for personal use only - capitaland · 2013 half year results briefing investor presentation 24 july...

TRANSCRIPT

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

1H13 Result 2013 first halfoverview.

Group CapitaLand strategic review concluded, Australand to remain a key investment

First half operating profit of $62m

O t k t d li th i ti i f FY13 On track to deliver growth in operating earnings for FY13

Interim distribution of 10.5 cents per security

Investment 10% EBIT growth in 1H13Investment Property

10% EBIT growth in 1H13

Occupancy of 95.3% and WALE of 5.4 years

141,000 sqm of leasing activity

Commercial & Industrial

Completed 7 projects with an end value of ~$225m

Secured ~75,000 sqm of new commitments from industrial tenants

Forward workload of 146,000 sqm, q

Residential Improved sales activity driven by strong pre-sales in Sydney

1,793 contracts on hand, 51% expected to settle in 2H13

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 2

Top 12 projects – FY13 sales targets 76% secured

For

per

sona

l use

onl

y

1H13 Result Group pfinancial results.

1H13 1H121

Investment Property $96m $88m

Commercial & Industrial $10m $10m

Residential $22m $40m

Corporate $(9)m $(13)mCorporate $(9)m $(13)m

Operating EBIT $119m $125m

Operating profit after tax2 $62m $68m

Investment property revaluation gain $17m $34m

Unrealised gain/loss on interest rate derivatives $10m $(12)mUnrealised gain/loss on interest rate derivatives $10m $(12)m

Corporate activity expenses $(1)m -

Statutory profit after tax $88m $90m

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 3

1. 1H12 EBIT restated for AASB112. Operating profit after tax is consistent with Property Council White Paper guidelines for disclosing FFO

For

per

sona

l use

onl

y

1H13 Result Key operatingy p gmetrics.

1H13 earnings lower with a stronger 2H13 expected

Key metrics 1H13 1H12

Operating EPS 10.8c 11.8c

S Distribution of 10.5 cents per security,

consistent with full year guidance

Gearing remains within target range

DPS 10.5c 10.5c

% recurrent earnings 81% 70%

Jun 13 Dec 12g g g(25-35%)

Improved average cost of debt to 7.5%

NTA increase driven by MTM of

Jun 13 Dec 12

Gearing1 33.0% 32.1%

Weighted average debt maturity 2.7 yrs 3.2 yrs

Weighted average cost of debt2 7 5% 7 7% NTA increase driven by MTM of derivatives ($0.04) and property revaluation gains ($0.03)

Weighted average cost of debt2 7.5% 7.7%

NTA per security $3.57 $3.49

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 4

1. Interest bearing debt / total tangible assets (cash adjusted), based on the drawn amount of debt excluding fair value adjustments and associated derivative financial instruments. Dec 12 restated for AASB112. All in cost of debt excluding establishment fees and net of interest income

For

per

sona

l use

onl

y

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

InvestmentProperty

FinancialProperty performance.

Results 1H13 1H12

EBIT $96m $88m1 $ $

EBIT growth of 10% driven by:

− Comparable rental growth of 3.1%Revaluation gain1 $17m $34m

Metrics2 Jun 13 Dec 12

Portfolio value $2.3bn $2.3bn

− Income from internal development completions including 357 Collins St (VIC), Rhodes F (NSW) and Coles (QLD) Portfolio value $2.3bn $2.3bn

Occupancy (by income) 95.3% 97.6%

Industrial occupancy 98.6% 100.0%

Office occupancy 91 6% 94 9%

(QLD)

Revaluation gain of $17m driven primarily by rental growth

P tf li i il i ffi d Office occupancy 91.6% 94.9%

Comparable rental growth 3.1% 3.2%

WALE (by income) 5.4 yrs 5.5 yrs

Portfolio vacancy, primarily in office, due to unlet space at:

− 357 Collins St (74% leased)

Average cap rate 8.06% 8.09%1. Includes gains on internal developments of $3m (1H13) and $10m (1H12)2. Portfolio value includes properties under development, all other metrics exclude properties

under development and assets held for sale

− Rhodes F (63% leased)

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 6

For

per

sona

l use

onl

y

InvestmentProperty

2013 leasing Property

gactivity.

Renewals and new leasing activity of 141,000 sqm

Major renewals Type Area (sqm) Expiry

Coles Industrial 61,300 2019

Amcor Industrial 15 200 2023− Represents 7% of portfolio income

− Rents on renewals were in line with in place rents

Amcor Industrial 15,200 2023

L&L Products Industrial 14,000 2024

Sumitomo Industrial 12,350 2017

Smith Lewis Industrial 3,800 2017

− WALE of 5.1 years

Tenant retention of 75% (by income)Major new leases

Holman Fresh Industrial 5,000 2016

Vanguard Office 1,400 2020

Leasing metricsArea

(sqm)Rent

changeAverage

incentiveAverage

WALE

Renewals 113,200 +1% 5% 5.6 yrs

New leases 27,800 N/A 14% 3.7 yrs

Total 141,000 +1% 7% 5.1 yrs

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 7

For

per

sona

l use

onl

y

InvestmentProperty

Lease expiry Property

p yprofile.

50% Portfolio WALE remains strong at 5.4 years

− 1% expires in 2H13

Lease expiry profile1

83% expiring post FY14

5%1%

11% 11% 8%14%

− 11% expires in FY14 (down from 16% at Dec 12)

− 83% expires post FY14

p g p

Vacancy 2H13 FY14 FY15 FY16 FY17 FY18+

% p p

Strong focus on addressing near term expiries and portfolio vacancy

Portfolio income supported by quality Major 2H13 and FY14 l i i

Area ( )

% portfolio i E iPortfolio income supported by quality

tenant covenant

− 85% of income from government, ASX listed and multinational companies

lease expiries (sqm) income Expiry

LG, Eastern Creek (NSW) 29,045 2.3% 3Q14

Qantas, Mascot (NSW) 10,255 2.0% 2Q14

NAB, Rhodes (NSW) 7,490 1.7% 2Q14

Laminex, Murarrie (QLD) 21,530 0.8% 3Q14

Commonwealth Govt, Sydney (NSW) 5,675 0.7% 2Q14

Qantas, Mascot (NSW) 3,370 0.6% 3Q13

C t i P th Ai t (WA) 9 540 0 6% 2Q14

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 8

1. By portfolio income, excludes properties under development

Centurion, Perth Airport (WA) 9,540 0.6% 2Q14

For

per

sona

l use

onl

y

InvestmentProperty

PositioningProperty

g& outlook.

EBIT growth expected in FY13

− 2H13 EBIT expected to be at least in line with 1H13

− Full year contributions from internal developments

− Embedded rental growth(Average ~3% pa fixed rent increases over 94% of portfolio income)

Mi i l l i i FY13− Minimal lease expiry in FY13

Leasing remains a key focus

− Progressively de-risking near term expiries

− Leasing up vacant space including 357 Collins St and Rhodes F

B ildi F

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 9

357 Collins St, VIC

Building FRhodes, NSW

For

per

sona

l use

onl

y

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

Commercial& Industrial

Financial& Industrial performance.

