for live program only form 5471: preparing schedule c

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:-On the web, use the Chat function to send a message

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Form 5471: Preparing Schedule C Income Statement and Schedule F Balance SheetTHURSDAY, AUGUST 5, 2021, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound QualityWhen listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, please e-mail [email protected] so we can address the problem.

Recording our programs is not permitted. However, today's participants can order a recorded version of this event at a special attendee price. Please call Customer Service at 800-926-7926 ext.1 or visit Strafford’s website at www.straffordpub.com.

FOR LIVE EVENT ONLY

August 5, 2021

Form 5471: Preparing Schedule C Income Statement and Schedule F Balance Sheet

Anthony V. Diosdi

Partner

Diosdi Ching & Liu, LLP

Alison N. Dougherty, J.D., LL.M., CPA

Partner

Aronson LLC

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

Alison N. Dougherty, J.D., LL.M., CPA

Partner

Aronson LLC

Rockville, Maryland USA

Washington, DC Metro Area© 2021 | All Rights Reserved | Alison N. Dougherty |

6

Form 5471: Preparing Schedule C Income Statement and Schedule F Balance SheetOvercoming Challenges with Functional Currency,

U.S. GAAP Presentation, andTranslation Adjustments

August 5, 2021

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations,

Schedule C Income Statement and Schedule F Balance Sheet

7

Presentation Outline

I. Form 5471 OverviewII. Schedule C Income StatementIII. Schedule F Balance SheetIV. Best Practices

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations,

Schedule C Income Statement and Schedule F Balance Sheet Overview

8

The December 2017 U.S. federal tax legislation in the Tax Cuts and Jobs Act (P.L. 115-97 12/22/2017) brought significant changes to U.S. federal international tax provisions in the Internal Revenue Code.

Consequently, the IRS substantially revised the 2018, 2019, and 2020 Form 5471 and many of the required schedules including the Schedule C income statement and the Schedule F balance sheet.

© 2021 | All Rights Reserved | Alison N. Dougherty |

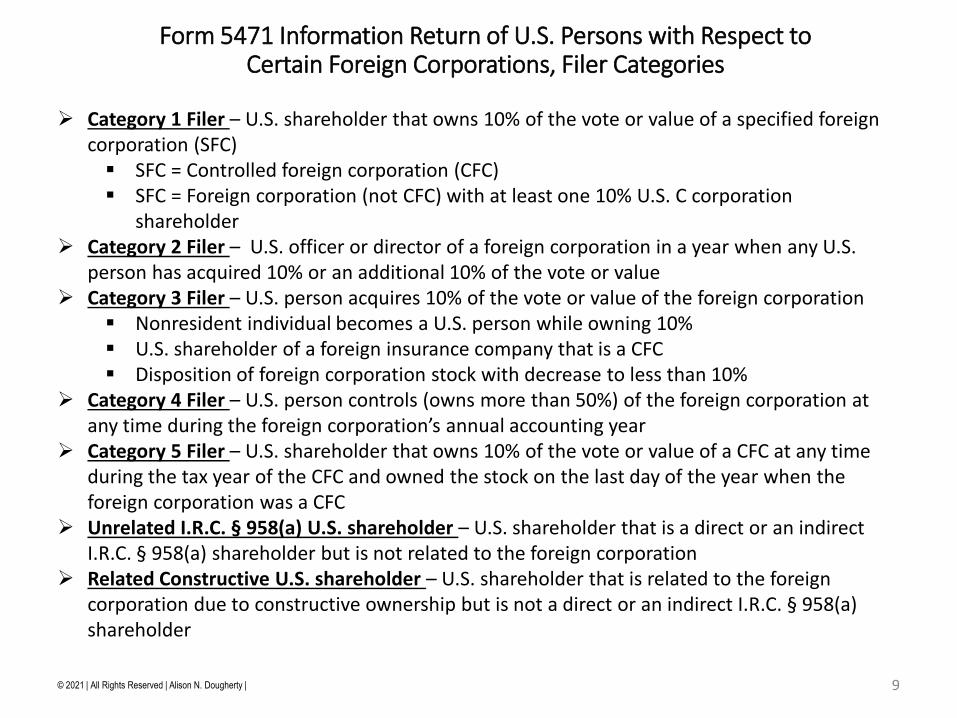

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Filer Categories

9

Category 1 Filer – U.S. shareholder that owns 10% of the vote or value of a specified foreign corporation (SFC) SFC = Controlled foreign corporation (CFC) SFC = Foreign corporation (not CFC) with at least one 10% U.S. C corporation

shareholder Category 2 Filer – U.S. officer or director of a foreign corporation in a year when any U.S.

person has acquired 10% or an additional 10% of the vote or value Category 3 Filer – U.S. person acquires 10% of the vote or value of the foreign corporation

