flexibility on switching option

DESCRIPTION

Flexibility on Switching OptionTRANSCRIPT

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 1/38

A Real Option Approach to Valuation of Manufacturing

Flexibility with 2 State Variables and Regime Switching

M.I.M. Wahab†, Chi-Guhn Lee†,1, Namkyu Park‡

†Department of Mechanical and Industrial Engineering

University of Toronto, Toronto, Ontario, M5S 3G8, Canada

‡Department of Industrial and Manufacturing Engineering

Wayne State University, Detroit, Michigan, 48202, USA

March 21, 2005

1Corresponding author can be reached at [email protected]

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 2/38

Abstract

We propose a real option approach to quantification of the value of flexibility in a manu-

facturing system, where the capacity level is optimally adjusted between two products so

as to maximize the total discounted expected profit over a given planning horizon. The

manufacturing system has three options in capacity adjustment: capacity expansion from

external sources, capacity contraction to external sources, and capacity switching within

the system. The demands for the two products are assumed to follow correlated Wiener

processes and to evolve through 2-stage product life: the growing regime first and then the

decaying regime. The original correlated processes are transformed into un-correlated ones

before a lattice is constructed, upon which a dynamic programming-based algorithm applied

to compute the value of manufacturing flexibility. Numerical studies on an example with

various combinations of cost parameters shed light on interesting aspects of manufacturing

flexibility.

Keywords: real option, regime switching, 2 state variables, product life cycle, lattice ap-

proach, manufacturing flexibility

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 3/38

1 INTRODUCTION

CBC News on October 29, 2004 excitingly reports Ford Motor’s grand investment plan on

its facilities in Oakville, Ontario as follows:

The company has decided to build a flexible manufacturing plant at the site.....

With the flexible manufacturing system, the Oakville plant will be capable of

producing up to four different vehicles based on two product platforms, Stevens,

Ford group vice president for Canada, Mexico, and South America, explained.

And the revamped operation will be able to rapidly respond to market fluctua-

tions, avoiding the time and expense required in traditional auto plant retooling.

Oakville will be Ford’s third flexible manufacturing facility. ..... By 2010, Ford

plans to have three-fourths of its 19 North American assembly plants converted

to the flexible system.

It is not only auto makers but firms in just about every industry sector who have suffered

from unsettled customer demands. The product life cycle has become shorter and shorter

and firms not being able to adapt to the whimsical market fail away. In an effort to remain

competitive in such a harsh business environment, more and more firms realize the impor-

tance of being flexible. For example, Ford Motor Co. plans to deliver 65 new Ford, Mercury

and Lincoln in five years and flexible manufacturing is rapidly recognized as a key cog in

unleashing new product to up market share.

While the importance of flexibility in manufacturing systems is well acknowledged, many

manufacturers fail to understand the benefits and the costs of being flexible. As a result it is

often seen too much flexible, not enough flexibility, or even wrong flexibility in manufacturing

1

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 4/38

systems. Such mismatches are almost always extremely costly since investments on flexible

manufacturing systems involve an astronomical dollar figures. In case of the Ford Motor’s

investment plan for the Oakville plant involves $1.2 billion dollars including $1 billion from

Ford Motor, $100 million from the Province of Ontario, and $100 million from the federal

government of Canada1.

In academia there have been continuous efforts to understand the value of manufacturing

flexibility for the last decade or so. A wide range of manufacturing options have been valued

using the financial theories mainly developed for the value of financial derivatives such as

options. Pindyck [17] and He and Pindyck [9] study capacity choice and expansion when

the system is irreversible. Tannous [19] develops a model to evaluate the effect of volume

flexibility and determines the optimal degree of automation. Triantis and Hodder [20] value

the option to switch the output mix over time in a flexible production system. Kulatilaka

[12] determines the value of flexibility of a system to produce specific output while switching

the production mode. Brennan and Schwartz [7] value interdependent options such as open,

close, reopen and abandon in natural resource investments. McDonald and Siegel [14] study

optimal timing of investment in an irreversible project, and McDonald and Siegel [15] study

investment project where there is an option to shut down. Majd and Pindyck [13] consider

the option to delay a irreversible project and determine the effect of time to build.

Despite the ample body of real options literature on manufacturing flexibility, it is often

the case that the nature of stochasticity of the underlying variable is assumed to be determin-

istic and constant. To address the shortcoming, Bollen [4] proposes a lattice framework with

regime switching, in which the probability distribution governing the uncertain evolution of

1All the dollar figures are in Canadian currency

2

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 5/38

underlying variable shifts across regimes. He then reports a significant error in valuing man-

ufacturing flexibility when such non-stationary behavior of the random variable is ignored.

His framework fits well in modeling the product life cycle, that usually starts in growing

phase, and then ends in decaying phase. However, his approach can only deal with a single

underlying variable, thereby fails to value the flexibility under which the manufacturing sys-

tem can reallocate its current capacity between different products within the system. This

flexibility is sometimes called the product-mix flexibility in the literature, which is one of the

most extensively studied flexibility type along with the volume flexibility. Manufacturing

flexibility types include product-mix flexibility, volume flexibility, new-product flexibility,

and delivery-time flexibility, routing flexibility, process flexibility, product flexibility, just to

name a few (more detailed discussion on various types of manufacturing flexibility can be

found in Bengtsson [2], Kulatilaka [12], Sethi and Sethi [18], among many).

We propose a lattice-based approach to valuation of manufacturing flexibility that has

three options: capacity expansion, capacity contraction, and capacity switching. Capacity

expansion and contraction constitute the volume flexibility, whereas capacity switching can

considered as product-mix flexibility. We assume that the demands for two products are

correlated and the correlation factor can change as the products shift toward the next phase

in their product life cycle. The manufacturing system can expand or contract its aggregate

capacity level through external sources as well as switching capacity dedicated to one product

to the other. The former flexibility will be called capacity expansion and capacity contraction,

while the latter will be called capacity switching in the paper.

This paper is organized as follows. Section 2.1 presents model that describes product

life cycles, demand process, cost and profit functions, fixed and flexible system. Section 3

3

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 6/38

describes lattice approach and flexibility valuation. Section 4 presents numerical example to

investigate the value of flexibility. Section 5 gives conclusions.

2 THE PROBLEM DEFINITION

In this section we define the market and the manufacturing system. The demand process

consists of two streams of random variables over time, whose stochastic characteristics may

change over time. We consider two manufacturing systems: one with fixed capacity and the

other with flexible capacity.

2.1 The Market Model

According to the literature of new product diffusion, demand for a new product typically

begins with start-up regime, and then growth regime. Later as the taste of the customer

changes or a new generation of product replaces existing product, the product life cycle

undergoes maturation regime, and finally decaying regime. Bass [1] proposes a forecasting

model based on two-regime product life cycle with exponential growth and exponential decay.

Bollen [4] addresses the value of manufacturing flexibility when the manufacturing system

produces a product with stochastic demand centered around two-regime product life cycle.

He points out that a significant error in the value of manufacturing flexibility is observed

when product life cycle is ignored.

Figure 1 depicts one possible realization of the future demand evolution of two products,

in which demands of both products grow up to time t1, and then demand of product 1 starts

decaying while that of product 2 continues to grow up to time t2(t2 > t1). After time t2,

4

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 7/38

demands of both products decay. We denote the combined regimes between time 0 and t1

as (G1, G2), the combined regime between time t1 and t2 as (D1, G2), and the other as

(D1, D2). When all possible realizations of the future demand evolution of both products

are considered, there will be one more combined regime (G1, D2). Thus, we have four

possible combinations of regimes when each of two products has two regimes. The number

of combinations becomes 9 when each product has 3 regimes, 16 when each has 4 regimes,

and so on.

