“fuel cell material handling: u.s. - uk hfca · fuel cell material handling: u.s. success and...

TRANSCRIPT

Celia Greaves +44 (0) 1206 241360

Webinar 27th November, 2013

“Fuel Cell Material Handling: U.S. success and European growth”

Representing the UK Hydrogen and Fuel Cell Industry

by enabling

accelerated innovation

access to funding

partnerships

international engagement

cross-sector links

technology deployment

Energy Generation & Supply KTN A dynamic network delivering strategic value

to the UK energy sector

Representing the UK Hydrogen and Fuel Cell Industry

Wave & Tidal

Fuel Cells & Hydrogen Maximising Oil & Gas

Resources

Future & Emerging Opportunities

Offshore Wind

Carbon Abatement Technologies

Large Power Stations

Nuclear

EG&S KTN Priority Areas Representing the UK Hydrogen and Fuel Cell Industry

Benefits of membership

greater awareness of developments in the energy space, particularly the cross-cutting issues

the opportunity to attend regular workshops and networking events,

the opportunity to participate in webinars,

access to reports and other KTN materials,

participation in focus working groups, and

insights into new funding opportunities and key developments across the fuel cell and hydrogen landscape

…over 4,500 members

Membership of the EG&S KTN is free of charge and provides multiple benefits, including:

Representing the UK Hydrogen and Fuel Cell Industry

Events Representing the UK Hydrogen and Fuel Cell Industry

Events: Stimulating access to funding

Fuel cells manufacturing and supply chain Competition – Consortium Building Event, November 2013

Joint TSB and EG&S KTN workshops on “Fuel Cell Manufacturing and Supply Chain”, August / September 2013

Joint TSB, EG&S KTN and RCUK workshop on “Outstanding Business and Research Challenges for Hydrogen”, May 2013

Joint EG&S KTN and EU Energy Focus webinar on the FCH JU 2013 Call, March 2013

Expanding your reach into energy – we can help you:

Find new partners / build new relationships

Gain deeper understanding of challenges and opportunities and how you can respond

Access new funding

Events: Exploring specific themes

Fuel Cell Material Handling: U.S. success and European growth- webinar, November 2013

Power to Gas: New Opportunities - webinar, March 2013

Facilitating on-line collaboration

Focus work groups to support new Calls

On-line sub-groups to provide a focus for specific interests / activities

Private groups to allow sharing and exchange

Representing the UK Hydrogen and Fuel cell industry.

Accelerating the commercialization of fuel cell and hydrogen energy.

Helping fuel cells and hydrogen energy to become a key component of a low carbon economy – reducing greenhouse gases, enhancing energy security and delivering ‘green collar’ jobs.

We cover:

All fuel cell types and applications;

The full fuel cell supply chain (from research into material science through to systems integration and distribution);

Hydrogen production and storage;

Hydrogen infrastructure; and

Other issues around the delivery, storage and use of associated fuels.

UK HFCA

Representing the UK Hydrogen and Fuel Cell Industry

Representing the UK Hydrogen and Fuel Cell Industry Representing the UK Hydrogen and Fuel Cell Industry

Webinar tips

Please type any questions that arise during the presentations in the

chat box. These will be addressed to speakers during the Q&A part of

the webinar.

If you face any technical difficulties please send Nikoleta a private note

via the chat box by choosing her name from the list, give her a call on

07580 945008 or send an e-mail at [email protected].

Please keep your microphones muted throughout the session to avoid

interference.

Representing the UK Hydrogen and Fuel Cell Industry

This event will:

Provide an overview of U.S. and European developments in fuel cell material handling

Explain how DOE support and other activities have helped stimulate the sector

Give a commercial view of recent progress and prospects for further growth, both in the U.S. and Europe

Webinar objectives

Representing the UK Hydrogen and Fuel Cell Industry

Agenda 14.00pm Introduction, Celia Greaves, Energy Generation and Supply KTN

and UK Hydrogen and Fuel Cell Association

14.10pm U.S. DOE funded performance validation of fuel cell material handling deployments and current status, Jennifer Kurtz, National Renewable Energy Laboratory

14.40pm Fuel Cell Material Handling: Commercial progress and prospects for further growth in U.S. and Europe, Warren Brower, Plug Power / HyPulsion

15.10pm Q&A session

15.30pm Close

Representing the UK Hydrogen and Fuel Cell Industry

NREL is a na*onal laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable Energy, operated by the Alliance for Sustainable Energy, LLC.

U.S. DOE Funded Performance Valida7on of Fuel Cell Material Handling Equipment

UK Hydrogen and Fuel Cell Associa7on Webinar

Jennifer Kurtz, Sam Sprik, Todd Ramsden, Genevieve Saur, Chris Ainscough, MaN Post, Mike Peters

November 27, 2013

2

FCMHE Valida7on Overview

• U.S. DOE enabling early fuel cell markets • Na7onal Fuel Cell Technology Evalua7on Center objec7ves

• FCMHE Performance Status

3 | Fuel Cell Technologies Office eere.energy.gov

Enabling Early Markets Deployments help catalyze market penetration and ensure continued technology

utilization growth while providing data and lessons learned.

Leveraging DOE Funds: Government as “catalyst” for market success of emerging technologies.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Cost Share Deployments ~1,600

Additional Purchases without DOE Funding

~9,000

Lift Trucks BU Power

Backup Power

Lift Trucks

DOE cost-shared deployments led to >5X additional purchases and orders.

~9,000 ADDITIONAL FUEL CELL LIFT TRUCKS AND BACKUP POWER UNITS PLANNED OR INSTALLED with NO DOE funding Examples of industry* sectors in DOE ARRA projects

• Telecommunications (e.g. AT&T, PG&E. Sprint, etc.) • Distribution Centers/Warehouses (e.g. FedEx, Genco,

Sysco, Wegmans, Whole Foods, etc.)

