flying geese in asia: the impacts of japanese mncs as a source

TRANSCRIPT

Tijdschrift voor Economische en Sociale Geografie – 2004, Vol. 95, No. 1, pp. 3–26.© 2004 by the Royal Dutch Geographical Society KNAGPublished by Blackwell Publishing Ltd., 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden MA 02148, USA

FLYING GEESE IN ASIA: THE IMPACTS OF JAPANESE MNCs AS A SOURCE OF INDUSTRIAL LEARNING

ROGER HAYTER* & DAVID W. EDGINGTON**

*

Department of Geography, Simon Fraser University, Burnaby, British Columbia V5A 1S6, Canada. E-mail: [email protected]

**

Department of Geography, University of British Columbia, Vancouver, British Columbia V6T 1Z2, Canada. E-mail: [email protected]

Received: February 2003; revised June 2003

ABSTRACTPacific Asia has looked to direct foreign investment (DFI) to achieve economic growth andtechnological catch-up, and Japanese multinational corporations (MNCs) have responded mass-ively. This paper evaluates Japanese MNCs as a source of industrial learning and technologicaltransfer in the region, drawing from a large research literature and from the authors’ own surveysof Japanese DFI in the electronics sector. Japan’s historic learning-based approach to industrialisa-tion is captured by the flying geese metaphor of structural transformation. As an explanation ofthe transfer of technological know-how from Japan to Pacific Asia, however, the flying geese modelis problematical. This paper reflects on the effectiveness, problems and dilemmas of JapaneseMNCs in transferring such know-how to the region from a political economy perspectivesummarised as a ‘reverse product cycle model’. This model portrays DFI as a ‘bargain’ betweenJapanese MNCs and host countries, and which becomes more difficult to negotiate as DFI movesfrom low-skilled manufacturing to more innovative activities. The bases for this hypothesis relateto the increased complexity of industrial know-how and the conflicting motivations between MNCsand host countries in early stages of the product life cycle. In practice, however, this ‘bargain’ hasdeveloped differently among Asian countries, and we illustrate these differences by comparingthe experiences of South Korea, Taiwan and Malaysia.

Key words: Japanese MNCs, industrial learning, the reverse product cycle model, Malaysia, Taiwan

and Korea

In Freeman’s (1987, 1988) model of long-runindustrialisation, the Japanese economy fea-tures highly distinctive innovation systemsand leading exemplars of flexible production,the signature development of post-Fordism, orwhat he signifies as ‘the information and com-munication techno-economic [ICT] paradigm’(see also Fruin 1992; Kenney & Florida 1993).This model has global relevance as Japan hasbecome a leading exporter of manufacturedgoods and as Japanese multinational corpora-tions (MNCs) have expanded their overseas’

operations substantially during the last 20 years(Edgington 1993). Indeed, in the USA, theonly national economy now larger than Japan,the Federal Government sponsored a study toassess what the United States might learn fromJapanese-style production systems (Liker

et al.

1999). Japanese competitiveness has subse-quently been critiqued (Porter

et al.

2000), butits industrial companies are tenacious andremain powerful (Nihon Indasutoriaru Pafo-mansu Linkai 1997; Karatsu 1999). The studentof industrialisation once thought only to be

4

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

good at copying, has now apparently become ateacher.

1

This paper reflects on the impacts of JapaneseMNCs in Pacific Asia as a source of industriallearning or know-how.

2

Countries in the regionhave actively sought to ‘catch-up’ economicallyand technologically with advanced countries byattracting direct foreign investment (DFI), andJapanese MNCs have invested there to a greaterdegree (overall) than those from the UnitedStates or from Europe. Indeed, these MNCsbind together a Japanese centred, dynamic divi-sion of labour that is the Asian basis for the glo-bal triad of dominant economic regions (Gibb& Michalak 1994). Moreover, Japan is still theonly country in Asia, or beyond the realm of theNorth Atlantic, to reach industrial core status,providing a cultural model impossible for US orEuropean MNCs to duplicate. Japanese imper-ialism in the first half of the 20th century thatthreatened Asia, often savagely, also helped nur-ture notions of independence from Europeancolonists (Wong 1997). Whether or not JapaneseMNCs can significantly aid the technologicalaspirations of other Pacific Asia countries, how-ever, is uncertain. Moreover, within the devel-oping (or latecomer) countries of Pacific Asia,there is recognition that technology growth isfacilitated by various institutional channels, suchas original equipment manufacturing (OEM),licensing and joint ventures as well as by DFI.Consequently, host country attitudes towardsJapanese MNCs have varied greatly (Andersson& Poon 2001).

Debates about the implications of MNCs forlocal technology transfer are not new and theconventional view of MNCs as sources of indus-trial learning and catalysts for modernisationhas long been questioned. For example, LatinAmerican dependency theorists saw MNCs asagents of ‘underdevelopment’ (Frank 1967)and Canadian nationalists have criticised MNCsfor their ‘truncating’ effects on domestic tech-nology capacity (Britton 1980; Hayter 1982).Recently, these concerns have been reinforcedby the ‘regional fragmentation’ and ‘cathedralin the desert’ hypotheses (Amin & Robins 1990;Grabher 1993). The debate remains unresolved,however, and in Pacific Asia Japanese DFIcontinues to be justified in terms of technolog-ical transfer

qua

technological capability thatwe define as the endogenous ‘ability to solve

scientific and technological problems and tofollow, assess, and exploit scientific and tech-nological developments’ in the market place(Britton & Gilmour 1978, p. 130). Moreover,Japanese production systems are regarded asdistinctive, notably because Japanese MNCshave helped pioneer the idea of firms aslearning organisations (Patchell 1993a, 1993b).In addition, host countries in Pacific Asia areacutely conscious of technological transferissues and have introduced various policies tostimulate transfers of know-how from MNCs.

The special relationships or ‘embrace’ (Hatch& Yamamura, 1996) between Japan and Asia iscaptured by the ‘flying geese’ metaphor, whichcentres upon the importance of Japanese DFIfor Asian industrialisation (Phongpaichit 1990;Kwan 1994; Dobson & Yue 1997; Itagaki 1997;Edgington & Hayter 2000). According to theproponents of this (made-in-Japan) economicmodel of development, the Japanese MNCs, the‘lead geese’, are prime organisers of a rapidlyevolving division of labour in Asia, as successivewaves of DFI incorporate new (Asian) industrialspaces while upgrading the spaces previouslyindustrialised (Ozawa 1999). Readily incorpor-ated within neo-liberal orthodoxy the flyinggeese model powerfully communicates a senseof close links between the explosion of JapaneseFDI in Asia and Asian growth (Nomura ResearchInstitute 1995; Dobson 1997). However, with itsconnotations of apparent seamless transfer ofJapanese capabilities to Asia, this model has notgone uncontested (see Bernard & Ravenhill1995; Fujita & Hill 1996; Hatch & Yamamura1996; Hart-Landsberg & Burkett 1998). Therecent Asian currency crisis and economic slow-down in Japan has sharpened this censure whilepointing paradoxically to a long-term commit-ment to Asia by Japanese companies (Edging-ton & Hayter 2001a). Moreover, Japan’s ownindustrialisation and the original formulationof the flying geese model that addressed solelydomestic transformation in Japan, did not anti-cipate a major role for DFI.

3

Can, therefore,the rest of Asia be expected to develop via arevised flying geese model that gives primacyto overseas investments and MNC-centredindustrialisation?

This study examines both the experiences ofJapan, ‘the teacher’ and of ‘student’ host coun-tries in Pacific Asia who are learning (or have

FLYING GEESE IN ASIA

5

© 2004 by the Royal Dutch Geographical Society KNAG

learned) the secrets of industrialization. Inthe latter regard, the discussion distinguishesbetween host countries that differ in terms ofthe stage of industrialisation and attitudestowards DFI from Japan. In particular, the studyfocuses on the experience of two north-eastAsian host countries, namely South Korea andTaiwan, that have attracted Japanese DFI sincethe 1960s, and Malaysia in Southeast Asia, acountry that has been especially active in entic-ing Japanese MNCs since the 1980s. Examplesare used from the electronics industry becauseit exemplifies well the ‘staged development’patterns inherent in the flying geese model(Edgington & Hayter 2000) and because it hasbeen the leading export sector for the threecase study host economies.

4

The discussion isbased on a review of the burgeoning literaturethat seeks to make sense of Japanese MNCs asa source of learning in Asia, combined with ourown field research conducted in Japan, HongKong, mainland China, Singapore and Malaysiaduring 1997 to 2001.

The remainder of the paper proceeds inthe following way. The second section empha-sises the historical significance of the Japaneseapproach to the ‘problem of industrial trans-formation’, one which largely avoided DFI fromoverseas and featured a remarkable commitmentto understanding leading-edge technologyand institutions overseas, regardless of origin(Freeman 1987; Fruin 1992; Reischauer 1991).The evolution of Japanese MNCs as learningorganisations has been an inherent, dynamiccomponent of this commitment. In the follow-ing three sections, the evolution of JapaneseMNCs in Asia is traced and their effectiveness,problems and dilemmas of Japanese MNCsin transferring ‘learning’ and ‘know-how’ tothe region is studied. In particular, we extendHobday’s (1995a) novel political economyinterpretation of technology transfer, speci-fically developed in the context of Japanese FDIin Asia. This interpretation is summarised as a‘reverse product cycle model’, one that portraysFDI as a ‘bargain’ between Japanese MNCsand host countries, and which becomes moredifficult to negotiate as FDI moves from low-skilled manufacturing to more innovative activ-ities. The bases for this hypothesis relate to theincreased complexity of industrial know-howand the conflicting motivations between MNCs

and host countries in early stages of the productlife cycle. In practice, however, this ‘bargain’ hasdeveloped differently among Asian countries,and in sections three and four the experienceof South Korea, Taiwan and Malaysia is com-pared. The authors claim these differences helpunderpin variations in overall economic per-formance among Pacific Asia countries duringthe last 30 years or so. In the conclusion, theassessment of this model includes thoughtson China, where Japanese FDI has recentlyfocused.

