financial institutions and financial marketsjnujprdistance.com/assets/lms/lms jnu/mba/mba -...

TRANSCRIPT

Financial Institutions and Financial Markets

Board of Studies

Prof. H. N. Verma Prof. M. K. GhadoliyaVice- Chancellor Director, Jaipur National University, Jaipur School of Distance Education and Learning Jaipur National University, JaipurDr. Rajendra Takale Prof. and Head AcademicsSBPIM, Pune

___________________________________________________________________________________________

Subject Expert Panel

Dr. S. U. Gawade Somrita MitraHead Research, SIOM Subject Matter ExpertPune

___________________________________________________________________________________________

Content Review Panel

Shreya Saraf Shweta MutttalmaniSubject Matter Expert Subject Matter Expert

___________________________________________________________________________________________Copyright ©

This book contains the course content for Financial Institutions and Financial Markets.

First Edition 2014

Printed byUniversal Training Solutions Private Limited

Address05th Floor, I-Space, Bavdhan, Pune 411021.

All rights reserved. This book or any portion thereof may not, in any form or by any means including electronic or mechanical or photocopying or recording, be reproduced or distributed or transmitted or stored in a retrieval system or be broadcasted or transmitted.

___________________________________________________________________________________________

I

Index

Content ........................................................................... II

List of Figures ...............................................................VI

List of Tables ............................................................... VII

Abbreviations ............................................................VIII

Case Study .................................................................. 140

Bibliography ............................................................... 144

Self Assessment Answers ........................................... 147

II

Contents

Chapter I ....................................................................................................................................................... 1Financial Markets: Role and Structure in the Industry ........................................................................... 1Aim ................................................................................................................................................................ 1Objectives ...................................................................................................................................................... 1Learning outcome .......................................................................................................................................... 11.1 Financial System Structure and Functions ............................................................................................... 21.2 Financial Markets and their Economic Functions ................................................................................... 31.3 Stock Exchanges in India ......................................................................................................................... 51.4 Security Measures and Operational Features of BSE and NSE ............................................................... 6 1.4.1 Market Timings ........................................................................................................................ 6 1.4.2 Automated Trading System ...................................................................................................... 6 1.4.3 Rolling Settlement and Settlement Cycle ................................................................................ 61.5 Financial Intermediaries and Their Functions ......................................................................................... 81.6 Financial Markets Structure ..................................................................................................................... 9 1.6.1. Financial Instruments .............................................................................................................. 9 1.6.2 Classification of Financial Markets ....................................................................................... 121.7 Financial Market Regulation .................................................................................................................. 131.8 Role of Financial Institutions ................................................................................................................. 13 1.8.1 Role of Depository Institutions .............................................................................................. 13 1.8.2 Role of Non-depository Financial Institutions ....................................................................... 141.9 Role of Financial Markets ...................................................................................................................... 15 1.9.1 Accommodating Corporate Finance Needs ........................................................................... 16 1.9.2 Accommodating Investment Needs ....................................................................................... 16 1.9.3 Primary versus Secondary Markets ....................................................................................... 16Summary ..................................................................................................................................................... 18References ................................................................................................................................................... 18Recommended Reading ............................................................................................................................. 19Self Assessment .......................................................................................................................................... 20

Chapter II ................................................................................................................................................... 22Determination of Interest Rates................................................................................................................ 22Aim .............................................................................................................................................................. 22Objectives .................................................................................................................................................... 22Learning outcome ........................................................................................................................................ 222.1 Introduction ............................................................................................................................................ 232.2 Interest Rate Determination ................................................................................................................... 23 2.2.1 The Rate of Interest ................................................................................................................ 23 2.2.2 Interest Rate Theories: Loanable Funds Theory .................................................................... 24 2.2.3 Interest Rate Theories: Liquidity Preference Theory ............................................................. 252.3 Determinants of Interest Rates for Individual Securities ....................................................................... 25 2.3.1 Inflation is the Rate of Change in the Overall Price Level .................................................... 25 2.3.2 Default or Credit Risk ............................................................................................................ 26 2.3.3 Liquidity Risk ........................................................................................................................ 26 2.3.4 Special Provisions of Covenants ............................................................................................ 26 2.3.5 Term to Maturity .................................................................................................................... 272.4 Forecasting Interest Rates ...................................................................................................................... 27Summary ..................................................................................................................................................... 28References ................................................................................................................................................... 28Recommended Reading ............................................................................................................................. 29Self Assessment ........................................................................................................................................... 30

III

Chapter III .................................................................................................................................................. 32Term Structure of Interest Rates .............................................................................................................. 32Aim .............................................................................................................................................................. 32Objectives .................................................................................................................................................... 32Learning outcome ........................................................................................................................................ 323.1 Introduction ............................................................................................................................................ 333.2 Theories of Term Structure of Interest Rates ......................................................................................... 33 3.2.1 Expectations Theory .............................................................................................................. 33 3.2.2 Liquidity Premium Theory .................................................................................................... 35 3.2.3 Market Segmentation Theory ................................................................................................ 36 3.2.4 The Preferred Habitat Theory ................................................................................................ 363.3 Forward Interest Rates and Yield Curve ................................................................................................ 37Summary ..................................................................................................................................................... 39References ................................................................................................................................................... 39Recommended Reading ............................................................................................................................. 39Self Assessment ........................................................................................................................................... 40

Chapter IV .................................................................................................................................................. 42Money Market ............................................................................................................................................ 42Aim .............................................................................................................................................................. 42Objectives .................................................................................................................................................... 42Learning outcome ........................................................................................................................................ 424.1 Introduction ............................................................................................................................................ 43 4.1.1 The Role of Money Markets .................................................................................................. 43 4.1.2 Money Market Segments ....................................................................................................... 44 4.1.3 Money Market Participants .................................................................................................... 454.2 Money Market Instruments .................................................................................................................... 46 4.2.1 Treasury Bills and other Government Securities ................................................................... 46 4.2.2 The Interbank Market Loans .................................................................................................. 50 4.2.3 Commercial Papers ................................................................................................................ 51 4.2.4 Certificates of Deposit ........................................................................................................... 52 4.2.5 Repurchase Agreements ......................................................................................................... 53 4.2.6 International Money Market Securities ................................................................................. 554.3 Money Market Interest Rates and Yields ............................................................................................... 56Summary ..................................................................................................................................................... 59References ................................................................................................................................................... 59Recommended Reading ............................................................................................................................. 59Self Assessment ........................................................................................................................................... 60

Chapter V .................................................................................................................................................... 62Debt Markets .............................................................................................................................................. 62Aim .............................................................................................................................................................. 62Objectives .................................................................................................................................................... 62Learning outcome ........................................................................................................................................ 625.1 Debt Market Instrument Characteristics ................................................................................................ 63 5.1.1 Important Characteristics of Bonds ...................................................................................... 63 5.1.2 The Types of Bonds .............................................................................................................. 635.2 Bond Market .......................................................................................................................................... 64 5.2.1 Bond Market Characteristics ................................................................................................. 64 5.2.2 Bond Market Yields ............................................................................................................... 655.3 Bond Valuation ....................................................................................................................................... 66 5.3.1 Discounted Models ................................................................................................................ 66 5.3.2 Bond Duration and Risk ........................................................................................................ 67 5.3.3 Bond Price Volatility .............................................................................................................. 67 5.3.4 Behaviour of Macaulay’s Duration ........................................................................................ 68

