fonterra strategy refresh - new zealand … · fonterra strategy refresh & 2012 interim results...

TRANSCRIPT

FONTERRA STRATEGY REFRESH& 2012 INTERIM RESULTS

29 March 2012

Fonterra Co-operative Group Ltd

OVERVIEW• 2012 INTERIM RESULTS• STRATEGY REFRESH

Page 2Fonterra Co-operative Group Ltd

• QUESTIONS & ANSWERS

SIR HENRY VAN DER HEYDEN

Fonterra Co-operative Group Ltd

HIGHLIGHTS• Net profit after tax up 18% to $346m

• Normalised earnings before interest and tax(1)

up 8% to $552m552

Normalised EBIT ($m)(1)

Page 4Fonterra Co-operative Group Ltd

up 8% to $552m

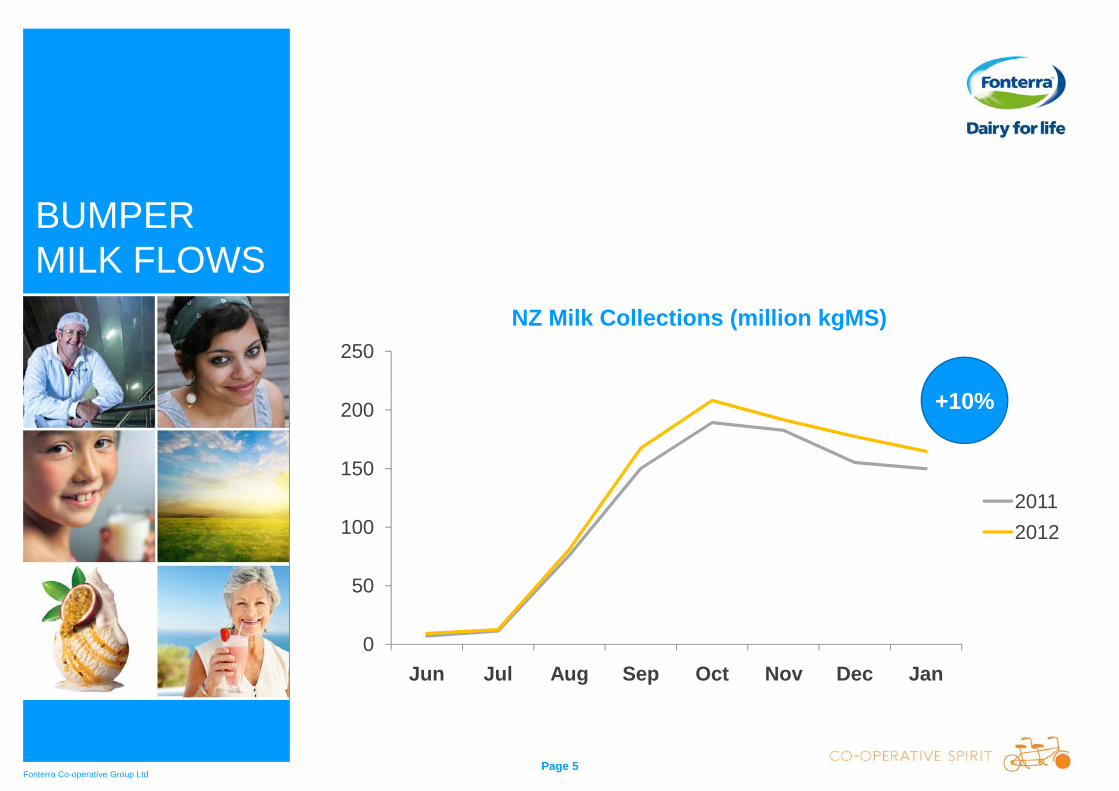

• Strong growth in NZ milk production, up 10% season-to-date

• Sales volume gains of 5%(2) were broad based, reflecting attractiveness of dairy around the world

• Declared higher interim dividend of 12 cents per share, up 4 cents

Notes:(1) Represents normalised earnings before interest and tax, adjusted for non-recurring items(2) Excludes the sales volumes of the Western Australia business that was sold in March 2011

509496

H1 2011 H2 2011 H1 2012

BUMPER MILK FLOWS

250NZ Milk Collections (million kgMS)

+10%

Page 5Fonterra Co-operative Group Ltd

0

50

100

150

200

Jun Jul Aug Sep Oct Nov Dec Jan

20112012

+10%

4 500

5,000

GDTTM WMP Prices

GDTTM PRICES RELATIVELY FLAT COMPARED TO LAST YEAR

Page 6Fonterra Co-operative Group Ltd

2,000

2,500

3,000

3,500

4,000

4,500

USD

per

met

ric to

nne

FONTERRACO-OP CHALLENGES

$8.25 $6.75-$6.85

Page 7Fonterra Co-operative Group Ltd

2011 Final Payout

Latest Payout Forecast(1)

Note:(1) Payout before retentions assumes a farmer is 100 per cent shared up (owning one share per kg MS of annual milk production).

