financial services industry: a primer

TRANSCRIPT

DERAYAH’S DIRECTION

Investment Outlook

3rd Quarter, 2010

CONTENTS

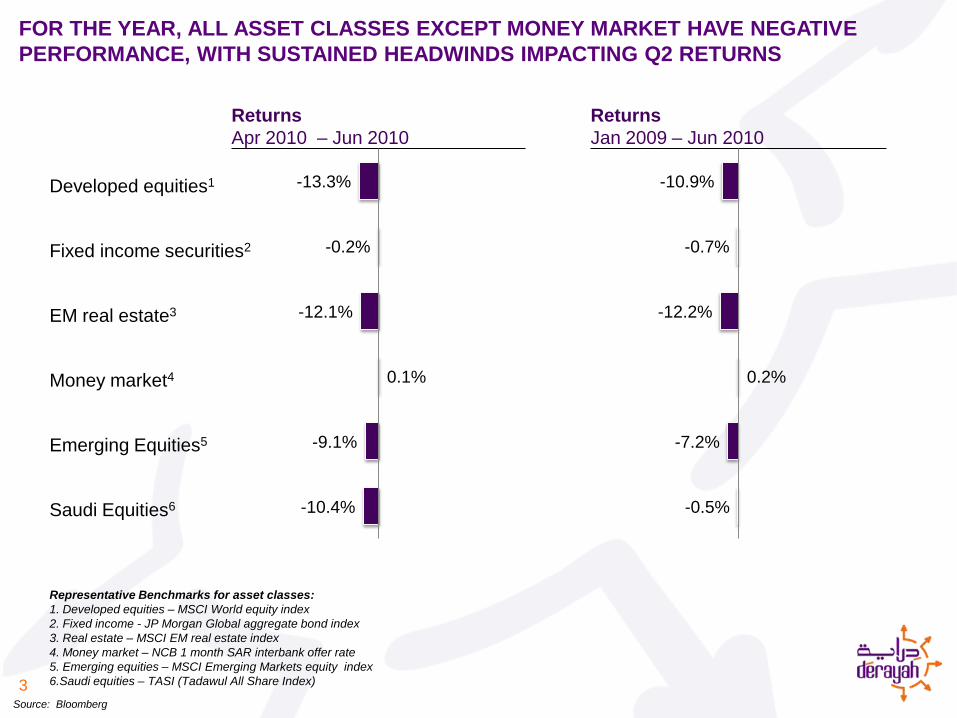

Summary of market performance for the last quarter1

2

Outlook for various asset classes2

Derayah’s recommended asset allocation3

3

Returns

Apr 2010 – Jun 2010

-13.3%

-0.2%

-12.1%

0.1%

-9.1%

-10.4%

Developed equities1

Fixed income securities2

EM real estate3

Money market4

Emerging Equities5

Saudi Equities6

-10.9%

-0.7%

-12.2%

0.2%

-7.2%

-0.5%

Returns

Jan 2009 – Jun 2010

Representative Benchmarks for asset classes:

1. Developed equities – MSCI World equity index

2. Fixed income - JP Morgan Global aggregate bond index

3. Real estate – MSCI EM real estate index

4. Money market – NCB 1 month SAR interbank offer rate

5. Emerging equities – MSCI Emerging Markets equity index

6.Saudi equities – TASI (Tadawul All Share Index)

Source: Bloomberg

FOR THE YEAR, ALL ASSET CLASSES EXCEPT MONEY MARKET HAVE NEGATIVE

PERFORMANCE, WITH SUSTAINED HEADWINDS IMPACTING Q2 RETURNS

4

-10.4%

-24.7%

-7.5%

-13.1%

-9.7%

-9.5%

1.0%

-22.9%

-13.4%

-11.9%

-13.4%

-15.4%

US

(S&P 500)

UK (FTSE

100)

Japan

(Nikkei 225)

India

(BSE Sensex)

China

(Shanghai)

Brazil

(IBOV Index)

Saudi Arabia

(Tadawul)

UAE

(DFM 20)

Qatar

(DSM 20)

Kuwait

(KWSEIDX)

Bahrain

(BHSEASI)

Oman

(MSM 30)

Apr 2010 – Jun 2010 Jan 2010 – Jun 2010

De

ve

lop

ed

Em

erg

ing

GC

C

Percent returns

-0.5%

-23.9%

-0.9%

-6.6%

-4.2%

-4.9%

1.4%

-26.8%

-11.2%

-7.6%

-9.2%

-11.0%

Source: Bloomberg

GLOBALLY, EQUITY MARKETS HAVE PROVIDED NEGATIVE RETURNS, INDIA

BEING THE ONLY EXCEPTION

5

OVER THE LONG TERM, LOCAL EQUITIES (FOLLOWED BY EMERGING EQUITIES)

HAVE BEEN AT THE FOREFRONT OF CREATING INVESTOR WEALTH

Indexed returns of various asset classes for the last 21 years from earliest available date

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

(Compounded annual returns)

CAGR

Value of 100 invested in June 1989

8.81%

Emerging Equity1 8.57%

Local Equity2

6.95%Fixed Income3

3.61%Developed Equity4

2. 73%Money Market5

Real Estate6 -4.63%

Representative Benchmarks for asset classes:

1.Emerging equities – MSCI EM Equities Index

2. Local equities – Tadawul All Shares (TASI) Index

3. Fixed JP Morgan Global aggregate bond index

4 Developed Equity – MSCI World Index

5. Money market – NCB 1 month interbank offer rate

6. Real Estate – MSCI Emerging Market Real Estate Index

CONTENTS

Summary of market performance for the last quarter1

6

Outlook for various asset classes2

Derayah’s recommended asset allocation3

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/ Sukuk

DERAYAH TACTICAL ASSET ALLOCATION

7

Fixed Income

(Sukuk)

Moderate Overweight

Developed

Equity

Moderate Overweight

++Emerging

Equity

Overweight

Money Markets Underweight

---

Regional

Real Estate

Moderate Underweight

--

Asset class Recommendation Comments

++

GCC

Equity

Moderate Overweight

++

+++

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

8

Outlook for various asset classes2

Derayah’s recommended asset allocation3

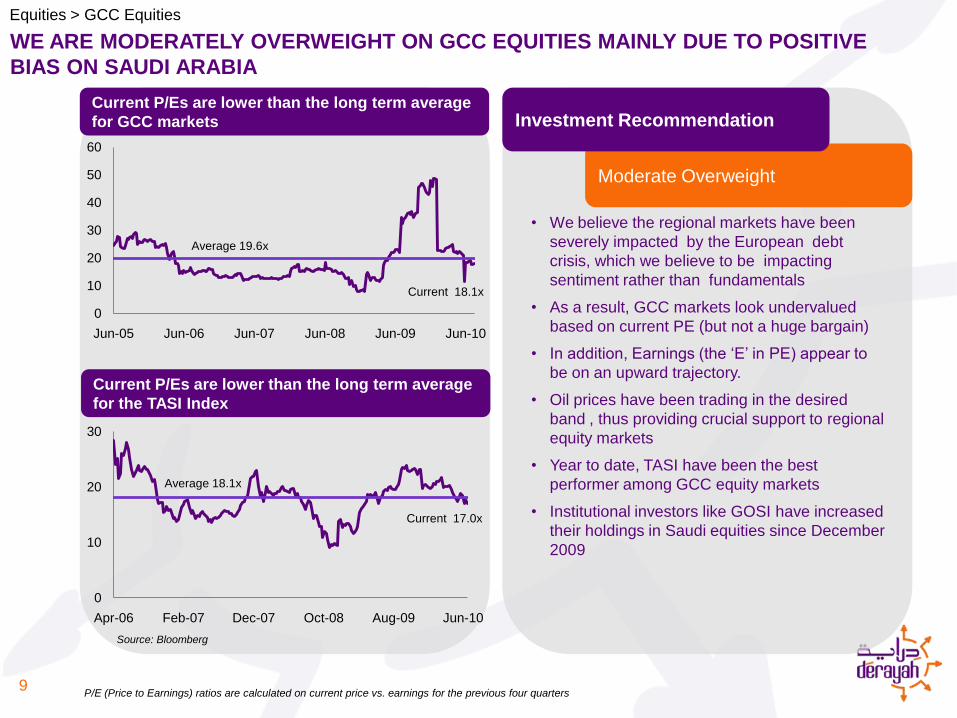

WE ARE MODERATELY OVERWEIGHT ON GCC EQUITIES MAINLY DUE TO POSITIVE

BIAS ON SAUDI ARABIA

9

Moderate Overweight

Investment RecommendationCurrent P/Es are lower than the long term average

for GCC markets

Current P/Es are lower than the long term average

for the TASI Index

Equities > GCC Equities

0

10

20

30

40

50

60

Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10

Average 19.6x

Current 18.1x

Source: Bloomberg

P/E (Price to Earnings) ratios are calculated on current price vs. earnings for the previous four quarters

