final ppt green shoe

TRANSCRIPT

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 1/17

By

Pegasus(Team No. 2)

Underwriting IPO of Seyad Shariyat Finance

:Team Members

:PiyushSamaria .piyushsmr2@gmail com

:Rishab Bucha .rishab1203@gmail com

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 2/17

In d e x

Brief about Islamic bank

About the firm

Price band and details about issue

Market scenario

Valuation

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 3/17

About Islamic Bank

through the development of Islamic economics. Sharia prohibits the payment or acceptance of interest fees for loa

About Present State Scenario in India

Present StateAbout Scenario in India

*

Scenario in IndiaPresent State

.

About

•No full time Islamic bank available.•RBI has send out report saying Islamic bank model is not suitable•Kerala High court has asked CPM govt to be away from the model of Islamic bank

l

amic banking was undertaken in Egypt under cover without projecting an Islamic image in 1963. ject became part of Nasr Social Bank which, currently, is still in business in Egypt and is the largest Islamic bank incountries

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 4/17

Seyad Shariat Finance Limited

Background Businesses Features

BusinessesBackground Features

FeaturesBusinesses

q

qSeyad Shariat Finance Ltd. is a non-banking financial company, approved by the Reserve Bank of

India as a Leasing company and registered under the Indian Companies Act, 1956.qFirst corporate finance institution functioning in Tamil Nadu as per Islamic Economic System.qRating recently upgraded from MB+ to MA- by ICRA.q

qOne of the entity of Syed shariat Limited, Others being Seyadu Beedi,Seyad Cotton Mills etc.qSyed shariat currently works in Leasing, Hire purchase & Venture Financing, Housing and other loans

for Rural Area.

Background

qClose customer interaction and relationship.qSpecialized Branch network.qFlexibility in shifting product and liability mix.qPopular model of Islamic banking

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 5/17

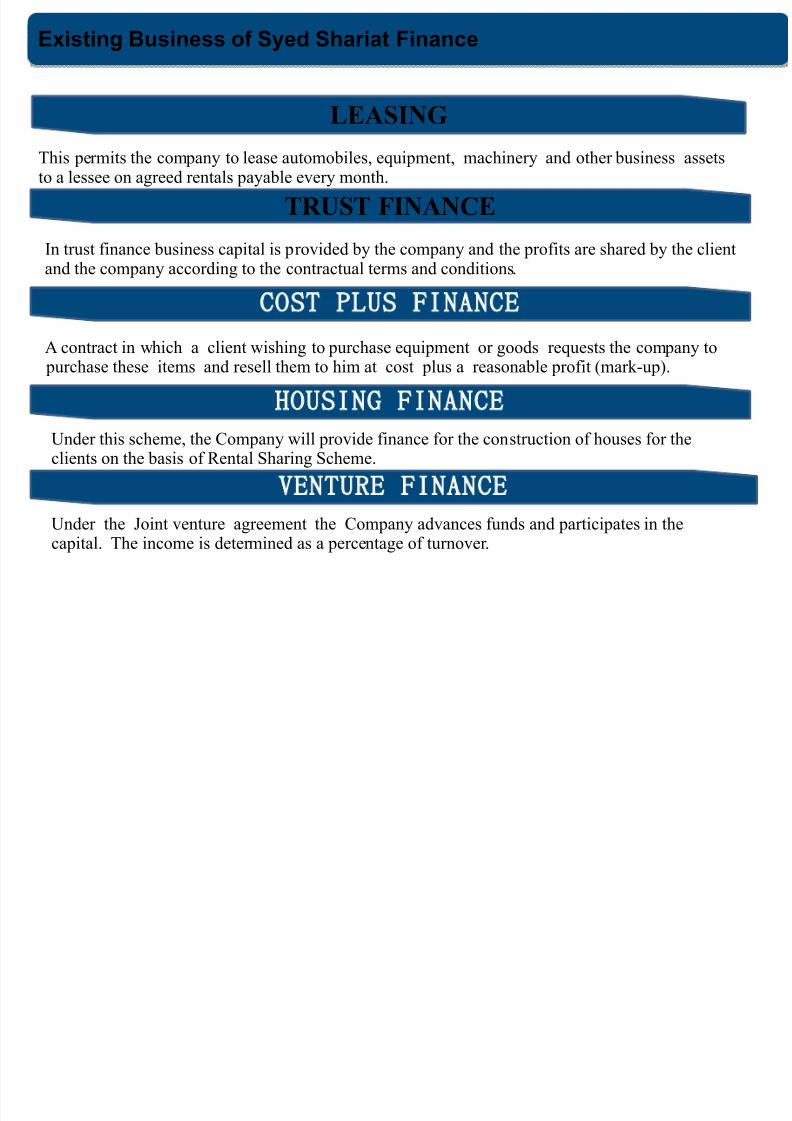

Existing Business of Syed Shariat Finance

LEASING

This permits the company to lease automobiles, equipment, machinery and other business assetsto a lessee on agreed rentals payable every month.

In trust finance business capital is provided by the company and the profits are shared by the client

and the company according to the contractual terms and conditions.