Nonresident individual becomes a U.S. person while owning 10% U.S. shareholder of a foreign insurance company that is a CFC Disposition of foreign corporation stock with decrease to less than 10%

Category 4 Filer – U.S. person controls (owns more than 50%) of the foreign corporation at any time during the foreign corporation’s annual accounting year

Category 5 Filer – U.S. shareholder that owns 10% of the vote or value of a CFC at any time during the tax year of the CFC and owned the stock on the last day of the year when the foreign corporation was a CFC

Unrelated I.R.C. § 958(a) U.S. shareholder – U.S. shareholder that is a direct or an indirect I.R.C. § 958(a) shareholder but is not related to the foreign corporation

Related Constructive U.S. shareholder – U.S. shareholder that is related to the foreign corporation due to constructive ownership but is not a direct or an indirect I.R.C. § 958(a) shareholder

© 2021 | All Rights Reserved | Alison N. Dougherty |

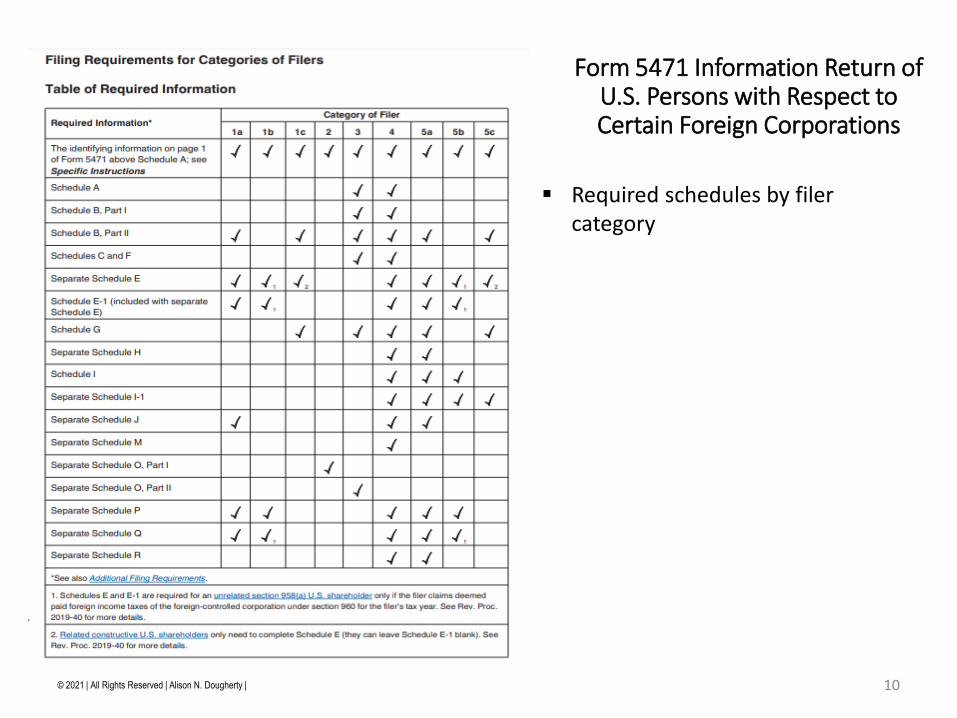

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations

10

Required schedules by filer category

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations,

Filer Categories Required to File Schedules C and F

11

Category 1 Filer – Schedules C and F not required Category 2 Filer – Schedules C and F not required Category 3 Filer – Schedules C and F are required Category 4 Filer – Schedules C and F are required Category 5 Filer – Schedules C and F not required Unrelated I.R.C. § 958(a) U.S. shareholder – Schedules C and F not required Related Constructive U.S. shareholder – Schedules C and F not required

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Reporting and Tax Years

12

All Form 5471 schedules except for information contained on Schedule O, report information for the tax year of the foreign corporation that ends with or within the tax year of the U.S. filer.

For Category 2 and 3 Filers of Schedule O - Report acquisitions, dispositions, and organizations or reorganizations that occurred during the U.S. filer’s tax year.

I.R.C. § 898 specified foreign corporation (SFC) - The annual accounting period of an SFC (including a CFC) generally is required to be the tax year of the corporation's majority U.S. shareholder. If there is more than one majority U.S. shareholder, the required tax year will be the tax year that results in the least aggregate deferral of income to all U.S. shareholders of the foreign corporation.

Different constructive ownership attribution rules apply in determining different Form 5471 filer categories (i.e., Category 3, 4, and 5 filers).

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations,

Page One

13

All filer categories complete page one

Filer information Foreign corporation information Filer Categories Tax Year Filing on behalf of others U.S. or foreign agent Custodian of books and records Category 3 and 4 filers complete

Schedule A stock issued and outstanding

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, The Importance of Schedule C Income Statement

14

Why is the Form 5471 Schedule C important?