• We believe the regional markets have been

severely impacted by the European debt

crisis, which we believe to be impacting

sentiment rather than fundamentals

• As a result, GCC markets look undervalued

based on current PE (but not a huge bargain)

• In addition, Earnings (the ‘E’ in PE) appear to

be on an upward trajectory.

• Oil prices have been trading in the desired

band , thus providing crucial support to regional

equity markets

• Year to date, TASI have been the best

performer among GCC equity markets

• Institutional investors like GOSI have increased

their holdings in Saudi equities since December

2009

0

10

20

30

Apr-06 Feb-07 Dec-07 Oct-08 Aug-09 Jun-10

Average 18.1x

Current 17.0x

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money market

- Fixed income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

10

Outlook for various asset classes2

Derayah’s recommended asset allocation3

GCC Equity

Developed

Equity

Emerging

Equity

Emerging

Real Estate

Money

Markets

US

Euro Zone

Developed

Asia

WE MAINTAIN MODERATE OVERWEIGHT FOR DEVELOPED EQUITIES

11

Developed equities comprises three major markets:

Developed

equity

++

--

++

++

Moderate overweight – Weaker Yen and strong growth

prospects favor the market

Moderate Underweight – Despite low P/Es economic

problems should keep investors away

Moderate Overweight – Positive EPS revision and

increasing risk appetite should help the market outperform

on a relative basis (esp. as Europe is expected to under

perform)

Fixed

Income/Sukuk

Equities > Developed Equities

Moderate overweight

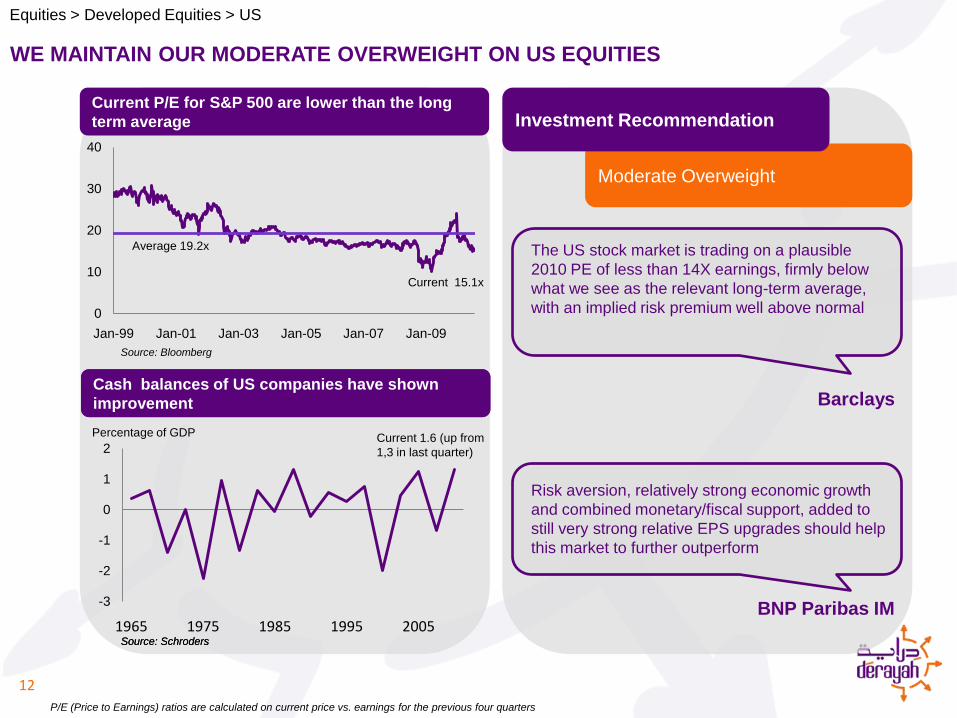

WE MAINTAIN OUR MODERATE OVERWEIGHT ON US EQUITIES

12

Moderate Overweight

Investment RecommendationCurrent P/E for S&P 500 are lower than the long

term average

XX

Equities > Developed Equities > US

Source: Bloomberg

Source: Schroders

Barclays

BNP Paribas IM

Risk aversion, relatively strong economic growth

and combined monetary/fiscal support, added to

still very strong relative EPS upgrades should help

this market to further outperform

P/E (Price to Earnings) ratios are calculated on current price vs. earnings for the previous four quarters

The US stock market is trading on a plausible

2010 PE of less than 14X earnings, firmly below

what we see as the relevant long-term average,

with an implied risk premium well above normal0

10

20

30

40

Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

Average 19.2x

Current 15.1x

-3

-2

-1

0

1

2

1965 1975 1985 1995 2005

Cash balances of US companies have shown

improvement

Source: Schroders

Percentage of GDP Current 1.6 (up from

1,3 in last quarter)

WE MAINTAIN OUR MODERATE UNDERWEIGHT ON DEVELOPED EUROPE EQUITIES AND

MODERATE OVERWEIGHT ON DEVELOPED ASIA

13

Investment RecommendationCurrent P/Es are lower than the long term average

P/E for European Union

Current P/Es are lower than the long term average

P/E for Japan’s Nikkei

Equities > Developed Equities > Euro Zone / Developed Asia

Source: Bloomberg

Source: Bloomberg

Recent policy moves have sown confusion and

the economic problems of the Eurozone remain

acute

Credit Suisse

Schroders

P/E (Price to Earnings) ratios are calculated on current price vs. earnings for the previous four quarters

Moderate underweight: Europe

Moderate overweight: Developed Asia

0

10

20

30

40

50

60

Jan-04 Apr-05 Jul-06 Oct-07 Jan-09 Apr-10

Average 22.1x

Current 15.2x

The macro backdrop has continued to improve

and we have upgraded our growth forecast for

Japan. However, Japanese equities have suffered

from the strength of the yen, although a weaker

currency could eventually spur equity gains.

Forward-looking metrics on the region’s corporate

earnings are also positive.

0

10

20

30

40

50

60

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Current 15.2x

Average 20.7x

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

14

Outlook for various asset classes2

Derayah’s recommended asset allocation3

Fixed

Income/Sukuk

GCC Equity

Developed

Equity

Emerging

Equity

Emerging

Real Estate

Money

Markets

Emerging

Europe

Latin

America

WE RECOMMEND OVERWEIGHT ON EMERGING EQUITIES

15

Emerging

equity

+++

Emerging

Asia

+++

+++

+++

Overweight

Overweight - Russia is experiencing broad based

recovery

Overweight – China and India have sound economic

fundamentals and offer good value

Overweight

Equities > Emerging Equity

WE RECOMMEND AN OVERWEIGHT ON EMERGING MARKET EQUITIES

16

Moderate Overweight

Investment RecommendationCurrent P/Es are lower than the long term average

for Emerging markets

Equities > Emerging Equity

Source: Bloomberg

MSCI Emerging Markets Equity Index

We maintain our overweight emerging markets for

the following reasons:

1) Emerging markets offer comparable 2010

earnings growth at a discount

2) Long term superior fundamentals of emerging

markets remain well in place

3) Emerging markets are no longer a pure play

on global growth but a region having its own

set of qualities and opportunities. This is not

fully reflected yet in investors’ portfolios

ING

JP Morgan

z

Overweight markets that are more remote from

the epicenter of the crisis, such as US industry

groups with little euro exposure, and India and

Mexico in EM.