Figure 1: Possible Combinations of Regimes

We consider a pair of correlated random demand processes, each of which has a two-regime

life cycle. Extension to more than two regimes can be done using a technique discussed in

Wahab and Lee [21]. Let θit denote demand of product i (i ∈ {A, B}) at time t. As commonly

assumed in real option literature, the continuously compounded rate of the demand of a

product within a regime is assumed to follow a stationary geometric Wiener process. The

5

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 8/38

drift rate of product i in the growing regime, µig, is typically larger than that in the decaying

regime µid. The volatilities of product i in the growing regime and the decaying regime are

σig and σi

d, respectively. Table 1 summarizes the mean and the volatility of the two products

in different regimes.

Table 1: The instantaneous mean and volatility of 2 processes

Product Growing Regime Decaying Regime

A (µAg , σA

g ) (µAd , σA

d )

B (µBg , σB

g ) (µBd , σB

d )

We assume that the current regime is always perfectly observable implying that the dis-

tribution governing realization of the random demand in the next period is known. However,

regime switching may occur at the beginning of the next period leaving the distribution for

the next transition is unknown. As mean and volatility of demands vary across the regimes,

correlation between two demands also varies since they are all functions of the same random

variables. With two products, each having a two-regime life cycle, there are four possible

combinations of regimes, and each possible combination of regimes has different correlations.

The correlations of four possible combinations of regimes (G1, G2), (D1, D2), (G1, D2), and

(D1, G2) are denoted as ρ1, ρ2, ρ3, and ρ4, respectively as shown Table 2, where ρ1 and ρ2

are more likely to be positive, while ρ3 and ρ4 are more likely to be negative. The signs of

correlations indicate that both demands in regime (G1, G2) grow or both demands in regime

(D1, D2) decay. On the other hand, in regime (G1, D2) and (D1, G2), one demand grows

and the other decays.

Regime switching determines duration of a certain demand pattern, thereby influences the

6

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 9/38

Table 2: Correlation of between processes in each combination of regimes

Combinations of regimes (G1, G2) (D1, D2) (G1, D2) (D1, G2)

Correlation ρ1 ρ2 ρ3 ρ4

NPV of the manufacturing system. We employ the approach used in Bollen [4] by assuming

the probability of switching from the growing to the decaying regime in the next period is

cumulative normal distribution function in the time elapsed since the introduction of the

product to the market. This implies that pt, the probability of switching from the growing

to the decaying regime, conditional on still being in the growing regime, is as follows

pt =

t0

Φ(x|µs, σs)dx,

where Φ(s) is a normal distribution with a given mean µs and variance σs. Motivation behind

this approach is that there will be next-generation of product to replace an existing product

in the market after some years. The regime switching could also be modeled as function of

demand or cumulative demand using diffusion and substitution model by Norton and Bass

[16] or pure diffusion model by Bass [1].

We assume that regime switching is unidirectional; switching is always from the growing

to the decaying. Although this assumption is not necessary in our approach to valuation of

flexibility, it would make more sense in reality since products rarely revive its popularity once

it becomes insipid. Bidirectional regime switching makes sense in financial options pricing

and option pricing with multiple underlying assets that switch across multiple regime in a

bidirectional way can be found in Wahab and Lee [21].

7

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 10/38

2.2 The Manufacturing System

The cost model in this paper is motivated by a manufacturing firm who supplies dozens of

products in a wide range of price to a highly competitive market. The presence of many

competing firms supplying substituting products leaves the manufacturer with no room to

control the price. The price is set by the market so that the manufacturer is forced to be a

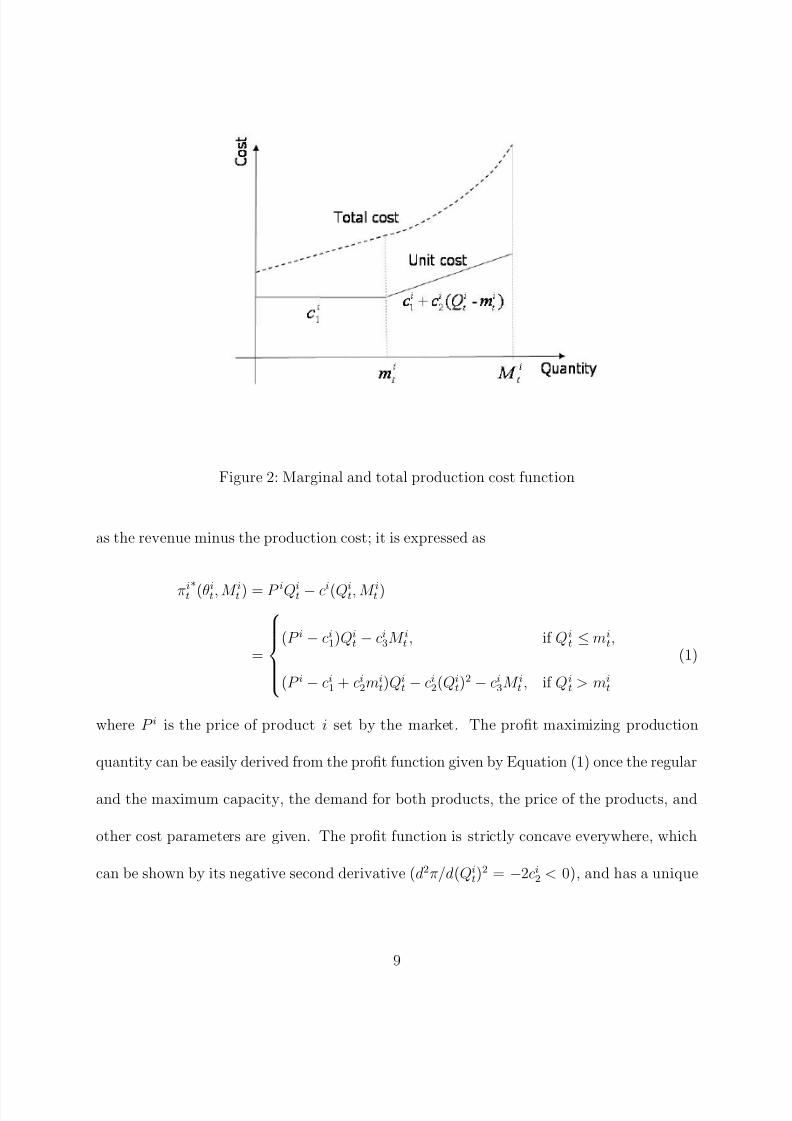

price taker and the cost function is as shown in Figure 2. In period t, the marginal production

cost, shown as a solid curve in Figure 2, is a constant ci1 while utilization is below a regular

capacity level mit, which is less than or equal to the maximum capacity level M it , and starts

increasing linearly with a slope ci2 as utilization exceeds the regular capacity. As a result the

total production cost, shown as a dotted curve, increases linearly up to the regular capacity

and quadratically above the regular capacity. There is also overhead cost ci3 to maintain a

unit capacity for product i(i ∈ {A, B}) in each period.

Let Qit be the production quantity of product i in period t. The cost function is expressed

as follows:

ci(Qit, M ii ) =

ci1Qit + ci3M it , if Qi

t ≤ mit,

ci1Qit + ci2(Qi

t − mit)Qi

t + ci3M it , if Qit > mi

t,

In order to determine the NPV of the system, profit from each product i must be calcu-

lated in each period t. The profit of product i in period t, denoted by πit(Qi

t, M ii ), is expressed

8

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 11/38

Figure 2: Marginal and total production cost function

as the revenue minus the production cost; it is expressed as

πit

∗

(θit, M it ) = P iQit − ci(Qit, M it )

=

(P i − ci1)Qit − ci3M it , if Qi

t ≤ mit,

(P i − ci1 + ci2mit)Qi

t − ci2(Qit)2 − ci3M it , if Qi

t > mit

(1)

where P i is the price of product i set by the market. The profit maximizing production

quantity can be easily derived from the profit function given by Equation (1) once the regular

and the maximum capacity, the demand for both products, the price of the products, and

other cost parameters are given. The profit function is strictly concave everywhere, which

can be shown by its negative second derivative (d2π/d(Qit)2 = −2ci2 < 0), and has a unique

9

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 12/38

minimum

Q̄it =

P i − ci1 + ci2mit

2ci2.