U.S. GAAP book net income or loss is reported in retained earnings on the Schedule F balance sheet

U.S. GAAP book net income or loss flows to Schedule H as a starting point for calculating current year earnings and profits (CEP) with adjustments

U.S. GAAP book net income or loss flows from Schedule C to Schedule H CEP and then to Schedules J and P for CEP and previously taxed earnings and profits (PTEP) reporting

U.S. GAAP book net income or loss from Schedule C is the starting point in calculating IRC section 951A GILTI on Schedule I-1 that flows to the Form 8992 to report GILTI

Schedule C income statement will reflect items of Subpart F income that flows to Schedule I and to Schedules J and P for PTEP reporting

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement and Schedule F Balance Sheet

15

U.S. GAAP presentation considerations on Schedules C and F Revenue and expense recognition Recording assets and liabilities Measurement and classification Accounting methods and estimates Translation of functional currency to reporting currency

Form 5471 variances from U.S. GAAP FX translation gain or loss in Other Comprehensive Income (OCI)

reflected on Schedule C income statement instead of in equity section on the Schedule F balance sheet More of a Comprehensive Income presentation

with Net Income and OCI Form 5471 instructions require conversion of foreign currency to

USD based on the divide convention instead of the multiplication convention which is customary for U.S. GAAP Consistency with U.S. federal tax rules

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement

17

Filer categories 3 and 4 complete Schedule C

U.S. GAAP presentation in functional currency

U.S. GAAP translation to USD Schedule C Dec. 2020 revision same

as Dec. 2019 revision

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement

18

Schedule C income statement must be presented in accordance with U.S. GAAP Translation and FX conversion are based on U.S. GAAP consolidation rules Are the foreign corporation’s financial statements in the functional currency? Functional currency = the currency of the primary economic environment in

which the foreign corporation operates (ASC 830) Functional currency is generally the currency in which cash is received and paid Translation (current rate) method to convert foreign corporation’s functional

currency to U.S. parent company’s reporting currency Remeasurement (temporal) method to convert from foreign corporation’s

foreign currency that is not the functional currency to the foreign corporation’s functional currency and then follow translation to the U.S. parent’s reporting currency

Remeasurement (temporal) method to convert from foreign corporation’s foreign currency that is not the functional currency to the U.S. parent’s reporting corporation that is the same as the functional currency

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement

Translation (Current Rate) Method

19

Translation (current rate) method - Functional currency converted to reporting currency

Income statement - all items converted at weighted average exchange rate Current year net income converted at weighted average rate reported in

retained earnings Balance sheet – Assets and liabilities converted at year end exchange rate Common stock and APIC – converted at historical rate FX translation gain or loss – Report in Other Comprehensive Income (OCI) U.S. GAAP presents OCI in Accumulated Other Comprehensive Income in equity

section on the balance sheet Form 5471 shows the FX translation gain or loss in OCI on the income statement Form 5471 balance sheet does not reflect AOCI as identifiable component of

equity Query: Will the Form 5471 balance sheet balance?

Report the FX translation G/L plug in APIC? Report the FX translation G/L in net income and retained earnings?

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement

Remeasurement (Temporal) Method

20

Remeasurement (temporal) method – Convert foreign corporation’s financial statements to functional currency

Balance sheet – Convert monetary items at the year end exchange rate Monetary items = cash, A/R, notes receivable, bond investments, A/P,

notes payable, bond liabilities Balance sheet – Convert nonmonetary items at the historical exchange rate

Nonmonetary items = Marketable securities investments, inventory, equity method investment, PPE, A/D, preferred and common stock equity

Income statement – Convert items not relating to the balance sheet at the weighted average rate

Income statement – Convert items relating to the balance sheet at the historical exchange rate COGS, depreciation, amortization

FX remeasurement gain or loss – Report in income statement in calculating net income

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule C Income Statement

21

Schedule C notable items Line 8 realized and unrealized foreign currency transaction gain and loss Line 14 depreciation Line 16 taxes excluding income tax Line 20 unusual or infrequently occurring items Line 21 current and deferred income tax expense and benefit Line 23a foreign currency translation adjustments Line 23c income tax related to OCI Line 24 other comprehensive income or loss (OCI)

Special rules for Dollar Approximate Separate Transactions Method (DASTM) for hyperinflationary currency

Report local hyperinflationary currency amounts in functional currency column

Reflect adjustments for DASTM under Reg. § 1.985-3 on Schedule H to reflect difference in USD U.S. GAAP book net income and CEP calculated based on U.S. tax principles

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Non-U.S. GAAP Accounting Frameworks

22

Non-U.S. GAAP Special Purpose Accounting frameworks Other Comprehensive Basis of Accounting (OCBOA)

Cash basis Modified cash basis Income tax basis Regulatory basis Contractual basis

Non-U.S. GAAP Other Country Accounting Frameworks International Financial Reporting Standards (IFRS) Foreign country accounting principles

