financial accounting - himpub.com · preface the book on “financial accounting” is tailor-made...

TRANSCRIPT

Financial Accounting(As Per Revised Syllabus (CBCS) for Second Semester, B.Com. of All

Universities in Andhra Pradesh w.e.f. 2015-2016)

Prof. (Mrs) Prashanta AthmaProfessor,

Department of Commerce,Osmania University,

Hyderabad, Telangana State.

MUMBAI NEW DELHI NAGPUR BENGALURU HYDERABAD CHENNAI PUNE LUCKNOW AHMEDABAD ERNAKULAM BHUBANESWAR KOLKATA GUWAHATI

© AuthorNo part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form orby any means, electronic, mechanical, photocopying, recording and/or otherwise without the priorwritten permission of the publisher.

First Edition : 2016

Published by : Mrs. Meena Pandey for Himalaya Publishing House Pvt. Ltd.,“Ramdoot”, Dr. Bhalerao Marg, Girgaon, Mumbai - 400 004.Phone: 022-23860170/23863863, Fax: 022-23877178E-mail: [email protected]; Website: www.himpub.com

Branch Offices :

New Delhi : “Pooja Apartments”, 4-B, Murari Lal Street, Ansari Road, Darya Ganj,New Delhi - 110 002. Phone: 011-23270392, 23278631; Fax: 011-23256286

Nagpur : Kundanlal Chandak Industrial Estate, Ghat Road, Nagpur - 440 018.Phone: 0712-2738731, 3296733; Telefax: 0712-2721215

Bengaluru : No. 16/1 (Old 12/1), 1st Floor, Next to Hotel Highlands, Madhava Nagar,Race Course Road, Bengaluru - 560 001.Phone: 080-32919385; Telefax: 080-22286611

Hyderabad : No. 3-4-184, Lingampally, Besides Raghavendra Swamy Matham, Kachiguda,Hyderabad - 500 027. Phone: 040-27560041, 27550139; Mobile: 09390905282

Chennai : New-20, Old-59, Thirumalai Pillai Road, T. Nagar, Chennai - 600 017.Mobile: 9380460419

Pune : First Floor, "Laksha" Apartment, No. 527, Mehunpura, Shaniwarpeth(Near Prabhat Theatre), Pune - 411 030. Phone: 020-24496323/24496333;Mobile: 09370579333

Lucknow : House No 731, Shekhupura Colony, Near B.D. Convent School, Aliganj,Lucknow - 226 022. Mobile: 09307501549

Ahmedabad : 114, “SHAIL”, 1st Floor, Opp. Madhu Sudan House, C.G. Road, Navrang Pura,Ahmedabad - 380 009. Phone: 079-26560126; Mobile: 09377088847

Ernakulam : 39/176 (New No: 60/251) 1st Floor, Karikkamuri Road, Ernakulam,Kochi - 682011, Phone: 0484-2378012, 2378016; Mobile: 09344199799

Bhubaneswar : 5 Station Square, Bhubaneswar - 751 001 (Odisha).Phone: 0674-2532129, Mobile: 09338746007

Kolkata : 108/4, Beliaghata Main Road, Near ID Hospital, Opp. SBI Bank, Kolkata -700 010,Phone: 033-32449649, Mobile: 09883055590, 07439040301

Guwahati : House No. 15, Behind Pragjyotish College, Near Sharma Printing Press,P.O. Bharalumukh, Guwahati - 781009, (Assam).Mobile: 09883055590, 09883055536

DTP by : Rakhi

Printed at : M/s Sri Sai Art Printer Hyderabad. On behalf of HPH.

Dedicated to my Dad

Preface

The book on “Financial Accounting” is tailor-made to meet the requirements of contentsof the new syllabi of B.Com. Semester II of the Universities in Andhra Pradesh and alsoprovide requisite knowledge in Accounting.

An earnest and sincere attempt is made to present the information in a non-technical,simple and lucid manner so as to enable the reader to understand the subject with ease.

The book contains sufficiently a large number of illustrations for a better grasp in thesubject matter. Wherever necessary, working notes and explanations have been provided.

At the end of each Chapter, questions and problems are given for practice.

Suggestions for improvement of the book are solicited.

I express my heartfelt gratitude to my husband Mr. S. Chandra Babu, HR and LegalProfessional, who was a constant source of inspiration, support and encouragementthroughout the completion of the book.

I also thank the publishers for the timely publication and my special thanks toMr. Krishna Poojari for the keen interest taken by him in bringing out this book.

— Author

SyllabusKrishna University

Financial AccountingI. B.Com. General/CA/ASM/TAX (Semester II)

Paper 104 PPW: 06 Hours

Sr. No. Modules/UnitsUnit 1 Final Accounts

Meaning – Features – Manufacturing Account – Preparation of Trading Account,Profit and Loss Account and Balance Sheet with Adjustments – Problems.

Unit 2 Consignment AccountsConsignment – Features – Proforma Invoice – Account Sales – Del CredreCommission – Accounting Treatment in the Books of Consigner and Consignee –Valuation of Closing Stock – Normal and Abnormal Loss – Problems.

Unit 3 Joint Venture AccountsJoint Venture – Features – Difference between Joint Venture and Consignment –Accounting Procedure – Methods of Keeping Records – Problems.

Unit 4 DepreciationMethods of Depreciation - Straight line method - Diminishing balancing method –Sum of Digits Method - Problems.

Unit 5 Provisions and ReservesMeaning – Provision vs. Reserve – Preparation of Bad Debts Accounts – Provisionof Bad Debts Accounts – Provision for Bad and Doubtful Debts Accounts –Provision for Discount on Debtors Accounts – Provision for Discount on CreditorsAccounts – Repairs and Renewals Account – Problems.

SyllabusSri Venkateswara University

Financial Accounting – III. B.Com. General/CA/ASM/TAX (Semester II)

Paper 104 PPW: 06 Hours

Sr. No. Modules/UnitsUnit 1 Final Accounts And Rectification of Errors

Meaning – Features – Manufacturing Account – Preparation of Trading Account,Profit and Loss Account and Balance Sheet with Adjustments – Types of Errors –Rectification of Errors – Suspense Account – Problems.

Unit 2 Consignment AccountsConsignment – Features – Proforma Invoice – Account Sales – Del CredreCommission – Accounting Treatment in the Books of Consigner and Consignee –Valuation of Closing Stock – Normal and Abnormal Loss – Problems.

Unit 3 Joint Venture AccountsJoint Venture – Features – Difference between Joint Venture and Consignment –Accounting Procedure – Methods of Keeping Records – Problems.

Unit 4 DepreciationMethods of Depreciation – Straight Line Method – Diminishing Balancing Method –Problems.

Unit 5 Provisions and ReservesMeaning – Provision vs. Reserve – Preparation of Bad Debts Accounts – Provisionfor Bad and Doubtful Debts Accounts – Provision for Discount on DebtorsAccounts – Provision for Discount on Creditors Accounts – Provision for Repairsand Renewals Account – Problems.

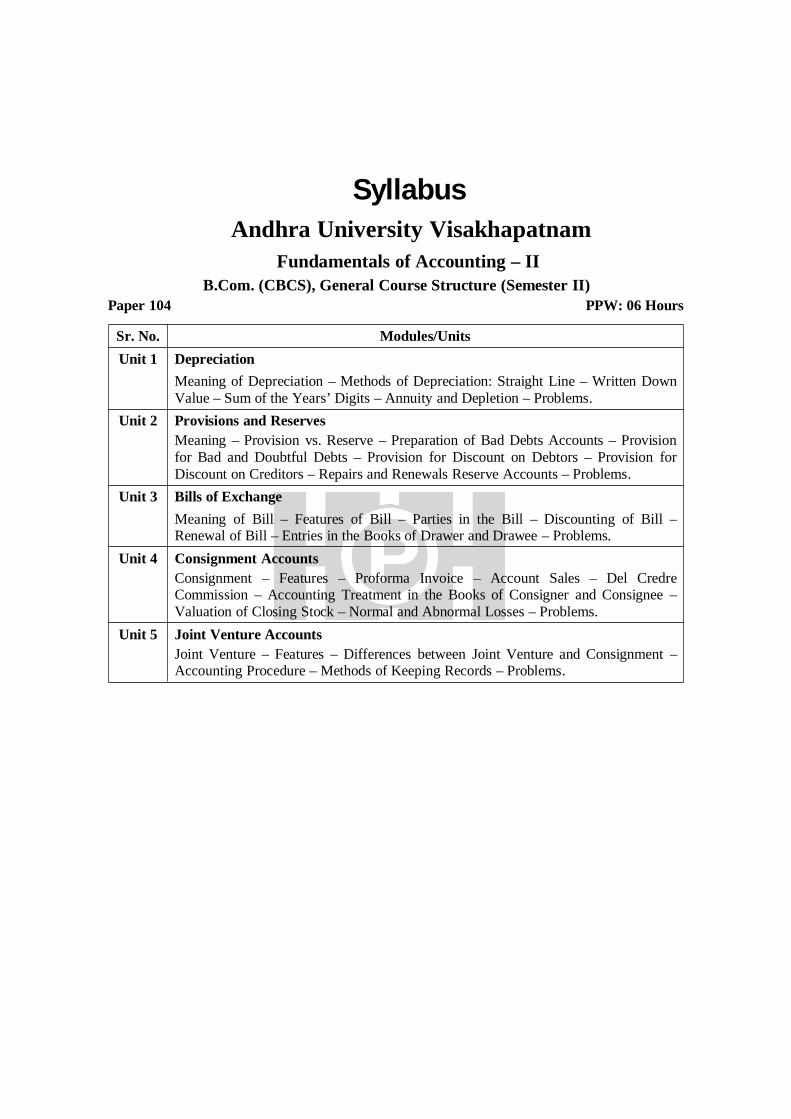

SyllabusAndhra University Visakhapatnam

Fundamentals of Accounting – IIB.Com. (CBCS), General Course Structure (Semester II)

Paper 104 PPW: 06 Hours

Sr. No. Modules/UnitsUnit 1 Depreciation

Meaning of Depreciation – Methods of Depreciation: Straight Line – Written DownValue – Sum of the Years’ Digits – Annuity and Depletion – Problems.

Unit 2 Provisions and ReservesMeaning – Provision vs. Reserve – Preparation of Bad Debts Accounts – Provisionfor Bad and Doubtful Debts – Provision for Discount on Debtors – Provision forDiscount on Creditors – Repairs and Renewals Reserve Accounts – Problems.

Unit 3 Bills of ExchangeMeaning of Bill – Features of Bill – Parties in the Bill – Discounting of Bill –Renewal of Bill – Entries in the Books of Drawer and Drawee – Problems.

Unit 4 Consignment AccountsConsignment – Features – Proforma Invoice – Account Sales – Del CredreCommission – Accounting Treatment in the Books of Consigner and Consignee –Valuation of Closing Stock – Normal and Abnormal Losses – Problems.

Unit 5 Joint Venture AccountsJoint Venture – Features – Differences between Joint Venture and Consignment –Accounting Procedure – Methods of Keeping Records – Problems.

SyllabusAcharya Nagarjuna University

Nagarjunanagar-522 510Fundamentals of Accounting – II

I Year B.Com. (CBCS), General (Semester II)Paper 104 PPW: 06 Hours

Sr. No. Modules /UnitsUnit 1 Depreciation

Meaning of Depreciation – Methods of Depreciation: Straight Line – Written DownValue – Sum of the Years’ Digits – Annuity and Depletion – Problems.

Unit 2 Provisions and ReservesMeaning – Provision vs. Reserve – Preparation of Bad Debts Account – Provisionfor Bad and Doubtful Debts – Provision for Discount on Debtors – Provision forDiscount on Creditors – Repairs and Renewals Reserve A/c – Problems.

Unit 3 Bills of ExchangeMeaning of Bill – Features of Bill – Parties in the Bill – Discounting of Bill –Renewal of Bill – Entries in the Books of Drawer and Drawee – Problems.

Unit 4 Consignment AccountsConsignment – Features – Proforma Invoice – Account Sales – Del CredreCommission – Accounting Treatment in the Books of Consigner and Consignee –Valuation of Closing Stock – Normal and Abnormal Losses – Problems.

Unit 5 Joint Venture AccountsJoint Venture – Features – Differences between Joint Venture and Consignment –Accounting Procedure – Methods of Keeping Records – Problems.

