financial results for the first half of 2015 - danske bank · pdf filefinancial results for...

TRANSCRIPT

22 July 2015

Thomas F. Borgen Chief Executive Officer

Financial results for the first half of 2015

Henrik Ramlau-Hansen Chief Financial Officer

2

Financial results for Q1 2013 Financial results for H1 2015

Agenda

Selected topics 7

Appendix 14

Executive summary and financial results 3

Q&A 13

Outlook for full-year 2015 12

Business unit update 5

3

Financial results for Q1 2013 Financial results for H1 2015

Executive summary for H1 2015

Net profit & ROE Net profit of DKK 9.4 bn and ROE of 12.5%

Income Total income of DKK 23.2 bn – up 6% vs H1 2014

Expenses Expenses of DKK 10.8 bn – down 2% vs H1 2014 – and cost/income ratio of 46.4%

Impairments Impairments of DKK 0.3 bn – down 78% vs H1 2014

Capital Common equity tier 1 ratio of 14.3% and total capital ratio of 18.7%

Share buy-back DKK 1.9 bn of the 5 bn share buy-back programme completed

Rating Moody’s upgrade in June to A2/P-1 and stable outlook from S&P in July

Outlook Revised guidance of net profit for 2015 of above DKK 16 bn – previously above DKK 14 bn

4

Financial results for Q1 2013 Financial results for H1 2015

Net profit: DKK 9.4 bn, up 36% from first half of 2014

Income statement & key figures (DKK m) Key points, H1 2015 vs H1 2014

Key points, Q2 2015 vs Q1 2015

• Return on equity improved to 12.5% from 9.4%

• Total income up 6%, with gains in all income lines except NII

• Expenses down 2%, with cost/income ratio of 46.4%

• Impairments down 78%

• Lending volume up 2% and deposit volume up 10%

• NII up 4%, owing partly to one-offs and mitigating effects offsetting margin pressure

• Trading and insurance income down owing to exceptionally strong Q1

• Other income up owing to one-off tax refund

• Expenses down 2%

• Net reversals in Q2: loan loss ratio of –5 bp in core activities

H1 2015 H1 2014 Index Q2 2015 Q1 2015 Index

Net interest income 10,829 10,836 100 5,516 5,313 104

Net fee income 6,134 5,207 118 3,088 3,046 101

Net trading income 4,240 4,152 102 1,525 2,715 56

Other income 866 674 128 506 360 141

Net income from insurance business 1,110 927 120 333 777 43

Total income 23,179 21,797 106 10,968 12,211 90

Expenses 10,750 11,021 98 5,313 5,437 98

Profit before loan impairment charges 12,429 10,776 115 5,655 6,774 83

Loan impairment charges 283 1,267 22 -219 502 -

Profit before tax, core 12,146 9,509 128 5,874 6,272 94

Profit before tax, Non-core 30 -794 - -60 90 -

Profit before tax 12,176 8,715 140 5,814 6,362 91

Tax 2,757 1,791 154 1,346 1,411 95

Net profit 9,419 6,924 136 4,468 4,951 90

Return on avg. shareholders' equity (%) 12.5 9.4 11.8 13.3

Cost/income ratio 46.4 50.6 48.4 44.5

Common equity tier 1 capital ratio (%) 14.3 14.4 14.3 14.0

EPS 9.2 6.9 4.4 4.9

Lending (DKK bn) 1,601 1,566 102 1,601 1,605 100

Deposits (DKK bn) 840 764 110 840 827 102

5

Financial results for Q1 2013 Financial results for H1 2015

Banking units: Strong performance vs H1 2014 at all units

Pre-tax return on allocated capital ex goodwill charge (%) Financial highlights, H1 2015 vs H1 2014

Income statement (DKK m)

Personal Banking

• Lower NII due to substantial pressure on margins • High fee income reflecting strong customer activity • Impairments down 32% as household finances improved

Business Banking

• Higher total income, with gains in all income lines • Net reversals driven by improved collateral values

C&I

• NII up because of higher volumes • Trading and fee income up on increased client activity • Impairments down owing to net reversals in Q2 C&I Business Personal

20.6

10.5

16.7

21.1

13.1 14.5

H1 2015 H1 2014

H1 2015 H1 2014 Index H1 2015 H1 2014 Index H1 2015 H1 2014 IndexNet interest income 4,728 5,343 88 4,537 4,368 104 1,363 1,288 106 Net fee income 2,734 2,186 125 1,139 1,017 112 1,156 1,033 112 Net trading income 416 318 131 442 315 140 2,973 2,212 134 Other income 340 330 103 339 266 127 2 3 88 Total income 8,218 8,177 101 6,457 5,966 108 5,494 4,535 121 Expenses 5,224 5,278 99 2,610 2,649 99 2,284 2,303 99 Profit before loan impairment charges 2,994 2,899 103 3,847 3,317 116 3,210 2,232 144 Loan impairment charges 375 553 68 -103 504 - 11 210 5 Profit before tax 2,619 2,346 112 3,950 2,813 140 3,199 2,022 158

