february 2015 oil & gas update - great american...

TRANSCRIPT

1 February 2015 — Oil & Gas Update

1

In this issue Trending News 1

Introduction to GA 1

Commodity Prices 2

Rig Count 2

Texas Drilling Activity 3

Drilling Rig Day Rates 4

Drilling Rig Utilization 5

Well Service Rigs 6

Drilling Activity Trends 7

Natural Gas Storage 7

FEBRUARY 2015

Oil & Gas Update

1 February 2015 — Oil & Gas Update

1 Trending News

GA has built a quality team to deliver

both tangible and intangible valuations

across the O&G platform.

Recently appraised assets include:

Compression Equipment

Drilling & Well Service Equipment

Frac Tank Rental/Manufacturing

Well Logging Tools

Pipeline Equipment

Pressure Pumping Units

Rental Tools

Transportation Assets

Wire Line Services

Saltwater Disposal Wells

Valves

Tubular Goods

Robert Callaway

Head of Oil & Gas

Great American Group

(972) 589‐3308

Drew Jakubek

Managing Director

Great American Group

(214) 455‐7081

Contact Us

Introduction to GA

U.S. Shale Oil’s Crash Diet Likely to Bring Forward Output Dip

Rig Count Reaches Five‐year Low; Forecast Projects More Losses

Shale Producers Postpone Well Completions

EIA’s February Short‐Term Energy Outlook

IEA’s Oil Market Report

GA is a leading provider of appraisal services to the Oil and Gas (“O&G”)

sector. When a reliable valuation is required, our industry experts are

there to assist private equity groups, investment and commercial banks,

finance companies, as well as oilfield service companies across the U.S.

and Canada.

2 February 2015 — Oil & Gas Update

2 Commodity Prices

Drilling activity continues to slow. For

the week of February 20, 2015, drilling

rigs turning totaled 1,310, which

represented a decrease of 48 units from

the prior week, and is down

approximately 600 rigs from 2014 highs.

Land‐based rigs decreased by 48 to

1,250 rigs, while the Inland Waters was

down two rigs and the Offshore rig

count gained two rigs.

Week‐over‐week, Oil rigs were down

by 37 to 1,019 rigs, while the Gas rig

count was down by 11. The number of

Directional rigs increased five units to

128 rigs, Horizontal rigs were down by

46 to 979, and Vertical drilling rigs

decreased by seven to 203.

Rigs in the Permian Basin were down

by six to 362, and the Eagle Ford Shale

decreased by four to 160 rigs. The

Williston Basin was down five to 123,

and the Marcellus Shale count was flat

at 69 rigs.