EBIT in line with prior period

− Lower land sales offset by increased

Results1 1H13 1H12

Revenue $108m $65m

EBIT $10 $10third party built form activity

Total contribution (including NTA uplift) lower due to a reduced level of internal development

EBIT $10m $10m

NTA uplift $3m $10m

Total contribution $13m $20mdevelopment

Secured ~75,000 sqm of new commitments from industrial tenants

F tli VIC (22 000 )

Development activity

Built form - Third party (sqm) 90,200 28,400

Built form Internal (sqm) 8 900 38 500− Fastline, VIC (22,000 sqm)

− OfficeMax, NSW (19,300 sqm)

− Schenker, VIC (14,000 sqm)

Built form - Internal (sqm) 8,900 38,500

Land sales (sqm) 81,500 127,000

Metrics Jun 13 Dec 12

Two additional facilities committed to the GIC JV with an end value of $42m

Capital employed2 $377m $376m

Forward workload (sqm) 146,000 183,000

1. Includes ALZ share of joint arrangements. 1H12 revenue & EBIT restated for AASB11

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 11

2. Total assets less non interest bearing liabilities at period end. Dec 12 restated for AASB11

For

per

sona

l use

onl

y

Commercial& Industrial

Forward& Industrial workload.

INTERNAL DEVELOPMENTArea Estimated end Timing

(sqm) value ($m) % to go 2H13 1H14

NSW Kangaroo Drive, Eastern Creek 15,750 22 65% Total forward workload of 146,000

sqm across 11 industrial projects, end value ~$280m

DEVELOPED FOR EXTERNAL SALEArea Estimated end Revenue Revenue timing

(sqm) value ($m) % to go 2H13 1H14

NSW Office Max, Eastern Creek (GIC) 19,300 26 100%

Kangaroo Drive, Eastern Creek 20,500 25 100%

CH2 Eastern Creek (GIC) 8 150 16 40%

end value $280m

10 projects developed for external sale with an estimated end value of ~$260m

CH2, Eastern Creek (GIC) 8,150 16 40%

QLD Ceva, Berrinba (GIC) 41,000 60 15%

Siltstone Place, Berrinba 9,450 13 100%

VIC Fastline & Spec, Westpark 46,850 42 24%

Kimpton Way Altona 25 700 24 100%

− 60% leased

− 72% sold

9 j t t t d f l ti Kimpton Way, Altona 25,700 24 100%

Rinnai, Keysborough 14,800 20 65%

Southern Court, Keysborough 17,850 18 100%

Symbion, Keysborough 12,800 17 100%

− 9 projects targeted for completion in 2H13

A detailed table outlining the forward workload is set out in the AppendicesA detailed table outlining the forward workload is set out in the Appendices

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 12

For

per

sona

l use

onl

y

Commercial& Industrial

Industrial market & Industrial overview.

Prime grade vacancy remains relatively low

− High level of tenant renewal activity

Prime industrial vacancy Jun 13Melbourne 1.7%

Sydney 5 1%

− Supply remains constrained despite some speculative activity

Tenants remain selective and conversion of

Sydney 5.1%

Brisbane 5.3%Source: Savills

2,500

Industrial completions

enquiry is challenging

− Retail and logistics related users are most active

1,000

1,500

2,000

sqm

(000

's)

− Supply chain efficiencies key driver

− Sydney currently most active market

Some land markets showing early signs of

0

500

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

S d M lb B i b

Some land markets showing early signs of improved enquiry

Increased focus on sustainability

Strong investor appetite remains for prime assets*

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Sydney Melbourne Brisbane

13

* Includes properties currently under constructionSource: Jones Lang LaSalle REIS 2Q13

Strong investor appetite remains for prime assets

For

per

sona

l use

onl

y

Commercial& Industrial

Positioning& Industrial

g& outlook.

Fully zoned landbank and strong operating platform with multiple revenue streams

− Industrial pre-leases and land sales

− Development for owner occupiers

− Selective speculative developmentp p

Expand capital partnering relationships

FY13 outlook

− Operating conditions to remain challenging

− Earnings skewed to 2H13, in line with delivery of forward workloaddelivery of forward workload

− FY13 EBIT expected to be similar to FY12

Capital expected to trend down

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 14

GMEWinston Hills, NSW

− Capital expected to trend down

For

per

sona

l use

onl

y

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

Residential Financial performance.

Revenue and EBIT lower reflecting:

− Timing of built form settlements

Results1 1H13 1H12

Revenue $192m $260m

EBIT $22m $40m− Reduced contribution from high margin

land projects

Lot sales down slightly but activity up driven

EBIT $22m $40m

Lots sold 409 489

Contracts on hand (lots) 1,108 824

C t t h d ( l ) $558 $406g y y p

by strong pre-sales in Sydney

Strong growth in contracts on hand

− 51% expected to settle in 2H13

Contracts on hand (value) $558m $406m

Activity2

Sales activity3 1,244 1,03151% expected to settle in 2H13

− 33% expected to settle in 2014

− 16% expected to settle in 2015

Gross lots sold 620 654

Gross contracts on hand (lots) 1,793 1,316

Metrics Jun 13 Dec 12

1 I l d ALZ h f j i t t d PDA 1H12 & EBIT t t d f AASB11

Capital elevated reflecting construction of built form projects due to settle in 2H13 & 2014

Metrics Jun 13 Dec 12

Capital employed4 $920m $873m

Lots under management2 18,900 20,400

Pipeline end value2 $7 6bn $8 0bn

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 16

1. Includes ALZ share of joint arrangements and PDAs. 1H12 revenue & EBIT restated for AASB112. Includes 100% of joint arrangements and PDAs3. Total new sales and contracts on hand for the 6 months to 30 Jun4. Total assets less non interest bearing liabilities at period end. Dec 12 restated for AASB11

Pipeline end value $7.6bn $8.0bn

For

per

sona

l use

onl

y

Residential VIC overview.

Market stabilising

− Activity levels for land sales improved in 1H13Land sales activity

(by lots)2VIC1

58% 350− Re-introduction of FHB incentives for new

dwellings and enhanced NRAS expected to assist recovery

Steady sales at medium density projects in 1H13

58%

50100150200250300

Contracts on hand (by lots)2

y y p j

− Carlton, 72 sales

− Parkville, 32 sales

Pi li i ll di ifi d b l ti

050

2H11 1H12 2H12 1H13

Pipeline remains well diversified: by location, product type, ownership structure and price point

− 4 out of 9 active projects are medium density

88% f i li i i j i t t PDA

283

513

346

508

− 88% of pipeline is in joint arrangements or PDAs

High level of contracts on hand underpinned by medium density pipeline

508 gross lots ith an end al e of $225mLandMedium Density

Dec 11 Jun 12 Dec 12 Jun 13

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

− 508 gross lots with an end value of ~$225m

17

1. Pipeline by geography (by lots, includes 100% of joint arrangements and PDAs)

2. Includes 100% of joint arrangements and PDAs

For

per

sona

l use

onl

y

Residential NSW overview.

