financial management assessment and projections a. introduction€¦ · · 2014-10-03financial...

TRANSCRIPT

Madhya Pradesh Power Transmission and Distribution System Improvement Project (RRP IND 47100)

FINANCIAL MANAGEMENT ASSESSMENT AND PROJECTIONS

A. Introduction

1. Under the Power Sector Reform Program, the Government of Madhya Pradesh (GOMP) has unbundled the Madhya Pradesh State Electricity Board (MPSEB) into five wholly owned State Government Companies. Madhya Pradesh Power Transmission Company (MP Transco) is one of such five companies carved out of MPSEB to undertake the activities relating to electricity transmission within the State of Madhya Pradesh. With effect from 1 June 2005, the company has assumed the functions of intra-state transmission of electricity, State Transmission Utility and State Load Dispatch Center as its own business and not as an agent of Madhya Pradesh State Electricity Board. 2. There were three distribution companies (DISCOMs) formed as well namely – Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Limited Bhopal (DISCOM-C), Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited Jabalpur (DISCOM-E) and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited Indore (DISCOM-W). 3. Subsequently, in May 2006 one more company, namely Madhya Pradesh Power Trading Company (MP Tradeco) has been carved out of MPSEB to look after the trading of power and other associated activities. In accordance with GOMP decision, the name of MP Tradeco has been changed to MP Power Management Company. The MP Power Management Company (Holding Company) has been made holding company for all the DISCOMS of MP.

4. DISCOM-C, DISCOM-E, DISCOM-W and the MP Transco are the four executing agencies for this proposed loan from the Asian Development Bank (ADB). 5. A financial management assessment (FMA) and review of their past performances and future business projections of the four executing agencies are conducted as part of the financial due diligence of the executing agencies to assess their capacities to implement the Power Transmission and Distribution System Improvement project administered by ADB. B. Project Description

6. The Project has three outputs: (i) transmission system improvement; (ii) distribution system improvement; and (iii) capacity building for the executing agency staff. The transmission system improvement includes augmentation of sub-station capacity and line lengths across all the voltage levels (132 kV, 220 kV, 400 kV). For the 220 kV and 400 kV voltage levels, the focus is to upgrade the transformer capacity at the existing sub-stations. For the 132 kV transmission network, the target is to create more sub-stations to feed the distribution network while improving the overall quality and reliability of supply. About 1,800 circuit km of transmission line is proposed to be constructed under the project. A total of 32 substations, (12.5% of the current number of sub-stations) comprising of two 400 kV, four 220 kV and twenty-six 132 kV substations are proposed to be constructed. The total capacity addition under the project would be about 4,000 megavolt ampere (MVA) which is 25% of the targeted sub-station capacity addition by MP Transco during the period of 2013-2017. This would result in an increase in the transmission substation capacity from 37,000 MVA in 2013 to 41,000 MVA by 2020. 7. The distribution system improvement includes the construction of new 33/11 kV sub-stations, bifurcation of overloaded 33 kV feeders, additional/augmentation of power transformers, installation of distribution transformers and capacitor banks. Approximately 2,225 circuit kilometers (km) of 33 kV lines and 915 circuit km of 11 kV lines are proposed to be

2

constructed. A total of 149 new 33/11 kV sub stations are proposed to be constructed and another 328 33/11 kV substation to be upgraded.

C. Financial Management Assessment

8. An effective financial management within the executing agency is a critical success factor for project sustainability, both in the effective use of funds and in the safeguard of assets once created. A FMA of the four executing agencies was conducted as part of the financial due diligence of the executing agencies to assess their capacities to implement the Power Transmission and Distribution System Improvement project administered by ADB. The approach as outlined below has been taken for the study which is also consistent with the methodology recommended as per “Financial Due Diligence A Methodology Note, ADB, January 2009.” 9. The adequacy of the existing financial management at the executing agencies was evaluated to assess its compliance with ADB’s Guidelines1 and to identify measures that would need to be instituted to ensure compliance with ADB requirements.

10. As part of the due diligence, earlier assessments conducted by ADB were also reviewed. To fully understand the appropriateness of the financial management system in the executing agency, an overall evaluation of the risks is carried out by determining to what extent the current system complies with the requirements of the standards of practice, and what measures need to be taken to ensure effective and acceptable financial management systems prior to beginning of the project. 11. The ADB Financial Management Assessment Questionnaire2 (FMAQ) was used to collect the relevant information from the executing agencies. Once the issues/weaknesses are identified, the most appropriate mitigation measures have also been recommended for each category of review being undertaken.

1. Findings of the Study and Recommendations – MP TRANSCO

a. Budgeting and Planning

12. MP Transco is a wholly owned State Government Organization. The company’s revenue is determined through the tariff approved by the MPERC based on the Multi Year Tariff (MYT) framework. MP Transco has to prepare a business plan including capital expenditure plan for the MYT control period (usually 3 years), based on which the Commission approves the Tariff. The contribution from the State Government in terms of equity/loan is however reliant on the State Annual Budget provided by the Government considering the resource availability. 13. The foreign exchange received from ADB by GOMP via the Central Government and designated for MP Transco is disbursed under the following ways – (i) it is transferred to MP Transco account if the expenses are to be reimbursed or (ii) there is a direct payment to the designated bank in case a letter of credit (LC) is opened for payment to the contractor for turnkey package implementations. The foreign exchange risk is entirely absorbed by GOMP in all the cases.

b. Accounting and Reporting

1 “Financial Due Diligence A Methodology Note, ADB, January 2009.”

2 Responses to the FMAQ are provided in the Annexure Tables.

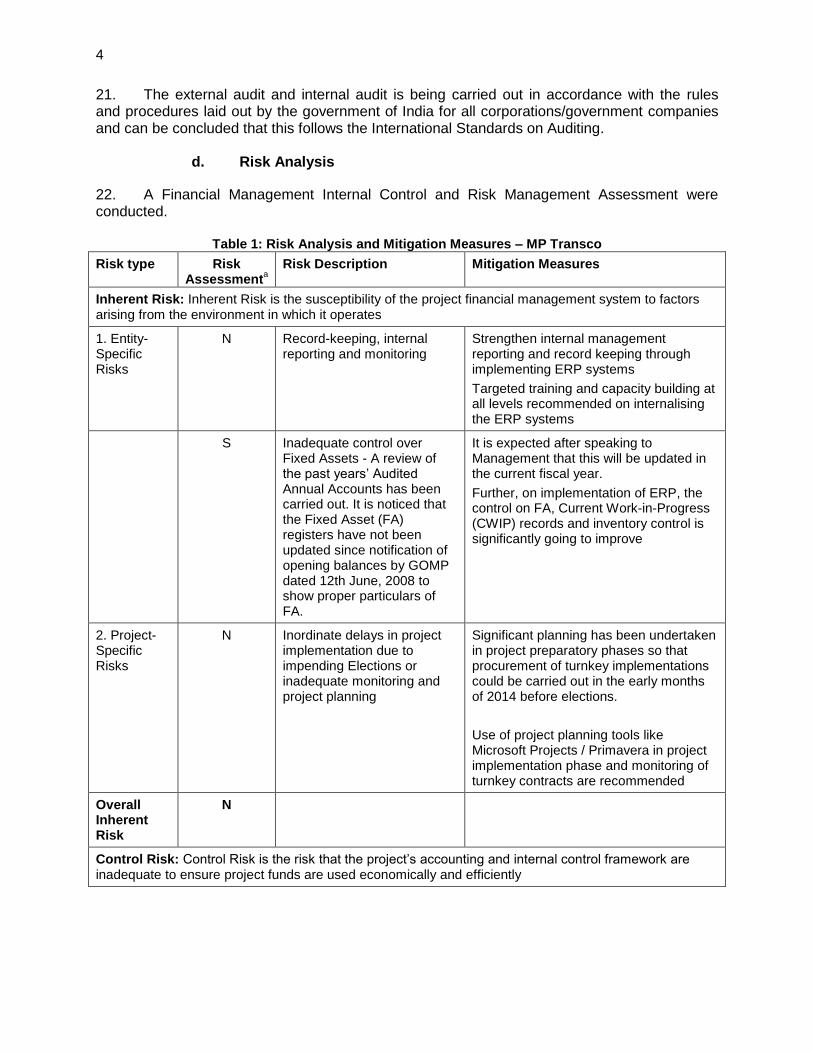

3

14. MP Transco has adequate capacity for project accounting, reporting, and managing funds flow, and has previously managed external projects financed by multilateral and bilateral donor agencies. 15. MP Transco’s annual accounts are prepared on accrual accounting basis in accordance with Indian accounting standards. The accounts department is adequately staffed with qualified professionals and recent recruitments have been all qualified chartered accountants. There are few vacant positions which being promotional in nature cannot be filled in on immediate basis and from lateral recruitments. There is no training policy manual existing in the company. However, need based training is provided.

