fourth edition copyright ©2003 prentice hall, inc. part 5........................ managing...

TRANSCRIPT

Fourth EditionFourth Edition

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc.

PART 5 . . . . . . . . . . . . . . . . . . . . . . . .PART 5 . . . . . . . . . . . . . . . . . . . . . . . .Managing InformationManaging Information

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 22

Chapter 13Chapter 13

Understanding Principles of Accounting

Understanding Principles of Accounting

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 33

“I am incredibly nervous that we will implode in a wave of accounting scandals”

~ Sherron Watkins, Enron Vice President,four months prior to Enron’s collapse

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 44

Key Topics

The role of public and private accountants

The CPA vision project

The accounting equation and double-entry accounting

Basic financial statements

Key financial ratios

Accounting in international businesses

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 55

What Is Accounting?

Business managersBusiness managers

Employees and unionsEmployees and unions

Investors and creditorsInvestors and creditors

Tax authoritiesTax authorities

Government regulatory Government regulatory agenciesagencies

A comprehensive system for A comprehensive system for collectingcollecting, , analyzinganalyzing and and communicatingcommunicating financial financial informationinformation

A comprehensive system for A comprehensive system for collectingcollecting, , analyzinganalyzing and and communicatingcommunicating financial financial informationinformation

Users of accounting information:Users of accounting information:

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 66

Financial AccountingFinancial Accounting

Managerial AccountingManagerial Accounting

Accountants and Their Responsibilities

Controller: Managers all of a firm’s accounting activities

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 77

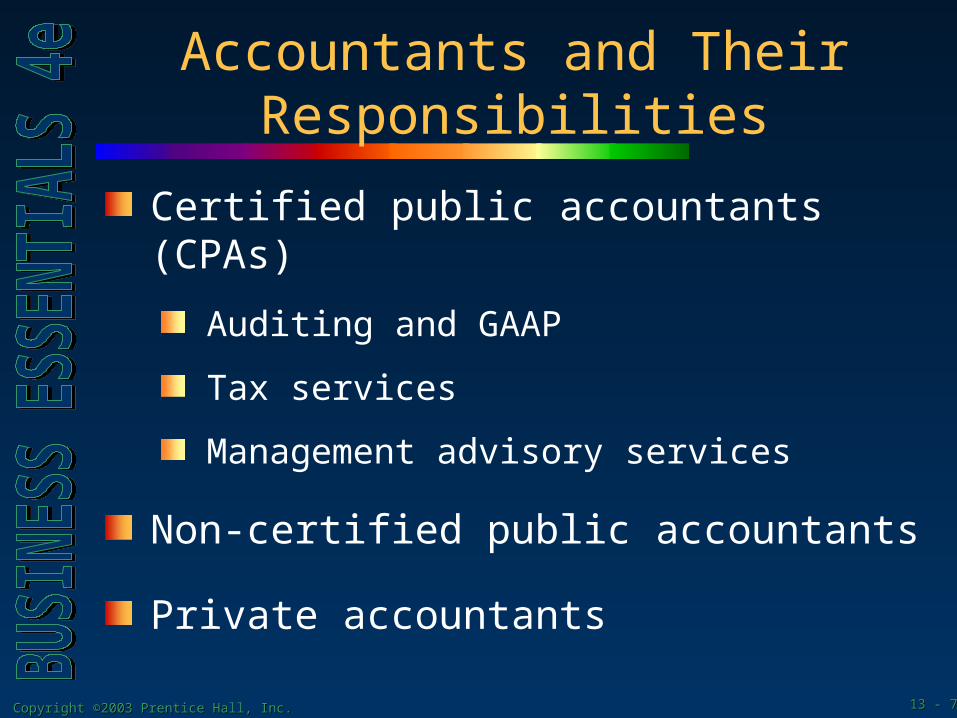

Accountants and Their Responsibilities

Certified public accountants (CPAs)