Contents

1. Final Accounts 1 – 46

2. Rectification of Errors 47 – 74

3. Consignment 75 – 108

4. Joint Venture 109 – 133

5. Bills of Exchange 134 – 162

6. Depreciation 163 – 184

7. Provisions and Reserves 185 – 206

1

Chapter

ObjectivesThe objectives of the study are to: Understand the concept of Final Accounts Grasp the treatment of adjustments Learn the preparation of Final Accounts

Structure Introduction Trading Account

Explanation to Certain Items Manufacturing Account Profit and Loss Account Balance Sheet Adjustments

Depreciation Bad Debts Provision for Bad and Doubtful Debts Provision for Discount on Debtors Provision for Discount on Creditors Outstanding Expenses Prepaid Expenses Income Earned But not Received Unearned Income Interest on Capital Interest on Drawings Loss of Stock by Fire/Theft

Final Accounts

2 Financial Accounting

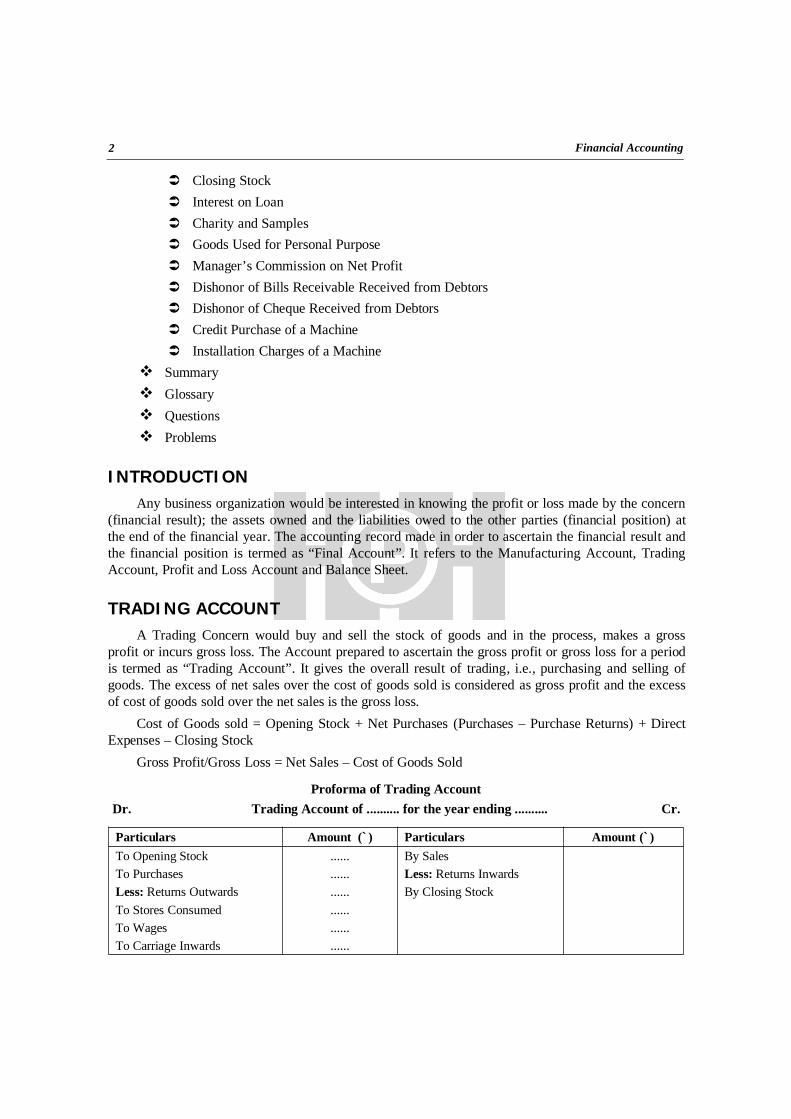

Closing Stock Interest on Loan Charity and Samples Goods Used for Personal Purpose Manager’s Commission on Net Profit Dishonor of Bills Receivable Received from Debtors Dishonor of Cheque Received from Debtors Credit Purchase of a Machine Installation Charges of a Machine

Summary Glossary Questions Problems

INTRODUCTIONAny business organization would be interested in knowing the profit or loss made by the concern

(financial result); the assets owned and the liabilities owed to the other parties (financial position) atthe end of the financial year. The accounting record made in order to ascertain the financial result andthe financial position is termed as “Final Account”. It refers to the Manufacturing Account, TradingAccount, Profit and Loss Account and Balance Sheet.

TRADING ACCOUNTA Trading Concern would buy and sell the stock of goods and in the process, makes a gross

profit or incurs gross loss. The Account prepared to ascertain the gross profit or gross loss for a periodis termed as “Trading Account”. It gives the overall result of trading, i.e., purchasing and selling ofgoods. The excess of net sales over the cost of goods sold is considered as gross profit and the excessof cost of goods sold over the net sales is the gross loss.

Cost of Goods sold = Opening Stock + Net Purchases (Purchases – Purchase Returns) + DirectExpenses – Closing Stock

Gross Profit/Gross Loss = Net Sales – Cost of Goods Sold

Proforma of Trading AccountDr. Trading Account of .......... for the year ending .......... Cr.

Particulars Amount (`) Particulars Amount (`)To Opening Stock ...... By SalesTo Purchases ...... Less: Returns InwardsLess: Returns Outwards ...... By Closing StockTo Stores Consumed ......To Wages ......To Carriage Inwards ......

3Final Accounts

To Cartage Inwards ......To Octroi ......To Fuel ......To Motive Power ......To Import Duty ......To Dock Charges ......To Clearing Charges ......To Royalty ......To Manufacturing Expenses ......To Depreciation on Machinery ......To Factory Rent ......To Factory Lighting ......To Factory Heating ......To Factory Insurance ......To Oil, Gas and Water ......To Gross Profit ......

Explanation to Certain Items Opening Stock: It means the goods lying unsold by the businessman at the beginning of the

financial/accounting year. Closing Stock: It means the goods lying unsold by the businessman at the end of the

financial/accounting year which would become the opening stock for the next accounting year. Purchases: It includes the total purchase of goods for resale, i.e., cash and credit purchases.

Net purchases should be taken which is the net of purchase returns, i.e., purchases –purchase returns.

Wages: It is the amount paid to the workers in the factory. If wages are paid for thepurchase of fixed asset, it should be added to the concerned asset.

Customs and Import Duty: It is the expenditure incurred when the goods are importedfrom outside the country.

Freight, Carriage and Cartage: When these expenses are incurred on purchases, theybecome the direct expenses and hence appear in Trading Account. If they are incurred onsales, then such expenses are treated as indirect expenses and taken in the Profit and LossAccount.

Royalty: It is the amount paid to the owners of mines, patent for using their rights, which isa direct expense. In case it is based on sales, then it would appear in the Profit and LossAccount.

Packing Material: It is used for packing the goods purchased for bringing them to thebusiness concern or incurred for converting them into a saleable state which are consideredto be direct expenses and hence taken in Trading Account. Whereas, if it is incurred formaking the product attractive for sale, it would be then an indirect expense which wouldappear in Profit and Loss Account.

4 Financial Accounting

Illustration 1

From the following information, prepare the Trading Account for the year ending 31st March2015.

Cost of goods sold ` 7,79,700; Sales ` 8,55,000; Closing Stock ` 60,500

Solution

Dr. Trading A/c for the year ending 31st March 2015 Cr.

Particulars Amount (`) Particulars Amount (`)

To Cost of Goods Sold 7,79,700 By Sales 8,55,000To Gross Profit (transferred toP & L A/c)

75,300

8,55,000 8,55,000

Note: Cost of goods sold= Opening Stock + Purchases – Closing Stock + Direct Expenses. Therefore,closing stock is not taken as it is already adjusted in cost of goods sold.

Illustration 2

From the following information, prepare the Trading Account for the year ending 31st March2015.

Adjusted Purchases ` 7,79,700; Sales ` 8,55,000; Closing Stock ` 60,500; Freight and CartageInward ` 4,700, Wages ` 3,500; Freight and Cartage Outwards ` 2,900.

Solution

Dr. Trading A/c for the year ending 31st March 2015 Cr.

Particulars Amount (`) Particulars Amount (`)

To Adjusted Purchases 7,79,700 By Sales 8,55,000To Freight and Cartage Inward 4,700To Freight and Cartage Inward 3,500To Gross Profit (transferred toP & L A/c)

67,100

8,55,000 8,55,000

Notes:

1. Adjusted Purchases = Opening Stock + Purchases – Closing Stock + Direct Expenses. Therefore,closing stock is not taken as it is already adjusted in Adjusted Purchases.

2. Freight and Cartage outwards is on sales and hence will appear in Profit and Loss Account (DebitSide) and not in Trading Account.

5Final Accounts

Illustration 3From the following information, prepare the Trading Account for the year ending on 31st March 2015.Opening Stock ` 90,000; Credit Purchases ` 6,50,000; Cash Purchases ` 60,000; Returns

Outward ` 3,000; Cash Sales ` 36,000; Credit Sales ` 8,20,000; Cartage Inwards ` 400; Closing Stock` 60,400; Freight Inwards ` 1,300; Wages and Salaries ` 3,600; Carriage Inwards ` 1,400; ReturnsInwards ` 15,000.

SolutionDr. Trading A/c for the year ending 31st March 2015 Cr.

Particulars Amount(`) Particulars Amount (`)

To Opening Stock 90,000 By SalesTo Purchases: Cash 36,000

Cash 60,000 Credit 8,20,000Credit 6,50,000 8,56,000

7,10,000 Less: Sales Returns 15,000 8,41,000Less: Returns Outward 3,000 7,07,000 By Closing Stock 60,400To Wages and Salaries 3,600To Carriage Inwards 1,400To Freight Inwards 1,300To Cartage Inwards 400To Gross Profit(transferred to P & L A/c)

97,700

9,01,400 9,01,400

Illustration 4Prepare a Trading Account for the year ended as at March 31, 2015 from the following

particulars.Stock (April 1, 2014) ` 2,000; Credit Purchases ` 20,000; Cash Purchases ` 30,000; Purchase

Returns ` 1,000; Cash Sales ` 50,000; Credit Sales ` 20,000; Loss of Goods by Fire ` 1,500; OctroiDuty ` 750; Drawing of Goods by Proprietor ` 500; Clearing Charges ` 250; Goods Given for Charity` 100; Closing Stock ` 3,500; Railway Freight ` 1,500; Wages ` 500; Carriage Inwards ` 100;Returns Inwards ` 2,000; Goods Given in Samples ` 100; Commission on Purchases ` 200; GoodsSent on Consignment at Cost ` 1,500.

SolutionDr. Trading A/c for the year ending 31st March 2015 Cr.Particulars Amount (`) Particulars Amount (`)To Opening Stock By SalesTo Purchases: Cash 50,000

Cash 30,000 Credit 20,000Credit 20,000 70,000

50,000 Less: Sales Returns 2,000 68,000

6 Financial Accounting

Less: Returns Outward 1,000 49,000 By Goods Sent onConsignment

1,500

Goods WithdrawnCharity

500100

By Profit and Loss A/c(Loss by Fire)

1,500

Sample 100 700 By Closing Stock 3,50048,300

To Railway Freight 1,500To Octroi Duty 750To Clearing Charges 250To Wages 500To Carriage Inwards 100To Commission onPurchases

200

To Gross Profit(transferred to P & L A/c)

22,900

74,500 74,500

MANUFACTURING ACCOUNTWhen a concern is a manufacturing concern, the manufacturer purchases the raw materials and

converts them into finished goods and sells the finished products to the customers. While convertingthe raw material into the finished products, the manufacturer incurs various expenses and he would beinterested in ascertaining the cost of the goods manufactured during a particular period. Hence,Manufacturing Account is prepared. The opening and closing stock of goods may consist of rawmaterials, work-in-progress and finished goods.

Proforma of a Manufacturing AccountDr. Manufacturing Account of .......... for the year ending .......... Cr.

Particulars Amount (`) Particulars Amount (`)

To Opening Stock By Sales ......Raw Materials ...... Less: Returns Inwards ......Work-in-progress ...... By Closing Stock ......

To Purchase of Raw MaterialLess: Returns Outwards

......

......By Trading Account (Cost ofManufacture transferred to TradingAccount)

......

To Wages ......To Freight ......To Import Duty ......To Octroi ......To Coal, Gas and Water ......To Factory Rent ......To Motive Power ......To Factory Insurance ......To Consumable Stores ......

...... ......

7Final Accounts

In case of a Manufacturing Concern, Trading Account would appear as follows:

Dr. Trading Account of .......... for the year ending .......... Cr.

Particulars Amount (`) Particulars Amount (`)

To Opening Stock ...... By Sale of Finished Goods ......Finished Goods ...... Less: Returns Inwards ......

To Manufacturing Account ...... By Closing Stock of Finished Goods ......To Purchase of Finished Goods ......

Less: Returns Outwards ......To Direct Expenses on FinishedGoods ......To Gross Profit ......

...... ......

Illustration 5

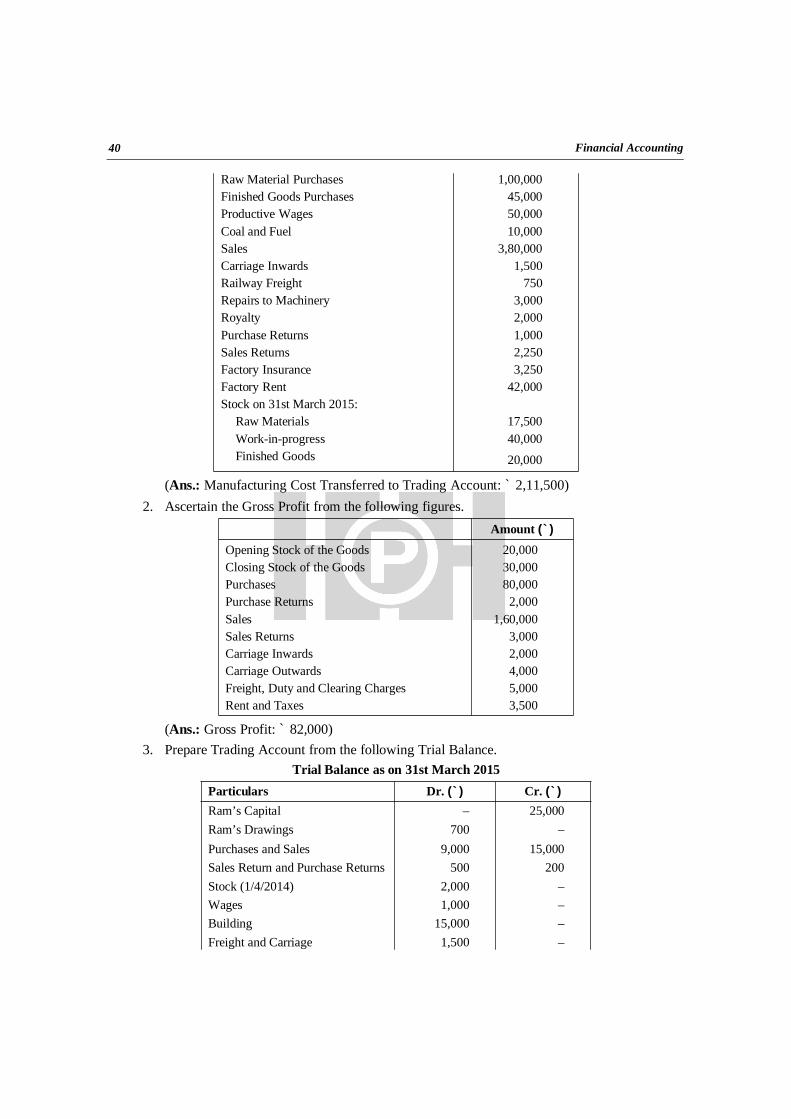

Following are the balances extracted from the books of M/s Harish Motors as on 31st March2015, you are required to prepare the Manufacturing Account for the year ended on that date.

