for personal use only - australian securities · pdf filepro forma results (i) ... involvement...

TRANSCRIPT

COLLINS FOODS LIMITED 0

FY13 HALF YEAR RESULTS

30 November 2012

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 1

Today’s agenda

SECTION 1 – HY13 IN REVIEW

SECTION 2 – FINANCIAL PERFORMANCE

SECTION 3 – KFC

SECTION 4 – SIZZLER

SECTION 5 – INDUSTRY DYNAMICS AND MARKET

OUTLOOK

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 2

HY13 IN REVIEW

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 3

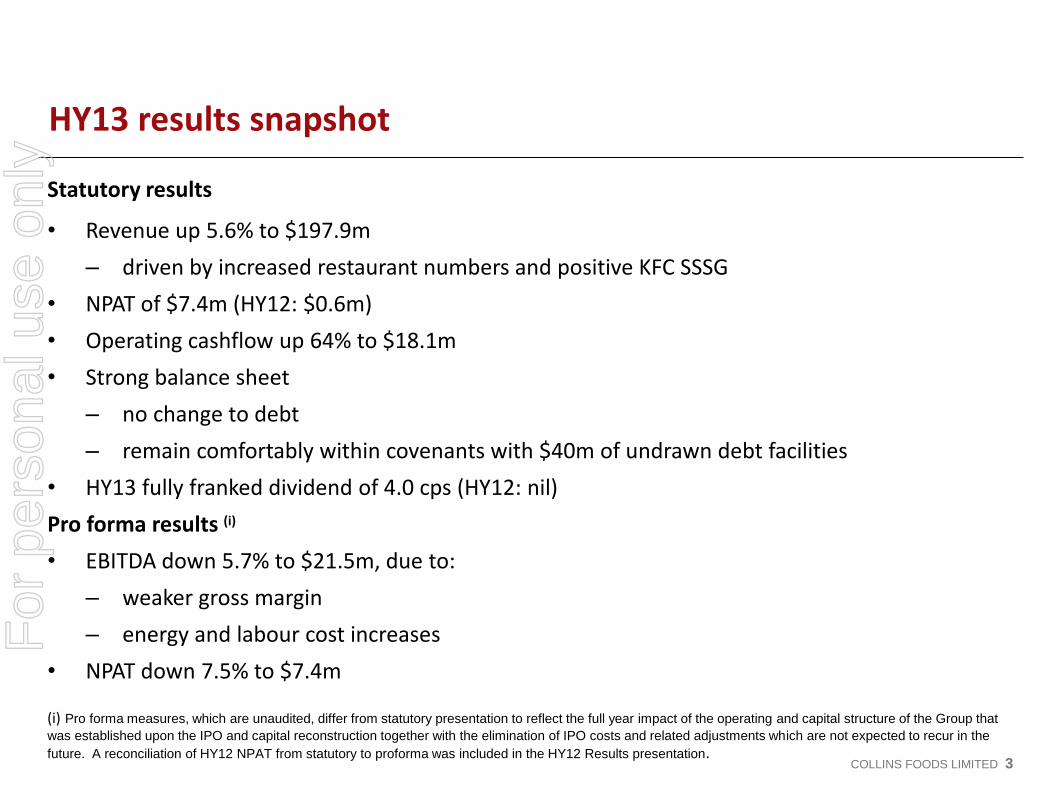

HY13 results snapshot

Statutory results

• Revenue up 5.6% to $197.9m

– driven by increased restaurant numbers and positive KFC SSSG

• NPAT of $7.4m (HY12: $0.6m)

• Operating cashflow up 64% to $18.1m

• Strong balance sheet

– no change to debt

– remain comfortably within covenants with $40m of undrawn debt facilities

• HY13 fully franked dividend of 4.0 cps (HY12: nil)

Pro forma results (i)

• EBITDA down 5.7% to $21.5m, due to:

– weaker gross margin

– energy and labour cost increases

• NPAT down 7.5% to $7.4m

(i) Pro forma measures, which are unaudited, differ from statutory presentation to reflect the full year impact of the operating and capital structure of the Group that

was established upon the IPO and capital reconstruction together with the elimination of IPO costs and related adjustments which are not expected to recur in the

future. A reconciliation of HY12 NPAT from statutory to proforma was included in the HY12 Results presentation.

