finance and audit committee meeting - building changes 2015... · guests mark raker and megan...

TRANSCRIPT

Finance and Audit Committee

Meeting

Wednesday, April 15, 2015

Meeting Location: BC, 2nd floor conference room

4:00 – 5:30pm

Proposed meeting results

1. Finance & Audit Committee members have Executive Session with Auditor. 2. Committee has the opportunity to review and discuss Year End Financials.

Agenda

I. Auditor Report (Peterson Sullivan to join)……………...........................All (30 mins) Result: Committee has the opportunity to ask questions regarding the annual audit.

II. Review of Form 990………………………………………………….....…..All (45 mins) Result: Committee gains understanding of the contents of the 990.

III. Review of 2/28/15 Financial Statements…………………………………….All (5 mins)

Result: Committee gains understanding of Building Changes operations through financial reports.

IV. Review and Approve Minutes from 2/18/15 Finance and Audit Committee meeting…………………………………………………………..……………...All (5 min) Result: Committee members approve that last meeting’s minutes reflect what happened.

Please let Alice MW. know if you plan to join via phone in advance: Conference line: 877-594-8353, code 78904181

Next Meeting: June 17, 2015

BC Finance & Audit Committee Packet Pg. 1 of 77

Finance and Audit Committee

Meeting Minutes

Wednesday, February 18, 2015

4 – 5 PM

Board Attendance Brian Abeel, Barb Herr, Lori Kaiser, Cheryl DeBoise, Bob Davis, Arnaz Bharucha

Guests Mark Raker and Megan Hurley

Staff Attendance Tekle Bushen, Armilito Pangilinan, Alice Shobe

I. Executive Session with Auditor (Peterson Sullivan) Mark Raker and Megan Hurley joined the executive session of the meeting to discuss the annual audit of Building Changes’ finances.

II. Introduction to the Finance Committee for New Members

Committee members introduced themselves by giving short information about their job and experience working/volunteering in non-profit organizations.

III. Review and Approval of Minutes from 11/19/14 meeting The minutes from the 11/19/14 meeting, as written, having been reviewed, were approved unanimously.

IV. Year End Financials Armilito presented the Financial Statements for the period that ended December 31.Discussion ensued. Actions: a) Armilito will modify the discussion portion of the financial report to say that “Net of revenues over

expenses before grants is $161K.” b) Armilito and Alice will work on strategy on best way to share with the Board the Operational issues

that affect the financials. c) Lori and Armilito will make themselves available to individual Board members if s/he would like to

have a deeper understanding of Building Changes’ finances; in particular in trying to understand the Financial Dashboard.

d) The Committee will schedule discussion of the operating reserves in future meeting to answer the question, “What do we want to add or not add to the rainy day fund?”

Committee meeting adjourned at 5:05pm.

BC Finance & Audit Committee Packet Pg. 2 of 77

091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

FINANCIAL REPORT

DECEMBER 31, 2014

BC Finance & Audit Committee Packet Pg. 3 of 77

091665fs123114 Revised: 4/7/2015 8:37 AM mcp

C O N T E N T S

Page

INDEPENDENT AUDITORS' REPORT .................................................................................................... 1 and 2

FINANCIAL STATEMENTS

STATEMENTS OF FINANCIAL POSITION ............................................................................................................................... 3

STATEMENTS OF ACTIVITIES ...................................................................................................................................................... 4

STATEMENT OF FUNCTIONAL EXPENSES - 2014 .............................................................................................................. 5

STATEMENT OF FUNCTIONAL EXPENSES - 2013 .............................................................................................................. 6

STATEMENTS OF CASH FLOWS ................................................................................................................................................ 7

NOTES TO FINANCIAL STATEMENTS ........................................................................................................................... 8 - 16

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL

STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING

STANDARDS ......................................................................................................................................... 17 and 18

BC Finance & Audit Committee Packet Pg. 4 of 77

INDEPENDENT AUDITORS' REPORT

To the Board of Directors

Building Changes

Seattle, Washington

We have audited the accompanying financial statements of Building Changes, which comprise the

statement of financial position as of December 31, 2014, and the related statements of activities, functional

expenses, and cash flows for the year then ended, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with accounting principles generally accepted in the United States; this includes the design,

implementation, and maintenance of internal control relevant to the preparation and fair presentation of

financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with auditing standards generally accepted in the United States.

Those standards require that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in

the financial statements. The procedures selected depend on the auditor's judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or error.

In making those risk assessments, the auditor considers internal control relevant to the entity's preparation

and fair presentation of the financial statements in order to design audit procedures that are appropriate

in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's

internal control. Accordingly, we express no such opinion. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness of significant accounting estimates

made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our audit opinion.

BC Finance & Audit Committee Packet Pg. 5 of 77

2

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the

financial position of Building Changes as of December 31, 2014, and the changes in its net assets and its

cash flows for the year then ended in accordance with accounting principles generally accepted in the

United States.

Prior Period Financial Statements

The financial statements of Building Changes as of December 31, 2013, were audited by other auditors

whose report dated April 25, 2014, expressed an unmodified opinion.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated

________________________, on our consideration of internal control at Building Changes over financial

reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and

grant agreements and other matters. The purpose of that report is to describe the scope of our testing

of internal control over financial reporting and compliance and the results of that testing, and not to

provide an opinion on internal control over financial reporting or on compliance. That report is an

integral part of an audit performed in accordance with Government Auditing Standards in considering the

internal control at Building Changes over financial reporting and compliance.

