form 5471 for interests in foreign entities after tax...

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Form 5471 for Interests in Foreign Entities After Tax Reform

WEDNESDAY, JUNE 12, 2019, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

June 12, 2019

Form 5471 for Interests in Foreign Entities After Tax Reform

Alison N. Dougherty, J.D., LL.M., Director, Tax Services

Aronson LLC

John Samtoy, Tax Principal

Holthouse Carlin & Van Trigt

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

FOCUS • CLARITY • COMMITMENT

FORM 5471: REPORTING REQUIREMENTS AFTER TAX REFORM

June 12, 2019John Samtoy, HCVT [email protected]

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - TOPICS COVERED

I. Overview and Background

II. Filing Requirements

III. Attribution and Control

IV. Exceptions to Filing

V. Penalties and Remediation

6

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

OVERVIEW AND BACKGROUND

• Form 5471, Information Return of U.S. Persons With Respect To Certain

Foreign Corporations

• The requirements to file are established in IRC §§ 6038 and 6046.

• Form 5471 is an important IRS tool for assessing the scope of a

taxpayer's foreign holdings and operations.

• The Form is also useful for keeping track of the earnings and profits of

foreign corporations, determining whether an entity has undergone a

taxable restructuring event or change in ownership, and determining

whether a foreign entity is generating any income that may be subject

to current U.S. tax under an anti-deferral regime.

• Subpart F income, GILTI, 956, 965 deemed repatriation.

7

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

OVERVIEW AND BACKGROUND

• International Tax Enforcement

• Global efforts to combat base erosion, hybrid instruments - BEPS,

CBCR, ATAD.

• Cooperation between tax authorities (J5)

• Push towards global transparency – FATCA, CRS

• IRS LB&I Campaigns

• Loose Filed Forms 5471, OVDP Declines-Withdrawals Campaign,

Related Party Transactions Campaign, Repatriation via Foreign

Triangular Reorganizations, Section 965 Transition Tax, Section 956

Avoidance

8

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FILING REQUIREMENTS - FILING CATEGORIES

• Category 1 Filer (new) – A U.S. shareholder of a section 965 specified foreign corporation (SFC) at any during the year that also owned the stock on the last day in the year that it was an SFC.

• SFC = a CFC or

• FC that is not a CFC or PFIC to the extent that there is a U.S. corporate shareholder.

• Category 2 Filer is a U.S. citizen or resident who is an officer or director of a foreign corporation in which a U.S. person has acquired the requisite shares (10% vote or value) in one or more transactions.

• Category 3 Filer is a U.S. person who acquires or disposes of shares in a foreign corporation and exceeds or falls below a 10% ownership threshold, a U.S. person who acquires stock that would on its own meet the 10% threshold, or a person who becomes a U.S. person while meeting the requisite ownership requirements.

9

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FILING REQUIREMENTS - FILING CATEGORIES

•A Category 4 Filer is a U.S. person who had “control” of a foreign

corporation during the accounting period of the foreign corporation.

• 30 day requirement is gone.

•A Category 5 Filer is a “U.S. shareholder” that owns stock in a foreign

corporation that is a CFC at any time during the year (30 day

requirement gone) and that owned that stock on the last day of the

year in which it was a CFC.

• A “U.S. Shareholder” is defined as a U.S. Person that owns 10% of

a foreign corporation (vote or value) directly or indirectly or

constructively.

• A CFC is a foreign corporation with U.S. Shareholders that own

more than 50% of the vote or value of the corporation.

1 0

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

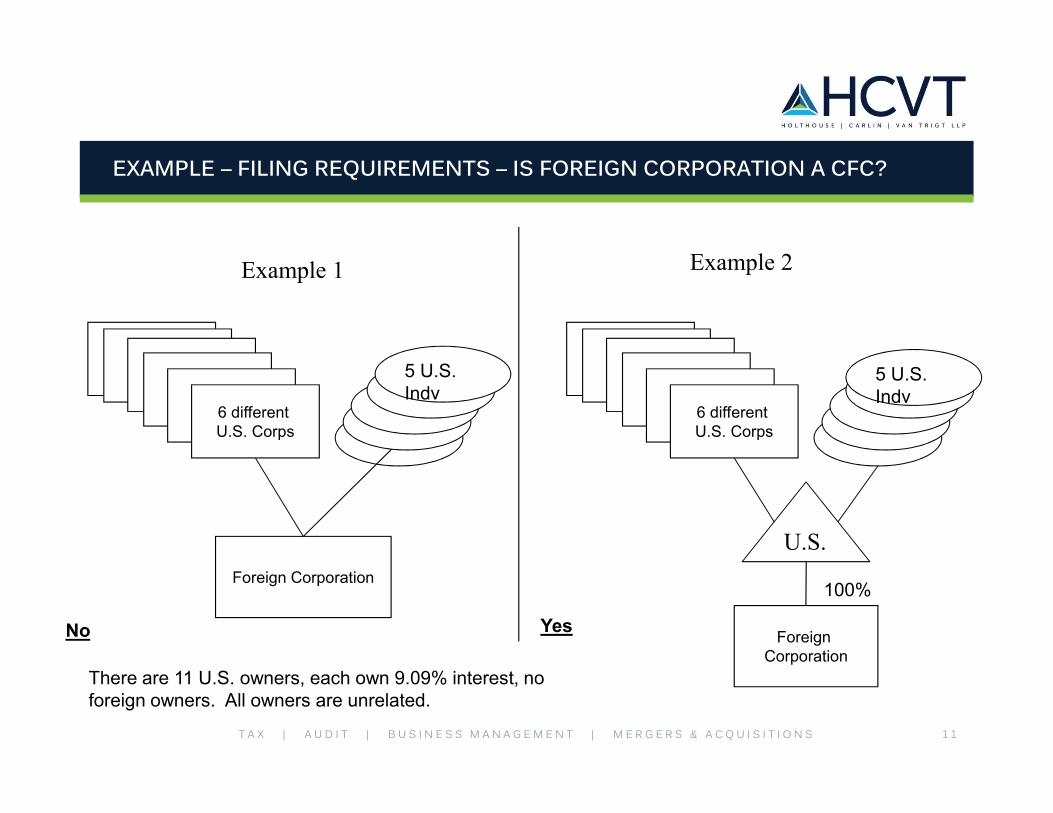

EXAMPLE – FILING REQUIREMENTS – IS FOREIGN CORPORATION A CFC?

Example 1

Foreign Corporation

6 different U.S. Corps

5 U.S. Indv

There are 11 U.S. owners, each own 9.09% interest, no foreign owners. All owners are unrelated.

No YesForeign

Corporation

6 different U.S. Corps

Example 2

U.S.

100%

5 U.S. Indv

1 1

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE – FILING REQUIREMENTS – IS FOREIGN CORPORATION A CFC?

No Yes

U.S. 1

Example 3

Foreign Corporation

FC U.S. 2 U.S. 3

45% 9% 9% 37%

U.S. 1

Example 4

Foreign Corporation

FC U.S. 2 U.S. 3

45% 15% 9% 31%

1 2

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

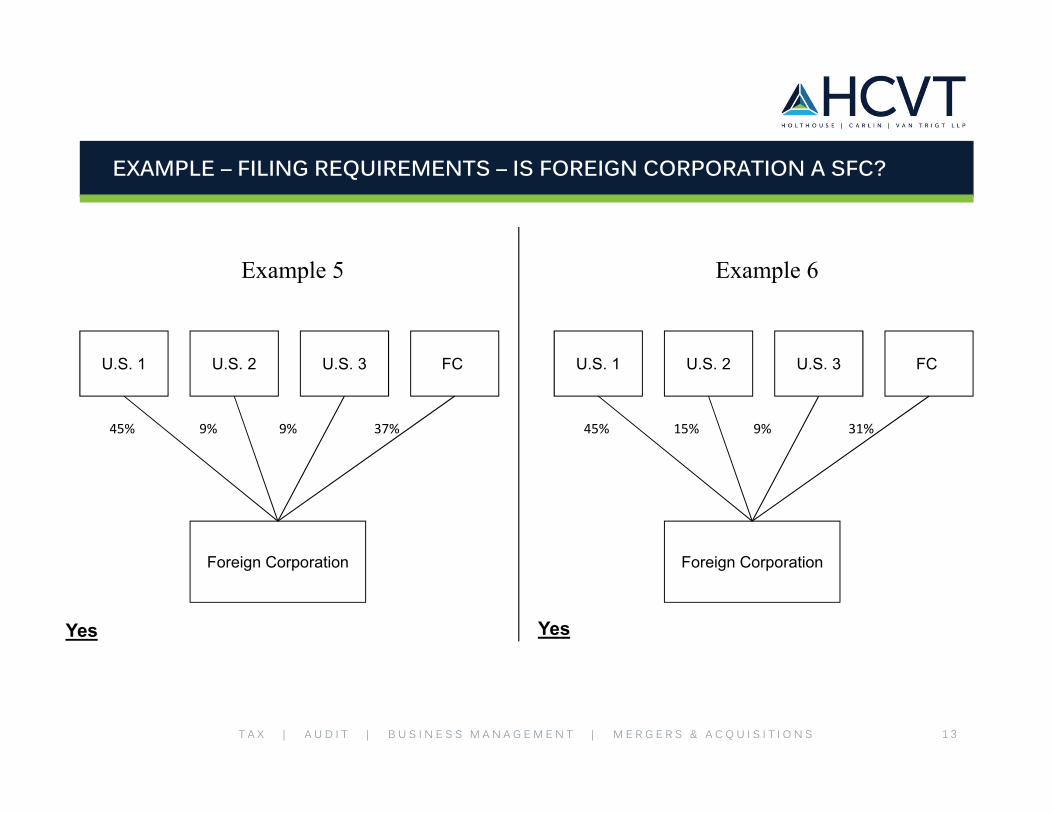

EXAMPLE – FILING REQUIREMENTS – IS FOREIGN CORPORATION A SFC?