Solid 1H13 sales activity driven by demand for product priced around the median price point

− Wolli Creek, 179 sales

Pipeline typediversity (by lots)2

NSW1 ,− Clemton Park, 117 sales− The Ponds, 58 sales

77% of pipeline is built form, with strong pre-sales Built form

Land23%

NSW22%

− Wolli Creek (447 pre-sales, $266m)− Clemton Park (212 pre-sales, $111m)− Lidcombe (82 pre-sales, $56m) Contracts on hand

Built form 77%

Rezoning at Ashlar progressing with first sales expected in 2015

Greenhills Beach continues to deliver solid sales and the project is expected to be ~90% sold by

(by lots)2

389

572 543

905

40%FY14

26%FY15

and the project is expected to be ~90% sold by year end

Significant increase in contracts on hand securing revenues for FY13 to FY15

389

Dec 11 Jun 12 Dec 12 Jun 13

34%2H13

FY14

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 18

− 905 gross lots with an end value of~$500m 1. Pipeline by geography (by lots, includes 100% of joint arrangements and PDAs)

2. Includes 100% of joint arrangements and PDAs

For

per

sona

l use

onl

y

Residential SE QLD overview.

Trading conditions in Brisbane have improved as affordability and interstate migration levels recover, although consumer sentiment remains fragile

More discretionary markets (Gold Coast & Sunshine Coast) remain challenging

QLD1

10%

y ( ) g g

Hamilton & Kangaroo Point generating enquiry and sales activity with $104m of pre-sales secured

− 79 contracts with an end value of ~$60m expected to settle in 2H13$ p

Net interstate migrationg

QLD102030405060

ing

sum

(000

s)

-40-30-20-10

0

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12

Annu

al ro

lli

NSW

VIC

WA

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 19

Hamilton, QLD

Source: ANZ, Dec 2012

1. Pipeline by geography (by lots, includes 100% of joint arrangements and PDAs)

For

per

sona

l use

onl

y

Residential WA overview.

Activity levels improving as increasing rents drive conversion of tenants into owneroccupiers, particularly at the affordable end of the market

− Byford, 68 land sales at $170k average price

WA1

10%

y , $ g p

− Cockburn Central, Kingston (Stage 2) 95% pre-sold at $450k average price

− Port Coogee, 36 land sales at $520k average price

Y h t t ( 1 200 l t ) ld l b t WA G t t i ht t i d Yanchep estate (~1,200 lots) sold englobo to WA Government, management rights retained

197 gross contracts on hand with an end value of $71m

Dwelling values and rents

120130140150

g

Rents

exed

8090

100110120

'08 '09 '10 '11 '12 '13

Values

Ind

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 20

1. Pipeline by geography (by lots, includes 100% of joint arrangements and PDAs) Cockburn Central, WA

Source: RP Data

For

per

sona

l use

onl

y

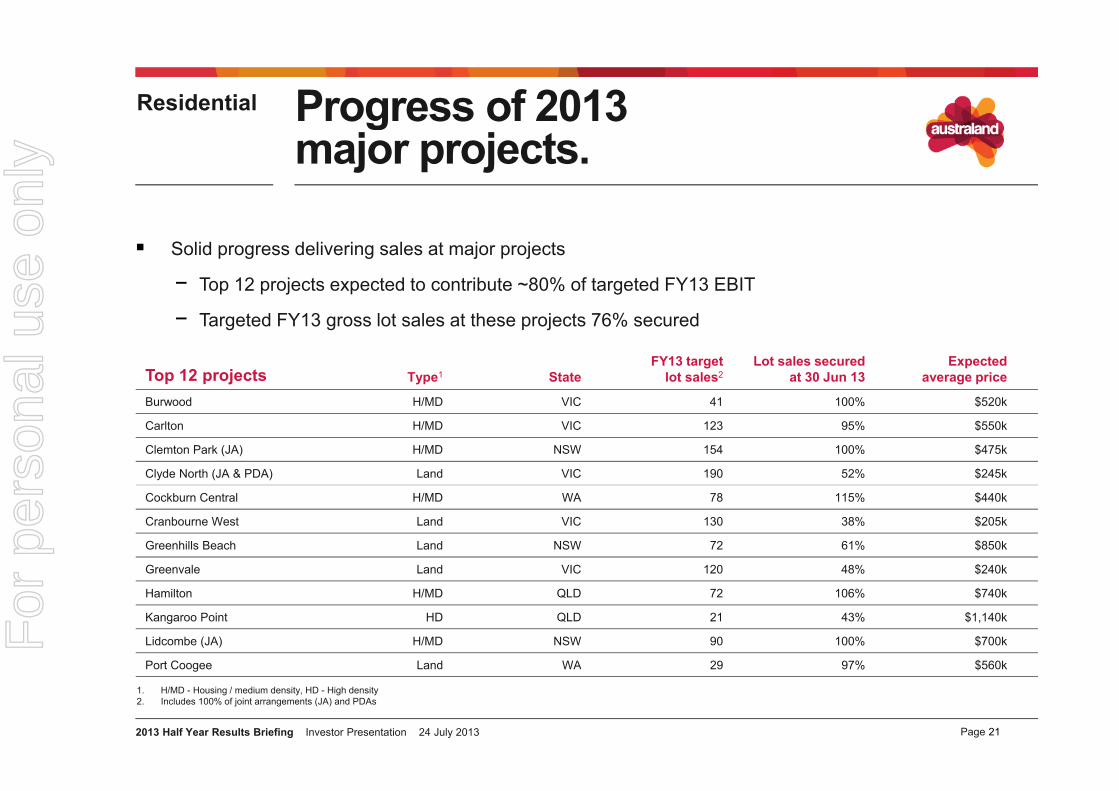

Residential Progress of 2013 gmajor projects.

Solid progress delivering sales at major projects

− Top 12 projects expected to contribute ~80% of targeted FY13 EBIT

− Targeted FY13 gross lot sales at these projects 76% secured

Top 12 projects Type1 StateFY13 target

lot sales2Lot sales secured

at 30 Jun 13Expected

average price

Burwood H/MD VIC 41 100% $520k

Carlton H/MD VIC 123 95% $550k

Clemton Park (JA) H/MD NSW 154 100% $475k

Clyde North (JA & PDA) Land VIC 190 52% $245k

Cockburn Central H/MD WA 78 115% $440k

Cranbourne West Land VIC 130 38% $205k

Greenhills Beach Land NSW 72 61% $850k

Greenvale Land VIC 120 48% $240k

Hamilton H/MD QLD 72 106% $740k

Kangaroo Point HD QLD 21 43% $1,140k

Lidcombe (JA) H/MD NSW 90 100% $700k

Port Coogee Land WA 29 97% $560k

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 21

Port Coogee Land WA 29 97% $560k

1. H/MD - Housing / medium density, HD - High density2. Includes 100% of joint arrangements (JA) and PDAs

For

per

sona

l use

onl

y

Residential 2013 outlook.

FY13 EBIT expected to be similar to FY12

− ~$330m of built form product expected to settle in 2H131

− Solid sales progress at top 12 projects

− Strong level of contracts on hand with 51% expected to settle in 2013

2H13 Major built form settlements StateNumber of contracts

on hand secured1Value of contractson hand secured1 ALZ ownership

Carlton VIC 117 $65m 65%

Hamilton QLD 76 $56m 100%Hamilton QLD 76 $56m 100%

Lidcombe NSW 61 $43m 50% & 100%

The Ponds NSW 77 $41m 20%

Clemton Park NSW 80 $40m 50%

P k ill VIC 58 $29 50%Parkville VIC 58 $29m 50%

Burwood VIC 41 $21m 100%

Cockburn Central WA 42 $19m 100%

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 22

1. Includes 100% of joint arrangements and PDAs

For

per

sona

l use

onl

y

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

Group outlook

2013 outlook.outlook

Outlook

While market conditions remain challenging, the Group continues to expect to deliver earnings growth in FY13 supported bygrowth in FY13 supported by

− Fixed increases in rental income from the Investment Property portfolio and full year contributions from internal developments

D li f C&I f d kl d k d t 2H13 ith t d l ti f 9 thi d t− Delivery of C&I forward workload skewed to 2H13 with expected completion of 9 third party projects

− Strong level of Residential contracts expected to settle in 2H13

Group earnings and distributions guidance

Group expects to deliver growth in FY13 operating earnings per security of 3-4%

FY13 di t ib ti id f 21 5 t it FY13 distribution guidance of 21.5 cents per security

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 24

For

per

sona

l use

onl

y

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

For

per

sona

l use

onl

y

Appendices Business model.