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 4

HY13 operational snapshot

• Improved trading conditions, still highly competitive

– KFC sales up with SSSG of 3.6%

– Sizzler trading improving, below long term trend

– margin pressures from value offers and higher input costs

• New store rollouts continue

– 1 new KFC restaurant, 2 rebuilds and 2 refurbishments completed

– returns on growth Capex improving

• Continued focus on brand building and marketing campaigns

– positive response to ‘Goodification’ campaign continues

– success with KFC targeted value play - 9 for $9.95 Tuesdays

– Legendary Sizzler Salad Bar brand campaign

– Sizzler promotions targeted at soft trade periods

• Focus on efficiency and service

– productivity initiatives and new service flow methods

– KFC online ordering pilot commenced in Townsville

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 5

FINANCIAL PERFORMANCE

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 6

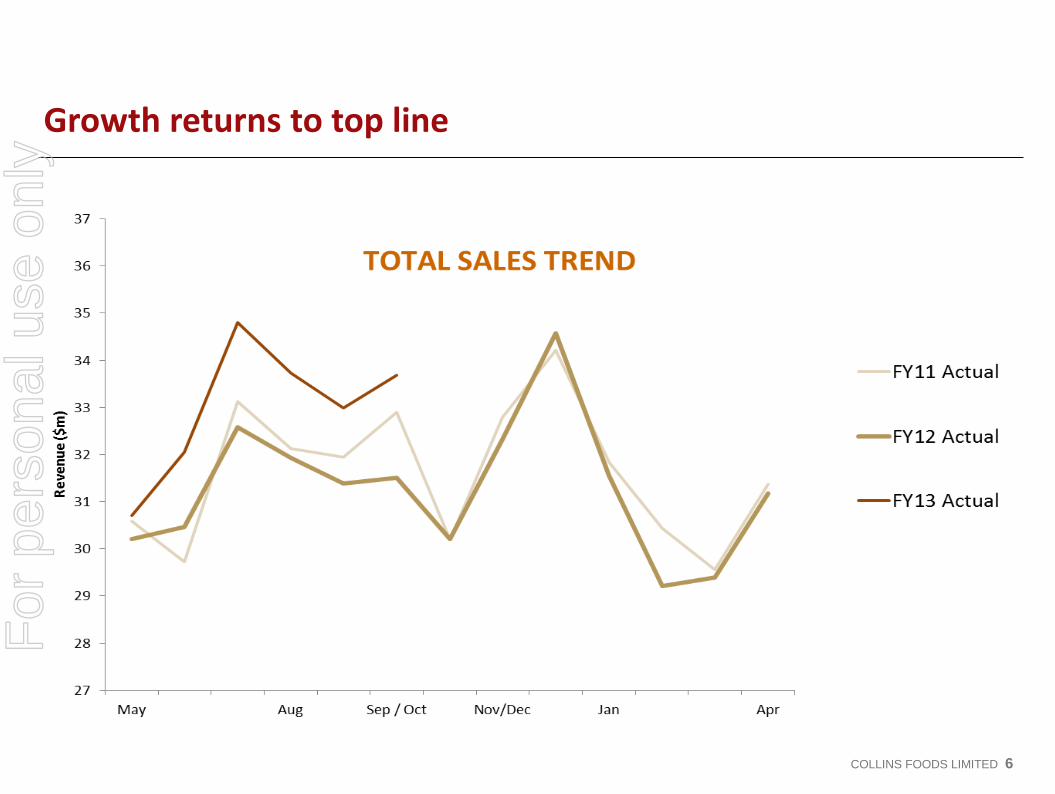

Growth returns to top line

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 7

Recovery is in progress

$million

HY13

Actual HY12

Proforma (a)

Change

Avg # restaurants(b) 147.7 144.3 3.4

Revenue 197.9 188.1 5.2%

% Growth 5.2% (1.3%)

Gross profit 103.9 99.1 4.7%

% margin 52.5% 52.7% 20bps

EBITDA 21.5 22.8 5.7%

% margin 10.9% 12.1% 120bps

EBIT 13.6 15.1 9.9%

% margin 6.9% 8.0% 110bps

NPAT 7.4 8.0 7.5%

% margin 3.7% 4.3% 60bps

• Revenue up 5.2% to $197.9m

− improved sales growth

value offers

brand and product initiatives

new stores

• EBITDA down 5.7% to $21.5m

− weaker gross margins

− energy cost increases carbon tax (in line with expectations)

− labour and admin cost increases

• NPAT down 7.5% to $7.4m

(a) Pro forma measures , which are unaudited, differ from statutory presentation to reflect the

full year impact of the operating and capital structure of the Group that was established

upon the IPO and capital reconstruction together with the elimination of IPO costs and

related adjustments which are not expected to recur in the future.

