financial results 1h 2016 - bank pekao · pdf file11 471 473 255 253 86 86 1q 16 2q 16...

TRANSCRIPT

FINANCIAL RESULTS 1H 2016

Warsaw, 03.08.2016

Growth in key volumes and core revenues

1

Disclaimer

This presentation (the ”Presentation”) has been prepared by Bank Polska Kasa Opieki Spółka Akcyjna („Bank”) for the clients, shareholders and financial analysts.

This presentation should not be treated as an offer or invitation to purchase any securities or financial instruments or as an advice or recommendation in respect

to such securities or financial instruments.

The presented data are only general information and does not refer to the offered by the Bank products or services. In order to take advantage of the services and

products of the Bank, one should be thoroughly familiar with the characteristics of the particular service or product, its rules, risk and legal and tax consequences

of the use of particular service or product.

The strategy presented in this presentation contains goals which are the ambition of the Management Board and do not constitute any financial results forecast.

Rights for the Presentation as a whole are entitled to the Bank. Presentation is a subject to the protection provided by the law, in particular: the Act dated on

February 4th, 1994 on Copyright and Related Rights (consolidated text in Journal. Laws of 2006, No. 90, item. 631, as amended); the Act dated on July 27th,

2001 on the Databases protection(Journal of Laws No. 128, item. 1402, as amended); the Act dated on April 16, 1993 on Combating Unfair Competition

(consolidated text in Journal of Laws of 2003 , No. 153, item 1503, as amended) and the Act dated on June 30, 2000 on Industrial Property Law (consolidated text

in Journal. Laws of 2003, No. 119, item. 1117 as amended).

This presentation may include forward looking statements, Bank’s outlook for the future, future plans and strategies or anticipated events that are not historical

facts. Since these statements are based on assumptions, expectations, projections and provisional data about future events, the content is inherently uncertain.

Factors that could cause or contribute to differences in current expectations include, but are not limited to: (i) general economic conditions, among which the

economic conditions of the business areas and the markets in which Bank and its subsidiaries operate, (ii) the performance of financial markets (iii) changes in

laws or regulations and (iv) general competitive conditions locally, regionally, nationally and/or internationally.

The Bank does not undertake to publish any updates, modifications or revisions of the information, data or statements contained herein should there be any

change in the strategy or intentions of the Bank, or should facts or events occur that affect the Bank’s strategy or intentions, unless such reporting obligations

arises under applicable laws and regulations.

Bank, nor any of its representatives shall not be responsible for any loss or damage it may arise from the use of this Presentation or of any information contained

herein or otherwise arising in connection to this Presentation.

This presentation is not for the distribution, in or into countries where the public dissemination of the information contained herein may be restricted or prohibited

by law.

2

▪ First half net profit of PLN 1 264m, +1.6% yoy; excluding banking tax PLN 1 465m, +17.8% yoy.

▪ First half core revenues +2.2% yoy, supported by Q2 acceleration +3.5% qoq.

▪ Double digit growth in key retail loans and retail deposits, + 11% yoy and +16% yoy respectively.

▪ Further improvement of NIM, +5bps qoq.

▪ Operational efficiency and effective risk management confirmed.

1H16 highlights

3

Net profit

691

573

1Q 16 2Q 16

+20.4%

- dynamic excluding impact of new banking tax; PLN 201m in H1 2016

1H 15 1H 16

1 244 1 264

+17.8%

PLNm

▪ First half net profit at PLN 1 264m, +1.6% yoy (excluding banking tax PLN 1 465m) with Q2 atPLN 691m, +20.4% qoq supported by commercial acceleration and VISA impact.

▪ ROE at 10.7% with Core Tier I at 18.1%.

+1.6%

4

1 005

1 201

1Q 16 2Q 16

+19.5%

▪ First half operating profit at PLN 2 206m +12.0% yoy, supported by good second quarter.

Gross operating profit

1 9692 206

1H 15 1H 16

+12.0%

PLNm

5

Operating incomePLNm

1 5871 533

284426

1Q 16 2Q 16

+10.8%

1 8172 013

3 1203 052

530710

1H 15 1H 16

+6.9%

3 5823 830

▪ First half core operating income up by +2.2% yoy, supported by strong Q2 results (+3.5%qoq).

▪ Total operating income after 6 months at PLN 3 830m, +6.9% yoy.

Core operating income Other

+3.5% +2.2%

6

1 0821 070

1Q 16 2Q 16

Net interest income (PLNm)

Net interest income and net interest margin

2 058 2 152

1H 15 1H 16

+1.1%

+4.5%

2,76%2,73% 2,73%

2,75%

2,80%

2Q 15 3Q 15 4Q 15 1Q 16 2Q 16

Net interest margin

▪ First half NII at PLN 2 152m, +4.5% yoy, driven by customer volumes.▪ NIM at 2.8% in Q2, +5bps qoq thanks to asset/liabilities mix improvement.

7

25 995

44 29641 851 43 828

25 264 24 695

Jun 15 Mar 16 Jun 16

48 97244 105

47 739

7 634 6 7646 752

Jun 15 Mar 16 Jun 16

Key corporate loans

Loans

+5.8%

+1.1%

Key retail loans Other retail loans

+11.0%

Other corporate loans(*)

+2.6%

(*) excl. BSB and reverse repo transactions

Retail loans (PLNm) Corporate loans (PLNm)

▪ Solid growth in both key retail lending +11.0% yoy and key corporate lending +5.8% yoy.

8

New key retail lending

▪ PLN 3.7bn in new retail loans in the second quarter driven by strong performance ofconsumer loans.

