flat glass

DESCRIPTION

From the stained glass windows of medieval churches to the Renaissance monopoly of Venetian mirror makers, flat glass has brought us protection from our environment, while also reflecting itsbeauty. Today’s flat glass still exhibits those ancient characteristics of form and function, while carrying us into the future as a performance platform for both practical and exotic technologies.TRANSCRIPT

28 GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

ABSTRACT

From the stained glass windows of medievalchurches to the Renaissance monopoly of Venetianmirror makers, flat glass has brought us protectionfrom our environment, while also reflecting itsbeauty. Today’s flat glass still exhibits those ancientcharacteristics of form and function, while carryingus into the future as a performance platform forboth practical and exotic technologies.

Using a wide variety of batch combinations,we take glass from our float lines and coat, bend,shape, laminate, and temper it. The resultingproducts provide us with year-round comfort,protect our fabrics from fading, reduce our energycosts, block sound transmission, improve oursecurity, and allow us to replace walls of brickand mortar with panoramas of light and naturalbeauty. Flat glass products also support leading-edge technologies such as flat-panel displays,liquid crystal, and computerization.

Flat glass is a product that is common to all ofus—but how we manufacture, distribute,fabricate, and market glass today is as unique asour individual cultures and customer bases. Toprepare for the future, we simply have to listen tothe needs of our customers—and respond withthe kinds of innovations that have characterizedour industry for the past 3500 years. While ourcustomer base has changed from the local princeand bishop to thousands of product applicationsworldwide, innovation continues to be the key tomeeting our customers’ needs—and carrying ona tradition of success.

1. INTRODUCTION

AFG Industries, owned by Asahi of Japan, isone of North America’s leading glass manu-facturers, with expertise in flat glass, coatingtechnologies, fabrication, and packaging. With 10float lines located across North America, AFGsupplies glass products to many leading windowfabricators, with a special focus on flat glass withlow-emissivity, energy-efficient coatings. AFG

also manufactures auto-motive, tinted, low-iron,and patterned glass.

With 51 fabrication and distribution locationsthroughout North America, AFGD specializes inarchitectural and commercial flat glass. AFGDmanufactures a wide variety of clear, mirror, lami-nated, tint, medium-performance, and high-per-formance products that can be found in buildingsacross North America.

This article will focus on the past, present, andfuture of the flat glass industry, and I’d like tobegin by looking back briefly at the history ofglass manufacturing, which began nearly 3500years ago.

2. THE HISTORY OF GLASSMANUFACTURING

Though the earliest glass was obsidian,naturally formed by volcanic eruptions, themanufacturing of glass began around 1500 B.C.in Egypt and Mesopotamia. These ancientcultures manufactured glass beads and glassvessels, using crude molding processes. Earlyglassmakers shaped soft glass by wrapping itaround a core of sand or clay, then cooling theglass and removing the core material. Finally, thecooled glass was cut and polished.

During the next millennium, glassmanufacturing became more widely practicedthroughout the ancient world, and severalimprovements were made in the basicglassmaking process, as well as the cutting ofglass. Glassmakers learned to add differentingredients to the glass to improve its strength,produce clearer glass, or produce glass in aspecific color. However, glass continued to bedifficult to produce, and was used primarily byroyalty or in religious services.

The glass industry saw its first revolution inabout 300 B.C., when Syrian glassmakersinvented the blowpipe, which enabled theproduction of glass in countless shapes andthicknesses. The invention of the blowpipe wassoon followed by the introduction of the two-part

THE HISTORY AND FUTURE OF THEFLAT GLASS INDUSTRY

Roger Kennedy, President and Chief Executive Officer, AFGD, Inc.AFG Industries, Inc.

1400 Lincoln Street, P.O. Box 929, Kingsport, Tennessee 37662, USA

29GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

glass mold, which made it easy for glassmakersto mass produce identical glass objects. Thesetwo developments made glass productsaffordable, and for the first time they wereavailable to the average citizen.

The Romans revolutionized glassmaking in thefirst century A.D. by using a variety ofmanufacturing processes—including free blowing,mold blowing, and mold pressing—to produce awide range of ornately shaped glass products. Flatwindow glass was produced by pouring moltenglass onto an iron table and stretching it—whichchanged the face of architecture. The RomanEmpire also produced flat glass by blowing hugeglass bubbles or cylinders, which were thenopened and flattened. They also began tomanufacture mirrors by applying a silver amalgamto their flat glass. These Roman innovations soonbegan to spread throughout Europe.

With the fall of the Roman Empire, however,much of the fine art of glassmaking was lost. InWestern Europe, glass again became a productreserved for the wealthy, and flat glass was usedto produce stained glass windows for medievalchurches. However, the Byzantine glass industrycontinued to produce some innovations. Around650 A.D., Syrian glassmakers developed arevolutionary new manufacturing method forproducing “crown” glass. Crown glass was madeby making a hole in a molten glass bubble, thenspinning the soft glass to produce a thin, circularpiece of glass with a distinctive “bulls-eye”pattern at its center. Because it was relativelyinexpensive to produce, crown glass would beused in windows until the late 19th century.