Yes Yes

U.S. 1

Example 5

Foreign Corporation

FC U.S. 2 U.S. 3

45% 9% 9% 37%

U.S. 1

Example 6

Foreign Corporation

FC U.S. 2 U.S. 3

45% 15% 9% 31%

1 3

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

ATTRIBUTION AND CONTROL – DETERMINING TOTAL OWNERSHIP

•Determining ownership of a foreign company is not as straightforward as looking at a U.S.

person’s direct ownership percentage. Attribution rules can combine direct, indirect, and

constructive ownership to determine total ownership of a foreign corporation.

•There are attribution rules for a variety of purposes and the rules are not always the same.

Attribution is used to determine:

• Acquisitions and dispositions reporting total ownership determination - § 1.6046-1(i) –

includes siblings – Category 3

• Determination of control for information reporting requirements - § 1.6038-2(c) based on

§318 with modifications – Category 4

• Determining U.S. Shareholder and CFC status - IRC § 958(b) – based on §318 with

modifications – Category 5

•Indirect – IRC § 958(a) stock owned through foreign entities is treated as being actually

proportionately owned.

•Constructive Ownership – IRC § 318(a) as modified by IRC § 958(b)

1 4

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

ATTRIBUTION AND CONTROL – ATTRIBUTION RULES

a) Family – Induvial owns stock owned directly or indirectly by spouse, children, grandchildren, and parents.

b) From partnerships – stock is owned proportionately by partners.

c) From corporations – If 10% or more of the value is owned, then considered to own the stock owned by the

corporation proportionately .

d) To Partnership – partnership is considered to own stock owned by the partner.

e) To Corporations – If 50% or more of a corporation is owned, then corporation will own stock owned by

shareholder.

f) Do not attribute from NRA or nonresident entity for purposes of (a), (d), or (e)

a) “Downward” attribution after tax reform; Limitation on family attribution from an NRA still applies

g) For (b) and (c) if a partnership or corporation owns more than 50% of the voting stock it shall be

considered to own all of the voting stock.

h) Do not re-attribute stock owned by reason of:

a) (a) for re-applying (a) to another person.

b) (d) or (e) for applying (b) or (c) to another person

1 5

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

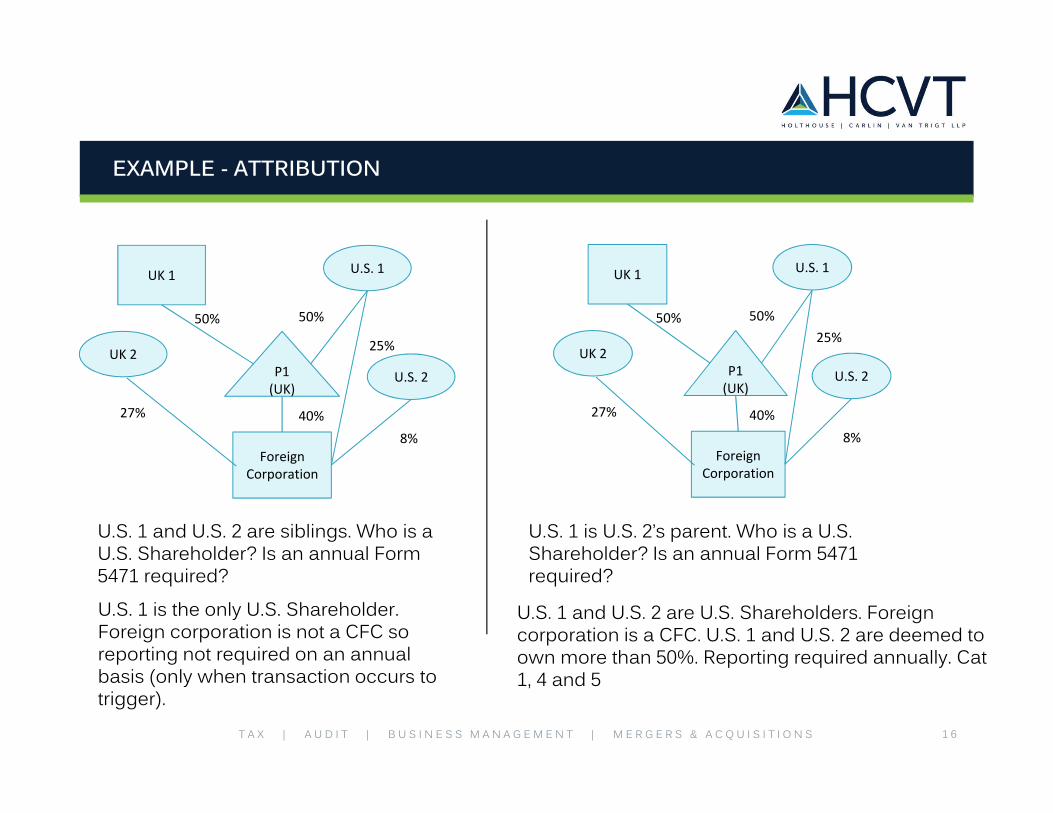

EXAMPLE - ATTRIBUTION

1 6

50%50%

25%

U.S. 1

Foreign Corporation

UK 1

P1 (UK)

40%

UK 2

U.S. 2

8%

27%

U.S. 1 and U.S. 2 are siblings. Who is a U.S. Shareholder? Is an annual Form 5471 required?

U.S. 1 is the only U.S. Shareholder. Foreign corporation is not a CFC so reporting not required on an annual basis (only when transaction occurs to trigger).

50%50%

25%

U.S. 1

Foreign Corporation

UK 1

P1 (UK)

40%

UK 2

U.S. 2

8%

27%

U.S. 1 is U.S. 2’s parent. Who is a U.S. Shareholder? Is an annual Form 5471 required?

U.S. 1 and U.S. 2 are U.S. Shareholders. Foreign corporation is a CFC. U.S. 1 and U.S. 2 are deemed to own more than 50%. Reporting required annually. Cat 1, 4 and 5

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE – CONSTRUCTIVE OWNERSHIP AFTER TCJA

1 7

• Under prior law, U.S. Sub would not be a U.S. shareholder of FC 1 because section 958(b)(4) prevented constructive ownership under section 318 from a foreign person to a U.S. entity.

• After the repeal of §958(b)(4), U.S. Sub is considered to have constructive ownership of Foreign Sub and thus Foreign Sub is considered a CFC.

• Jill is allocated subpart F income because she is a >10% indirect shareholder of FC 1 which is now a CFC.

FC 1

Foreign Corp

FP

Jill(U.S.

resident)

15% 85%

100%

U.S. Sub

100%

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE – CONSTRUCTIVE OWNERSHIP AFTER TCJA

1 8

• Potential for future guidance –

• May 1st 2019 – IRS technical reviewer announces that the IRS intend to address “… non-Subpart F issues caused by the repeal of Section 958(b)(4) to the extent we have authority to do so”

• May 20th 2019 – Proposed regulations limit downward attribution for determining related party and control but only for determining related parties for Subpart F (954).

FC 2

FC 1

100%

U.S. Sub

100%

Jill(U.S.

resident)FP1

15% 85%

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

ATTRIBUTION AND CONTROL – CONTROL (CATEGORY 4)

• A person in control of a corporation which, in turn, owns more

than 50 % of the vote or of the value of all classes of stock of

another corporation is also treated as being in control of that

other corporation.

• A U.S. C corporation ABC Co is a 51 % owner of a U.S.

corporate joint venture and the joint venture entity controls a

foreign corporation. As a result, ABC Co controls the foreign

corporation

• Steve, a U.S. person, owns 51% of foreign company X. Foreign

company X owns 51% of foreign company Y. Steve controls

both foreign company X and foreign company Y.

1 9

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE - CONTROL (CATEGORY 4)

2 0

U.S. Corp 1

FC 1

FC 2

U.S. Person

51%

51%

51%

Foreign 3rd Party

49%

Foreign 3rd Party

49%

• What is U.S. Person’s ownership of FC 1 and FC 2?

• Using Category 4 constructive ownership rules we get to:

• FC 1 – 26%• FC 2 - 13%

• U.S. Person controls both FC 1 and FC 2 for Category 4 filing purposes.

• Is FC 2 a CFC ? • YES – if more than 50% of voting

stock is owned then 958 attribution rules state that all voting stock shall be considered owned. See examples in 1.958-2(g)

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE – ATTRIBUTION

2 1

Example From Reg 1.958-2(g)

Y(foreign)

G1 G2 G3 G4 FE

15%

5%20% 20% 20%

20%

• Facts: United States citizen E owns 15 percent of the one class of stock in foreign corporation Y, and United States citizen F, E's spouse, owns 5 percent of such stock. E and F's four nonresident alien grandchildren each own 20 percent of the stock in Y Corporation.

Abbreviated analysis:

• E owns what F owns and F owns what E owns so they each constructively own 20 % of the stock of Y.

• E and F are not attributed any of the stock that G1-G4 own because of the restriction on family attribution from an NRA.

• What if G1 and G2 moved to the U.S. to attend college and became U.S. persons?