Lending (DKK bn) 806 802 100 652 630 103 179 168 107 Deposits (DKK bn) 353 336 105 259 256 101 230 171 134

Personal Business C&I

6

Financial results for Q1 2013 Financial results for H1 2015

Danske Capital and Danica Pension: Strong performance continued in H1 2015

Danske Capital: Income statement (DKK m) Danica Pension: Income statement (DKK m)

Danica Pension: Financial highlights, H1 2015 vs H1 2014 Danske Capital: Financial highlights, H1 2015 vs H1 2014

• Result from insurance business up 1% owing to larger business volume

• Premiums of DKK 15.5 bn, up 8%

• Risk allowance booked in full for all four interest rate groups

• Shadow account balance unchanged at DKK 0.6 bn

• Total income up 12% owing to increased assets under management and a slight rise in margins

• Assets under management up 4% to DKK 803 bn vs DKK 770 bn in H1 2014

• Net sales of DKK 24 bn, with 21% to clients outside Denmark

• Danske Capital improved its positions in Norway and Sweden, with market shares of net sales increasing to over 20% and 10%, respectively

• In Q1, DKK 37 bn of assets were transferred to Danica Pension as a result of a new investment strategy in Danica

H1 2015 H1 2014 Index

Net interest income -3 1 -

Net fee income 1,150 1,023 112

- portion from performance fees 33 28 118

Other income 1 -1 -

Total income 1,148 1,023 112

Expenses 477 488 98

Profit before tax 671 535 125

Assets under management (bn) 803 770 104

H1 2015 H1 2014 Index

Premiums 15,475 14,364 108

Danica Traditionel (insurance result) 672 710 95

Unit-linked (insurance result) 300 302 99

Health and accident (ins. result) -81 -128 -

Result from insurance business 891 884 101

Return on investments 290 249 116

Financing result -29 -74 -

Special allotments -42 -51 -

Net income bef. postponed risk allow. 1,110 1,009 110

Change in shadow account - -82 -

Net income 1,110 927 120

7

Financial results for Q1 2013 Financial results for H1 2015

Expenses: Down 2% vs H1 2014 despite higher activity, bonuses and one-off pension charge Total expenses ex goodwill charge (DKK m) Change in expenses ex goodwill (DKK m)

90

H1 2015 10,750

Other costs 59

Depreciation, tangibles

122

Office expenses 171

IT 25

Severance payments

Staff costs 28

H1 2014 11,021

762

826

542

873

931 590

694

780

2014

22,641

19,810

2013

23,794

20,627

Other costs

Bonuses

Deposit scheme guarantee / bank packages

Severance payments

Consultants etc.

H1 2015

10,750

9,750

387

350 99

164

8

Financial results for Q1 2013 Financial results for H1 2015

Impairments: Loan loss ratio for Q2 of -5 bp for core activities and -4 bp for the entire Group Group impairments, 2011 to Q2 15 (DKK bn/bp) Impairments (DKK m)

* The loan loss ratio is defined as annualised impairment charges as a percentage of loans and guarantees.

Loan loss ratio, annualised (bp)

-4

26

99

59

-10

0

10

20

30

40

50

60

70

80

90

1005.0

4.5

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

-0.5

Q213 Q214 Q211 Q212

8

Q215

Loan loss ratio* (rhs) Impairments H1 15 H1 14 Index Q2 15 Q1 15 Index

Personal Banking 375 553 68 130 245 53

Business Banking -103 504 - -194 91 -

C&I 11 210 5 -153 164 -

Other activities 1 - - - 1 -

Total core 283 1,267 22 -219 502 -

Non-core -137 380 - -1 -136 -

Group 146 1,647 9 -220 366 -

H1 15 H1 14 Index Q2 15 Q1 15 Index

Personal Banking 9 14 64 6 12 50

Business Banking -3 17 - -12 6 -

C&I - 8 - -13 11 -

Total core 3 14 21 -5 11 -

Non-core -89 179 - -1 -176 -

Group 2 17 12 -4 8 -

9

Financial results for Q1 2013 Financial results for H1 2015

Impairments (continued): Improved credit quality and higher collateral values result in net reversals in Q2 Individual loan impairment charges* (DKK bn)

0.9

Q414

-0.1

Q314

0.8

Q214

0.0

Q115 Q215

-0.3

-2.5

1.5

0.8

Reversal Increased New

Impairment drivers, Q2 2015 vs Q1 2015

• Impairments decreased at all business units, with lower charges at Personal Banking and net reversals at Business Banking and C&I

• The lower impairment level at Personal Banking was driven by housing price increases in major Danish cities

• Reversals at Business Banking related mainly to commercial property, where residential rental property prices improved in Copenhagen

• Impairments at C&I relate to a few individual exposures

3.1

20.0

8.2

40.9

-11%

Q414

40.9

Q314

44.5

Q214

45.7

Q215 Q115

36.3

5.1

Business Banking Non-core

Corporates & Institutions Personal Banking

Allowance account by business unit (DKK bn)

* Excludes Baltics.