*Provided as examples and not intended as endorsement

DOE FCTO Fall 2013 http://www1.eere.energy.gov/hydrogenandfuelcells/presentations.html

4 | Fuel Cell Technologies Office eere.energy.gov

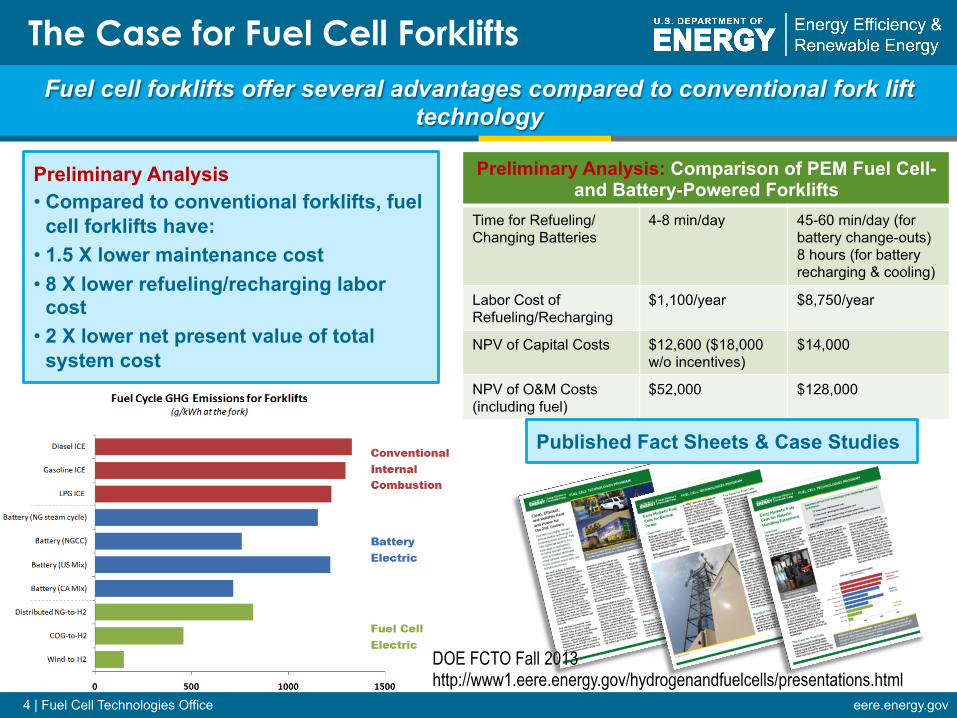

The Case for Fuel Cell Forklifts Fuel cell forklifts offer several advantages compared to conventional fork lift

technology

Preliminary Analysis • Compared to conventional forklifts, fuel

cell forklifts have: • 1.5 X lower maintenance cost • 8 X lower refueling/recharging labor

cost • 2 X lower net present value of total

system cost

Preliminary Analysis: Comparison of PEM Fuel Cell- and Battery-Powered Forklifts

Time for Refueling/ Changing Batteries

4-8 min/day 45-60 min/day (for battery change-outs) 8 hours (for battery recharging & cooling)

Labor Cost of Refueling/Recharging

$1,100/year $8,750/year

NPV of Capital Costs $12,600 ($18,000 w/o incentives)

$14,000

NPV of O&M Costs (including fuel)

$52,000 $128,000

Published Fact Sheets & Case Studies

DOE FCTO Fall 2013 http://www1.eere.energy.gov/hydrogenandfuelcells/presentations.html

5

www.nrel.gov/hydrogen/proj_tech_valida5on.html

NFCTEC Analysis Approach

National Fuel Cell Technology Evaluation Center

NFCTEC

Analysis and repor7ng of real-‐world opera7on data

6

Objec7ves

• Assess technology o Perform independent technology assessment in real world opera*on condi*ons o Focus on fuel cell system and hydrogen infrastructure: performance, opera*on, and

safety o Leverage data processing and analysis capabili*es developed under the fuel cell vehicle

Learning Demonstra*on project o Evaluate material handling equipment (MHE) and backup power o Analysis includes up to 1,000 fuel cell systems deployed with American Recovery and

Reinvestment Act (ARRA) funds

• Support market growth o Provide analyses and results relevant to the markets’ value proposi*on o Report on technology status to fuel cell and hydrogen communi*es and other key

stakeholders such as end users

Assess the technology status in real world operations, establish performance baselines, report on fuel cell and hydrogen

technology, and support market growth by evaluating performance relevant to the markets’ value proposition

7

74 MHE CDPs—Count and Category

Deployment & Site Overview (1, 40)

Fuel Cell Opera7on (2, 7, 8, 11, 15,

16, 17, 23, 24, 63) Fuel Cell Reliability (28, 29, 30, 31)

Fuel Cell Safety (26, 27, 53, 56, 57)

Infra. Safety (25, 41, 46, 51, 55)

Infra. Reliability (45, 48, 49, 50)

FC Maintenance (12, 13, 14, 43, 54, 61)

NREL cdp_mhe_58 Created: Sep-23-11 4:32 PM

Cost of Ownership (58, 59, 60,64)

NREL cdp_mhe_59 Created: Sep-23-11 4:32 PM

Fuel Cell Durability (32, 33, 34, 38, 39, 73)

< 10000 hours > 10000 hours 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Fuel Cell Stacks Projected Hours to 10% Voltage Degradation

Projected Hours to 10% Voltage Degradation 1,3

FC S

tack

s [%

]

In ServiceNot In Service2

NREL cdp_mhe_97

Created: Apr-02-13 9:36 AM | Data Range: 2009Q1-2012Q4

1) Projection using field data, calculated at high stack current, from operation hour 0. Projected hours may differ from an OEM's end-of-life criterion and does not address "catastrophic" failure modes.2) Indicates stacks that are no longer accumulating hours either a) temporarily or b) have been retired for non- stack performance related issues or c) removed from DOE program.3) Projected hours limited based on demonstrated hours.