16. The current accounting system is being run by a mix of manual book keeping and a legacy batch processing financial accounting system. An enterprise resource planning (ERP) is awaited where finance and accounts will also be adequately addressed, post which the system will have provisions to generate accounting and reporting statements for management discussions and management information system (MIS) purpose. 17. MP Transco’s existing accounting system, the legacy batch processing financial accounting system is inadequate. The company is in advanced stages of implementation of ERP (tender prepared for appointing consultant) and is expected to be on ERP by 2015. A comprehensive ERP is therefore awaited and to fully operationalize the software so as to prepare the accounting and reporting requirements, the MP Transco staff needs to be entirely aware of the features and functionalities of the enterprise system. This may require additional trainings, over and above the knowledge sharing workshops planned by the implementing agency.

c. External and Internal Audit

18. The annual accounts of MP Transco are audited by the statutory auditor appointed by the company and approved by the Comptroller Auditor General’s (CAG’s) office. A supplementary audit of the annual accounts is being carried out by the CAG office as well. 19. A review of the past years’ audited annual accounts has been carried out. It is noticed that the fixed asset registers have not been updated since notification of opening balances by GOMP dated 12 June 2008 to show proper particulars of fixed asset. This will help determine and maintain appropriate schedules of depreciation of fixed asset. It is expected after speaking to Management that this will be updated in the current fiscal year. As the company will be on ERP, it is expected that fixed asset register, current work-in-progress (CWIP) records and inventory control is significantly going to improve and filing tariff petitions and submission of data to MPERC will become easier. Also, the Statutory Auditor has commented on strengthening of the internal audit function to commensurate the size and nature of the business 20. An internal audit department exists with MP Transco which appoints and monitors the work carried out by a chartered accountant firm undertaking the internal audit and also coordinates with other departments for implementing any action recommended by the internal audit team. The chartered accountant firm is appointed through a publicly tendered competitive process. The findings of the internal audit carried out are reported to respective departments and the audit committee. There is a quarterly review by screening committee headed by Managing Director on the compliance. The representatives of Members of Board are members of the Audit Committee as well. No major observation of internal audit has been reported except reporting of minor observations which are rectified.

4

21. The external audit and internal audit is being carried out in accordance with the rules and procedures laid out by the government of India for all corporations/government companies and can be concluded that this follows the International Standards on Auditing.

d. Risk Analysis

22. A Financial Management Internal Control and Risk Management Assessment were conducted.

Table 1: Risk Analysis and Mitigation Measures – MP Transco

Risk type Risk Assessment

a

Risk Description Mitigation Measures

Inherent Risk: Inherent Risk is the susceptibility of the project financial management system to factors arising from the environment in which it operates

1. Entity-Specific Risks

N Record-keeping, internal reporting and monitoring

Strengthen internal management reporting and record keeping through implementing ERP systems

Targeted training and capacity building at all levels recommended on internalising the ERP systems

S Inadequate control over Fixed Assets - A review of the past years’ Audited Annual Accounts has been carried out. It is noticed that the Fixed Asset (FA) registers have not been updated since notification of opening balances by GOMP dated 12th June, 2008 to show proper particulars of FA.

It is expected after speaking to Management that this will be updated in the current fiscal year.

Further, on implementation of ERP, the control on FA, Current Work-in-Progress (CWIP) records and inventory control is significantly going to improve

2. Project-Specific Risks

N Inordinate delays in project implementation due to impending Elections or inadequate monitoring and project planning

Significant planning has been undertaken in project preparatory phases so that procurement of turnkey implementations could be carried out in the early months of 2014 before elections.

Use of project planning tools like Microsoft Projects / Primavera in project implementation phase and monitoring of turnkey contracts are recommended

Overall Inherent Risk

N

Control Risk: Control Risk is the risk that the project’s accounting and internal control framework are inadequate to ensure project funds are used economically and efficiently

5

Risk type Risk Assessment

a

Risk Description Mitigation Measures

1. Staffing N Staffing skills are satisfactory for book keeping, but staff responsibilities for the effectiveness of the accounting systems and reports could be improved.

Vacant positions may be temporarily filled with contract appointments.

Accounting staff to be mentored to higher skills levels

Rotation of accounting duties to be used where feasible

Provide regular training on ADB’s procurement and disbursement processes to new recruits.

2. Accounting and Reporting

S Inadequate control over management reporting - Current accounting system is being run by a mix of manual book keeping and a legacy batch processing Financial Accounting system

Comprehensive ERP system to be implemented

Training on system skills and use of ERP

N The Gratuity, Pension fund, Leave Encashment has been accounted for on the basis of Actuarial Valuation report 2009 and thereafter no Actuarial Valuation was done – This may lead to delay in True-Up of Annual Revenue Requirement

A revised / renewed actuarial valuation be undertaken

3. Internal Audit

S The Statutory Auditor has commented on strengthening of the Internal Audit (IA) function to commensurate the size and nature of the business

Even though all processes for Internal Audit have been laid out adequately, the IA Department staffing needs to be strengthened for coordinating and monitoring compliance of other Departments on the IA findings

Screening Committee review of the IA findings needs to be strengthened and personally driven and monitored by Managing Director

Overall Control Risk

S

a H = high, M = moderate, N = negligible or low, S = substantial

e. Assurances / Covenants

23. Right of Audit: MP Transco will ensure that contracts financed from the ADB loan facility will include provisions specifying the right of ADB to audit and examine the accounts of the MP Transco detailing records of all contractors, suppliers, consultants, and other service providers as they relate to the project(s) under the facility.

6

24. Financial Management: MP Transco will engage independent auditor to ensure timely and rigorous reconciliations, orderly record keeping, and strict adherence to financial management policies and internal controls, for the preparation and audit of annual project accounts.

2. Findings of the Study and Recommendations – All DISCOMs

a. Budgeting and Planning

25. DISCOM-C, DISCOM-W and DISCOM-W are wholly owned State Government Organizations. Similar to MP Transco, the revenue billed for these companies is also determined through the tariff approved by the MPERC every year. Following the similar principles of tariff filing, the DISCOMs have to project the annual revenue requirement for the ensuing year including the capital investment plan to MPERC for approval and fixation of tariff. The contribution from the State Government in terms of equity/loan support is however reliant on the State Annual Budget provided by the Government considering the resource availability. 26. The foreign exchange received from ADB by GOMP and designated for each of the DISCOM’s use is disbursed a similar way as is disbursed for MP Transco and the foreign exchange risk is absorbed by GOMP.

b. Accounting and Reporting

27. All the DISCOMs have adequate capacity for project accounting, reporting, and managing funds flow, and have previously managed external projects financed by ADB. 28. DISCOMs annual accounts’ are prepared on accrual accounting basis in accordance with Indian Accounting Standards. Also, the accounts department for each DISCOM is adequately staffed with qualified professionals. A training Institute have recently been commissioned to facilitate DISCOM staff where need based training is provided. 29. There is a Sybase based legacy accounting system in all the DISCOMs. The current accounting system is partially being run on it for generating certain MIS reports. An ERP is awaited where finance and accounts will also be adequately addressed, post which the system will have provisions to generate accounting and reporting statements for management discussions and MIS purpose. In DISCOM-C, this is expected to be rolled out by December, 2013 (HR and few other modules are already being run on ERP and Tata Consultancy Services is the chosen vendor for implementing ERP) while in the other two DISCOMs (DISCOM-E and DISCOM-W), ERP is expected to be rolled out by the year 2015.

30. Additional training on ERP is recommended once implemented in all three DISCOMs.

c. External and Internal Audit

31. The annual accounts of the DISCOMs are audited by the statutory auditor appointed by each of the DISCOM through a competitive process from a list of empaneled vendors approved by CAG. A supplementary audit of the annual accounts is being carried out by the CAG office as well. 32. A review of the audited annual accounts has been carried out for all the DISCOMs. It is observed that capitalization from CWIP is being done only on receipt of technical certificate from the respective field officers and there have been no inconsistencies reported by MPERC in the

7

tariff orders regarding financial accounting registers, CWIP records and inventory control. The Statutory Auditor for DISCOM-E has commented on strengthening the internal audit practices and extending this to all distribution centers audit. A lack of adequate internal control is observed in most departments with missing audit trails. Also, there have been pending entries in the reconciliation statements in relation to bank accounts of the DISCOM-E which have not been rectified. These balances upon reconciliation may affect the assets/liabilities and profit and loss of prior years. There have been inconsistencies reported by the statutory auditor of DISCOM-W in the year 2011-2012 in the amounts of receivables as recorded in Consumer Ledgers vis-à-vis Consumer Ledgers. The figures are under reconciliation and will be taken up by MPERC during the True-Up exercise. 33. Internal audit is outsourced and carried out by chartered accountant firm in all the three DISCOMs. The internal audit department exists with each of the DISCOMs and is staffed by qualified chartered accountants and it reports to Additional Director, Finance and Accounts. The findings of the internal audit carried out are reported to respective Departments and the audit committee. There is a quarterly review by Screening Committee headed by Managing Director on the compliance. The representatives of Members of Board are members of the Audit Committee as well. No major observation of internal audit has been reported as per Additional Director, DISCOM-C. Minor observations include interest wrongly calculated for ‘n’ number of days; provisions have been made in wrong account codes, etc.

d. Institutional Structure

34. Each of the three DISCOMs, every year, files individual tariff petitions to the Honorable Commission specifying their Annual Revenue Requirements for the ensuing year(s) to which the Commission comes out with a single Tariff Order notifying tariffs for the entire state for various categories of consumers. It was conveyed by GOMP in FY2012-2013 that the tariff for the each consumer category will be kept the same across the state in the foreseeable future. 35. The Madhya Pradesh Power Management Company (the Holding Company), does all the power procurement on behalf of the DISCOMs and allocates the generating capacities to each of the DISCOM based on share of their revenues. With 85% of the total expenses being the power purchase cost for any DISCOM, there is a centralized cash management being carried out by the Holding Company. The revenue receipts from each of the DISCOM are transferred to the Holding Company. There is a book entry adjustment in each DISCOM Account for the power purchase cost. The salary expenses and other O&M expenses are compensated by the Holding Company. There is a non-revenue receipt account with each DISCOM which includes revenues from supervision charges, meter testing charges, interest income, proceeds from sale of scrap, etc. This account is being adjusted against the administrative & general expenses and the civil related contractor payables.