MSCI EM Trailing Return on Equity (ROE) is 33%

higher compared to MSCI World

Source: Bloomberg

Source: Morgan Stanley

P/E (Price to Earnings) ratios are calculated on current price vs. earnings for the previous four quarters

0

10

20

30

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Average 15.8x

Current 14.6x

0.00

3.00

6.00

9.00

12.00

15.00

18.00

1992 1995 1998 2001 2004 2007 2010

MSCI EM – 13.6

MSCI World – 10.2

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

17

Outlook for various asset classes2

Derayah’s recommended asset allocation3

0

2

4

6

8

10

12

May-08 Nov-08 May-09 Nov-09

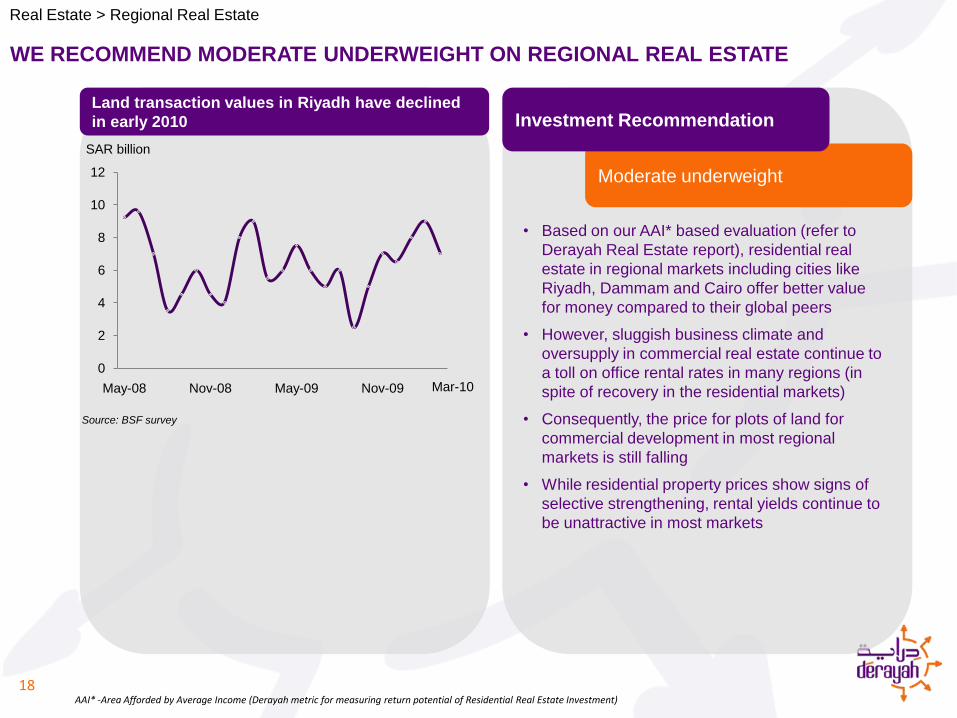

WE RECOMMEND MODERATE UNDERWEIGHT ON REGIONAL REAL ESTATE

18

Moderate underweight

Investment RecommendationLand transaction values in Riyadh have declined

in early 2010

Real Estate > Regional Real Estate

Source: BSF survey

• Based on our AAI* based evaluation (refer to

Derayah Real Estate report), residential real

estate in regional markets including cities like

Riyadh, Dammam and Cairo offer better value

for money compared to their global peers

• However, sluggish business climate and

oversupply in commercial real estate continue to

a toll on office rental rates in many regions (in

spite of recovery in the residential markets)

• Consequently, the price for plots of land for

commercial development in most regional

markets is still falling

• While residential property prices show signs of

selective strengthening, rental yields continue to

be unattractive in most markets

Mar-10

SAR billion

AAI* -Area Afforded by Average Income (Derayah metric for measuring return potential of Residential Real Estate Investment)

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

19

Outlook for various asset classes2

Derayah’s recommended asset allocation3

WE HAVE A BEARISH OUTLOOK FOR MONEY MARKETS

20

Underweight

Investment RecommendationMoney market returns for SIBOR and USD LIBOR

Money Market

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Jan-02 Apr-04 Jul-06 Oct-08

Source: Bloomberg

1 month USD LIBOR

1 month SIBOR

On a six-month view we still expect global equities

to outperform other assets – particularly cash

Barclays

We continue to play a long assets/short cash type

of allocation

BNP Paribas IM

Percentage

- GCC Equity

- Developed Equity

- Emerging Equity

- Emerging Real Estate

- Money Markets

- Fixed Income/Sukuk

CONTENTS

Summary of economic performance for the last quarter1

21

Outlook for various asset classes2

Derayah’s recommended asset allocation3

GCC Equity

Developed

Equity

Emerging

Equity

Emerging

Real Estate

Money

Markets

Government

Debt

Investment

Grade

Corporate

High Yield

Corporate

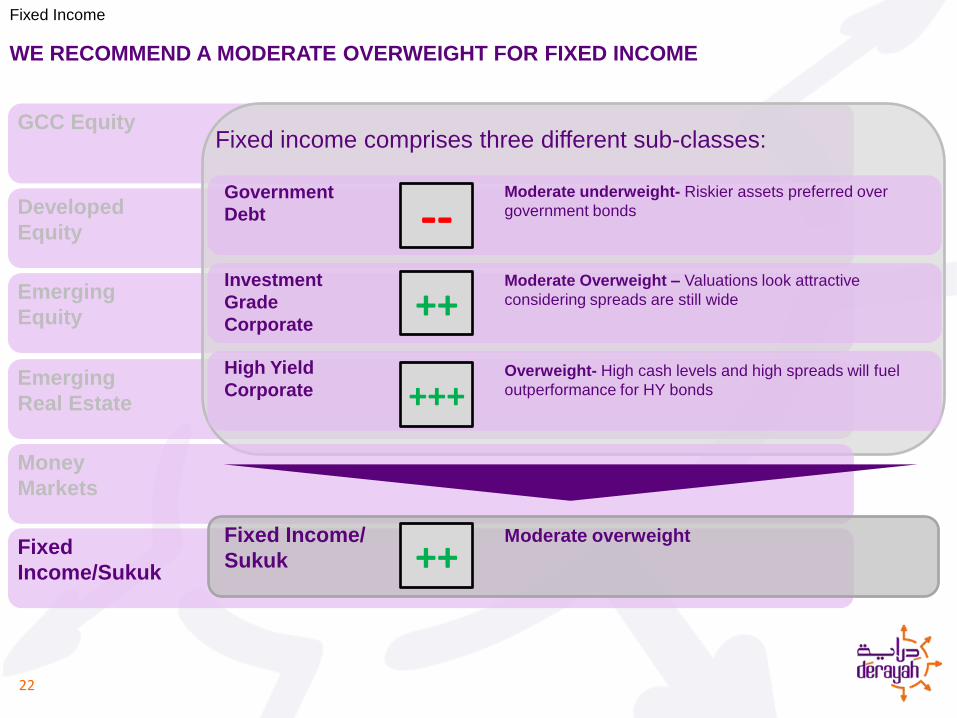

WE RECOMMEND A MODERATE OVERWEIGHT FOR FIXED INCOME

22

Fixed income comprises three different sub-classes:

--

++

Fixed Income/

Sukuk

Overweight- High cash levels and high spreads will fuel

outperformance for HY bonds

Moderate Overweight – Valuations look attractive

considering spreads are still wide

Moderate underweight- Riskier assets preferred over

government bonds

Moderate overweight

++Fixed

Income/Sukuk

Fixed Income

+++

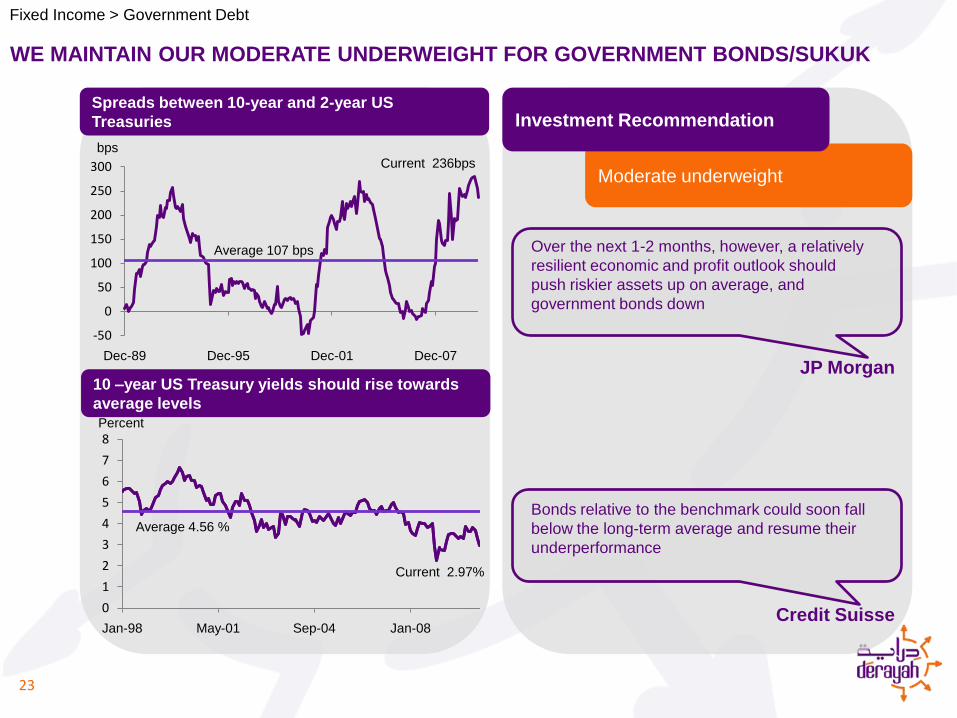

WE MAINTAIN OUR MODERATE UNDERWEIGHT FOR GOVERNMENT BONDS/SUKUK

23

Moderate underweight

Investment RecommendationSpreads between 10-year and 2-year US

Treasuries

10 –year US Treasury yields should rise towards

average levels

Fixed Income > Government Debt

JP Morgan

-50

0

50

100

150

200

250

300

Dec-89 Dec-95 Dec-01 Dec-07

Average 107 bps

Current 236bpsbps

Credit Suisse

Over the next 1-2 months, however, a relatively

resilient economic and profit outlook should

push riskier assets up on average, and

government bonds down

Bonds relative to the benchmark could soon fall

below the long-term average and resume their

underperformance

0

1

2

3

4

5

6

7

8

Jan-98 May-01 Sep-04 Jan-08

Average 4.56 %

Percent

Current 2.97%

0.0

4.0

8.0

12.0

16.0

20.0

Feb-09 May-09 Aug-09 Nov-09 Feb-10 May-10

WE RECOMMEND AN OVERWEIGHT FOR HIGH YIELD AND UPGRADE INVESTMENT GRADE

BONDS/SUKUK TO MODERATE OVERWEIGHT FROM NEUTRAL

24

Source: Bloomberg

Percentage

Moderate Overweight :Invest Grade

Overweight : High Yield

Investment RecommendationSpreads between Investment grade and High yield

bonds still above pre-recession levels

GCC Sukuk yields have dropped significantly

since early 2009

* Equal weighted basket of local and foreign currency Investment grade Sukuk, average maturity 3 years

Fixed Income > Corporate Investment Grade

Current 4.12%

In 3Q we are significantly overweight high yield and

emerging market bonds, more modestly overweight

equities and investment grade bonds and

underweight government bonds

Merrill Lynch

• From a valuation perspective, IG spreads are

looking more attractive given spread widening in

recent months

• Interest rates are expected to stay low for some

time. This suggests that IG should remain

attractive relative to cash given the strong search

for yield amongst investors.

Schroders

Percentage

0.0

4.0

8.0

12.0

16.0

20.0

Oct-02 Oct-04 Oct-06 Oct-08

Source: HSBC-DIFX Sukuk index

Max 17.2%

Current 5.0%

CONTENTS

Summary of economic performance for the last quarter1

25

Outlook for various asset classes2

Derayah’s recommended asset allocation3

26

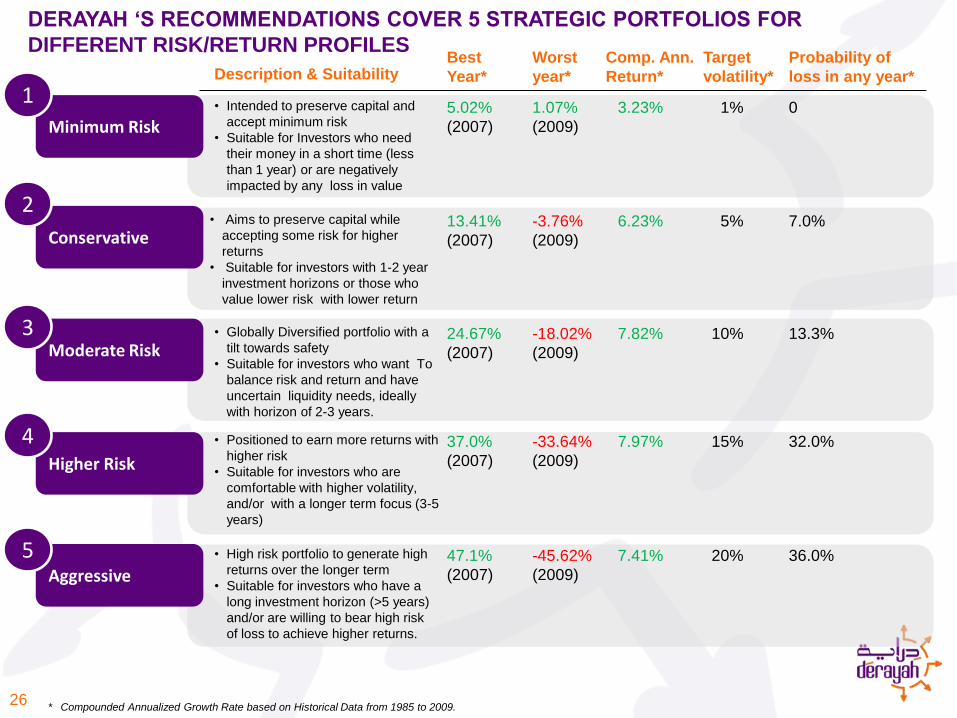

DERAYAH ‘S RECOMMENDATIONS COVER 5 STRATEGIC PORTFOLIOS FOR

DIFFERENT RISK/RETURN PROFILES

Description & Suitability

Minimum Risk

1• Intended to preserve capital and

accept minimum risk

• Suitable for Investors who need

their money in a short time (less

than 1 year) or are negatively

impacted by any loss in value

• Aims to preserve capital while

accepting some risk for higher

returns

• Suitable for investors with 1-2 year

investment horizons or those who

value lower risk with lower return

Conservative

• Globally Diversified portfolio with a

tilt towards safety

• Suitable for investors who want To

balance risk and return and have

uncertain liquidity needs, ideally

with horizon of 2-3 years.

• Positioned to earn more returns with

higher risk

• Suitable for investors who are

comfortable with higher volatility,

and/or with a longer term focus (3-5

years)

• High risk portfolio to generate high

returns over the longer term

• Suitable for investors who have a

long investment horizon (>5 years)

and/or are willing to bear high risk

of loss to achieve higher returns.

Aggressive

5

Higher Risk

4

2

* Compounded Annualized Growth Rate based on Historical Data from 1985 to 2009.