INDUSTRIALISATION AND ‘LEARNING TECHNOLOGY’: JAPANESE EXPERIENCE FOLLOWING THE MEIJI RESTORATION AND THE SECOND WORLD WAR

In the modern history of industrialisation, ini-tiated by the Industrial (and related) Revolu-tion(s) in the United Kingdom in the late 18thcentury, Japan became the world’s most impor-tant example of a ‘late developer’ (Saxenhouse1999). In this regard, choice and outside forcesshaped the timing of Japan’s late development.For over 250 years, during the Tokugawa or Edoperiod (1600–1867), unified Japan chose self-imposed exclusion from the rest of the worldand developed an enormous lag in technolog-ical and institutional development compared tothe leading industrial powers. Suddenly, in the1850s, threatened by US and British warships,Japan was forced to allow foreign ships (andsailors) to gain refuge and replenishment at(selected) Japanese ports, and to sign ‘unequaltreaties’ (already imposed on China) withWestern powers. The once mighty (Tokyo-based)Tokugawa Shogunate was defenceless to outsidethreats and, perhaps with surprising ease, wasoverturned by a dynamic cadre of samurai whojustified their revolution through control of the(Kyoto-based) emperor, the symbol of nationalunity (Reischauer 1991, pp. 114–122). In 1868,Japan changed the name of the year period to‘Meiji’ (Enlightened Rule) in honour of theemperor who posthumously inherited the namein 1912.

However, this period, subsequently labelledthe Meiji Restoration, was not simply a politicalrevolution. The symbolic restoration of the em-peror justified and channelled a massive nationalcommitment and energy to play catch-up with

6

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

the West and become a global power. Accordingto Reischauer (1991, p. 131), Japan’s transfor-mation from feudalism to a modern nation statein just two decades was an ‘an extraordinary andperhaps unique story’.

Under the slogan

Wakon Yosai

( JapaneseSpirit, Western Technology), the Meiji Restora-tion, established Japan’s signature to the ‘prob-lem of industrial transformation’ (McMillan,1985, p. 10). Japan learned from the West onvirtually all aspects of economy and used thislearning as the basis for industrial (and mili-tary) leadership. Hand picked students, includ-ing girls, were sent around the world to learnscience and technology in disciplines whereverthey were most advanced, while foreign expertsin leading edge industries were paid high sal-aries to work in Japan. Domestically, the Japan-ese government innovated a system of populareducation (including girls in the primary grades)‘free of the aristocratic aura and religious dom-ination of many Western educational systemsof the time’ (Reischauer 1991, p. 127). If thissystem proved vulnerable to indoctrination,Reischauer argues that by the early 1890s Japanhad become more egalitarian than Britain andwas fostering learning as a broad basis for long-run competitive advantage.

The Japanese approach to the problem ofindustrial transformation was rooted in thephilosophy of Frederich List (1922) (see Fallows1995). Thus, investment in transportation andcommunication infrastructure was a priority asthe government sought to provide the condi-tions to allow the realisation of List’s ‘productiveforces’ across the industrial spectrum. Neitherbranch plants nor foreign loans were welcome.Rather, the government strove hard, eventuallysuccessfully, to replace the unequal treaties withtariff barriers to protect ‘infant industries’, andthe foreign experts were engaged only tempor-arily. Whether industry was small scale or largescale, the Japanese sought to ‘reverse engineer’Western technology (Freeman 1988). In thisapproach, defined as ‘innovation mediatedproduction’ by Kenney and Florida (1993), ‘copy-ing’ set the stage for selecting, adapting andimproving technology (and institutions) toJapanese conditions, that in turn provided thebasis for global innovation. In the case of cut-lery, a small-scale industry, metal workers in theremote community of Tsubame, using cutlery

samples provided to them by Tokyo wholesalers,conducted trial and error experiments on apart-time basis (Patchell & Hayter 1992; Hayter& Patchell 1993). In the case of ships, the ‘high-tech’ product of the late 19th century, vital tomilitary and industrial power, the governmentwas directly involved in highly focused, sub-sidised efforts to transfer technological know-how (Howe 1996).

As Howe (1996) notes, during the Tokugawaperiod of seclusion the construction of ocean-going ships was forbidden and Japan did nothave the navigational abilities to cross thePacific. In the 1840s, however, Japan began tostudy Western shipbuilding technology, aninterest accelerated by the arrival of US ‘blackships’ in Tokyo Bay in the 1850s. To master thecomplex, rapidly evolving naval technology,Japan imported foreign ships, established agovernment-controlled shipyard, organised ex-haustive demonstrations of ship performance,hired the best naval architects from aroundthe world, obtained licences, sent workers toforeign shipyards, suggested specifications toenhance capability, and stimulated privatesector involvement initially around the giantMitsubishi ‘zaibatsu’ (or financial conglomerate).The record speaks for itself. In 1867, Japan wasable to muster a navy of nine foreign-built shipswith a combined horsepower of 2,000 hp. By1907, Japan had constructed a naval fleet (andmerchant marine fleet) on a par with US andEuropean technology, although still importingkey components, such as engines. The horse-power was over 1 million. By 1918, Japan hadmastered all aspects of shipbuilding technology,was domestically self sufficient, and a majorexporter.

A key part of the story of Japan’s rise to theforefront of shipbuilding technology is the stim-ulation by the government of the private sector.Thus, in the period, 1883–1906, almost 75 percent of Japan’s warships was imported, andjust over 1 per cent were built in private yards(Howe 1996, p. 289). Over the next 15 years,imports provided only 7 per cent of Japan’s war-ships, the rest being supplied from naval yards(48%) and private yards (45%). The govern-ment had ‘targeted’ shipbuilding as a develop-ment priority, built shipyards that channelledand demonstrated learning processes, under-wrote efforts to learn Western technology, and

FLYING GEESE IN ASIA

7

© 2004 by the Royal Dutch Geographical Society KNAG

gave accreditation to preferred shipyards. Longbefore Japan’s Ministry of International Tradeand Industry (MITI), established in the post-1945 period the Japanese government led bythe Ministry of Finance saw its role as ‘facilita-tor’ and ‘guidance councilor’ for private sectorinitiative ( Johnson 1982).

In fostering industrialisation, the Japanesegovernment supported the domination ofgiant firms over a large population of small andmedium-sized enterprises (SMEs). Nevertheless,Japanese policy contrasted sharply with the West,where conventional economists shared Marx’sview about the inevitable demise of SMEs. More-over, in Japan, SMEs did not simply provide areservoir of cheap labour, as favoured by con-ventional interpretations of the dual model(Patchell 1992). As Fruin (1992) emphasises,SMEs played vital roles in creating specialisedand cooperative social divisions of labour dur-ing Japanese industrialisation, a developmenthe contends was an institutional response to thetechnological gap between Japan and the West.To ‘catch-up’ with more powerful Western firms,Japanese companies had to focus their activitiesmore sharply and mutually share their expertise.

By 1914, Japan’s emergence as a world power,with its own colonies in Asia, was rapidlyenlarged and equally rapidly destroyed duringthe Second World War. Japan’s economy waseffectively de-industrialised. In re-industrialising,Japan’s approach closely parallelled that ofthe Meiji Restoration. Again the emperor wasrestored to help hold together the nation andchannel its energies, only this time the restora-tion depended upon US acumen, especiallythat of General MacArthur, rather than samuraifrom Kyushu. Again, Japan opted for a ‘Listian’model of development based on economicnationalism rather than the ‘Anglo-saxon’ modelof economic liberalism. While the latter favouredpriority on Japan’s low-wage comparative advan-tage in textiles, the former encouraged policyemphasis on the progressive development ofthe main and leading edge technologies inconsumer and producer goods (Okimoto 1989).The creation and ascendancy of MITI reflectedthis choice, albeit not without debate ( Johnson1982). Again, industrialisation was realisedthrough the relentless pursuit of ‘reverse engi-neering’ with Japanese control tightly protectedby tariff barriers and constraints on inward DFI.

In two or three decades, Japan became a globaleconomic giant.

