full year 2016 results - schneider electric · pdf filefull year 2016 performance highlights4...

TRANSCRIPT

February 16, 2017

Full Year 2016 Results

All forward-looking statements are Schneider Electric management’s present expectations of future events and are subject to a number of factors and

uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. For a detailed description of

these factors and uncertainties, please refer to the section “Risk Factors” in our Annual Registration Document (which is ava ilable on www.schneider-

electric.com). Schneider Electric undertakes no obligation to publicly update or revise any of these forward-looking statements.

This presentation includes information pertaining to our markets and our competitive positions therein. Such information is based on market data and

our actual revenues in those markets for the relevant periods. We obtained this market information from various third party sources (industry

publications, surveys and forecasts) and our own internal estimates. We have not independently verified these third party sources and cannot

guarantee their accuracy or completeness and our internal surveys and estimates have not been verified by independent experts or other independent

sources.

Page 2 Schneider Electric – Investor Relations

Disclaimer

30 Full year 2017 targets

32 Appendices

Page 3 Schneider Electric – Investor Relations

Full year 2016 performance highlights 4

Full year 2016 finance presentation 22

Full year 2016 performance highlights

Page 4 Schneider Electric – Investor Relations

Page 5 Schneider Electric – Investor Relations

•We successfully delivered on our roadmap in 2016

• Adj. EBITA c.+90 bps before FX, exceeding initial target and top-end of revised target

• All time high FCF of €2.2bn

•We focus on creating shareholder value:

•TSR c.48% in last 12 months.

•€2.04 dividend proposed, up +2%

•Company well positioned for profitable growth:

• Major geographies set to improve though geo-political uncertainty remains

• Strategy to focus on products, services and better systems fully delivering

•Ramping up EcoStruxure, our Digital architecture, across major markets

•Consistent & solid execution of “Schneider is On.” Margin improvement underway with focus on

organizational simplification, consistent execution and potential portfolio pruning

Solid execution of Schneider is On: Strong improvement in Adjusted EBITA

margin, all time high Free Cash Flow and Net Income up +24%

Page 6

28% North

America

18% Rest of

the World

27% Western

Europe

27% Asia-

Pacific

Four integrated and synergetic businesses – FY 2016 revenues

43% 15% 22% 20%

Building Industry IT Infrastructure

Balanced geographies – FY 2016 revenues

€24.7 billion FY 2016 revenues

44% of FY revenues as

Solutions

5% of FY revenues

devoted to R&D

41% of FY revenues in

new economies

Schneider Electric 2016 highlights

Schneider Electric – Investor Relations

Page 7 Schneider Electric – Investor Relations

● 100% of new large customer projects with

CO2 impact quantification

● All our entities pass our internal Ethics &

Responsibility assessment 93.4%

16%

● 10% energy savings

● 100% of products in R&D designed with

Schneider ecoDesign WayTM

7.1%

81.6%

● One day training for every employee

every year

● 85% of employees work in countries with

Schneider gender pay equity plan

92%

75%

In 2016, Schneider Electric was awarded by:

See detailed results in appendix

79%

-

5.9%

46%

83%

57%

Q4 2016 Q3 2016 Indicators & objectives 2017 - selection

This quarter, our Planet & Society barometer reaches 8.48/10

Fortune Magazine: #24 / 50 Companies that are changing the world

DJSI Industry Leader

for the 4th consecutive year

CDP Climate Leader

part of the “Climate A list” for the 6th consecutive year

Ethisphere, world's most ethical companies

listed for the 6th consecutive year

FTSE4Good: listed for the 1st time since inception in 2001

4th company globally for clean-energy in Carbon Clean 200 List

12th most sustainable company in the world in Global 100 most

sustainable corporations

10th greenest company in the world in Newsweek Global Green

Ranking

Vigeo Eiris Industry Leader

Oekom Industry Leader

Page 7 Schneider Electric – Investor Relations

• Growth in Products, Software

& Services

• Better project and equipment

selection and execution

• c.+1% organic growth ex-systems1 & transformers

• Services up +5% organic

• Systems1 gross margin up ~+40bps (~+70bps before FX)

• Global strategic accounts orders up mid-teens

PROGRESS UPDATE IN 2016

• Growth by innovation

• EcoStruxure: building, power, grid, industry, machines, datacenters

• Software & Analytics: StruxureOn, Wonderware online

• Connected products: Masterpact MTZ, Altivar Process & Others

DO MORE

INNOVATE

• Target cost reduction of c.