1 5001 659

1Q 16 2Q 16

1 294

2 005

1Q 16 2Q 16

+10.5%+55%

Consumer loans (PLNm) PLN mortgage loans (PLNm)

9

60 10165 362

57 586

Jun 15 Mar 16 Jun 16

Savings

-8.0%

+4.4%

Retail deposits MF

+16.1%

68 174

58 709

65 895

17 723 16 14016 338

Jun 15 Mar 16 Jun 16

+3.5%

(*) excl. SBB and repo transactions

Retail savings (PLNm) Corporate deposits (*) (PLNm)

▪ Double-digit growth in retail deposits +16.1% yoy, supported by strong quarterly performance+3.5% qoq.

▪ Corporate deposits dynamic reflecting tactical approach in safe liquidity management.

10

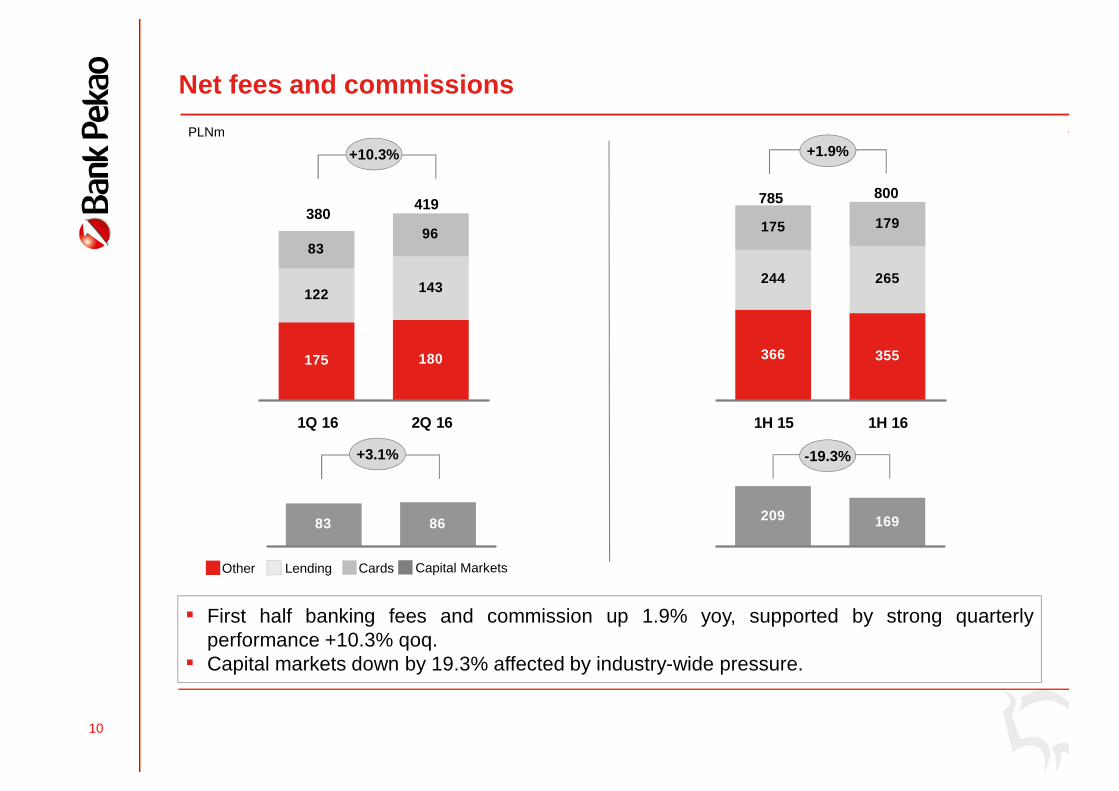

122 143

83

175 180

96

1Q 16 2Q 16

Net fees and commissions

LendingOther Cards Capital Markets

PLNm

▪ First half banking fees and commission up 1.9% yoy, supported by strong quarterlyperformance +10.3% qoq.

▪ Capital markets down by 19.3% affected by industry-wide pressure.

244 265

175

366 355

179

1H 15 1H 16

785 800

+10.3% +1.9%

380419

+3.1%

209 169

-19.3%

83 86

11

471 473

255 253

86 86

1Q 16 2Q 16

Operating costs

812

Non-personel costsPersonnel costs Depreciation

Cost

PLNm

812

952 944

496 509

165 171

1H 15 1H 16

1 613 1 624

+0.7%0.0%

960 996

BFG+ banking tax

Cost incl. BFG, banking tax

148 184

1 750 1 956

138 332

▪ First half operating costs PLN at 1 624m, +0.7% yoy, C/I at 42.4%.▪ Regulatory charges at PLN 332m.

12

2Q 15 1Q 16 2Q 16

8 425

117 517114 538109 653

7 964 8 030

Jun 15 Mar 16 Jun16

Assets quality

Provision coverage ratio

PerformingNPL NPL ratio

Jun 15 Mar 16 Jun 16

6.5%

73.8%

6.4%

Note: Performing loans excl. BSB and reverse repo transactions

Loans (PLNm)

▪ Cost of risk at 47 bp.▪ NPL ratio at 6.4%, coverage ratio at 74.2%.

7.1%

74.2%70.8%

Cost of risk

0.47%0.50% 0.47%

13

Conclusions

� First half net profit of PLN 1 264m, +1.6% yoy, supported by

strong Q2.

� Double digit growth of retail volumes and acceleration in key

corporate lending supporting sound core revenue

generation.

� Achieved results and solid commercial development, with

visible acceleration in Q2, confirm our 2016 single digit

ambition.