(1)

THEO SPIERINGS

Fonterra Co-operative Group Ltd

STRONG FIRST HALF 1H 2012 $m Change %

External Volume(thousand metric tonnes) 1,927 5(1)

Revenue 10,026 7

Page 9Fonterra Co-operative Group Ltd

Normalised EBIT(2) 552 8

Normalised EBIT Margin(3) 5.5% 7 bps

Profit after tax 346 18

Earnings per share(4) 24 14

Dividend per share(4) 12 50

Note:(1) Excludes the sales volumes of the Western Australia business that was sold in March 2011(2) Earnings before interest and tax, adjusted for non-recurring items(3) Calculated as normalised EBIT as percentage of revenue(4) Cents per share

KEY DRIVERS

• Solid growth in total sales volume • Improved margins in Standard & Premium

Page 10Fonterra Co-operative Group Ltd

Ingredients• ANZ impacted by challenging trading conditions• Stronger NZD had negative impact on earnings

of our Asia/AME & Latam operations

OUTLOOK• Stronger global milk production expected in

2012

Page 11Fonterra Co-operative Group Ltd

• Milk powder demand appears robust but dairy commodity prices likely to remain under some pressure through to mid 2012

• Forecast Farmgate Milk Price of $6.35 per kgMS and net profit after tax guidance of 40-50 cents per share equating to $570-$720 million

MILK FOR SCHOOLS

• Milk is packed with goodness for growing children

• Fonterra Milk for Schools aims to

Page 12Fonterra Co-operative Group Ltd

Fonterra Milk for Schools aims to give New Zealand primary-aged children the opportunity to enjoy the goodness of dairy every school day by offering free milk in schools

JONATHAN MASON

Fonterra Co-operative Group Ltd

STANDARD & PREMIUM INGREDIENTS

• Normalised EBIT growth of 44%(1)

• Key performance drivers:- improved margins

External Volume

Growth(1)

+7%273

Normalised EBIT ($m)

Page 14Fonterra Co-operative Group Ltd

improved margins

- swapping long-term contracts to those with shorter tenure indexed to GDTTM

- strong underlying growth in foodservice & infant nutrition

- effective optimisation of sales book

- productivity improvements and cost savings helped offset cost of inflation on a per unit basis

+7%

Revenue Growth(1)(2)

+10%

Notes:(1) H1 2012 versus H1 2011(2) Includes inter-segment revenue of $868m (H1 2011 - $873m)