€1.7-1.8bn by 2017

• c. €620m cost reduction2 in 2016, c.€1.3bn in past 2 years SIMPLIFY

1: Systems is comprised of Projects & Equipment

2: Gross support function cost reduction plus industrial productivity

• Develop connected offer

• Digitize customer experience

• Number of connected assets +15%

• Connected Customers +40% DIGITIZE

SCHNEIDER IS ON INITIATIVES

Page 8 Schneider Electric – Investor Relations

Focus on strategic priorities yielded strong results in 2016; Well positioned for

further organic sales growth and margin improvement

Page 9 Schneider Electric – Investor Relations

FINANCIAL OBJECTIVES

About flat organic growth ex-impact of

selectivity in 2016 •Slightly positive organic growth excl. selectivity1

2016 RESULTS

Expand Adj. EBITA margin +60bps to

+90bps before FX (initial target +20-60bps)

c.100% FCF conversion of Net income

through an economic cycle

Portfolio pruning

c. €1.5bn share buyback by 2016

•Adj. EBITA margin of 14.1%, up c.+90bps before FX

•All time high FCF of €2.2bn, 118% FCF conversion

•Completed disposal of Telvent Transportation, launched

strategic review of DTN

•€1.5bn share buyback executed in 2015/2016 at ~€57

per share

1: Excluding the impact of selectivity for c.€280-300m

All financial targets achieved in 2016

FY 2016 ORGANIC GROWTH, %

Group: -0.9% org,

Slightly positive underlying1

Page 10 Schneider Electric – Investor Relations

IT

-0.8

Infrastructure

-3.4

~0.3

Industry

-1.2

Building

0.3

Excl.

selectivity

ORGANIC GROWTH, %

~-0.5 -0.1

Q4 2016

~+1.6

~+0.9

H2 2016

-1.7 -1.7

H1 2016

Group underlying Organic Growth (%)

Group Organic Growth (%)

1: Estimated FY underlying organic growth excluding the impact of selectivity for c.€280-300m (neutral working day impact)

2: Estimated Q4 underlying organic growth excluding impact of c.-€150-€160m from selectivity and -1.1pt working day

Slightly positive underlying1 organic growth in 2016 with c.+1.6% underlying2

growth in Q4

Page 11 Schneider Electric – Investor Relations

Group

-0.9

Services

5.0

Services Growth across all the

businesses

MORE SERVICES

& SOFTWARE

Organic growth (%)

MORE PRODUCTS

THROUGH PARTNERS

BETTER SYSTEMS

Low-single digit organic

growth in products sold

through partners

Mid-single digit organic

growth in Wiring Devices &

Final Distribution

Revenues

outperforming Group

by c.+1.5pts organic

OEM Solution

Datacenters

Building

Automation

Grid

Automation

Software down low-single digit driven

by process industries & transition of

some offers to SaaS

Grow specialized business

Systems gross

margin improved

(~+0.7pt before FX)

Improve margins

Our strategic priorities achieved good results in a mixed market

Page 12 Schneider Electric – Investor Relations

Organic growth

+0.3% Adj. EBITA margin

19.6%/ +1.6pt

Performance in 2016

€10.7bn 43% of Group 2016 revenues

Low Voltage & Building Automation

#1

worldwide

Performance highlights

• 2 largest countries (U.S., China) both delivered growth,

Western Europe about flat

• New economies grew with India and CIS up strongly, Middle-

East declined

• Final Distribution & Wiring Devices grew mid-single digit

• Project business still impacted by soft activity in some markets

• Margin expansion of c.+1.5pts organic, mainly driven by

industrial productivity & cost control

Execution priorities

• Maximize all businesses sales through partners

• Continue to drive Wiring Devices/ Final Distribution

• Grow new connected offers EcoStruxure for Building & Power

• Keep growing analytics and digital services

• Attention to cost and pricing

Building delivers growth and a c.+1.5pt organic margin improvement

Page 13 Schneider Electric – Investor Relations

Organic growth

-0.8%

Adj. EBITA margin

16.8%/ -0.8pt

Performance in 2016

€3.6bn 15% of Group 2016 revenues

Critical Power, Cooling & Services

#1

worldwide

Performance highlights

• 2 largest markets (U.S. and India) grew

• Weakness in Western Europe, Middle-East & Africa

• Services performed strongly

• Margin declined by c. -0.5pt organic impacted by mix and

investments in digital and services capabilities

Execution priorities

• Leverage the Group’s complete portfolio for datacenters

• Grow EcoStruxure for Datacenter offer with 2016 launch of

cloud based Software

• Drive product business through channel expansion and new

offers

• Keep services growth momentum

• Continued focus on cost discipline

IT grew in large markets but suffered from weakness in EMEA. Margin

decreased but remains resilient at high level

Page 14 Schneider Electric – Investor Relations

Organic growth

-3.4%/ c.+0.3%1

Adj. EBITA margin

9.7%/ +0.6pt

Performance in 2016

€4.9bn 20% of Group 2016 revenues

Medium voltage & grid automation

#1

worldwide

Performance highlights

• Margin improved c.+1.3pt organic thanks to higher system

margin and strong cost control but was below 2016 target

of 10% due to strong negative FX (c. -0.9pt)