14

AGENDA

▪ Appendix

15

Polish economy outlook 2016

Note: Internal macroeconomic scenario

2015 2016F

GDP, % y/y 3.6 3.5

Consumption, % y/y 3.1 4.0

Investments, % y/y 5.8 2.3

Unemployment, % eop 9.8 9.0

CPI, % avg -0.9 -0.6

3M Wibor, % avg 1.72 1.70

Reference rate, % eop 1.50 1.50

Exchange rate EUR, eop 4.24 4.30

Exchange rate USD, eop 3.90 3.91

Public sector balance, % GDP -2.6 -2.9

16

Polish banking sector outlook 2016

(1) all non-mortgage retail loans

(2) Internal scenario

(3) deposits + assets in mutual funds dedicated to retail cliens

(4) assets in mutual funds dedicated to retail clients

2015 2016F(2)

Loans, % y/y 6.8 3,1

Retail, % y/y 6.6 3,7

Mortgage loans PLN 10.4 6,8

Consumer loans(1) 6.8 5,8

Corporate, % y/y 8.1 5,9

SME loans 7,0 4,0

Savings (3)

, % y/y 7,6 6,9

Deposits, % y/y 7.4 7,6

Retail, % y/y 9.4 9,9

Corporate, % y/y 10.3 8,7

Mutual Funds (4)

, % y/y 8,9 0,0

17

Polish economy trendsKey parameters (1)

TRADE BALANCE ACCOUNT (bln EUR)

GDP (% YoY) FIXED INVESTMENTS (% YoY)

PRIVATE CONSUMPTION (% YoY)

Source: Central Statistical Office; March 2007 – June 2016

7,7

1,9

0,90,1 0

0,51,8

2,63,3 3,3 3,3 3,3

3,63,1

3,44,3

33,3

5,3

54,84,94,8

4

3,6

1,5

2,1

4,2

1,92,7

5,5

7,36,9 6,9

4,93,7

2,33,3

-4

-2

0

2

4

6

8

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

101Q

112Q

11

3Q 1

14Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q13

2Q13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

GDP Pr Consumption contribution

Net export contribution Investment contribution

9,66,7

-0,1

-3,2

-4,9-

2,5

-3,5

-0,20,3

12,0

9,69,79,711

,85,8

4,44,4-1

,81,5

10,4

7,8

5,4

0,12,5

24,0

0,7

-9,3

-2,9

-4,7

-0,7

5,3

0,0

5,0

15,9

22,6

19,2

13,014

,5

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

10

1Q 1

12Q

11

3Q 1

14Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

2,4

2,1

0,8

0,2

0 0,2

-0,5

0,7

0,7

2,3

2,9

2,3 2,

8 3,1

3,1

3,1

3 3,2

3,8

66,4

5,96,

34,

9

6

3,2

5,8

42,

63,

6

1,7

2,7

8,2

3,1

2,6

3,7

3,6

3,3

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

10

1Q 1

12Q

11

3Q 1

14Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

-3,4-

2,8-2

,2-1

,2-1

,9-1

,10,50,3

-0,1

-0,8 -0

,4-1

,21,7

0,2-0

,91,11

,20,8

-3,3

-4,1

-2,5

-3,1

-3,5-3

,3

-2,3-2

,0

-2,1-1

,6

-6,5

-5,2

-4,1-3

,8-4

,6-5

,9

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

101Q

112Q

11

3Q 1

14Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

18

4 800,00

4 900,00

5 000,00

5 100,00

5 200,00

5 300,00

5 400,00

5 500,00

5 600,00

5 700,00

5 800,00

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

101Q

11

2Q 1

13Q

11

4Q 1

11Q

12

2Q 1

23Q

12

4Q 1

21Q

13

2Q 1

33Q

13

4Q 1

31Q

14

2Q 1

43Q

14

4Q 1

41Q

15

2Q 1

53Q

15

4Q 1

51Q

16

2Q

Polish economy trendsKey parameters (2)

UNEMPLOYMENT (%)

CORPORATE EMPLOYMENT (ths. eop)

RETAIL SALES (real terms, % YoY)

AVERAGE CORPORATE WAGES (% YoY)