In the electronics sector, Gregory (1986,p. 421) notes that mass merchandisers in theUnited States, and eventually Europe, providedthe major impetus for Japanese firms to launchinto global markets. Thus ‘Sears, Roebuck, J.C.Penny, Montgomery Ward and other leadingchain stores in the United States placed massivecontracts with Japanese makers supplyingdesigns, specifications and quality control . . .Only Sony insisted on selling its products underits own trademark in overseas markets at theoutset’. In the late 1960s mass merchandisersin the US (and Europe) shifted their purchasesto Hong Kong when assemblers trimmed costsbelow that of Japanese manufacturers, usingJapanese components. Hong Kong then becamethe world’s largest producer of transistor radios.Initially, Hong Kong assembled transistor radiosaimed at United Kingdom and other Common-wealth country markets, facilitated by the sys-tem of Imperial Preference. The first transistorradios assembled in Hong Kong, by ChampaignEngineering (later renamed Atlas Electronics)were under subcontractor arrangements withTokyo Tsushin Kogyo KK (later renamed SonyCorporation). ‘Hong Kong entrepreneurs werequick to “reverse engineer” the latest Japaneseradio models and produce near-replicas whichwere sold at prices considerably below those ofJapanese makers. However, rather than attemptto inhibit this process, Japanese radio manufac-turers, also producers of important components,generally rode with what they came to accept asthe natural course of events’ (Gregory 1986,pp. 422–423).

During the 1980s and 1990s, as Japanese DFIproliferated around the world in the wake ofJapanese exports, Japanese firms have becomethe teachers rather than the students. In thisregard, the interpretation of Japanese industri-alisation as a minor variation of ‘regulationtheory’ (Peck & Miyamachi 1994) and notespecially significant in economic geography’s‘cultural turn’ (Sayer 1997, p. 22) misses thepoint. Japanese industrialisation is of globalsignificance as a model of learning and innova-tion (Asanuma 1989; Fruin 1992; Freeman 1987,1988; Kenney & Florida 1993; Patchell 1993a,1993b). There is extensive documentation ofthe distinctive, deeply embedded features of

8

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

Japanese industrialisation. There is particularrecognition of the uniqueness of Japan’s socialdivisions of labour, inter-firm relations (espe-cially the co-development of principles ofcompetition and co-operation), human relationpractices within firms and factories, and theorganisation of research and development (R&D)in relation to manufacturing. If the world is aclassroom, the Japanese have been remarkablydiligent and ultimately imaginative students,transforming lessons elsewhere into distinctJapanese practices. If economic geographersthink geography matters, then the Japanesemodel continues to deserve serious attention.Above all, Japan is the (non-western) model ofindustrial learning, one that has unusualsignificance for Asia.

FLYING GEESE, PRODUCT CYCLES AND DEVELOPING ASIAN HOST COUNTRIES

The flying geese model was originally devel-oped as a metaphor for

domestic

structural trans-formation as Japan evolved from student toteacher of industrialisation based on the ‘longterm’ philosophy of reverse engineering thatenvisaged copying and reconstruction of estab-lished technology from elsewhere as a necessarystep for global innovative leadership. As ametaphor

of domestic sectoral transformationthree characteristics of the flying geese modelare worth noting. First, reference to ‘leadingedge’ sectors does not mean that they weregiven exclusive priority in Japanese policies,public or private. Indeed, Japanese firms havevigorously sought to maintain the viability ofmature industries in Japan, even if this attitudehas become harder to sustain in recent yearsbecause of ‘hollowing out’ (Edgington 1997,1999). Second, the transformations achieved byJapan during the Meiji period and after 1945were not automatic or certain outcomes. Rather,as revealed by the post-1945 policy debate overwhether development priority should exploitestablished low-cost industries or progressivelypromote more sophisticated and value-addedproduction, there was much controversy in theway that public policy towards manufacturingevolved ( Johnson 1982).

Third, in the original model, the flying geeseare domestic, as reverse engineering relegatesDFI from abroad to a demonstration or part-

nership role, and then only on a temporarybasis. Even when Japan enlisted the help ofpowerful foreign MNCs, for example, Germanchemical firms in the 1930s or European autofirms in the 1950s, the arrangements took theform of joint ventures that were temporary,or at least terminated after a few years. In theelectronics industry, Japanese firms absorbedoverseas technology through licences and OEM(original equipment manufacturing) arrange-ments when exporting (Ozawa 1974; Gregory1986). In Japanese thinking (comparable tomany Western countries), at least in the earlystages of development, industrial leadershipand foreign control were incompatible.

When the flying geese metaphor was itselftransformed as a framework for Japanese DFI,Japan’s history of technological independenceand self-interest implied the suspension of thatbelief for other countries. Thus, in the transla-tion of the flying geese model to an Asiancontext Japanese DFI, rather than indigenousfirms, have been anticipated to play a pivotalrole in the dynamic shift of industries from onecountry to another (Chen 1989; Yamazawa1990). As Bernard and Ravenhill (1995) note,in the Asian context the flying geese model hasbecome closely associated with the productcycle model of international investment, whichin its original formation predicts the relocationof ‘mature’ products to low wage regions(Vernon 1966). The idea that the flying geese(here the Japanese MNCs investing overseas)can change factor endowments in (Asian) hostcountries implies that technological capabilityis transferred back along the product cyclemodel. That is, the flying geese model predictsa staged sequence of expansion for any industry,beginning with mature products, from Japan tothe NIEs (newly industrialising economies),followed by ASEAN, China, Vietnam and India.Indeed, through the transfer of know-how viaJapanese FDI, the model raises the possibilitythat the technology gap between Japan and Asiamight be narrowed (but not closed).

In political economy terms, the flying geeseframework predicts (‘promises’) that host coun-tries will achieve progressively improving levelsof technological capability by moving backalong the product life cycle and is predicated ona changing bargain between Japanese MNCs overtime. An assessment of the dynamics of this

FLYING GEESE IN ASIA

9

© 2004 by the Royal Dutch Geographical Society KNAG

bargain and the promise of technological catch-up through DFI can be illustrated by the ‘reverseproduct life-cycle’ model shown in Figure 1,based on Hobday’s (1995b) studies of ‘latecomercountry’ development in Asia. It provides asimple, stylised framework for assessing thenature, direction and determinants of the im-pact of Japanese DFI and learning on Asiancountries. Its purpose is to locate the case-studymaterial presented in sections 4 and 5, and togenerate further questions for analysis.

As a template, the model suggests that in the‘mature stage’ (Stage I in Figure 1), JapaneseMNCs are looking for cheap labour locationsoverseas, while developing (Asian) host econ-omies are themselves looking for investmentand exports. In this initial stage the establishment

of mass production and assembly operationsrequires workers to learn simple skills and ‘factoryculture’ under tight supervisory control. WhileMNCs have a bargaining advantage rooted inlocation options, the motivations of these twomain parties are generally congruent.

In the innovation, or fast growth stage (StageII in Figure 1), production depends upon agreater level of skilled workers with ‘enterprisespecific skills’ (ESS) and local suppliers thatprovide ‘relation specific skills’ (RSS). For Kiokeand Inoke (1990), ESSs are created when workersadd to productivity improvements throughtheir intellectual capabilities that are developedthrough ‘depth’ and ‘width’ of experience asthey learn to solve both routine problem andmore significant changes that occur on the shop

Figure 1. The reverse product cycle model and the transfer of technological capability.

10

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

floor (see Patchell & Hayter 1995). For manyobservers, supply relations are at the heart ofthe competitive advantage of Japanese productionsystems (Asanuma 1989; Patchell 1993a). Con-sequently, the RSS defines the technologicalbonding between core firms and their suppliers asthey organise stable exchanges of technologicalknow-how in a way that promotes innovation in amutually beneficial way. In this stage, there is stillstrong overlap in the motivations of ( Japanese)MNCs and (Asian) hosts, although the formeris likely to face increasing concerns in donoreconomies ( Japan) over the ‘export of jobs’. Thedevelopment of worker skills and supply systemsin host economies is also more complicated.

In the more advanced R&D stage (Stage IIIin Figure 1), the transfer of expertise to hosteconomies is highly problematical. In this stage,the need for a highly educated workforce andsophisticated external economies within hostcountries has to be related to the threats suchtransfers pose to the core competitive advan-tages of MNCs. Thus, the motivations of MNCsand host economies in transferring technologyare in direct conflict to some extent, and anysuch transfers are likely to be carefully con-trolled, if not entirely prohibited. That is, itsmovement back along the product cycle becomesmore difficult as local skills requirementsincrease for both individual workers and supplysystems (i.e. the lessons become harder), whilethe motivations between MNC and host coun-try (regarding the transfer of technology) areincreasingly in conflict.