Extracts from the books of M/s Harish Motors as on 31st March 2015

Particulars (`)

Raw Materials (Opening Stock) 45,000Work-in-progress (Opening Stock) 30,000Finished Goods (Opening Stock) 40,000

Raw Material Purchases 1,10,000Finished Goods Purchases 55,000Productive Wages 60,000Coal and Fuel 12,000Sales 3,50,000Carriage Inwards 2,000Railway Freight 1,000Repairs to Machinery 3,250Royalty 2,250Purchase Returns 900Sales Returns 2,000Factory Insurance 3,000Factory Rent 45,000Stock on 31st March 2015:

Raw materials 18,000Work-in-progress 42,000Finished Goods 23,000

8 Financial Accounting

Solution

Dr. M/s Harish Motors Manufacturing Account for the year ended March 31, 2015 Cr.

Particulars Amount (`) Particulars Amount (`)To Opening Stock By Closing Stock

Raw- Material 45,000 Raw- Materials 18,000Work-in-progress 30,000 75,000 Work-in-progress 42,000 60,000

To Purchases 1,10,000 By Manufacturing Cost(transferred to TradingAccount)

2,52,600

Less: Returns 900 1,09,100To Productive Wages 60,000To Coal and Fuel 12,000To Carriage Inwards 2,000To Railway Freight 1,000To Repairs toMachinery

3,250

To Royalty 2,250To Factory Insurance 3,000To Factory Rent 45,000

3,12,600 3,12,600

Note: Stock and Purchase of Finished Goods; Sales and Sales Returns would appear in TradingAccount and not in Manufacturing Account.

PROFIT AND LOSS ACCOUNTProfit and Loss Account is prepared to ascertain the net profit or net loss of an organization. The

excess of the amount on the credit side over the debit side of the account is termed as Net Profit and itis a case of Net Loss when the total of the amount on the debit side exceed the credit side. Net Profitincreases the owner’s equity and hence added to capital, whereas Net Loss reduces owner’s equity andtherefore deducted from capital.

The items on the debit side of the Profit and Loss Account may be classified into:(a) Management Expenses: Salaries to the employees, office rent, postage and telegram

expenses, telephone charges, lighting expenses of the office, trade expenses, audit fees,director’s fees, insurance and taxes, repairs, office rent, law charges, subscriptions to tradecommittees, etc.

(b) Financial Expenses: Interest on capital, interest on loan, bad debts, discount on debtors,bank expenses, charity, discount on bills discounted, etc.

(c) Selling and Distribution Expenses: Advertisement expenses, export duty, carriage outward,commission to sales agents, salaries to selling personnel, insurance of goods sold, packingexpenses, transportation charges, sales tax, remuneration to sales agents, etc.

(d) Other Expenses: Depreciation on office furniture, vehicles and other indirect expenses.

9Final Accounts

The items on the credit side of the Profit and Loss Account are Gross Profit brought forwardfrom the Trading Account, discount received, rent received, commission received, interest oninvestments received, interest on bank deposits, interest on drawings, bad debts recovered, profit onjoint venture, rent from subletting, etc.

Illustration 6

A book-keeper has submitted you the following Trial Balance.

Particulars Dr (`) Cr (`)Capital – 7,600Cash in Hand 50 –Purchases 8,500 –Sales – 11,000Cash at Bank 880 –Fixtures and Fittings 200 –Freehold Premises 1,300Lighting and Heating 50Bills Receivable 800Returns Inward 100Salaries 1,200Creditors – 2,000Debtors 5,000 –Stock on April 1, 2014 3,500 –Printing 200 –Bills Payable – 1,200Rates, Taxes and Insurance 120 –Discount Received – 420Discount Allowed 320 –

22,220 22,220

Stock on March 31, 2015 was valued at ` 2,000. You are required to prepare a Trading and Profitand Loss A/c for the year ended March 31, 2015.

Solution

Dr. Trading and Profit and Loss Account for the year ended 31st March 2015 Cr.

Particulars Amount (`) Particulars Amount (`)To Opening Stock 3,500 By Sales 11,000To Purchases 8,500 Less: Returns 100 10,900To Gross Profit c/d 900 By Closing Stock 2,000

12,900 12,900

10 Financial Accounting

To Salaries 1,200 By Gross Profit b/d 900To Lighting and Heating 50 By Discount Received 420To Printing 200 By Net Loss 570To Rates, Taxes and Insurance 120To Discount Allowed 320

1,890 1,890

BALANCE SHEETThe financial position of the business as on a particular date is represented in the Balance Sheet.

It is a statement showing the balances of all the ledger accounts as at the end of the financial year. Itconsists of assets owned and liabilities owing. It is a sheet of balances of all the real and personalaccounts.

Financial transactions that take place in a business concern are recorded in the Journal and thenposted to the Ledger from the Journal. Later, the balances of Ledger are recorded in the Trial Balance.

From the Trial Balance, the balances of Nominal Accounts are transferred to the TradingAccount and the Profit and Loss Account. The balances of Real and Personal Accounts from the TrialBalance are taken in the Balance Sheet.

The Gross Profit or Gross Loss in the Trading Account is transferred to the Profit and LossAccount and the Net Profit/Net Loss in the Profit and Loss Account is transferred to the Balance Sheet.Thus, the Balance Sheet consists of the ledger accounts directly taken from the Trial Balance andcertain items indirectly through the gist (Net Profit/Net Loss) of the Profit and Loss Account. Hence,the Balance Sheet is a summary of the whole of the accounting record. The two statements, viz.,Trading and the Profit and Loss Account (Income Statement) and Balance Sheet together are termedas ‘Final Accounts’.

There are no hard and fast rules for the order of writing assets and liabilities in case of a soletrader concern and partnership firms. But still, the Balance Sheet is prepared either according to theOrder of Permanence or Order of Liquidity. Arrangement of assets and liabilities in any of these twoorders is called as “Marshalling of Assets and Liabilities”. The proforma of Profit and Loss Accountand Balance Sheet are already learnt in the earlier chapter.

ADJUSTMENTSAdjustments are the transactions which are related to the Accounting Period for which Final

Accounts are prepared but are not taken in the Trial Balance of that period due to the reason that eitherthey are not recorded or recorded not completely. Sometimes, they are recorded and appear in TrialBalance but they do not belong to that Accounting Period of the Final Accounts. Therefore, thesetransactions have to be adjusted by making Adjustment Entries at the time of preparing the FinalAccounts.

Adjustment Entries recorded appear at two places – one in Trading and Profit and Loss Accountand the other in Balance Sheet. Sometimes, the double effect would be in Balance Sheet itself or inTrading and Profit and Loss Account itself. The point to be remembered is that if one record ofadjustment is debit the other record must be credit.

11Final Accounts

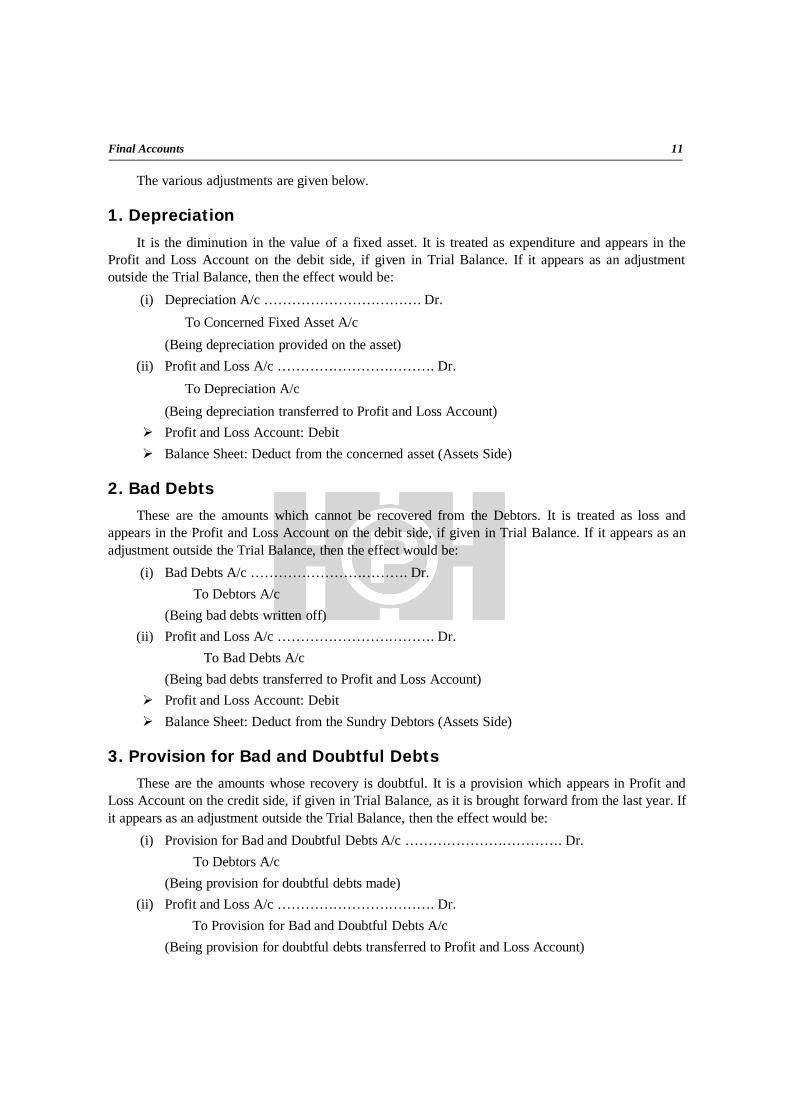

The various adjustments are given below.

1. DepreciationIt is the diminution in the value of a fixed asset. It is treated as expenditure and appears in the

Profit and Loss Account on the debit side, if given in Trial Balance. If it appears as an adjustmentoutside the Trial Balance, then the effect would be:

(i) Depreciation A/c ……………………………. Dr.To Concerned Fixed Asset A/c

(Being depreciation provided on the asset)(ii) Profit and Loss A/c ……………………………. Dr.

To Depreciation A/c(Being depreciation transferred to Profit and Loss Account)

Profit and Loss Account: Debit Balance Sheet: Deduct from the concerned asset (Assets Side)

2. Bad DebtsThese are the amounts which cannot be recovered from the Debtors. It is treated as loss and

appears in the Profit and Loss Account on the debit side, if given in Trial Balance. If it appears as anadjustment outside the Trial Balance, then the effect would be:

(i) Bad Debts A/c ……………………………. Dr.To Debtors A/c

(Being bad debts written off)(ii) Profit and Loss A/c ……………………………. Dr.

To Bad Debts A/c(Being bad debts transferred to Profit and Loss Account)

Profit and Loss Account: Debit Balance Sheet: Deduct from the Sundry Debtors (Assets Side)

3. Provision for Bad and Doubtful DebtsThese are the amounts whose recovery is doubtful. It is a provision which appears in Profit and

Loss Account on the credit side, if given in Trial Balance, as it is brought forward from the last year. Ifit appears as an adjustment outside the Trial Balance, then the effect would be:

(i) Provision for Bad and Doubtful Debts A/c ……………………………. Dr.To Debtors A/c

(Being provision for doubtful debts made)(ii) Profit and Loss A/c ……………………………. Dr.

To Provision for Bad and Doubtful Debts A/c(Being provision for doubtful debts transferred to Profit and Loss Account)

12 Financial Accounting

Profit and Loss Account: Debit Balance Sheet: Deduct from the Sundry Debtors (Assets Side)

Alternatively, in the Profit and Loss Account, the difference between the provision given in theTrial Balance (opening balance) and the adjustment provision would be accounted for. If the TrialBalance provision is more than the Adjustment provision, then the difference would appear on thecredit side of the Profit and Loss Account and vice versa.

Provision for Doubtful Debts would be ascertained after deducting the amount of adjustment baddebts from the Sundry Debtors.

4. Provision for Discount on DebtorsIt is calculated after deducting adjustment bad debts and provision for bad and doubtful debts

from the Sundry Debtors. It is a provision which appears in the Profit and Loss Account on the creditside, if given in Trial Balance, as it is brought forward from the last year. If it appears as an adjustmentoutside the Trial Balance, then the effect would be:

(i) Provision for Discount on Debtors A/c ……………………………. Dr.To Debtors A/c

(Being provision for discount on debtors made)(ii) Profit and Loss A/c ……………………………. Dr.