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Non-U.S. GAAP Accounting Frameworks

IFRS to U.S. GAAP

23

IFRS to U.S. GAAP Revenue and expense recognition

Convergence of IFRS and GAAP revenue recognition steps Some differences

Recording of assets and liabilities Measurement and classification Valuation and revaluation Impairment and reversal of losses Intangible and fixed assets Inventory

Methods (IFRS does not allow LIFO) IFRS allows write down reversals

Leases Deferred tax accounts

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Non-U.S. GAAP Accounting Frameworks

Cash Basis to U.S. GAAP Accrual

24

Cash basis income statement: Statement of Cash Receipts and Disbursements Cash received Cash paid

Cash basis balance sheet: Statement of Cash and Equity Assets: Cash Liabilities: Not presented Equity: Equals cash

Accrual basis income statement Apply methodologies to convert from cash basis to accrual revenue,

COGS, operating expenses, and net income Revenue realized and earned Expense incurred

Accrual basis balance sheet Assets: Current, noncurrent, and other assets Liabilities: Current and long-term liabilities Equity: Preferred stock, common stock, APIC, retained earnings, AOCI,

and treasury stock

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Best Practices

25

Review direct, indirect, and constructive ownership of foreign corporation each year to determine the impact of any changes in percentages, filer categories, and CFC status

Refer to the chart with the filing requirements to make sure that all required schedules are attached when preparing and reviewing the Form 5471

Prepare and maintain workpapers each year for U.S. GAAP adjustments and FX translation of foreign corporation’s financial statements

Account for any adjustments to prior year ending balances and current year beginning balances of AEP and PTEP on Schedules J and P

Consider interdependence of Form 5471 data with other U.S. international reporting forms (e.g., Form 8992 GILTI, Form 8993 I.R.C. § 250 GILTI deduction, Form 926 transfers to foreign corporations, Form 8938 foreign asset reporting, FBAR, etc.)

Coordinate with a U.S. international tax reporting specialist to ensure accurate preparation and review to mitigate risk of penalties

File the Form 5471 on time with the U.S. filer’s U.S. federal income tax return by the original orvalid extended due date

Always be mindful of Form 5471 penalties $10,000 penalty for failure to file substantially complete and accurate Form 5471 on time Additional $10,000 continuation penalty for each 30 day period that noncompliance continues more

than 90 days after IRS sends notice up to $50,000 maximum penalty Understatement penalties relating to foreign asset disclosures Criminal penalties

Address and remediate prior year noncompliance Consider available IRS amnesty procedures in filing prior year Forms 5471 late or not substantially complete

© 2021 | All Rights Reserved | Alison N. Dougherty |

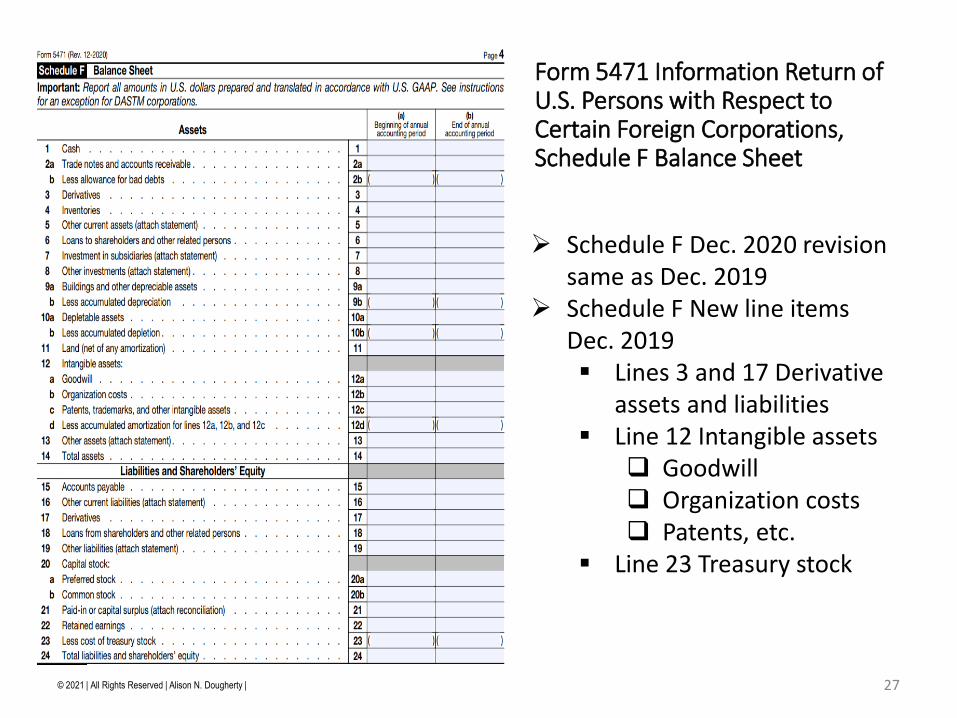

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule F Balance Sheet

26

Category 3 and 4 filers complete Schedule F Balance Sheet

© 2021 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule F Balance Sheet

27

Schedule F Dec. 2020 revision same as Dec. 2019

Schedule F New line items Dec. 2019 Lines 3 and 17 Derivative

assets and liabilities Line 12 Intangible assets

Goodwill Organization costs Patents, etc.