The reverse product cycle model and itsimplications for technology transfer betweenMNCs and host economies can be further elab-orated by reference to Ernst’s (1997) indicatorsof the ways in which know-how is potentiallytransferred from Japanese firms’ headquartersto their Asian subsidiaries. Thus Ernst’s (five)indicators are: increases in value-added produc-tion (from low to high); the training of localpersonnel (simple or comprehensive); the local-isation of management (degree of localisation);the localisation of innovation capacity – involv-ing design and development capacity (presentor absent); and R&D capability (present orabsent). Adding value, training, product designand R&D strongly suggest contributions of onekind or another to the ESS while investment inlocal management also implies greater likeli-

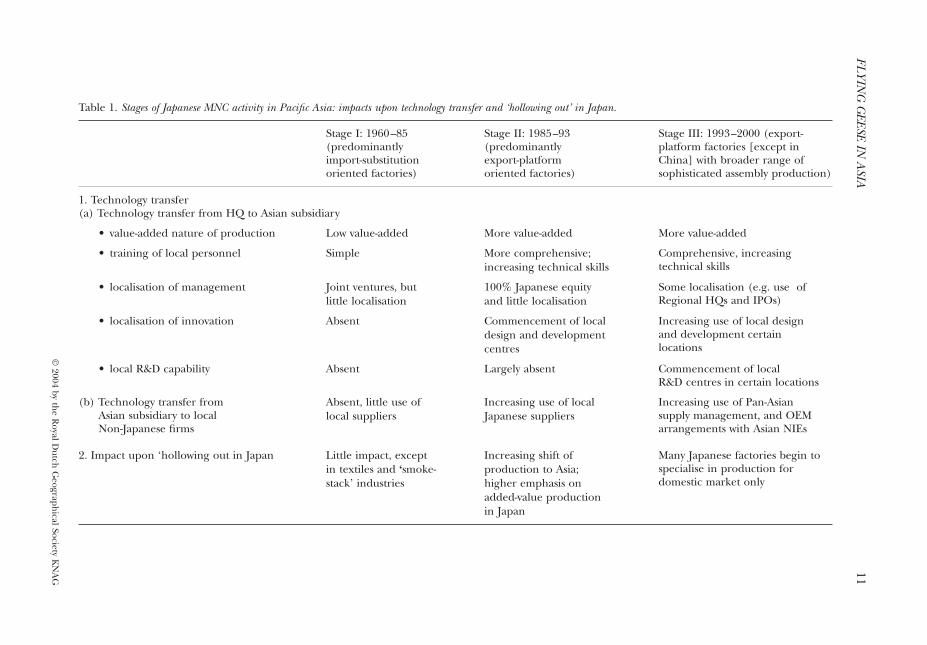

hood of subsidiaries undertaking initiativesand solving problems. Ernst’s indicators donot reflect the RSS although he admits thesignificance of non-Japanese subcontractors forlocal development. The ESS and RSS, however,are difficult to measure and Ernst’s indicatorshelp crudely identify a broad-scale chronologyof Japanese DFI in Asia in relation to tech-nology transfer (Table 1). To Ernst’s indicators wehave added an indicator, namely the technologytransfer from Japanese MNCs’ subsidiaries inAsia to local (non-Japanese) supply firms. Wealso consider the impact of the ‘hollowing out’of industry through DFI on Japan.

Three broad stages in the changing bargainbetween Japanese DFI and Asian host countriescan be identified. From the 1960s to about 1984,notwithstanding a few export-oriented invest-ments, Japanese DFI in Asia emphasised invest-ments in import substitution factories orientedtowards local markets, especially Southeast coun-tries, such as South Korea and Taiwan. Malaysia,Singapore and Hong Kong also became import-ant destinations (Edgington 1993). The

endaka

(yen appreciation) of 1985 stimulated a secondperiod of Japanese DFI in Asia, especially South-east countries such as Thailand, Indonesia andthe Philippines, to serve global export markets. Amore volatile period (Stage II in Table 1) com-menced in 1993 after a second major

endaka

, andwas greatly complicated by the Asian currencycrisis of 1997/98 that triggered an intensiverethinking by Japanese MNCs of their operationsthroughout Asia (Edgington & Hayter 2001a).This crisis also marked a time when the tech-nology transfer implications of DFI becameproblematical because of the ‘hollowing out’ ofindustry in Japan (Edgington 1997). In thisperiod, China has become the overwhelminglydominant host country, while other very lowwage countries, such as Vietnam and India, alsobegan to receive some investments.

The remainder of this paper reveals howthe stylised learning processes portrayed inFigure 1 and Table 1 have varied considerablyamong Asian host countries.

JAPANESE FLYING GEESE IN ASIA I: NORTHEAST ASIAN CASE STUDIES

Analysis of Japanese electronics DFI in the PacificAsia region by Edgington and Hayter (2000)

FLYIN

G G

EESE IN A

SIA

11

© 2004 by th

e Royal D

utch G

eographical Society K

NA

G

Table 1.

Stages of Japanese MNC activity in Pacific Asia: impacts upon technology transfer and ‘hollowing out’ in Japan.

Stage I: 1960–85 (predominantly import-substitution oriented factories)

Stage II: 1985–93 (predominantly export-platform oriented factories)

Stage III: 1993–2000 (export-platform factories [except in China] with broader range of sophisticated assembly production)

1. Technology transfer(a) Technology transfer from HQ to Asian subsidiary

• value-added nature of production Low value-added More value-added More value-added

• training of local personnel Simple More comprehensive;

increasing technical skillsComprehensive, increasing technical skills

• localisation of management Joint ventures, but little localisation

100% Japanese equity and little localisation

Some localisation (e.g. use of Regional HQs and IPOs)

• localisation of innovation Absent Commencement of local design and development centres

Increasing use of local design and development certain locations

• local R&D capability Absent Largely absent Commencement of local R&D centres in certain locations

(b) Technology transfer from Asian subsidiary to local Non-Japanese firms

Absent, little use of local suppliers

Increasing use of local Japanese suppliers

Increasing use of Pan-Asian supply management, and OEM

arrangements with Asian NIEs

2. Impact upon ‘hollowing out in Japan Little impact, except in textiles and

‘

smoke-stack’ industries

Increasing shift of production to Asia; higher emphasis on added-value production in Japan

Many Japanese factories begin to specialise in production for domestic market only

12

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

showed that northeast Asian countries com-prised the very first wave of Japanese flyinggeese (here the major electronics MNCs) dur-ing the 1960s. Japanese firms, such as Sharp,Sanyo and Hitachi, arrived in Hong Kong,Taiwan and South Korea searching for cheaplabour and access to local markets. For theseNortheast Asian NIES, Hobday’s (1994a, 1995a)accounts indicate that Japanese firms providedall the forms of industrial learning presentedearlier in Table 1 for period I. During the start-up phase (Stage I of the reverse product cyclemodel in Figure 1) Japanese firms acted asexemplars for local firms and helped initiatethe very first electronics’ ventures and exportindustries. As part of joint venture arrange-ments, they began training local engineers andtechnicians, transferring valuable foreign tech-nical and management skills. However, ingeneral, local firms in these countries retainedcontrol and provided the major contributions tohost country growth, investments and employ-ment in this sector. What Hobday (1995b) calls‘latecomer’ firms imitated Japan’s own histor-ical experience, as outlined earlier in the paper.They graduated from their joint ventures withJapanese MNCs by assimilating part of thelatter’s technological know-how, and gainingaccess to export markets. This was done by strat-egies such as licensing and OEM arrangementsas local firms in Northeast Asia upgraded theirelectronics capabilities and narrowed (but nottruly catching-up with) the technological gapbetween themselves and the Japanese elec-tronic sector leaders. By the end of the 1990s,large-scale South Korean firms (the

chaebol

)achieved world class technological capabilitiesin semiconductor memories as well as colourTVs, camcorders and CD players. In Taiwan,small and medium-sized enterprises emerged tobecome the largest exporters of printed circuitboards for personal computers (PCs) and majorsuppliers of colour monitors, finished PCs, faxmachines and calculators (Hobday 1995b).Hong Kong’s development was different. Whileit achieved significant export success in faxmachines, digital watches, cordless telephonesand workstations, it lost much of its industrialcapacity in the 1980s as local firms relocated toChina and as MNC factories left the territory(Berger & Lester 1997). Hong Kong will not beexamined further here.

South Korea –

The example of how SamsungElectronics Corporation (SEC), South Korea’slargest electronic producer, entered the sectorunder joint venture and OEM arrangementswith Japanese firms is an illustrative case (seeHobday 1995a, 1997; Kim 2000). The founderof Samsung, Lee Byung Chall, was educated inJapan during the Korean colonial period (1910–1945) and established fortuitous contacts withJapanese firms after 1945. Kim (2000) notesthat Samsung had considered cooperationwith American firms, but due to the languagedifficulties inherent in using American tech-nology it established ties with Japan’s Sanyo andNEC in a bargain tied to their entry into theSouth Korean market. Table 2 shows the jointventure arrangements between Samsung (andSouth Korean firms Goldstar and Anam) andJapanese electronics firms in the 1960s and early1970s. Hobday (1995a) observes that Japanesecompanies in this early period were more likelyto use joint ventures than US firms in Asia,both to gain entry into local markets and tocontract manufacturers for overseas exports. USfirms, however, created wholly owned branchplants in South Korea for low cost semiconduc-tor exports back to the US market. Moreover,these US firms imparted little technologicalknow-how as they imported most of their rawmaterials and components. By contrast, Sam-sung sent 106 employees to Sanyo and NEC fortraining in the manufacture of radios, colourtelevisions and simple electronic components.Under its joint ventures with Sanyo, NEC andSumitomo, SEC was able to absorb foreign tech-nology in a variety of consumer goods and com-ponents. Importantly for the purposes of thispaper’s argument, all of these joint ventureswere under Samsung’s management control,allowing it to develop eventually as a verticallyintegrated assembler and parts manufacturerof a wide array of electronic products (radios,television sets, telecommunications and semi-conductors).