RECURRENT INCOME

INVESTMENT PORTFOLIO

GROWTH

DEVELOPMENT PIPELINE

RECURRENT INCOME(60-70% of Group EBIT)

GROWTH(30-40% of Group EBIT)

Commercial& Industrial

ResidentialOffice & Industrial & Industrial

$2.0bn1$2.3bn& Industrial

$7.6bn1

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 26

1. Estimated pipeline end values

For

per

sona

l use

onl

y

Summary of profit Appendices y pand loss statement.Financial

1H13$m

1H121

$m

Investment Property 96 88

Commercial & Industrial 10 10

Residential 22 40

Corporate (9) (13)

Operating EBIT 119 125Net interest (46) (44)

Profit before tax 73 81

Tax - -

Non-controlling interest (ASSETS) (11) (12)

Operating profit after tax (FFO)2 62 68p g p ( )

Maintenance CAPEX (2) (2)

Cash incentives (3) (11)

Adjusted funds from operations (AFFO)2 58 55

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Adjusted funds from operations (AFFO) 58 55

27

1. 1H12 EBIT and net interest restated for AASB112. Consistent with Property Council White Paper guidelines for disclosing FFO & AFFO

For

per

sona

l use

onl

y

1H13 operating Appendices p gsegment.Financial

$m Residential Commercial & Industrial

Investment Property Corporate

1H13 Consolidated

1H12Consolidated1

Property development sales 135 101 - - 236 299Rent from investment properties - - 116 - 116 106Rent from investment properties 116 116 106Interest received or receivable - - - 1 1 3Management fees from joint arrangements 7 - 2 - 9 8Other income from joint arrangements 10 - - - 10 4Sundry income 13 - 2 4 19 10Revenue from continuing operations 165 102 121 4 392 430Property development sales from joint ventures 27 7 - - 34 9Revenue including sales from joint ventures 192 108 121 4 425 440Segment result before interest and equity accounted results 25 10 92 - 126 133Sh f t fit f i t d j i t t (2) 4 2 4Share of net profits of associates and joint ventures (2) - 4 - 2 4Unallocated corporate costs - - - (9) (9) (13)Earnings before interest and tax 22 10 96 (9) 119 125Capitalised interest in cost of goods sold & other interest (47) (46)Interest income 1 3Interest income 1 3Operating profit before tax 73 81Income tax (expense)/credit on operating activities - -Net profit attributable to ASSETS hybrid equity holders (11) (12)Net operating profit after tax 62 68

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 28

1. 1H12 revenue, EBIT and interest restated for AASB11

For

per

sona

l use

onl

y

Interest Appendices

reconciliation.Financial

1H13$m

1H12$m

Gross finance costs 54 59

Less: capitalised interest – developer (23) (24)

Less: capitalised interest – investment property (0) (7)

Add: unrealised (gain)/loss on interest rate derivatives (10) 12

Finance costs in profit and loss 22 40

Less: unrealised gain/(loss) on interest rate derivatives 10 (12)g ( ) (12)

Add: capitalised interest expensed via COGS1 15 18

Finance costs included in operating profit1 47 46

Interest income 1 3

Net interest expense in operating profit1 46 44

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 29

1. 1H12 restated for AASB11

For

per

sona

l use

onl

y

Balance sheet Appendices

by segment.Financial

$m ResidentialCommercial& Industrial

Investment Property Corporate

Jun 13 Consolidated

Dec 12Consolidated1

AssetsCash and cash equivalents 16 4 8 82 110 92Receivables 174 20 16 2 213 215Inventories 846 358 - - 1,204 1,151Investment properties - - 2,337 - 2,337 2,286Investment properties held for sale - - 49 - 49 114Equity accounted investments - 9 110 - 119 126Equity accounted investments - 9 110 - 119 126Derivative financial instruments2 - - - 38 38 22Deferred tax assets - - - 30 30 30Other assets 2 - 5 37 44 47

Total assets 1,038 391 2,526 189 4,143 4,084Liabilities

Payments 62 8 29 6 106 123Interest bearing liabilities 762 285 420 - 1,466 1,393Land vendor liabilities 48 - - - 48 62Provisions 7 6 69 12 94 99Derivative financial instruments2 - - - 96 96 122

Total liabilities 880 299 518 114 1,810 1,800Net assets 158 93 2,008 75 2,333 2,284ASSETS hybrid equity 269 269 269Net assets (after hybrid) 2 064 2 015

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 30

Net assets (after hybrid) 2,064 2,015

1. Dec 12 restated for AASB112. Derivative financial instruments allocated to Corporate. Segment note in Appendix 4D allocates derivatives to Investment Property.

For

per

sona

l use

onl

y

NTA and securities on Appendices

issue reconciliation.Financial

Net tangible assets $m $ per security

As at 1 January 2013 2,015 3.49

Gains from property revaluations 17 0.03

Unrealised gain/(losses) on interest rate derivatives 26 0.04

Retained operating earnings/other 6 0.01p g g 0.01

As at 30 June 2013 2,064 3.57

Securities on issue No. of securities

As at 1 January 2013 576,846,597

Issue of securities for employee incentive scheme 4 March 2013 1,478,073

As at 30 June 2013 578,324,670

Weighted average number of securities 577,810,203

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 31

For

per

sona

l use

onl

y

Appendices Capital Financial

pmanagement.

Jun 13 Dec 12

Gearing1 33.0% 32.1%

Look-through gearing2 33.4% 33.5%

Weighted average debt maturity 2.7 yrs 3.2 yrs

Undrawn facilities plus cash $420m $436m

Weighted average cost of debt3 7 5% 7 7%Weighted average cost of debt3 7.5% 7.7%

% of debt fixed by hedges 78% 81%

Debt maturity profile

$100

$504m

$371m$350m $394m

$200m

Debt maturity profile

Undrawn$100m $134m

$29m

2H13 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

$100m$200m

Drawn

1 Interest bearing debt / total tangible assets (cash adjusted) based on the drawn amount of debt excluding fair value adjustments and associated derivative financial instruments Dec 12 restated for AASB11

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 32

1. Interest bearing debt / total tangible assets (cash adjusted), based on the drawn amount of debt excluding fair value adjustments and associated derivative financial instruments. Dec 12 restated for AASB112. Interest bearing debt plus share of off-balance sheet interest bearing debt / total tangible assets plus share of off-balance sheet assets (cash adjusted) based on the drawn amount of debt excluding fair value

adjustments and associated derivative financial instruments. Dec 12 restated for AASB113. All in cost of debt excluding establishment fees and net of interest income

For

per

sona

l use

onl

y

Reported gearing.Appendices p g gFinancial

$mStatutory balance

sheet Jun 13 Adjustments1Adjusted balance

sheet Jun 13

Cash 110 - 110

Other assets 4,033 (38) 3,995

Total tangible assets 4,143 (38) 4,105

Interest bearing liabilities 1,466 (38) 1,428

Gearing2 33.0%g 33.0%

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 33

1. The adjustments reflect the restatement of the USPP notes at the foreign currency hedge rate for the purposes of the gearing calculation2. Interest bearing debt / total tangible assets (cash adjusted), based on the drawn amount of debt excluding fair value adjustments and associated derivative financial instruments

For

per

sona

l use

onl

y

Appendices ALZ share of joint Financial

jventure balance sheet.