(b) Excludes Asian franchise restaurants

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 8

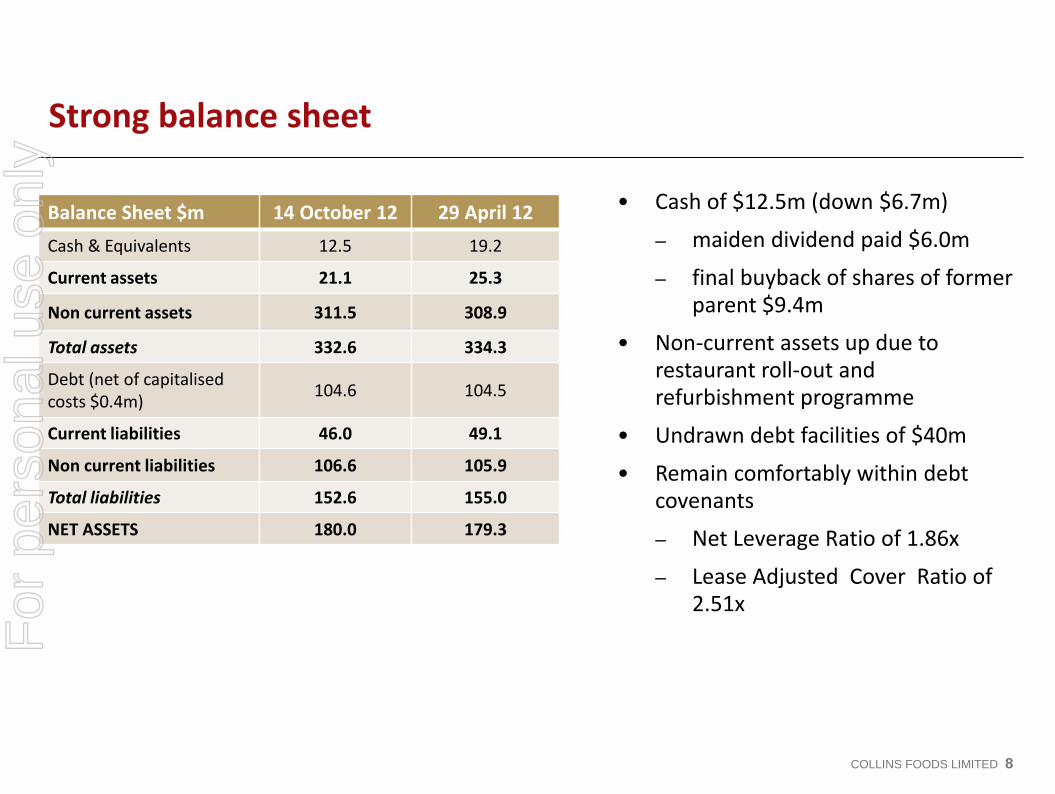

Strong balance sheet

Balance Sheet $m 14 October 12 29 April 12

Cash & Equivalents 12.5 19.2

Current assets 21.1 25.3

Non current assets 311.5 308.9

Total assets 332.6 334.3

Debt (net of capitalised costs $0.4m)

104.6 104.5

Current liabilities 46.0 49.1

Non current liabilities 106.6 105.9

Total liabilities 152.6 155.0

NET ASSETS 180.0 179.3

• Cash of $12.5m (down $6.7m)

– maiden dividend paid $6.0m

– final buyback of shares of former parent $9.4m

• Non-current assets up due to restaurant roll-out and refurbishment programme

• Undrawn debt facilities of $40m

• Remain comfortably within debt covenants

– Net Leverage Ratio of 1.86x

– Lease Adjusted Cover Ratio of 2.51x

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 9

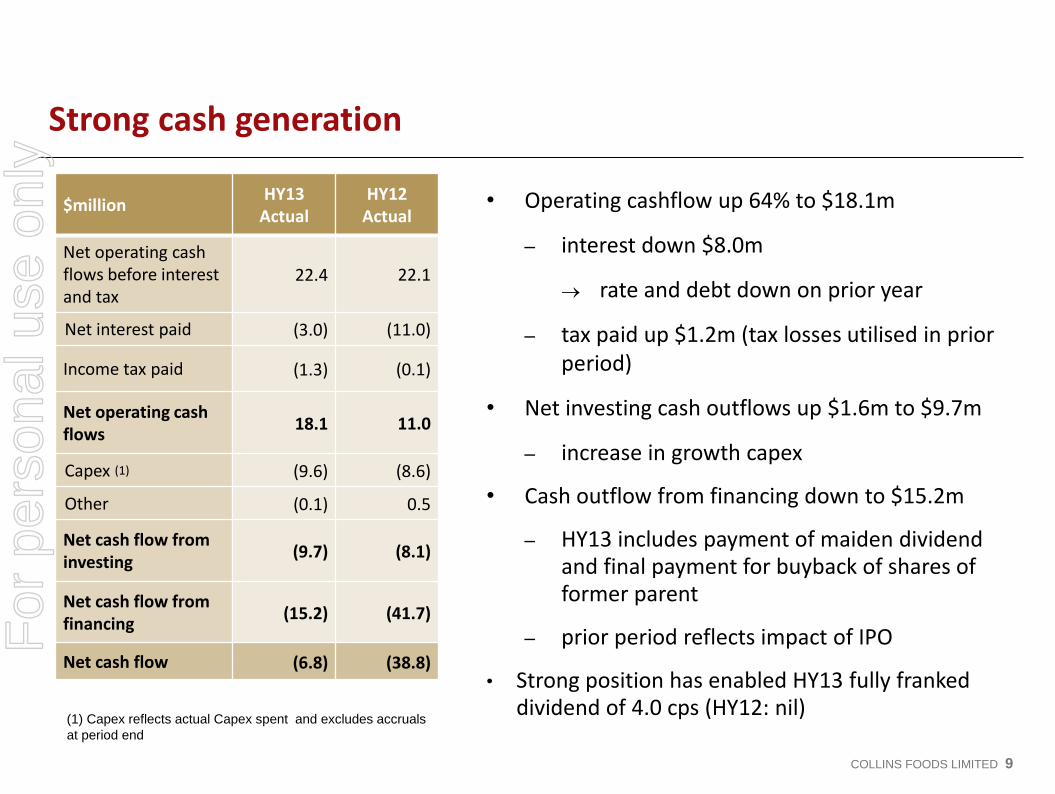

Strong cash generation

• Operating cashflow up 64% to $18.1m

– interest down $8.0m

rate and debt down on prior year

– tax paid up $1.2m (tax losses utilised in prior period)

• Net investing cash outflows up $1.6m to $9.7m

– increase in growth capex

• Cash outflow from financing down to $15.2m

– HY13 includes payment of maiden dividend and final payment for buyback of shares of former parent

– prior period reflects impact of IPO

• Strong position has enabled HY13 fully franked dividend of 4.0 cps (HY12: nil)

$million HY13

Actual HY12

Actual

Net operating cash flows before interest and tax

22.4 22.1

Net interest paid (3.0) (11.0)

Income tax paid (1.3) (0.1)

Net operating cash flows

18.1 11.0

Capex (1) (9.6) (8.6)

Other (0.1) 0.5

Net cash flow from investing

(9.7) (8.1)

Net cash flow from financing

(15.2) (41.7)

Net cash flow (6.8) (38.8)