However, the production quantity exceeding the demand is clearly suboptimal, while it is

limited to the maximum capacity. Therefore, when demand θit, the maximum capacity M it

are given, the optimal production quantity of product i in period t is:

Qit

∗= min{θit,

Q̄it, M it}. (2)

Now that the profit in each period can be maximized by the production quantity given

in Equation (2), the next step is to maximize the total profit over a given planning horizon.

As mentioned earlier, the profit depends on the demand and the capacity. Assuming the

regular capacity is a certain fraction of the maximum capacity, the only control is the level

of the maximum capacity in each period since the demand is exogenous to the manufacturer.

In this paper we consider two systems: a fixed capacity system where the capacity ad-

justment is allowed only at the beginning of the project and a flexible capacity system where

the capacity adjustment is allowed throughout the life of the project. With a fixed capacity

system, the production quantities of product i in any period are bounded by optimal capacity

levels installed at time zero. Let π it

∗(θit, M i0) denote the optimal profit of product i in period

t when the maximum capacity is M i0 for product i. The net present value (NPV) of the fixed

system from time 1 to T is given by

NP V (M A0 , M B0 ) = −(cA4 M A0 + cB4 M B0 ) +T t=1

e−rt{E [πA∗t (θAt , M A0 )] + E [πB∗

t (θBt , M B0 )]}

where T is the terminal period of the project, r is the risk-free rate, and ci4 is the cost of

installing one unit of capacity for product i in period 0. An interesting point is how to set the

10

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 13/38

value of project life T , which can be viewed as the economic life of the manufacturing system.

This depends on various factors such as the demand for the products that the manufacturing

system is producing, the operating cost increasing over time due to aging, etc. The project

life T will have a huge impact on the project value and is uncertain for many reasons. One

of reasonable approaches is to define a probability distribution for project termination that

is a function of the duration of the project, cumulative demands, and so on. For simplicity

of exposition, we assume that T is given a priori. Extension to random termination would

not be a problem in our lattice-based approach.

Unlike the fixed capacity system, the flexible capacity system has the freedom to adjust

capacity. The initial capacity levels should be determined with consideration of the option

to adjust capacity and to respond optimally to the future demand evolution. In each period,

the flexible capacity system can not only expand and contract but also switch capacity from

one product to the other in an effort to maximize the total profit over a given horizon. We

assume that expansion, contraction and switching capacity take place between equally spaced

discrete capacity levels. This has been motivated by the fact that in industrial applications

the production capacity is determined by the number of machines or operators employed,

which is integer. Further, we assume that changes in the capacities are to be effective in

the following period to address time lag between decision made to change capacity and the

implementation of the capacity.

Capacity adjustment comes with cost or revenue. Let ∆ it be the change in the maximum

capacity level for product i between period t − 1 and t. That is,

∆it = M it − M it−1, i ∈ {A, B}.

11

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 14/38

A function S (∆At , ∆B

t ) is introduced to represent the cash flows in period t associated with

capacity adjustment decision made in period t − 1 to change the maximum capacity level for

product A by ∆At and that for product B by ∆B

t , effective in period t.

Cost parameters associated with capacity expansion and contraction are given in Table 3.

The flexible system, whenever it increases its maximum production level by a unit capacity

to produce product i (i ∈ {A, B}), incurs a fixed cost of si5 as well as a variable cost si1

fraction of the unit capacity installation cost ci4 for product i (i.e., si5 + si1ci4x where x is a

capacity increase). Similarly contraction of the maximum capacity for product i results in a

fixed cost si6 plus a variable cost equal to si2 fraction of the unit capacity installation cost ci4

for product i. Notice that the variable cost could be negative (i.e., positive revenue) in case

that the flexible system can find a good use for the capacity to be removed. Examples include

payment for producing OEM (original equipment manufacturer) products and salvage value

of machines to be removed.

Table 3: Cost parameters for capacity expansion and contraction

Capacity TypeExpansion Contraction

Variable Cost Fixed Cost Variable Cost Fixed Cost

Product A sA1 sA5 sA2 sA6

Product B sB1 sB5 sB2 sB6

Capacity switching between two products can be thought of as a combination of an ex-

pansion with one product and an contraction with the other. Since such capacity adjustment

takes place internally, cost or revenue associate with capacity switching may have to be based

on different parameters than those shown in Table 3. Parameters in Table 4 are for internal

12

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 15/38

capacity adjustment, under which an expansion inevitably eventuates in a contraction and

vice versa. For simplicity we assume that an expansion (or contraction) of a unit capacity

of a product could coincide with a contraction (or expansion) of a unit capacity of the other

product.

Table 4: Cost parameters for capacity switching

Capacity TypeExpansion Contraction

Variable Cost Fixed Cost Variable Cost Fixed Cost

Product A sA3 sA7 sA4 sA8

Product B sB3 sB7 sB4 sB8

When an capacity adjustment is either pure expansion or pure contraction or ∆At ·∆B

t ≥ 0,

the associated cash flow can be given by

S (∆At , ∆B

t ) = i={A,B}

{(si5 + si1ci4∆it)I {∆i

t>0} + (si6 − si2ci4∆i

t)I {∆it<0}

}.

When an capacity adjustment involves switching capacity from one product to the other or

∆At · ∆B

t < 0, the associated cash flow can be expressed as

S (∆At , ∆B

t ) = [sA7 + sB8 + (sA3 cA4 + sB4 cB4 )(−∆Bt ) + sA1 cA4 (∆A

t + ∆Bt )]I {∆A

t >−∆Bt >0}

+ [sA7 + sB8 + (sA3 cA4 + sB4 cB4 )∆At + sB2 cB4 (−∆B

t − ∆At )]I {−∆B

t >∆At >0}

+ [sB7 + sA8 + (sB3 cA4 + sA4 cB4 )(−∆At ) + sB1 cB4 (∆Bt + ∆At )]I {∆Bt >−∆

At >0}

+ [sB7 + sA8 + (sB3 cA4 + sA4 cB4 )∆Bt + sA2 cA4 (−∆A

t − ∆Bt )]I {−∆A

t >∆Bt >0}

(3)

where I {H } is an indicator function that takes value of 1 if the statement H is true and 0,

otherwise. The first term in Equation (3) is the cost of reallocating capacity of −∆Bt from

13

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 16/38

product B to A and of expanding capacity of (∆At + ∆B

t ) for product A (recall ∆Bt < 0 and

∆At + ∆B

t is the pure capacity increase). The second term is for the case of reallocating

capacity of ∆A from product B to A and of further contracting capacity for product B by

(−∆Bt − ∆A

t ) (remember −∆Bt > 0 and |∆B

t | > |∆At |). The third and the fourth terms are

the cost of reallocating capacity and expansion/contraction for the other cases.

The profit from each period is computed considering all future managerial options to

expand, contract and switch capacities. For a finite life of T years, the NPV of the flexible

system is given by

NP V (M A0 , M B0 ) = −(cA4 M A0 + cB4 M B0 ) +T t=1

e−rt{E [πA∗t (θAt , M At−1)]

+ E [πB∗t (θBt , M Bt−1)] + S (∆A

t , ∆Bt )}.

Once the NPVs of the fixed capacity system and the flexible are computed, the value of the

flexibility is merely the difference between the two NPVs.

3 THE VALUATION MODEL

This section presents steps to compute the value of manufacturing flexibility using a lattice

framework. We first perform a transformation to un-correlate the given correlated processes,

and then construct a lattice for the un-correlated processes across regimes. Finally, we apply

a dynamic programming approach to valuation of the manufacturing flexibility.

14

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 17/38

3.1 Lattice Construction

Bollen [2] introduces pentanomial lattice for a single random process with two regimes. The

random process assumes a constant growth rate and a constant volatility within a regime.

His pentanomial lattice consists of a binomial lattice and a trinomial lattice: a binomial

lattice representing the growing regime and a trinomial lattice for the decaying regime. The

advantage of the pentanomial lattice is, although more nodes are branched out from a single

node, the reduced number of nodes in the whole lattice by setting up the step size of the

lattice so that nodes from different regimes merge into a single node.