• Org. growth up slightly (+0.3%) excl. the impact of project

selectivity

• Services grew mid-single digit

• EcoStruxure Grid grew double-digit organically

Execution priorities

• Grow products, services and EcoStruxure Grid

• Continue project selectivity and better execution

• Further adjust cost-base and optimize industrial footprint

• Reach 10% to mid-teen adj. EBITA margin level

1: excluding c. €190m of selectivity in 2016

Infrastructure improves margin by c.+1.3pt organic in difficult markets

Page 15 Schneider Electric – Investor Relations

Organic growth

-1.2% Adj. EBITA margin

16.7%/ -0.4pt

Performance in 2016

€5.5bn 22% of Group 2016 revenues

#2

Worldwide

Discrete #4

Worldwide

Process

Performance highlights

FY org. growth impacted by weak O&G, China and U.S.

Growth in Western Europe and New economies ex-China

Positive performance in Q4 with improvement in OEM notably

China (up mid-single digit) and for Process Automation orders

Margin c.-0.2pt organic mainly driven by lower volumes

OEM business up thanks to innovation & channel initiatives

Execution priorities

Grow business through partners & integrators

Continue to develop OEM solutions

Develop EcoStruxure for Plant & Machines

Continue developing Software packages by segments

Continuous control of SFC

Industry delivers a resilient performance in a mixed environment, with positive

momentum in Q4

Page 16 Schneider Electric – Investor Relations

GROUP ACHIEVEMENTS IN 2016

IMPROVE EXECUTION

• Deeper screening of projects through experienced

solution committees and tighter processes and hurdles

• Focus on repetitive segments.

• Impact: ~20% projects above 5m€ refused at tendering

phase in 2016

• Rationalization of project and equipment footprint and up-

skilling of teams

• Systematic proactive risk assessment, mitigation plan

definition

Hit rate improved significantly

(>10pts)

Systems gross margin improved

(+0.4pt, ~0.7pt before FX)

INCREASE SELECTIVITY

GROUP: ACTIONS LAUNCHED

Increased cash generation

Good progress in improving project management and margin

Page 17 Schneider Electric – Investor Relations

Target ’15-’17

(Investor Day)

1.7-1.8

1.0

0.7-0.8

2015-2016

Achieved

1.3

0.7

0.5

2016

0.6

0.4

0.2

SFC Gross savings

Industrial productivity

KEY ACTIONS IN 2016

Industrial productivity (c. €380m)

• Ranked #18 Top Global Supply Chain

• Purchasing efficiency

• Quality value engineering

• Transport: improved container loading factor

SFC Savings (c.€240m Gross savings)

• Non-manufacturing headcount down -4% organically in 2016

• Marketing & Finance simplification

• Regional setup simplification

Reinvestments (c.€60m)

• R&D for EcoStruxure development

• Digital and mobile tools

• Services & marketing capabilities

TOTAL SAVINGS (€bn)

We continue to simplify our operations for greater efficiency

Page 18 Schneider Electric – Investor Relations

Deployment of EcoStruxure.io

Connected Products

Edge Control

Apps, Analytics & Services

En

d to

En

d

Cyb

ers

ecu

rity

Clo

ud

an

d/o

r O

n

Pre

mis

e

Grid Building Data Center Industry

GRID DATA CENTER PLANT

MACHINE BUILDING POWER

EcoStruxure Platform

Asset Performance

Management as a Service

Page 19

Apps &

Analytics,

Services

Edge

Control

Connected

Products

Buildings Industrial & machines Utilities & infrastructure Data Centers & Networks