TRUST FINANCE

OST PLUS FINANCEA contract in which a client wishing to purchase equipment or goods requests the company to purchase these items and resell them to him at cost plus a reasonable profit (mark-up).

OUSING FINANCE

Under this scheme, the Company will provide finance for the construction of houses for theclients on the basis of Rental Sharing Scheme.

ENTURE FINANCEUnder the Joint venture agreement the Company advances funds and participates in the

capital. The income is determined as a percentage of turnover.

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 6/17

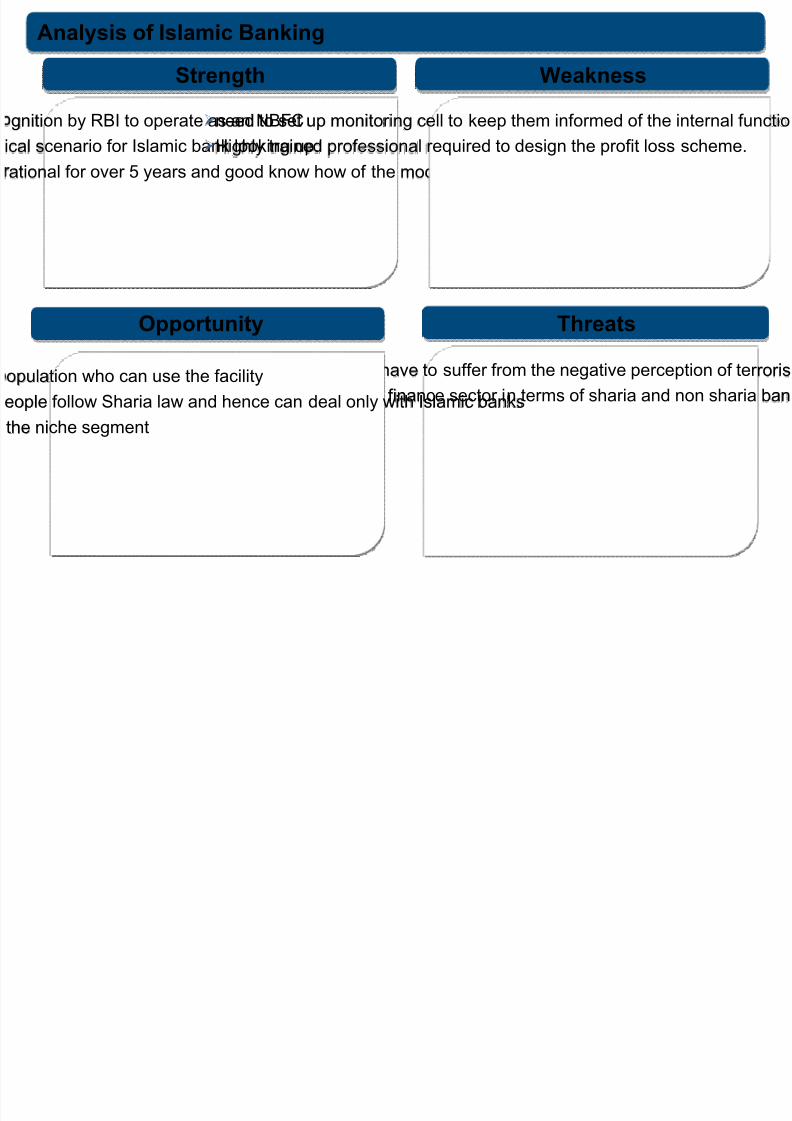

Ø“Islamic” bank may have to suffer from the negative perception of terroris

ØCommunalization of finance sector in terms of sharia and non sharia ban

Opportunity

opul

ation who can use the facility

eople follow Sharia law and hence can deal only with Islamic banks

the niche segment

Threats

Analysis of Islamic Banking

gnition by RBI to operate as an NBFC

ical scenario for Islamic bank looking up.

ational for over 5 years and good know how of the model

Strength

Øneed to set up monitoring cell to keep them informed of the internal functio

ØHighly trained professional required to design the profit loss scheme.

