for a/m 306v -...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

A/M 306vReport No. 7417-CHA

STAFF APPRAISAL REPORT

CHINA

HUBEI PHOSPHATE PROJECT

APRIL 25, 1989

Industry, Trade and Finance Operations DivisionCountry Department IIIAsia Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(As of February 5, 1989)

Currency name Renminbi (RMB)Currency unit - Yuan (Y) = 100 FenY lQon US$0.27US$1.00 - Y 3.72

WEIGHTS AND MEASURES

1 hectare (ha) 2.47 acres1 metric tcn (ton) 1,000 kilograms (kg)1 kilometer (km) 0.621 miles1 cuibic meter (m3 ) 35.3147 cubic feet (cf)1 kilocalories (kcal) 3,968 British thermal units (BTU)1 kilowatt (kW) 1,000 watts1 megawatt (MW) 1,000 kilowatts (kW)

FISCAL YEARJanuary 1 - December 31

GLOSSARY OF ABBREVIATIONS AND ACRONYMS

ABC - Ammonium Bicarbon'tte K20 - Potassium OxideAMPC - Agricultural Means of Production kWh - Kilowatt Hour

Corporation MA" - Ministry of Agriculture, AnimalBICEM - Beijing Institute of Chemical Husbandry and Fishery

Engineering and Management MgO - Magnesium OxideCIB - China Investment Bank MAP Monoammonium PhosphateCIF - Cost, Insurance and Freight MCI - Ministry of Chemical IndustryCNCCC - China National Chemical MOC - Ministry of Commerce

Construction Corporation Mtpy - Million Tons per YearCMP - Calcium Magnesium Phosphate MWh - Megawatt HourCMPDI - Chinese Chemical Mines Planning N - Nitrogen Content in Fertilizer

and Design Institute NCDI - Nanjing Chemical DesignCMRDI - Chinese Chemical Mines Research Institute

and Dasign Institute NPK - Complex Fertilizers of N.P205CPI - Chemical Planning Institute and K20DAP - Diammonium Phosphate p.a. - Per AnnumFOB - Free on Board PA - Phosphoric AcidFAO - Food and Agricultural PCBC - People's Construction Bank of

Organization of the United ChinaNations P205 - Phosphorous Pentoxide

FY - Fiscal Year ppm - Parts per MillionGDP - Gross Domestic Product PRS - Production Responsibility SystemGOC - Government of Cnilna ROM Run of Mineha - Hectare SAM State Audit AdministrationHAZOP - Hazard and Operability SINOCHEM - China Chemical Export and ImportHMC - Huangmailing Mining Company CorporationHPCC - Huangmailing Phosphate Chemical SPB - State Pricing Bureau

Company SPC - State Planning CommissionHPG - Hubei Provincial Government SSP - Single SuperphosphateICB - International Competitive Bidding TSP - Triple SuperphosphateICBC - Industrial and Commercial Bank of tpd - Tons per Day

China tpyn - Tons per Year of NutrientsIDC - Interest During Construction UNIDO - United Nations IndustrialIFC - International Finance Corporat.on Development OrganizationJPCC - Jinxiang Phosphate Chemical WCEDI - Wuhan Chemical Engineering

Company Design Institute

FOR OFFICIAL USE3 ONLY

CHINA

HUBEI PHOSPHATE PROJECT

Table of Contents

Page No.

LOAN AND PROJECT SUMKARY ..................................... i-iii

I. INTRODUCTION ................................................. 1

II. AN OVERIIEW OF THE CHINESE INDUSTRY .......................... 2

A. General Industry Background ............................. 2B. Government Objectives and Strategy for Industrial

Development ........................................... 3C. Bank Support for Industry ............................... 3

III. THE FERTILIZER SECTOR ........................................ 5

A. Agricultural Background ................................. 5B. Fertilizer Use in Agriculture ........................... 6C. Fertilizer Demand and Supply ............................ 6D. Structure of the Fertilizer Industry .................... 9E. Fertilizer Marketing and Distribution ................... 9F. Fertilizer Pricing ...................................... 10G. Goveranent Strategy in the Fertilizer Sector ............ 13

IV. THE PHOSPHATE SUBSECTOR ...................................... 14

A. World Phosphate Market .---------------------------- 14B. The Chinese Phosphate Industry ......................... 15C. Supply of Raw Materials ................................ 16D. The Phosphate Subsector Study-.......................... 17E. lnvestment Program for the Phosphate Subsector .18F. Bank Role and Project Justification .18

V. PROJECT INSTITUTIONS .........................................-19

A. Background ........................ 20B. The Jinxiang Phospb te Chemical Company (JPCC) .......... 21C. The Huangmailing ehosphate Chemical Company (HPCC) ....... 2D. The Ministry of Chemical Industry (MCI) ................. 23

This report has been prepared by Messrs. K. Song (AS3IF), K. Constant (ASTIF),H. Hendriks (ASTEG), and D. Lilaoonwala (CTRMI). Messrs. W. Sheldrick(Consultant) and B. Stone (Consultant) contributed to the fertilizer sectorand phosphate subsector chapters. Ms. G. Mohadjer-Niederreiter and Mr. K. Hur(AS3IF) contributed to the financial and economic analysis chapters. Ms. D.Christmas provided secretarial support in the preparation of this report.

This document has a restricted distribution and may be used by recipients only in the ptrformanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

Page No.

VI. THE PROJECT ......... ... 23

A. Objectivesb.. .. ................... 23B. Dayukou Phosphate Mine and Fertilizer Development

Component ... . ....... 24C. Huangmailing Phosphate Mine and Fertilizer

Development Component ... 24D. Technical Assistance Component . . 24

VII. PROJECT MANAGEMENT AND ENVIRONMENTAL PROTECTION... 25

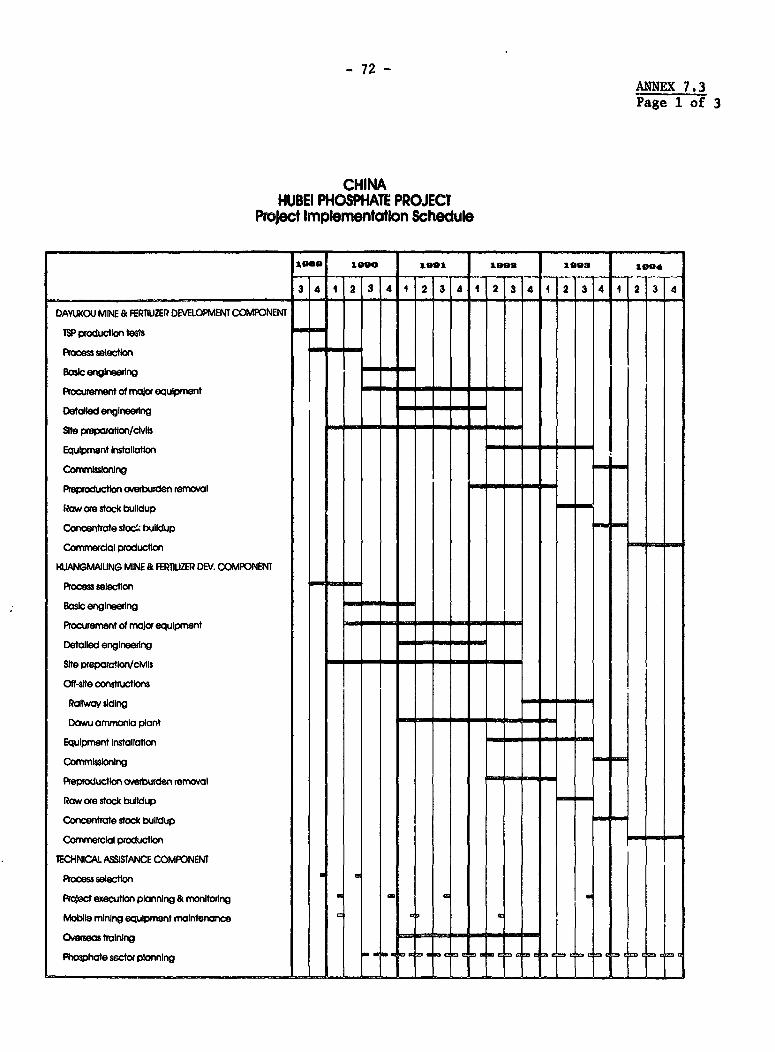

A. Engineering Arrangements..... 25B. Project Management..... 26C. Implementation Schedule..... 26D. Training. .. 27E. Environmental Aspects. . ...... 27

VIII. CAPITAL COSTS, FINANCING PLAN, PROCUREMENT AND DISBURSEMENT.. 28

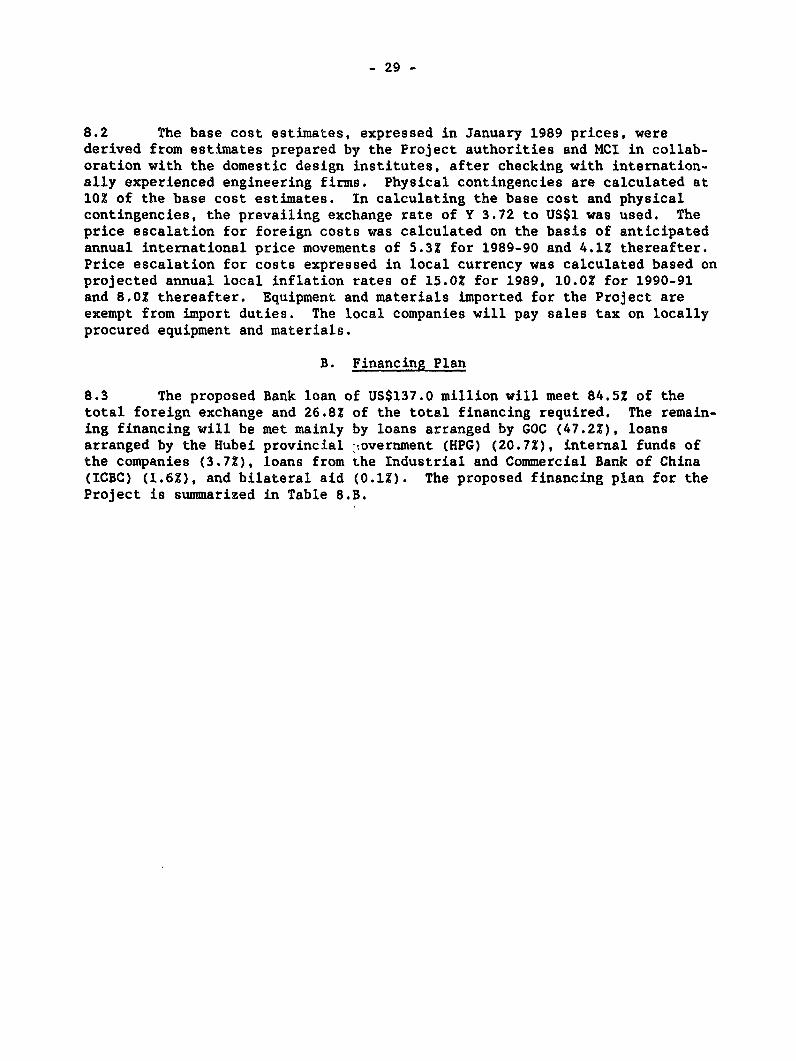

A. Capital Cost Estimates ......... 28B. Financing Plan ......... 29C. Procurement ......... 31D. Allocation and Disbursement of the Bank Loan . ...... 32