In the 1970s the South Korean governmentintervened to restrict further DFI per se by with-drawing lucrative tax benefits for Japanese (andUS) investors while allowing tie-ups betweendomestic and foreign firms. Japanese (andmost) MNCs subsequently retreated from theSouth Korean market due both to governmentpolicy as well as rising wage costs. Indeed, until

FLYING GEESE IN ASIA

13

© 2004 by the Royal Dutch Geographical Society KNAG

after the 1997 Asian financial crisis, SouthKorea remained virtually closed to DFI in elec-tronics. Japanese MNCs, however, continued tomaintain important links with South Koreanelectronics companies. Licensing arrangementsin particular persisted, as these became the onlyway for Japanese MNCs to access South Koreanmarkets and an important means by whichSouth Korean firms obtained foreign tech-nology. Japanese MNCs appear to have dominatedthese licensing arrangements. Moreover, aswages rose in Japan, Samsung, and other SouthKorean

chaebol

such as Goldstar, offered alter-native locations for large-scale, low-cost stand-ardised goods under OEM arrangements. Itwas not straightforward for Samsung and otherlocal firms to extend their know-how beyondsimple assembly under OEM and licensingarrangements with Japanese (and also US) elec-tronics companies. Indeed, Hobday (1995a,p. 67) comments that ‘OEM was a harsh industrialtraining school for South Korean firms wholearned their skills from Japanese and Amer-ican MNCs. Invariably they had to provide thehighest quality at the lowest prices’. Gradually,local firms grew in competence, and OEMbuyers from Japan (and elsewhere) providedSouth Korean firms with product designs, stafftraining in quality controls, and engineeringsupport, though not through DFI directly. Thisstrategy allowed Samsung, and other electronicmajors such as Goldstar and Daewoo Electron-ics, to concentrate on increasing their manufac-

turing capabilities through intensive trainingof employees, particularly shop-level technicians,mirroring Japanese OEM relations with USfirms in previous decades (Kim 2000).

During the 1980s, South Korean firms gainedrudimentary R&D expertise to reverse engineerproducts and learn how to impose processes,equivalent to Stage II of the reverse productcycle (Figure 1). However, once South Koreanfirms’ learning reached advanced levels thenfurther access to Japanese technology dependedupon expensive licensing agreements andpurchases of key components. Hobday (1995b,p. 63) notes that the South Korean integratedcircuit industry imported nearly 75 per centof all materials and equipment needed forproduction during the 1980s and that royaltiesoften comprised 10 per cent of corporate sales.Goldstar, for instance, licensed 4 and 16 mega-bit DRAMS from Hitachi. Korean firms alsoremained largely dependent upon Japanese (aswell as US) firms for key components, capitaland materials through their OEM and licencingagreements.

During the next period (following the

endaka

in 1985) Samsung and other South Koreanfirms took important steps to move closer to thetechnology frontier (Stage III in Figure 1) bysetting up their own research institutes, both athome and overseas, including Silicon Valley inthe United States. Decades previously, to com-pensate for private sector deficiencies, the gov-ernment had funded applied R&D initiatives.

Table 2. Early joint ventures and technical assistance between South Korean firms and Japanese electronic companies.

Year Technology activity and firms

1961 and 1962 Matsushita Electronic Industries and Sanyo Corporation provide technical assistance to Samsung and Goldstar to set up transistor radio factories

Late 1960s Toshiba Corporation formed a joint venture and two major technical agreements to assemble consumer goods, cathode ray tubes (CTRs) and parts for CTRs, in South Korea

1969 Samsung Electronic Engineering began assembly of black and white TVs following technology transfer agreements with Sanyo Corporation

1969 Joint venture (Samsung-Sanyo) formed to manufacture electronic parts1970 NEC formed two joint ventures, with Goldstar Electronic and Samsung.

Samsung-NEC produced electronic components for CRTs1973 Samsung Electronic Parts, a joint venture, was established in 1973 with Sanyo1973 Anam Industrial of South Korea formed a jointly-owned venture with

Matsushita Electronic Industries to produce colour TVs

Source : adapted from Hobday (1995a, p. 66).

14

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

Thus the Korea Institute for Science and Tech-nology (KIST) was set up in 1966 to help absorband adapt foreign technologies. The Ministryof Science and Technology also invested intraining and vocational programmes (Hobday1995b). By around 1990, private sector R&Dhad become significant in South Korea andallowed firms to enter joint-technology devel-opments with Japanese companies in a broadrange of products, such as telecommunications,computers and semiconductors (Hobday 1995a,p. 70). In addition, South Korean firms acquiredoverseas technology-intensive firms (such asSamsung’s 51 per cent control of Japan’s hi-fiaudio maker LUX in 1994) and followed Japan-ese companies into Southeast Asia. Indeed,Samsung’s component producing subsidiariesin Thailand and Malaysia supplied more than80 per cent of their output to Japanese com-panies during the last decade (Kim 2000). Inthe 1990s, Samsung also established joint ven-tures with Chinese partners as a prerequisite toits market entry into the PRC. According to Kim(2000, p. 162): ‘Its joint ventures [in China] arethus the mirror of those it established in Koreain the 1970s with Japanese partners, tradingproduction know-how for market success – onlynow the know-how is Samsung’s’. Even if theyremain more heavily dependent upon foreignsources of technology and market channelsthan equivalent Japanese companies (Hobday1995a, 1997), South Korean firms such as Sam-sung have moved a considerable distance backalong the product life cycle. Taiwanese firmshave enjoyed similar, perhaps greater success.

Taiwan –

As with South Korea, aided by priorcolonial links (1895–1945), Japanese MNCs andtheir investments were important in the initialdevelopment of an electronics industry in Tai-wan, beginning in 1963 when Sanyo formed ajoint venture with a Taiwanese importer to servethe domestic market. This company was one ofthe first in Taiwan to produce white goods suchas air conditioning products, audio electronics,and then later on TV sets and VCRs and in 1970it began exporting to the United States andother global markets (Hobday 1995a, p. 104).Hitachi, Matsushita, Mitsubishi, Sharp andToshiba were among other Japanese MNCs thatinvested in Taiwan’s electronics sector in the1960s, many as part of joint ventures with local

companies. Japanese MNCs were also active inlicencing technology to Taiwanese firms. Intotal, Dodwell Marketing Consultants (1974)recorded 14 cases of 100 per cent Japaneseequity holding, 36 joint ventures and 38 casesof technology licensing. A selection of Japanesejoint venture and licensing arrangements in Tai-wan as of 1974 is shown in Table 3.

In addition to the Japanese MNCs, Philips ofHolland and several US-based MNCs, includingRCA, became significant players in Taiwan’selectronics sector in this early period, in Philips’case since 1961. As in South Korea, Japanesefirms initially focused on Taiwan’s domesticmarket and then began to export whereas theUnited States exported at start-up and subse-quently also served local markets. The UnitedStates also had a stronger preference for 100 percent equity control of their subsidiaries in Tai-wan while Japanese MNCs were more willingto enter into joint ventures, if not to the samedegree as they did in South Korea, possiblybecause of the smaller size of Taiwanese firms(Ernst 2000a, 2000b). In Taiwan, in contrast toSouth Korea, government policy ensured thatvirtually equal treatment was granted to domes-tic and Japanese MNCs. Indeed, in Taiwan therewas considerable competition among firmsand some MNCs, notably RCA, were casualties.Yet, Taiwanese firms, small and large, were not‘crowded out’, an effect that occurred in South-east Asian countries such as Singapore or Malay-sia (see Lim & Pang 1991). Rather, the oppositeoccurred. As Hobday (1995a, p. 112) notes:‘Japanese corporations acted as pacing horsesfor (Taiwanese) firms. They stimulated compe-tition in consumer electronics and white goods,and helped to create a thriving network oflocal suppliers of parts and services’. Indeed, heclaims that Taiwanese entrepreneurs ‘eventu-ally [made] the TNCs dependent on theirmanufacturing skills and their highly productiveengineering talent. Hundreds of local com-panies learned to innovate by clustering aroundthe TNCs’ (Hobday 1995a, p. 109). Further,out of these ‘hundreds’ of small firms, larger,innovative ‘latecomer firms’, such as Acer andTatung, emerged in Taiwan, to help solidifydense domestic inter-firm networks within Tai-wan’s electronic industry (Henderson 1997).

As a result of rising wages, Sanyo and otherJapanese MNCs ceased to expand in Taiwan

FLYING GEESE IN ASIA

15

© 2004 by the Royal Dutch Geographical Society KNAG

Table 3.

Selected operations of Japanese electronics firms in Taiwan, 1974.

