fringe benefits - tax academy · extra benefits (goods or services), given free to all employees in...

TRANSCRIPT

Fringe BenefitsFASTAX

6 Jun 2017

1

Extra benefits (goods or services), given free to allemployees in addition to wages/ salaries.

Can I claim input tax incurred on fringe benefit

provided to my employees?

Do I need to account for output tax when I let my

employees use my business goods for free?

2

Fringe Benefits

• Based on 2nd edition of e-tax guide on “GST: Fringe Benefits”

• Applies with effect from 16 May 2016

• Before 16 May 2016, you may have claimed input tax on the provisionof fringe benefits to your employees based on previous versions of thee-Tax Guide. No input tax needs to be repaid.

• However, you are still required to account for output tax if the fringebenefits are goods that have either been:

i. Given as gifts to employees under the Gift Rule; or

ii. Used temporarily by your employees for their privatepurposes.

3

Fringe Benefits

Start

Input tax disallowed

NO

Yes

Input tax allowed.

Expense incurred for biz purpose? (Close Nexus

Test)

Is supply contractually

made to taxable person?

Is the employee acting as the agent of the taxable person in

receiving the supply or have you met the

admin concession?

Yes

NOYes

NO

Yes

Input tax disallowed because supply is made to employee e.g. telephone bill

made in the name of employee for personal calls

Input tax disallowed e.g. club subscription fees, medical &

accident insurance premiums, medical expenses, family benefits,

cost and running expenses of motor cars.

NO

Is input tax specifically disallowed

under Regulations

26 & 27?

4

Claiming Input Tax

Input Tax Claims

Input tax is claimable if all of the following conditions are satisfied:

• You are GST-registered

• Goods or services are supplied to you

• Goods or services are used for the purpose of your business

• Goods or services are used for the making of taxable supplies or

out-of-scope supplies which would be taxable supplies if made in

Singapore

• It must not be disallowed under Regulations 26 and 27 of the GST

(General) Regulations

5

Claiming Input Tax

Goods and services acquired solely for the private use by:

i. GST-registered sole-proprietor;ii. partners of a GST-registered partnership;iii. directors of a GST-registered company; andiv. persons connected to the GST-registered sole

proprietor, partnership or company, as the case maybe.

→ NOT allowed to claim GST because the purchases willnot be considered as used “for the purpose of business”.

6

Claiming Input Tax

Supplied to you = Contractually made to business

• Tax invoice issued by the supplier is addressed to you

Prima facie, supply will be treated as contractually made to you

• Tax invoice addressed to your employee

Your employee must be acting as your agent in acquiring the supply ofgoods or services

• There are fringe benefits that are clearly contracted in theemployee’s name and he is unlikely to be acting as an agent

E.g. professional memberships, educational courses and mobilephone plans

7

Claiming Input Tax – Admin Concession

• For tax invoices addressed to your employee, you can claiminput tax if: your employee is reimbursed; and the expenses are recognised as business expenses in

your business’ accounts

• If you partially reimburse your employee, you will beallowed to claim GST in proportion to the amountreimbursed

• Only the portion attributable to business usage isclaimable

8

Claiming Input Tax – Admin Concession

• If you have difficulties determining the business andprivate portions of the expenses, you may claim input taxas follows:

a) For full reimbursements: based on 4/7 of the GSTincurred on the expenses. 4/7 is an estimate of the number of days that an employee

spends at work in a week

b) For partial reimbursements: based on 7/107 of theamount reimbursed or 4/7 of the GST incurred on theexpenses, whichever is lower.

9

Claiming Input Tax

Allowances:

• Pre-determined amount to cover an estimated expenseand will be given to your employee regardless of whetherit is incurred.

• GST is NOT claimable even if receipt/ invoice is provided byyour employee after the expense is incurred.