(1) Capex reflects actual Capex spent and excludes accruals

at period end

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 10

KFC

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 11

KFC performance reflects improved sales momentum

$million HY13

Actual HY12

Actual Change

Restaurants Average Period end

120.7 121.0

118.3 120.0

2.4 1.0

Revenue 148.2 140.3 5.6%

% SSSG 3.6% 0.0%

EBITDA 20.7 21.7 4.6%

% margin 14.0% 15.5% 150bps

• Revenue up 5.6% to $148.2m

increase in average restaurant numbers

SSSG up to 3.6%

free-standing restaurants driving growth

food courts continue to struggle

• EBITDA down 4.6% to $20.7m

− margin tightened 150 bps

lower gross margin from input pressures and promotional discounting

indirect labour restructuring costs

energy cost increases

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 12

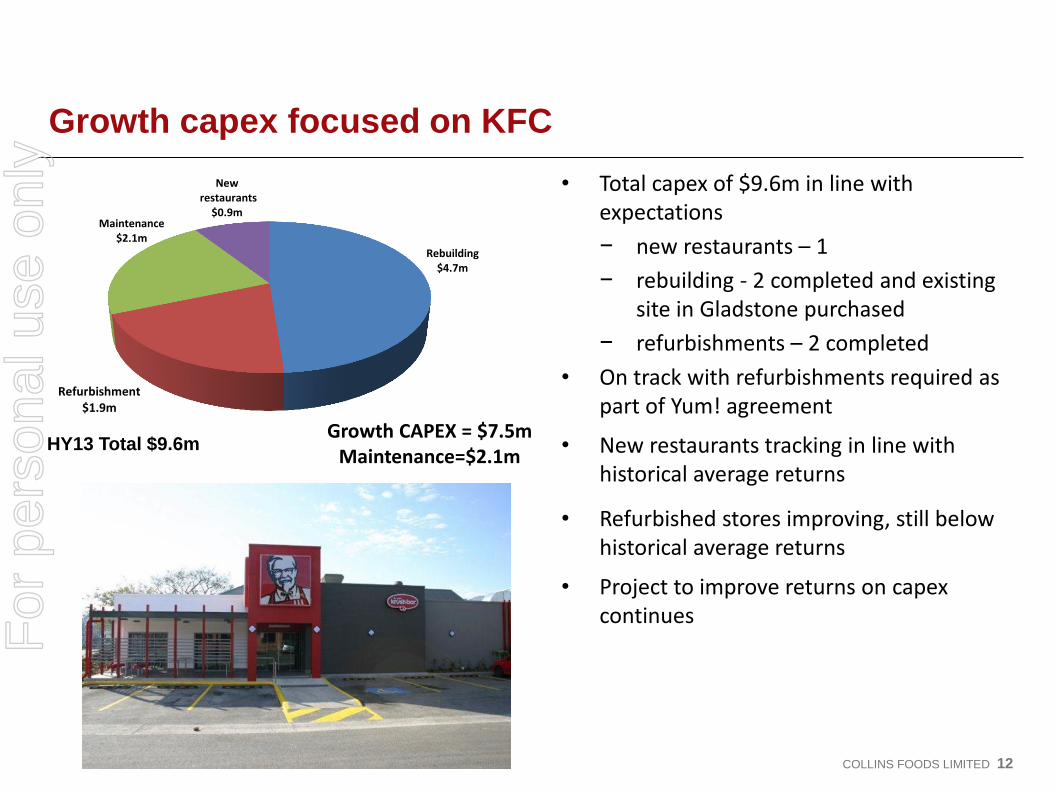

Growth capex focused on KFC

• Total capex of $9.6m in line with expectations

− new restaurants – 1

− rebuilding - 2 completed and existing site in Gladstone purchased

− refurbishments – 2 completed

• On track with refurbishments required as part of Yum! agreement

• New restaurants tracking in line with historical average returns

• Refurbished stores improving, still below historical average returns

• Project to improve returns on capex continues

Growth CAPEX = $7.5m Maintenance=$2.1m

HY13 Total $9.6m

Rebuilding $4.7m

Refurbishment $1.9m

Maintenance $2.1m

New restaurants

$0.9m

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 13

New stores

Valley Metro – opened Aug 2012

Financial Snapshot

Capital Spend $ 843,000

Sales Variance

(Actual v Capex Sales) +4.2%

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 14

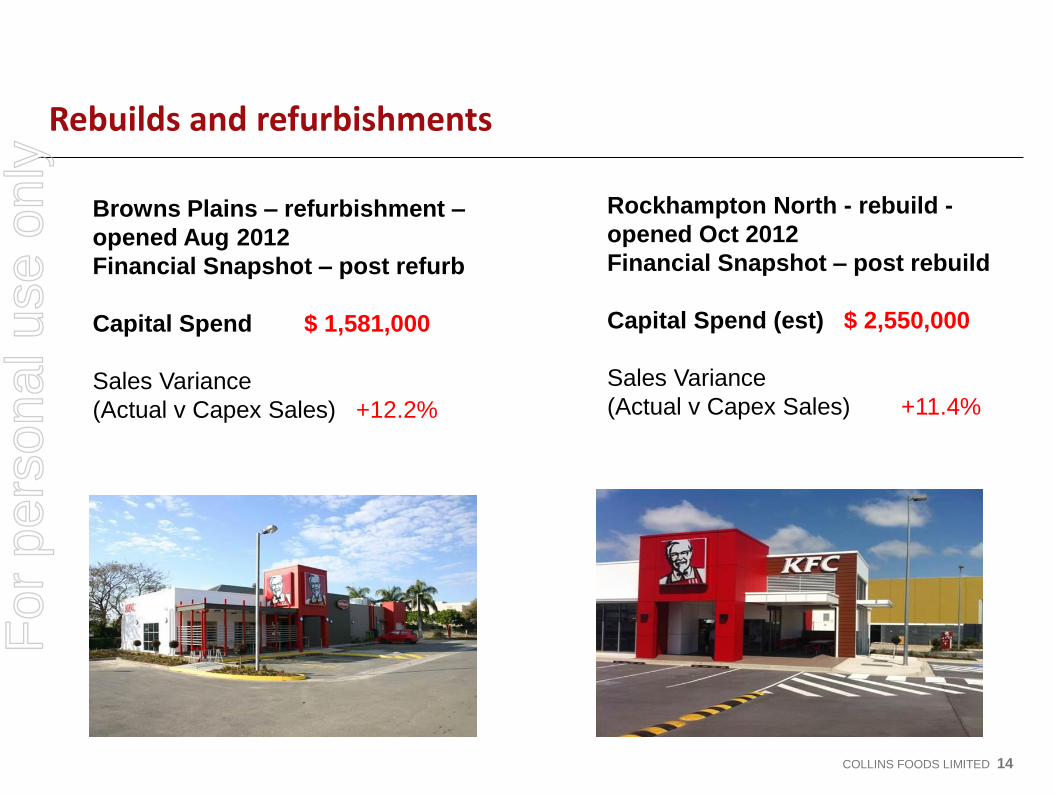

Rebuilds and refurbishments

Browns Plains – refurbishment –

opened Aug 2012

Financial Snapshot – post refurb

Capital Spend $ 1,581,000

Sales Variance

