final report - ehima · final report march 2016 jean de kervasdoué professor emeritus,...

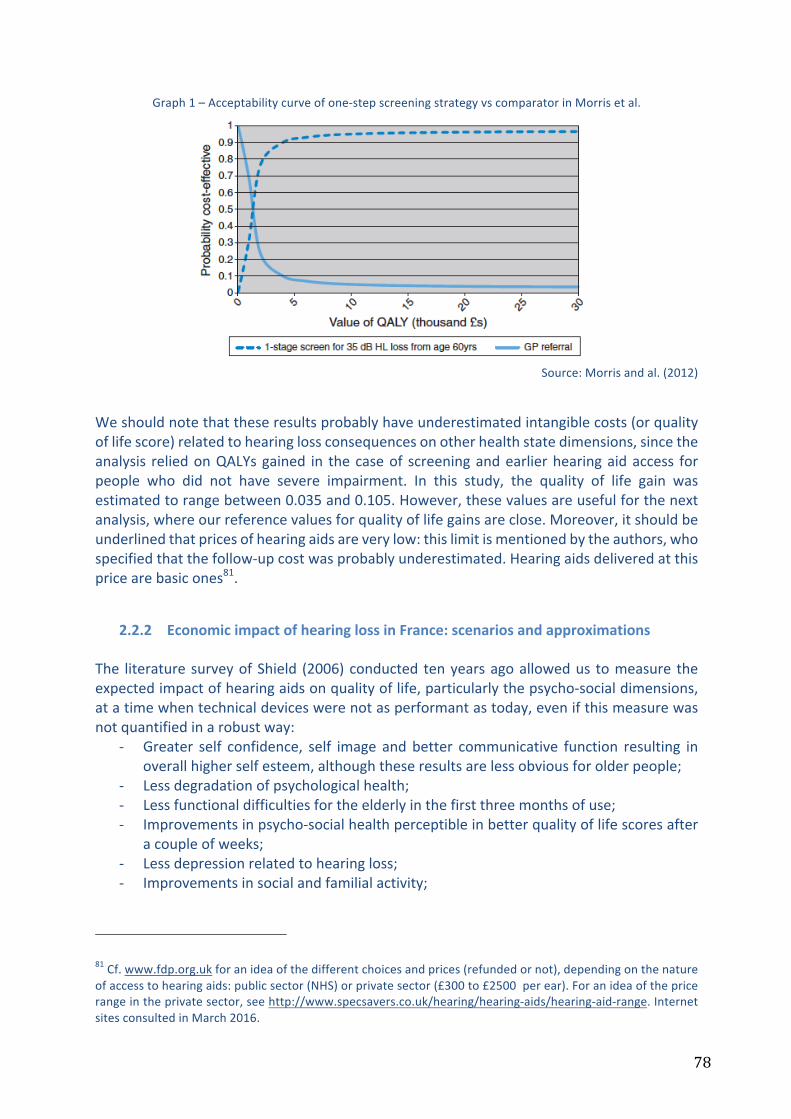

TRANSCRIPT

Economic Impact of Hearing Loss in France and Developed Countries A survey of academic literature 2005-2015

FINALREPORTMarch2016

JeandeKervasdouéProfessoremeritus,ConservatoireNationaldesArtsetMétiers

LaurenceHartmann

Seniorlecturer,ConservatoireNationaldesArtsetMétiers

2

ListofabbreviationsAFL AuditivefunctionallimitationsALD AffectiondelongueduréeAMC AssurancemaladiecomplémentaireAMO AssurancemaladieobligatoireAPA Allocationpersonnaliséed’autonomieAPHAB AbbreviatedProfileofHearingAidBenefitBLSA BaltimorelongitudinalstudyofagingBS BaromètresantéSurveyBSI BriefsymptomInventoryBSSM BaromètresantésourdsetmalentendantsSurveyCASF Codedel’actionsocialeetdelafamilleCEPP Commissiond’évaluationdesproduitsetprestationsCEPS ComitééconomiquedesproduitsdesantéCMUC CouverturemaladieuniversellecomplémentaireCNAMTS Caissenationaled’assurancemaladiedestravailleurssalariésCNEDiMTS Commissionnationaled’évaluationdesdispositifsmédicauxetdestechnologiesde

santédB Decibel(s)DREES Directiondelarecherche,desétudes,del’évaluationetdesstatistiquesDSS DirectiondelasécuritésocialeEHIMA EuropeanHearingInstrumentManufacturersAssociationENT Ear,NoseandThroatspecialistESPS EnquêtesantéetprotectionsocialeSurveyEQ-5D QualityoflifequestionnaireEuroQolHA(s) Hearingaid(s)HAS HauteAutoritédeSantéHCAAM HautConseilpourl’avenirdel’assurancemaladieHID Handicaps-Incapacités-DépendancesSurvey1998HUI3 QualityoflifequestionnaireHealthutilitiesindexMark3IGAS InspectionGénéraledesAffairesSocialesICER IncrementalCost-EffectivenessRatioINSEE InstitutNationaldelaStatistiqueetdesEtudesEconomiquesInVS InstitutNationaldeVeilleSanitaireINPES InstitutNationaldePréventionetd’EducationàlaSantéMMSE MinimentalstateexaminationNHANES NationalhealthandnutritionexaminationsurveyNHI NationalHealthInsuranceNHS NationalHealthSystemNICE NationalInstituteofClinicalExcellenceOCAM Organismescomplémentairesd’assurancemaladieOECD OrganisationforEconomicCooperationandDevelopmentOOP Out-of-pocketPCH PrestationdecompensationduhandicapPHQ9 Patienthealthquestionnaire-depressionQALYs QualityadjustedLifeYearsROSP RémunérationsurobjectifsdesantépubliqueRQTH ReconnaissancedelaqualitédetravailleurhandicapéSF12 QualityoflifequestionnaireShortform12dimensionsSNIIRAM Systèmenationalinter-régimesdel’assurancemaladieSNITEM SyndicatNationaldel’IndustriedesTechnologiesMédicalesUNPS UnionNationaledesProfessionnelsdeSantéUNSAF UnionNationaledesSyndicatsdesAudioprothésistesFrançaisVAT Valueadded-taxVSL ValueofstatisticallifeWHO WorldwideHealthOrganisationWHO-QoL QualityoflifequestionnaireofWHO

3

Contents

Listofabbreviations...........................................................................................................2Contents.............................................................................................................................3

Summary............................................................................................................................5

Introduction.......................................................................................................................91 Hearingloss:outlinedata...........................................................................................111.1 PrevalenceofhearinglossandauditivefunctionallimitationsinFrance...............................121.1.1 Estimationsofhearinglossprevalencein“Handicap-Santé”Frenchsurvey2008.............131.1.2 Estimateddataforhearinglossprevalencein2015.........................................................................151.1.3 Mainfeaturesofthepopulationaffectedbyauditivefunctionallimitations.........................16

1.2 AccesstohearingaidsinFrance:anoverview....................................................................................181.2.1 PublicandprivatehearingaidsexpenditureinFrance...................................................................181.2.1.1 Overallhearingaidsexpenditure...............................................................................................................181.2.1.2 Estimationsofthenumberofhearingaidusers..................................................................................211.2.1.1 Estimationsoftheaveragepriceofahearingaid...............................................................................26

1.2.2 Financinghearingaids...................................................................................................................................301.2.2.1 Financingrulesforhearingaidsaseithertechnicalsupportormedicaldevices.................301.2.2.2 Publicandprivatefinancingrulesforhearingaidequipment......................................................311.2.2.3 Estimationsofout-of-pocketpaymentandhealthcarerenouncement.....................................35

1.2.3 Thehearingaid:adurablegoodassociatedwithaparamedicalservice................................401.2.4 Hearingaidpricingissues:ananalyticaleconomicframework..................................................42

1.3 Hearinglossprevalence,hearingaidaccessandpricingincomparablecountriestoFrance ...................................................................................................................................................................................481.3.1 Hearinglossprevalence,equipmentrateandaccessratetohearingaids.............................481.3.2 Estimationoftherealaccessrateforhearingaidsdependingontheeligiblepopulationandoncompliance............................................................................................................................................................501.3.3 Determinantsofaccesstohearingaids..................................................................................................521.3.4 Theroleofhealthsystemsinhearingaidaccessandperceivedefficiencybyusers...........55

2 Healthandeconomicconsequencesofhearingloss:impactstudy..............................622.1 Observedscientificconnectionsbetweenhearinglossandmorbi-mortalityinadultsandelderlypopulations..........................................................................................................................................................622.1.1 HearinglossandassociatedlimitationsinFrance............................................................................632.1.1.1 Associateddeficiencieswithhearingloss...............................................................................................632.1.1.2 Functionallimitationsassociatedwithhearingloss..........................................................................642.1.1.3 Activityrestrictionsandsocialinvolvementassociatedwithhearingloss..............................65

2.1.2 Mainfindingsinmedicalscientificliterature......................................................................................662.1.2.1 Anincreasedriskofmortality......................................................................................................................662.1.2.2 Anincreasedriskoffalls................................................................................................................................672.1.2.3 Adegradationinmentalhealth...................................................................................................................672.1.2.4 Deteriorationincognitivecapacities........................................................................................................692.1.2.5 Healthatwork.....................................................................................................................................................71

4

2.2 Economicimpactofhearingloss...............................................................................................................712.2.1 Economicassessmentsinscientificliteratureofhearingloss:healthcareaccess,expenditureandscreening............................................................................................................................................732.2.1.1 Higherhealthcareaccessandexpenditurelevel................................................................................732.2.1.2 Economicconcernsofearlierscreeningforhearingloss................................................................74

2.2.2 EconomicimpactofhearinglossinFrance:scenariosandapproximations.........................782.2.2.1 Qualityoflife,preference-basedscores,QALYsandstatisticalvalueofahumanlife:aframework792.2.2.2 Annualcostofhearingloss(2014)accordingtothequalityoflifeperspective....................812.2.2.3 Additionalhealthcarecostsduetonon-equippedhearinglossandefficiencyofhearingaidsregardingeligiblepopulation:approximations.................................................................................................86

3 Conclusion..................................................................................................................90References.......................................................................................................................93