In this paper we address the case of two random processes with regime switching. Re-

call that, in case of two random processes and two regimes for each process, we identified

four possible combinations of regimes in Section 2.1, where each combination consists of two

correlated processes with constant growth rates, volatilities, and a correlation factor. There-

fore, for each of four combinations of regimes, the lattice to be constructed and the original

continuous processes should have not only the first and the second moments but also the

joint moment to be matched. Although matching three moments or coefficients of moment

generating functions of two processes can be easily done as shown in Boyle [5, 6], matching

all three moments across the four combinations of regimes – not to mention the general case

of m variables with n j( j = 1, 2, . . . , m) regimes – is a big challenge. In this paper, we present

a technique to un-correlate two process in each of four pairs of correlated processes and to

build a single lattice for all the four combinations. Those who are interested in the general

case of m variables with n j( j = 1, 2, . . . , m) regimes can find a detailed exposition of the

general approach in Wahab and Lee [21]. It should be also noticed that the technique to be

15

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 18/38

presented in this paper may not be generalized to the case of m(m > 2) processes but can

be easily extended to the case with more than 2 regimes for each process.

Let x1 and x2 be two correlated processes as given below:

dx1 = α1dt + β 1dz 1, (4)

dx2 = α2dt + β 2dz 2, (5)

where αi and β i are constants, and dz 1 and dz 2 are correlated Wiener processes with corre-

lation factor ρ. Following Hull and White [11], a new pair of processes dy1 and dy2 can be

defined from the original correlated processes given in Equation (4) and (5).

dy1 = (α1β 2 + α2β 1)dt + β 1β 2

2(1 + ρ)dz 3,

dy2 = (α1β 2 − α2β 1)dt + β 1β 2

2(1 − ρ)dz 4,

where dz 3 and dz 4 are “un-correlated” Wiener processes. The new processes dy1 and dy2

have instantaneous mean of α1β 2 + α2β 1 and α1β 2 − α2β 1, respectively, and volatility of

β 1β 2

2(1 + ρ) and β 1β 2

2(1 − ρ), respectively.

Now consider a pair of correlated demand processes dθ1 and dθ2, which are in known

regimes. That is

dθ1 = µ1θ1dt + σ1θ1dz 1, (6)

dθ2 = µ2θ2dt + σ2θ2dz 2, (7)

where µi and σi are the growth rate and the volatility of process i in the known regimes,

and dz 1 and dz 2 are correlated Wiener processes. We convert, by using Ito’s Lemma [10],

the processes given in Equation (6) and (7) into the form of Equation (4) and (5) to obtain

16

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 19/38

the following:

d ln θ1 =

µ1 − σ2

1

2

dt + σ1dz 1,

d ln θ2 =

µ2 − σ2

2

2

dt + σ2dz 2.

Let ψ1 and ψ2 be such that

ψ1 = σ2 ln θ1 + σ1 ln θ1, (8)

ψ2 = σ2 ln θ1 − σ1 ln θ2, (9)

which follow the following processes:

dψ1 =

µ1 − σ2

1

2

σ2 +

µ2 − σ2

2

2

σ1

dt + σ1σ2

2(1 + ρ)dz 3,

dψ2 =

µ1 − σ2

1

2

σ2 −

µ2 − σ2

2

2

σ1

dt + σ1σ2

2(1 − ρ)dz 4,

where dz 3 and dz 4 are un-correlated Wiener processes and ρ is the instantaneous correlation

between Wiener process dz 1 and dz 2. In summary, we obtain a pair of un-correlated pro-

cesses dψ1 and dψ2 with new growth rate

µ1 − σ212

σ2 +

µ2 − σ22

2

σ1 and

µ1 − σ21

2

σ2 −

µ2 − σ222

σ1, respectively, and new volatility σ1σ2

2(1 + ρ) and σ1σ2

2(1 − ρ), respec-

tively.

Suppose that we are given with two correlated demand processes with the instanta-

neous mean and volatility as given in Table 1 and correlation factors as given in Ta-

ble 2. By repeatedly applying the transformation of a pair of correlated processes to a

pair of un-correlated processes, we obtain 8 processes, which are coupled into 4 pairs of

un-correlated processes:{(G1G2a),(G1G2b)},{(D1D2a),(D1D2b)},{(G1D2a),(G1D2b)}, and

{(D1G2a),(D1G2b)}. In Table 5, the instantaneous mean and volatility of the resulting 8

17

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 20/38

Table 5: Instantaneous mean and volatility of 8 un-correlated processes

Process Instantaneous Mean Instantaneous Volatility

G1G2a µ1 = (µA

g − (σAg )

2

2 )σB

g

+ (µB

g − (σBg )

2

2 )σA

g

σ1 = σA

g

σB

g 2(1 + ρ1)

G1G2b µ2 = (µAg − (σAg )

2

2 )σBg − (µB

g − (σBg )2

2 )σAg σ2 = σA

g σBg

2(1 − ρ1)

D1D2a µ3 = (µAd − (σAd )

2

2 )σBd + (µB

d − (σBd )2

2 )σAd σ3 = σA

d σBd

2(1 + ρ2)

D1D2b µ4 = (µAd − (σAd )

2

2 )σB

d − (µBd − (σBd )

2

2 )σA

d σ4 = σAd σB

d

2(1 − ρ2)

G1D2a µ5 = (µAg − (σAg )

2

2 )σB

d + (µBd − (σB

d )2

2 )σA

g σ5 = σAg σB

d

2(1 + ρ3)

G1D2b µ6 = (µAg − (σAg )

2

2 )σB

d − (µBd − (σBd )

2

2 )σA

g σ6 = σAg σB

d

2(1 − ρ3)

D1G2a µ7 = (µAd

−

(σAd )2

2 )σB

g + (µBg

−

(σBg )2

2 )σA

d σ7 = σAd σB

g 2(1 + ρ4)

D1G2b µ8 = (µAd − (σAd )

2

2 )σBg − (µB

g − (σBg )2

2 )σAd σ8 = σA

d σBg

2(1 − ρ4)

processes are shown, where process G1G2a and G1G2b are from the original demand process

of product A in the growing regime G1 and that of product B in the growing regime G2,

process D1D2a and D1D2b are from the two original correlated processes in their decaying

regime, process G1D2a and G1D2b from original process for product A in the growing and

B in the decaying, and process D1G2a and D1G2b from original process A in decaying and

B in growing regime. Therefore, process G1G2a, D1D2a, G1D2a, and D1G2a can be seen as

four regimes of one un-correlated process and processes G1G2b, D1D2b, G1D2b, and D1G2b

as four regimes of the other new un-correlated process.

The next step is to build a lattice for the un-correlated processes, each of which has four

regimes with known means and known volatilities. In what follows, the exposition assumes

the general case of a single process with n regimes. As discussed in Bollen [3] and Wahab

and Lee [21], the step size of the lattice of all regimes except for one must be adjusted so that

further branching results in nodes to be merged into a fewer number of nodes. The step size

18

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 21/38

of n − 1 regimes must be adjusted so that all the nodes generated for n regimes are evenly

spaced. In order to determine the n − 1 regimes of which step sizes are to be adjusted, step

size of all n regimes are independently calculated as follows:

σ2i h + µ2

ih2, i = 1, 2, . . . , n ,

where µi and σi are mean and volatility in regime i, and h is the time interval corresponding

to a layer of the lattice. More details of the standard binomial tree construction can be found

in Cox et al. [8], Hull [10], among many. Let φ1, φ2, ....,φn be step size of regime 1, 2, . . . , n,

respectively (i.e., φi =

σ2i h + µ

2ih

2

for i = 1, 2, . . . , n). After re-naming the regimes so that

φ1 < φ2 < φ3,..,< φn, we set φ = max(φ1, φ22

, φ33

, ....., φnn

). Let φ = φkk

(i.e.,φkk ≥ φj

j , ∀ j),

then the step size φ j should be as follows:

φ j =

φk, if j = k,

j φkk

, if j = k.

