fiscal updates and uniform guidancefiles.ctctcdn.com/9a69fb8e201/ed060512-7c5a-478f-846a-c7...fiscal...

TRANSCRIPT

Fiscal Updates andUniform Guidance

Belinda Rinker

Senior Policy Analyst

Office of Head Start

Play in Slide Show mode to activate hyperlinks.

THE UNIFORM GUIDANCE

45 CFR Part 75—Uniform Administrative Requirements, Cost Principles and Audit Requirements

2

Change in Focus

• The Uniform Guidance reflects a focus on performance over compliance for accountability.

• What does this mean for fiscal management?

Performance

(Quality of Outcome)

Staff

Money

Property

3

Compliance

Uniform Guidance Overview

• Applies to awards and award increments made after December 26, 2014.

• Procurement requirements must be implemented by December 26, 2015.

• Information to assist Head Start grantees with implementation has been reorganized on the Early Childhood Learning and Knowledge Center (ECLKC) website.

• The Council on Financial Assistance Reform (COFAR) has issued new Frequently Asked Questions and responses updated as of September, 2015.

• The Uniform Guidance isn’t Uniform and it isn’t Guidance.

• All grantees need to review and update their fiscal policies and procedures to implement the new Uniform Guidance.

4

Uniform Guidance Resources on ECLKC

5

Council on Financial Assistance Reform (COFAR) New Uniform Guidance Resources

6

Council on Financial Assistance Reform (COFAR) New Uniform Guidance Resources

7

TableActivity

8

• Spend a few minutes talking with others at your table about implementing the new Uniform Guidance at your program.

• What kinds of changes have programs made in response to the new regulations?

• What challenges have been encountered in fully implementing the new regulations?

A QUIZ – BE SURE TO KEEP SCORE

How well do you know the requirements of the new Uniform Guidance?

9

Fact or Fiction?Personnel activity reports (PARs) are gone for good. No more PARs.

Fact(ish)45 CFR §75.430 Compensation – Personnel Services. The non-Federal entity's system of internal controls includes processes to review after-the-fact interim charges made to a Federal awards based on budget estimates. All necessary adjustment must be made such that the final amount charged to the Federal award is accurate, allowable, and properly allocated. 10

Fact or Fiction?The new fiscal regulations supersede the 15% administrative cost limitation in the Head Start Act.

Fiction45 CFR §75.104 Supersession. Regulations and guidance required by statute are not superseded.

11

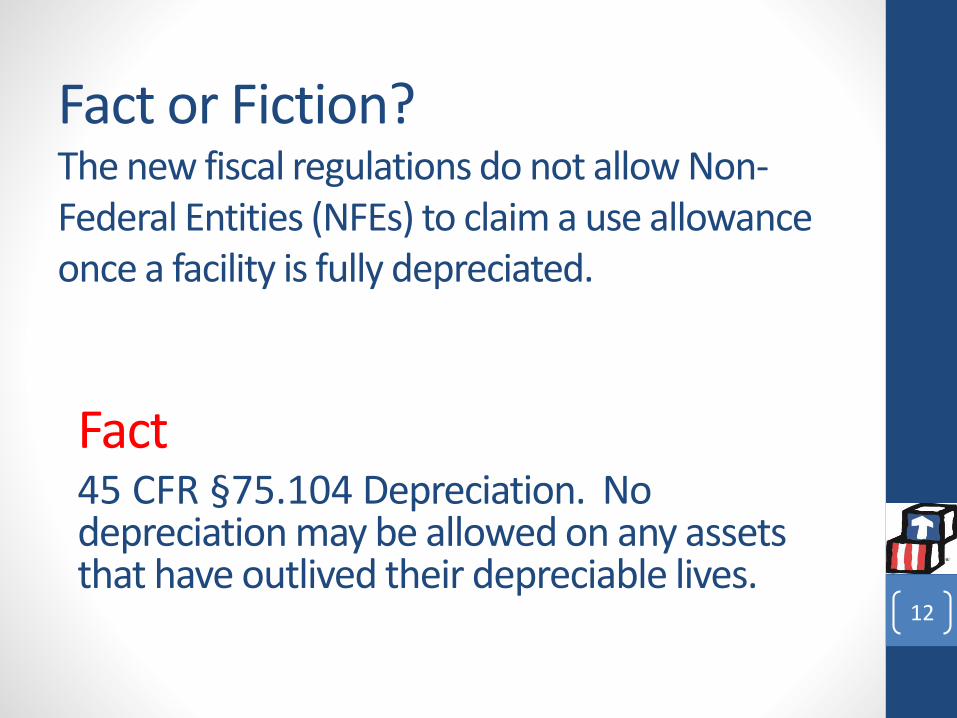

Fact or Fiction?The new fiscal regulations do not allow Non-Federal Entities (NFEs) to claim a use allowance once a facility is fully depreciated.

Fact45 CFR §75.104 Depreciation. No depreciation may be allowed on any assets that have outlived their depreciable lives.

12

Fact or Fiction?Prior ACF approval is required for transfers among budget categories that exceed 10% of the total budget.