$m ResidentialCommercial & Industrial

Investment Property Corporate

Jun 13 Consolidated

Dec 12Consolidated1

Assets

Cash and cash equivalents 4 1 2 - 7 14Cash and cash equivalents 4 1 2 7 14

Receivables 2 1 - - 3 6

Inventories 65 13 - - 77 87

Investment properties - - 126 - 126 127

Investment properties held for sale2 - - 10 - 10 -

Other assets 33 - 1 - 34 26

Total assets 103 15 138 - 257 260

LiabilitiesPayables 55 1 2 - 58 43

Interest bearing liabilities 48 5 26 - 80 90

Land vendor liabilities - - - - - -

Provisions - - - - 1 1

Total liabilities 104 6 28 - 138 134

Equity accounted investments (0) 9 110 - 119 126

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 34

1. Dec 12 restated for AASB112. Healesville shopping centre (VIC) held for sale

For

per

sona

l use

onl

y

Liquidity and Appendices q ydebt facilities.Financial

Facility limit $m

Drawn amount $m Maturity date Security

Tranche A - syndicated 100 100 Sep 2013 Unsecured

Tranche B - syndicated 350 350 Jul 2014 Unsecured

Tranche 2015 - syndicated 304 304 Jan 2015 Unsecured

Tranche C - syndicated 200 90 Sep 2015 Unsecured

Tranche 2016 - syndicated 371 371 Sep 2016 Unsecured

Tranche D - syndicated 200 - May 2017 Unsecured

US private placement1 134 134 May 2021 Unsecured

US private placement1 29 29 May 2023 Unsecured

Total 1,688 1,378

Available facilities 310

Cash 110

Available liquidity 420

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 35

1. US private placement at initial issuance amount (excludes fair value adjustments)

For

per

sona

l use

onl

y

Debt covenants. AppendicesFinancial

Measure Covenant 1H13

Interest cover ratio (cash basis) >2.0x 2.5xEBIT / cash interest paid

Investment Property interest cover ratio >1.3x 1.8xNet operating income of IP / cash interest paid

Covenant gearing (look-through) <55% 43.8%Total liabilities plus share of off-balance sheet liabilities / total tangibleassets plus share of off-balance sheet assets (cash adjusted)

Covenant gearing (contingent liabilities) <55% 45 7%Covenant gearing (contingent liabilities) <55% 45.7%Total liabilities plus contingent liabilities / total tangible assets (cash adjusted)

Priority debt <7.5% 0.1%Secured debt / total tangible assetsSecured debt / total tangible assets

Tangible net worth >$1.7bn $2.3bnTotal tangible assets less total liabilities

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 36

For

per

sona

l use

onl

y

Interest rate Appendices

hedging profile.Financial

5.50%$1,200m

4 50%

5.00%

$800m

$1,000m

4.00%

4.50%

$400m

$600m

3.50%

$

$200m

3.00%$0m2013 2014 2015 2016 2017 2018 2019 2020

Hedge position (LHS)

Hedge rate at Dec 2012 (RHS)

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 37

g ( )

Hedge rate at Jun 2013 (RHS)

For

per

sona

l use

onl

y

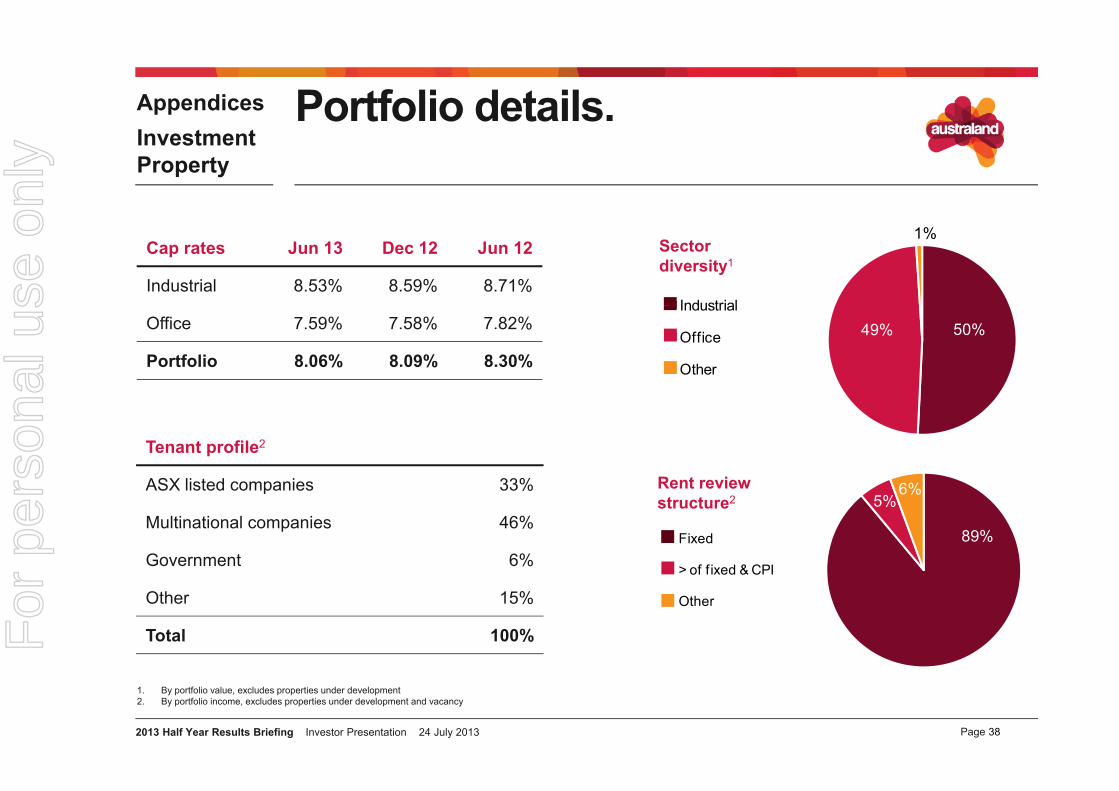

Portfolio details.AppendicesInvestment Property

Cap rates Jun 13 Dec 12 Jun 12

Industrial 8.53% 8.59% 8.71%Industrial

Sector diversity1

1%

Office 7.59% 7.58% 7.82%

Portfolio 8.06% 8.09% 8.30%

Industrial

Office

Other

50%49%

Tenant profile2

ASX listed companies 33% Rent review 6%

Fixed

> of fixed & CPI

ASX listed companies 33%

Multinational companies 46%

Government 6%

Rent review structure2

89%

5%6%

OtherOther 15%

Total 100%

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

1. By portfolio value, excludes properties under development2. By portfolio income, excludes properties under development and vacancy