IX. FINANCIAL ANNALJSIYSIS ......... 35

A. Financial Management Practices in China. . 35B. Financial Performance and Projections . . .36

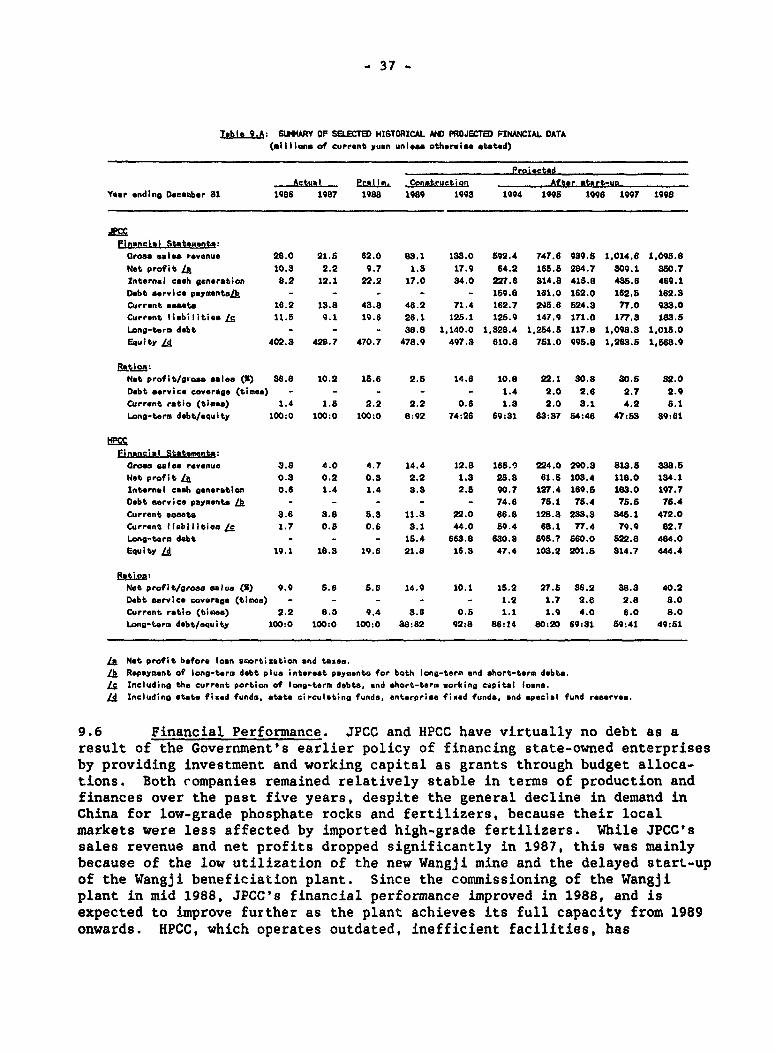

C. Financial Rate of Return and Sensitivity Analysis 38D. Financial Covenants. 39E. Auditing and Reporting Requirements .. .39

X. ECONOMIC ANALYSIS .40

A. Economic Costs and Benefits .40B. Economic Rate of Return and Sensitivity Analyss .40C. Other Benefits .41D. Project Risks .42

XI. AGREEMENTS REACHED DURING LOAN NEGOTIATIONSAND RECOMMENDATION .42

ANNkXES

3.1 Fertilizer Application Rates for Various Countries, 19853.2 Consumption, Production and Imports of Chemical Fertilizers, 1972-873.3 Comparison of Domestic and international Prices of Fertilizers, Main

Energy Inputs, and Main Agricultural Products, December 1988

- iii -

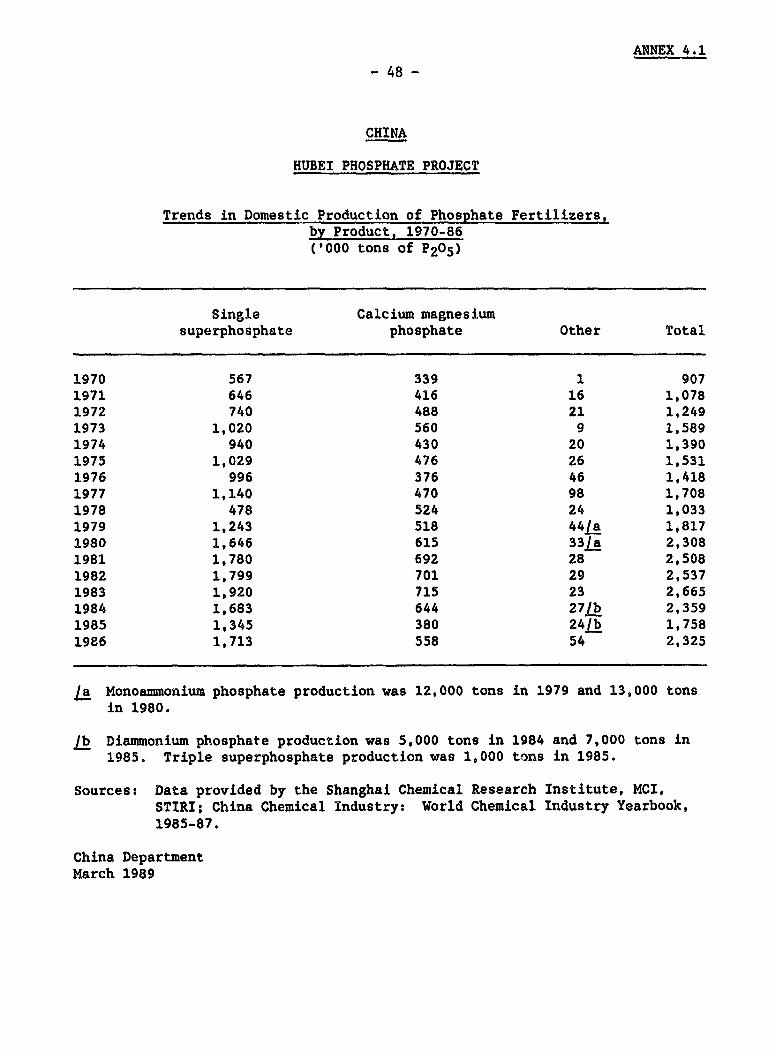

4.i Trends in Domest.ic Iroduction of Phosphate Fertilizers, by Product,1970-86

4.2 Domestic Production of Phosphate Fertilizers by Produict and Province,1985

4.3 Consumption of Chemical Fertilizers by Province, 19854.4 Major Phosphate Deposits in China4.5 Major Pyrite Eieposits and Mines in China4.6 An Outline of the Phosphate Subsector Investment Optimization Model4.7 Planned Phosphate Investment Projects to the lear 2000

5.1 Production Performance of JPCC and HPCC5.2 Organization Chart of JPCC5.3 Organization Chart of HPCC

6.1 Summary of the Dayukou Mine and Fertilizer Development Component6.2 Summary of the Huangmailing Mine and Fertilizer Development Component6.3 Summary of the Terms of Reference for Consulting Services to Support

Project Implementation Under the Technical Assistance Componient6.4 Outline for Training on Hazard and Operability (HAZOP) Analysis

7.1 Organizat' _hart of MCI's Project Coordination Unit7.2 Organization Chart of Project Management Teams for JPCC and HPCC7.3 Project Implementation Schedule and Key Milestones7.4 Environmental Protectiun and Standards

8.1 Capital Cost Estimates8.2 Estimated Disbursement Schedule for Bank Loan

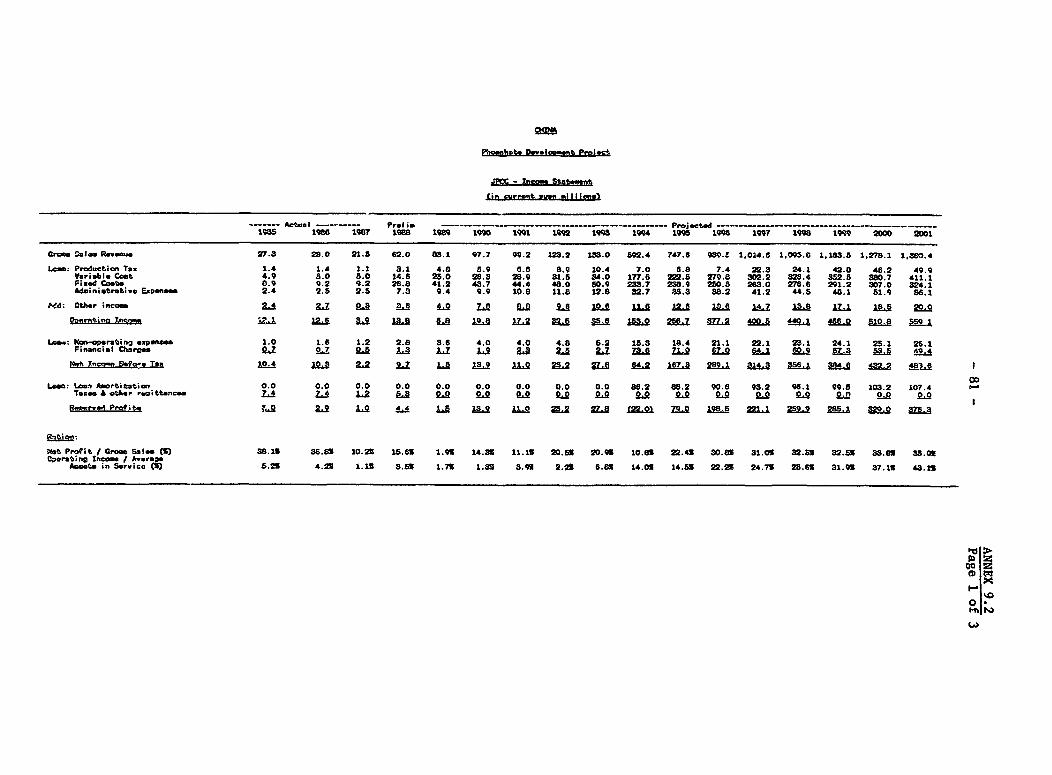

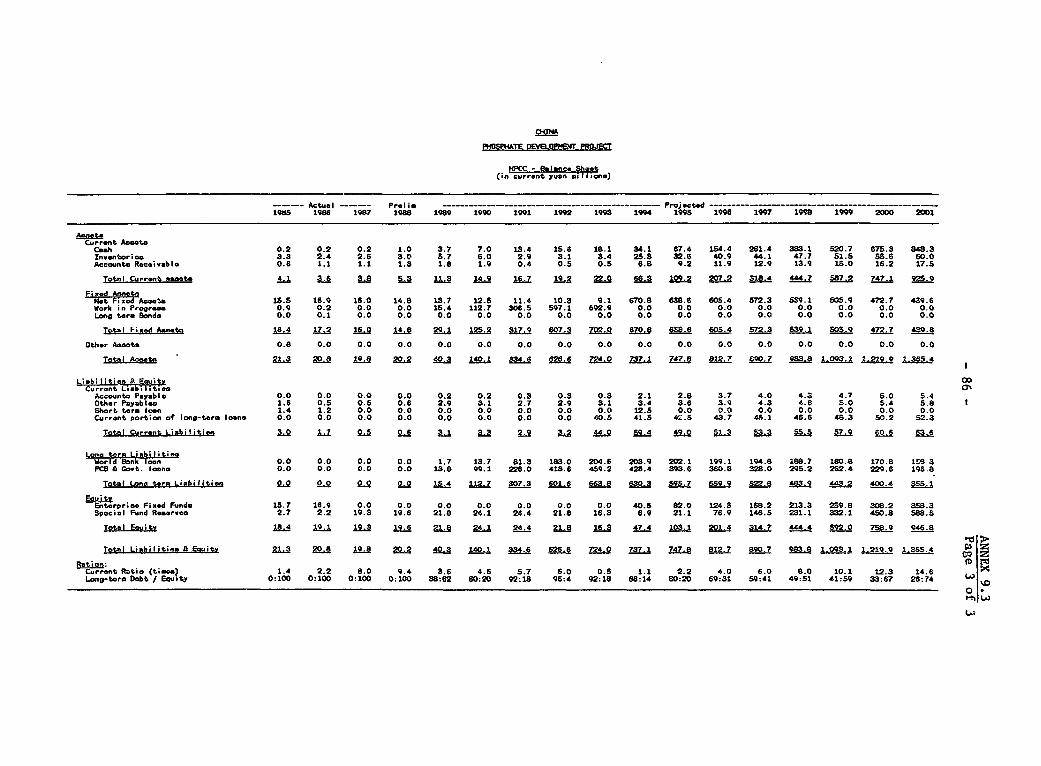

9.1 Assumptions Underlying the Financial Analysis9.2 JFCC - Summary of Historical and Projected Financial Statements9.3 HPCC - Summary of Historical and Projected Financial Statements9.4 Incremental Cost and Revenue Streams for FRR Calculations