(Actual v Capex Sales) +12.2%

Rockhampton North - rebuild -

opened Oct 2012

Financial Snapshot – post rebuild

Capital Spend (est) $ 2,550,000

Sales Variance

(Actual v Capex Sales) +11.4%

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 15

Marketing campaigns rebuilding and growing core business

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 16

Focus on innovation in product development and targeted value offers

• Ongoing development of non-fried products

new grilled product developed - launch before year end

• Value offers resonating well with customers

Family Dinner Box and WOW Dinner – 9 pieces for $9.95 and 2 sides for $5 Tuesday only

• Successful Winter campaign with a new chicken on the bone variant (Sweet Sesame Chicken)

• Breakfast offering being trialled by Yum!

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 17

Initiatives to improve operating efficiencies

• New service flow methodologies rolled out in select stores

• Online ordering trial

• Indirect labour restructuring

• Rollout of Small Ticket Pre Approved payment facility (for up to $35 payments) commenced

• New maintenance system and streamlined processes

• Tandem drive thru trial underway in 3 stores

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 18

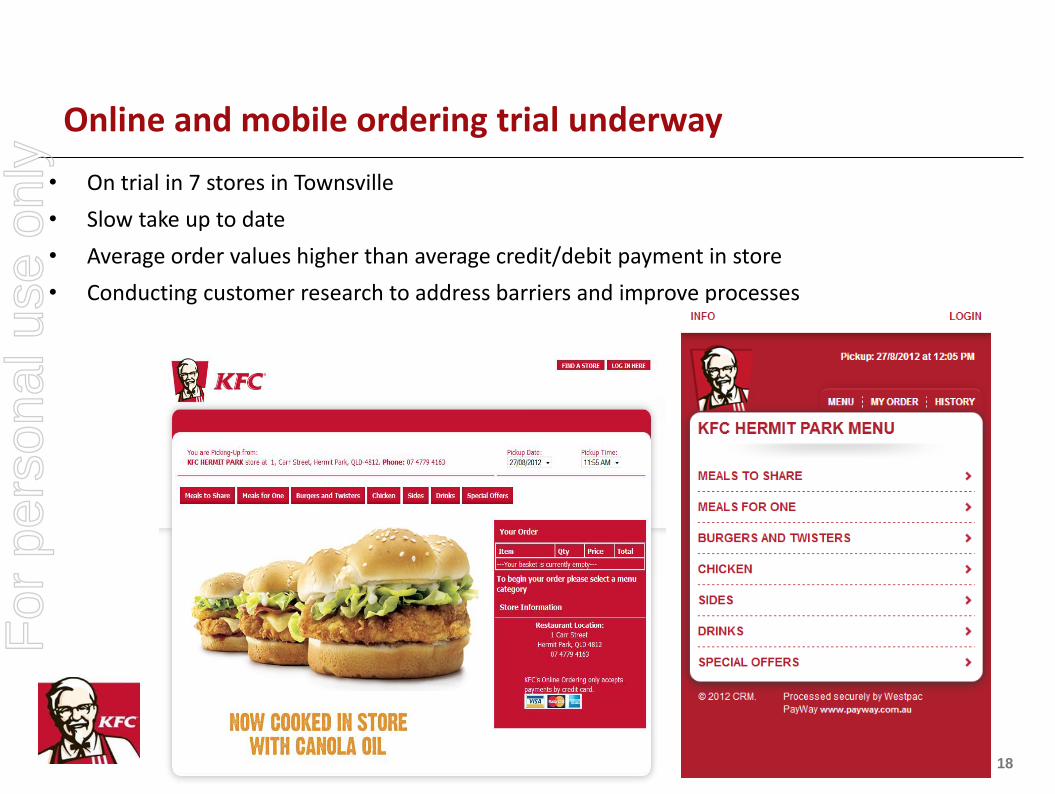

Online and mobile ordering trial underway

• On trial in 7 stores in Townsville

• Slow take up to date

• Average order values higher than average credit/debit payment in store

• Conducting customer research to address barriers and improve processes

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 19

Key priorities for 2H13

• 2 new stores and 4 refurbishments

• Innovative brand marketing campaigns

− Summer Cricket Campaign

− local area marketing activities to leverage involvement with KFC T20 Big Bash

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 20

Key priorities for 2H13 (cont’d)