The Venetians, who had been importingByzantine glassware, began their own thrivingglass industry in the late 13th century. In order toprotect “trade secrets,” all Venetian glasshouseswere moved to the island of Murano, where theItalian glassmaking Renaissance continued forthe next several centuries. The Venetiansperfected a manufacturing process for plateglass, which involved casting colorless glass onan iron table, and then polishing the sheet ofglass until no distortions remained. TheVenetians also developed a mercury foilingprocess that produced mirrors renownedthroughout Europe. While many people involvedin this process died of mercury poisoning at ayoung age, these mirrors could be sold at anenormous profit—and the city fathers instituted adeath penalty for anyone who revealed the secretof the manufacturing process.

But, despite Italy’s best efforts, Venetianglassmaking expertise spread throughoutEurope. Soon French glassmakers had improvedupon Italian processes by using larger tables tomake more sizable pieces of flat glass, and

creating annealing ovens which cooled glasssheets over the course of several days.Glassmaking was also being perfected inGermany, Northern Bohemia, and England,where lead glass was invented by GeorgeRavenscroft in the 1670s. Around this same time,plate glass was first produced in France throughthe cylinder process. Improving on a processdeveloped by the ancient Romans, Frenchglassmakers blew a long glass cylinder, crackedit open, and flattened it with a block of wood toform a rectangle.

With the founding of the British Plate GlassCompany in 1773, England became the world’scenter for quality plate glass for windows. Thisperiod marked the first time in the history ofglassmaking that glazed window glass was widelyavailable and affordable for most homeowners.

England first sought to make its Americancolonies a glassmaking center then, fearingcompetition for its domestic glass houses, out-lawed glassmaking in America. With the Ameri-can Revolution, however, came an influx ofEuropean glass manufacturing expertise that ledto a burgeoning glass industry in the UnitedStates. The first American glassmaking inno-vation was a glass pressing machine that waspatented in 1825. In the pressing process, moltenglass was poured into a mold, and pressed intothe desired shape by a plunger.

The Industrial Revolution brought a number ofinnovations to glassmaking, beginning with thedevelopment of an air-pressure pump in England in1859. This pump automated the process ofglassblowing, reducing the need for skilledcraftsmen. Advances in chemistry also impactedglassmaking, by enabling manufacturers to alterthe composition of glass products—making themstronger and more heat-resistant. In 1871, WilliamPilkington invented a machine which automated theproduction of plate glass made using the cylinder

Figure 1. This photo shows an American glassmanufacturing plant in the 1920s.

30 GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

method; this mechanized process was improved byJ.H. Lubber in America in 1903.

Around the turn of the century, glassmakersdiscovered that plate glass could be “tempered” byreheating it and then cooling it again quickly. Theresulting compression of the glass material wouldincrease its strength by as much as 400 percent.This would prove especially important in theautomobile industry, which was still in its infancy.

The cylinder process was made virtuallyobsolete when the American Irving Colburn andthe Belgian Emile Fourcault simultaneouslydeveloped a new automated glassmakingprocess which drew molten glass from thefurnace in a thin stream, then flattened andcooled it by pulling it between asbestos rollers.Though glass produced by the “draw” processwas still not distortion-free, it was the highest-quality flat glass ever produced—and it helped todrive down prices across the industry. In fact,between 1920 and 1930, as the “draw” processbegan to dominate glassmaking, the price of flatglass dropped by more than 60 percent.

The “draw” process also made it possible toproduce patterned glass, by pulling the glassthrough imprinted asbestos rollers. Architects andbuilders quickly embraced patterned glass for anumber of uses in which privacy was a concern.

In the years following World War I, the flatglass industry saw phenomenal growth, thanks toa worldwide housing boom and the growth of theautomobile industry. By 1929, 70 percent of allflat glass produced in the U.S. was sold to theauto-motive industry. Much of this was “safetyglass,” produced by bonding two sheets of glassto a center layer of cellulose acetate.

However, despite improved processes used tomake flat glass, the polishing process needed toproduce high-quality plate glass continued to betime-consuming and expensive. As early as 1848,glassmakers around the world were searching fora way to make high-quality, polished sheets ofglass without adding a separate production step.

Glass manufacturing was changed foreverwhen Alastair Pilkington developed the modernfloat glass process in the 1950s, eliminating thedistinction between flat glass and polished plateglass. In Pilkington’s process, molten glass waspoured in a continuous stream into a shallow poolof molten metal, typically tin. The molten glasswould spread onto the surface of the metal,producing a high-quality, consistently level sheetof glass that was polished by heat.

Pilkington’s process revolutionized theworldwide flat glass industry in a number of ways.It drove down the cost of plate glass dramatically,and created new applications for flat glassproducts, such as the exterior of high-rise officebuildings. This new high-quality glass began to

dominate the construction, automotive, andmirror industries, because it was a superiorproduct at a lower price. Today, 90 percent of theworld’s flat glass is still made using Pilkington’sfloat process.