To Provision for Discount on Debtors A/c(Being provision for discount on debtors transferred to Profit and Loss Account)

Profit and Loss Account: Debit Balance Sheet: Deduct from the Sundry Debtors (Assets Side)

5. Provision for Discount on CreditorsIt is the discount earned from the creditors. It is the discount on the creditors of this year, which

would be received in the next year. As it relates to the current year, it must be recorded in the currentyear Profit and Loss Account. Hence, provision for discount on creditors account is debited and profitand loss account is credited.

(i) Creditors A/c ……………………………. Dr.To Provision for Discount on Creditors A/c

(Being provision for discount on creditors made)(ii) Provision for Discount on Creditors A/c ……………………………. Dr.

To Profit and Loss A/c(Being provision for discount on creditors transferred to Profit and Loss Account)

Profit and Loss Account: Credit Balance Sheet: Deduct from the Sundry Creditors (Liabilities Side)

6. Outstanding ExpensesThese are the expenses which relate to the current financial year but not yet paid. Normally,

expenses of the current month are paid in the first week of next month. Therefore, some expenses

13Final Accounts

remain outstanding at the time of preparing the final accounts for the financial year. It is treated as aliability and appears in the Balance Sheet, if given in Trial Balance. If it appears as an adjustmentoutside the Trial Balance, then the effect would be:

(i) Concerned Expenses A/c ……………………………. Dr.To Outstanding Expenses A/c

(Being the entry for outstanding expenses)(ii) Profit and Loss A/c ……………………………. Dr.

To Concerned Expenses A/c(Being expenses transferred to Profit and Loss Account)

Trading and Profit and Loss Account: Add to the concerned expenses (Debit Side) Balance Sheet: Liability

7. Prepaid ExpensesThese are the unexpired expenses which relate to the next financial year, but paid during the

current financial year. It is treated as an asset and appears in the Balance Sheet, if given in TrialBalance. If it appears as an adjustment outside the Trial Balance, then the effect would be:

(i) Prepaid Expenses A/c ……………………………. Dr.To Concerned Expenses A/c

(Being the entry for prepaid expenses)(ii) Concerned Expenses A/c ……………………………. Dr.

To Profit and Loss A/c(Being expenses transferred to Profit and Loss Account)

Trading and Profit and Loss Account: Deduct from the concerned expenses (Debit Side) Balance Sheet: Asset

8. Income Earned But Not ReceivedWhen the income is earned in the current financial year, but not yet received, then such an item is

treated as an asset and appears in the Balance Sheet, if given in Trial Balance. If it appears as anadjustment outside the Trial Balance, then the effect would be:

(i) Income Earned A/c ……………………………. Dr.To Concerned Income A/c

(Being the entry for income earned)(ii) Concerned Income A/c ……………………………. Dr.

To Profit and Loss A/c(Being the income transferred to Profit and Loss Account)

Profit and Loss Account: Add to the concerned income (Credit Side) Balance Sheet: Asset

14 Financial Accounting

9. Unearned IncomeIt is the income which is received in the current financial year, but the services for which will be

rendered in the next financial year. Such an item is treated as a liability and appears in the BalanceSheet, if given in Trial Balance. If it appears as an adjustment outside the Trial Balance, then the effectwould be:

(i) Concerned Income A/c ……………………………. Dr.To Income Received in Advance A/c

(Being the entry for unearned income)(ii) Profit and Loss A/c ……………………………. Dr.

To Concerned Income A/c(Being the income transferred to Profit and Loss Account)

Profit and Loss Account: Deduct from the concerned income (Credit Side) Balance Sheet: Liability

10. Interest on CapitalIt is a financial expenditure and appears in Profit and Loss Account on the debit side, if given in

Trial Balance. If it appears as an adjustment outside the Trial Balance, then the effect would be:(i) Interest on Capital A/c ……………………………. Dr.

To Capital A/c(Being interest on capital provided for)

(ii) Profit and Loss A/c ……………………………. Dr.To Interest on Capital A/c

(Being interest on capital transferred to Profit and Loss Account) Profit and Loss Account: Debit Balance Sheet: Added to the Capital (Liabilities Side)

11. Interest on DrawingsIt is a gain and appears in Profit and Loss Account on the credit side, if given in Trial Balance. If

it appears as an adjustment outside the Trial Balance, then the effect would be:(i) Drawings A/c ……………………………. Dr.

To Interest on Drawings A/c(Being interest on drawings provided for)

(ii) Interest on Drawings A/c ……………………………. Dr.To Profit and Loss A/c

(Being interest on drawings transferred to Profit and Loss Account) Profit and Loss Account: Credit Balance Sheet: Added to the drawings and deducted from the Capital (Liabilities Side)

15Final Accounts

12. Loss of Stock by Fire/TheftIn a business concern, the goods may be destroyed by fire or stolen by thieves. If the goods are

not insured, it would be a total loss and if they are insured, to the extent the Insurance Companyadmits would be recovered by the business concern and to the extent it is not admitted would be a lossto the concern. The effect would be:

(i) Loss by Fire/Theft A/c ……………………………. Dr.To Trading A/c

(Being loss of stock by fire/theft)If not insured(ii) Profit and Loss A/c ……………………………. Dr.

To Loss by Fire/Theft A/c(Being the transfer of loss to Profit and Loss Account)

Trading Account: Treat it as Closing Stock (Credit Side) Profit and Loss Account : Loss (Debit Side)

If insured and the Insurance Company admits the loss fully(ii) Insurance Company ……………………………. Dr.

To Loss by Fire/ Theft A/c(Being the transfer of loss to the Insurance Company)

Trading Account: Treat it as Closing Stock (Credit Side) Balance Sheet: Insurance Company as a Debtor (Assets Side)

If insured but the Insurance Company admits only a portion of such loss(ii) Insurance Company ……………………………. Dr.

Profit and Loss A/c ……………………………. Dr.To Loss by Fire/Theft A/c

(Being the transfer of loss to Profit and Loss Account) Trading Account: Treat it as Closing Stock (Credit Side: full amount)

When the stock is destroyed, closing stock is reduced to that extent and the gross profit isalso reduced. As gross profit is compared from period to period, it is necessary to eliminateabnormal losses and hence, the loss of stock is taken as closing stock reversing the earliereffect.

Profit and Loss Account: Loss (Debit Side: to the extent not admitted by the InsuranceCompany)

Balance Sheet: Insurance Company as a Debtor (Assets Side: to the extent admitted by theInsurance Company)

13. Closing StockIt is the stock which is not yet sold and remaining with the business concern at the end of the

accounting period. It will be treated as an asset and appears in the Balance Sheet, if given in Trial

16 Financial Accounting

Balance. Normally, Closing Stock is given as an adjustment. But, sometimes, when the purchases areadjusted, opening stock does not appear in Trial Balance instead Closing Stock is given in TrialBalance. In such a case, adjusted purchases are taken in the Trading Account and Closing Stockappears in the Balance Sheet.

Adjusted Purchases = Opening Stock + Net Purchases – Closing StockIf Closing Stock appears as an adjustment outside the Trial Balance, then the effect would be:(i) Closing Stock A/c ……………………………. Dr.

To Trading A/c(Being closing stock brought into the books)

Trading Account: Credit Balance Sheet: Asset

14. Interest on LoanIt is a financial expenditure and appears in Profit and Loss Account on the debit side, if given in

Trial Balance. If it appears as an adjustment outside the Trial Balance, then the effect would be:(i) Interest on Loan A/c ……………………………. Dr.

To Loan A/c(Being interest on loan provided for)

(ii) Profit and Loss A/c ……………………………. Dr.To Interest on Loan A/c

(Being interest on loan transferred to Profit and Loss Account) Profit and Loss Account: Debit Balance Sheet: Added to the Loan (Liabilities Side)

15. Charity and SamplesSometimes, the business concerns may distribute goods as charity or samples. Such an item is an

expenditure which appears in the Profit and Loss Account on the debit side, if given in Trial Balance.If it appears as an adjustment outside the Trial Balance, then the effect would be:

(i) Charity/Samples A/c ……………………………. Dr.To Purchases A/c

(Being goods used for charity and samples)(ii) Profit and Loss A/c ……………………………. Dr.

To Charity/Samples A/c(Being charity/samples transferred to Profit and Loss Account)

Trading Account: Deduct from Purchases (Debit Side) Profit and Loss Account: Expense (Debit Side)

17Final Accounts

16. Goods Used for Personal PurposeWhen the proprietor uses the goods from the business concern for his personal use, they should

be treated as Drawings. The effect would be:(i) Drawings A/c ……………………………. Dr.

To Purchases A/c(Being goods used for personal purpose)

Trading Account: Deduct from Purchases (Debit Side) Balance Sheet: Added to the drawings and deducted from the Capital (Liabilities Side)

17. Manager’s Commission on Net ProfitIt is an expenditure which appears in the Profit and Loss Account on the debit side, if given in

Trial Balance. If it appears as an adjustment outside the Trial Balance, then the effect would be:(i) Manager’s Commission A/c ……………………………. Dr.

To Outstanding Commission A/c(Being commission to manager recorded)

(ii) Profit and Loss A/c …………………………….............. Dr.To Manager’s Commission A/c

(Being manager’s commission transferred to Profit and Loss Account) Profit and Loss Account: Expense (Debit Side) Balance Sheet: Outstanding Commission (Liabilities Side)

Calculation of Manager’s Commission(a) Manager’s Commission given as a percentage of net profit before charging such commission:

Commission =100

CommissionofPercentageofitPrNet

(b) Manager’s Commission given as a percentage of net profit after charging such commission:

Commission =CommissionofPercentage100

CommissionofPercentageofitPrNet

18. Dishonor of Bills Receivable Received from DebtorsThe bills receivable received from the debtor, when dishonored, the position would be reversed.

The entry would be:(i) Debtors A/c ……………………………. Dr.

To Bills Receivable A/c(Being bills receivable received dishonored)

Balance Sheet: Add to Debtors (Assets Side) Balance Sheet: Deduct from Bills Receivable (Assets Side)

18 Financial Accounting

19. Dishonor of Cheque Received from DebtorsThe cheque received from the debtor, when dishonored, the position would be reversed. The

entry would be:(i) Debtors A/c ……………………………. Dr.

To Bank A/c(Being cheque received dishonored)

Balance Sheet: Add to Debtors (Assets Side) Balance Sheet: Deduct from Bank (Assets Side)

20. Credit Purchase of a MachineThe machinery purchased, when given in Trial Balance, it would appear as an asset in the

Balance Sheet. If the same is given as an adjustment, then the entry would be:(i) Machinery A/c ……………………………. Dr.

To Creditors A/c(Being credit purchase of a machine)

Balance Sheet: Add to Machine (Assets Side) Balance Sheet: Add to Creditors (Liabilities Side)

21. Installation Charges of a MachineThe installation charges of a machine purchased, when given in Trial Balance, it would be added

to the machine and appears as an asset in the Balance Sheet. If the same is given as an adjustment asalready included in wages, then the entry would be:

(i) Machinery A/c ……………………………. Dr.To Wages A/c

(Being credit purchase of a machine) Trading Account: Deduct from Wages (Debit Side) Balance Sheet: Add to Machine (Assets Side)

Illustration 7

From the following Ledger Accounts, prepare a Profit and Loss Account and Balance Sheet as on31st March 2015.

Ledger Accounts Debit (`) Credit (`)Salaries 10,000Establishment Expenses 7,000Wages Outstanding 3,000Unexpired Insurance 500Rent 25,000Plant and Machinery 40,000Land and Buildings 60,000

19Final Accounts

Adjustments:(a) Outstanding salaries amounted to ` 2,000.(b) Prepaid rent amount to ` 3,000.(c) The value of Plant and Machinery be depreciated by 10%.(d) Establishment Expenses for March 2015 are still to be paid amounted to ` 700.Prepare Profit and Loss Account and Balance Sheet.

Solution

Extracts of Profit and Loss Account for the year ended 31st March 2015

Particulars (`) Particulars (`)

To Salaries 10,000Add: Outstanding 2,000 12,000

To Rent 25,000Less: Prepaid 3,000 22,000

To Establishment Expenses 7,000Add: Outstanding 700 7,700

To Depreciation on Plant andMachinery 40,000*10/100 4,000

Extracts of Balance Sheet as on 31st March 2015

Liabilities (`) Assets (`)

Wages Outstanding 3,000 Unexpired Insurance 500Salaries Outstanding 2,000 Prepaid Rent 3,000Outstanding EstablishmentExpenses 700

Plant and Machinery 40,000

Less: Depreciation 4,000 36,000Land and Building 60,000

Illustration 8From the following Trial Balance of Krishang, prepare Trading and Profit and Loss Account for

the year ending 31st March 2015 and Balance Sheet as on that date.

Trial Balance of Krishang as on 31st March 2015

Particulars Debit (`) Credit (`)

Buildings 50,000Capital 96,000Purchases and Sales 15,000 40,450Opening Stock (1/4/2014) 8,000Debtors and Creditors 10,000 5,000Drawings 3,500

20 Financial Accounting

Sales Returns and Purchase Returns 1,000 500Freight 3,250Office Salaries 10,000Wages 1,200Postage and Telegrams 1,000Machinery 20,000Bills Receivable and Bills Payable 9,000 3,000Advertisement 4,000Cash in Hand 5,000Loose Tools 4,000

1,44,950 1,44,950

Adjustments:(a) Closing Stock was valued at ` 10,000.(b) Depreciate Building by 5% and Loose Tools are revalued at ` 3,500.(c) Interest on Capital is at 5% and on Drawings is at 10%.