0 10 20 30 40 50 600

1

2

3

4

5

6

7

8

9

10

Amount Fueled in an Hour [kg]

Freq

uenc

y [%

of t

otal

]

Hydrogen Dispensed Per Hour - ARRA

NREL cdparra_mhe_69

Created: Apr-02-13 8:41 AM | Data Range: 2010Q1-2012Q4

Average: 4.8 kgs per hourMedian: 3.5 kgs per hourMax: 52.5 kgs per hour

Infra. Opera7on (3, 4, 5, 6, 9, 10, 21, 22, 35, 37, 42, 62, 65, 68, 69, 70,

71)

1 2 3 4 5 6 7 80

10

20

30

40

50

60

70

80

90

100

Station (Sorted By Increasing Max Daily Amount)

Cap

acity

Util

izat

ion

2 [%]

Station Capacity Utilization

Max Daily20 kg

Max Daily25 kg

Max Daily64 kg

Max Daily99 kg

Max Daily102 kg

Max Daily135 kg

Max Daily293 kg

Max Daily358 kg

42.9%

Average Daily Utilization1

Maximum Daily Utilization

NREL cdparra_mhe_71NREL cdparra_mhe_71

Created: Apr-02-13 10:48 AM | Data Range: 2009Q4-2012Q4

1Maximum quarterly utilization considers all days; average daily utilization considers only days when at least one filling occurred2100% represents maximum daily amount dispensed for each individual site

1 2 3 4 5 6 7 80

50

100

150

200

250

Station (Sorted By Increasing Max Daily Amount)

Fills

Per

Day

Station Usage

Maximum Daily Fills

Average Daily Fills1

NREL cdparra_mhe_70

Created: Apr-02-13 8:52 AM | Data Range: 2010Q1-2012Q4

1Average daily fills considers only days when at least one fill occurred

0 5 10 15 20 25 30 35 40 450

2

4

6

8

10

12

Number of Fuelings in an Hour

Freq

uenc

y [%

of t

otal

]

Number of Fuelings Per Hour - ARRA

NREL cdparra_mhe_68

Created: Apr-02-13 8:25 AM | Data Range: 2010Q1-2012Q4

Average: 7.3 per hourMedian: 5.0 per hourMax: 39.0 per hour

<0 0 2 4 6 8 10 12 14 16 18 200

5

10

15

20

25

30

Sim

ulta

neou

s Fi

lls

Back-to-Back Fills

36 % of fills are within 0-5 minutes of each other23 % of fills have more than 20 minutes between them228912 Total Fills

Time Between Fuelings* [min]

# of

Fue

lings

[% o

f tot

al]

Histogram of Time Between Fuelings

All Sites CombinedIndividual Sites

200 225 250 275 300 325 350 375 400 425 4500

1

2

3

4

5x 104 Final Pressures for Fills with <5 Minutes in Between

# of

Fue

lings

Final Pressure [bar]

Previous FillNext Fill

NREL cdparra_mhe_65

Created: Apr-02-13 8:12 AM | Data Range: 2010Q1-2012Q4 *Time is from end of fill to start of next fill.

Infra. Maintenance (18, 19, 20, 44, 47, 52,

66, 67, 72,76,77)

0

50

100

150

200

250

AIR SYSTEM

CONTROL ELECTRONICS

DISPENSER

FITTINGS&PIPIN

G

HYDROGEN COMPRESSOR

VALVES

MTB

F (D

ays)

MTBF by Equipment Category: Infrastructure (Delivered H2 Only)

Median SiteLowest Site

NREL cdparra_mhe_72

Created: Apr-02-13 11:01 AM | Data Range: 2010Q1-2012Q4

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

20

40

60

80

100

120

140

160

Month

Cou

nt o

f Mai

nten

ance

Eve

nts

Infrastructure Maintenance by Month

UnscheduledScheduled

NREL cdp_mhe_67

Created: Apr-02-13 9:36 AM | Data Range: 2009Q1-2012Q4

8%

19%

23%

50%

Total Events = 1,0581

64% unscheduled

entiresystem 46

misc 124

multiplesystems 221

classifiedevents1 667

Event Count

8%

19%

17%

56%

Total Hours = 7,08062% unscheduled

hydrogen compressor

control electronics

dispenser

air system

NREL cdp_mhe_66

Created: Apr-02-13 9:35 AM | Data Range: 2009Q1-2012Q4

Delivered Hydrogen Infrastructure Maintenance By Equipment Type

MISC includes the following failure modes: seal, fuel system, safety,thermal management, storage, electrical, software, fittings&piping, valves,

sensors, other

0

10

20

30

40

50

60

70

80

90

100

Apr-201

0

Jul-2

010

Oct-20

10

Jan-20

11

Apr-201

1

Jul-2

011

Oct-20

11

Jan-20

12

Apr-201

2

Jul-2

012

Oct-20

12

Jan-20

13

Apr-201

3

% o

f Tot

al M

onth

ly M

aint

enan

ce L

abor

Hou

rs

Equipment Percentage of Repair Labor Hours Over Time*

HYDROGEN COMPRESSORCONTROL ELECTRONICSDISPENSERAIR SYSTEMNREL cdparra_mhe_77

Created: Sep-30-13 12:56 PM | Data Range: 2010Q10-2013Q2

*Calculated as a percentageof all maintenance each month; bars maynot total to 100% if other maintenancecategories were present.