36. The loans are in the books of the DISCOMs and are credited directly to each of the DISCOM accounts, with all project related expenditure being disbursed from the proceeds of the same. A demand is raised by each of DISCOM to the Holding Company for any repayment and interest payment.

e. Risk Analysis

37. A Financial Management Internal Control and Risk Management Assessment were conducted.

8

Table 2: Risk Analysis and Mitigation Measures - DISCOMs

Risk type Risk Assessment

a

Risk Description Mitigation Measures

Inherent Risk: Inherent Risk is the susceptibility of the project financial management system to factors arising from the environment in which it operates

1. Entity-Specific Risks

N Record-keeping, internal reporting and monitoring

Strengthen internal management reporting and record keeping through implementing ERP systems

Targeted training and capacity building at all levels recommended on internalising the ERP systems

S Inadequate loss reduction and failure to achieve loss reduction targets as given by Commission

100 % Meterization of Agriculture and Domestic (BPL) consumers as suggested by MPERC

Intensify efforts in reducing the Distribution Losses through various Technical and Commercial interventions - Aerial Bunched (AB) cabling instead of overhead lines in LT networks in rural as well as in urban area, Automated Meter Reading (AMR) of LT high value consumer, etc.

2. Project-Specific Risks

N Inordinate delays in project implementation due to impending Elections or inadequate monitoring and project planning (progress review of past ADB Loans show compliance in most cases except few milestones falling short of targets)

Significant planning has been undertaken in project preparatory phases so that procurement of turnkey implementations could be carried out in the early months of 2014 before elections.

Use of project planning tools like Microsoft Projects / Primavera in project implementation phase and monitoring of turnkey contracts are recommended

Overall Inherent Risk

N

Control Risk: Control Risk is the risk that the project’s accounting and internal control framework are inadequate to ensure project funds are used economically and efficiently

1. Staffing N Staffing skills are satisfactory for book keeping, but staff responsibilities for the effectiveness of the accounting systems and reports could be improved.

Accounting staff to be mentored to higher skills levels

Rotation of accounting duties to be used where feasible

Provide regular training on ADB’s procurement and disbursement processes to new recruits.

9

Risk type Risk Assessment

a

Risk Description Mitigation Measures

2. Accounting and Reporting

S Inadequate control over management reporting - Current accounting system is being run on a Sybase based legacy Accounting System in all DISCOMs and provide inadequate control over Management Reporting

Comprehensive ERP system to be implemented

Training on system skills and use of ERP

N There have been pending entries in the reconciliation statements in relation to Bank accounts of the DISCOM-E which have not been rectified. These balances upon reconciliation may affect the Assets/ Liabilities and profit and loss of prior years

Undertake account and bank reconciliations on a periodic basis

3. Internal Audit

H The Statutory Auditor has commented on strengthening the Internal Audit practices and extending this to all Distribution Centers’ Audit. A lack of adequate internal control is observed in most Departments with missing Audit trails.

Even though adequate internal audit processes have been laid out in the DISCOMs, the IA has been restricted to Head Quarters and not been extended to all Division and Sub-Division offices

IA to be extended to all Distribution Centers.

Internal Audit Department staffing needs to be strengthened for coordinating and monitoring compliance of other Departments on the IA findings

Screening Committee review of the IA findings needs to be strengthened and personally driven by Managing Director

Overall Control Risk

S

a H = high, M = moderate, N = negligible or low, S = substantial

f. Assurances / Covenants

38. Right of Audit: DISCOMs will ensure that contracts financed from the ADB Loan facility will include provisions specifying the right of ADB to audit and examine the accounts of the DISCOMs detailing records of all contractors, suppliers, consultants, and other service providers as they relate to the Project(s) under the Facility. 39. Financial Management: DISCOMs will engage independent Auditor to ensure timely and rigorous reconciliations, orderly record keeping, and strict adherence to financial management policies and internal controls, for the preparation and audit of annual project accounts.

10

D. Past Financial Performance and Projections

40. MPSEB allocated assets and liabilities to the individual companies as at 31 May 2005. These balance sheets allocations were only provisional. The final opening Balance sheet was notified on 12th June 2008. The utilities accordingly prepared the annual accounts for the year FY2007-08, FY2008-09 and FY2010-11 and had it audited as per final opening balance sheet.

1. Past Financial Performance and Projections - MP TRANSCO

a. Past Financial Performance

41. MP Transco transmission losses came down from 5.23% to 3.74% over the last 5 years. It has also been able to meet the target as given by MPERC. The summary of MP Transco past financial performance is given in Table 2. MP Transco has been consistently reporting losses since 2007-2008. These losses have resulted in an erosion of equity in the balance sheet. The total cumulative losses post unbundling stood at Rs1,386 million as on March 2012. The financial losses for FY2010-2011 are mainly attributed to disallowance of terminal benefits which is allowed in 2013 during True-UP. Also there has been a payment of ‘deferred tax for current year’ FY2009-2010 until FY2011-12 in spite of MP Transco reporting negative profit before tax (PBT). There has also been a write-off of Rs3,273 million shown in extraordinary items which has contributed to the loss in FY2011-2012.

Table 3 : Summary of MP Transco Past Financial Performance (Rs Million)

Particulars FY 08 FY 09 FY 10 FY 11 FY 12

P&L Items

Income 8,049 8,189 10,995 14,489 17,262

R&M 159 216 185 331 450

Employee 1,238 1,404 2,252 1,732 1,918

Terminal Benefit 3,080 3,375 4,826 6,428 7,084

A&G 171 96 245 191 344

Others 0 399 - - -

Extraordinary Items - - - - 3,273

PBITDA 3,400 2,599 3,488 5,807 4,193

Depreciation 1,776 1,947 2,166 2,471 2,668

PBIT 1,624 652 1,321 3,336 1,525

Finance Charges 2,023 705 1,389 3,339 1,556

PBT (399) (53) (68) (3) (31)

Tax 12 (6) 888 181 71

PAT (412) (47) (956) (184) (102)

Balance Sheet Items

GFA 35,760 39,541 45,446 50,226 52,567

Accumulated Depreciation (16,824) (18,772) (20,916) (23,358) (25,951)

WIP 4,802 7,217 6,911 4,186 5,945

Current Assets 11,878 9,947 17,503 21,422 23,635

Total Assets 35,615 37,934 48,944 52,477 56,195

Equity* 11,394 13,101 20,007 20,260 20,458

Long Term Borrowings 20,169 20,730 21,747 16,752 18,339

Deferred Tax Liability - - 887 1,068 1,139

Consumer Contribution - - - 1,398 1,691

11

Particulars FY 08 FY 09 FY 10 FY 11 FY 12

Liability for Terminal Benefits 670 - - - -

Current Liabilities & Provisions 3,382 4,103 6,303 12,999 14,568

Total Liabilities 35,615 37,934 48,944 52,477 56,195

Cash Flow Statement

Net P&L for the year (412) (47) (69) (3) (31)

Depreciation 1,776 1,947 2,166 2,480 2,668

Interest and finance charges 2,023 705 1,389 3,383 1,556

Preliminary Exp W/off 0 0 0 - -

Interest Received (26) (70) (86) (165) (273)

Change in Working capital (3,633) 2,464 (4,157) (3,701) 1,918

Cash flow from operating activities (271) 5,000 (757) 1,995 5,838

Capital Expenditure (781) (6,196) (5,620) (1,871) (4,328)

Investments - - - - (3,223)

Interest Received 26 70 86 165 273

Cash flow from investing activities (755) (6,127) (5,534) (1,706) (7,278)

Equity 1,038 1,754 7,862 437 300

Loan 2,785 564 1,016 3,254 1,587

Interest and finance charges (2,023) (705) (1,389) (3,383) (1,556)

Long-Terms Provisions - - - - 316

Cash flow from financing activities 1,799 1,614 7,489 308 648

Cash Generated 773 487 1,198 597 (792)

Ratios

Return on GFA -1.15% -0.12% -2.10% -0.37% -0.19%

Debt (LT) / Debt (LT)+Equity* 64% 61% 52% 45% 47%

Basic Earnings Per Share (4.56) (0.52) (10.61) (1.65) (0.50)

Diluted Earnings Per Share (4.13) (0.39) (7.00) (0.87) (0.50)

Current Ratio 3.51 2.42 2.78 1.65 1.62

Return on Net Worth -3.6% -0.4% -4.8% -0.9% -0.5%

PAT/Revenue -5.1% -0.6% -8.7% -1.3% -0.6% GFA = general fix asset, LT = long term, PAT = profit after tax, PBIT = profit before income tax, PBITDA = profit before income tax, depreciation, and amortization, PBT = profit before tax, P&L = profit and loss, R&M = repair and maintenance, WIP = work in progress. * Equity includes accumulated profits/losses. Source: MP Transco Annual Reports, ADB analysis.

b. Financial Projections

42. This section sets out the financial projections for MP Transco from FY2012-2013 to FY2019-2020. The MPERC approved tariff order for MP Transco for the period FY2013-2014 to FY2015-2016 has been referred to for drawing projections for revenue and expenses and the Commission’s approach on approving tariff for the MYT Period has been considered to determine the transmission tariff applicable in the state for future years. The physical assets additions have been projected based on the 12th Year Plan and the past trend of capital expenditure incurred by MP Transco vis a vis expenditure proposed as per 11th year plan. The operations and maintenance (O&M) expenses have been projected based on the commission’s defined norms. A return on equity of 15.5% is considered as approved by commission. Loans required for future capital expenditure has been considered to be repaid in 10 years with a

