financial ratios and stock return: a panel data analysis ratios and stock return ; a... ·...

TRANSCRIPT

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

Liaw Huan Huan

Bachelor of Finance (Honours)

2012

Pusat Kbidmat Makumat Akademik UNNERSm MALAYSIA SARAWAK

PKHIDMAT MAKLUMAT AKADEMIK

1IIIIIIIIIfiim 111111111 1000245035

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

LIA W HUAN HUAN

This project is submitted in partial fulfillment of the reqt1uements for the degree of Bachelor of Finance with Honours

Faculty of Economics and Business UNIVERSITI MALAYSIA SARA W AK

2012

Statement of Originality

The work described in this Final Year Project entitled FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

is to the best of the authors knowledge that of the author except where due reference is made

10 1UIE 2012

(Date submitted) (Students signature) Liaw Huan Huan 23847

ASBTRACT

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

By

Liaw Huan Ruan

The main objective of this study is to examine the role of the financial ratios such as

dividend yield (DIY) book-to-market (BM) ratio price earnings (PIE) ratio size payout ratio

and leverage to predict the stock return for the 5 different sectors in Malaysia from 2006 to 20 I O

Using panel data analysis the result shows that the financial ratios such as size were the most

powerful in predicting the stock return in all sectors Dividend yields also show the high

predictability in stock return in all sectors except banking sector Besides that the book-to-market

ratios showed the negative significant relati()nship between stock return in servicing banking

food producer and construction sectors However the financial ratios such as leverage payout

and price earnings ratio were indicated less predictive power to predict the stock return

Therefore the results imply that investors can rely on the financial ratios such as dividend yields

and size information to gain abnormal returns in the market The results further ind icate that the

Malaysian stock market is not informational efficient

Key Words Hausman Test financial ratios ~tock return panel data analysis

ABSTRAK

NISBAH KEWANGAN DAN PULANGAN SAHAM ANALISIS PANEL DATA

Oleh

Liaw Huan Huan

Objektif utama bagi kajian ini adalah untuk mengkaji peranan nisbah kewangan seperti

hasil dividen (DIY) nisbah buku (BM) nisbah harga (PIE) saiz nisbah pembayaran dan

leverage untuk meramalkan pulangan saham bagi 5 sektor yang berbeza di Malaysia dari tahun

2006 hingga 20 I O Dengan menggunakan analisis data panel hasH kajian menunjukkan bahawa

nisbah kewangan seperti saiz adalah paling berkesan untuk membuat ramalan terhadap pulangan

saham dalam semua sektor Hasil dividen juga menunjukkan kebolehramalan pada pulangan

saham dalam semua sektor kecuali sektor pmiddoterbankan Selain itu nisbah buku menunjukkan

hubungan signifikan yang negatif dengan pulangan saham dalam sektor perkhidmatan

perbankan pengeluaran makanan dan pembinaan Walaubagaimanapun nisbah kewangan yang

seperti leverage nisbah pembayaran dan nisbah harga didapati tidak signifikan mempengaruhi

pulangan saham Secara keseluruhan kajian ini menunjukkan para pelabur dapat menggunakan

maklumat saiz and hasil dividen untuk memperoleh pulangan abnormal di pasaran Justeru hasil

kajian ini juga menur~jukkan pasaran saham di Malaysi~ adalah kurang cekap

Kata Kunci Hausman test nisbah kewangan saham pulangan panel data analisis

ACKNOWLEDGEMENT

Apart from the efforts of me the success of my thesis highly depends on the

encouragement and support from many of others I would like to take this opportunity to express

my greatest appreciation to the people who have been instrumental in the successful completion

of my Final Year Project

I would like to take this opportunity to deliver acknowledgement and thankful toward the

people who had assisted guided advised and encouraged me in the preparation of my final year

project especially to my respected project supervisor Encik Bakri Abdul Karim who had always

instructed me patiently I m felt motivated and encouraged every time I attended his meeting

With his valuable opinion expert guidance and support this project able to completed in well

timed

Hereby I would like to express my gratitude to my beloved family which is always give

support and encouragement to me from the initial to the final level of my project Moreover my

family members also help me in term of moneys aspect The high budget in completed this

research thus the monetary support from family members are very important to me

Furthermore I also would like to acknowledge to my friends who not forget to support me and guide me in doing this project Lastly I offer my regards and blessings to all of those who

supported me in any respect during the completion of the project

I

Pusat Khidmat MakJumat Akademik VNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

LIST OF TABLES IX

LIST OF FIGURES X

CHAPTER ONE INTRODUCTION

10 Introduction

11 Background of the Research

12 The Malaysian Economic 4

13 The Stock Development in Malaysia 9

14 Problem Statement 16

15 Objective 19

bmiddotmiddot bull151 General 0 ~ectlve 19

152 Specific Objectives 19

16 Significant of Study 20

17 Scope of Study 21

CHAPTER TWO LITERATURE REVIEW AND LITERATURE REVIEW

20 Introduction of Theoretical Framework 22

21 Market Efficient Hypothesis 23

22 Literature Review 24

221 Capital Asset Pricing Model 24

222 Asset Pricing Theory 27

223 Financial Ratios 29

VI

2231 Dividend Yields 29

~

223 2 Book-to-Market Ratio 31

2233 Price Earnings Ratio 32

2234 Size 33

2235 Payout Ratio 34

2236 Leverage 34

CHAPTER THREE METHODOLOGY

30 Introduction 36

31 Conceptual Framework 37

32 Research Design 38

321 Salnple 38

32 2 Model Specification~ 39

323 Data Collection 40

324 Data Analysis 40

33 Methodology 41

331 Panel Data 41

332 Dependent and Independent Variables 42

332 1 Stock Return 43

3322 Dividend yields 43

3323 Book-to-Market Ratio 44

3324 Price Earnings Ratio 44

3325 Size 45

3326 Payout Ratio 45

vii

~-

3327 Leverage 45

J

34 Hausman Test 46

35 Fixed Effect Model 48

36 Random Effect Model 49

37 Diagnostic Checking 50

CHAPTER FOUR EMPIRICAL FINDINGS AND DISCUSSIONS

40 Introduction 52

41 Statistical Descriptive 52

42 Discussion on Hausman Test Analysis 54

43 Discussion on Fixed Effect Model Analysis 56

44 Discussion on Random Effect Model Analysis 58

45 Summary of Discussion 59

CHAPTER FIVE DISCUSSION OF FINDINGS

50 Introduction 65

51 Sulnmary 65

52 Implication of Study 68

53 Recomlnendation 69

54 Limitation 70

REFERENCES 71

Vill

I

-

LIST OF TABLES

Table 1 Dependent and Independent Variables 39

Table 2 Summary Statistics for Data Used 53

Table 3 Hausman Test 55

Table 4 Fixed Effect Model 56

Table 5 Random Effect Model 58

p

IX

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

LIST OF FIGURES

Malaysia Gross Domestic Product by Sector on 2010 5

Gross Domestic Product and Annual Growth Rate from Period

2008 to 2010 6

Malaysia - Annual GOP Growth Rates by Sectors 2008 to 2010 7

Comparison the GOP in Malaysia by Sectors between 2009 and

2010 8

Number of Listed Companies in Malaysia from Period 1990 to

2010 11

Market Capitalizations in Malaysia from Period 1990 to 2010 12

Price Earnings Ratio and Gross Dividend Yield in Bursa

Malaysia from Period r990 to 2010 13

Kuala Lumpur Composite Index from Period 1990 to 2010 14

Value of Share Trading from Period 1990 to 2010 15

Conceptual Framework 45

The Summarize Findings of Financial Ratios Based on Sectors 64

x

CHAPTER ONE

INTRODUCTION

10 Introduction

This research is study on the relationship between the financial ratios and stock

return This chapter discusses the background of the research Besides that this study

also covers problem statement purpose of research significant of research and scope of

research

11 Background of Study

Nearly five decades ago study on the pred iction of stock return has been one of

the most challenging topics in financial economics A number of theoretical models

have been developed to explain stock return such as Capital Asset Pricing Model

(CAPM) Arsitrage Pricing Theory (APT) Fama and French three factor model and

others financial ratios

In the early stages a number of studies on CAPM were considerably written in

the academic research CAPM consider as one of the most important modern capital

theory which originally proposed by Sharpe (1964) The parallel) work was also

~

performed by Lintner (1965) and Black (1972) CAPM had been continuously used in

practical portfolio management and the capital equilibrium model for the academic

research guiding purpose (Koo amp Olson 2007) Besides that CAPM were widely used

to measures the powerful explanation on the expected risk and return theoretical as well

as empirical studies (Michailidis Tsopoglou Papanastasiou amp Mariola 2006 Nguyen

amp Puri 2010) However Michailidis et at (2006) found that the basic theory hypothesis

of higher risk was associated with higher return which is not supportive The early test