Weakness

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 7/17

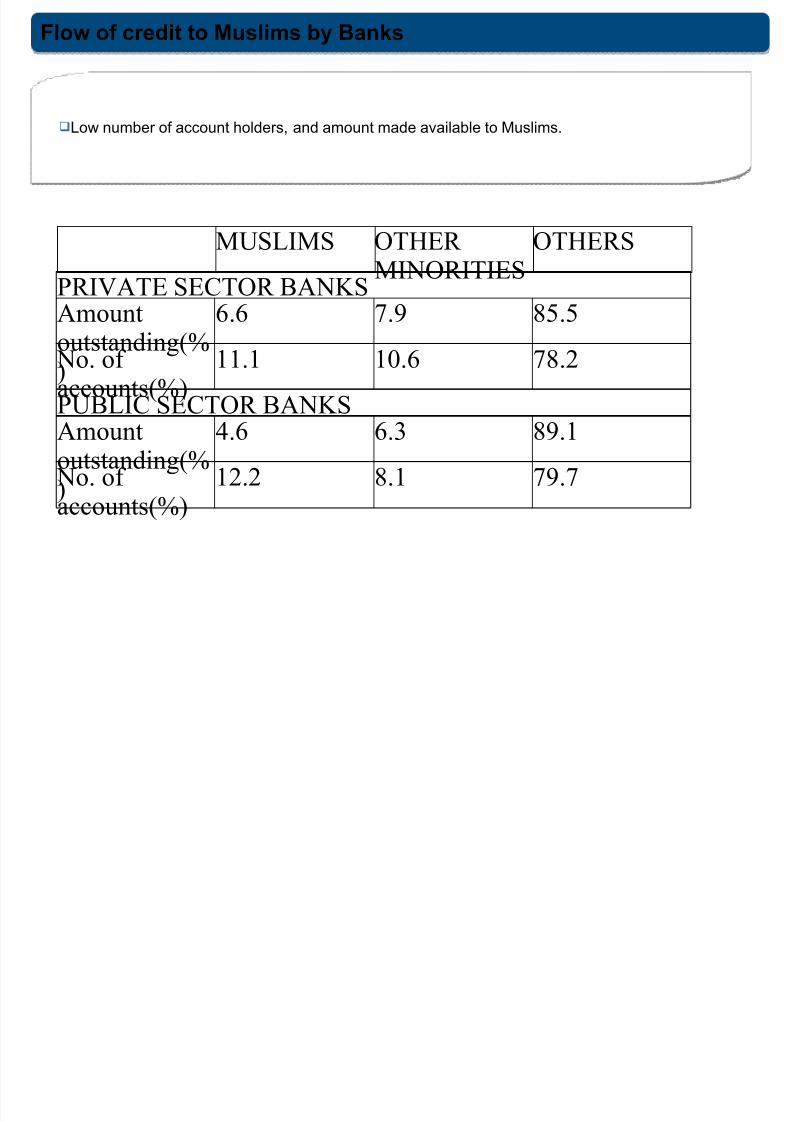

Flow of credit to Muslims by Banks

qLow number of account holders, and amount made available to Muslims.

MUSLIMS OTHER

MINORITIES

OTHERS

PRIVATE SECTOR BANKSAmountoutstanding(%)

6.6 7.9 85.5

No. of accounts(%)

11.1 10.6 78.2

PUBLIC SECTOR BANKSAmountoutstanding(%)

4.6 6.3 89.1

No. of accounts(%)

12.2 8.1 79.7

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 8/17

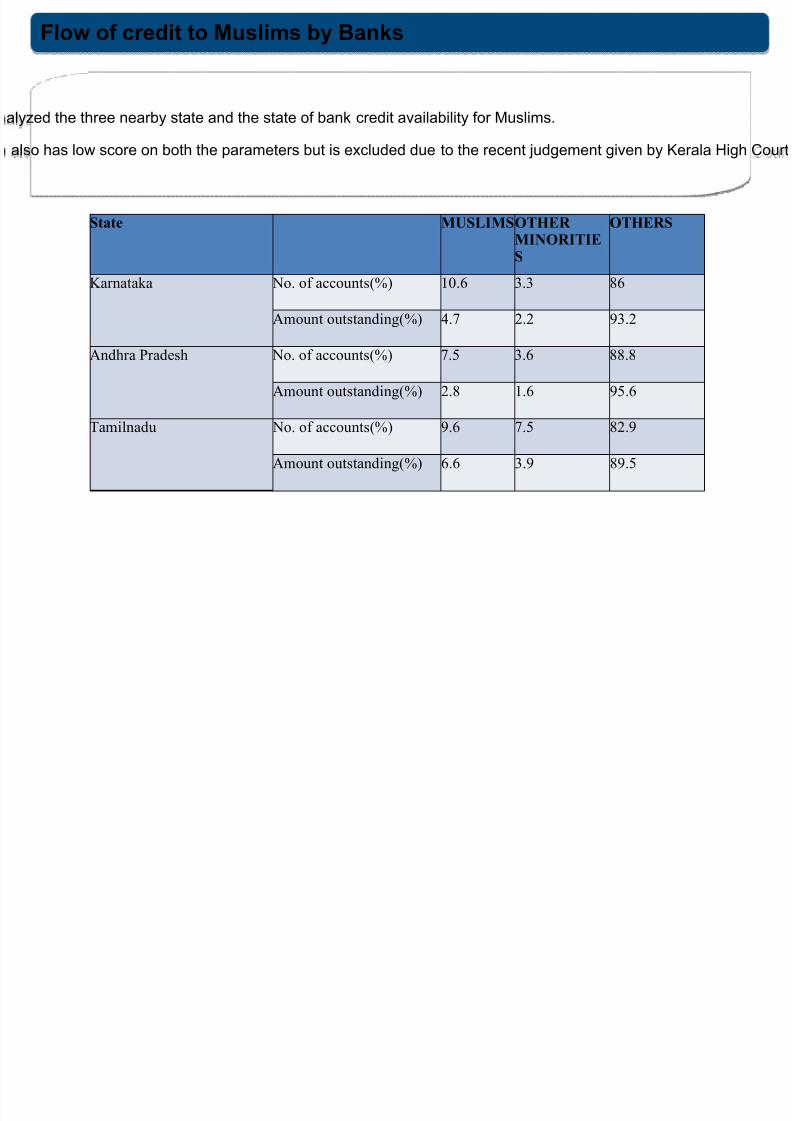

Flow of credit to Muslims by Banks

alyzed the three nearby state and the state of bank credit availability for Muslims.