• Interests of G1 and G2 would be attributed to E and F and interests of E and F would be attributed to G1 and G2.

• Y would be a CFC. E, F, G1, and G2 would be U.S. shareholders of Y.

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FILING EXCEPTIONS – MULTIPLE FILERS

• One person may file Form 5471 and the applicable schedules for

other persons who have the same filing requirements

• For example, a category 4 filer may file on behalf of a category

5 filer

• Category 3 filers - form may only by filed by another person

having an equal or greater interest (measured in terms of vote

or value)

• The person filing Form 5471 must complete item F on page 1 of the

form.

• All persons identified in F must attach a statement to their income

tax return. Category 1, 4, and 5 filers – must attach Schedule P

2 2

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FILING EXCEPTIONS – MULTIPLE FILERS

2 3

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FILING EXCEPTIONS – CONSTRUCTIVE OWNERS

•A U.S. person described in Category 1, 3, 4 or 5 does not have to file Form 5471

if all of the below apply:

• The U.S. person does not own a direct interest in the foreign corporation,

• The U.S. person is required to furnish the information requested solely

because of constructive ownership from another U.S. person, and

• The U.S. person through which the U.S. person constructively owns an

interest in the foreign corporation files Form 5471 to report all of the required

information.

•The instructions clarify that there is no statement that needs to be attached for

persons claiming the constructive owners exception. The regulations have

been updated to reflect this as well (previously some ambiguity).

2 4

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

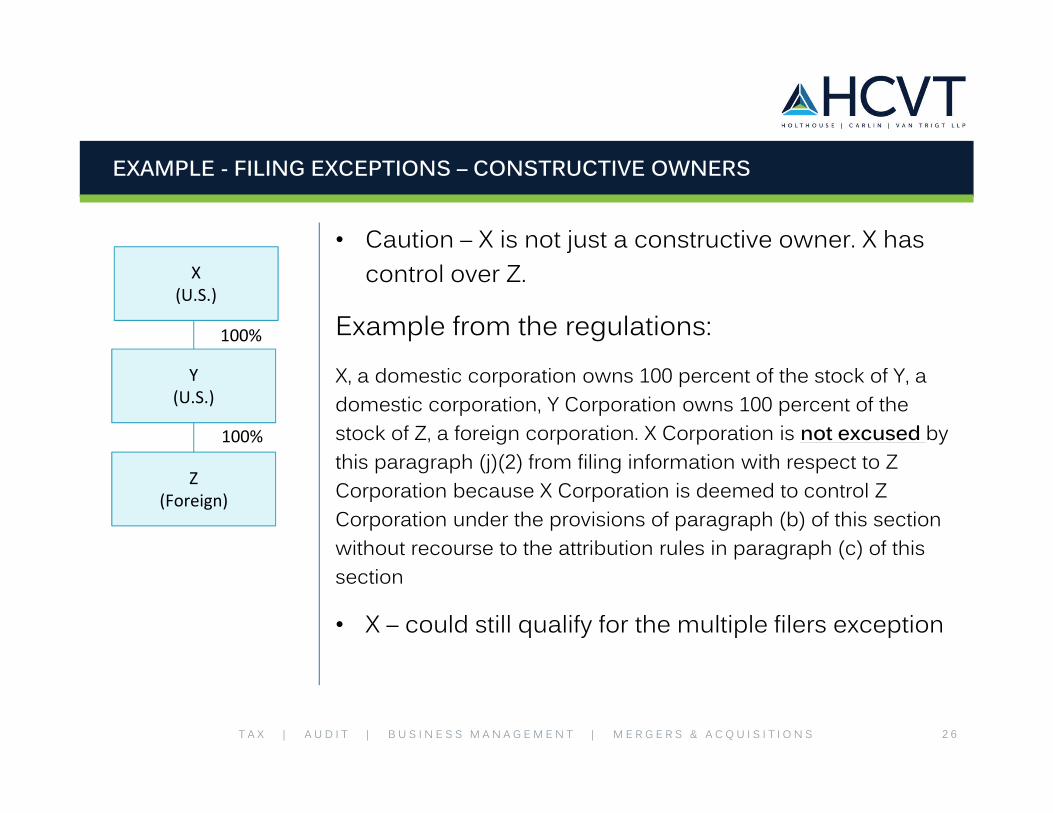

EXAMPLE - FILING EXCEPTIONS – CONSTRUCTIVE OWNERS

2 6

Y(U.S.)

Z(Foreign)

100%

100%

X(U.S.)

• Caution – X is not just a constructive owner. X has

control over Z.

Example from the regulations:

X, a domestic corporation owns 100 percent of the stock of Y, a

domestic corporation, Y Corporation owns 100 percent of the

stock of Z, a foreign corporation. X Corporation is not excused by

this paragraph (j)(2) from filing information with respect to Z

Corporation because X Corporation is deemed to control Z

Corporation under the provisions of paragraph (b) of this section

without recourse to the attribution rules in paragraph (c) of this

section

• X – could still qualify for the multiple filers exception

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - FILING EXCEPTIONS – CONSTRUCTIVE OWNERS

2 7

Example from the regulations:

A, a U.S. person owns 100 percent of the stock of M, a domestic corporation. A also

owns 100 percent of the stock of N, a of foreign corporation. A files a Form 5471

furnishing all of the information required of M Corporation with respect to N

Corporation. M Corporation does not need to file a Form 5471.

M (U.S.)N (FC)

100%

A (U.S.)

100%

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - FILING EXCEPTIONS – CONSTRUCTIVE OWNERS

• Category 2 filer is not required to file if either of the below apply:

• Immediately after the acquisition, 3 or fewer U.S. persons own

95% or more of the CFC and the U.S. acquirer is filing a

category 3 Form 5471; or

• U.S. person for which the Category 2 filer is required to file does

not directly own an interest in FC but is required to file under

constructive ownership rules and the U.S. person from whom

the stock ownership is attributed properly files Form 5471.

• Category 4 or 5 filers – constructive from nonresident alien

• U.S. person does not own a direct or indirect interest and is

required to file solely due to constructive ownership from a

non-resident alien.

2 8

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - FILING EXCEPTIONS – CONSTRUCTIVE OWNERS

• Category 1 or 5 filers – exception for downward attribution

• No U.S. shareholder (including potential filer) owns the foreign

corporation directly or indirectly through foreign entities and

the foreign corporation is an SFC or CFC solely because of

downward attribution from a foreign person to a U.S. entity.

• Limited to scenarios where there is no U.S. shareholder other

than a U.S. shareholder from downward attribution.

2 9

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

EXAMPLE – DOWNWARD ATTRIBUTION FILING EXCEPTION

3 0

FC 1

Foreign Corp

FP

Jill(U.S.

resident)

15% 85%

100%

U.S. Sub

100%

FC 1

Foreign Corp

FP

Jill(Foreign)

15% 85%

100%

U.S. Sub

100%

Exception does not apply Exception does apply

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - FILING EXCEPTIONS – ENTITIES TREATED AS DOMESTIC CORPORATIONS

• Forms 5471 are not required for certain entitles that are treated as

domestic corporations.

• Form 5471 not required for insurance companies that have elected

under section 953(d) to be treated as domestic and have filed their

U.S. income tax returns.

• Category 4 filers are not required to file a Form 5471 for a

corporation defined in section 1504(d) that files a consolidated

return for the tax year.

3 1

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - APPLICABLE FOREIGN CORPORATIONS

•What is an association taxable as a corporation (“corporation”)? Consider the check-the-box regulations.

• By default a foreign entity with limited liability for all members will be treated as a foreign corporation. An entity with unlimited liability for at least one member will be treated as a pass-through.

• A member of a foreign eligible entity has limited liability if the member has no personal liability for the debts of or claims against the entity by reason of being a member

• We are permitted to elect whether or not a foreign entity is treated as a corporation or pass-through by filing Form 8832 “check-the-box” election.

• If we are dealing with a per se corporation, it is a corporation for U.S. tax purposes.

• The foreign legal form of the entity can be useful in classifying it e.g., SA or SrL

•Remember that a separate 5471 is required for each foreign entity even if it is included in a foreign consolidated group, e.g., a German “Organschaft.”

3 2

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - PENALTIES

•IRC §§ 6038(a) and 6046 - Penalties for failure to file Form 5471, Schedule M, and Schedule O

• $10,000 failure to file penalty is automatically imposed for each late or incomplete Form 5471

• If not filed within 90 days after IRS notice of failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof up to $50,000 per Form per year.

•IRC §6038(c) – 10% reduction of foreign taxes available for credit under 901 and 960.

• If the failure continues 90 days or more after the IRS mails a notice of failure, an additional 5% reduction for each 3-month period (or fraction thereof) during which the failure continues after the 90-day period has expired.

• Limitation on the 6038(c) penalties - the greater of $10,000 or the income of the foreign business entity for its annual accounting period with respect to which the failure occurs.

3 3

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 - PENALTIES

•IRC §6662(j) – 40% accuracy related penalty for underpayments of tax

as a result of transactions involving an undisclosed specified foreign

financial asset.

•IRC §6501(c)(8) – Will keep the statute of limitations open indefinitely

when information is required to be reported under Sections 6038,

6038A, 6038B, 6046, 6046A or 6048 and is not reported.

3 4

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 – PENALTY REMEDIATION

•Abatement, reduction, or modification of penalties is possible.

• Taxpayers now have several options for submitting late returns due to IRS efforts to encourage taxpayers to come forward.

