full year results 2004 -...

TRANSCRIPT

Full Year Results 2004

25 November 2004

GrainCorp Full Year Presentation

Corporate Results

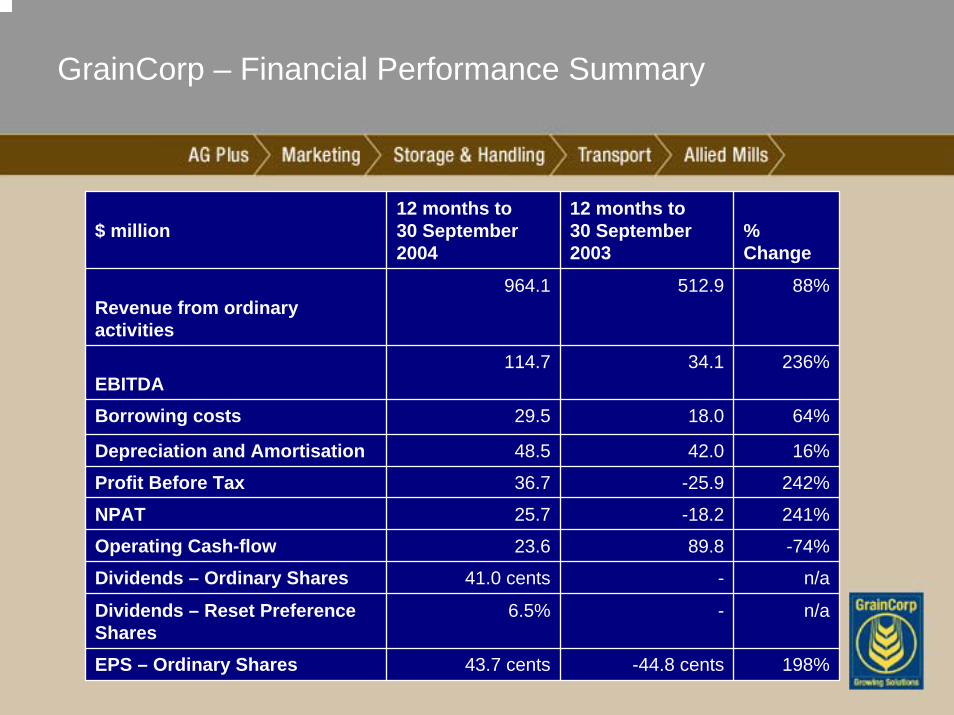

GrainCorp – Financial Performance Summary

$ million12 months to 30 September 2004

12 months to 30 September 2003

% Change

Revenue from ordinary activities

964.1 512.9 88%

EBITDA114.7 34.1 236%

Borrowing costs 29.5 18.0 64%

Depreciation and Amortisation 48.5 42.0 16%

Profit Before Tax 36.7 -25.9 242%

NPAT 25.7 -18.2 241%

Operating Cash-flow 23.6 89.8 -74%

Dividends – Ordinary Shares 41.0 cents - n/a

Dividends – Reset Preference Shares

6.5% - n/a

EPS – Ordinary Shares 43.7 cents -44.8 cents 198%

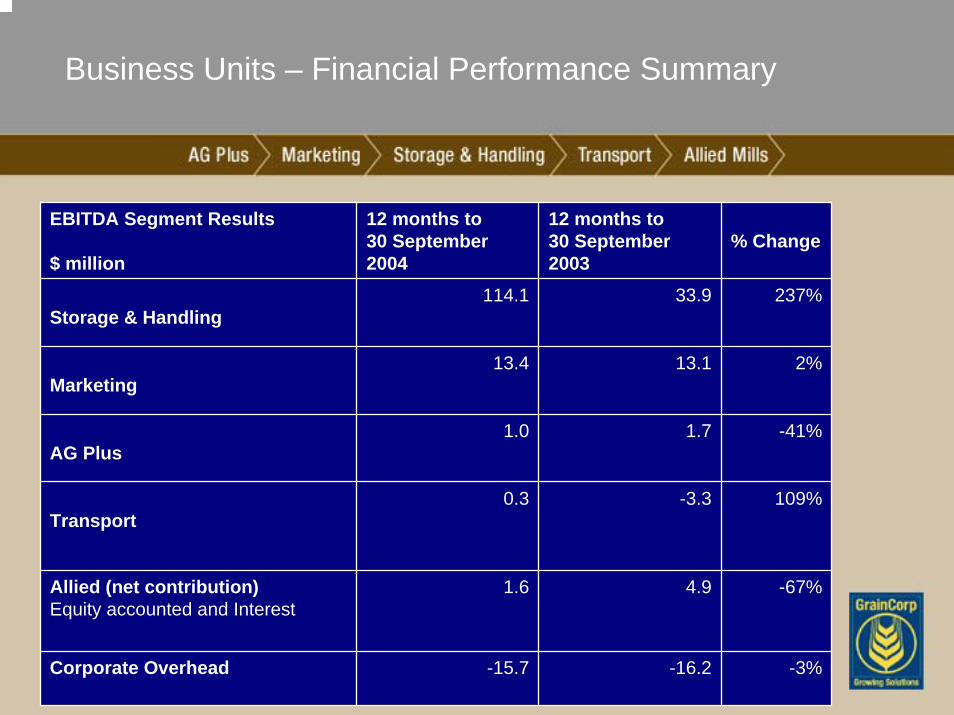

Business Units – Financial Performance Summary

EBITDA Segment Results

$ million

12 months to 30 September 2004

12 months to 30 September 2003

% Change

Storage & Handling114.1 33.9 237%

Marketing13.4 13.1 2%

AG Plus1.0 1.7 -41%

Transport0.3 -3.3 109%

Allied (net contribution) Equity accounted and Interest

1.6 4.9 -67%

Corporate Overhead -15.7 -16.2 -3%

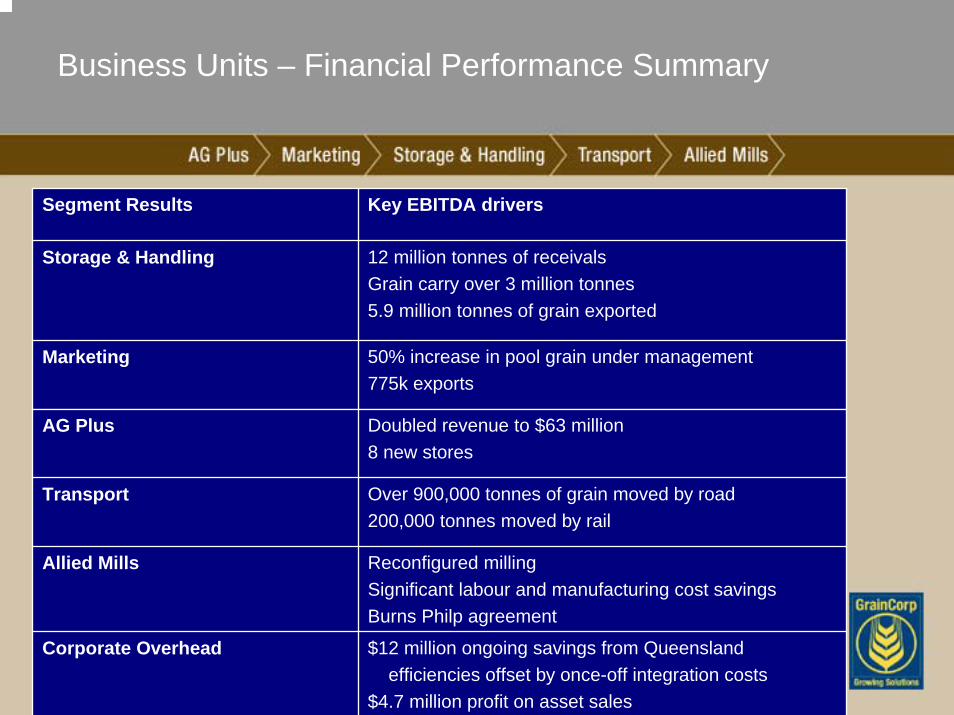

Business Units – Financial Performance Summary

Segment Results Key EBITDA drivers

Storage & Handling 12 million tonnes of receivalsGrain carry over 3 million tonnes 5.9 million tonnes of grain exported

Marketing 50% increase in pool grain under management775k exports