0123456789

101112

AIR SYSTEM

CONTROL ELECTRONICS

DISPENSER

ELECTRICAL

ENTIRE SYSTEM

FITTINGS&PIPIN

G

FUEL SYSTEM

HYDROGEN COMPRESSOR

MULTIPLE SYSTEMS

OTHER

SAFETY

SENSORS

SOFTWARE

STORAGE

THERMAL MANAGEMENT

VALVES

Rep

air L

abor

Tim

e (H

ours

)

Equipment Category Repair Time: Infrastructure (Delivered H2 Only)

NREL cdparra_mhe_76

Created: Sep-28-13 10:08 AM | Data Range: 2010Q10-2013Q2

75% Percentile

Median

25% Percentile

Mean

8

MHE Opera7on Summary 2009 Q4–2013 Q2

Units in opera*on*

Hydrogen fills

Hydrogen dispensed in kg

Opera*on hours

Average opera*on hours between fills

Average fill amount in kg

Average fill *me in minutes *One project has completed

Valida*on of MHE is based on real-‐world opera*on data from high-‐use facili*es

9

Study of FC Voltage Degrada7on Against 10,000 Hours

< 10000 hours > 10000 hours 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Fuel Cell Stacks Projected Hours to 10% Voltage Degradation

Projected Hours to 10% Voltage Degradation 1,3

FC S

tack

s [%

]

In ServiceNot In Service2

NREL cdp_mhe_97

Created: Sep-28-13 12:46 PM | Data Range: 2009Q1-2013Q2

1) Projection using field data, calculated at high stack current, from operation hour 0. Projected hours may differ from an OEM's end-of-life criterion and does not address "catastrophic" failure modes.2) Indicates stacks that are no longer accumulating hours either a) temporarily or b) have been retired for non- stack performance related issues or c) removed from DOE program.3) Projected hours limited based on demonstrated hours.

More than 50% of stacks have projected hours to 10% voltage degrada*on >10,000 hours.

10

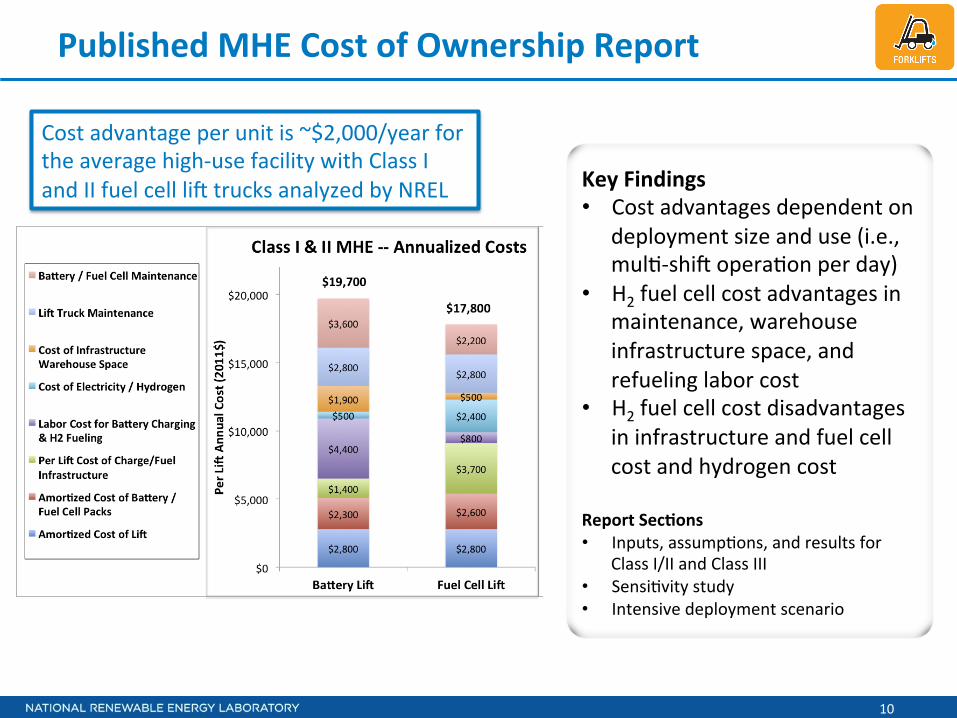

Published MHE Cost of Ownership Report

Key Findings • Cost advantages dependent on

deployment size and use (i.e., mul*-‐shi_ opera*on per day)

• H2 fuel cell cost advantages in maintenance, warehouse infrastructure space, and refueling labor cost

• H2 fuel cell cost disadvantages in infrastructure and fuel cell cost and hydrogen cost

Report Sec7ons • Inputs, assump*ons, and results for

Class I/II and Class III • Sensi*vity study • Intensive deployment scenario (1) Total cost represents the annualized cost of ownership of Class I, II, and III forklifts on a net present value basis, accounting for

capital, operating, and maintenance costs of forklifts, power packs, and infrastructure (labor costs for maintenance and for charging or fueling are included, but labor costs of forklift material handling operations are excluded). Costs are calculated assuming that the material handling operations are ongoing, with equipment replacements made as necessary. Capital, operating, and maintenance costs are assumed to remain constant in real-dollar terms, and capital purchases are discounted using a discount rate representing the time value of money. Fuel cell system costs reflect the current fuel cell tax credit of $3,000/kW or 30% of purchase price. Analysis does not consider the potential productivity increases resulting from the constant power output of fuel cell systems, which may be significant. Costs of ownership of Class II forklifts are expected to be similar for Class I forklifts, though the cost of the lift itself is expected to be higher. Costs are based on information provided by deployment host partners (end-users) based on a questionnaire developed by NREL, supplemented with data provided by project partners, and are reflective of the material handling operations of these deployments. Where appropriate, fuel cell deployment data were used in place of end-user questionnaire data; in particular, data from CDPs 1, 6, 8, 14, and 22 were used. Cost assessment will be further refined as additional data are available.