StruxureWare Building Operations

allows data collection, analysis,

and management

Smart Building Service Plans

State of the art service plans

Altivar 340

Variable speed drive with

superior performance

and productivity

PACis 5.4

Digital Control System

Modicon M580 is the first PAC*

with built-in Cybersecure

Ethernet capabilities

Wonderware Online,

leading cloud based offering turning data into action

StruxureOn™ increases data

center resiliency

Data Center Operation 8.0

Allow monitoring & Operation

of DC’s incl. Multi-tenant

*Programmable Automation Controller

Galaxy VX™

3-phase power protection

Numerous key launches in 2016 supporting EcoStruxure deployment

Building Industry Data Center Grid

Easergy T300

Remote Terminal Unit

Schneider Electric – Investor Relations

Masterpact MTZ performance and reliability with

new digital capabilities

Page 20

Wiser Air Solution

• Complete home energy

management solution

PowerTag meter

• Smallest power and

energy meter in the

world

FUGA

• One of the most

successful launches of

wiring device ranges

Resi 9

distribution board

• Transforms homes into

vibrant, stylish living spaces

Smartlink ELEC solution

• Simple intuitive monitoring

of the status of devices and alerts

Mureva Styl

• Complete

waterproof system

Bond

switch range

• Designed to be stylish,

practical and set the mark

in terms of functionality and modularity

AvatarOn wiring

devices range

• Allows switch customization

Clipsal / PDL Iconic

• The new standard in residential

electrical accessories

… with continued focus on home and small buildings

Schneider Electric – Investor Relations

Page 21 Schneider Electric – Investor Relations

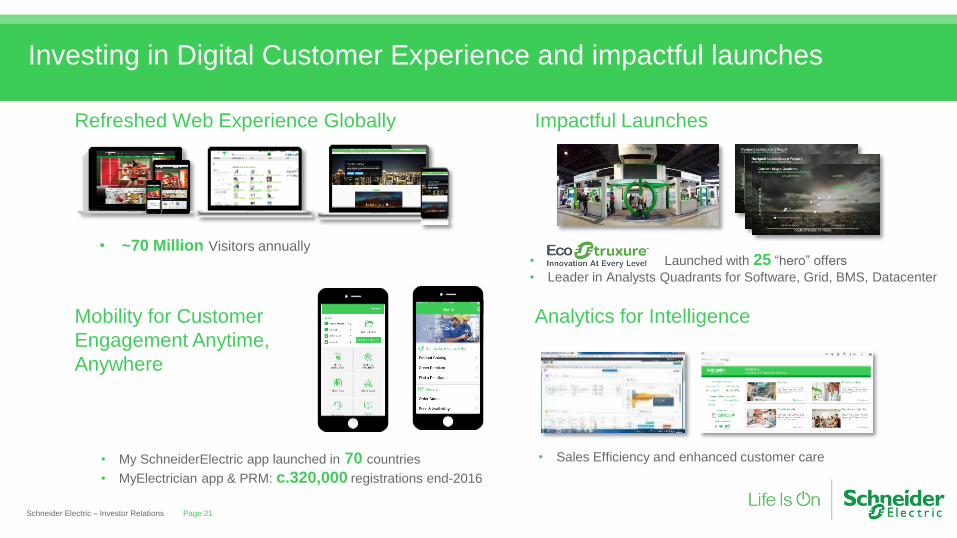

Refreshed Web Experience Globally Impactful Launches

Mobility for Customer

Engagement Anytime,

Anywhere

Analytics for Intelligence

• ~70 Million Visitors annually • Launched with 25 “hero” offers

• Leader in Analysts Quadrants for Software, Grid, BMS, Datacenter

• My SchneiderElectric app launched in 70 countries

• MyElectrician app & PRM: c.320,000 registrations end-2016

Investing in Digital Customer Experience and impactful launches

• Sales Efficiency and enhanced customer care

Full year 2016 finance presentation

Page 22 Confidential Property of Schneider Electric |

ANALYSIS OF CHANGE IN GROUP REVENUES (in €m)

• Based on current rates, the FX impact on FY 2017 revenues is estimated to be around +€400m. The FX impact at

current rates is expected to be about neutral on margin

2016

24,693 -7.3%

Fx

-2.5%

Scope

-3.9%

Rest of World

-3%

North America

-1%

Asia-Pacific

-1%

Western Europe

+0%

2015

26,640

Group: -0.9% org,

slightly positive underlying growth1

Page 23 Schneider Electric – Investor Relations

1: Excluding the impact of selectivity for c.€280-300m

Mainly Delixi

deconsolidation, Juno

& Telvent transport.

disposals

Primarily due to weaker

CNY, GBP and other

new economies

currencies vs €

Slightly positive underlying organic growth. Scope and FX main driver for

revenue decline

GROSS MARGIN: ANALYSIS OF CHANGE (%)

38.0

Scope &

Others

Productivity

-0.2

Mix

-0.4

R&D & Prod.

Labor infl.