5

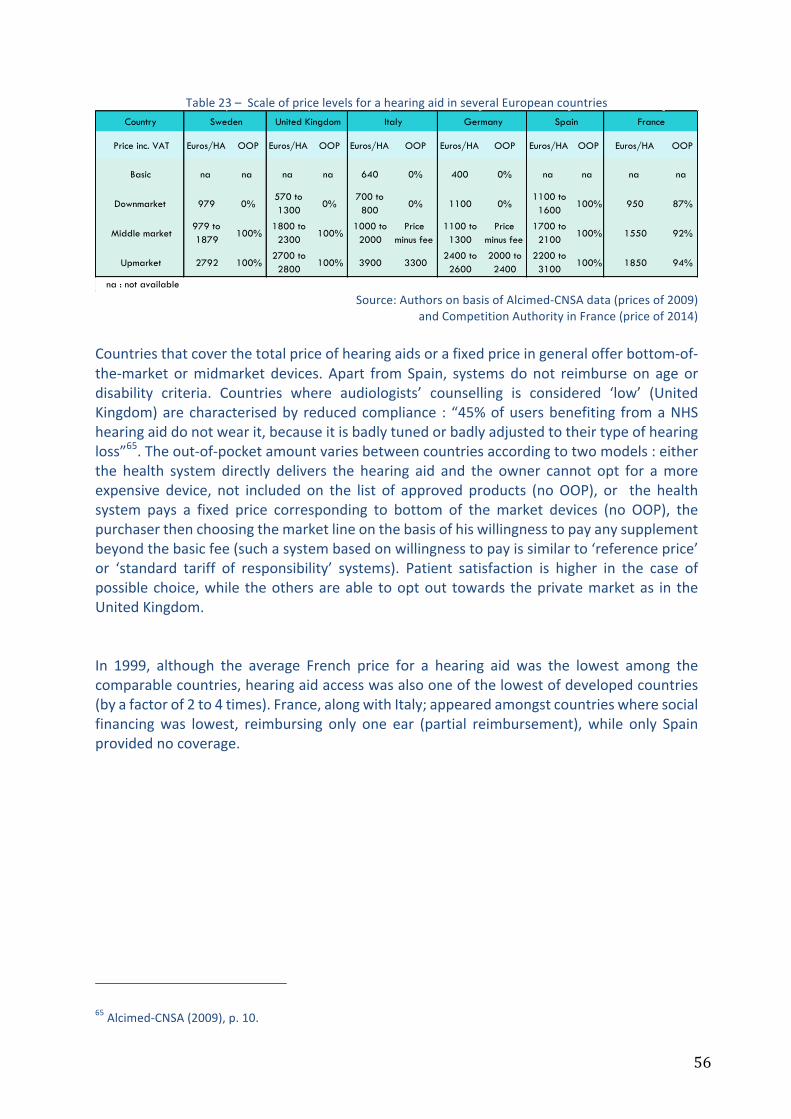

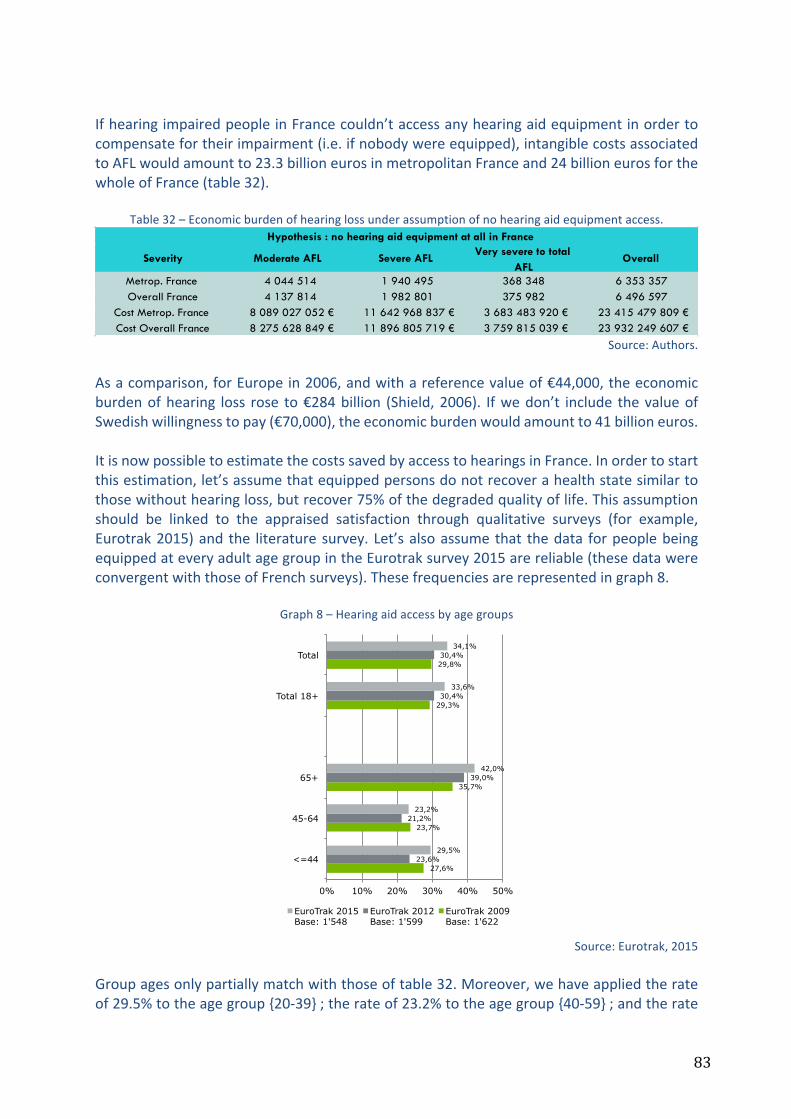

SummaryHearinglossinFranceaffectsabout10%ofthepopulation,namelyover6millionpeoplehavetofacehearingdifficultiesindailylife.Olderadults(over50yearsold)arethemostconcerned–onethirdof thispopulation–ashearing lossarisesduringthecourseof life (for88%ofFrench people), through a natural and progressive phenomenon (presbycusis) or afterexposuretonoise.InEurope,JapanandtheUnitedStates,prevalenceratesarecomparabletothoseinFrance.TheWHOestimatesthisburdenofillnesstocurrentlyconcernmorethan5% of the global population, representing 360 billion people. Nowadays, hearing loss isconsideredasamajorpublichealthissueinthescientificliteratureandbyinternationalhealthagencies.Notonly is hearing loss apparent throughdirect functional limitations (understandingandcommunicationdifficulties),buthearingimpairmentisalsoassociatedwithahigherfrequencyof mental disorders, cognitive decline, falls and even mortality, independently of ageingeffects. Hearing loss could precipitate the elderly into dependency.Hearing aids (‘medicaldevices for individual use’) compensate, to a certain extent, for hearing impairment and,furthermore,ensuresomeindividualrehabilitation:in2015,morethan2millionFrenchpeopleownedhearingaidsoutof3millioneligiblepeople.Thistechnicalsolutionshouldbefurtherencouraged,since1millionFrenchpeopledeclareaneedforhearingaidsbutdon’tgetthem.Asaresult,improvingaccesstohearingaidsrepresentsadecisiveissue,notonlyintermsoffinancialaccessibilityandfairness,butalso intermsofefficiency:hearingaidequipment ispresumedtoreducethesignificantimplicationsofhearinglossonhealthstateandhealthcareexpenditureand,thus,improvethepatient’squalityoflife.Yet,thehearingaidsectorinFrancehasbeenlongcharacterizedbyawait-and-seepublicpolicy:theregulatoryruleshavebeenfrozenforseveraldecades,duetoalackofreliableinformationontheexpectedaddedvalueofhearingaids(ineconomictermsofutility).Thislackofinformationandstalledregulationshaveresultedinseveralrecentreports,releasedbytheCourtofAccounts(Courdescomptes)and the General Inspectorate for Social Affairs (Inspection générale des affaires sociales),whichbothunderlinetheurgentneedtore-examinetheaccessrulestohearingaidsandtoprovide,atthesametimeaneconomicassessmentofthisequipment.ThemainobstacletohearingaidaccessinFrance(financialbarrier)concernscurrentfinancingrules,andparticularlythepublictrade-offsthathaveledhearingaidstobeclassifiedinthe‘low risk’ category and practically excluded from socialised health care. This classificationimplicitlyindicatesthatthehearingaidisaluxuryproductwhosemedicaladded-valueisverylow: incomparisontothetrade-offs fordrugclassification, thehearingaidmedicaladded-valuerangesbetween‘low’and‘insufficient’,sinceitsobservedreimbursementrateisunder15%.Yet,wideaccesstohearingaids(2/3intermsof‘realaccess’oftheeligiblepopulation)showsclearlythatdemandelasticityislow:theyareanecessaryitem.Ingeneral,thepublicchoiceofcoinsurancedependsonthecombinationof‘lowrisk’and‘commitment’.Thereisonlypartialreimbursementinrelationto‘lowrisk’,oreventotallyexclusionfromthesocialhealthcarebasketwhenitdoesnotdependonthecollectiveresponsibilityandimpliesanindividualjudgementonthetrade-offconsumption-price(inordertoavoidover-consumptionor,ineconomics,the‘moralhazard’risk).Yet,notonlyisaccesssignificantdespitetheout-of-pocketpayment,butmoreover itshealthconsequencesaswellas itseconomic impactare

6

likelytobemajor.Thecosttosocietyofhearingaidrenunciation,intermsofqualityoflife,expenditure and social inequalities is in total opposition to the objectives assigned to theFrenchhealthsystem.Hearingloss:outlinedataDisablinghearinglossprevalenceisestimatedtodaytorangebetween8.6%and11.2%oftheoverallFrenchpopulation.Theanalysisofhearingaidaccessshowsthat30%to35%ofhearingimpairedpeopleareequipped,namely2millionoutof6millionpeople.Thisgapisreducedwhenconsideringpeoplebeingequippedandpeopleeligibleforhearingaids:whatevertheexpertassessments,surveydataorempiricalstatements(monographsbycountry),onlyhalfofhearingimpairedpeoplewouldbeeligibleforhearingaids,thus3millionpeopleinFrance.Thus, 65%of eligible Frenchpeoplearehearingaidownerswhereas35%of them remainunequipped.Thereare twomain reasonswhich canexplain this renunciation: a lowpublic andprivatecoverage(provision),andalackofinformation.Indeed,theaveragepriceforonehearingaidcomes to1,535euros,and3,070euros forbinauralequipment.But thisexpense ispoorlycoveredbytheNationalHealthInsurance(8%)andpoorlyreinsuredbycomplementaryhealthinsurances(30%),leavingahighout-of-pocketpaymentfortheadultinsured(62%),namely950eurosperapparatus.Thepriceforhearingaidequipmentcomprisesboththedeviceandtheaudiologist’scounsellingandfollow-upservices.Forthehearingaidowners,theequipmenthasanaveragedurationof5to6years,duringwhichaqualifiedcheck-upisensuredbytheaudiologist.Thequalityoftheequipmentaswellasthequalityofthefollow-upshould influencehearingaidefficiency,usersatisfactionandbeneficial compliance. This hypothesis seems to be confirmed throughout internationalcomparisons:incountrieswhereaccessratetohearingaidsishigher,thesocialcoverageisbetter for downmarket or middle market equipment. However, these countries don’tnecessarilyhavegreaterratesofrealHAsusers(i.e.ratesconsideringeffectiveeligiblepeopleforhearingaidsandeffectivewearingofhearingaids).Takenthus,FrancewouldpresentarealrateofuseclosetothoseoftheUnitedKingdom,GermanyandNorwayandstartingfromvery different situations in terms of financial access to equipment. If there is room forimprovement in France regarding the need for hearing aid equipment – due to financialimpediment-thereisalsoroomforgrowthincountrieswherehearingaidsare(almost)freelydeliveredbutwherethecomplianceisn’tsufficientlyperformant.Areviewoffinancialrulesrelatingtohearingaidshastoconsiderthecompliancefactorsdeterminingtheeffectiveuseofequipmentand,thus,thelevelofsatisfactionforhearingaidusers.Concerningthepaymentschemesforaudiologists,aneconomicanalysisisnecessary,takinginto account their incentiveproperties. In order to regulate thehearing aid sector and todesignanincentivepaymentforhearingaids,atrade-offisnecessarybetweentheobjectivesofexpenditurecontrol,healthcarequalityandfreedomofchoice,inahypotheticframeworkassumingahighercoverageofhearingaids.Therearemanytoolsallowingustorealisetheoptimaltrade-offforpublicfinancing,butacautiousapproachisrequiredregardingtheissueofapossibledecouplingofthedeviceandtheservice.Thisdecouplingmodelbringsupadverseeffectswhich are similar to those of ‘cost-plus’ payment, leading to increasing prices and

7

puttingpatients’complianceatstake,i.e.affectingthetherapeuticefficiencyofhearingaidsfor some of them. At the same time that recourse to prospective payment systems isincreasingly implementedforpricinginhealthsystems,andasgrowingattentionispaidtopatients’empowerment, this conceptofdivisibilitydevice/service fallswithinabackwardseconomicapproach intermsofoptimal incentives. Internationalcomparisonshighlighttheimpactofcoverageandhealthcareorganisationonhearingaidaccess,equipmentrenewaland patients’ compliance. They showalso that French prices for one hearing aid are verysimilartothoseofotherEuropeancountries.Healthandeconomicconsequencesofhearingloss:impactstudyInternationalmedical scientific literatureaswellasFrenchsurveydataareprofuseon theburden of illness topics and these start to provide evidence-based studies on the causalallegedconnectionbetweenhearinglossandhealthstatedegradation.Disablinghearingloss(ormoderatetototalauditivefunctionallimitations),byreducingtheperson’scommunicationcapacities, rebounds significantly onto the whole dimensions of health state (mobility,autonomy,dailyactivities,pain/discomfort,anxiety/depression)throughasuccessionofchainreactions,themainonesbeingsocial isolation,cognitivedecline,sufferingatwork,mentaltroublesandfalls.Hearinglossrepresentsamajorimpairmentwhich,byaffectingmorethansixmillion(oftenolder)Frenchpeople,notonlyhasdeleteriouseffectsonqualityoflifebutalsoleadstoadditionalhealthandsocialcareexpenditureforsocietyasawhole.Thescientificliteratureunambiguouslyreportsthenegativewaterfalleffectsofhearingloss,butalsoshowthebeneficialeffectsofhearingaidwearing:reducedmortalityrisk;improvedpsycho-socialhealthstate;andanormalisingeffectoncognitivedeclinerisk.Publicationsalsopointoutthatthisfavourableimpactonmentalhealthisappreciablestartingfromthefirst3monthsof equipment. In the sameperspective, some studies show the reliability and theefficiencyofearlierscreeningforpeopleattheendoftheirworkinglives,screeningthosewhoareoldenoughto justifysecondaryprevention,butyoungenoughtobenefit from itsincetheirhearinglosslevelismoderatetosevere.Earlierscreeningappearstobeaveryefficientstrategyregardingcostandqualityoflife.Itshouldbeimplementedoverthecourseofmedicalconsultations,intheformoftwoshortquestionswithoutadditionalcoststogeneralpractice.Startingfromthisliteratureandthesurveydata,twoscenariosforeconomicassessmentofhearinglossareproposed.ThefirstonegivesroughestimatesforintangiblecostsrelatedtoqualityoflifedegradationinFrance.Theaimistoassessthemonetaryvalueoflosthealthyyears by valuing them in terms of the implicit price of human life. Based on realisticassumptions,thisestimationdrawsanimageofsavedcoststhankstohearingaidequipmentor compliance, as well as the economic burden of hearing loss related to its prevalence:without equipment, this burden would amount to 23.4 billion euros. The real rate ofequipment(effectiveaccessandeffectiveuseofhearingaids)reducesthisburdenby30%,whereas the target equipment rate (i.e. 50%ofhearing impairedpeople related to actualcompliance)wouldlightentheburdenby40%.The secondscenario relieson severalassumptions inorder toestimate,on theonehand,medical costs related tohearing losswithoutequipment and,on theotherhand, averagescoresof lostutility related toqualityof life.Bothdimensionsaregraduatedaccording toFrench hearing loss prevalence rates by age groups and by severity levels, then they are