10.1 Assumptions Underlying the Economic Analysis10.2 Incremental Cost and Benefit Streams for ERR Calculations10.3 Net Savings of Foreign Exchange over Project Life

MAP

IBRD 20919R: China - Phosphate Reserves and Production FacilitiesIBRD 20504R: Dayukou Phosphate Mine and Fertilizer Development

ComponentIBRD 20505R: Huangmailing Phosphate Mine and Fertilizer Development

Component

DOCUMENTS AVAILABLE IN PROJECT FILES

Reference

1. Feasibility Studies for the Two Development Components2. Terms of Reference for Consulting Services to Support Project

Implementation3. A Blackbook Explaining the Economic and Financial Analyses

- i -

CHINA

HUBEI PHOSPHATE PROJECT

Loan and Project Summary

Borrower: The People's Republic of China

Beneficiaries: Jinxiang Phosphate Chemical Company (JPCC, Hubei Province);Huangmailing Phosphate Chemical Company (HPCC, Hubei Prov-ince); Ministry of Chemical Industry (MCI)

Loan Amount: US$137.0 million equivalent

Terms of Loan: 20-year repayment, including 5 years of grace, at the stan-dard variable interest rate

On-lending Terms: The Government will on-lend the loan proceeds, through theHubei provincial government, to the two Project companiesat an on-lending rate equal to 105% of the IBRD variablerate, with a repayment period of 20 years, including 5years of grace. The commitment charge and foreign exchangerisks will be passed on to the companies.

ProjectObjectives: The Project will assist China in achieving its priority for

the fertilizer sector under the Seventh and Eighth Five-Year Plans (1986-95), which is to reduce the nutrientimbalance in fertilizer use by expanding the productioncapacity for phosphate fertilizers, particularly high-gradeproducts such as monoammonium phosphate (MAP) and triplesuperphosphate (TSP), based on domestic phosphateresources. More specifically, the Project will help GOCto: (a) implement the integrated development of two majorphosphate mines and their downstream high-grade fertilizercomplexes, the first such operations in China in terms ofsize and configuration; and (b) strengthen MCI's projectmanagement capabilities and the capacity cf Chinese designinstitutes to identify and analyze potential safety hazardsand plant operability in chemical plant design and opera-tions. The major investments to be implemrnted under theProject are consistent with the overall dLvelopment strate-gies worked out through the Phosphate Subsector Study (theStudy), which was carried out during project preparationjointly by the Bank and MCI and which resulted in a phos-phate subsector investment program to the year 2000. Theproject investments which comprise the integrated develop-ment of domestic phosphate deposits and fertilizers usingmodern mining, beneficiation and fertilizer productiontechnologies, are also expected to serve as models for thefuture development of the fertilizer sector. The Project

- ii -

will increase China's local supply of phosphate fertilizersby about 25Z.

ProjectDescriptiont The Project has three componentst (a) Dayukou mine and

fertilizer developmernt - initiation of a new open-pit mineof 1.5 Mtpy ROM rock capacity, construiction of a bereficia-tion plant, and establishment of a 560,000 t-py TSP ferti-lizer complex; (b) Huang&ailin& mine and fertilizer devel-opment - expansion of the capacity of an existing opern-pitmine from 0.3 Mtpy ROM rock to J.0 Mtpy, constrlictiozn of abeneficiation plant, rehabilita:ion of a small low-gradenitrogenous fertilizer plant to supply ammoinla as feedstockfor MAP production, and establishment of a l0,O000 tpy MAPplant near the mine site; and (c) technical assistance -consulting services for project implementation, technologyselection, production start-up and mine workshop mainte-nance and for training on modern methodologies for Hazardand Operability (HAZOP) analysis.

Project Benefits The Project will generate indirectly significant economicand Risks: benefits in agriculture by reducing the nutrient imbalance

and increasing the synergism of fertilizer application. Noextraordinary commercial risk are foreseen, given thegeneral shortage of phosphate fertilizers and theapparently buoyant Chinese fertilizer market. The maintechnical risks relate to the need for coordinated imple-mentation and commissioning of high-grade phosphate ferti-lizer plants and associated mines. In the past, the lackof proper coordination has been a persistent problem inimplementing integrated mine and fertilizer investments,executed by separate entities under separate budgets. Thisrisk will be mitigated by implementing both mine develop-ment and fertilizer plant construction under the sameproject management team and from the same budget, as wellas by assurances of diligent monitoring and coordinationfrom the Government. The risk will be further mitigated byinvolving internationally experienced consultants under thetechnical assistance component; they will assist MCI'sproject coordination team and the project companies withproject implementation and production start-up. In addi-tion, the project coripanies will undertake comprehensivestaff recruitment and training .rograms for core opera-tional and maintenance personnel during Project implementa-tion.

- iii -

Project Costt Local Foreign Total----- (US$ million) -----

Dayukou mine and fertilizer development160.2 73.4 233.6

Huangmailing mine and fertilizerdevelopment 75.5 35.1 110.6

Technical assistance - 0.4 0.4

Base cost (January 1989 prices) 235.7 108.9 344.6

Physical contingencies 23.6 10.9 34.5Price contingencies 37.4 19.6 57.0

Installed cost 296.7 139.4 436.1

Incremental working capital 27.2 - 27.2Interest during construction 24.4 22.9 47.3

Total Financing Required /a 348.3 162.3 510.6

Financing Plan: Local Foreign Total----- (US$ million) -----

IBRD loan - 137.0 137.0GOC loan 240.7 - 240.7Provincial government loan 80.4 25.2 105.6Industrial and Commercial Bank loans 8.3 - 8.3Companies' internal funds 18.9 - 18.9Bilateral aid - 0.1 0.1

Total Financing 348.3 162.3 510.6

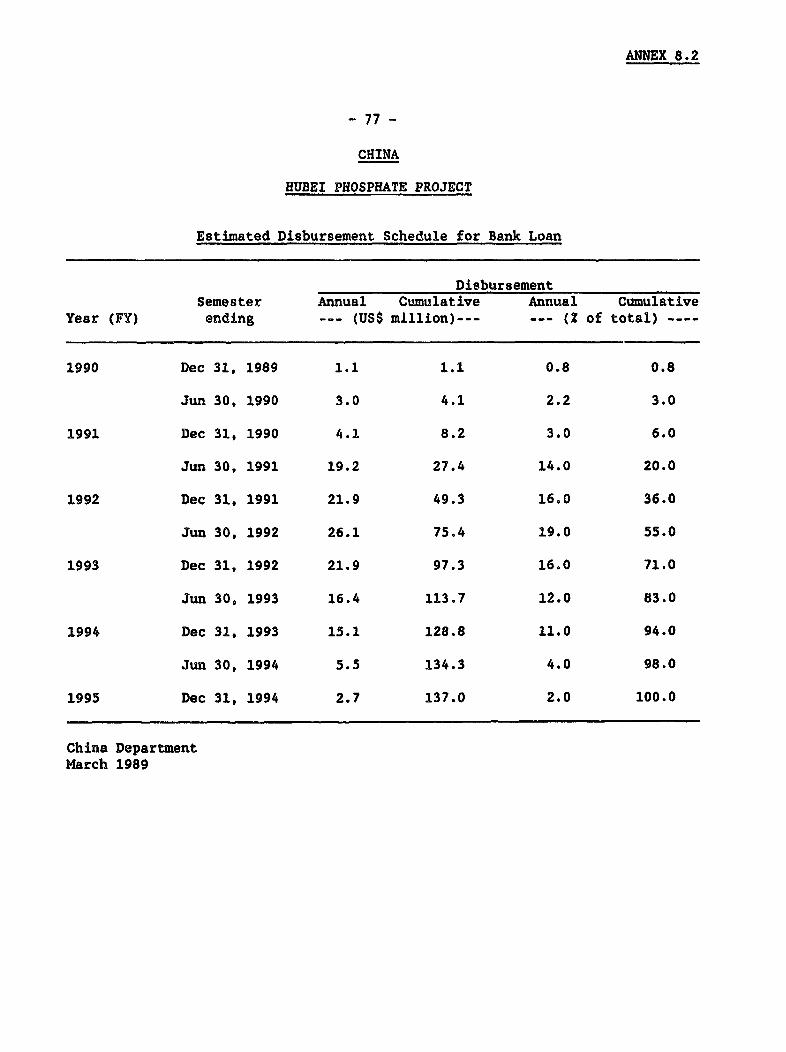

Estimated Disbursements:

IBRD PY 1990 1991 1992 1993 1994 1995-------------- (US$ million) ----------------

Annual 4.1 23.3 48.0 48.3 20.6 2.7Cumulative 4.1 27.4 75.4 113.7 134.3 137.0

Economic Rate of Return: 172

La The total cost net of sales taxes on locally purchased equipment and mate-rials (US$6.0 million) is US$504.6 million.

CHINA

HUBEI PHOSPHATE PROJECT

I. INTRODUCTION

1.1 The Government of the People's Republic of China (the Government,GOC) has requested a Bank loan of US$137.0 million equivalent to finance aHubei Phosphate Project for (the ProJect). The Project embodies an evolutionof the Bank's fertilizer operations in China, geared toward broadening theimpact of Bank support for developing and improving the efficiency of theentire fertilizer sector. The Fertilizer Rehabilitation and Energy SavingProject (Loan 2541-CHA, FY85), the first Ba fertilizer operation, supportsthe rehabilitation of four large and one medium-sized nitrogenous fertilizerplants. The subsequent Fertilizer Rationalization Project (Loan 2838-CHA,FY87) aims to demonstrate alternatives for improving production efficiency atmedium-size nitrogenous fertilizer plants, which currently produce low-gradefertilizers, by converting products from five such plants into high-gradefertilizers. It also aims to strengthen sector-wide institutional efficiencyby introducing improved management systems at the enterprise level. ThePhosphate Development Project (Loan 2958-CHA, FY88), the third Bank-supportedoperation in the fertilizer sector in China (which was prepared and appraisedconcurrently with the Project), broadens the Bank's involvement beyond thenitrogenous fertilizer subsector. It supports the development of a large-scale, modern phosphate mine in Guizhou Province which would provide high-quality phosphate concentrates to several downstream fertilizer plants.Through the Phosphate Sector Study carried out during the preparation of thethird project and this project (prepared concurrently), a subsectoral approachto Bank assistance was initiated, with the Bank providing financial and tech-nical support to the Ministry of Chemical Industry (MCI) for the design ofsubsector-wide strategies. That effort resulted in the preparation of anoptimal investment program that would allow China to meet its rapidly growingdemand for phosphate fertilizers in the least-cost manner.