Solution

Dr. Trading and Profit and Loss Account of Krishang for the year ending 31.03.2015 Cr.

Particulars Amount (`) Particulars Amount (`)To Opening Stock 8,000 By Sales 40,450To Purchases

15,000Less: Returns 1,000 39,450

Less: Returns 500 14,500 By Closing Stock 10,000To Freight 3,250To Wages 1,200To Gross Profit c/d 22,500

49,450 49,450To Office Salaries 10,000 By Gross Profit b/d 22,500To Postage and Telegrams 1,000 By Interest on

Drawings (@ 10 on `3,500)

350

To Advertisement 4,000To Depreciation:

Building 2,500Loose Tools (4,000 – 3,500) 500

To Interest on Capital (96,000* 5/100)

4,800

To Net Profit 5022,850 22,850

21Final Accounts

Balance Sheet of Krishang as on 31.03.2015

Particulars Amount(`)

Particulars Amount(`)

Capital 96,000 Cash in Hand 5,000Add: Interest (5%) 4,800 Machinery 20,000

1,00,800 Buildings 50,000Add: Net Profit 50 Less: Depreciation (5%) 2,500 47,500

1,00,850 Loose Tools 4,000Less: Drawings 3,500 Less: Depreciation 500 3,500Less: Interest on Drawing 350 97,000 Sundry Debtors 10,000Sundry Creditors 5,000 Bills Receivable 9,000Bills Payable 3,000 Closing Stock 10,000

1,05,000 1,05,000

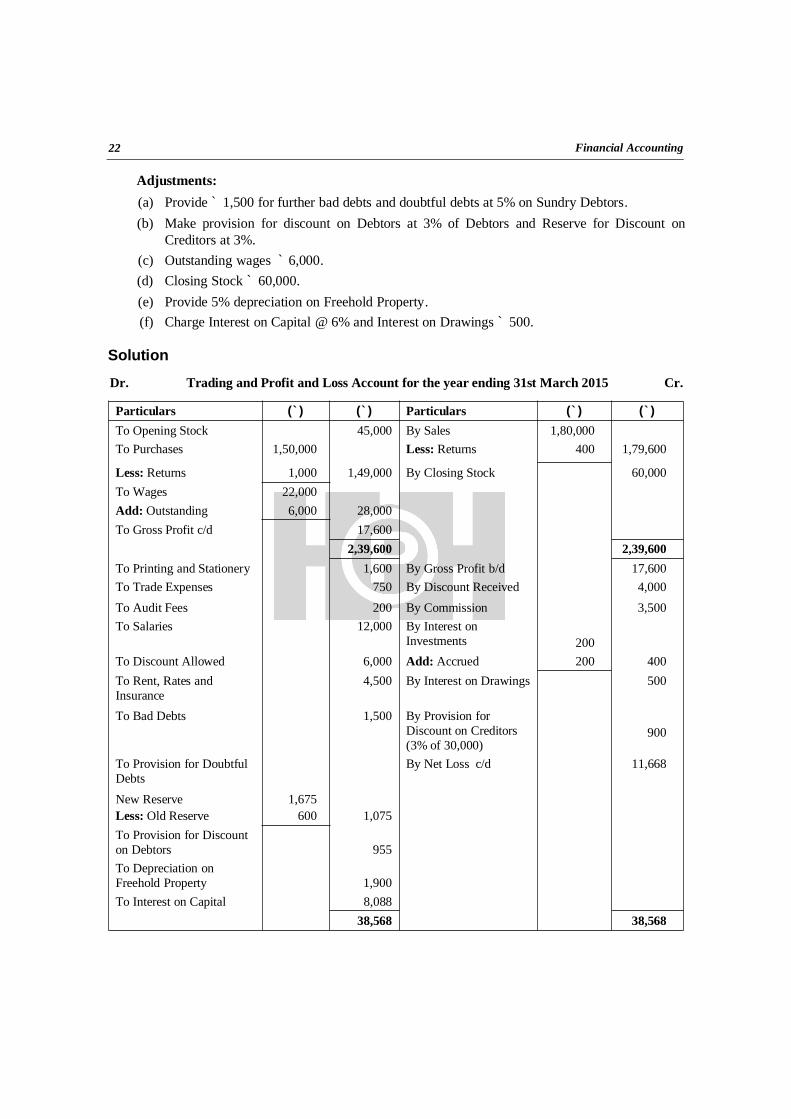

Illustration 9From the following Trial Balance, prepare Trading and Profit and Loss Account for the year

ended 31st March 2015 and Balance Sheet as on that date.

Trial Balance as on 31st March 2015

Particulars (`) Particulars (`)

Printing and Stationery 1,600 Bills Payable 10,000Trade Expenses 750 Provision for Doubtful Debts 600Freehold Property 38,000 Sales 1,80,000Cash at Bank 21,000 Discount Received 4,000Cash in Hand 3,000 Capital 1,34,800Purchases 1,50,000 Sundry Creditors 30,000Opening Stock 45,000 Interest on Investments 200Audit Fees 200 Commission Received 3,500Investments on 1/1/14 @ 10% 4,000 Purchase Returns 1,000Sundry Debtors 35,000Wages 22,000Salaries 12,000Income Tax 1,100Discount Allowed 6,000Sales Returns 400Bills Receivable 2,500Furniture 2,050Rent, Rates and Insurance 4,500Drawings 15,000

3,64,100 3,64,100

22 Financial Accounting

Adjustments:(a) Provide ` 1,500 for further bad debts and doubtful debts at 5% on Sundry Debtors.(b) Make provision for discount on Debtors at 3% of Debtors and Reserve for Discount on

Creditors at 3%.(c) Outstanding wages ` 6,000.(d) Closing Stock ` 60,000.(e) Provide 5% depreciation on Freehold Property.(f) Charge Interest on Capital @ 6% and Interest on Drawings ` 500.

Solution

Dr. Trading and Profit and Loss Account for the year ending 31st March 2015 Cr.

Particulars (`) (`) Particulars (`) (`)

To Opening Stock 45,000 By Sales 1,80,000To Purchases 1,50,000 Less: Returns 400 1,79,600

Less: Returns 1,000 1,49,000 By Closing Stock 60,000To Wages 22,000Add: Outstanding 6,000 28,000To Gross Profit c/d 17,600

2,39,600 2,39,600To Printing and Stationery 1,600 By Gross Profit b/d 17,600To Trade Expenses 750 By Discount Received 4,000To Audit Fees 200 By Commission 3,500To Salaries 12,000 By Interest on

Investments 200To Discount Allowed 6,000 Add: Accrued 200 400To Rent, Rates andInsurance

4,500 By Interest on Drawings 500

To Bad Debts 1,500 By Provision forDiscount on Creditors(3% of 30,000)

900

To Provision for DoubtfulDebts

By Net Loss c/d 11,668

New ReserveLess: Old Reserve

1,675600 1,075

To Provision for Discounton Debtors 955To Depreciation onFreehold Property 1,900To Interest on Capital 8,088

38,568 38,568

23Final Accounts

Balance Sheet as on 31st March 2015

Particulars (`) (`) Particulars (`) (`)

Bills Payable 10,000 Cash in Hand 3,000Sundry Creditors 30,000 Cash at Bank 21,000

Less: Discount onCreditors 900 29,100

Bills Receivable 2,500

Outstanding Wages 6,000 Closing Stock 60,000Capital 1,34,800 Sundry Debtors 35,000Add: Interest (6%) 8,088 Less: Bad Debts 1,500

1,42,888 33,500Less: Net Loss 11,668 Less: New Reserve (5%) 1,675

1,31,220 31,825Less: Drawings 15,000 Less: Discount on

Debtors (3%)955 30,870

Less: Interest on Drawings 500 Investment 4,000

1,15,720 Add: Interest Accrued 200 4,200Less: Income Tax 1,100 1,14,620 Freehold Property 38,000

Less: Depreciation (5%) 1,900 36,100Furniture 2,050

1,59,720 1,59,720

Illustration 10

The following Trial Balance is extracted from the books of Sri on March 31, 2015.

Trial Balance of Sri on March 31, 2015

Particulars Dr (`) Cr (`)Salaries 35,000General Expenses 7,000Taxes and Insurance 8,000Sundry Debtors 25,000Stock 46,000Purchases 60,000Wages 4,000Sales 1,50,000Bank Overdraft 17,000Commission 3,500Advertising 9,000Interest 2,000Furniture 60,000Building 60,000Motor Vehicle 80,000

24 Financial Accounting

Capital 1,25,000Bad Debts 2,000Provision for Doubtful Debts 2,500Loan 60,000Sundry Creditors 40,000

3,98,000 3,98,000

Adjustments:(a) Stock on hand on March 31, 2015 was estimated to be ` 40,000.(b) Depreciate: Building @ 6% and Motor Vehicles @ 10%.(c) ` 1,500 is due for interest on Loan.(d) Write off further ` 1,000 as Bad Debts and Provision for Bad Debts is to be made equal to

6% on Sundry Debtors.You are required to prepare Trading and Profit and Loss Account, Balance Sheet as on that date.

Solution

Dr. Trading and Profit and Loss Account of Sri for the year ending March 31, 2015 Cr.

Particulars (`) Particulars (`)

To Opening Stock 46,000 By Sales 1,50,000To Purchases 60,000 By Closing Stock 40,000To Wages 4,000To Gross Profit c/d 80,000

1,90,000 1,90,000To Salaries 35,000 By Gross Profit b/d 80,000To General Expenses 7,000 By Commission 3,500To Advertising 9,000To Depreciation:

Building 3,600Motor Vehicles 8,000

To Interest 2,000Add: Outstanding 1,500 3,500To Taxes and Insurance 8,000To Bad Debts 2,000Add: Further Bad Debts 1,000

3,000Add: New Provision 1,440

4,440Less: Old Provision 2,500 1,940To Net Profit 7,460

83,500 83,500

25Final Accounts

Balance Sheet of Sri as on 31st March 2015 (Order of Liquidity)

Liabilities (`) (`) Assets (`) (`)

Bank Overdraft 17,000 Cash in Hand 25,000Outstanding Interest 1,500 Less: Bad Debts 1,000

Sundry Creditors 40,000 24,000Loan 60,000 Less: New Reserve (6%) 1,440 22,560Capital 1,25,000 Stock 40,000Less: Net Loss 7,460 1,32,460 Furniture 60,000

Motor Vehicles 80,000Less: Depreciation 8,000 72,000Building 60,000Less: Depreciation (6%) 3,600 56,400

2,50,960 2,50,960

Illustration 11

The following is the Trial Balance of Murali Ltd. Prepare a Trading Account, Profit and LossAccount and Balance Sheet as on 31st March 2015.

Trial Balance of Murali Ltd. as on 31st March 2015

Particulars Dr (`) Cr (`)Sundry Creditors – 60,000Sundry Debtors 1,50,000 –Capital Account – 8,00,000Drawings 52,000 –Insurance 8,000 –General Expenses 35,000 –Salaries 1,45,000 –Patents 70,000 –Machinery 2,50,000 –Freehold Land 1,00,000 –Building 3,90,000 –Stock on 1/4/2014 58,000 –Carriage on Purchases 25,000 –Carriage on Sales 30,000 –Fuel and Power 48,000 –Wages 1,20,000 –Return Outwards – 10,000Return Inwards 5,000 –Sales – 10,00,000

26 Financial Accounting

Purchases 3,50,000 –Cash at Bank 29,000 –Cash in Hand 5,000 –

18,70,000 18,70,000

The following adjustments are to be made:(a) Stock on 31st March 2015 was valued at ` 70,000.(b) A Provision for Bad and Doubtful Debts is to be created to the extent of 5% on Sundry

Debtors.(c) Depreciate Machinery by 20% and Patents by 10%.(d) Wages include a sum of ` 10,000 spent on the erection of a Cycle Shed for employees and

customers.(e) Salaries for the Month of March 2015 amounting to ` 10,000 were unpaid.

Solution

Dr. Trading and Profit and Loss Account of Murali Ltd. for the year ending 31.03.2015 Cr.