Japanese company Taiwanese partner Operations (date ‘Established’/period of contract)

A. Direct investments ( Japanese equity %)Hitachi (61.5%) Taiwan Hitachi Manufacturing of air conditioners for

local Market (1964)Hitachi (20.0%) Yung Tay Engineering Manufacture of lifts and escalators for

local Market (1968)Matsushita Electric Industrial (60.0%)

Taimatsu Industrial Assembly of radios and record players parts from Matsushita (1966)

Mitsubishi Electric (22.5%) China Electric Manufacture of fluorescent lamps (technical assistance from Mitsubishi Electric) (1962)

Mitsubishi Electric (40%) China Ryoden Installation of lifts (1968)Mitsubishi Electric (27.8%) Shihlin Electric and

EngineeringManufacturing of transformers and other electronic products (1968)

Oki Electric Industry (49.0%) Fareastern Electric Industry

Manufacturing of telephone sets and switching systems (1958)

Sharp (11.0%) Sanpo Corporation Manufacturing of household appliances with Sharp’s brand for local market (1971)

Toshiba (12.5%) Tatung Manufacturing of electric equipment e.g. fans and refrigerators (1961)

B. Technology licencing arrangementsFuji Electric Chan Shing Electric Technology for electronic

transformers (1970)Hitachi New Asia Electric Technology for fluorescent lights

(1970–75)Hitachi Prince Electronic Technology for colour TV set

transistors (1970–75)Hitachi Taigene Electric Machinery Technology for automobile

engines (1970)Mitsubishi Electric Shihlin Electric and

EngineeringTechnology for transformers and other electronic parts (1962–74)

Mitsubishi Electric Chung Hsin Electric and Machinery

Technology for colour TV sets (1970–80)

Sharp Corporation Sanpo Corporation Technical assistance for refrigerator factory (1968–78)

Toshiba Tatung Use of Toshiba’s patent on wattmeter (1954)

Toshiba Tatung Use of Toshiba’s patent on magnets (1964–74)

Toshiba Tatung Use of Toshiba’s patent on electric refrigerators (1964–74)

Toshiba Tatung Use of Toshiba’s patent on electric Motors (1969–74)

Toshiba Tatung Use of Toshiba’s patent on colour TV sets (1969–79)

Source

: adapted from Dodwell Marketing Consultants (1974).

16

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

itself after the late-1970s. Still, Taiwanese firmscontinued to develop, free from dependenceon Japanese DFI, by joining in internationalsubcontracting arrangements (OEMs), mainlywith US retail firms, but also with the giantJapanese

sogo shosha

(trading companies). Tech-nology was also acquired by Taiwanese firmsfollowing the original Japanese template, that isby copying, reverse engineering, foreign licenc-ing, rigorous local training combined with over-seas education. Japanese MNCs, therefore, hada significant impact on the development ofconsumer electronics in Taiwan during the 1970s,especially by offering tacit knowledge embodiedin human capital and the start of new firms.Taiwanese firms such as Tatung sent engineersto Japan for training and became a source oftechnology and entrepreneurs in Taiwan, inpart attracted by government incentives and thelure of high rewards.

In the 1970s Taiwanese electronics exportswere confined largely to parts and components.But these evolved gradually into more added-value products and Stage II (Figure 1) oper-ations, such as customisation, product design,and production technology (Ernst, 2000b). Therise of the Japanese yen in 1985 further in-creased Japanese MNC purchases of Taiwanese-made keyboards, TV monitors, printed circuitboards and printers, even as Japanese electronicsfirms shifted their own (post-

endaka

) assemblyplants into Southeast Asian countries. A fewcompanies, such as Acer and Tatung, had alsoinvested in R&D by the end of the 1990s whilethe government’s main technology institute,The Industrial and Technological ResearchInstitute (ITRI), had spun-off successful export-ing firms (Wade 1990). Admittedly, Ernst(2000b) and Hobday (1995a, 1997) noted diffi-culties for Taiwanese firms wishing to move intothe technology intensive Stage III (Figure 1),mainly because of a lack of capital for R&D.

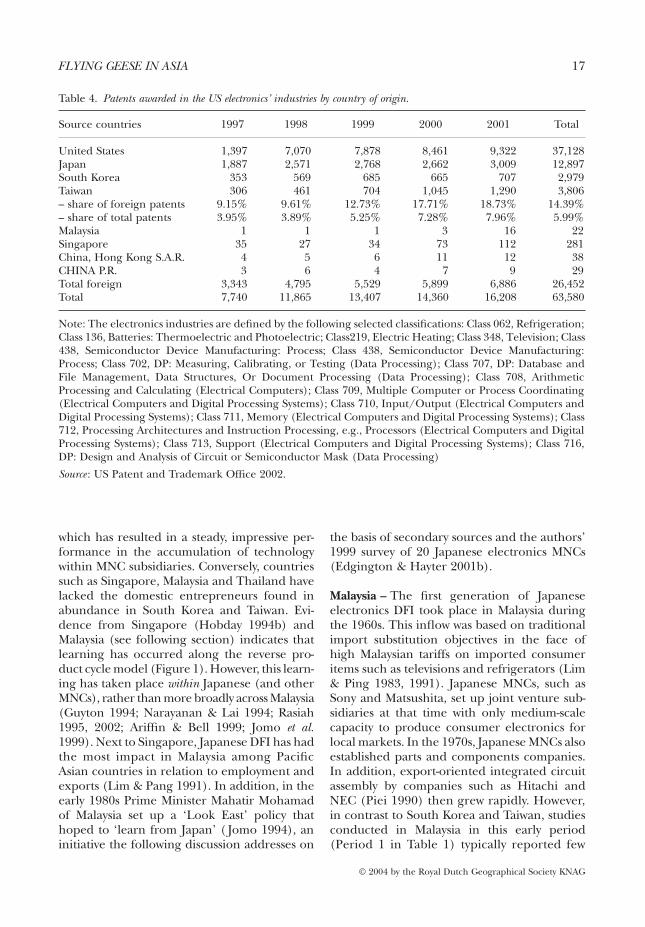

Yet, the reverse product cycle model expectsincreased difficulty as firms seek more sophist-icated technological capability and notwith-standing such difficulties Taiwanese firms (andSouth Korean firms) have moved substantiallydown this road. A crude indicator of this move-ment is provided by US patent data. Thus, withrespect to

all

patents granted by the UnitedStates, in 1988 Taiwanese inventors accountedfor just 0.59 per cent in 1988 but this share has

steadily grown reaching 3.23 per cent in 2001.For the same period, South Korea’s share grewfrom 0.12 per cent to 2.13 per cent (Figures cal-culated from US Patent and Trademark Office2002). Specifically with respect to electronicgoods, Taiwan’s share of US patents increasedfrom 3.95 per cent in 1997 to 7.96 per cent in2001 while South Korea’s share remainedsteady (4.56 per cent and 4.36 per cent) in thesame period (Table 4).

Indeed, in 2001 Taiwan accounted for18.73 per cent of the foreign patents in electronicsproducts patented in the US. Korea’s shareamounts 10.23 per cent and, on this basis, bothcountries, but especially Taiwan, can claim to beglobal contributors to innovation in electronics.Ernst (2001), using patent data for the early1990s, has noted that the increasingly superiorpatenting record of Taiwanese over SouthKorean firms relates to excessive corporate con-centration, specifically domination of just four

chaebol

firms in South Korea and problems withtheir innovation management. He notes: ‘theorganization of innovation

within

these firmsfollows an outdated centralized R&D model, incontrast to the progressive decentralization ofR&D typical today for Japanese, US and Euro-pean firms’ (Ernst 2001, p. 151). Interestingly,Taiwan’s insistence on a strong role for thesocial division of labour echoes the Japanesedomestic model of industrialisation.

Malaysia, meanwhile, has remained a virtualnon-player in US patent activity.

JAPANESE FLYING GEESE IN ASIA II: SOUTHEAST ASIA

As with South Korea and Taiwan, SoutheastAsia’s electronics industry has been amongthe largest overall contributor to export growthover the past 15 years (Hobday 1995a, p. 20)and Japanese MNCs have been attracted to theregion’s lower labour costs and markets (Lim& Pang 1991; Ernst 2000b). However, unlikeNortheast Asia, local firms have so far made fewcontributions to the electronics industry. Asnoted by Hobday (2001, p. 23), Malaysia andThailand in particular present a radical contrastto both South Korea and Taiwan. Together withSingapore, they have followed a markedly suc-cessful strategy of attracting MNCs into export-led consumer and industrial electronics sectors

FLYING GEESE IN ASIA

17

© 2004 by the Royal Dutch Geographical Society KNAG

which has resulted in a steady, impressive per-formance in the accumulation of technologywithin MNC subsidiaries. Conversely, countriessuch as Singapore, Malaysia and Thailand havelacked the domestic entrepreneurs found inabundance in South Korea and Taiwan. Evi-dence from Singapore (Hobday 1994b) andMalaysia (see following section) indicates thatlearning has occurred along the reverse pro-duct cycle model (Figure 1). However, this learn-ing has taken place

within

Japanese (and otherMNCs), rather than more broadly across Malaysia(Guyton 1994; Narayanan & Lai 1994; Rasiah1995, 2002; Ariffin & Bell 1999; Jomo

et al.

1999). Next to Singapore, Japanese DFI has hadthe most impact in Malaysia among PacificAsian countries in relation to employment andexports (Lim & Pang 1991). In addition, in theearly 1980s Prime Minister Mahatir Mohamadof Malaysia set up a ‘Look East’ policy thathoped to ‘learn from Japan’ ( Jomo 1994), aninitiative the following discussion addresses on

the basis of secondary sources and the authors’1999 survey of 20 Japanese electronics MNCs(Edgington & Hayter 2001b).

Malaysia –

The first generation of Japaneseelectronics DFI took place in Malaysia duringthe 1960s. This inflow was based on traditionalimport substitution objectives in the face ofhigh Malaysian tariffs on imported consumeritems such as televisions and refrigerators (Lim& Ping 1983, 1991). Japanese MNCs, such asSony and Matsushita, set up joint venture sub-sidiaries at that time with only medium-scalecapacity to produce consumer electronics forlocal markets. In the 1970s, Japanese MNCs alsoestablished parts and components companies.In addition, export-oriented integrated circuitassembly by companies such as Hitachi andNEC (Piei 1990) then grew rapidly. However,in contrast to South Korea and Taiwan, studiesconducted in Malaysia in this early period(Period 1 in Table 1) typically reported few

Table 4. Patents awarded in the US electronics’ industries by country of origin.