38

For

per

sona

l use

onl

y

Portfolio Appendices

OffiI d t i l

diversification.Investment Property

1%5%

VICVIC

Office geographic diversity

Industrial geographic diversity

55%44%34%28%

NSW

QLD

QLD

NSW

WA & SA33%

Industrial - Key metrics Jun 13

Portfolio value $1.16bn

N b f t 51

Office - Key metrics Jun 13

Portfolio value $1.15bn

N b f t 14Number of assets 51

GLA 926,914 sqm

Occupancy (by income) 98.6%

C bl t l th 2 9%

Number of assets 14

NLA 268,314 sqm

Occupancy (by income) 91.6%

C bl t l th 3 4%Comparable rental growth 2.9%

Cap rate 8.53%

WALE (by income) 6.1 years

Portfolio age 7 2 years

Comparable rental growth 3.4%

Cap rate 7.59%

WALE (by income) 4.7 years

P tf li 7 2

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Portfolio age 7.2 years Portfolio age 7.2 years

39

Note: Metrics exclude properties under development, except for portfolio value and number of assets

For

per

sona

l use

onl

y

Lease expiry profile Appendices p y p& rent review structure.Investment

Property

Industrial lease expiry1 Office lease expiry157%

41%

1% 1%

12% 15%7% 7% 8%

2%11%

7% 10%

21%

I d t i l Offi4%

Vacancy 2H13 FY14 FY15 FY16 FY17 FY18+ Vacancy 2H13 FY14 FY15 FY16 FY17 FY18+

Other

FixedFixed

> of fixed & CPI

Industrial rent reviews2

Office rent reviews2

86%

10%94%

6%

Other> of fixed & CPI

Other

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 40

1. By portfolio income, excludes properties under development2. By portfolio income, excludes properties under development and vacancy

For

per

sona

l use

onl

y

Top 10 tenants Appendices pby income.Investment

Property

Portfolio Industrial Office

Wesfarmers - Coles & Kmart (11%) Wesfarmers - Coles & Kmart (16%) C’wealth Govt of Australia (9%)

Nestle Australia (4%) LG Electronics Australia (4%) Nestle Australia (9%)

C’wealth Govt of Australia (4%) H.J. Heinz Co. Australia (4%) PwC (7%)

PwC (3%) Toll Holdings (3%) CBA (6%)

CBA (3%) Schweppes Australia (3%) Wesfarmers - Coles (6%)

Qantas Airways (3%) DHL Global Forwarding (3%) Qantas Airways (5%)y ( ) g ( ) y ( )

LG Electronics Australia (2%) Inchcape Motors Australia (3%) TNT Australia (4%)

TNT Australia (2%) Retail Adventures (3%) State Govt of NSW (4%)

Toll Holdings (2%) Costco (3%) National Australia Bank (3%)

H.J. Heinz Co. Australia (2%) BJ Ball (2%) Service Stream (3%)

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 41

Note: By portfolio income, excludes properties under development

For

per

sona

l use

onl

y

Equity accounted Appendices q yinvestments.Investment

Property

Australand Wholesale Property Fund No. 6 (ALZ 27.9% interest) State Type

Area(sqm) Major tenants

1A Homebush Bay Drive, Rhodes NSW Office 14,639 Link Market Services 1C Homebush Bay Drive, Rhodes NSW Office 10,647 Australand, National Australia Bank 5 Butler Boulevard, Adelaide Airport SA Industrial 12,257 Tyco Industries, Bayer Material Services 80-96 South Park Drive, Dandenong South VIC Industrial 20,245 Shiro Australia and Ausmart International 34 Australis Drive, Derrimut VIC Industrial 25,243 Mitre 1089 West Park Drive, Derrimut VIC Industrial 17,024 Dempsey Group32-40 Garden Street, Kilsyth VIC Industrial 10,647 Radio Frequency Systems140 Sharps Road Tullamarine VIC Industrial 10 508 Star Track Express140 Sharps Road, Tullamarine VIC Industrial 10,508 Star Track Express

Australand Logistics Joint Venture1

(ALZ 19.9% interest) State TypeArea

(sqm) Value($m) Cap rate Major tenants

Eucalyptus Place, Eastern Creek NSW Industrial 21,694 29.7 8.25% QLS & CEVALot 122, Wonderland Drive, Eastern Creek NSW Industrial 51,709 76.6 7.75% KMart1 & 7 -15 Kellet Close, Erskine Park NSW Industrial 23,267 31.8 8.25% Strandbags & Diageog gLot 14 Powers Road, Seven Hills NSW Industrial 13,555 18.3 8.50% Sigma62 Sandstone Place, Parkinson QLD Industrial 9,260 16.1 8.00% Salmat92 Sandstone Place, Parkinson QLD Industrial 13,738 20.9 8.00% Kimberly Clark81 - 89 Drake Boulevard, Altona VIC Industrial 14,099 13.7 8.13% Schenker2-34 Aylesbury Drive, Altona VIC Industrial 17,513 15.2 8.50% Toll Altona35 61 S th P k D i D d S th VIC I d t i l 32 167 29 2 8 25% P i li35-61 South Park Drive, Dandenong South VIC Industrial 32,167 29.2 8.25% Priceline162 Australis Drive, Derrimut VIC Industrial 23,252 20.5 8.50% Queensland CottonTotal 272.0

Australand Retail Trust(ALZ 50% interest) State Type

Area(sqm)

Value($m) Cap rate Major tenants

Berwick Southside Shopping Centre Berwick VIC Retail 3 081 7 9 8 50% IGA

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 42

Berwick Southside Shopping Centre, Berwick VIC Retail 3,081 7.9 8.50% IGATotal 7.9

1. Excludes properties under development

For

per

sona

l use

onl

y

1H13 disposals.Appendices pInvestment Property

Property State TypeArea

(sqm)Sale price

($m) Major tenantsSettlement

date

111 Darlinghurst Road, Kings Cross NSW Other 13,811 65.0 Hotel (Accor Management) Jun 13

C f C J 139 Amcor Way, Campbellfield VIC Industrial 9,530 6.9 Amcor Jun 13

Sovereign Apartments, 138 Ferny Ave QLD Other N/A 0.1 N/A Jan & Jun 13

Total 72.0

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 43

For

per

sona

l use

onl

y

Pipeline positioning.Appendices p p gCommercial & Industrial

Pipeline positioning($2.0bn estimated end value)

Industrial landbankpositioning (260ha)

62%38% West27%

6%51%16%

8%

East/South East

24%25%

Industrial VIC

QLDOffice QLD

NSW

SA

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Note: Includes 100% of joint arrangements

44

For

per

sona

l use

onl

y

Forward workload.AppendicesCommercial & Industrial

Type Ownership State

Estimated end value

($m) % to goArea

(sqm)

Forward workload

(sqm)

Estimated revenue

finish% leased(by area)

% sold(by area) % built

Kangaroo Drive, Eastern Creek Internal 100% NSW 22 65% 15,750 10,230 2H13 0% 100% 35%

Sub total - Internal development

Office Max, Eastern Creek (GIC)1 Third party 100% NSW 26 100% 19,300 19,300 2H13 100% 100% 0%

Kangaroo Drive, Eastern Creek2 Owner occupier 100% NSW 25 100% 20,500 20,500 1H14 100% 100% 0%