3. MODERN DEVELOPMENTS IN THEFLAT GLASS INDUSTRY

In the 1960s, companies that were licensingPilkington’s float process were increasing theircapacity, while lowering the price of flat glass—leading to difficulties for smaller firms who didn’tyet have float capabilities. By 1975, float plantswould account for 97 percent of all plate glassplants worldwide—making Pilkington’s floatprocess one of the greatest innovations in thehistory of the glass industry.

The float process, in turn, enabled a numberof new technologies and product developments inflat glass manufacturing. For the first time,uniform, high-quality sheet glass could be madein a variety of thicknesses, ranging from .5millimeters to 19 millimeters or even thicker.Glass could be made thicker to address safety,security, or noise reduction concerns, while stillmeeting the highest aesthetic standards. Inaddition, the float process made it easy for glassmanufacturers to vary the composition of the

Figure 2. High- and medium-performance coatings, deve-loped in the late 1970s and early 1980s, enable theconstruction of attractive, energy-efficient buildingssuch as the Place Nouveau in North York.

31GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

molten glass to make plate products for specialapplications—including tinted glass.

As insulating glass units and storm windowsgrew in popularity during the 1960s, the recentlyintroduced float process enabled the flat glassindustry to keep up with the demand for attractive,efficient, and cost-effective window glass.

With the worldwide energy crisis in the early1970s, the demand for flat glass declined—andthe entire industry suffered. Because of energy-efficiency concerns, glass was used less often inhigh-rise buildings. The housing industry saw asteep decline, thanks to a severe economicrecession. Compact cars were using less glass

and, to make matters worse, the Ford MotorCompany began to produce its float glass in-house,greatly reducing sales to the auto industry. In fact,in 1970 Ford’s Nashville facility was the largestglass manufacturing plant in the world.

The glass industry responded with newtechnologies that answered consumers’ growingconcerns about energy efficiency—andaddressed new performance concerns. Forexample, with expanded awareness of solarenergy, glassmakers developed new coatingsthat would help flat glass to retain passive solarand radiant heat more efficiently, as well as solarcontrol coatings that would help to block the sun’sheat in warmer climates—while still allowingvisible light transmittance. The 1970s also saw

the introduction of low-iron glasses for photo-voltaic applications. These products increasesolar transmittance and help convert the sun’senergy to electricity.

In addition, glass manufacturers began tointroduce new high- and medium-performancereflective coatings that would enable builders andarchitects to achieve specific performancecharacteristics in terms of visible light trans-mittance, solar reflectance, and shading coefficient.These new high-performance products, appliedthrough off-line vacuum deposition processes, andmedium-perform-ance on-line pyrolytic coatingshelped to revolutionize the architectural industry inthe late 1970s and early 1980s—making possiblethe wide range of attractive, energy-efficientbuildings we see around us today.

New mileage requirements imposed in the1970s also presented the automobile industrywith a number of challenges—and the flat glassindustry developed new products and processesto help address them. For instance, glassmakersdeveloped new laminations that made it easier tobend flat glass, accommodating the autoindustry’s more aerodynamic designs. Inaddition, safety glass—first manufactured forcars during the 1920s—became lighter andthinner, with better shaping capabilities thathelped to eliminate distortion.

As the worldwide economy improved in theearly 1980s, concerns about energy efficiencyremained—and glass manufacturers continuedtheir efforts to develop innovative newtechnologies and processes that would maximizewindow performance.

Without a doubt, low-emissivity coatings wereone of the biggest developments in the flat glassindustry during the last decade. These coatingsenable homeowners and commercial architects totake advantage of passive solar heat during thewinter months, while reflecting radiant furnace heatback into the building’s interior. In addition, thesenew coatings reduce condensation levels byincreasing the glass temperature. These revo-lutionary products are still gaining ground in themarketplace, as builders and consumers learnabout the advantages of “low-E” coatings. In fact,sales of low-emissivity coated flat glass productshave grown 13 percent each year since 1990.

In addition to developing its own energy-efficiency technologies, the glass industry hashad to respond to new developments in thewindow fabrication industry. The continuinggrowth of vinyl windows and argon fillings, forexample, has placed new demands on glass-makers who sell to window fabricators.

Another far-reaching innovation was theintroduction in the late 1980s of “warm-edge”technologies, or spacer systems which reduce

Figure 3. Low-emissivity coatings, which are still growing inpopularity, allow homeowners to enjoy increasedyear-round comfort.

32 GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

heat transfer between interior and exterior lites ina sealed insulating unit. These design improve-ments are aimed at meeting consumers’increasing demands for year-round comfort,greater energy efficiency, and reduced conden-sation levels.

We’ve also seen product and designinnovations in the area of security and noise-abatement windows. The flat glass industry hasdeveloped a number of innovative tempering andlaminating processes which make glass strongerto address security concerns. And, worldwide,window fabricators have created new windowdesigns for homes and buildings in noisy areas.For example, some European manufacturershave combined different thicknesses of glass tofilter various sound ranges, while others haveadded laminated glass to reduce noise pollution.

