fiscal 2014 - 沖縄銀行 · 2016. 4. 15. · the bank of okinawa,ltd 2 people’s bank...

TRANSCRIPT

The Bank of Okinawa,Ltd1

Bank of Okinawa - Results BriefingFiscal 2014

The Bank of Okinawa,Ltd2

People’s Bank

Participant

Contents

Supplemental Materials

Business Strategies 28

41

The Business Environment in Okinawa

Outline of Business Results for FY2014

3

11

President : Yoshiaki Tamaki

◉ Competitive Advantage of Okinawa’s Ideal Location◉ Okinawa International Hub Cluster Asian Market IN Strategy◉ Strategy for further development as international distributionbase◉ Population of Okinawa (Future Prospects)◉ Number of Visitors to Okinawa◉ Recent Economic Trends 1 (Official land prices, BOJ Tankan)◉ Recent Economic Trends 2 (Economic growth rate, Unemployment rate)

45

678

9

10

・・・・・・・・・ ・・・ ・・・・・

・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・

・・・・ ・・・・・・・・・・・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・・・・・・・・・・・・・・・・

・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・ ・・

・ ・・・・・ ・・・・・ ・・・・ ・・・・・ ・・・・・ ・・・・・ ・・・・・ ・・・・・・

・・・・・ ・・・・・ ・・・・・ ・・・・・ ・・・・・ ・・・・・・・・

◉ Highlights for FY2014◉ Earnings◉ Deposits (Average Balance)◉ Loans (Average Balance)◉ Loans to Individuals (Term-End Balance)◉ Fees and Commissions (Excluding Trust Fees)◉ Loan / Deposit Interest Margin (Domestic)◉ Loan / Deposit Spreads (Domestic)◉ Securities (Term-End Balance) ◉ Securities Allocation◉ Core OHR and Expenses◉ Capital Ratio (Basel III Standard)◉ Risk Management - Capital Allocation -◉ Credit Cost◉ Mandatory Disclosure of Bad Debt under the Financial Reconstruction Law◉ Our Share of the Market Served by the Three Okinawan Regional Banks (FY2014)

1213141516171819202122232425

26

27

・・ ・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・ ・・・ ・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・ ・・・・・・・・・・・・・・・・・・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・ ・・・ ・・・・・・・・

・・・・・・・・・・・・・・・・・・・ ・・・ ・・・・・・・・・・・・・・・・・・・・・ ・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・ ・・・ ・・・ ・・・・・・・・・・・・・・・・・・・

・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・・

・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・・

◉ 17th Medium-Term Business Plan (From Customer Focused Operational Reforms to New Value Creation)◉ 17th Medium-Term Business Plan (Achievements of “Customer Focused”Strategy)◉ 17th Medium-Term Business Plan (Management Goal)◉ 17th Medium-Term Business Plan (Growth Strategy I: Expansion of Corporate (Business) Customers)◉ 17th Medium-Term Business Plan (Growth Strategy II: Expansion of Individual Customers)◉ 17th Medium-Term Business Plan (Initiative for the First Year, “Customer Focused” Operational Reform)◉ Business Performance Forecasts◉ Consumer Loans◉ Strategy for Assets in Custody◉ Aggressive Investment Strategy◉ Branch Network Strategy◉ Shareholder Returns

29

3031

32

33

34353637383940

・・・ ・・・ ・・・ ・・・ ・・・・・・・・・・ ・・・・ ・・・・ ・・・・・・・・

・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・ ・・・・ ・・・・・・・・ ・・・ ・・・ ・ ・・・・ ・・・・

・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・・・・・・ ・・・・ ・・・・

・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・ ・・・・ ・・・・

・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・ ・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・ ・・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・ ・・・・ ・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・ ・・・・・・・

42

43

444546

◉ Business Performance◉ Term-End Balance, Average Balance, Yield, and Loan Balance by Industrial Segment◉ Changes in Loan Balance by Assets Category (FY2013 and FY2014)◉ Interest Sensitivity◉ Major Economic Indicators in Okinawa Prefecture

・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

・ ・・・・・・ ・・・・・・ ・・・・・・ ・・・・・・ ・・・・・・ ・・・・・・・・・・・・・・・・・・

・・ ・・・・・・ ・・・・・・ ・・・・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ ・・・・・・ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

・・・・・・・・・・・・・・・・・・・・・・・

The Bank of Okinawa,Ltd3

The Business Environment in Okinawa Prefecture

The Bank of Okinawa,Ltd4

People’s Bank

Amoy

Competitive Advantage of Okinawa’s Ideal Location

With major Asian cities within range of 4 hours, located in the heart of East Asia

Narita

Haneda

Nagoya

Kansai

Seoul

Tsingtao

Shanghai

Taipei

Hong Kong

BangkokO

kinawa Singapore

Amoy

Manila(From October 2015)

(From October 2015)

2h 10min

2h 50min

2h 5min

1h 30min

2h 35min

4h 25min

2h

3h

2h 25min

2h 20min

2h 15min

1h 50min

5h

(1)

Hanoi

VientianeMacau

BangkokPhnom Penh Ho Chi Minh

Kuala Lumpur

Singapore

Hong KongTaipei

Manila

Hangzhou

Shanghai

Tsingtao

Tianjin

BeijingDalianSeoul

Busan

Okinawa

Narita

KansaiNagoyaHaneda

Locations within 4-hour flight from

Okinawa

The Bank of Okinawa,Ltd5

People’s Bank

Okinawa International Hub Cluster Strategy for Asian Market

Source: International Hub Cluster Office

We will build a logistics and distribution channels innovation cycle for Asian economic zone to contribute to the development of an environment for B to B and B to C business of small and medium-sized businesses through opportunities such as business conventions by pursuing reduction in CIQ process load in trading business, while aiming to build development, processing, and production bases of high value-added products as “Central Kitchen” by concentrating nationwide foods and goods in Okinawa in order to export safe and trusted foods of Japan, according to the market needs. Furthermore, we will take initiative to develop systems to nurture human resources who would boldly challenge businesses in Asian region.

Asian economic zone Okinawa Nationwide

Purchase frequency

Product unit price

Frequency of visits

Regional characteristics

Number of purchase

itemsInventory

status

Time of purchase

Customer attribute

ID-POS data of Asian Markets

Just-in-time delivery Develop and process high value-added products by precisely capturing market needs and export them effectively Gather nationwide goods and foods in Okinawa

Place of production

Production in collaboration

Production skills

Technology

Inventory status

Production and processing

information of Japan

globally competent human resources

Simplification and optimization of CIQ

Product development using big data

Central Kitchen(cooking, processing, packaging, etc.)

Develop products capturing customer needs for each region through data analysis of Asian markets, establish direct sales system for purchasers

Contents utilization

(EC site)

Okinawa International Hub Cluster

Study of simplification and optimization of CIQ (Customs, Immigration, and Quarantine)

- Development of high value-added products- Establishing structure for efficient and stable supply- Manufacturing under JAPAN brand

International business convention / exhibition

(Okinawa Great Trade Fair)

The Bank of Okinawa,Ltd6

People’s Bank

Strategy for further development as international logistics hub point

◆ Parts center for electronic components

◆ EC inventory control center for Asia

(1) Completion of logistics center (2015)

◆ Gather nationwide foods and goods in Okinawa to build a business model to expand into Asia

(2) Collaboration with other regions in Japan

(3) Development of large-scale MICE facility with capacity of around 20,000 people (2020)

For company meetings

For exhibitions /trade fairs

For trainings / incentive travels

For domestic / international meetings

< Example of collaborated business between Okinawa and other regions (budgeted by METI, etc.)>Product development using commercial products of Okinawa (Hokkaido x Okinawa)Project to develop food market in Middle Eastern Gulf area (Hokkaido x Kyushu x Okinawa)Global collaboration project of agriculture, commerce and industry (Hokkaido x Okinawa)Global collaboration project of agriculture, commerce and industry (Mie x Okinawa)Okinawa International Hub Cluster Project (Okinawa x wider region)Asia global human resource development project (Okinawa x Kyushu)Regional brand overseas development project (Okinawa x Hokkaido x other regions)

The Bank of Okinawa,Ltd7

People’s Bank

Population of Okinawa (Future Prospects)

Projected population

The population of Okinawa is expected to take a downward turn in and after 2025.Population is on the increase at this stage, but active steps towards population

growth are being taken now.