Moderate Risk3

Best

Year*

Worst

year*

Comp. Ann.

Return*

Target

volatility*

Probability of

loss in any year*

5.02%

(2007)

1.07%

(2009)

3.23% 1% 0

13.41%

(2007)

-3.76%

(2009)

6.23% 5% 7.0%

24.67%

(2007)

-18.02%

(2009)

7.82% 10% 13.3%

37.0%

(2007)

-33.64%

(2009)

7.97% 15% 32.0%

47.1%

(2007)

-45.62%

(2009)

7.41% 20% 36.0%

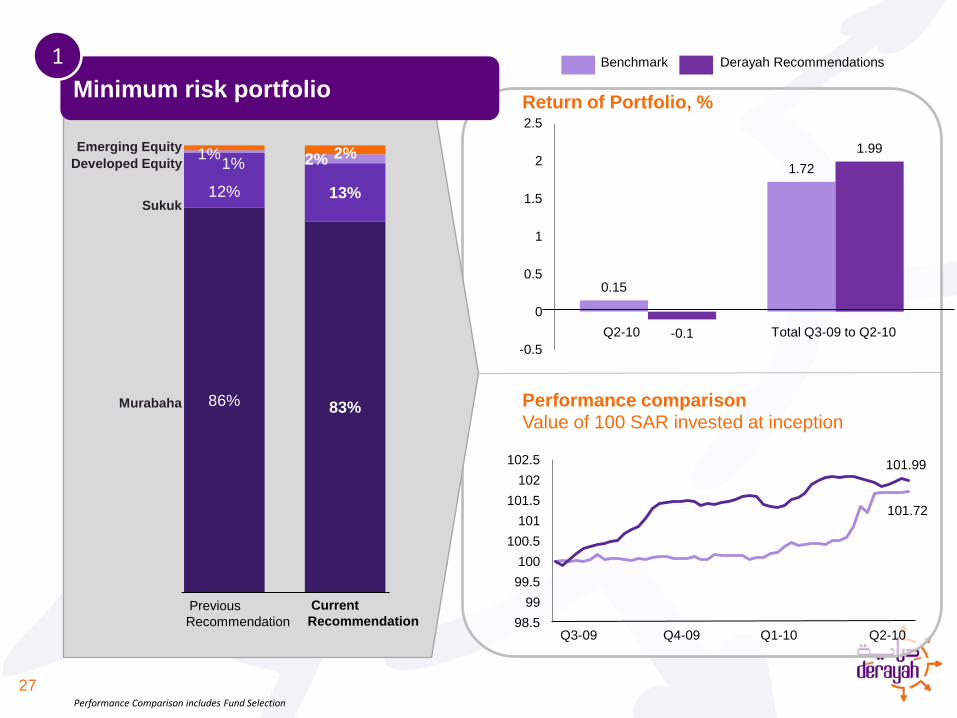

86% 83%

12% 13%

0.15

1.72

-0.1

1.99

-0.5

0

0.5

1

1.5

2

2.5

27

Murabaha

Previous

Recommendation

Current

Recommendation

Minimum risk portfolio

Sukuk

1%1%

Developed Equity

Emerging Equity

1 Benchmark Derayah Recommendations

Return of Portfolio, %

2% 2%

Total Q3-09 to Q2-10Q2-10

Performance comparisonValue of 100 SAR invested at inception

98.5

99

99.5

100

100.5

101

101.5

102

102.5 101.99

101.72

Performance Comparison includes Fund Selection

Q2-10Q1-10Q4-09Q3-09

92

94

96

98

100

102

104

106

108

110

112

114

28

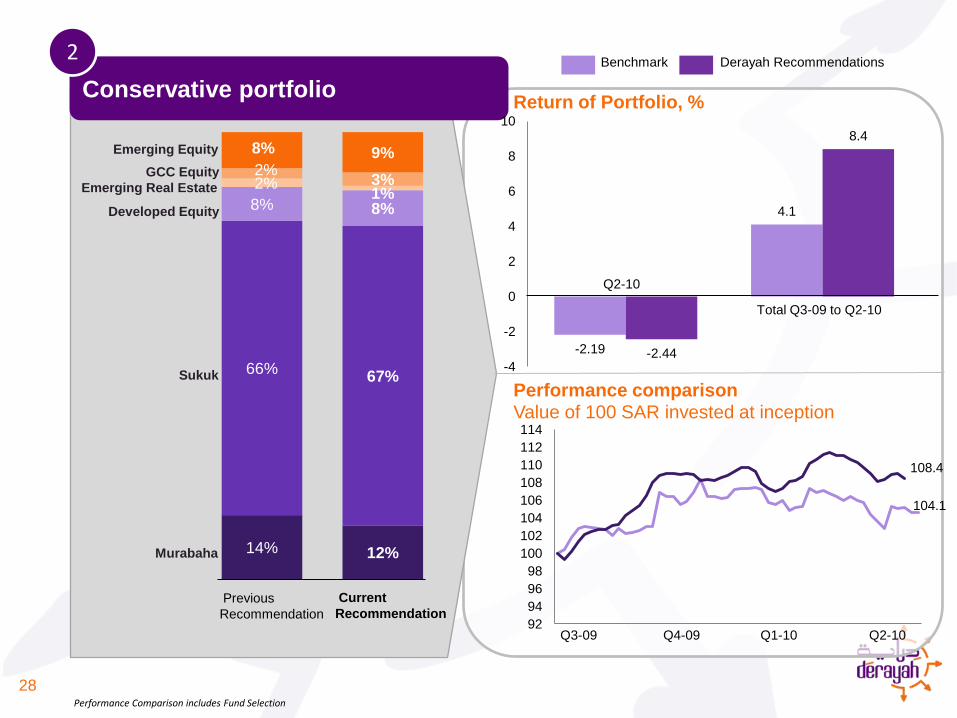

Conservative portfolio

14% 12%

66%67%

8% 8%

2%1%

2%3%

8% 9%

Sukuk

GCC Equity

Developed Equity

Murabaha

Emerging Equity

Emerging Real Estate

Previous

Recommendation

Current

Recommendation

2

-2.19

4.1

-2.44

8.4

-4

-2

0

2

4

6

8

10

Total Q3-09 to Q2-10

Q2-10

104.1

108.4

Return of Portfolio, %

Performance comparisonValue of 100 SAR invested at inception

Benchmark Derayah Recommendations

Performance Comparison includes Fund Selection

Q2-10Q1-10Q4-09Q3-09

85

90

95

100

105

110

115

120

57% 54%

14%14%

5%5%

8% 9%

16% 17%

29

Moderate Risk portfolio

Sukuk

GCC Equity

Developed Equity

Emerging Equity

Emerging Real Estate

Previous

RecommendationCurrent

Recommendation

3

-5.5

6.2

-4.6

10.65

-8

-6

-4

-2

0

2

4

6

8

10

12

Total Q3-09 to Q2-10

Q2-10

110.65

106.2

Benchmark Derayah Recommendations

Return of Portfolio, %