189231

H1 2011 H2 2011 H1 2012

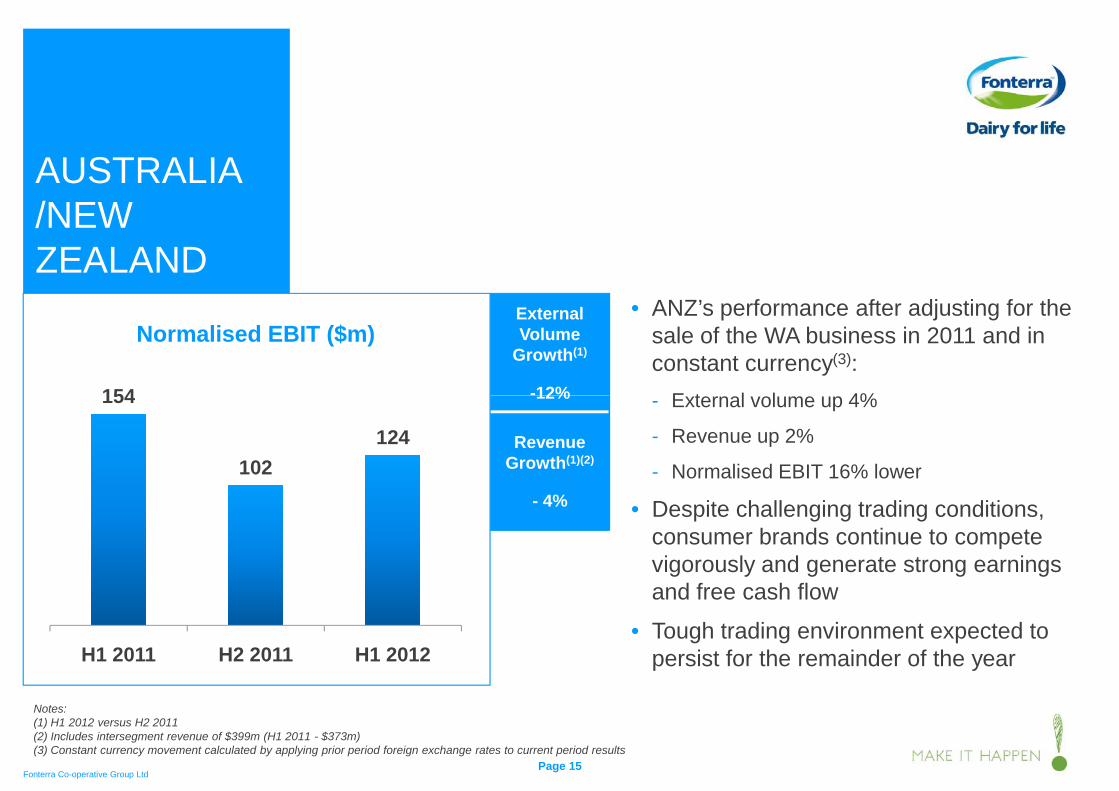

AUSTRALIA /NEW ZEALAND

• ANZ’s performance after adjusting for the sale of the WA business in 2011 and in constant currency(3):

E t l l 4%

External Volume

Growth(1)

-12%154

Normalised EBIT ($m)

Page 15Fonterra Co-operative Group Ltd

- External volume up 4%

- Revenue up 2%

- Normalised EBIT 16% lower

• Despite challenging trading conditions, consumer brands continue to compete vigorously and generate strong earnings and free cash flow

• Tough trading environment expected to persist for the remainder of the year

12%

Revenue Growth(1)(2)

- 4%

Notes:(1) H1 2012 versus H2 2011(2) Includes intersegment revenue of $399m (H1 2011 - $373m)(3) Constant currency movement calculated by applying prior period foreign exchange rates to current period results

154

102124

H1 2011 H2 2011 H1 2012

ASIA/AFRICA & MIDDLE EAST

• On a constant currency basis, normalised EBIT was 5%(1)(2) lower, due largely to:

hi h l & k ti t

External Volume

Growth(1)

+4%

Normalised EBIT ($m)

Page 16Fonterra Co-operative Group Ltd

Notes:(1) H1 2012 versus H2 2011(2) Constant currency movement calculated by applying prior period foreign exchange rates to current period results

- higher sales & marketing costs

- increased input costs

• Core focus is execution of growth strategy:

- investing in China

- growing foodservices

- category expansion

• Continued positive outlook for the region

+4%

Revenue Growth(1)

+7%

97 9684

H1 2011 H2 2011 H1 2012

LATIN AMERICA

• On a constant currency basis, normalised EBIT was up 6%(1)(3)

• Soprole had a strong first half in

External Volume

Growth(1)

-6%64 62

Normalised EBIT ($m)

Page 17Fonterra Co-operative Group Ltd

p gconstant currency terms with earnings up 15%

• Normalised contribution from Dairy Partners of America was $2m lower, impacted by trading conditions in Brazil

6%

Revenue Growth(1)(2)

-5%

Notes:(1) H1 2012 versus H2 2011(2) Includes no inter-segment revenue (H1 2011:$3m)(3) Constant currency movement calculated by applying prior period foreign exchange rates to current period results

556

H1 2011 H2 2011 H1 2012

STRONG BALANCE SHEET

57.6%

59.6%

53.0%54.3%

48 5%

Economic Gearing(1)

Page 18Fonterra Co-operative Group Ltd

44.9%

48.5%

41.8%

46.9%

Jul 08 Jan 09 Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12

Target Range 45-50%

Note:(1) Gearing is measured in terms of economic net interest bearing debt over economic net interest bearing debt plus equity (reflecting the effect of debt hedging in place at balance date). Equity excludes the cashflow hedge reserve

TRADING AMONG FARMERS

MARCH

• Strategy Refresh

APRIL/MAY

• Board considers

JUNE/JULY

• Shareholders’

AUGUST-DECEMBER

• Workshops on the

Page 19Fonterra Co-operative Group Ltd

gy

• Interim Result

first four pre-conditions and prepares report to Shareholders’ Council

Council considers Board report and fifth pre-condition

• DIRA Amendment Bill final reading expected

• Due Diligence Committee Report

• Board and Shareholders’ Council formal resolution on pre-conditions

ponline broker system for farmer shareholders, and registration for share trading