Since a double-digit decline in demand in theNorth American market in 1991, the flat glassindustry has seen steady growth in the 1990s,responding to growth in both the automotive andhousing industries. Glass use in the auto industrycontinues to grow each year, due in part to theincreasing popularity of sport utility vehicles andminivans, which require more glass than tradit-ional cars. Newer housing designs are also usingmore flat glass than ever before. And, whilewe’ve seen the construction of high-rise buildingsslow a bit in recent years, that decline has beenmatched by a growth in the construction of three-and four-story suburban office complexes.

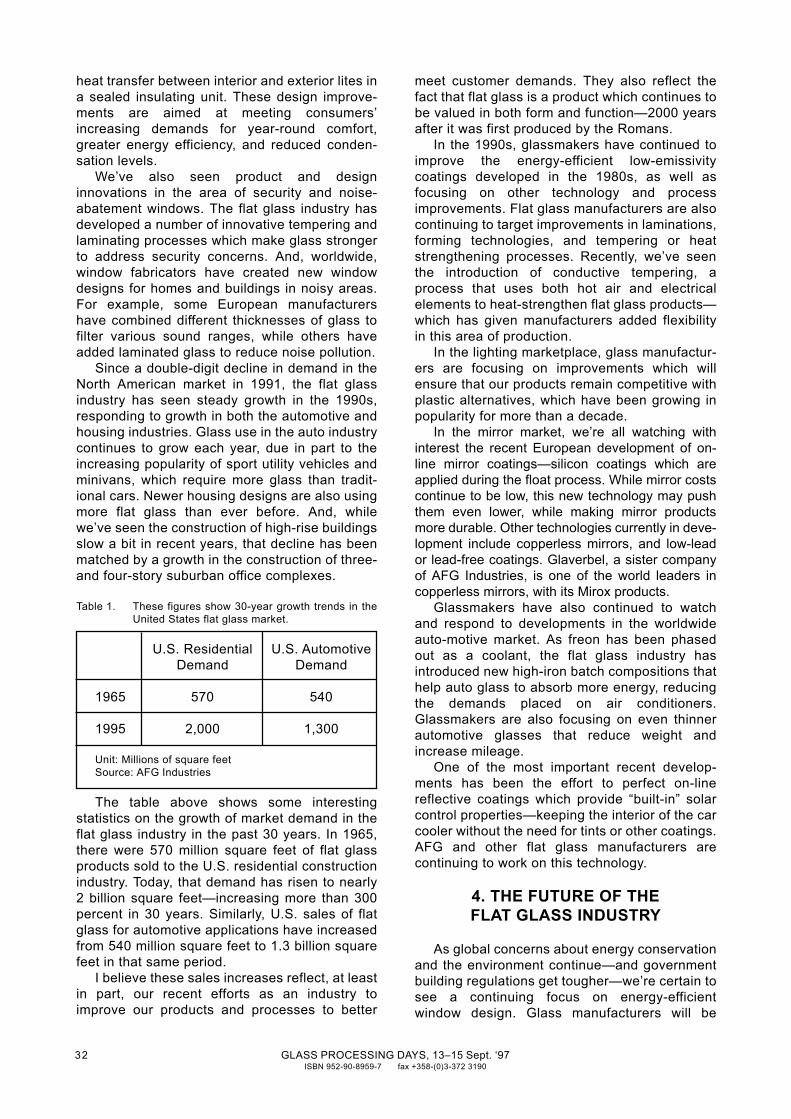

Table 1. These figures show 30-year growth trends in theUnited States flat glass market.

U.S. Residential U.S. AutomotiveDemand Demand

1965 570 540

1995 2,000 1,300

Unit: Millions of square feetSource: AFG Industries

The table above shows some interestingstatistics on the growth of market demand in theflat glass industry in the past 30 years. In 1965,there were 570 million square feet of flat glassproducts sold to the U.S. residential constructionindustry. Today, that demand has risen to nearly2 billion square feet—increasing more than 300percent in 30 years. Similarly, U.S. sales of flatglass for automotive applications have increasedfrom 540 million square feet to 1.3 billion squarefeet in that same period.

I believe these sales increases reflect, at leastin part, our recent efforts as an industry toimprove our products and processes to better

meet customer demands. They also reflect thefact that flat glass is a product which continues tobe valued in both form and function—2000 yearsafter it was first produced by the Romans.

In the 1990s, glassmakers have continued toimprove the energy-efficient low-emissivitycoatings developed in the 1980s, as well asfocusing on other technology and processimprovements. Flat glass manufacturers are alsocontinuing to target improvements in laminations,forming technologies, and tempering or heatstrengthening processes. Recently, we’ve seenthe introduction of conductive tempering, aprocess that uses both hot air and electricalelements to heat-strengthen flat glass products—which has given manufacturers added flexibilityin this area of production.

In the lighting marketplace, glass manufactur-ers are focusing on improvements which willensure that our products remain competitive withplastic alternatives, which have been growing inpopularity for more than a decade.

In the mirror market, we’re all watching withinterest the recent European development of on-line mirror coatings—silicon coatings which areapplied during the float process. While mirror costscontinue to be low, this new technology may pushthem even lower, while making mirror productsmore durable. Other technologies currently in deve-lopment include copperless mirrors, and low-leador lead-free coatings. Glaverbel, a sister companyof AFG Industries, is one of the world leaders incopperless mirrors, with its Mirox products.