AG Plus Doubled revenue to $63 million8 new stores

Transport Over 900,000 tonnes of grain moved by road200,000 tonnes moved by rail

Allied Mills Reconfigured millingSignificant labour and manufacturing cost savings Burns Philp agreement

Corporate Overhead $12 million ongoing savings from Queenslandefficiencies offset by once-off integration costs

$4.7 million profit on asset sales

Debt to Equity Ratio

36%

66%

81%

95%

79%

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004

Debt/Equity Ratio

GrainCorp 5 year average 71% (FY)

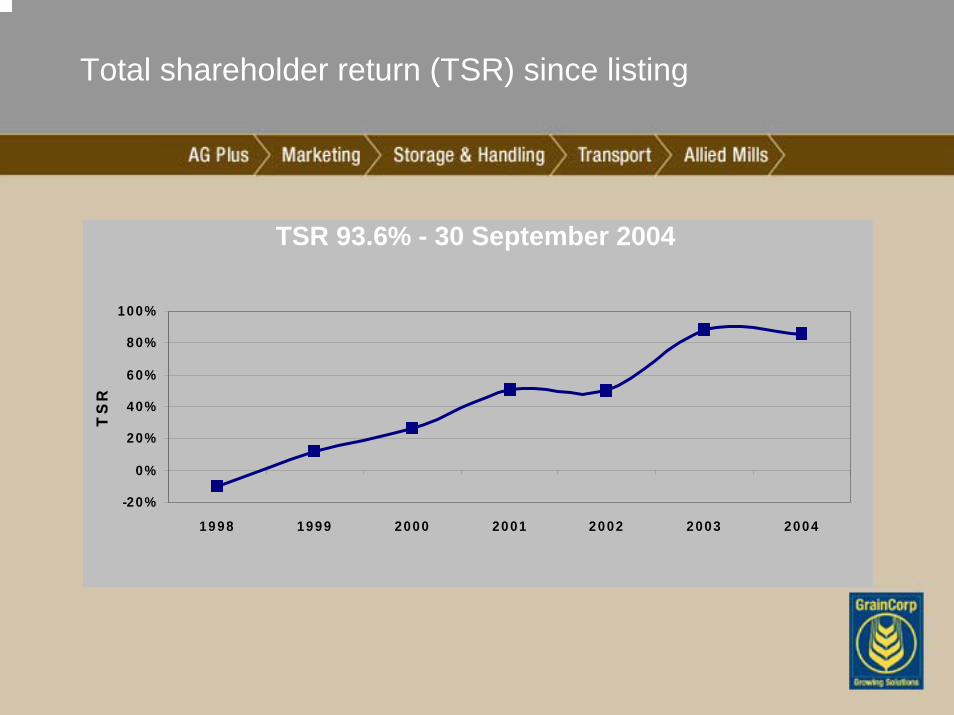

Total shareholder return (TSR) since listing

-20%

0%

20%

40%

60%

80%

100%

1998 1999 2000 2001 2002 2003 2004

TS

R

TSR 93.6% - 30 September 2004

Capital Management

Dividend Policy a minimum of 70% profit after tax – up from 65%

Dividend Re-investment Plan (DRP) – currently approved by shareholders and may be re-activated at the discretion of the Board

Ordinary Share buyback – on market currently operative

Multipurpose infrastructure

utilisation

Environment

Supply chain extension

Farm to primary processing

Cross ag sector consolidation: livestock, grain

etc, finance

Long term trend to domestic consumption:

-Livestock-processing

GrainCorp is well positioned to grow

earnings in this environment

Export market deregulation (non-

wheat)