(10)

Notice that the step size is adjusted so as to ensure that nodes are spaced equidistant from

each other.

The regime with step size φk must be constructed by a binomial lattice and the other

regimes (∀ j = 1, 2, 3,..,n, and j = k) must be constructed by trinomial lattices. The

conditional probabilities for all the branches emanating from a node can be computed by

matching the first and the second moments of the lattice and the given continuous processes.

The conditional branch probability of binomial lattice for regime k is given by

πφk,u = 1

2

1 +

µkh

φk

, (11)

πφk,d = 1 − πφk,u, (12)

19

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 22/38

where πφk,u is the probability for the upward branch and πφk,d is for the downward branch

in the binomial lattice. The conditional branch probabilities of trinomial lattice for regime

j = 1, 2, . . . , n( j

= k) are given by

πφj ,u = 1

2

φ2

j

( j φkk

)2+

µ jh

j φkk

, (13)

πφj ,d = 1

2

φ2

j

( j φkk

)2− µ jh

j φkk

, (14)

πφj ,m = 1 − πφj ,u − πφj,d, (15)

where πφj ,u, πφj ,m, and πφj ,d are probabilities for the upward, the middle, and the downward

branch of the trinomial lattice, respectively. Notice that Equation (13), (15), and (14)

become Equation (11) and (12) when j = k as the middle branch degenerates.

Applying the lattice construction steps to the two un-correlated processes – one with 4

regimes G1G2a, D1D2a, G1D2a and D1G2a, and the other with 4 regimes G1G2b, D1D2b,

G1D2b, and D1G2b – gives two nanonomial lattices. One of the four regimes is represented

by a binomial lattice and the rest three regimes are represented by trinomial lattices.

Now that two lattices are built for the two un-correlated processes, the last step is to

combine the two nanonomial lattices to get a higher dimensional lattice for a two-state-

variable process. We will call the resulting lattice as a product lattice. An example of

spatial pattern of 29 child nodes emanating from a parent node is illustrated in Figure 3.

The example is under the following conditions:

(φ7

4 >

φ5

3 >

φ3

2 > φ1) and (

φ8

4 >

φ6

3 >

φ4

2 > φ2)

It should be noticed that in the product lattice nodes are defined only for 4 valid combina-

tions of regimes: (G1G2a,G1G2b), (D1D2a,D1D2b), (G1D2a,G1D2b), and (D1G2a,D1G2b).

20

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 23/38

For example, nodes are generated for a combination (G1G2a, G1G2b) but not for a com-

bination (G1G2a, D1D2b). Therefore, each parent node has 29 child nodes, with 3 nodes

stacked at the center node, rather than 81. Conditional branch probability of each branch

of the product lattice is computed as the product of two conditional branch probabilities of

the two corresponding branches from the original nanonomial lattice.

Figure 3: Pattern of Child Nodes

Numbers in the parenthesis at each node of the lattice in Figure 3 are conditional probabil-

ities from the two nanonomial lattices. These probabilities can be calculated using Equation

(11) through (14). First subscript of the probability indicates the step size of the branch that

21

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 24/38

corresponds to the nonanomial lattice, and the second subscript indicates the position of the

branch in the nonanoimal lattice. Step size in the vertical direction is one-forth of the step

size of the process that is modeled in binomial lattice in the first nonanomial lattice; step

size in the horizontal direction is one-fourth of the step size of the process that is modeled in

binomial lattice in the second nonanomial lattice. The conditional branching probability of

the branch in the product lattice is simply a product of the two probabilities in parenthesis.

The step size has been set so that nodes generated from a single node will be merged

into 64n2 − 168n + 109 nodes after n(> 1) layers of nodes are generated. As more layers are

generated, nodes in a vicinity are branching to common nodes. The reduction in the number

of nodes due to the merger enabled by carefully determined step size is simply dramatic.

It must be noted that the lattice is constructed over some integer, n, time steps. The

duration, t, between adjacent layers in the lattice is equal to T /n. In order to generate the

process in the lattice the demand quantity and capacity levels must be scaled by t. When

the annual continuous rate of change of the demand is assumed to be normally distributed

with mean µ and volatility σ, the continuous rate of change of the demand over time step t is

normally distributed with a mean of µt and volatility σ√

t. The moment matching between

the lattice and the original processes should be done accordingly.

3.2 Valuing the Project and the Flexibility

The way in which the manufacturing flexibility is exercised is significantly more complex

than do financial options and analytical valuation models developed for financial options

may often fail to value managerial options in manufacturing system such as flexibility. This

22

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 25/38

motivates us to develop a lattice-based approach to valuation of manufacturing flexibility.

At each node we know what combination of regimes the current node is generated for

along with values of the two un-correlated random variables. Let ψ1 and ψ2 be the values

represented by the current node, which are realizations of the two un-correlated variables.

From the regime information, we choose appropriate volatilities in order to recover the values

of original correlated variable by using the transformation given by Equation (8) and (9) in

the exactly reversed direction. For example, if the current node is for un-correlated processes

G1G2a and G1G2b, that is the node is for the two original variables in regime combination

(G1,G2), and contains two values ψ1 and ψ2 for un-correlated variables, variables θAt (demand

for product A at time t) and θBt (demand for product B at time t) start in growing regime,

the value of correlated variables θAt and θBt are given below:

θAt = exp

ψ1 + ψ2

2σBg

and θBt = exp

ψ1 − ψ2

2σAg

, (16)

where t can be uniquely determined by the layer from which the current node is drawn.

Similarly if the current node is from a different regime combination, we again use Equation

(16) but with different volatilities.

The standard numerical approach to valuing real options is the backward dynamic pro-

gramming. The valuation procedure begins at the terminal nodes and rolls back recursively

toward the root of the lattice. For all terminal nodes, project value is the final cash flow

conditional on demand levels at terminal nodes and capacity levels at prior nodes. For inter-

mediate nodes, the project value is the sum of the current project value and the discounted

expected project value in the next time period and on. In order to choose the optimal capac-

ity levels, for the given capacity level of prior node, the project value is maximized over all

23

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 26/38

possible capacity levels. Therefore, the discounted expected future values reflect the possibil-

ity of capacity adjustment (expansion, contraction and switching). The expectation is also

with respect to possible regime switching in the next period. The value of the project (or

the manufacturing system over a given horizon) is simply the discounted expected project

value at the root node of the lattice. The same calculation with fixed capacity levels for

two product gives the project value of the fixed manufacturing system. The value of the

flexibility is merely the difference between the two project values.

Let NPV(θAt , θBt , j, M At , M Bt , t) be the net present value (NPV) of the project conditional

on demand level of product A, θAt , demand level of product B, θBt , j-th combination of regimes

(where (G1, G2), (D1, D2), (G1, D2), and (D1, G2) are the 1-st, the 2-nd, the 3-rd, and

the 4-th regime combination, respectively), the maximum capacity level for product A, M At ,

and for product B, M Bt . Furthermore, let EV(θAt+1, θBt+1, j , M At+1, M Bt+1, t) be the discounted

expected future value given that the maximum capacity level for product A and B have

been changed to M At+1 and M

Bt+1, respectively. The NPV is maximized by searching over all

possible combinations of capacity levels. This is

NP V (θAt , θBt , j, M At , M Bt , t) =

maxM At+1,M Bt+1

πA∗t (θAt , M At ) + πB∗

t (θBt , M Bt ) + S (M At , M At+1, M Bt , M Bt+1)

+ EV [θAt+1, θBt+1, j , M At+1, M Bt+1, t]

.

The discounted expected value, EV [·, ·, ·, ·, ·, ·], differs across different regimes because

each regimes is represented by different set of branches. The unidirectional regime switching

complicates the computation of the discounted expected value. For example, if the current

regimes is (G1, G2), regime in the next period can be (G1, G2), (G1, D2), (D1, G2), or (D1,

24

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 27/38

D2), whereas if the current regime is (D1, D2), it can be only (D1, D2) in the next period.