1.2 Consistent with the overall development strategies and investmentprogram worked out under the above Study, the Project will support: (a) inte-grated development of two pnosphate mines in Hubei Province and their down-stream high-grade phosphate fertilizer (MAP and TSP) plants at the mine sites;and (b) provision of consultant services to MCI's project coordination teamand the project companies for project implementation, technology selection,production start-up, and mine workshop maintenance.

1.3 The Project investments were initially identified in 1985, and wereprepared and appraised by the Bank's project team as part of the PhosphateDevelopment Project in December 1987. However, GOC wished to delay the loanprocessing for these investments and prepare a separate project on a differentschedule as its own internal review of them was getting delayed. Consideringthe urgency of developing the Guizhou mine in time for the commissioning ofdownstream fertilizer plants currently under construction, the remaining por-tion of the Phosphate Development Project was processed according to the ori-

- 2

ginal schedule, and presented to the Board in June 1988. Key parameters ofthe Project were updated during postappraisal in February 1989. The earlierPhosphate Subsector Study was carried out during 1986-88.

1.4 This report recommends a Bank loan of US$137.0 million equivalent,which would cover 26.82 of the total financing required and 84.5Z of the totalforeign exchange financing tequired (equivalent to 98.3% of the foreign com-ponent of the installed cost).

II. AN OVERVIEW OF THE CHINESE INDUSTRY

A. General Industry Background

2.1 Industry is China's largest productive sector, accounting for nearly47X of its Gross Domestic Product (GDP) and employing 18% of the total laborforce. About 97,600 state enterprises generate 62X of total industrial out-put, the remainder being produced by more than a million non-stateenterprises, mainly urban and rural collectives. While state enterprisesproduce mainly important raw materials, capital goods and strategiccommodities such as fertilizers, and light industrial and consumer goods, mostnon-state enterprises are involved in the production of downstream consumerproducts. Gross industrial output amouinted to Y 1,381 billion (US$371billion) in 1987. The chemical industry, which produces mainly fertilizers,petrochemicals and pharmaceuticals, accounted for 10% of the total industrialoutput.

2.2 The grois value of industrial production has grown rapidly !etween1978 and 1987, at a rate of over 10.8X in real terms per year. This growthreflects in large part the high rate of capital accumulation in industry.Until the late 1970s, when the Government began to view external trade as animportant element of economic development, Chinese industry was orientedmainly toward the domestic market. Since then, Chinese manufactured exportshave grown rapidly from around US$9 billion equivalent in 1980 to about US$26billion equivalent in 1987. The share of exports in industrial output was7.4Z in 1987.

2.3 China's industrial development has been constrained by several struc-tural deficiencies which stemmed mainly from rigid economic planning and thepast industrial strategies oriented towards self-sufficiency at the nationaland regional levels. Major deficiencies include outdated technologies,institutional rigidities stemming in part from quota and price controls, adistorted structure of prices, inadequate infrastructure, and an under-developed financial sector. Reflecting these problems, labor productivity andthe efficiency of resource use for Chinese plants are low. Nearly 80% of thecurrent capital stock is obsolete and needs replacement or technical renova-tion. The industry structure is biased toward basic, heavy industry. Anover-emphasis on self-sufficiency at the regional level has also led to afragmented national market, reduced domestic competition, and the suboptimaluse of scarce skills and resources. Consequently, potential gains from econ-omies of scale are often missed. Institutional inflexibility, compounded byinadequate market integration, has provided little incentives for industrial

enterprises to improve managerial efficiency and product quality. The lowprices of energy and basic intermediates for industrial production also con-tribute to the inefficient use of inputu. nvestments in infrastructure,particularly for transportation and telecomriunication, have lagged behindthose in industry. This in turn has posed a major constraint to industrialdevelopment. The financial markets, which are in their infancy, have untilrecently only provided limited intermediation services for enterprises.

B. Government Objectives and Strategy for Industrial Development

2.4 Since 1979, the Chinese Government has shifted the focus of indus-trial development towards light industry and introduced incentives and marketforces as a means of improving economic efficiency under ongoing economicreforms. The development strategy has emphasized modernization of existingequipment, development of manufactured exports and more efficient lightindustry, and material and energy conservation in industry. Price reforms,which the Government views as one of the most important elements of the on-going economic reforms, are designed to gradually reduce distortions toenhance allocative economic efficiency, particularly by allowing market forcesto play a greater role in price determination. Since the start of economicreforms, the prices of major industrial inputs, including energy, have beenraised significantly qo that effect. Recently the worries relating to theinflationary implications of these reforms have resulted in a cautiousapproach, and the reform process has been temporarily slowed at present.However, price reforms remain a critical item on the Government's reformagenda. Reforms adopted in 1984 aim to decentralize economic decision-makingtoward the provinces and enterprises, and make greater use of market signalsto provide production incentives. State enterprise reforms, which includeirT'roduction of the contract management responsibility system and, uniformprofit tax rates (55Z) and wage incentives, have provided greater autonomy andmore appropriate incentives for enterprise management. However, significantdistortions in relative prices still remain, and the objective of replacingthe traditionally "soft" enterprise budget constraint has yet to be achieved.Reforms in the financial sector have focused on reducing the role of centralplanning in the economy by increasing competition among existing and newfinancial institutions and the introduction of new types of financial instru-ments. The reforms are being implemented at different paces among the regionsand subsectors. Because of the nature and structure of the fertilizer sector,the process of decentralization has already progressed to a greater degreethan in some other industrial sectors.

C. Bank Support for Industry

2.5 The Bank Group's industrial lending operations in China began inDecember 1982 with the approval of a loan of US$70.6 million to finance theFirst China Investment Bank Project (Loan/Credit 2226/1313-CHA, FY83). Threeadditional loans/credits of US$575 million to the China Investment Bank (CIB)(Loan/Credit 2434/1491-CHA in FY84; Loan/Credit 2659/1594-CHA in FY86; andLoan/Credit 2783/1763-CHA in FY87) have been approved subsequently. The mainpurpose of the CIB operations has been to develop CIB as the premier financialintermediary providing term financing for small- and medium-sized enterprises.CIB operations to date have supported a wide range of subsectors, including:textile, light industry, electronics, food processing, pharmaceuticals, pack-

- 4 -

aging materials, machinery and spare parts, building materials, chemicals andmetallurgical, and other, in a number of provinces. Disbursementl of the CIBloans and cred..~s have, apart from some delays in the first operation, pro-ceeded satisfactorily. Altiuough CIB's manoower and system require furtherstrengthening, the basis of a sound development bank in China has been estab-lished.

2.6 Besides the four CIB operations, Bank involvement in the industrialsector comprisess (a) three fertilizer loans, totaling US$257.3 million (para.1.1); (b) a loan of US$100 million for the Shanghai Machine Tool Project (Loan2784-CHA, FY87), involving rehabilitation and modernization of the machinetool sector in Shanghai; (c) a loan of US$128 million for the PharmaceuticalsProject (Loan 2943-CHA, FY88), to expand pharmaceutical production usingmodern technologies and improve manufacturing practices; (d) a regionaldevelopment project for Gansu Province (Loan 2812-CHA, and Credit 1793-CHA,FY87), including an industrial development component of US$20 million, to beused for diversification and modernization of the predominantly rural indus-trial base in the province; and (e) a loan of US$154 million for the TianjinLight Industry Project (Loan 3022-CHA, FY89) to support the restructuring ofthree important subsectors (textile dyeing and finishing, pulp and paper, andpackaging) of the light industry in Tianjin Municipality. Physical implemen-tation of the three fertilizer projects is proceeding generally on schedule.A Planning Support and Special Studies Project, which includes components forsupporting long-term planning activities in selected subsectors includingpetrochemicals, was approved in June 1987. No Project Completion Reports(PCRs) have been prepared on any of the above projects. The InternationalFinancial Corporation (IFC) has provided support of US$44.3 million equivalent(equity participation of US$4.3 million and loans of US$40.0 million) sinceits first operation in 1985, through the following five investments:Guangzhou and Peugeot Automobile Co., Ltd. (Investment No. 813, FY85), ChinaInvestment Co., Ltd. (Investment No. 974, FY87), Shenzhen China Bicycles Co.,Ltd. (Investment No. 1020, PY87), Shenzhen Crown Electronics Co., Ltd.(Investment No. 1066, FY88), and Shenzhen Chronar Solar Energy Co., Ltd.(Investment No. 1119, FY89).

2.7 The Bank's overall objectives in support of China's industrialdevelopment are to assist the Government in: (a) improving the policy frame-work for the industrial sector as a whole; (b) building sound institutions andpractices for financial intermediation, subsector planning, project approvaland implementation; (c) promoting and implementing technology upgrading, plantrestructuring and rehabilitation, and energy and material conservation inselected sectors at the national and provincial levels; and (d) carrying outthe reforms needed in the financial system.

2.8 Specific plans include further support for both CIB and other finan-cial intermediaries and industrial enterprises in the overall sector reformnow under way, assistance to selected major subsectors at the national andprovincial levels: fertilizers, pharmaceuticals and machine tools, and thedevelopment of broad-based industrial lending operations at the provinciallevel, involving restructuring of major subsectors. The increasing devolutionof planning and implementation responsibility to the provinces has the poten-tial to have a significant impact on industrial development provided that theprovincial authorities can effectively formulate and carry out their new role.The anticipated series of provincial operations is designed to help selected

- 5 -

provinces articulate and implement their new responsibilities. The Bank'sprogram for economic and sectcr work in industry and finance has prov,ded thebasis for an active dialogue with the Government. Major studies completed sofar include those on the state enterprise management system, finance andinvestment, external trade and capital, and phosphate subsector planning.Further work is being carried out and is planned in such areas as tax reform,enterprise and financial reforms, and several subsector studies at thenational and provincial levels. This work is increasingly being carried outjointly with Chinese agencies.

2.9 The various reform measures introduced in recent years have expandedsignificantly the scope for non-state enterprises, mainly urban and ruralcollectives. The environment for foreign investment in China has alsoimproved significantly since the promulgation of the joint venture law in1979. Bank operations designed to assist the rapidly growing non-state sectorare contemplated. For example, assistance to the rural industrial sector isexpected through support for the Government's SPARK program, and CIB, hithertothe major beneficiary of Bank support for financial intermediation, isexpected to gradually expand its financing of non-state enterprises and jointventures. IFC support for the Chinese industrial sector has hitherto beenlimited to export-oriented joint ventures. With minor exceptions only, jointventures are required to earn their own foreign exchange to service foreignobligations, which in turn has tended to make it difficult for IFC to supportimport substituting joint ventures; most potential joint venture partners inChina are interested in the domestic market. As part of the ongoing economicand sector dialogue, both the Bank and IFC have proposed major changes in theforeigni exchange allocation and management system designed to alleviate thesedifficulties. The growing importance and role of the foreign exchange cen-ters, which were established recently in important trading cities and prov-inces, have the potential for alleviating this constraint.

III. THE FERTILIZER SECTOR

A. Agricultural Background

3.1 The agriculture sector in China employs some 190 million farmfamilies and accounts for about 34X of the country's GDP. Although it has ashortage of cultivatable land--only 102 of China's 960 million hectares (ha)is cultivated, compared with 75Z in India--China has achieved self-sufficiencyin its basic food requirements. That accomplishment is all the more remark-able given that China has 22% of the world's population but only 8% of itscultivated area. The reasor. for this success is intensive cultivation prac-tices, with relatively heavy inputs of labor, chemical and organic ferti-lizers, and water per unit of land. Foodgrains occupy about 70Z of the totalcultivated area. Cotton is the most important industrial crop.