Grain entity consolidation

continuesRail

consolidation

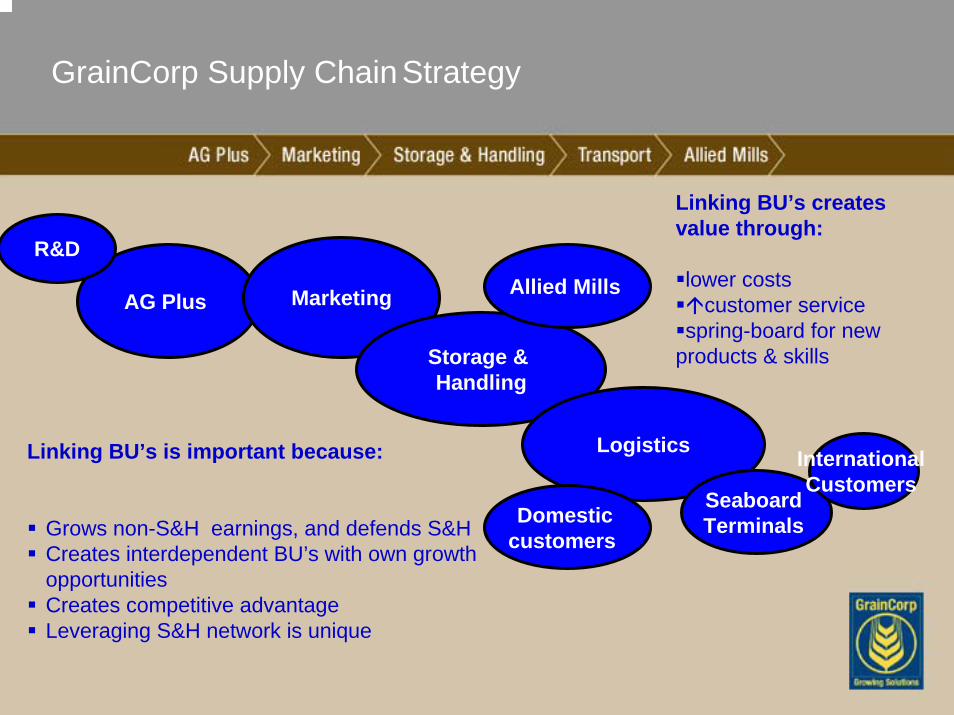

GrainCorp’s grain supply chain focus

Cost management Service capabilityIntegrated product offersRationale investment decisionsStrategic partners

AG Plus Marketing

Storage & Handling

GrainCorp Supply Chain Strategy

R&D

Allied Mills

Logistics

Seaboard Terminals

International Customers

Linking BU’s is important because:

Grows non-S&H earnings, and defends S&HCreates interdependent BU’s with own growth opportunitiesCreates competitive advantageLeveraging S&H network is unique

Linking BU’s creates value through:

lower costscustomer service

spring-board for new products & skills

Domestic customers

GrainCorp Full Year Presentation

Business OperationsStorage & Handling

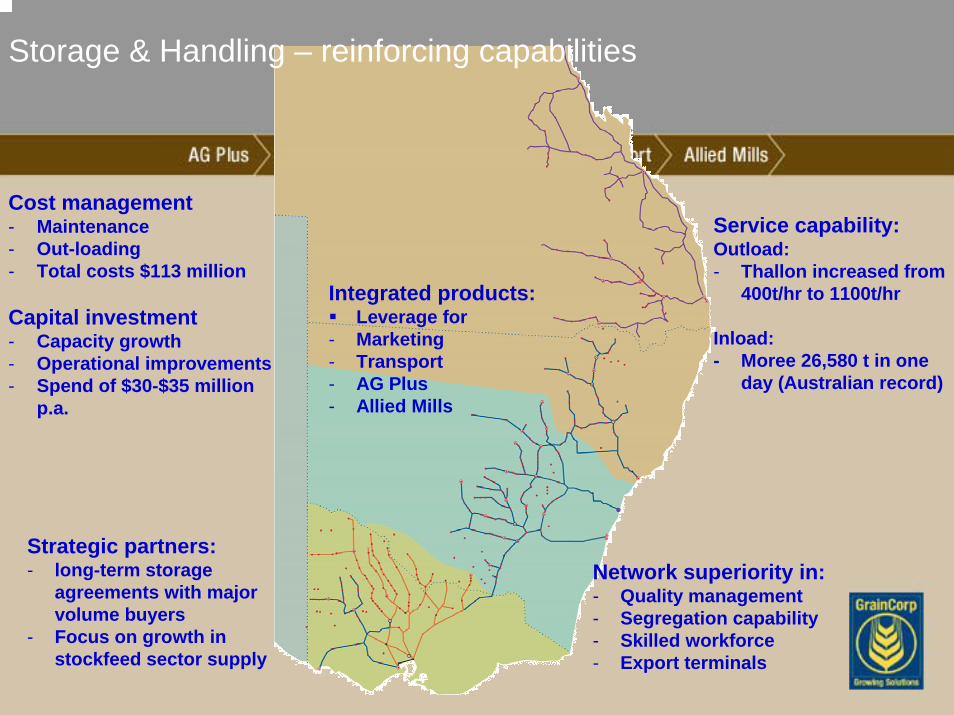

Storage & Handling – reinforcing capabilities

Cost management - Maintenance - Out-loading- Total costs $113 million

Capital investment - Capacity growth- Operational improvements- Spend of $30-$35 million

p.a.

Service capability:Outload:- Thallon increased from

400t/hr to 1100t/hr

Inload:- Moree 26,580 t in one

day (Australian record)

Network superiority in:- Quality management - Segregation capability- Skilled workforce- Export terminals