Fiction45 CFR §75.308 (e) Revision of Budget. The HHS awarding agency may, at its option, restrict the transfer of funds among direct cost categories when the cumulative amount of such transfers exceeds or is expected to exceed 10 percent of the total budget as last approved by the HHS awarding agency. ACF continues to utilize the following definition of significant re-budgeting: cumulative transfers among direct cost budget categories for the current budget period exceed 25 percent of the total approved budget (inclusive of direct and indirect costs and Federal funds and required matching or cost sharing) for that budget period or $250,000, whichever is less.

13

Fact or Fiction?The new fiscal regulations require that every NFE obtain a negotiated indirect cost rate from the cognizant Federal agency.

FictionAppendices IV through VIII and 45 CFR §75.104.

Direct allocation is recognized as acceptable so long as shared costs are prorated based on proportional benefit. 14

Fact or Fiction?Supplies with an aggregate value of $2,500 can be purchased from a local discount store without competition.

Fact45 CFR §75.329(a) Procurement. Micro-purchases may be awarded without soliciting competitive quotations if the non-Federal entity considers the price to be reasonable. 45 CFR §75.2 Micro-purchase means a purchase of supplies or services using simplified acquisition procedures, the aggregate amount of which does not exceed $3,000.

15

Fact or Fiction?Costs of organized fund raising are unallowable.

Fact45 CFR §75.104. Costs of organized fund raising, including financial campaigns, endowment drives, solicitation of gifts and bequests, and similar expenses incurred to raise capital or obtain contributions are unallowable. Fund raising costs for the purposes of meeting the Federal program objectives are allowable with prior written approval from the Federal awarding agency.

16

Fact or Fiction?NFEs can charge the cost of professional grant writers directly to the Head Start program.

Fiction45 CFR §75.460. Proposal costs are the costs of preparing bids, proposals, or applications on potential Federal and non-Federal awards or projects, including the development of data necessary to support the non-Federal entity's bids or proposals. Proposal costs of the current accounting period of both successful and unsuccessful bids and proposals normally should be treated as indirect (F&A) costs and allocated currently to all activities of the non-Federal entity. No proposal costs of past accounting periods will be allocable to the current period.

17

Fact or Fiction?During the budget year a grantee can replace equipment worth up to $25,000.

Fiction45 CFR §75.308(c)(11). Prior approval is required to dispose of, replace or encumber title to equipment acquired with a Federal award. 45 CFR §75.2 Equipmentmeans tangible personal property (including information technology systems) having a useful life of more than one year and a per-unit acquisition cost which equals or exceeds the lesser of the capitalization level established by the non-Federal entity for financial statement purposes, or $5,000. 18

Fact or Fiction?Small purchases at or below $150,000 do not require free and open competition and can be sole sourced.

Fiction

45 CFR §75.329(b) Procurement. Price or rate quotations shall be obtained from an adequate number of qualified sources.

19

TableActivity

20

• Spend a few minutes talking with others at your table about the Uniform Guidance quiz.

• How many of the quiz questions did you answer correctly?

• Did anything surprise you as a result of taking the quiz?

• Have you identified any next-steps as a result of the quiz?

SF-429

Real Property Reporting and Request Requirements

21

Real Property Reporting

Information about real property acquired or improved with Federal funds must be reported annually: Effective for budget periods beginning on or after Dec. 26, 2014, all grantees, including those with no covered real property, are instructed to use and submit Standard Form (SF) 429. It includes the following real property reporting and request forms:• Instructions for 429 [PDF, 111KB]• SF-429-A (General Reporting; includes the cover page) [PDF, 163KB]• SF-429-B (Request to Acquire, Improve, or Furnish; includes the

cover page) [PDF, 143KB] • SF-429-C (Disposition or Encumbrance Request; includes the cover

page) [PDF, 117KB]

Real Property Reporting and Request Requirements ACF-IM-HS-15-01. 22

ANNUAL AUDIT

45 CFR Part 75—Uniform Administrative Requirements, Cost Principles and Audit Requirements

23

Audit Resources

• Audit threshold is now $750,000 per 45 CFR §75.501(a).• Audits in Head Start and Early Head Start

programs: 2014 Head Start Audit Compliance SupplementACF-IM-HS-14-05.• 2015 OMB Compliance Supplement is at

https://www.whitehouse.gov/omb/circulars/a133_compliance_supplement_2015. See HHS PDF Page 154.

24

OMB Circular A-133 Compliance Supplement 2015 Matrix Error –No Special Tests and Provisions

25

FISCAL OVERSIGHT

Early Head Start –Office of Child Care

Partnership Agreements

26

Early Head Start Child Care PartnershipsFiscal Monitoring of Partners

• Contractors

• Awardee must oversee contractor performance (§75.327(b)). Non-Federal entities must maintain oversight to ensure that contractors perform in accordance with the terms, conditions, and specifications of their contracts or purchase orders.

• Subrecipients

• Awardee must assure compliance with applicable Federal (fiscal) requirements and performance expectations (§75.352(d)). Non-Federal entities must monitor the activities of the subrecipient as necessary to ensure that the subaward is used for authorized purposes, in compliance with Federal statutes, regulations, and the terms and conditions of the subaward; and that subawardperformance goals are achieved.

• Specific actions are noted in §75.352(d)(1) – (3) and (e) – (f).27

Questions & Comments