• Prepare & launch market

THEO SPIERINGS

Fonterra Co-operative Group Ltd

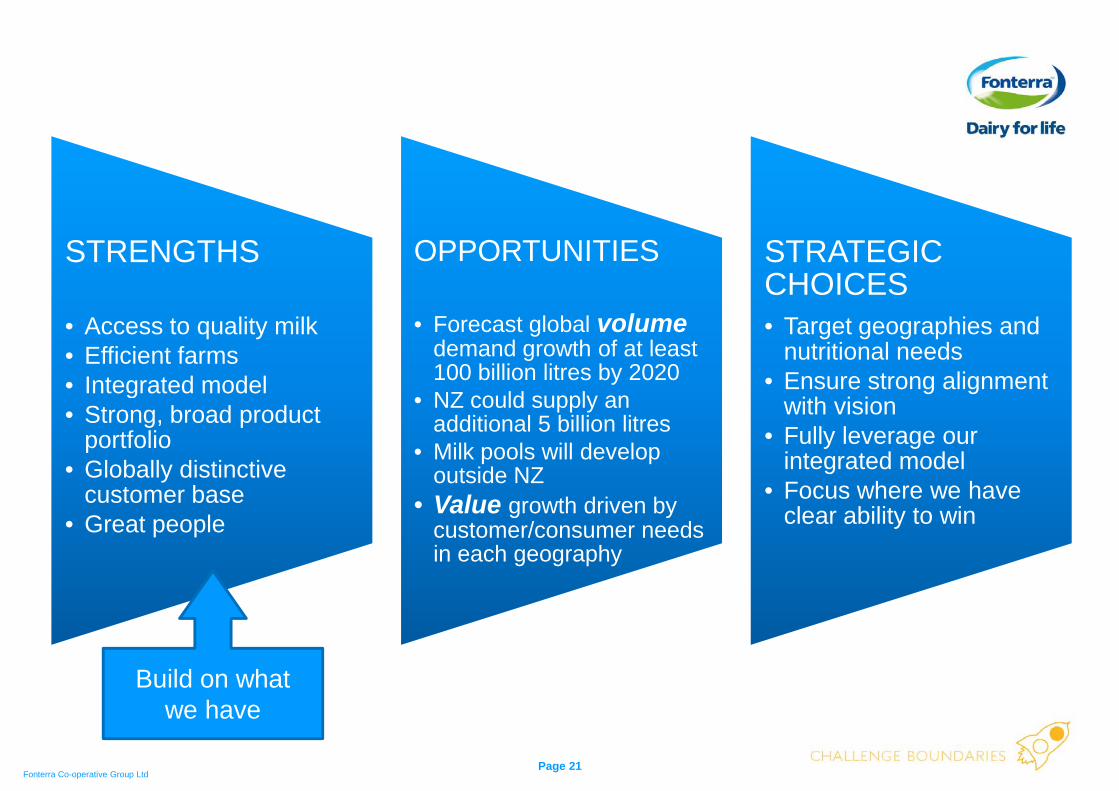

STRENGTHS

• Access to quality milk• Efficient farms• Integrated model

OPPORTUNITIES

• Forecast global volumedemand growth of at least 100 billion litres by 2020NZ ld l

STRATEGIC CHOICES• Target geographies and

nutritional needs• Ensure strong alignment

Page 21Fonterra Co-operative Group Ltd

g• Strong, broad product

portfolio• Globally distinctive

customer base• Great people

• NZ could supply an additional 5 billion litres

• Milk pools will develop outside NZ

• Value growth driven by customer/consumer needs in each geography

with vision• Fully leverage our

integrated model• Focus where we have

clear ability to win

Build on what we have

EMERGING MARKETS ARE KEY 10%

2%

7%

China

4%

1%

Nth America

<1%

Outlook to 2020

<1%

Europe

<1%

STRENGTHS OPPORTUNITIESOPPORTUNITIES STRATEGIC CHOICES

Page 22Fonterra Co-operative Group Ltd

Demand Growth Milk Supply Growth

MENA

2%4% India

2-3%

LATAM

2%2%

ANZ

<1%

Nth America

Source: FAO, Euromonitor, Fonterra estimates

EXCITING GROWTH FORECASTS

Globally Traded D i M k t

Formal Dairy Market

500 bn L by 2020 (3% CAGR)

STRENGTHS OPPORTUNITIESOPPORTUNITIES STRATEGIC CHOICES

Page 23Fonterra Co-operative Group Ltd

17 Bn L

49 billion litres

375 billion litresNew Zealand

Dairy Market

22 bn L by 2020(2% CAGR)

84 bn L by 2020 (5-6% CAGR)

Source: FAO, UN Comtrade, Euromonitor, Fonterra estimates

GLOBAL MEGATRENDS INFORMING STRATEGY

STRENGTHS OPPORTUNITIESOPPORTUNITIES STRATEGIC CHOICES

Rise of Emerging

Increase in commodity

Rising demand for

dairy

Social demographics (e g Aging in

Nutrition for Healthy

Increased focus on

New technology

Page 24Fonterra Co-operative Group Ltd

Markets & Urbanisation

prices & volatility

dairy nutritional benefits

(e.g. Aging in OECD & China)

Healthy Ageing

focus on sustainability

technology & innovation

STRATEGY PRINCIPLES

Our Vision and Objectives

Cash Generators Growth Generators New Business Generators

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 25Fonterra Co-operative Group Ltd

Organisational Capabilities

Generators

Capital Structure

What is our source of cash to generate &

finance our growth?