10

Financial results for Q1 2013 Financial results for H1 2015

Capital: Solid capital base, CET1 ratio of 14.3%, and Non-core deleveraging reduces REA CET1 ratio, Q1 15 to Q2 15 (%) Capital highlights

• Tier 1 capital ratio and total capital ratio of 16.5 % and 18.7 %, respectively

• Effect of CRR/CRD IV on fully loaded CET1 ratio is a decline of about 1 percentage point from the Q2 2015 ratio level

• CRD IV leverage ratio: 4.2% according to the transitional rules; 3.8% fully phased-in

10

6

?

Pro forma Q4 2015 ex. growth

895

Q1 2015*

-15

Credit risk

-4

Market and CCP models

Market and CCP risk

892

Q2 2015 Optimisation incl. Non-Core approx. 5-15

FSA orders and approvals

approx. 0-5

Growth

REA, Q1 2015 to Q4 2015 (DKK bn)

Q2 2015

14.3

REA impact

0.0

Expected dividends**

0.3

Net profit

0.6

Q1 2015*

14.0

* Adjusted for change in accounting for pension schemes at Danica Pension. ** 50% dividend accrual.

Core Non-core

11

Financial results for Q1 2013 Financial results for H1 2015

Business review: New operating model for Danske Bank Northern Ireland Business review findings Our Northern Irish branch network

Beginning in January 2016, Danske Bank Northern Ireland will operate as a separate business unit

Only limited operational synergies and customer interactions with the rest of the Group

More efficient operation as a stand-alone business

Enables local management to develop and protect the franchise for the benefit of customers

Continues to benefit from group cost efficiency

Strengthens the Nordic universal bank organisation

46 branches

20 % market share by lending

12

Financial results for Q1 2013 Financial results for H1 2015

Note: This guidance is subject to uncertainty and depends on economic conditions, including developments in monetary policy at central banks.

Total income Income is expected to increase from the level in 2014

Expenses Expenses are expected to be below DKK 22 bn

Impairments Impairment charges in our core activities are expected to decline to a level significantly lower than in 2014

Non-core Non-core pre-tax result is expected at around DKK 0 million

Net profit Net profit of above DKK 16 bn

Outlook for full-year 2015: Net profit of above DKK 16 bn

13

Financial results for Q1 2013 Financial results for H1 2015

Q&A session

www.danskebank.com/ir

Press * then 1 to ask a question Press * then 2 to cancel

Press “Ask a question” in your webcast player

14

Financial results for Q1 2013 Financial results for H1 2015

Appendix

Funding, liquidity and ratings 30

Business units 15

Tax 33

Macro, credit quality and portfolio reviews 25

Special topics: NII, trading income, expenses and allowance account 20

Contact details 34

15

Financial results for Q1 2013 Financial results for H1 2015

Personal Banking: Positive momentum in fees, impairments and costs in Q2; good trend in Norway continues Income statement & key figures (DKK m) Lending volume by country,* Q1 2014 = Index 100

Profit before tax by country (DKK m)

90

100

110

120

130

Q2 2015 Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014

Northern Ireland

Norway

Sweden

Finland

Denmark

* Based on local currency lending volumes. ** Includes day effect, FX effect, capital costs and off-balance-sheet items

Q2 2015

1,322

Q1 2015

1,298

Q4 2014

929

Q3 2014

1,373

Q2 2014

1,315

Denmark

Finland

Sweden

Norway

Northern Ireland

Other

Personal Banking NII bridge (DKK m)

Q2 2015 Q1 2015 IndexNet interest income 2,330 2,398 97 Net fee income 1,383 1,351 102 Net trading income 148 268 55 Other income 187 153 122 Total income 4,048 4,170 97 Expenses 2,597 2,627 99 Profit before loan impairment charges 1,451 1,543 94 Loan impairment charges 130 245 53 Profit before tax 1,322 1,298 102

Lending (DKK bn) 806 808 100 Deposits (DKK bn) 353 335 105 FTE 6,695 6,713 100

707

4,728

H1 15 Other**

7

Lending volume

4

H1 14

5,343

Deposit margin

Deposit volume

4

Lending margin

77

16

Financial results for Q1 2013 Financial results for H1 2015

Business Banking: Positive trend in income, costs and impairments in Q2; good momentum in Nordic lending Income statement & key figures (DKK m)

Profit before tax by country (DKK m)

* Based on local currency lending volumes. ** Includes day effect, FX effect, capital costs and off-balance-sheet items

Lending volume by country,* Q1 2014 = Index 100

90

100

110

120

130

Q2 2014 Q1 2014 Q2 2015 Q1 2015 Q4 2014 Q3 2014

Northern Ireland

Norway

Sweden

Finland

Denmark

Q2 2015

2,182

Q1 2015

1,769

Q4 2014

1,465

Q3 2014

1,455

Q2 2014

1,541

Denmark

Finland

Sweden

Norway

Northern Ireland

Baltics

Other

Business Banking NII bridge (DKK m)