IV

5.3.5 Immunisation ......................................................................................................................... 69 5.3.6 Bond Convexity ..................................................................................................................... 695.4 Bond Analysis ........................................................................................................................................ 70 5.4.1 Inverse Floaters and Floating Rate Notes .............................................................................. 70 5.4.2 Callable Bonds ....................................................................................................................... 71 5.4.3 Convertible Bonds ................................................................................................................. 72Summary ..................................................................................................................................................... 74References ................................................................................................................................................... 74Recommended Reading ............................................................................................................................. 75Self Assessment ........................................................................................................................................... 76

Chapter VI .................................................................................................................................................. 78Equity Markets........................................................................................................................................... 78Aim .............................................................................................................................................................. 78Objectives .................................................................................................................................................... 78Learning outcome ........................................................................................................................................ 786.1 Introduction ............................................................................................................................................ 796.2 Equity Instruments ................................................................................................................................. 79 6.2.1 Common Shares ..................................................................................................................... 79 6.2.2 Preferred Shares ..................................................................................................................... 80 6.2.3 Private Equity ........................................................................................................................ 81 6.2.4 Global Shares and American Depository Receipts (ADR) .................................................... 826.3 Primary Equity Market .......................................................................................................................... 83 6.3.1 Primary Public Market ........................................................................................................... 846.4 Secondary Equity Market ...................................................................................................................... 86 6.4.1 Organised exchanges ............................................................................................................. 86 6.4.2 Over-the-Counter (OTC) Market ........................................................................................... 88 6.4.3 Electronic Stock Markets ....................................................................................................... 886.5 Secondary Equity Market Structure ....................................................................................................... 90 6.5.1 Cash vs. Forward Markets ..................................................................................................... 90 6.5.2 Continuous Markets and Auction Markets ............................................................................ 90 6.5.3 Order-driven Markets and Quote-driven Markets ................................................................. 90 6.5.4 Hybrid Markets ...................................................................................................................... 916.6 Equity Market Transactions ................................................................................................................... 91 6.6.1 Bid-ask Spread ....................................................................................................................... 91 6.6.3 Margin Trading ...................................................................................................................... 93 6.6.4 Short Selling .......................................................................................................................... 94 6.6.5 Stock Trading Regulations ..................................................................................................... 946.7 Equity Market Characteristics ................................................................................................................ 95 6.7.1 Stock Indicators ..................................................................................................................... 95 6.7.2 Stock Market Indexes ............................................................................................................ 96 6.7.3 Stock Market Indicators ......................................................................................................... 97 6.7.4 Transaction Execution Costs .................................................................................................. 986.8 Stock Valuation ...................................................................................................................................... 99 6.8.1 Fundamental Analysis ............................................................................................................ 99 6.8.2 Technical Analysis ............................................................................................................... 100Summary ................................................................................................................................................... 104References ................................................................................................................................................. 104Recommended Reading ........................................................................................................................... 104Self Assessment ......................................................................................................................................... 105

V

Chapter VII .............................................................................................................................................. 107Derivative Market .................................................................................................................................... 107Aim ............................................................................................................................................................ 107Objectives .................................................................................................................................................. 107Learning outcome ...................................................................................................................................... 1077.1 Hedging Against Risk .......................................................................................................................... 1087.2 Description of Derivatives Markets ..................................................................................................... 1087.3 Forward and Futures Contracts ............................................................................................................ 109 7.3.1 Principles of Forward and Futures Contracts ...................................................................... 109 7.3.2 Forward and Futures Valuation .............................................................................................111 7.3.3 Use of Forwards and Futures ................................................................................................112 7.3.4 Futures Contracts: Stock Index Futures ................................................................................114 7.3.5 Contracts for Difference (CFD) ............................................................................................1147.4 Swaps ....................................................................................................................................................1157.5 Options ..................................................................................................................................................116 7.5.1 Options Definition ................................................................................................................116 7.5.2 Components of the Option Price ...........................................................................................119 7.5.3 Determinants of the Option Price ........................................................................................ 120 7.5.4 Option Pricing Models ......................................................................................................... 122 7.5.5 Mixed Strategies in Options Trading ................................................................................... 1227.6 Depository System ............................................................................................................................... 123 7.6.1 Depository Participant (DP) ................................................................................................. 123 7.6.2 Need and Importance of Depository System ....................................................................... 124Summary ................................................................................................................................................... 125References ................................................................................................................................................. 125Recommended Reading ........................................................................................................................... 125Self Assessment ......................................................................................................................................... 126

Chapter VIII ............................................................................................................................................. 128Financial Institutions in India................................................................................................................. 128Aim ............................................................................................................................................................ 128Objectives .................................................................................................................................................. 128Learning outcome ...................................................................................................................................... 1288.1 Introduction .......................................................................................................................................... 1298.2 Institutional Support............................................................................................................................. 129 8.2.1 National Small Industries Corporation (NSIC) ................................................................... 129 8.2.2 Small Industries Development Organisation (SIDO) .......................................................... 129 8.2.3 Small Industries Service Institutes (SISI) ............................................................................ 130 8.2.4 Small-Scale Industries Board (SSIB) .................................................................................. 130 8.2.5 State Small Industries Development Corporations (SSIDC) ............................................... 131 8.2.6 District Industries Centres (DIC) ......................................................................................... 1318.3 Financial System and Banking System ................................................................................................ 1328.4 Constituents of the Financial System ................................................................................................... 132 8.4.1 Financial Institutions ............................................................................................................ 1328.5 Indian Financial System ....................................................................................................................... 1338.6 Indian Banking System Evolution of Commercial Banking in India .................................................. 134 8.6.1 Phase of Banking Consolidation: 1951-1964 ...................................................................... 134 8.6.2 Phase of Innovative Banking: 1964-1990 ............................................................................ 135 8.6.3 Phase of Prudential Banking - Since Early Nineties ............................................................ 136Summary ................................................................................................................................................... 137References ................................................................................................................................................. 137Recommended Reading ........................................................................................................................... 137Self Assessment ......................................................................................................................................... 138

VI

List of Figures

Fig. 1.1 The structure of financial system ...................................................................................................... 2Fig. 1.2 Comparison of roles among financial institutions ............................................................................ 9Fig. 1.3 How financial markets facilitate corporate finance and investment management ......................... 17Fig. 3.1 How interest rate expectations affect the yield curve ..................................................................... 35Fig. 3.2 Impact of liquidity premium on the yield curve under three scenarios .......................................... 36Fig. 4.1 Key money market instruments ...................................................................................................... 44Fig. 4.2 Prices in a sealed-bid auction ......................................................................................................... 47Fig. 4.3 Impact of single-price auction upon demand curve ........................................................................ 48Fig. 4.4 Money market rates and yields ....................................................................................................... 57Fig. 5.1 Duration and convexity .................................................................................................................. 69Fig. 5.2 Callable bond .................................................................................................................................. 71Fig. 5.3 Values of callable bonds, non-callable bonds and the call option .................................................. 72Fig. 5.4 Convertible bonds ........................................................................................................................... 73Fig. 7.1 Profit profile for perfect hedge ......................................................................................................113Fig. 7.2 Profit profile for a cross hedge ......................................................................................................113Fig. 7.3 Program trading arbitrage ..............................................................................................................114Fig. 7.4 Profit profiles for a call option ......................................................................................................117Fig. 7.5 Profit profile for writing a covered call option ..............................................................................118Fig. 7.6 Profit profile for a put option .........................................................................................................118Fig. 7.7 Merton‘s bound............................................................................................................................. 120Fig. 7.8 Impact of longer remaining life on the value of a call option ...................................................... 121Fig. 7.9 Impact of the volatility of the underlying asset on the value of a call option .............................. 121Fig. 7.10 Impact of higher interest rate on value of call option ................................................................. 122