• Core product building

− burger campaign launch

• Product development with ‘Better for You’ range launches

− grilled product

− kids menu

• Establishing a permanent sustainable “value” layer

• Ongoing trials of online ordering

• Breakfast pilot in New Year with Yum!

• Operational improvement initiatives

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 21

SIZZLER

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 22

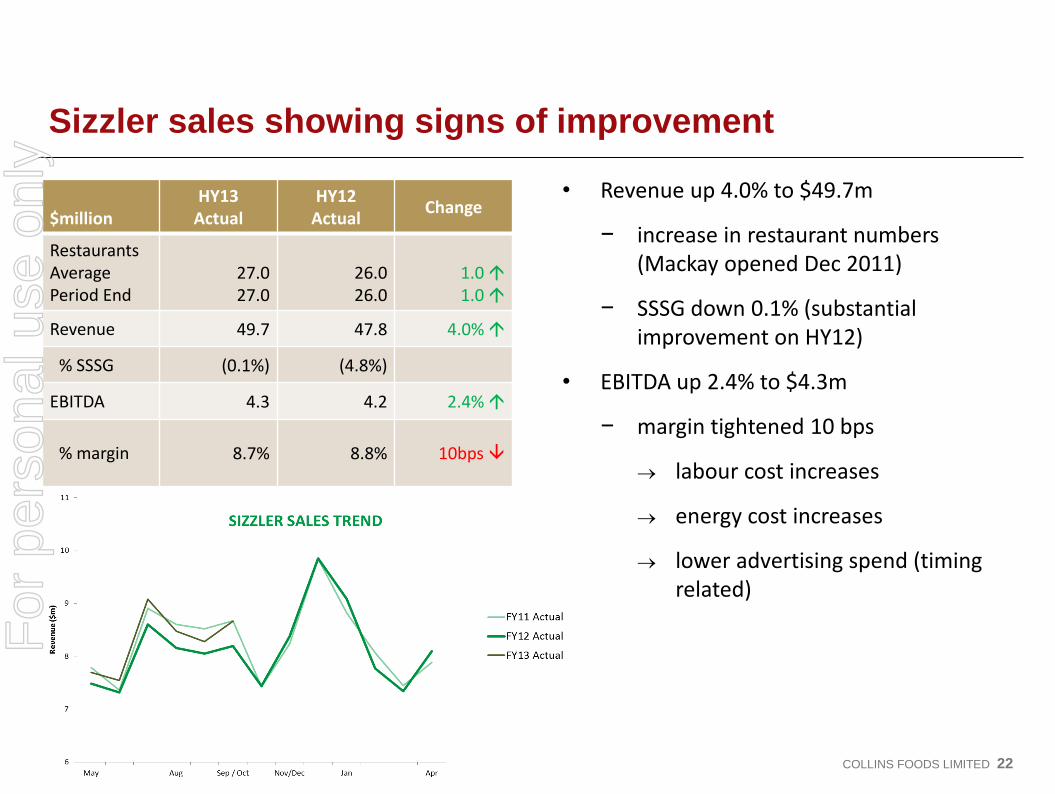

Sizzler sales showing signs of improvement

• Revenue up 4.0% to $49.7m

− increase in restaurant numbers (Mackay opened Dec 2011)

− SSSG down 0.1% (substantial improvement on HY12)

• EBITDA up 2.4% to $4.3m

− margin tightened 10 bps

labour cost increases

energy cost increases

lower advertising spend (timing related)

$million HY13

Actual HY12

Actual Change

Restaurants Average Period End

27.0 27.0

26.0 26.0

1.0 1.0

Revenue 49.7 47.8 4.0%

% SSSG (0.1%) (4.8%)