Therefore, EV [·, ·, ·, ·, ·, ·] is conditional on the current regime. Let pA(t) and pB(t) be the

probabilities of switching from growing to decaying at time t in the life cycles of product A

and B, respectively.

If the current regime is (G1, G2):

EV (θAt+1,θBt+1, (G1, G2), M At+1, M Bt+1, t) =

e−rt{(1 − pA(t))(1 − pB(t))E [NP V (θAt+1, θBt+1, (G1, G2), M At+1, M Bt+1, t + 1)]

+ pA(t) pB(t)E [N P V (θAt+1, θBt+1, (D1, D2), M At+1, M Bt+1, t + 1)]

+ (1 − pA(t)) pB(t)E [N P V (θAt+1, θBt+1, (G1, D2), M At+1, M Bt+1, t + 1)]

+ pA(t)(1 − pB(t))E [N P V (θAt+1, θBt+1, (D1, G2), M At+1, M Bt+1, t + 1)]}

If the current regime is (D1, D2):

EV (θAt+1,θBt+1, (D1, D2), M At+1, M Bt+1, t) =

e−rt{E [N P V (θAt+1, θBt+1, (D1, D2), M At+1, M Bt+1, t + 1)]}

If the current regime is (G1, D2):

EV (θAt+1,θBt+1, (G1, D2), M At+1, M Bt+1, t) =

e−rt{ pA(t)E [N P V (θAt+1, θBt+1, (D1, D2), M At+1, M Bt+1, t + 1)]

+ (1 − pA(t))E [N P V (θAt+1, θBt+1, (G1, D2), M At+1, M Bt+1, t + 1)]}

If the current regime is (D1, G2):

EV (θAt+1,θBt+1, (D1, G2), M At+1, M Bt+1, t) =

e−rt{ pB(t)E [NP V (θAt+1, θBt+1, (D1, D2), M At+1, M Bt+1, t + 1)]

+ (1 − pB(t))E [NP V (θAt+1, θBt+1, (D1, G2), M At+1, M Bt+1, t + 1)]}

25

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 28/38

We assume switching probabilities are from a cumulative normal distribution function

of the time elapsed from the introduction of product. The expectation of NPV can be

computed as the product of conditional branch probabilities and their corresponding NPV.

The backward dynamic programming approach is carried out from the terminal layer to the

root node of the lattice. At the root node, the discounted expected value of the whole project

can be found for each possible combination of initial capacity levels. The initial capacity

level that maximizes the NPV values of project at the root node is an optimal capacity level.

4 NUMERICAL EXAMPLE

We present a numerical example of a manufacturing system producing two products to

meet random demand streams over a given horizon. We investigate the impact of various

parameters of the manufacturing system on the value of manufacturing flexibility. The

project spans over a 5 years period, during which time the flexible capacity manufacturing

system optimally determines the production levels for two products at every period, whereas

the fixed capacity system has a single chance to set the capacity levels at time 0, so as

to maximize the total discounted expected profit over the horizon. Both products are in

growing regime at the beginning of the project and may switch into decaying regime anytime

with probability drawn from normal distribution with the mean 2.8 years and the variance

0.5 years for product A and the mean 2.3 years and the variance 0.5 years for product B,

respectively.

The capacity level for product A and B can be adjusted among 10 equally spaced levels

with a unit increment in capacity amounting to production of 2 additional units of corre-

26

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 29/38

sponding product per period. In each period the maximum capacity levels M it for product

A and B are sought for among 100 possible combinations of capacity levels to maximize the

profit in the current period as well as the discounted expected profit in the remaining future.

Regular capacity level of type A is 75% of the maximum capacity level; types B is 80% of

the maximum capacity level. The parameters used in the example related to the demand

evolution are given below:

ρ1 = 0.60, (µAg , σA

g ) = ( 36%, 30%),

ρ2 = 0.55, (µAd , σA

d ) = (-18%, 20%),

ρ3 = -0.45, (µBg , σB

g ) = ( 24%, 20%),

ρ4 = -0.50, (µBd , σB

d ) = (-24%, 25%).

The riskless rate of interest is 10% and the initial monthly demand of product A is 10 and

product B is 12. Unit prices of product A and B are $30,000 and $25,000, respectively. Cost

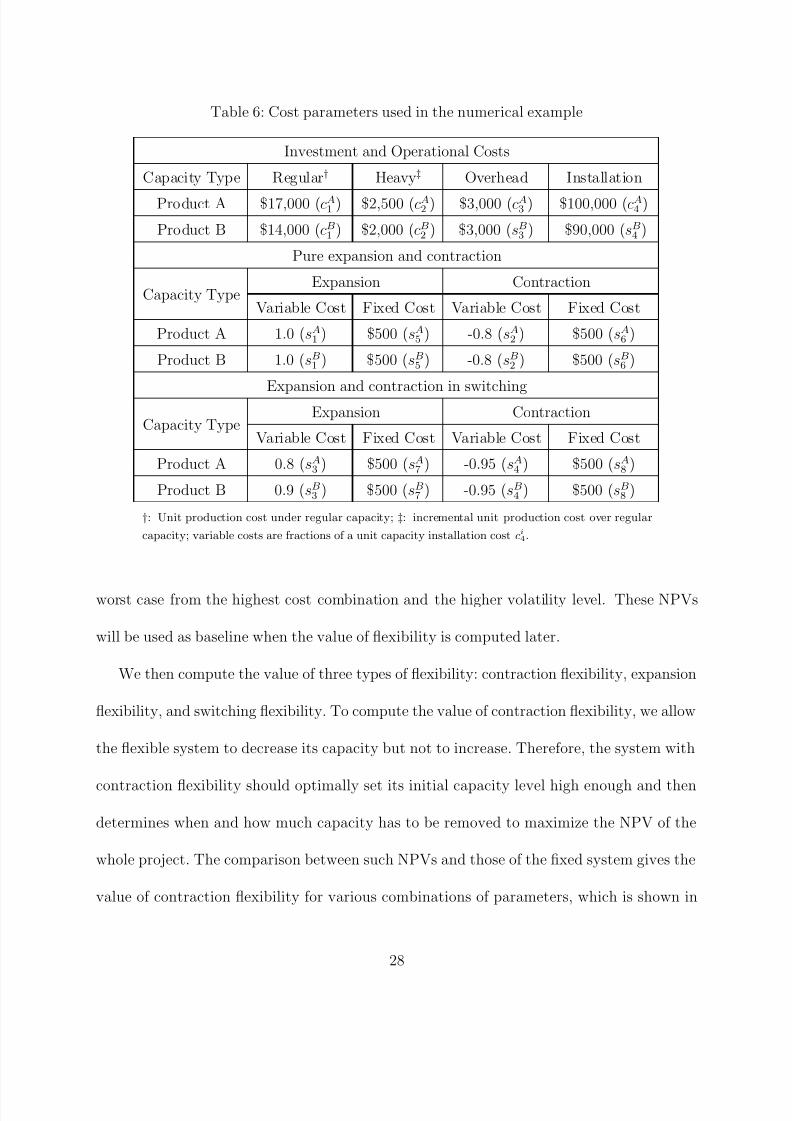

parameters associated with production and capacity adjustment are given in Table 6.