CAPM worked efficiently as a pred ictor of the stock return but many of studies found

anomalies in CAPM (Padney 2001)

More to the point in the early 1976s Arbitrage Pricing Theory (APT) proposed

by Stephen Ross as an alternative to replace CAPM to explain stock return The main

idea of APT was the price of security driven by number of factors There were several

dependent macroeconomics factors influenced on the asset return such as inflation rate

GOP exchange rate change in price indexes and etc (Somoye Akintoye amp Oseni

2009) The asset return were relying on the influences of macroeconomic factors and

others incident that were distinctive to the firm but the expected risk premium only

affected by the macroeconomic factors (Hohling 2009) In the efficeint market

hypothesis the informat ion change in the macroeconomic variables fully reflect the

current stock prices therefore this caused the investors to get the anomalies return in

the future stock market movment (Balvers Cosimano amp Mcdonald 1990)

2

Additionally Fama and French (1992) co written came out a new model which

was known as Fama-French three model factor Fama-French three model factor

measured by the combination of the market beta such as size Leverage book-to market

equity and price earnings ratio with the cross sectional of expected stock return (Fama

amp French 1992) The Fama-French three model factor was a simple variation in stock

return compare with CAPM due to the additional of size and book-to-market-equity in

the model (Ajili 200 I) CAPM was only using one variable (beta) to describe the stock

return but reversely Fama-French three model factor was using three variables such as

small caps book-to-market ratio and the additional of size (Fama amp French 2008)

However CAPM and Fama-French three model factor had performed a good job in

explaining the cross section of stock return (Ajlis 200 I)

As Fama (1970) recommended that an efficient capital market is all the security

prices adjust rapidly new information and the prices of an asset reflect all available

information However the stock prices wandered randomly over the time period and the

stock prices change could use predictors (Padney 200) An efficient market as a

dominate sources of allocation in order to provide an accurate signal for the firm to

make investment decision and investor can choose among securities that represent

ownership of firms activities (Brown amp KReiIlY 2009) Besides that if the abnormal

rate of return on the stock market which were lower than the normal rate of return it

means that the capital market was efficient and vice versa

3

12 The Malaysian Economic

Since Malaysia became independent on 1957 Malaysias economic had grown

rapidly Malaysia is a developing country which consists of thirteen states and three

federal territories Malaysia considers as a small country where totals landmass of

329847 square kilometres (127315 sq mi) which separated by the South China

Sea into two regions Peninsular Malaysia and Malaysia Borneo In the year of201 0 the

population exceeded 283 million (United States State Department 20 I 0)

According to the United States State Department (2010) the Malaysia annual

real gross domestic product (GOP) growth rate grew by the average of 446 per year

from period 2006 to 20FO The total Nominal GOP on 2010 is $2553 billion and the

total nominal per capital Income (GNI) is $8126 Malaysia is a country which

prosperity In the mineral natural resources and agricultural product The natural

resources are such as petroleum liquefied natural gas (LNG) tin minerals and others

where the agricultural products are such as palm oil rubber timber cocoa rice tropical

fruit fish coconut and others

The Malaysia economy is expected to grow healthy and strong by switching

from the agricultural and commodities sectors to the manufacture and export sectors

Based on the United States State Department (20 I 0) stated that the Malaysia traded on

merchandise export is 2103 billion where the traded includes electronic products

machinery liquid natural gas petroleum products and telecom equipment The recent

4

Pu at Khldm rMIIJdum tAk UNlVERsm MALAYSIA

impressive perfonnance shows the export as a main contribution in services sector to

lead the economic growth in Malaysia (Economy Watch 2010)

F 1 MImiddot G oss Do f Product b S ctor on 2010 -

change2010 ChangeSector (Q4 2010(RM billion) (20102009)Q42009)

Source Ministry of International Trade and Industry 2011

Figure above shows the Malaysias gross domestic product on 2010 was mostly

contributed by services sector which shows RM3206 billion compare to the

construction sectors which only shows RM 182 billion Nowadays Malaysia is a

middle-income country which focuses most on the services and manufacturing sector

Moreover Malaysia become one of the largest exporters of world in semiconductor

devices electric goods and as well as infonnation and communication technology (lCT)

products

5

Figure 2 Gross Domestic Product and Annual Growth Rate from Period 2008 to 2010

40

Source Ministry ofIntemational Trade and Industry 2011

Figure above represents the annual gross domestic product growth in Malaysia

from period 2008 to 2010 taken as whole was moving average but the abnonnal

circumstance happened during 2009 quarter 1 The annual gross domestic product

growth in 2008 average was RM13255 million The average amount drops to

RM13030 million in 2009 However the amount annual gross domestic product growth

in 2010 recovers and increases to RM13390 million

6

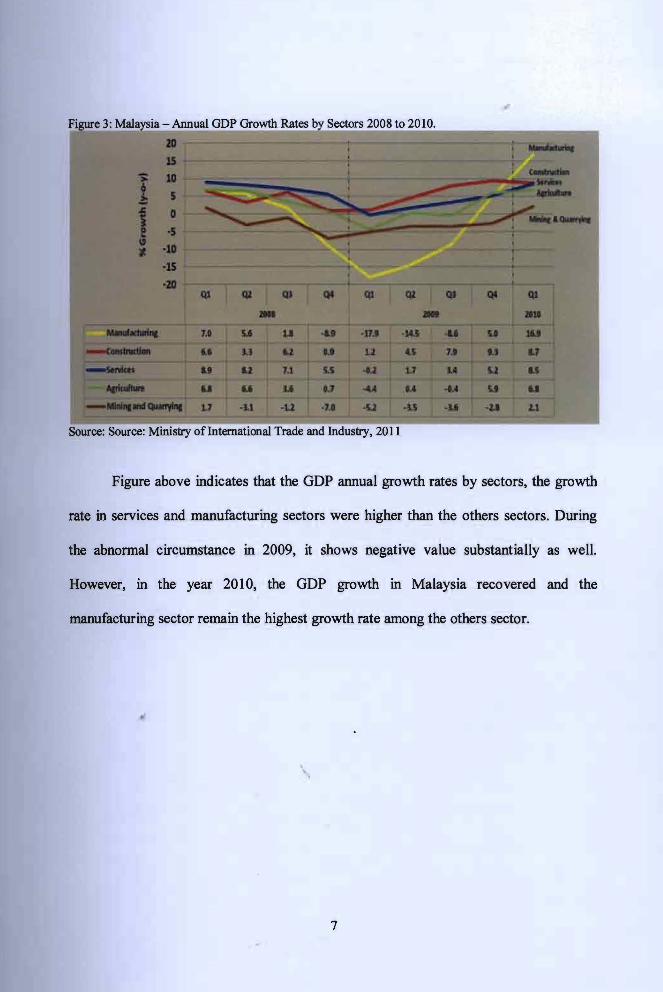

3 Malaysia - Annual GDP Growth Rates by Sectors 2008 to 2010

Source Source Ministry of Intemational Trade and Industry 2011

Figure above indicates that the GDP annual growth rates by sectors the growth

rate in services and manufacturing sectors were higher than the others sectors During

the abnormal circumstance in 2009 it shows negative value substantially as well

However in the year 2010 the GDP growth in Malaysia recovered and the

manufacturing sector remain the highest growth rate among the others sector

7

Figure 4 Comparison the GDP in Malaysia by Sectors between 2009 and 2010

I(I~ IM111AI

Source Ministry of International Trade and Industry 2011

Figure above is the comparison between the GDP by sector in Malaysia for 2009

and 2010 and it show that the total (1)P increase from RM5211billion in 2009 and

became RM5584 billion in 2010 The sectors such as services and manufacturing

sectors indicated the growth in the GDP However the sectors like mining amp quarrying

agricultural and construction indicated the percentages of decrease in the GDP growth

rate

8

13 The Stock Development in Malaysia

In 1960 the Malaysia Stock Exchange was first setting up and known as

Malayan Stock Exchange and in 1965 it was changed to Stock Exchange of Malaysia

and Singapore due to the secession of Singapore from Malaysia In 1973 the currency

interchange ability between Malaysia and Singapore had been ceased and the Stock

Exchange of Malaysia and Singapore were divided into Kuala Lumpur Stock Exchange

Bcrhad (KLSEB) and Stock Exchange of Singapore (SES) (Bursa Malaysia 20 L1)