also has low score on both the parameters but is excluded due to the recent judgement given by Kerala High Court

State MUSLIMS OTHER

MINORITIE

S

OTHERS

Karnataka No. of accounts(%) 10.6 3.3 86

Amount outstanding(%) 4.7 2.2 93.2

Andhra Pradesh No. of accounts(%) 7.5 3.6 88.8

Amount outstanding(%) 2.8 1.6 95.6

Tamilnadu No. of accounts(%) 9.6 7.5 82.9

Amount outstanding(%) 6.6 3.9 89.5

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 9/17

sh flow to firm as the model for estimation of the value of firm.f IPO is to allow the firm to open additional branches and raise additional capital for operations

m:-

t target for number of branches to be opened is assumed.alyze branch wise profitability and then bring the change in the balance sheet and income statement and final cashumption of stable growth after year 6

Analysis of profit made per branch

he number of employee figure is taken from the K. Ahamed Hussain,ranch Manager,Tirunvelli.

Interest expense from the profit given out in last 3 years (8.2, 7, 9.5)

rofit estimated per branch come out to be 36,46,000 for an year with added asset base for 5.2 crore per branch

& L of Branch

Valuation of the Firm

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 10/17

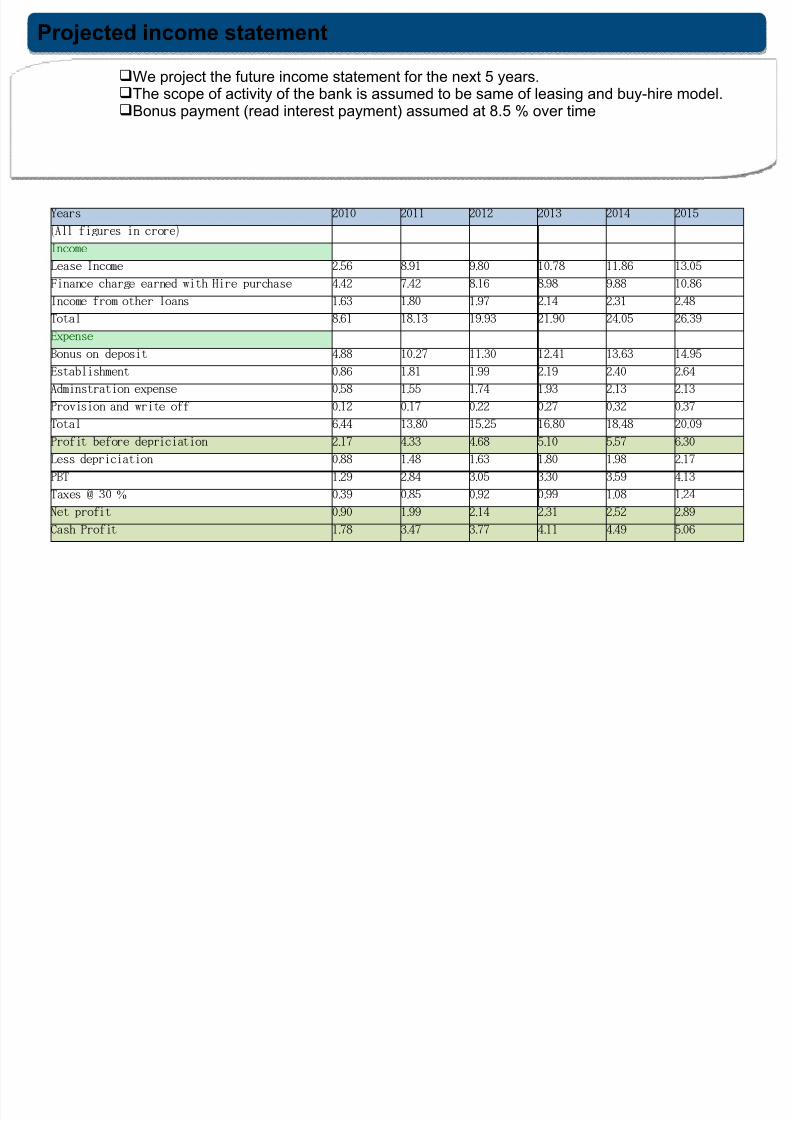

qWe project the future income statement for the next 5 years.qThe scope of activity of the bank is assumed to be same of leasing and buy-hire model.qBonus payment (read interest payment) assumed at 8.5 % over time