Q2 2015 Q1 2015 IndexNet interest income 2,313 2,224 104 Net fee income 567 572 99 Net trading income 230 212 108 Other income 165 174 95 Total income 3,275 3,182 103 Expenses 1,288 1,322 97 Profit before loan impairment charges 1,988 1,860 107 Loan impairment charges -194 91 -Profit before tax 2,182 1,769 123

Lending (DKK bn) 652 644 101 Deposits (DKK bn) 259 262 99 FTE 3,065 3,115 98

143

253 33499

H1 15

4,537

Other** Deposit margin

Deposit volume

9

Lending margin

Lending volume

H1 14

4,368

17

Financial results for Q1 2013 Financial results for H1 2015

Corporates & Institutions: NII up 6%; trading income down after exceptional Q1 Income statement & key figures (DKK m) Key points, Q2 15 vs Q1 15

Income breakdown (DKK m)

Q215

2,523

Q115

2,971

Q414

2,103

Q314

2,483

Q214

2,201

General Banking Capital Markets FICC

• Profit before tax down 6% after exceptionally strong Q1

• Trading income in Q2 in line with expectations as we managed the risks from interest rate increases

• Expenses down 3%

• Impairments driven by reversals

• The expected decline in capital consumption was delayed slightly as volatile market conditions continued

Corporates & Institutions NII bridge (DKK m)

Q2 2015 Q1 2015 IndexNet interest income 703 660 106 Net fee income 580 577 100 Net trading income 1,240 1,732 72 Other income - 2 - Total income 2,523 2,971 85 Expenses 1,126 1,158 97 Profit before loan impairment charges 1,398 1,813 77 Loan impairment charges -153 164 -Profit before tax 1,551 1,649 94

Lending (DKK bn) 179 190 94 Deposits (DKK bn) 230 230 100 FTE 1,832 1,826 100

141

90 77

105 1,363

H1 15 Other** Deposit margin

Deposit volume

Lending margin

25

Lending volume

H1 14

1,288

* Based on local currency lending volumes. ** Includes day effect, FX effect, capital costs and off-balance-sheet items

18

Financial results for Q1 2013 Financial results for H1 2015

Danske Capital: AuM down 1% in Q2 because of value adjustments despite good inflow Income statement (DKK m)

Net inflow – AuM (DKK bn)

0

5

10

15 2.5

2.0

1.5

1.0

0.5

0.0

Q314

1.1%

8.5

Q214

1.0%

7.7

Q215

12.3

1.5%

Q115

1.4%

11.4

Q414

0.8%

6.2

Net inflow as % of AuM (rhs) Net inflow

Key points, Q2 15 vs Q1 15

* Retail includes Danske Invest.

159

340

288

Q115 Q414 Q314 Q214 Q215

16 Life insurance Institutions

Retail* Private Equity

AuM — customer breakdown (DKK bn)

• Non-performance-based income up 2%

• Performance fee income of DKK 19 m vs DKK 14 m in Q1 15

• Expenses down 5% because of lower staff costs

• Assets under management down 1% to DKK 803 bn

Q2 2015 Q1 2015 Index

Net interest income -1 -2 -

Net fee income 583 567 103

- portion from performance fees 19 14 136

Other income -1 2 -

Total income 581 567 102

Expenses 233 244 95

Profit before tax 349 323 108

Assets under management (bn) 803 813 99

19

Financial results for Q1 2013 Financial results for H1 2015

Q2 2015 Q1 2015 Index

Premiums 7,122 8,353 85

Danica Traditionel (insurance result) 339 333 102

Unit-linked (insurance result) 147 153 96

Health and accident (ins. result) -45 -36 -

Result from insurance business 441 450 98

Return on investments -70 360 -

Financing result -17 -12 -

Special allotments -21 -21 -

Net income bef. postponed risk allow. 333 777 43

Change in shadow account - - -

Net income 333 777 43

Danica Pension: Full risk allowance booked for all four interest rate groups; investment return down owing to volatile market Income statement (DKK m) Investment allocation for Danica Traditionel, end-Q2 15 (%)

14 11 8

7 109

16

2111

148

49 6660

65

9 10

7

High

3

Medium Low

2

New schemes

Alternative investments Credit bonds

Property Bonds

Equities

% c

han

ge in

eq

uit

ies

Percentage point change in interest rates

Possibility of booking risk allowance in 2015 (%)

-25%

25%

-1,00% 0,00% 1,00%

Full risk allowance

Partial risk allowance

20

Financial results for Q1 2013 Financial results for H1 2015

Non-core: Commercial portfolio is almost run down; REA decline owing mainly to the sale of the SME portfolio

Property pipeline and sales (No. of properties)

Key points Non-core loan portfolio, Q2 2015 (DKK bn)

Total REA (DKK bn)

• Profit before tax rose to DKK 30 m in H1 2015 compared with a loss before tax of DKK -794 m in H1 2014

• Deleveraging of the commercial portfolio is almost complete, with DKK 2 bn left in net credit exposure

• Total loans decreased DKK 12 bn since H1 2014, although exposure to Personal Banking Baltics was transferred to the book in Q1 15

• REA fell DKK 15 bn from the level in Q1 15 owing to the sale of the SME portfolio and continuing deleveraging of the portfolio

28 31 35 37 27

2130

8

75

Total

42

Conduits etc.