Line 23 Treasury stock

28© 2021 | All Rights Reserved | Alison N. Dougherty |

ALISON N. DOUGHERTY, J.D., LL.M., CPAPartnerAronson LLCAlison N. Dougherty provides tax services as a Partner at Aronson LLC. She specializes inU.S. international tax reporting, compliance, consulting, planning, and structuring. She is atechnical subject matter leader of Aronson’s international tax services practice area. She hasextensive experience assisting clients with U.S. tax reporting and compliance for offshoreassets and foreign accounts. She provides outbound U.S. international tax guidance to U.S.individuals and businesses with activities in other countries. She also provides inbound U.S.international tax guidance to nonresident individuals and foreign businesses with activitiesin the United States. She has worked extensively in the area of U.S. international taxreporting and compliance with the preparation and review of the U.S. Federal Forms 5471,8992, 8993, 926, 8865, 8858, 5472, 1042, 1042-S, 8621, 8804, 8805, 8813, 8288, 8288-A,8288-B, 1116, 1118, 1120-F, 1040-NR, 3520, 3520-A, 2555, 5713, 8832, 8833, 8840, 8843,8854, 8938, and FBAR. She has counseled U.S. taxpayers regarding the outbound formation,capitalization, acquisition, operation, reorganization, and liquidation of foreign companies.She has advised on the inbound structuring and related U.S. tax consequences of U.S.businesses owned by nonresident individuals and foreign companies. She has significantexperience with U.S. Federal nonresident withholding tax, foreign partner withholding tax,and FIRPTA withholding tax. She has assisted U.S. taxpayers with IRS amnesty programdisclosures of offshore assets and foreign accounts. Alison is responsible for tax servicesclient engagements for U.S. taxpayers including U.S. C corporations, S corporations,partnerships, individuals, and foreign companies.

Alison is a tax attorney and a CPA with more than 11 years of experience working in publicaccounting with a focus on international tax services for businesses and individuals. Alisonpracticed law as a corporate tax attorney and she worked as a tax manager in corporateindustry prior to joining Aronson in 2010.

Alison is a student in the online Bachelor of Science degree program in Computer Sciencewith concentration in Software Engineering at Southern New Hampshire University. Shecompleted online graduate level accounting courses at SNHU to earn academic creditsrequired for the CPA exam. Alison completed the AICPA U.S. International Tax Certificate in2021 with 48.5 CPE credits earned in 12 international tax courses. She completed the LL.M.(Master of Laws) in Securities and Financial Regulation in 2004 with academic distinction atGeorgetown University Law Center. She completed the LL.M. (Master of Laws) in Taxationin 2000 and the Juris Doctor in 1999 at the University of Denver College of Law. Shecompleted a Bachelor of Arts degree in Foreign Language in 1995 at Virginia CommonwealthUniversity.

(301) [email protected]

Aronson LLC111 Rockville Pike Suite 600Rockville, Maryland 20850 USAWashington, DC Metro Area

Form 5471: Preparing Schedule C Income Statement and Schedule F Balance Sheet

30

August 5, 2021Anthony V. Diosdi, Diosdi Ching & Liu, [email protected]

PURPOSE OF FORM 5471

Form 5471 is used by certain U.S. persons who are officers, directors, or shareholders of foreign entities that are classified as corporations for U.S. tax purposes. The schedules of Form 5471 are used to satisfy the reporting requirements of the Internal Revenue Code. Schedule F of Form 5471 requires the shareholders of a foreign entity classified as a controlled foreign corporation (“CFC”) to prepare a balance sheet for the entity. The balance sheet of the foreign corporation should be prepared and translated in accordance with the U.S. GAAP.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 31

WHO MUST COMPLETE FORM 5471 SCHEDULE F

There are five categories of U.S.persons that are required to complete a Form 5471 for each tax year. Whether or not a filer is required to complete Schedule F depends on what category of filer he or she can be classified. For purposes of Form 5471 Schedule F, Categories 3, 4, and 5 must complete and attach Schedule F to their Form 5471.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 32

WHO MUST COMPLETE FORM 5471 SCHEDULE F

Category 3- A US person who (a) has acquired a cumulative ten percent or greater ownership in the outstanding stock of the foreign corporation, (b) since the last filing of Form 5471 has acquired an additional ten percent or greater ownership in such stock, (c) owns ten percent or greater of the value of the outstanding stock of the foreign corporation when it is reorganized, or (d) disposes of sufficient stock in the foreign corporation to reduce the value of his ownership of stock in that corporation to less than ten percent, or who becomes a US person while owning ten percent, or who becomes a US person while owning ten percent or greater in value of the outstanding stock of the foreign corporation.