• Quiet Disclosure

• Delinquent International Information Return Submission Procedures

• OVDP - Program has ended

• New disclosure program with CI

• Streamlined Filing Compliance Procedures

• Reasonable cause – Where taxpayer can demonstrate that failures to file are due to reasonable cause and not due to willful neglect.

• The regulations indicate what the IRS deems reasonable cause as exercising “ordinary business care and prudence”.

• The Internal Revenue Manual says that “ordinary business care and prudence standard requires that taxpayers make reasonable efforts to determine their tax obligations.... Reasonable cause may be established if the taxpayer shows ignorance of the law in conjunction with other facts and circumstances”

3 5

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 – PENALTY REMEDIATION

• Reliance on a professional advisor constitutes reasonable cause where special training is required – U.S. v. Boyle

• Neonatology Assocs., P.A. – confirms that taxpayers may rely on a professional advisor and establishes three factors for reliance:

• The advisor was a competent professional with sufficient expertise to justify reliance.

• The taxpayer provided necessary and accurate information to the adviser.

• The taxpayer actually relied in good faith on the adviser’s judgement.

• Reliance on a professional advisor continues to be upheld – See James v. U.S.

• Complexity is a factor that should be considered – IRM, Court cases –Congdon v. U.S. , Dillin v. Commissioner

3 6

T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

FORM 5471 – PENALTY REMEDIATION – STREAMLINED FILING

• Eligibility for individuals including estates. Two separate programs:

• Streamlined Foreign Offshore Procedures - resident outside the U.S.

• Streamlined Domestic Offshore Procedures – U.S. residents

• Both - filers must certify failure to file was not due to willful conduct

• Payment Requirements:

• Full amount of tax and interest

• 5% of highest aggregate balance for any year (Domestic only)

• Foreign Offshore Procedures requirements for eligibility:

• U.S. citizens or green card holders - 1 of last 3 years did not have a U.S. abode and outside the U.S. for at least 330 days during the year

• Non-U.S. citizens and non-green card holders - 1 of the last 3 years the individual did not meet the substantial presence test

• Filing Requirements: three most recent years’ U.S. tax returns (including information returns) and six most recent years’ FBARs

3 7

3 8T A X | A U D I T | B U S I N E S S M A N A G E M E N T | M E R G E R S & A C Q U I S I T I O N S

JOHN SAMTOY – INTERNATIONAL TAX PRINCIPAL HCVT LLP

Alison N. Dougherty, J.D., LL.M.

Director, Tax Services

Aronson LLC

Rockville, Maryland USA

Washington, DC Metro Area© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 for Interests in Foreign Entities after Tax Reform

New Schedules, Determining Ownership Share and Correct Filing Status

June 12, 2019

© 2019 | All Rights Reserved | Alison N. Dougherty | 40

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, New and Revised Schedules

Page 1 New Filer Category 1 Schedule B, Part II Direct Shareholders of Foreign Corporation Schedule C Income Statement Schedules E and E-1 Foreign Taxes Paid or Accrued

and Tracking by E&P Schedule F Balance Sheet Schedule G Other Information (Extensive Questions) Schedule I Summary of Shareholder’s Income from Foreign

Corporation Schedule I-1 Information for Global Intangible Low-Taxed

Income (GILTI) Schedule J Accumulated Earnings and Profits (AEP) of CFC Schedule M Transactions between CFC and Shareholders or

Other Related Persons Schedule P Previously Taxed Earnings and Profits (PTEP)

© 2019 | All Rights Reserved | Alison N. Dougherty | 41

© 2019 | All Rights Reserved | Alison N. Dougherty | 42

Form 5471 Page One

All Filer Categories Must Complete Page One Information

Filer Categories 3 and 4 Complete Schedule A

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Page One

Form 5471, Page One Filer’s Name, address, FEIN of the foreign corporation Required tax year of the foreign corporation Line B check boxes for filer categories 1, 2, 3, 4, and 5 Line C total percentage of the voting stock owned at end of the foreign

corporation’s tax year Filer’s tax year Line D check box if final Form 5471 filed for the foreign corporation Line E check box to indicate if stock is an excepted foreign financial

asset with respect to Form 8938 Line F to indicate person on whose behalf the Form 5471 is filed

(another shareholder, officer, or director) Lines 1a through 1c foreign corporation’s name, address, FEIN,

reference ID number, and country of incorporation Lines 1d through 1h report date of incorporation, principal place of

business, business activity code number, principal business activity, and functional currency

Line 2a name, address, and identifying number of U.S. branch or agent Line 2b(i) and (ii) indicate U.S. taxable income or loss and U.S. tax paid Line 2c statutory or resident agent’s name and address in country of

incorporation Line 2d name and address of person with custody of books and records,

and location of books and records, if different Schedule A Stock of the Foreign Corporation (a) description of each

class of stock, and (b) number of shares issued and outstanding at beginning and end of annual accounting period

43

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Page One Updates

Form 5471, Page One Updates – New Filer Category 1 New filer category 1 for a U.S. shareholder of a foreign corporation that

is subject to the transition tax provisions of I.R.C. § 965. I.R.C. § 965 imposed a one-time toll charge on a U.S. shareholder’s

share of the non-previously taxed and undistributed earnings and profits of a foreign corporation determined as of 11/2/2017 or 12/31/2017, whichever was greater.

I.R.C. § 965 applies to a U.S. shareholder for the year of the U.S. shareholder that ends with or within the last year of the foreign corporation that begins before 1/1/2018.

A U.S. shareholder is a direct, indirect, or constructive shareholder of the foreign corporation that owns 10% or more of the vote of the foreign corporation (or value for a tax year of the foreign corporation beginning after 12/31/2017).

Specified foreign corporation is a controlled foreign corporation (CFC) owned more than 50% by U.S. shareholders or a foreign corporation with at least one U.S. C corporation shareholder.

Only an I.R.C. § 958(a) U.S. shareholder would have an actual I.R.C. § 965 transition tax inclusion, I.R.C. § 951A GILTI inclusion, or Subpart F income inclusion.

44

© 2019 | All Rights Reserved | Alison N. Dougherty | 45

Form 5471 Page TwoSchedule BParts I and II

Filer Categories 3 and 4 Complete Part I

Filer Categories 1, 3, 4, and 5 Complete Part II

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Page Two

Schedule B, Parts I and II

Form 5471, Page Two – Schedule B, Parts I and II Category 3 and 4 filers complete Schedule B, Part I for U.S. persons that

owned at any time during the year 10% directly or indirectly through foreign entities (I.R.C. § 958(a) U.S. shareholders).

Part I U.S. Shareholders of Foreign Corporation report name, address, ID number, description of each class of stock held corresponding to Schedule A, number of shares held at beginning and end of annual accounting period, Subpart F income percentage

Category 1, 3, 4, and 5 filers must complete Schedule B, Part II. Part II Direct Shareholders of Foreign corporation report name,

address, ID number, number of shares held at beginning and end of annual accounting period

For FDE shareholders of the foreign corporation, report the regarded entity owner of the FDE on the Schedule B.

Category 1, 3, or 5 filers must report direct owners through which they indirectly own the foreign corporation on Part II.

46

© 2019 | All Rights Reserved | Alison N. Dougherty | 47

Form 5471 Page ThreeSchedule CIncome Statement

Filer Categories 3 and 4 Complete Schedule C

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Page Three – Schedule C

Form 5471, Page Three Schedule C Income Statement Category 3 and 4 filers complete Schedule C Report income statement of the foreign corporation consistent with

U.S. GAAP Report income statement in functional currency converted to USD

based on U.S. GAAP translation principles Note that Form 5471 instructions require divide by convention to

convert to USD New specific line items for

Lines 8a and 8b unrealized and realized foreign currency translation gain or loss

Line 20 unusual or infrequently occurring items Lines 21a and 21b current and deferred income tax expense

and benefit (more detail for the tax provision items) Line 24 Other Comprehensive Income – Line 23a FX translation

adjustments, line 23b other items, and line 23c income tax expense or benefit related to OCI

Line 14 depreciation per U.S. GAAP Line 16 taxes should be taxes other than income tax

