from the desk of managing partner - kg · pdf filefrom the desk of managing partner ......

TRANSCRIPT

KGS

From the desk of Managing Partner

It is with great pleasure, I would like to mention that we had organized a

full day seminar on GST with board theme “All you want to know about

GST” in collaboration with SCOPE at SCOPE complex New Delhi on

22nd December 2016. It is heartening to note that the seminar was a

great success, with about 80 participants from the various Public Sector

Undertakings throughout India and the participants included many

Managing Directors, Director (Finance) and senior personnel from the

Public Sector Undertakings. It is my pleasure to share the presentation

made by us at the said seminar. I am sure this would be of assistance for

persons interested in the subject, which is of significance impact for

trade and Industry in the country.

K.G.Somani Partner K.G.Somani & Co.

KGS

“It takes 20 years to build a reputation and five

minutes to ruin it. If you think about that, you'll

do things differently.”

Warren Buffet

INTEGRITY FIRST

KGS

Cost

S. No. Topic

1.

Tax Benefits of Home Loan

2.

Taxation Laws (Second Amendment) Act, 2016

3.

Brightside of Demonetisation

4.

GST Enrollment Procedure for existing VAT Dealers

5.

Tackling Black Money

INDEX

MANAGERIAL REMUNERATION UNDER COMPANIES ACT 2013

w

This article aims to:

Tax Benefits of Home Loan

Tax

Benefits

Of

Home loan

CA Chandan Kumar & Rohit Madaan

KGS

Tax Benefits on Home Loan

Buying a home is always a dream. It needs to be well planned and then executed so as to make the most of it. In fact it is quite an important step in Financial Planning. Managing to buy a home out of once own savings seems a faraway dream even for high net worth individuals. There is always a case of savings falling short of the property value. Thus, Home Loan comes to the rescue! However, with the falling interest rate regime during the period from 1999 to 2016 and the introduction of tax benefits on the interest paid on housing loan and repayment of principal amount, taking a home loan is not only easy but also a favored option. In fact, even if you have the money to buy it outright, availing a home loan may be mathematically a better option. Multiple tax benefits are one of the most important reasons for availing a Home Loan.

Tax Benefits for Various Sections of Home Loan: The tax benefits under various sections of the Income Tax Act not only attract people who need a loan but is also beneficial for people who can pay out of there on source of savings, as it provides them flexibility in payment and they need not do away with their liquidity.

Let’s first note the various income tax provisions under which tax benefits are available to the tax payers: 1. Tax Benefits for Interest paid on housing loan: Repayment of housing loan is through

Equated Monthly Instalments (EMI) which consists of principal and interest component. Interest component of the EMI is allowed as deduction under the head ‘Income from Housing Property’, u/s 24 of the Income Tax Act. The amount permissible for deduction is Rs. 2,00,000/for A.Y.2017 - 18.

Further, in case the house against which loan is taken is given on rent, there is no cap on the amount of interest allowed as deduction.

2. Tax Benefits for Repayment of principal on Home Loan: The principal component paid

out of the EMI is permissible as deduction up to Rs. 1,50,000/under section 80C of the Income Tax Act.

3. Interest paid during the preconstruction period on Home Loan: Interest deduction

cannot be claimed for under construction property. However, once the construction is completed, the amount of interest paid on the loan borrowed prior to completion, which is ‘Preconstruction Interest’, can be claimed as deduction in 5 equal instalments from the financial year in which construction is completed. Further, construction has to be completed within 5 years from the end of the financial year in which loan is taken.

Thus, the above deductions if availed prudently could benefit the tax payer and home loan becomes a favoured option to putting in savings.

Also, keep in mind the following points while maximizing deduction benefits:

Higher deduction in case of a Joint Home loan and ownership: In case both husband and wife are working, the deduction with respect to interest on home loan and repayment of principal can be claimed by both in proportion of their ownership share.

KGS

Avail both Home loan deduction and House Rent Allowance (HRA) exemption: The deduction u/s 24 (Interest on home loan) and u/s 80C (Repayment of principal) can be claimed along with exemption of HRA. For e.g. A person has bought a flat in Pune and taken a home loan for the same. However, due to his job requirement he needed to shift to Mumbai in a rented apartment. In this case he can claim rent paid for the Mumbai Property as HRA exemption [u/s 10(13A)] along with deduction of interest and principal for the Pune property.