Source countries 1997 1998 1999 2000 2001 Total

United States 1,397 7,070 7,878 8,461 9,322 37,128Japan 1,887 2,571 2,768 2,662 3,009 12,897South Korea 353 569 685 665 707 2,979Taiwan 306 461 704 1,045 1,290 3,806– share of foreign patents 9.15% 9.61% 12.73% 17.71% 18.73% 14.39%– share of total patents 3.95% 3.89% 5.25% 7.28% 7.96% 5.99%Malaysia 1 1 1 3 16 22Singapore 35 27 34 73 112 281China, Hong Kong S.A.R. 4 5 6 11 12 38CHINA P.R. 3 6 4 7 9 29Total foreign 3,343 4,795 5,529 5,899 6,886 26,452Total 7,740 11,865 13,407 14,360 16,208 63,580

Note: The electronics industries are defined by the following selected classifications: Class 062, Refrigeration;Class 136, Batteries: Thermoelectric and Photoelectric; Class219, Electric Heating; Class 348, Television; Class438, Semiconductor Device Manufacturing: Process; Class 438, Semiconductor Device Manufacturing:Process; Class 702, DP: Measuring, Calibrating, or Testing (Data Processing); Class 707, DP: Database andFile Management, Data Structures, Or Document Processing (Data Processing); Class 708, ArithmeticProcessing and Calculating (Electrical Computers); Class 709, Multiple Computer or Process Coordinating(Electrical Computers and Digital Processing Systems); Class 710, Input/Output (Electrical Computers andDigital Processing Systems); Class 711, Memory (Electrical Computers and Digital Processing Systems); Class712, Processing Architectures and Instruction Processing, e.g., Processors (Electrical Computers and DigitalProcessing Systems); Class 713, Support (Electrical Computers and Digital Processing Systems); Class 716,DP: Design and Analysis of Circuit or Semiconductor Mask (Data Processing)

Source : US Patent and Trademark Office 2002.

18

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

linkages with local subcontractors, few examplesof local design and development activities, andlimited promotion and autonomy for Malaystaff or engineers (Fong 1990; Onn 1990; Aoki1992). Joint venture partners were typically ofthe ‘ali baba’ kind, a cynical reference to Malay-sian ‘sleeping partners’ in politically arrangedjoint operations who showed no interest inunlocking the secrets of Japanese technologythrough reverse engineering. Despite attemptsby the Malaysian government to bargain forbetter joint venture deals, head offices in Japanused and controlled their Malaysian joint ven-tures as branch plants (Piei 1990). The smallscale of the local market, together with the lackof suitable supply companies in Malaysia alsoresulted in minimal development of Japaneseassembly factories in this early period (Piei1990; Anazawa 1994).

Following the rise of the yen in 1985 a ‘newwave’ of large-scale assembly production tookplace aimed at overseas exports markets, espe-cially involving colour television and video cas-sette recorder (VCR) production. These occurredin the states of Penang, Selangor (the KlangValley) and Johor Bahru (Ikuta 1997; Edgington& Hayter 2000). At the same time, changes inMalaysian investment promotion attracted fur-ther inward DFI, creating a ‘bandwagon’ effectamong Japan’s electronic companies (Anazawa1994). By 1987, due mainly to Japanese (andUS) assembly plants, Malaysia had become oneof the world’s largest exporters of semiconduc-tors and third largest producer of VCRs afterJapan and the United States. The local factoriesof Matsushita Electronics Industries Corpora-tion alone were estimated in the early 1990s toaccount for around four per cent of Malaysia’sGDP (

The Economist

1993).During the late 1980s and early 1990s, with-

out a pool of appropriate indigenous firms,Japanese small- and medium-scale suppliersincreased their DFI into Malaysia, aiming tomanufacture components (e.g. hi-fi speakersand motors) for local assemblers as well as forexport. Moreover, a general move to higherlevels of investment and sophistication in theindustry led to increased levels of localisation interms of design engineering capacity, but strictlywithin Japanese-controlled assembly firms.For instance, the Matsushita Air-conditioningGroup (MACG) in Malaysia made much progress

in localising its activities. From its initialset-up as a production base for productsdesigned in Japan, MACG used its facilities asa base for local product design development ofair conditioners exported to the United States,China and Japan (Craig 1997). During the sametime, the Malaysian government under its SixthMalaysia Plan (1991–95) began to follow thepolicies of nearby Singapore and encouragedMNCs to shift their operations from labour-intensive DFI to more technology-intensiveindustries. Eventually, Japanese MNCs startedto commit themselves to the higher value-addedproduction that the Malaysian governmentsought. By way of illustration, Fuji Electric makescomputer disk substrates for the hard disk driveindustry and Sharp Corporation is assemblingsophisticated consumer products such ascamcorders. Certain companies, such as Hitachiand Matsushita Electronic Industries, haveadded R&D centres focusing on product designadaptations for Asian markets. However, withrespect to the localisation of management orsuppliers there has been little progression. Thus,at the end of the 1990s, component inputstended to involve either

keiretsu

(in-house) linkswith a new generation of Japanese parts supplycompanies, or the local operations of SouthKorean and Taiwanese MNCs, rather than localMalaysian firms (authors’ interviews, 1999;Guyton 1995; Capanenelli 1998; Linden 2000).

From the early 1990s, however, some indi-genous Malaysian components’ makers beganto respond generally to the growing number ofJapanese assembly investments, especially inthe electronic sector (Aoki 1992). A more recentsurvey of local procurement behaviour byJapanese firms (Ling & Young 1997) suggestedthat critical changes were made following the‘second

endaka

’ of 1993. These involved thegreater use of non-Japanese local firms whospecialised in a range of generic parts, such asresistors, diodes, capacitors, transformers, powersupplies, coils and filters and loudspeakers.In part, this development was due to furthercost cutting by Japanese firms, but in part itis explained by the introduction of a moreaggressive ‘vendor-development program’ during1993 by the Malaysian government in order topromote Malay small and medium enterprises.Buyer firms in government-approved schemeswere eligible for tax breaks in return for local

FLYING GEESE IN ASIA

19

© 2004 by the Royal Dutch Geographical Society KNAG

procurement. The vendors were often SMEsregistered with Malaysia’s MITI (Ministry ofInternational Trade and Industry) subcontract-ing network under the

payang

or umbrella con-cept, designed to build linkages between largeMNCs and local SMEs. Examples of local Malay-sian inputs bought by Japanese electronicsfirms included moulded compounds for plasticcasings, silicon wager packaging materials, solderfor joints, spare parts, supportive tools, indus-trial chemicals, lubricants, ancillary materialsand final packaging, and shipping materials(authors’ survey 1999). While these inputswere all low-to-medium value-added, Japanesefirms expressed considerable interest in fur-ther domestic sourcing as more materials andcomponents of high standard became availablelocally.

Jomo and Chen (1997) argue that Malaysianlocal content rules for export-credit incentivesaimed at MNCs encouraged higher local con-tent for assembly operations. Thus, firms suchas Hitachi closely co-operated with the govern-ment’s programme for promoting domesticindustries in Penang’s integrated circuit pro-duction complex by participating in the SkillDevelopment Centre of the Penang Free ExportZone. Jomo and Chen (1997) also note thatMalaysian politics, which work in favour of

bumiputra

(indigenous Malay) enterprises, oper-ate against localisation and a viable local partsindustry by actively discriminating againstentrepreneurial Chinese-Malaysian firms. Thispartisan support for Malay-only businesses onethnicity grounds reflects an overall strategyimplemented since 1970 to carry out the govern-ment’s NEP (New Economic Policy) redistri-bution objectives, particularly those aimed atincreasing the share of Malay ownership in theeconomy. Consequently, Ling and Yong (1997)consider that developing a network of highquality local vendors would likely take a longtime.

With regard to the development of localworker skills, Smith (1994) notes that duringthe 1970s local Japanese managers ‘idealised’the traditional Japanese work system, with itsemphasis on firm loyalty, teamwork and dedica-tion to work. While many Japanese MNCs intro-duced some aspects of Japanese workplaces,including quality control groups and

kaizen

(continuous improvement), other features,

notably seniority principles, could not be soeasily transferred to local factories. For instance,seniority principles were rejected, she argues,because Malay people believe that those workerswith higher ability and motivation shouldadvance more quickly than the group as a whole.Indeed, Smith (1994) portrays Japanese man-agers as ‘culturally inept’ in relating to indigen-ous workers as well as the overall society inMalaysia. Because of an inability to assess localstaff according to strict Japanese corporatenorms, human resource issues below the man-agement level have been generally left to indigen-ous Malay or Chinese directors and managers.Nonetheless, formal training and ‘on-the-job’learning increased over the period since 1985(Stage II, Table 1) (authors’ 1999 survey).

5

During the mid 1990s (Stage III, Table 1)

Japanese firms retained a traditional Japanesemanagement style and control in their assemblyplants, but have had to increase the facilitiesoffered to employees to compete for increas-ingly scarce factory labour (e.g. gyms, rest roomsduring Ramadan when Muslims fast during theday). ‘Job hopping’ by both Chinese and Malayengineers and assembly workers has under-mined Japanese interest in long-term trainingprogrammes. While labour mobility appearsendemic in Malaysian culture, it has declinedsince the Asian financial crisis of 1997. Whilelarger companies (e.g. Hitachi) had openedlocally-based training institutions for their engi-neers and operatives, commitment to long-termR&D by Japanese electronics firms was stilllacking.