12

moratorium period of 1 year. The average rate of interest for past loan has been considered for future interest projections. 43. MP Transco financial projections show that with progressive tariff increases (approved by MPERC) profitability could be achieved from FY2012-2013 onwards. The GFA will grow at a CAGR of ~10% to reach Rs141 billion by the end of FY2021-2022. With profitability in FY2012-2013, MPPTCL’s return on average net fixed assets increases to 6.07% in FY2012-2013 to reach 7.36% in FY2021-2022. As a result of this, the company will have sufficient internal cash accrual to contribute to the capital expenditure in the future. As a result of profitability in future, the reserve and surplus will increase and the debt/debt plus equity ratio is forecast to fall from 47% in FY2012-2013 to 41% by FY2016-2017 and to 37% by FY2021-2022. As a result of accumulation of retained earnings from FY2012-13 onwards, MP Transco equity position would be Rs76 billion at the end of FY2021-2022. Current assets equal or exceed current liabilities in all years indicating that MPPTCL can meet its current liabilities. 44. The summary of MP Transco financial projections is given in Table 4:

Table 4: Summary MP TRANSCO Financial Projections (Rs million)

Particulars FY13 FY14 FY15 FY16 FY17 FY18 FY19

P&L

Revenue from Transmission

of Power 17,175 19,190 21,029 22,789 25,173 28,140 31,353

Other Income 345 300 255 210 165 120 75 Total Revenue 17,520 19,490 21,284 22,998 25,338 28,260 31,428

Operating Expenses 10,621 11,752 12,964 14,273 15,741 17,444 19,391 Depreciation 2,862 3,204 3,531 3,812 4,130 4,601 5,082 Interest Charges 1,681 1,821 1,919 2,001 2,151 2,401 2,635 Total Expenses 15,163 16,776 18,414 20,086 22,021 24,445 27,109 Profit Before Tax 2,356 2,714 2,870 2,912 3,316 3,814 4,319 Tax 471 569 602 610 695 800 905 Profit After Tax 1,885 2,145 2,268 2,302 2,621 3,015 3,414

Balance Sheet

Gross Fixed Assets 59,850 65,975 72,695 77,037 85,171 95,525 104,087 Accumulated Depreciation 28,813 32,017 35,548 39,360 43,490 48,091 53,173 Net Fixed Assets 31,037 33,958 37,147 37,677 41,681 47,434 50,914 WIP 4,161 2,378 - - - - - Current Assets 30,804 35,084 39,483 43,882 48,733 54,007 59,508 Total Assets 66,001 71,421 76,630 81,559 90,414 101,441 110,422

Equity* 23,993 27,441 31,012 34,616 39,677 45,798 51,781 Long term Liabilities 21,087 22,641 23,890 24,836 28,132 32,412 34,714 Deferred Tax Liability 1,139 1,139 1,139 1,139 1,139 1,139 1,139 Consumer Contribution 1,691 1,691 1,691 1,691 1,691 1,691 1,691 Current Liabilities 18,091 18,509 18,898 19,277 19,774 20,400 21,097 Total Equity & Liabilities 66,001 71,421 76,630 81,559 90,414 101,441 110,422

Cash Flow

Net P&L for the year 1,885 2,145 2,268 2,302 2,621 3,015 3,414 Depreciation 2,862 3,204 3,531 3,812 4,130 4,601 5,082 Interest and finance charges 1,681 1,821 1,919 2,001 2,151 2,401 2,635 Change in Working capital (3,522) (418) (389) (379) (498) (626) (697) Cash flow from operating 2,905 6,751 7,329 7,737 8,404 9,390 10,434

13

Particulars FY13 FY14 FY15 FY16 FY17 FY18 FY19

activities

Capital Expenditure (5,500) (4,342) (4,342) (4,342) (8,134) (10,354) (8,562) Cash flow from investing

activities (5,500) (4,342) (4,342) (4,342) (8,134) (10,354) (8,562)

Equity 1,650 1,303 1,303 1,303 2,440 3,106 2,569 Loan 2,749 1,553 1,249 946 3,296 4,280 2,302 Interest and finance charges (1,681) (1,821) (1,919) (2,001) (2,151) (2,401) (2,635) Short term loans 3,522 418 389 379 498 626 697 Cash flow from financing

activities 6,241 1,453 1,022 626 4,084 5,612 2,932

Cash Generated 3,646 3,863 4,009 4,020 4,353 4,648 4,804

Ratios

Return on NFA 6.07% 6.32% 6.11% 6.11% 6.29% 6.36% 6.70%

DSCR 3.59 3.64 3.68 3.67 3.72 3.71 3.70 Debt/(Debt + Equity*) 47% 45% 44% 42% 41% 41% 40%

DSCR = debt service coverage ratio; P&L = profit and loss; WIP = work-in-progress.

* Equity includes accumulated profits/losses.

2. Past Financial Performance and Projections - DISCOMs

a. Past Financial Performance

45. DISCOM-C has been consistently making losses since MPSEB allocated assets and liabilities to the individual companies as at 31 May 2005. These balance sheets allocations were only provisional. The final opening balance sheet was notified on 12 June 2008. The Commission has not taken the impact of final opening balance sheet while finalizing the Tariff order of FY2010-2011 and has allowed considering it during the time of true up. 46. DISCOM-C made a loss of Rs5,503 million in FY2008-2009 and the losses have risen up to the tune of Rs6,322 million in FY2011-2012. The accumulated losses in FY2011-2012 for DISCOM-C were to the tune of Rs44,080 million. The debt service coverage ratio has been negative in all these years, which indicates that the company is caught in a debt trap, where it is required to borrow from external sources in order to fulfill its financial liability. 47. The deteriorating financial health of the company can be attributed to the low operational efficiency of the company. The T&D losses of the company are around 32.70% (FY 2011-12) and the collection efficiency of the company is close of 90% (including subsidy). 48. DISCOM-C, in FY2011-2012, was sitting on a huge arrear figure. The arrears although represent the current assets of the company but a majority of these arrears are irrecoverable and hence cannot be liquidated into cash and hence are non-performing assets. Another major reason for significant financial losses is that the tariff increase allowed by MPERC is not in-line with the increase in expenses of the company. These losses resulted in an erosion of equity in the balance sheet. DISOMC–C does not meet its own debt service. 49. There is absence of 100% metering in LT domestic consumers and most of the agricultural consumers are unmetered and billed as per assessed units determined by the

14

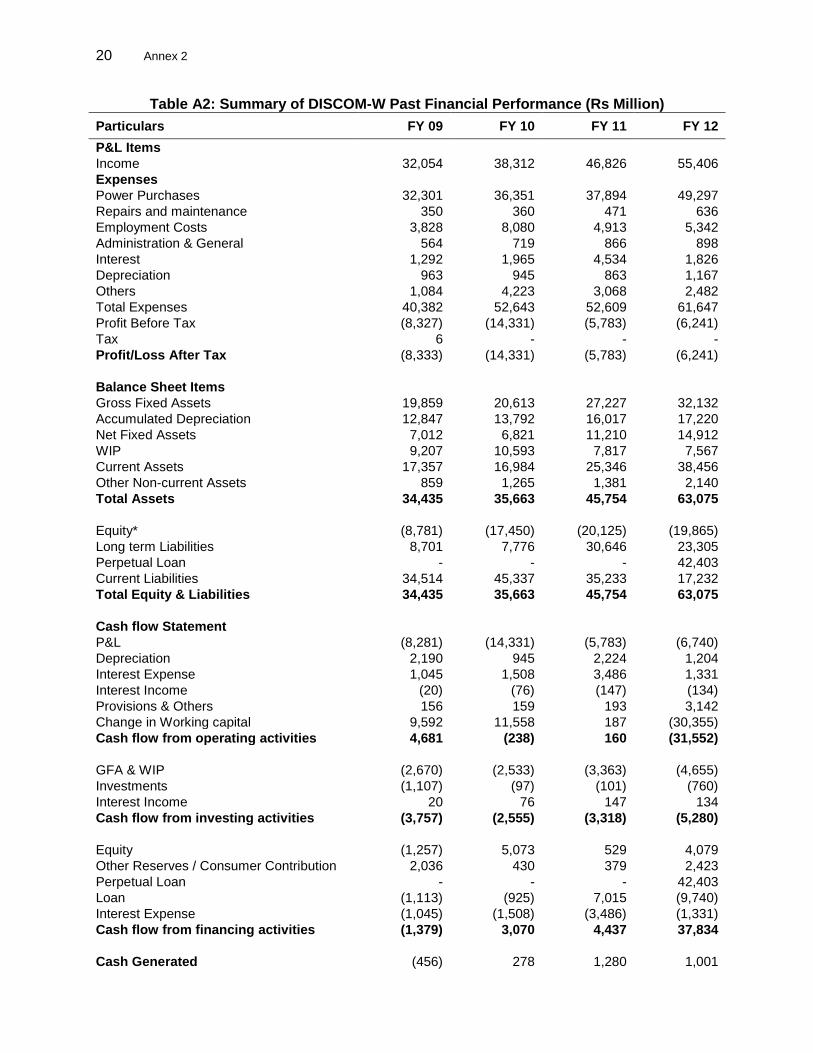

Commission. This point to the inability of DISCOM-C in reliably measuring its operational performance. 50. The negative operating cash flow and low Current Ratio along with high receivables and payables days indicate DISCOM-C is not able to generate enough cash to meet its obligations in the past. The summary of DISCOM-C past financial performance is given in Table 5. The summary of DISCOM-W and DISCOM-E are provided in the Annex Tables 1 and Table 2.