9

Commercial portfolio

4

1

Personal customers

(incl. Baltics)

29

Performing credit exposure

Non-performing credit exposure

Allowance account

789

523 470

908

348405626

Sold

1,423

Agreed to sale On the market

1,634

2014 2013 H1 2015

34 33 33 36

23

9 8 8

7

8

Q414

42

Q314

41

Q215

Q115

45 42

Q214

-33%

30

Non-core conduits, etc.

Non-core Banking

21

Financial results for Q1 2013 Financial results for H1 2015

Net interest income: Flat vs. H1 2014 as lending effects and repayment of the state hybrid offset deposit margin pressure Quarterly net interest income (DKK m) Changes in net interest income (DKK m)

Balance sheet items (DKK bn)

-3%

Q215

5,516

Q115

5,313

Q414

5,742

Q314

5,735

Q214

5,681

271

355

288

H1 15 10,829

Other* 94

State hybrid

Deposit margin 1,118

Deposit volume 103

Lending margin

Lending volume

H1 14 10,836

840

820

800

780

760

0

1,610

1,600

1,590

1,580

1,570

0

Q215 Q115 Q414 Q314 Q214

Deposits (rhs) Loans and advances

* Contains FX effect, hold-to-maturity portfolio and a DKK 77 m one-off income in Q2 15 related to interest on a refund of payroll tax

22

Financial results for Q1 2013 Financial results for H1 2015

Trading income: Lower customer activity in financial markets and negative value adjustments in Q2 Trading income by business unit (DKK m) Key points

Refinancing income (DKK m)

Q115

2,715

Q414

928

Q314

1,613

Q214

2,251

Q215

1,525

Personal Business C&I Other incl. Treasury • Trading income down in Q2 owing to lower customer activity in financial markets

• Income from Treasury lower because of unrealised negative value adjustments on bonds

• Personal Banking and Business Banking benefitted from DKK 141 m in refinancing fees in Q1

Q4 2014

Q1 2015

141

186

Q1 2014

148

Q4 2013

242

Q1 2013

138

23

Financial results for Q1 2013 Financial results for H1 2015

Expenses: Down 2% because of continued cost focus and lower bonuses in Q2

Change in expenses ex goodwill (DKK m) Total expenses ex goodwill charge (DKK m)

82

45

Q2 2015 5,313

Other costs 41

IT

Severance payments

Bonuses 102

Staff costs ex. bonuses and severance

108

Q1 2015 5,437

Q1 15

5,437

4,867

Q4 14

6,090

5,174

Q3 14

5,530

4,861

Q2 14

5,589

4,921

Q2 15

5,313

4,882

Other costs

Deposit guarantee scheme/bank packages

Bonuses

Severance payments

Consultants etc.

24

Financial results for Q1 2013 Financial results for H1 2015

Allowance account: Commercial property and personal customers make up 52% of the individual allowance account

* In addition, the Group has booked DKK 5.7 bn in collective impairment charges. Note: Non-performing loans are loans in rating categories 10 and 11 against which individual impairments have been made.

Gross non-performing loans, ex Non-core (DKK bn)

1.4

Transportation

8.3

Consumer staples

7.6

Investment funds

2.6

Non-profit & associations

2.4

Materials

2.0

Industrial services etc

1.8 Construction & building products

1.5

Shipping

1.2

Consumer discretionary

1.0

Agriculture

0.4

Commercial property

0.3

Personal customers

0.2

Other

Individual allowance account by industry* (DKK bn)