Rent a home and avail higher deduction: There is good news to those who intend to buy a second home and rent the same as the amount of interest deduction on home loan which is capped at Rs. 2,00,000/in case of self-occupied property, is not applicable for the rented property.

Thus, tax benefits on home loan makes a case to avail home loan and buy your dream home.

This article aims to:

Levy of higher tax under section 115BBE.

Levy of higher penalty under section

271AAB.

Taxation Laws

(Second Amendment) Act, 2016

CA. Chandni Chandak

KGS

Taxation Laws (Second Amendment) Act, 2016

Consequent to demonetisation of high value currency, declaring specified bank notes as not legal

tender, the Taxation Laws (Second Amendment) Bill, 2016 was introduced in Lok Sabha on November

28, 2016. This Bill was passed by the Lok Sabha on November, 29, 2016. It seeks to amend the

Income-tax Act, 1961 and Finance Act, 2016. The Taxation Laws (Second Amendment) Bill, 2016

received the assent of the President on December 15, 2016.

The Taxation Laws (Second Amendment) Act, 2016 has introduced a special scheme namely, the

“Taxation and Investment Regime for Pradhan Mantri Garib Kalyan Yojana, 2016”. Under the

scheme, taxpayers may declare undisclosed income possessed in the form of cash or deposits in an

account with a bank, post office or specified entity. Under this special scheme, tax @30% of the

undisclosed income, surcharge @33% of tax and penalty @10% of such income is payable besides

mandatory deposit of 25% of the undisclosed income in Pradhan Mantri Garib Kalyan Deposit

Scheme, 2016. The deposits are interest free and have a lock-in period of four years. The income

declared under the Scheme shall not be included in the total income of the declarant under the

Income-tax Act for any assessment year. The declarations of undisclosed income made under the

Yojana will not be used as evidence under provisions of any other law (viz. Central Excise Act, 1944,

the Companies Act, 2013 etc.). However, no immunity would be available under Criminal laws

mentioned in section 119-O of the Scheme, which includes (i) the Prohibition of Benami Property

Transactions Act, 1988, (ii) the Prevention of Money Laundering Act, 2002, (iii) the Unlawful

Activities (Prevention) Act, 1967, (iv) the Black Money (Undisclosed Foreign Income and Assets) and

Imposition of Tax Act, 2015, (v) the Special Court (Trial of Offences Relating to Transactions in

Securities) Act, 1992. This special scheme shall commence on 17th December, 2016 and shall remain

open for declarations up to 31st March, 2017. The rules in this regard have been notified vide

Notification No.116 dated 16th December, 2016. A separate notification has also been issued for

Pradhan Mantri Garib Kalyan Deposit Scheme, 2016 by Department of Economic Affairs.

Levy of higher tax under section 115BBE

With effect from A.Y. 2017-18, higher rate of tax @ 60% under section 115BBE plus surcharge @ 25%

of such tax and cess @ 3% of such tax and surcharge will be applicable in respect of unexplained

investment, unexplained expenditure etc. referred to in section 68 and sections 69 to 69D, which are

included in the total income of the assessee, and reflected in the return of income furnished under

section 139 or determined by the Assessing Officer. The effective rate of tax under section 115BBE

would, therefore, be 77.25% of such undisclosed income etc., if declared in the return of income. In

case the same is not shown in the return of income, there would be a further levy of penalty under new

section 271AAC@10% of tax payable under section 115BBE. However, if income by way of undisclosed

cash or deposit is declared as per the special scheme introduced by the Taxation Laws (Second

Amendment) Act, 2016, the same will not be subject to tax under section 115BBE.

Levy of higher penalty under section 271AAB in respect of searches

initiated on or after 15th December, 2016.

The Taxation Laws (Second Amendment) Act, 2016 has also amended the penalty provisions under

section 271AAB, which are attracted in search and seizure cases. The existing slab for penalty under

section 271AAB at 10%, 20% & 60% of undisclosed income in respect of searches initiated on or after

1.7.2012, have now been made more stringent in respect of searches initiated on or after 15.12.2016.