VII

List of Tables

Table 1.1 Rolling settlement & settlement cycle ........................................................................................... 7Table 1.2 Financial instrument categories.................................................................................................... 10Table 1.3 Fixed-income markets ...................................................................................................................11Table 1.4 Debt versus equity .........................................................................................................................11Table 1.5 Financial market classification ..................................................................................................... 12

VIII

Abbreviations

ADR - American Depository ReceiptsARPS - Auction Rate Preferred SharesATS - Alternative Trading SystemsBOLT - BSE’s Online TradingBSE - Bombay Stock ExchangeCD - CertificateofDepositCDSL - Central Depository Services LimitedCFD - Contract for DifferenceCFS - Committee on Financial SectorCP - Commercial PaperCPI - Consumer Price IndexCRA - Credit Rating AgenciesDIC - District Industries CentersDOT - Designated Order TurnaroundDP - Depository ParticipantDRP - Default Risk PremiumsECB - European Central BankECN - Electronic Communication NetworksEONIA - Euro Overnight Index AverageETF - Exchange Traded FundsEURIBOR - Euro Interbank Offered RateFTSE - Financial Times Stock ExchangeGDR - Global Depository ReceiptsICICI - Industrial Credit and Investment Corporation of India IDBI - Industrial Development Bank of IndiaIFCI - Industrial Finance Corporation of IndiaIMF - International Mutual FundsIOI - Indications of InterestIPO - Initial Public OfferingsLIBOR - London Inter Bank Offer RateLIC - Life Insurance Corporation of IndiaMRO - MainRefinancingOperationsNABARD - National Bank for Agriculture and Rural DevelopmentNEAT - National Exchange for Automated TradingNSDL - National Securities Depository LimitedNSE - National Stock ExchangeNSIC - National Small Industries CorporationOTC - Over-the CounterPERCS - Preferred Equity Redemption Cumulative StocksPMRY - Prime Minister Rojgar YojanaREPO - Re Earnable Point OpportunitySEO - Seasoned Equity OfferingSIDBI - Small Industrial Development Bank of IndiaSISI - Small Industries Service InstitutesSPO - Secondary Public OfferingSSIB - Small Scale Industries BoardSSIDC - State Small Industries Development CorporationsUTI - Unit Trust of India

1

Chapter I

Financial Markets: Role and Structure in the Industry

Aim

The aim of this chapter is to:

introducethestructureofafinancialsystem•

explainthefunctionsofafinancialsystem•

elucidatemajorfinancialmarketparticipants•

Objectives

The objectives of this chapter are to:

determineclassificationoffinancialmarkets•

elaborate key attributes determining transaction costs•

analysefinancialmarketregulations•

Learning outcome

At the end of this chapter, you will be able to:

distinguishthekeyfeaturesoffinancialintermediaries•

understandthestructureandkeyfeaturesoffinancialmarkets•

describe costs of contracting and monitoring•

Financial Institutions and Financial Markets

2

1.1 Financial System Structure and FunctionsThefinancialsystemplaysthekeyroleintheeconomybystimulatingeconomicgrowth,influencingeconomicperformanceoftheactorsaffectingeconomicwelfare.Thisisachievedbyfinancialinfrastructure,inwhichentitieswithfundsallocatethosefundstothosewhohavepotentiallymoreproductivewaystoinvestthosefunds.Afinancialsystemmakesitpossibleamoreefficienttransferoffunds.Asonepartyofthetransactionmaypossesssuperiorinformationthantheotherparty,itcanleadtotheinformationasymmetryproblemandinefficientallocationoffinancialresources.Byovercomingtheinformationasymmetryproblemthefinancialsystemfacilitatesbalancebetween those with funds to invest and those needing funds.

Accordingtothestructuralapproach,thefinancialsystemofaneconomyconsistsofthreemaincomponents:Financial markets•Financial intermediaries (institutions)•Financial regulators•

Eachofthecomponentsplaysaspecificroleintheeconomy.Accordingtothefunctionalapproach,financialmarketsfacilitatetheflowoffundsinordertofinanceinvestmentsbycorporations,governmentsandindividuals.Financialinstitutionsarethekeyplayersinthefinancialmarketsastheyperformthefunctionofintermediationandthusdeterminetheflowoffunds.Thefinancialregulatorsperformtheroleofmonitoringandregulatingtheparticipantsinthefinancialsystem.

Firms

Stock market

Bond market

Short term fixed securities market

Banking sector

Governments

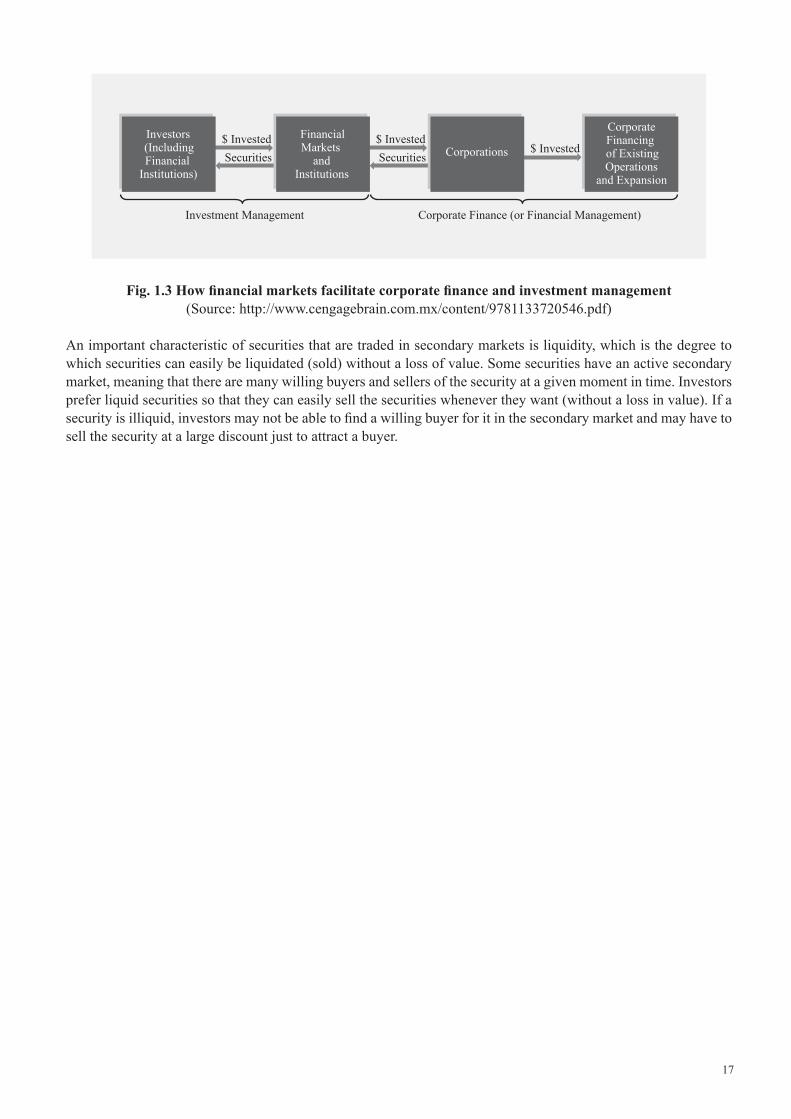

Fig. 1.1 The structure of financial system(Source: http://www.bcci.bg/projects/latvia/pdf/7_Financial_markets.pdf)