9 9 11 11 11

19 19 19 19 18

31 31 29 3027

60

Q215

56

Q115

59

Q414

58

Q314

60

Q214

Net exposure, Not in default

Individual allowance account

Net exposure, In default

25

Financial results for Q1 2013 Financial results for H1 2015

90

100

110

120

130

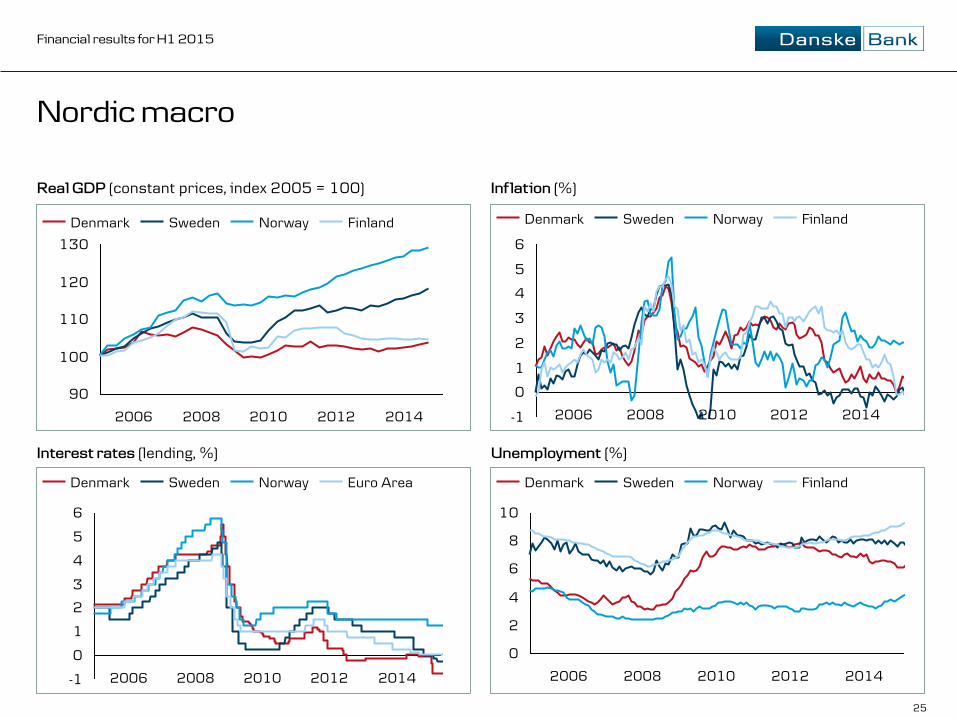

Nordic macro

Real GDP (constant prices, index 2005 = 100) Inflation (%)

Interest rates (lending, %) Unemployment (%)

2014 2008 2010 2006 2012

Finland Norway Sweden Denmark

0

2

4

6

8

10

2014 2012 2010 2008 2006

Finland Norway Sweden Denmark

-1

0

1

2

3

4

5

6

2014 2012 2010 2008 2006

Finland Norway Sweden Denmark

-1

0

1

2

3

4

5

6

2014 2012 2010 2008 2006

Denmark Euro Area Norway Sweden

26

Financial results for Q1 2013 Financial results for H1 2015

Nordic housing market

Apartment prices (index 2005 = 100) Apartment prices/nom. GDP (index 2005 = 100)

130

120

110

100

90

2014 2012 2010 2008 2006

Sweden Finland Norway Denmark

100

140

180

120

160

200

2010 2014 2008 2012 2006

Norway Denmark Sweden Finland

Property prices (index 2005 = 100) House prices/nom. GDP (index 2005 = 100)

2012 2006 2008

100

150

200

250

2014 2010

Sweden Denmark Finland Norway

100

2014 2006

80

180

2012

120

2008

140

160

2010

Denmark Sweden Norway Finland

27

Financial results for Q1 2013 Financial results for H1 2015

Realkredit Danmark and the Danish housing market: Portfolio overview Portfolio facts, Realkredit Danmark, end-Q2 15

Unemployment and foreclosures (%) Trend in mortgage margins, 80% LTV, owner-occupied (bp)

• Approx. 377,000 loans (residential and commercial)

• 2,131 loans in 3- and 6-month arrears

• 67 repossessed properties

• DKK 14 bn of loans with LTV ratio > 100%, including DKK 6 bn with public guarantee

• Average LTV ratio of 68%

LTV ratio at origination (legal requirement)

• Residential: max. 80%

• Commercial: max. 60%

52

68

86

101

118Adjustable rate Fixed rate All products

2011 Jan13: with amortisation Jan 13: interest-only

+ r

efin

anci

ng

fee*

+ r

efin

anci

ng

fee*

* We charge a fee of 30 bp of the bond price for refinancing of 1- and 2-year floaters and a fee of 20 bp for floaters of 3 or more years .

Stock of retail loans, Realkredit Danmark, end-Q2 15 (%)

8%

41%

26%

25%

Fixed rate interest-only

Variable rate interest-only

Fixed rate instalments

Variable rate instalments

0

5

10

0

500

1,000

1,500

No. of forced sales (rhs) 10Y swap rate

Unemployment

1997 2002 2006 2010 1993 2015

28

Financial results for Q1 2013 Financial results for H1 2015

Realkredit Danmark: Increase in fixed-rate loans driven by very low interest rates

* Based on the assumption that the portion of interest-only mortgages of new loans is unchanged and that the observed trend in customers who start to amortise at the end of the IO period continues.

Expected trend in RD portfolio* (%)

Loan portfolio, FlexLån F1 and F2 (DKK bn)

191160

130109 99 8090

-58%

Q1 15

Q4 14

Q3 14

107

Q2 14

Q1 14

111

Q4 13

Q3 13

161

Q2 13

Q1 13

169

Q4 12

Q2 15

Key points

• Trend away from short-term Flexlån® continued in Q2 2015

• The share of total new mortgages represented by fixed-rate instalment loans increased to 57% in Q2 2015 from 36% in Q2 2014

• Since end-Q4 2012, the amount of Flexlån® F1 and F2 loans has been reduced by DKK 111 bn, or 58%