8

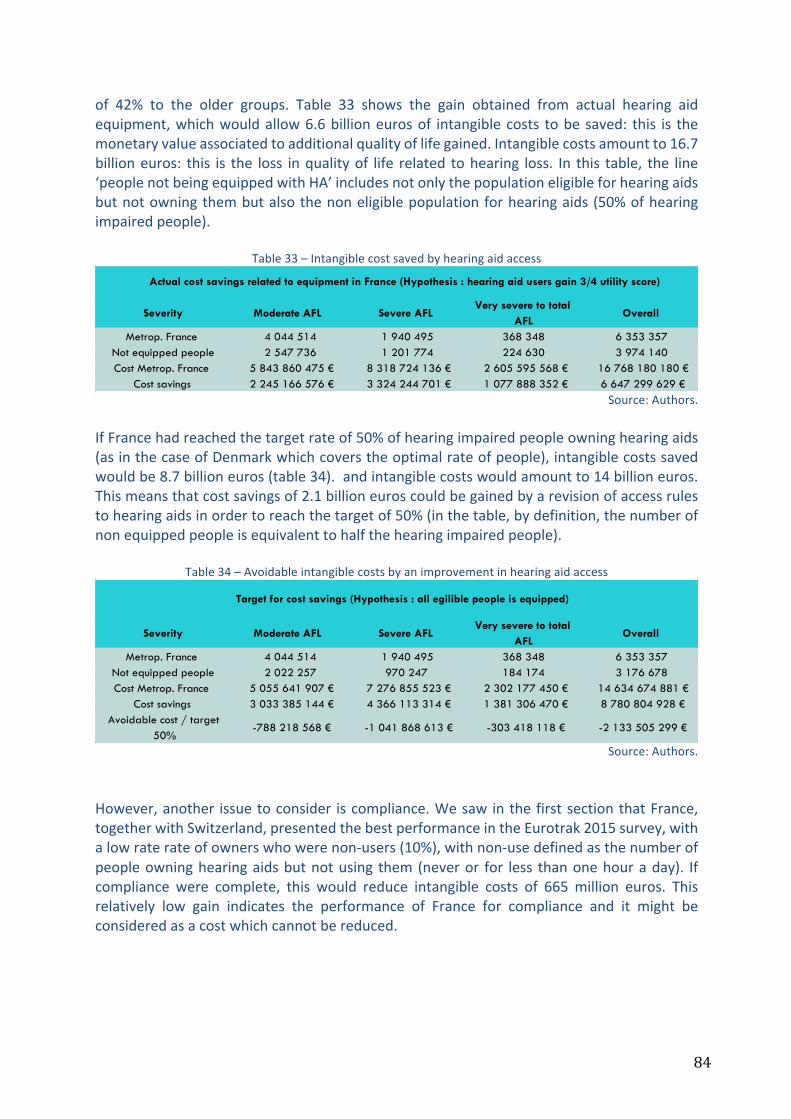

connectedwiththerateofeligiblepeopleforhearingaidsbutwhoarenotbeingequipped.Forthisspecificpopulation,weassumethatagainshouldbeexpectedinqualityoflifeandincost savings, if equipmentweredelivered for 6 years.Assessing these values allowsus toroughlyestimatearangefortheincrementalcost-utilityratio,expressingthecosttopayinordertogainoneadditionalhealthyyearfortheperiod.Yet,throughthissimplesimulation,thetargetstrategy(i.e.equipmentforeligiblepopulationnotaccessinghearingaids)wouldbedominant,eventakingintoaccountthecomplianceratethatreducesqualityoflifegainsandcostssavings:theoverallcostofthisadditionalequipmentwouldbe1.5billioneuros,with48,000QALYsgainedandwithcostsavingsworth1.7billioneuros,namelya ICERof -830euros/QALY.Inotherwords,thetargetstrategyof‘alleligiblepeopleareequipped’savescostsandprovidesanincreasedqualityoflife,andisthusthedominantstrategy.Thisentirecasestudy,whichreliesonacceptableassumptions,underlinestherequirementforasubstantialeconomicassessmentthatwouldcorroboratetheseresults,thatisthehighlyefficienttargetstrategy that ‘all eligible hearing impaired people are equipped’, since the annual overallexpenditureofthehearingaidsectorcomescloseto1billioneuros.However,itremainstosolve the touchy question of hearing aid financing likely to support access to them, andespecially thequestionof therelativefinancialcontributionsofpayers,asseen inthefirstsectionofthereport.Moreover, if theNationalHealth Insurancecouldgreatly increase itsfinancialroleinhearingaidreimbursement,wewouldanticipateabounceeffectforpeoplebeing equipped but having postponed hearing aid renewing. This effect would inevitablyincreasethebudgetimpactofhearingaidaccess.That’swhyanoverallscenariohastobesetup,throughprospectivecost-efficiencyassessments,bycollectingusefuldatainsequentialorregularsurveysbasedontheworkingandolderpopulation,inordertoinferthedifferentialcost-utilityratiobetweenstrategies.ThisoverallscenariowouldbecompletedbyestimatingthebudgetimpactofhearingaidequipmentdependingonseveralcoveragescenariosfromtheNationalHealthInsurance’spointofview.Comingoutofthisoverview,thehealthpolicyforsecondaryprevention,thatcouldconsistofscreeningandequippinghearingimpairedpeoplewithhearingaids,isnon-existentregardingpublicreimbursement.NationalHealthInsurance,bycoveringonly8%ofhearingaidpriceforadults,hasalmostexcludedhearinglossfromitsmanagementpolicyforhealthrisk,leavingtheout-of-pocketpaymenttocomplementaryinsurancebodiesandabovealltopatients.Infine,families,closerelativesandthewholesocietybearsthecostsofthisimpairment,aswellasforthelossofautonomysinceonethirdoftheeligiblepopulationforhearingaidsdon’tgettothem.Moreover,inequalitiesrelatingtotherightsofthoseinsuredwithcomplementaryhealthbodies,theirrevenueandabilitytopayforequipmentcontributetomaintainthesesocialinequalitiesinhealth,bytherenouncementeffect.ThesestatementswouldimposetheneedforanurgentexaminationoftheregulatoryrulesforthehearingaidsectorinFrance,atamomentwhereageing,andlisteningtoamplifiedmusicamongtheyoungriskscontributingtoaggravatedhearinglossprevalenceinFrance.

9

IntroductionInFrance,over6millionpeoplehavedisablinghearingloss,leadingtodifficultiesindailylife.Olderadults(over50yearsold)arethemostconcerned–onethirdofthispopulation–ashearing loss arises during life course (for 88% of French people), through a natural andprogressivephenomenon(presbycusis)orafterexposuretonoise.Notonly is hearing loss apparent throughdirect functional limitations (understandingandcommunicationdifficulties),buthearingimpairmentisalsoassociatedwithahigherfrequencyof mental disorders, cognitive decline, falls and even mortality, independently of ageingeffects. Hearing loss could precipitate the elderly into dependency. Medical scientificliteratureisprofuseonthistopicandstartstoprovideevidence-basedstudiesonthecausalallegedconnectionbetweenhearinglossandhealthstatedegradation.Moreover,ithighlightstheburdenofillnessanditsimpactonhealthcareconsumptionandexpenditure.Therefore,hearinglossisamajortopicforpublichealth.Hearingaidscompensate,toacertainextent,forhearinglossand,furthermore,ensuresomeindividual rehabilitation: in 2015,more than 2million French people owned hearing aids.However,thistechnicalsolutionshouldbefurtherencouraged,since1millionFrenchpeopleareeligibleforhearingaidsbutdon’tgetthem.Therearetwomainreasonswhichcanexplainthis renunciation:a lowpublicandprivatecoverage (provision),anda lackof information.Indeed, the average price for one hearing aid comes to 1,535 euros, and 3,070 euros forbinauralequipment.ButthisexpenseispoorlycoveredbytheNationalHealthInsuranceandpoorlyreinsuredbycomplementaryhealthinsurances,leavingahighout-of-pocketpaymentfortheinsured.Asaresult,improvingaccesstohearingaidsrepresentsadecisiveissue,notonlyintermsoffinancialaccessibilityandfairness,butalso intermsofefficiency:hearingaidequipment ispresumedtoreducethesignificantimplicationsofhearinglossonhealthstateandhealthcareexpenditure and, thus, improve the patient’s quality of life. Yet, the hearing aid sector inFrancehasbeenlongcharacterizedbyawait-and-seepublicpolicy:theregulatoryruleshavebeenfrozenforseveraldecades,duetoalackofreliableinformationontheexpectedaddedvalue of hearing aids (in economic terms of utility). This lack of information and stalledregulationshaveresultedinseveralrecentreports,releasedbytheCourtofAccounts(Courdescomptes)andtheGeneralInspectorateforSocialAffairs(Inspectiongénéraledesaffairessociales),whichbothunderlinetheurgentneedtore-examinetheaccessrulestohearingaidsandtoprovide,atthesametimeaneconomicassessmentofthisequipment.Economic assessment of hearing aids should corroborate their efficiency and, if relevant,shouldleadtoacorrectionofthescopeforsocialreimbursement,asfarasthebudgetimpactonNationalHealthInsuranceisaffordable.Suchanassessmentrequiresthinkingintermsofutilityandqualityoflifeforpeoplewearinghearingaidsandtocomparethecost-utilityratioofequipmentwithrespecttonon-equipment.Inlinewiththesequestions,anotherissueisthereliabilityofhearinglossscreeninginordertopreventearlylossofautonomy.Shouldageneralised screening program be considered appropriate for people at the end of theirworkinglives?Ifso,underwhichconditionsandforwhatefficiency?

10

Thepurposeofthepresentstudyistogatherandreviewthemajorpapersinthescientificliteratureaswellasthegreyliteraturereleasedonthistopicovertheperiod2005-2015.Weput this literature into perspective using some economic tools in order to propose aneconomical framework for regulatory analysis of the hearing aid sector. Then, we bringforwardroughestimatesforthecostandtheutilityofhearingaids.This report is structured in twomain sections as follows: section 1 focuses specifically onhearinglossinFranceandpresentstheruleswhichorganiseaccessanddeliveryofhearingaidequipment.AninternationalcomparisonforkeycountriesinEuropeisaddressedwhensimilarcollectionofdataisavailable.Section2outlinestheglobalburdenofhearingloss,onthebasisofkeypapersreleasedinthemedicalscientific literature.Asanextensionofthissurvey,ahypotheticalscenarioforeconomicassessment issetoutonthebasisofavailabledataforFrance.

11

1 Hearingloss:outlinedataHearinglossprevalenceinFranceanditsconsequencesonhealthstateemphasizethispublichealthissue,eventhoughtherearedifferingdefinitions:approximately16%ofFrenchpeoplereportsomedifficultieswithhearing(inthebroadestsense,definedby‘auditivefunctionallimitations’)whereasdisablinghearinglossaffects8.6%to11.2%ofFrenchpeople(definedby‘disablinghearingloss’)(Haeuslerandal.,2014;EHIMA,2015)1.Hearinglossaffectsmostlyadultsaged50yearsandover(progressivehearingimpairmentwitholderageorpresbycusis).Inthegeneralcase,hearinglossalleviationreliesontheuseofhearingaids(HAs),whicharea ‘medical device for individual-use’ in the French classification. The analysis of access tohearing aids is tricky because not only is available data lacking, but values are variablebetween sources, surveys or databases. There is an obvious and important gap betweenpeoplebeing fittedwith aprosthesis (in the study, ‘hearing aidowners’) andpeoplewithdisablinghearingloss:only30%to35%ofthelatterarehearingaidowners2.Theaverageprice foronehearingaid (HA) isaround1,535euros,while social coverage isparticularlylow(120eurosforoneear,thatisabasisforsocialreimbursementof200eurosassociatedwithacoinsurancerateof60%).Hence,thegrossout-of-pocketsumis likelytorepresentahighbarriertoaccess,inthatcomplementaryinsurancecoversaminorpartofit.There is also significant inequalitybetweenbeneficiariesdue to thediversityof contracts.Indeed,thenetout-of-pocketsumisestimatedtobe62%ofthetotalprice(i.e.958eurosapiece) and is associated with healthcare renunciation. For the hearing aid owners, theequipmenthasanaveragedurationof5years,duringwhichaqualifiedcheck-upisensuredbytheaudiologist: thepricecomprisesboththedeviceandtheservice.Thequalityof theequipment as well as the quality of the follow-up should influence user satisfaction andbeneficialcompliance.Thishypothesisseemstobeconfirmedthroughoutinternationalcomparisons:startingfromthedataoftheEHIMA(2015)andonthebasisofthemethodologyofAlcimed-CNSA(2009),wecanstatethefactthatincountrieswhereaccessratetohearingaidsishigher,thesocialcoverageisbetterfordownmarketormiddlemarketequipment.However,thesecountriesdon’tnecessarilyhavegreaterratesofrealHAsusers(i.e.ratesconsideringeffectivewearingofhearingaids).Takenthus,Francewouldpresentarealrateofusecloseto61%(combiningtherateofeligiblepeopleforhearingaidsandtherateofeffectiveuse),aratesimilartothoseoftheUnited-Kingdom,GermanyandNorwayandstartingfromverydifferentsituationsintermsoffinancialaccesstoequipment.IfthereisroomforimprovementinFranceregardingtheneedforhearingaidequipment–duetofinancial impediment-there isalsoroomforgrowth in countries where hearing aids are (almost) freely delivered but where the

1Thereissomevariabilityinestimationsofthenumberofpeopleaffectedbyhearingloss,dependingonthefieldsofsurveysandtheirmethodology.Inthisstudy,wequalifyhearinglossinthebroadsensewhenitincludesslightlimitationsnotassociatedwithaneedforhearingaids,anddisablinghearingloss(orhearinglossinthestrictsenseoftheterm)whentheimpairmenthasanimpactuponthedailyactivities.2As shown further, theseestimationsarewidely variable in surveys.Moreover, the reportwill focuson thedifferencebetweenpeopleabletobeequippedandpeoplewithdisablinghearingloss.Hence,theseestimationshavetobetakenasapproximations.

12

compliance isn’tsufficientlyperformant.Areviewoffinancialrulesrelatingtohearingaidshastoconsiderthecompliancefactorsdeterminingtheeffectiveuseofequipmentand,thus,thelevelofsatisfactionforhearingaidusers.Atrade-offhastobeundertakenbetween,onone hand, financial access and, on the other hand, suppliers’ and users’ commitment tohearingaiduse.

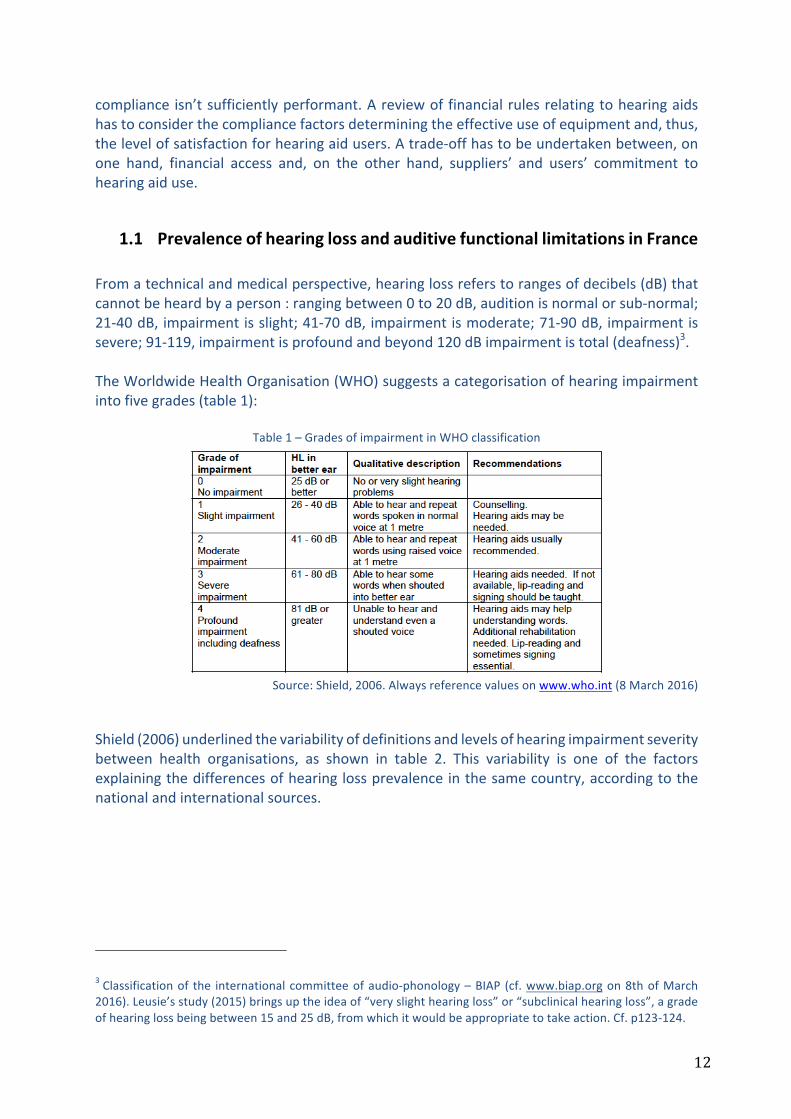

1.1 PrevalenceofhearinglossandauditivefunctionallimitationsinFranceFromatechnicalandmedicalperspective,hearinglossreferstorangesofdecibels(dB)thatcannotbeheardbyaperson:rangingbetween0to20dB,auditionisnormalorsub-normal;21-40dB,impairmentisslight;41-70dB,impairmentismoderate;71-90dB,impairmentissevere;91-119,impairmentisprofoundandbeyond120dBimpairmentistotal(deafness)3.TheWorldwideHealthOrganisation(WHO)suggestsacategorisationofhearingimpairmentintofivegrades(table1):

Table1–GradesofimpairmentinWHOclassification

Source:Shield,2006.Alwaysreferencevaluesonwww.who.int(8March2016)

Shield(2006)underlinedthevariabilityofdefinitionsandlevelsofhearingimpairmentseveritybetween health organisations, as shown in table 2. This variability is one of the factorsexplainingthedifferencesofhearinglossprevalenceinthesamecountry,accordingtothenationalandinternationalsources.