Table 5: Summary of DISCOM-C Past Financial Performance (Rs million)

Particulars FY 08 FY 09 FY 10 FY 11 FY 12

P&L Items

Income 24,128 27,387 30,986 35,792 43,518

Expenses

Power Purchases 22,603 24,786 27,632 30,639 40,270

Repairs and maintenance 301 403 273 234 267

Employment Costs 3,162 3,822 4,796 5,103 5,084

Administration/Other 1,910 2,356 2,053 1,276 1,421

Interest 480 645 1,120 3,558 1,554

Depreciation 613 874 978 1,087 1,244

Total Expenses 29,069 32,885 36,851 41,896 49,840

Profit Before Tax (4,941) (5,498) (5,865) (6,104) (6,322)

Tax 4 5 - - - Profit/Loss After Tax (4,945) (5,503) (5,865) (6,104) (6,322)

Balance Sheet Items

Gross Fixed Assets 16,879 20,446 22,567 23,969 30,966 Accumulated Depreciation 10,571 11,344 12,322 13,409 14,653 Net Fixed Assets 6,307 9,103 10,246 10,561 16,313 WIP 4,231 3,630 4,182 6,616 4,109 Current Assets 14,218 22,261 24,230 32,008 37,770 Other Non-current Assets 753 488 5,172 6,558 9,562 Total Assets 25,510 35,482 43,829 55,742 67,755

Equity* (7,229) (10,477) (12,692) (15,421) (23,153) Long term Liabilities 12,006 17,796 26,629 23,237 54,505 Other Long term liabilities and

provisions

2,475 7,829 10,819 12,977 15,450

Current Liabilities 18,258 20,334 19,074 34,948 20,953 Total Equity & Liabilities 25,510 35,482 43,829 55,742 67,755

Cash flow Statement**

Net P&L for the year (6,104) (6,322) Depreciation 1,069 1,244 Provisions & Others 1,395 (2,715) Change in Working capital (5,122) (18,408) Cash flow from operating activities (8,762) (26,200)

GFA & WIP (5,208) (7,426) Cash flow from investing activities (5,208) (7,426)

Equity 2,542 1,186 Other Reserves / Consumer

Contribution 835 2,560

Loan 13,516 30,913 Others cash equivalents fdrs (2,195) (125)

15

Particulars FY 08 FY 09 FY 10 FY 11 FY 12

Cash flow from financing activities 14,698 34,534

Cash Generated 727 908

Ratios

Return on NFA -78% -60% -57% -58% -39%

PAT/Revenue -20% -20% -19% -17% -15%

D/E* (1.66) (1.70) (2.10) (1.51) (2.35)

Current Ratio 0.78 1.09 1.27 0.92 1.80

D/E = debt/equity; Current Ratio = current assets / current liabilities; P&L = profit and loss; WIP = work-in-progress.

* Equity includes accumulated profits/losses.

** Cash flow Statement for FY2008 to FY2010 is not available in English Language.

Source: DISCOM-C Annual Reports.

c. Financial Projections

51. This section sets out the financial projections for DISCOM-C from FY2012-2013 to FY2016-2017. The category wise tariff has been projected to reach the cross subsidy target of +/- 20% by FY2014-2015. The R&M has been projected based on the past trend of R&M expenses as a percent of gross fixed assets and the A&G has been projected based on past trend of A&G expense as a percent of revenue from sale of power. Employee expenses has been projected based on the future projection of manpower additions and retirement. 52. DISCOM-C has committed to bring down the distribution losses during the six year plan period, such that the aggregate distribution losses by FY2016-2017 are 19%, down from the 33% at the end of FY2011-2012. One of the other measures which is proposed to be undertaken to achieve the improved performance is the revision of normative agricultural consumption to reflect the actual consumption and also metering all unmetered consumers as suggested by the Commission as well in the Tariff Order FY2013-14. 53. It is assumed that GOMP shall provide all the support in form of government guarantee for new loans till a period the company is able to raise loans from the market without any guarantee, the necessary equity contribution committed towards capital investments and other administrative support for improving the collection efficiency and prevention of theft. 54. A Financial Restructuring Plan3 (FRP) was approved by GOMP vide order no 6054/13/2011/02 dated 13.07.2011. Under the FRP, along with conversion of outstanding working capital loans from GOMP into perpetual loan, retention of ED and Cess for the next three years and conversion of this outstanding ED and Cess into perpetual loans, retention of power purchase payables for Sardar Sarovar and conversion of these outstanding payables into perpetual loans, it is also approved that to provide an interest holiday for three years to ensure that the distribution companies have some relief in the cash flows, while the interest rate to be charged thereon would be the base rate of SBI. This FRP intervention would benefit the distribution companies immensely in short term (next 6 years) while in long term it would not decrease the benefit (value) to the Government.

3 Ministry of Power vide order no 20/11/2012-APDRP dated 5 October 2012 proposed a scheme for Financial

Restructuring of State Distribution Companies. There has been no confirmation from GOMP / DISCOMs to endorse the same as most items proposed under the scheme have been considered in earlier notified FRP by GOMP.

16

55. DISCOM-C financial projections show that with progressive tariff4 increase as approved by MPERC at cost plus return on equity (ROE) basis, profitability could be achieved by FY2014-FY2015. With profitability in FY2014-FY2015, DISCOM-C’s return on average net fixed assets (RONA) increases to 18%. The cash flow position improves with debt service ratio becoming positive and improving to 2.07 in FY2016-FY2017. 56. The self-financing capacity of the company is limited in the short term but improves over the longer term so that the company should be able to contribute to their capital expenditure in the future. As a result of a negative equity position in FY2011-FY2012 and continuing losses until FY2013-FY2014, the debt/equity ratio is forecast to improve but will still remain negative As a result of accumulation of retained earnings from FY2014-FY2015 onwards, DISCOM-C’s equity position would be improving from FY2014-FY2015 onwards. The summary of DISCOM-C financial projections is given in Table 6.

Table 6: Summary DISCOM-C Financial Projections (Rs Million)

Particulars FY13 FY14 FY15 FY16 FY17

Sales (Mus) 9,940 13,143 16,077 20,088 23,952

%change 32% 22% 25% 19%

Average Revenue (Rs/kWh) 4.82 5.31 5.94 5.34 4.71

%change 10% 12% -10% -12%

P&L

Revenue from Sale of Power 47,959 69,780 95,450 107,365 112,924 Other Income 1,025 1,396 1,302 1,439 1,438 Total Revenue 48,984 71,176 96,753 108,804 114,362

Operating Expenses 54,438 70,088 75,696 86,581 90,564 Depreciation 1,544 2,117 2,723 3,193 3,546 Interest Charges 2,552 2,552 8,579 8,051 7,938 Total Expenses 58,534 74,757 86,997 97,825 102,048 Profit Before Tax (9,550) (3,580) 9,755 10,978 12,314 Tax - - 1,944 2,188 2,454 Profit After Tax (9,550) (3,580) 7,811 8,790 9,860

Balance Sheet

Gross Fixed Assets 39,148 52,318 63,705 71,471 79,486

Accumulated Depreciation 16,196 18,314 21,037 24,230 27,776

Net Fixed Assets 22,952 34,004 42,669 47,241 51,710

WIP 10,742 14,444 15,318 14,691 17,825

Current Assets 38,747 40,361 43,324 44,099 43,499

Other Non-current Assets 8,069 11,478 15,627 18,208 19,691

Total Assets 80,510 100,287 116,938 124,240 132,725

Equity* (30,847) (30,570) (19,486) (8,253) 10,134

Long term Liabilities 56,124 69,777 85,740 85,951 87,116

Other Long term liabilties and

provisions 14,768 19,749 23,433 24,308 25,520

Current Liabilities 40,465 41,330 27,251 22,233 9,956

Total Equity & Liabilities 80,510 100,287 116,938 124,240 132,725

Cash Flow

Net P&L for the year (9,550) (3,580) 7,811 8,790 9,860

4 DISCOMs have been achieving the loss targets as provided by MPERC; therefore no disallowance has been

assumed in PP cost; disallowances in O&M cost has been considered as per past trends

17

Particulars FY13 FY14 FY15 FY16 FY17

Depreciation 1,544 2,117 2,723 3,193 3,546

Interest and finance charges 2,552 2,552 8,579 8,051 7,938

Change in Working capital (1,820) 3,357 324 5,972 1,467

Cash flow from operating activities (7,274) 4,446 19,437 26,007 22,812

GFA (8,182) (13,169) (11,388) (7,766) (8,015)

WIP (6,633) (3,702) (874) 626 (3,134)

Investment 1,492 (3,408) (4,149) (2,581) (1,483)

Cash flow from investing activities (13,322) (20,280) (16,411) (9,720) (12,632)

Equity 1,168 1,879 2,395 2,616 7,827

Other Reserves / Consumer

Contribution 689 1,979 878 (173) 700

Loan 1,619 13,653 15,963 211 1,164

Other Long term liabilities and

provisions (682) 4,981 3,684 875 1,212

Interest and finance charges (2,552) (2,552) (8,579) (8,051) (7,938)

Short term loans 20,630 (3,805) (17,101) (11,478) (12,835)

Cash flow from financing activities 20,871 16,135 (2,760) (16,001) (9,870)

Cash Generated 274 301 265 286 309

Ratios

Return on NFA -42% -11% 18% 19% 19%

D/E* (1.82) (2.28) (4.40) (10.41) 8.60

DSCR (1.99) (0.27) 1.79 1.95 2.07

Current Ratio 0.96 0.98 1.59 1.98 4.37 D/E = debt/Equity; Current Ratio = current assets / current liabilities; P&L = profit and loss; WIP = work-in-progress. * Equity includes accumulated profits/losses. Source: DISCOM-C Business Plan as approved by Board in the year 2013, ADB Analysis.