The penalty would now be 30% of undisclosed income, in a case where such income is admitted in the

course of search initiated on or after 15th December, 2016 in a statement furnished under section

132(4), the manner in which such income was derived is explained by the assessee and tax together

with interest is paid by him on or before the specified date. In all other cases, penalty @60% of

undisclosed income shall be levied. This implies that there would be no concessional rate of penalty,

where the undisclosed income is subsequently disclosed by the assessee in the return of income filed

after the date of search and tax along with interest, if any, is paid before the specified date.

Consequently, in such a case also, penalty would be leviable@60% under section 271AAB.

Garima Sharma & Kajali Aggrawal

Brightside of

Demonetisation

This article aims to:

Movement towards cashless economy

Share of cash-based transactions

Discount on Service Charges

KGS

Brightside of Demonetization

Movements towards Cashless Economy It's been over a month since the Indian Government banned old ₹ 500 and ₹ 1000 notes, which is taking a

toll on general public. In a bid to promote cashless transaction and less cash economy, the Finance

Minister, Arun Jaitley announced 11 measures that the government has taken to expedite the digital

switchover, including discount on fuel rates and an array of services like toll tax, when paid via the digital

medium.

Our country is cash based economy. 68% of the total transactions in India are cash based. A comparison of

% of cash based transactions to total transactions’ value under different economy is shown in the figure

below:

Source-Business Standard

As Similar Comparison of currency Circulation in % of GDP as shown below-

Source-Business Standard

KGS

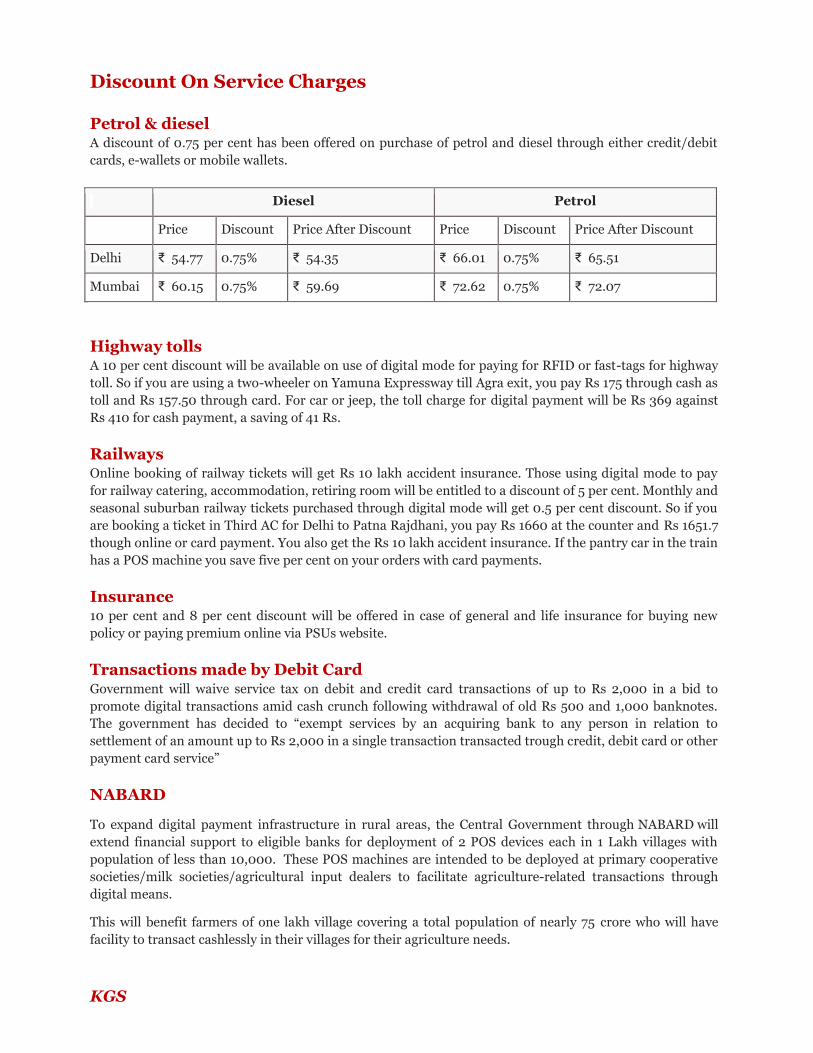

Discount On Service Charges

Petrol & diesel A discount of 0.75 per cent has been offered on purchase of petrol and diesel through either credit/debit

cards, e-wallets or mobile wallets.