-0.5

FX

0.1

1.5

Net price

0.5

Volume

0.0

2015 GM

37.0

2016 GM

• Improving trends

vs. 2015 thanks to

selectivity initiatives

on systems R&D increase

impacted c. -0.1pt

• Price positive outside China. In China,

despite price investments, strong

industrial productivity and cost efficiency

protected the margin

• Given the resurgence of raw material

inflation, the Group expects a negative

raw material impact in 2017 of c. - €200

million at current prices

Page 24 Schneider Electric – Investor Relations

Divestments & Delixi

deconsolidation

c.+0.4pt

Strong productivity, net price and improving mix trend drove a strong gross

margin improvement

In €m FY 2015 FY 2016 Organic change

Revenues 26,640 24,693

Gross Profit 9,845 9,390 +1%

Gross margin (%) 37.0% 38.0% +1pt

Support function costs (6,204) (5,910)

SFC1 ratio (% Revenues) 23.3% 23.9%

Adjusted EBITA 3,641 3,480 +4%

Margin % 13.7% 14.1% +70 bps

• Gross profit improved organically

through strong productivity & system margin improvement

Page 25 Schneider Electric – Investor Relations

1: Support function cost

• SFC organic reduction of -0.5%

thanks to c.€240m gross SFC savings

• Main driver for higher SFC ratio is

linked to divestments & Delixi deconsolidation (c.+40 bps impact)

Adj. EBITA margin improves c.+90 bps before FX, +70 bps organic thanks to

strong gross margin improvement

In €m FY2015 FY2016 % change

Adjusted EBITA 3,641 3,480 -4%

Other income and expenses (522) (63)

Restructuring (318) (313)

Amortization & depr. of purchase accounting intangibles (572) (153)

EBIT 2,229 2,951 +32%

Financial costs (446) (462)

Income tax (389) (712)

Equity investment & Minorities 13 (27)

Net income (Group share) 1,407 1,750 +24%

Adjusted Net income1 2,119 2,117

Adjusted Earning per share1 3.73 3.77 +1%

Page 26 Schneider Electric – Investor Relations

• Restructuring costs expected to be c. €900m in 2015-2017 to drive

efficiency initiatives.

• Includes exceptional3 -€119m. Without exceptional, ETR of 23.8%. • Effective tax rate expected in 2017: 26%-28%, not factoring potential US

tax changes at this stage

• €23m decrease in Net cost of financing but increased exchange losses due to currency volatility

1. Adjusted Net Income and EPS calculation in appendix

2. Growth of c.+2% at 31 December spot share count

• Growth of c.+2% at 31 December spot share count

EBIT and Net income increased by +32% and +24% on reported basis and

adjusted EPS1 up c.+2%2

3. Linked to the negative adjustment of net deferred tax assets

• Strong control over inventories

Analysis of debt change in €m FY2015 FY2016

Net debt at opening Dec 31 (5,022) (4,631)

Operating cash flow 2,715 2,942

Capital expenditure – net (787) (764)

Change in trade working capital 91 82

Change in non-trade working capital 26 (54)

Free cash flow 2,045 2,206

Dividends (1,219) (1,227)

Acquisitions – net 1 322 47

Net capital increase (448) (689)

FX & other (309) (531)

(Increase) / Decrease in net debt 391 (194)

Net debt Dec 31 (4,631) (4,824)

Page 27 Schneider Electric – Investor Relations

• Includes €853m share

buyback

1: including dividend from CST holding in 2015

> 90% FCF

RETURNED TO

SHAREHOLDERS

OVER PAST 2

YEARS

Record Free cash flow, up +8% thanks to improving operating cash flow and

good working capital management

• Mainly due to FX impact

Page 28 Schneider Electric – Investor Relations

109

2016

1183

2015

1132

2014

961

2016

1.1

2015

1.0

2014

1.2

CASH CONVERSION, % NET DEBT/ ADJ. EBITDA

1: Based on Net income adjusted for discontinued ops

2: Based on Net income adjusted for business disposals impact and Pelco impairment (see p25)

3: Based on Net income adjusted for non-cash c.€120m income tax increase due to deferred tax assets adjustment

Strong cash conversion and solid balance sheet

1: Based on share price prior to dividend payment, or Feb.15th 2017 for 2016 dividend

2: Subject to shareholder approval in AGM

DIVIDEND HISTORY

0

1

2

3

4

52.5

2.0

1.5

1.0

0.5

1.70

2010

1.60

2009

1.03

20162

2.04

2015

2.00

2014

1.92

2013

1.87

2012

1.87

2011

Dividend (€ per share)