Total Cost of Ownership for Class I, II & III Forklifts1

NREL cdp_mhe_58 Created: Sep-23-11 4:32 PM

Cost advantage per unit is ~$2,000/year for the average high-‐use facility with Class I and II fuel cell li_ trucks analyzed by NREL

11

Study of Infrastructure Usage by Daily Fills

1 2 3 4 5 6 7 80

50

100

150

200

250

Station (Sorted By Increasing Max Daily Amount)

Fills

Per

Day

Station Usage

Maximum Daily Fills

Average Daily Fills1

NREL cdparra_mhe_70

Created: Sep-26-13 10:20 AM | Data Range: 2009Q4-2013Q2

1Average daily fills considers only days when at least one fill occurred

The maximum daily fill count for two sites was >200 fills. Those two sites average nearly 100 fills per day.

12

0 25 50 75 100 125 150 175 200 225 250 275 3000

1

2

3

4

5

6

7

8

9

10

Site MTBF1 (Days)

Cou

nt o

f Site

sSite MTBF (Calendar Days In Operation): Infrastructure

NREL cdp_mhe_48

Created: Sep-28-13 12:45 PM | Data Range: 2009Q1-2013Q21. Cumulative Mean Time Between Failure

Infrastructure Reliability Analysis

Infrastructure consistently delivering 250 and 350 bar fills even though the majority of the sites have a MTBF of 25 days or less

Compressor 51%

Control Electronics 20%

Dispenser 19%

Air System 10%

Delivered H2 Maintenance Count by Category 1,330 Maintenance Events

63% unscheduled

13

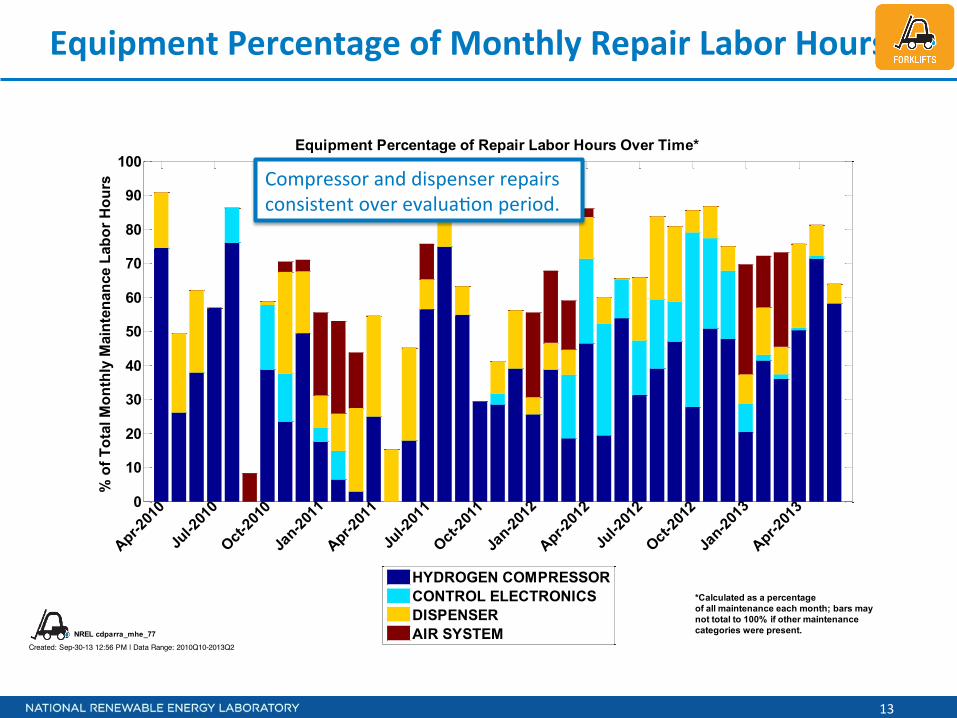

Equipment Percentage of Monthly Repair Labor Hours

0

10

20

30

40

50

60

70

80

90

100

Apr-201

0

Jul-2

010

Oct-20

10

Jan-20

11

Apr-201

1

Jul-2

011

Oct-20

11

Jan-20

12

Apr-201

2

Jul-2

012

Oct-20

12

Jan-20

13

Apr-201

3

% o

f Tot

al M

onth

ly M

aint

enan

ce L

abor

Hou

rs

Equipment Percentage of Repair Labor Hours Over Time*

HYDROGEN COMPRESSORCONTROL ELECTRONICSDISPENSERAIR SYSTEMNREL cdparra_mhe_77

Created: Sep-30-13 12:56 PM | Data Range: 2010Q10-2013Q2

*Calculated as a percentageof all maintenance each month; bars maynot total to 100% if other maintenancecategories were present.

Compressor and dispenser repairs consistent over evalua*on period.

14

0

50

100

150

200

250

AIR SYSTEM

CONTROL ELECTRONICS

DISPENSER

FITTINGS&PIPIN

G

HYDROGEN COMPRESSOR

SENSORS

VALVES

MTB

F (D

ays)

MTBF by Equipment Category: Infrastructure (Delivered H2 Only)

Median SiteLowest Site

NREL cdparra_mhe_72

Created: Sep-26-13 10:24 AM | Data Range: 2010Q1-2013Q2

Breakdown of MTBF by Key Delivered Hydrogen Infrastructure Categories

Consistent across all sites are failures with control electronics and hydrogen compressors. These two categories have low MTBF.

15

Breakdown of Failure Modes for Top Four Maintenance Categories for Infrastructure

0 100 200 300 400

HYDROGEN COMPRESSOR

DISPENSER

CONTROL ELECTRONICS

AIR SYSTEM

Event Count

51%*

20%*

19%*

10%*

DATA ERROR

DRIVE OFF

EXCESSIVE NOISE

FAILED CLOSED

HYDROGEN LEAK

INSPECT TROUBLE ALARM OR REPORT

LIGHTNING STRIKE

METAL FATIGUE

MOISTURE INFILTRATION

OUT OF CALIBRATION

PRESSURE LOW

REPLACE FAILED PARTS

TEMPERATURE HIGH

MISC

0 500 1000 1500 2000 2500 3000 3500

HYDROGEN COMPRESSOR

DISPENSER

CONTROL ELECTRONICS

AIR SYSTEM

Labor Hours

58%*

18%*

14%*

9%*

NREL cdp_mhe_52

Created: Sep-26-13 9:51 AM | Data Range: 2009Q1-2013Q2

Failure Modes for Top Four Infrastructure Equipment Categories

* Percentage of total events or hours, reference CDP 66.