Diesel Petrol

Price Discount Price After Discount Price Discount Price After Discount

Delhi ₹ 54.77 0.75% ₹ 54.35 ₹ 66.01 0.75% ₹ 65.51

Mumbai ₹ 60.15 0.75% ₹ 59.69 ₹ 72.62 0.75% ₹ 72.07

Highway tolls A 10 per cent discount will be available on use of digital mode for paying for RFID or fast-tags for highway

toll. So if you are using a two-wheeler on Yamuna Expressway till Agra exit, you pay Rs 175 through cash as

toll and Rs 157.50 through card. For car or jeep, the toll charge for digital payment will be Rs 369 against

Rs 410 for cash payment, a saving of 41 Rs.

Railways Online booking of railway tickets will get Rs 10 lakh accident insurance. Those using digital mode to pay

for railway catering, accommodation, retiring room will be entitled to a discount of 5 per cent. Monthly and

seasonal suburban railway tickets purchased through digital mode will get 0.5 per cent discount. So if you

are booking a ticket in Third AC for Delhi to Patna Rajdhani, you pay Rs 1660 at the counter and Rs 1651.7

though online or card payment. You also get the Rs 10 lakh accident insurance. If the pantry car in the train

has a POS machine you save five per cent on your orders with card payments.

Insurance 10 per cent and 8 per cent discount will be offered in case of general and life insurance for buying new

policy or paying premium online via PSUs website.

Transactions made by Debit Card Government will waive service tax on debit and credit card transactions of up to Rs 2,000 in a bid to

promote digital transactions amid cash crunch following withdrawal of old Rs 500 and 1,000 banknotes.

The government has decided to “exempt services by an acquiring bank to any person in relation to

settlement of an amount up to Rs 2,000 in a single transaction transacted trough credit, debit card or other

payment card service”

NABARD

To expand digital payment infrastructure in rural areas, the Central Government through NABARD will

extend financial support to eligible banks for deployment of 2 POS devices each in 1 Lakh villages with

population of less than 10,000. These POS machines are intended to be deployed at primary cooperative

societies/milk societies/agricultural input dealers to facilitate agriculture-related transactions through

digital means.

This will benefit farmers of one lakh village covering a total population of nearly 75 crore who will have

facility to transact cashlessly in their villages for their agriculture needs.

KGS

The Central Government through NABARD will also support Rural Regional Banks and Cooperative

Banks to issue “Rupee Kisan Cards” to 4.32 crore Kisan Credit Card holders to enable them to make digital

transactions at POS machines/Micro ATMs/ATMs.

Rentals for POS Terminals/Micro ATMs/Mobile POS Public sector banks are advised that merchant should not be required to pay more than Rs. 100 per month

as monthly rental for POS terminals/Micro ATMs/mobile POS from the merchants to bring small

merchant on board the digital payment eco system.

Nearly 6.5 lakh machines by Public Sector Banks have been issued to merchants who will be benefitted by

the lower rentals and promote digital transactions. With lower rentals, more merchants will install such

machines and promote digital transactions.

MDR Charges The Central Government Departments and Central Public Sector Undertakings will ensure that

transactions fee/MDR charges associated with payment through digital means shall not be passed on to the

consumers and all such expenses shall be borne by them. State Governments are being advised that the

State Governments and its organizations should also consider to absorb the transaction fee/MDR charges

related to digital payment to them and consumer should not be asked to bear it.

USSD Charges (Unstructured Supplementary Service Data) The TRAI also reduced USSD charges from Rs. 1.50 to 50 paise for feature phones (not smartphones) - as

feature phones comprise over 65% of all phones.