Dividend Yield (%) 1

Page 29 Schneider Electric – Investor Relations

Proposed dividend of €2.04 per share, increased by +2%

Full Year 2017 Targets

Page 30 Schneider Electric – Investor Relations

Page 31 Schneider Electric – Investor Relations

In 2017 the Group expects more positive momentum in its major end-markets. In North America, modest growth is

anticipated with improvement in industrial activity and continued growth in residential markets. Western Europe is

expected to grow moderately, benefiting from an environment with a lower Euro and still relatively low oil price, while

some Brexit-related risks remain. China is expected to improve in Industry and Infrastructure markets while the

construction market should grow at a slower pace due to policy tightening. The Group will still face headwinds from O&G

and continued weakness in some resource driven economies, although these may ease towards the end of the year.

Additionally, in 2017 the Group will face a strong increase in raw material costs estimated at c.-€200m at current prices.

In this environment, the Group’s priorities are to grow its partner network through the launch of many new integrated

offers, accelerate services and software, working on margin improvement through continued selectivity on projects and

keep a strong attention on cost control. In addition, the Group should benefit from the recent deployment of its

EcoStruxure architectures in several domains to create further opportunities for growth.

Therefore, in line with the objectives announced at the 2016 Investor day, the Group targets for 2017:

> Organic revenue growth between +1% and +3% for the Group outside Infrastructure. For Infrastructure the priority

remains margin improvement and the organic growth target for the division is to be about flat underlying, before an

expected -4% to -5% impact from project selectivity for the division in 2017.

> +20bps to +50bps organic improvement on adjusted EBITA margin. The FX impact at current rates is expected to be

about neutral on margin

DRAFT 2017 Targets

Appendixes

Page 32 Schneider Electric – Investor Relations

Definitions

Page 33 Schneider Electric – Investor Relations

● EBITA: EBIT before amortization and impairment of purchase accounting

intangibles and impairment of goodwill

● Adjusted EBITA: EBITA before restructuring and other operating income and expenses

● EBITDA: EBIT before depreciation, amortization, provisions and before share-

based compensation cost

● Adjusted EBITDA: Adjusted EBITA before depreciation, provisions and before share-based

compensation cost

● Cash conversion: Free cash flow / Net income (Group share)

● Free cash flow: Operating cash flow less change in working capital less net capital

expenditures

● ROCE: Return On Capital Employed

Page 34 Schneider Electric – Investor Relations

2016 key messages: •The Planet & Society barometer reaches 8.48/10, outpacing year-end target 2016 (7.5/10).

•More than 20 million people benefited from our Access to Energy offers. Launch of Homaya, a solar home system for off-grid

households: complete solution comprises solar panels, in-built battery and 3-4 lamps;

•Commitment highly recognized by worldwide sustainability raters: DJSI (Industry Leader), CDP (in Climate A list), Global 100

(27th), Ethisphere, Vigeo Eiris (Industry Leader), Oekom (Industry Leader) and more

•Schneider Electric at COP22 Marrakech, mobilization for access to energy in Africa with Homaya, Schneider Electric

Foundation’s partnership with Art of Change 21, conferences & side events at Riad Yima.

•Company signed the Science-based targets initiative to support carbon neutrality commitment in own value chain &

ecosystem. Program launched to quantify CO2 impact and savings of large customer projects.

•Successful first “integrated report” released in 2016.

Main trends 2017: • Company engaged to accomplish the 17 SDGs (UN Sustainable Development Goals)

• Towards first carbon neutral marathon (Marathon de Paris 70% carbon neutral in 2017 – 100% in 2018)

• Human rights policy and program in accordance with the UN Guiding Principles on Business & Human Rights

Sustainability key messages 2016 and trends 2017

The arrow shows if the indicator has risen, stayed the same or fallen compared to the previous quarter. The colour shows if the indicator is above or below the objective of 8/10. 1 2 Change in scope of consolidation in Q4 2016

10% energy savings

10% CO2 savings from transportation

Towards zero waste to landfill for 100 industrial sites

100% of products in R&D designed with Schneider ecoDesign WayTM

30% reduction in the Medical Incident Rate (MIR)