5,47,8

8,99,81

0,111

,812,0

11,0

7,86,3

3,53,43,62,7

3,83,3

4,34,35,25,3

4,6

2,02,23,03,0

4,14,13,53,4

3,93,1

3,63,43,74,0

2,32,6

5,43,8

4Q 0

61Q

07

2Q 0

73Q

07

4Q 0

71Q

08

2Q 0

83Q

08

4Q 0

81Q

09

2Q 0

93Q

09

4Q 0

91Q

10

2Q 1

03Q

10

4Q10

1Q 1

12Q

11

3Q 1

14Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

16

Avg. Corporate Wages CPI

6,98,4

2,71,9-2

,00,01

,53,94,2

5,55,12,6

3,74,23,52,84,84,4

5,7

7,1

8,8

6,0

2,97,3

17,4

1,10,3

3,6

1,01,0

4,8 4,7

8,4

12,114

,012

,816

,111

,8

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

101Q

11

2Q 1

13Q

11

4Q 1

11Q

12

2Q 1

23Q

12

4Q 1

21Q

13

2Q 1

33Q

13

4Q 1

31Q

14

2Q 1

43Q

14

4Q 1

41Q

15

2Q 1

53Q

15

4Q 1

51Q

16

2Q 1

6

12,5

13,3

12,312,4

13,4

14,3

13,2

13,01

3,413,5

12,0

11,411,5

10,2

9,79,8108,8

9,4

10,9

11,6

12,3

11,2

8,9

12,1

9,511

,110

,610,9

13,0

11,7

14,3

12,4

11,5

13,3

11,9

11,8

11,5

1Q 0

72Q

07

3Q 0

74Q

07

1Q 0

82Q

08

3Q 0

84Q

08

1Q 0

92Q

09

3Q 0

94Q

09

1Q 1

02Q

10

3Q 1

04Q

101Q

11

2Q 1

13Q

11

4Q 1

11Q

12

2Q 1

23Q

12

4Q 1

21Q

13

2Q 1

33Q

13

4Q 1

31Q

14

2Q 1

43Q

14

4Q 1

41Q

15

2Q 1

53Q

15

4Q 1

51Q

16

2Q 1

6

Source: Central Statistical Office; March 2007 – June 2016

19

2,0 2,

4

3,5

4,1

3,2 3,

7

2,2

2,9

3,8

4,6

4,1 4,

64,

1

-0,7

-1,5 -0

,9 -0,7 -0,5

-0,9

-0,9

4,5 4,

8 5,0

5,8

3,5

3,5

3,5

3,5

3,5 3,

84,

54,

54,

54,

5 4,8

4,8

4,2

3,33,6

-0,3

0,30,

60,

7

0,5

1,3

2,9

3,94,

0

3,7

4,3

4,7

1,1

2,0

3,0

2,2

1,5

1,5

1,5

1,5

1,5

6,0

6,0

4,3

2,8

2,5 2,5

2,5

2,5

2,5

1,52,0

3,53,5

4,0 5,

03,

8

3,3

1,711,67

1,72

1,731,72

4,2

4,7

5,1 5,

7 6,2 6,7

6,6

5,9

4,4

4,2 4,

34,

13,

9 3,8 4,0 4,

24,

7

4,8

5,0

4,9 5,

14,

94,

1

3,4

2,7 2,7 2,

72,

72,

7

2,12,

3

1,9

1Q 0

7

2Q 0

7

3Q 0

7

4Q 0

7

1Q 0

8

2Q 0

8

3Q 0

8

4Q 0

8

1Q 0

9

2Q 0

9

3Q 0

9

4Q 0

9

1Q 1

0

2Q 1

0

3Q 1

0

4Q10

1Q 1

1

2Q 1

1

3Q 1

1

4Q 1

1

1Q 1

2

2Q 1

2

3Q 1

2

4Q 1

2

1Q 1

3

2Q 1

3

3Q 1

3

4Q 1

3

1Q 1

4

2Q 1

4

3Q 1

4

4Q 1

4

1Q 1

5

2Q 1

5

3Q 1

5

4Q 1

5

1Q 1

6

2Q 1

6

CPI

REF. RATE

3M WIBOR

Polish economy trendsKey parameters (3)

EXCHANGE RATES

INFLATION, INTEREST RATES

Source: NBP

20

8

14 13

26

3338

45

1214

1210

84

03 2 4 5 5 5 6 7 8

51 2

-4

3

14

2428

-40

19 1815 15

3 2 2 0 2

9 8 7

6 4 7

588 9

79

65

-9

1

11

21

31

41

51

4Q 0

24Q

03

4Q 0

44Q

05

4Q 0

64Q

07

4Q 0

84Q

09

4Q 1

04Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

16

Households

Corporate

Banking sector trendsKey parameters - yoy (4)

HOUSEHOLDS AND CORPORATE LENDING (% YoY) HOUSEHOLDS AND CORPORATE DEPOSITS (% YoY)

TOTAL SECTOR LENDING (% YoY) TOTAL SECTOR DEPOSITS (% YoY)

Source: NBP; December 2002 – June 2016

-2 -21

910 11

26

10

14 12 1313

89

8 6 6 5 6 79 8 9

11

2

17

4

10 1012

8

2 2

-8

-1

57

107

5

11 11 1210

8

15

9 10 9

2425 26

14

9

12

7

-9

-4

1

6

11

16

21

26

31

4Q 0

24Q

03

4Q 0

44Q

05

4Q 0

64Q

07

4Q 0

84Q

09

4Q 1

04Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

16

Households

Corporate

4 57 8 8 7

553

13

23

30

36

8 9

1413

119 9

2 4 4 45 5

-30369

121518212427303336

4Q 0

24Q

03

4Q 0

44Q

05

4Q 0

64Q

07

4Q 0

84Q

09

4Q 1

04Q

11

1Q 1

22Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

16

5

8 8 8 8 9 911

667 675

1212

99

15

3-

1010

21

15

13

8

4

-4

2

7

12

17

22

4Q 0

24Q

03

4 Q 0

44Q

05

4Q 0

64Q

07

4Q 0

84Q

09

4Q 1

04Q

11

1Q 1

22 Q

12

3Q 1

24Q

12

1Q 1

32Q

13

3Q 1

34Q

13

1Q 1

42Q

14

3 Q 1

44Q

14

1Q 1

52Q

15

3Q 1

54Q

15

1Q 1

62Q

16

21

-5%

0%

5%

10%

15%

20%

25%

30%

35%

I II III IV V VI VII VIII IX X XI XII

2007 2008 2009 20102011 2012 2013 20142015 2016

Banking sector trendsKey parameters - YTD (5)

HOUSEHOLDS LENDING (% YTD) HOUSEHOLDS DEPOSITS (% YTD)

CORPORATE DEPOSITS (% YTD)CORPORATE LENDING (% YTD)

Source: NBP; January 2007 – June 2016

-5%0%5%

10%15%20%

25%30%35%40%45%50%

XII' I II III IV V VI VII VIII IX X XI XII

2007 2008 20092010 2011 20122013 2014 20152016

-5%

0%

5%

10%

15%

20%

25%

30%

35%

XII' I II III IV V VI VII VIII IX X XI XII

2007 2008 20092010 2011 20122013 2014 20152016

-13%

-8%

-3%

2%

7%

12%

17%

XII' I II III IV V VI VII VIII IX X XI XII

2007 2008 2009 20102011 2012 2013 20142015 2016

22

Banking sector trendsNon-performing loans (6)