Performance comparisonValue of 100 SAR invested at inception

Performance Comparison includes Fund Selection

Q2-10Q1-10Q4-09Q3-09

90

95

100

105

110

115

120

-8.7

6.74

-6.7

10.74

-10

-5

0

5

10

15

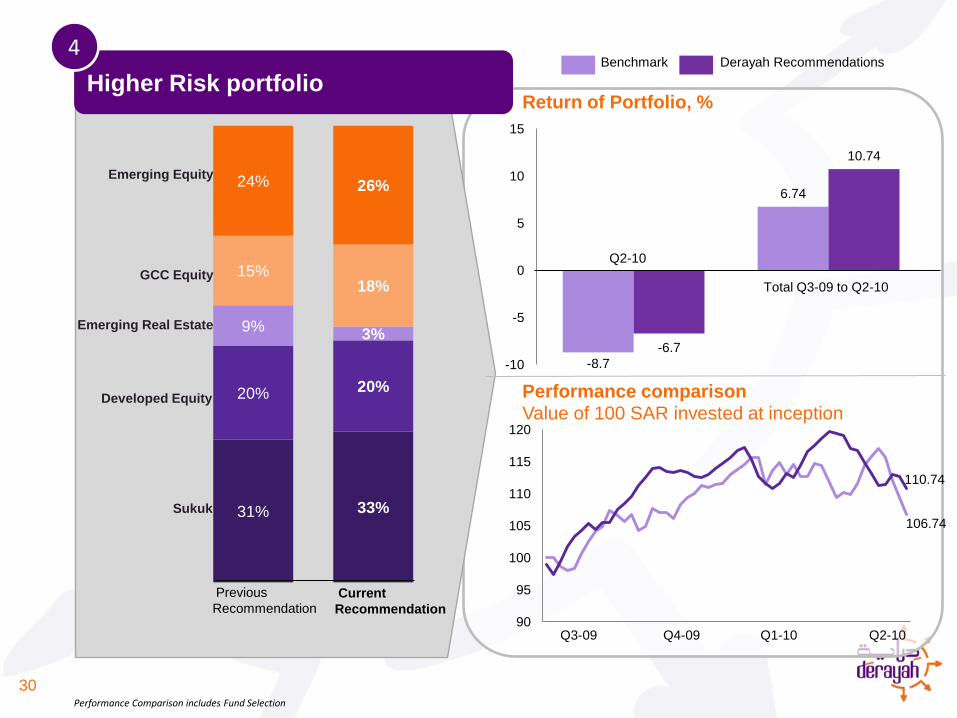

30

Higher Risk portfolio

31% 33%

20% 20%

9%3%

15%18%

24% 26%

Sukuk

GCC Equity

Developed Equity

Emerging Equity

Emerging Real Estate

Previous

RecommendationCurrent

Recommendation

4

Total Q3-09 to Q2-10

Q2-10

106.74

110.74

Benchmark Derayah Recommendations

Return of Portfolio, %

Performance comparisonValue of 100 SAR invested at inception

Performance Comparison includes Fund Selection

Q2-10Q1-10Q4-09Q3-09

90

95

100

105

110

115

120

125

31

Aggressive portfolio

GCC Equity

Developed Equity

Sukuk

Emerging Equity

Emerging Real Estate

12% 12%

25% 25%

12%7%

21%23%

30% 33%

Previous

RecommendationCurrent

Recommendation

5

-11

6.7

-8.2

12.7

-15

-10

-5

0

5

10

15

Total Q3-09 to Q2-10

Q2-10

112.7

106.7

Benchmark Derayah Recommendations

Return of Portfolio, %

Performance comparisonValue of 100 SAR invested at inception

Performance Comparison includes Fund Selection

Q2-10Q1-10Q4-09Q3-09

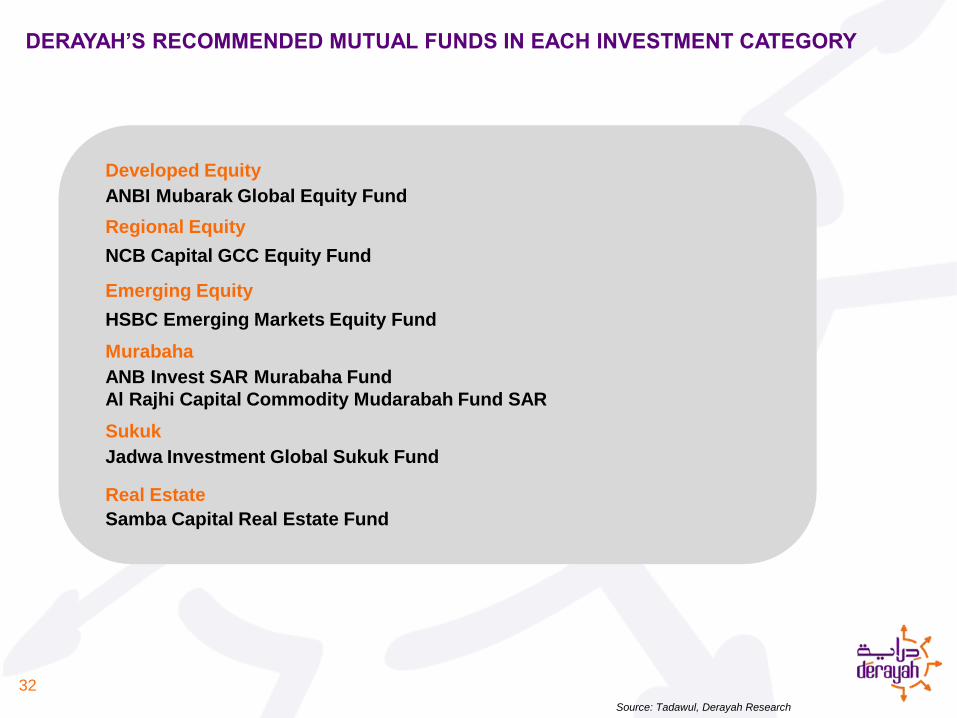

DERAYAH’S RECOMMENDED MUTUAL FUNDS IN EACH INVESTMENT CATEGORY

32

Developed Equity

HSBC Emerging Markets Equity Fund

NCB Capital GCC Equity Fund

ANBI Mubarak Global Equity Fund

Murabaha

ANB Invest SAR Murabaha Fund

Al Rajhi Capital Commodity Mudarabah Fund SAR

Sukuk

Jadwa Investment Global Sukuk Fund

Real Estate

Samba Capital Real Estate Fund

Source: Tadawul, Derayah Research

Emerging Equity

Regional Equity

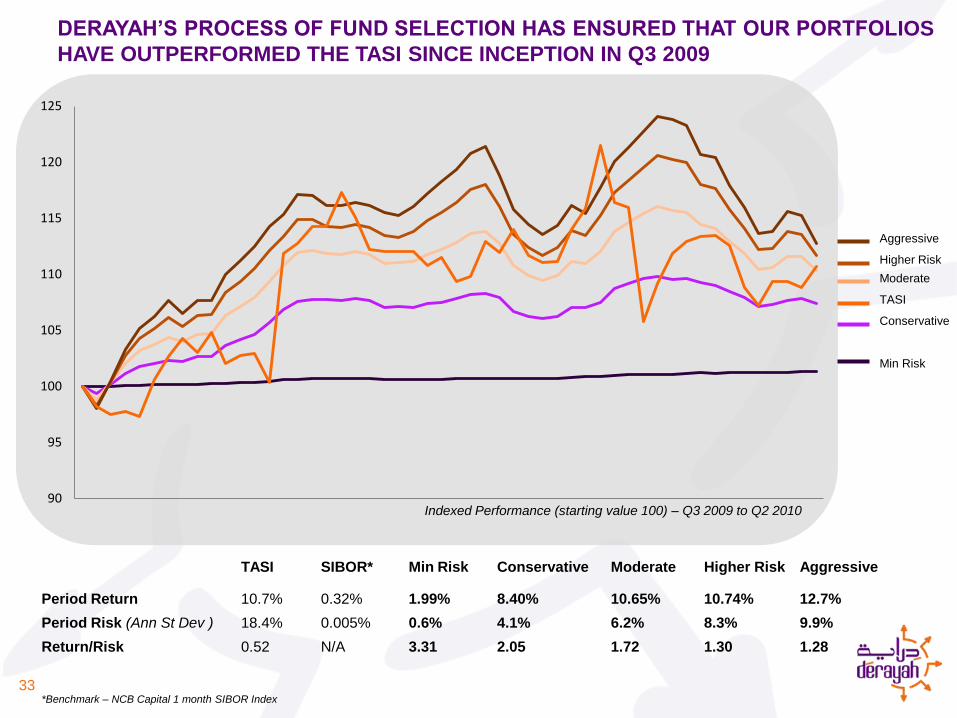

DERAYAH’S PROCESS OF FUND SELECTION HAS ENSURED THAT OUR PORTFOLIOS

HAVE OUTPERFORMED THE TASI SINCE INCEPTION IN Q3 2009

33

Period Return

Period Risk (Ann St Dev )