(2100)2,030

(2100)

840

◆ Elimination of childcare waining list◆ Promotion of “health and longevity in Okinawa” campaign

(2050)

1,610(2135)

1,540(2024)

1,440

Efforts to facilitate natural increase in population

(Creation of a society that allows people to marry, give birth to and raise children without undue worries)

◆ Job creation and securing diverse human resources◆ Addressing to increase tourists and visitors

Efforts to enhance growth of society

(Creation of a dynamic society that is open to the world)

◆ Improvement of conditions for long-term residence◆ Industrial development by demonstrating attractive regional characteristics

Aims to resolve challenges faced by isolated islands and

depopulated regions(Creation of a society that delivers well-balanced and

sustainable population growth)

(in thousands)

The Bank of Okinawa,Ltd8

People’s Bank

Number of Visitors to Okinawa

FY2014 marked a record 7.16 million tourists visiting OkinawaThe number of overseas tourists was 980,000 (up 57% YoY), reaching a record high

(¥ billion)(in thousands)

Number of port call by cruise ships in 2014: 162

Scheduled number of port call in 2015: 212 (up 30%)

Number of visitors in FY2014

7,160,000

2003 14131205 100908070604 11 2015 2021

Japanese visitors(left axis)

Overseas visitors(left axis)

Tourism revenues(right axis)

600

500

400

300

200

100

(fiscal year)

The Bank of Okinawa,Ltd9

People’s Bank

Recent Economic Trends 1

Highest value on record

¥817,000/sqm

Highest value on record

¥211,000/sqm

BOJ TankanOfficial land prices

(%)

(%)

Source: BOJ Naha BranchSource: Ministry of Land, Infrastructure, Transport and Tourism

20152014201320122011

Okinawa

Fukuoka

KumamotoNational average

Okinawa

Fukuoka

KumamotoNational average

20142013201220112010Mar. 2012 Mar. 2013 Mar. 2014 Mar. 2015Sep. 2012 Sep. 2013 Sep. 2014

Okinawa

National average

The Bank of Okinawa,Ltd10

People’s Bank

Unemployment rate

Recent Economic Trends 2

◆ Okinawa has maintained higher rates of economic growth than the national average◆ In the past, Okinawa suffered nearly twice the unemployment rate of the national average,

but the rates have steadily fallen, becoming closer to the national level.

Economic growth rate (actual)

Comparison of economic growth rate -Okinawa vs. National average

Trends in unemployment rates

Okinawa National average

Okinawa National average

Difference

(%) (%)

Source: Okinawa Prefecture, Cabinet Office, Government of Japan Source: Okinawa Prefecture, Ministry of Internal Affairs and Communications

20102009 2011 2012 2013 forecast 2011 2012 2013 2014 Mar. 2015 2021

The Bank of Okinawa,Ltd11

Outline of Business Results for FY2014

The Bank of Okinawa,Ltd12

People’s Bank

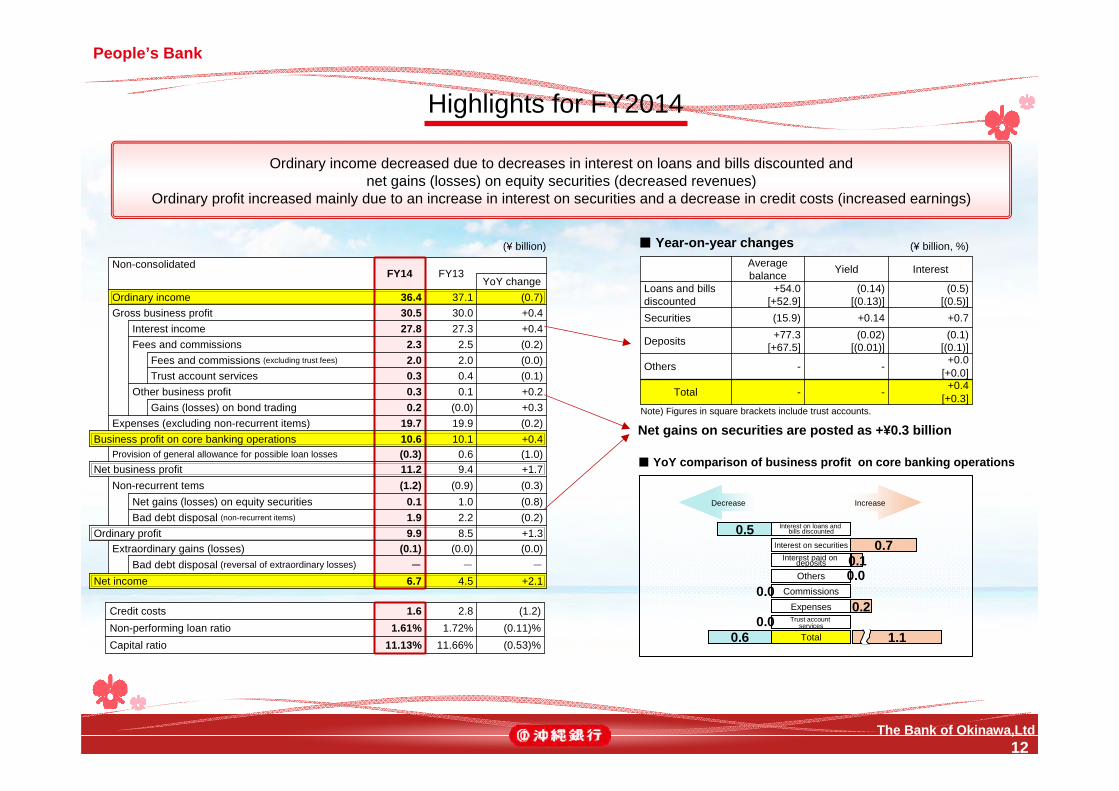

Highlights for FY2014

(¥ billion)

Non-consolidatedFY14 FY13

YoY changeOrdinary income 36.4 37.1 (0.7)Gross business profit 30.5 30.0 +0.4

Interest income 27.8 27.3 +0.4Fees and commissions 2.3 2.5 (0.2)

Fees and commissions (excluding trust fees) 2.0 2.0 (0.0)Trust account services 0.3 0.4 (0.1)

Other business profit 0.3 0.1 +0.2Gains (losses) on bond trading 0.2 (0.0) +0.3

Expenses (excluding non-recurrent items) 19.7 19.9 (0.2)Business profit on core banking operations 10.6 10.1 +0.4

Provision of general allowance for possible loan losses (0.3) 0.6 (1.0)Net business profit 11.2 9.4 +1.7

Non-recurrent tems (1.2) (0.9) (0.3)Net gains (losses) on equity securities 0.1 1.0 (0.8)Bad debt disposal (non-recurrent items) 1.9 2.2 (0.2)

Ordinary profit 9.9 8.5 +1.3Extraordinary gains (losses) (0.1) (0.0) (0.0)

Bad debt disposal (reversal of extraordinary losses) - - -

Net income 6.7 4.5 +2.1

Credit costs 1.6 2.8 (1.2)Non-performing loan ratio 1.61% 1.72% (0.11)%Capital ratio 11.13% 11.66% (0.53)%

(¥ billion, %)Average balance Yield Interest

Loans and bills discounted

+54.0[+52.9]

(0.14)[(0.13)]

(0.5)[(0.5)]

Securities (15.9) +0.14 +0.7

Deposits +77.3[+67.5]

(0.02)[(0.01)]

(0.1)[(0.1)]

Others - - +0.0[+0.0]

Total - - +0.4[+0.3]

■ Year-on-year changes

Net gains on securities are posted as +¥0.3 billion

■ YoY comparison of business profit on core banking operations

Interest on securities

0.5

Interest paid on deposits

OthersCommissions

ExpensesTrust account

services

Interest on loans and bills discounted

IncreaseDecrease

Total 1.10.6

0.1

0.2

0.7

0.00.0

0.0

Note) Figures in square brackets include trust accounts.

Ordinary income decreased due to decreases in interest on loans and bills discounted and net gains (losses) on equity securities (decreased revenues)

Ordinary profit increased mainly due to an increase in interest on securities and a decrease in credit costs (increased earnings)

The Bank of Okinawa,Ltd13

People’s Bank

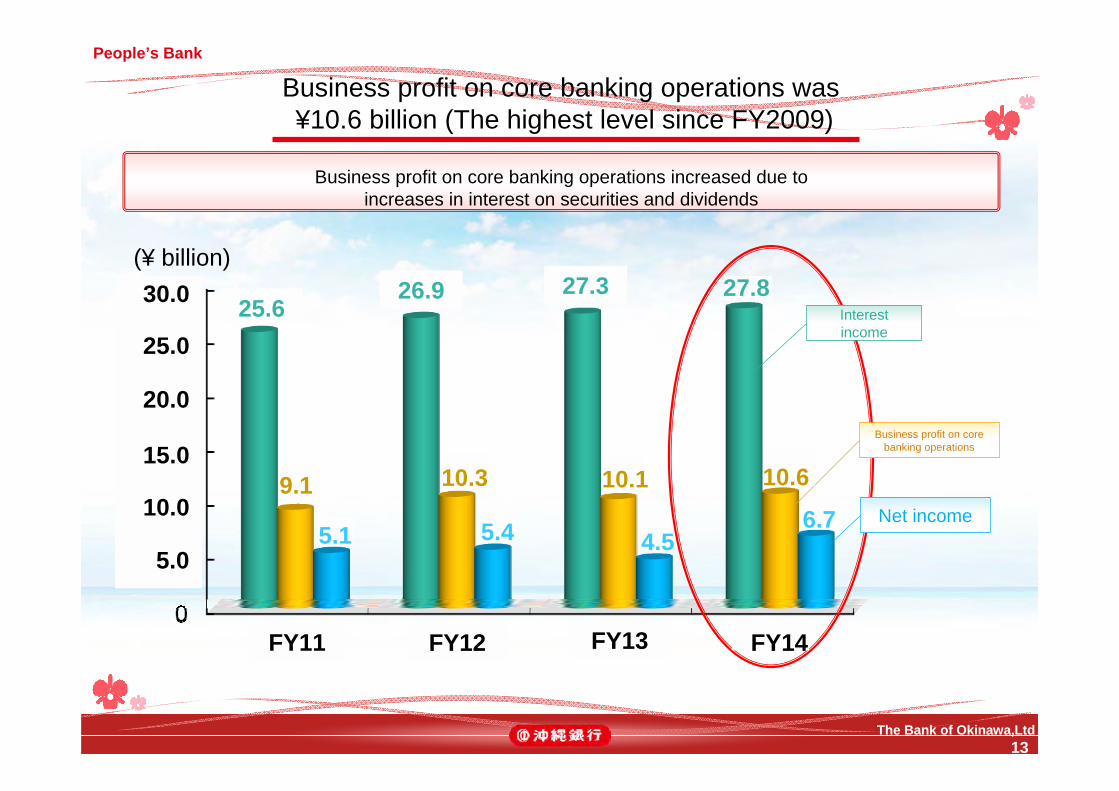

Business profit on core banking operations increased due to increases in interest on securities and dividends