11,2%

7,4%

7,3%

11,4

%

11,5

%12,5

%

12,4

%

12,7

%

12,7

%

11,2

% 12,3

%

12,7

%

13,1

%

12,2

% 13,2

%

12,3

%

12,6

%13,4

%14,1%

12,4

%

9,9%

7,6%8,

2%8,8%9,

3%

9,0%9,

4%8,

4%9,1%9,

8%

9,7%

7,6%7,7%

8,7%

9,7%

9,6%

7,5%

6,6%

Mar

09

Sep

09

Mar

10

Sep

10

Mar

11

Sep

11

Mar

12

Sep

12

Mar

13

Sep

13

Mar

14

Sep

14

Dec

14

Mar

15

Jun

15

Sep

15

Dec

15

May

16

May

16

SME Corporate

CORPORATE NPL RATIO

Source: NBP

HOUSEHOLDS NPL RATIO

1,2%1,3%1,4%1,5%1,5%1,6%1,8%

1,9%2,0%2,1%2,2%2,3%2,5%2,6%2,7%2,8% 3,0%

3,0%3,1%

3,1%3,2%

3,2%

3,1%3,4%3,4%

3,3%

2,9%2,9%

2,9%

9,1%10

,0%11,3%

13,1%

14,8%15

,8%16,9%17

,2%18,0%

17,8%18

,2%

18,2%

17,8%

17,9%

17,3

%

16,1%

15,6%

14,7%

14,4

%14

,2%13

,9%12

,8%13

,0%12

,3%12

,2%12

,3%12

,4%12

,2%

2,9%

17,3%17

,8%

Mar

09

Sep

09

Mar

10

Sep

10

Mar

11

Sep

11

Mar

12

Sep

12

Mar

13

Sep

13

Mar

14

Sep

14

Mar

15

Sep

15

Mar

16

Mortgage Cash

4,5%4

,9%

6,0%

6,6%6,7%7,

2%7,

2%7,4%

7,2%7,3%

7,2%7,

5%7,

3%7,5%

7,4%7,5%

7,2%

7,1%

7,0%7,0%

6,9%

6,5%6,

8%6,

6%6,

5%6,

2%6,3%

6,2%7,

1%

Mar

09

Jun

09

Dec

09

Mar

10

Jun

10S

ep 1

0D

ec 1

0

Mar

11

Jun

11S

ep 1

1D

ec 1

1M

ar 1

2

Jun

12S

ep 1

2D

ec 1

2M

ar 1

3Ju

n 13

Sep

13

Dec

13

Mar

14

Jun

14S

ep 1

4

Dec

14

Mar

15

Jun

15S

ep 1

5D

ec 1

5

Mar

16

May

16

Total retail

11,5

%11

,5%

10,7

%11

,2%

11,3

%10

,9%

10,6%

9,8%

9,7%

9,5%

11,4

%

8,4%

9,6%

11,5

%11

,2%12

,2%

12,4

%11

,5%12

,2%

10,9

%10

,7%

10,5%

10,1

%

10,4

%11,1%11,3

%11

,7%

11,8

%11

,8%

Mar

09

Jun

09S

ep 0

9D

ec 0

9M

ar 1

0Ju

n 10

Sep

10

Dec

10

Mar

11

Jun

11S

ep 1

1D

ec 1

1M

ar 1

2Ju

n 12

Sep

12

Dec

12

Mar

13

Jun

13S

ep 1

3D

ec 1

3M

ar 1

4Ju

n 14

Sep

14

Dec

14

Mar

15

Jun

15S

ep 1

5D

ec 1

5M

ar 1

6M

ay 1

6

Total corporate

23

▪ Selected data

24

Consolidated income statement

(4) Operating cost excluding guarantee funds charges (3) Net profit attributable to equity holders of the Bank

(2) Costs excl. guarantee funds charges (1) NII and dividends and other income from equity investments

(5) ROE assuming TCR at 10%(6) NIM calculated based on average daily working assets(7) Loans excluding repo and buy-sell-back transactions, deposits includes only clients liabilities and debt issue excluding reverse repo transactions and sell–buy-back

mln PLN 2Q 15 1Q 16 2Q 16 Q/Q% Y/Y% 1H 2015 1H 2016 Y/Y %

Net interest income (1) 1 043 1 080 1 108 2,6% 6,2% 2 102 2 188 4,1%

Net fee and commission 513 463 505 9,0% -1,6% 994 968 -2,5%

Operating income 1 774 1 817 2 013 10,8% 13,5% 3 582 3 830 6,9%

Operating costs (2) -811 -812 -812 0,0% 0,1% -1 613 -1 624 0,7%

OPERATING PROFIT 963 1 005 1 201 19,5% 24,7% 1 969 2 206 12,0%

Provisions -130 -129 -131 1,4% 0,8% -267 -261 -2,5%

Guarantee funds charges -69 -67 -64 -4,3% -6,6% -138 -131 -4,7%

Banking tax 0 -81 -120 49,1% #DZIEL/0! #ARG! -201 #ARG!