Integrated products:Leverage for

- Marketing- Transport- AG Plus- Allied Mills

Strategic partners:- long-term storage

agreements with major volume buyers

- Focus on growth in stockfeed sector supply

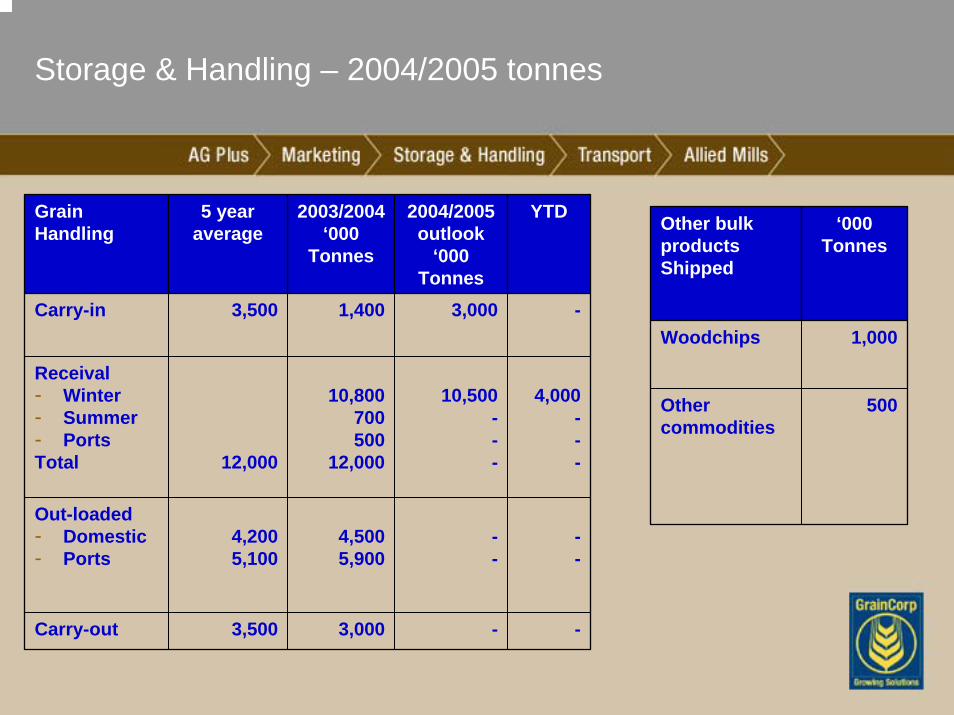

Storage & Handling – 2004/2005 tonnes

Other bulk products Shipped

‘000 Tonnes

Woodchips 1,000

Other commodities

500

Grain Handling

5 year average

2003/2004‘000

Tonnes

2004/2005outlook

‘000 Tonnes

1,400 3,000

10,500---

--

-

10,800700500

12,000

4,500 5,900

3,000

3,500

12,000

4,2005,100

3,500

YTD

Carry-in -

4,000---

--

Receival- Winter- Summer - PortsTotal

Out-loaded- Domestic- Ports

Carry-out -

GrainCorp Full Year Presentation

Business OperationsGrain Marketing

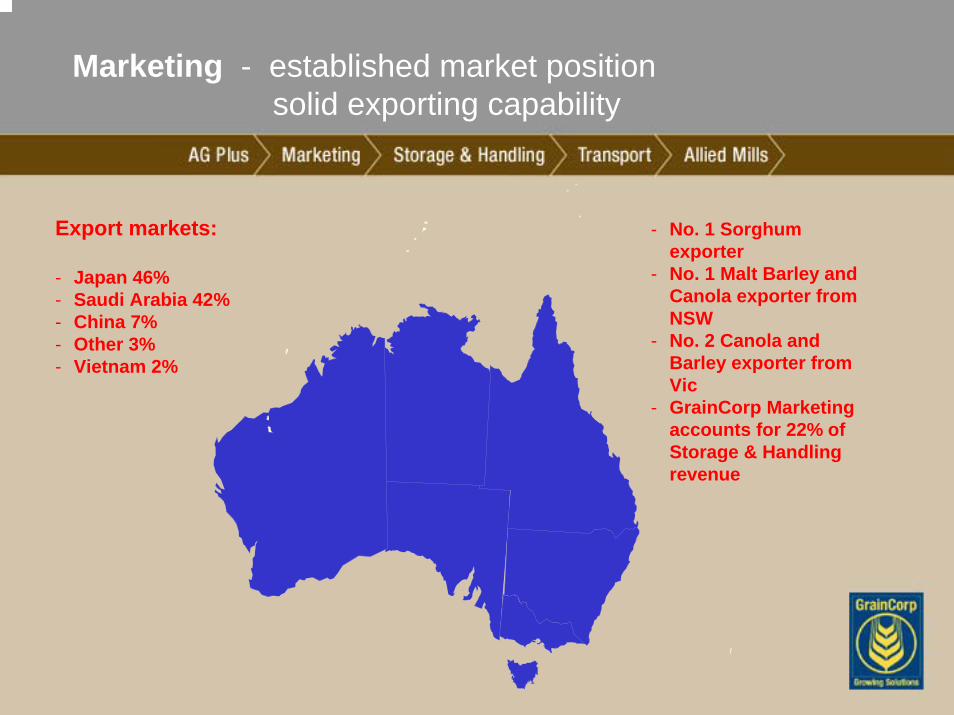

Export markets:

- Japan 46%- Saudi Arabia 42%- China 7%- Other 3%- Vietnam 2%

Marketing - established market positionsolid exporting capability

- No. 1 Sorghum exporter

- No. 1 Malt Barley and Canola exporter from NSW

- No. 2 Canola and Barley exporter from Vic

- GrainCorp Marketing accounts for 22% of Storage & Handling revenue

GrainCorp Marketing Performance – key drivers

Low cost accumulation and O/H – Australian Grain Accumulation

Superior Pool returns attracting grower loyalty

International grain trading skills – bulk/containers

Domestic supply agreements improving

Leveraging infrastructure relationship with customers e.g. Japan – highly regarded