50 50 51 52 53 54 56

50 50 49 48 47 46 44

2020E 2019E 2018E 2017E 2016E 2015E 2014

Interest-only Amortising

29

Financial results for Q1 2013 Financial results for H1 2015

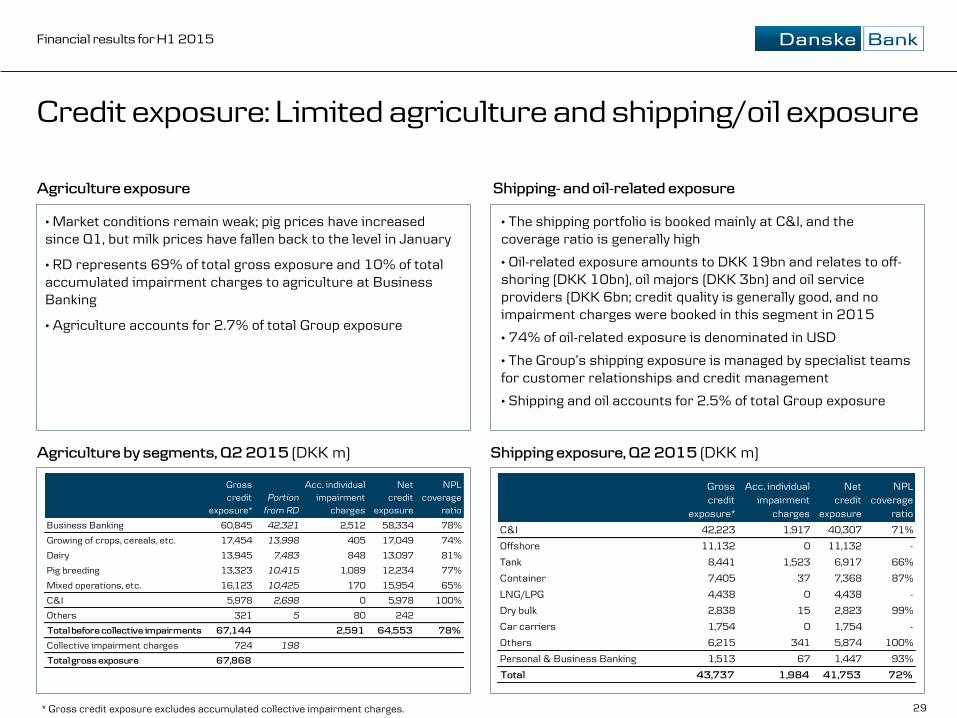

Credit exposure: Limited agriculture and shipping/oil exposure

Shipping- and oil-related exposure

Agriculture by segments, Q2 2015 (DKK m)

• Market conditions remain weak; pig prices have increased since Q1, but milk prices have fallen back to the level in January

• RD represents 69% of total gross exposure and 10% of total accumulated impairment charges to agriculture at Business Banking

• Agriculture accounts for 2.7% of total Group exposure

Shipping exposure, Q2 2015 (DKK m)

Agriculture exposure

• The shipping portfolio is booked mainly at C&I, and the coverage ratio is generally high

• Oil-related exposure amounts to DKK 19bn and relates to off-shoring (DKK 10bn), oil majors (DKK 3bn) and oil service providers (DKK 6bn; credit quality is generally good, and no impairment charges were booked in this segment in 2015

• 74% of oil-related exposure is denominated in USD

• The Group’s shipping exposure is managed by specialist teams for customer relationships and credit management

• Shipping and oil accounts for 2.5% of total Group exposure

Grosscredit

exposure*Portion

from RD

Acc. individualimpairment

charges

Netcredit

exposure

NPLcoverage

ratio

Business Banking 60,845 42,321 2,512 58,334 78%

Growing of crops, cereals, etc. 17,454 13,998 405 17,049 74%

Dairy 13,945 7,483 848 13,097 81%

Pig breeding 13,323 10,415 1,089 12,234 77%

Mixed operations, etc. 16,123 10,425 170 15,954 65%

C&I 5,978 2,698 0 5,978 100%

Others 321 5 80 242

Total before collective impairments 67,144 2,591 64,553 78%

Collective impairment charges 724 198

Total gross exposure 67,868

Grosscredit

exposure*

Acc. individualimpairment

charges

Netcredit

exposure

NPLcoverage

ratio

C&I 42,223 1,917 40,307 71%

Offshore 11,132 0 11,132 -

Tank 8,441 1,523 6,917 66%

Container 7,405 37 7,368 87%

LNG/LPG 4,438 0 4,438 -

Dry bulk 2,838 15 2,823 99%

Car carriers 1,754 0 1,754 -

Others 6,215 341 5,874 100%

Personal & Business Banking 1,513 67 1,447 93%

Total 43,737 1,984 41,753 72%

* Gross credit exposure excludes accumulated collective impairment charges.

30

Financial results for Q1 2013 Financial results for H1 2015

Funding and liquidity: 36 bn of long-term funding issued in H1; 45 bn of funding up for redemption in H2

64

39

95

73

2015E

50-70

36

2014 2013 2012 2011

Completed

Funding plan

133125 129 131 130

100

125

150

110***

Q2 15 Q1 15 Q4 14 Q3 14 Q2 14

* Spread over 3M EURIBOR. **LCR is calculated in accordance with the Danish FSA’s specifications and includes holdings of covered bonds and Danish mortgage bonds, including own issued bonds. ***Minimum requirement of the Danish FSA.