57. The current financial position of DISCOM-E and DISCOM-W and the financial projections for each of these entities have been developed based on similar lines and have been presented in the Annexure Tables 3 and Table 4. It is evident from the analysis that given the commitment from the DISCOMs on loss reduction and an appropriate financial restructuring package offered by GOMP, the financial health of all the DISCOMs can significantly improve in the longer term.

18 Annex 1

Table A1: Summary of DISCOM-E Past Financial Performance (Rs Million)

Particulars FY 09 FY 10 FY 11 FY 12

P&L Items

Income 24,249 29,294 33,639 39,601

Expenses

Power Purchases 27,280 27,782 28,581 39,650

Repairs and maintenance 307 231 291 449

Employment Costs 4,102 4,661 5,690 6,230

Administration & General 725 774 743 1,265

Interest 867 1,342 3,412 1,268

Depreciation 851 1,091 948 1,170

Others 876 4,720 3,712 1,256

Total Expenses 35,008 40,601 43,377 51,287

Profit Before Tax (10,758) (11,307) (9,738) (11,686)

Tax 11 - - -

Profit/Loss After Tax (10,769) (11,307) (9,738) (11,686)

Balance Sheet Items

Gross Fixed Assets 19,443 21,966 26,002 31,737

Accumulated Depreciation 11,877 12,967 13,915 15,086

Net Fixed Assets 7,566 8,999 12,087 16,651

WIP 6,408 7,669 5,871 6,182

Current Assets 20,087 24,050 29,025 27,964

Other Non-current Assets 507 2,265 4,313 6,030

Total Assets 34,568 42,984 51,296 56,827

Equity* (12,618) (16,950) (23,343) (31,609)

Long term Liabilities 10,197 18,652 42,794 56,198

Current Liabilities 36,989 41,282 31,845 32,238

Total Equity & Liabilities 34,568 42,984 51,296 56,827

Cash flow Statement

P&L (10,769) (11,307) (9,738) (11,668)

Depreciation 851 1,091 948 1,170

Interest Expense 867 1,342 3,412 1,268

Provisions & Others 464 1,242 2,068 1,950

Change in Working capital 8,202 (685) (4,135) (2,210)

Cash flow from operating activities (387) (8,317) (7,445) (9,491)

GFA & WIP (2,892) (3,785) (4,928) (6,045)

Investments (467) (1,758) - -

Cash flow from investing activities (3,359) (5,543) (4,928) (6,045)

Equity 1,104 4,111 1,795 1,970

Other Reserves / Consumer Contribution 1,619 2,764 1,306 1,234

Loan 1,859 8,454 13,759 13,404

Interest Expense (867) (1,342) (3,412) (1,268)

Cash flow from financing activities 3,716 13,988 13,448 15,339

Cash Generated (29) 128 1,076 (197)

Ratios

Return on NFA -142% -126% -81% -70%

Annex 1 19

Particulars FY 09 FY 10 FY 11 FY 12

PAT/Revenue -44% -39% -29% -30%

D/E* (0.81) (1.10) (1.83) (1.78)

Current Ratio 0.54 0.58 0.91 0.87

D/E: Debt / Equity; Current Ratio = Current Assets / Current Liabilities; P&L: Profit & Loss; WIP: Work-in-

progress

* Equity includes accumulated profits/losses

Source: DISCOM-E Annual Reports

20 Annex 2

Table A2: Summary of DISCOM-W Past Financial Performance (Rs Million)

Particulars FY 09 FY 10 FY 11 FY 12

P&L Items

Income 32,054 38,312 46,826 55,406

Expenses

Power Purchases 32,301 36,351 37,894 49,297

Repairs and maintenance 350 360 471 636

Employment Costs 3,828 8,080 4,913 5,342

Administration & General 564 719 866 898

Interest 1,292 1,965 4,534 1,826

Depreciation 963 945 863 1,167

Others 1,084 4,223 3,068 2,482

Total Expenses 40,382 52,643 52,609 61,647

Profit Before Tax (8,327) (14,331) (5,783) (6,241)

Tax 6 - - -

Profit/Loss After Tax (8,333) (14,331) (5,783) (6,241)

Balance Sheet Items

Gross Fixed Assets 19,859 20,613 27,227 32,132

Accumulated Depreciation 12,847 13,792 16,017 17,220

Net Fixed Assets 7,012 6,821 11,210 14,912

WIP 9,207 10,593 7,817 7,567

Current Assets 17,357 16,984 25,346 38,456

Other Non-current Assets 859 1,265 1,381 2,140

Total Assets 34,435 35,663 45,754 63,075

Equity* (8,781) (17,450) (20,125) (19,865)

Long term Liabilities 8,701 7,776 30,646 23,305

Perpetual Loan - - - 42,403

Current Liabilities 34,514 45,337 35,233 17,232

Total Equity & Liabilities 34,435 35,663 45,754 63,075

Cash flow Statement

P&L (8,281) (14,331) (5,783) (6,740)

Depreciation 2,190 945 2,224 1,204

Interest Expense 1,045 1,508 3,486 1,331

Interest Income (20) (76) (147) (134)

Provisions & Others 156 159 193 3,142

Change in Working capital 9,592 11,558 187 (30,355)

Cash flow from operating activities 4,681 (238) 160 (31,552)

GFA & WIP (2,670) (2,533) (3,363) (4,655)

Investments (1,107) (97) (101) (760)

Interest Income 20 76 147 134

Cash flow from investing activities (3,757) (2,555) (3,318) (5,280)

Equity (1,257) 5,073 529 4,079

Other Reserves / Consumer Contribution 2,036 430 379 2,423

Perpetual Loan - - - 42,403

Loan (1,113) (925) 7,015 (9,740)

Interest Expense (1,045) (1,508) (3,486) (1,331)

Cash flow from financing activities (1,379) 3,070 4,437 37,834

Cash Generated (456) 278 1,280 1,001

Annex 2 21

Particulars FY 09 FY 10 FY 11 FY 12

Ratios

Return on NFA -119% -210% -52% -42%

PAT/Revenue -26% -37% -12% -11%

D/E* (0.99) (0.45) (1.52) (1.17)

Current Ratio 0.50 0.37 0.72 2.23

D/E: Debt / Equity; Current Ratio = Current Assets / Current Liabilities; P&L: Profit & Loss; WIP: Work-in-progress

* Equity includes accumulated profits/losses

Source: DISCOM-W Annual Reports

22 Annex 3

Table A3: Summary DISCOM-E Financial Projections (Rs Million)

Particulars FY13 FY14 FY15 FY16 FY17

Sales (Mus) 9,674 10,158 10,666 11,199 11,759

%change 15% 5% 5% 5% 5%

Average Revenue (Rs/kWh) 4.70 4.95 5.84 5.79 5.71

%change 4% 5% 18% -1% -1%

P&L

Revenue from Sale of Power 45,440 50,310 62,253 64,818 67,168

Other Income 3,160 3,540 3,970 4,430 4,710

Total Revenue 48,600 53,850 66,223 69,248 71,878

Operating Expenses 48,570 48,310 50,740 52,390 54,260

Depreciation 3,810 5,020 5,540 5,860 6,160

Interest Charges 3,030 3,840 4,140 4,430 4,670

Total Expenses 55,410 57,170 60,420 62,680 65,090

Profit Before Tax (6,810) (3,320) 5,803 6,568 6,788

Tax - - - - -

Profit After Tax (6,810) (3,320) 5,803 6,568 6,788

Balance Sheet

Gross Fixed Assets 59,310 84,720 97,940 107,580 116,220

Accumulated Depreciation 20,110 25,130 30,670 36,530 42,690

Net Fixed Assets 39,200 59,590 67,270 71,050 73,530

WIP 21,220 9,220 5,380 4,280 4,030

Current Assets 29,520 31,300 37,793 42,771 47,799

Total Assets 89,940 100,110 110,443 118,101 125,359

Equity* (26,930) (28,220) (20,397) (11,819) (3,011)

Long term Liabilities 46,870 44,430 42,170 39,170 35,020

Current Liabilities 70,000 83,900 88,670 90,750 93,350

Total Equity & Liabilities 89,940 100,110 110,443 118,101 125,359

Cash Flow Statement

Net P&L for the year (6,810) (3,320) 5,803 6,568 6,788

Depreciation 3,810 5,020 5,540 5,860 6,160

Interest and finance charges 3,030 3,840 4,140 4,430 4,670

Change in Working capital 11,420 14,190 4,950 2,170 2,570

Cash flow from operating activities 11,450 19,730 20,433 19,028 20,188

GFA (16,640) (25,410) (13,220) (9,640) (8,640)

WIP (3,500) 12,000 3,840 1,100 250

Investment (970) (2,070) (120) (800) (1,160)

Cash flow from investing activities (21,110) (15,480) (9,500) (9,340) (9,550)

Equity 1,790 1,790 1,780 1,770 1,770

Other Reserves / Consumer

Contribution 3,220 240 240 240 250

Loan 7,680 (2,440) (2,260) (3,000) (4,150)

Interest and finance charges (3,030) (3,840) (4,140) (4,430) (4,670)

Cash flow from financing activities 9,660 (4,250) (4,380) (5,420) (6,800)

Cash Generated - - 6,553 4,268 3,838

Annex 3 23

Particulars FY13 FY14 FY15 FY16 FY17

Ratios -17% -6% 9% 9% 9%

Return on NFA -17% -6% 9% 9% 9%

D/E* (1.74) (1.57) (2.07) (3.31) (11.63)

Current Ratio 0.42 0.37 0.43 0.47 0.51

D/E: Debt / Equity; Current Ratio = Current Assets / Current Liabilities; P&L: Profit & Loss; WIP: Work-in-progress