CA Kunal Jain & Shweta Tripathi

GST Enrollment

Procedure for existing

VAT Dealers

This article aims to:

GST Enrollment Procedure

Mandatory Information and Documents required

KGS

GST Enrolment Procedure for existing VAT Dealers

Step by Step procedure to enroll into GST: The State VAT Department will be communicating provisional ID and password to every

registered tax payer.

In case you are a registered tax payer with state VAT department and you have not received your

provisional ID and password, contact your State VAT Department.

Once you get provisional ID and password, you need to access the GST common

portal gst.gov.in to create unique username and new password using provisional ID and

password.

Before you create user name and password for GST common portal, you need to have a valid e-

mail and mobile phone number.

After creating user ID and password login to the GST common portal www.gst.gov.in

Fill Enrolment Application and provide business details.

Verify the auto populated details from state VAT system

Sign the Enrolment Application electronically.

Submit Enrolment Application with necessary attachment electronically

Once submitted, the details will be verified by the GST systems.

If details are satisfactory an Application Reference Number (ARN) will be issued to applicant in

‘migrated” status. The status of provisional ID will change to “Active” on the approved date and

a provisional registration Certificate will be issued.

Electronically signing of Enrolment Application: After verifying the Enrolment application, you need to sing the form. There are two option to

electronically sign the Application, You can E-Sign or sign using Digital Signature Certificate

(DSC).

You can e-sign only if Aadhaar details of the authorised signatory are provided in the authorised

signatory tab of the Enrolment Application.

In case of Companies, LLP, it is mandatory to sign the form electronically using DSC.

Mandatory information and document required for GST enrollment:

Before enrolling with GST system portal, you must ensure to have the following information and

documents available with you.

KGS

Information:

Provisional ID and password received from VAT authority

Valid e-mail address

Valid Mobile Number

Bank Account Number

Bank IFSC code

Registration number of all departments i.e. Central Excise, Service Tax, and Luxury Tax etc.

Documents:

Proof of constitution of business

o In case of Partnership Firm – deed of Partnership

o In case of others-Registration Certificate of Business Entity

Proof of principal place of Business.

Photo of Promoter, Partner, Karta of HUF

Proof of appointment of Authorized Signatory

Photo of Authorized signatory

Opening page of Bank Passbook / Statement containing Bank Account Number, Branch

address, address of account holder and latest transaction details.

Tackling Black Money

This article aims to explain:

How does the current government differ the black money is previous one as far as tackling

concerned.

CA V.K Verma & Shivam Agrawal

Introduction

In Indian economy, black money refers to the money earned in the black market on which no taxes (income and others) have been paid. While a part of it is held in the form of domestic currency, it is alleged that a substantial amount is held as real estate, gold and also in foreign accounts abroad. In February 2012, the director of India´s Central Bureau of Investigation (CBI) said that Indians have US$500 billion of illegal funds in foreign tax havens – more than any other country. According to McKinsey, the share of the black economy was about a quarter of Indian (gross domestic product) GDP in 2013.

Where it all began In response to a writ petition, in January 2011, the Supreme Court of India (SC) asked the government why the names of those who have hidden money in the Liechtenstein Bank have not been disclosed. On 4 July 2011, the SC ordered the appointment of a Special Investigating Team (SIT) headed by former SC judge B.P. Jeevan Reddy to act as a watchdog and monitor investigations dealing with black money, to be reported back to the SC directly. The two-judge bench observed that the failure of the government to control the phenomenon of black money is an indication of weakness and softness of the government. In 2016, the Panama Papers that included information on 214,000 offshore entities over a 40-year period exposed the names of 500 Indians, who scoffed government rules and regulations to build their empires abroad.

A new hope for government May 2014, PM Narendra Modi rose to power on the big promise of curbing corruption, tax evasion and black money, and is very keen to be acknowledged as a pioneer in this respect. Surely, no one disagrees with the government about the dire need to tackle black money. But the question raised here is whether the government’s stance to tackle black money has really differed from its predecessors, and how far the government is willing to go in this respect.