3Classificationof the internationalcommitteeofaudio-phonology–BIAP (cf.www.biap.orgon8thofMarch2016).Leusie’sstudy(2015)bringsuptheideaof“veryslighthearingloss”or“subclinicalhearingloss”,agradeofhearinglossbeingbetween15and25dB,fromwhichitwouldbeappropriatetotakeaction.Cf.p123-124.

13

Table2–Variabilityofreferencevaluesinhearingimpairmentclassifications

WHO:WorldwideHealthOrganisation;ANSI:AmericanNationalStandardsInstitute;RNID:RoyalNationalInstituteofDeafand hard of hearing people; BSI: British Society of Audiology; NIDCD: National Institute of Deafness and otherCommunicationDisorders.

Source:Shield,2006The quantitativemeasure of hearing levels in dB, performed by the ear, nose and throatspecialist (ENT specialist) or the audiologist, doesn’t allow for a direct estimation of thehearing loss prevalence in the general population, as far as this measure occurs when aconsultation is effective (inotherswords, there is a long timebetween theoccurrenceofdisabling hearing loss and healthcare access and the needs for hearing aids cannot beappreciatedonlythroughhealthcareconsumption).Theestimationofhearinglossprevalencerelies in general on population studies and self-reported qualitative data. The ten-yearlyFrench survey ‘Handicap-Santé’ (i.e. ‘Impairment-Health’) 2008, carried-outby twoFrenchnational institutesofstatistics,theINSEEandtheDREES,andreleasedin2014,isthemaindeclarativeFrenchsurveyallowinganestimationofhearinglossprevalenceandanappraisalof auditive functional limitations (Haeusler, Mordier, 2014; Haeusler and al., 2014; InVS,2015)4.However,giventhatthedatawerecollectedin2008,itisadvisabletobringthemuptodate,onthebasisofafewhypothesesandonotherrecentdatasources,asfollows.

1.1.1 Estimationsofhearinglossprevalencein“Handicap-Santé”Frenchsurvey2008Followingthe“Handicap-Santé”survey2008,hearingimpairmentisrecognisedeitherthroughindividualstatementsofusinghearingaidsorstatementsofaneedforhearingaidequipment.Inthisway,1,112,000peoplewerehearingaidowners in2008,whereas2,043,000peopledeclared a need for hearing aid equipment (being 35% of the equipment for the wholepopulationeligibleforhearingaids).Thispopulationrepresentedmorethan3millionpeopleaffectedbyalevelofhearinglosssignificantlydamagingtheirhealthstatus(table3).

4 Data are gathered from several surveys, of which the latest in France is the “Handicap-Santé” survey,implementedin2008.EstimatedstatisticsreportedbyHaeuslerandMordier(2014)relyonapanelsampleof28,500peopleandareextrapolatedtotheFrenchwholepopulation.EstimatedstatisticsreportedbyHaeuslerandal.(2014)arebasedonqualitativestatementsof30,000peopleinordinaryhouseholdsand9,000peopleininstitutions.

14

Table3–Numberofpeoplewhoarehearingaidusersordeclaringaneedforhearingaidsin2008

Source:DREES,2014

Moreover,thenumberofpeopledeclaringatleastonehearingimpairmentrisestomorethan7million–being11.2%oftheFrenchpopulation–providedthateverytypeofdisability isincludedinthesurvey(table4).Therefore,fromdeductionsbasedonthedataintable3andtable4,therateofequipmentrelativetodisablinghearingpeopleiscloseto15.8%in2008.

Table4–Numberofpeopledeclaringhearingimpairments

Source:DREES,2014

In the 2008 survey, disabling hearing, on one hand, is estimated directly by ‘hearingimpairment’(hearingaidsusers/declaredneedforahearingaid,hearingdisability)and,ontheotherhand,isassessedindirectlyby‘auditivefunctionallimitations’(forinstance,difficultytohearinaconversationwithseveralparticipants).Theprevalencedataarethenreckonedbytheauthorsonthisdoublesource(hearingimpairmentandauditivefunctionallimitations).Auditive functional limitations (AFL) are classified into four levels of severity in order toidentifytheminthesurvey(table5).

Table5–Referencegroupsofseverityforauditivefunctionallimitations(AFL)

Source:DREES,2014

Are you a hearing aids user ? Number of people % of total population

Yes 1 112 000 1.8%No, but I would need to use them 2 043 000 3.2%

No and I don't need them 59 875 000 94.9%Doesn't know, withdraws from answer 54 000 0.1%

Total population 63 084 000 100%

Hearing loss : do you have some hearing troubles ? (hard of hearing, tinnitus). If yes, which ones ?

Number of people

% of the total population

Deafness 182 000 0.3%Hard of hearing 1 062 000 1.7%Single-sided deafness 974 000 1.5%Other hearing loss but neither hard of hearing, nor deaf 3 153 000 0,05Other hearing trouble (tinnitus, buzzing, ringing in the ears…) 2 012 000 3.2%At least one hearing impairment 7 056 000 11.2%

Level of AFL Rule for findings

Very severe or totalCannot hear at all a conversation with several participants and declares him/herself to bedeaf (single-sided or double-sided) or hard of hearing

SevereHas a lot of difficulties to hear a conversation with several participants or cannot hear atall a conversation with several people and declares a hearing impairment other thandeafness (single-sided or double-sided) or hard of hearing

Moderate

Has some difficulties to hear a conversation with several participants or being a personequipped with hearing aids and able to follow a conversation without any difficulty orbeing a person hard of hearing or being a person single-sided deaf having declared aneed for hearing aids and following a conversation without any difficulty

SlightHas some difficulties to hear a conversation, but hasn't a declared hearing impairment orhasn't difficulties to hear a conversation and declares a hearing impairment such as tinnitusor ringing in the ears and doesn't use hearing aids

15

In2008,10millionpeoplewereaffectedbyAFL:thiswas16.1%ofthemainpopulation.ModeratetosevereAFL(threelevelsofseverityhigher)affect5.4millionpeople(8.6%ofthegeneralpopulation)and16%ofthemhaveasocialrecognitionofinvalidityordisabilityfortheir impairment (amongst people younger than 60 years). Among this social recognitiongroup,only2%arefoundinaninstitution(whereas10%ofpeoplewithverysevereortotalAFLliveinaninstitution)5.

Table6–Wholeprevalenceofauditivefunctionallimitations(AFL)duetohearinglossinFrance

Source:DREES,2014

TheoverallAFLconcern15.9%ofpeoplelivingathome,18%ofpeoplelivingininstitutionsfordisabledpersonsand42%ofpeoplelivingininstitutionsfortheelderly6.Inotherwords,peoplelivingininstitutionsaremorefrequentlyaffectedbyAFL.

1.1.2 Estimateddataforhearinglossprevalencein2015TheEurotrakdata2015releasedbytheEHIMA(EuropeanHearingInstrumentManufacturersAssociation)arebasedonaqualitativesurveyrelyingonarepresentativesampleof14,824French people. Hearing loss prevalence was stated to be around 9.3% of the generalpopulation(11.4%forpeopleolderthan18),andthisestimationhasbeensteadysince2009(2009:10.4%;2012:9.4%)7.

5AsunderlinedbytheDREES(Haeuslerandal.,2014),the“Handicaps-Incapacités-Dépendances”(‘Impairments-Incapacities-Dependencies’) 1998 survey assessed 5.2 million people affected by moderate to total hearingdifficulties, including303,000people concernedbyvery severe to totalAFL.Theseestimationsappear tobesteadyovertime,despitesomedifferencesintheassessmentmethod.6Thus,36.2%ofpeople in institutionsareaffectedbyslight tototalAFL.However, theDREESconsiders thatthereisprobablyanunderstatementofhearinglossamongtheelderlyininstitutions,becausehearinglossmightbejudgedas“normal”inrelationtootherimpairmentswhicharelikelytobemoremarked(Haeuslerandal.,2014,p.20).7Since2009theEHIMAassociationhasconductedatriennialsurveyintothemajorEuropeanmarkets(France,Germany,UnitedKingdom),whichhasextendedsince2012toSwitzerland,Denmark,NorwayandItalyaswellas to Japan.Themethodology for thesurveyreproducesthatofoneof theAmericanmodels,Marketrak. Itsconception, design and conduction are operated by a Swiss company (Anovum). Thus, because of a similarmethodologyforsurveysonsignificantpanelsofthenationalpopulation(onaverage14,000peopleinsamples),thedataallowsomeinternationalcomparisons.Moreover,itshouldbeunderlinedthattheseEHIMAdataareputintoperspectiveintheDREESreport2014andareconsistentwithFrenchdatareleasedinnationalsurveys.

Auditive limitation scale Number Confidence interval 95% %

Not any problem* 52 931 000 52438000-53424000 82,50%Slight 4 730 000 4471000-4989000 8%Moderate 3 474 000 3264000-3684000 5,90%Severe 1 600 000 1477000-1723000 2,70%Profound or total 359 000 311000-406000 0,60%Whole population 63 094 000 100%Total with auditive limitations 10 163 000 9822000-10503000 16,10%

Including moderate to profound 5 433 000 5190000-5675000 8,61%

Field : People living at home or in institutionSources : Disability-health survey 2008 ('enquête Handicap-Santé 2008')*including 1 353 000 people not able to answer the question about conversation (young people or having heavy impairments)

16

Chart1–PrevalenceofhearinglossinFrance2009,2012and2015(Eurotrak2015)

Source:EHIMA,2015

In the last section of this study (cf. section 2.2), an estimation of the 2014 hearing lossprevalencebyadultagegroupwillbecarriedoutonthebasisofINSEEdemographicdataandhearing loss rates available in the 1998 survey “Handicap-Incapacité-Dépendance”(‘Impairment–Disability–Dependency’).Theserateswerealsoconsideredassteadyovertime.

1.1.3 MainfeaturesofthepopulationaffectedbyauditivefunctionallimitationsAFLconcernedmorementhanwomen(17.2%and15.1%),andarederivedfromprofessionalstatus(exposuretonoisyenvironments)orleisurehabits(soundinjuryduetoloudmusicorheadphones).InthegroupofmoderatetototalAFL,thegapbetweenmenandwomenwasmorepronounced(10,4%and7%)8.Thisgapappearedfromtheageof40years(whereasitappearedatanageof50yearsinthe1998survey).ThelinkbetweentheprevalenceofAFLandageisveryclose:10%ofpeopleaged50yearsandoverwereaffectedbymoderatetototalAFL,asshowninchart2.8Thisestimationisstandardisedbyage,meaningthatitreliesonthehypothesisofasimilarstructureofmaleandfemalepopulationsbyagegroup.

2,1%

4,6%

6,4%

6,4%

10,7%

14,8%

21,3%

31,3%

12,7%

10,4%

1,6%

3,2%

4,8%

5,5%

8,8%

12,6%

18,2%

33,7%

11,5%

9,4%

1,7%

3,2%

4,9%

5,5%

7,9%

12,3%

18,0%

33,0%

11,4%

9,3%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

<=14

15-24

25-34

35-44

45-54

55-64

65-74

74+

Total 18+

Total

EuroTrak 2015 Base: 14'824

EuroTrak 2012 Base: 15'430

EuroTrak 2009 Base: 15'545

17

Chart2–Prevalenceofauditivefunctionallimitationsbyageandseverity

Interpretation:“moinsde10ans”:youngerthan10yearsold;“entre10et19ans”:agerangingbetween10and19years–

“LFAlégères”:slightAFL;“LFAmoyennes”:moderateAFL;“LFAgraves”:severeAFL;“LFAtrèsgravesoutotales”:veryseveretototalAFL

Source:DREES,2014NotonlydoestheprevalenceofAFLincreasewithage,butfrom60yearsonwardstherelativesizeofmoderatetototalAFLovertakesslightAFL:59%ofpeoplesufferingfrommoderatetototalAFLwereaged60yearsandolder9.Moreover,startingfrom80years,AFL–alllevelsofseverityinclusive–affectsmorethanoneoutofeverytwoindividuals.IftheageofoccurrenceforveryseveretototalAFLisalwaysknown,itremainsunknowninthegeneralcaseforthegroupofmoderatetototalAFL,aswellasthecausesofhearingloss,whicharenotspecifiedinmostcases.Anadvancedage is likely tobeassociatedwithmoredifficultieswithsocialintegration.As regards the professional category (actual or former occupation), the prevalence ofmoderate to total AFL is variable: workers and farmers weremore affected (+13%) thancraftspeople, shopkeepers and company heads (+9%) or senior managers (+10%).Nevertheless, it isn’t possible to interpret the direction of causality (impact of AFL onoccupationorimpactofoccupationonAFLoccurrence,exceptforfarmersforwhomanexcessofriskduetoworkingconditionsisdemonstrated)10.ThepresenceofAFLseemstohaveanimpact on qualification level or job occupation (InVS, 2015). However, job rates andunemploymentratesaresimilartonationalaveragerates,exceptwhenAFLisverysevereortotal.Moreover, for theworkingpopulation, the search formultivariatedemographic andsocio-economicfactorslikelytoexplaintheprevalenceofmoderatetototalAFLonlybringsouttheage,thesexandthelevelofqualification(particularlywhenthequalificationishigherthanabachelor’sdegree)11.