Category 4- a US person who had “control” of a foreign corporation for an uninterrupted period of at least 30 days during the foreign corporation’s annual accounting period. Control means more than 50 percent of the voting power or value of the CFC applying the Section 958 attribution rules.

Category 5- A US person who is a ten percent or greater shareholder in a corporation that was a CFC for an uninterrupted period of thirty days during its annual accounting period and who owned stock in the CFC on its last day of its annual accounting period.

Filers that are classified as Category 3 and Category 4, and Category 5 filers must complete and attach Schedule F to their Form 5471.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 33

WHO MUST COMPLETE FORM 5471 SCHEDULE F

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l34

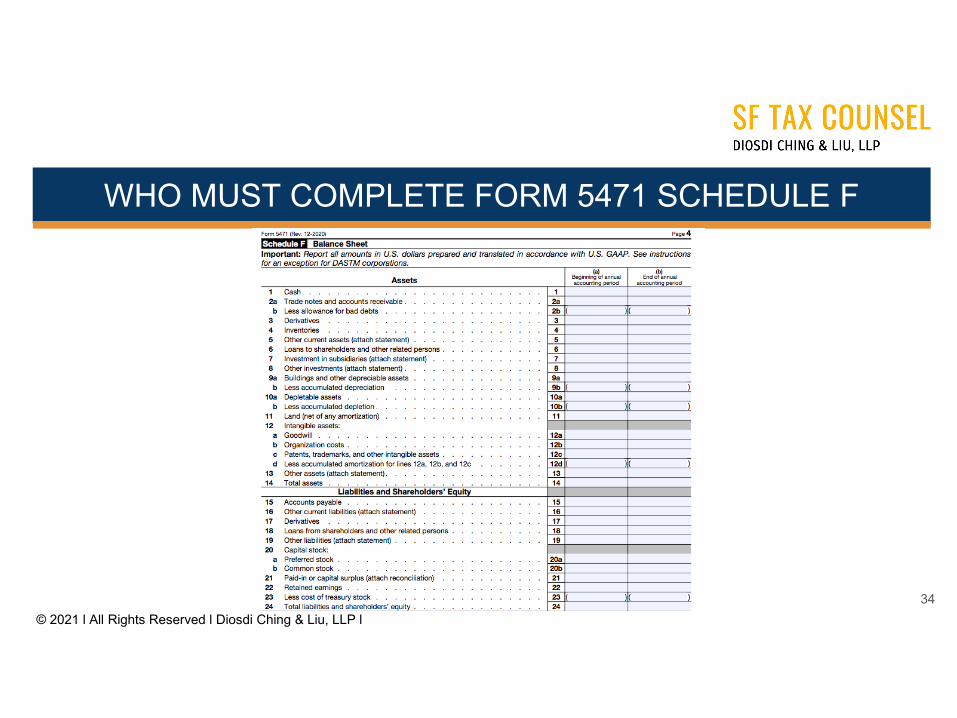

SCHEDULE F BALANCE SHEET

The Schedule F “Balance Sheet” is broken down into column (a) entitled “beginning of annual accounting period” and column (b) entitled “end of annual accounting period.”. The filer must report all information in the foreign corporation’s functional currency in accordance with U.S. GAAP and translate using U.S. GAAP transaction rules. Section 985(b)(1)A) states the general rule that the functional currency will be “the dollar.” However, the functional currency will be “the currency of theeconomic environment in which a significant part of the CFC’s activities is “conducted and which is used by such CFC in keeping its books and records. See IRC Section 985(b)(1)(B). If the foreign corporation uses DASTM, the balance sheet on Schedule F should be prepared and translated into U.S. dollars according to Treasury Regulation Section 1.985-3(d), rather than U.S. GAAP. A CFC that would otherwise have to use a foreign functional currency may be permitted under the regulations to elect to treat the dollar as its functional currency if it keeps books and records in dollars or uses a method of accounting that “approximates a separate transaction method.” See IRC Section 985(b)(3). This method (sometimes called the “dollar approximate separate transaction method of “DASTAM”), which is explained at Treasury Regulation Section 1.985-3, basically requires conversion into dollar equivalents when discrete transactions in other currencies occur. This election to use the dollar as the functional currency has been authorized for a CFC that would otherwise have used a “hyperinflationary currency.” See Treas. Reg. Section 1.985-2(b).