Rig Count

3 February 2015 — Oil & Gas Update

3 Texas Drilling Activity

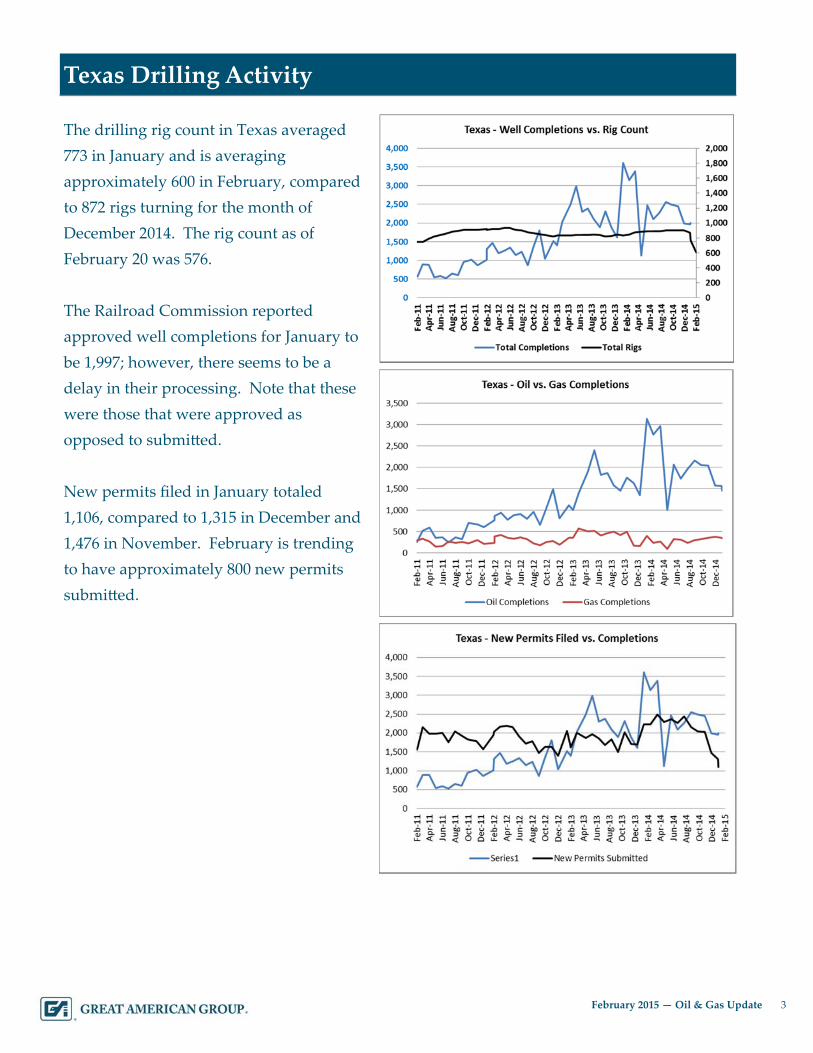

The drilling rig count in Texas averaged

773 in January and is averaging

approximately 600 in February, compared

to 872 rigs turning for the month of

December 2014. The rig count as of

February 20 was 576.

The Railroad Commission reported

approved well completions for January to

be 1,997; however, there seems to be a

delay in their processing. Note that these

were those that were approved as

opposed to submitted.

New permits filed in January totaled

1,106, compared to 1,315 in December and

1,476 in November. February is trending

to have approximately 800 new permits

submitted.

4 February 2015 — Oil & Gas Update

4 Drilling Rig Day Rates and Utilization

While there is an approximate six‐week lag from when the data is reported, the day rate

pricing is showing a drop in the major rig classes for January. Month‐over‐month, Class C and

D rigs dropped by about 0.25% in December of 2014 and then another 1.0% to 1.25% in January

of this year.

5 February 2015 — Oil & Gas Update

5 Drilling Rig Utilization

Utilization rate data as provided by RigData shows significant drops, especially in Class C

(1000‐1499 hp) and Class E (2000+ hp). These have dropped from around 85% to near 65% to

70%. Likewise, Class D (1500‐1999 hp) rigs have gone from 90% to 95% to around 82% in

January. Class B (500‐999 hp) has suffered even more and dropped from 60% to 65% to near

40% utilization.

This data is changing very rapidly and is challenging to gather real time. Based on recent

trends seen first hand in the Permian Basin, GA expects to see these rates drop even further in

the short‐term.

Source: RigData

6 February 2015 — Oil & Gas Update

6 Well Service Rigs

Well service rig counts through January 2015 are shown above by region. The service rig

count in the Permian Basin was down 50 to 625 on a month‐over‐month basis. This represents

a drop of roughly 100 rigs or 15% from the peak in January 2014. A good portion of the

reduction is said to come from rigs associated with completion work. The rig count associated

with maintaining producing wells or doing workover operations is reported to be more

resilient. The Rockies were down 10 rigs to 336, a drop of 37 from its peak. The Midcontinent

was down two rigs to 201. The Texas Gulf Coast ended the month at 196, down by 16 rigs.

The ArkLaTex region ended at 132, down seven units, and the Eastern U.S. was down five to

74.

7 February 2015 — Oil & Gas Update

7 Drilling Activity Trends

According to RigData’s survey dated

February 16, there is more negative news

about cuts in day rates. While some

contract drillers feel there may be a

bottoming out in day rates, most feel any

recovery is many months away.

Most drillers are expecting declines in rates

ranging from 10% to 30%, though a few feel

it could be more along the lines of 20% to

40%. Nearly two‐thirds expect work

volumes to decline further, but nearly a

third felt the industry was at bottom now.

Those surveyed report that operating costs

have decreased due to lower trucking rates

and fuel costs.

Margins are still reported to be tightening as

day rates are dropping more rapidly than

operating costs. Wages are being cut in a

range of 2% to 20%, but those reductions

have not yet caught up to the drop in day

rates.

Working gas in storage was 2,157 Bcf as of

February 13, 2015, according to EIA

estimates. This represents a net decline of

111 Bcf from the previous week. Stocks

were 678 Bcf higher than

last year at this time and 58

Bcf above the five‐year

average of 2,099 Bcf. In the

East Region, stocks were

28 Bcf below the five‐year

average following net

withdrawals of 97 Bcf.

Stocks in the Producing

Region were 26 Bcf above

the five‐year average of

772 Bcf after a net

withdrawal of 18 Bcf.

Stocks in the West Region were 60 Bcf above

the five‐year average after a net addition of

four Bcf. At 2,157 Bcf, total working gas is

within the five‐year historical range.

Natural Gas Storage