MISC includes the following failure modes: ambient temperature too low, broken wire,cavitation, data error, debris infiltration, electrical short, failed closed, false alarm, flow

high, flow low, fluid leak non-hydrogen, fluid leak non_hydrogen, fluidleak_non_hydrogen, inspect trouble alarm or report, maintenance error, manufacturing

defect, metal fatigue, moisture infiltration, network malfunction, operator protocol, other,power outage, pressure high, pressure low, replace failed parts, software bug,

unspecified electronics failure, vandalism, voltage low, other

There are many different failure modes for the top four categories and these modes provide insight for RD&D needs

16

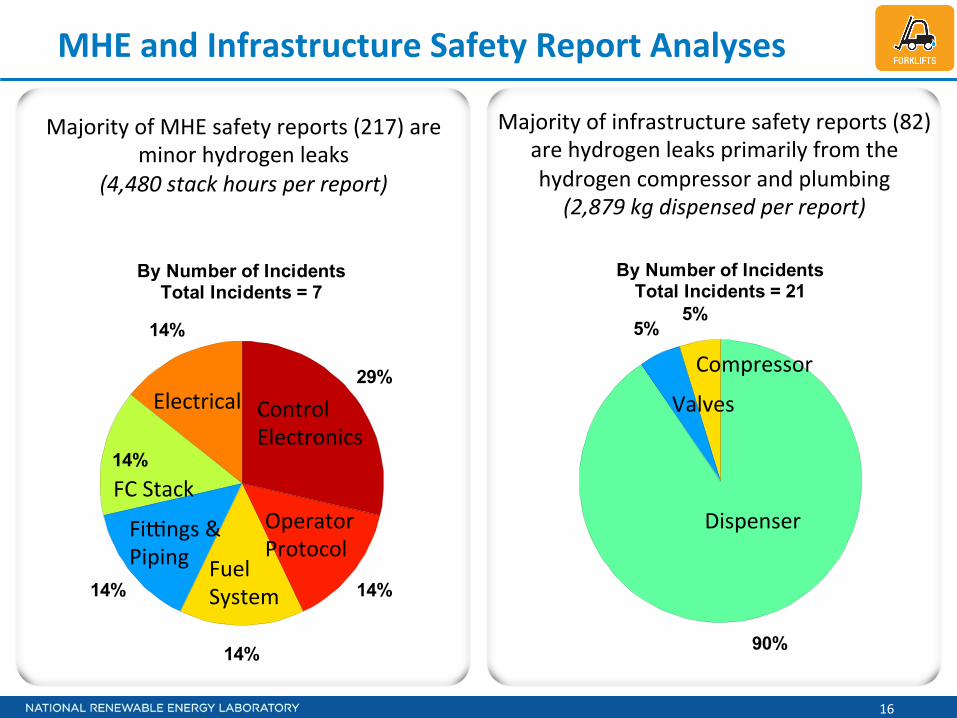

MHE and Infrastructure Safety Report Analyses

5%5%

7%

10%

21%

50%

By Number of ReportsTotal Near Miss Reports = 210

14%

14%

14%

14%

14%

29%

By Number of IncidentsTotal Incidents = 7

control electronics

operator protocol

electrical

fuel system

fc stack

valves

air system

fittings & piping

thermal management

Misc

NREL cdparra_mhe_57

Created: Mar-26-12 4:23 PM

Safety Reports By Equipment Category: ARRA MHE

MISC includes the following categories:SOFTWAREELECTRICALREFORMERSENSORS

SEALOTHER

An INCIDENT is an event that results in: - a lost time accident and/or injury to personnel - damage/unplanned downtime for project equipment, facilities or property - impact to the public or environment - any hydrogen release that unintentionally ignites or is sufficient to sustain a flame if ignited - release of any volatile, hydrogen containing compound (other than the hydrocarbons used as common fuels)A NEAR-MISS is: - an event that under slightly different circumstances could have become an incident - unplanned H2 release insufficient to sustain a flame

Control Electronics

Operator Protocol

Fuel System

Fikngs & Piping

FC Stack

Electrical

Majority of MHE safety reports (217) are minor hydrogen leaks

(4,480 stack hours per report)

Majority of infrastructure safety reports (82) are hydrogen leaks primarily from the hydrogen compressor and plumbing

(2,879 kg dispensed per report)

18%

20%

48%

By Number of ReportsTotal Near Miss Reports = 71

5%5%

90%

By Number of IncidentsTotal Incidents = 21hydrogen compressor

fittings & piping

dispenser

seal

valves

reformer

Misc

NREL cdp_mhe_46

Created: Sep-26-13 2:14 PM | Data Range: 2009Q1-2013Q2

Safety Reports By Equipment Category: Infrastructure

MISC includes the following categories:STORAGE

FUEL SYSTEMOTHER

An INCIDENT is an event that results in: - a lost time accident and/or injury to personnel - damage/unplanned downtime for project equipment, facilities or property - impact to the public or environment - any hydrogen release that unintentionally ignites or is sufficient to sustain a flame if ignited - release of any volatile, hydrogen containing compound (other than the hydrocarbons used as common fuels)A NEAR-MISS is: - an event that under slightly different circumstances could have become an incident - unplanned H2 release insufficient to sustain a flame

Dispenser

Compressor

Valves

17

Technical Summary—What We’ve Learned

• Opera*ng with an average availability of ~98% at eight end-‐user facili*es.

• Most systems operate at least 6 hours a day.

• Cost of ownership comparison between fuel cell and balery MHE indicate significant cost savings for refueling labor and infrastructure space but much greater cost for hydrogen infrastructure and fuel.