Projected income statement

Years 2010 2011 2012 2013 2014 2015

( )All figures in crore

Income

Lease Income .2 56 .8 91 .9 80 .10 78 .11 86 .13 05

Finance charge earned with Hire purchase .4 42 .7 42 .8 16 .8 98 .9 88 .10 86

Income from other loans .1 63 .1 80 .1 97 .2 14 .2 31 .2 48

Total .8 61 .18 13 .19 93 .21 90 .24 05 .26 39

Expense

Bonus on deposit .4 88 .10 27 .11 30 .12 41 .13 63 .14 95

Establishment .0 86 .1 81 .1 99 .2 19 .2 40 .2 64

Adminstration expense .0 58 .1 55 .1 74 .1 93 .2 13 .2 13

Provision and write off .0 12 .0 17 .0 22 .0 27 .0 32 .0 37

Total .6 44 .13 80 .15 25 .16 80 .18 48 .20 09

Profit before depriciation .2 17 .4 33 .4 68 .5 10 .5 57 .6 30

Less depriciation .0 88 .1 48 .1 63 .1 80 .1 98 .2 17

PBT .1 29 .2 84 .3 05 .3 30 .3 59 .4 13

%Taxes @ 30 .0 39 .0 85 .0 92 .0 99 .1 08 .1 24

Net profit .0 90 .1 99 .2 14 .2 31 .2 52 .2 89

Cash Profit .1 78 .3 47 .3 77 .4 11 .4 49 .5 06

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 11/17

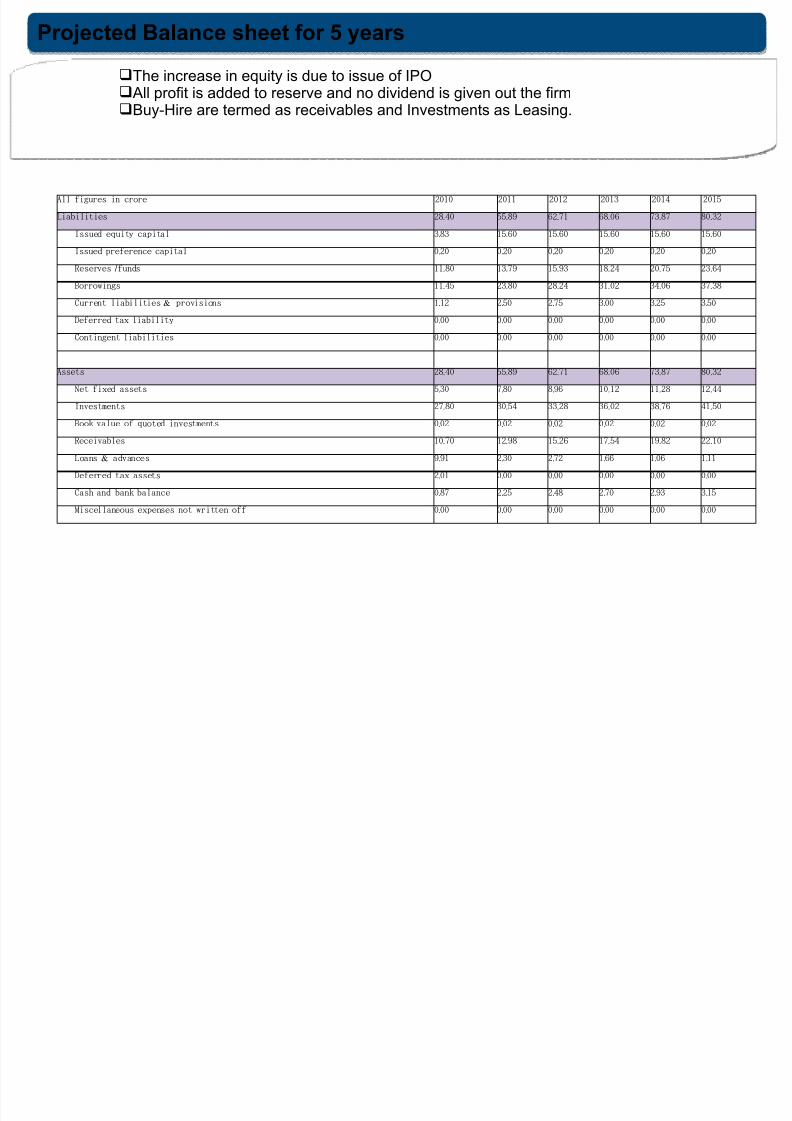

qThe increase in equity is due to issue of IPOqAll profit is added to reserve and no dividend is given out the firmqBuy-Hire are termed as receivables and Investments as Leasing.