Aller demutualize exercise on 14th April 2004 Kuala Lumpur Stock Exchange (KLSE)

was renamed to Bursa Malaysia On 18 th March 2005 Bursa Malaysia was listed on the

Main Board of Bursa Malaysia Securities Berhad (Chong amp Puah 2009) However

Bursa Malaysia currently consists of 988 companies which 637 companies on Main

Board 227 companies on Second Board and 124 companies on MESDAQ (Lee amp Lee

2008)

Moreover Capital market is a place for investor and institute trade financial

securities in order to raise funds Thus the market where securities traded is known as

Sccurities Market it comprised of both the primary and secondary markets The primary

market is known as new issue market where it deals with new issue securities in

Malaysia whereas the secondary market focuses on the trading of existing securities and

it often termed as stock exchange market According to Lee and Lee (2008) generally

the investor desire to earn a positive return in their investment The return of the shares

9

I

trade for the short term investor is capital gain and the dividend is for the long term

in cstor

However the stock market in Malaysia should always be in the range o[

effic k ncy This is because the efficient capital market assumes that an initial premise of

an fftcient market request that a large number of profit maximizing participant analyze

and va lue securities Besides that the new information regarding the securities comes to

the market in a random fashion However the buyer and seller decision of all those

profit maximizing investor who adjust security prices rapidly reflect the effect of new

intormation (Brown amp Reilly 2009)

In Malaysia therc are no practices on the tax loss-selling hypothesis therefore

there arc no capital gain taxes for the residents or non-residents The stock return

seasonality in Malaysia indicates that stock market in Malaysia is not efficient in

reflecting the information I-Ience investor can spend time in getting higher returns

Generally the efficient market hypothesis (EMH) stated that the stock price and return

are not able to be predicted by using the past price information However the

seasonality effect presence and this implies the efficiency market and negates the weak

form oCthe efficiency market hypothesis (Padney 2004)

The Malaysian capital market is focus on the weak form efficiency market and

risk of return relationship The weak form efficiency markets where the prices reflect all

the historical market trading information Most of the tests show this information unable

10

to generate abnormal return (Nasir Mohamad amp Hamid 1998) Based on Tan (2006)

Ma laysia stock index futures market does not subscribe to random walk hypothesis but

stock return are predictable

Figure 5 Number of Listed Companies in Malaysia fiom Period 1990 to 20 I 0

Units

1200

1000

800

600

400

200

0 Years

Columnl

S lire World federation of Exchange 2010

Based on Figure above World Federal of Exchange (2010) shows the total

numb r of listed companies in Malaysia have been increasing since 1990 from 271

listed companies to 1025 companies at the year of 2006 but had slightly decrease due to

the economic crisis on 2007 The numbers of listed companies in 2008 were 976 units

and cuntinue drop to 956 in 2010

11

Figure G Market Capitalizations in Malay~ia from Period 1990 to 200--______

USD million

45000000

40000000

35000000

30000000

25000000

20000000

15000000

10000000

5000000

000

-

-

i shy

1-

-

- i-=_

- - - -~

rshy

-~ -

-~ - - I ~ - - - - I-

- - - - 1-

~ -

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Years

Source World Federation of Exchange 20 I O

figure above demonstrates the market capitalization in Malaysia from period

1990 to 20 I 0 was inconsistent World Federal of Exchange (20 10) found that the

domestic capitalization in 1990 was USD 47868 8 million and continue to increase to

USD 306 1650 million on 1996 After 1996 it started to drop significantly on the year

0[2008 to USD 1892392 million due to the post crisis on 2007

12

-------

~

Figur~ 7 Price Earnings Ratio and Gross Dividend Yield in Bursa Malay-sia from Period 1990 to 2010

11R Gross Dividend Yield (Yo)

5 =-=- _-II-_~ -50 990 1992 1994 i9---- ~===---~=J

2002 2004 2006 ------shy 2008 2010-100 - ----- Years

-150

~--=--~J

Source World Federation of Exchange 2010

Figure above shows the price earnings ratio and gross dividend yield in Bursa

Malays ia from period 1990 to 20 I 0 The movement of the price earnings ratio and gross

dividend yield were stable and average over thc year The abnormal circulllstance

happcned in 1998 because of the crisis period and this caused the price earnings ratio

droppcd drastically in negative value

bull

13

Pusat Kbidmat Makumat Akademik UNNERSm MALAYSIA SARAWAK

PKHIDMAT MAKLUMAT AKADEMIK

1IIIIIIIIIfiim 111111111 1000245035

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

LIA W HUAN HUAN

This project is submitted in partial fulfillment of the reqt1uements for the degree of Bachelor of Finance with Honours

Faculty of Economics and Business UNIVERSITI MALAYSIA SARA W AK

2012

Statement of Originality

The work described in this Final Year Project entitled FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

is to the best of the authors knowledge that of the author except where due reference is made

10 1UIE 2012

(Date submitted) (Students signature) Liaw Huan Huan 23847

ASBTRACT

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

By

Liaw Huan Ruan

The main objective of this study is to examine the role of the financial ratios such as

dividend yield (DIY) book-to-market (BM) ratio price earnings (PIE) ratio size payout ratio

and leverage to predict the stock return for the 5 different sectors in Malaysia from 2006 to 20 I O

Using panel data analysis the result shows that the financial ratios such as size were the most

powerful in predicting the stock return in all sectors Dividend yields also show the high

predictability in stock return in all sectors except banking sector Besides that the book-to-market

ratios showed the negative significant relati()nship between stock return in servicing banking

food producer and construction sectors However the financial ratios such as leverage payout

and price earnings ratio were indicated less predictive power to predict the stock return

Therefore the results imply that investors can rely on the financial ratios such as dividend yields

and size information to gain abnormal returns in the market The results further ind icate that the

Malaysian stock market is not informational efficient

Key Words Hausman Test financial ratios ~tock return panel data analysis

ABSTRAK

NISBAH KEWANGAN DAN PULANGAN SAHAM ANALISIS PANEL DATA

Oleh

Liaw Huan Huan

Objektif utama bagi kajian ini adalah untuk mengkaji peranan nisbah kewangan seperti

hasil dividen (DIY) nisbah buku (BM) nisbah harga (PIE) saiz nisbah pembayaran dan

leverage untuk meramalkan pulangan saham bagi 5 sektor yang berbeza di Malaysia dari tahun

2006 hingga 20 I O Dengan menggunakan analisis data panel hasH kajian menunjukkan bahawa

nisbah kewangan seperti saiz adalah paling berkesan untuk membuat ramalan terhadap pulangan

saham dalam semua sektor Hasil dividen juga menunjukkan kebolehramalan pada pulangan

saham dalam semua sektor kecuali sektor pmiddoterbankan Selain itu nisbah buku menunjukkan

hubungan signifikan yang negatif dengan pulangan saham dalam sektor perkhidmatan

perbankan pengeluaran makanan dan pembinaan Walaubagaimanapun nisbah kewangan yang

seperti leverage nisbah pembayaran dan nisbah harga didapati tidak signifikan mempengaruhi

pulangan saham Secara keseluruhan kajian ini menunjukkan para pelabur dapat menggunakan

maklumat saiz and hasil dividen untuk memperoleh pulangan abnormal di pasaran Justeru hasil

kajian ini juga menur~jukkan pasaran saham di Malaysi~ adalah kurang cekap

Kata Kunci Hausman test nisbah kewangan saham pulangan panel data analisis

ACKNOWLEDGEMENT

Apart from the efforts of me the success of my thesis highly depends on the

encouragement and support from many of others I would like to take this opportunity to express

my greatest appreciation to the people who have been instrumental in the successful completion

of my Final Year Project

I would like to take this opportunity to deliver acknowledgement and thankful toward the

people who had assisted guided advised and encouraged me in the preparation of my final year

project especially to my respected project supervisor Encik Bakri Abdul Karim who had always

instructed me patiently I m felt motivated and encouraged every time I attended his meeting

With his valuable opinion expert guidance and support this project able to completed in well

timed

Hereby I would like to express my gratitude to my beloved family which is always give

support and encouragement to me from the initial to the final level of my project Moreover my

family members also help me in term of moneys aspect The high budget in completed this

research thus the monetary support from family members are very important to me

Furthermore I also would like to acknowledge to my friends who not forget to support me and guide me in doing this project Lastly I offer my regards and blessings to all of those who

supported me in any respect during the completion of the project

I

Pusat Khidmat MakJumat Akademik VNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