EBITDA 4.3 4.2 2.4%

% margin 8.7% 8.8%

10bps

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 23

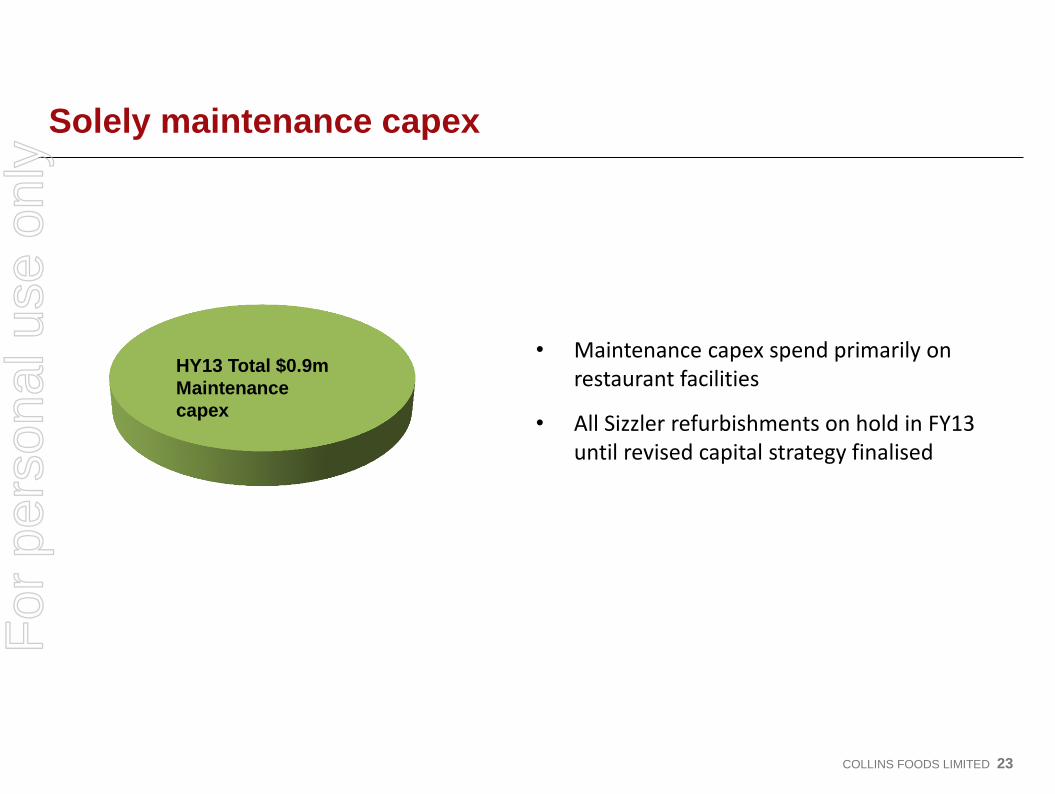

Solely maintenance capex

• Maintenance capex spend primarily on restaurant facilities

• All Sizzler refurbishments on hold in FY13 until revised capital strategy finalised

HY13 Total $0.9m

Maintenance

capex

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 24

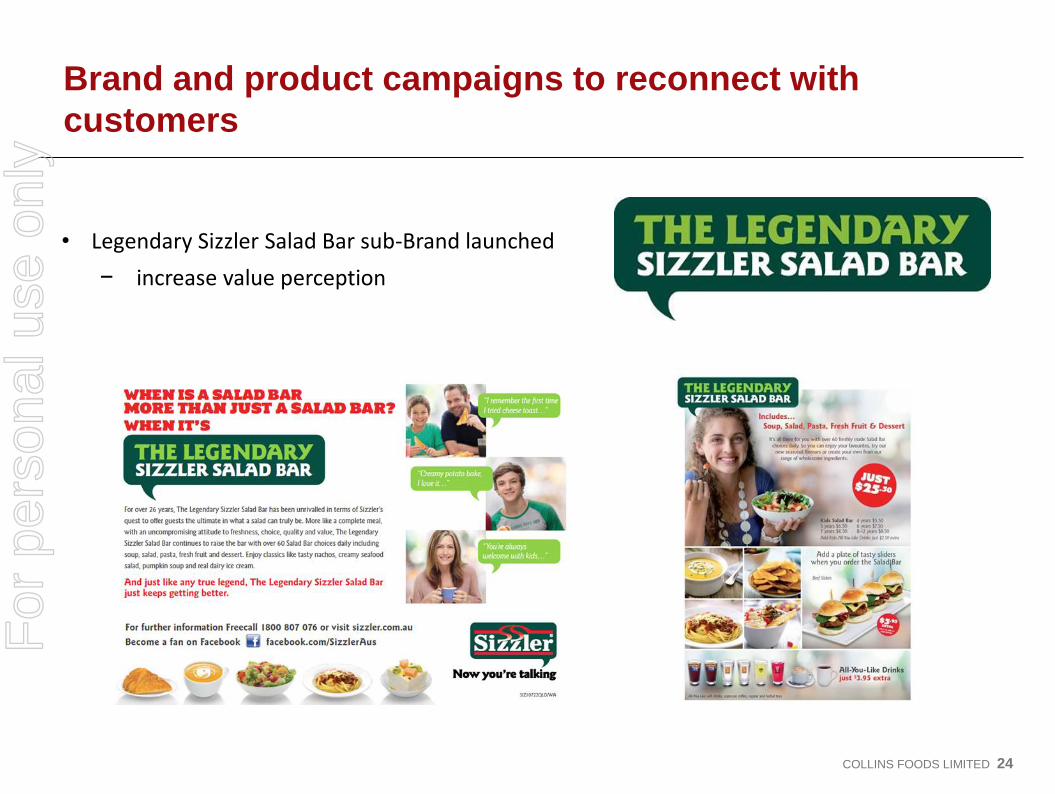

Brand and product campaigns to reconnect with

customers

• Legendary Sizzler Salad Bar sub-Brand launched

− increase value perception

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 25

Product development and promotional initiatives

• New Winter Menu and combos rolled out

• Soft trade period opportunities targeted

− early week promotions

− day part offers including

special light lunches

“one trip” salad bar

• Key event promotions such as Mother’s Day resonated well with guests

• Special offers introduced including

− 20% student discount

− Facebook competitions

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 26

Key priorities for 2H13

• Continued focus on brand building

− Legendary Sizzler Salad Bar campaign

• Targeted promotional and value plays, with focus on soft trade periods

− add on promotion

− 2 for 1 Tuesdays

− value priced lunch meals

• New product and promotional initiatives with menu price increase

− Seafood Spectacular Summer Salad Bar

− new grill meals

• Online booking system (testing Xmas 2012)