2003/2004 ‘000 Tonnes

Grain Marketed 2,698

Grain Under Management 1,397

Grain Exported 775

GrainCorp Full Year Presentation

Business OperationsAG Plus

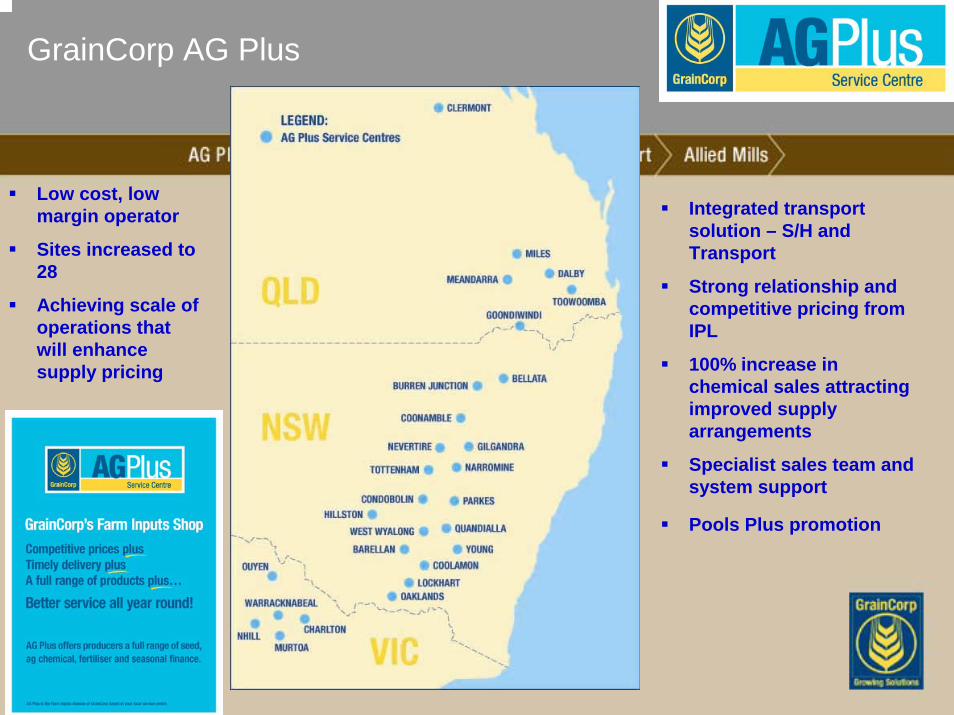

GrainCorp AG Plus

Low cost, low margin operator

Sites increased to 28

Achieving scale of operations that will enhance supply pricing

Integrated transport solution – S/H and Transport

Strong relationship and competitive pricing from IPL

100% increase in chemical sales attracting improved supply arrangements

Specialist sales team and system support

Pools Plus promotion

GrainCorp Full Year Presentation

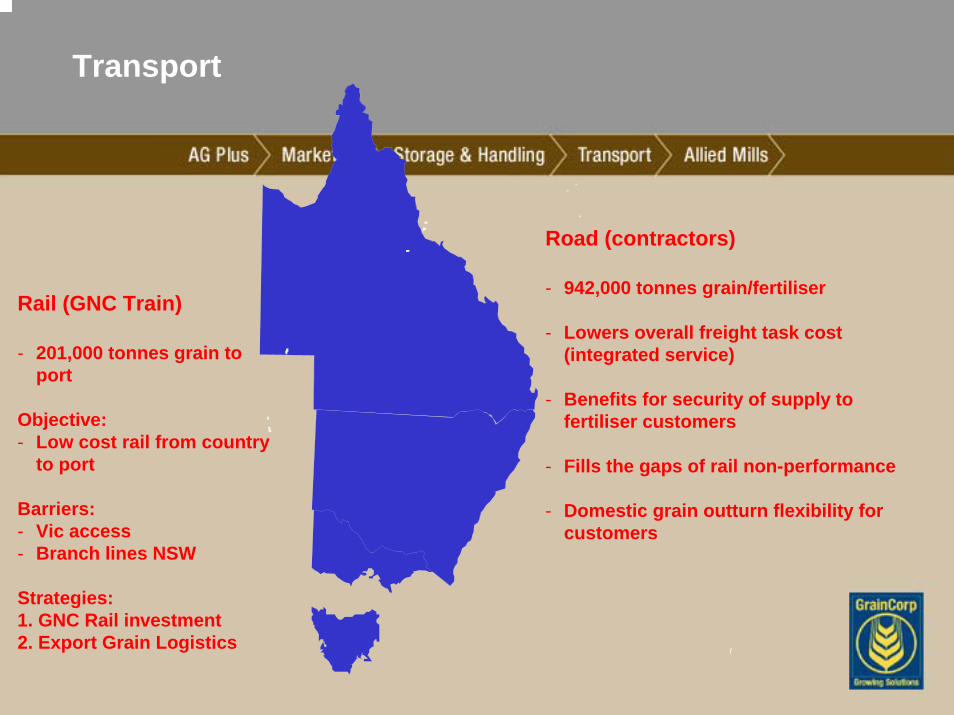

Business OperationsTransport

Transport

Road (contractors)

- 942,000 tonnes grain/fertiliser

- Lowers overall freight task cost (integrated service)

- Benefits for security of supply to fertiliser customers

- Fills the gaps of rail non-performance

- Domestic grain outturn flexibility for customers

Rail (GNC Train)

- 201,000 tonnes grain to port

Objective:- Low cost rail from country

to port

Barriers: - Vic access - Branch lines NSW

Strategies:1. GNC Rail investment 2. Export Grain Logistics

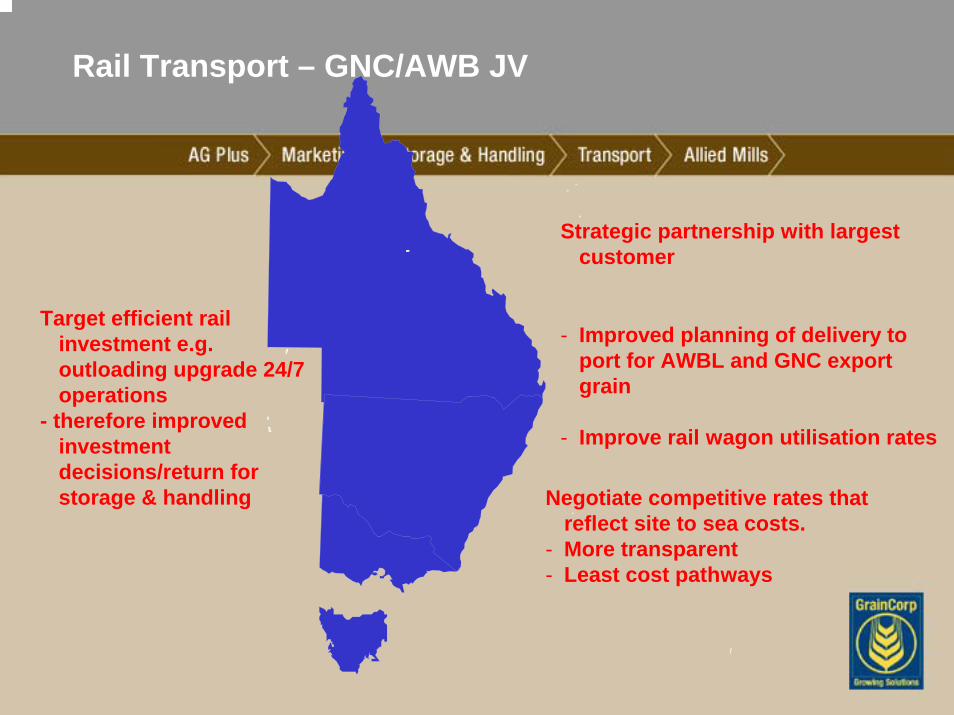

Rail Transport – GNC/AWB JV

Strategic partnership with largest customer

Target efficient rail investment e.g. outloading upgrade 24/7 operations

- therefore improved investment decisions/return for storage & handling

- Improved planning of delivery to port for AWBL and GNC export grain

- Improve rail wagon utilisation rates

Negotiate competitive rates that reflect site to sea costs.