Projected Balance sheet for 5 years

All figures in crore 2010 2011 2012 2013 2014 2015

Liabilities .28 40 .55 89 .62 71 .68 06 .73 87 .80 32

Issued equity capital .3 83 .15 60 .15 60 .15 60 .15 60 .15 60

Issued preference capital .0 20 .0 20 .0 20 .0 20 .0 20 .0 20

/Reserves funds .11 80 .13 79 .15 93 .18 24 .20 75 .23 64

Borrowings .11 45 .23 80 .28 24 .31 02 .34 06 .37 38

&Current liabilities provisions .1 12 .2 50 .2 75 .3 00 .3 25 .3 50

Deferred tax liability .0 00 .0 00 .0 00 .0 00 .0 00 .0 00

Contingent liabilities .0 00 .0 00 .0 00 .0 00 .0 00 .0 00

Assets .28 40 .55 89 .62 71 .68 06 .73 87 .80 32

Net fixed assets .5 30 .7 80 .8 96 .10 12 .11 28 .12 44

Investments .27 80 .30 54 .33 28 .36 02 .38 76 .41 50

Book value of quoted investments .0 02 .0 02 .0 02 .0 02 .0 02 .0 02

Receivables .10 70 .12 98 .15 26 .17 54 .19 82 .22 10

&Loans advances .9 91 .2 30 .2 72 .1 66 .1 06 .1 11

Deferred tax assets .2 01 .0 00 .0 00 .0 00 .0 00 .0 00