9Thisstudymostoftenfocusesontheelderlycategory,giventhegreaterseverityofhearingtroublesandthesignificantsizeofthispopulationinhearinglossprevalence.10Odds-ratio1.49*(1.08-2.06):allageandsexbeingequal,thelikelihoodofbeingaffectedbymoderatetototalAFLforaworkerorafarmeris1.5timesgreaterthanformanagersandself-employedprofessionals.11Cf.Haeuslerandal.(2014),p.22andfollowing.

18

Compensationofhearinglossleadstohearingaidequipment(eventocochlearimplantsinsomeseverecases).However,therateofpeoplebeingequippedissubstantiallylowerthantherateofprevalenceformoderatetototalAFL.Itisconvenienttoanalysethemaintriggersofaccesstohearingaids,inordertolaterquestiontheeconomicimpactofhearingloss.

1.2 AccesstohearingaidsinFrance:anoverviewHearing aids (“audioprothèses”) are a device allowing thewearer to receive, process andamplifysounds,whichhavetobeadaptedtotheuser’sabilityofunderstanding(perception)andtolerance.Thus,theyareamedicaldeviceforindividualuse.In order to highlight some approximations relating to the expenditure of the hearing aidsector,totheaveragepriceofapieceofequipmentandtohearingaidaccess,severaldatasourceshavebeencross-referenced.Moreover,therulesforsocialfinancingofhearingaidsarefeatured,wherepublicandprivateinsurancecoverageisassociatedwithalargenetout-of-pocketexpenseforadultHAsusers.Finally,theprovisionoftheequipment,combiningthedeviceandtheservice,isaddressedinitsspecificity.

1.2.1 PublicandprivatehearingaidsexpenditureinFranceHearingaidexpenditureisneitherdirectlyestimated,noratleastreleasedinpublishedFrenchhealthaccountsorintheopendatabase‘Eco-santéOCDE’.Indeed,theexpenditureforthisitemiscompriseswithintheoverallrangeofprosthesis(includinghearingaids,orthopaedicbracesandvehiclesforimpairedpersons)12.Hence,anestimationisproposedonthebasisofsomeavailabletrenddata,andthentheexpenditureissplitupintobothavolumeeffect–dependingonthenumberofhearingaidusers–andanaveragepriceeffect.

1.2.1.1 OverallhearingaidsexpenditureOverallhearingaidexpenditurerangedaroundonebillioneurosin2015,anestimationbasedonthepreviousdatacombinedwiththegrowthrateofsales,aswellasthefiguresintheIGF-IGASreport(2015)13.Estimationoftheoverallexpenditurefor2011In2011,overallhearingaidexpenditurewasestimatedtobearound800millioneurosbythe“HautConseilpour l’avenirde l’assurancemaladie” (‘HighCouncil for theFutureofHealthInsurance’)HCAAM(2013b)andtheCourtofAccounts(2013)14,with:

- 114 million euros funded by National Health Insurance (“Assurance maladieobligatoire”,AMO)(around14%oftheoverallexpenditure);

12AdifficultywhichisunderlinedbytheCourtofAccounts(2013).Asforthefieldof‘othermedicaldevices’forindividualuse,itdepicts80000differentproducts(CourtofAccounts,2014).13IGF:GeneralInspectionofFinances.Cf.volume2,form8,p.59.14Cf.p.395,bydeductingoptics.

19

- 246millioneurosfundedbycomplementaryhealth insurances(“Assurancemaladiecomplémentaire”,AMC)(around31%oftheoverallexpenditure).

Socialexpenditurepresentedasustainedaverageannualgrowthratethatwassustainedatarateof11%between1997and2009(IGAS,2010).Estimationoftheoverallexpenditurefor2012In2012(IGAS,2014),overallhearingaidexpenditureroseto824millioneuros,including:

- areimbursableamountof169millioneuros(cf.infra);- a reimbursable amount of 112million euros coveredbyNationalHealth Insurance

(AMO)(abaserateforreimbursementof65.5%,andarealrateofreimbursementof13,6%);

- agrossout-of-pocketamount(includingcoverageofcomplementaryhealthinsuranceAMC)of711millioneuros.

Inadditiontotheseoverallestimates,theNationalHealthInsurancedata(database‘SNIIRAM)used by the French trade union of audiologists (UNSAF - “Union nationale des syndicatsd’audiprothésistes français”), andmembers of the National Union of Health Professionals(UNPS,“Unionnationaledesprofessionnelsdesanté”),enableustohighlightthedistributionbyageofthehearingaidexpenditurefor2012,thenestimatedtobe822877925euros15.This distribution illustrates the strong concentration of reimbursed social expenditure forpeopleaged54to95(chart3).

15Thegapbetweenestimations–ontheonehandIGAS(2014)andontheotherhandUNSAF(Godinho,2015a)– for 2012 data should be explained either by the different areas of inclusion for social expenditure in theSNIIRAMdatabase(anon-exhaustivefieldat100%dependingontheinclusionornotofthedifferenthealthcareinsurance funds) or else by the portion of hearing aid expenditure not presented for reimbursement. TheCompetitionsAuthorityassesstheamountofrevenuetobe927millioneurosinits2016publicnotice(withoutspecifyingayearofreference,whichwasprobably2014or2015).

20

Chart3–Distributionoftheitem“electronicdevicesforhearingloss”byageinSNIIRAMdatabase(2012)

Source:Sniiram–dataandchartUNSAF(2015).

Twoshortagesarevisibleinthisdistribution,interpretedbyUNSAFasthresholdeffectsduetocoveragerules:theendofspecificrightsforyoungerpeoplewhentheyreachtheageof20years;andtheendofeligibilitytocollectivecontracts,well-knowntobemoregenerous,fromtheageof65years(cf.infra).Thehighestexpenditureisobservableat81years(around31millioneuros).Thecumulatedexpenditureclearlybringsaboutdelayedaccesstohearingaids,regardingtheAFLprevalencedatareleasedbyDREES(Haeusleretal.,2014).Indeed,olderpeopleover65representthree-quartersoftheexpenditurewhereaspeopleover75comprisemorethanhalfoftheexpenditure(54%)16(chart4).

16AsforUNSAF(2015),thenoteworthycumulatedpercentagesare:3.1%<age20,9.1%<age50,24.9%<age65,45.9%<age75.

0 €

5 000 000 €

10 000 000 €

15 000 000 €

20 000 000 €

25 000 000 €

30 000 000 €

35 000 000 €

Estimationofexpenditure"electronicdevicesforhearingloss" (chapter3)in2012byage(registeredatthemomentofequipment)

Overallexpenditure=822877925€

21

Chart4–Cumulatedexpenditurebyage,onitem“electronicdeviceforhearingloss”in2012

Source:SNIIRAM–dataandchartUNSAF(2015).

Finally,themaindatarelatingtooverallhearingaidexpenditureareshownintable7.

Table7–Summarytable:overallhearingaidsexpenditureineurosdependingondatasources

Source:Authorsonbasisonavailabledata

1.2.1.2 EstimationsofthenumberofhearingaidusersEstimationsofthenumberofhearingaidusersinFrancevaryaccordingtotheextrapolateddataofsurveys(decennialsurvey‘HandicapSanté’2008;Alcimed/DSS,2011;biennialsurveyESPS2012;Eurotrak2015).

0€

100 000 000€

200 000 000€

300 000 000€

400 000 000€

500 000 000€

600 000 000€

700 000 000€

800 000 000€

900 000 000€0… 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 102

Cumulatedexpendituredependingonage(in%)

75 yearsandover:54%ofHAexpenditure65yearsandover:75%ofHAexpenditure

Year Source Overall HAs

expenditure in euros

AMO (National Health Insurance)

AMC (Complementary health insurances)

Gross OOP

2011 HCAAM (2013b) 800 million 114 million (14%) 246 million (31%)

2012 IGAS (2014) 824 million112 million

(13,6%)711 million

2012SNIIRAM (UNSAF

2015)822,877,925

2015 IGF-IGAS (2015) 1 billion

22

Estimationsofthe‘Handicap-Santé’survey2008Following the ‘Handicap-Santé’ survey of 2008 (Haeusler et al., 2014), in 2008 access tohearingaidsconcerned1,112,000people(1.8%ofthewholepopulation,giventhatonly20%ofpeopleaffectedbymoderatetototalAFLworehearingaid(s)–andweremorefrequentlywomen and senior executives, all sex and severity levels of hearing loss being equal)17 .However,therateofhearingaidownershadincreasedby7pointsbetween1998(13%)–theyearoftheprevioussurvey–and2008:thiscouldbeexplainedbyabetterqualityofhearingaidequipment.

Table8–HearingaidequipmentrateforpeopleaffectedbymoderatetototalAFL

Source:DREES,2014

Youngerpeopleagedunder20(37%)aremoreoftenequippedwithhearingaidsthanthoseaged75andover(32%against21%in1998),whichcanbeexplained,simultaneously,byabettersocialcoverageoftheformergroupandabetterresponsetoequipmentintermsofitseffectiveness(cf.infra).Also,itshouldbeunderlinedthat:

- Womenaremoreoftenequippedthanmenamongpeopleagedover60;- Seniorexecutivesaremoreoftenequippedthanworkers,alllevelsofseveritybeing

equal(theyaretwiceaslikelytobeequipped)andindependentofanyincomeeffect(notsignificantinthesurvey);

- Impairedpeoplearemoreoftenequippedthanotherpeopleintheagegroup60-74years,duetoFrenchsocialcoverageruleswhichdistinguishimpairmentandoldage(cf.infra);

- In the labour force, there is no significant difference between employed andunemployedpeople(despitethefactthatthelatterhavelowerincomes).

Asfarastheincomeeffectisnotperceptibleonhearingaidaccessinthesurvey,thisaccessseemstodependmorelargelyonasocio-psychologicaleffect(hearingaidsaremorediscreetfor women than for men), on a socio-cultural effect probably due to information (socio-economicclasseffect)andonthelevelofpublicand(aboveall)privatecoverage.EstimationsofAlcimed-DSS(2011)fortheyear2009TheAlcimed-DSSsurveyestablishedthefollowingobservations:

- 1.25millionFrenchpeoplearehearingaid(s)users(estimationbasedontradeuniondata),being31.7%ofthepopulationeligibleforhearingaids;

17Theratewouldbeof10.7%ifthewholeAFLhadbeentakenintoaccount.

Age Under 20 20-44 45-59 60-74 75 and over Overall

Moderate AFL 13% 8% 17% 31% 18,4%Severe AFL 9% 8% 20% 30% 21,8%

Very severe to total AFL 25% 19% 26% 41% 33,5%Moderate to total AFL 37% 14% 8% 15% 32% 20,4%

Moderate AFL 22% 28% 32% 41% 32%Severe AFL 35% 45% 51% 51% 47%

Very severe to total AFL 32% 51% 63% 49% 51%Moderate to total AFL 9% 26% 34% 38% 45% 37%

Equipment rate

Need for an equipment

23

- amonghardofhearingpeople(6,300,000people),halfwereeligibleforhearingaidequipment;

- hence, there isnotable roomfor improvementgiven the targetof3millionpeople(being1,75millionpeoplewhoneedatleastonehearingaid);

- the average age at first equipment is estimated to be 71, thus at a late age, as aconsequenceofadelayinthediagnosisfollowedbyadelayinaccess.Thegapbetweentheperceptionofadecline inhearingandthepurchaseofadevice isestimated inyears18.

EstimationsofthebiennialsurveyESPSfortheperiod1992-2012Thebiennialsurveys“Santéetprotectionsociale”ESPS(‘HealthandSocialWelfareSurvey’)showaremarkableevolutioninhearingaidaccessbetween1992and201219(table9):

Table9–Evolutionofthenumberofhearingaidsownersfrom1992to2012

Source:BiennialsurveyESPS,dataEco-SantéOCDE

(availableonlineFebruary2016).

18 According to Le Monde 29 September 2009, access to hearing aids requires “seven years of reflection”(estimation based on the ‘Ipsos’ survey, June 2009). The Eurotrak survey for France 2015 estimates morepreciselythat84%ofpeoplebeingequippedwaited justunder6yearsbeforeaccessingequipmentand43%waitedbetween3to6years.19 The ESPS survey collects data from a panel sample of 8000 ordinary households (20,000 people) and isconsideredasrepresentativeof97%oftheFrenchmetropolitanpopulation.

A B C D

Hearing aids

owners

Hearing aids

owners aged 65

and over

Inhabitants Hearing owners

In % of total

population

In % of total

population

Number Estimated number

1992 1,0 6,0 56 975 597 569 7561993 1,1 7,0 57 239 847 629 6381994 0,9 6,0 57 467 085 517 2041995 0,9 5,5 57 658 772 518 9291996 1,0 5,0 57 844 247 578 4421997 1,2 5,8 58 025 989 696 3121998 1,0 5,7 58 207 490 582 0751999 nd nd 58 397 788 nd2000 1,0 4,9 58 677 406 586 7742001 nd nd 59 062 385 nd2002 1,9 7,8 59 476 236 1 130 0482003 nd nd 59 893 870 nd2004 1,5 7,1 60 303 631 904 5542005 nd nd 60 734 343 nd2006 2,2 9,1 61 181 499 1 345 9932007 nd nd 61 597 486 nd2008 2,3 8,6 61 965 052 1 425 1962009 nd nd 62 615 472 nd2010 2,3 8,6 62 917 790 1 447 1092011 nd nd 63 223 158 nd2012 3,7 11,4 63 514 003 2 350 018

AAGR 6,8% 3,3% 0,5% 7,3%

Me

tro

po

lita

n

Fra

nce

24

- Theproportionofhearingaidusershas risen from1%to3.7%,namelyanaverageannualgrowthrateof6.8%;

- Theproportionofhearingaidusersolderthan65yearshasgrownfrom6%to11.4%,namelyanaverageannualgrowthrateof3.3%.Atthesametime,therateofthesepeopledeclaringhearingtroublerisesto23%;

- Takingintoaccounttheselatterobservations,theriseinaccesstohearingaidsappearstobepushedupwardsbypeopleyoungerthan65years,ratherthanbythoseover65,indicatingearlieraccesstohearingaids;

- Theestimatednumberofhearingaidusershasincreasedby7.3%perannumovertheentireperiod,growingfrom569,756peoplein1992to2,350,018peoplein2012.Thisaverageannualgrowthrateisduetoacombinationinthegrowingnumberofpeoplebeingequippedanddemographicgrowthof7.6%intheperiod2002to2012;

- In 2012, there is probably an overestimation in the number of hearing aid users’numbers (2.35 million people according to the survey). This presumption ofoverestimationisreinforcedwhencomparedtootheravailablerecentdata(cf.infratable18).Accordingtoourestimation,thenumberofhearingaidusersoughttobeabout1.8millionpeoplein2012.