- More transparent- Least cost pathways

GrainCorp Full Year Presentation

Business OperationsAllied Mills

ToowoombaTennysonDalby

Tamworth

Kingsgrove and Summer Hill

Albury

KensingtonBallarat

North Fremantle

BridgewaterMile End

Perth

Darwin

Brisbane

SydneyAdelaide

Melbourne

Hobart

State or Territory capital cityAllied Mills

production site

Primary Processing Opportunities and Strategy - Allied Mills

Strong focus on commercial customers

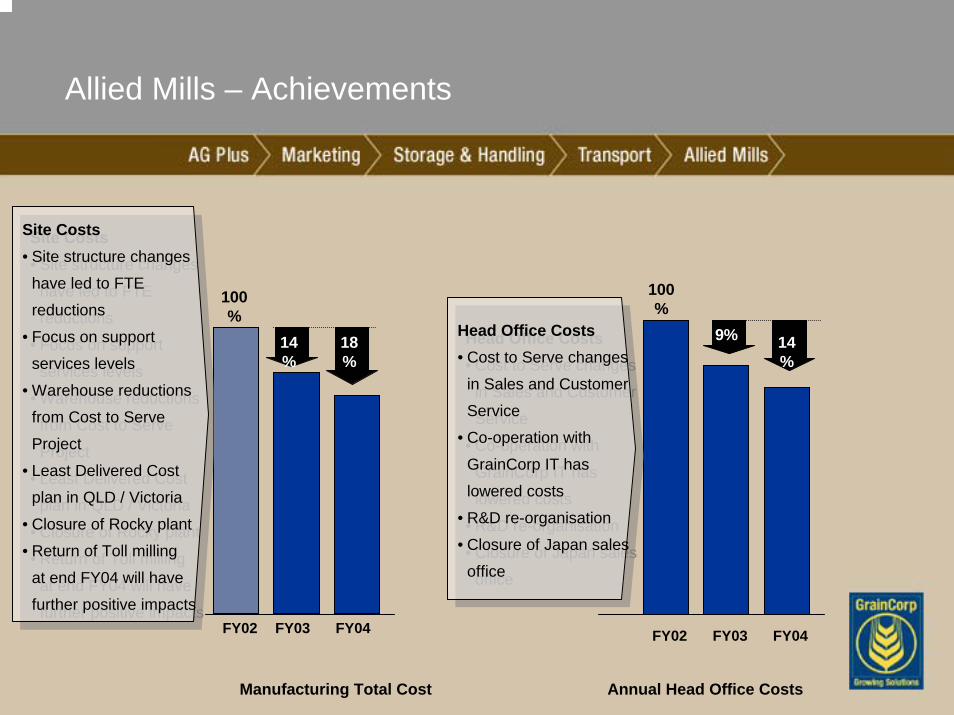

Reduction of workforce by 30%

Reconfiguration of mill operations and focus on high value mixing products – LDC program well advanced

Extended long-term supply agreement with Burns Philp

Potential development of Picton site to meet least cost manufacturing objectives

Margin improvements expected in 2004/2005

Market share at 50%

Ownership of primary processing adding value to the rest of GrainCorp business

Grain sales revenue from Allied $24.7m

Storage revenue from Allied $7.2m

FY02 FY03 FY04 FY02 FY03 FY04

Site Costs• Site structure changes

have led to FTE

reductions

• Focus on support

services levels

• Warehouse reductions

from Cost to Serve

Project

• Least Delivered Cost

plan in QLD / Victoria

• Closure of Rocky plant

• Return of Toll milling

at end FY04 will have

further positive impacts

Site Costs• Site structure changes

have led to FTE

reductions

• Focus on support

services levels

• Warehouse reductions

from Cost to Serve

Project

• Least Delivered Cost

plan in QLD / Victoria

• Closure of Rocky plant

• Return of Toll milling

at end FY04 will have

further positive impacts

Head Office Costs• Cost to Serve changes

in Sales and Customer

Service

• Co-operation with

GrainCorp IT has

lowered costs

• R&D re-organisation

• Closure of Japan sales

office

Head Office Costs• Cost to Serve changes

in Sales and Customer

Service

• Co-operation with

GrainCorp IT has

lowered costs

• R&D re-organisation

• Closure of Japan sales

office

100%

18%

100%

14%

Allied Mills – Achievements

14%

9%

Manufacturing Total Cost Annual Head Office Costs

GrainCorp Full Year Presentation

OutlookGrainCorp Limited

GrainCorp Outlook

Key drivers (Storage & Handling):

- Winter crop – 10.5 million tonnes- Summer crop – recent rains in Queensland, Northern NSW positive for

summer crop- Export program

Key drivers (other Business Units):

- Marketing performance- Allied Mills margin outcome- AG Plus sales and market share growth