Interest income

Business profit on core banking operations

Net income

Business profit on core banking operations was¥10.6 billion (The highest level since FY2009)

25.626.9 27.3 27.8

9.1

5.1 5.4 4.56.7

10.3 10.1 10.6

FY11 FY12 FY13 FY14

30.0

25.0

20.0

15.0

10.0

5.0

(¥ billion)

The Bank of Okinawa,Ltd14

People’s Bank

Deposits (Average Balance)

Deposits by corporations rose by ¥47.5 billion (+9.9%)Deposits by individuals rose by ¥17.1 billion (+1.5%)

Total deposits rose by ¥67.5 billion (+3.8%) to ¥1,813.1 billion

Deposits by corporations

Deposits by individuals

Increased liquidity in deposits due to enhanced

function to trace funds

Increased liquidity in deposits due to opening of new salary payment and pension accounts

(¥ billion)

* Including trust accounts

1,800

1,600

1,400

1,200

1,000

800

600

400

200

FY11

1,670.4

149.2

433.5

1,071.8

1,706.515.8 158.2

441.1

1,100.0

1,745.6

134.6

479.5

1,124.2

1,813.1

128.7

527.1

1,141.4

7.0 7.3

FY12 FY13 FY14

The Bank of Okinawa,Ltd15

People’s Bank

Loans (Average Balance)

Business loans rose by ¥25.4 billion, loans to individuals rose by ¥28.7 billionTotal loans and bills discounted rose by ¥52.9 billion (+4.4%) to ¥1,254.9 billion

Local government bodies and other public

organizations

(¥ billion)

Business loansFactors for increase

in loans:Apartment loans

Loans to individualsFactors for increase

in loans:Mortgage loans

* Including trust accounts

1,200

1,000

800

600

400

200

1,121.7

607.1

1,154.7

101.3

624.7

428.6

1,202.0

100.8

649.4

451.8

1,254.9

99.6

480.6405.6

Individuals

674.8

Corporations

109.1

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd16

People’s Bank

Loans to Individuals (Term-End Balance)

Mortgage loans rose by ¥26.4 billion, other loans rose by ¥0.5 billionLoans to individuals rose by ¥27.0 billion (+5.1%) year on year to ¥556.8 billion

(¥ billion)

Mortgage loans

Other loans

* Including trust accounts

500

400

300

100

200

473.2

61.1

412.1

496.8

63.5

433.3

529.8

65.2

464.6

556.8

65.7

491.0

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd17

People’s Bank

Fees and Commissions (Excluding Trust Fees)

(¥ billion)

Fees and commissions remained flat overall・Increased fees due to increased

assets in custody・Increased premium expense for creditor group insurance due to

increased mortgage loans

2.5

2.0

1.5

0.5

1.0

1.51.8

2.0 2.0

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd18

People’s Bank

Loan / Deposit Interest Margin

Loan / Deposit Interest Margin (Domestic)

Loan / Deposit Interest Margin

Expense ratio

Yield on loans

(%)

Yield on deposits

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd19

People’s Bank

Loan / Deposit Spreads

Loan / Deposit Spreads (Domestic)

(%) Bank of Okinawa

Average of regional banks Difference

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd20

People’s Bank

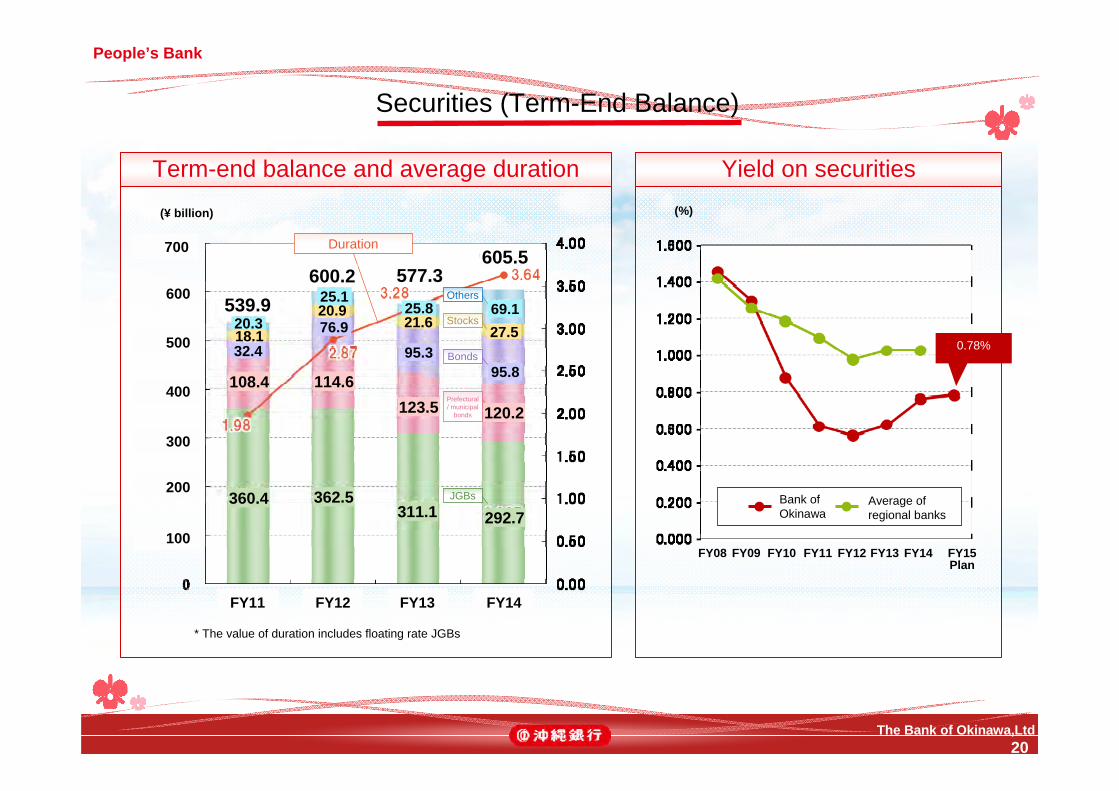

Securities (Term-End Balance)

Term-end balance and average duration Yield on securities

(¥ billion)

Duration

* The value of duration includes floating rate JGBs

Average of regional banks

Bank of Okinawa

(%)

