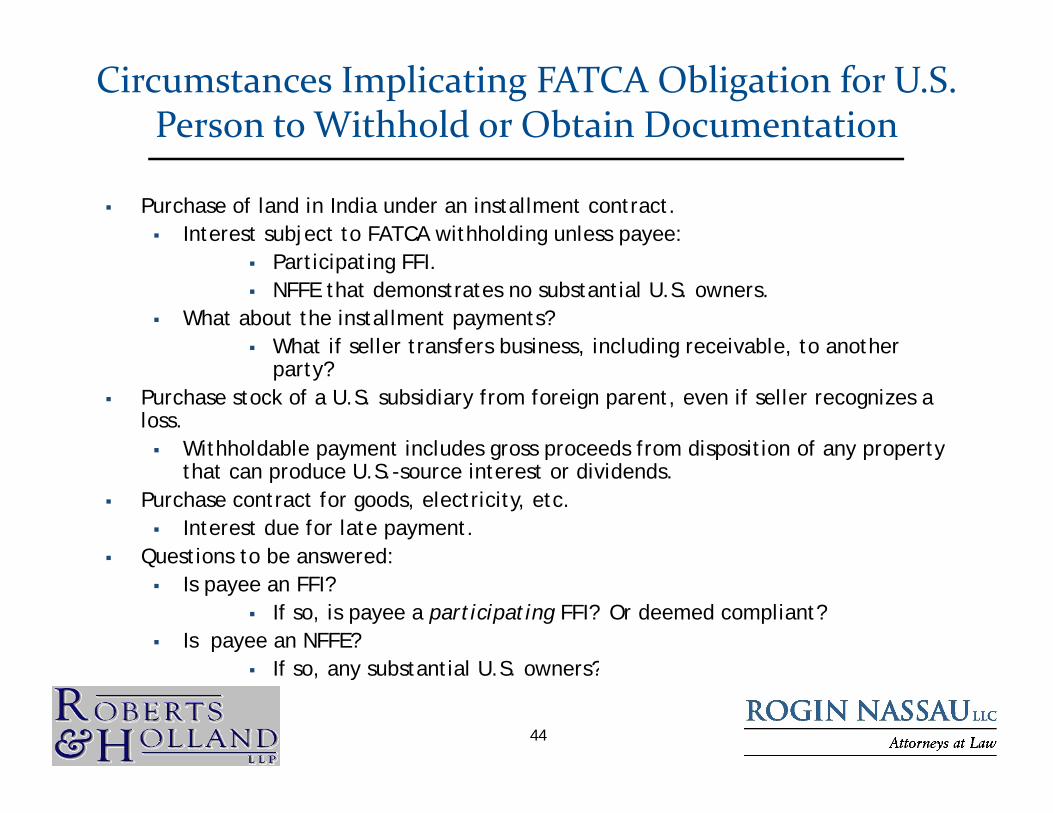

Circumstances Implicating FATCA Obligation for U.S. Person to Withhold or Obtain Documentation

Purchase of land in India under an installment contract. Interest subject to FATCA withholding unless payee:

Participating FFI. NFFE that demonstrates no substantial U.S. owners.

What about the installment payments? What if seller transfers business, including receivable, to another , g ,

party? Purchase stock of a U.S. subsidiary from foreign parent, even if seller recognizes a

loss. Withholdable payment includes gross proceeds from disposition of any property p y g p p y p p y

that can produce U.S.-source interest or dividends. Purchase contract for goods, electricity, etc.

Interest due for late payment. Questions to be answered:Questions to be answered:

Is payee an FFI? If so, is payee a participating FFI? Or deemed compliant?

Is payee an NFFE?If b t ti l U S ? If so, any substantial U.S. owners?

44

FBAR ISSUES

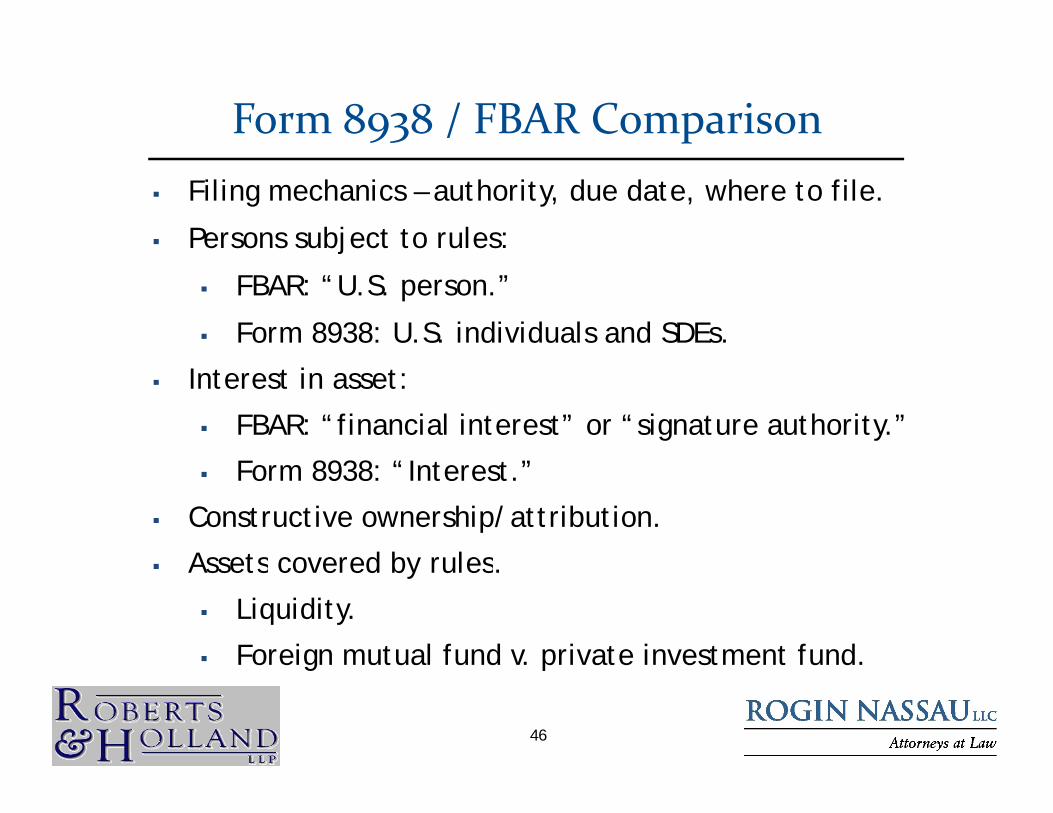

Form 8938 / FBAR Comparison Filing mechanics – authority, due date, where to file.

Persons subject to rules:j

FBAR: “U.S. person.”

Form 8938: U.S. individuals and SDEs.

Interest in asset:

FBAR: “financial interest” or “signature authority.”

Form 8938: “Interest.”

Constructive ownership/attribution.

Assets covered by rules Assets covered by rules.

Liquidity.

Foreign mutual fund v. private investment fund.Foreign mutual fund v. private investment fund.

46

Form 8938 / FBAR Comparison (cont’d)

Penalties – scope and stacking.

Statute of limitations Statute of limitations.

47

Q tiQuestions

Daniel L. Gottfried, Esq. Michael J. Miller, Esq.Rogin Nassau LLC

185 Asylum Street, 22nd FloorHartford, CT 06103

Roberts & Holland LLC825 Eighth Avenue, 37th Floor

New York, NY 10019t. (860) 256-6335f. (860) 278-2179

t. (212) 903-8757f. (212) 974-3059

These materials are provided for educational and informational purposes only,and are not intended and should not be construed as legal advice.g

48