48

© 2019 | All Rights Reserved | Alison N. Dougherty | 49

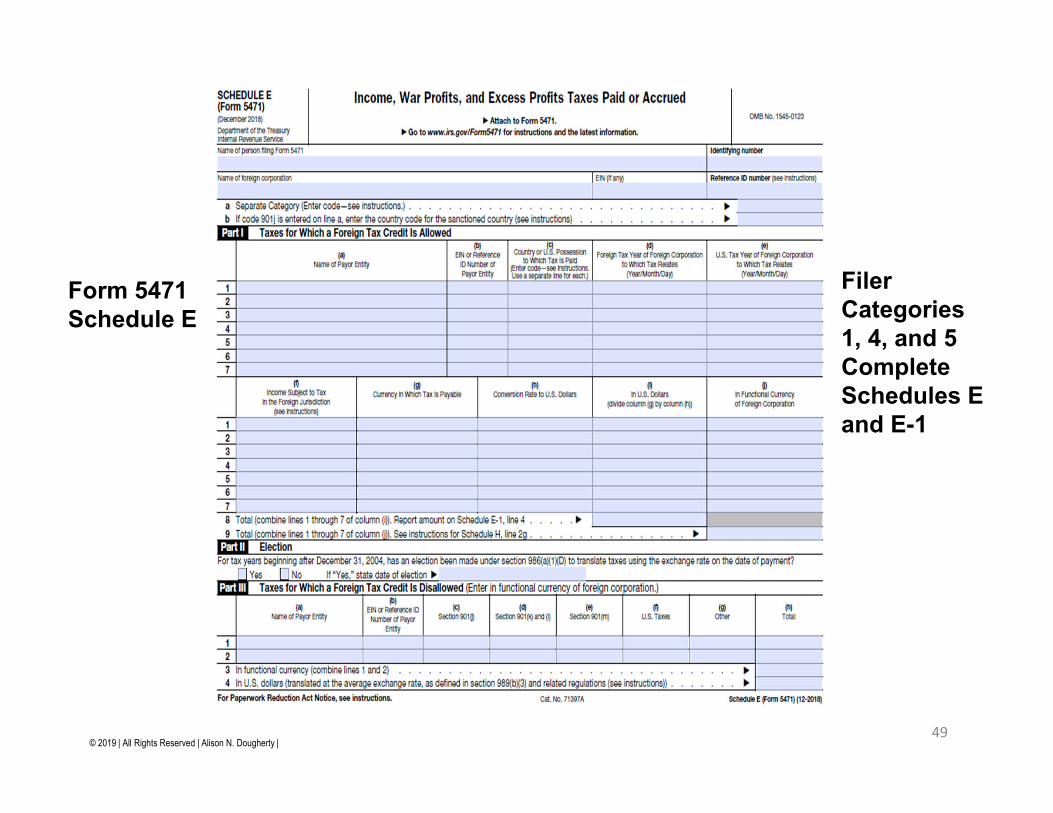

Form 5471Schedule E

Filer Categories 1, 4, and 5 Complete Schedules E and E-1

© 2019 | All Rights Reserved | Alison N. Dougherty | 50

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule E

Form 5471, Schedule E Foreign Income Tax Paid or Accrued Category 1, 4, and 5 filers complete Schedule E Schedule E Part I report creditable foreign taxes

Name of foreign company paying the foreign tax FEIN or reference ID of the foreign payor Country or U.S. possession to which foreign tax paid Foreign tax year of foreign corporation to which tax relates U.S. tax year of foreign corporation to which tax relates Amount of income subject to foreign tax in the foreign jurisdiction Currency in which tax is payable Average exchange rate to convert tax to USD based on divide by

convention Foreign tax converted to USD Foreign tax in functional currency

Schedule E Part II report election to convert foreign tax based on the exchange rate on the date of the payment

Schedule E Part III foreign taxes for which foreign tax credit is disallowed I.R.C. § 901(j) listed countries I.R.C. §§ 901(k) and (l) withholding taxes on dividends and gain or

other income when minimum holding period requirement is not satisfied

I.R.C. § 901(m) covered asset acquisitions resulting in additional foreign source taxable income due to differences in basis adjustments

52

© 2019 | All Rights Reserved | Alison N. Dougherty |

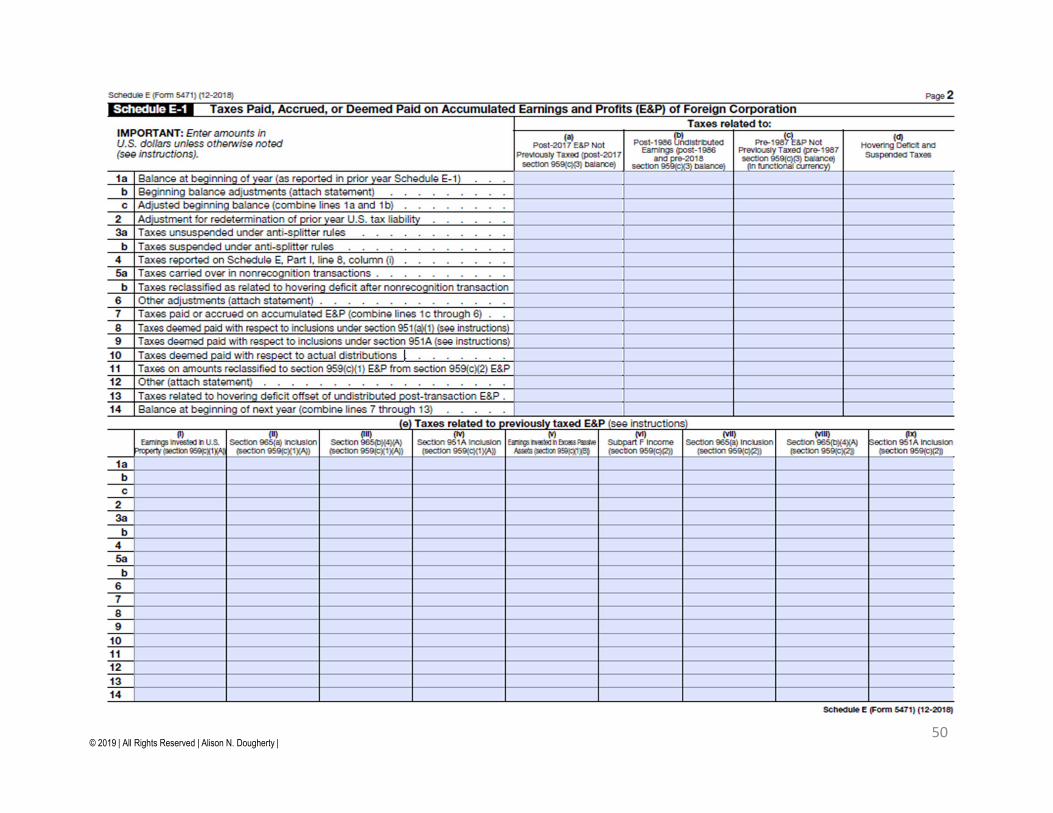

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule E-1

Form 5471, Schedule E-1 Foreign Income Tax Paid or Accrued Category 1, 4, and 5 filers complete Schedule E-1 Schedule E-1 tracks the changes in and the adjustments to the cumulative

balance of the foreign corporation’s foreign tax pool Schedule E-1 reports the foreign taxes based on different categories of

not previously taxed E&P in columns (a) through (d) Post-2017 E&P not previously taxed Post-1986 and pre-2018 undistributed E&P per I.R.C. § 959(c)(3) Pre-1987 not previously taxed E&P per I.R.C. § 959(c)(3) Hovering deficit and foreign tax credit splitter suspended taxes

Schedule E-1 reports the foreign taxes based on nine different categories of previously taxed E&P (PTEP) in columns (e)(i) through (ix) consistent with Schedules J and P

E&P for I.R.C. § 956 inclusions, I.R.C. 965 transition tax inclusions, I.R.C. § 951A GILTI inclusions, and I.R.C. § 951(a)(1) Subpart F inclusions

53

© 2019 | All Rights Reserved | Alison N. Dougherty | 54

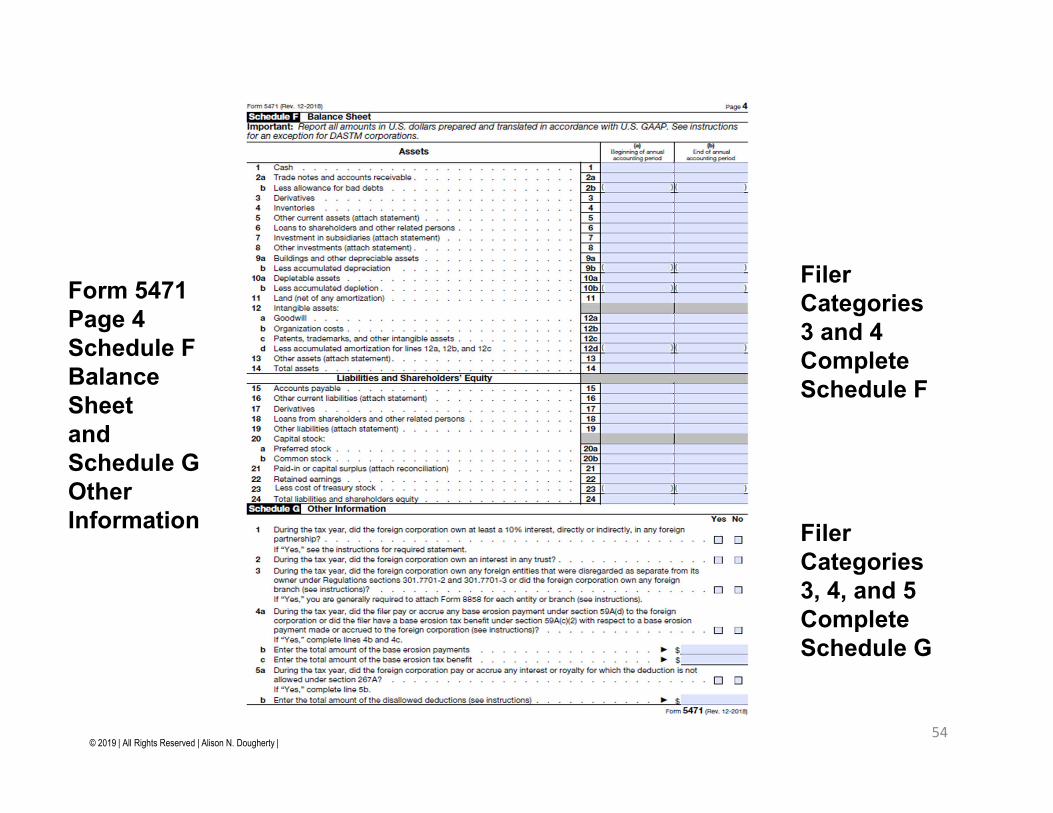

Form 5471 Page 4Schedule F Balance Sheetand Schedule G Other Information

Filer Categories 3 and 4 Complete Schedule F

Filer Categories 3, 4, and 5 Complete Schedule G

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule F

Form 5471, Schedule F Balance Sheet Category 3 and 4 filers complete Schedule F Report balance sheet of foreign corporation consistent with U.S. GAAP Translate balance sheet into USD based on U.S. GAAP translation

principles Note that Form 5471 instructions require divide by convention to

convert to USD Report assets, liabilities, and equity New specific line items for derivative assets and liabilities and treasury

stock in equity

55

© 2019 | All Rights Reserved | Alison N. Dougherty | 56

Form 5471 Pages 4 and 5Schedule G Other Information (Continued)