Changes in funding , 2015 (DKK bn and bp*)

Liquidity coverage ratio** (%)

Long-term funding ex RD (DKK bn)

6 52

1013

6

New H1 2015: DKK 36bn

574bp

37bp

11bp 21

Redeemed H1 2015: DKK 20bn

55bp

80bp

73bp

0

Redemptions 2015: DKK 65bn

0

62bp

107bp

51bp

33 26

Tier 1 Tier 2 Senior Cov. bonds

2018: DKK 52 bn

0

191bp

54bp

42bp

12 15

26

2017: DKK 58 bn

65bp

0

103bp

49bp

13

27

18

2016: DKK 60 bn

0 0

97bp 93bp

32 29

Maturing funding, 2016-18 (DKK bn and bp*)

Senior Tier 1 Tier 2 Cov. bonds

31

Financial results for Q1 2013 Financial results for H1 2015

Funding: Structure and sources; Danish mortgage system is fully pass-through Loan portfolio and long-term funding, Q2 15 (DKK bn)

740740

192319

840542

114

Issued RD bonds

Bank mortgages

RD mortgages

Covered bonds

Deposits Bank loans

Senior debt

Funding

1,886

Loans

1,601

Funding sources (%)

Short-term funding Long-term funding

9

2

11

6

47

18

1

6

Rep

os

CD

& C

P

Co

vere

d

bo

nd

s

Eq

uit

y

Su

bo

rd.

deb

t

Dep

osi

ts

cred

it in

st.

Dep

osi

ts

Sen

ior

u

nse

cure

d

Q2 2015 Q1 2015

32

Financial results for Q1 2013 Financial results for H1 2015

Three distinct methods of rating banks

Individual Rating/Viability Rating

Support Rating/Support Rating Floor

Issuer Default Rating (IDR)

IDR is the higher of the Viability Rating and the Support Floor

a

A-

A

(Stable)

Danske Bank’s rating

* Stand-Alone Credit Profile. ** Baseline Credit Assessment. *** Loss Given Failure.

Rating methodology

Anchor SACP*

Extraord. Support

Add. factors

Issuer Rating

+ + + = + + +

bbb+ +1 0 0 0 0 0 A

(Stable)

SACP

a-

= 1 2 3 4

1=Business Position 2=Capital & Earnings 3=Risk Position 4=Funding & Liquidity

ALAC

+1

+

Macro Profile

Quali- tative

Factors

Gov. Support

Issuer Rating + =

Strong

Plus

baa1 a1 baa2 ba1 0 +1

+ 1 2 3 4

1=Asset Risk 2=Capital 3=Profitability 4=Funding Structure 5=Liquidity Resources

BCA**

Baa1 a3

5

A2

(Stable)

+ LGF***

+1

+ + + + = Affiliate Support

0

+ +

33

Financial results for Q1 2013 Financial results for H1 2015

Tax

Tax drivers Actual and adjusted tax rates (DKK m)

• The difference between profit before tax and adjusted pre-tax profit relates mainly to previous years’ losses in Ireland

• Further, permanent non-taxable difference derives mainly from tax-exempt dividends and value adjustments of shares

Q22015 Q12015 Q42014 Q32014 Q22014

Profit before tax 5,814 6,362 -5,298 4,503 5,000

Ireland core and non-core -206 -433 434 79 87

Permanent non-taxable difference -278 20 8,969 45 -1,240

Adjusted pre-tax profit, Group 5,330 5,949 4,105 4,627 3,847

Tax according to P&L 1,346 1,411 987 1,231 953

Taxes from previous years -107 33 44 -60 -5

Adjusted tax 1,240 1,445 1,031 1,171 948

Adjusted tax rate 23.3% 24.3% 25.1% 25.3% 24.6%

Actual tax rate 23.2% 22.2% N/A 27.3% 19.1%

34

Financial results for Q1 2013 Financial results for H1 2015

Contacts

Henrik Ramlau-Hansen Direct: +45 45 14 06 66 Chief Financial Officer Mobile: +45 22 20 73 10 [email protected]

Claus Ingar Jensen Direct: +45 45 12 84 83 Head of IR Mobile: +45 25 42 43 70 [email protected]

John Bäckman Direct: +45 45 14 07 92 Chief IR Officer Mobile: +45 30 51 46 85 [email protected]

Robin Hjelgaard Løfgren Direct: +45 45 14 06 04 IR Officer Mobile: +45 24 75 15 40 [email protected]

Louisa Grue Baruch Direct: +45 45 13 92 34 IR Officer Mobile: +45 21 56 19 35 [email protected]

35

Financial results for Q1 2013 Financial results for H1 2015

Disclaimer

Important Notice

This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Danske Bank A/S in any jurisdiction, including the United States, or an inducement to enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. The securities referred to herein have not been, and will not be, registered under the Securities Act of 1933, as amended (“Securities Act”), and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Securities Act. This presentation contains forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Danske Bank believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors many of which are beyond Danske Bank’s control. This presentation does not imply that Danske Bank has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.