• Productivity and efficiency initiatives

• New stores in China and Thailand

• Explore further growth avenues

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 27

INDUSTRY DYNAMICS AND MARKET OUTLOOK

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 28

QSR landscape

• Product innovation is key to stimulating demand

• Need to focus on increasing average transaction value

• Retail is doing it tough in multi-speed economy

• Margin pressures persist... discounting to drive sales and increased costs

• QSR sales trend appears to be improving for both domestic and international operators... casual dining sector continues to lag

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 29

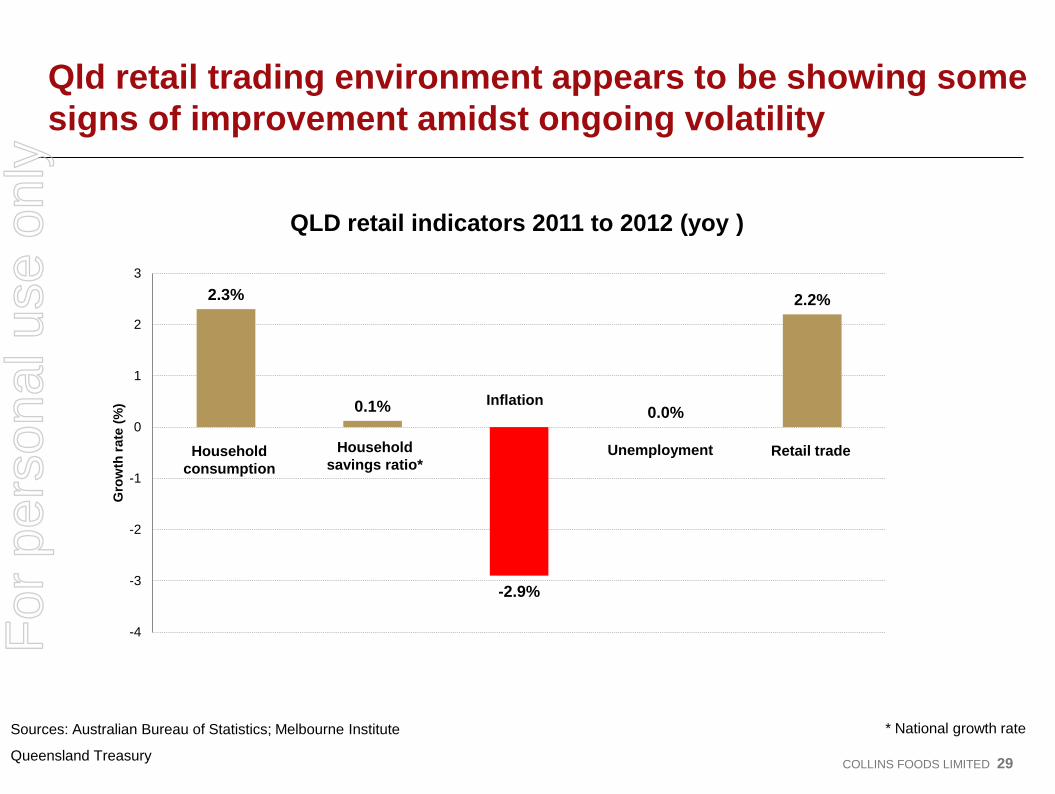

Qld retail trading environment appears to be showing some

signs of improvement amidst ongoing volatility

29

Sources: Australian Bureau of Statistics; Melbourne Institute

Queensland Treasury

2.3%

0.1%

-2.9%

0.0%

2.2%

-4

-3

-2

-1

0

1

2

3

Gro

wth

rate

(%

)

QLD retail indicators 2011 to 2012 (yoy )

Household

consumption

Household

savings ratio*

Inflation

Unemployment Retail trade

* National growth rate

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 30

FY13 outlook

• Return to same store sales growth

– KFC FY13 SSSG expected of 4.8%

– Sizzler FY13 SSSG expected of 1.9%

• Carbon Tax is impacting as expected ($2.5m pre-tax for FY13)

– current trading conditions do not allow CKF to pass on full cost increases

• Further increases in labour and raw material input costs expected in Q4

• Working to counter part of labour and cost increases with productivity improvements

• FY13 earnings outlook remains unchanged

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 31

In summary…

• HY13 financial performance driven by improved KFC top line offset by margin compression

• Strong balance sheet

• HY13 fully franked dividend of 4.0 cps

• Continued focus on growing and rebuilding core businesses

– new KFC stores to leverage attractive opportunities in key growth corridors

– continued commitment to innovation & product development

– new brand building marketing campaigns

– use of technologies to generate operating efficiencies

• Macro environment remains challenging, although signs of improvement continue to emerge F

or p

erso

nal u

se o

nly

COLLINS FOODS LIMITED 32

THANK YOU & QUESTIONS

For

per

sona

l use

onl

y

COLLINS FOODS LIMITED 33

DISCLAIMER

"This presentation contains forward looking statements which may be subject to significant uncertainties beyond CKF's control. No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based. Circumstances may change and the forward looking statements may become outdated as a result so you are cautioned not to place undue reliance on any forward looking statement.”

All financial amounts contained in this presentation are expressed in Australian currency and rounded to the nearest $0.1 million unless otherwise stated. Any discrepancies between totals, sums of components and differences in tables and percentage variances calculated contained in this presentation are due to rounding.

For

per

sona

l use

onl

y