____________________________

BC Finance & Audit Committee Packet Pg. 6 of 77

See Notes to Financial Statements

3 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

STATEMENTS OF FINANCIAL POSITION

December 31, 2014 and 2013

ASSETS 2014 2013

Current Assets

Cash and cash equivalents 10,914,720$ 10,583,442$

Restricted cash 294,130 70,308

Investments 2,489,604 3,048,207

Current portion of accounts and grants receivable 1,801,945 1,595,117

Current portion of promises to give 2,373,651 2,843,807

Prepaid expenses and deposits 100,387 43,753

Total current assets 17,974,437 18,184,634

Accounts and Grants Receivable, less current portion 1,391,365 1,581,742

Promises to Give, less current portion 1,293,925 9,709

Property and Equipment, net - 6,463

Total assets 20,659,727$ 19,782,548$

LIABILITIES AND NET ASSETS

Current Liabilities

Accounts payable and accrued expenses 219,889$ 188,693$

Current portion of grants payable 5,524,839 6,915,780

Total current liabilities 5,744,728 7,104,473

Grants payable, less current portion 2,937,314 3,575,920

Total liabilities 8,682,042 10,680,393

Net Assets

Unrestricted

Undesignated 1,269,134 1,335,826

Board designated 480,726 622,266

1,749,860 1,958,092

Temporarily restricted 10,227,825 7,144,063

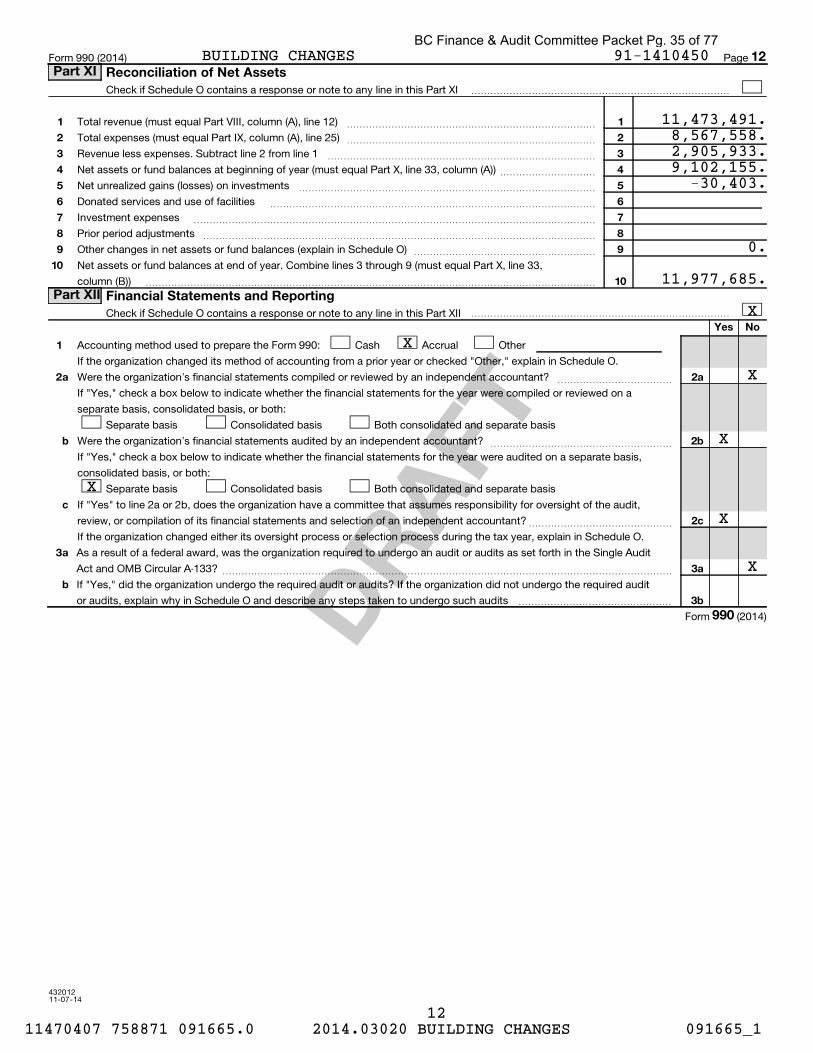

Total net assets 11,977,685 9,102,155

Total liabilities and net assets 20,659,727$ 19,782,548$

BC Finance & Audit Committee Packet Pg. 7 of 77

See Notes to Financial Statements

4 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

STATEMENTS OF ACTIVITIES

For the Years Ended December 31, 2014 and 2013

Unrestricted

Temporarily

Restricted Total Unrestricted

Temporarily

Restricted Total

Support and Revenue

Foundation and corporation contributions 71,316 8,259,863 8,331,179 235,205 7,810,000 8,045,205

Government grants and contracts 2,731,554 2,731,554 576,720 576,720

Technical assitance and other 213,997 213,997 23,293 23,293

Individual contributions 110,434$ 10,000$ 120,434$ 232,915$ -$ 232,915$

Net assets released from restrictions 5,204,428 (5,204,428) 8,372,934 (8,372,934)

Total support and revenue 8,331,729 3,065,435 11,397,164 9,441,067 (562,934) 8,878,133

Expenses

Program services 7,737,845 7,737,845 8,402,141 8,402,141

Management and general 570,634 570,634 595,683 595,683

Fundraising 259,079 259,079 250,923 250,923

Total expenses 8,567,558 - 8,567,558 9,248,747 - 9,248,747

Change in net assets before investment income (235,829) 3,065,435 2,829,606 192,320 (562,934) (370,614)

Investment income 27,597 18,327 45,924 16,147 10,140 26,287

Change in net assets (208,232) 3,083,762 2,875,530 208,467 (552,794) (344,327)

Net Assets, beginning of year 1,958,092 7,144,063 9,102,155 1,749,625 7,696,857 9,446,482

Net Assets, end of year 1,749,860$ 10,227,825$ 11,977,685$ 1,958,092$ 7,144,063$ 9,102,155$

2014 2013

BC Finance & Audit Committee Packet Pg. 8 of 77

See Notes to Financial Statements

5 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

STATEMENT OF FUNCTIONAL EXPENSES

For the Year Ended December 31, 2014

Grantmaking

and

Evaluation

Capacity

Building

Advocacy

and Policy

Total

Program

Services

Management

and General Fundraising Total

Salaries and wages 422,823$ 775,322$ 139,038$ 1,337,183$ 315,567$ 121,897$ 1,774,647$

Payroll taxes and benefits 80,972 175,951 30,678 287,601 64,681 24,324 376,606

Total payroll expenses 503,795 951,273 169,716 1,624,784 380,248 146,221 2,151,253

Grants to others 5,168,204 5,350 5,173,554 5,173,554

Professional fees 283,779 227,438 13,039 524,256 84,143 59,017 667,416

Occupancy 41,918 78,423 14,209 134,550 27,849 12,385 174,784

Conferences and meetings 8,331 56,214 6,812 71,357 7,427 18,149 96,933

Travel 17,733 57,001 9,334 84,068 7,142 520 91,730

Supplies 9,477 22,129 2,770 34,376 20,164 2,176 56,716

Staff recruitment and development 4,660 11,134 885 16,679 18,955 1,546 37,180

Telephone 5,560 12,150 3,334 21,044 4,215 1,424 26,683

Printing and publications 3,230 9,758 1,934 14,922 2,651 5,689 23,262

Dues and licenses 5,188 955 7,786 13,929 6,184 320 20,433

Miscellaneous 242 252 145 639 5,797 7,986 14,422

Insurance 2,422 5,155 1,068 8,645 2,118 884 11,647

Postage and delivery 27 5,924 36 5,987 522 1,939 8,448

Equipment rental and maintenance 1,302 2,417 438 4,157 2,093 384 6,634

Depreciation 1,570 2,822 506 4,898 1,126 439 6,463

Total expenses 6,057,438$ 1,448,395$ 232,012$ 7,737,845$ 570,634$ 259,079$ 8,567,558$

BC Finance & Audit Committee Packet Pg. 9 of 77

See Notes to Financial Statements

6 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

STATEMENT OF FUNCTIONAL EXPENSES

For the Year Ended December 31, 2013

Grantmaking

and

Evaluation

Capacity

Building

Advocacy

and Policy

Total

Program

Services

Management

and General Fundraising Total

Salaries and wages 307,524$ 669,833$ 211,924$ 1,189,281$ 278,528$ 131,634$ 1,599,443$

Payroll taxes and benefits 67,846 145,960 45,686 259,492 55,922 29,332 344,746

Total payroll expenses 375,370 815,793 257,610 1,448,773 334,450 160,966 1,944,189

Grants to others 6,231,457 11,323 6,242,780 6,242,780

Professional fees 231,908 139,397 18,783 390,088 120,977 40,400 551,465

Occupancy 37,215 70,460 19,931 127,606 32,213 13,623 173,442

Conferences and meetings 8,880 13,996 8,107 30,983 2,875 17,463 51,321

Travel 7,521 25,041 9,166 41,728 9,055 250 51,033

Supplies 4,062 11,388 3,219 18,669 39,012 2,266 59,947

Staff recruitment and development 15,038 2,607 840 18,485 15,010 947 34,442

Telephone 4,747 8,354 4,567 17,668 3,831 1,366 22,865

Printing and publications 46 311 357 17,240 2,800 20,397

Dues and licenses 5,365 6,432 7,932 19,729 2,009 646 22,384

Miscellaneous 1,918 3,913 1,114 6,945 1,834 735 9,514

Insurance 136 7,245 14 7,395 909 1,365 9,669

Postage and delivery 2,010 6,853 1,320 10,183 3,129 6,078 19,390

Equipment rental and maintenance 5,764 6,998 1,674 14,436 11,467 1,209 27,112

Depreciation 1,689 3,597 1,030 6,316 1,672 672 8,660

In-kind expense - 137 137

Total expenses 6,933,126$ 1,133,708$ 335,307$ 8,402,141$ 595,683$ 250,923$ 9,248,747$

BC Finance & Audit Committee Packet Pg. 10 of 77

See Notes to Financial Statements

7 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

BUILDING CHANGES

STATEMENTS OF CASH FLOWS

For the Years Ended December 31, 2014 and 2013

2014 2013

Cash Flows from Operating Activities

Cash received from:

Contributions 7,637,553$ 8,344,215$

Government grants and contracts 2,715,103 1,821,921

Technical assistance and ather 213,997 17,630

Investment income 78,827 84,821

Cash paid for:

Grants to others (7,203,101) (5,980,559)

Personnel (2,124,529) (1,972,822)

Services and supplies (1,288,450) (1,178,546)

Net cash flows from operating activities 29,400 1,136,660

Cash Flows from Investing Activities

Purchases of investments (450,647) (2,311,310)

Proceeds from sales of investments 976,347 3,087,397

Increase in restricted cash (223,822)

Net cash flows from investing activities 301,878 776,087

Change in cash and cash equivalents 331,278 1,912,747

Cash and cash equivalents, beginning of year 10,583,442 8,670,695

Cash and cash equivalents, end of year 10,914,720$ 10,583,442$

Reconciliation of Change in Net Assets

to Net Cash Flows from Operating Activities

Change in net assets 2,875,530$ (344,327)$

Depreciation 6,463 8,660

Realized and unrealized loss on investments 32,903 53,008

Change in operating assets and liabilities

Accounts and grants receivable (16,451) 1,245,201

Promises to give (814,060) 66,095

Prepaid expenses and deposits (56,634) 96,893

Accounts payable and accrued expenses 31,196 (251,091)

Grants payable (2,029,547) 262,221

Net cash flows from operating activities 29,400$ 1,136,660$

BC Finance & Audit Committee Packet Pg. 11 of 77

8 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

NOTES TO FINANCIAL STATEMENTS

Note 1. Nature of Activities and Organization

Building Changes is a nonprofit organization conducting activities in Washington State to transform the

ways communities work together to end family and youth homelessness. Building Changes believes that

homelessness can be significantly reduced in Washington State when nonprofits, government, and

philanthropy work seamlessly together in a high-performing system that tailors solutions to the needs of

each individual and family.

Mission: Building Changes believes everyone deserves the opportunity for a home, a healthy life, and a

good job. Building Changes unites public and private partners to create innovative solutions through

expert advice, grantmaking, and advocating for lasting change.

Vision: End homelessness together.

Values: Integrity, equity, collaboration, and results.

How Building Changes Works

Building Changes works collaboratively with nonprofits, government, and philanthropy to advance proven

strategies that hold the promise of ending homelessness. Building Changes provides capacity building,

funding, and policy guidance so its partners can do the best work possible. Building Changes' primary

activities are:

Building the capacity of front-line providers and government agencies so they have the knowledge

and skills they need to improve and sustain their programs.

Demonstrating impact through data collection and evaluation.

Providing grants for promising programs and proven solutions to homelessness.

Targeting policy changes that strengthen the approach of collaborative partners to ending

homelessness.

Building Changes' Approach

Building Changes acts as a "compassionate engineer," designing and implementing a better system to end

homelessness. If Building Changes can change the systems that serve the homeless, it can help

communities make more efficient use of their resources - and ultimately, transform lives. Building Changes

applies and tests the following proven and promising strategies:

Economic Opportunities - Promote long-term stability by collaborating with workforce systems and

incorporating educational and employment programs and services into housing.

Rapid Re-Housing - Quickly move people into housing; provide short-term rental assistance, case

management, and employment assistance.

Evaluation - Collect data and evaluate the impact of these approaches to continually improve the

work of communities.

Prevention - Keep families and individuals from falling into homelessness by coordinating efforts

among housing, education, child welfare, health care, social services, and government.

Coordinated Entry - Improve and streamline access to housing and services into one entry point to

quickly meet the specific needs of people experiencing homelessness.

BC Finance & Audit Committee Packet Pg. 12 of 77

9 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Tailored Programs and Services - Meet the varying service and housing needs of families and individuals

by delivering a customized level of service at the right time.

Notable Accomplishments for 2014

Coordinated entry is now fully underway in King, Pierce and Snohomish counties. It is helping to

streamline access, assessment, and referral processes for housing and other services across agencies in the

community. All three counties have a better sense of the scope of homelessness and are beginning to

use data to refine their systems and address emerging needs. New data is showing that coordinated

entry has simplified access for families, that many homeless families are ready and able to work and that

the majority of families have many strengths, including recent home ownership or lease, no previous

evictions, recent positive work history, and a high school diploma or higher.

Building Changes played a significant role in implementing Rapid Re-Housing in King County and

throughout Washington State in 2014. This model quickly moves homeless families into permanent

housing using short-term rental assistance, case management, and individualized employment services.

Under a contract with the Washington State Department of Commerce, Building Changes provided

technical assistance to all 39 Washington counties to support effective Rapid Re-housing implementation.

The Washington State Department of Commerce adopted Rapid Re-Housing as an essential tool for

ending family homelessness, making it one of three programs that serves low income families who are

homeless or at risk of homelessness.

Diversion is a new model that engages homeless families as early as possible, moves them from the street

to their own housing, and avoids costly interventions, while freeing up limited shelter beds. The goal is to

serve more families with quick and flexible interventions and the results are encouraging. In 2014,

125 King County families avoided homelessness thanks to a diversion pilot program that provides

recipients the assistance they need. Families received small stipends to rent housing in the private

market, or financial help such as funds for car repair so a parent can keep his or her job. Building

Changes believes this solution can work for many families, while reserving shelter for families who have no

other options.

Building Changes provided training and technical assistance to implement the $6 million Washington State

Department of Labor's Workforce Innovations Fund grant to expand and replicate the Housing and

Employment Navigator model developed in 2010 by Building Changes and its partners. By 2016, this

project will engage 720 homeless families served by housing programs in four Washington counties

(Pierce, Whatcom, Skagit, and Yakima).

BC Finance & Audit Committee Packet Pg. 13 of 77

10 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

In 2014, Building Changes continued its work to improve the connection between housing and

Healthcare. Building Changes hired a Senior Manager to manage its healthcare initiatives and build

stronger relationships with healthcare organizations. Building Changes' Executive Director Alice Shobe

became the official housing representative on the Washington State-level Behavioral Health Steering

Committee ("the Committee") convened by Washington State's Department of Social & Health Services.

As charged by two recently enacted laws, Senate Bill 5732 and House Bill 1519, the Committee was created

in early 2014 to support the Washington State Health Care Innovation Plan to develop performance

measures in seven areas, including increases in housing stability for people who receive behavioral health

treatments. Building Changes recruited homeless/housing representatives to the Committee's work

groups and convened them to exchange information and ensure broad input in defining housing stability.

During the 2014 legislative session, the work groups participated in weekly phone calls with the

Governor's policy office and other healthcare advocates to ensure housing stability was included in

healthcare bills. Three healthcare bills included significant opportunities for housing and healthcare

cooperation to improve services for people experiencing homelessness, including funding for a pilot

supportive housing program for people exiting behavioral health facilities.

During 2014, Building Changes deepened its racial equity work to address disparities and

disproportionality among families at risk for homelessness. Building Changes' Racial Equity Framework

was finalized in 2014 and articulates the vision of its racial equity work as a primary lens through which it

conducts its work, both internally as part of its organizational culture and externally as reflected

throughout all of its activities, collaborations, and results. Building Changes believes its intentional focus

on building skills among staff on reducing racial disproportionality across its work will lead to

population-level impacts in its work as well. The Racial Equity Framework is now being used to inform

and guide all of Building Changes' work, including grantmaking, capacity building, policy, and evaluation.

Building Changes is leading the Leadership in Action Program, a nine-month Results-Based Leadership

model, in Pierce County. This unique model, developed by the Annie E. Casey Foundation, builds the

capacity of a diverse group of cross-sector community leaders to accelerate measurable improvements in

the well-being of families, children, and communities in the Pierce community. The Pierce County

Leadership in Action Program is the first such offering in Washington State. It launched in

September 2014 with 36 leaders representing more than 30 organizations, and met three times in 2014.

Through the Washington Youth and Families Fund (formerly Washington Families Fund), a successful

public-private partnership, Building Changes made grants in King, Pierce and Snohomish counties to drive

fundamental, systemic changes to the way that homeless families receive support. These private grants

are matched 2.5 to 1 with realigned public funding, to ensure sustainability and increase the impact and

pace of change. Since the fund launched in 2004, Washington State has allocated $17 million to the

Washington Youth and Families Fund, which has leveraged $38.5 million in investments from 25 different

private funders.