LIST OF TABLES IX

LIST OF FIGURES X

CHAPTER ONE INTRODUCTION

10 Introduction

11 Background of the Research

12 The Malaysian Economic 4

13 The Stock Development in Malaysia 9

14 Problem Statement 16

15 Objective 19

bmiddotmiddot bull151 General 0 ~ectlve 19

152 Specific Objectives 19

16 Significant of Study 20

17 Scope of Study 21

CHAPTER TWO LITERATURE REVIEW AND LITERATURE REVIEW

20 Introduction of Theoretical Framework 22

21 Market Efficient Hypothesis 23

22 Literature Review 24

221 Capital Asset Pricing Model 24

222 Asset Pricing Theory 27

223 Financial Ratios 29

VI

2231 Dividend Yields 29

~

223 2 Book-to-Market Ratio 31

2233 Price Earnings Ratio 32

2234 Size 33

2235 Payout Ratio 34

2236 Leverage 34

CHAPTER THREE METHODOLOGY

30 Introduction 36

31 Conceptual Framework 37

32 Research Design 38

321 Salnple 38

32 2 Model Specification~ 39

323 Data Collection 40

324 Data Analysis 40

33 Methodology 41

331 Panel Data 41

332 Dependent and Independent Variables 42

332 1 Stock Return 43

3322 Dividend yields 43

3323 Book-to-Market Ratio 44

3324 Price Earnings Ratio 44

3325 Size 45

3326 Payout Ratio 45

vii

~-

3327 Leverage 45

J

34 Hausman Test 46

35 Fixed Effect Model 48

36 Random Effect Model 49

37 Diagnostic Checking 50

CHAPTER FOUR EMPIRICAL FINDINGS AND DISCUSSIONS

40 Introduction 52

41 Statistical Descriptive 52

42 Discussion on Hausman Test Analysis 54

43 Discussion on Fixed Effect Model Analysis 56

44 Discussion on Random Effect Model Analysis 58

45 Summary of Discussion 59

CHAPTER FIVE DISCUSSION OF FINDINGS

50 Introduction 65

51 Sulnmary 65

52 Implication of Study 68

53 Recomlnendation 69

54 Limitation 70

REFERENCES 71

Vill

I

-

LIST OF TABLES

Table 1 Dependent and Independent Variables 39

Table 2 Summary Statistics for Data Used 53

Table 3 Hausman Test 55

Table 4 Fixed Effect Model 56

Table 5 Random Effect Model 58

p

IX

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

LIST OF FIGURES

Malaysia Gross Domestic Product by Sector on 2010 5

Gross Domestic Product and Annual Growth Rate from Period

2008 to 2010 6

Malaysia - Annual GOP Growth Rates by Sectors 2008 to 2010 7

Comparison the GOP in Malaysia by Sectors between 2009 and

2010 8

Number of Listed Companies in Malaysia from Period 1990 to

2010 11

Market Capitalizations in Malaysia from Period 1990 to 2010 12

Price Earnings Ratio and Gross Dividend Yield in Bursa

Malaysia from Period r990 to 2010 13

Kuala Lumpur Composite Index from Period 1990 to 2010 14

Value of Share Trading from Period 1990 to 2010 15

Conceptual Framework 45

The Summarize Findings of Financial Ratios Based on Sectors 64

x

CHAPTER ONE

INTRODUCTION

10 Introduction

This research is study on the relationship between the financial ratios and stock

return This chapter discusses the background of the research Besides that this study

also covers problem statement purpose of research significant of research and scope of

research

11 Background of Study

Nearly five decades ago study on the pred iction of stock return has been one of

the most challenging topics in financial economics A number of theoretical models

have been developed to explain stock return such as Capital Asset Pricing Model

(CAPM) Arsitrage Pricing Theory (APT) Fama and French three factor model and

others financial ratios

In the early stages a number of studies on CAPM were considerably written in

the academic research CAPM consider as one of the most important modern capital

theory which originally proposed by Sharpe (1964) The parallel) work was also

~

performed by Lintner (1965) and Black (1972) CAPM had been continuously used in

practical portfolio management and the capital equilibrium model for the academic

research guiding purpose (Koo amp Olson 2007) Besides that CAPM were widely used

to measures the powerful explanation on the expected risk and return theoretical as well

as empirical studies (Michailidis Tsopoglou Papanastasiou amp Mariola 2006 Nguyen

amp Puri 2010) However Michailidis et at (2006) found that the basic theory hypothesis

of higher risk was associated with higher return which is not supportive The early test

CAPM worked efficiently as a pred ictor of the stock return but many of studies found

anomalies in CAPM (Padney 2001)

More to the point in the early 1976s Arbitrage Pricing Theory (APT) proposed

by Stephen Ross as an alternative to replace CAPM to explain stock return The main

idea of APT was the price of security driven by number of factors There were several

dependent macroeconomics factors influenced on the asset return such as inflation rate

GOP exchange rate change in price indexes and etc (Somoye Akintoye amp Oseni

2009) The asset return were relying on the influences of macroeconomic factors and

others incident that were distinctive to the firm but the expected risk premium only

affected by the macroeconomic factors (Hohling 2009) In the efficeint market

hypothesis the informat ion change in the macroeconomic variables fully reflect the

current stock prices therefore this caused the investors to get the anomalies return in

the future stock market movment (Balvers Cosimano amp Mcdonald 1990)

2

Additionally Fama and French (1992) co written came out a new model which

was known as Fama-French three model factor Fama-French three model factor

measured by the combination of the market beta such as size Leverage book-to market

equity and price earnings ratio with the cross sectional of expected stock return (Fama

amp French 1992) The Fama-French three model factor was a simple variation in stock

return compare with CAPM due to the additional of size and book-to-market-equity in

the model (Ajili 200 I) CAPM was only using one variable (beta) to describe the stock

return but reversely Fama-French three model factor was using three variables such as

small caps book-to-market ratio and the additional of size (Fama amp French 2008)

However CAPM and Fama-French three model factor had performed a good job in

explaining the cross section of stock return (Ajlis 200 I)

As Fama (1970) recommended that an efficient capital market is all the security

prices adjust rapidly new information and the prices of an asset reflect all available

information However the stock prices wandered randomly over the time period and the

stock prices change could use predictors (Padney 200) An efficient market as a

dominate sources of allocation in order to provide an accurate signal for the firm to

make investment decision and investor can choose among securities that represent

ownership of firms activities (Brown amp KReiIlY 2009) Besides that if the abnormal

rate of return on the stock market which were lower than the normal rate of return it

means that the capital market was efficient and vice versa

3

12 The Malaysian Economic

Since Malaysia became independent on 1957 Malaysias economic had grown

rapidly Malaysia is a developing country which consists of thirteen states and three

federal territories Malaysia considers as a small country where totals landmass of

329847 square kilometres (127315 sq mi) which separated by the South China

Sea into two regions Peninsular Malaysia and Malaysia Borneo In the year of201 0 the

population exceeded 283 million (United States State Department 20 I 0)

According to the United States State Department (2010) the Malaysia annual

real gross domestic product (GOP) growth rate grew by the average of 446 per year

from period 2006 to 20FO The total Nominal GOP on 2010 is $2553 billion and the

total nominal per capital Income (GNI) is $8126 Malaysia is a country which

prosperity In the mineral natural resources and agricultural product The natural

resources are such as petroleum liquefied natural gas (LNG) tin minerals and others

where the agricultural products are such as palm oil rubber timber cocoa rice tropical

fruit fish coconut and others

The Malaysia economy is expected to grow healthy and strong by switching

from the agricultural and commodities sectors to the manufacture and export sectors

Based on the United States State Department (20 I 0) stated that the Malaysia traded on

merchandise export is 2103 billion where the traded includes electronic products

machinery liquid natural gas petroleum products and telecom equipment The recent

4

Pu at Khldm rMIIJdum tAk UNlVERsm MALAYSIA

impressive perfonnance shows the export as a main contribution in services sector to

lead the economic growth in Malaysia (Economy Watch 2010)

F 1 MImiddot G oss Do f Product b S ctor on 2010 -

change2010 ChangeSector (Q4 2010(RM billion) (20102009)Q42009)

Source Ministry of International Trade and Industry 2011

Figure above shows the Malaysias gross domestic product on 2010 was mostly

contributed by services sector which shows RM3206 billion compare to the

construction sectors which only shows RM 182 billion Nowadays Malaysia is a

middle-income country which focuses most on the services and manufacturing sector