Liabilities (`) (`) Assets (`) (`)

To Opening Stock 58,000 By Sales 10,00,000To Purchases 3,50,000 Less: Sales Returns 5,000 9,95,000

Add: Carriage onPurchases 25,000

By Closing Stock 70,000

Less: Return Outward 10,000 3,65,000To Wages 1,20,000Less: Wages for CycleShed 10,000 1,10,000To Fuel and Power 48,000To Gross Profit 4,84,000

10,65,000 10,65,000To Insurance 8,000 By Gross Profit 4,84,000To General Expenses 35,000To Salaries 1,45,000Add: Outstanding 10,000 1,55,000To Carriage on Sales 30,000To Provision for BadDebts

7,500

To Depreciation on:Machinery 50,000Patents 7,000

To Net Profit 1,91,5004,84,000 4,84,000

27Final Accounts

Balance Sheet of Murali Ltd as on 31.03.2015

Liabilities (`) (`) Assets (`) (`)

Capital 8,00,000 Freehold Land 1,00,000Add: Net Profit 1,91,500 Building 3,90,000

9,91,500 Machinery 2,50,000Less: Drawings 52,000 9,39,500 Less: Depreciation 50,000 2,00,000Sundry Creditors 60,000 Patents 70,000Outstanding Salaries 10,000 Less: Depreciation 7,000 63,000

Cycle Shed 10,000Stock 70,000Sundry Debtors 1,50,000Less: Provision for BadDebts 7,500 1,42,500Cash at Bank 29,000Cash in Hand 5,000

10,09,500 10,09,500

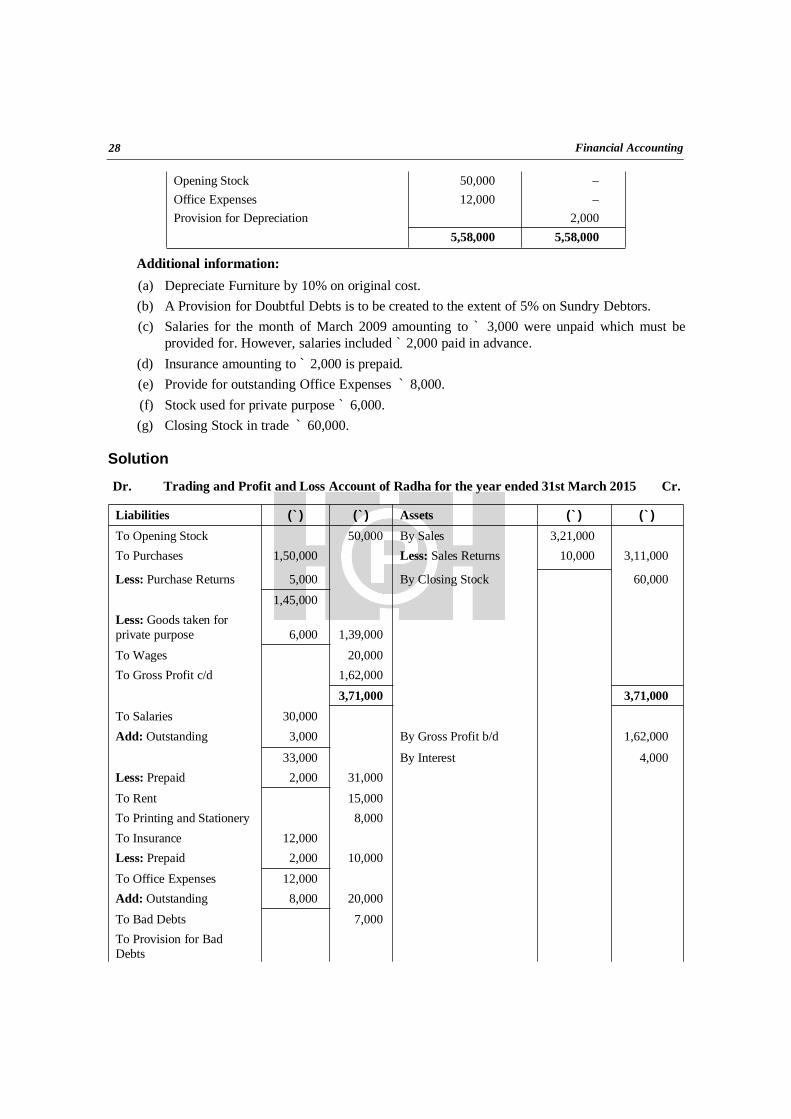

Illustration 12From the following Trial Balance of Radha, prepare a Trading and Profit and Loss Account for

the year ended 31st March 2015 and a Balance Sheet as on that date.

Trial Balance of Radha as on 31st March 2015

Particulars Dr (`) Cr (`)

Capital – 1,00,000Furniture 20,000 –Purchases 1,50,000 –Debtors 2,00,000 –Interest Earned – 4,000Salaries 30,000 –Sales – 3,21,000Purchase Returns – 5,000Wages 20,000 –Rent 15,000 –Sales Returns 10,000 –Bad Debt written off 7,000 –Creditors – 1,20,000Drawings 24,000 –Provision for Bad Debts – 6,000Printing and Stationery 8,000 –Insurance 12,000 –

28 Financial Accounting

Opening Stock 50,000 –Office Expenses 12,000 –Provision for Depreciation 2,000

5,58,000 5,58,000

Additional information:(a) Depreciate Furniture by 10% on original cost.(b) A Provision for Doubtful Debts is to be created to the extent of 5% on Sundry Debtors.(c) Salaries for the month of March 2009 amounting to ` 3,000 were unpaid which must be

provided for. However, salaries included ` 2,000 paid in advance.(d) Insurance amounting to ` 2,000 is prepaid.(e) Provide for outstanding Office Expenses ` 8,000.(f) Stock used for private purpose ` 6,000.(g) Closing Stock in trade ` 60,000.

Solution

Dr. Trading and Profit and Loss Account of Radha for the year ended 31st March 2015 Cr.

Liabilities (`) (`) Assets (`) (`)

To Opening Stock 50,000 By Sales 3,21,000To Purchases 1,50,000 Less: Sales Returns 10,000 3,11,000

Less: Purchase Returns 5,000 By Closing Stock 60,0001,45,000

Less: Goods taken forprivate purpose 6,000 1,39,000To Wages 20,000To Gross Profit c/d 1,62,000

3,71,000 3,71,000To Salaries 30,000Add: Outstanding 3,000 By Gross Profit b/d 1,62,000

33,000 By Interest 4,000Less: Prepaid 2,000 31,000To Rent 15,000To Printing and Stationery 8,000To Insurance 12,000Less: Prepaid 2,000 10,000To Office Expenses 12,000Add: Outstanding 8,000 20,000To Bad Debts 7,000To Provision for BadDebts

29Final Accounts

New 10,000Less: Old 6,000 4,000To Provision forDepreciation

2,000

To Net Profit 69,0001,66,000 1,66,000

Balance Sheet of Radha as on 31st March 2015

Liabilities (`) (`) Assets (`) (`)

Capital 1,00,000 Furniture (at cost) 20,000Add: Net Profit 69,000 Less: Provision for

Depreciation(` 2,000 + ` 2,000) 4,000 16,000

1,69,000 Stock in trade 60,000Less: Drawings(` 24,000 + ` 6,000) 30,000 1,39,000

Debtors 2,00,000

Creditors 1,20,000 Less: Provision for BadDebts 10,000 1,90,000

Outstanding Liabilities: Prepaid Expenses:Salaries 3,000 Salaries 2,000Office Expenses 8,000 11,000 Insurance 2,000 4,000

2,70,000 2,70,000

Illustration 13

The following is the Trial Balance of Sirish Marketing as on 31st March 2015. You are requiredto prepare the Trading and Profit and Loss Account for the year ended 31st March 2015 and BalanceSheet as on that date after making necessary adjustments.

Trial Balance of Sirish Marketing as on 31st March 2015

Particulars Dr (`) Cr (`)

Stock on 1/4/2015 6,20,000Purchases 15,00,000Sales 30,00,000Wages and Salaries 2,00,000Discount Received 15,000Carriage Inwards 45,000Bills Payable 2,50,000Insurance 32,000Creditors 10,00,000Trade Expenses 40,000Bills Receivable 3,50,000

30 Financial Accounting

Debtors 16,00,000Capital 9,50,000Furniture 1,20,000Commission 50,000Interest 25,000Cash in Hand 5,73,000

Cash at Bank 50,000Rent & Taxes 25,000Sale of Furniture on 31/3/15 15,000

52,30,000 52,30,000

Adjustments:(a) Stock on 31st March 2015 ` 8,00,000.(b) Furniture sold was appearing in the Balance Sheet on 31st March 2013 – ` 20,000(c) Included in the Debtors, an amount of ` 10,000 which is expected to realize not more than

50 paise in the rupee.

Solution

Dr. Trading and Profit and Loss Account of Sirish Marketing for the year ending 31.3.2015 Cr.

Particulars (`) Particulars (`)

To Opening Stock 6,20,000 By Sales 30,00,000To Purchases 15,00,000 By Closing Stock 8,00,000To Wages and Salaries 2,00,000To Carriage Inwards 45,000To Gross Profit c/d 14,35,000

38,00,000 38,00,000To Insurance 32,000 By Gross Profit b/d 14,35,000To Commission 50,000 By Discount Received 15,000To Interest 25,000To Trade Expenses 40,000To Rates and Taxes 25,000To Loss on Sale of Furniture 5,000To Bad Debts 5,000To Net Profit 12,68,000

14,50,000 14,50,000

Notes:1. When wages and salaries are given, the item would appear in Trading Account and if the same

item is given as salaries and wages, the item would appear in Profit and Loss Account.2. Debtors ` 10,000

Good Debts (10,000 × 0.50) ` 5,000Bad Debts ` 5,000

31Final Accounts

3. Cost of Furniture sold ` 20,000Sale Value ` 15,000Loss on Sale of Furniture ` 5.000

Balance Sheet of Sirish Marketing as on 31st March 2015 (Order of Liquidity)

Liabilities (`) (`) Assets (`) (`)

Bills Payable 2,50,000 Cash in Hand 5,73,000Sundry Creditors 10,00,000 Cash at Bank 50,000Capital 9,50,000 Debtors 16,00,000Add: Net Profit 12,68,000 22,18,000 Less: Bad Debts 5,000 15,95,000

Bills Receivable 3,50,000Closing Stock 8,00,000Furniture 1,20,000Less: Sale of furniture 20,000 1,00,000

34,68,000 34,68,000

Illustration 14

The following is the Trial Balance of Mr. Pradeep on 31st March 2015.

Trial Balance of Mr. Pradeep on 31st March 2015

Particulars Dr (`) Cr (`)

CapitalSundry CreditorsPlant & MachineryOffice Furniture and FittingsStock as on 1st April 2008Motor VanSundry DebtorsCash in HandCash at BankWagesSalariesPurchasesSalesBills payableBills ReceivableReturns InwardsProvision for Doubtful DebtsDrawingsReturn OutwardsRentFactory Lighting and Heating

––

5,000260

4,8001,2004,570

40650

15,0001,400

21,350––

720930

–700

–60080

4,0005,200

––––––––––

48,000560

––

250–

550––

32 Financial Accounting

InsuranceGeneral ExpensesBad DebtsDiscount

630100250650

–––

37058,930 58,930

The following adjustments are to be made:(a) Stock on 31st March 2015 ` 5,200.(b) 3 months factory lighting and heating is due, but not paid ` 30.(c) 5% depreciation to be written off on Furniture.(d) Write off further Bad Debts ` 70.(e) The provision for doubtful debts to be increased to ` 300 and provision for discount on

debtors @ 2% to be made.(f) During the year, Machinery was purchased for ` 2,000, but it was debited to Purchases

Account.You are required to prepare a Trading and Profit and Loss Account and the Balance Sheet.

Solution

Dr. Trading and Profit and Loss Account of Mr. Pradeep for the year ended 31.03.2015 Cr.

Particulars (`) (`) Particulars (`) (`)

To Opening Stock 4,800 By Sales 48,000To Purchases 21,350 Less: Return Inwards 930 47,070Less: Return Outwards 550 By Closing Stock 5,200

20,800Less: Purchase ofMachinery 2,000 18,800To Wages 15,000To Factory Lighting andHeating

80

Add: Outstanding 30 110To Gross Profit c/d 13,560

52,270 52,270To Salaries 1,400 By Gross Profit b/d 13,560To Rent 600 By Discount 370To Insurance 630To General Expenses 100To Discount 650To Bad Debts 250Add: Further Bad Debts 70 320To Provision forDoubtful Debts

New 300

33Final Accounts

Less: Old 250 50To Provision forDiscount on Debtors 84To Depreciation onFurniture 13To Net Profit 10,083

13,930 13,930

Balance Sheet of Mr. Pradeep as on 31.03.2015

Liabilities (`) (`) Assets (`) (`)

Capital 4,000 Plant and Machinery 5,000Add: Net Profit 10,083 Add: Purchases 2,000 7,000

14,083 Motor Van 1,200Less: Drawings 700 13,383 Office Furniture 260Bills Payable 560 Less: Depreciation @ 5% 13 247Sundry Creditors 5,200 Sundry Debtors 4,570Outstanding Factory

Lighting and Heating 30 Less: Further Bad Debts 70

4,500Less: Provision for BadDebts 300

4,200Less: Provision forDiscount on Debtors 84 4,116Closing Stock 5,200Bills Receivable 720Cash at Bank 650Cash in Hand 40

19,173 19,173

Illustration 15

Following is the Trial Balance of Smt. Ramya. Prepare Trading and Profit and Loss Account forthe year ended 31/03/2015 and a Balance Sheet as on that date.

Trial Balance of Smt. Ramya as on 31st March 2015

Particulars (`) (`)Capital 20,000Drawings 4,000

Stock (1/4/2014) 15,000Return Inwards 500Carriage Inwards 1,200Deposit with Ram 2,500

34 Financial Accounting

Return Outwards 800Carriage Outwards 750Loan to Chandra @ 5% p.a. on 1/4/2014 1,000Interest on the above loan 25Rent 800Rent Outstanding 100Purchases 13,000Debtors 5,000Creditors 2,000Provision for Doubtful Debts 1,000Advertisement Expenses 800Bad Debts 500Patents 645Sales 25,000Discount Allowed 300Wages 750Cash 80Goodwill 2,100

48,925 48,925

Adjustments:(a) The Manager of Smt. Ramya is entitled to a commission of 5% of the net profit calculated

after charging such commission.(b) Increase Bad Debts by ` 500. Provision for Doubtful Debts is to be created @ of 10% and

provision for discount on Debtors is to be @ 5% on Sundry Debtors.(c) Stock valued at ` 2,000 was destroyed by fire on 25/03/2015 but the insurance company

admitted a claim of ` 1,000 only and paid it in June 2010.(d) ` 300 out of the advertisement expenses are to be carried forward to the next year.(e) Closing Stock was valued at ` 20,000.