In 2014, Building Changes granted $5,173,554 to 37 nonprofits. These grants supported employment,

rapid re-housing, coordinated entry, and other changes to the systems that support homeless families.

Along with funding, Building Changes provides grantees ongoing support in the form of capacity building,

technical assistance, and evaluation.

2014 marked the 10th anniversary of the Washington Youth and Families Fund, which is dedicated to

reducing and ending youth and family homelessness statewide. Building Changes celebrated

Washington Youth and Families Fund's achievements in December, when Governor Inslee and other

Washington State philanthropic and private sector leaders signed a new memorandum of understanding

pledging to make youth, young adult, and family homelessness in Washington a rare, brief, and one-time

occurrence by 2020.

BC Finance & Audit Committee Packet Pg. 14 of 77

11 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Note 2. Significant Accounting Policies

Financial Statement Presentation

Building Changes reports information regarding its financial position and activities according to

three classes of net assets: unrestricted net assets, temporarily restricted net assets, and permanently

restricted net assets. Building Changes has no permanently restricted net assets, so this class of net

assets is not shown on the financial statements.

Temporarily Restricted Net Assets

Temporarily restricted net assets consist of unexpended contributions or grants restricted for particular

purposes or time periods. Temporarily restricted net assets are transferred to unrestricted net assets as

expenditures are incurred for the restricted purpose, or as time restrictions expire. Temporarily restricted

net assets at December 31 consist of:

2014 2013

Washington Families Fund expansion 7,333,538$ 4,295,376$

Washington Families Fund service grantmaking 1,401,433 2,048,510

Contributions restricted for time 327,914 130,000

Youth homelessness 238,990 62,454

WFF high level services evaluation 232,333 267,163

Business planning 225,000

Economic opportunities 206,135 194,258

Healthcare 150,000

Racial disproportionality in homelessness 70,787 146,302

Other 41,695

10,227,825$ 7,144,063$

Unrestricted Net Assets

A portion of unrestricted net assets are designated by the Board for an Innovation Fund, which is intended

to be used to fund new program opportunities.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the

United States requires management to make estimates and assumptions that affect certain reported

amounts and disclosures. Actual results could differ from the estimated amounts.

Cash and Cash Equivalents

Cash and cash equivalents consist of checking, savings, and money market accounts. Cash balances held

in investment accounts are included with investments in the statements of financial position.

Building Changes occasionally has amounts deposited with financial institutions in excess of federally

insured limits.

BC Finance & Audit Committee Packet Pg. 15 of 77

12 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Restricted Cash

Restricted cash is not available for general operating purposes and is restricted by donors to be used to

fund grants under the Washington Youth and Family Fund program.

Investments

Investments are reported at their fair values (using Level 1 inputs of the fair value hierarchy, which are

quoted market prices in active markets for identical assets) in the statements of financial position.

Unrealized gains and losses are included in the change in net assets.

Accounts and Grants Receivable

Accounts and grants receivable are due primarily from the Washington State Department of Commerce.

Management provides for probable uncollectible amounts through a charge to expense and a credit to a

valuation allowance based on its assessment of the current status of individual accounts. Balances still

outstanding after management has used reasonable collection efforts are written off through a charge to

the valuation allowance and a credit to the receivable account. Management determined that no

allowance was necessary at December 31, 2014 and 2013. Accounts and grants receivable expected to be

collected after one year from the statement of financial position date are presented as long-term in the

accompanying financial statements.

Promises to Give

Promises to give consist of contributions pledged but not yet received from individuals, foundations, and

corporations. Promises to give that are expected to be collected within one year are recorded at net

realizable value. Promises to give expected to be collected in future years are initially recorded at fair

value, which is measured as the present value of the expected future cash flows. The discount on those

amounts is computed using a risk adjusted interest rate which is applicable to the year in which the award

was received (using Level 3 inputs of the fair value hierarchy, which are unobservable inputs developed by

Building Changes). Of the total promises to give, 74% and 81% were due from one foundation as of

December 31, 2014 and 2013, respectively. Management determined that no allowance was necessary at

December 31, 2014 and 2013.

BC Finance & Audit Committee Packet Pg. 16 of 77

13 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Property and Equipment

Property and equipment are recorded at cost or, if donated, at fair value at date of receipt. Building

Changes capitalizes all expenditures for property and equipment with a useful life greater than one year

and a cost in excess of its capitalization threshold of $5,000. Depreciation expense is provided for using

the straight-line method over the assets' estimated useful lives. Depreciation expense for leasehold

improvements is recorded over the shorter of the useful life or the lease term using the straight-line

method. Property and equipment consists of the following at December 31:

2014 2013

Leasehold improvements 143,739$ 143,739$

Furniture and equipment 134,707 353,777

278,446 497,516

Accumulated depreciation (278,446) (491,053)

-$ 6,463$

Grants Payable

Grants payable consist of unconditional promises to pay grants to others. Grants payable are recognized

as expense, and the related liability recognized, at fair value in the period grants are awarded or paid. In

general, grants are payable over three years. In some instances, grants are payable in more than

three years and are recognized in the period it becomes probable that the grants will be paid. Fair value

is measured as the present value of the expected future cash flows. The discount on those amounts is

computed using a risk adjusted interest rate which is applicable to the year in which the award was made

(using Level 3 inputs of the fair value hierarchy, which are unobservable inputs developed by

Building Changes).

Revenue Recognition

Contributions: Unconditional promises to give are recognized as unrestricted, temporarily restricted, or

permanently restricted support depending on the existence and/or nature of any donor restrictions at fair

value during the period a cash gift or non-cash gift is received or pledged.

Government grants: Revenue related to governmental grants and contracts is recognized when grants

payable to others have been awarded or paid.

Technical assistance service fees: Technical assistance service fees represent fees for training and

consulting services, and are recognized as the services are provided.

One foundation and the Washington State Department of Commerce accounted for 60% and 23%,

respectively, of total support and revenue for 2014. One foundation and the Washington State

Department of Commerce accounted for 84% and 9%, respectively, of total support and revenue for 2013.

Functional Allocation of Expenses

The costs of providing the various programs and other activities have been summarized on a functional

basis in the statements of activity and statements of functional expenses. Accordingly, certain costs have

been allocated between the program and supporting services benefited.

BC Finance & Audit Committee Packet Pg. 17 of 77

14 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Income Taxes

Building Changes is exempt from federal income taxes under Section 501(c)(3) of the Internal Revenue

Code, and its federal returns are open to review by federal taxing authorities for the last three years.

Reclassifications

Certain balances have been reclassified in the 2013 financial statements in order to conform to current

year presentation. These reclassifications had no effect on net assets or the change in net assets as of or

for the year ended December 31, 2013.

Subsequent Events

Building Changes has evaluated subsequent events through the date these financial statements were

available to be issued, which is the same date as the independent auditors' report.