Moreover Malaysia become one of the largest exporters of world in semiconductor

devices electric goods and as well as infonnation and communication technology (lCT)

products

5

Figure 2 Gross Domestic Product and Annual Growth Rate from Period 2008 to 2010

40

Source Ministry ofIntemational Trade and Industry 2011

Figure above represents the annual gross domestic product growth in Malaysia

from period 2008 to 2010 taken as whole was moving average but the abnonnal

circumstance happened during 2009 quarter 1 The annual gross domestic product

growth in 2008 average was RM13255 million The average amount drops to

RM13030 million in 2009 However the amount annual gross domestic product growth

in 2010 recovers and increases to RM13390 million

6

3 Malaysia - Annual GDP Growth Rates by Sectors 2008 to 2010

Source Source Ministry of Intemational Trade and Industry 2011

Figure above indicates that the GDP annual growth rates by sectors the growth

rate in services and manufacturing sectors were higher than the others sectors During

the abnormal circumstance in 2009 it shows negative value substantially as well

However in the year 2010 the GDP growth in Malaysia recovered and the

manufacturing sector remain the highest growth rate among the others sector

7

Figure 4 Comparison the GDP in Malaysia by Sectors between 2009 and 2010

I(I~ IM111AI

Source Ministry of International Trade and Industry 2011

Figure above is the comparison between the GDP by sector in Malaysia for 2009

and 2010 and it show that the total (1)P increase from RM5211billion in 2009 and

became RM5584 billion in 2010 The sectors such as services and manufacturing

sectors indicated the growth in the GDP However the sectors like mining amp quarrying

agricultural and construction indicated the percentages of decrease in the GDP growth

rate

8

13 The Stock Development in Malaysia

In 1960 the Malaysia Stock Exchange was first setting up and known as

Malayan Stock Exchange and in 1965 it was changed to Stock Exchange of Malaysia

and Singapore due to the secession of Singapore from Malaysia In 1973 the currency

interchange ability between Malaysia and Singapore had been ceased and the Stock

Exchange of Malaysia and Singapore were divided into Kuala Lumpur Stock Exchange

Bcrhad (KLSEB) and Stock Exchange of Singapore (SES) (Bursa Malaysia 20 L1)

Aller demutualize exercise on 14th April 2004 Kuala Lumpur Stock Exchange (KLSE)

was renamed to Bursa Malaysia On 18 th March 2005 Bursa Malaysia was listed on the

Main Board of Bursa Malaysia Securities Berhad (Chong amp Puah 2009) However

Bursa Malaysia currently consists of 988 companies which 637 companies on Main

Board 227 companies on Second Board and 124 companies on MESDAQ (Lee amp Lee

2008)

Moreover Capital market is a place for investor and institute trade financial

securities in order to raise funds Thus the market where securities traded is known as

Sccurities Market it comprised of both the primary and secondary markets The primary

market is known as new issue market where it deals with new issue securities in

Malaysia whereas the secondary market focuses on the trading of existing securities and

it often termed as stock exchange market According to Lee and Lee (2008) generally

the investor desire to earn a positive return in their investment The return of the shares

9

I

trade for the short term investor is capital gain and the dividend is for the long term

in cstor

However the stock market in Malaysia should always be in the range o[

effic k ncy This is because the efficient capital market assumes that an initial premise of

an fftcient market request that a large number of profit maximizing participant analyze

and va lue securities Besides that the new information regarding the securities comes to

the market in a random fashion However the buyer and seller decision of all those

profit maximizing investor who adjust security prices rapidly reflect the effect of new

intormation (Brown amp Reilly 2009)

In Malaysia therc are no practices on the tax loss-selling hypothesis therefore

there arc no capital gain taxes for the residents or non-residents The stock return

seasonality in Malaysia indicates that stock market in Malaysia is not efficient in

reflecting the information I-Ience investor can spend time in getting higher returns

Generally the efficient market hypothesis (EMH) stated that the stock price and return

are not able to be predicted by using the past price information However the

seasonality effect presence and this implies the efficiency market and negates the weak

form oCthe efficiency market hypothesis (Padney 2004)

The Malaysian capital market is focus on the weak form efficiency market and

risk of return relationship The weak form efficiency markets where the prices reflect all

the historical market trading information Most of the tests show this information unable

10

to generate abnormal return (Nasir Mohamad amp Hamid 1998) Based on Tan (2006)

Ma laysia stock index futures market does not subscribe to random walk hypothesis but

stock return are predictable

Figure 5 Number of Listed Companies in Malaysia fiom Period 1990 to 20 I 0

Units

1200

1000

800

600

400

200

0 Years

Columnl

S lire World federation of Exchange 2010

Based on Figure above World Federal of Exchange (2010) shows the total

numb r of listed companies in Malaysia have been increasing since 1990 from 271

listed companies to 1025 companies at the year of 2006 but had slightly decrease due to

the economic crisis on 2007 The numbers of listed companies in 2008 were 976 units

and cuntinue drop to 956 in 2010

11

Figure G Market Capitalizations in Malay~ia from Period 1990 to 200--______

USD million

45000000

40000000

35000000

30000000

25000000

20000000

15000000

10000000

5000000

000

-

-

i shy

1-

-

- i-=_

- - - -~

rshy

-~ -

-~ - - I ~ - - - - I-

- - - - 1-

~ -

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Years

Source World Federation of Exchange 20 I O

figure above demonstrates the market capitalization in Malaysia from period

1990 to 20 I 0 was inconsistent World Federal of Exchange (20 10) found that the

domestic capitalization in 1990 was USD 47868 8 million and continue to increase to

USD 306 1650 million on 1996 After 1996 it started to drop significantly on the year

0[2008 to USD 1892392 million due to the post crisis on 2007

12

-------

~

Figur~ 7 Price Earnings Ratio and Gross Dividend Yield in Bursa Malay-sia from Period 1990 to 2010

11R Gross Dividend Yield (Yo)

5 =-=- _-II-_~ -50 990 1992 1994 i9---- ~===---~=J

2002 2004 2006 ------shy 2008 2010-100 - ----- Years

-150

~--=--~J

Source World Federation of Exchange 2010

Figure above shows the price earnings ratio and gross dividend yield in Bursa

Malays ia from period 1990 to 20 I 0 The movement of the price earnings ratio and gross

dividend yield were stable and average over thc year The abnormal circulllstance

happcned in 1998 because of the crisis period and this caused the price earnings ratio

droppcd drastically in negative value

bull

13

Statement of Originality

The work described in this Final Year Project entitled FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

is to the best of the authors knowledge that of the author except where due reference is made

10 1UIE 2012

(Date submitted) (Students signature) Liaw Huan Huan 23847

ASBTRACT

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

By

Liaw Huan Ruan

The main objective of this study is to examine the role of the financial ratios such as

dividend yield (DIY) book-to-market (BM) ratio price earnings (PIE) ratio size payout ratio

and leverage to predict the stock return for the 5 different sectors in Malaysia from 2006 to 20 I O

Using panel data analysis the result shows that the financial ratios such as size were the most

powerful in predicting the stock return in all sectors Dividend yields also show the high

predictability in stock return in all sectors except banking sector Besides that the book-to-market

ratios showed the negative significant relati()nship between stock return in servicing banking

food producer and construction sectors However the financial ratios such as leverage payout

and price earnings ratio were indicated less predictive power to predict the stock return

Therefore the results imply that investors can rely on the financial ratios such as dividend yields

and size information to gain abnormal returns in the market The results further ind icate that the

Malaysian stock market is not informational efficient

Key Words Hausman Test financial ratios ~tock return panel data analysis

ABSTRAK

NISBAH KEWANGAN DAN PULANGAN SAHAM ANALISIS PANEL DATA

Oleh

Liaw Huan Huan

Objektif utama bagi kajian ini adalah untuk mengkaji peranan nisbah kewangan seperti

hasil dividen (DIY) nisbah buku (BM) nisbah harga (PIE) saiz nisbah pembayaran dan

leverage untuk meramalkan pulangan saham bagi 5 sektor yang berbeza di Malaysia dari tahun