Financialmarketsstudies,basedoncapitalmarkettheory,focusonthefinancialsystem,thestructureofinterestratesandthepricingoffinancialassets.Anassetisanyresourcethatisexpectedtoprovidefuturebenefits,andthus possesses economic value. Assets are divided into two categories: tangible assets with physical properties and intangibleassets.Anintangibleassetrepresentsalegalclaimtosomefutureeconomicbenefits.Thevalueofanintangible asset bears no relation to the form, physical or otherwise, in which the claims are recorded.

Financialassets,oftencalledfinancialinstruments,areintangibleassets,whichareexpectedtoprovidefuturebenefitsintheformofaclaimtofuturecash.Somefinancialinstrumentsarecalledsecuritiesandgenerallyincludestocksandbonds.Anytransactionrelatedtofinancialinstrumentincludesatleasttwoparties

The party that has agreed to make future cash payments and is called the issuer•Thepartythatownsthefinancialinstrument,andthereforetherighttoreceivethepaymentsmadebytheissuer,•is called the investor

Financial assets provide the following key economic functions:They allow the transfer of funds from those entities, who have surplus funds to invest to those who need funds •to invest in tangible assets.Theyredistributetheunavoidableriskrelatedtocashgenerationamongdeficitandsurpluseconomicunits.•

3

Theclaimsheldbythefinalwealthholdersgenerallydifferfromtheliabilitiesissuedbythoseentitieswhodemandthosefunds.Theroleisperformedbythespecificentitiesoperatinginfinancialsystems,calledfinancialintermediaries.Thelatteronestransformthefinalliabilitiesintodifferentfinancialassetspreferredbythepublic.

1.2 Financial Markets and their Economic FunctionsAfinancialmarketisamarketwherefinancialinstrumentsareexchangedortraded.Financialmarketsprovidethefollowing three major economic functions:

Price discovery•Liquidity•Reduction of transaction costs•

Pricediscoveryfunctionmeansthattransactionsbetweenbuyersandsellersoffinancialinstrumentsinafinancialmarket determine the price of the traded asset. At the same time, the required return from the investment of funds is determinedbytheparticipantsinafinancialmarket.Themotivationforthoseseekingfunds(deficitunits)dependsontherequiredreturnthatinvestorsdemand.Itisthesefunctionsoffinancialmarketsthatsignalhowthefundsavailable from those who want to lend or invest funds will be allocated among those needing funds and raise those fundsbyissuingfinancialinstruments.

Liquidityfunctionprovidesanopportunityforinvestorstosellafinancialinstrument,sinceitisreferredtoasameasure of the ability to sell an asset at its fair market value at any time. Without liquidity, an investor would be forcedtoholdafinancialinstrumentuntilconditionsarisetosellitortheissueriscontractuallyobligatedtopayitoff. Debt instrument is liquidated when it matures, and equity instrument is until the company is either voluntarily or involuntarilyliquidated.Allfinancialmarketsprovidesomeformofliquidity.However,differentfinancialmarketsare characterised by the degree of liquidity.

Thefunctionofreductionoftransactioncostsisperformed,whenfinancialmarketparticipantsarechargedand/orbearthecostsoftradingafinancialinstrument.Inmarketeconomies,theeconomicrationalefortheexistenceofinstitutions and instruments is related to transaction costs, thus the surviving institutions and instruments are those that have the lowest transaction costs. The key attributes determining transaction costs are as follows:

Assetspecificity•Uncertainty•Frequency of occurrence•

Assetspecificityisrelatedtothewaytransactionisorganisedandexecuted.Itislowerwhenanassetcanbeeasilyputtoalternativeuse,canbedeployedfordifferenttaskswithoutsignificantcosts.Transactionsarealsorelatedtouncertainty, which has the following:

External sources (when events change beyond control of the contracting parties)•Depends on opportunistic behaviour of the contracting parties•

Ifchangesinexternaleventsarereadilyverifiable,thenitispossibletomakeadaptationstooriginalcontracts,takinginto account problems caused by external uncertainty. In this case, there is a possibility to control transaction costs. However, when circumstances are not easily observable, opportunism creates incentives for contracting parties to review the initial contract and creates moral hazard problems. The higher the uncertainty, the more opportunistic behaviour may be observed, and the higher transaction costs may be borne.

Frequency of occurrence plays an important role in determining if a transaction should take place within the market orwithinthefirm.Aone-timetransactionmayreducecostswhenitisexecutedinthemarket.Conversely,frequenttransactionsrequiredetailedcontractingandshouldtakeplacewithinafirminordertoreducethecosts.Whenassetsarespecific,transactionsarefrequent,andtherearesignificantuncertaintiesIntra-firmtransactionsmaybetheleastcostlyand,viceversa.Ifassetsarenon-specific,transactionsareinfrequent,andtherearenosignificantuncertainties. The least costly may be market transactions.

Financial Institutions and Financial Markets

4

The mentioned attributes of transactions and the underlying incentive problems are related to behavioural assumptions about the transacting parties. The economists, Williamson, Akerl and (others) have contributed to transactions costs economics by analysing behaviour of the human beings, assumed generally self-serving and rational in their conduct, and also behaving opportunistically. Opportunistic behaviour was understood as involving actions with incomplete and distorted information that may intentionally mislead the other party. This type of behaviour requires efforts of ex-ante screening of transaction parties, and ex-post safeguards as well as mutual restraint among the parties, which leadstospecifictransactioncosts.Transactioncostsareclassifiedinto:

Costs of search and information•Costs of contracting and monitoring•Costsofincentiveproblemsbetweenbuyersandsellersoffinancialassets•

Costsofsearchandinformationaredefinedinthefollowingway:Search costs fall into categories of explicit costs and implicit costs:•

Explicitcostsincludeexpensesthatmaybeneededtoadvertiseone’sintentiontosellorpurchaseafinancial �instrument. Implicit costs include the value of time spent in locating counterparty to the transaction. The presence of �anorganisedfinancialmarketreducessearchcosts.

Informationcostsareassociatedwithassessingafinancialinstrument’sinvestmentattributes.Inapriceefficient•market,pricesreflecttheaggregateinformationcollectedbyallmarketparticipants

Costs of contracting and monitoring are related to the costs necessary to resolve information asymmetry problems, when the two parties entering into the transaction possess limited information on each other and seek to ensure that thetransactionobligationsarefulfilled.