• E.g. Flat $20 meal allowance if he works beyond normaloffice hours. NOT claimable

10

Accounting for Output Tax

11

YES

when the taxable person is entitled to claim/has been allowed input tax in respect of

the goods given free to employees

Accounting for Output Tax

• You must account for output tax based on the Open Market Value ofthe supply of goods given away for free to your employees exceptwhen:

• The cost of the goods (gift) is ≤ $200 (exclusive of GST); or

• No input tax was allowed on the purchase or importation of thosegoods (e.g. purchase from non GST-registered supplier anddisallowed expenses); or

• Free catering of food/beverage; or

• Free accommodation in a hotel, inn, boarding house or similarestablishment.

12

Accounting for Output Tax

Are free services provided by employer to employees subject to output tax?

13

NO

GST need not be accounted on services provided for free

Examples

Even though you are able to claim GST on the followingservices procured, you are not required to account foroutput tax when they are provided free to your employee:

Transportation provided from MRT to workplace

Insurance required under Work Injury Compensation Act

Accounting for Output Tax

14

Accounting for Output Tax

Important!

• You need to distinguish free services from deemed supplyof services

• A deemed supply of service occurs when goods held forbusiness purposes are put to private use

15

Accounting for Output Tax

Business goods used temporarily for free by employees fortheir private purpose

• You are required to account for output tax if you allowyour business goods to be used temporarily for free byemployees, except where:

No input tax has been allowed on the purchase of thegoods; or

There is a close nexus to your business activities notregarded as provided for employees’ private use

16

Accounting for Output Tax

Deemed Supply of Services

Example

A carpet cleaning company allows its employee to use itscarpet cleaning equipment free of charge for his privateusage. Input tax has been claimed on the equipment.

No close nexus output tax is accountable

Value of supply = COST of letting your staff use for free

17

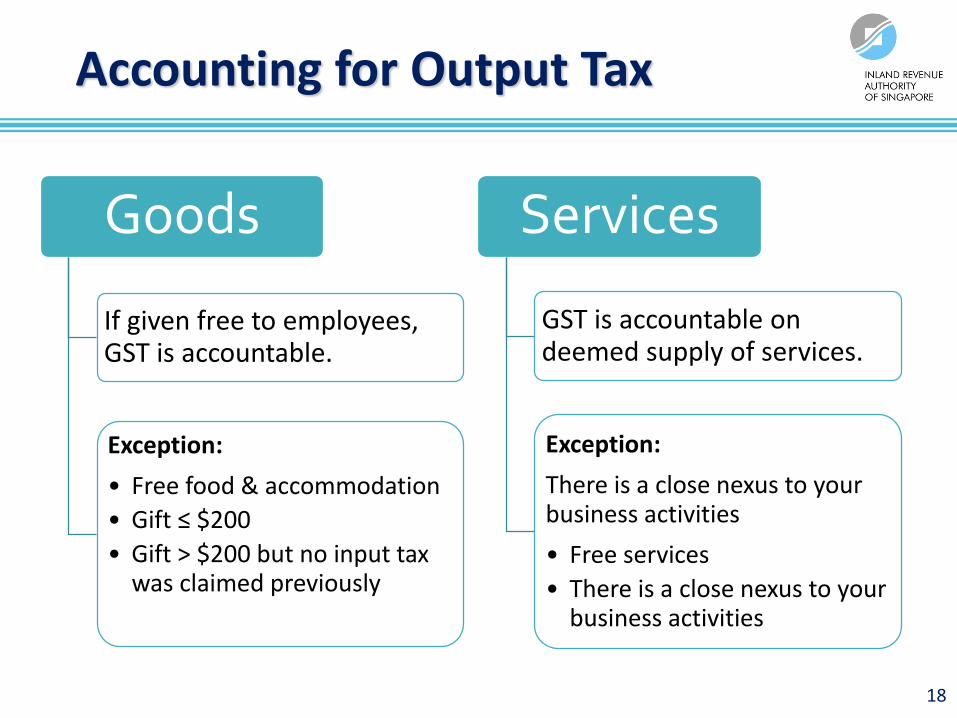

Accounting for Output Tax

18

Goods

If given free to employees, GST is accountable.