Filer Categories 3, 4, and 5 Complete Schedule G

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule G

Form 5471, Schedule G Other Information Category 3, 4 and 5 filers complete Schedule G Revised Schedule G with extensive list of 19 main questions with subparts It is advisable and recommended that a U.S. international tax specialist reviews Many questions include issues related to international tax reform provisions Must disclose whether the foreign corporation owned an interest in a foreign

partnership, trust, or disregarded entity I.R.C. § 59A BEAT disclosure, must report whether the U.S. filer paid or accrued a

base erosion payment to the foreign corporation I.R.C. § 267A hybrid payment disclosure, must report whether foreign

corporation paid or accrued an interest or royalty payment that would be disallowed as a deduction

I.R.C. § 250 FDII deduction disclosure, must report whether the U.S. filer is claiming the FDII deduction for any amount reported on Schedule M and disclose certain amounts in FDDEI calculation

More extensive I.R.C. § 482 transfer pricing questions related to cost sharing agreements for intangible asset development and platform contributions

Disclosure whether foreign corporation was involved in a triangular reorganization with acquisition of shareholder’s stock or securities

I.R.C. § 367(d) disclosure, must report if annual income inclusion from taxable offshore transfer of intangible property to the foreign corporation

Must report whether the foreign corporation was an expatriated subsidiary Must report whether foreign corporation had transactions reportable on Form

8886 I.R.C. § 901(m) disclosure, must report whether foreign corporation paid or

accrued a non-creditable tax I.R.C. § 909 disclosure, must report whether foreign corporation paid or

accrued a foreign tax suspended or unsuspended under foreign tax credit splitter rules

57

© 2019 | All Rights Reserved | Alison N. Dougherty | 58

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule H

Form 5471, Schedule H Current Earnings and Profits (CEP) Category 4 and 5 filers complete Schedule H Complete separate Schedule H for each separate category of income Report Schedule C line 21 U.S. GAAP “book” net income or loss in

functional currency as starting point for Schedule H line 1 Report positive and negative E&P adjustments on Schedule H lines 2

through 4 E&P adjustments convert current year book net income or loss based

on U.S. GAAP to E&P based on U.S. tax accounting principles Note difference between book net income, retained earnings, and

earnings and profits for U.S. tax purposes Common E&P adjustments may include the following:

Deferred tax expense Unrealized foreign currency exchange gain or loss Difference in book and tax FX gain or loss Difference in book depreciation and ADS tax depreciation Bad debt reserves Inventory reserves Advance payments Contingencies, severance, and restructuring reserves Difference in book and tax amortization of intangible assets Cumulative translation account Prior period adjustments Unicap

Convert E&P in foreign currency after adjustments to USD based on the average exchange rate and the divide by convention

59

© 2019 | All Rights Reserved | Alison N. Dougherty | 60

© 2019 | All Rights Reserved | Alison N. Dougherty |

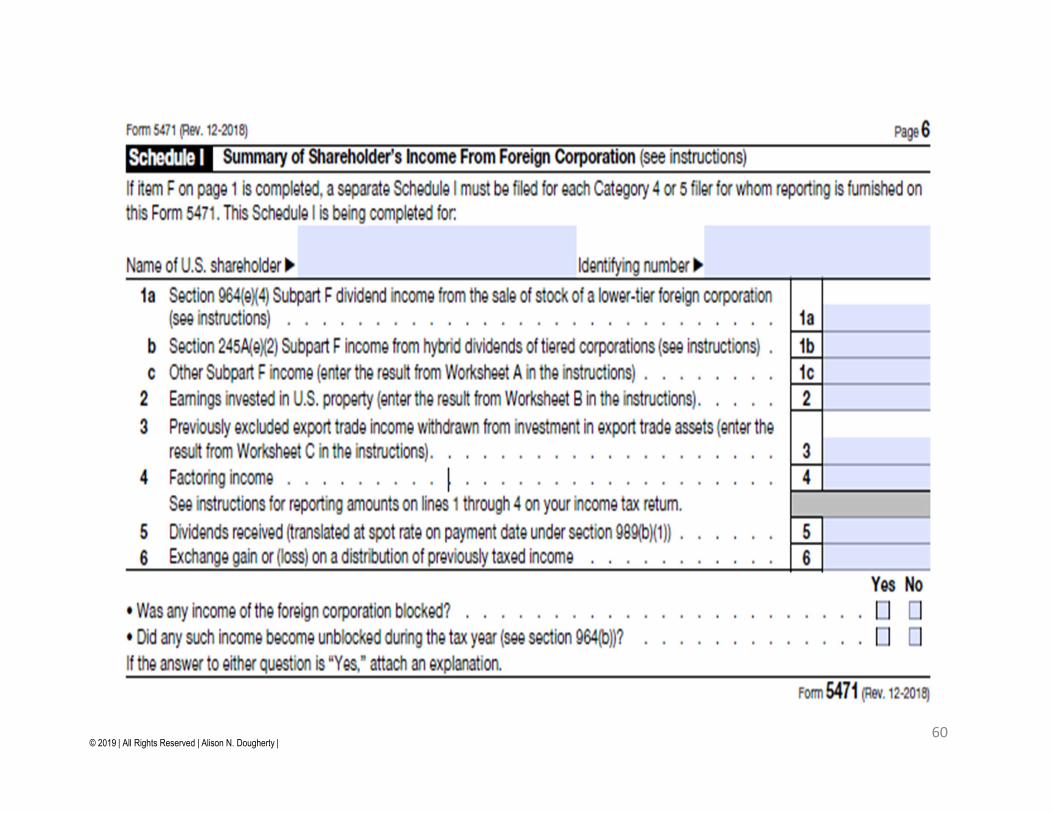

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule I

Form 5471, Schedule I Summary of Income from Foreign Corporation Category 4 and 5 filers complete Schedule I Report I.R.C. § 964(e)(4) Subpart F dividend income

from sale of stock of a lower-tier foreign corporation Report I.R.C. § 245A(e)(2) Subpart F income from

hybrid dividends of tiered corporations Report other Subpart F income from Form 5471

instructions worksheet A Report I.R.C. § 956 inclusion from Worksheet B Report previously excluded export income withdrawn

from investment in export trade assets from Worksheet C

Report factoring income (sale or transfer of A/R) Report dividends received translated at spot

exchange rate on the payment date Report foreign currency exchange gain or loss on a

distribution of previously taxed income Indicate whether any income of the foreign

corporation was blocked or unblocked according to applicable foreign country export controls

61

© 2019 | All Rights Reserved | Alison N. Dougherty | 62

© 2019 | All Rights Reserved | Alison N. Dougherty |

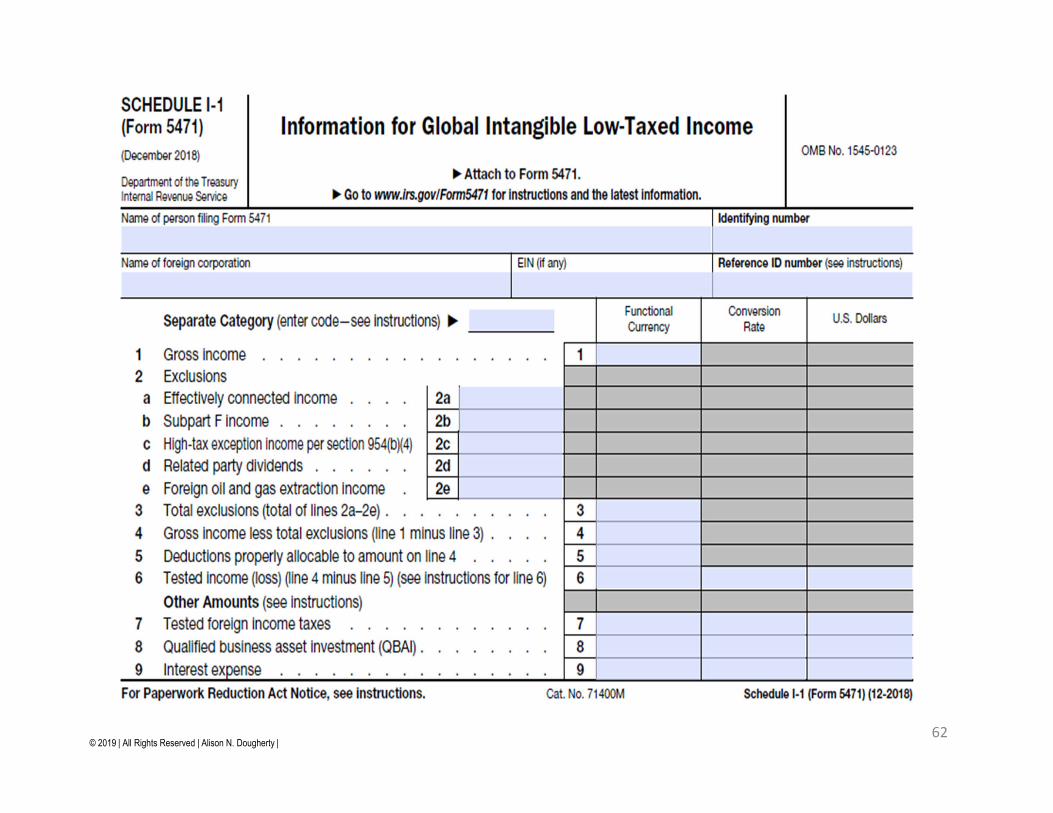

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule I-1

Form 5471, Schedule I-1 Information for Global Intangible Low-Taxed Income (GILTI) Category 4 and 5 filers complete Schedule I-1 GILTI is a new global minimum tax under I.R.C.