CH2, Eastern Creek (GIC)1 Third party 50% NSW 16 40% 8,150 3,255 2H13 100% 100% 60%

Ce a Berrinba (GIC)1 Third part 100% QLD 60 15% 41 000 6 150 2H13 100% 100% 85%Ceva, Berrinba (GIC)1 Third party 100% QLD 60 15% 41,000 6,150 2H13 100% 100% 85%

Siltstone Place, Berrinba Third party 100% QLD 13 100% 9,450 9,450 2H13 0% 0% 0%

Fastline, Westpark Third party 100% VIC 42 24% 46,850 11,250 2H13 47% 100% 76%

Kimpton Way, Altona Third party 100% VIC 24 100% 25,700 25,700 2H13 0% 0% 0%

Rinnai, Keysborough Owner occupier 100% VIC 20 65% 14,800 9,600 2H13 100% 100% 35%y g p

Southern Count, Keysborough Third party 100% VIC 18 100% 17,850 17,850 2H13 0% 0% 0%

Symbion, Keysborough Third party 100% VIC 17 100% 12,800 12,800 2H13 100% 0% 0%

Sub total - For external sale 261 216,400 135,855 60% 72%

Total 283 232,150 146,085Total 283 232,150 146,085

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 45

1. Proposed for the Australand Logistics Joint Venture with GIC – ALZ interest 19.9%2. % leased under Heads of Agreement

For

per

sona

l use

onl

y

Pipeline overview.Appendices pCommercial & Industrial

Landbank OwnershipIndustrial pre-lease

Industrialland & build

Industrialspeculative

Industrialland sales Commercial

NSW Botany 100%Eastern Creek 100% & 50%Macquarie Park 50%Winston Hills 100%

QLD Berrinba 100%Northgate 100%Parkinson 50%Pinkenba 100% & 50%Richlands 100%Yatala 50%

VIC Altona 100%Dandenong 100%gFreshwater (Stage 3) 100%Keysborough 100%Laverton 100%Mulgrave 50%Rowville 100%West Park 100%

SA Beverley 100%Burbridge Business Park PDAGillman 50%

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 46

For

per

sona

l use

onl

y

Pipeline positioning.Appendices p p gResidential

Pipeline by product type

Pipeline by geography

Pipeline by price point

1%

58%10%

10%

67%24%

9%

71%28%

1%

22%

24%

VIC

NSW

Affordable

Housing &

Land

NSW

WA

QLD

Medium range

Premium rangeHigh density

Housing & medium density

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 47

Note: By number of lots, includes 100% of joint arrangements and PDAs

For

per

sona

l use

onl

y

Pipeline breakdown.Appendices pResidential

Land Housing & medium density High density

Projects 19 Projects 15 Projects 5

Lots 12,624 Lots 4,622 Lots 1,672

End value $3.8bn End value $2.7bn End value $1.1bn

1 1 1Average age1 7.1 yrs Average age1 5.4 yrs Average age1 10.8 yrs

Development life1 14.9 yrs Development life1 5.2 yrs Development life1 3.9 yrs

Elderslie NSW Carlton VIC Kangaroo Point QLD

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Elderslie, NSW Carlton, VIC Kangaroo Point, QLD

48

Note: Includes 100% of joint arrangements and PDAs1. Weighted average by lots remaining

For

per

sona

l use

onl

y

Pipeline detail.Appendices pMajor wholly owned projectsResidential

5,588 lots with an estimated on-completion value of $3.1bn

Project Type1Acquisition

dateTotal

lots Lots sold

Lots (to go)

End value to go ($m)

Contracts on hand Ownership

Revenue start

Estimated revenue

finish NSW Ashlar H/MD 2011 750 - 750 454 - 100% 2015 2019

Elderslie Land 2006 143 92 51 12 51 100% 2008 2013Greenhills Beach Land 1965 236 173 63 54 7 100% 2012 2014Lidcombe H/MD 2002 229 132 97 53 4 100% 2007 2015Wolli Creek2 HD 2002 707 707 402 100% 2014 2018Wolli Creek2 HD 2002 707 - 707 402 - 100% 2014 2018

QLD Hamilton H/MD 2010 652 12 640 522 135 100% 2012 2022Hope Island Land and H/MD 2003 516 59 457 221 5 100% 2010 2021Ivadale Lakes Land 2003 652 498 154 39 10 100% 2003 2017Kangaroo Point HD 2003 170 55 115 101 20 100% 2012 2017gPark Ridge Land 2008 319 - 319 69 - 100% 2014 2019Springfield Land 2008 279 139 140 35 13 100% 2010 2016

VIC Burwood H/MD 2008 241 200 41 21 41 100% 2011 2013Carlton H/MD 2009 675 185 490 295 176 65% 2011 2018Cranbourne West Land 2007 687 380 307 63 18 100% 2010 2015Greenvale Land 2007 659 197 462 126 36 100% 2011 2017

WA Cockburn Central H/MD 2006 795 272 523 277 61 100% 2008 2019Port Coogee Land 2005 378 130 248 324 15 100% 2007 2021

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 49

1. H/MD – Housing / medium density, HD – High density2. Project was restructured in 2011

For

per

sona

l use

onl

y

Pipeline detail.Appendices pMajor joint arrangements and PDAs1Residential

13,330 lots with an estimated on-completion value of $4.5bn

Project Type2Acquisition

dateTotal

lots Lots sold

Lots (to go)

End value to go ($m)

Contracts on hand Ownership

Revenue start

Estimated revenue

finish NSW Clemton Park H/MD 2011 721 75 646 389 212 50% (JO) 2013 2017

Lidcombe H/MD 2006 461 383 78 54 78 50% (JO) 2007 2013Shell Cove Land 1993 2,512 1,662 850 401 29 50% (PDA) 1997 2025The Ponds Land and H/MD 2003 1,323 1,245 78 44 77 20% (PDA) 2007 2014Wolli Creek3 HD 2002 788 788 560 447 50% (JO) 2014 2016Wolli Creek3 HD 2002 788 - 788 560 447 50% (JO) 2014 2016

VIC Beveridge Land 2008 3,800 - 3,800 940 - 50% (PDA) 2016 2041Clyde North Land 2007 2,588 195 2,393 723 21 50% (JO & PDA) 2011 2028Croydon Land 2004 572 345 227 80 23 50% (JV) 2009 2015Parkville H/MD 2002 858 326 532 273 138 50% (JO) 2006 2019( )Point Cook Land 2001 601 - 601 212 - 50% (JV) 2015 2019Sunbury Land 2012 391 - 391 93 - 100% (PDA) 2015 2018Sunshine H/MD 2005 658 450 208 84 51 50% (JO) 2009 2015Wallan Land 2007 1,697 382 1,315 232 4 50% (JO) 2009 2023Westmeadows H/MD 2010 221 - 221 91 - 50% (PDA) 2014 2018

WA Baldivis Land 2008 837 - 837 181 - 50% (JO) 2014 2020Byford Land 2006 400 204 196 37 64 50% (JV) 2010 2015Port Coogee Land 2005 414 317 97 113 3 50% (JO) 2006 2015

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 50

1. Includes 100% of joint arrangements (Joint operation-JO and Joint venture-JV) and PDAs2. H/MD – Housing / medium density, HD – High density3. Project was restructured in 2011