Costsofincentiveproblemsbetweenbuyersandsellersarise,whenthereareconflictsofinterestbetweenthetwoparties,havingdifferentincentivesforthetransactionsinvolvingfinancialassets.

Thefunctionsofamarketareperformedbyitsdiverseparticipants.Theparticipantsinfinancialmarketscanbealsoclassifiedintovariousgroups,accordingtotheirmotivefortrading:

Public investors, who ultimately own the securities and who are motivated by the returns from holding the •securities. Public investors include private individuals and institutional investors, such as pension funds and mutual funds.Brokers, who act as agents for public investors and who are motivated by the remuneration received (typically •in the form of commission fees) for the services they provide. Brokers thus trade for others and not on their own account.Dealers,whotradeontheirownaccountbutwhoseprimarymotiveistoprofitfromtradingratherthanfrom•holding securities. Typically, dealers obtain their return from the differences between the prices at which they buy and sell the security over short intervals of time.Credit rating agencies (CRAs) that assess the credit risk of borrowers.•

In reality three groups are not mutually exclusive. Some public investors may occasionally act on behalf of others; brokers may act as dealers and hold securities on their own, while dealers often hold securities in excess of the inventories needed to facilitate their trading activities. The role of these three groups differs according to the trading mechanismadoptedbyafinancialmarket.

5

1.3 Stock Exchanges in IndiaIndian stock market marks to be one of the oldest stock markets in Asia. It dates back to the close of 18th century when the East India Company used to transact loan securities. In the 1830s, trading on corporate stocks and shares in Bank and Cotton presses took place in Bombay.

Though the trading was broad but the brokers were hardly half dozen during 1840 and 1850.An informal group of 22 stockbrokers began trading under a banyan tree opposite the Town Hall of Bombay from the mid-1850s, each investing a (then) princely amount of Rupee 1. This banyan tree still stands in the Horniman Circle Park, Mumbai. In1860,theexchangeflourishedwith60brokers.Infactthe‘ShareMania’inIndiabeganwiththeAmericanCivilWar broke and the cotton supply from the US to Europe stopped. Further the brokers increased to 250. The informal group of stockbrokers organised themselves as the The Native Share and Stockbrokers Association which, in 1875, was formally organised as the Bombay Stock Exchange (BSE).BSE was shifted to an old building near the Town Hall. In 1928, the plot of land on which the BSE building now stands (at the intersection of Dalal Street, Bombay Samachar Marg and Hammam Street in downtown Mumbai) was acquired, and a building was constructed and occupied in 1930.

Premchand Roychand was a leading stockbroker of that time, and he assisted in setting out traditions, conventions, and procedures for the trading of stocks at Bombay Stock Exchange and they are still being followed. Several stock brokingfirmsinMumbaiwerefamily-runenterprises,andwerenamedaftertheheadsofthefamily.Thefollowingis the list of some of the initial members of the exchange, and who are still running their respective business:

D.S. Prabhudas & Company (now known as DSP, and a joint venture partner with Merrill Lynch)•Jamnadas Morarjee (now known as JM)•Champaklal Devidas (now called Cifco Finance)•Brijmohan Laxminarayan•

In1956,theGovernmentofIndiarecognisedtheBombayStockExchangeasthefirststockexchangeinthecountryunder the Securities Contracts (Regulation) Act. The most decisive period in the history of the BSE took place after 1992. In the aftermath of a major scandal with market manipulation involving a BSE member named Harshad Mehta, BSE responded to calls for reform with intransigence. The foot-dragging by the BSE helped radicalise the position of the government, which encouraged the creation of the National Stock Exchange (NSE), which created an electronic marketplace. NSE started trading on 4 November 1994. Within less than a year, NSE turnover exceeded the BSE. BSE rapidly automated, but it never caught up with NSE spot market turnover.

The second strategic failure at BSE came in the following two years. NSE embarked on the launch of equity derivatives trading. BSE responded by political effort, with a friendly SEBI chairman (D. R. Mehta) aimed at blocking equity derivatives trading. The BSE and D. R. Mehta succeeded in delaying the onset of equity derivatives trading by roughlyfiveyears.However,thistradingandtheaccompanyingshiftofthespotmarkettorollingsettlementdidcome along in 2000 and 2001. Helped by another major scandal at BSE involving the then President Mr. Anand Rathi. NSE scored nearly 100% market share in the runaway success of equity derivatives trading, thus consigning BSE into clearly second place. Today, NSE has roughly 66% of equity spot turnover and roughly 100% of equity derivatives turnover. Stock Exchange provides a trading platform, where buyers and sellers can meet to transact in securities.

Stock marketsStock Market is a market where the trading of company stock, both listed securities and unlisted takes place. It is different from stock exchange because it includes all the national stock exchanges of the country. For example, we use the term, ‘the stock market was up today’ or ‘the stock market bubble.’

Stock exchangesStock Exchanges are an organised marketplace, either corporation or mutual organisation, where members of the organisation gather to trade company stocks or other securities. The members may act either as agents for their customers, or as principals for their own accounts. Stock exchanges also facilitates for the issue and redemption

Financial Institutions and Financial Markets

6

ofsecuritiesandotherfinancialinstrumentsincludingthepaymentofincomeanddividends.Therecordkeepingis central but trade is linked to such physical place because modern markets are computerised. The trade on an exchange is only by members and stock broker do have a seat on the exchange.

1.4 Security Measures and Operational Features of BSE and NSEThe leading stock exchanges in India have developed itself to a large extent since its emergence. These stock exchanges aim at offering the investors and traders better transparency, genuine settlement cycle, honest transaction and to reduce and solve investor grievances if any.

1.4.1 Market TimingsTrading on the equities segment takes place on all days of the week (except Saturdays and Sundays and holidays declared by the Exchange in advance). The market timings of the equities segment are:Normal Market Open: 09:55 hoursNormal Market Close: 15:30 hoursThe post closing session is held between 15.50 to 16.00 hours

1.4.2 Automated Trading SystemToday our country has an advanced trading system which is a fully automated screen based trading system. This system adopts the following principles of an order-driven market as opposed to a quote driven system.

NSE operates on the ‘National Exchange for Automated Trading’ (NEAT) system.•BSE operates on the ‘BSE’s Online Trading’ (BOLT) system.•

Order management in automated trading systemThetradingsystemprovidescompleteflexibilitytomembersinthekindsofordersthatcanbeplacedbythem.Ordersarefirstnumberedandtime-stampedonreceiptandthenimmediatelyprocessedforpotentialmatch.Everyorder has a distinctive order number and a unique time stamp on it. If a match is not found, then the orders are stored in different ‘books’. Orders are stored in price-time priority in various books in the following sequence Best Price, Within Price, by time priority. Price priority means that if two orders are entered into the system, the order having the best price gets the higher priority. Time priority means if two orders having the same price are entered, theorderthatisenteredfirstgetsthehigherpriority.

Order matching rules in automated trading systemThe best buy order is matched with the best sell order. An order may match partially with another order resulting in multiple trades. For order matching, the best buy order is the one with the highest price and the best sell order is the one with the lowest price. This is because the system views all buy orders available from the point of view of a seller and all sell orders from the point of view of the buyers in the market. So, of all buy orders available in the market at any point of time, a seller would obviously like to sell at the highest possible buy price that is offered. Hence, the best buy order is the order with the highest price and the best sell order is the order with the lowest price.