* Equity includes accumulated profits/losses

Source: DISCOM-E Business Plan, ADB Analysis

24 Annex 4

Table A4: Summary DISCOM-W Financial Projections (Rs Million)

Particulars FY13 FY14 FY15 FY16 FY17

Sales (Mus) 14,680 18,771 20,731 22,572 24,528

%change 24% 28% 10% 9% 9%

Average Revenue (Rs/kWh) 48.58 57.56 76.71 73.55 70.95 %change 11% 18% 33% -4% -4%

P&L

Revenue from Sale of Power 71,315 108,041 159,014 166,022 174,014 Other Income 3,629 3,629 3,629 3,629 3,629 Total Revenue 74,944 111,669 162,642 169,651 177,643

Operating Expenses 89,966 110,634 121,343 129,167 136,777 Depreciation 1,355 1,748 2,234 2,639 2,930 Interest Charges 3,541 6,244 14,903 13,063 10,859 Total Expenses 94,861 118,626 138,480 144,869 150,566 Profit Before Tax (19,917) (6,957) 24,162 24,781 27,077 Tax - - 7,557 7,349 7,829 Profit After Tax (19,917) (6,957) 16,605 17,432 19,248

Balance Sheet

Gross Fixed Assets 40,455 53,795 67,212 76,090 83,217 Accumulated Depreciation 18,575 20,323 22,557 25,196 28,125 Net Fixed Assets 21,880 33,472 44,655 50,894 55,092 WIP 11,532 13,623 9,380 8,298 8,967 Current Assets 41,511 53,354 74,303 63,807 60,460 Other Non-current Assets 3,287 5,082 7,891 12,288 19,171 Total Assets 78,210 105,531 136,229 135,288 143,690

Equity* (35,984) (37,963) (18,038) 2,315 24,281 Long term Liabilities 67,621 83,735 84,245 84,068 84,029 Other Non-current liabilities and

provisions 7,235 6,935 6,635 6,335 5,995

Current Liabilities 39,337 52,822 63,386 42,569 29,385 Total Equity & Liabilities 78,210 105,530 136,228 135,287 143,690

Cash Flow Statement

Net P&L for the year (19,917) (6,957) 16,605 17,432 19,248 Depreciation 1,355 1,748 2,234 2,639 2,930 Provisions for Bad & doubtful debt 3,013 4,098 5,345 4,864 4,347 Interest and finance charges 3,541 6,244 14,903 13,063 10,859 Change in Working capital (9,304) (13,529) (10,831) 7,486 853 Cash flow from operating activities (21,313) (8,396) 28,256 45,484 38,237

GFA (8,323) (13,341) (13,416) (8,878) (7,127) WIP (3,965) (2,091) 4,243 1,082 (669) Investment (1,136) (1,795) (2,809) (4,397) (6,882) Cash flow from investing activities (13,425) (17,226) (11,983) (12,194) (14,679)

Equity 897 2,894 1,687 1,364 1,443 Other Reserves / Consumer

Contribution 1,635 2,083 1,632 1,557 1,275

Loan 10,739 16,115 510 (177) (39)

Annex 4 25

Particulars FY13 FY14 FY15 FY16 FY17

Other Long term liabilities and

provisions (1,591) (300) (300) (300) (340)

Interest and finance charges (3,541) (6,244) (14,903) (13,063) (10,859) Short term loans 24,830 10,573 (3,898) (23,172) (15,538) Cash flow from financing activities 32,970 25,121 (15,272) (33,792) (24,059)

Cash Generated (1,768) (501) 1,002 (501) (501)

Ratios

Return on NFA -91% -21% 37% 34% 35%

D/E* (1.88) (2.21) (4.67) 36.31 3.46 Current Ratio 1.06 1.01 1.17 1.50 2.06

D/E: Debt / Equity; Current Ratio = Current Assets / Current Liabilities; P&L: Profit & Loss; WIP: Work-in-progress

* Equity includes accumulated profits/losses

Source: DISCOM-W Business Plan, ADB Analysis

26 Annex 5

Table A5: FMAQ - MP TRANSCO

Topic Response Remarks

1. Implementing Agency

1.1 What is the entity’s legal status / registration? Company

1.2 Has the entity implemented an externally-

financed project in the past

Yes

1.3 What are the statutory reporting requirements

for the entity?

As per Company Act

1.5 Is the organizational structure appropriate for

the needs of the project?

Yes

2. Funds Flow Arrangements

2.1 Describe (proposed) project funds flow

arrangements, including a chart and

explanation of the flow of funds from ADB,

government and other financiers.

2.2 Are the (proposed) arrangements to transfer

the proceeds of the loan (from the government

/ Finance Ministry) to the entity satisfactory?

Yes

2.3 What have been the major problems in the

past in receipt of funds by the entity?

No

2.4 In which bank will the Imprest Account be

opened?

UBI / ICICI

2.7 Does the entity have/need a capacity to

manage foreign exchange risks? How is the

foreign exchange risk mitigated?

Managed at GoMP level

2.8 How will be the counterpart funds accessed? Through GoMP for SGIA / re-

imbursement;

Direct funds flow from ADB for

EPC in case of LC / direct

payment mode

3. Staffing

3.1 What is the (proposed) organizational structure

of the F&A department? Attach an organization

chart.

3.3 Is the project finance and accounting function

staffed adequately?

Yes; if required more staff will

be deployed

3.4 Is the finance and accounts staff adequately

qualified and experienced?

Yes

3.7 Indicate key positions vacant and the

estimated date of appointment.

Yes, however being promotional

post it cannot be filled

immediately and from outside. If

required, same may be

temporarily filled with contract

appointments

3.12 What is the training policy for the finance and

accounting staff?

No written manual; however

most of the recruitment are

being done with qualification of

CA / ICWA

Annex 5 27

Topic Response Remarks

4. Accounting Policies and Procedures

4.3 Is the chart of accounts adequate to properly

account for and report on project activities and

disbursement categories?

Yes

4.4 Are cost allocations to the various funding

sources made accurately and in accordance

with established agreements?

Yes

4.9 Are bank reconciliations prepared by someone

other than those who make or approve

payments?

Yes

Budgeting System

4.12 Are actual expenditures compared to the

budget with reasonable frequency, and

explanations required for significant variations

from the budget?

Yes, on quarterly basis;

reviewed by Management

4.14 Who is responsible for preparation and

approval of budgets?

CE P&D (Planning & Design) –

Capital budget

Policies And Procedures

4.20 What is the basis of accounting (e.g., cash,

accrual)?

Accrual

4.21 What accounting standards are followed? ICAI AS

4.23 Is the accounting policy and procedure manual

updated for the project activities?

N/A

4.25 Are there written policies and procedures

covering all routine financial management and

related administrative activities?

5. Internal Audit

5.1 Is there an internal audit department in the

entity?

Yes

5.2 What are the qualifications and experience of

audit department staff?

Mainly outsourced to CA firm

5.5 Are actions taken on the internal audit

findings?

Yes

6. External Audit

6.1 Is the entity financial statement audited

regularly by an independent auditor? Who is

the auditor?

Statutory auditor appointed by

CAG, supplementary audit of

the same by the CAG

6.2 Are there any delays in audit of the entity? 5-6 months (no pending)

6.3 Is the audit of the entity conducted according to

the International Standards on Auditing?

Yes as per AS prescribed by

ICAI

6.4 Were there any major accountability issues

brought out in the audit report of the past three

years?

No

6.6 Are there any recommendations made by the

auditors in prior audit reports or management

letters that have not yet been implemented?

Not anything which is material to

Company’s operations and

business processes

28 Annex 5

Topic Response Remarks

7. Reporting and Monitoring

7.1 Are financial statements prepared for the

entity? In accordance with which accounting

standards?

Yes, as per Indian Accounting

Standards

7.5 Does the reporting system have the capacity to

link the financial information with the project’s

physical progress?

The company is in advanced

stages of implementation of

ERP (tender floated for

appointing consultant)

7.8 Do the financial reports compare actual

expenditures with budgeted and programmed

allocations?

Yes

7.9 Are financial reports prepared directly by the

automated accounting system or are they

prepared by spreadsheets or some other

means?

Partially; Company is using

legacy batch processing FA

system

8. Information Systems

8.1 Is the financial management system

computerized?

8.2 Is the billing system integrated with

accounting system (including payments, etc);

Also is there a MIS which gets generated from

the system and used for Management review?

Manual basis; The company is

in advanced stages of

implementation of ERP (tender

floated for appointing

consultant)

8.3 Can the system produce the necessary project

financial reports?

No; ERP awaited

8.4 Is the staff adequately trained to maintain the

system?

N/A

Annex 6 29

Table Annexure-6: FMAQ – DISCOM-C

Topic Response Remarks

1. Implementing Agency

1.1 What is the entity’s legal status / registration? Company

1.2 Has the entity implemented an externally-

financed project in the past

Yes

1.3 What are the statutory reporting requirements

for the entity?

As per Company’s Act

1.5 Is the organizational structure appropriate for

the needs of the project?

Yes

2. Funds Flow Arrangements

2.1 Describe (proposed) project funds flow

arrangements, including a chart and

explanation of the flow of funds from ADB,

government and other financiers.

2.2 Are the (proposed) arrangements to transfer

the proceeds of the loan (from the government

/ Finance Ministry) to the entity satisfactory?

Yes

2.3 What have been the major problems in the

past in receipt of funds by the entity?

No

2.4 In which bank will the Imprest Account be

opened?

Second Generation Imprest

Account / State Bank of India

2.7 Does the entity have/need a capacity to

manage foreign exchange risks? How is the

foreign exchange risk mitigated?