For

per

sona

l use

onl

y

Pipeline overview.Appendices pLots under management1Residential

Lots remaining End value ($m)

Housing & medium High

Housing& medium High

No. projects Land density density Total Land density density Total

NSW 11 964 1,667 1,495 4,126 466 1,011 961 2,438

VIC 14 9,502 1,492 - 10,994 2,471 766 - 3,237

QLD 7 773 937 132 1,842 200 686 117 1,003

WA 7 1385 526 45 1,956 656 278 24 958

Total 39 12,624 4,622 1,672 18,918 3,793 2,741 1,102 7,636ota 39 ,6 ,6 ,6 18,918 3, 93 , , 0 7,636

Wholly owned 19 1,910 2,856 822 5,588 780 1,805 503 3,088

JO 10 2,159 1,467 788 4,414 414 801 560 1,775

JV / PDAs 10 8,555 299 62 8,916 2,599 135 39 2,773

Total 39 12,624 4,622 1,672 18,918 3,793 2,741 1,102 7,636

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 51

1. Includes 100% of joint arrangements and PDAs

For

per

sona

l use

onl

y

Pipeline overview.Appendices pALZ share1Residential

Lots remaining End value ($m)

Housing & medium High

Housing& medium High

No. projects Land density density Total Land density density Total

NSW 11 539 1,243 1,101 2,883 266 754 681 1,701

VIC 14 5,228 840 0 6,068 1,345 438 0 1,783

QLD 7 773 937 124 1,834 200 686 109 995

WA 7 817 524 22 1,363 490 278 12 780

Total 39 7,357 3,544 1,247 12,148 2,301 2,156 802 5,259ota 39 ,35 3,5 , 12,148 ,30 , 56 80 5,259

Wholly owned 19 1,910 2,685 822 5,417 780 1,701 503 2,984

JO 10 1,080 733 394 2,207 207 401 280 888

JV / PDAs 10 4,367 126 31 4,524 1,314 54 19 1,387

Total 39 7,357 3,544 1,247 12,148 2,301 2,156 802 5,259

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

1. Includes ALZ share of joint arrangements and PDAs

52

For

per

sona

l use

onl

y

Appendices Pipeline emergence.Residential

p gMajor built form projects

Project Stage State 2H13 2014 2015Hamilton Watermarque QLD 78 lots (85% pre-sold)

Built form projects underpin earnings momentum in the medium term

qClemton Park Air NSW 78 lots (100% pre-sold)

Burwood 333 Burwood VIC 32 lots (100% pre-sold)

Carlton Local Carlton VIC 120 lots (98% pre-sold)

Parkville Hyde VIC 58 lots (100% pre-sold)

Cockburn Central Kingston (Stage 2) WA 44 lots (95% pre sold)Cockburn Central Kingston (Stage 2) WA 44 lots (95% pre-sold)

Hamilton Watermarque on the Park QLD 68 lots (72% pre-sold)

Wolli Creek Linc NSW 126 lots (99% pre-sold)

Wolli Creek Arc NSW 88 lots (100% pre-sold)

Wolli Creek Watervue NSW 74 lots (91% pre-sold)

Clemton Park Lime NSW 70 lots (89% pre-sold)

Carlton Zest Carlton VIC 105 lots (56% pre-sold)

Parkville The Green VIC 57 lots (100% pre-sold)

East Perth Bronte WA 48 lots (92% pre-sold)

Cockburn Central Kingston (Stage 3) WA 39 lots (49% pre-sold)g ( g )Kangaroo Point Linc QLD 45 lots (27% pre-sold)

Wolli Creek Summit NSW 200 lots (84% pre-sold)

Clemton Park Mint NSW 90 lots (13% pre-sold)

Clemton Park Olive NSW 64 lots (91% pre-sold)

Parkville Jardin VIC 68 Lots (34% pre-sold)

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013

Note: Includes 100% of joint arrangements and PDAs

53

Parkville Jardin VIC 68 Lots (34% pre-sold)

For

per

sona

l use

onl

y

1H13 lots sold.Appendices

ALZ share1Residential

VIC

Lot sales by geography

Land 1H13

Lots sold 279

R $119 32%

14%

VIC

NSW

WA

Revenue $119m

Average sale price2 $469k

Housing & medium density 1H13

32%

27%

27%

QLDHousing & medium density 1H13

Lots sold 116

Revenue $64m2 $

27%

4%

Land

Lot sales by segment

Average sale price2 $547k

High density 1H13

Lots sold 14 68%28%

4%

High density

Housing & medium density

LandLots sold 14

Revenue $9m

Average sale price $643k

68%8%

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 54

1. Includes ALZ share of joint arrangements and PDAs2. Average sale price adjusted to exclude lots and revenue sold under PDA structures as sales from PDAs are not included in reported revenue

For

per

sona

l use

onl

y

1H13 lots sold by state.Appendices

L t ld NSW VIC WA QLD T t l

yALZ share1Residential

Lots sold NSW VIC WA QLD Total

Land 53 117 59 50 279

Housing & medium density 56 7 53 - 116

High density - 8 - 6 14

Total 109 132 112 56 409

Wholly owned 41 68 61 56 226

JO 44 41 21 - 106

JV / PDA 24 23 30 77JV / PDAs 24 23 30 - 77

Total 109 132 112 56 409

Revenue ($m) NSW VIC WA QLD Total

L d2 30 25 53 11 119Land2 30 25 53 11 119

Housing & medium density2 30 11 23 - 64

High density - 2 - 7 9

Total 60 38 76 18 192

Wholly owned 30 20 26 18 94

JO 24 12 24 - 60

JV / PDAs 6 6 26 - 38

Total 60 38 76 18 192

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 55

Total 60 38 76 18 1921. Includes ALZ share of joint arrangements and PDAs2. Excludes revenue from projects under PDA structures

For

per

sona

l use

onl

y

Disclaimer.HY13ResultsResults Briefing

Australand Holdings Limited (ABN 12 008 443 696)Australand Property Limited (ABN 90 105 462 137; AFSLN 231 130) as the responsible entity of Australand Property Trust (ARSN 106 680 424) and Australand ASSETS Trust (ARSN 115 338 513)Trust (ARSN 106 680 424) and Australand ASSETS Trust (ARSN 115 338 513) Australand Investments Limited (ABN 12 086 673 092; AFSLN 228 837) as the responsible entity of Australand Property Trust No.4 (ARSN 108 254 413) and Australand Property Trust No.5 (ARSN 108 254 771)

Level 3, 1C Homebush Bay DriveRhodes NSW 2138Rhodes NSW 2138Ph: +61 2 9767 2000Fax: +61 2 9767 2900

Disclaimer of liabilityWhile every effort is made to provide accurate and complete information, Australand does not warrant or represent that the information in this presentation is free from errors or omissions or is suitable for the recipients’ intended use. Subject to any terms implied by law and which cannot be excluded, Australand accepts no responsibility for any loss, damage, cost or expense (whether direct or indirect) incurred by any recipient as a result of any error, omission or misrepresentation in information in this presentation. All information in this presentation is subject to change without notice.

Page Investor Presentation2012 Half Year Results Briefing26 June 2012

Page2013 Half Year Results Briefing Investor Presentation 24 July 2013 56

Note: All numbers subject to rounding

For

per

sona

l use

onl

y