PROFIT BEFORE INCOME TAX 763 729 884 21,3% 15,8% 1 539 1 612 4,8%

Income tax -144 -155 -193 24,4% 34,3% -295 -348 18,2%

GROUP NET INCOME (3) 619 573 691 20,4% 11,5% 1 244 1 264 1,6%

Cost/Income Ratio (%) (4) 45,7% 44,7% 40,3% 4,3 - 5,4 - 45,0% 42,4% 2,6 -

Cost of Risk (%) 0,50% 0,47% 0,47% 0,0 0,0 - 0,51% 0,47% 0,0 -

ROE (%) 10,3% 9,7% 11,7% 2,0 1,4 10,3% 10,7% 0,4

ROE normalised (%) (5) 15,5% 14,9% 18,4% 3,5 2,9 15,4% 16,7% 1,3

ROA (%) 1,5% 1,4% 1,5% 0,1 - 1,5% 1,5% -

TCR (%) - Basel 3 17,8% 18,4% 18,1% 0,3 - 0,3 17,8% 18,1% 0,3

NIM (%) (6) 2,76% 2,75% 2,80% 0,1 0,0 2,80% 2,80% -

L/D (%) (7) 90,7% 94,9% 93,6% 1,3 - 2,9 90,7% 93,6% 2,9

25

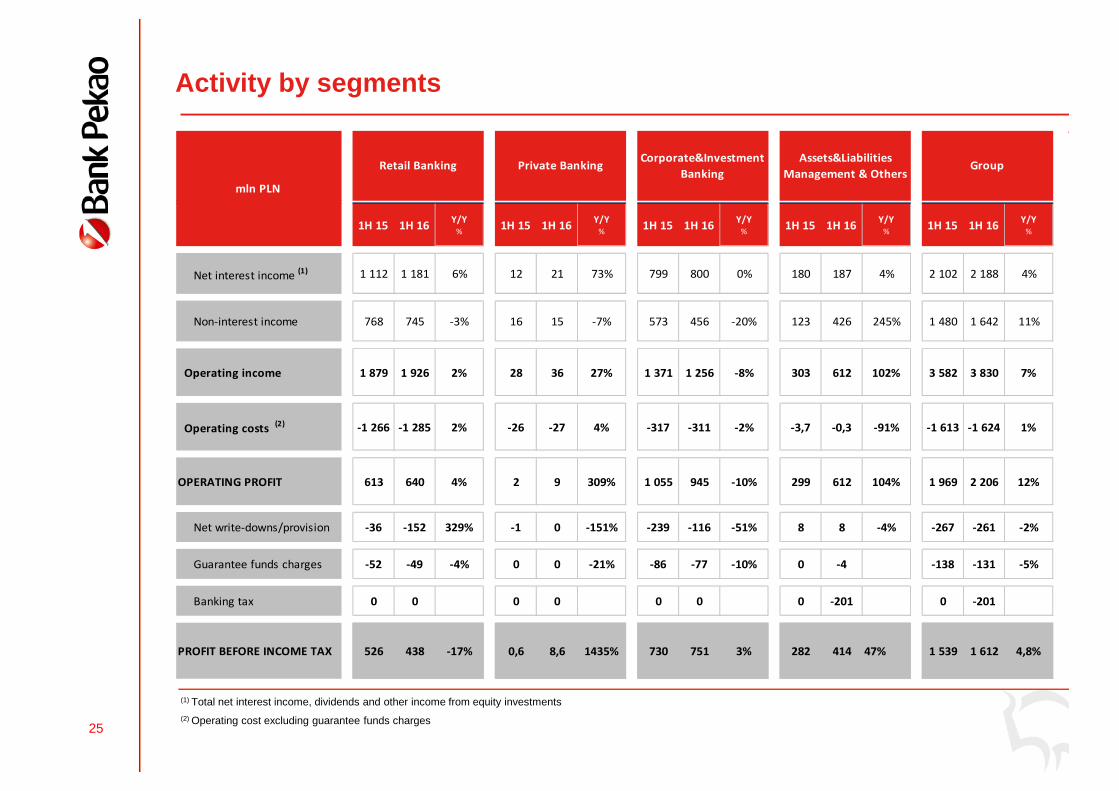

Activity by segments

(1) Total net interest income, dividends and other income from equity investments

(2) Operating cost excluding guarantee funds charges

1H 15 1H 16Y/Y

%1H 15 1H 16

Y/Y

%1H 15 1H 16

Y/Y

%1H 15 1H 16

Y/Y

%1H 15 1H 16

Y/Y

%

Net interest income (1) 1 112 1 181 6% 12 21 73% 799 800 0% 180 187 4% 2 102 2 188 4%

Non-interest income 768 745 -3% 16 15 -7% 573 456 -20% 123 426 245% 1 480 1 642 11%

Operating income 1 879 1 926 2% 28 36 27% 1 371 1 256 -8% 303 612 102% 3 582 3 830 7%

Operating costs (2) -1 266 -1 285 2% -26 -27 4% -317 -311 -2% -3,7 -0,3 -91% -1 613 -1 624 1%

OPERATING PROFIT 613 640 4% 2 9 309% 1 055 945 -10% 299 612 104% 1 969 2 206 12%

Net write-downs/provision -36 -152 329% -1 0 -151% -239 -116 -51% 8 8 -4% -267 -261 -2%

Guarantee funds charges -52 -49 -4% 0 0 -21% -86 -77 -10% 0 -4 -138 -131 -5%

Banking tax 0 0 0 0 0 0 0 -201 0 -201

PROFIT BEFORE INCOME TAX 526 438 -17% 0,6 8,6 1435% 730 751 3% 282 414 47% 1 539 1 612 4,8%

mln PLN

Retail Banking Private BankingCorporate&Investment

Banking

Assets&Liabilities

Management & OthersGroup

26

The structure of the Group net profit

(**) Group net profit attributable to equity holders of the Bank (reported)

NOTE: Data as reported

(*) Entities in liquidation, sold or indirect ownership not presented

mln PLN cumulative

Group's share in

capital % 6M 15 6M 16 Y/Y %

Bank Pekao S.A. Banking - Poland 1 348,8 1 303,9 -3,3%

Entities - consolidated under full method 121,9 53,8 -56%

of which: (*)