EstimationsEurotrak2015TheEurotraksurveyestimatestherateofhearingaidaccessat34.1%ofthehearingimpairedpopulation in 2015 and shows also that older people aged over 65, affected by hearingimpairment, are equipped at 42% (23.2% for the age group 45-64 and 29.5% for peopleyoungerthan45years).

Chart5–Evolutionoftherateofhearingaidaccessrelativetohearinglossprevalence(2009,2012,2015)Eurotrakdata

Source:EHIMA,2015

70%ofpeoplebeingequippedhavegotabinauraldevice(bothears).Moreover,accessisasgreatashearinglossseverityissevere(chart6)20.

20Severity isassessedonthebasisofahearing loss level thatdependson:monauralorbinauralequipment,grade of hearing loss (moderate to severe), score on APHAB scale, and degree of difficulty to follow a

9,3% 9,4% 10,4%

3,2% 2,8% 3,1%

34,1% 30,4% 29,8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

EuroTrak 2015 EuroTrak 2012 EuroTrak 2009

Hearing impaired (stated) Adoption (% of population) Adoption (% of stated impaired)

25

Chart6–Rateofhearingaidsaccessrelativeonhearinglossseverity(Eurotrak)

Source:EHIMA,2015

ReferencevaluesAccordingtothevariabilityofestimations(cf.table10),itseemstoberelevanttotakeonanaccessraterangingbetween30%to35%ofthepopulationaffectedbydisablinghearingloss21.Reader’sattentionshouldbedrawnto themeaningof thedifferencebetweentherateofhearing loss prevalence and the rate of people being equipped with hearing aids: thisdifferencedoesn’tfitwiththepopulationthatwouldbebothnotequippedandabletobeequipped. For different reasons relative to feasibility of equipment, to the relevance of ahearingcompensation,topossibletherapeuticoptionsforseverecases(i.e.cochlearimplant),orelsetosocialandpsychologicalfactors(rejectionofhearingaids),theaccesstohearingaidsisforeseeableonlyforafractionofhearingimpairedpeople.Itisusuallyconsideredthatthepopulationeligibleforhearingaidequipmentrepresentshalfoftheimpairedpopulation.Thisreferencetarget,centralinthisreport,ishighlightedfurther(cf.1.2.2.3).

conversationinanoisybackgroundwithouthearingaidequipment.Thisestimationleadsto6groupsofidenticalsize(16,67%).21TheIGAS(2014)estimatesthenumberofimpairedpeopletobe7million,ofwhom15%areequipped.The“UFC-Quechoisir”(FrenchConsumersAssociation–periodical‘WhattoChoose’)(2015)estimatesthisnumberat6million,with25%equipped.These ratesofequipmentareamong the lowestvalues in thewholesetofsurveys.

13% 14% 31%

42% 49% 69%

87% 86% 69%

58% 51% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6

Hearing aid No Hearing aid

26

Table10–Summaryofestimatedratesofhearingaidsaccessintheliteratureandsurveys

Source:Authorsonbasisofdifferentsurveydata.

Anotherwaytoestimatethisrateofhearingaidaccessistobasenumbersonthequantityofdevicessold(accordingtothe“Syndicatnationaldel’industrieetdestechnologiesmédicales”SNITEM–‘NationalUnionofMedicalIndustryandTechnologies’)duringthelast6years(themedianlifespanforequipmentis6yearsaccordingtotheEurotraksurvey2015forFrance),andthentoconsidertheshareforbinauralequipment(70%,samesource).Thus,itispossibletoestimatethenumberofwearersofhearingaids,byassumingthatthedevicesboughtinthelastsixyearshaveasyettoberenewed,giving2,041,075hearingaidowners.Givenarateofhearinglossprevalenceof10%in2012,theaccessratewouldthenbeabout32,6%22.Hence,thisstudyisbasedonareferencerateforhearingaidaccessrangingbetween30to35%ofthehearingimpairedpopulation.

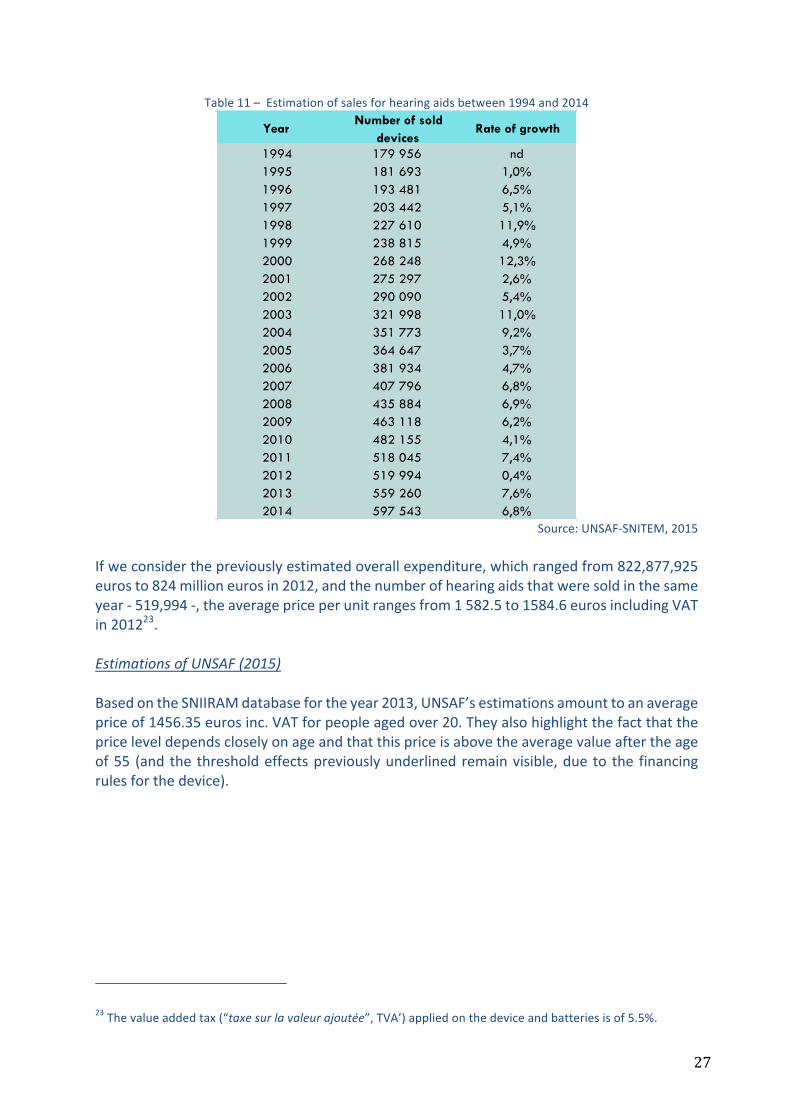

1.2.1.1 EstimationsoftheaveragepriceofahearingaidAccordingtotheSNITEM(2015),hearingaidsaleshavefollowedadynamictrendforthe20yearsfrom1994to2014:

22ItwouldbeinterestingtoestimateretrospectivelyandprospectivelytheprogressionoftherateofhearingaidsownersonthebasisofSNITEMsalesdata,onthedemographicstructureofpopulationandlifeexpectancy,ontherateofdevicerenewal(medianof6years)andtherateofnewpurchasersandonthebinauralrateofequipment.However,thisestimationwouldbedependentonseveralassumptions(stabilityofdevicedurationandof rateofbinauralequipmentand, for the forecasting, stabilityofaverageannualgrowth rate for sales,stabilityoftherenewaltimeoccurrence,stabilityoftherateofdiffusionrelatedtoacceptance,forecastofthenoiseexposure impact for younggenerations). This longitudinal analysiswould require thedesignof severalscenariosthatgoesbeyondthescopeofthisstudy.

Year Survey and HL criteria Access rate to equipmentPrevalence rate of

hearing loss

2008Handicap Santé (disabling

hearing loss)15,8% 11,2%

2008Handicap santé (moderate to

total AFL)20,4% 8,6%

2008 ESPS 23,0% 10,0%

2009 Eurotrak 29,8% 10,4%

2009 Alcimed-DSS 31,7% 10%*

2010 ESPS 23,0% 10%*

2012 Eurotrak 30,4% 9,4%

2012 ESPS 37,0% 10%*

2015 Eurotrak 34,1% 9,3%

* Assumption

27

Table11–Estimationofsalesforhearingaidsbetween1994and2014

Source:UNSAF-SNITEM,2015

Ifweconsiderthepreviouslyestimatedoverallexpenditure,whichrangedfrom822,877,925eurosto824millioneurosin2012,andthenumberofhearingaidsthatweresoldinthesameyear-519,994-,theaveragepriceperunitrangesfrom1582.5to1584.6eurosincludingVATin201223.EstimationsofUNSAF(2015)BasedontheSNIIRAMdatabasefortheyear2013,UNSAF’sestimationsamounttoanaveragepriceof1456.35eurosinc.VATforpeopleagedover20.Theyalsohighlightthefactthatthepriceleveldependscloselyonageandthatthispriceisabovetheaveragevalueaftertheageof55 (and the thresholdeffectspreviouslyunderlinedremainvisible,due to the financingrulesforthedevice).

23Thevalueaddedtax(“taxesurlavaleurajoutée”,TVA’)appliedonthedeviceandbatteriesisof5.5%.

YearNumber of sold

devicesRate of growth

1994 179 956 nd1995 181 693 1,0%1996 193 481 6,5%1997 203 442 5,1%1998 227 610 11,9%1999 238 815 4,9%2000 268 248 12,3%2001 275 297 2,6%2002 290 090 5,4%2003 321 998 11,0%2004 351 773 9,2%2005 364 647 3,7%2006 381 934 4,7%2007 407 796 6,8%2008 435 884 6,9%2009 463 118 6,2%2010 482 155 4,1%2011 518 045 7,4%2012 519 994 0,4%2013 559 260 7,6%2014 597 543 6,8%

28

Chart7–Averagepriceasafunctionofageinin2013

Source:Sniiram–dataandchartUNSAF(2015).

Thedistributionofaveragepricesbyageshowsthatahearingaidismoreexpensiveforolderpeopleaged65andover(1,560.83eurosinc.VAT),thenforyoungerpeopleunder20yearsold(1,503.60eurosVAT)andforpeopleagedbetween20and64(1,349.51eurosVAT).

Table12–AverageVATpriceforahearingaidbyagegroupsin2013

Source:SNIIRAM–dataandtableUNSAF(2015).

OtherestimationsinthegreyliteratureThegreyliteraturecapturesingeneralanaverageunitpriceof1,600eurosinc.VATin2009(Alcimed-DSS,2011),or1,550eurosinc.VATin2014(Autoritédelaconcurrence,2016)or1,535eurosinc.VATin2011(estimationoftheNationalHealthInsuranceCNAMTSthathasbeenusedbytheCourtofAccounts(Courdescomptes,2013),theIGAS(2014)andtheIGF-IGAS(2015)),beingaround3,070eurosinc.VATforbothears24.

24Theseestimationsdon’tincludethetechnicalcostofmaintenance(batteriesetc.).

0

2 000

4 000

6 000

8 000

10 000

12 000

0 €

200 €

400 €

600 €

800 €

1 000 €

1 200 €

1 400 €

1 600 €

1 800 €

1051009590858075706560555045403530252015105

Qua

ntity

of d

evic

es

Aver

age

pric

e

Age

Year 2013 / Source : Sniiram

Average price (scale on the right) Quantity of devices (scale on the left)

Age Under 20 20-64 Over 64Overall

population

Average price 1,503.60€ 1,349.83€ 1,560.83€ 1,465.37€

Number of people 8,064 59,458 218,271 285,793

Number of devices 16,054 100,312 339,435 455,801

Binaural Rate 99.08% 68.71% 55.51% 59.49%

29

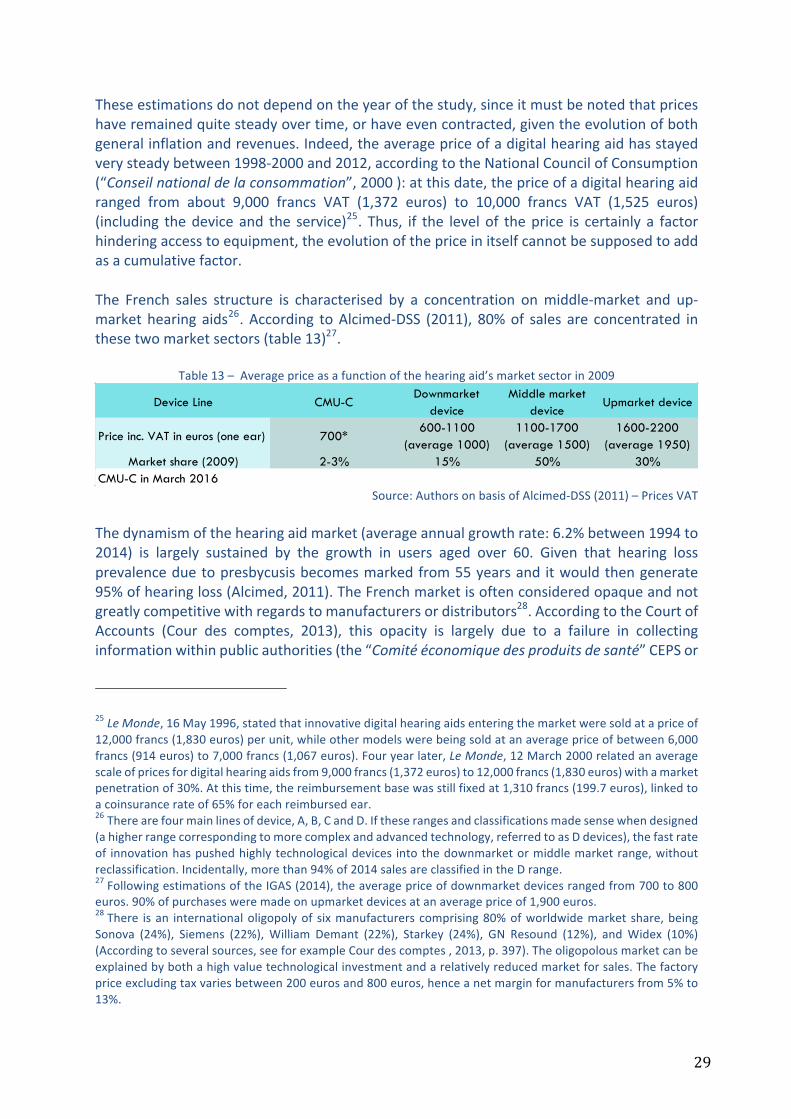

Theseestimationsdonotdependontheyearofthestudy,sinceitmustbenotedthatpriceshaveremainedquitesteadyovertime,orhaveevencontracted,giventheevolutionofbothgeneralinflationandrevenues.Indeed,theaveragepriceofadigitalhearingaidhasstayedverysteadybetween1998-2000and2012,accordingtotheNationalCouncilofConsumption(“Conseilnationaldelaconsommation”,2000):atthisdate,thepriceofadigitalhearingaidranged from about 9,000 francs VAT (1,372 euros) to 10,000 francs VAT (1,525 euros)(including thedevice and the service)25. Thus, if the level of theprice is certainly a factorhinderingaccesstoequipment,theevolutionofthepriceinitselfcannotbesupposedtoaddasacumulativefactor.The French sales structure is characterised by a concentration onmiddle-market and up-markethearing aids26.According toAlcimed-DSS (2011), 80%of sales are concentrated inthesetwomarketsectors(table13)27.