By the end of the 1990s Japanese MNCs inMalaysia had committed themselves to highervalue-added production and, overall, engagedin upgrading their operations according tothe schema of Table 1. But Dobson (1993) andLinden (2000) argue that Japanese firms havecontinually functioned in more restricted waysthan US electronics firms in Malaysia (andmore widely throughout Southeast Asia), withless technology spill-over effects. They espe-cially emphasise the Japanese firms’ protractedreliance upon Japanese ex-patriot managers,Japanese-style human-resource management,and a deep-seated general aversion towardsnon-Japanese suppliers, especially for hightechnology parts and products. Moreover,Malaysia has not yet generated an array of

20

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

locally-based electronics majors. Accordingly,whether Malaysia can follow South Korea andTaiwan and travel further backward alongthe reverse product-life cycle (from Stage II toStage III, Figure 1), progressively learning howto shift innovation towards the technologyfrontier, is uncertain. As Morris-Suzuki (1992)notes, for Southeast Asian countries, such asMalaysia, with little post-war experience in localindustry, it may be difficult to derive usefullessons from the Japanese experience of tech-nology acquisition.

CONCLUSION

This paper has critically interrogated the flyinggeese model of Japanese DFI as a model ofindustrial learning in Asia. Japanese industrial-isation itself featured production systems createdfrom a comprehensive and systematic approachto endogenous learning. When applied to Asia,however, the flying geese model anticipates thatlate developers will catch up with the tech-nological capabilities of advanced countries byreliance on DFI from Japan (Figure 1 and Table 1).In the electronics sector, the technologicalimpacts of Japanese DFI have varied. The maindifferences in the interactions between Japan,

Northeast Asia and Southeast Asia are sum-marised in Figure 2.

During the 1960s, linkages with JapaneseMNCs played a critical part in South Koreanand Taiwanese technology absorption andexport market growth. The start-up, joint ven-ture phase (up to the early 1970s) correspondsroughly to the passive capacity stage describedin the reverse product cycle model (Stage I,Figure 1). In this stage OEM, licencing andsubcontracting arrangements were more im-portant here than DFI per se and provideda different kind of ‘training school’ for SouthKorean and Taiwanese firms’ engineers andmanagers. Their firms attained economies ofscale by accessing large volume internationalmarkets. Firms such as Samsung and Acer, whobegan as junior partners in Japanese joint ven-tures, moved on to licencing, once sufficient in-house technology had been acquired (roughlyStage II in Figure 1). Following

endaka

in 1985,the level of in-house technology took a furtherjump as South Korean and Taiwanese firmsobtained advantage from reduced Japanesecompetitiveness. In the post-1993 phase, thelarger firms moved to in-house R&D efforts, thepurchase of overseas companies and jointpartnership with Japanese MNCs themselves.

Figure 2. Major interactions between Japan and other Pacific Asia countries in the electronics industry, 1960–2000.

FLYING GEESE IN ASIA

21

© 2004 by the Royal Dutch Geographical Society KNAG

Indeed, there were few opportunities for Japan-ese DFI to expand in Taiwan and South Korea,in contrast to Southeast Asia, but Japanese MNCsused South Korean and Taiwanese firms assources for components at their own assemblyplants in Southeast Asia, and also China.Still, the latter failed to establish sufficient R&Dcapabilities to enable them to compete withJapanese leaders at the technology frontier (StageIII in Figure 1) over a wide range of products.Thus both South Korea and Taiwan had anegative trade balance in electronics with Japanthroughout the 1990s, usually balanced out bya trade surplus with the United States andEurope (Guerrieri 2000).

DFI by Japanese MNCs offered SoutheastAsian countries an alternative route to tech-nology acquisition and participation in inter-national production networks. Japanese branchplants have moved back along the productcycle, but stopped short of investing in long-term R&D or focal factories (as predicted byStage III, Figure 1). Further, as wages rose inMalaysia, China has increasingly considered amore desirable location for electronics assemblyoperations and parts production (Mukoyama1994). Consequently, at the end of the 1990s itwas unclear how Malaysia and other southeastAsian countries would emerge and stake outa position in the evolving regional division oflabour, and how their Japanese subsidiarieswould be positioned along the Pan-Asian value-added production chain.

The overall conclusion for Southeast Asiancountries, therefore, is that despite the rela-tively ‘seamless’ promise offered by the flyinggeese metaphor, too much reliance on JapaneseMNCs for technological transfer misreads theJapanese model of how to industrialise. Thismodel emphasises a ‘do-it-yourself ’ or reverseengineering ethic that councils against relianceon DFI. To move further back along the prod-uct cycle, Southeast Asian countries may haveto develop their own systems of innovation andforms of R&D based around Hobday’s (1995b)ideas about indigenous latecomer firms. Indifferent ways, South Korea and Taiwan havealready moved along this path. Singaporeremains the region’s high-tech and financialfulcrum, and the regional headquarters ofJapanese MNCs prefer to locate there. Nonetheless,little mainstream product design or R&D is

carried out in this location (see Perry

et al.

1997).The Malaysian government had ambitioustechnology-driven plans (the ‘high-tech mediacorridor’) drawing upon Japanese and SouthKorean/Taiwanese Science City models. How-ever, much more policy assistance is needed toencourage the development of fundamentalengineering skills and design-competent SMEsin order to attract higher local content andtechnological deepening from Japanese MNCs(Narayanan and Wah 2000).

6

Other SoutheastAsian countries (e.g. Indonesia, the Philippinesand Thailand) are unlikely to develop past StageI assembly operations due to poorly designedgovernment policies to support local industryand their poorly educated workforces (authors’interviews in Japan with electronic firms’ head-offices during 1998 and 1999). It could beargued that the forces of ‘globalisation’, how-ever defined, undermine strong local initiatives.But is the global context of indigenous-basedindustrialisation any more or less daunting thanthe situation that faced the Japanese in 1868 or1945?

In the near future, how Japanese electronicsfirms arrange their operations in mainlandChina will provide further insight into the rel-evance of the flying geese model for develop-ment in Asia. Japanese electronics firms beganto sell in China soon after the country openedup to overseas trade and DFI in the late 1970s.In the 1980s the Chinese market was lucrativefor Japanese electronics consumer and indus-trial products, but conditions changed in thelate 1980s as the Chinese government imposedimport restrictions to offset ballooning balanceof trade deficits (Cheung & Wong 2000).Consequently, Japanese electronics firms wereforced to engage in some kind of local oper-ations, often in joint venture arrangements, inorder to sell into the Chinese market. Duringthe early 1990s Japanese firms, such as Matsus-hita, Sanyo and Sharp, set up a wide range ofconsumer electronics factories, but in mostcases these were aimed at securing sources oflow-cost labour and materials for productionaimed at Japan and other global markets, ratherthan China itself. Indeed, compared with muchlarger investments by European and NorthAmerican electronics companies (e.g. Nokiaand Motorola), Japanese firms to date havebeen loathe to commit large-scale production

22

ROGER HAYTER & DAVID W. EDGINGTON

© 2004 by the Royal Dutch Geographical Society KNAG

and distribution networks in China. This hesi-tancy reflects their perception of the high riskof business in China (interview with S. Amano,Assistant Director, China and North Asia Divi-sion, Overseas Research Department, JapanExternal Trade Organisation, Tokyo, August,2002). However, after 2000, when China firstbegan negotiations to enter the World TradeOrganisation (WTO), many Japanese changedtheir strategy towards China, and planned moreextensive networks there in order to localisetheir production and other operations. Thereis a perception in Japan that the once highly-regulated Chinese market will become increas-ingly open under stringent WTO rules. Thereis also awareness that because China remainssocialist it will require a special type of commit-ment (through DFI and technology transfer)compared with other parts of Asia (Interviewwith Kenichi Takayasu, Senior Economist,Centre for Pacific Business Studies, The JapanResearch Institute Limited, Tokyo, July 2002).To what degree the Chinese government andlocal enterprises will be able to broker agree-ments involving technology transfer betweenJapanese and Chinese firms (leading to shifts inlocal production along the reverse productcycle model in Figure 1) remains to be seen.

Notes

1. Despite the economic recession of the 1990s,Japanese electronics companies have generated awide array of new products, including the digitalstill cameras, minidisk players and flat-screentelevisions (Karatsu 1999).

2. Without debating the precise boundaries ofPacific Asia, the major countries of the regionconventionally comprise Japan, the four Asiannewly industrialising economies (NIEs) of SouthKorea, Singapore, Taiwan, and Hong Kong SAR,the ASEAN countries (i.e. Association of South-east Asian Nations, including Thailand, Malaysia,Indonesia and the Philippines), China, Laos,Myanmar, Vietnam, Cambodia and Brunei.

3. Under the original formulation by Akamatsu(1962) the flying geese are industrial sectors (tex-tiles, steel, chemicals, cars and electronics) thatpushed Japan’s industrial development to tech-nically more sophisticated levels, inevitably relyingon high levels of exports, including those to Asia.In this framework each ‘lead’ industry (and pro-