Profit guidance will be provided in February 2005

Questions

Appendix

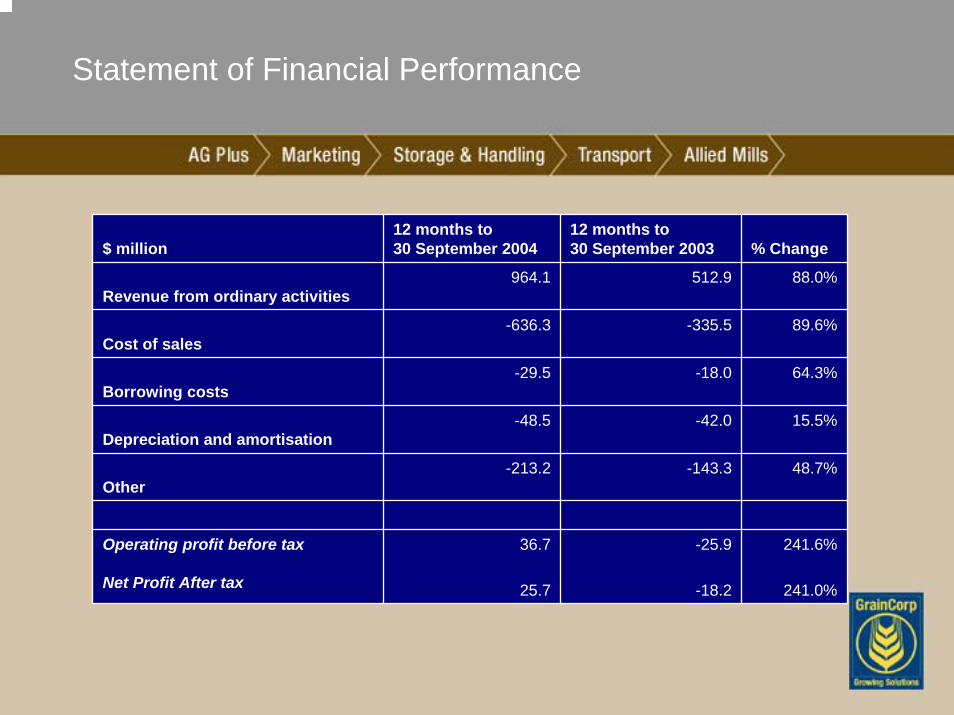

Statement of Financial Performance

$ million12 months to 30 September 2004

12 months to 30 September 2003 % Change

Revenue from ordinary activities964.1 512.9 88.0%

Cost of sales-636.3 -335.5 89.6%

Borrowing costs-29.5 -18.0 64.3%

Depreciation and amortisation-48.5 -42.0 15.5%

Other-213.2 -143.3 48.7%

Operating profit before tax

Net Profit After tax

36.7

25.7

-25.9

-18.2

241.6%

241.0%

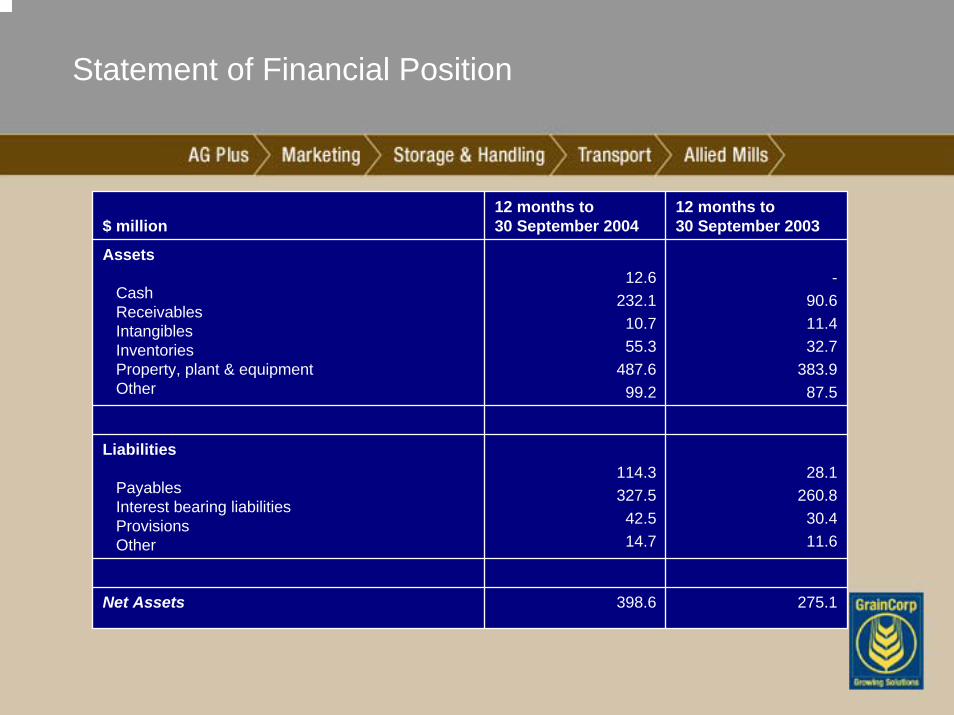

Statement of Financial Position

$ million12 months to 30 September 2004

12 months to 30 September 2003

Assets

CashReceivablesIntangiblesInventoriesProperty, plant & equipmentOther

12.6232.110.755.3

487.699.2

-90.611.432.7

383.987.5

Liabilities

PayablesInterest bearing liabilitiesProvisionsOther

114.3327.542.514.7

28.1260.830.411.6

Net Assets 398.6 275.1

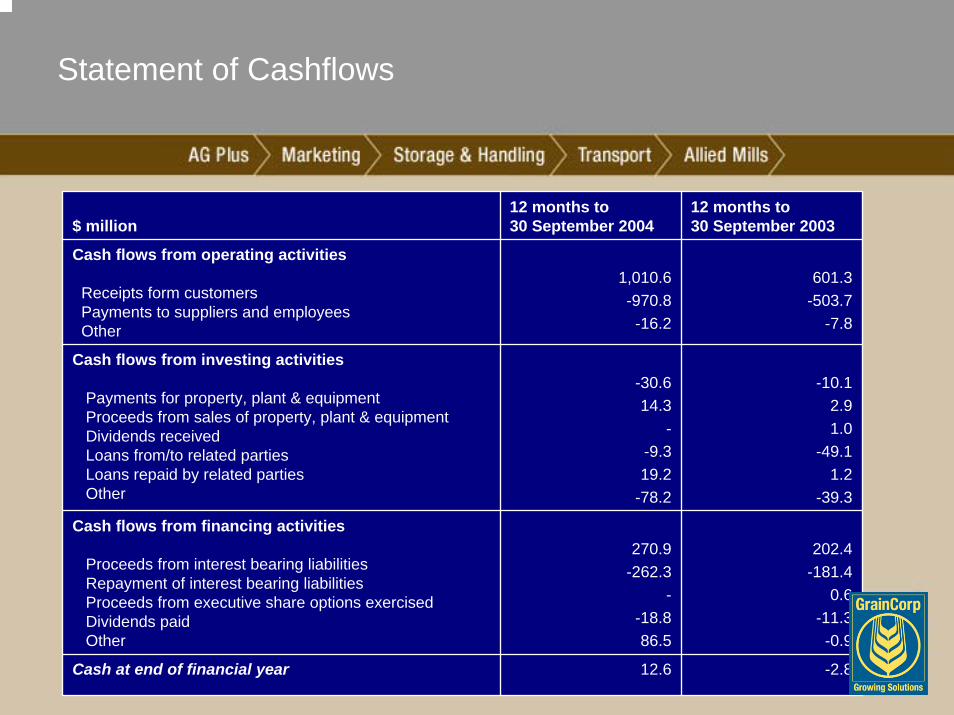

Statement of Cashflows

$ million12 months to 30 September 2004

12 months to 30 September 2003

Cash flows from operating activities

Receipts form customersPayments to suppliers and employeesOther

1,010.6-970.8-16.2

601.3-503.7

-7.8

Cash flows from investing activities

Payments for property, plant & equipmentProceeds from sales of property, plant & equipmentDividends receivedLoans from/to related partiesLoans repaid by related partiesOther