Pekao Leasing Sp. z o.o. Leasing 36% 18,8 18,3 -3%

Centralny Dom Maklerski Pekao S.A. Brokerage 100% 23,5 11,6 -51%

Pekao Bank Hipoteczny S.A. Mortgage Bank 100% 3,3 3,2 -3%

Pekao Pioneer PTE S.A. Pension Fund 65% 1,0 0,6 -40%

Pekao Faktoring Sp. z o.o. Factoring 100% 4,0 4,4 10%

Pekao Investment Banking S.A. Brokerage 100% 5,5 10,6 93%

Centrum Bankowości Bezpośredniej Sp. z o.o. Call Centre 100% 0,9 0,8 -11%

Pekao Financial Services Sp. z o.o. Servicing MF/PF 100% 4,1 3,8 -7%

Centrum Kart S.A. Cards 100% -0,3 0,4 -233%

Pekao Fundusz Kapitałowy Sp. z o.o. Business consulting 100% 0,1 0,2 100%

Pekao Property S.A. Real estate development 100% -0,1 -0,2 100%

FPB "MEDIA" Sp. z o.o. Real estate development 100% 0,2 0,1 -50%

Entities - valued under the equity method 30,1 19,8 -34%

Pioneer Pekao Investment Management S.A. Mutual Funds 49% 23,7 18,9 -20%

Krajowa Izba Rozliczeniowa S.A. Clearing Services 5,70% 5,5 0,0 -100%

Dom Inwestycyjny Xelion Sp. z o.o. Financial Advisory 50% 0,9 0,9 0%

Exclusions and consolidation adjustments -257,2 -114,0 -56%

Group Net Profit (**) 1 243,6 1 263,9 1,6%

27

Consolidated balance sheet

(*) Including loans and advances from customers and receivables from finance leases

mln PLN Jun 15 Mar 16 Jun 16Q/Q

%

Y/Y

%

Cash and amounts due from Central Bank 6 682 5 882 5 892 0% -12%

Loans and advances to banks 5 156 2 677 4 351 63% -16%

Loans and advances to customers* 120 814 117 237 120 247 3% 0%

Investment securities 27 362 26 615 26 613 0% -3%

Assets held for sale 63 46 50 8% -21%

Intangible assets 645 615 599 -3% -7%

Tangible fixed assets 1 484 1 429 1 409 -1% -5%

TOTAL ASSETS 170 897 159 695 166 012 4,0% -2,9%

Amounts due to the Central Bank 1 6 6 0% 566%

Amounts due to other banks 8 867 4 636 4 981 7% -44%

Financial liabilities held for trading 81 267 786 194% 872%

Amounts due to customers 125 311 121 819 126 894 4% 1%

Debt securities issued 3 980 2 354 2 085 -11% -48%

Total liabilities 148 779 135 642 143 812 6,0% -3,3%

Total Shareholders' equity 22 118 24 052 22 200 -7,7% 0,4%

28

Customers’ financing

(***) Total customers’ financing includes Loans and advances at nominal value , Securities issued by non monetary entities , reverse repo transactions and buy-sell-back

(*) Including debt securities eligible for rediscounting at Central Bank, net investments in financial leases to customers(**) Securities issued by non monetary entities including local governments

mln PLN Jun 15 Mar 16 Jun 16Q/Q

%

Y/Y

%

YTD

%

Loans* 106 697 109 635 112 525 2,6% 5,5% 2,3%

retail 51 738 54 491 55 737 2% 8% 3%

corporate 54 959 55 144 56 788 3% 3% 1%

Non quoted securities 11 178 12 511 12 623 0,9% 12,9% 2,3%

Other 515 628 612 -3% 19% 14%

Nominal value adjustment 103 282 291 3% 182% 19%

Impairment losses -5 963 -5 879 -5 954 1% 0% 2%

Net loans and advances 120 809 117 233 120 097 2% -1% -2%

Securities issues by non monetary

entities**980 869 879 1,2% -10,3% -1,5%

Reverse repo and buy-sell-back

transactions 8 278 57 149 160,9% -98,2% -96,9%

TOTAL CUSTOMERS’ FINANCING*** 127 132 123 072 126 176 3% -1% -1%

29

Selected data

(***) Pożyczka Ekspresowa (Express Loan)

(*) Number of accounts including pre-paid card accounts (**) Retail clients’ accounts

(*****) Pioneer Pekao Investment Management S.A.(******) Including: Dom Maklerski Pekao (Dom Maklerski), subsidiaryCentralny Dom Maklerski Pekao S.A. (CDM), and associated entity Dom Inwestycyjny Xelion Sp. z o.o. (Xelion)

(****) Credit Union (SKOK) Kopernik included since Dec 2014

Bank Jun 15 Mar 16 Jun 16Q/Q

%

Y/Y

%

YTD

%

Outlets 1 013 959 947 -1,3% -6,5% -2,9%

ATM's 1 789 1 750 1 754 0,2% -2,0% -0,3%

Employees 16 631 16 403 16 258 -0,9% -2,2% -0,8%

No of PLN current accounts (ths)* 5 248 5 338 5 377 0,7% 2,5% 1,2%

No of mortgage loan accounts (ths)** 299 314 319 1,4% 6,7% 2,8%

No of clients holding a consumer loan accounts (ths)*** 578 573 574 0,3% -0,6% -0,3%

Number of individuals with an access to electronic banking Pekao24 (ths) 2 788 2 955 3 019 2,2% 8,3% 4,1%

Number of individuals with an access to mobile banking (ths) 729 1 117 1 243 11,2% 70,5% 22,5%