Note 3. Investments

Investments consist of the following at December 31:

2014 2013

Cash and cash equivalents 143,484$ 309,722$

Fixed income securities

Government mortgage backed securities 948,125 1,054,838

Corporate bonds 878,349 1,019,437

Treasury notes 519,646 664,210

2,489,604$ 3,048,207$

Investment income was composed of:

2014 2013

Realized and unrealized losses (32,903)$ (53,008)$

Interest income 78,827 79,295

45,924$ 26,287$

BC Finance & Audit Committee Packet Pg. 18 of 77

15 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Note 4. Promises to Give

Promises to give were due as follows as of December 31:

2014 2013

Receivable in less than one year 2,373,651$ 2,843,807$

Receivable in one to five years 1,320,000 10,000

3,693,651 2,853,807

Unamortized discount (2%) (26,075) (291)

3,667,576$ 2,853,516$

Included in the statements of financial position as follows:

2014 2013

Promises to give - current portion 2,373,651$ 2,843,807$

Promises to give - long-term portion 1,293,925 9,709

3,667,576$ 2,853,516$

Note 5. Grants Payable

Grants are payable as follows at December 31:

2014 2013

Payable in less than one year 5,524,839$ 6,915,780$

Payable in one to five years 3,005,388 3,639,526

8,530,227 10,555,306

Unamortized discount (1.5% - 2%) (68,074) (63,606)

8,462,153$ 10,491,700$

Included in the statements of financial position as follows:

2014 2013

Grants payable - current portion 5,524,839$ 6,915,780$

Grants payable - long-term portion 2,937,314 3,575,920

8,462,153$ 10,491,700$

BC Finance & Audit Committee Packet Pg. 19 of 77

16 091665fs123114 Revised: 4/7/2015 8:37 AM mcp

Note 6. Line of Credit

Building Changes has a $200,000 line of credit agreement with a bank, collateralized by all of its assets,

which is renewable on July 9, 2015. Interest is payable monthly at LIBOR plus 4.095% (resulting in a rate

of 4.18% at December 31, 2014). There was no outstanding balance under this agreement at

December 31, 2014 or 2013.

Note 7. Operating Leases

Building Changes leases office space and certain equipment under operating leases. The term of the

office space lease expires on August 31, 2015. On January 15, 2015, Building Changes executed a lease

for new office space with an initial 60 month term beginning August 2015 and ending August 2020. Rent

expense under these operating leases amounted to $170,147 and $172,707 for the years ended

December 31, 2014 and 2013, respectively. Future minimum payments under the leases are as follows for

the years ending December 31:

2015 107,946$

2016 64,530

2017 57,984

2018 59,712

2019 61,501

Thereafter 41,823

393,496$

Note 8. Retirement Plan

Building Changes participates in a defined-contribution tax-sheltered 403(b) annuity plan covering

substantially all permanent employees upon commencement of employment. Employees are eligible to

receive employer contributions after one year of service. Employer contributions are a minimum of 3% of

eligible employees' annual compensation. Total expense related to contributions to the plan were

$40,924 and $36,428 for the years ended December 31, 2014 and 2013, respectively. Building Changes

also sponsors a tax-deferred annuity plan to which employees may make voluntary contributions.

BC Finance & Audit Committee Packet Pg. 20 of 77

17

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVER FINANCIAL

REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT

OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT

AUDITING STANDARDS

To the Board of Directors

Building Changes

Seattle, Washington

We have audited, in accordance with the auditing standards generally accepted in the United States and

the standards applicable to financial audits contained in Government Auditing Standards issued by the

Comptroller General of the United States, the financial statements of Building Changes, which comprise

the statement of financial position as of December 31, 2014, and the related statements of activities,

functional expenses, and cash flows for the year then ended, and the related notes to the financial

statements, and have issued our report thereon dated __________________.

Internal Control over Financial Reporting

In planning and performing our audit of the financial statements, we considered Building Changes' internal

control over financial reporting (internal control) to determine the audit procedures that are appropriate in

the circumstances for the purpose of expressing our opinion on the financial statements, but not for the

purpose of expressing an opinion on the effectiveness of Building Changes' internal control. Accordingly,

we do not express an opinion on the effectiveness of the Building Changes' internal control.

A deficiency in internal control exists when the design or operation of a control does not allow

management or employees, in the normal course of performing their assigned functions, to prevent, or

detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a

combination of deficiencies, in internal control, such that there is a reasonable possibility that a material

misstatement of the entity's financial statements will not be prevented, or detected and corrected on a

timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control

that is less severe than a material weakness, yet important enough to merit attention by those charged

with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this

section and was not designed to identify all deficiencies in internal control that might be material

weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any

deficiencies in internal control that we consider to be material weaknesses. However, material

weaknesses may exist that have not been identified.

BC Finance & Audit Committee Packet Pg. 21 of 77

18

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Building Changes' financial statements are free

from material misstatement, we performed tests of its compliance with certain provisions of Jaws,

regulations, contracts, and grant agreements, noncompliance with which could have a direct and material

effect on the determination of financial statement amounts. However, providing an opinion on

compliance with those provisions was not an objective of our audit, and accordingly, we do not express

such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that

are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance

and the results of that testing, and not to provide an opinion on the effectiveness of the

Building Changes' internal control or on compliance. This report is an integral part of an audit performed

in accordance with Government Auditing Standards in considering the Building Changes' internal control

and compliance. Accordingly, this communication is not suitable for any other purpose.

____________________________

BC Finance & Audit Committee Packet Pg. 22 of 77

Resolution 15-07 Accept Annual Audit

WHEREAS, Article VIII, Section 8.07 of the Bylaws of Building Changes requires an annual independent audit of its financial statements; and WHEREAS, the audit has been completed by the auditor Peterson & Sullivan, PLLC, reviewed by the Finance and Audit Committee on 4/15/2015 and recommended to the Board of Directors for adoption; NOW, THEREFORE, BE IT RESOLVED by the Board of Directors of Building Changes that the audit of the combined financial statements of Building Changes for the year ended December 31, 2014, is hereby adopted. Attested, ______________________________

Barbara Dingfield, Secretary

(as an agent of the board) April 24, 2014

BC Finance & Audit Committee Packet Pg. 23 of 77

DR

AFT

Checkifself-employed

OMB No. 1545-0047

Department of the TreasuryInternal Revenue Service

Check ifapplicable:

AddresschangeNamechangeInitialreturn

Finalreturn/termin-ated Gross receipts $

AmendedreturnApplica-tionpending

Are all subordinates included?

432001 11-07-14

| Do not enter social security numbers on this form as it may be made public.

Beginning of Current Year

Paid

Preparer

Use Only

Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Open to Public Inspection| Information about Form 990 and its instructions is at

A For the 2014 calendar year, or tax year beginning and ending

B C D Employer identification number

E

G

H(a)

H(b)

H(c)

F Yes No

Yes No

I

J

K

Website: |

L M

1

2

3

4

5

6

7

3

4

5

6

7a

7b

a

b

Ac

tivi

tie

s &

Go

vern

an

ce

Prior Year Current Year

8

9

10

11

12

13

14

15

16

17

18

19

Re

ven

ue

a

b

Ex

pe

ns

es

End of Year

20

21

22

Sign

Here

Yes No

For Paperwork Reduction Act Notice, see the separate instructions.

(or P.O. box if mail is not delivered to street address) Room/suite

)501(c)(3) 501(c) ( (insert no.) 4947(a)(1) or 527

|Corporation Trust Association OtherForm of organization: Year of formation: State of legal domicile:

|

|

Net

Ass

ets

orFu

nd B

alan

ces

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is

true, correct, and complete. Declaration of preparer (other than officer) is based on all information of which preparer has any knowledge.

Signature of officer Date

Type or print name and title

Date PTINPrint/Type preparer's name Preparer's signature

Firm's name Firm's EIN

Firm's address

Phone no.

Form

Name of organization

Doing business as

Number and street Telephone number

City or town, state or province, country, and ZIP or foreign postal code

Is this a group return

for subordinates?Name and address of principal officer: ~~

If "No," attach a list. (see instructions)

Group exemption number |

Tax-exempt status:

Briefly describe the organization's mission or most significant activities:

Check this box if the organization discontinued its operations or disposed of more than 25% of its net assets.