3.2 The agricultural sector has performed exceptionally well since 1979,when the Government introduced a new agricultural incentive program, the"production responisibility system (PRS).n Reflecting these initiatives, thegross value of agricultural production increased by 10% p.a. over the period1980-86, compared to an average of 3% p.a. in the preceding 20 years. Majorchanges that have taken Dlace under the PRS include: (a) a larger role for

-6-

farm households, which now function as the fundamental units of agriculturalproduction and management; (b) replacement of the mandatory procurement quotawith voluntary contracts, which gives farmers more flexibility in determiningwhat to grow and where to sell; (c) price increases for major farm products;and (d) the introduction of some flexibility in prices for deliveries of cer-tain products by collectives and individual producers in excess of contractedtargets.

B. Fertilizer Use in Agriculture

3.3 While China is the third largest user of chemical fertilizers and thelargest consumer of nitrogen in the world, the level of fertilizer use in1985--167 kg of nutrients per hectare of culti"zated land--was still only abouta third of that in neighboring countries such as Japan and Korea (see Annex3.1 for a comparison with other countries). The implication is that thepotential for increased fertilizer use is large. Since expansion of the cul-tivated area is not feasible, increasing and more balanced fertilizer use willremain central to China's strategy for increased agricultural output.

3.4 At present, there is an imbalance in the use of nitrogen (N), phos-phate (P205) and potash (K20) fertilizers. China's low application of phos-phate and potash (para. 3.6) reduces the synergistic benefits that couldderive from the relatively high level of nitrogen application. This imbalanceis a major constraint to increasing the application of nitrogenousfertilizers. Compared with the application rates in the other countries givenin Annex 3.1, China's level of application of phosphate and potash fertilizersis quite low. According to results from surveys by the Ministry of Agricul-ture, Animal Husbandry and Fishery (MAAF) during 1981-83, the soil throughout73.4X of the cultivated area was deficient in phosphate, and 39.8X of it wasseriously deficient.

C. Fertilizer Demand and Supply

3.5 Table 3.A summarize the consumption, producti(n and importation ofchemical fertilizers from 1974 to 1986 and presents projections of these acti-vities for 1990 and 1995 (greater detail can be found in Annex 3.2).

TIb ..LA: O4INA - Q4EICAL tERTILIZER CONSUMPTION, PRODUCTION AND ISPOR, PAST AND PROJECtED L

('000 tons of nutrient)

Nitrooan Pho8shntbm 445).... PqoQsos h Total nutrient.

Cone.La Prod. Imp. Cono.zaa Prod. Imp. Cons.LN Prod. Imp. Con&./a Prod. Imp.

1072 3,168 2,444 1,342 1.038 1,249 11 12 8 2 4,219 3,701 1,S5S

1Q81 10,36S 9,868 1,641 2,785 2,508 499 281 24 2E0 13,349 12,390 2,290

1984 18,878 12,211 2,828 8,686 2,389 1.342 804 31 788 17,868 14,601 4,928

1988 18,477 11,438 2,052 3,531 1,760 960 920 24 364 17.898 18,222 3,866

1986 18,728 11,888 1,700 4,802 2,826 648 1,078 25 600 19,306 18,987 2,045

1990 (proj.)g 14.860 18,160 2,899 S,880 3,000 8,880 1,768 10 1,786 22,505 16.800 8.005

1995 (proj.)/d 16,400 lS,160 2,562 8,200 4,900 3,956 3,280 160 8,S92 27,880 20,200 9,910

_veran Annug

(trowth Rate (O)

1972-41 14.1 16.8 11.4 8.1 40.2 18.0 18.7 19.1

1972-6 11.0 11.8 11.0 - - - ll.8 9.9

1981-86 8.8 8.8 10.5 (1.4) 47.7 0.8 7.7 2.4

16 8.6 1.8 12.4 38.0 (2.8) 4.2 8.7 5.6

1986-95 2.0 8.5 6.9 10.7 18.2 22.0 4.2 -

L The consumption figures (sales to farmers) do not equal production plus imports because of distribution losses,

stock changes and some unrecorded imports.

L Actual phosphate fertilizer consumption figures include phosphate rock. directly applied without processing.

, Actual potash consumption figures appear to be overestimated because of atstieticsl Inconsistency.

Ld The projected Imports for the yesr4 1990, 1995 snd 2000 were darived from supply Caps between domestic production

and consumption, takino into account an S8 fertilizer lo"s in transit, storage and distribution.

Sources: Consumption data--Chins Agricultural Handbooks 1981-86, Agricultural Yearbook of China 1988 and KMAF;

production dats--MCI. and Food and Agriculture Organization (FAO); and trade data--General Administration of

Custom and FAD.

3.6 Fertilizer Demand. The consumption of all fertilizers increased from4.2 million tons per year of nutrients (tpyn) in 1975 to 19.3 million tpyn in1986, representing an average annual growth rate of 14.1Z. Growth in nitrogenconsumption, which increased at an average annual rate of 14.1Z during1972-81, has slowed in recent years, mainly because the level of nitrogenapplication is relatively high, especially compared to the use of phosphateand potash fertilizers, whose supplies are limited. The consumption ofphosphate and potash showed average growth rates of 11.0? and 37.91respectively,l/ during 1972-86; this coincides with the Government'scontinued emphasis on increasing their application to improve the overallnutrient balance.

1/ Potash consumption has grown very quickiy from its low base in theearly 1970s, but it is still very low.

3.7 China also has a long history of using organic fertilizer. This willcontinue to be a valuable source of nutrients and will complement furtherincreases in the use of chemical fertilizer. Total nutrients supplied byorganic fertilizers in 1986 are estimated at about 15 million tons.

3.8 Based on its agricultural targets, the Government has projected thatthe demand for chemical fertilizer will reach 27.9 million tpyn in 1995, withimplied average annual growth rates of about 2.0X for nitrogen (N) 6.9% forphosphorous (P205) and 13.2X for potassium (K20). These projections appear tobe somewhat conservative, based on the limited supplies of phosphate andpotash fertilizers. According to MAAF, ths desirable long-term target for theratio of these nutrients is 100:50:20, compared with a current ratio of100:33:8. GOC plans to achieve the target by 1995 by rapidly expanding theconsumption of phosphate and potash fertilizers. However, it may be difficultto satisfy these requirements owing to domestic raw material constraints forpotash and limited financial resources for investments and imports.

3.9 Fertilizer Supply. China has about 1,900 operating fertilizer plantsof varying types and sizes and is the world's third largest producer of chem-ical fertilizers after the USSR and the US. Chemical fertilizer productionincreased from 3.7 million tpyn in 1972 to 14.6 million tpyn in 1984, and thenfell to 13.2 million tpyn in 1985. In 1986, production reached 14.0 milliontpyn. Juring 1972-86, phosphate fertilizer production increased at a modestrate of 4.6%, while nitrogenous fertilizer production increased at the muchfaster rate of 11.82 p.a. For potash the figure was 8.5Z.

3.10 The decline in domestic production of both nitrogenous and phosphatefertilizers in 1985 was mainly due to the Government's decision to close some200 of the small, inefficient plants. These plants produced low quality, lownutrient fertilizers such as ammonium bicarbonate (ABC), single superphosphate(SSP), and calcium magnesium phosphate (CMP). The Government took this stepin response to diminishing demand for these fertilizers. Despite the aggres-sive buildup of capacity for high-grade fertilizers in recent years, a signi-ficant portion of the fertilizer production in China still is low grade: in1985, only 30% of nitrogen production and 2X of phosphate production involvedhigh-grade products such as urea (46% N), MAP (522 P205) and TSP (46% P205).

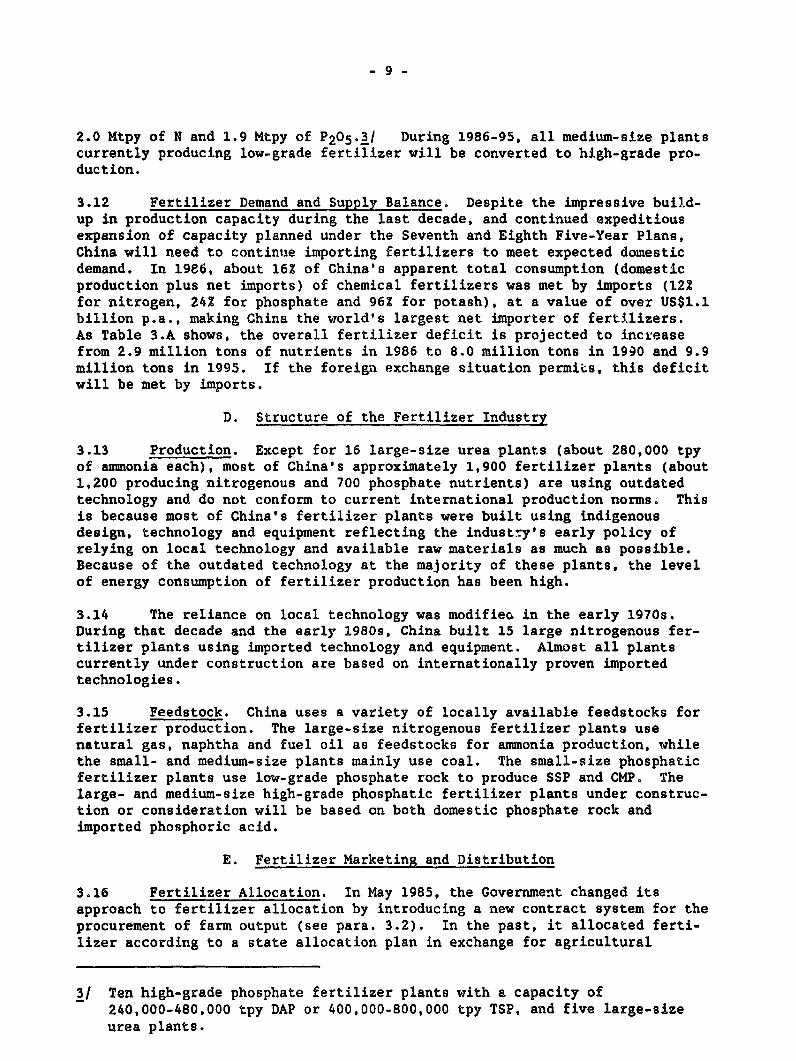

3.11 China plans to continue expanding its production capacity for chem-ical fertilizer, particularly high-grade phosphate fertilizer, during theSeventh and Eighth Five-Year Plan periods (1986-95). It also intends torationalize existing low-grade fertilizer production facilities, by convertingtheir products to high-grade fertilizers. New large- ard medium-scalefertilizer plants to be completed during the Seventh Five-Year Plan period 2/are expected to increase China's high-grade fertilizer production capacity byapproximately 1.2 Mtpy of N, 0.6 Mtpy of P205, and 0.1 Mtpy of K20. Projectsunder the Eighth Five-Year Plan, which is currently being formulated, areexpected to include further expansion in capacity for chemical fertilizers of

2/ Two 1,740 tpd urea plants, three 800 tpd DAP plants, a 400 tpd DAPplant, a 2,970 tpd nitrophosphate plant, a 500 tpd nitrophosphateplant, an 1,800 tpd NPK plant, a 500 tpd NPK plant, and 200,000 tpypotassium-chloride plant.

2.0 Mtpy of N and 1.9 Mtpy of P205.3/ During 1986-95, all medium-size plantscurrently producing low-grade fertilizer will be converted to high-grade pro-duction.