Number of business clients (SME) with an access to electronic banking systems (ths) 243 250 252 0,8% 3,5% 1,6%

Group Jun 15 Mar 16 Jun 16Q/Q

%

Y/Y

%

YTD

%

Employees**** 18 629 18 315 18 150 -0,9% -2,6% -1,0%

Outlets**** 1 013 959 947 -1,3% -6,5% -2,9%

ATM's**** 1 789 1 750 1 754 0,2% -2,0% -0,3%

Number of MF accounts (ths)***** 894 826 810 -2,0% -9,4% -4,6%

Number of Brokerage accounts (ths)****** 350 346 345 -0,3% -1,5% -0,4%

30

Loans exposure - sectors

Note: Based on the annual Group data including current exposure and commitment

SECTOR DESCRIPTION* 31.12.2013 31.12.2014 31.12.2015 30.06.2016

Wholesale and retail trade; repair of motor vehicles and motorcycles 12,9% 14,2% 15,2% 15,2%

Public administration and defence; compulsory social security 13,0% 11,9% 10,9% 10,9%

Real estate activities 12,6% 10,4% 10,5% 12,0%

Electricity, gas, steam and air conditioning supply 8,8% 9,0% 8,6% 8,0%

Finanace and Insurance activity 5,9% 9,6% 7,8% 3,7%

Transportation and storage 6,3% 6,8% 7,2% 6,8%

Construction 5,8% 5,1% 6,3% 6,7%

Mining and quarrying 3,0% 3,9% 4,4% 3,3%

Manufacture of metals, metal products and machinery 3,8% 3,8% 4,0% 4,8%

Manufacture of beverages and food products 3,4% 3,1% 3,8% 4,0%

Manufacture of chemicals, pharmaceuticals and refined petroleum

products3,8% 2,8% 2,9% 4,5%

Information and communication 4,3% 5,0% 2,7% 2,6%

Manufacture of rubber, plastic and non-metalic products 2,3% 1,9% 2,1% 2,3%

Other manufacturing 5,4% 4,5% 5,2% 5,5%

Other sectors 8,7% 8,0% 8,4% 10,0%

Total 100% 100% 100% 100%

31

Mutual funds

Mutual funds – volumes (mln PLN )

Mutual funds - assets structure (PPIM SA)

Market share (%)

PPIM SA

Third party funds distributed by the Group

Note: Market share – funds distributed by Pekao Group, compared with the market of retail investment funds available for individuals

17 372 16 002 15 812

5 5535 266 5 364

Jun 15 Mar 16 Jun 16

17,3%17,4%18,2%

Jun 15 Mar 16 Jun 16

71%

16%

13%

Equity fundsBalance funds

Money and bonds funds

-0.4%

-7.6%

21 26722 925 21 176

32

Key lending productsStock

35 661 36 808 37 95538 729 39 538

Jun 15 Sep 15 Dec 15 Mar 16 Jun 16

9 4349 0098 9518 7088 444

Jun 15 Sep 15 Dec 15 Mar 16 Jun 16

PLN mortgage loans volumes (mln PLN) Consumer loans volumes (mln PLN)

+2.1%

+10.9% +11.7%

+4.7%

33

50,1%49,9%

Ownership structure

UniCredit GroupMinority shareholders

Before transaction After transaction

40,1%

59,9%

▪ UniCredit Group sold 10% stake on July 12th in successful accelerated book-buildingprocess, keeping after transaction controlling stake of 40.1%.

34

Ratings of Bank Pekao S.A.

FITCH RATINGS PEKAO POLAND

Long-term rating (IDR) A- A-

Short-term rating F2 F2

Viabil ity rating a-

Support rating 2

Outlook Stable Stable

S&P GLOBAL RATINGS* PEKAO POLAND

Long-term rating BBB+ BBB+

Short-term rating A-2 A-2

Stand-alone bbb+

Outlook Negative Negative

MOODY'S INVESTORS SERVICE LTDPEKAO

(unsolicited rating)POLAND

Long-term foreign-currency deposit rating A2 A2

Short-term deposit rating Prime-1 Prime-1

BCA baa1

Outlook Stable/ Negative** Negative

* On April 28, 2016, the name Standard & Poor's Ratings Services was changed to S&P Global Ratings.

** Outlook Stable on rating of liabilities in domestic currency / Negative on rating of liabilities in foreign currenciesBank Pekao S.A. has the highest viability rating assigned by Fitch Ratings, the highest Stand-Alone Credit Profile rating assigned by S&P Global Ratings, and the highest Baseline Credit Assessment as well as long- and short-term counterparty risk ratings assigned by Moody’s Investors Service.

35

Investor relations team’s contact and calendar

Dariusz ChoryłoExecutive Directorph.: +48 22 524 55 27 e-mail: [email protected]

Dorota Faszczewska-Wardph.: +48 22 524 55 30e-mail: [email protected]

Iwona Milewskaph.: +48 22 524 55 28 e-mail: [email protected]

Krzysztof Szlichci ńskiph.: +48 22 524 55 29 e-mail: [email protected]

Visit us at: www.pekao.com.plBlackout Period – two weeks period before publication of financial statements. During this period we do not organise meetings with investors and analysts

Q&A related to the presentation:

CONTACT DETAILS FINANCIAL CALENDAR

9 February 2016

26 April 2016

10 May 2016

20 July 2016

3 August 2016

27 October 2016

10 November 2016

Annual Report 2015 and Webcasting

Start of Blackout Period

First Quarter Report and Webcasting

Start of Blackout Period

Semi-annual Report and Webcasting

Start of Blackout Period

Third Quarter Report and Webcasting