The State Government

manages the foreign exchange

risks; on-lending to DISCOMs at

Rs

2.8 How will be the counterpart funds accessed? Loan

3. Staffing

3.1 What is the (proposed) organizational structure

of the F&A department? Attach an organization

chart.

3.3 Is the project finance and accounting function

staffed adequately?

Yes

3.4 Is the finance and accounts staff adequately

qualified and experienced?

Yes

3.7 Indicate key positions vacant and the

estimated date of appointment.

NA

3.12 What is the training policy for the finance and

accounting staff?

Need based training

4. Accounting Policies and Procedures

4.3 Is the chart of accounts adequate to properly

account for and report on project activities and

disbursement categories?

Yes

4.4 Are cost allocations to the various funding

sources made accurately and in accordance

with established agreements?

Yes

30 Annex 6

Topic Response Remarks

4.9 Are bank reconciliations prepared by someone

other than those who make or approve

payments?

Audited by Statutory Auditor

Budgeting System

4.12 Are actual expenditures compared to the

budget with reasonable frequency, and

explanations required for significant variations

from the budget?

Estimation and their comparison

with actuals are done

4.14 Who is responsible for preparation and

approval of budgets?

CGM (RP) & Dir (Fin) – Prep

Board / MD – Approval

Policies And Procedures

4.20 What is the basis of accounting (e.g., cash,

accrual)?

Accrual

4.21 What accounting standards are followed? Yes

4.23 Is the accounting policy and procedure manual

updated for the project activities?

Yes

4.25 Are there written policies and procedures

covering all routine financial management and

related administrative activities?

Yes

5. Internal Audit

5.1 Is there an internal audit department in the

entity?

Yes

5.2 What are the qualifications and experience of

audit department staff?

Chartered Accountant

5.5 Are actions taken on the internal audit

findings?

Yes

6. External Audit

6.1 Is the entity financial statement audited

regularly by an independent auditor? Who is

the auditor?

Yes. M/s Tasky Associates for

FY12 and FY13

6.2 Are there any delays in audit of the entity? No

6.3 Is the audit of the entity conducted according to

the International Standards on Auditing?

India Accounting Standard is

followed

6.4 Were there any major accountability issues

brought out in the audit report of the past three

years?

All material issues are disclosed

6.6 Are there any recommendations made by the

auditors in prior audit reports or management

letters that have not yet been implemented?

No

6.7 Is the project subject to any kind of audit from

an independent government entity

Yes, CAG

7. Reporting and Monitoring

7.1 Are financial statements prepared for the

entity? In accordance with which accounting

standards?

Yes

Annex 6 31

Topic Response Remarks

7.5 Does the reporting system have the capacity to

link the financial information with the project’s

physical progress?

Yes; ERP is awaited

7.8 Do the financial reports compare actual

expenditures with budgeted and programmed

allocations?

Estimations are compared with

originals

7.9 Are financial reports prepared directly by the

automated accounting system or are they

prepared by spreadsheets or some other

means?

Sybase based Accounting

System

8. Information Systems

8.1 Is the financial management system

computerized?

Partially

8.2 Is the billing system integrated with

accounting system (including payments, etc);

Also is there a MIS which gets generated from

the system and used for Management review?

Partially

8.3 Can the system produce the necessary project

financial reports?

No; ERP awaited

8.4 Is the staff adequately trained to maintain the

system?

Yes

32 Annex 7

Table A7: FMAQ – DISCOM-E

Topic Response Remarks

1. Implementing Agency

1.1 What is the entity’s legal status / registration? Company

1.2 Has the entity implemented an externally-

financed project in the past

Yes

1.3 What are the statutory reporting requirements

for the entity?

As per Company’s Act

1.5 Is the organizational structure appropriate for

the needs of the project?

Yes

2. Funds Flow Arrangements

2.1 Describe (proposed) project funds flow

arrangements, including a chart and

explanation of the flow of funds from ADB,

government and other financiers.

2.2 Are the (proposed) arrangements to transfer

the proceeds of the loan (from the government

/ Finance Ministry) to the entity satisfactory?

Yes

2.3 What have been the major problems in the

past in receipt of funds by the entity?

No

2.4 In which bank will the Imprest Account be

opened?

2.7 Does the entity have/need a capacity to

manage foreign exchange risks? How is the

foreign exchange risk mitigated?

No need to manage the foreign

exchange risks

2.8 How will be the counterpart funds accessed? Loan

3. Staffing

3.1 What is the (proposed) organizational structure

of the F&A department? Attach an organization

chart.

3.3 Is the project finance and accounting function

staffed adequately?

Yes

3.4 Is the finance and accounts staff adequately

qualified and experienced?

Yes

3.7 Indicate key positions vacant and the

estimated date of appointment.

NA

3.12 What is the training policy for the finance and

accounting staff?

Need based training

4. Accounting Policies and Procedures

4.3 Is the chart of accounts adequate to properly

account for and report on project activities and

disbursement categories?

Yes

4.4 Are cost allocations to the various funding

sources made accurately and in accordance

with established agreements?

Yes

Annex 7 33

Topic Response Remarks

4.9 Are bank reconciliations prepared by someone

other than those who make or approve

payments?

Budgeting System

4.12 Are actual expenditures compared to the

budget with reasonable frequency, and

explanations required for significant variations

from the budget?

Estimation and their comparison

with actuals are done

4.14 Who is responsible for preparation and

approval of budgets?

Director Finance

Policies And Procedures

4.20 What is the basis of accounting (e.g., cash,

accrual)?

Accrual

4.21 What accounting standards are followed? Yes

4.23 Is the accounting policy and procedure manual

updated for the project activities?

Yes

4.25 Are there written policies and procedures

covering all routine financial management and

related administrative activities?

Yes

5. Internal Audit

5.1 Is there an internal audit department in the

entity?

Yes

5.2 What are the qualifications and experience of

audit department staff?

Chartered Accountant

5.5 Are actions taken on the internal audit

findings?

Yes

6. External Audit

6.1 Is the entity financial statement audited

regularly by an independent auditor? Who is

the auditor?

Yes. Changes every 2 years

6.2 Are there any delays in audit of the entity? No

6.3 Is the audit of the entity conducted according to

the International Standards on Auditing?

India Accounting Standard is

followed

6.4 Were there any major accountability issues

brought out in the audit report of the past three

years?

Internal Control function to be

strengthened

6.6 Are there any recommendations made by the

auditors in prior audit reports or management

letters that have not yet been implemented?

No

6.7 Is the project subject to any kind of audit from

an independent government entity

Yes, CAG

7. Reporting and Monitoring

7.1 Are financial statements prepared for the

entity? In accordance with which accounting

standards?

Yes

34 Annex 7

Topic Response Remarks

7.5 Does the reporting system have the capacity to

link the financial information with the project’s

physical progress?

Yes; manual interventions are

required

7.8 Do the financial reports compare actual

expenditures with budgeted and programmed

allocations?

Estimations are compared with

originals

7.9 Are financial reports prepared directly by the

automated accounting system or are they

prepared by spreadsheets or some other

means?

Yes, Accounting System

8. Information Systems

8.1 Is the financial management system

computerized?

Yes a Sybase based system

8.2 Is the billing system integrated with

accounting system (including payments, etc);

Also is there a MIS which gets generated from

the system and used for Management review?

Partially

8.3 Can the system produce the necessary project

financial reports?

No; Tenders prepared for

implementation of ERP

8.4 Is the staff adequately trained to maintain the

system?

NA

Annex 8 35

Table A8: FMAQ – DISCOM-W

Topic Response Remarks

1. Implementing Agency

1.1 What is the entity’s legal status / registration? Company

1.2 Has the entity implemented an externally-

financed project in the past

Yes

1.3 What are the statutory reporting requirements

for the entity?

As per Company’s Act

1.5 Is the organizational structure appropriate for

the needs of the project?

Yes

2. Funds Flow Arrangements

2.1 Describe (proposed) project funds flow

arrangements, including a chart and

explanation of the flow of funds from ADB,

government and other financiers.

2.2 Are the (proposed) arrangements to transfer

the proceeds of the loan (from the government

/ Finance Ministry) to the entity satisfactory?

Yes

2.3 What have been the major problems in the

past in receipt of funds by the entity?

No

2.4 In which bank will the Imprest Account be

opened?

State Bank of India

2.7 Does the entity have/need a capacity to

manage foreign exchange risks? How is the

foreign exchange risk mitigated?

No need to manage foreign

exchange risks for ADB loan

2.8 How will be the counterpart funds accessed? Loan

3. Staffing

3.1 What is the (proposed) organizational structure

of the F&A department? Attach an organization

chart.

3.3 Is the project finance and accounting function

staffed adequately?

Yes

3.4 Is the finance and accounts staff adequately

qualified and experienced?

Yes

3.7 Indicate key positions vacant and the

estimated date of appointment.

NA

3.12 What is the training policy for the finance and

accounting staff?

Need based training

4. Accounting Policies and Procedures

4.3 Is the chart of accounts adequate to properly

account for and report on project activities and

disbursement categories?

Yes

4.4 Are cost allocations to the various funding

sources made accurately and in accordance

with established agreements?

Yes

36 Annex 8

Topic Response Remarks

4.9 Are bank reconciliations prepared by someone

other than those who make or approve

payments?

Audited by Statutory Auditor

Budgeting System

4.12 Are actual expenditures compared to the

budget with reasonable frequency, and

explanations required for significant variations

from the budget?

4.14 Who is responsible for preparation and

approval of budgets?

Director Finance and Managing

Director

Policies And Procedures

4.20 What is the basis of accounting (e.g., cash,

accrual)?

Accrual

4.21 What accounting standards are followed? Yes

4.23 Is the accounting policy and procedure manual

updated for the project activities?

Yes