Table13–Averagepriceasafunctionofthehearingaid’smarketsectorin2009

Source:AuthorsonbasisofAlcimed-DSS(2011)–PricesVAT

Thedynamismofthehearingaidmarket(averageannualgrowthrate:6.2%between1994to2014) is largely sustained by the growth in users aged over 60. Given that hearing lossprevalenceduetopresbycusisbecomesmarkedfrom55yearsand itwouldthengenerate95%ofhearingloss(Alcimed,2011).TheFrenchmarketisoftenconsideredopaqueandnotgreatlycompetitivewithregardstomanufacturersordistributors28.AccordingtotheCourtofAccounts (Cour des comptes, 2013), this opacity is largely due to a failure in collectinginformationwithinpublicauthorities(the“Comitééconomiquedesproduitsdesanté”CEPSor

25LeMonde,16May1996,statedthatinnovativedigitalhearingaidsenteringthemarketweresoldatapriceof12,000francs(1,830euros)perunit,whileothermodelswerebeingsoldatanaveragepriceofbetween6,000francs(914euros)to7,000francs(1,067euros).Fouryearlater,LeMonde,12March2000relatedanaveragescaleofpricesfordigitalhearingaidsfrom9,000francs(1,372euros)to12,000francs(1,830euros)withamarketpenetrationof30%.Atthistime,thereimbursementbasewasstillfixedat1,310francs(199.7euros),linkedtoacoinsurancerateof65%foreachreimbursedear.26Therearefourmainlinesofdevice,A,B,CandD.Iftheserangesandclassificationsmadesensewhendesigned(ahigherrangecorrespondingtomorecomplexandadvancedtechnology,referredtoasDdevices),thefastrateof innovationhaspushedhighlytechnologicaldevices intothedownmarketormiddlemarketrange,withoutreclassification.Incidentally,morethan94%of2014salesareclassifiedintheDrange.27FollowingestimationsoftheIGAS(2014),theaveragepriceofdownmarketdevicesrangedfrom700to800euros.90%ofpurchasesweremadeonupmarketdevicesatanaveragepriceof1,900euros.28There isan internationaloligopolyof sixmanufacturerscomprising80%ofworldwidemarket share,beingSonova (24%), Siemens (22%),William Demant (22%), Starkey (24%), GN Resound (12%), andWidex (10%)(Accordingtoseveralsources,seeforexampleCourdescomptes,2013,p.397).Theoligopolousmarketcanbeexplainedbybothahighvaluetechnologicalinvestmentandarelativelyreducedmarketforsales.Thefactorypriceexcludingtaxvariesbetween200eurosand800euros,henceanetmarginformanufacturersfrom5%to13%.

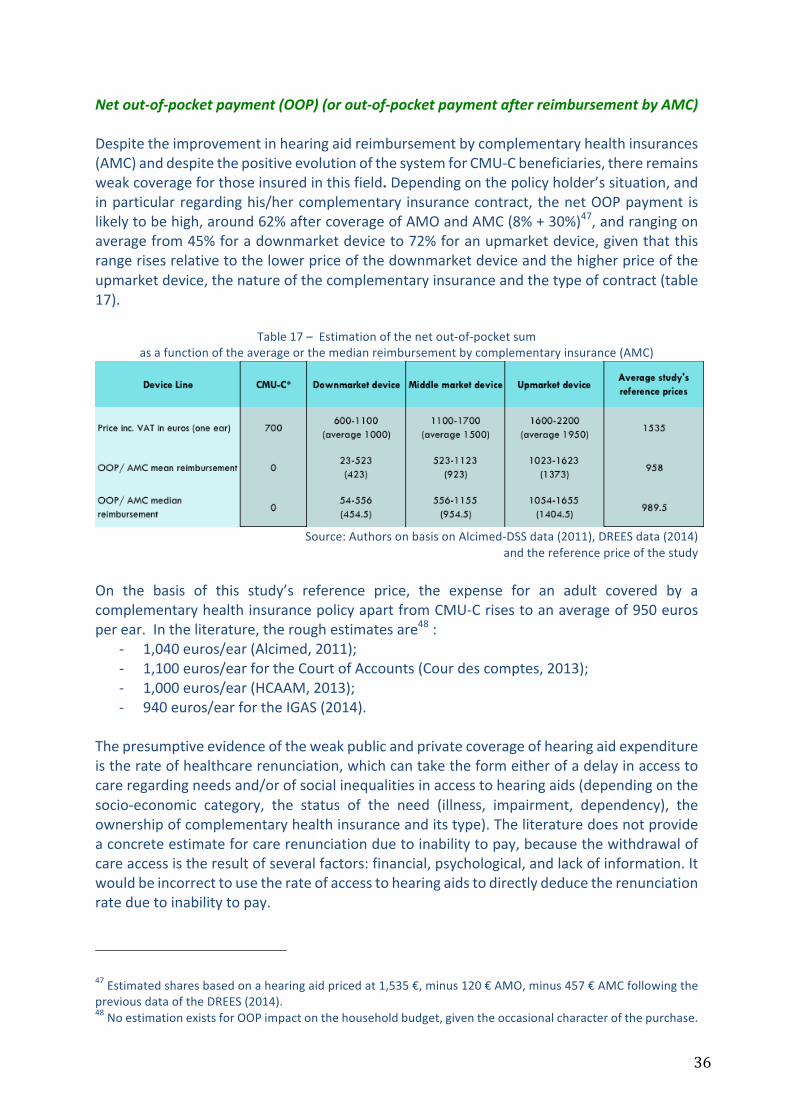

Device Line CMU-CDownmarket

deviceMiddle market

deviceUpmarket device

Price inc. VAT in euros (one ear) 700*600-1100

(average 1000)1100-1700

(average 1500)1600-2200

(average 1950)Market share (2009) 2-3% 15% 50% 30%

CMU-C in March 2016

30

‘Economiccommitteeofhealthproducts’itselfnothavingavailablesalesstatisticsformedicaldevices).Thetopicsofcompetition,marketcharacteristics,productdifferentiationstrategies,hearingaiddistributionnetworksand sector regulationsgobeyond the frameworkof thisstudybuttheinterestedreadershouldrefertorecentstudiesbytheCourtofAccounts(Courdescomptes,2013and2014),bytheDirectorateofSocialSecurity(“Directiondelasécuritésociale”-DSS,2011),theIGAS(2013and2014),theIGF-IGAS(2015),andbytheCompetitionAuthority(Autoritédelaconcurrence,2016)29.

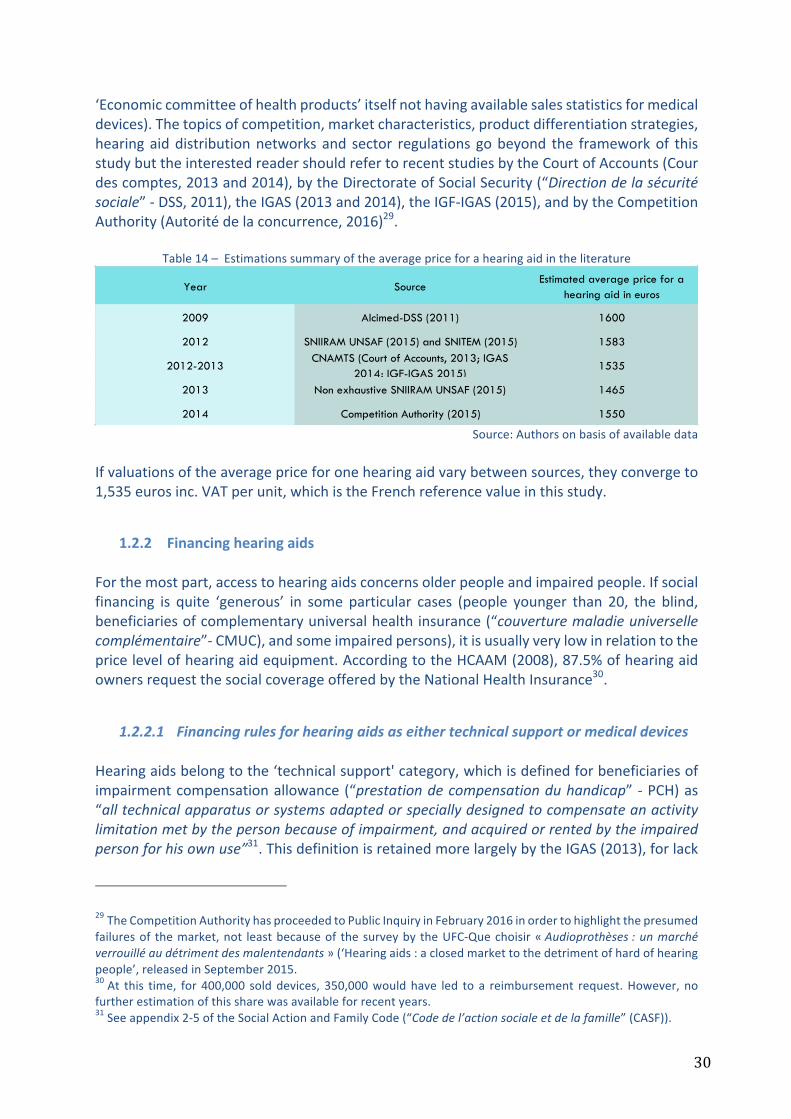

Table14–Estimationssummaryoftheaveragepriceforahearingaidintheliterature

Source:Authorsonbasisofavailabledata

Ifvaluationsoftheaveragepriceforonehearingaidvarybetweensources,theyconvergeto1,535eurosinc.VATperunit,whichistheFrenchreferencevalueinthisstudy.

1.2.2 FinancinghearingaidsForthemostpart,accesstohearingaidsconcernsolderpeopleandimpairedpeople.Ifsocialfinancing is quite ‘generous’ in some particular cases (people younger than 20, the blind,beneficiariesofcomplementaryuniversalhealthinsurance(“couverturemaladieuniversellecomplémentaire”-CMUC),andsomeimpairedpersons),itisusuallyverylowinrelationtothepricelevelofhearingaidequipment.AccordingtotheHCAAM(2008),87.5%ofhearingaidownersrequestthesocialcoverageofferedbytheNationalHealthInsurance30.

1.2.2.1 FinancingrulesforhearingaidsaseithertechnicalsupportormedicaldevicesHearingaidsbelongtothe‘technicalsupport'category,whichisdefinedforbeneficiariesofimpairmentcompensationallowance(“prestationdecompensationduhandicap”-PCH)as“alltechnicalapparatusorsystemsadaptedorspeciallydesignedtocompensateanactivitylimitationmetbythepersonbecauseofimpairment,andacquiredorrentedbytheimpairedpersonforhisownuse”31.ThisdefinitionisretainedmorelargelybytheIGAS(2013),forlack

29TheCompetitionAuthorityhasproceededtoPublicInquiryinFebruary2016inordertohighlightthepresumedfailuresof themarket,not leastbecauseof thesurveyby theUFC-Quechoisir«Audioprothèses:unmarchéverrouilléaudétrimentdesmalentendants»(‘Hearingaids:aclosedmarkettothedetrimentofhardofhearingpeople’,releasedinSeptember2015.30At this time, for 400,000 solddevices, 350,000wouldhave led to a reimbursement request.However, nofurtherestimationofthissharewasavailableforrecentyears.31Seeappendix2-5oftheSocialActionandFamilyCode(“Codedel’actionsocialeetdelafamille”(CASF)).

Year Source Estimated average price for a

hearing aid in euros

2009 Alcimed-DSS (2011) 1600

2012 SNIIRAM UNSAF (2015) and SNITEM (2015) 1583

2012-2013CNAMTS (Court of Accounts, 2013; IGAS

2014; IGF-IGAS 2015)1535

2013 Non exhaustive SNIIRAM UNSAF (2015) 1465

2014 Competition Authority (2015) 1550

31

of a similar definition for beneficiaries of the personalised autonomy subsidy (“allocationpersonnaliséed’autonomie”,APA).Suchapitfallisrevealing–asunderlinedbytheIGAS–ofthegreatconfusionsurroundingtherightsandwaitingperiodsinvolvedinfinancingtechnicalsupport,dependingonrecipients’classificationintoillness,impairmentoroldage(thisdifferentiationofneeds,rightsorstatus– illness, invalidity, impairment, dependency - is particular to France). This confusion isreinforcedbythemultiplefinancingbodiesincaseofimpairmentandbythevariationinrightsdependingontheareaofresidence.Furthermore, hearing aids are not only technical supports but are also medical devices(“dispositifsmédicaux”,DM),andthusrelatetohealthcare,andtothe listofreimbursableproducts and service provision (“Liste des produits et prestations remboursables” - LPPR)definedbytheNationalHealthInsurance32.However,registrationintheLPPRisnotlinkedtoanupperpricelimit(unlikemostmedicaldevices)andthegapbetweenpricesandtariffsisremarkablywide(CEPS,2015)33.Thejuxtapositionofdefinitions,publicbodiesandrightshasfinallyresultedinalackofmanagementoftheaccesstotechnicalsupports,tohighcostsduetoorganisationandtheriskoferrors,andtoinequalitiesbetweencustomerswhoselevelofinformationaboutaccessibilityvariesgreatly.