Cash and bank balance .0 87 .2 25 .2 48 .2 70 .2 93 .3 15

Miscellaneous expenses not written off .0 00 .0 00 .0 00 .0 00 .0 00 .0 00

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 12/17

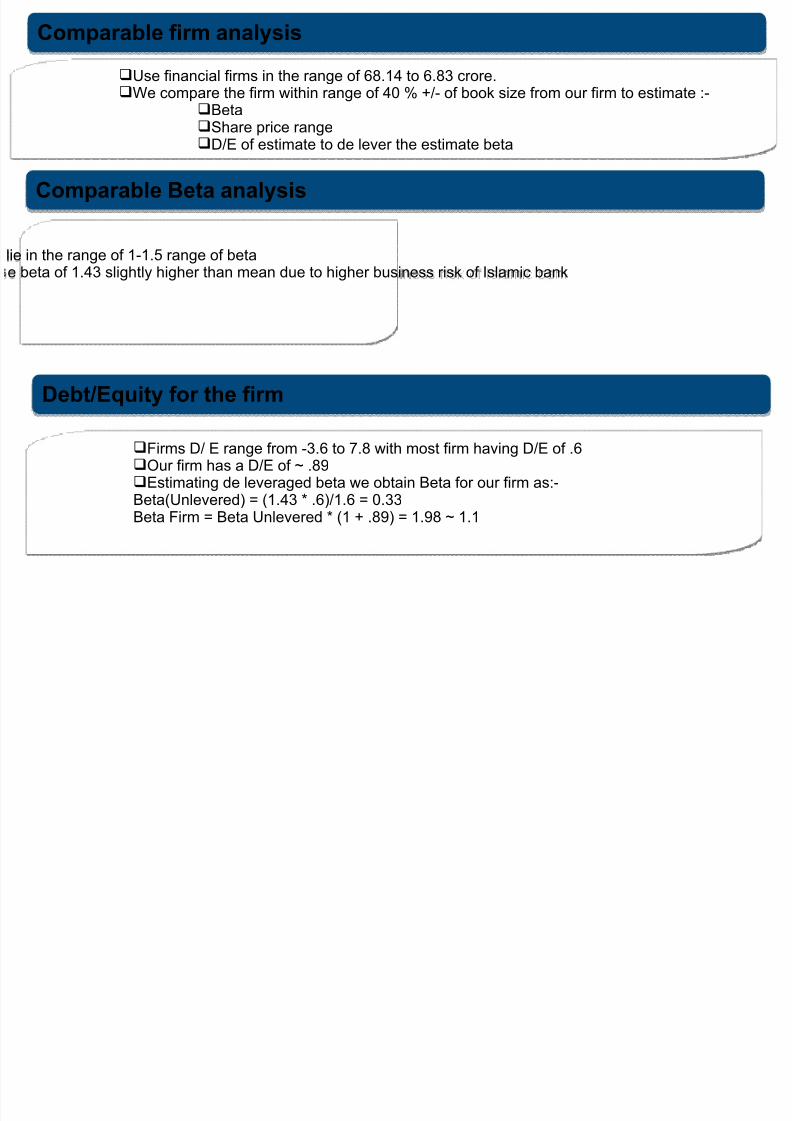

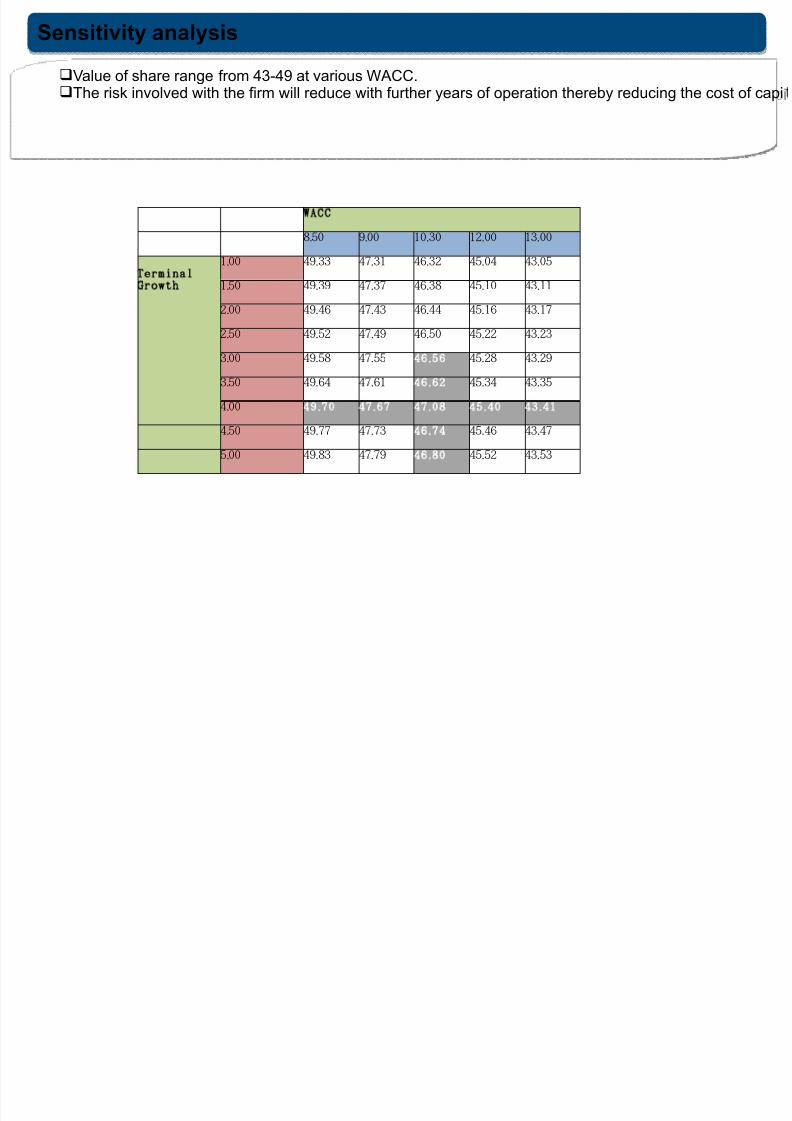

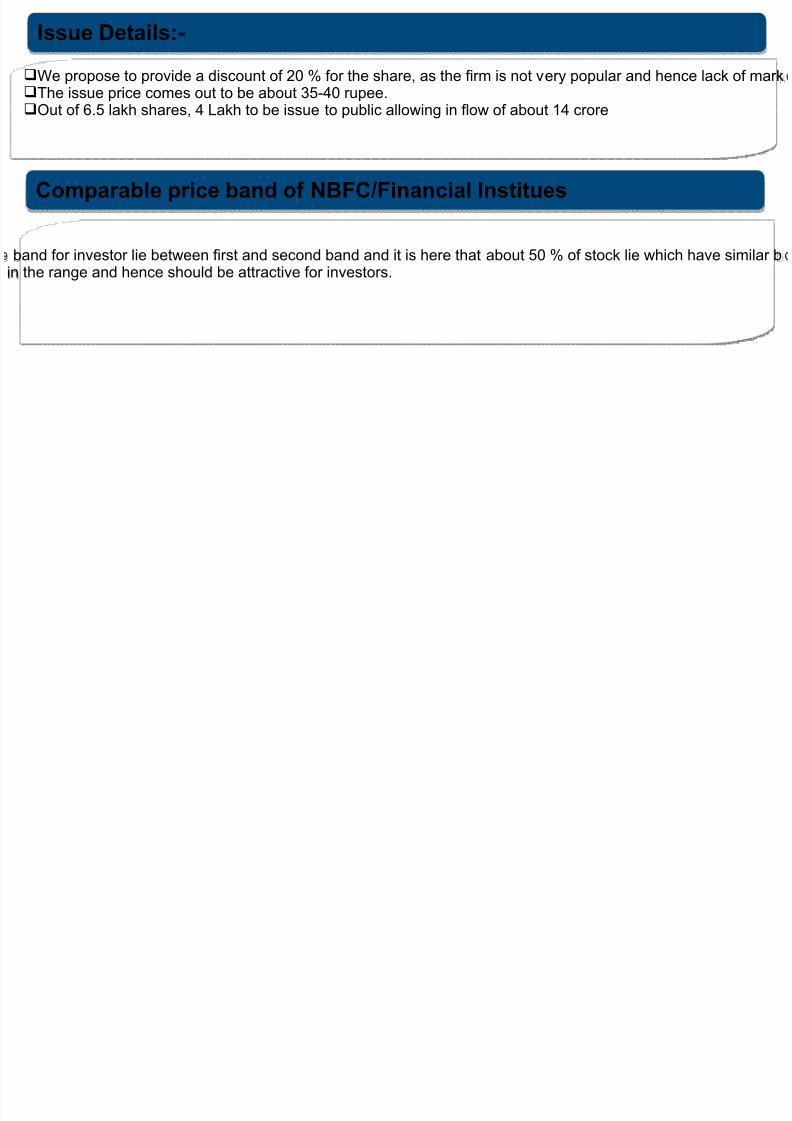

qUse financial firms in the range of 68.14 to 6.83 crore.qWe compare the firm within range of 40 % +/- of book size from our firm to estimate :-

qBetaqShare price range

qD/E of estimate to de lever the estimate beta

Comparable firm analysis

Comparable Beta analysis

lie in the range of 1-1.5 range of beta

e beta of 1.43 slightly higher than mean due to higher business risk of Islamic bank

Debt/Equity for the firm

qFirms D/ E range from -3.6 to 7.8 with most firm having D/E of .6qOur firm has a D/E of ~ .89qEstimating de leveraged beta we obtain Beta for our firm as:-Beta(Unlevered) = (1.43 * .6)/1.6 = 0.33Beta Firm = Beta Unlevered * (1 + .89) = 1.98 ~ 1.1