Members can proactively enter orders in the system, which will be displayed in the system till the full quantity is matched by one or more of counter-orders and result into trade(s) or is cancelled by the member. Alternatively, members may be reactive and put in orders that match with existing orders in the system. Orders lying unmatched in the system are ‘passive’ orders and orders that come into match the existing orders are called ‘active’ orders. Orders are always matched at the passive order price. This ensures that the earlier orders get priority over the orders that come in later.

1.4.3 Rolling Settlement and Settlement CycleIn a rolling settlement, each trading day is considered as a trading period and trades executed during the day are settled based on the net obligations for the day. At NSE, trades in rolling settlement are settled on a T+2 basis, i.e., on the 2nd working day. For arriving at the settlement day all intervening holidays, which include bank holidays, NSE holidays, Saturdays and Sundays are excluded. Typically trades taking place on Monday are settled on Wednesday, Tuesday’s trades settled on Thursday and so on.

7

Settlement for trades is done on a trade-for-trade basis and delivery obligations arise out of each trade. The settlement cycle for this segment is same as for the rolling settlement viz:

Activity Day

Trading Rolling settlement trading T

Clearing Custodialconfirmation T+1 working days

Delivery generation T+1 working days

Settlement Securities and funds pay in T+2 working days

Securities and funds pay out T+2 working days

Post Settlement Assigning of shortages for close out T+3 working days

Reporting and pick-up of bad delivery T+4 working days

Close out of shortages T+5 working days

Replacement of bad delivery T+6 working days

Reporting of re-bad and pick-up T+8 working days

Close out of re-bad delivery T+9 working days

Table 1.1 Rolling settlement & settlement cycle

Salient features of settlementDelivery of shares in street name and market delivery (clients holding physical shares purchased from the •secondary market) is treated as bad delivery. The shares standing in the name of individuals/HUF only would constitute good delivery. The selling/delivering member must necessarily be the introducing member.Any delivery of shares, which bears the last transfer date on or after the introduction of the security for trading •in the LP market, is construed as bad delivery.Any delivery in excess of 500 shares is marked as short and such deliveries are compulsorily closed-out.•Shortages,ifany,arecompulsorilyclosed-outat20%overtheactualtradedprice.Uncertifiedbaddeliveryand•re-bad delivery are compulsorily closed-out at 20% over the actual traded price.All deliveries are compulsorily required to be attested by the introducing/ delivering member.•The buyer must compulsorily send the securities for transfer and dematerialisation, latest within three months •from the date of pay-out.Company objections arising out of such trading and settlement in this market are reported in the same manner •as is currently being done for normal market segment. However, securities would be accepted as valid company objection, only if the securities are lodged for transfer within three months from the date of pay-out.Institutionalsegment:TheReserveBankofIndiahadvideapressreleaseonOctober21,1999,clarifiedthat•inter-foreign-institutional-investor(inter-FII)transactionsdonotrequirepriorapprovalorpost-factoconfirmationof the Reserve Bank of India, since such transactions do not affect the percentage of overall FII holdings in Indian companies. (Inter FII transactions are however not permitted in securities where the FII holdings have already crossed the overall limit due to any reason).

To facilitate execution of such inter-institutional deals in companies where the cut-off limit of FII investment has been reached, the Exchange introduced a new market segment on December 27, 1999. The securities where FII investorsandFIIholdinghasreachedthecut-offlimitasspecifiedbyRBI(2%lowerthantheceilingspecifiedbyRBI) from time –to- time would be available for trading in this market type for exclusive selling by FII clients. The cut-off limits for companies with 24% ceiling is 22%, for companies with 30% ceiling is 28% and for companies with 40% ceiling is 38%. Similarly, the cut- off limit for public sector banks (including State Bank of India) is 18% whose ceiling is 20%. The list of securities eligible/become ineligible for trading in this market type would be notifiedtomembersfromtime-to-time.

Financial Institutions and Financial Markets

8

Brokerage and other transaction costsBrokerage is negotiable. The Exchange has not prescribed any minimum brokerage. The maximum brokerage is subject to a ceiling of 2.5 percent of the contract value. However, the average brokerage charged by the members to the clients is much lower. Typically there are different scales of brokerages for delivery transaction, trading transaction, etc. The Stamp Duty on transfer of securities in physical form is to be paid by the seller but in practice it is paid by the buyer while registering the shares in his name. In case of transfer of shares, the rate is 50 paisa for every Rs.100/- or part thereof on the basis of the amount of consideration and that for transfer of debentures the rateofstampdutyvariesfromState-to-State,wheretheregisteredofficeofaCompanyissuingthedebenturesislocated.

Transfer of ownershipTransfer of ownership of securities, if the same is not delivered in demat form by the seller, is effected through a date stamped transfer-deed which is signed by the buyer and seller. The duly executed transfer-deed along with the share certificatehastobelodgedwiththecompanyforchangeintheownership.Anominaldutybecomespayableintheformofstampstobeaffixedonthetransfer-deeds.Transfer-deedremainsvalidfortwelvemonthsorthenextbookclosure following the stamped date whichever occurs later for transfer of shares in the name of buyer. However, for delivery of shares in the market, transfer deed is valid till book closure date of the company.

1.5 Financial Intermediaries and Their FunctionsFinancialintermediaryisaspecialfinancialentity,whichperformstheroleofefficientallocationoffunds,whenthereareconditionsthatmakeitdifficultforlendersorinvestorsoffundstodealdirectlywithborrowersoffundsinfinancialmarkets.Financialintermediariesincludedepositoryinstitutions,insurancecompanies,regulatedinvestmentcompanies, investment banks, and pension funds.

Theroleoffinancialintermediariesistocreatemorefavourabletransactiontermsthancouldberealisedbylenders/investorsandborrowersdealingdirectlywitheachotherinthefinancialmarket.Thefinancialintermediariesareengaged in the following manner:

Obtaining funds from lenders or investors•Lending or investing the funds that they borrow to those who need funds•

Thefundsthatafinancialintermediaryacquiresbecome,dependingonthefinancialclaim,eithertheliabilityofthefinancialintermediaryorequityparticipantsofthefinancialintermediary.Thefundsthatafinancialintermediarylendsorinvestsbecometheassetofthefinancialintermediary.