Auditing and GAAP

Tax services

Management advisory services

Non-certified public accountants

Private accountants

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 88

The CPA Vision Project

Identifying issues for the future

Global forces as drivers of change

Recommendations

A new directionCore services

Core competencies

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 99

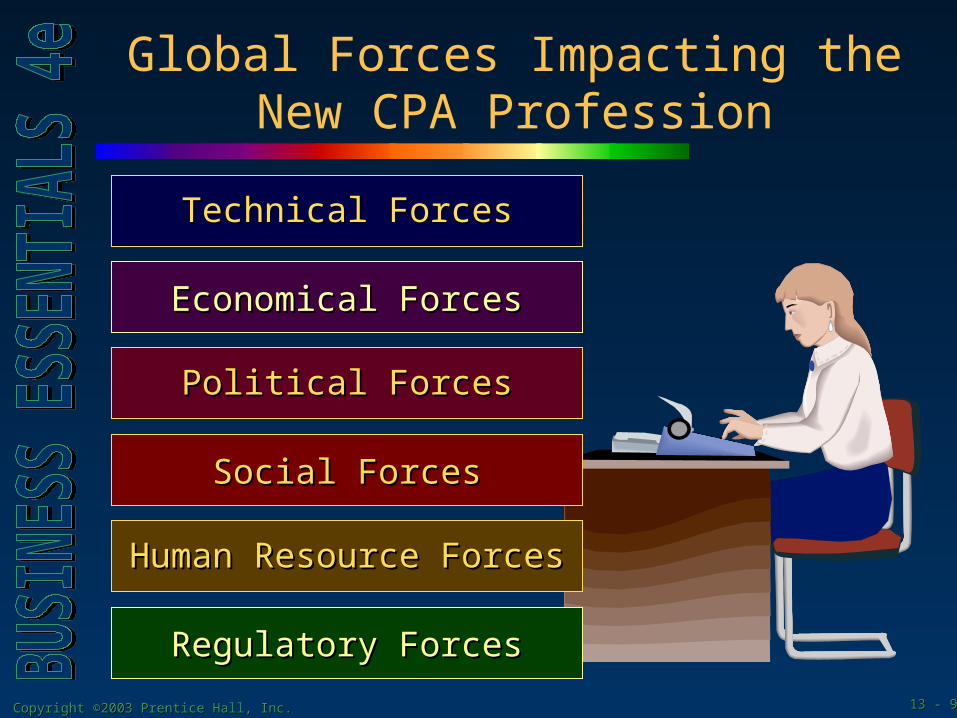

Global Forces Impacting the New CPA Profession

Technical ForcesTechnical Forces

Economical ForcesEconomical Forces

Political ForcesPolitical Forces

Social ForcesSocial Forces

Human Resource ForcesHuman Resource Forces

Regulatory ForcesRegulatory Forces

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1010

Key Tools of the Accounting Trade

Accounting EquationAccounting Equation

Double-Entry AccountingDouble-Entry AccountingEvery transaction affects two accountsEvery transaction affects two accounts

Double-Entry AccountingDouble-Entry AccountingEvery transaction affects two accountsEvery transaction affects two accounts

Assets = Liabilities + Owners’ EquityAssets = Liabilities + Owners’ Equity

Assets – Liabilities = Owners’ Equity Assets – Liabilities = Owners’ Equity

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1111

Financial Statements

Balance Sheets

Income Statements

Statements of Cash Flows

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1212

ASSETS

Perfect Posters’

Balance Sheet Example

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1313

LIABILITIES & OWNER'S

EQUITY

Perfect Posters’

Balance Sheet Example

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1414

Perfect Posters’

Income StatementExample

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1515

Statements of Cash Flows

Cash flows from:Cash flows from:

OperationsOperations

InvestingInvesting

FinancingFinancing

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1616

Perfect Posters’

Sales Budget Example

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1717

Reporting Standards and Practices

Revenue Recognition

Matching

Full Disclosure

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1818

Solvency Solvency RatiosRatios

Profitability Profitability RatiosRatios

Activity Activity RatiosRatios

Analyzing Financial Statements

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 1919

Short Term Solvency Ratios

Current Ratio:Current Ratio:

Current Assets – Current LiabilitiesCurrent Assets – Current Liabilities

Working Capital:Working Capital:

Current Assets Current Assets

Current LiabilitiesCurrent Liabilities

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 2020

Long-term Solvency Ratios

Debt to Owners’ Equity Ratio:Debt to Owners’ Equity Ratio:

Ability to finance an investment through Ability to finance an investment through borrowed fundsborrowed funds

Leverage:Leverage:

DebtDebt

Owners’ EquityOwners’ Equity

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 2121

Profitability and Activity Ratios

Return on Equity:Return on Equity:

Earnings Per Share:Earnings Per Share:

Net IncomeNet Income

Total Owners' EquityTotal Owners' Equity

Inventory Turnover Ratio:Inventory Turnover Ratio:

Net IncomeNet Income

# of Shares Outstanding# of Shares Outstanding

Cost of Goods SoldCost of Goods Sold

Average InventoryAverage Inventory

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 2222

International International Accounting Accounting StandardsStandards

International International TransactionsTransactions

Foreign Foreign Currency Currency ExchangeExchange

International Accounting

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 2323

Chapter Review

Explain the role of accountants, public and private

Discuss the CPA Vision Project

Explain the accounting equation and double-entry accounting

Describe the three basic financial statements

Copyright ©2003 Prentice Hall, Inc.Copyright ©2003 Prentice Hall, Inc. 13 - 13 - 2424

Chapter Review

Explain how key financial ratios can help analyze the financial strength of a business

Explain some of the special issues facing accountants at firms that do international business