Solution

Dr. Trading and Profit and Loss Account of Smt. Ramya for the year ended 31.03.2015 Cr.

Particulars Amount(`)

Amount(`)

Particulars Amount(`)

Amount(`)

To Opening Stock 15,000 By Sales 25,000To Purchases 13,000 Less: Returns 500 24,500Less: Returns 800 12,200 By Loss of Stock by

Fire2,000

To Wages 750 By Closing Stock 20,000To Carriage Inwards 1,200To Gross Profit c/d 17,350

46,500 46,500To Carriage Outwards 750 By Gross Profit b/d 17,350

35Final Accounts

To Rent 800 By Provision forDoubtful Debts

To Bad Debts 500 Old Provision 1,000Add: New Bad Debts 500 1,000 Less: New Provision 450 550To Provision for Discounton Debtors

202.5 By Interest on Loan 25

To Advertisement Expenses 800 Add: Accrued Interest 25 50Less: Prepaid 300 500To Discount Allowed 300To Accidental Loss 1,000To Manager’s Commission 638

To Net Profit c/d 12,759.517,950 17,950

Balance Sheet of Smt. Ramya as on the date 31st March 2015

Particulars Amount(`)

Amount(`)

Particulars Amount(`)

Amount(`)

Capital 20,000 Goodwill 2,100Add: Net Profit 12,759.5 Patents 645

32,759.5 Closing Stock 20,000Less: Drawings 4,000 28,759.5 Debtors 5,000Creditors 2,000 Less: New Bad 500Manager’s Commission 638 Debts 4,500Outstanding Rent 100 Less: Provision for Bad

Debts 4504050

Less: Provision forDiscount on Debtors 202.5 3,847.5Loan to Chandra 1,000Add: Accrued Intereston Loan 25 1,025Deposit with RamPrepaid 2,500

Advertisement 300Insurance Claim 1,000Cash in Hand 80

31,497.5 31,497.5

36 Financial Accounting

Working Notes:1. Calculation of provision for doubtful debts

Total Debtors as per Trial Balance 5,000Less: New Bad Debts 500

4,500Provision for doubtful debts is to be calculated @ 10% on 4,500 450Provision for Discount on Debtors is to be calculated@ 5% on (4,500 – 450) 4,050

` 202.5

2. Goods lost by fire ` 2000, Insurance claim admitted is ` 1,000 only. Therefore, the net lossof ` 1,000 (2,000 – 1,000) is to be charged to Profit and Loss Account.

3. Profit before charging Manager’s Commission is `13,397.50. Commission is payable @ 5%after charging such commission.The position would be as below.Profit before charging Commission 105Less: Manager’s Commission 5Net Profit after charging Commission 100Therefore, Commission = 13,397.5 * 5/105 ` 638

Illustration 16

The following is the Trial Balance of Lakshmi as on 31st March 2015.

Trial Balance of Lakshmi as on 31st March 2015

Debit Balance (`) Credit Balance (`)

Drawings 15,000 Capital 1,20,000Sundry Debtors 75,000 Sundry Creditors 85,000Cash in Hand 5,000 Loan 50,000Interest 1,500 Sales 1,62,000Stock 45,000 Purchase Returns 7,300Cash at Bank 10,000 Discount 2,500

Bad Debts 5,000 Bills Payable 15,000Land and Buildings 1,00,000 Rent Received 4,000Sales Returns 8,000 Provision for Bad Debts 8,500Purchases 1,30,000Carriage Outwards 2,500Carriage Inwards 4,500Establishment Charges 13,000Rates and Taxes 3,750

37Final Accounts

Advertisement 5,550General Expenses 5,000Wages 15,000Bills Receivable 10,500

4,54,300 4,54,300

Adjustments:(a) The Stock in hand on March 31, 2015 is valued at ` 80,000.(b) Depreciate Land and Buildings @ 10% p.a.(c) Bad Debts Provision is to be increased by ` 2,000.(d) Provide for the Manager’s Commission at 6% on the net profit after charging such

commission.You are required to prepare the Trading and Profit and Loss Account for the year ending 31st

March 2015 and a Balance Sheet as on that date.Solution

Dr. Trading and Profit and Loss of Lakshmi for the year ending March 31st 2015 Cr.

Particulars Amount(`)

Amount(`)

Particulars Amount(`)

Amount(`)

To Opening Stock 45,000 By Sales 1,62,000To Purchases 1,30,000 Less: Returns 8,000 1,54,000Less: Returns 7,300 1,22,700 By Closing Stock 80,000To Carriage Inwards 4,500To Wages 15,000To Gross Profit c/d 46,800

2,34,000 2,34,000To Interest 1,500 By Gross Profit b/d 46,800To Bad Debts 5,000 By Discount 2,500Add: New Provision 10,500 By Rent Received 4,000

15,500Less: Old Provision 8,500 7,000To Carriage Outwards 2,500To Establishment Charges 13,000To Rates and Taxes 3,750To Advertisement 5,550To General Expenses 5,000To Depreciation onBuildings

10,000

To Manager’s Commission(5,000 * 6/106)

283

To Net Profit 4,71753,300 53,300

38 Financial Accounting

Balance Sheet of Lakshmi as on 31st March 2015 (Order of Liquidity)

Liabilities Amount(`)

Amount(`)

Assets Amount(`)

Amount(`)

Bills Payable 15,000 Cash in Hand 5,000Manager’s Commission 283 Cash at Bank 10,000Sundry Creditors 85,000 Bills Receivable 10,500Loan 50,000 Sundry Debtors 75,000Capital 1,20,000 Less: New Provision 10,500 64,500Add: Net Profit 4,717 Stock 80,000

1,24,717 Land and Buildings 1,00,000Less: Drawings 15,000 1,09,717 Less: Depreciation 10,000 90,000

2,60,000 2,60,000

Working Notes:1. Calculation of Manager’s Commission:

`

Net Profit before Manager’s Commission (106) = 5,000 (53,300 – 48,300)Manager’s Commission (6) = 283 (5,000 * 6/106)Net Profit after Manager’s Commission (100) = 4,717

2. Bad Debts provision is to be increased by ` 2,000Old Provision ` 8,500Increase in Provision ` 2,000New Provision ` 10,500

SUMMARYAny business organization would be interested in knowing the profit or loss made by the concern

(financial result); the assets owned and the liabilities owed to the other parties (financial position) atthe end of the financial year. The accounting record made in order to ascertain the financial result andthe financial position is termed as “Final Account”. It refers to the Manufacturing Account, TradingAccount, Profit and Loss Account and Balance Sheet.

The Account prepared to ascertain the gross profit or gross loss for a period is termed as “TradingAccount”. It gives the overall result of trading, i.e., purchasing and selling of goods. In case, theconcern is also a Manufacturing Concern, the Manufacturing Account is prepared to ascertain the costof the goods manufactured during a particular period, which is transferred to the Trading Account.

Profit and Loss Account is prepared to ascertain the net profit or net loss of an organization. NetProfit increases the owner’s equity and hence added to capital, whereas Net Loss reduces the owner’sequity and therefore deducted from capital.

Balance Sheet represents the financial position of the business as on a particular date. TheBalance Sheet consists of the ledger accounts directly taken from the Trial Balance and certain itemsindirectly through the gist (Net Profit/Net Loss) of the Profit and Loss Account. Hence, the Balance

39Final Accounts

Sheet is a summary of the whole of the accounting record. The two statements, viz., Trading and theProfit and Loss Account (Income Statement) and Balance Sheet together are termed as ‘FinalAccounts’.

GLOSSARY Final Account: The accounting record made in order to ascertain the financial result and the

financial position. It refers to the Manufacturing Account, Trading Account, Profit and LossAccount and Balance Sheet.

Trading Account: The Account prepared to ascertain the gross profit or gross loss for aperiod. It gives the overall result of trading, i.e., purchasing and selling of goods.

Manufacturing Account: The Account prepared to ascertain the cost of the goodsmanufactured during a particular period.

Profit and Loss Account: The Account prepared to ascertain the net profit or net loss of anorganization.

Balance Sheet: The statement prepared to ascertain the financial position of the business ason a particular date.

Marshalling of Assets and Liabilities: It is the arrangement of assets and liabilities in theBalance Sheet either in Permanency Order or in Liquidity Order.

QUESTIONS1. What are Final Accounts? What purpose do they serve?2. Discuss any of the six adjustment entries.3. What is the purpose of Manufacturing and Trading Account?4. Differentiate between:

(a) Outstanding Income and Income received in advance(b) Outstanding Expenses and Prepaid Expenses(c) Interest on Capital and Interest on Drawings(d) Provision for Discount on Debtors and Provision for Discount on Creditors(e) Provision for Doubtful Debts and Provision for Discount on Debtors

5. Distinguish between Trial Balance and Balance Sheet.

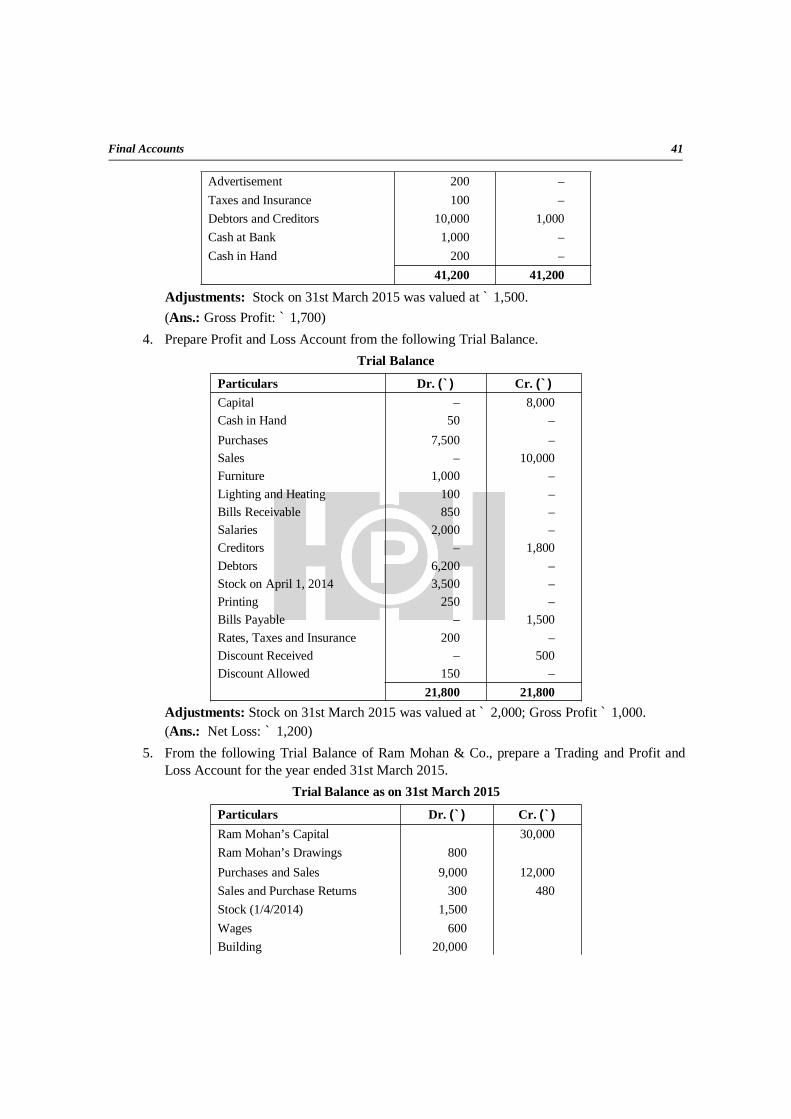

PROBLEMS1. Following are the balances extracted from the books of M/s Geetha Cycles as on 31st March

2015. You are required to prepare the Manufacturing Account for the year ended on thatdate.

Particulars (`)

Raw Materials (Opening Stock)Work-in-progress (Opening Stock)Finished Goods (Opening Stock)

40,00017,50040,000

40 Financial Accounting

Raw Material PurchasesFinished Goods PurchasesProductive WagesCoal and FuelSalesCarriage InwardsRailway FreightRepairs to MachineryRoyaltyPurchase ReturnsSales ReturnsFactory InsuranceFactory RentStock on 31st March 2015:

Raw MaterialsWork-in-progressFinished Goods

1,00,00045,00050,00010,000

3,80,0001,500

7503,0002,0001,0002,2503,250

42,000

17,50040,000

20,000

(Ans.: Manufacturing Cost Transferred to Trading Account: ` 2,11,500)2. Ascertain the Gross Profit from the following figures.

Amount (`)

Opening Stock of the GoodsClosing Stock of the GoodsPurchasesPurchase ReturnsSalesSales ReturnsCarriage InwardsCarriage OutwardsFreight, Duty and Clearing ChargesRent and Taxes

20,00030,00080,0002,000

1,60,0003,0002,0004,0005,0003,500

(Ans.: Gross Profit: ` 82,000)3. Prepare Trading Account from the following Trial Balance.