Number of voting members of the governing body (Part VI, line 1a)

Number of independent voting members of the governing body (Part VI, line 1b)

Total number of individuals employed in calendar year 2014 (Part V, line 2a)

~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~

Total number of volunteers (estimate if necessary)

Total unrelated business revenue from Part VIII, column (C), line 12

Net unrelated business taxable income from Form 990-T, line 34

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~

����������������������

Contributions and grants (Part VIII, line 1h) ~~~~~~~~~~~~~~~~~~~~~

Program service revenue (Part VIII, line 2g) ~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~Investment income (Part VIII, column (A), lines 3, 4, and 7d)

Other revenue (Part VIII, column (A), lines 5, 6d, 8c, 9c, 10c, and 11e) ~~~~~~~~

Total revenue - add lines 8 through 11 (must equal Part VIII, column (A), line 12) ���

Grants and similar amounts paid (Part IX, column (A), lines 1-3)

Benefits paid to or for members (Part IX, column (A), line 4)

Salaries, other compensation, employee benefits (Part IX, column (A), lines 5-10)

~~~~~~~~~~~

~~~~~~~~~~~~~

~~~

Professional fundraising fees (Part IX, column (A), line 11e)

Total fundraising expenses (Part IX, column (D), line 25)

~~~~~~~~~~~~~~

Other expenses (Part IX, column (A), lines 11a-11d, 11f-24e)

Total expenses. Add lines 13-17 (must equal Part IX, column (A), line 25)

Revenue less expenses. Subtract line 18 from line 12

~~~~~~~~~~~~~

~~~~~~~

����������������

Total assets (Part X, line 16)

Total liabilities (Part X, line 26)

Net assets or fund balances. Subtract line 21 from line 20

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~

��������������

May the IRS discuss this return with the preparer shown above? (see instructions) ���������������������

LHA Form (2014)

www.irs.gov/form990.

Part I Summary

Signature BlockPart II

990

Return of Organization Exempt From Income Tax990 2014

§

==

999

BUILDING CHANGES91-1410450

2014 EAST MADISON STREET 200 (206)805-610012,452,350.

SEATTLE, WA 98122ALICE SHOBE X

SAME AS C ABOVEX

WWW.BUILDINGCHANGES.ORGX 1988 WA

ENDING HOMELESSNESS INWASHINGTON STATE

151534180.0.

8,854,977. 11,183,167.23,156. 213,997.

115,785. 74,027.73. 2,300.

8,993,991. 11,473,491.6,242,780. 5,173,554.

0. 0.1,944,189. 2,151,255.

0. 49,500.259,079.

1,061,778. 1,193,249.9,248,747. 8,567,558.-254,756. 2,905,933.

19,782,548. 20,659,727.10,680,393. 8,682,042.9,102,155. 11,977,685.

ALICE SHOBE, EXECUTIVE DIRECTOR

RAYMON G. HOLMDAHL RAYMON G. HOLMDAHL 04/07/15 P00120599PETERSON SULLIVAN LLP, CPA'S 91-0605875601 UNION ST, STE 2300SEATTLE, WA 98101-2345 2063827777

X

BC Finance & Audit Committee Packet Pg. 24 of 77

DR

AFT

Code: Expenses $ including grants of $ Revenue $

Code: Expenses $ including grants of $ Revenue $

Code: Expenses $ including grants of $ Revenue $

Expenses $ including grants of $ Revenue $

43200211-07-14

1

2

3

4

Yes No

Yes No

4a

4b

4c

4d

4e

Form 990 (2014) Page

Check if Schedule O contains a response or note to any line in this Part III ����������������������������

Briefly describe the organization's mission:

Did the organization undertake any significant program services during the year which were not listed on

the prior Form 990 or 990-EZ?

If "Yes," describe these new services on Schedule O.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization cease conducting, or make significant changes in how it conducts, any program services?

If "Yes," describe these changes on Schedule O.

~~~~~~

Describe the organization's program service accomplishments for each of its three largest program services, as measured by expenses.

Section 501(c)(3) and 501(c)(4) organizations are required to report the amount of grants and allocations to others, the total expenses, and

revenue, if any, for each program service reported.

( ) ( ) ( )

( ) ( ) ( )

( ) ( ) ( )

Other program services (Describe in Schedule O.)

( ) ( )

Total program service expenses |

Form (2014)

2Statement of Program Service AccomplishmentsPart III

990

BUILDING CHANGES 91-1410450

X

BUILDING CHANGES BELIEVES EVERYONE DESERVES THE OPPORTUNITY FOR AHOME, HEALTHY LIFE AND A GOOD JOB. WE UNITE PUBLIC AND PRIVATEPARTNERS TO CREATE INNOVATIVE SOLUTIONS THROUGH EXPERT ADVICE,GRANTMAKING, AND ADVOCATING FOR LASTING CHANGE.

X

X

6,056,313. 5,173,554.GRANTMAKING & EVALUATION - WE LEAD THE WASHINGTON FAMILIES FUND (WFF)WHICH IDENTIFIES, FUNDS, AND EVALUATES INNOVATIVE PROGRAMS THAT PREVENTAND END HOMELESSNESS. CREATED IN 2004 BY THE WASHINGTON STATELEGISLATURE, WFF FUNDS MODEL PROGRAMS AND INNOVATIVE STRATEGIES THATADDRESS THE PROBLEMS OF HOMELESSNESS BOTH AT A SYSTEM AND FAMILY LEVEL.IN 2014, WITH FUNDING FROM 25 PUBLIC AND PRIVATE PARTNERS, WE GRANTEDFUNDS TO 35 ORGANIZATIONS THROUGHOUT WASHINGTON STATE.

1,288,869.CAPACITY BUILDING - WE GIVE WASHINGTON COMMUNITIES THE RIGHT TOOLS ANDKNOWLEDGE TO PREVENT AND END HOMELESSNESS. WE HELP COMMUNITIES TO MAKEIMPORTANT SHIFTS NOW - CHANGES THAT HELP PEOPLE IMMEDIATELY - WHILE WETACKLE FUNDAMENTAL CHANGE OVER THE LONGER TERM. WE TRAIN AND BUILD THECAPACITY OF FRONTLINE HOMELESSNESS PROVIDERS, FUNDERS AND GOVERNMENTAGENCIES SO THEY CAN USE LIMITED RESOURCES MORE EFFICIENTLY, LEARN FROMDATA AND PROMISING PRACTICES AROUND THE COUNTRY, AND ADOPT NEW WAYS TODELIVER SERVICES THAT LEAD TO BETTER OUTCOMES FOR FAMILIES.

232,169.POLICY AND ADVOCACY - OUR POLICY EFFORTS FOCUS ON REGULATORY ANDLEGISLATIVE CHANGES THAT PREVENT, REDUCE AND MITIGATE THE IMPACT OFHOMELESSNESS IN WASHINGTON STATE. WE WORK ACROSS SYSTEMS WITH PARTNERSIN CHILD WELFARE, EMPLOYMENT AND EDUCATION TO IDENTIFY KEY POLICYINITIATIVE, PURSUE FIXES AND INFLUENCE LONG-TERM POLICY AGENDAS THATRESULT IN MORE EFFICIENT HOMELESS AND HOUSING SYSTEMS - AND REDUCE THEBARRIERS THAT HOMELESS FAMILIES FACE WHEN THEY SEEK HELP.

160,494. 213,997.7,737,845.

11470407 758871 091665.0 2014.03020 BUILDING CHANGES 091665_1 2

BC Finance & Audit Committee Packet Pg. 25 of 77

DR

AFT

43200311-07-14

Yes No

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

1

2

3

4

5

6

7

8

9

10

Section 501(c)(3) organizations.

a

b

c

d

e

f

a

b

11a

11b

11c

11d

11e

11f

12a

12b

13

14a

14b

15

16

17

18

19

20a

20b

a

b

a

b

If "Yes," complete Schedule ASchedule B, Schedule of Contributors

If "Yes," complete Schedule C, Part I

If "Yes," complete Schedule C, Part II

If "Yes," complete Schedule C, Part III

If "Yes," complete Schedule D, Part I

If "Yes," complete Schedule D, Part IIIf "Yes," complete

Schedule D, Part III

If "Yes," complete Schedule D, Part IV

If "Yes," complete Schedule D, Part V

If "Yes," complete Schedule D,Part VI

If "Yes," complete Schedule D, Part VII

If "Yes," complete Schedule D, Part VIII

If "Yes," complete Schedule D, Part IXIf "Yes," complete Schedule D, Part X

If "Yes," complete Schedule D, Part XIf "Yes," complete

Schedule D, Parts XI and XII

If "Yes," and if the organization answered "No" to line 12a, then completing Schedule D, Parts XI and XII is optionalIf "Yes," complete Schedule E

If "Yes," complete Schedule F, Parts I and IV

If "Yes," complete Schedule F, Parts II and IV

If "Yes," complete Schedule F, Parts III and IV

If "Yes," complete Schedule G, Part I

If "Yes," complete Schedule G, Part IIIf "Yes,"

complete Schedule G, Part IIIIf "Yes," complete Schedule H

Form 990 (2014) Page

Is the organization described in section 501(c)(3) or 4947(a)(1) (other than a private foundation)?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Is the organization required to complete ?

Did the organization engage in direct or indirect political campaign activities on behalf of or in opposition to candidates for

public office?

~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization engage in lobbying activities, or have a section 501(h) election in effect

during the tax year?

Is the organization a section 501(c)(4), 501(c)(5), or 501(c)(6) organization that receives membership dues, assessments, or

similar amounts as defined in Revenue Procedure 98-19?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~

Did the organization maintain any donor advised funds or any similar funds or accounts for which donors have the right to

provide advice on the distribution or investment of amounts in such funds or accounts?

Did the organization receive or hold a conservation easement, including easements to preserve open space,

the environment, historic land areas, or historic structures?

Did the organization maintain collections of works of art, historical treasures, or other similar assets?

~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report an amount in Part X, line 21, for escrow or custodial account liability; serve as a custodian for

amounts not listed in Part X; or provide credit counseling, debt management, credit repair, or debt negotiation services?

Did the organization, directly or through a related organization, hold assets in temporarily restricted endowments, permanent

endowments, or quasi-endowments?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~

If the organization's answer to any of the following questions is "Yes," then complete Schedule D, Parts VI, VII, VIII, IX, or X

as applicable.

Did the organization report an amount for land, buildings, and equipment in Part X, line 10?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report an amount for investments - other securities in Part X, line 12 that is 5% or more of its total

assets reported in Part X, line 16?

Did the organization report an amount for investments - program related in Part X, line 13 that is 5% or more of its total

assets reported in Part X, line 16?

~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report an amount for other assets in Part X, line 15 that is 5% or more of its total assets reported in

Part X, line 16?

Did the organization report an amount for other liabilities in Part X, line 25?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~

Did the organization's separate or consolidated financial statements for the tax year include a footnote that addresses

the organization's liability for uncertain tax positions under FIN 48 (ASC 740)?

Did the organization obtain separate, independent audited financial statements for the tax year?

~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Was the organization included in consolidated, independent audited financial statements for the tax year?