In December 2014, SIT asked the investigation agencies – Enforcement Directorate (ED) and

Directorate of Revenue Intelligence – to take action against companies claiming duty drawback without repatriating export proceeds. It also asked the Reserve Bank of India (RBI) to develop an institutional mechanism and IT (information technology) system to red- flag those cases where exports have been outstanding in violation of the 1999 Foreign Exchange Management Act (FEMA) guidelines.

In early 2015, SIT asked the capital markets regulator Securities and Exchange Board of India (SEBI)

to have an effective monitoring mechanism to study the unusual rise in stock prices of companies, and to regulate participatory notes issued by registered foreign institutional investors to overseas investors who wish to invest in the Indian stock markets without registering themselves with SEBI, especially those from Cayman Islands, Mauritius, and Bermuda. In 2016, SIT also recommended a ban on cash transactions above Rs. 300,000 and sought a cap on cash holdings of companies and individuals at Rs. 1,500,000. Further, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act was introduced in May 2015 to bring back illegal money stashed abroad.

Demonetisation : The turning point Instead, on 8 November 2016, PM Modi introduced demonetisation as he announced – in a broadcast to the nation – that Rs. 1,000 and 500 currency notes (constituting about 86% of total currency in circulation) would no longer be recognised legally as currency. While the policy was initially hailed as a major breakthrough to tackle black money in some quarters, there are now growing concerns about its effectiveness and implementation. Most importantly, only a small proportion of black money is estimated to be held in cash (about 6%, as evident from income tax raids), and there are loopholes in the implementation of the law, example, it exempts hands offered to temples, which may help specific religious groups to convert black money into white (this can be regarded as unconstitutional, given secular nature of the State). As such, it is unlikely to have a significant effect on existing black money held domestically.

KGS

KGS

The Future Prospectus Data released by the RBI in 2016 shows that about 86% of the currency in circulation is in the form of Rs. 1,000 and 500 notes, which comes to about Rs. 13 trillion. Some may argue that cleaning up the cash part of the black money induced by demonetisation may boost the economy. This would depend on how much of the ‘lost’ currency notes plus all the idle cash held by all sorts of people will return as deposits into the banking system. while no one has a good estimate about the amount of idle cash (both legal and illegal) held by people outside the banking system, it is fair to assume that a substantial amount of this money would come back as commercial bank deposit (even allowing for the tax penalty for depositing cash over Rs. 250,000 per person). Indeed, newspaper reports confirm that about Rs. 8.5 trillion were raised from cash deposits (though no one knows what proportion of it is black money) in the first 17 days of demonetisation, a significant proportion of which will be held in various State-controlled banks. However, SBI itself has written off Rs. 480 billion worth of bad loans, as of 30 June 2016. If ‘increasing the bank deposits via demonetisation’ policy is directed towards balancing books of bankrupt State-controlled banks with huge bad debts, its potential productivity benefit is likely to be rather limited. Since the government has failed to recover much black money and is widely perceived as being soft on corporate defaulters and Swiss Bank/Panama Papers bigwigs, it felt the need to signal that it is serious about black money by purporting to shake the system. The result was the introduction of demonetisation that is hard to implement not only because of infrastructural deficiencies, but also regulatory loopholes. The government’s anti-corruption rhetoric thus appears to be more like tall talk rather than effective action.

KGS

Contact Name E-mail Mobile Mr. Anuj Somani [email protected] +91 9871098777 Mr. Bhuvnesh Maheshwari [email protected] +91 9810031993

Head office: Branch Offices: Network Offices: DELHI MUMBAI BANGALORE

Delite Cinema Hall GHAZIABAD BHOPAL 3rd Floor, Gate No. 2, New Delhi, India GURGAON BUBNESHWAR

SILIGURI CHENNAI

CHENNAI KOLKATA

Disclaimer

• This material and the information contained herein prepared by the authors is of a general nature and does not exhaustively deal with the subject discussed. • Although the authors have put their earnest effort in providing accurate and appropriate information, the article is not intended to be relied upon as the sole basis for any decision which may affect you or your business. The authors recommend you take professional advice before acting on specific issues. • KGS is neither responsible for any views, opinions and statements made by the authors nor is liable for consequences, if any, arising from actions based on such views or opinion.

Contact Us