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 13/17

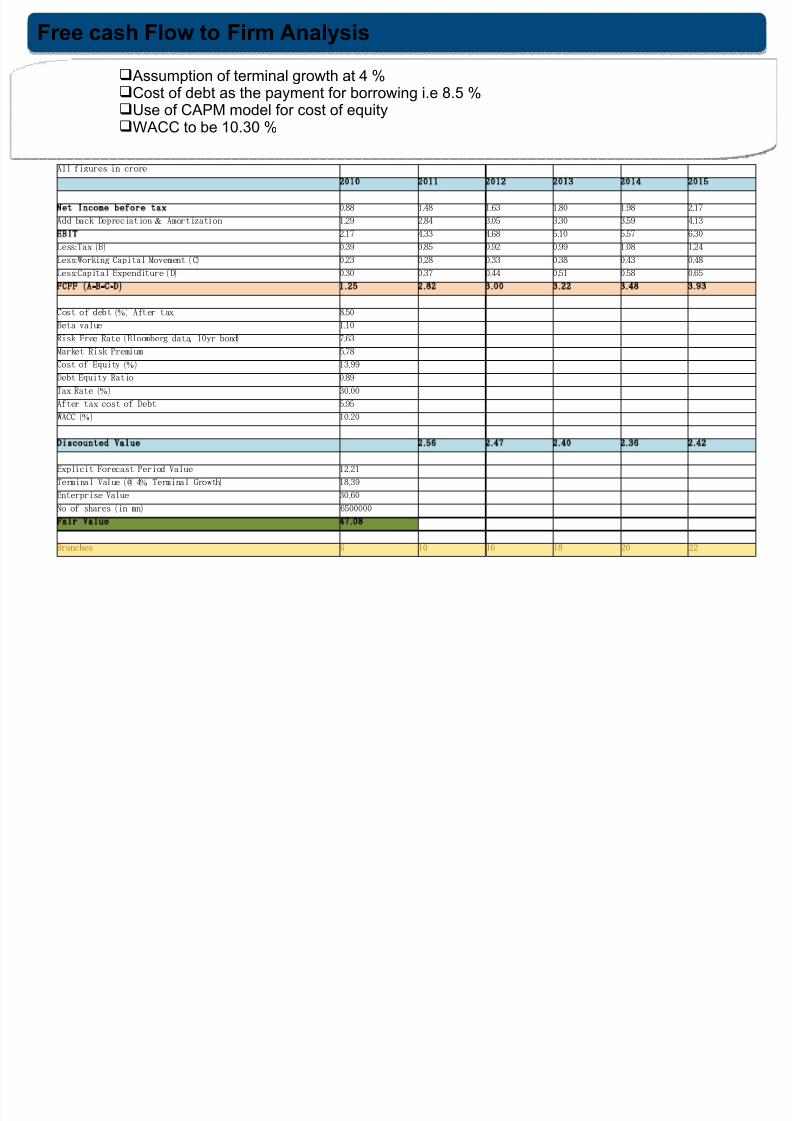

qAssumption of terminal growth at 4 %qCost of debt as the payment for borrowing i.e 8.5 %qUse of CAPM model for cost of equityqWACC to be 10.30 %

Free cash Flow to Firm Analysis

All figures in crore

2010 2011 2012 2013 2014 2015

et Inc ome before tax .0 88 .1 48 .1 63 .1 80 .1 98 .2 17

&Add back Depreciation Amortization .1 29 .2 84 .3 05 .3 30 .3 59 .4 13

EBIT .2 17 .4 33 .4 68 .5 10 .5 57 .6 30

: ( )Less Tax B .0 39 .0 85 .0 92 .0 99 .1 08 .1 24

: ( )Less Working Capital Movement C .0 23 .0 28 .0 33 .0 38 .0 43 .0 48

: ( )Less Capital Expenditure D

.0 30

.0 37

.0 44

.0 51

.0 58

.0 65

( - - - )CFF A B C D .25 .82 .00 .22 .48 .93

(%)C os t o f d eb t A ft er t ax .8 50

Beta value .1 10

( , )Risk Free Rate Bloomberg data 10yr bond .7 63

Market Risk Premium .5 78

(%)Cost of Equity .13 99

Debt Equity Ratio .0 89

(%)Tax Rate .30 00

After tax cost of Debt .5 95

(%) WACC .10 20

iscounted Value .56 .47 .40 .36 .42

Explicit Forecast Period Value .12 21

( % )Terminal Value @ 4 Terminal Growth .18 39

Enterprise Value .30 60

( )No of shares in mn 6500000

a ir V al ue .7 08

Branches 6 10 16 18 20 22

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 14/17

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 15/17

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 16/17

qSocial, economic and educational status of Muslim in India, by Prime Minister committee 2008qProwess database for stock related detailsqSeyad Shariat annual report, 2007, 2008, 2009,

qAswath Damodaran on ValuationqAswath Damodaran on Evaluation of Finacial services

Information from Firm

qTelephonic interview was done for Mr K. Ahamed Hussain - Deputy General Manager,

qProvided information on staff and operation

qProfit % paid over the period

qFuture plan of the firm

References

8/8/2019 Final Ppt Green Shoe

http://slidepdf.com/reader/full/final-ppt-green-shoe 17/17

•

•

•

Questions?????