2006 hingga 20 I O Dengan menggunakan analisis data panel hasH kajian menunjukkan bahawa

nisbah kewangan seperti saiz adalah paling berkesan untuk membuat ramalan terhadap pulangan

saham dalam semua sektor Hasil dividen juga menunjukkan kebolehramalan pada pulangan

saham dalam semua sektor kecuali sektor pmiddoterbankan Selain itu nisbah buku menunjukkan

hubungan signifikan yang negatif dengan pulangan saham dalam sektor perkhidmatan

perbankan pengeluaran makanan dan pembinaan Walaubagaimanapun nisbah kewangan yang

seperti leverage nisbah pembayaran dan nisbah harga didapati tidak signifikan mempengaruhi

pulangan saham Secara keseluruhan kajian ini menunjukkan para pelabur dapat menggunakan

maklumat saiz and hasil dividen untuk memperoleh pulangan abnormal di pasaran Justeru hasil

kajian ini juga menur~jukkan pasaran saham di Malaysi~ adalah kurang cekap

Kata Kunci Hausman test nisbah kewangan saham pulangan panel data analisis

ACKNOWLEDGEMENT

Apart from the efforts of me the success of my thesis highly depends on the

encouragement and support from many of others I would like to take this opportunity to express

my greatest appreciation to the people who have been instrumental in the successful completion

of my Final Year Project

I would like to take this opportunity to deliver acknowledgement and thankful toward the

people who had assisted guided advised and encouraged me in the preparation of my final year

project especially to my respected project supervisor Encik Bakri Abdul Karim who had always

instructed me patiently I m felt motivated and encouraged every time I attended his meeting

With his valuable opinion expert guidance and support this project able to completed in well

timed

Hereby I would like to express my gratitude to my beloved family which is always give

support and encouragement to me from the initial to the final level of my project Moreover my

family members also help me in term of moneys aspect The high budget in completed this

research thus the monetary support from family members are very important to me

Furthermore I also would like to acknowledge to my friends who not forget to support me and guide me in doing this project Lastly I offer my regards and blessings to all of those who

supported me in any respect during the completion of the project

I

Pusat Khidmat MakJumat Akademik VNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

LIST OF TABLES IX

LIST OF FIGURES X

CHAPTER ONE INTRODUCTION

10 Introduction

11 Background of the Research

12 The Malaysian Economic 4

13 The Stock Development in Malaysia 9

14 Problem Statement 16

15 Objective 19

bmiddotmiddot bull151 General 0 ~ectlve 19

152 Specific Objectives 19

16 Significant of Study 20

17 Scope of Study 21

CHAPTER TWO LITERATURE REVIEW AND LITERATURE REVIEW

20 Introduction of Theoretical Framework 22

21 Market Efficient Hypothesis 23

22 Literature Review 24

221 Capital Asset Pricing Model 24

222 Asset Pricing Theory 27

223 Financial Ratios 29

VI

2231 Dividend Yields 29

~

223 2 Book-to-Market Ratio 31

2233 Price Earnings Ratio 32

2234 Size 33

2235 Payout Ratio 34

2236 Leverage 34

CHAPTER THREE METHODOLOGY

30 Introduction 36

31 Conceptual Framework 37

32 Research Design 38

321 Salnple 38

32 2 Model Specification~ 39

323 Data Collection 40

324 Data Analysis 40

33 Methodology 41

331 Panel Data 41

332 Dependent and Independent Variables 42

332 1 Stock Return 43

3322 Dividend yields 43

3323 Book-to-Market Ratio 44

3324 Price Earnings Ratio 44

3325 Size 45

3326 Payout Ratio 45

vii

~-

3327 Leverage 45

J

34 Hausman Test 46

35 Fixed Effect Model 48

36 Random Effect Model 49

37 Diagnostic Checking 50

CHAPTER FOUR EMPIRICAL FINDINGS AND DISCUSSIONS

40 Introduction 52

41 Statistical Descriptive 52

42 Discussion on Hausman Test Analysis 54

43 Discussion on Fixed Effect Model Analysis 56

44 Discussion on Random Effect Model Analysis 58

45 Summary of Discussion 59

CHAPTER FIVE DISCUSSION OF FINDINGS

50 Introduction 65

51 Sulnmary 65

52 Implication of Study 68

53 Recomlnendation 69

54 Limitation 70

REFERENCES 71

Vill

I

-

LIST OF TABLES

Table 1 Dependent and Independent Variables 39

Table 2 Summary Statistics for Data Used 53

Table 3 Hausman Test 55

Table 4 Fixed Effect Model 56

Table 5 Random Effect Model 58

p

IX

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

LIST OF FIGURES

Malaysia Gross Domestic Product by Sector on 2010 5

Gross Domestic Product and Annual Growth Rate from Period

2008 to 2010 6

Malaysia - Annual GOP Growth Rates by Sectors 2008 to 2010 7

Comparison the GOP in Malaysia by Sectors between 2009 and

2010 8

Number of Listed Companies in Malaysia from Period 1990 to

2010 11

Market Capitalizations in Malaysia from Period 1990 to 2010 12

Price Earnings Ratio and Gross Dividend Yield in Bursa

Malaysia from Period r990 to 2010 13

Kuala Lumpur Composite Index from Period 1990 to 2010 14

Value of Share Trading from Period 1990 to 2010 15

Conceptual Framework 45

The Summarize Findings of Financial Ratios Based on Sectors 64

x

CHAPTER ONE

INTRODUCTION

10 Introduction

This research is study on the relationship between the financial ratios and stock

return This chapter discusses the background of the research Besides that this study

also covers problem statement purpose of research significant of research and scope of

research

11 Background of Study

Nearly five decades ago study on the pred iction of stock return has been one of

the most challenging topics in financial economics A number of theoretical models

have been developed to explain stock return such as Capital Asset Pricing Model

(CAPM) Arsitrage Pricing Theory (APT) Fama and French three factor model and

others financial ratios

In the early stages a number of studies on CAPM were considerably written in

the academic research CAPM consider as one of the most important modern capital

theory which originally proposed by Sharpe (1964) The parallel) work was also

~

performed by Lintner (1965) and Black (1972) CAPM had been continuously used in

practical portfolio management and the capital equilibrium model for the academic

research guiding purpose (Koo amp Olson 2007) Besides that CAPM were widely used

to measures the powerful explanation on the expected risk and return theoretical as well

as empirical studies (Michailidis Tsopoglou Papanastasiou amp Mariola 2006 Nguyen

amp Puri 2010) However Michailidis et at (2006) found that the basic theory hypothesis

of higher risk was associated with higher return which is not supportive The early test

CAPM worked efficiently as a pred ictor of the stock return but many of studies found

anomalies in CAPM (Padney 2001)

More to the point in the early 1976s Arbitrage Pricing Theory (APT) proposed

by Stephen Ross as an alternative to replace CAPM to explain stock return The main

idea of APT was the price of security driven by number of factors There were several

dependent macroeconomics factors influenced on the asset return such as inflation rate

GOP exchange rate change in price indexes and etc (Somoye Akintoye amp Oseni

2009) The asset return were relying on the influences of macroeconomic factors and

others incident that were distinctive to the firm but the expected risk premium only

affected by the macroeconomic factors (Hohling 2009) In the efficeint market

hypothesis the informat ion change in the macroeconomic variables fully reflect the

current stock prices therefore this caused the investors to get the anomalies return in

the future stock market movment (Balvers Cosimano amp Mcdonald 1990)

2

Additionally Fama and French (1992) co written came out a new model which

was known as Fama-French three model factor Fama-French three model factor

measured by the combination of the market beta such as size Leverage book-to market

equity and price earnings ratio with the cross sectional of expected stock return (Fama

amp French 1992) The Fama-French three model factor was a simple variation in stock

return compare with CAPM due to the additional of size and book-to-market-equity in

the model (Ajili 200 I) CAPM was only using one variable (beta) to describe the stock

return but reversely Fama-French three model factor was using three variables such as

small caps book-to-market ratio and the additional of size (Fama amp French 2008)

However CAPM and Fama-French three model factor had performed a good job in

explaining the cross section of stock return (Ajlis 200 I)

As Fama (1970) recommended that an efficient capital market is all the security

prices adjust rapidly new information and the prices of an asset reflect all available

information However the stock prices wandered randomly over the time period and the

stock prices change could use predictors (Padney 200) An efficient market as a

dominate sources of allocation in order to provide an accurate signal for the firm to

make investment decision and investor can choose among securities that represent

ownership of firms activities (Brown amp KReiIlY 2009) Besides that if the abnormal

rate of return on the stock market which were lower than the normal rate of return it

means that the capital market was efficient and vice versa

3

12 The Malaysian Economic

Since Malaysia became independent on 1957 Malaysias economic had grown

rapidly Malaysia is a developing country which consists of thirteen states and three

federal territories Malaysia considers as a small country where totals landmass of

329847 square kilometres (127315 sq mi) which separated by the South China

Sea into two regions Peninsular Malaysia and Malaysia Borneo In the year of201 0 the

population exceeded 283 million (United States State Department 20 I 0)