10.7%

18.4%

TASI SIBOR* Min Risk Conservative Moderate Higher Risk Aggressive

0.32%

0.005%

1.99%

0.6%

8.40%

4.1%

10.65%

6.2%

10.74%

8.3%

12.7%

9.9%

90

95

100

105

110

115

120

125

Indexed Performance (starting value 100) – Q3 2009 to Q2 2010

Aggressive

Min Risk

TASI

Conservative

Higher Risk

Moderate

*Benchmark – NCB Capital 1 month SIBOR Index

Return/Risk 3.31 2.05 1.72 1.30 1.280.52 N/A

AND HAVE ALSO HELPED US OUTPERFORM OUR PEERS ON A RISK ADJUSTED

BASIS*

34

Manager Fund Return Volatility Return/Risk

NCB Capital (Al Manarah)

Conservative 2.47% 5.11% 0.48

Balanced 4.89% 10.20% 0.48

Growth 8.73% 15.06% 0.58

HSBC KSA(Amanah)

Defensive 3.06% 7.12% 0.43

Balanced 6.02% 13.44% 0.45

Growth 9.56% 19.27% 0.50

SHC Al Yusr Aman 2.34% 3.13% 0.75

Mizan 4.45% 8.27% 0.54

Tamoh 5.87% 17.17% 0.34

Al Rajhi Capital Balanced Fund 1 4.40% 6.23% 0.71

Balanced Fund 2 11.03% 20.09% 0.55

ANBI Balanced 9.96% 19.41% 0.51

Jadwa Conservative 2.08% 4.57% 0.46

Balanced 8.06% 11.74% 0.69

Aggressive 15.63% 23.80% 0.66

Derayah Low Risk 7.40% 3.58% 2.07

Conservative 10.38% 6.08% 1.71

Aggressive 12.80% 10.02% 1.28

* Period under consideration – Q3’2009 to Q2’2010

We attribute our outperformance to:

Focus on diversification and efficient Asset allocation

Focus on selecting the most appropriate product for portfolio execution

Focus on tactical shifts to take advantage of temporary market dislocations

35

APPENDIX

DERAYAH’S FRAMEWORK FOR PORTFOLIO STRUCTURING AND TACTICAL ASSET

ALLOCATION

36

1.Develop strategic

asset allocation

2.Synthesize tactical

asset allocation shifts

3.Recommend tactical

allocation to investors

• Derayah has developed

its proprietary framework

that creates an efficient

frontier including a

diversified set of asset

classes

• For various risk levels

the target portfolio is

designed to maximize

risk adjusted returns

based on historical and

expected future

performance of these

asset classes*

• Derayah collates analyst

expectations on

expected performance

of various asset classes

from a selected set of

global Asset

Management firms

• Derayah creates its own

consensus rating for

each asset class based

on its framework and

analyst expectations.

This rating is then used

to arrive at the tactical

shifts for the weights in

each asset class

included in the portfolios

• Tactical asset allocation

recommends that the

investors adjust their the

long term asset

allocation to take

advantage of

opportunities rising from

short term market

dislocations to generate

higher returns

• Derayah incorporates

the tactical adjustments

(Step 2) on the strategic

asset allocation (Step 1)

to design the portfolios

1. FOR THE STRATEGIC ASSET ALLOCATION, WE PERFORMED A MEAN-VARIANCE

OPTIMIZATION USING THE FOLLOWING INPUTS

37

Historical Correlations among various asset classes2

Historical Risk and return for various asset classes1

1Maximum available time period starting January 1970

Mean Variance Optimization – Developed by Harry Markowitz, Mean-variance optimization, is a quantitative asset allocation

technique which allows investors to use diversification to balance the risk and return in their portfolio.

Standard Deviation - A measure of the variability of a data set, or a probability distribution. A low standard deviation indicates that the

portfolio has low uncertainty i.e. returns tend to be very close to the mean, while high standard deviation indicates that the returns are

more uncertain and are spread out over a large range of values.

The output

from the

process is

multiple

optimized

portfolios

that are

suitable for

investors

with various

levels of

risk

tolerance

ASSET CLASS

MSCI

World

JPM Agg

Index

MSCI

EM/Real

Estate

SAR

Interbank

rates

MSCI

Emerging

Mkts

MSCI

GCC

Countries

MSCI World 1.00

JPM Agg Bond Index 0.13 1.00

MSCI EM/Real Estate 0.21 0.12 1.00

SAR Interbank rates -0.12 -0.13 0.05 1.00

MSCI Emerging Mkts 0.72 0.00 0.25 -0.11 1.00

MSCI GCC Countries 0.57 0.12 0.16 -0.08 0.58 1.00

MSCI

World

JPM Agg

Bond

Index

MSCI

EM/Real

Estate

SAR

Interbank

rates

MSCI

Emerging

Mkts

MSCI GCC

Countries

Historical Risk (St Deviation) 14.88% 3.65% 32.00% 0.46% 24.27% 30.03%

Historical Returns 6.38% 7.28% -4.61% 2.85% 10.65% -15.19%

ILLUSTRATION

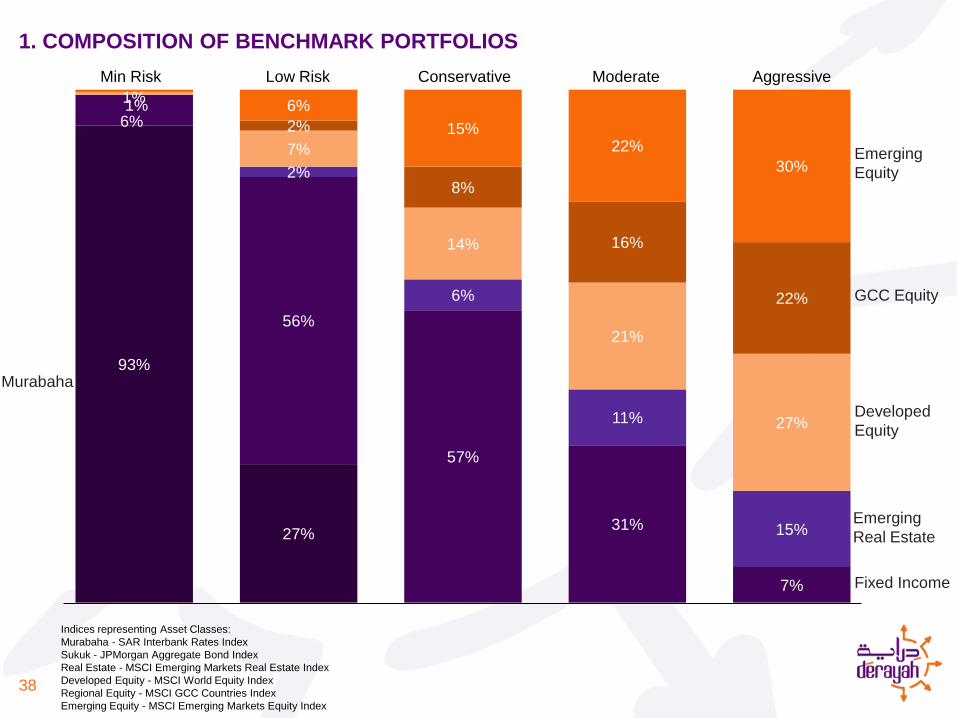

1. COMPOSITION OF BENCHMARK PORTFOLIOS

38

Indices representing Asset Classes:

Murabaha - SAR Interbank Rates Index

Sukuk - JPMorgan Aggregate Bond Index

Real Estate - MSCI Emerging Markets Real Estate Index

Developed Equity - MSCI World Equity Index

Regional Equity - MSCI GCC Countries Index

Emerging Equity - MSCI Emerging Markets Equity Index

93%

27%

6%

56%

57%

31%

7%

2%

6%

11%

15%

1%

7%

14%

21%

27%

2%

8%

16%

22%

1%6%

15%22%

30%

Min Risk Low Risk Conservative Moderate Aggressive

Emerging

Equity

GCC Equity

Developed

Equity

Emerging

Real Estate

Fixed Income

Murabaha

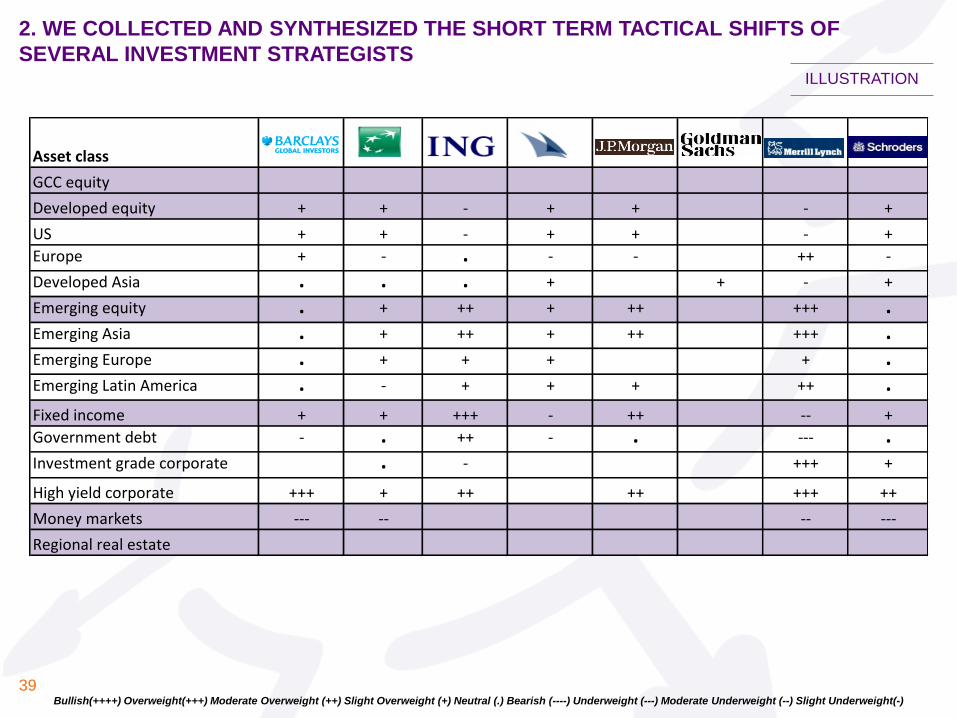

2. WE COLLECTED AND SYNTHESIZED THE SHORT TERM TACTICAL SHIFTS OF

SEVERAL INVESTMENT STRATEGISTS

39Bullish(++++) Overweight(+++) Moderate Overweight (++) Slight Overweight (+) Neutral (.) Bearish (----) Underweight (---) Moderate Underweight (--) Slight Underweight(-)

Asset class

GCC equity

Developed equity + + - + + - +

US + + - + + - +

Europe + - . - - ++ -

Developed Asia . . . + + - +

Emerging equity . + ++ + ++ +++ .Emerging Asia . + ++ + ++ +++ .Emerging Europe . + + + + .Emerging Latin America . - + + + ++ .Fixed income + + +++ - ++ -- +

Government debt - . ++ - . --- .Investment grade corporate . - +++ +

High yield corporate +++ + ++ ++ +++ ++

Money markets --- -- -- ---

Regional real estate

ILLUSTRATION

40

3. WE THEN APPLIED THESE TACTICAL SHIFTS TO OUR STRATEGIC PORTFOLIOS

Minimum Risk

Low Risk

Conservative

Moderate

Aggressive

Strategic portfolios Tactical portfolios

Minimum Risk

Low Risk

Conservative

Moderate

Aggressive

Fixed Income(Sukuk)

Developed Equity +GCC Equity -

Money Markets --

Emerging Real estate .

EmergingEquity +

+

ILLUSTRATION

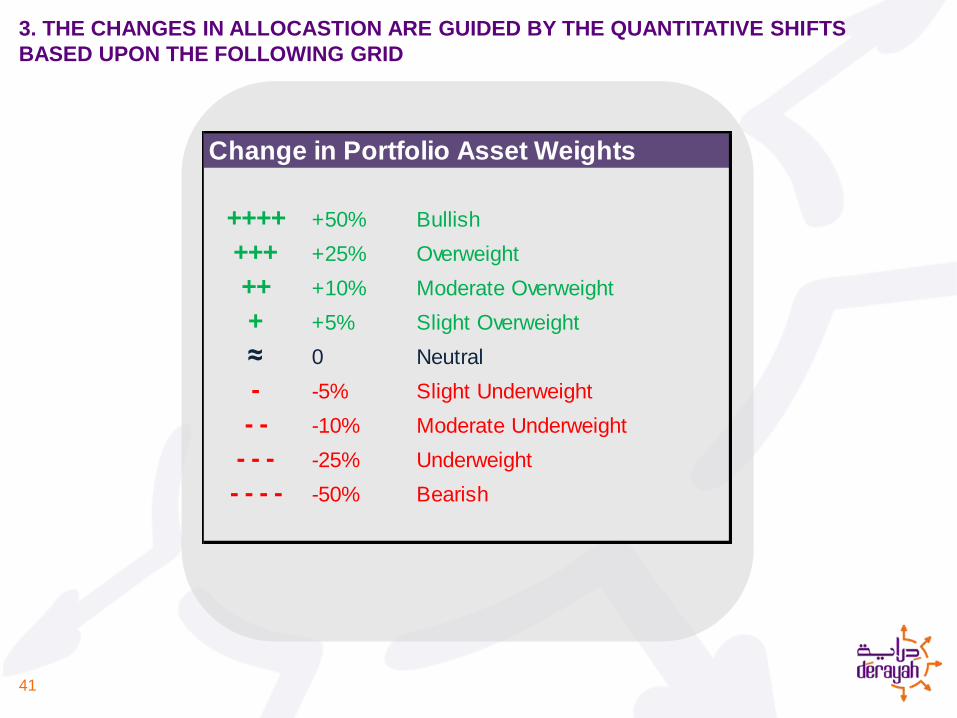

3. THE CHANGES IN ALLOCASTION ARE GUIDED BY THE QUANTITATIVE SHIFTS

BASED UPON THE FOLLOWING GRID

41

Change in Portfolio Asset Weights

++++ +50% Bullish

+++ +25% Overweight

++ +10% Moderate Overweight

+ +5% Slight Overweight

≈ 0 Neutral

- -5% Slight Underweight

- - -10% Moderate Underweight

- - - -25% Underweight

- - - - -50% Bearish

Second Floor , Olaya Center , Olaya Main St.

P.O. Box 286546 Riyadh 11323 Saudi Arabia

Tel: +966 1 299 8000

Fax: +966 1 419 6498

Website: www.derayah.com

Email: [email protected]

NOTICE OF DISCLAIMER

While every precaution has been taken in the preparation of this document, Derayah Financial assumes no responsibility for errors, omissions, or for any damages resulting

from the use of the information herein. Product or corporate names may be trademarks or registered trademarks of other companies and used for the purpose of explanation

and evaluation, without intent to infringe.

Past performance is not indicative of future returns. This document is not and should not be construed an offer to sell securities or investment products. This document does not

purport to incorporate all relevant information and as such should not be deemed as a formal investment advice or recommendation. Investors should consult an authorized

financial advisor and make individual decisions. Derayah shall not be liable for any direct or indirect loss arising out of investments based on this document.

This disclaimer statement, presented on this page, is an integral part of this document. Should this page of the document, in its electronic or printed formats, be lost, deleted,

destroyed or otherwise discarded, this disclaimer statement applies despite the consequences.

For queries and clarifications, please contact:

Anirban Kundu

Email: [email protected]

Direct: +966 1 299 8033

Cell: + 966 563 289 401