§ 951A that requires an I.R.C. § 958(a) U.S. shareholder to report a taxable inclusion of undistributed income from a foreign corporation similar to Subpart F income

Complete separate Schedule I-1 for each separate category of income

Schedule I-1 information is used by an I.R.C. § 958(a) U.S. shareholder and filer of Form 5471 to complete Form 8992 to report a GILTI inclusion

The Schedule I-1 tracks the calculation of GILTI under I.R.C. § 951A with exclusions from tested income or loss calculation, QBAI, and specified interest expense

Reduction in GILTI calculation for 10% of QBAI QBAI is the average of the tangible property asset

basis at the end of each quarter

63

© 2019 | All Rights Reserved | Alison N. Dougherty | 64

© 2019 | All Rights Reserved | Alison N. Dougherty | 65

© 2019 | All Rights Reserved | Alison N. Dougherty |

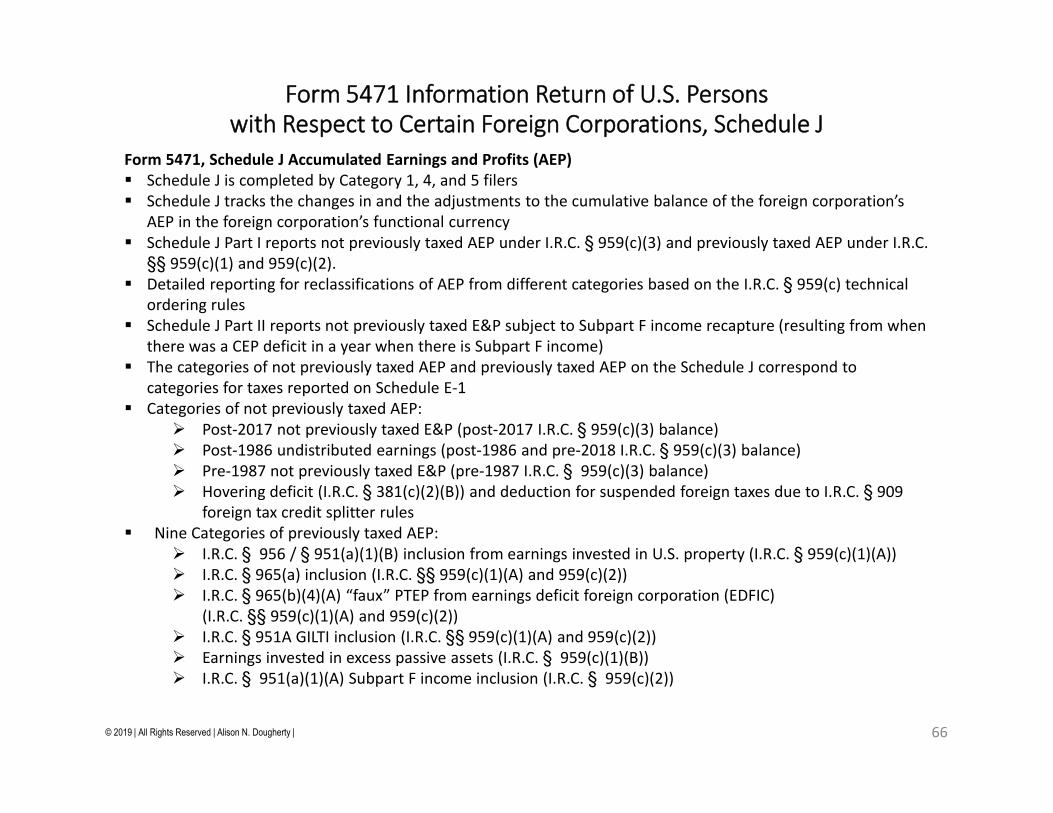

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule J

Form 5471, Schedule J Accumulated Earnings and Profits (AEP) Schedule J is completed by Category 1, 4, and 5 filers Schedule J tracks the changes in and the adjustments to the cumulative balance of the foreign corporation’s

AEP in the foreign corporation’s functional currency Schedule J Part I reports not previously taxed AEP under I.R.C. § 959(c)(3) and previously taxed AEP under I.R.C.

§§ 959(c)(1) and 959(c)(2). Detailed reporting for reclassifications of AEP from different categories based on the I.R.C. § 959(c) technical

ordering rules Schedule J Part II reports not previously taxed E&P subject to Subpart F income recapture (resulting from when

there was a CEP deficit in a year when there is Subpart F income) The categories of not previously taxed AEP and previously taxed AEP on the Schedule J correspond to

categories for taxes reported on Schedule E-1 Categories of not previously taxed AEP:

Post-2017 not previously taxed E&P (post-2017 I.R.C. § 959(c)(3) balance) Post-1986 undistributed earnings (post-1986 and pre-2018 I.R.C. § 959(c)(3) balance) Pre-1987 not previously taxed E&P (pre-1987 I.R.C. § 959(c)(3) balance) Hovering deficit (I.R.C. § 381(c)(2)(B)) and deduction for suspended foreign taxes due to I.R.C. § 909

foreign tax credit splitter rules Nine Categories of previously taxed AEP:

I.R.C. § 956 / § 951(a)(1)(B) inclusion from earnings invested in U.S. property (I.R.C. § 959(c)(1)(A)) I.R.C. § 965(a) inclusion (I.R.C. §§ 959(c)(1)(A) and 959(c)(2)) I.R.C. § 965(b)(4)(A) “faux” PTEP from earnings deficit foreign corporation (EDFIC)

(I.R.C. §§ 959(c)(1)(A) and 959(c)(2)) I.R.C. § 951A GILTI inclusion (I.R.C. §§ 959(c)(1)(A) and 959(c)(2)) Earnings invested in excess passive assets (I.R.C. § 959(c)(1)(B)) I.R.C. § 951(a)(1)(A) Subpart F income inclusion (I.R.C. § 959(c)(2))

66

© 2019 | All Rights Reserved | Alison N. Dougherty | 67

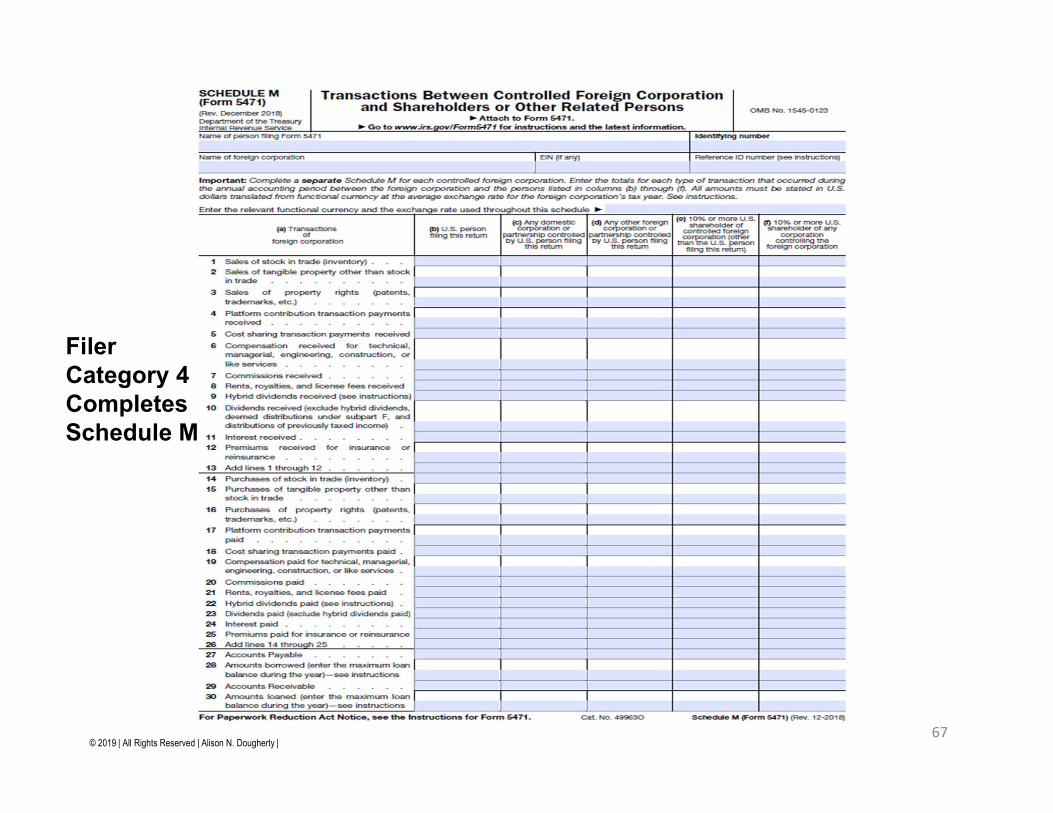

Filer Category 4 Completes Schedule M

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule M

Form 5471, Schedule M Transactions between CFC and Shareholders or Other Related Persons Category 4 filers complete the Schedule M Schedule M reports transactions between:

The U.S. filer of the Form 5471 and the CFC Any U.S. corporation or partnership controlled by the U.S. filer and the CFC Any other foreign corporation or partnership controlled by the U.S. filer and the CFC Any other 10% or greater U.S. shareholder of the CFC and the CFC A 10% or greater U.S. shareholder of any corporation controlling the CFC and the CFC

Schedule M reports commercial business transactions that involve payments between the parties New specific line items for:

Hybrid dividends that do not qualify for the I.R.C. § 245A 100% dividends received deduction (DRD)

Dividends (other than deemed distributions of Subpart F income and distributions of PTEP) received or paid

Accounts receivable related to providing services or sales of property Accounts payable related to providing services or sales of property

68

© 2019 | All Rights Reserved | Alison N. Dougherty | 69

Filer Category 2 Completes Schedule O, Part I

Filer Category 3 Completes Schedule O, Part II

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule O, Part I

Form 5471, Schedule O Organization or Reorganization of Foreign Corporation, and Acquisitions and Dispositions of Its Stock Category 2 filers complete Schedule O, Part I Category 3 filers complete Schedule O, Part II U.S. officers or directors report acquisitions of

10% stock ownership interest in foreign corporation by any U.S. person in Schedule O, Part I

Report name, address, and U.S. taxpayer ID number of U.S. shareholder that acquired 10% of stock, and dates of original and current year acquisition in Part I

Report information for Category 3 filer that is completing Schedule O, Part II, Section A

Report information for U.S. officers and directors in Schedule O, Part II, Section B

Report information regarding class of stock acquired, date of acquisition, and whether owned directly, indirectly, or constructively in Schedule O, Part II, Section C

70

© 2019 | All Rights Reserved | Alison N. Dougherty |

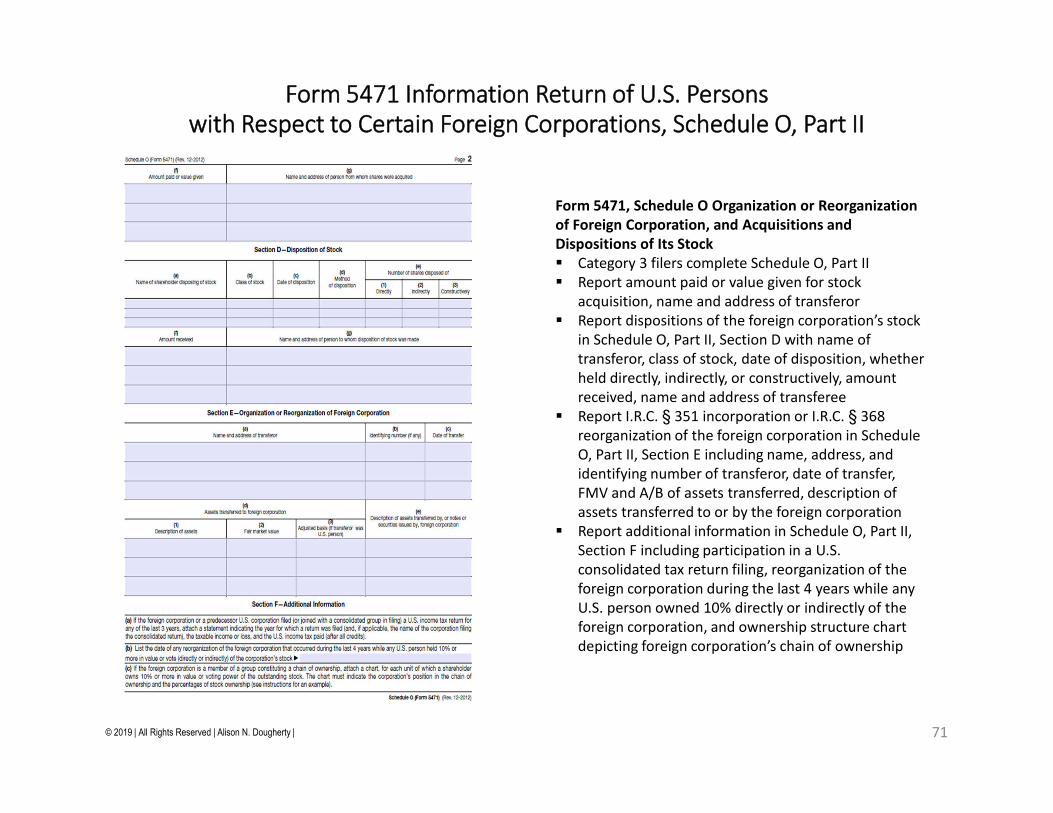

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule O, Part II

Form 5471, Schedule O Organization or Reorganization of Foreign Corporation, and Acquisitions and Dispositions of Its Stock Category 3 filers complete Schedule O, Part II Report amount paid or value given for stock

acquisition, name and address of transferor Report dispositions of the foreign corporation’s stock

in Schedule O, Part II, Section D with name of transferor, class of stock, date of disposition, whether held directly, indirectly, or constructively, amount received, name and address of transferee

Report I.R.C. § 351 incorporation or I.R.C. § 368 reorganization of the foreign corporation in Schedule O, Part II, Section E including name, address, and identifying number of transferor, date of transfer, FMV and A/B of assets transferred, description of assets transferred to or by the foreign corporation

Report additional information in Schedule O, Part II, Section F including participation in a U.S. consolidated tax return filing, reorganization of the foreign corporation during the last 4 years while any U.S. person owned 10% directly or indirectly of the foreign corporation, and ownership structure chart depicting foreign corporation’s chain of ownership

71

© 2019 | All Rights Reserved | Alison N. Dougherty | 72

© 2019 | All Rights Reserved | Alison N. Dougherty | 73

Schedule P PTEPFiler Categories 1, 4, and 5 Complete Schedule P

© 2019 | All Rights Reserved | Alison N. Dougherty |

Form 5471 Information Return of U.S. Persons with Respect to Certain Foreign Corporations, Schedule P

Form 5471, Schedule P Previously Taxed Earnings and Profits of U.S. Shareholder of Certain Foreign Corporations Category 1, 4, and 5 filers complete Schedule P Schedule P tracks Previously Taxed Earnings and Profits (“PTEP”) in the foreign corporation’s functional currency Schedule P tracks the changes in and the adjustments to the cumulative balance of the foreign corporation’s PTEP in

the foreign corporation’s functional currency Schedule P reports PTEP under I.R.C. §§ 959(c)(1) and 959(c)(2). Detailed reporting for reclassifications of AEP from different categories based on the I.R.C. § 959(c) technical

ordering rules Schedule P tracks the same nine categories of PTEP as Schedules E and J Nine Categories of PTEP:

I.R.C. § 956 / § 951(a)(1)(B) inclusion from earnings invested in U.S. property (I.R.C. § 959(c)(1)(A)) I.R.C. § 965(a) inclusion (I.R.C. §§ 959(c)(1)(A) and 959(c)(2)) I.R.C. § 965(b)(4)(A) “faux” PTEP from earnings deficit foreign corporation (EDFIC) (I.R.C. §§ 959(c)(1)(A) and

959(c)(2)) I.R.C. § 951A GILTI inclusion (I.R.C. §§ 959(c)(1)(A) and 959(c)(2)) Earnings invested in excess passive assets (I.R.C. § 959(c)(1)(B)) I.R.C. § 951(a)(1)(A) Subpart F income inclusion (I.R.C. § 959(c)(2))

74

© 2019 | All Rights Reserved | Alison N. Dougherty |

ALISON N. DOUGHERTY, J.D., LL.M.Director, Tax ServicesAronson LLC

Alison N. Dougherty provides tax services as a Director at AronsonLLC. She specializes in U.S. international tax reporting, compliance,consulting, planning, and structuring. She has extensive experienceassisting clients with U.S. tax reporting and compliance for offshoreassets and foreign accounts. She provides outbound U.S. internationaltax guidance to U.S. individuals and businesses with activities in othercountries. She also provides inbound U.S. international tax guidanceto nonresident individuals and businesses with activities in the UnitedStates. She has worked extensively in the area of U.S. internationaltax reporting and compliance with the preparation of the U.S. FederalForms 5471, 926, 8865, 8858, 5472, 1042, 1042-S, 8621, 8804, 8805,8813, 8288, 8288-A, 8288-B, 1116, 1118, 1120-F, 1040-NR, 3520,3520-A, 2555, 5713, 8832, 8833, 8840, 8843, 8854, 8938, and FBAR.She has counseled U.S. taxpayers regarding the outbound formation,capitalization, acquisition, operation, reorganization, and liquidation offoreign companies. She has significant experience with U.S. Federalnonresident tax withholding, foreign partner tax withholding, andFIRPTA withholding. She works closely with nonresident individualsand businesses regarding inbound U.S. real property investment. Shehas assisted U.S. taxpayers with IRS amnesty program disclosures ofoffshore assets and foreign accounts.

Alison completed the LL.M. (Master of Laws) in Securities andFinancial Regulation in 2004 with academic distinction at GeorgetownUniversity Law Center. She completed the LL.M. (Master of Laws) inTaxation in 2000 and the Juris Doctor in 1999 at the University ofDenver College of Law. She completed a Bachelor of Arts degree inForeign Language in 1995 at Virginia Commonwealth University.

(301) [email protected]

Aronson LLC805 King Farm Blvd Suite 300Rockville, Maryland 20850 USAWashington, DC Metro Area

75