3.12 Fertilizer Demand and Supply Balance. Despite the impressive build-up in production capacity during the last decade, and continued expeditiousexpansion of capacity planned under the Seventh and Eighth Five-Year Plans,China will need to continue importing fertilizers to meet expected domesticdemand. In 1986, about 16% of China's apparent total consumption (domesticproduction plus net imports) of chemical fertilizers was met by imports (122for nitrogen, 24% for phosphate and 96Z for potash), at a value of over US$1.1billion p.a., making China the world's largest net importer of fertilizers.As Table 3.A shows, the overall fertilizer deficit is projected to increasefrom 2.9 million tons of nutrients in 1986 to 8.0 million tons in 1990 and 9.9million tons in 1995. If the foreign exchange situation permics, this deficitwill be met by imports.

D. Structure of the Fertilizer Industry

3.13 Production. Except for 16 large-size urea plants (about 280,000 tpyof ammonia each), most of China's approximately 1,900 fertilizer plants (about1,200 producing nitrogenous and 700 phosphate nutrients) are using outdatedtechnology and do not conform to current irternational production norms. Thisis because most of China's fertilizer plants were built using indigenousdesign, technology and equipment reflecting the industry's early policy ofrelying on local technology and available raw materials as much as possible.Because of the outdated technology at the majority of these plants, the levelof energy consumption of fertilizer production has been high.

3.14 The reliance on local technology was modifiec, in the early 1970s.During that decade and the early 1980s, China built 15 large nitrogenous fer-tilizer plants using imported technology and equipment. Almost all plantscurrently under construction are based on internationally proven importedtechnologies.

3.15 Feedstock. China uses a variety of locally available feedstocks forfertilizer production. The large-size nitrogenous fertilizer plants usenatural gas, naphtha and fuel oil as feedstocks for ammonia production, whilethe small- and medium-size plants mainly use coal. The small-size phosphaticfertilizer plants use low-grade phosphate rock to produce SSP and CMP. Thelarge- and medium-size high-grade phosphatic fertilizer plants under construc-tion or consideration will be based on both domestic phosphate rock andimported phosphoric acid.

E. Fertilizer Marketing and Distribution

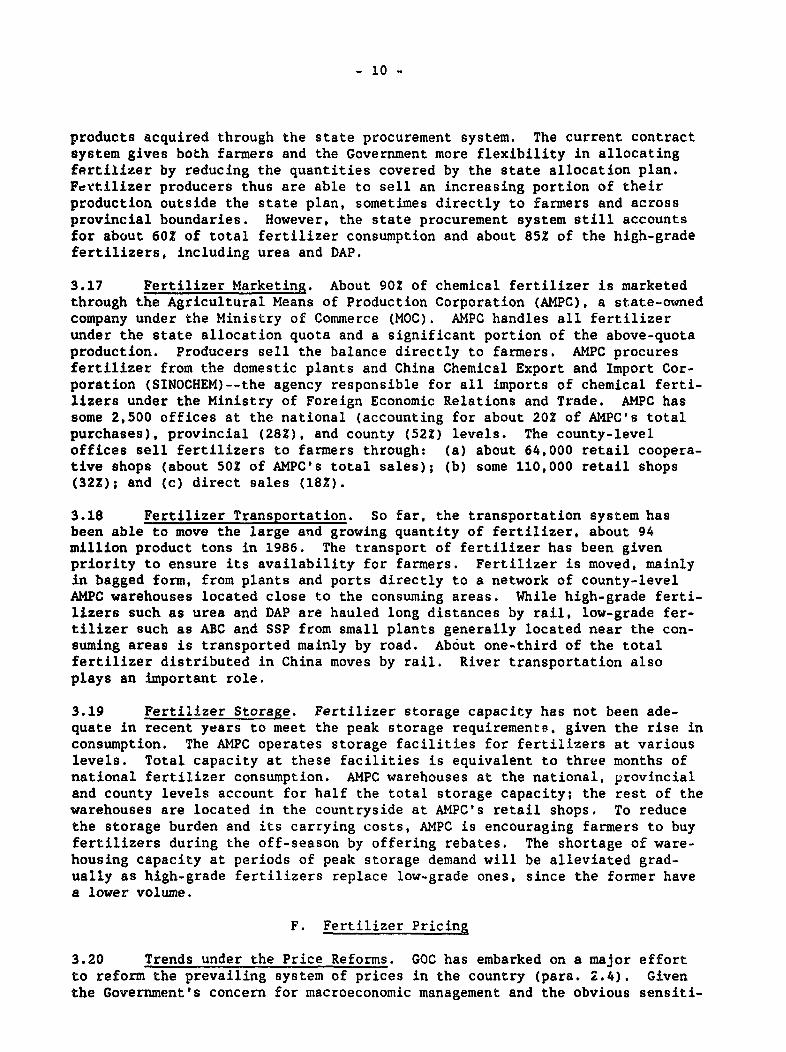

3.16 Fertilizer Allocation. In May 1985, the Government changed itsapproach to fertilizer allocation by introducing a new contract system for theprocurement of farm output (see para. 3.2). In the past, it allocated ferti-lizer according to a state allocation plan in exchange for agricultural

3/ Ten high-grade phosphate fertilizer plants with a capacity of240,000-480,000 tpy DAP or 400,000-800,000 tpy TSP, and five large-sizeurea plants.

- 10 -

products acquired through the state procurement system. The current contractsystem gives both farmers and the Government more flexibility in allocatingfertilizer by reducing the quantities covered by the state allocation plan.Fertilizer producers thus are able to sell an increasing portion of theirproduction outside the state plan, sometimes directly to farmers and acrossprovincial boundaries. However, the state procurement system still accountsfor about 60? of total fertilizer consumption and about 85Z of the high-gradefertilizers, including urea and DAP.

3.17 Fertilizer Marketing. About 90? of chemical fertilizer is marketedthrough the Agricultural Means of Production Corporation (AMPC), a state-ownedcompany under the Ministry of Commerce (MOC). AMPC handles all fertilizerunder the state allocation quota and a significant portion of the above-quotaproduction. Producers sell the balance directly to farmers. AMPC procuresfertilizer from the domestic plants and China Chemical Export and Import Cor-poration (SINOCHEM)--the agency responsible for all imports of chemical ferti-lizers under the Ministry of Foreign Economic Relations and Trade. AMPC hassome 2,500 offices at the national (accounting for about 202 of AKPC's totalpurchases), provincial (282), and county (52Z) levels. The county-leveloffices sell fertilizers to farmers through: (a) about 64,000 retail coopera-tive shops (about 50? of AMPC's total sales); (b) some 110,000 retail shops(32Z); and (c) direct sales (18Z).

3.18 Fertilizer Transportation. So far, the transportation system hasbeen able to move the large and growing quantity of fertilizer, about 94million product tons in 1986. The transport of fertilizer has been givenpriority to ensure its availability for farmers. Fertilizer is moved, mainlyin bagged form, from plants and ports directly to a network of county-levelAMPC warehouses located close to the consuming areas. While high-grade ferti-lizers such as urea and DAP are hauled long distances by rail, low-grade fer-tilizer such as ABC and SSP from small plants generally located near the con-suming areas is transported mainly by road. Ab6ut one-third of the totalfertilizer distributed in China moves by rail. River transportation alsoplays an important role.

3.19 Fertilizer Storage. Fertilizer storage capacity has not been ade-quate in recent years to meet the peak storage requirements. given the rise inconsumption. The AMPC operates storage facilities for fertilizers at variouslevels. Total capacity at these facilities is equivalent to three months ofnational fertilizer consumption. AMPC warehouses at the national, provincialand county levels account for half the total storage capacity; the rest of thewarehouses are located in the countryside at AMPC's retail shops. To reducethe storage burden and its carrying costs, AMPC is encouraging farmers to buyfertilizers during the off-season by offering rebates. The shortage of ware-housing capacity at periods of peak storage demand will be alleviated grad-ually as high-grade fertilizers replace low-grade ones, since the former havea lower volume.

F. Fertilizer Pricing

3.20 Trends under the Price Reforms. GOC has embarked on a major effortto reform the prevailing system of prices in the country (para. 2.4). Giventhe Government's concern for macroeconomic management and the obvious sensiti-

- 11 -

vities involved, the pace of reform inevitably will vary from sector to sectorand over time. Recently the Government has taken a cautious approach to over-all price reforms due to concerns about their inflationary implications (para.2.4). However, the overall direction of reform has been clearly set. Theongoing economic reforms involve expansion of the role of market forces infertilizer production and allocation. In the past, the Governmentadministered fertilizer prices strictly, as it did those of other essentialcommodities. The current strategy assigns a greater role to market forces infertilizer pricing and allocation so as to improve the efficiency of produc-tion and application. As a result, a two-tier pricing system has emerged.The State Pricing Bureau (SPB) and local (province, city and county) bureausset the prices for the production subject to the state plan quotas at both theex-factory and farm-gate levels. Market-influenced prices negotiated withinthe limits of guideline retail prices set by local pricing authorities prevailfor production outside the state plan quota.4/ Fertilizer producers marketthese products directly.

3.21 At present, about 402 of total consumption is sold at negotiatedprices, although the percentage varies significantly across products andlocalities and with the financial situation of individual manufacturers. Ingeneral, high-grade fertilizers are subject to stricter state allocation.About S5% of these products, including urea and DAP, are being sold at con-trolled prices under the state allocation plan.

3.22 The Government views the two-tier pricing system as an intermediatestep in the evolution of sectoral pricing policy, given its well-recognizedlimitations, including: (a) discrimination across producers and consumers;(b) administrative complexity; and (c) distortions and time lags in theadjustment of the prices of inputs and outputs. Despite these limitations,the Government expects to use this transitional system until it introduces abroader price reform package. The reason is partly the close inter-relationship between fertilizer and the agricultural sector and the potentialfor disruption if the allocation and pricing arrangements for fertilizers wereto be liberalized in isolation.

3.23 The Government's strategy is to continue gradually reducing itsadministrative control of fertilizer pricing in parallel with the gradualdismantling of annual production planning and allocation, so that the economycan "grow out of the plan." Guidelines for future policy reforms are beingdeveloped by an inter-agency working group that is carrying out a compre-hensive review of the fertilizer pricing and allocation policies according toa program discussed with the Bank. Through these reforms, GOC is committed toremoving the irrationalities in the price relationships between inputs, ferti-lizers and agricultural products. The working group is headed by the Directorof the Department for Heavy Industry and Communication and comprises repre-sentatives from related Government agencies, including the Ministry of Finance(MOF), MCI, MOC, MAAF and China Petrochemical Corporation (SINOPEC). However,

4/ At present, there is a ceiling on the negotiated prices of all high-grade fertilizers, such as urea and MAP, at the retail level. Thisceiling currently is set by the SPB, but in the future it will be setby provincial authorities following guidelines to be given by the SPB.

- 12 -

specific guidelines are expected to emerge only after the agenda for furtheroverall price reforms is firmly in place (para. 2.4).

3.24 Fertilizer Prices. The ex-factory prices of major high-grade fert-ilizers and ABC, the delivered prices of the main inputs, and farmers' pricesfor major grains, together with comparable international border prices in1988, are shown in Annex 3.3. Presently, the controlled ex-factory prices ofurea and DAP are below the border prices, while their negotiated prices areclose to the economic prices. In December 1988, the controlled bagged ureaprice--Y 428 (US$115)/ton--represented about 62% of the CIF import price ofUS$185/ton, while the ceiling for the nei iated price quota, which differsamong provinces and is set by respective provincial pricing authorities, was95-102Z of the economic value. For DAP, the figures are, for plan quota,Y 570 (US$153)/ton, equivalent to 67% of the current import parity price ofUS$229, and for the negotiated price, Y 700-860 (US$188-231), or 82-101Z. Atpresent, there is no local production of TSP and MAP, and controlled ex-factory prices therefore have not been established. The ceilings for nego-tiated prices for future TSP and MAP production are expected to be set in linewith those for DAP. The Government provides subsidies to make up the differ-ence between the import and sale prices for imported fertilizers. Actualnegotiated ex-factory prices have usually been equal or close to the ceiling;reflecting market conditions, these prices have frequently exceeded the ceil-ing, with approval from the pricing authorities, at least during the peakseason.