According to the United States State Department (2010) the Malaysia annual

real gross domestic product (GOP) growth rate grew by the average of 446 per year

from period 2006 to 20FO The total Nominal GOP on 2010 is $2553 billion and the

total nominal per capital Income (GNI) is $8126 Malaysia is a country which

prosperity In the mineral natural resources and agricultural product The natural

resources are such as petroleum liquefied natural gas (LNG) tin minerals and others

where the agricultural products are such as palm oil rubber timber cocoa rice tropical

fruit fish coconut and others

The Malaysia economy is expected to grow healthy and strong by switching

from the agricultural and commodities sectors to the manufacture and export sectors

Based on the United States State Department (20 I 0) stated that the Malaysia traded on

merchandise export is 2103 billion where the traded includes electronic products

machinery liquid natural gas petroleum products and telecom equipment The recent

4

Pu at Khldm rMIIJdum tAk UNlVERsm MALAYSIA

impressive perfonnance shows the export as a main contribution in services sector to

lead the economic growth in Malaysia (Economy Watch 2010)

F 1 MImiddot G oss Do f Product b S ctor on 2010 -

change2010 ChangeSector (Q4 2010(RM billion) (20102009)Q42009)

Source Ministry of International Trade and Industry 2011

Figure above shows the Malaysias gross domestic product on 2010 was mostly

contributed by services sector which shows RM3206 billion compare to the

construction sectors which only shows RM 182 billion Nowadays Malaysia is a

middle-income country which focuses most on the services and manufacturing sector

Moreover Malaysia become one of the largest exporters of world in semiconductor

devices electric goods and as well as infonnation and communication technology (lCT)

products

5

Figure 2 Gross Domestic Product and Annual Growth Rate from Period 2008 to 2010

40

Source Ministry ofIntemational Trade and Industry 2011

Figure above represents the annual gross domestic product growth in Malaysia

from period 2008 to 2010 taken as whole was moving average but the abnonnal

circumstance happened during 2009 quarter 1 The annual gross domestic product

growth in 2008 average was RM13255 million The average amount drops to

RM13030 million in 2009 However the amount annual gross domestic product growth

in 2010 recovers and increases to RM13390 million

6

3 Malaysia - Annual GDP Growth Rates by Sectors 2008 to 2010

Source Source Ministry of Intemational Trade and Industry 2011

Figure above indicates that the GDP annual growth rates by sectors the growth

rate in services and manufacturing sectors were higher than the others sectors During

the abnormal circumstance in 2009 it shows negative value substantially as well

However in the year 2010 the GDP growth in Malaysia recovered and the

manufacturing sector remain the highest growth rate among the others sector

7

Figure 4 Comparison the GDP in Malaysia by Sectors between 2009 and 2010

I(I~ IM111AI

Source Ministry of International Trade and Industry 2011

Figure above is the comparison between the GDP by sector in Malaysia for 2009

and 2010 and it show that the total (1)P increase from RM5211billion in 2009 and

became RM5584 billion in 2010 The sectors such as services and manufacturing

sectors indicated the growth in the GDP However the sectors like mining amp quarrying

agricultural and construction indicated the percentages of decrease in the GDP growth

rate

8

13 The Stock Development in Malaysia

In 1960 the Malaysia Stock Exchange was first setting up and known as

Malayan Stock Exchange and in 1965 it was changed to Stock Exchange of Malaysia

and Singapore due to the secession of Singapore from Malaysia In 1973 the currency

interchange ability between Malaysia and Singapore had been ceased and the Stock

Exchange of Malaysia and Singapore were divided into Kuala Lumpur Stock Exchange

Bcrhad (KLSEB) and Stock Exchange of Singapore (SES) (Bursa Malaysia 20 L1)

Aller demutualize exercise on 14th April 2004 Kuala Lumpur Stock Exchange (KLSE)

was renamed to Bursa Malaysia On 18 th March 2005 Bursa Malaysia was listed on the

Main Board of Bursa Malaysia Securities Berhad (Chong amp Puah 2009) However

Bursa Malaysia currently consists of 988 companies which 637 companies on Main

Board 227 companies on Second Board and 124 companies on MESDAQ (Lee amp Lee

2008)

Moreover Capital market is a place for investor and institute trade financial

securities in order to raise funds Thus the market where securities traded is known as

Sccurities Market it comprised of both the primary and secondary markets The primary

market is known as new issue market where it deals with new issue securities in

Malaysia whereas the secondary market focuses on the trading of existing securities and

it often termed as stock exchange market According to Lee and Lee (2008) generally

the investor desire to earn a positive return in their investment The return of the shares

9

I

trade for the short term investor is capital gain and the dividend is for the long term

in cstor

However the stock market in Malaysia should always be in the range o[

effic k ncy This is because the efficient capital market assumes that an initial premise of

an fftcient market request that a large number of profit maximizing participant analyze

and va lue securities Besides that the new information regarding the securities comes to

the market in a random fashion However the buyer and seller decision of all those

profit maximizing investor who adjust security prices rapidly reflect the effect of new

intormation (Brown amp Reilly 2009)

In Malaysia therc are no practices on the tax loss-selling hypothesis therefore

there arc no capital gain taxes for the residents or non-residents The stock return

seasonality in Malaysia indicates that stock market in Malaysia is not efficient in

reflecting the information I-Ience investor can spend time in getting higher returns

Generally the efficient market hypothesis (EMH) stated that the stock price and return

are not able to be predicted by using the past price information However the

seasonality effect presence and this implies the efficiency market and negates the weak

form oCthe efficiency market hypothesis (Padney 2004)

The Malaysian capital market is focus on the weak form efficiency market and

risk of return relationship The weak form efficiency markets where the prices reflect all

the historical market trading information Most of the tests show this information unable

10

to generate abnormal return (Nasir Mohamad amp Hamid 1998) Based on Tan (2006)

Ma laysia stock index futures market does not subscribe to random walk hypothesis but

stock return are predictable

Figure 5 Number of Listed Companies in Malaysia fiom Period 1990 to 20 I 0

Units

1200

1000

800

600

400

200

0 Years

Columnl

S lire World federation of Exchange 2010

Based on Figure above World Federal of Exchange (2010) shows the total

numb r of listed companies in Malaysia have been increasing since 1990 from 271

listed companies to 1025 companies at the year of 2006 but had slightly decrease due to

the economic crisis on 2007 The numbers of listed companies in 2008 were 976 units

and cuntinue drop to 956 in 2010

11

Figure G Market Capitalizations in Malay~ia from Period 1990 to 200--______

USD million

45000000

40000000

35000000

30000000

25000000

20000000

15000000

10000000

5000000

000

-

-

i shy

1-

-

- i-=_

- - - -~

rshy

-~ -

-~ - - I ~ - - - - I-

- - - - 1-

~ -

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Years

Source World Federation of Exchange 20 I O

figure above demonstrates the market capitalization in Malaysia from period

1990 to 20 I 0 was inconsistent World Federal of Exchange (20 10) found that the

domestic capitalization in 1990 was USD 47868 8 million and continue to increase to

USD 306 1650 million on 1996 After 1996 it started to drop significantly on the year

0[2008 to USD 1892392 million due to the post crisis on 2007

12

-------

~

Figur~ 7 Price Earnings Ratio and Gross Dividend Yield in Bursa Malay-sia from Period 1990 to 2010

11R Gross Dividend Yield (Yo)

5 =-=- _-II-_~ -50 990 1992 1994 i9---- ~===---~=J

2002 2004 2006 ------shy 2008 2010-100 - ----- Years

-150

~--=--~J

Source World Federation of Exchange 2010

Figure above shows the price earnings ratio and gross dividend yield in Bursa

Malays ia from period 1990 to 20 I 0 The movement of the price earnings ratio and gross

dividend yield were stable and average over thc year The abnormal circulllstance

happcned in 1998 because of the crisis period and this caused the price earnings ratio

droppcd drastically in negative value

bull

13

ASBTRACT

FINANCIAL RATIOS AND STOCK RETURN A PANEL DATA ANALYSIS

By

Liaw Huan Ruan

The main objective of this study is to examine the role of the financial ratios such as

dividend yield (DIY) book-to-market (BM) ratio price earnings (PIE) ratio size payout ratio

and leverage to predict the stock return for the 5 different sectors in Malaysia from 2006 to 20 I O

Using panel data analysis the result shows that the financial ratios such as size were the most

powerful in predicting the stock return in all sectors Dividend yields also show the high

predictability in stock return in all sectors except banking sector Besides that the book-to-market

ratios showed the negative significant relati()nship between stock return in servicing banking

food producer and construction sectors However the financial ratios such as leverage payout

and price earnings ratio were indicated less predictive power to predict the stock return