‘Must do’

What will be the sources of our future cash flow?

‘Can do’

What are our mould-breaking opportunity

areas to invest in?

‘Want to do’

NEW GROUP PORTFOLIO

Our Vision and Objectives

Cash Generators

‘M t d ’

Growth Generators

‘C d ’

New Business

‘W t t d ’

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 26Fonterra Co-operative Group Ltd

‘Must do’ ‘Can do’ ‘Want to do’

Organisational Capabilities Capital Structure

New Zealand Milk

Middle-east & North Africa (MENA)

ANZ

US

Europe

China

ASEAN

Latin America (LATAM)

Out-of-Home Nutrition

India

Advanced Nutrition

Optimise

Right size

SEVEN STRATEGIC PATHS

1. Optimise New Zealand milk

2. Build and grow beyond our current consumer positions

3. Deliver on foodservice potential

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 27Fonterra Co-operative Group Ltd

4. Grow our position in mobility

5. Develop selected leading positions in paediatrics and maternal

6. Selectively invest in milk pools

7. Alignment of business & organisation to enable strategy

Source: FAO, Euromonitor, Fonterra estimates

1.OPTIMISE NEW ZEALAND MILK

• Grow with the market• Enhance asset footprint

D i i d i

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 28Fonterra Co-operative Group Ltd

• Drive improved price achievement and cost to serve

• Increase speed/agility of our supply chain

• Expand financial risk management tools

2.BUILD & GROW BEYOND CURRENT CONSUMER POSITIONS

• Leverage our leadership position in ANZ

• Invest in key emerging markets

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 29Fonterra Co-operative Group Ltd

Invest in key emerging markets- New/underpenetrated Asian

markets- China- Latin America- MENA

3.DELIVER ON FOODSERVICE POTENTIAL

• Drive cash from established & profitable businesses

• Drive growth in key emerging

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 30Fonterra Co-operative Group Ltd

Drive growth in key emerging markets- China- ASEAN- LATAM- MENA

• Continue innovation investment

4.GROW OUR POSITION IN MOBILITY

• Strengthen Anlene leadership in ASEAN through portfolio expansion and increased

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 31Fonterra Co-operative Group Ltd

ppenetration

• Drive Anlene in China across selected regions

5. DEVELOP SELECTED LEADING POSITIONS IN PAEDIATRICS & MATERNAL

• Step change in focus on paediatric ingredients in China

• Strengthen our leadership

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 32Fonterra Co-operative Group Ltd

g pposition in our branded maternal category

• Enhance position in infant formula in selected Asian markets

• Continued investment in supply innovation

6.SELECTIVELY INVEST IN MILK POOLS

• Maintain strong milk supply position in New Zealand, Australia & Latam

• Stage-gated investment in additional

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 33Fonterra Co-operative Group Ltd

g gChina farms, through partnerships

• Focus on food security & safety• Pilot farms in selected markets to

test and create options for integrated business models

7.ALIGNMENT OF BUSINESS & ORGANISATION TO ENABLE STRATEGY

• Re-align overhead spend to focus on fastest growing markets

• Exit unprofitable uncompetitive

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 34Fonterra Co-operative Group Ltd