One day training for every employee every year

64% scored in our Employee Engagement Index

85% of employees work in countries with Schneider gender pay equity plan

150,000 underprivileged people trained in energy management

1,300 missions within Schneider Electric Teachers NGO

75% of product revenue with Green PremiumTM eco-label

100% of new large customer projects with CO2 impact quantification

120,000 tons of CO2 avoided through maintenance, retrofit and end-of-life services

x5 turnover of Access to Energy program to promote development

100% of our recommended suppliers embrace ISO 26000 guidelines

All our entities pass our internal Ethics & Responsibility assessment

-

-

34

-

10%

10%

100

100%

60.5%

-

-

-

48%

-

75%

100%

120,000

x5

100%

100%

30%

85%

64%

85%

150,000

1,300

-

79%

61%

-

73,339

460

5.9%

8.5%

91

46%

66.3%

-

83,485

x3.3

72%

79%

37%

83%

63%

57%

119,140

1,203

7.1%

11.2%

99

81.6%

74.8%

16%

101,508

x2.11

82.3%

93.4%

33%

92%

64%

75%

123,839

1,0652

Planet & Society barometer

Overall score (out of 10)

Start

01/2015

3.00

Target

12/2017

8/10

Results

Q4 2016

8.48

Results

Q3 2016

7.65 Our megatrends 2015-2020 and our targets 2015-2017

The Planet & Society barometer 2015-2017 - Results as of Q4 2016

Adj. EBITA up +4% organic thanks to positive net price and

strong productivity

Page 36 Schneider Electric – Investor Relations

Analysis of change of adjusted EBITA (in €m)

377

102 3,480

Currency

effects

-199

Net

acquisition

impact

-117

Other

-82

SFC COGS

(Inflation

& R&D)

28 -107

Productivity Net price1 Mix

-50

Volume

-113

FY 2015

3,641

FY 2016

1: Of which RMI: c.€130m

ROCE calculation

2016

P&L items Reported

EBITA (1) 3,104

Restructuring costs (2) -313

Other operating income & expenses (3) -63

= Adjusted EBITA (4) = (1)-(2)-(3) 3,480

x Effective tax rate of the period1 (5) 23.8%

= After-tax Adjusted EBITA (A) = (4) x (1-(5)) 2,650

2015 2016 2016

Balance sheet items reported reported Avg of 4

quarters

Shareholders' equity 21,289 20,653 (B) 20,256

Net financial debt 4,631 4,825 (C) 5,253

Adjustment for Associates and Financial assets (fair value) -492 -762 (D) -756- Sunten Electric Equipment (25% stake) 98 52 80

- Fuji Electric FA Components & Systems (36.8% stake) 108 115 120

- NVC Lighting (8.9% stake) 33 35 30

- Delixi (50% stake) 279 273

- CST Holding (30% stake) 93 77 87

- Other non-current financial investments 159 204 166

= Capital Employed 25,428 24,716 (E) = (B)+(C)+(D) 24,753

= ROCE (A) / (E) 10.7%

1. Effective Tax rate corrected for the adjustment of the net deferred tax assets in France

ROCE calculation

Page 37 Schneider Electric – Investor Relations

1: Effective Tax rate corrected for the adjustment of the net deferred tax assets in France

• ROCE would be c.+90bps higher

excluding FX impacts since

2014

Adjusted net income calculation

In €m FY2015 FY2016

Net income (group share) 1,407 1,750

Invensys integration cost post-tax1 57

Impact of business disposals (in OOIE, share of profit

on associates & discontinued ops) 226 10

Impairment on Pelco net of tax 180

Restructuring charges post-tax1 249 238

Tax rate: deferred tax net assets depreciation2 119

Adjusted Net income 2,119 2,117

Adjusted EPS (€) 3.73 3.77

Page 38 Schneider Electric – Investor Relations

1: Calculated post-tax at the year effective tax rate (ETR).

2: see Press release from 9 January 2017

Q4 Performance

Page 39 Schneider Electric – Investor Relations

Q4 revenues underlying organic growth up c.+1.6% with

Industry turning positive in Q4

Page 40 Schneider Electric – Investor Relations

Analysis of change in Group revenues (€m)

Q4 2016

6,783 -5.8%

Fx

-1.0%

Scope

-3.1%

IT

+0.3%

Infrastructure

-6.7%

Industry

+1.4%

Building

-1.2%

Q4 2015

7,198

Organic Growth: -1.7%

c.+1.6% underlying growth1

1: Estimated underlying growth excluding Q4 impact of c.-€150-€160m from selectivity and -1.1pt working day

Building grew in Asia-Pacific but declined in North America and

Rest of the World

Page 41 Schneider Electric – Investor Relations

3,112

Q4 2016

2,848 -8.5%

Fx

-1.2%

Scope

-6.1%

Organic

-1.2%

Q4 2015

Analysis of change in Q4 Revenues (€m) North America declined, as the U.S. suffered from lower

project activity in commercial & industrial buildings mainly

due to selectivity and a high base of comparison in solar

markets. Residential activity continued to show good

growth in a favorable market. Mexico grew while Canada

was about flat.