Financialintermediariesareengagedintransformationoffinancialassets,whicharelessdesirableforalargepartoftheinvestingpublicintootherfinancialassetstheirownliabilitieswhicharemorewidelypreferredbythepublic.Asset transformation provides at least one of the following three economic functions:

Maturity intermediation•Riskreductionviadiversification•Cost reduction for contracting and information processing•

9

Surplus Units

Policyholders

Employers and

Employees

Depository Institutions

(Commercial Banks, Savings Institutions,

Credit Unions)

Finance Companies

Mutual Funds

Insurance Companies

Pension funds

Deficit Units (Firms,

Government, Agencies, Some

Individuals)

Deposits

Purchase Securities

Purchase Shares

Premiums

Employee Contributions

Fig. 1.2 Comparison of roles among financial institutions(Source: http://www.bcci.bg/projects/latvia/pdf/7_Financial_markets.pdf)

Theseeconomic functionsareperformedbyfinancialmarketparticipantswhileproviding the specialfinancialservices,e.g.,thefirstandsecondfunctionscanbeperformedbybrokers,dealersandmarketmakers.Thethirdfunctionisrelatedtotheserviceofunderwritingofsecurities.Otherservicesthatcanbeprovidedbyfinancialintermediaries include the following:

Facilitating the trading of financial assets for the financial intermediary’s customers through brokering•arrangements.Facilitatingthetradingoffinancialassetsbyusingitsowncapitaltotakeapositioninafinancialassetthe•financialintermediary’scustomerwanttotransactin.Assistinginthecreationoffinancialassetsforitscustomersandtheneitherdistributingthosefinancialassets•to other market participants.Providing investment advice to customers•Managethefinancialassetsofcustomers•Providing a payment mechanism•

1.6 Financial Markets StructureFinancial market structure is further divided into two sections. They are explained in the paragraphs given below:

1.6.1. Financial InstrumentsThereisagreatvarietyoffinancialinstrumentinthefinancialmarketplace.Theuseoftheseinstrumentsbymajormarket participants depends upon their offered risk and return characteristics, as well as availability in retail or wholesalemarkets.Thegeneralviewonthefinancialinstrumentcategoriesisprovidedintablebelow.

Financial Institutions and Financial Markets

10

Category Risk Determinants Expected Returns Main Participants

Non-tradables and non-transferables

In wholesale money markets: transaction volumes

In wholesale money markets: low

In wholesale money markets: banks

In retail markets: low transparency, lack of standardisation, low creditworthiness

In credit markets: lowIn retail markets banks andnon-bankfirmsandhouseholds

In foreign exchange\ markets: high volatility, change of currency

In foreign exchange markets: high

In foreign exchange markets:financialinstitutions, companies

SecuritiesMarket volatility, individual risks and failures

Comparably high Banks and non-bank firms,individuals

Derivatives Market volatility, leverage Very high Banks and non-bank firms,individuals

Table 1.2 Financial instrument categories

Afinancialinstrumentcanbeclassifiedbythetypeofclaimsthattheinvestorhasontheissuer.Afinancialinstrumentin which the issuer agrees to pay the investor interest plus repay the amount borrowed is a debt instrument. A debt instrument also referred to as an instrument of indebtedness, can be in the form of a note, bond, or loan. The interest paymentsthatmustbemadebytheissuerarefixedcontractually.Forexample,inthecaseofadebtinstrumentthatisrequiredtomakepaymentsinEuros,theamountcanbeafixedEuroamountoritcanvarydependinguponsomebenchmark. The investor in a debt instrument can realise no more than the contractual amount. For this reason, debt instrumentsareoftencalledfixedincomeinstruments.

Fixedincomeinstrumentsformawideanddiversifiedfixedincomemarket.Thekeycharacteristicsofitareprovidedin Table 1.3.

Market Features Issuers

Long- term

Bonds Long-term obligations to make a seriesoffixedpayments Governments,firms

Convertibles Bonds that can be swapped for equity atpre-specifiedconditions Firms

Asset-backed securities Securitised “receivables” presenting future streams of payments

Financial institutions, firms

Preferred stock, subordinated debt Debt and equity hybrids Firms

Medium-term

Notes Medium-term obligations Governments

Floating-rate notesMedium-term instruments with interest rates based on LIBOR or another index

Firms

11

Short-term

Bills Short-term obligations Governments

Commercial paper Short-term debt instruments Firms

Certificatesofdeposit Short-term debt instruments Banks

Table 1.3 Fixed-income markets

Incontrasttoadebtobligation,anequityinstrumentspecifiesthattheissuerpaystheinvestoranamountbasedonearnings,ifany,aftertheobligationsthattheissuerisrequiredtomaketoinvestorsofthefirm’sdebtinstrumentshavebeenpaid.Common stock is an example of equity instruments. Somefinancial instruments due to theircharacteristics can be viewed as a mix of debt and equity.

Preferredstockisafinancialinstrument,whichhastheattributeofadebtbecausetypicallytheinvestorisonlyentitledtoreceiveafixedcontractualamount.However,itissimilartoanequityinstrumentbecausethepaymentisonlymadeafterpaymentstotheinvestorsinthefirm’sdebtinstrumentsaresatisfied.

Another ‘combination’ instrument is a convertible bond, which allows the investor to convert debt into equity under certain circumstances.Aspreferred stockholders typically are entitled to afixedcontractual amount, preferredstockisreferredtoasafixedincomeinstrument.Hence,fixedincomeinstrumentsincludedebtinstrumentsandpreferredstock.ThefeaturesofdebtandequityinstrumentsarecontrastedinTable1.4.Theclassificationofdebtand equity is especially important for two legal reasons. First, in the case of a bankruptcy of the issuer, investor in debt instruments has a priority on the claim of the issuer’s assets over equity investors. Second, the tax- treatment ofthepaymentsbytheissuercandifferdependingonthetypeoffinancialinstrumentclass.

Debt Equity

Characteristic Borrower-lenderrelation,fixedmaturities Ownership, no time limit

Advantage for the firm Predictability, independence from shareholders’influence

Flexibility,lowcostoffinance,reputation

Advantage for the investor Low risk High expected return

Disadvantages for the firm Debt servicing obligationShareholder dependence, shortsightedness, market volatility influencingmanagementdecisions

Disadvantage for the investor Low returns High risk

Table 1.4 Debt versus equity

Financial Institutions and Financial Markets

12

1.6.2 Classification of Financial MarketsTheredifferentwaystoclassifyfinancialmarkets.Theyareclassifiedaccordingtothefinancialinstrumentstheyare trading, features of services they provide, trading procedures, key market participants, as well as the origin of themarkets.ThegeneralisedfinancialmarketclassificationisgiveninTable1.5.

Criterion Features Examples

ProductsTradability, transferability, ownership, maturity, denomination, substance

Equity, debt instruments, derivatives

ServicesTechnical, advisory, information and knowledge based, administrative

IT support, research and analysis, custody

Ways of trading Physical, electronic, virtual Over the counter, exchange, internet

Participants Professionals, non-professionals, institutions,officials

Banks, central banks, non-bank financialcompanies,institutionalinvestors,businessfirms,households

Origin Domestic, cross-border, regional, international

National markets, regionally integrated markets, Euromarkets, domestic/foreign currency markets, onshore/offshore markets

Table 1.5 Financial market classification

Fromtheperspectiveofcountry-origin,itsfinancialmarketcanbebrokendownintoaninternalmarketandanexternal market. The internal market, also called the national market, consists of two parts: the domestic market and the foreign market. The domestic market is where issuers domiciled in the country issue securities and where those securities are subsequently traded. The foreign market is where securities are sold and traded outside the country of issuers. External market is the market where securities with the following two distinguishing features are trading:

At issuance they are offered simultaneously to investors in a number of countries•They are issued outside the jurisdiction of any single country•

The external market is also referred to as the international market, offshore market, and the Euromarket (despite thefactthatthismarketisnotlimitedtoEurope).Moneymarketisthesectorofthefinancialmarketthatincludesfinancialinstrumentsthathaveamaturityorredemptiondatethatisoneyearorlessatthetimeofissuance.Theseare mainly wholesale markets.