Glassmakers have also continued to watchand respond to developments in the worldwideauto-motive market. As freon has been phasedout as a coolant, the flat glass industry hasintroduced new high-iron batch compositions thathelp auto glass to absorb more energy, reducingthe demands placed on air conditioners.Glassmakers are also focusing on even thinnerautomotive glasses that reduce weight andincrease mileage.

One of the most important recent develop-ments has been the effort to perfect on-linereflective coatings which provide “built-in” solarcontrol properties—keeping the interior of the carcooler without the need for tints or other coatings.AFG and other flat glass manufacturers arecontinuing to work on this technology.

4. THE FUTURE OF THEFLAT GLASS INDUSTRY

As global concerns about energy conservationand the environment continue—and governmentbuilding regulations get tougher—we’re certain tosee a continuing focus on energy-efficientwindow design. Glass manufacturers will be

33GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

investing in ongoing research on energy-efficientcoatings and tints, while the entire windowindustry will be working to improve warm-edgetechnologies and other window design features.

Today, more than 90 percent of all windowssold in North America are insulating glass units,and we expect that this percentage will only risein the future. Though many windows currentlysold in the Asia-Pacific marketplace are single-glazed units, this market will probably see anincreased demand for insulating units as airconditioning becomes standard and buildingcodes become more strict. As an example of themarket potential in this area, today only 25percent of windows produced in Japan areinsulating glass units.

We’re also sure to see a continuing rise in thesale of replacement windows, as existing homesage. Already, replacement windows havesurpassed new windows in volume. This will mostlikely mean that vinyl windows will continue to bea growing product category. In fact, it is expectedthat sales of vinyl windows will exceed sales ofwood sash windows in the U.S. by the year 2001.

The trend toward smaller suburban officebuildings will probably continue as well, whichmeans that there will be less demand for “curtainwall” windows, and increasing orders of smaller,medium-perform-ance architectural window units.Sales of “storefront” glass should also remainstrong, as the retail industry continues to expandaround the world.

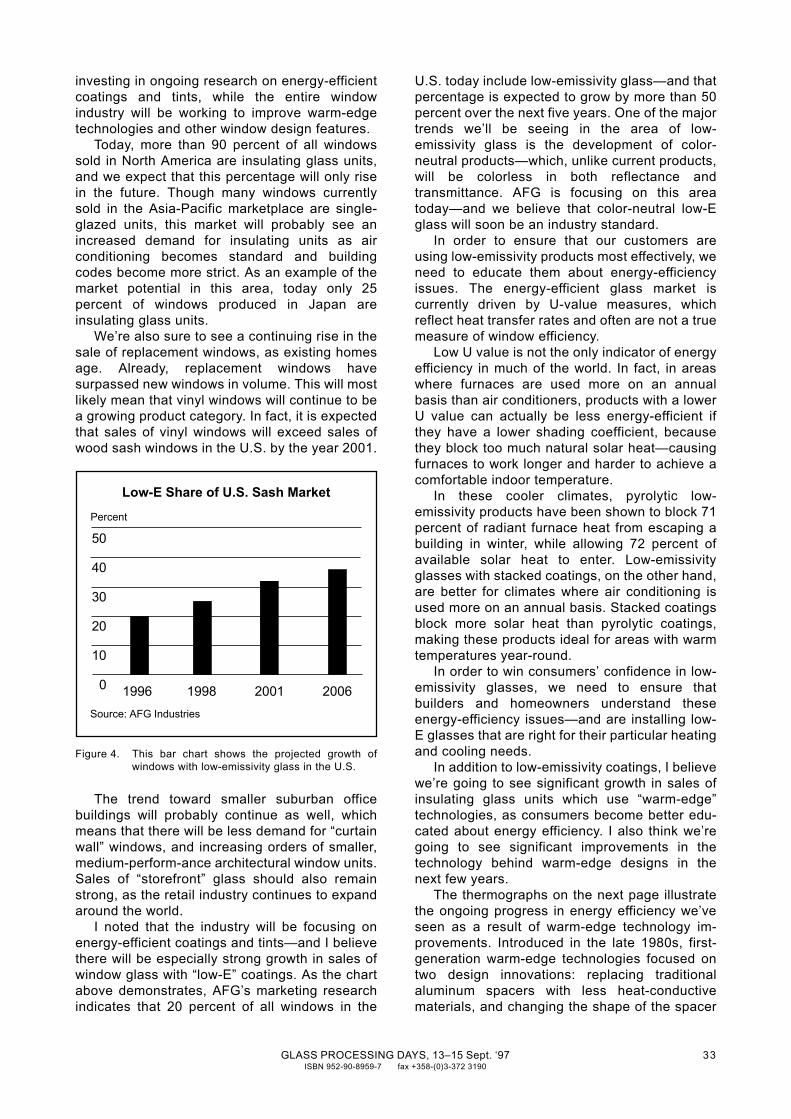

I noted that the industry will be focusing onenergy-efficient coatings and tints—and I believethere will be especially strong growth in sales ofwindow glass with “low-E” coatings. As the chartabove demonstrates, AFG’s marketing researchindicates that 20 percent of all windows in the

U.S. today include low-emissivity glass—and thatpercentage is expected to grow by more than 50percent over the next five years. One of the majortrends we’ll be seeing in the area of low-emissivity glass is the development of color-neutral products—which, unlike current products,will be colorless in both reflectance andtransmittance. AFG is focusing on this areatoday—and we believe that color-neutral low-Eglass will soon be an industry standard.