Exit unprofitable, uncompetitive and non-core categories and markets

• Improve efficiency and effectiveness of corporate centre

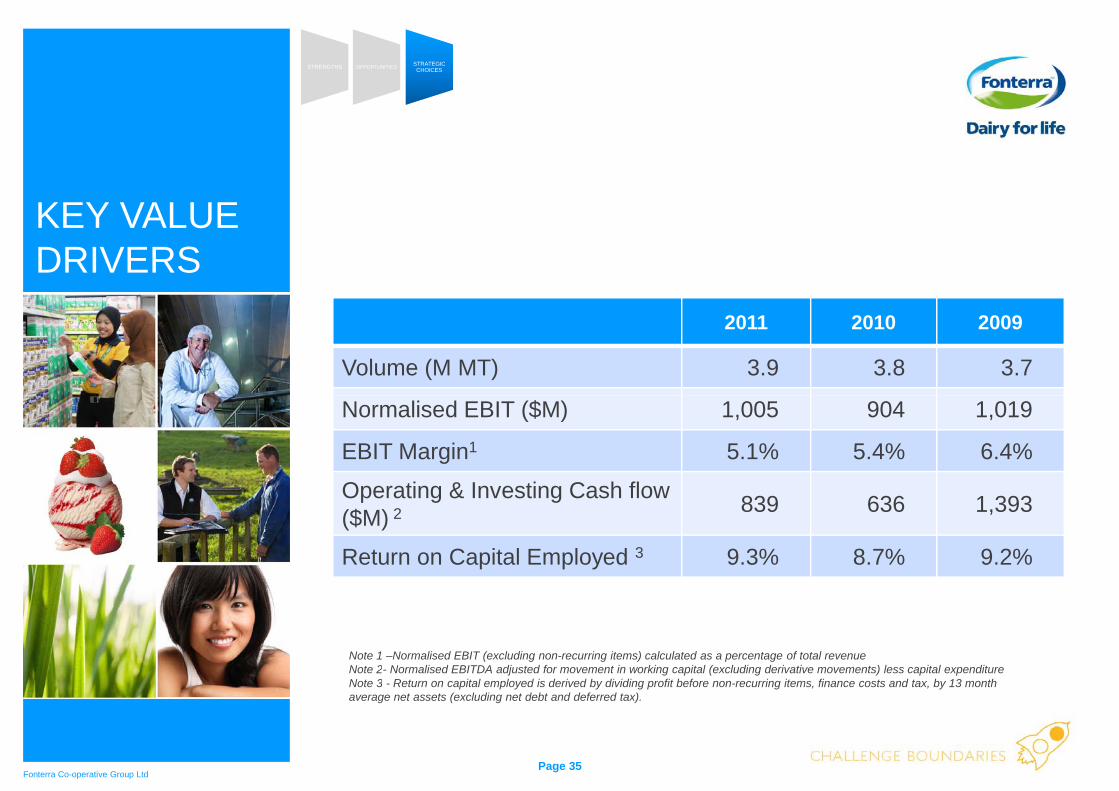

KEY VALUE DRIVERS

2011 2010 2009

Volume (M MT) 3.9 3.8 3.7

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 35Fonterra Co-operative Group Ltd

Normalised EBIT ($M) 1,005 904 1,019

EBIT Margin1 5.1% 5.4% 6.4%

Operating & Investing Cash flow ($M) 2 839 636 1,393

Return on Capital Employed 3 9.3% 8.7% 9.2%

Note 1 –Normalised EBIT (excluding non-recurring items) calculated as a percentage of total revenueNote 2- Normalised EBITDA adjusted for movement in working capital (excluding derivative movements) less capital expenditureNote 3 - Return on capital employed is derived by dividing profit before non-recurring items, finance costs and tax, by 13 month average net assets (excluding net debt and deferred tax).

STRATEGY SETS PLATFORM FOR GROWTH

Dri e Ret rn on Impro e Shareholder

STRENGTHS OPPORTUNITIES STRATEGIC CHOICES

STRATEGIC CHOICES

Page 36Fonterra Co-operative Group Ltd

Improve Value Drivers Drive Return on Capital (ROCE)