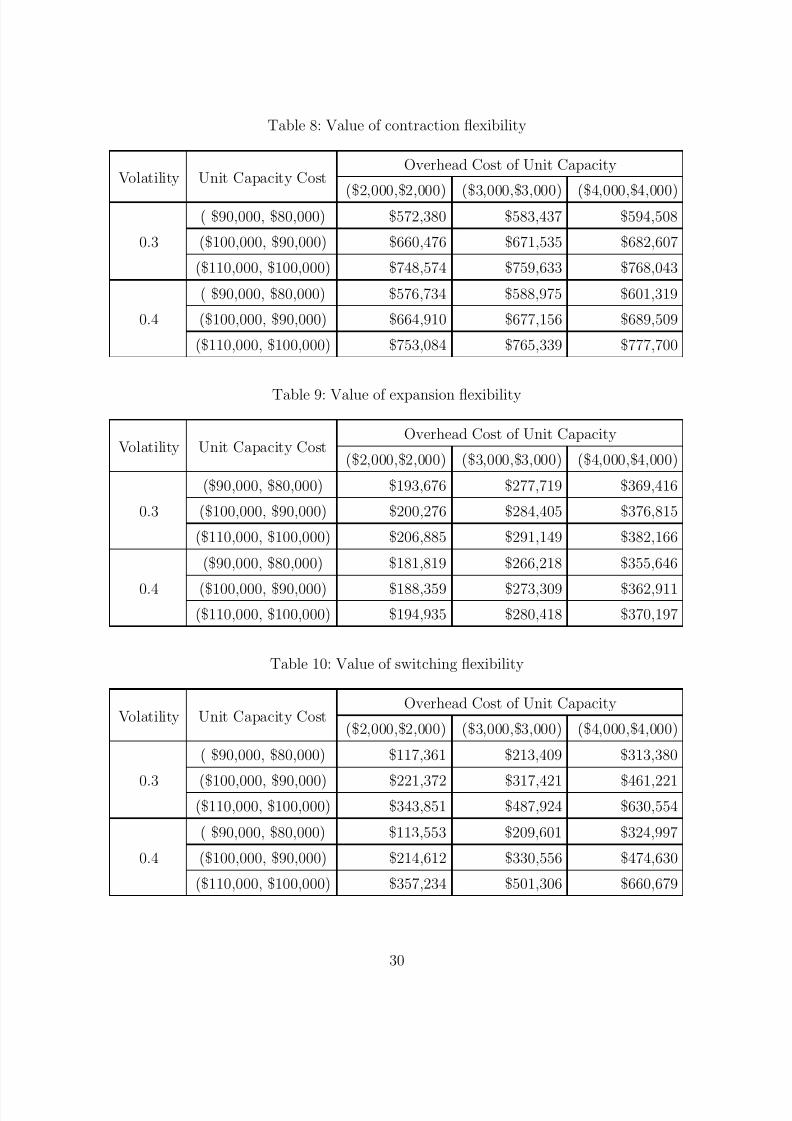

The first experiment is carried out to compute the value of different types of manu-

facturing flexibility – expansion, contraction, switching, and the combination of all three

flexibilities – with changing values for the cost parameters such as the overhead cost of unit

capacity for product A (cA3 ) and B (cB3 ), the unit capacity installation cost for product A

(cA4 ) and B (cB4 ), and the volatility level of product A in its growing regime. The results are

presented in Table 7 through Table 11.

Table 7 shows the net present value (NPV) of the fixed capacity system for total 18 com-

binations of 5 parameters. For every combination, the initial capacity level is set optimally

to maximize the NPV at time 0. As clearly shown, the NPV decreases as the unit capacity

installation cost and/or the unit capacity overhead cost increase. The maximum NPV, which

is from the lowest cost combination and the lower volatility level, is 25% higher than the

27

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 30/38

Table 6: Cost parameters used in the numerical example

Investment and Operational Costs

Capacity Type Regular† Heavy‡ Overhead Installation

Product A $17,000 (cA1 ) $2,500 (cA2 ) $3,000 (cA3 ) $100,000 (cA4 )

Product B $14,000 (cB1 ) $2,000 (cB2 ) $3,000 (sB3 ) $90,000 (sB4 )

Pure expansion and contraction

Capacity TypeExpansion Contraction

Variable Cost Fixed Cost Variable Cost Fixed Cost

Product A 1.0 (sA1 ) $500 (sA5 ) -0.8 (sA2 ) $500 (sA6 )

Product B 1.0 (sB1 ) $500 (sB5 ) -0.8 (sB2 ) $500 (sB6 )

Expansion and contraction in switching

Capacity TypeExpansion Contraction

Variable Cost Fixed Cost Variable Cost Fixed Cost

Product A 0.8 (sA3 ) $500 (sA7 ) -0.95 (sA4 ) $500 (sA8 )

Product B 0.9 (sB3 ) $500 (sB7 ) -0.95 (sB4 ) $500 (sB8 )

†: Unit production cost under regular capacity; ‡: incremental unit production cost over regular

capacity; variable costs are fractions of a unit capacity installation cost ci4.

worst case from the highest cost combination and the higher volatility level. These NPVs

will be used as baseline when the value of flexibility is computed later.

We then compute the value of three types of flexibility: contraction flexibility, expansion

flexibility, and switching flexibility. To compute the value of contraction flexibility, we allow

the flexible system to decrease its capacity but not to increase. Therefore, the system with

contraction flexibility should optimally set its initial capacity level high enough and then

determines when and how much capacity has to be removed to maximize the NPV of the

whole project. The comparison between such NPVs and those of the fixed system gives the

value of contraction flexibility for various combinations of parameters, which is shown in

28

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 31/38

Table 7: NVP of Fixed System

Volatility Unit Capacity CostOverhead Cost of Unit Capacity

($2,000,$2,000) ($3,000,$3,000) ($4,000,$4,000)

( $90,000, $80,000) $12,179,293 $11,218,808 $10,258,323

0.3 ($100,000, $90,000) $11,979,293 $11,018,808 $10,058,323

($110,000, $100,000) $11,779,293 $10,818,808 $9,858,323

( $90,000, $80,000) $12,107,645 $11,147,158 $10,186,670

0.4 ($100,000, $90,000) $11,907,645 $10,947,158 $9,986,670

($110,000, $100,000) $11,707,645 $10,747,158 $9,786,670

Table 8. Similar experiments find the value of expansion flexibility shown in Table 9 and the

value of switching flexibility shown in Table 10.

Interesting patterns are observed. First, the value of switching flexibility is almost equally

sensitive to the capacity installation cost and to the capacity overhead cost, whereas the value

of contraction flexibility is sensitive only to the capacity installation cost and the value of

expansion capacity is sensitive only to the capacity overhead cost. Due to its sensitivity

to both costs, it sways over a wider range: its lowest value is $113,553 and its highest

value is $660,679. Second, as the volatility of product A in the growing regime increases

from 30% to 40%, the value of switching flexibility decreases in three instances, where

both the installation and the overhead cost are low: {($2,000,$2,000),($90,000,$80,000)},

{($2,000,$2,000),($100,000,$90,000)

}, and

{($3,000,$3,000),($90,000,$80,000)

}). High volatil-

ity typically implies high value of flexibility. However, in the three instances, the optimal

initial capacity level of is 8 for product A and 9 for product B, which are close to the maxi-

mum capacity level that the flexible system can take, and the flexible system has little room

to shift its capacity between the two products (This is also why the value of contraction

29

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 32/38

Table 8: Value of contraction flexibility

Volatility Unit Capacity CostOverhead Cost of Unit Capacity

($2,000,$2,000) ($3,000,$3,000) ($4,000,$4,000)( $90,000, $80,000) $572,380 $583,437 $594,508

0.3 ($100,000, $90,000) $660,476 $671,535 $682,607

($110,000, $100,000) $748,574 $759,633 $768,043

( $90,000, $80,000) $576,734 $588,975 $601,319

0.4 ($100,000, $90,000) $664,910 $677,156 $689,509

($110,000, $100,000) $753,084 $765,339 $777,700

Table 9: Value of expansion flexibility

Volatility Unit Capacity CostOverhead Cost of Unit Capacity

($2,000,$2,000) ($3,000,$3,000) ($4,000,$4,000)

($90,000, $80,000) $193,676 $277,719 $369,416

0.3 ($100,000, $90,000) $200,276 $284,405 $376,815

($110,000, $100,000) $206,885 $291,149 $382,166

($90,000, $80,000) $181,819 $266,218 $355,646

0.4 ($100,000, $90,000) $188,359 $273,309 $362,911($110,000, $100,000) $194,935 $280,418 $370,197

Table 10: Value of switching flexibility

Volatility Unit Capacity CostOverhead Cost of Unit Capacity

($2,000,$2,000) ($3,000,$3,000) ($4,000,$4,000)

( $90,000, $80,000) $117,361 $213,409 $313,380

0.3 ($100,000, $90,000) $221,372 $317,421 $461,221($110,000, $100,000) $343,851 $487,924 $630,554

( $90,000, $80,000) $113,553 $209,601 $324,997

0.4 ($100,000, $90,000) $214,612 $330,556 $474,630

($110,000, $100,000) $357,234 $501,306 $660,679

30

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 33/38

flexibility is much higher than that of expansion flexibility). Third, the value of contraction

flexibility is much more sensitive to the capacity installation cost than to the overhead cost,

whereas the value of expansion flexibility is much more sensitive to the overhead cost than

to the installation cost. This is quite counter-intuitive in that one would guess that the

capability of reducing the capacity is more and more important as the cost of maintaining

capacity becomes more costly. Since two types of flexibility are sensitive to two different

cost parameters, the total flexibility becomes sensitive to the overhead and installation cost

to more or less the same degree.