• MHE infrastructure can provide insight into infrastructure performance for the light duty vehicle applica*on.

Aggregated data showcase performance over the last two

years in MHE and backup power.

Performance results address a need for published results on

the technology status.

Data analyses develop as systems operate and based on the key performance areas in

the markets.

18

This project is supported by the U.S. Department of Energy Fuel Cell Technology Office EERE, Jason

Marcinkoski, Sara Dillich, & Pete Devlin

Jennifer Kurtz jennifer.kurtz nrel.gov @

Image Source: NREL

1 1

Fuel Cell Material Handling:

U.S. Success & European Growth

Warren Brower, November 27, 2013

The content of this presentation is

PLUG POWER INC. PROPRIETARY AND

CONFIDENTIAL.

Copyright 2013 by Plug Power Inc.

2

This communication contains statements that are not historical facts and are considered forward-looking within the meaning of Section 27A of the

Securities Act and Section 21E of the Exchange Act. These forward-looking statements contain projections of our future results of operations or of our

financial position or state other forward-looking information. We believe that it is important to communicate our future expectations to our investors.

However, there may be events in the future that we are not able to accurately predict or control and that may cause our actual results to differ

materially from the expectations we describe in our forward-looking statements. Investors are cautioned not to unduly rely on forward-looking

statements because they involve risks and uncertainties, and actual results may differ materially from those discussed as a result of various factors,

including, but not limited to: the risk that we continue to incur losses and might never achieve or maintain profitability, the risk that we expect we will

need to raise additional capital to fund our operations and such capital may not be available to us; the risk that we do not have enough cash to fund

our operations to profitability and if we are unable to secure additional capital, we may need to reduce and/or cease our operations; the risk that a

"going concern” opinion from our auditors, KPMG LLP, could impair our ability to finance its operations through the sale of equity, incurring debt, or

other financing alternatives; the recent restructuring plan we adopted may adversely impact management’s ability to meet financial reporting

requirements; our lack of extensive experience in manufacturing and marketing products may impact our ability to manufacture and market products

on a profitable and large-scale commercial basis; the risk that unit orders will not ship, be installed and/or converted to revenue; the risk that pending

orders may not convert to purchase orders; the risk that our continued failure to comply with NASDAQ’s listing standards may result in our common

stock being delisted from the NASDAQ stock market, which may severely limit our ability to raise additional capital; the cost and timing of developing,

marketing and selling our products and our ability to raise the necessary capital to fund such costs; the ability to achieve the forecasted gross margin

on the sale of our products; the actual net cash used for operating expenses may exceed the projected net cash for operating expenses; the cost and

availability of fuel and fueling infrastructures for our products; market acceptance of our GenDrive systems; our ability to establish and maintain

relationships with third parties with respect to product development, manufacturing, distribution and servicing and the supply of key product

components; the cost and availability of components and parts for our products; our ability to develop commercially viable products; our ability to

reduce product and manufacturing costs; our ability to successfully expand our product lines; our ability to improve system reliability for our GenDrive

systems; competitive factors, such as price competition and competition from other traditional and alternative energy companies; our ability to protect

our intellectual property; the cost of complying with current and future federal, state and international governmental regulations; and other risks and

uncertainties discussed under “Item IA—Risk Factors” in Plug Power’s annual report on Form 10-K for the fiscal year ended December 31, 2012, filed

with the Securities and Exchange Commission (“SEC”) on April 1, 2013 and as amended on April 30, 2013 and the reports Plug Power filed from time

to time with the SEC. These forward-looking statements speak only as of the date on which the statements were made and are not guarantees of

future performance. Except as may be required by applicable law, we do not undertake or intend to update any forward-looking statements after the

date of this communication.

3

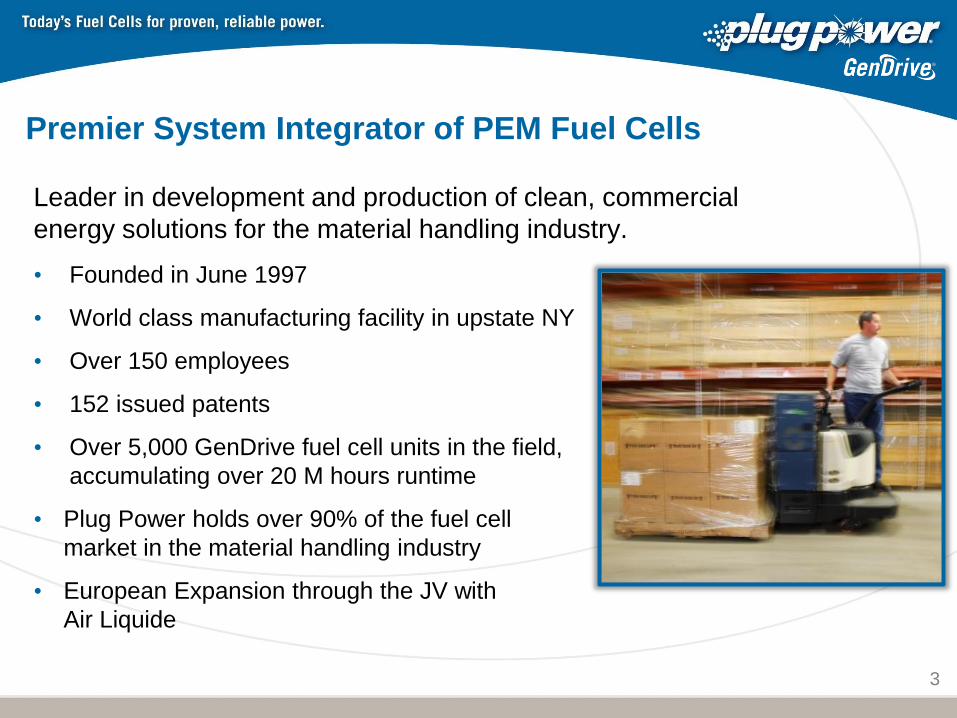

Leader in development and production of clean, commercial

energy solutions for the material handling industry.