3.25 An average distribution margin of about Y 140 (US$38/ton of product)is added to the ex-factory price of high-grade fertilizer at the farm-gatelevel to cover AMPC's transport and storage costs.

3.26 During negotiations, an assurance was obtained from the Governmentthat the Project companies would be allowed to market their entire output (TSPand MAP) outside the state allocation plan at negotiated prices.

3.27 Prices of Fertilizer Inputs Relative to Fertilizers. The pricestructure of major inputs is also similar to that of fertilizers. However,there are no country-wide uniform prices for these inputs, and the controlledprices applied to individual suppliers are set by each supplier's respectivesupervisory pricing authority at the central, provincial and county levels.Although these prices vary to a large extent depending on the quality ofproduct and the location and geological condition of supply sources, on thewhole they are far below their border prices. The controlled price of naturalgas under the state allocation quota is around 55-65% of its fuel oil equiva-lent value, based on border prices. The controlled price of coal is 65-75Z ofits export value. The average ex-mine controlled price of domestic phosphaterock, the quality of which is usually too low to be tradeable in the inter-national market, is about 45% of the import parity price based on nutrientcontents. Negotiated prices above the quota are generally 15-25% higher thanthe controlled prices; although in some cases they have, subject to approvalby pricing authorities, approached border prices. The entire production ofphosphate concentrate from Wengfu mine, to be developed under the Bank-supported Phosphate Development Project (Loan 2958-CHA, FY88), will be allowedto be sold outside the state allocation plan at market influenced negotiatedprices.

- 13 -

3.28 Prices of Fertilizers Relative to Agricultural Products. The pricestructure of agcicultural products is similar to that of fertilizers. Agri-cultural products traded by the state procurement system are subject to con-trolledI prices. While some exceptions exist, the prices of these productsgenerally are below border prices, while the market-influenced negotiatedprices more closely approximate the border prices. For example, as of January1988, thR controlled price ef rice was Y 632 (UTS$167)/ton, about 65Z of itsexport value of US$258/ton, whereas its negotiated price was Y 840 (US$226)/ton (Annex 3.2). The controlled price of wheat was Y 328 (US$119)/ton, about682 of the CIF in.port price of US$1.75, the negotiated price, Y 500 (US$161)/ton.

G. Government SLrategy in the Fertilizer Sector

3.29 In view of its importance to agriculture, the fertilizer sector hasbeen, and will continue to be, a sector of high priority for the allocation ofinvestment resources. In recent years, the Government rei.erated thispriority on several occasions, including statements published by the StateCouncil, respectively, in September 1987 and September 1988.

3.30 The Government's main objectives in the fertilizer sector are tc:(a) achieve the desirable nutrient balance of 100(N): 5U (P205): 20 (K20) bythe end of the Eighth Five-Year Plan (1991-95) by rapidly expanding the pro-duction capacity for phosphate fertilizers based on domestic phosplhate rockand the development of domestic potash resources; and (b) move toward self-sufficiency in fertilizer production during the Ninth Five-Year Plan(1996-2000). Other priorities include the rationalization of low-gradefertilizer facilities through technical renovation, energy-saving measures andimprovement in product quality, and greater efficiency in enterpriseoperations through improvements in management efficiency.

3.31 The Government's strategy for sectoral investment during the SeventhFive-Year Plan envisages: (a) bringing on-line the newi fertilizer productioncapacity currently under constraction (see para. 3.11); (b) converting medium-size low-grade fertilizer plants to high-grade fertilizer proluction;(c) intensifying the exploitation and development of d3mestic phosphateresources, including seven large new phosphate mines and the expansion ofpyrite mining capacity; and (d) rationalization of many small-size low-gradefertilizer plants, including their conversion to high-grade operations usingadaptive technologies. At present, the Government does not contemplate anyinvestments in new small-size SSP or ABC plants.

3.32 During the Eigh-n and Ninth Five-Year Plans (1991-2000), Governmentstrategy will focus on further expanding phosphate fertilizer production capa-city. With the recent decentralization of project implementation responsi-bilities, State resources will be used mainly for phosphate fertilizer; thecentral Government will ntot initiate ary new nitrogenous fertilizer projectsand these will be implemented by the provincial authorities as necessary.This strategy is considered appropriate, given the nutrient imbalance in fert-ilizer use and China's endowment of phosphate rock.

- 14 -

IV. THE PHOSPHATE SUBSECTOR

A. World Phosphate Market

4.1 Consumption. World phosphate fertilizer consumption grew steadily inthe 1970s and 1980s except in 1985/86, when a decline of 2.62 from Zhe pre-vious year's consumption was registered. According to statistics published bvFAO, world consumption of phosphate fertilizers rose from 19.8 million tons ofP205 to 34.3 million tons during 1969/70 to 1984/85, at an annual average rateof 3.5Z. The decline in 1985/86 reflects the reduced application of ferti-lizers in several countries exporting agricultural products due to the record-low prices of grains and agricultural products in the international market.In 1986/87, world phosphate consumption rsbounded to 34.4 million tons ofP205, largely due to a rapid increase in consumption in the developing coun-tries. The 1987/88 consumption is estimated at 36.4 million tons of P205, oran increase of 5.82 from the previous year's consumption. World phosphateconsumption is projected by the Bank's International Economics Department toincrease at anL annual average rate of 2.7Z between 1987/88 and the year2000/2001. In 1986/87, the major consumers of phosphate fertilizers were theUSSR (24.3X of the world consumption), US (10.6Z), China (8.OZ), India (5.7z),Brazil (4.9Z), and France (3.9%).

4.2 Production. World production of phosphate fertilizers also grewsteadily, from 20.6 million tons of P205 in 1969/70 to 37.2 million tons in1984/85. In response to the trends in demand for phosphate fertilizers, worldphosphate production fell to 34.6 million tons in 1985/86, and rebounded to37.0 million toDs in 1986/87. In 1987/88, the world production level reachedan estimated peak of 38.3 million tons of P205. In 1986/87, the majorproducers of phosphate fertilizers were the USSR (22.9% of world production),US (22.0%), China (5.8%), India (4.62), Brazil (4.12), France (2.7Z), Tunisia(1.92) and Morocco (1.3Z). According to supply projections by theFAO/UNIDO/World Bank Fertilizer Working Group in May 1987, world phosphatefertilizer supply potential, which is derived from world nominal capacity inoperation and under constrution and country-specific operation rates, wasestimated at 36.8 million tons of P205 in 1986/87, and was expected to reach41.8 million tons by 1991/92, representing an annual average growth rate of2.4Z. A major increase in capacity is expected to ,take place in developingcountries, particularly in Morocco, Tunisia, Jordan, China and Egypt wheremajor raw materials are abundant. The recent worldwide trend is to locate newproduction facilities near phosphate rock mine sites.

4.3 International Trade and Market Prices. The international phosphatemarket is competitive; the two main exporting regions are North America andNorthern Africa and all other regions import. Phosphate fertilizer prices inthe world market, which fell sharply during the 1980-83 worldwide recessionand reached a record low in 1986, have increased steadily in recent years asworld demand particularly in developing countries recovered. While the worldmarket prices of phosphate fertilizers are not expected to increasesignificantly in the short run given the forecast movement in the agriculturalmarket and the industry's investment behavior, the recovery of these prices isexpected to continue gradually and steadily throughout the 19909. Fertilizer

- 15 -

production facilities to be established under the Project are expected to comeon stream in early 1994.

B. The Chinese Phosphate Industry

4.4 Although the domestic production and use of phosphate fertilizers hasincreased steadily over the last two decades, development of the phosphateindustry in China has been less spectacular than that of the nitrogenindustry. The main constraint has been technical difficulties in processingChinese rock, which has a high magnesium content, into concentrates suitablefor the production of high-grade fertilizers. Production of phosphate ferti-lizer therefore has been limited to low-grade products such as SSP and CMP atsmall provincial phosphate fertilizer plants. Accordingly, there was littleplanning or coordination of the development of the phosphate fertilizer indus-try at the state level. However, several years ago the Government shifted thepriority in the fertilizer .ector from nitrogenous to phosphate fertilizers,in order to correct the large imbalance in fertilizer use.

4.5 Domestic Phosphate Fertilizer Production. Recent trends in the pro-duction of phosphate fertilizers are summarized in Table 4.A below (furtherdetails are given in Annex 4.1). As of the end of 1987, almost all phosphatefertilizer production was low-grade, with SSP comprising more than 70Z and CMPmost of the balance. Domestic production of other phosphate fertilizers hasbeen insignificant--in 1985, ammonium phosphate production was only 7,000 tonsof P205, while the total capacity of the phosphoric acid plants was only about50,000 tpy of P205. About 400,000 tons of ground phosphate rock were alsobeing applied directly.

Table 4.A: PRODUCTION OF PHOSPHATE FERTILIZEPS, 1972-86('000 tons of P2 05 , Z)

SS? CMP Others /a TotalYear Volume I Volume Z Volume X Volume Z

1972 740 59.2 488 39.1 21 1.7 1,249 100.01981 1,780 71.0 692 27.6 36 1.4 2,508 100.01983 1,920 72.0 715 26.8 30 1.1 2,665 100.01984 1,683 71.3 644 27.3 32 1.4 2,359 100.01985 1,345 76.5 380 21.6 33 1.9 1,758 100.01986 1,713 73.7 558 24.0 54 2.3 2,325 100.0

Ja Ammonium phosphate productiont 3,000 tons in 1984, 7,000 tons in1985; the 1986 figure is not available.

Source: MCI

4.6 There are about 700 phosphate fertilizer plants in China, scatteredamong almost all the provinces (see Annex 4.2). The average output capacity

- 16 -

is 15,000-30,000 tpy, except for a few SSP plants that have capacities of morethan 100,000 tpy. Most of the production in each province is consumed withinits boundaries (Annex 4.3).

C. Supply of Raw Materials

4.7 The two main materials required for producing high-grade phosphatefertilizers are phosphate rock and sulfuric acid.

4.8 Phosphate Rock. China is well endowed with more than 3 billion tonsof phosphate rock (see Annex 4.4). The physical nature of the rock is similaracross deposits-- usually hard and with a high magnesium oxide (MgO) contentvarying from about 2.5-6.0Z. Until recently, when a new process for benefici-ating these rocks was developed in China, domestic rocks were not suitable forproducing high-grade phosphate fertilizers. Now, however, the Government isplanning several large new undertakings to exploit the major deposits of rock,particularly in Hubei, Guizhou and Yunnan Provinces. The Project will supportseveral such efforts. Recent exploration also indicates large rock resourcesin Sichuan Province.

4.9 Relative to the large size of the phosphate rock reserves, the cur-rent level of production is low, for the reasons given above. Annualproduction of phosphate rock in 1986 amounted to only 15 million tons of runof mine (ROM) rock, mainly in five provinces, as shown in Table 4.B. In 1986,most of this rock was used as ROM rock; only about 5X was beneficiated beforeuse.

Table 4.B: AVERAGE ANNUAL PHOSPHATE ROCK PRODUCTION BY PROVINCE, 1986('000 tons rock)

Yunnan Guizhou Hubei Hunan Sichuan Other Total

Production 3,264 2,484 5,460 1,090 2,953 294 14,957

Source: MCI.