~~~~~

Is the organization a school described in section 170(b)(1)(A)(ii)?

Did the organization maintain an office, employees, or agents outside of the United States?

~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~

Did the organization have aggregate revenues or expenses of more than $10,000 from grantmaking, fundraising, business,

investment, and program service activities outside the United States, or aggregate foreign investments valued at $100,000

or more? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report on Part IX, column (A), line 3, more than $5,000 of grants or other assistance to or for any

foreign organization?

Did the organization report on Part IX, column (A), line 3, more than $5,000 of aggregate grants or other assistance to

or for foreign individuals?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report a total of more than $15,000 of expenses for professional fundraising services on Part IX,

column (A), lines 6 and 11e? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report more than $15,000 total of fundraising event gross income and contributions on Part VIII, lines

1c and 8a? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report more than $15,000 of gross income from gaming activities on Part VIII, line 9a?

Did the organization operate one or more hospital facilities?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~

If "Yes" to line 20a, did the organization attach a copy of its audited financial statements to this return? ����������

Form (2014)

3Part IV Checklist of Required Schedules

990

BUILDING CHANGES 91-1410450

XX

X

X

X

X

X

X

X

X

X

X

X

XX

X

X

XXX

X

X

X

X

X

XX

11470407 758871 091665.0 2014.03020 BUILDING CHANGES 091665_1 3

BC Finance & Audit Committee Packet Pg. 26 of 77

DR

AFT

43200411-07-14

Yes No

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

21

22

23

24a

24b

24c

24d

25a

25b

26

27

28a

28b

28c

29

30

31

32

33

34

35a

35b

36

37

38

a

b

c

d

a

b

Section 501(c)(3), 501(c)(4), and 501(c)(29) organizations.

a

b

c

a

b

Section 501(c)(3) organizations.

Note.

(continued)

If "Yes," complete Schedule I, Parts I and II

If "Yes," complete Schedule I, Parts I and III

If "Yes," completeSchedule J

If "Yes," answer lines 24b through 24d and completeSchedule K. If "No", go to line 25a

If "Yes," complete Schedule L, Part I

If "Yes," completeSchedule L, Part I

If "Yes,"complete Schedule L, Part II

If "Yes," complete Schedule L, Part III

If "Yes," complete Schedule L, Part IVIf "Yes," complete Schedule L, Part IV

If "Yes," complete Schedule L, Part IVIf "Yes," complete Schedule M

If "Yes," complete Schedule M

If "Yes," complete Schedule N, Part IIf "Yes," complete

Schedule N, Part II

If "Yes," complete Schedule R, Part IIf "Yes," complete Schedule R, Part II, III, or IV, and

Part V, line 1

If "Yes," complete Schedule R, Part V, line 2

If "Yes," complete Schedule R, Part V, line 2

If "Yes," complete Schedule R, Part VI

Form 990 (2014) Page

Did the organization report more than $5,000 of grants or other assistance to any domestic organization or

domestic government on Part IX, column (A), line 1? ~~~~~~~~~~~~~~

Did the organization report more than $5,000 of grants or other assistance to or for domestic individuals on

Part IX, column (A), line 2? ~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization answer "Yes" to Part VII, Section A, line 3, 4, or 5 about compensation of the organization's current

and former officers, directors, trustees, key employees, and highest compensated employees?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization have a tax-exempt bond issue with an outstanding principal amount of more than $100,000 as of the

last day of the year, that was issued after December 31, 2002?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization invest any proceeds of tax-exempt bonds beyond a temporary period exception?

Did the organization maintain an escrow account other than a refunding escrow at any time during the year to defease

any tax-exempt bonds?

Did the organization act as an "on behalf of" issuer for bonds outstanding at any time during the year?

~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~

Did the organization engage in an excess benefit

transaction with a disqualified person during the year?

Is the organization aware that it engaged in an excess benefit transaction with a disqualified person in a prior year, and

that the transaction has not been reported on any of the organization's prior Forms 990 or 990-EZ?

~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization report any amount on Part X, line 5, 6, or 22 for receivables from or payables to any current or

former officers, directors, trustees, key employees, highest compensated employees, or disqualified persons?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization provide a grant or other assistance to an officer, director, trustee, key employee, substantial

contributor or employee thereof, a grant selection committee member, or to a 35% controlled entity or family member

of any of these persons? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Was the organization a party to a business transaction with one of the following parties (see Schedule L, Part IV

instructions for applicable filing thresholds, conditions, and exceptions):

A current or former officer, director, trustee, or key employee? ~~~~~~~~~~~

A family member of a current or former officer, director, trustee, or key employee?

An entity of which a current or former officer, director, trustee, or key employee (or a family member thereof) was an officer,

director, trustee, or direct or indirect owner?