Thecapitalmarketisthesectorofthefinancialmarketwherelong-termfinancialinstrumentsissuedbycorporationsandgovernmentstrade.Here‘long-term’referstoafinancialinstrumentwithanoriginalmaturitygreaterthanoneyear and perpetual securities (those with no maturity). There are two types of capital market securities those that represent shares of ownership interest, also called equity, issued by corporations, and those that represent indebtedness, ordebtissuedbycorporationsandbythestateandlocalgovernments.Financialmarketscanbeclassifiedintermsof cash market and derivative markets. The cash market, also referred to as the spot market is the market for the immediatepurchaseandsaleofafinancialinstrument.

Incontrast,somefinancialinstrumentsarecontractsthatspecifythatthecontractholderhaseithertheobligationor the choice to buy or sell another something at or by some future date. The ‘something’ that is the subject of the contractiscalledtheunderlying(asset).Theunderlyingassetisastock,abond,afinancialindex,aninterestrate,acurrency or a commodity. As the price of such contracts derives their value from the value of the underlying assets, these contracts are called derivative instruments and the market where they are traded is called the derivatives market.

13

Whenafinancialinstrumentisfirstissued,itissoldintheprimarymarket.Asecondarymarketissuchinwhichfinancialinstrumentsareresoldamonginvestors.Nonewcapitalisraisedbytheissuerofthesecurity.Tradingtakesplaceamonginvestors.SecondarymarketsarealsoclassifiedintermsoforganisedstockexchangesandOver-TheCounter(OTC)markets.Stockexchangesarecentraltradinglocations,wherefinancialinstrumentsaretraded.Incontrast,anOTCmarketisgenerallywhereunlistedfinancialinstrumentsaretraded.

1.7 Financial Market RegulationIngeneral,financialmarketregulationisaimedtoensurethefairtreatmentofparticipants.Manyregulationshavebeen enacted in response to fraudulent practices. One of the key aims of regulation is to ensure business disclosure of accurate information for investment decision- making. When information is disclosed only to limited set of investors, those have major advantages over other groups of investors. Thus, regulatory framework has to provide the equal access to disclosures by companies. The recent regulations were passed in response to large bankruptcies, overhauled corporate governance, in order to strengthen the role of auditors in overseeing accounting procedures.

The Sorbanes-Oxley Act of 2002 in US was designed particularly to tighten companies’ governance after dotcom bustandEnron’sBankruptcy.Ithaddirectconsequencesinternationally,firstofallthroughglobalcompanies.TheUSWallStreetReformandConsumerProtectionAct(Dodd-Frank)of2010aimsat imposingtighterfinancialregulationforthefinancialmarketsandfinancialintermediariesintheUS,inordertoensureconsumerprotection.ThisisintunewithmajorfinancialregulationsystemdevelopmentinEUandotherpartsoftheworld.

1.8 Role of Financial InstitutionsAsfinancialmarketsareimperfect,securitiesbuyersandsellersdonothavefullaccesstoinformation.Individualswith available funds are not normally capable of identifying creditworthy borrowers to whom they could lend those funds. In addition, they do not have the expertise to assess the creditworthiness of potential borrowers. Financial institutions are needed to resolve the limitations caused by market imperfections. They accept funds from surplus unitsandchannelthefundstodeficitunits.Withoutfinancialinstitutions,theinformationandtransactioncostsoffinancialmarkettransactionswouldbeexcessive.Financialinstitutionscanbeclassifiedasdepositoryandnon-depository institutions.

1.8.1 Role of Depository InstitutionsDepository institutionsacceptdeposits fromsurplusunitsandprovidecredit todeficitunits through loansandpurchasesofsecurities.Theyarepopularfinancialinstitutionsforthefollowingreasons:

They offer deposit accounts that can accommodate the amount and liquidity characteristics desired by most •surplus units.They repackage funds received fromdeposits to provide loans of the size andmaturity desiredbydeficit•units.They accept the risk on loans provided.•Theyhavemoreexpertisethanindividualsurplusunitsinevaluatingthecreditworthinessofdeficitunits.•Theydiversifytheirloansamongnumerousdeficitunitsandthereforecanabsorbdefaultedloansbetterthan•individual surplus units could.

Toappreciatetheseadvantages,considertheflowoffundsfromsurplusunitstodeficitunitsifdepositoryinstitutionsdidnotexist.Eachsurplusunitwouldhavetoidentifyadeficitunitdesiringtoborrowthepreciseamountoffundsavailable for the precise time period in which funds would be available. Furthermore, each surplus unit would have to perform the credit evaluation and incur the risk of default. Under these conditions, many surplus units would likelyholdtheirfundsratherthanchannelthemtodeficitunits.Hence,theflowoffundsfromsurplusunitstodeficitunits would be disrupted.

When a depository institution offers a loan, it is acting as a creditor, just as if it had purchased a debt security. The more personalised loan agreement is less marketable in the secondary market than a debt security, however, because theloanagreementcontainsdetailedprovisionsthatcandiffersignificantlyamongloans.Anypotentialinvestorswouldneedtoreviewallprovisionsbeforepurchasingloansinthesecondarymarket.Amorespecificdescriptionofeachdepositoryinstitution’sroleinthefinancialmarketsfollows.

Financial Institutions and Financial Markets

14

Commercial banksIn aggregate, commercial banks are the most dominant depository institution. They serve surplus units by offering awidevarietyofdepositaccounts,andtheytransferdepositedfundstodeficitunitsbyprovidingdirectloansorpurchasing debt securities. Commercial bank operations are exposed to risk because their loans and many of their investments in debt securities are subject to the risk of default by the borrowers.

Commercial banks serve both the private and public sectors; their deposit and lending services are utilised by households, businesses, and government agencies. Some commercial banks (including Bank of America, J.P. Morgan Chase, Citigroup, and SunTrust Banks) have more than $100 billion in assets.Some commercial banks receive more funds from deposits than they need to make loans or invest in securities. Other commercial banks need more funds to accommodate customer requests than the amount of funds that they receive from deposits. The federal funds market facilitatestheflowoffundsbetweendepositoryinstitutions(includingbanks).Abankthathasexcessfundscanlendtoabankwithdeficientfundsforashort-termperiod,suchasonetofivedays.Inthisway,thefederalfundsmarketfacilitatestheflowoffundsfrombanksthathaveexcessfundstobanksthatareinneedoffunds.

Commercial banks are subject to regulations that are intended to limit their exposure to the risk of failure. In particular, banks are required to maintain a minimum level of capital, relative to their size, so that they have a cushion to absorb possible losses from defaults on some loans provided to households or businesses. The Federal Reserve (The Fed) serves as a regulator of banks.

Savings institutions Savings institutions, which are sometimes referred to as thrift institutions, are another type of depository institution. Savings institutions include savings and loan associations (S&Ls) and savings banks. Like commercial banks, savingsinstitutionsofferdepositaccountstosurplusunitsandthenchannelthesedepositstodeficitunits.SavingsbanksaresimilartoS&Lsexceptthattheyhavemorediversifiedusesoffunds.Overtime,however,thisdifferencehas narrowed. Savings institutions can be owned by shareholders, but most are mutual (depositor owned). Like commercial banks, savings institutions rely on the federal funds market to lend their excess funds or to borrow funds on a short-term basis.