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15Plan

JGBs

Prefectural / municipal

bonds

Bonds

Others

Stocks

0.78%

600

500

400

300

200

100

700

FY11 FY12 FY13 FY14

360.4 362.5311.1 292.7

108.4 114.6123.5 120.2

32.476.9

95.395.8

18.1

20.921.6 27.520.3

25.125.8 69.1539.9

600.2 577.3605.5

The Bank of Okinawa,Ltd21

People’s Bank

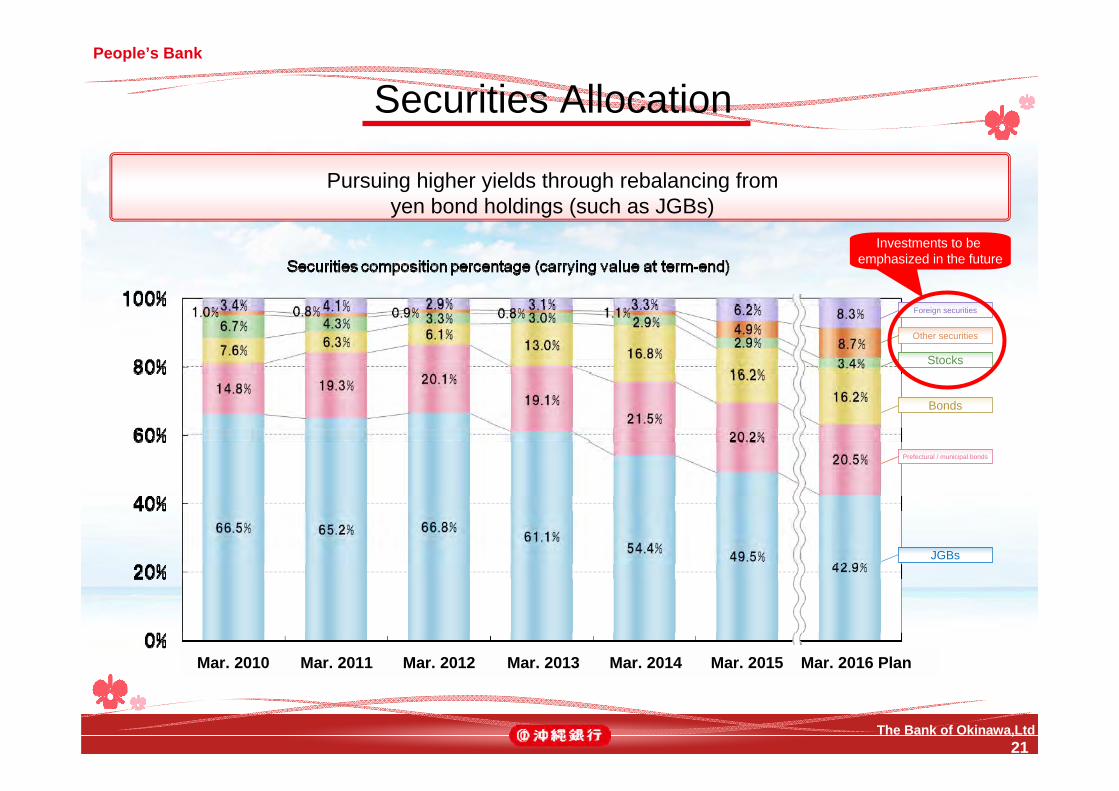

Securities Allocation

Pursuing higher yields through rebalancing from yen bond holdings (such as JGBs)

Stocks

Prefectural / municipal bonds

Foreign securities

JGBs

Bonds

Other securities

Investments to be emphasized in the future

Mar. 2016 PlanMar. 2010 Mar. 2011 Mar. 2012 Mar. 2013 Mar. 2014 Mar. 2015

The Bank of Okinawa,Ltd22

People’s Bank

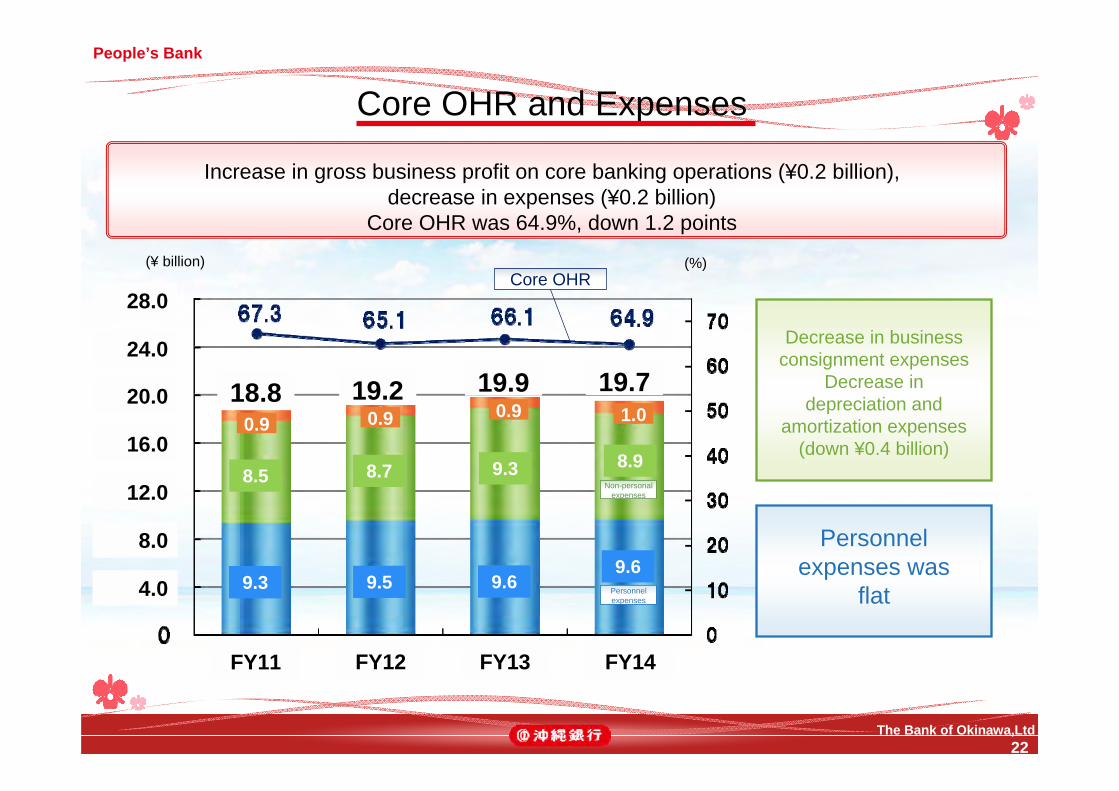

Core OHR and Expenses

Increase in gross business profit on core banking operations (¥0.2 billion), decrease in expenses (¥0.2 billion)

Core OHR was 64.9%, down 1.2 points

(¥ billion) (%)

Decrease in business consignment expenses

Decrease in depreciation and

amortization expenses(down ¥0.4 billion)

Personnel expenses was

flat

Non-personal expenses

Personnel expenses

Core OHR28.0

24.0

20.0

16.0

12.0

8.0

4.0

18.80.9

8.5

9.3

19.20.9 0.9

8.7

9.5

9.3

19.9

9.69.6

19.71.0

8.9

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd23

People’s Bank

Full application based capital ratio

Capital Ratio (Basel III Standard)

Capital ratio (domestic standard) at 11.13%

Outlier Ratio

Total interest rate risk Outlier ratio

End of March 2015

¥5,321 million 4.44%

Yen: 1 percentile, Foreign currencies: 99 percentile

Core deposits are assumed to be 50% of the term-end balance of liquid deposits.The average maturity is assumed to be 2.5 years.

Capital ratio Tier I ratio

Average capital ratio of regional banks in the term ended March 2015 (domestic standard): 10.59%

Core capital

Calculated by new standard

(%)

Source: Bank of Okinawa

(Non-consolidated) 10.93%11.13%

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd24

People’s Bank

Risk Management - Capital Allocation -

Controlling risks within the scope of allocated economic capital

Credit risk Market risk Loan / deposit interest risk Operational risk

Holding period 1 year

Strategic share holdings:1 yearOthers:1 month

1 yearBasic indication approach (BIA)Confidence

interval 99% 99% 99%Observation

period 1 year 1 year 1 year

■ Basis for risk calculation

Buffer

Unallocated capital

Allocated risk capital

(¥ billion)

Operational risk

Loan / deposit interest risk

Market risk

Credit risk

120

100

80

60

40

20

112.0

40.0

20.0

52.0

52.05.012.0

19.0

16.0

4.424.1

3.08.77.9

Breakdown of risk capital in FY14

Risk amount(end of FY14)

Allocated economic capital

The Bank of Okinawa,Ltd25

People’s Bank

Credit Cost

Reflecting a drop in historical loan loss rates, total credit costs amounted to ¥1.6 billion (down ¥1.2 billion YoY)

(¥ billion)

Provision of general allowance for possible loan losses

Credit cost ratio

(%)

(0.3)

Bad debt disposal

Reversal of general allowance for possible loan losses

3.0

2.5

2.0

1.5

1.0

0.5

1.1

1.6

2.8(2.2+0.6)

2.21.9 2.0

1.6(1.9-0.3)

Plan

FY15FY12 FY13 FY14

The Bank of Okinawa,Ltd26

People’s Bank

Mandatory Disclosure of Bad Debt under the Financial Reconstruction Law

¥21.4 billion (1.61%)Non-performing loan (NPL) ratio down 0.11% reflecting a decrease in bankrupt and quasi-bankrupt assets

(¥ billion) (%)

Assets requiring supervision

Bankrupt and quasi-bankrupt assets

NPL ratio

Doubtful assets

30.0

20.0

10.0

11.5

6.7

1.5

10.9

6.4

3.0

9.9

8.2

3.6

21.4

5.8

10.3

5.2

21.0

FY15 FY14 FY13 FY12 FY11

19.8 20.5 21.7

NPL ratio(regional bank average,

source: Bank of Okinawa)

The Bank of Okinawa,Ltd27

People’s Bank Our Share of the Market Served by the Three Okinawan Regional Banks (FY2014)

Deposits (average balance)

(%)(%)

Loans: 42.24% Loans: 42.24% (down 0.50 points YoY)(down 0.50 points YoY)

Deposits: 42.10% Deposits: 42.10% (up 0.13 points YoY)(up 0.13 points YoY)

Deterioration in shares of loans; increase in shares of deposits

Loans (average balance)

FY11 FY12 FY13 FY14 FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd28

Business Strategies

The Bank of Okinawa,Ltd29

People’s Bank

From Customer Focused Operational Reforms to New Value Creation1. Outline of Medium-Term Business Plan “CHANGE FOR VALUE – Three Years of New Value Creation –” (1)

17th Medium-Term Business Plan CHANGE FOR VALUE - Three Years of New Value Creation - April 2015 to March 2018 (3 years)

- From “Customer focused operational reforms (change)” to “Customer focused new value creation” -We will continue to grow together with regional customers as the “PEOPLE’S BANK,” most loved by people in Okinawa, by materializing

“operational reforms (change)” for the new era with our customer focused attitude that we have built to create and offer “customer focused new value” based on the well-established attitude.