1.2.2.2 PublicandprivatefinancingrulesforhearingaidequipmentCoveragebytheNationalHealthInsuranceAsofFebruary2016, theNationalHealth Insurancecovers, for standardcases (i.e.peopleolderthan20yearsand/ornoblindnessimpairment34),60%oftheLPPRtariffforahearingaid,fixedat199.71euros,thatis119.83eurosperunit35.Thisreferencetariff includesnotonlythedeviceitself,butalsotheaccessories,theadaptationandprostheticeducationbythe

32ArticleL.5211-1ofthePublicHealthCodewhichimposesnorms,suchastheCEmarkbythemanufacturer(articleL.5211-3).33“Fixingaceilingpriceforsalesimplies,however,ifneedbe,theresolutionofthequestionofanysurchargebilledinreturnfor/againstservicesoraccessoriesexceedingthedefinitionofthereimbursableproductorservicespecifiedbythelist.Inparticular,thisisthecaseintheexternalprosthesisororthoticssectors,wherepatientsoughttoaskfor,andsuppliersoughttooffer,technicaloraestheticaccessories,butnotonlythat.Forexample,inthefieldofhearingaidsforveryyoungpeople,professionalsarguethatthegapbetweenpricesandtariffsallowsforpaymentforaudiologistswhoseinterventionisneededtoadapttheequipmentfortheirpatients,andcould,dependingonthecase,representagreatnumberofconsultationsforveryyoungpeopleormulti-impairedpersons. Indeed, the resulting out-of-pocket sum was mostly reimbursed either by the CMU-C, or bycomplementary insurancesandinothercasesbymeansofregionalor localassistancebodies,andwasoftenrequestedbyaudiologiststhemselves.Thedifficulty,eventheimpossibility,inthesesituationstodetermineaboundedpriceofsaleaccordingtorationalreferencesandexistingfinancepossibilitieshaveledtheCommitteetopostponethefixationofaceilingpriceforsalesforthesehearingaidsthatwouldbesuperiortothetariff”,CEPS(2015),p.142.34Intheseparticularcases,technicalsupportequipmentisreimbursedatacoinsurancerateof60%forpricesrangingbetween900and1,400euros,dependingonthedeviceclassification.Inthecaseofachronicdiseaseor‘long-term affliction’ (“Affection de longue durée”, ALD) or in the case of invalidity allowance, the rate ofreimbursementis100%oftheLPPRtariff.Cf.www.ameli.fraccessed24February2016.35Thereimbursementratedroppedfrom65%to60%in2011.

32

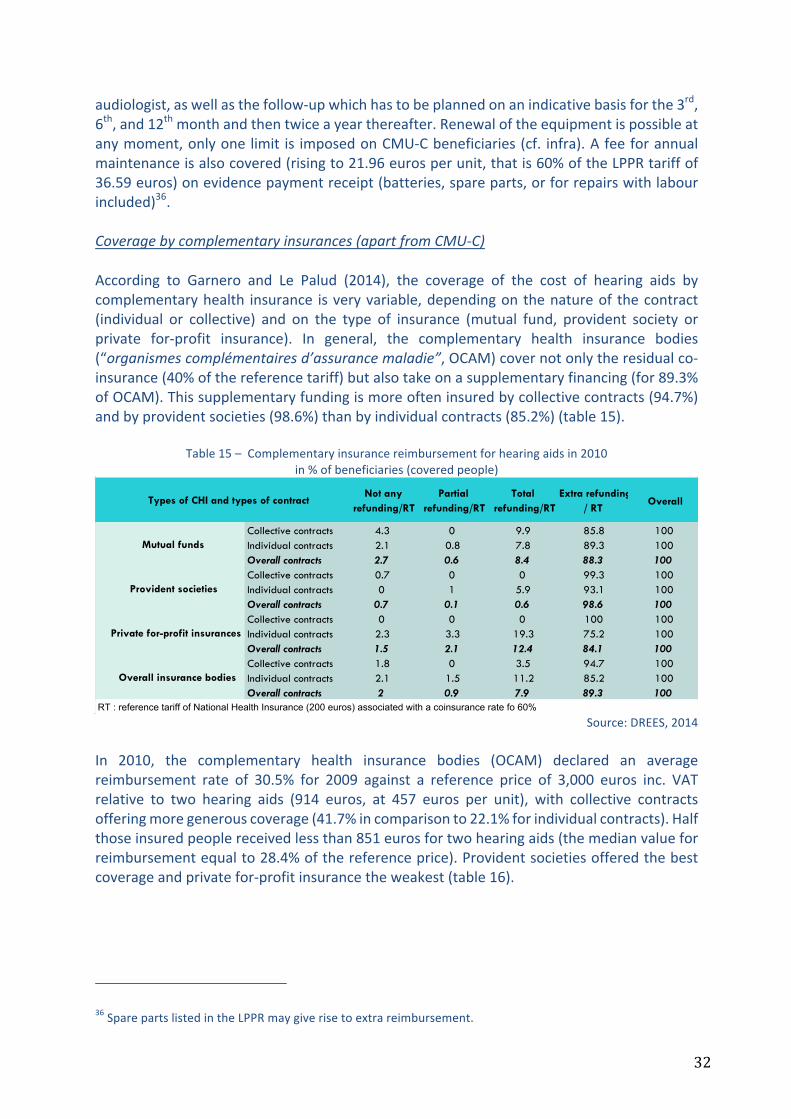

audiologist,aswellasthefollow-upwhichhastobeplannedonanindicativebasisforthe3rd,6th,and12thmonthandthentwiceayearthereafter.Renewaloftheequipmentispossibleatanymoment,onlyone limit is imposedonCMU-Cbeneficiaries(cf. infra).Afeeforannualmaintenanceisalsocovered(risingto21.96eurosperunit,thatis60%oftheLPPRtariffof36.59euros)onevidencepaymentreceipt(batteries,spareparts,orforrepairswithlabourincluded)36.Coveragebycomplementaryinsurances(apartfromCMU-C)According to Garnero and Le Palud (2014), the coverage of the cost of hearing aids bycomplementaryhealth insurance isveryvariable,dependingonthenatureof thecontract(individual or collective) and on the type of insurance (mutual fund, provident society orprivate for-profit insurance). In general, the complementary health insurance bodies(“organismescomplémentairesd’assurancemaladie”,OCAM)covernotonlytheresidualco-insurance(40%ofthereferencetariff)butalsotakeonasupplementaryfinancing(for89.3%ofOCAM).Thissupplementaryfundingismoreofteninsuredbycollectivecontracts(94.7%)andbyprovidentsocieties(98.6%)thanbyindividualcontracts(85.2%)(table15).

Table15–Complementaryinsurancereimbursementforhearingaidsin2010in%ofbeneficiaries(coveredpeople)

Source:DREES,2014

In 2010, the complementary health insurance bodies (OCAM) declared an averagereimbursement rate of 30.5% for 2009 against a reference price of 3,000 euros inc. VATrelative to two hearing aids (914 euros, at 457 euros per unit), with collective contractsofferingmoregenerouscoverage(41.7%incomparisonto22.1%forindividualcontracts).Halfthoseinsuredpeoplereceivedlessthan851eurosfortwohearingaids(themedianvalueforreimbursementequalto28.4%ofthereferenceprice).Providentsocietiesofferedthebestcoverageandprivatefor-profitinsurancetheweakest(table16).

36SparepartslistedintheLPPRmaygiverisetoextrareimbursement.

Not any refunding/RT

Partial refunding/RT

Total refunding/RT

Extra refunding / RT

Overall

Collective contracts 4.3 0 9.9 85.8 100Individual contracts 2.1 0.8 7.8 89.3 100Overall contracts 2.7 0.6 8.4 88.3 100Collective contracts 0.7 0 0 99.3 100Individual contracts 0 1 5.9 93.1 100Overall contracts 0.7 0.1 0.6 98.6 100Collective contracts 0 0 0 100 100Individual contracts 2.3 3.3 19.3 75.2 100Overall contracts 1.5 2.1 12.4 84.1 100Collective contracts 1.8 0 3.5 94.7 100Individual contracts 2.1 1.5 11.2 85.2 100Overall contracts 2 0.9 7.9 89.3 100

RT : reference tariff of National Health Insurance (200 euros) associated with a coinsurance rate fo 60%

Types of CHI and types of contract

Mutual funds

Provident societies

Private for-profit insurances

Overall insurance bodies

33

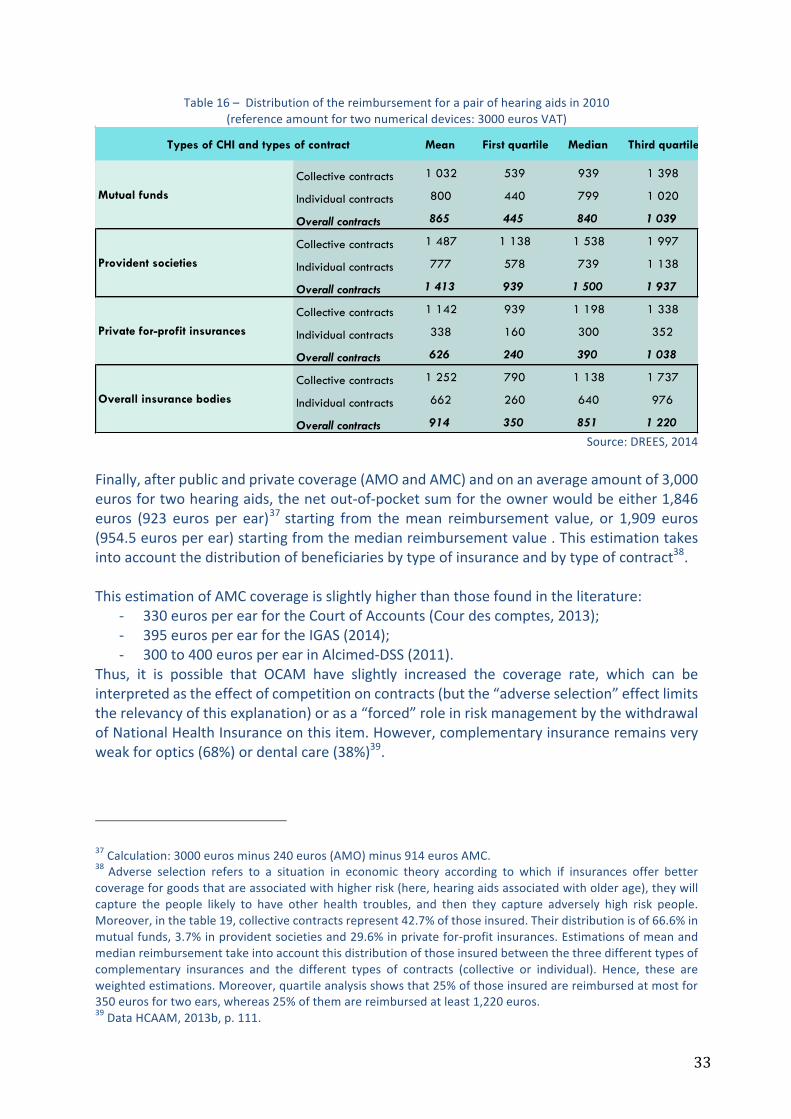

Table16–Distributionofthereimbursementforapairofhearingaidsin2010(referenceamountfortwonumericaldevices:3000eurosVAT)

Source:DREES,2014

Finally,afterpublicandprivatecoverage(AMOandAMC)andonanaverageamountof3,000eurosfortwohearingaids,thenetout-of-pocketsumfortheownerwouldbeeither1,846euros (923 euros per ear)37starting from themean reimbursement value, or 1,909 euros(954.5eurosperear)startingfromthemedianreimbursementvalue.Thisestimationtakesintoaccountthedistributionofbeneficiariesbytypeofinsuranceandbytypeofcontract38.ThisestimationofAMCcoverageisslightlyhigherthanthosefoundintheliterature:

- 330eurosperearfortheCourtofAccounts(Courdescomptes,2013);- 395eurosperearfortheIGAS(2014);- 300to400eurosperearinAlcimed-DSS(2011).

Thus, it is possible that OCAM have slightly increased the coverage rate, which can beinterpretedastheeffectofcompetitiononcontracts(butthe“adverseselection”effectlimitstherelevancyofthisexplanation)orasa“forced”roleinriskmanagementbythewithdrawalofNationalHealthInsuranceonthisitem.However,complementaryinsuranceremainsveryweakforoptics(68%)ordentalcare(38%)39.

37Calculation:3000eurosminus240euros(AMO)minus914eurosAMC.38 Adverse selection refers to a situation in economic theory according to which if insurances offer bettercoverageforgoodsthatareassociatedwithhigherrisk(here,hearingaidsassociatedwitholderage),theywillcapture the people likely to have other health troubles, and then they capture adversely high risk people.Moreover,inthetable19,collectivecontractsrepresent42.7%ofthoseinsured.Theirdistributionisof66.6%inmutualfunds,3.7%inprovidentsocietiesand29.6%inprivatefor-profitinsurances.Estimationsofmeanandmedianreimbursementtakeintoaccountthisdistributionofthoseinsuredbetweenthethreedifferenttypesofcomplementary insurances and the different types of contracts (collective or individual). Hence, these areweightedestimations.Moreover,quartileanalysisshowsthat25%ofthoseinsuredarereimbursedatmostfor350eurosfortwoears,whereas25%ofthemarereimbursedatleast1,220euros.39DataHCAAM,2013b,p.111.

Mean First quartile Median Third quartile

Collective contracts 1 032 539 939 1 398

Individual contracts 800 440 799 1 020

Overall contracts 865 445 840 1 039

Collective contracts 1 487 1 138 1 538 1 997

Individual contracts 777 578 739 1 138

Overall contracts 1 413 939 1 500 1 937

Collective contracts 1 142 939 1 198 1 338

Individual contracts 338 160 300 352

Overall contracts 626 240 390 1 038

Collective contracts 1 252 790 1 138 1 737

Individual contracts 662 260 640 976

Overall contracts 914 350 851 1 220

Types of CHI and types of contract

Mutual funds

Provident societies

Private for-profit insurances

Overall insurance bodies

34