In order to ensure that our customers areusing low-emissivity products most effectively, weneed to educate them about energy-efficiencyissues. The energy-efficient glass market iscurrently driven by U-value measures, whichreflect heat transfer rates and often are not a truemeasure of window efficiency.

Low U value is not the only indicator of energyefficiency in much of the world. In fact, in areaswhere furnaces are used more on an annualbasis than air conditioners, products with a lowerU value can actually be less energy-efficient ifthey have a lower shading coefficient, becausethey block too much natural solar heat—causingfurnaces to work longer and harder to achieve acomfortable indoor temperature.

In these cooler climates, pyrolytic low-emissivity products have been shown to block 71percent of radiant furnace heat from escaping abuilding in winter, while allowing 72 percent ofavailable solar heat to enter. Low-emissivityglasses with stacked coatings, on the other hand,are better for climates where air conditioning isused more on an annual basis. Stacked coatingsblock more solar heat than pyrolytic coatings,making these products ideal for areas with warmtemperatures year-round.

In order to win consumers’ confidence in low-emissivity glasses, we need to ensure thatbuilders and homeowners understand theseenergy-efficiency issues—and are installing low-E glasses that are right for their particular heatingand cooling needs.

In addition to low-emissivity coatings, I believewe’re going to see significant growth in sales ofinsulating glass units which use “warm-edge”technologies, as consumers become better edu-cated about energy efficiency. I also think we’regoing to see significant improvements in thetechnology behind warm-edge designs in thenext few years.

The thermographs on the next page illustratethe ongoing progress in energy efficiency we’veseen as a result of warm-edge technology im-provements. Introduced in the late 1980s, first-generation warm-edge technologies focused ontwo design innovations: replacing traditionalaluminum spacers with less heat-conductivematerials, and changing the shape of the spacer

Figure 4. This bar chart shows the projected growth ofwindows with low-emissivity glass in the U.S.

50

40

30

20

10

0 1996 1998 2001 2006

Percent

Low-E Share of U.S. Sash Market

Source: AFG Industries

34 GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

to provide a “thermal break” that would helpreduce heat transfer. These first-generationwarm-edge technologies provided marginalimprovements in both sill temperature andcondensation threshold, while in some casescosting less than traditional spacers.

The second generation of warm-edgeinnovations, introduced in the 1990s, eliminatedmetal components entirely, replacing them withsuch man-made materials as rubber andextruded plastics. Though more expensive thanfirst-generation spacer designs, these inno-vations brought about significant improvementsin both sill temperature and condensationthreshold. However, because of their higherprice, these spacer designs have not wonuniversal consumer acceptance—and much ofthe industry has continued to focus on first-generation technologies, even today.

I believe we’re about to see a new thirdgeneration of warm-edge technologies thatcombine first-generation cost benefits withsecond-generation performance. Flat glassmanufacturers need to monitor ongoing improve-ments in warm-edge technologies—and ensurethat our window products are compatible withthese warm-edge systems. We also need toactively support the development of even moreenergy-efficient window designs to help satisfyconsumers around the world.

Another major area of focus in the industry inthe next decade will be electrochromics andphotochromics. “Smart window” technologieshave already been developed that allow flat glassto sense changes in light and adjust accord-ingly—for example, to block out sunlight duringthe brightest parts of the day, or to capitalize onavailable light during overcast days. Theseglasses are coated with special materials whichchange as different voltages are applied acrosstheir surfaces. This technology, which has the

potential to make shutters,blinds, and draperies obso-lete, could become afford-able within the next three tofive years—and may signalthe next revolution in thewindow industry. Flat glassmanufacturers are alreadypreparing to enter this pro-mising new marketplace.

Today, 28 percent of all flatglass is used in theautomotive industry—and, assport utility vehicles andminivans continue to grow in

popularity, that percentage will only increase. Forthat reason, the flat glass industry continues tofocus much of its attention on innovations for thismarket. As concerns about performance and airconditioning use continue, flat glass manufacturerswill continue to focus their efforts on developingthinner, lighter, stronger glass products which alsocontrol solar energy.

An important development for the automotivemarket is the continuing work on flat glassproducts which will accommodate “heads-up”displays, which reflect dashboard readings ontoa car’s windshield, where they can be moreeasily read. This new technology, which is madepossible with specialty coatings, has thepotential to spread across the automotiveindustry, as well as the commercial airlineindustry. It is certainly an area of developmentthat deserves our attention.