-30.614.3

--9.319.2

-78.2

-10.12.91.0

-49.11.2

-39.3

Cash flows from financing activities

Proceeds from interest bearing liabilitiesRepayment of interest bearing liabilitiesProceeds from executive share options exercisedDividends paidOther

270.9-262.3

--18.886.5

202.4-181.4

0.6-11.3-0.9

Cash at end of financial year 12.6 -2.8

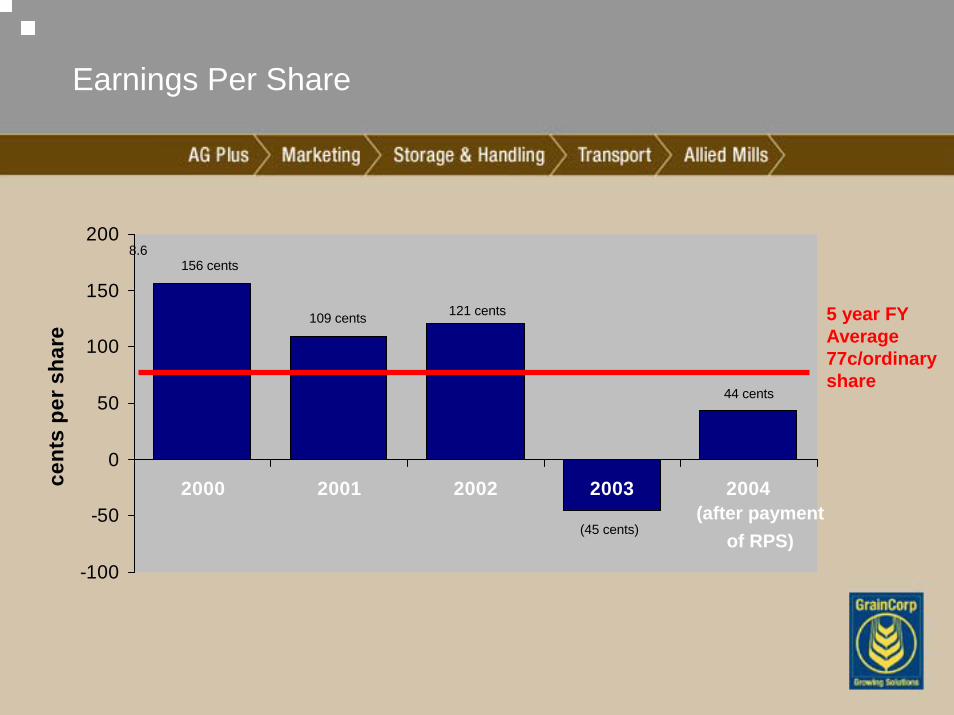

Earnings Per Share

-100

-50

0

50

100

150

200

2000 2001 2002 2003 2004cent

s pe

r sha

re

5 year FY Average 77c/ordinary share

(after payment of RPS)

156 cents

109 cents 121 cents

44 cents

8.6

(45 cents)

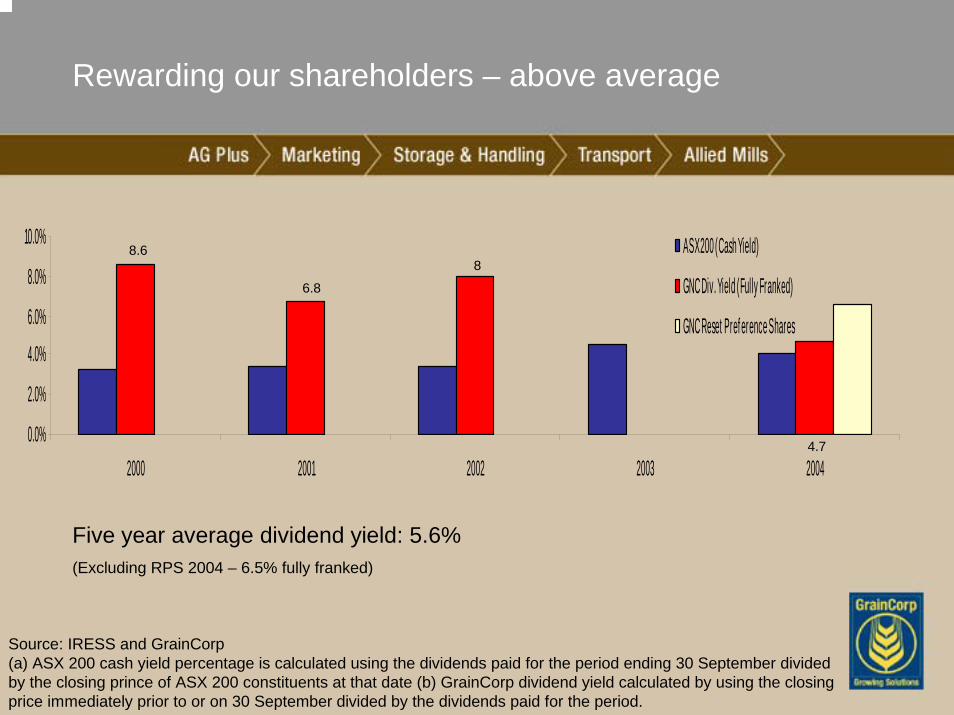

Rewarding our shareholders – above average

Source: IRESS and GrainCorp(a) ASX 200 cash yield percentage is calculated using the dividends paid for the period ending 30 September divided by the closing prince of ASX 200 constituents at that date (b) GrainCorp dividend yield calculated by using the closing price immediately prior to or on 30 September divided by the dividends paid for the period.

Five year average dividend yield: 5.6%(Excluding RPS 2004 – 6.5% fully franked)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2000 2001 2002 2003 2004

ASX 200 (Cash Yield)

GNC Div. Yield (Fully Franked)

GNC Reset Pref erence Shares

8.6

4.7

8

6.8