Three basic strategies to undertake in “Three Years of New Value Creation”

“Customer focused”operational reforms “Customer focused” new value creation Productivity improvement using strategic information

- Operational reforms materializing “customer’s point of view”(Delegation of power, downsizing, streamlining)

- Initiative toward fundamental improvement of customer waiting time

- Establishing sales structure which customers can feel the “attraction”

- Establish and put into practice the PDCA cycle for high quality humanresource development

- Expand service value at “customer contact point (sales base)”

- Materialize new services combined with our brand strategy

- Materialize PDCA that is backed by information

- Build strategies to utilize IT, which the value will be

acknowledged by customers(Shift from using IT for streamlining to value creation)

Materialization of a new sustainable business model which the value will be recognized by customers

Contribute to revitalization of regional communities as the No.1 bank in the region

The Bank of Okinawa,Ltd30

People’s Bank

Achievements of “Customer Focused” Strategy - Clarifying the Top Priorities to Address -

Clarify that “customer satisfaction” and “employee satisfaction” are the top priority issues for building a sustainable business model

Medium-Term Business Plan - CHANGE FOR VALUE -Past priority order

Priority

1. CustomersEmployees

1. Soundness 1. Profitability

1. Scale / share

Priority Basic concept

1. Customer satisfactionThe significance of our existence is “customer satisfaction” through implementation of “management philosophy (deeply rooted in the community/contribution to the community),” and we define this as the top priority in order to survive the era of great competition.

2. Employee satisfactionWe will realize the “PEOPLE’S BANK,” loved by people in Okinawa, filled with motivation and dynamics of our employees, by putting into practice that “customer satisfaction” is the true reward for working

3. Profitability Complete operational reforms to strengthen the top line revenue backed by customer satisfaction

4. Soundness Maintain the No.1 soundness within the prefecture and contribute to continued development of Okinawa

5. Scale / share in prefecture Steadily expand our customer base by being chosen by the customers, through increase of customer satisfaction level

The Bank of Okinawa,Ltd31

People’s Bank

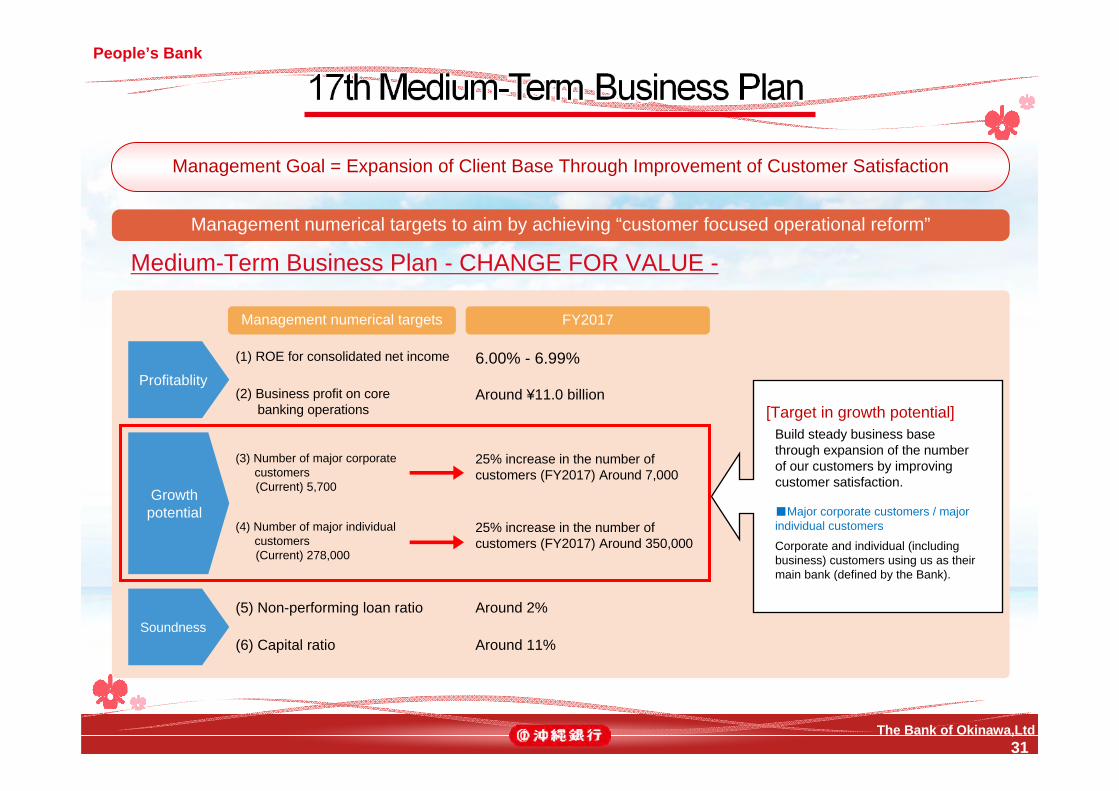

Management Goal = Expansion of Client Base Through Improvement of Customer Satisfaction

Management numerical targets to aim by achieving “customer focused operational reform”

Medium-Term Business Plan - CHANGE FOR VALUE -

Profitablity

Growth potential

Soundness

(1) ROE for consolidated net income

(2) Business profit on core banking operations

Management numerical targets FY2017

6.00% - 6.99%

Around ¥11.0 billion

(3) Number of major corporate customers (Current) 5,700

25% increase in the number of customers (FY2017) Around 7,000

(4) Number of major individual customers (Current) 278,000

25% increase in the number of customers (FY2017) Around 350,000

(5) Non-performing loan ratio

(6) Capital ratio

Around 2%

Around 11%

[Target in growth potential]Build steady business base through expansion of the number of our customers by improving customer satisfaction.

■Major corporate customers / major individual customers

Corporate and individual (including business) customers using us as their main bank (defined by the Bank).

The Bank of Okinawa,Ltd32

People’s Bank

Growth Strategy I: Expansion of Corporate (Business) Customers

Evaluation of business potentials:Financial institutions should facilitate the growth of companies and industries based

on an assessment of borrower companies’ business profiles and growth potential (evaluation of customers’ business potentials), providing financing and advice without overly relying on financial data, collateral and guarantees.(Excerpt from the Financial Monitoring Policy for 2014-2015)

Life cycle

Mission of Corporate Sales Division

[Life cycle of corporate customers]

Foundation Growth Downturn Recovery Stabilization Transition Growth

Foundation support

Sales channels expansion supportMatching

We will expand corporate (business) customers who would use us as their main bank by offering services by utilizing “consulting functions” according to the life cycle of corporate (business) customers.

Business revitalization supportManagement restructuring plan

Business successionM&As

Sales channels expansion supportMatching

Capital for foundation /

new businessWorking capital / Capital expenditure EXIT financing

Capital expenditure /

working capital

Exercising of consulting functions

[Building a new business model]ALL OKIGIN FOR OKINAWA

Collaboration with 21st Century Vision of Okinawa

Overseas development support

Continued support for Okinawa Great Trade

Fair

Growing industries support

PFI promotion

Syndication

Financial analysis Management plan formation support

Exercising of investment target spotting function

Evaluation of

business potentials

Implement activities to

increase sales to SR by 5%

The Bank of Okinawa,Ltd33

People’s Bank

Growth Strategy II: Expansion of Individual Customers

We will expand individual customers who would use us as their main bank by promptly offering appropriate financial services according to the life cycle of individual customers.

Salary payment deposit / pension

Tablet strategy(loans / assets in custody)

Variety of mortgage loans(proper / comprehensive guarantee / health care

service)

New products including reverse

mortgagesCredit card

strategyProvision of

services according to the customer’s

life cycle

Automobile loan, mortgage loan, education loan, renovation loan

Salary payment deposit, asset building, accumulation savings

Investment trust, JGBs, foreign-currency depositsWhole life insurance, personal pension insurance, medical insurance, educational endowment insurance

Pension insurance

Borrow

Save

Increase

Prepare

Leave

Life cycle 20’s 30’s 40’s 50’s 60’s 70’s and after

Mission of Individual Sales Division

[Life cycle of customers]

Employment Marriage Home purchase

Car purchase Childbirth and parentingChildren’s higher

education/marriage

Satisfying retirement life (trips, hobbies, etc.)