Exception:

• Free food & accommodation

• Gift ≤ $200

• Gift > $200 but no input tax was claimed previously

Services

GST is accountable on deemed supply of services.

Exception:

There is a close nexus to your business activities

• Free services

• There is a close nexus to your business activities

Close Nexus Test

Close Nexus Test

Whether fringe benefits are incurred

for the purpose of business

Input tax is claimable, if all other conditions in Slide 5

are met

Whether free use of business goods by

employees is for the purpose of business

Output tax need not be accounted on the free use of business goods

19

Close Nexus Test

The Close Nexus Test is satisfied if any of the following is met:

1. Is necessary for the proper operation of your business

2. Directly maintains or promotes the efficiency of yourbusiness operations

3. Primarily promotes staff interaction

4. Encourages the upgrading of your employee’s skills andknowledge relevant to the business

5. Is given in recognition of the contribution of youremployee towards the business

6. Promotes corporate identity

20

Close Nexus Test Indicator 1: Necessary for the proper operation of business

• Key idea: the benefit must be provided in order for yourbusiness to function

• Depends on factors such as the business nature,commercial requirements, industry practice and regulatoryrequirements

Example:

Dormitories provided to house foreign workers in theconstruction industry, so as to meet regulatoryrequirements and ensure the quick and efficientallocation of labour

21

Close Nexus Test Indicator 2: Directly maintains or increases the efficiency of business operations

• To allow your employee to better utilise his time and effortin carrying out his job duties contributes to efficiency ofbusiness operation

Example:

Provision of meals in the course of a business meetingwhich allows the meeting to be carried on without thedisruption of a lunch break

22

Close Nexus Test Indicator 3: Primarily promotes staff interaction

• Benefits incurred for corporate events/ activities thatprimarily promote staff interaction improve workingrelationship between staff and encourage futurecooperation

Example:

Goods (e.g. door gift) and services (e.g. entrance ticketis free) provided to employees at organised companyevents such as corporate dinner and dance

23

Close Nexus Test Indicator 4: Encourages the upgrading of employee’s skills and knowledge relevant to the business

• Expenses incurred to upgrade skills and knowledge will beregarded as having a close nexus if they enable youremployee to:

Better perform his job duties

Progress further in your company

Perform other job functions in your company

Example:

• Professional membership fees for accountants

• IT programming course for IT engineer

24

Close Nexus Test Indicator 5: Given in recognition of employee’s contribution towards the business• Goods and services must be given to reward your

employees for their past contributions or performance

• Strong link to job contribution or performance

Example:

• Excellent service award

• Long-term service award

25

Close Nexus Test Indicator 6: Promotes corporate identity

• Corporate identity is the overall image and brand of yourbusiness

• Provision of the benefit is primarily to promote the imageof your business

Example: provision of uniforms to promote thecorporate image

26

Application

Exercise

27

Application Exercise

Question 1ABC Pte Ltd has paid for its employee the subscription fee to Institute ofCertified Public Accountants of Singapore (ICPAS) as they believe thatbeing a member of a professional body would greatly aid the business interms of the accuracy of their financial statements. The tax invoice forthe subscription fee is billed to the company. Is the GST incurredclaimable?

Answer:

• The subscription to ICPAS is regarded as for business purpose sinceit helps the employees better perform their job duties (e.g.preparing financial statements) satisfies the Close Nexus TestIndicator 4: Encourages the upgrading of employee’s skills andknowledge relevant to the business.

• Hence, input tax incurred on the subscription fee of professionalbodies (e.g. ISCA and SIATP) is claimable if you satisfy the otherconditions for claiming input tax.

28

Application Exercise

Question 2In year 2013, Hao Lian Pte Ltd will be organizing an annuallucky draw for their employees where the top prize wouldconsist of S$2,000 and a 20-inch television which cost S$321(inclusive of GST). Is output tax accountable in the abovescenarios?

Answer:• For the cash amount of S$2,000, GST is not accountable

as cash rewards are not treated as a supply.