Therefore the results imply that investors can rely on the financial ratios such as dividend yields

and size information to gain abnormal returns in the market The results further ind icate that the

Malaysian stock market is not informational efficient

Key Words Hausman Test financial ratios ~tock return panel data analysis

ABSTRAK

NISBAH KEWANGAN DAN PULANGAN SAHAM ANALISIS PANEL DATA

Oleh

Liaw Huan Huan

Objektif utama bagi kajian ini adalah untuk mengkaji peranan nisbah kewangan seperti

hasil dividen (DIY) nisbah buku (BM) nisbah harga (PIE) saiz nisbah pembayaran dan

leverage untuk meramalkan pulangan saham bagi 5 sektor yang berbeza di Malaysia dari tahun

2006 hingga 20 I O Dengan menggunakan analisis data panel hasH kajian menunjukkan bahawa

nisbah kewangan seperti saiz adalah paling berkesan untuk membuat ramalan terhadap pulangan

saham dalam semua sektor Hasil dividen juga menunjukkan kebolehramalan pada pulangan

saham dalam semua sektor kecuali sektor pmiddoterbankan Selain itu nisbah buku menunjukkan

hubungan signifikan yang negatif dengan pulangan saham dalam sektor perkhidmatan

perbankan pengeluaran makanan dan pembinaan Walaubagaimanapun nisbah kewangan yang

seperti leverage nisbah pembayaran dan nisbah harga didapati tidak signifikan mempengaruhi

pulangan saham Secara keseluruhan kajian ini menunjukkan para pelabur dapat menggunakan

maklumat saiz and hasil dividen untuk memperoleh pulangan abnormal di pasaran Justeru hasil

kajian ini juga menur~jukkan pasaran saham di Malaysi~ adalah kurang cekap

Kata Kunci Hausman test nisbah kewangan saham pulangan panel data analisis

ACKNOWLEDGEMENT

Apart from the efforts of me the success of my thesis highly depends on the

encouragement and support from many of others I would like to take this opportunity to express

my greatest appreciation to the people who have been instrumental in the successful completion

of my Final Year Project

I would like to take this opportunity to deliver acknowledgement and thankful toward the

people who had assisted guided advised and encouraged me in the preparation of my final year

project especially to my respected project supervisor Encik Bakri Abdul Karim who had always

instructed me patiently I m felt motivated and encouraged every time I attended his meeting

With his valuable opinion expert guidance and support this project able to completed in well

timed

Hereby I would like to express my gratitude to my beloved family which is always give

support and encouragement to me from the initial to the final level of my project Moreover my

family members also help me in term of moneys aspect The high budget in completed this

research thus the monetary support from family members are very important to me

Furthermore I also would like to acknowledge to my friends who not forget to support me and guide me in doing this project Lastly I offer my regards and blessings to all of those who

supported me in any respect during the completion of the project

I

Pusat Khidmat MakJumat Akademik VNlVERSm MALAYSIA SARAWAK

TABLE OF CONTENTS

LIST OF TABLES IX

LIST OF FIGURES X

CHAPTER ONE INTRODUCTION

10 Introduction

11 Background of the Research

12 The Malaysian Economic 4

13 The Stock Development in Malaysia 9

14 Problem Statement 16

15 Objective 19

bmiddotmiddot bull151 General 0 ~ectlve 19

152 Specific Objectives 19

16 Significant of Study 20

17 Scope of Study 21

CHAPTER TWO LITERATURE REVIEW AND LITERATURE REVIEW

20 Introduction of Theoretical Framework 22

21 Market Efficient Hypothesis 23

22 Literature Review 24

221 Capital Asset Pricing Model 24

222 Asset Pricing Theory 27

223 Financial Ratios 29

VI

2231 Dividend Yields 29

~

223 2 Book-to-Market Ratio 31

2233 Price Earnings Ratio 32

2234 Size 33

2235 Payout Ratio 34

2236 Leverage 34

CHAPTER THREE METHODOLOGY

30 Introduction 36

31 Conceptual Framework 37

32 Research Design 38

321 Salnple 38

32 2 Model Specification~ 39

323 Data Collection 40

324 Data Analysis 40

33 Methodology 41

331 Panel Data 41

332 Dependent and Independent Variables 42

332 1 Stock Return 43

3322 Dividend yields 43

3323 Book-to-Market Ratio 44

3324 Price Earnings Ratio 44

3325 Size 45

3326 Payout Ratio 45

vii

~-

3327 Leverage 45

J

34 Hausman Test 46

35 Fixed Effect Model 48

36 Random Effect Model 49

37 Diagnostic Checking 50

CHAPTER FOUR EMPIRICAL FINDINGS AND DISCUSSIONS

40 Introduction 52

41 Statistical Descriptive 52

42 Discussion on Hausman Test Analysis 54

43 Discussion on Fixed Effect Model Analysis 56

44 Discussion on Random Effect Model Analysis 58

45 Summary of Discussion 59

CHAPTER FIVE DISCUSSION OF FINDINGS

50 Introduction 65

51 Sulnmary 65

52 Implication of Study 68

53 Recomlnendation 69

54 Limitation 70

REFERENCES 71

Vill

I

-

LIST OF TABLES

Table 1 Dependent and Independent Variables 39

Table 2 Summary Statistics for Data Used 53

Table 3 Hausman Test 55

Table 4 Fixed Effect Model 56

Table 5 Random Effect Model 58

p

IX

Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

Figure 9

Figure 10

Figure 11

LIST OF FIGURES

Malaysia Gross Domestic Product by Sector on 2010 5

Gross Domestic Product and Annual Growth Rate from Period

2008 to 2010 6

Malaysia - Annual GOP Growth Rates by Sectors 2008 to 2010 7

Comparison the GOP in Malaysia by Sectors between 2009 and

2010 8

Number of Listed Companies in Malaysia from Period 1990 to

2010 11

Market Capitalizations in Malaysia from Period 1990 to 2010 12

Price Earnings Ratio and Gross Dividend Yield in Bursa

Malaysia from Period r990 to 2010 13

Kuala Lumpur Composite Index from Period 1990 to 2010 14

Value of Share Trading from Period 1990 to 2010 15

Conceptual Framework 45

The Summarize Findings of Financial Ratios Based on Sectors 64

x

CHAPTER ONE

INTRODUCTION

10 Introduction

This research is study on the relationship between the financial ratios and stock

return This chapter discusses the background of the research Besides that this study

also covers problem statement purpose of research significant of research and scope of

research

11 Background of Study

Nearly five decades ago study on the pred iction of stock return has been one of

the most challenging topics in financial economics A number of theoretical models

have been developed to explain stock return such as Capital Asset Pricing Model

(CAPM) Arsitrage Pricing Theory (APT) Fama and French three factor model and

others financial ratios

In the early stages a number of studies on CAPM were considerably written in

the academic research CAPM consider as one of the most important modern capital

theory which originally proposed by Sharpe (1964) The parallel) work was also

~

performed by Lintner (1965) and Black (1972) CAPM had been continuously used in

practical portfolio management and the capital equilibrium model for the academic

research guiding purpose (Koo amp Olson 2007) Besides that CAPM were widely used

to measures the powerful explanation on the expected risk and return theoretical as well

as empirical studies (Michailidis Tsopoglou Papanastasiou amp Mariola 2006 Nguyen

amp Puri 2010) However Michailidis et at (2006) found that the basic theory hypothesis

of higher risk was associated with higher return which is not supportive The early test

CAPM worked efficiently as a pred ictor of the stock return but many of studies found

anomalies in CAPM (Padney 2001)

More to the point in the early 1976s Arbitrage Pricing Theory (APT) proposed

by Stephen Ross as an alternative to replace CAPM to explain stock return The main

idea of APT was the price of security driven by number of factors There were several

dependent macroeconomics factors influenced on the asset return such as inflation rate

GOP exchange rate change in price indexes and etc (Somoye Akintoye amp Oseni

2009) The asset return were relying on the influences of macroeconomic factors and

others incident that were distinctive to the firm but the expected risk premium only

affected by the macroeconomic factors (Hohling 2009) In the efficeint market

hypothesis the informat ion change in the macroeconomic variables fully reflect the

current stock prices therefore this caused the investors to get the anomalies return in

the future stock market movment (Balvers Cosimano amp Mcdonald 1990)

2

Additionally Fama and French (1992) co written came out a new model which

was known as Fama-French three model factor Fama-French three model factor

measured by the combination of the market beta such as size Leverage book-to market

equity and price earnings ratio with the cross sectional of expected stock return (Fama