Nursing care

ALL OKIGIN FOR OKINAWA(Enhance collaboration with credit card /

guarantee subsidiaries in particular)

The Bank of Okinawa,Ltd34

People’s Bank

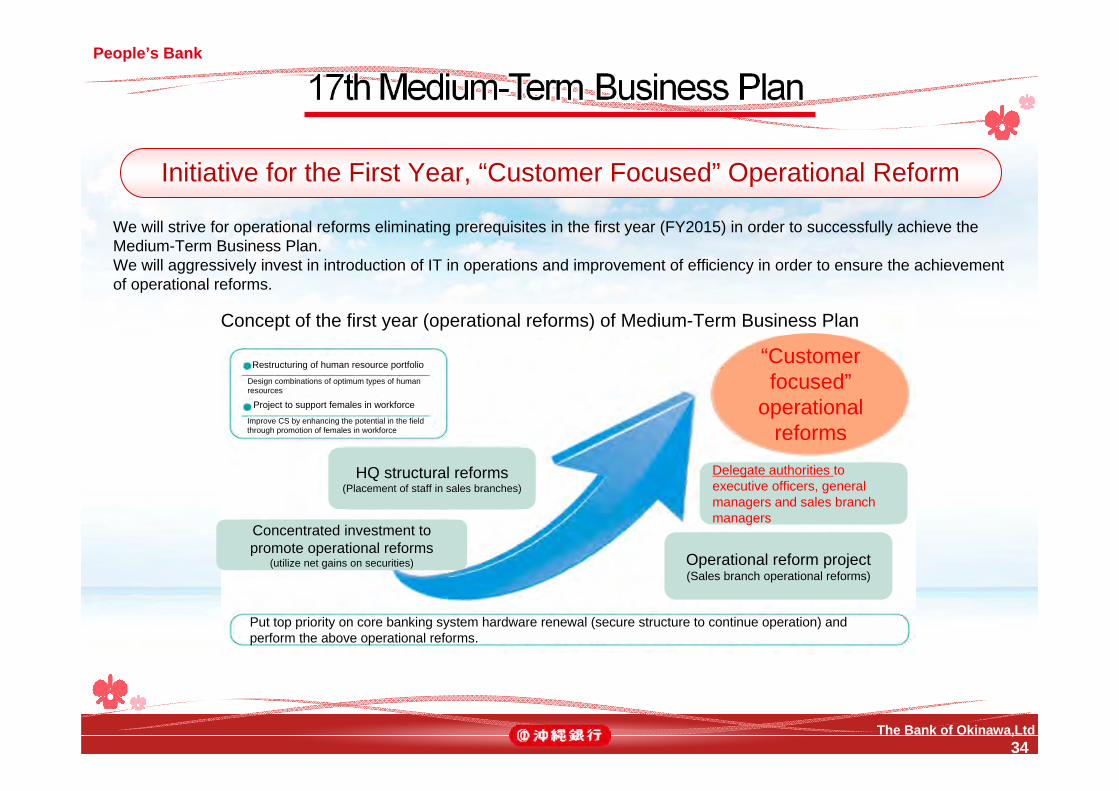

Initiative for the First Year, “Customer Focused” Operational Reform

Concept of the first year (operational reforms) of Medium-Term Business Plan

Restructuring of human resource portfolio

Project to support females in workforce

Improve CS by enhancing the potential in the field through promotion of females in workforce

Design combinations of optimum types of human resources

“Customer focused”

operational reforms

HQ structural reforms(Placement of staff in sales branches)

Concentrated investment to promote operational reforms

(utilize net gains on securities)

Delegate authorities to executive officers, general managers and sales branch managers

Operational reform project(Sales branch operational reforms)

Put top priority on core banking system hardware renewal (secure structure to continue operation) and perform the above operational reforms.

We will strive for operational reforms eliminating prerequisites in the first year (FY2015) in order to successfully achieve theMedium-Term Business Plan.We will aggressively invest in introduction of IT in operations and improvement of efficiency in order to ensure the achievementof operational reforms.

The Bank of Okinawa,Ltd35

People’s Bank

Business Performance Forecasts

Non-consolidatedFY14 FY15 YoY

change

Ordinary income 36.4 36.7 +0.2

Gross business profit 30.5 30.6 +0.0

Interest income 27.8 27.6 (0.1)

Fees and commissions 2.3 2.3 +0.0Fees and commissions (excluding trust fees) 2.0 2.0 +0.0

Trust account services 0.3 0.3 (0.0)

Other business profit 0.3 0.6 +0.2

Gains (losses) on bond trading 0.2 0.6 +0.3

Expenses (excluding non-recurrent items) 19.7 20.8 +1.0

Business profit on core banking operations 10.6 9.2 (1.4)

Provision of general allowance for possible loan losses (0.3) 0.0 +0.3

Net business profit 11.2 9.8 (1.3)

Non-recurrent items (1.2) (1.2) +0.0

Net gains (losses) on equity securities 0.1 0.4 +0.2

Bad debt disposal (non-recurrent items) 1.9 2.0 +0.0

Ordinary profit 9.9 8.5 (1.3)

Extraordinary gains (losses) (0.1) (0.0) 0.0

Net income 6.7 5.6 (1.1)

Credit costs 1.6 2.0 +0.3

Average balance Yield Interest

Loans and bills discounted

+68.8[+67.6]

(0.12)[(0.12)]

(0.2)[(0.3)]

Securities +4.7 +0.02 +0.1

Deposits +76.1[+76.5]

(0.00)[(0.00)]

(0.0)[(0.0)]

Others - - (0.0)[(0.0)]

Total - - (0.1)[(0.2)]

■ Year-on-year changes forecast(¥ billion)

■ YoY comparison of business profit on core banking operations

Note) Figures in square brackets include trust accounts.

Interest on securities

0.2

Interest paid on deposits

Others

Commissions

Expenses

Trust account services

Interest on loans and bills discounted

IncreaseDecrease

Total1.5

0.1

0.1

1.0

0.0

0.0

0.10.0

(¥ billion, %)

The Bank of Okinawa,Ltd36

People’s Bank

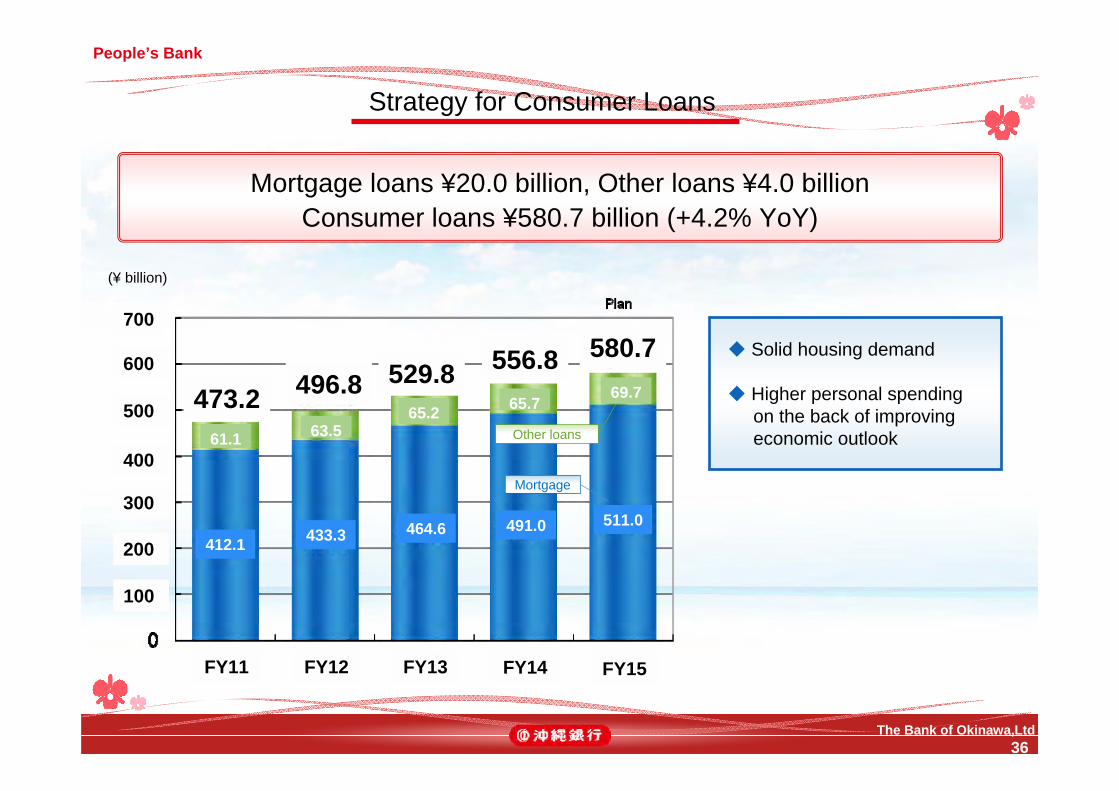

Strategy for Consumer Loans

Mortgage loans ¥20.0 billion, Other loans ¥4.0 billionConsumer loans ¥580.7 billion (+4.2% YoY)

(¥ billion)

◆ Solid housing demand

◆ Higher personal spending on the back of improving economic outlook

Mortgage

Other loans

100

200

300

400

500

600

700

473.261.1

412.1

496.863.5

433.3

529.865.2

464.6

556.865.7

491.0

580.769.7

511.0

FY15 FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd37

People’s Bank

Strategy for Assets in Custody

Boost sales focusing mainly on pension insurance and investment trusts

(¥ billion)

Investment trusts

Targeted sales volume¥21.0 billion

Investment trust

Targeted sales volume¥25.0 billion

Pension insurance

* Pension insurance totals are cumulative sums sold.* Sales target added to the balance as of the end of the previous fiscal year for the fiscal year ending March 31, 2015 excludes contract and other cancellations.