~~

~~~~~~~~~~~~~~~~~~~~~

Did the organization receive more than $25,000 in non-cash contributions?

Did the organization receive contributions of art, historical treasures, or other similar assets, or qualified conservation

contributions?

~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization liquidate, terminate, or dissolve and cease operations?

Did the organization sell, exchange, dispose of, or transfer more than 25% of its net assets?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization own 100% of an entity disregarded as separate from the organization under Regulations

sections 301.7701-2 and 301.7701-3?

Was the organization related to any tax-exempt or taxable entity?

~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization have a controlled entity within the meaning of section 512(b)(13)?

If "Yes" to line 35a, did the organization receive any payment from or engage in any transaction with a controlled entity

within the meaning of section 512(b)(13)?

~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~

Did the organization make any transfers to an exempt non-charitable related organization?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization conduct more than 5% of its activities through an entity that is not a related organization

and that is treated as a partnership for federal income tax purposes? ~~~~~~~~

Did the organization complete Schedule O and provide explanations in Schedule O for Part VI, lines 11b and 19?

All Form 990 filers are required to complete Schedule O �������������������������������

Form (2014)

4Part IV Checklist of Required Schedules

990

BUILDING CHANGES 91-1410450

X

X

X

X

X

X

X

X

XX

XX

X

X

X

X

XX

X

X

X

11470407 758871 091665.0 2014.03020 BUILDING CHANGES 091665_1 4

BC Finance & Audit Committee Packet Pg. 27 of 77

DR

AFT

43200511-07-14

Yes No

1

2

3

4

5

6

7

a

b

c

1a

1b

1c

a

b

2a

Note.

2b

3a

3b

4a

5a

5b

5c

6a

6b

7a

7b

7c

7e

7f

7g

7h

8

9a

9b

a

b

a

b

a

b

c

a

b

Organizations that may receive deductible contributions under section 170(c).

a

b

c

d

e

f

g

h

7d

8

9

10

11

12

13

14

Sponsoring organizations maintaining donor advised funds.

Sponsoring organizations maintaining donor advised funds.

a

b

Section 501(c)(7) organizations.

a

b

10a

10b

Section 501(c)(12) organizations.

a

b

11a

11b

a

b

Section 4947(a)(1) non-exempt charitable trusts. 12a

12b

Section 501(c)(29) qualified nonprofit health insurance issuers.

Note.

a

b

c

a

b

13a

13b

13c

14a

14b

e-file

If "No," to line 3b, provide an explanation in Schedule O

If "No," provide an explanation in Schedule O

Did the organization receive a payment in excess of $75 made partly as a contribution and partly for goods and services provided to the payor?

Form (2014)

Form 990 (2014) Page

Check if Schedule O contains a response or note to any line in this Part V ���������������������������

Enter the number reported in Box 3 of Form 1096. Enter -0- if not applicable ~~~~~~~~~~~

Enter the number of Forms W-2G included in line 1a. Enter -0- if not applicable ~~~~~~~~~~

Did the organization comply with backup withholding rules for reportable payments to vendors and reportable gaming

(gambling) winnings to prize winners? �������������������������������������������

Enter the number of employees reported on Form W-3, Transmittal of Wage and Tax Statements,

filed for the calendar year ending with or within the year covered by this return ~~~~~~~~~~

If at least one is reported on line 2a, did the organization file all required federal employment tax returns?

If the sum of lines 1a and 2a is greater than 250, you may be required to (see instructions)

~~~~~~~~~~

~~~~~~~~~~~

Did the organization have unrelated business gross income of $1,000 or more during the year?

If "Yes," has it filed a Form 990-T for this year?

~~~~~~~~~~~~~~

~~~~~~~~~~

At any time during the calendar year, did the organization have an interest in, or a signature or other authority over, a

financial account in a foreign country (such as a bank account, securities account, or other financial account)?~~~~~~~

If "Yes," enter the name of the foreign country:

See instructions for filing requirements for FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR).

Was the organization a party to a prohibited tax shelter transaction at any time during the tax year?

Did any taxable party notify the organization that it was or is a party to a prohibited tax shelter transaction?

~~~~~~~~~~~~

~~~~~~~~~

If "Yes," to line 5a or 5b, did the organization file Form 8886-T? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Does the organization have annual gross receipts that are normally greater than $100,000, and did the organization solicit

any contributions that were not tax deductible as charitable contributions?

If "Yes," did the organization include with every solicitation an express statement that such contributions or gifts

were not tax deductible?

~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

If "Yes," did the organization notify the donor of the value of the goods or services provided?

Did the organization sell, exchange, or otherwise dispose of tangible personal property for which it was required

to file Form 8282?

~~~~~~~~~~~~~~~

����������������������������������������������������

If "Yes," indicate the number of Forms 8282 filed during the year

Did the organization receive any funds, directly or indirectly, to pay premiums on a personal benefit contract?

~~~~~~~~~~~~~~~~

~~~~~~~

~~~~~~~~~Did the organization, during the year, pay premiums, directly or indirectly, on a personal benefit contract?

If the organization received a contribution of qualified intellectual property, did the organization file Form 8899 as required?

If the organization received a contribution of cars, boats, airplanes, or other vehicles, did the organization file a Form 1098-C?

~

Did a donor advised fund maintained by the

sponsoring organization have excess business holdings at any time during the year? ~~~~~~~~~~~~~~~~~~~

Did the sponsoring organization make any taxable distributions under section 4966?

Did the sponsoring organization make a distribution to a donor, donor advisor, or related person?

~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~

Enter:

Initiation fees and capital contributions included on Part VIII, line 12

Gross receipts, included on Form 990, Part VIII, line 12, for public use of club facilities

~~~~~~~~~~~~~~~

~~~~~~

Enter:

Gross income from members or shareholders

Gross income from other sources (Do not net amounts due or paid to other sources against

amounts due or received from them.)

~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Is the organization filing Form 990 in lieu of Form 1041?

If "Yes," enter the amount of tax-exempt interest received or accrued during the year ������

Is the organization licensed to issue qualified health plans in more than one state?

See the instructions for additional information the organization must report on Schedule O.

~~~~~~~~~~~~~~~~~~~~~

Enter the amount of reserves the organization is required to maintain by the states in which the

organization is licensed to issue qualified health plans

Enter the amount of reserves on hand

~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization receive any payments for indoor tanning services during the tax year?

If "Yes," has it filed a Form 720 to report these payments?

~~~~~~~~~~~~~~~~

����������

5Part V Statements Regarding Other IRS Filings and Tax Compliance

990

J

BUILDING CHANGES 91-1410450

310

X

34X

X

X

XX

X

X

X

XX

X

11470407 758871 091665.0 2014.03020 BUILDING CHANGES 091665_1 5

BC Finance & Audit Committee Packet Pg. 28 of 77

DR

AFT

432006 11-07-14

Yes No

1a

1b

1

2

3

4

5

6

7

8

9

a

b

2

3

4

5

6

7a

7b

8a

8b

9

a

b

a

b

Yes No

10

11

a

b

10a

10b

11a

12a

12b

12c

13

14

15a

15b

16a

16b

a

b

12a

b

c

13

14

15

a

b

16a

b

17

18

19

20

For each "Yes" response to lines 2 through 7b below, and for a "No" responseto line 8a, 8b, or 10b below, describe the circumstances, processes, or changes in Schedule O. See instructions.

If "Yes," provide the names and addresses in Schedule O(This Section B requests information about policies not required by the Internal Revenue Code.)

If "No," go to line 13

If "Yes," describein Schedule O how this was done

(explain in Schedule O)

If there are material differences in voting rights among members of the governing body, or if the governing

body delegated broad authority to an executive committee or similar committee, explain in Schedule O.

Did the organization contemporaneously document the meetings held or written actions undertaken during the year by the following:

Were officers, directors, or trustees, and key employees required to disclose annually interests that could give rise to conflicts?

Form (2014)

Form 990 (2014) Page

Check if Schedule O contains a response or note to any line in this Part VI ���������������������������

Enter the number of voting members of the governing body at the end of the tax year

Enter the number of voting members included in line 1a, above, who are independent

~~~~~~

~~~~~~

Did any officer, director, trustee, or key employee have a family relationship or a business relationship with any other

officer, director, trustee, or key employee? ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Did the organization delegate control over management duties customarily performed by or under the direct supervision

of officers, directors, or trustees, or key employees to a management company or other person? ~~~~~~~~~~~~~~

Did the organization make any significant changes to its governing documents since the prior Form 990 was filed?

Did the organization become aware during the year of a significant diversion of the organization's assets?

Did the organization have members or stockholders?

~~~~~

~~~~~~~~~