Western Europe was stable. France posted solid growth

thanks to good project execution and an improving

residential market. Italy, Spain and the U.K. grew benefiting

from commercial initiatives while Germany declined.

Asia-Pacific was up slightly thanks to growth in India and

residential activity in Australia. India continued to grow,

avoiding substantial impacts from government

demonetization policies through actions with partners.

China was slightly negative due to some delays in projects

in favorable construction markets in Tier 1 & Tier 2 cities.

Rest of the World posted mixed results, with growth in CIS,

Africa and South America and a strong decline in the

Middle-East.

44% of Q4 revenues

Industry turned positive in Q4 thanks to OEM and improvement

in China

Page 42 Schneider Electric – Investor Relations

Q4 2016

1,477 +0.9%

Fx

-0.9%

Scope

+0.4% Organic

+1.4%

Q4 2015

1,464

Analysis of change in Q4 Revenues (€m) Globally, the Group benefited from its focus on OEM in a

favorable market. Process automation declined

organically, though showing early signs of improvement in

order intake.

China was up high-single digit in an improved OEM

market, driving the growth of Asia-Pacific. Elsewhere in

Asia, the Group continued to see growth in India and

weakness in Australia.

Western Europe declined slightly, with an impact from

working days. Positive OEM demand in Italy and Spain

could not fully offset a decline in France, and lower project

execution in U.K. and Germany.

The U.S. was down slightly as it continued to be impacted

by low O&G investment but posted growth in the OEM

market. The priority remains to enhance cross-selling

through channel initiatives.

Rest of the World was positive, led by strong growth in

Russia and Africa while South America and the Middle-

East declined.

22% of Q4 revenues

Infrastructure was slightly up before the impact of the project

selectivity which accelerated as expected in Q4

Page 43 Schneider Electric – Investor Relations

Q4 2016

1,466 -10.6%

Fx

-1.3%

Scope

-2.6%

Organic

-6.7%

Q4 2015

1,639

Analysis of change in Q4 Revenues (€m) Negative impact from selectivity initiatives accelerated to ~-

€100m in Q4, in line with expectations.

North America was down due to selectivity and continued

weakness in resource and industrial markets in the U.S. and

Canada.

Western Europe was down. Germany declined mainly due

to project selectivity despite continued growth in

transactional and services business. In France, the business

remained stable with strong growth in services thanks to

targeted initiatives which compensated for a planned

decrease in projects due to selectivity.

In Asia-Pacific, China was down slightly on selectivity and

weakness in traditional segments. Indonesia benefited from

project execution while Australia continued to suffer from

lower investment in resources.

Rest of the World was down with a mixed picture, notably

with weakness in the Middle-East but growth in Russia.

22% of Q4 revenues

~flat organic

growth before

selectivity

IT grew slightly in Q4, thanks to North America and Asia Pacific

Page 44 Schneider Electric – Investor Relations

Q4 2016

992 +0.9%

Fx

+0.6% Scope

+0.0%

Organic

0.3%

Q4 2015

983

Analysis of change in Q4 Revenues (€m) North America was up led by the U.S. with strong

growth in IT channel sales, continued success in

services initiatives and project execution in data

centers. Mexico declined.

Western Europe was down mainly due to declines in

Germany and the U.K. Italy, France, and Nordic

countries grew.

Asia-Pacific was up as India continued to grow

strongly with little impact seen from government

demonetization initiatives. Elsewhere in Asia, the

Group saw growth in South East Asia and Japan and

declines in China and Australia.

Rest of the World declined, mainly driven by Russia

and the Middle-East.

Services continued to grow strongly.

15% of Q4 revenues

Asia-Pacific grew slightly with China & India while rest of

regions declined

Page 45 Schneider Electric – Investor Relations

Analysis of change in Group revenues (€m)

Q4 2016

6,783 -5.8%

Fx

-1.0%

Scope

-3.1%

Rest of

World

-2%

North

America

-4%

Asia-

Pacific

0%

Western

Europe

-1%

Q4 2015

7,198

Organic: -1.7 %

Western

Europe

Asia

Pacific

North

America

Rest of

the World

27%

27%

27%

19%

Q4 revenues

Contacts & agenda

Page 46 Schneider Electric – Investor Relations

Alexis Denaud – Senior Investor Relations Manager Tel: +33-1-41-29-51-24

Apr 20, 2017

Apr 25, 2017

Q1 2017 Revenues

Annual General Meeting

Conference call

Meeting

Amit Bhalla– Head of Investor Relations

Tel: +44-20-7592-8216