Improve Shareholder Value

• Volume growth

• Value growth

• Strong operating & investing cash flow

Improve Return on Capital Employed

Farmer Income

Value of Fonterra

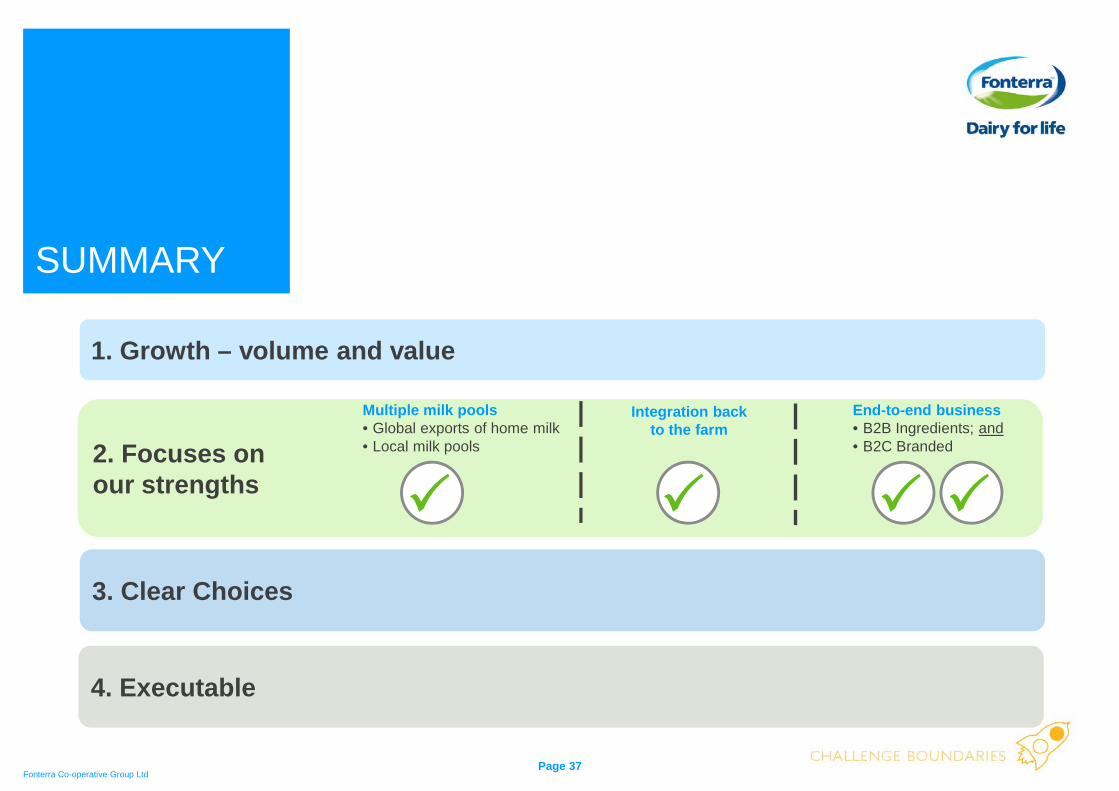

SUMMARY

1. Growth – volume and value

Page 37Fonterra Co-operative Group Ltd

2. Focuses on our strengths

3. Clear Choices

Multiple milk pools• Global exports of home milk• Local milk pools

Integration backto the farm

End-to-end business• B2B Ingredients; and• B2C Branded

4. Executable

SUPPLEMENTARY INFORMATION

Fonterra Co-operative Group Ltd

INTERIM RESULT

1H 2012 ($m) 1H 2011 ($m) Change ($m) Change %

Revenue 10,026 9,356 670 7.2

Page 39Fonterra Co-operative Group Ltd

Profit after tax 346 293 53 18.1

Normalised EBITDA(1) 795 752 43 5.7

Normalised EBIT(2) 552 509 43 8.4

Earnings per share(3) 24 21 3 14.3

Operating cash flow (442) (189) (253) (133.9)

Economic gearing(4) 46.9% 48.5% 160 bps

Notes:(1) Earnings before interest, tax, depreciation and amortisation, adjusted for non-recurring items(2) Earnings before interest and tax, adjusted for non-recurring items(3) Cents per share(4) Economic gearing is measured in terms of economic net interest bearing debt over economic net interest bearing debt plusequity (reflecting the effect of debt hedging in place at balance date). Equity excludes the cash flow hedge reserve.

NORMALISED EBIT

1H 2012 ($m) 1H 2011 ($m)

Operating Profit 516 452

Page 40Fonterra Co-operative Group Ltd

Plus share of profit of equity accounted investees 14 40

EBIT 530 492

Add back non-recurring items

- Impairment losses recorded in equity accounted investees 20

- Impact of Christchurch earthquake 3

- Costs associated with sale of Western Australia dairy business 3

- Other 2 11

Total Non-recurring Items 22 17

Normalised EBIT 552 509

STANDARD & PREMIUM INGREDIENTS

6 months to 31 Jan 2012

6 months to 31 Jan 2011 % Change

Volume (000 MT) 1,234 1,151 7.2

Page 41Fonterra Co-operative Group Ltd

Total Revenue ($M) 7,965 7,231 10.2

External Revenue ($M) 7,097 6,358 11.6

Normalised EBIT ($M) 273 189 44.4

Operating Margin(1) 3.4% 2.3%

Normalised EBITDA ($M) 463 378 22.5

EBITDA Margin(2) 5.8% 5.2%

Notes:(1) Normalised EBIT (excluding non-recurring items) less share of equity accounted investees earnings calculated as a percentage of total revenue(2) Normalised EBITDA calculated as a percentage of total revenue.