Targeted sales volume¥0.1 billion

JGBs

250

50

100

150

200

123.3

52.4

39.0

31.9

139.4

69.7

45.2

24.4

150.7

90.1

40.3

20.1

110.8

46.7

16.8

174.4

220.4

135.8

67.7

16.9

Plan

JGBs

Pension insurance

FY15 FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd38

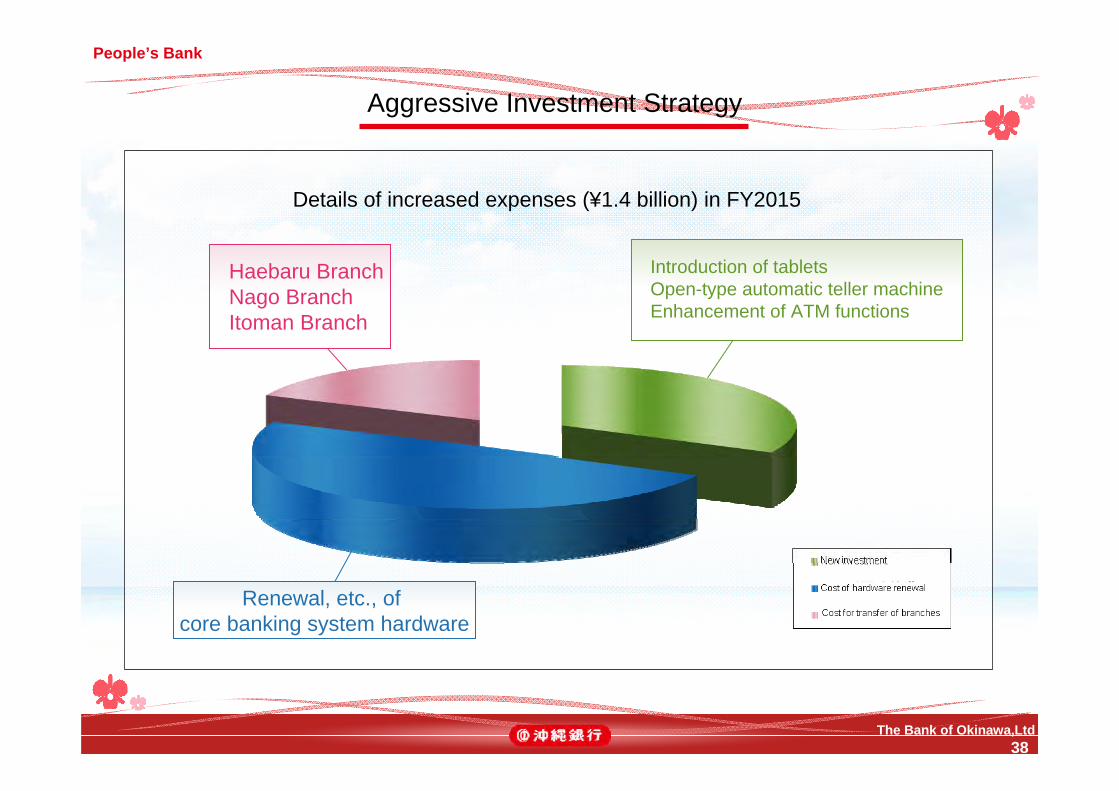

People’s Bank

Aggressive Investment Strategy

Details of increased expenses (¥1.4 billion) in FY2015

Renewal, etc., of core banking system hardware

Introduction of tabletsOpen-type automatic teller machineEnhancement of ATM functions

Haebaru BranchNago BranchItoman Branch

The Bank of Okinawa,Ltd39

People’s Bank

Branch Network Strategy

Efficient branch allocation through area marketingSetting up branches focusing on customer convenience

◆ October 2014 Yamauchi Branch (former Moromi Branch) relocated and re-opened for business

◆ April 2015 Haebaru Branch relocated and re-opened for business

◆ July 2015 Nago Branch scheduled to relocate, be newly built and re-opened for business

Yamauchi Branch Haebaru Branch Nago Branch

The Bank of Okinawa,Ltd40

People’s Bank

Shareholder Returns

FY11 FY12 FY13 FY14 FY15(forecast)

Payout ratio (%) 22.4 22.3 25.0 19.4 23.4 Total return ratio (%) 30.8 34.1 36.4 33.7Dividend (yen) 65 65 65 70 70Share buy back

(million yen) 498 700 602 1,055 -

Up ¥2.5 for the interim dividend for FY2014 (up ¥5 annually)Shareholder returns with stable dividend and flexible share buy back

Ordinary shares issued (excluding treasury shares)Purchase of treasury shares

Total return ratio (%)Payout ratio (%)

FY15 forecast

FY14FY13FY12FY11FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

The Bank of Okinawa,Ltd41

Supplemental Materials

The Bank of Okinawa,Ltd42

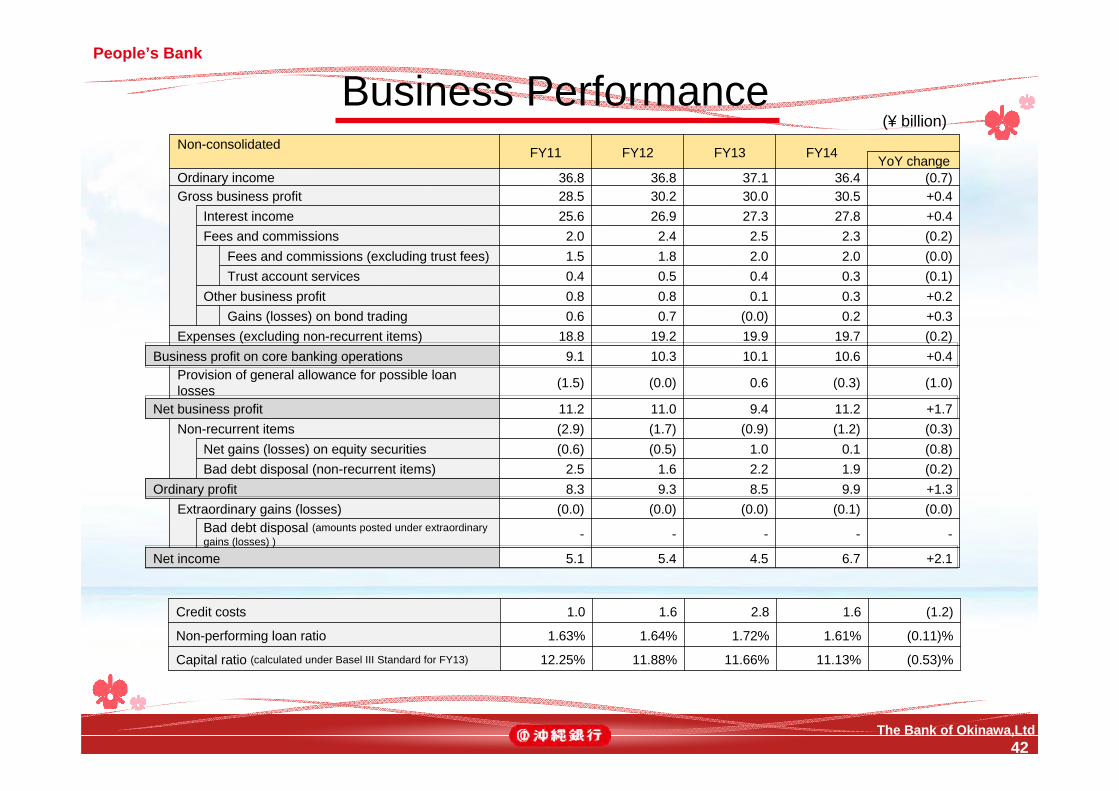

People’s Bank

Business PerformanceNon-consolidated FY11 FY12 FY13 FY14 YoY changeOrdinary income 36.8 36.8 37.1 36.4 (0.7)Gross business profit 28.5 30.2 30.0 30.5 +0.4

Interest income 25.6 26.9 27.3 27.8 +0.4Fees and commissions 2.0 2.4 2.5 2.3 (0.2)

Fees and commissions (excluding trust fees) 1.5 1.8 2.0 2.0 (0.0)Trust account services 0.4 0.5 0.4 0.3 (0.1)

Other business profit 0.8 0.8 0.1 0.3 +0.2Gains (losses) on bond trading 0.6 0.7 (0.0) 0.2 +0.3

Expenses (excluding non-recurrent items) 18.8 19.2 19.9 19.7 (0.2)Business profit on core banking operations 9.1 10.3 10.1 10.6 +0.4

Provision of general allowance for possible loan losses (1.5) (0.0) 0.6 (0.3) (1.0)

Net business profit 11.2 11.0 9.4 11.2 +1.7Non-recurrent items (2.9) (1.7) (0.9) (1.2) (0.3)

Net gains (losses) on equity securities (0.6) (0.5) 1.0 0.1 (0.8)Bad debt disposal (non-recurrent items) 2.5 1.6 2.2 1.9 (0.2)

Ordinary profit 8.3 9.3 8.5 9.9 +1.3Extraordinary gains (losses) (0.0) (0.0) (0.0) (0.1) (0.0)

Bad debt disposal (amounts posted under extraordinary gains (losses) ) - - - - -

Net income 5.1 5.4 4.5 6.7 +2.1

Credit costs 1.0 1.6 2.8 1.6 (1.2)

Non-performing loan ratio 1.63% 1.64% 1.72% 1.61% (0.11)%

Capital ratio (calculated under Basel III Standard for FY13) 12.25% 11.88% 11.66% 11.13% (0.53)%

(¥ billion)

The Bank of Okinawa,Ltd43

People’s Bank Term-End Balance, Average Balance, Yield, and Loan Balance by Industrial Segment

Term-end balance / Average balance / Yield Loan balance by industrial segment

FY11 FY12 FY13 FY14

Loans

Term-end balance 1,197.1 1,236.2 1,251.4 1,313.8

Average balance 1,121.7 1,154.7 1,202.0 1,254.9

Yield 2.44 2.32 2.17 2.03

Securities

Term-end balance 539.9 600.2 577.3 605.5

Average balance 509.6 581.8 583.6 551.7

Yield 0.61 0.56 0.62 0.76

Deposits

Term-end balance 1,714.8 1,789.8 1,755.1 1,865.4

Average balance 1,670.4 1,706.5 1,745.6 1,813.1

Yield 0.26 0.14 0.11 0.09

* Term-end and average balances are calculated on the basis of loan/deposit balances of the banking and trust accounts.