Another innovation that will impact the autoindustry is the development of “switchable”mirrors that respond to changes in light, reducingglare during night driving. In addition toimproving safety, these new mirrors are moredurable than existing automotive mirrors. Asthese mirror products decrease in cost, they willquickly become a standard feature in every newcar—and flat glass manufacturers need toprepare for this market shift.

Another standard feature will be metallic-coated windshield glass, which acts as anantenna and eliminates the need for a traditionalradio antenna. This technology has already beenintroduced in many new cars, and is expected tospread across the industry—increasing thedemand for these conductive glass products.

The display market is changing radically aswe approach the 21st century—and newtechnology developments are certain to have ahuge impact on the flat glass industry. Newdisplay technologies use special coatings togenerate electrical impulses across flat glass,making televisions much more precise, as wellas much flatter.

Figure 5. These thermographs are based on an outsidetemperature of 0° F and an inside temperature of70° F.

Traditional Aluminium Spacer First-Generation Warm-Edge Second-Generation Warm-Edge

35° sill temperature27° condensation threshold

37° sill temperature30° condensation threshold

45° sill temperature40° condensation threshold

35GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

As flat-panel displays become a reality—displacing standard cathode ray tube displays—an enormous new market opportunity is on thehorizon for glass manufacturers. We need to beready to supply this new market with high-precision specialty coatings that help to make thisnew technology cost-effective as demand forhigh-definition, flat-panel televisions increases.Much industry effort right now is focused on tryingto improve low-emissivity and other coatings forthis application.

Other opportunities in the display marketinclude improved glass for computer monitors, aswell as more sophisticated liquid crystal displaytechnologies. Again, flat glass manufacturers areinvesting in research and development work inthese areas. Just as the invention of theautomobile impacted the flat glass industry nearlya century ago, the new era of display technologyis sure to bring changes for all of us.

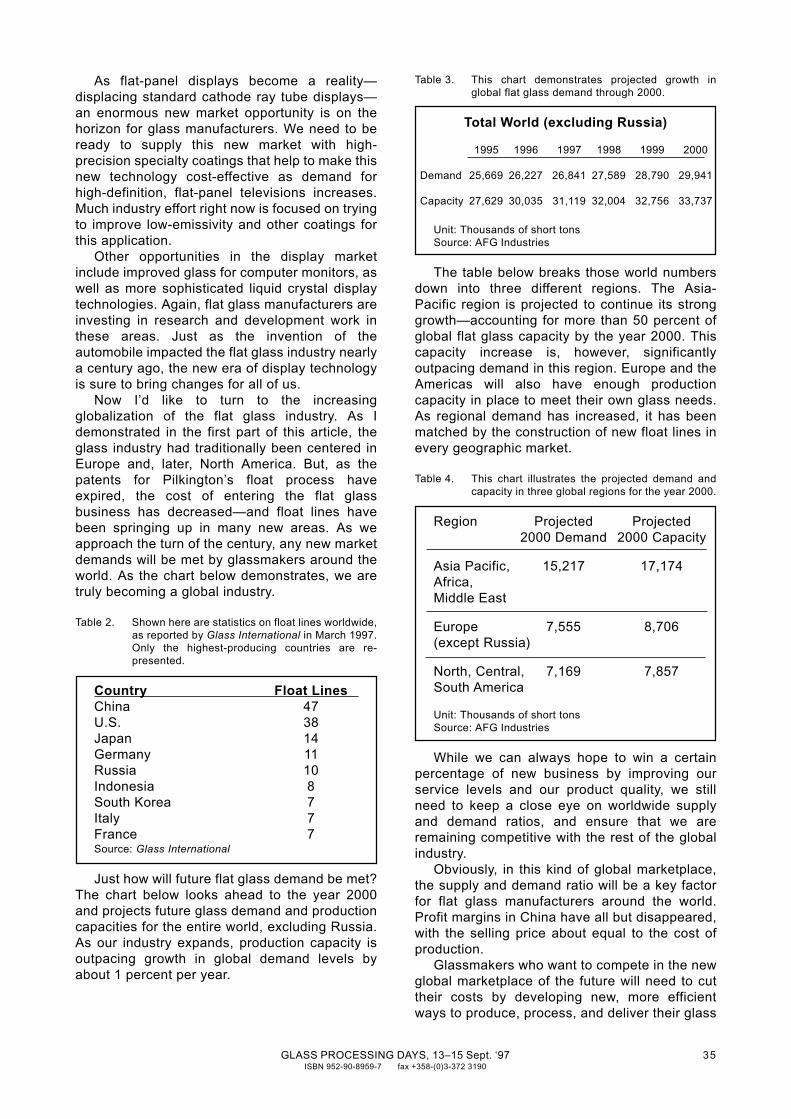

Now I’d like to turn to the increasingglobalization of the flat glass industry. As Idemonstrated in the first part of this article, theglass industry had traditionally been centered inEurope and, later, North America. But, as thepatents for Pilkington’s float process haveexpired, the cost of entering the flat glassbusiness has decreased—and float lines havebeen springing up in many new areas. As weapproach the turn of the century, any new marketdemands will be met by glassmakers around theworld. As the chart below demonstrates, we aretruly becoming a global industry.