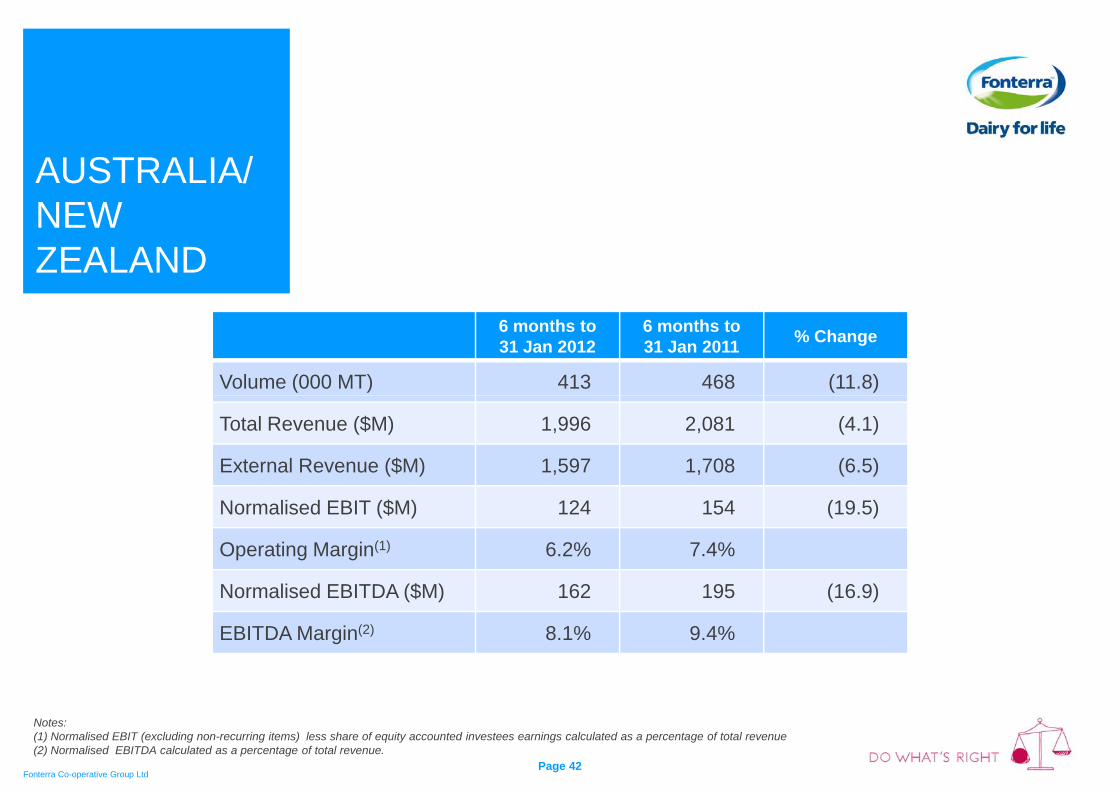

AUSTRALIA/ NEW ZEALAND

6 months to 31 Jan 2012

6 months to 31 Jan 2011 % Change

Volume (000 MT) 413 468 (11.8)

Page 42Fonterra Co-operative Group Ltd

Total Revenue ($M) 1,996 2,081 (4.1)

External Revenue ($M) 1,597 1,708 (6.5)

Normalised EBIT ($M) 124 154 (19.5)

Operating Margin(1) 6.2% 7.4%

Normalised EBITDA ($M) 162 195 (16.9)

EBITDA Margin(2) 8.1% 9.4%

Notes:(1) Normalised EBIT (excluding non-recurring items) less share of equity accounted investees earnings calculated as a percentage of total revenue(2) Normalised EBITDA calculated as a percentage of total revenue.

ASIA/AFRICA & MIDDLE EAST

6 months to 31 Jan 2012

6 months to 31 Jan 2011 % Change

Volume (000 MT) 132 127 3 9

Page 43Fonterra Co-operative Group Ltd

Notes:(1) Nil Intersegment Revenue(2) Normalised EBIT (excluding non-recurring items) less share of equity accounted investees earnings calculated as a percentage of total revenue(3) Normalised EBITDA calculated as a percentage of total revenue.

Volume (000 MT) 132 127 3.9

Total Revenue ($M) (1) 947 887 6.8

Normalised EBIT ($M) 84 97 (13.4)

Operating Margin(2) 8.9% 10.9%

Normalised EBITDA ($M) 88 101 (12.9)

EBITDA Margin(3) 9.3% 11.4%

LATIN AMERICA

6 months to 31 Jan 2012

6 months to 31 Jan 2011 % Change

Volume (000 MT) 148 157 (5.7)

Page 44Fonterra Co-operative Group Ltd

Notes:(1) Normalised EBIT (excluding non-recurring items) less share of equity accounted investees earnings calculated as a percentage of total revenue(2) Normalised EBITDA calculated as a percentage of total revenue.

o u e (000 ) 8 5 (5 )

Total Revenue ($M) 385 406 (5.2)

External Revenue ($M) 385 403 (4.5)

Normalised EBIT ($M) 62 64 (3.1)

Operating Margin(1) 13.8% 11.1%

Normalised EBITDA ($M) 73 73 -

EBITDA Margin(2) 19.0% 18.0%

CASHFLOW SUMMARY

6 months to 31 Jan 2012

($m)

6 months to 31 Jan 2011

($m)

C h fl f ti ti iti (442) (189)

Page 45Fonterra Co-operative Group Ltd

Cash flows from operating activities (442) (189)

Cash flows from investing activities (294) (257)

Cash flows from financing activities 621 724

Net cash (outflow)/inflow (115) 278

GEARING31Jan 2012

($m)31 Jan 2011

($m)31 July 2011

($m)

Net Interest bearing debt position

Page 46Fonterra Co-operative Group Ltd

Total borrowings 5,802 5,854 4,650Cash and cash equivalents (684) (831) (785)

Interest bearing advances included in other non-current assets (126) (117) (122)

Bank overdraft 27 29 23

Value of derivatives used to manage changes in hedged risks and other FX movement on debt

429 396 565

Economic net interest bearing debt 5,448 5,331 4,331Total equity less cash flow hedge reserves 6,179 5,654 6,025

Economic debt: debt plus equity 46.9% 48.5% 41.8%