* Yields on loans and deposits are those used for domestic operations only.

FY11 FY12 FY13 FY14

Manufacturing 40.5 37.9 36.6 37.0

Agriculture and forestry 0.5 0.4 0.5 0.8

Fishery 0.5 0.5 0.5 0.5

Mining and quarrying of stone and gravel 3.9 1.5 1.9 1.7

Construction 49.7 47.3 44.7 42.0

Electricity, gas, heat and water supply 4.0 2.5 3.5 6.8

Telecommunications 10.0 7.9 7.2 8.9

Transport and postal activities 16.4 15.0 14.8 16.6

Wholesaling and retailing 116.4 115.7 114.8 107.1

Finance and insurance 18.9 22.1 25.0 26.3

Real estate, and goods rental and leasing 227.4 261.9 294.8 326.3

Miscellaneous services 137.1 137.2 129.5 142.9

Local government bodies 123.8 127.3 98.3 99.9

Others 447.3 458.4 478.6 496.4

Total 1,197.1 1,236.2 1,251.4 1,313.8

* Including trust accounts

(¥ billion, %) (¥ billion)

The Bank of Okinawa,Ltd44

People’s Bank Changes in Loan Balance by Assets Category (FY2013 and FY2014)

Loan balance by assets category at the end of March 2014

Loan balance by assets category at the end of March 2015 (¥1,325.1 billion)

Normal assets

Assets requiring cautionPotentially bankrupt assets

Bankrupt and effectively

bankrupt assetsOther assets

requiring caution

Assets requiring

supervision

Normal assets 1,082.9 1,057.6 26.8 0.3 0.2 0.2

Assets requiring caution

Other assets requiring caution 156.5 18.9 118.2 2.9 4.4 0.9

Assets requiring supervision 4.7 0.0 0.2 2.5 1.2 0.0

Potentially bankrupt assets 8.2 0.0 0.5 0.2 4.1 0.3

Bankrupt and effectively bankrupt assets 9.9 0.1 0.2 0.2 0.1 4.2

New borrowers - 75.8 3.9 0.0 0.0 0.0

Total 1,262.4 1,152.6 149.9 6.3 10.3 5.8

(¥ billion)(¥ billion)

The Bank of Okinawa,Ltd45

People’s Bank

Interest Sensitivity

Loans Deposit

High

Low

High

Low

Total loans: ¥1,251.6 billionTotal deposits: ¥1,865.4 billion

Time deposits(over 1 year)

5.6%

Loans on bills / bills discounted(fixed portion)

8.6%

Current account deposits51.8%

Fixed interest32.9%

Time deposits(up to 1 year)

and money in trust42.6%

The Bank of Okinawa,Ltd46

People’s Bank

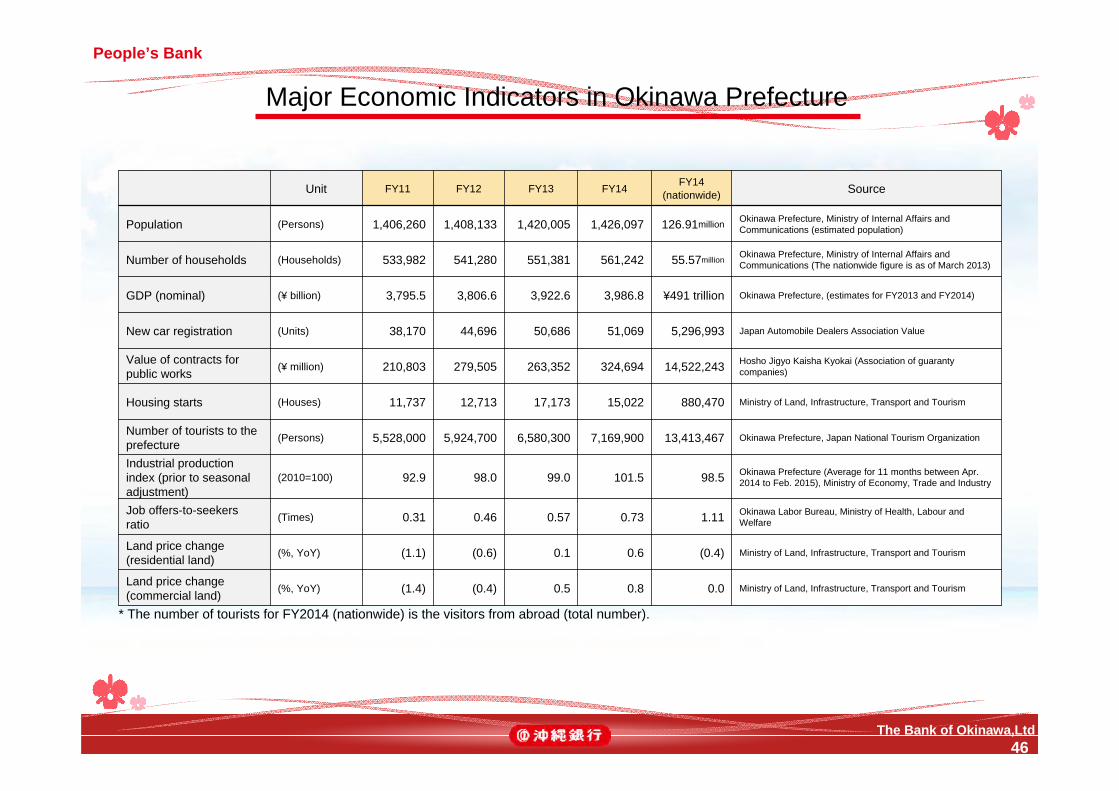

Major Economic Indicators in Okinawa Prefecture

Unit FY11 FY12 FY13 FY14 FY14(nationwide) Source

Population (Persons) 1,406,260 1,408,133 1,420,005 1,426,097 126.91million Okinawa Prefecture, Ministry of Internal Affairs and Communications (estimated population)

Number of households (Households) 533,982 541,280 551,381 561,242 55.57million Okinawa Prefecture, Ministry of Internal Affairs and Communications (The nationwide figure is as of March 2013)

GDP (nominal) (¥ billion) 3,795.5 3,806.6 3,922.6 3,986.8 ¥491 trillion Okinawa Prefecture, (estimates for FY2013 and FY2014)

New car registration (Units) 38,170 44,696 50,686 51,069 5,296,993 Japan Automobile Dealers Association Value

Value of contracts for public works (¥ million) 210,803 279,505 263,352 324,694 14,522,243 Hosho Jigyo Kaisha Kyokai (Association of guaranty

companies)

Housing starts (Houses) 11,737 12,713 17,173 15,022 880,470 Ministry of Land, Infrastructure, Transport and Tourism

Number of tourists to the prefecture (Persons) 5,528,000 5,924,700 6,580,300 7,169,900 13,413,467 Okinawa Prefecture, Japan National Tourism Organization

Industrial production index (prior to seasonal adjustment)

(2010=100) 92.9 98.0 99.0 101.5 98.5 Okinawa Prefecture (Average for 11 months between Apr. 2014 to Feb. 2015), Ministry of Economy, Trade and Industry

Job offers-to-seekers ratio (Times) 0.31 0.46 0.57 0.73 1.11 Okinawa Labor Bureau, Ministry of Health, Labour and

Welfare

Land price change (residential land) (%, YoY) (1.1) (0.6) 0.1 0.6 (0.4) Ministry of Land, Infrastructure, Transport and Tourism

Land price change (commercial land) (%, YoY) (1.4) (0.4) 0.5 0.8 0.0 Ministry of Land, Infrastructure, Transport and Tourism

* The number of tourists for FY2014 (nationwide) is the visitors from abroad (total number).

The Bank of Okinawa,Ltd47

Statements contained in these materials regarding forecasts of future events are based on information known to the management at the time of writing, and do not constitute any form of guarantee of the business performance of the Bank of Okinawa. These materials have been prepared to serve as a report on the settlement of accounts of the Bank for the fiscal 2014 term, ended March 2015, as well as to provide an explanation of the Bank’s future management vision: they are not intended as a solicitation of business.

For further details, please contact:The Bank of Okinawa, Ltd. General Planning Division,

Management Planning Group

Tel: 81-98-869-1253 / Fax: 81-98-869-1464