• Founded in June 1997

• World class manufacturing facility in upstate NY

• Over 150 employees

• 152 issued patents

• Over 5,000 GenDrive fuel cell units in the field,

accumulating over 20 M hours runtime

• Plug Power holds over 90% of the fuel cell

market in the material handling industry

• European Expansion through the JV with

Air Liquide

Premier System Integrator of PEM Fuel Cells

Plug Power: Poised for Profitability

Today’s focus: material handling market

• Endorsed via an investment by Air Liquide, a leading industrial gas firm

• Significant and new customers are buying

• Quality problems behind us

• EBITDA profitability within reach

• Success in materials transport is generating interest (and development funds)

from adjacent markets

4

This is the first step toward Plug Power’s long-term

goal to displace lead-acid batteries and diesel engines

in a broad array of applications.

HyPulsion - European Joint Venture Created 2012

• Luc VANDEWALLE : Managing Director

• Warren BROWER : Product, Marketing, OEM Director

• Paul DEPREZ : Sales & After Sales Director

• Sosthene GRANDJEAN : Program Management

• Camille VRIGNAUD : Customer Support – Service Technician

• Arnaud CERCEAU : Operations & Manufacturing

• Michael NINDEL : Business Dev. Germany

• Ranjieve WILLIAMS : Engineering Director European Team

• US Engineers : 7 Design Engineers (Plug Power)

6

• HyPulsion has completed one year of business and product development activities

• Shipment of product has begun in multiple countries with multiple OEMs

• Market opportunity greater than North America

• 9 CE certified products with multiple configurations available for deployment

• Collaboration projects in place with 7 fork lift OEMs

• Includes Jungheinrich, TMHE, Linde/Fenwick, Still, Crown, NACCO, Airmarrel

HyPulsion JV is Bearing Fruit

GenDrive Benefits

Operational Benefits

• Increased Productivity

• Reduced Operational Costs

• Additional Commercial Space

• Reduced Carbon Emissions

GenDrive® Products

Counterbalanced Trucks

Reach Trucks

Rider Order Picking Trucks

Total Power Solution

• Hydrogen Infrastructure

• Delivery, Storage

and Compression on exterior

• Dispensing

• Performed by operators in

convenient location (part of

work flow)

• Three step process < 3 minutes • Data collection cable

• De-watering hose

• Hydrogen nozzle

• Multiple locations if needed • Opportunity filling

• Eliminates drive time and queuing

• Mobile Hydrogen Solution for

Demonstration

9

Applications and Markets

Market Opportunity*

• Full suite of GenDrive fuel cell products to meet

material handling customer needs

• SAM Address 40% of today’s TAM*

• Address greenfield/brownfield sites in the markets:

• Retail and Food Distribution

• Manufacturing

• Potential for market expansion into Asia

*SAM: Serviceable Addressable Market

TAM: Total Available Market

Segment Experience Hydrogen Solutions Market Size

QTY*

Market Size

USD**

North

America Large

6 Years

(1 Year onsite

generation)

• Delivery with on-site liquefied storage

• Large on-site generation w/ gaseous

storage

15% (~180 K)

$ 4.2 Billion Medium

6 Years

(1 Year onsite

generation)

• Delivery with on-site liquefied or

gaseous storage

• Small on-site generation w/ gaseous

storage

25% (~300 K)

Small 1-3 Years

• Delivery with gaseous storage

• Small on-site generation w/gaseous

storage

20% (~240 K)

Retail Under development • Under development 40% (~480 K)

Europe All 1 Year • AL advanced hydrogen fueling stations ~1,700 K $5.7 Billion

Japan &

China All N/A • Under review N / A $7.8 Billion

ROW All N/A • Under review N / A $2.1 Billion

10

Expanding the Opportunity in the

$20B Material Handling Industry

* Sources: Analysis of Industrial Truck Association data, JVIA, and ongoing management discussions with OEM’s

North American shipments have been isolated to 40% of the total fork truck population

Low-cost Hydrogen Infrastructure is Crucial to Expansion

11 11 11

• 44 total site deployments with 24

different customers

• 29 brownfield sites

• 15 greenfield sites

• More than 5,000 units shipped

• >8,000 fills per day by customer

• More than 5,000 kg of H2 dispensed

per day

NA Customer Base Continues to Grow

European Customer Traction Growing

High Throughput

Distribution Centers

Consumer & Retail

Distribution Centers

Manufacturing

Facilities

Future Market Expansion

• Targeting adjacent markets that have the same

dynamics as materials handling

• Ground Support Equipment – 60,000 units deployed

• Big Rig Transportation Refrigeration Units – 290,000

units deployed

• Range extenders for heavy-duty electric vehicles

• President Obama target: 1M electric vehicles by 2015

• Significant development funds provided by external

agencies

• DOE: grant for Bridge Terminal Transport tuggers

(BTT)

• $2.5 Million

• NYSERDA: $500,000 for TRUs

• DOE RFP: planned application for range extenders

13

Charlatte BTT

Heavy Duty Electric Car

Transportation Refrigeration Unit

Summary

14

• Plug Power is the premier system integrator

for PEM fuel cells

• Materials handling first mover advantage – 90% market share;

HyPulsion JV gives us same advantage in Europe

• Air Liquide now a key strategic investor and joined board of

directors

• Compelling customer experience with Fortune 500 client list –

4,000 units to 24 firms

• Growing opportunities in adjacent markets with outside entities

committing development funds

• Momentum in lower-cost Hydrogen solutions is rapidly

expanding our opportunities

• Material handling success is the first step to

our goal of profitably displacing diesel engines

and batteries with fuel cells in a wide array of

applications

15 15