Schedule F is broken down into two sections. The first section of Schedule F requires filers to disclose the assets of the CFC at the beginning and ending of the reporting period. The second section of Schedule F requires filers to disclose the liabilities and shareholders’ equity in the CFC at the beginning and ending of the reporting period. We will now discuss each line of Schedule F.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 35

SCHEDULE F BALANCE SHEET

Line 1: Cash- Line 1 asks the filer to state the cash held by the CFC. The filer must disclose the CFC’s cash at the beginning and the end of the reporting period. If the CFC’s cash is held in foreign bank accounts, the filer should make sure the CFC’s cash is properly disclosed on FinCEN 114s and Form 8938s to the IRS.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 36

SCHEDULE F BALANCE SHEET

Line 2a: Trade Notes and Account Receivables- Line 2a asks the filer to list any trade notes or account receivables at the beginning and the end of the reporting period. A trade note is typically a payment such as a check or bank note. An account receivable is the balance of money due to a firm for goods or services delivered or used but not yet paid for by customers.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 37

SCHEDULE F BALANCE SHEET

Line 3: Derivatives- Line 3 asks the filer to list any derivatives at the beginning and the end of the reporting period. A derivative is a financial security with a value that is reliant upon or derived from, an underlying asset or group of assets. The derivative itself is a contract between two or more parties, and the derivative derives its price from fluctuations in the underlying asset. ASC 815 requires a derivative to be recorded on Schedule F as an asset or liability and to be measured at it’s fair value.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 38

SCHEDULE F BALANCE SHEET

Line 4: Inventories- Line 4 asks the filer to disclose inventories at the beginning and ending of the reporting period. Inventory should be disclosed on Schedule F using the cost of goods sold COGS Reconciliation Process.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 39

SCHEDULE F BALANCE SHEET

Line 5: Other Current Assets- Line 5 asks the filer to disclose “other current assets” at the beginning and the end of the reporting period. The filer should attach a detailed statement to Schedule F detailing the current assets of the CFC.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 40

SCHEDULE F BALANCE SHEET

Line 6: Loans to Shareholders and Other Related Persons- Line 6 asks the filer to disclose any loans to the shareholders or other related parties (as per Sections 958 and 318 of the Internal Revenue Code) at the beginning and the end of the reporting period. CFC shareholders should beware that loans from a CFC to U.S. shareholders could trigger a U.S. income tax consequence under Section 956 of the Internal Revenue Code.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 41

SCHEDULE F BALANCE SHEET

Line 7: Investment in Subsidiaries- Line 7 asks the filer to disclose any investments in subsidiaries at the beginning and the end of the reporting period. If the CFC invested in a subsidiary, the investment should be stated in a detailed attached statement. Any investment in a subsidiary may also trigger a reporting requirement on Schedule M of the Form 5471.Schedule M is designed to measure a CFC’s intercompany payments. Schedule M requires the majority CFC owners to provide information on transactions between the CFC and its shareholders or other related parties.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 42

SCHEDULE F BALANCE SHEET

Line 8: Other investments- Line 8 asks the filer to disclose any other investments on Line 8 at the beginning and the end of the reporting period. These other investments should be reported on a detailed attached statement. If the “other investments” are in other CFCs, the preparer should consider the reporting implications of Schedule O for Form 5471. Schedule O is used to report the organization or reorganization of a foreign corporation and the acquisition or disposition of stock.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 43

SCHEDULE F BALANCE SHEET

Line 9a. Building and other depreciable assets- Line 9a asks the filer to disclose any investments in buildings and depreciable assets at the beginning and end of the reporting period. The preparer should disclose any investments in buildings and depreciable assets on line 9a.

Line 9b. Less accumulated depreciation- Line 9b asks the filer to disclose any accumulated depreciation at the beginning and end of the reporting period. The preparer should disclose any accumulated depreciation. Accumulated depreciation is the cumulative depreciation of an asset up to a single point in its life.

Line 10a. Depletable assets- Line 10a asks the filer to disclose any depletable assets of the CFC at the depreciation at the beginning and the end of the reporting period. Examples of depletable assets are timber, coal, oil, precious metals such as gold and silver, and gemstones such as diamonds, rubies, and emeralds.

Line 10b. Less accumulated depletion- Line 10b asks the filer to disclose any accumulated depletion at the beginning and the end of the reporting period. Accumulated depletion is the amount of depletion expense that has built up over time in relation to the use of a natural resource.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 44

SCHEDULE F BALANCE SHEET

Line 11. Land (net of any amortization)- Line 11 asks the filer to disclose any net amortization taken on land held by the CFC. Line 11 asks the preparer to disclose the Net Plant and Equipment (“PP&E”) at the beginning and end of the reporting period. PP&E is the value of all buildings, land, furniture, and other physical capital that a business has purchased to run its business. The term “Net” means that it is “Net” of accumulated depreciation expenses. For example, assume that a CFC buys a building worth $1,000,000, along with $50,000 of furniture. The CFC’s Net PP&E at the moment of purpose is $1,050,000. Each year, however, the CFC must depreciate the value of the PP&E to account for the fact that it will wear out and need to fix or repurchase equipment. For example, assume that in the first year, the CFC depreciates the building and furniture by $105,000. As a result, at the end of its tax year, the CFC’s net PP&E will be:

$1,050,000 - $105,000 = $945,000

If the CFC acquires additional PP&E, the CFC’s net PP&E will increase. As time passes, the value of its PP&E will decrease.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 45

SCHEDULE F BALANCE SHEET

Line 12. Intangible Assets- Lines 12a through 12d asks the filer to disclose all intangible assets of the CFC at the beginning and end of the reporting period. Intangible assets must be separated into specific categories stated on the form. When reporting intangible items of Schedule F, U.S. GAAP accounting principles must be utilized.

Line 12a. Goodwill- CFCs’ can elect to amortize goodwill on a straight-line basis over 10 years.

Line 12b. Organization costs- CFC organizational costs should be expensed as incurred. This includes an analysis or survey of potential markets, products, labor supply, transportation facilities, advertisements for opening of the business, salaries and wages for employees who are being trained and their instructors, travel and other necessary costs for securing prospective distributors, suppliers, or customers, salaries and fees for executives and consultants, or for similar professional services.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 46

SCHEDULE F BALANCE SHEET

Line 12c. Patents, trademarks, and other intangible assets- patents, trademarks, and other intangible assets held by CFCs need to be amortized over the course of their life.

Line 12d. Less accumulated amortization for lines 12a, 12b, and 12c- line 12b requires the filer to disclose any accumulated amortization from lines 12a, 12b, and 12c. Accumulated amortization is the total amortization expense recorded for an intangible asset.

Line 13. Other Assets - Line 13 asks the filer to attach a detailed statement listing the assets of the CFC at the beginning and end of the reporting period. Line 13 may seem identical to Line 5 of Schedule F. Line 13 should only be utilized to disclose long term assets.

Line 14. Total Assets- Line 14 asks the filer to list the CFC’s total assets.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 47

SCHEDULE F BALANCE SHEET

Line 15. Accounts payable- Line 15 asks the filer to disclose the accounts payable at the beginning and end of the reporting period.

Line 16. Other current liabilities- Line 16 to list all current liabilities at the beginning and end of the reporting period. The filer should consider the impact of current liabilities on Schedule M of Form 5471.

Line 17. Derivatives- Line 17 asks the filer to list any derivatives which are liabilities at the beginning and end of the reporting period. The reporting must comply with Financial Accounting Series (“FASB”) accounting standards of Topic 815. The gross and not net position must be reported.

Line 18. Loans from shareholders and other related persons- Line 18 asks the filer to state any loans from shareholders and other related parties as defined under Sections 958 and 318 of the Internal Revenue Code at the beginning and end of the reporting period. The filer should consider the reporting of shareholder loans on Schedule M of the Form 5471 and whether an appropriate interest rate is being charged on the loans.

Line 19. Other Liabilities- Line 19 asks the filer to list any other liabilities at the beginning and end of the reporting period.

Line 20. Capital stock- Line 20 asks the filer to list any capital stock of the CFC at the beginning and end of the reporting period. Capital stock is the amount of common and preferred shares that a CFC is authorized to issue.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l48

SCHEDULE F BALANCE SHEET

Line 21. Paid-in or capital surplus- Line 21 asks the filer to list pid-in or capital stock. The filer must attach a reconciliation.

Line. 22 Retained earnings- Line 22 asks the filer to state the retained earnings of the CFC at the beginning and end of the reporting period. Retained earnings refers to profits earned by the CFC, minus any dividends it paid in the past. The filer should obtain audited financial statements if possible.

Line 23. Less cost of treasury stock- Line 22 asks the filer to reduce the cost of the treasury stock at the beginning and end of the reporting period. Treasury stock refers to previously outstanding stock that is bought back from shareholders by the CFC. These shares are issued but no longer outstanding and are not included in the distribution of dividends or the calculation of earnings per share.

Line 24. Total liabilities and shareholders’ equity- Line 24 asks the filer to list the total liabilities and shareholder equity at the beginning and end of the reporting period.

© 2021 l All Rights Reserved l Diosdi Ching & Liu, LLP l 49

505 Montgomery St., 11th FloorSan Francisco, CA 94111(415) [email protected] 50

ANTHONY V. DIOSDIAnthony advises clients on U.S. international tax matters, including tax planning with respect to their structures, operations, and transactions. In particular, Anthony advises clients on tax matters related to income tax deferral, maximization of tax treaty benefits, and subpart F planning. More recently, Anthony has focused on assisting clients navigate U.S. tax reform, including Global Intangible Low-Taxed income and Foreign-Derived Intangible Income and the new limitations on foreign tax credits. Anthony has a tax litigation background and also handles complex disputes involving cross-border income and FBAR violations.