Trial Balance as on 31st March 2015Particulars Dr. (`) Cr. (`)

Ram’s Capital – 25,000Ram’s Drawings 700 –Purchases and Sales 9,000 15,000Sales Return and Purchase Returns 500 200Stock (1/4/2014) 2,000 –Wages 1,000 –Building 15,000 –Freight and Carriage 1,500 –

41Final Accounts

Advertisement 200 –Taxes and Insurance 100 –Debtors and Creditors 10,000 1,000Cash at Bank 1,000 –Cash in Hand 200 –

41,200 41,200

Adjustments: Stock on 31st March 2015 was valued at ` 1,500.(Ans.: Gross Profit: ` 1,700)

4. Prepare Profit and Loss Account from the following Trial Balance.Trial Balance

Particulars Dr. (`) Cr. (`)

Capital – 8,000Cash in Hand 50 –Purchases 7,500 –Sales – 10,000Furniture 1,000 –Lighting and Heating 100 –Bills Receivable 850 –Salaries 2,000 –Creditors – 1,800Debtors 6,200 –Stock on April 1, 2014 3,500 –Printing 250 –Bills Payable – 1,500Rates, Taxes and Insurance 200 –Discount Received – 500Discount Allowed 150 –

21,800 21,800Adjustments: Stock on 31st March 2015 was valued at ` 2,000; Gross Profit ` 1,000.(Ans.: Net Loss: ` 1,200)

5. From the following Trial Balance of Ram Mohan & Co., prepare a Trading and Profit andLoss Account for the year ended 31st March 2015.

Trial Balance as on 31st March 2015

Particulars Dr. (`) Cr. (`)

Ram Mohan’s Capital 30,000Ram Mohan’s Drawings 800Purchases and Sales 9,000 12,000Sales and Purchase Returns 300 480Stock (1/4/2014) 1,500Wages 600Building 20,000

42 Financial Accounting

Freight and Carriage 2,500Trade Expenses 500Advertisement 300Interest 450Taxes and Insurance 150Debtors and Creditors 6,000 2,000Bills Receivable and Bills Payable 1,300 670Cash at Bank 1,500Cash in Hand 150Salaries 1,000

45,600 45,600

Adjustment: Stock on 31st Mar 2015 was valued at ` 2,500.(Ans.: Gross Profit: ` 1,580, Net Profit: ` 80)

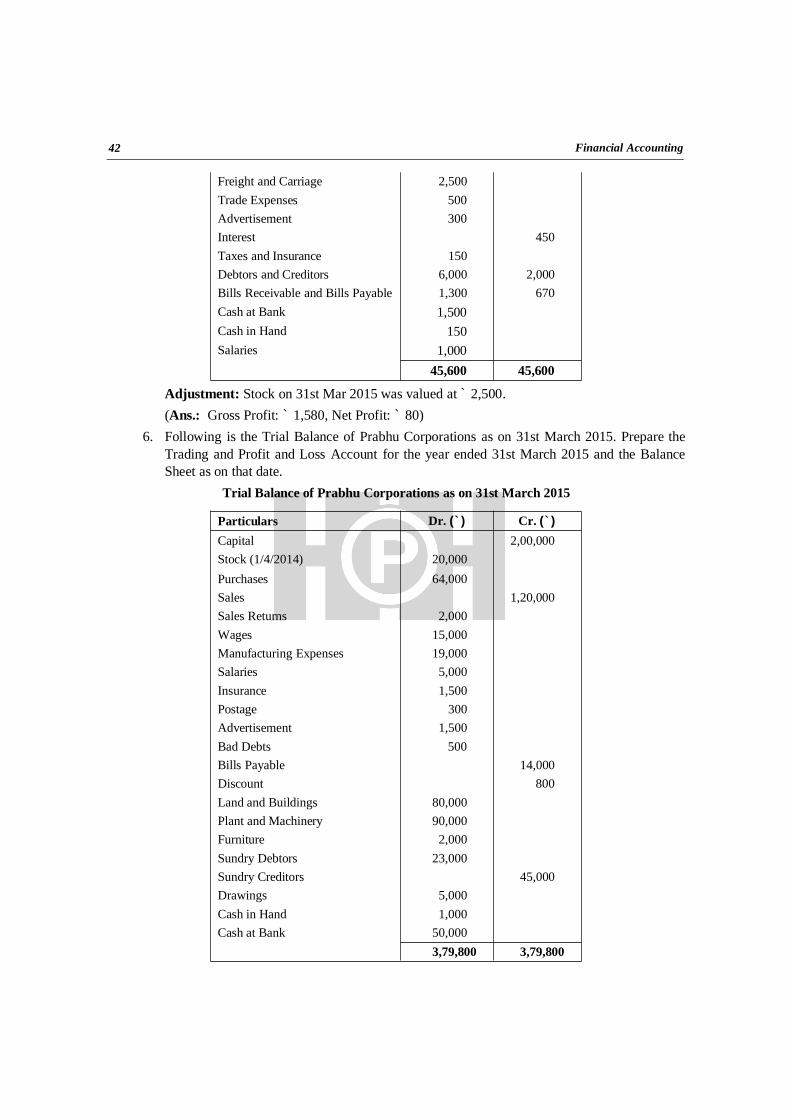

6. Following is the Trial Balance of Prabhu Corporations as on 31st March 2015. Prepare theTrading and Profit and Loss Account for the year ended 31st March 2015 and the BalanceSheet as on that date.

Trial Balance of Prabhu Corporations as on 31st March 2015

Particulars Dr. (`) Cr. (`)

Capital 2,00,000Stock (1/4/2014) 20,000Purchases 64,000Sales 1,20,000Sales Returns 2,000Wages 15,000Manufacturing Expenses 19,000Salaries 5,000Insurance 1,500Postage 300Advertisement 1,500Bad Debts 500Bills Payable 14,000Discount 800Land and Buildings 80,000Plant and Machinery 90,000Furniture 2,000Sundry Debtors 23,000Sundry Creditors 45,000Drawings 5,000Cash in Hand 1,000Cash at Bank 50,000

3,79,800 3,79,800

43Final Accounts

Adjustments:(a) Closing Stock as on 31st March 2015, was ` 30,000.(b) Provide depreciation on Land and Buildings @ 10%, on Furniture @ 5%, and on Plant

and Machinery @ 10%.(c) Outstanding expenses: Salaries ` 2,000 and Wages ` 1,600.(d) Insurance paid for 15 months up to March 2015.(Ans.: Gross Profit: ` 28,400; Net Profit: ` 1,600; Balance Sheet Total: ` 2,59,200)

7. From the following figures, prepare Trading and Profit and Loss Account for the year ended31 March 2015 and Balance Sheet as on that date.

Particulars (`)

CapitalDrawingsSundry CreditorsBills PayableSundry DebtorsBills ReceivableLoan advanced to Deepak & Co.Fixtures and FittingsOpening StockCash in HandCash at State Bank of IndiaOverdraft with Central Bank of IndiaPurchasesDuty and Clearing ChargesSalesSalariesReturns from CustomersReturn to CreditorsCommission and Travelling ExpensesGeneral ExpensesRent PaidCommission Received

30,0006,000

43,0004,000

51,0005,000

12,0008,500

47,000900

12,5006,000

50,0003,500

1,28,0009,5001,0001,1004,7002,5002,0004,000

Adjustments:(a) Closing Stock ` 50,000.(b) Interest to be received ` 200.(c) Outstanding salaries ` 500.(d) Depreciate fixtures and fittings by 10%.(e) Commission received in advance ` 600.(f) Allow interest on capital at 8%.(Ans. Gross Profit: ` 77,600; Net Profit: ` 58,750; Balance Sheet Total: ` 1,39,250)

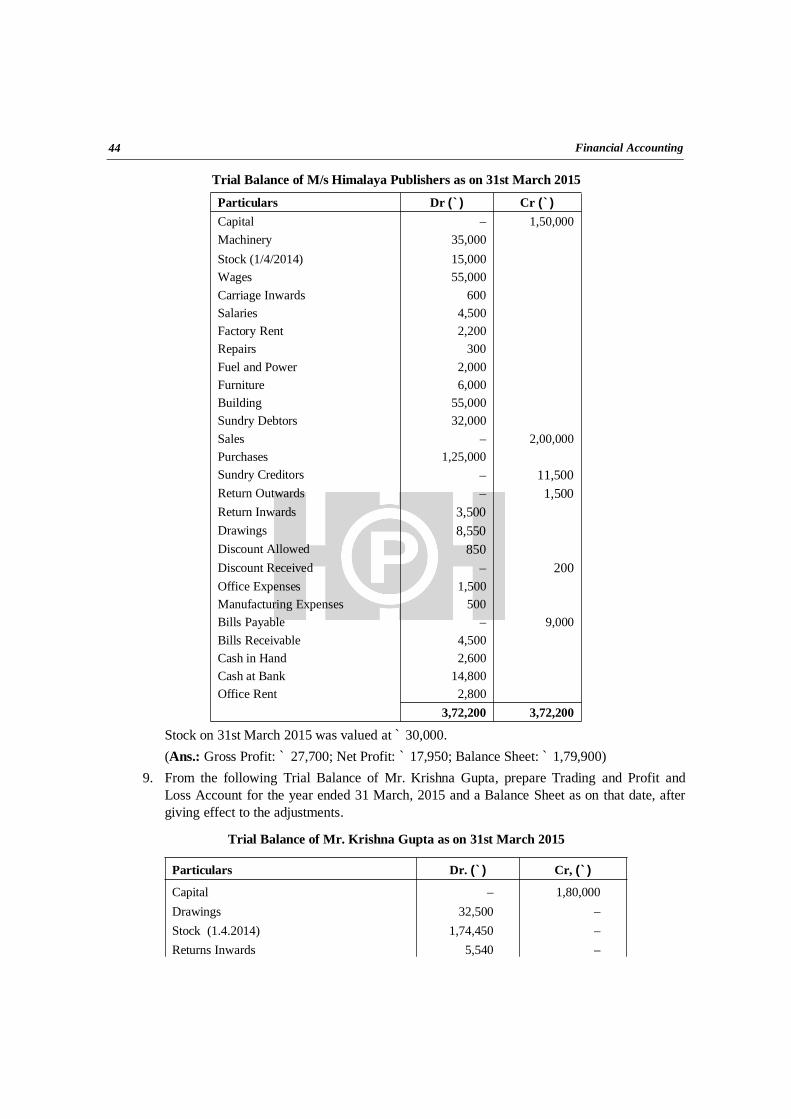

8. Prepare Trading, Profit and Loss Account and Balance Sheet from the following TrialBalance of M/s Himalaya Publishers.

44 Financial Accounting

Trial Balance of M/s Himalaya Publishers as on 31st March 2015

Particulars Dr (`) Cr (`)

Capital – 1,50,000Machinery 35,000Stock (1/4/2014) 15,000Wages 55,000Carriage Inwards 600Salaries 4,500Factory Rent 2,200Repairs 300Fuel and Power 2,000Furniture 6,000Building 55,000Sundry Debtors 32,000Sales – 2,00,000Purchases 1,25,000Sundry Creditors – 11,500Return Outwards – 1,500Return Inwards 3,500Drawings 8,550Discount Allowed 850Discount Received – 200Office Expenses 1,500Manufacturing Expenses 500Bills Payable – 9,000Bills Receivable 4,500Cash in Hand 2,600Cash at Bank 14,800Office Rent 2,800

3,72,200 3,72,200

Stock on 31st March 2015 was valued at ` 30,000.(Ans.: Gross Profit: ` 27,700; Net Profit: ` 17,950; Balance Sheet: ` 1,79,900)

9. From the following Trial Balance of Mr. Krishna Gupta, prepare Trading and Profit andLoss Account for the year ended 31 March, 2015 and a Balance Sheet as on that date, aftergiving effect to the adjustments.

Trial Balance of Mr. Krishna Gupta as on 31st March 2015

Particulars Dr. (`) Cr, (`)

CapitalDrawingsStock (1.4.2014)Returns Inwards

–32,500

1,74,4505,540

1,80,000–––

45Final Accounts

Carriage InwardsDeposits with Mr. Kamal (Interest free)Carriage OutwardsLoan to Anil @ 5% Given on 1.4.2014Return OutwardsInterest on above loanRentRent OutstandingPurchasesDebtorsGoodwillCreditorsAdvertisement ExpensesProvision for Doubtful DebtsBad DebtsPatents and Trade MarksCash in HandSalesDiscount allowedWagesPlant and Machinery (Purchased on 1.4.2014)

12,40013,7507,250

10,000––

8,200–

11,29,70040,00017,300

–9,540

–4,0005,000

620–

3,3007,540

30,000

––––

8,400250

–1,300

––

30,000–

12,000–––

12,79,140–––

15,11,090 15,11,090

Adjustments(a) Increase Bad Debts by ` 6,000. Make Provision for Doubtful Debts @ 10% and

Provision for Discount on Debtors @ 5%.(b) The value of the Closing Stock is ` 1,87,920.(c) Wages include ` 2000 paid for the erection of Machinery on 1-4-2009.(d) Provide depreciation on Machinery @ 10% p.a(Ans: Gross Profit: ` 1, 47,830, Net Profit: ` 1,13,910, Balance Sheet Total: ` 2,92,710)

10. The following Trial Balance is extracted from the books of Ram on March 31st, 2015.

Trial Balance of Ram as on March 31st, 2015

Particulars Dr. (`) Cr. (`)

SalariesGeneral ExpensesTaxes and InsuranceSundry DebtorsStockPurchasesWages

25,0006,200

10,50045,00030,000

1,00,0005,000

–

–––––––

46 Financial Accounting