4.10 Because the phosphate fertilizer plants are small and scatteredthroughout the country, phosphate rock is transported widely o-er China.Yunnan Province, for example, sends rock to 24 provinces, Guizhou to 18, andHubei to 19. The major importing provinces are Hubei, Liaoning, Jiangsu,Shandong and Guangxi. China imports a small quantity of rock (varying between0.2 to 0.3 Mtpy from year to year) for some plants near the coast. It alsoexports a small amount of phosphate rock under counter-trading arrangementswith other developing countries.

4.11 Sulfuric Acid. China's sulfuric acid consumption in 1986 was about7.6 million tons, of which about 5.0 million tons went for phosphate fertili-

- 17 -

zer production. China meets almost the entire demand for sulfuric acid domes-tically. About 1.5 million tons of acid comes from smelter gas, and almostall the remainder from pyrites; only a small amount comes from elementalsulfur.

4.12 The major deposits and mines of pyrites are located in Guangdong,Shanxi, Anhui, Liaoning, Hunan and Sichuan Provinces (Annex 4.5). The majorproducers of smelter acid are in Liaoning, Gansu and Hunan. China hasdiscovered sulfur deposits in Shandong Province, but attempts to exploit themhave not been successful. Little sulfur is recovered from the oil and gasindustry as most gas deposits are sweet.

4.13 The shortage of sulfur could inhibit development of the phosphateindustry unless new deposits of pyrites or sources of by-product sulfuric acid(e.g. phosphogypsum' are developed. GOC is avare of this possibility ancd. isestablishing a pilot plant in Yunnan to develop a process to recover sulfurfrom phosphogypsum.

D. Th? Phosphate Subsector Study

4.14 As mentioned earlier (para. 1.1 and 1.4), during Project preparationMCl and the World Bank carried out a joint Phosphate Subsector Study (theStudy) to help the Government identify appropriate strategies for developingan efficient domestic phosphate fertilizer industry. The main objective ofthe Study was to prepare an optimal investment program up to the year 2000that would allow China to meet its rapidly growing demand for phosphate fer-tilizers in the most economic wanner, given specified market requirements andtransport constraints.

4.15 The Phosphate Model. As part of the Study, the Bank designed acomputer-based mathematical programming model to facilitate review of theoptions, using data provided by MCI (see Annex 4.6 for the details). Themodel covers optimization of investment at the national level as well as ateach plant in terms of location, scale of operations, and level of productionin the context of the constraints associated with the transport of raw mate-rials, intermediates and final products. The selection of optimal strategieswas based on a comparison of different options and scenarios. The modelenabled the Government to review in a consistent and integrated manner themajor issues involved in developing the fertilizer industry, such as: (a)domestic fertilizer production versus importation; (b) optimal mode of trans-porting raw materials and finished products; (c) the location of new fert-ilizer production facilities; (d) the relative economics of producing dif-ferent types of phosphate fertilizers; and (e) priorities in developing thedifferent phosphate rock deposits. This model is being installed at MCI'sChemical Planning Institute (CPI) with technical and financial assistance fromthe Bank under the Phosphate Development Project (Loan 2958-CHA, FY88). Itwill be continuously updated to provide advice to planning and project imple-menting authorities on relevant subsector strategies.

4.16 The results of work with the model provided strong economic justifi-cation for development of China's domestic phosphate fertilizer industry,based on domestic raw materials. The analysis suggested that producing high-grade phosphate fertilizers such as TSP, DAP and MAP near the rock sources in

- 18 -

Yunnan, Guizhou and Hubei Provinces can be more economic than relying onimports. Construction of small DAP plants that use adaptive technology andlocal raw materials also will help China meet its phosphate requirements.

E. Investment Program for the Phosphate Subsector

4.17 To meet its agricultural production targets by the year 2000 withbalanced use of the three main fertilizer nutrients, China will have toincrease its phosphate consumption to about 9.1 million tons of P205 from itscurrent level of 4.5 million tons. 'f most of the presently known economicdeposits are fully developed by that time, China could increase domestic pro-duction from the 1986 level of 2.3 million tons of P205 to 9.0 million tons.This development would necessitate an increase in phosphate rock productionfrom about 11 to 35 million tpy of rock and in sulfuric acid from about 8 tomore than 20 million tons. Total related investment costs for the productionfacilities are estimated at about US$8-10 billion in 1988 prices, excludingthe large Investment required to upgrade the infrastructure to transport rawmaterials to the processing units and to distribute the final products to themarketplace.

4.18 During the Seventh Five-Year Plan, five large new phosphate rockmines and many small local mines are to be developed (the Wengfu mine inGuizhou, one mine in Yunnan, and three mines in Hubei). Output at the largepyrites mines in Guangdong, Meimonggol, Hunan and Anhui will be greatlyincreased to meet the demand for sulfuric acid. These local raw materialswill feed the new high-grade phosphate fertilizer plants to be implementedduring the Seventh and Eighth Five-Year Plan periods. Three DAP plants willbe implemented based on imported phosphoric acid. About 50 small SSP plantswill be revamped to produce DAP using adaptive technology, a move that willallow them to utilize relatively low-grade phosphate rock. During the Eighthand Ninth Five-Year Plans (1991-2000), the Government intends to fully expioitthe domestic phosphate resources to produce a total of 35 Mtpy of phosphaterock (30Z P205 basis) and 9.0 Mtpy of phosphate fertilizers (10O P205) by theyear 2000. Details of specific investments in the phosphate subsector up tothe year 2000, estimated on the above basis, are given in Annex 4.7.

F. Bank Role and Project Justification

4.19 In support of the Government's efforts to implement its stracegies inthe fertilizer sector (paras. 3.28-3.31), the Bank's main role is to providetechnical and financial assistance in: (a) strengthening GOC's capability forinvestment planning based on modern planning techniques, in order to optimizeinvestments in the sector, especially those for phosphate and potash fertili-zer; (b) assessing specific projects using suitable methodologies, includingthe selection of appropriate technologies; (c) building new fertilizer produc-tion capacity, as well as renovating existing facilities, particularly forphosphate and potash fertilizers; (d) enterprise-level restructuring andupgrading the efficiency of fertilizer distribution so as to reduce fertilizerlosses during distribution; and (e) improving the managerial efficiency ofsector companies through the introduction of modern enterprise-level manage-ment systems.

- 19 -

4.20 The two previous Bank-assisted nitrogenous fertilizer projectssupported China's priority objective during the early part of the SeventhFive-Year Plan (1986-90), which has been given to improving the technical andmanagerial efficiency of existing fertilizer plants. Most of the existinglarge- and medium-size fertilizer plants, including the large ones built withinternationally proven technologies in the 1970s, do not use up-to-date tech-nologies and require major investments to improve energy and production effi-ciencies. The first project (Fertilizer Rehabilitation and Energy SavingProject, Loan 2541-CHA, FY85), which was physically completed on schedule bythe end of 1988, provided financial assistance for improvements in efficiencyat one medium-size and four large nitrogenous fertilizer plants. The secondproject (Fertilizer Rationalizaton Project, Loan 2838-CHA, FY87) providesfinancial assistance both to upgrade the operations of five medium-size nitro-genous fertilizer plants, including conversion of their products to high-gradeones, and to introduce modern enterprise-level management systems in the fer-tilizer industry overall. Implementation of th.a project is proceeding welland on schedule. An IDA-financed technical credit also was provided tosupport project preparation, including tests of the phosphate rock and feasi-bility studies for the Project.

4.21 The Project, together with the third fertilizer project (the Phos-phate Development Project, Loan 2958-CHA, FY88), supports China's priority inthe fertilizer sector during tine Seventh and Eighth Five-Year Plans (1986-95),which is to reduce the nutrient imbalance in fertilizer use by rapidly expand-ing the production capacity for high-grade phosphate products. At the sametime, the process of project preparation has provided an opportunity to intro-duce modern subsector planning techniques and methodologies to the phosphateindustry and to help GOC articulate an optimal strategy for developing thesubsector. MCI's involvement in the joint phosphate subsector study hasstrengthened its subsector planning capability. The experience and metho-dologies learned from the Study also can be applied to other subsectors, aprocess in which the Chinese Government has already expressed an interest. Afurther innovation of this Project is the integrated development of phosphatemines and high-grade fertilizer complexes, the largest and most complex ofsuch operations in China to date. This effort will provide China with theexperience needed to implement similar other investments, which already havebeen identified in the Study. The technical assistance component is designedto ensure successful Project implementation.

V. PROJECT INSTITUTIONS

5.1 The Hubei Phosphate Project involves: (a) Jinxiang Phosphate Chemi-cal Company (JPCC), Hubei Province, which will carry out the Dayukou mine andfertilizer development component (paras. 6.3-6.4, 6.6); (b) Huangmailing Phos-phate Chemical Company (HPCC), Hubei Province, which will carry out the Huang-mailing mine and fertilizer development component (paras. 6.5-6.6); and (c)MCI, which will coordinate Project execution by the Project companies andimplement the technical assistance component (paras. 6.7-6.10). The opera-tional, managerial and organizational aspects of these institutions arereviewed in this chapter, while the financial aspects are reviewed in ChapterIX.

- 20 -

A. Background

5.2 Chinese chemical fertilizer companies and phosphate mines are state-onmed but operate as financially and administratively independent entities.In the past, the administrative, production, ma:ketiDg and financial opera-tions of these companies were under the direct supervision of the provincialgovernments. However, their autonomy in th'eir business decisions has beenexpanding, and is expected to continue doiag so, under the ongoing economicreforms. Large-size companies already enjoy wide autonomy in almost allaspects of their operations. The project companies have been registered withtheir respective provincial authorities to provide them with the status oflegal entities. Charters of the project companies describe the scope of theiractivities, responsibilities and authority in the conduct of business.

5.3 Organization and Management. The organization and management prac-tices of Chinese state-owned industrial enterprises reveal strong similar-ities. Their organization is basically flat--there are numerous unit work-shops and departments with their own management layers, all at the same organ-izational level. A general manager, appointed by the supervisory government,heads each company. Under the general manager are the second-layer managers,twho share functional responsibilities related to procurement and sales,administration, production, maintenance and construction. A chief engineer,also second-layer, is charged with all technical matters, including develop-ment and renovation. A chief accountant has a similar position in the area offinancial matters.

5.4 This structure has not promoted contemporary standards of organiza-tional and managerial efficiency, such as adequate scope of control,functional distribution of responsibilities among line managers, and adequatemanagerial and financial autonomy. The Government (SPC, MCI and the localGovernments) has been setting annual production targets, allocating inputs,distributing output, and allocating funds from budgets. Some managers, parti-cularly those responsible for production, have been overloaded with super-visory responsibilities. Horizontal coordination among various departmentsand workshops is not satisfactory. Because of insufficient autonomy, goodmanagement information and cost management systems do not exist.

5.5 Recent Management Reforms. Under the recent economic reforms,Chinese fertilizer companies have received increasing management autonomy.One result, however, is that there is now a two-tier planning and managementsystem. The state plan mandates a basic minimum level of activity, but beyondthat level each company is free to operate in response to market forces underits own flexible plan. Companies can make their own decisions regarding pro-duction levels, procurement of raw materials, sales of products above thequota, and utilization of funds generated by those sales, within the contextof the flexible plan. Although state planning for the fertilizer sector isexpected to continue in the near future, the scope for flexible planning andmanagement is to expand further, providing greater autonomy to management.

5.6 MCI recognizes the strong need to restructure the organization andmanagement of the chemical fertilizer companies so that they can effectivelycarry out their mandates for organizational change. This reatructuring can be

- 21 -