• For the television prize:• If input tax has been claimed, output tax should be accounted

(since the cost of TV w/o GST = 100/107 x $321 = $300).• If input tax is not claimed, output tax on such gift need not be

accounted.

29

Application Exercise

Question 3Shiok Enterprise is in the movie industry. Due to the nature ofsuch industries, employees incur high entertainment expenses.Out of goodwill, the directors have agreed to reimburse theentrance fee and subscription fee for recreational sporting club toemployees. The relevant tax invoices are issued to the company’sname. The business has decided that such expenses are incurredfor business purposes. Is the GST claimable?

Answer:No. Input tax claims are disallowed under Regulation 26 of theGST (General) Regulations.

30

Application Exercise

Question 4X Trading bought some goods from a non GST-registeredsupplier for S$5,000. It was later decided that these goodsare to be given free to one of their employees as arecognition of his hard work for the previous FY. Thedirectors has noted that it is necessary to account for outputtax for goods given free to employees. Is this correct?

Answer:There is no requirement to deem (account) output tax as noinput tax was allowed to them previously.

31

Application Exercise

Question 5(a)

XYZ LLP is currently providing 20 days of free hotelaccommodation in Singapore for their foreign employees who arerelocating to Singapore so that they are able to find a flat. Is theGST claimable and is output tax required to be deemed?

Answer:

As an administrative concession, you can claim GST incurred ontemporary accommodation (e.g. hotel room and servicedapartment) provided to your foreign employees who relocate toor come to Singapore for business activities, such as meetings andprojects. Generally, the provision of accommodation notexceeding a period of 30 days is regarded as “temporaryaccommodation”.

32

Application Exercise

Answer (CONTD):

• If the family members of foreign employees are stayingtogether in the provided temporary accommodation, any costsincurred to house the family members, even on temporarybasis, are blocked as family benefits under Regulation 26 of theGST (General) Regulations.

• However, if he is entitled under your company’s policy to aspecific type of accommodation (e.g. a hotel suite) for hisindividual stay, input tax will be allowed in full even if theaccommodation is used to house both the employee and hisfamily members so long as no additional cost is incurred toaccommodate the latter.

• E.g. if costs are incurred to provide additional beds in the hotelsuite for the family members, input tax on such additional costswill be disallowed.

33

Application Exercise

Answer (CONTD):

• Output tax is not required to be deemed since this isprovision of accommodation to employees.

34

Application Exercise

Question 5(b)

All of XYZ LLP’s potential employees are required to undergo a medicalcheck-up before they are assessed to be acceptable. Can input tax beclaimed? Is output tax required to be deemed?

AnswerThe input tax incurred for the pre-employment medical examinationwhich is a compulsory requirement in their employment criteria isclaimable. This is not disallowed under Regulation 26 of the GST(General) Regulations since they are yet to be employees of thecompany.

The accounting of output tax for such free services is not required.

35

Exercise –

Preparation of GST Return

36

Answers

Box Description S$

1 Total value of standard-rated supplies

2 Total value of zero-rated supplies

3 Total value of exempt supplies

4 Total value of (1)+(2)+(3)

5 Total Value of taxable purchases

6 Output tax due

7 Input tax and refunds claimed

8 Net GST to be paid to / claimed from IRAS

9 Total value of goods imported under MES and other approved schemes

37

Answers

Box Description S$

1 Total value of standard-rated supplies 4,000

2 Total value of zero-rated supplies 2,000

3 Total value of exempt supplies 300

4 Total value of (1)+(2)+(3) 6,300

5 Total Value of taxable purchases 50,935

6 Output tax due 280

7 Input tax and refunds claimed 3,565.45

8 Net GST to be claimed from IRAS 3,285.45

9 Total value of goods imported under MES and other approved schemes

0

38

Thank you! =)

Disclaimer: This information aims to provide a better general understanding of IRAS’ practices and is not intended to

comprehensively address all possible tax issues that may arise.

This information is correct as at 16 May 2017. While every effort has been made to ensure that this information is

consistent with existing law and practice, should there be any changes, IRAS reserves the right to vary our position

accordingly.39

40