When the system has the complete freedom in adjusting the capacity levels, the value

of flexibility is more than any of the restricted flexibilities. The total value of flexibility is

computed with the full flexibility and given in Table 11. Notice that the value of complete

flexibility is not necessarily equal to the sum of the values of three flexibility types.

Table 11: Total value of flexibility

Volatility Unit Capacity CostOverhead Cost of Unit Capacity

($2,000,$2,000) ($3,000,$3,000) ($4,000,$4,000)

( $90,000, $80,000) $955,449 $1,042,041 $1,130,198

0.3 ($100,000, $90,000) $1,092,556 $1,179,742 $1,268,591

($110,000, $100,000) $1,254,974 $1,345,924 $1,441,864

( $90,000, $80,000) $962,795 $1,049,542 $1,140,703

0.4 ($100,000, $90,000) $1,101,649 $1,189,665 $1,284,516

($110,000, $100,000) $1,264,983 $1,361,322 $1,461,855

As expected, the value of flexibility increases as the cost of capacity (installation and

maintenance cost) increases. The maximum value of flexibility among all 18 combinations of

various cost parameters is 53% more than the lowest value and amounts to 15% of the NPV

31

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 34/38

of the fixed capacity system.

Lastly, we investigate how the value of flexibility reacts to changes in the regime switching

mean and volatility. The mean and volatility of regime switching process are presented in

years in Table 12 along with the value of flexibility for each combination of the mean and the

volatility. It is intuitive to have the value of flexibility increasing as the mean of switching

Table 12: Total Value of Flexibility with Product Life cycles

Volatility Switch MeanVolatility of Switching Distribution

(0.25, 0.25) (0.5, 0.5) (0.75, 0.75)

(1.2, 1.1) $1,001,769 $987,964 $975,530

0.3 (2.8, 2.3) $1,185,993 $1,179,742 $1,174,355

(3.8, 3.6) $1,252,331 $1,249,066 $1,246,279

(1.2, 1.1) $1,011,410 $998,504 $987,007

0.4 (2.8, 2.3) $1,196,451 $1,189,665 $1,183,897

(3.8, 3.6) $1,277,420 $1,273,168 $1,269,557

distribution increases since the future demands are more likely to get larger as the products

stay in their growing regime longer. As a result the optimal level of capacity in the future is

higher than that of today and the expansion flexibility becomes more valuable. The reaction

of the value of flexibility to the uncertainty in the future demand is interesting. The value of

flexibility increases as the volatility of the future demand increases as we expect. However,

it decreases as the variance of the regime switching distribution increases. Considering that

both the volatility of future demand and the variance of the regime switching distribution

represent the different dimensions of uncertainty, it might seem somewhat contradictory. One

possible explanation for this is that the larger variance of the regime switching spreads the

32

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 35/38

peak demands for the two products over a wider range in time and the manufacturing system

would not dramatically change its capacity over time. Therefore, the value of flexibility is

reduced.

5 CONCLUSIONS

Unlike financial options, the lifespan of a real option such as manufacturing flexibility is typ-

ically over multiple years, which makes the assumption of stationarity unrealistic. Moreover,

it is often the case that a manufacturing system produces multiple products and the way to

exercise flexibility embedded in the system requires complicated steps. As a result it is not

possible to use analytical solutions developed for financial option valuation in the valuation

of complex manufacturing flexibility.

In this paper we construct a lattice for two correlated variables with regime switch-

ing. Transformation to obtain uncorrelated processes allows us to build a lattice using the

traditional moment matching approach. We employ a dynamic programming approach to

valuation of the manufacturing flexibility. The numerical studies on an example hint many

interesting aspects of manufacturing flexibility as discussed in Section 4. However, extensive

studies are required before generalizing our observations.

Due to the exponentially increasing number of node in the lattice as the number of

variables increases, it still remains a challenge to study manufacturing flexibility with more

than 2 variables. The approach presented in the paper would not support the case with

more than 2 variables and a general lattice framework dealing with n(n > 2) variables can

be found in Wahab and Lee [21].

33

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 36/38

References

[1] F. Bass. A new product growth model for consumer durables. Management Science ,

15:215–227, 1969.

[2] J. Bengtsson. Manufacturing flexibility and real options: A review. International Jour-

nal of Production Economic , 74:213–224, 2001.

[3] N. P. Bollen. Valuing options in regime-switching models. Journal of Derivatives , 6:38–

49, 1998.

[4] N. P. Bollen. Real option and product life cycle. Management Science , 45(5):670–684,

1999.

[5] P. P. Boyle. A lattice framework for option pricing with two state variables. Journal of

Financial and Quantitative Analysis , 23:1–12, 1988.

[6] P. P. Boyle, J. Evnine, and S. Gibbs. Numerical evaluation of multivariate contingent

claims. The Review of Financial Studies , 2(2):241–250, 1989.

[7] M. Brennan and E. Schwartz. Evaluating natural resource investment. Journal of

Business , 58:135–157, 1985.

[8] J. Cox, S. Ross, and M. Rubinstein. Option pricing: A simplified approach. Journal of

Financial Economics , 7:229–264, 1979.

[9] H. He and R. Pindyck. Investment in flexible production capacity. Journal of Dynamics

and Control , 16:575–599, 1992.

34

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 37/38

[10] J. Hull. Options, Futures, and Other Derivatives . Prentice-Hall, New Jersey, 2002.

[11] J. Hull and A. White. Valuing derivative securities using the explicit finite difference

method. Journal of Financial and Quantitative Analysis , 25:87–100, 1990.

[12] N. Kulatilaka. Valuing the flexibility of flexible manufacturing system. IEEE Transac-

tions on Engineering Management , 35:250–257, 1988.

[13] S. Majd and R. Pindyck. Time to build, option value, and investment decision. Journal

of Financial Economics , 19:7–27, 1987.

[14] R. McDonald and D. Siegel. Investment and the valuation of firms when there is an

option to shut down. International Economic Review , 26:331–349, 1985.

[15] R. McDonald and D. Siegel. The value of waiting to invest. The Quarterly Journal of

Economics , 101:707–727, 1986.

[16] J. Norton and F. Bass. A diffusion theory model od adoption and substitution for

successive generations of high-technology products. Management Science , 41:713–721,

1987.

[17] R. Pindyck. Irreversible investment, capacity choice, and the value of the firm. The

American Economic Review , 78:969–985, 1988.

[18] A. Sethi and S. Sethi. Flexibility in manufacturing: A survey. The International Journal

of Flexible Manufacturing Systems , 2:289–328, 1990.

[19] G. Tannos. Capital budgeting for volume flexible equipment. Decision Science , 27:157–

184, 1996.

35

7/17/2019 Flexibility on Switching Option

http://slidepdf.com/reader/full/flexibility-on-switching-option 38/38

[20] A. Triantis and J. Hodder. Valuing flexibility as a complex option. The Journal of

Finance , 45:549–565, 1990.

[21] M. Wahab and C.-G. Lee. A lattice approach to a multi-variate contingent claims with

regime switching. Technical Report (MIE-OR TR2005-03), Department of Mechanical

and Industrial Engineering at the Univefsity of Toronto, 2005.