Table 2. Shown here are statistics on float lines worldwide,as reported by Glass International in March 1997.Only the highest-producing countries are re-presented.

Country Float LinesChina 47U.S. 38Japan 14Germany 11Russia 10Indonesia 8South Korea 7Italy 7France 7Source: Glass International

Just how will future flat glass demand be met?The chart below looks ahead to the year 2000and projects future glass demand and productioncapacities for the entire world, excluding Russia.As our industry expands, production capacity isoutpacing growth in global demand levels byabout 1 percent per year.

Table 3. This chart demonstrates projected growth inglobal flat glass demand through 2000.

Total World (excluding Russia)

1995 1996 1997 1998 1999 2000

Demand 25,669 26,227 26,841 27,589 28,790 29,941

Capacity 27,629 30,035 31,119 32,004 32,756 33,737

Unit: Thousands of short tonsSource: AFG Industries

The table below breaks those world numbersdown into three different regions. The Asia-Pacific region is projected to continue its stronggrowth—accounting for more than 50 percent ofglobal flat glass capacity by the year 2000. Thiscapacity increase is, however, significantlyoutpacing demand in this region. Europe and theAmericas will also have enough productioncapacity in place to meet their own glass needs.As regional demand has increased, it has beenmatched by the construction of new float lines inevery geographic market.

Table 4. This chart illustrates the projected demand andcapacity in three global regions for the year 2000.

Region Projected Projected2000 Demand 2000 Capacity

Asia Pacific, 15,217 17,174Africa,Middle East

Europe 7,555 8,706(except Russia)

North, Central, 7,169 7,857South America

Unit: Thousands of short tonsSource: AFG Industries

While we can always hope to win a certainpercentage of new business by improving ourservice levels and our product quality, we stillneed to keep a close eye on worldwide supplyand demand ratios, and ensure that we areremaining competitive with the rest of the globalindustry.

Obviously, in this kind of global marketplace,the supply and demand ratio will be a key factorfor flat glass manufacturers around the world.Profit margins in China have all but disappeared,with the selling price about equal to the cost ofproduction.

Glassmakers who want to compete in the newglobal marketplace of the future will need to cuttheir costs by developing new, more efficientways to produce, process, and deliver their glass

36 GLASS PROCESSING DAYS, 13–15 Sept. ‘97ISBN 952-90-8959-7 fax +358-(0)3-372 3190

to customers around the world. For example, inthe past year, cargo shipping rates have droppedby 10 percent, and that trend is expected tocontinue. Historically, glass has been expensiveto transport. But, as the global industry baseevolves, we will find ourselves in more directcompetition. Cost-cutting, balanced by newproduct development and superior customerservice, will be essential to our survival.

The real key to success in the flat glassindustry lies in looking at the past of our industry.I believe it is innovation that will determine thecourse of the next 10 or 20 years in our industry,just as it has for the past 3500 years. From theearly development of glassmaking in the RomanEmpire to the invention of the float process, ourindustry has always been characterized byrevolution and innovation—by the ability ofglassmakers to look ahead to the future.

I believe that this pattern of innovation willcontinue to lead our industry to new heights —and help glass manufacturers around the worldto achieve success, even in today’s increasinglycompetitive marketplace. It is this challenge thatall of us must answer if we hope to live up to ourindustry’s past.

As glass manufacturers and processors, weare in a unique business, with a long tradition ofproviding products that customers find attractivein both form and function. After all, how manymodern industries are 3500 years old? Tocontinue our tradition of continuous productimprovement, we need to remember that it iscustomers who drive our industry. We need to beaware of the needs and expectations of ourcustomers around the world, and answer thoseneeds with product innovations that they trulyvalue. If we can do that, then we can not fail toachieve continued success as an industry.

REFERENCES

[1] B. Jones, Magic With Sand: A History of AFGIndustries, Inc., Wichita State University BusinessHeritage Series (1984).

[2] M. Northend, American Glass, Tudor PublishingCompany (1926).

[3] R. Smith and M. Massa, “Energy Efficient Glass:Stepping Up to the Challenge,” US Glass (February1997).

[4] R. Cunningham, “Industry Survey Finds Optimism in AllSegments,” Glass Digest (June 1996).

[5] P. Ita, “Flat Glass Market Prospects Improving in the1990s,” Glass Digest (September 1994).

[6] A. Ashfield, “Continued Expansion Predicted for Floatin Pacific Region,” Glass International (March 1997).

[7] “Report Projects Flat Glass Growth,” Glass Digest(March 1996).

[8] “New Survey Sees World Flat Glass Demand Growing5 Percent a Year,” Glass Industry (March 1995)

[9] J. Swanson, “Warm-Edge Insulating Glass DemandAccelerates,” Fenestration (September/October 1993).

[10] “Warm Edge Technology Fact vs. Fiction,” Door &Window Fabricator (October/November 1993).

[11] M. Glover, “Warm-Edge Technology and the Triple-Glazing Revival,” Glass Magazine (January 1994).