fundamentals of income taxation of trusts & form 1041

TRANSCRIPT

© 2010-2020 Keebler Tax & Wealth Education, Inc. 1

Successfully Completing an Income Tax Return for a Trust or Estate

Form 1041

© 2010-2020 Keebler Tax & Wealth Education, Inc. 2

Today’s presenter

Bob Keebler, CPA/PFS, MST, AEP (Distinguished), CGMA

Bob is a partner with Keebler & Associates, LLP and is a 2007 recipient of the prestigious Accredited Estate Planners (Distinguished) award from the National Association of Estate Planners & Councils. His practice includes family wealth transfer and preservation planning, charitable giving, retirement distribution planning, and estate administration. He is the author of more than 100 articles and columns and is the editor, author or co-author of many books and treatises on wealth transfer and taxation.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 3

Income Taxation of Trusts & Estates Overview

• Foundational concepts

• Grantor trusts

• Charitable Remainder Trusts (CRTs)

• Bracket Management

• Shifting Income with Trust Distributions

• Limit on Miscellaneous Itemized Deductions

• State Income Tax Planning for Trusts

• Form 1041 Examples

© 2010-2020 Keebler Tax & Wealth Education, Inc. 4

How this knowledge helps you

• Tax Compliance for Trusts

• Tax Planning for Trusts

• Litigation and Settlement Planning

• Protect the Trustee or Personal Representative

© 2010-2020 Keebler Tax & Wealth Education, Inc. 5FM415

© 2010-2020 Keebler Tax & Wealth Education, Inc. 6FM416

© 2010-2020 Keebler Tax & Wealth Education, Inc. 7FM417

© 2010-2020 Keebler Tax & Wealth Education, Inc. 8FM418

© 2010-2020 Keebler Tax & Wealth Education, Inc. 9

Form 1041Foundational Concepts

© 2010-2020 Keebler Tax & Wealth Education, Inc. 10

Foundational Concepts:Overview of Subchapter J of the Code

• General Rules for Taxation of Estates and Trusts §641 - §646

– §651 - §652 – Trusts Which Distribute Current Income Only

– §661 - §664 – Estates Which May Accumulate Income or Which Distribute Corpus

– §665 - §669 – Treatment of Excess Distributions by Trusts

– §671 - §679 – Grantors and Others treated as Substantial Owners

– §681 - §685 – Miscellaneous

© 2010-2020 Keebler Tax & Wealth Education, Inc. 11

Foundational concepts:Overview of Subchapter J of the Code

• General Rules for Taxation of Estates and Trusts §641 - §646

– §641 – Imposition of Tax

– §642 – Special Rules for Credits and Deductions

– §643 – Definitions applicable to subparts A,B,C and D

– §644 – Taxable Year of Trusts

– §645 – Certain Revocable Trusts Treated as Part of Estate

– §646 – Tax Treatment of Electing Alaska Native Settlement Trusts

© 2010-2020 Keebler Tax & Wealth Education, Inc. 12

Foundational concepts:Overview of Subchapter J of the Code

• Trusts Which Distribute Current Income Only §651- §652

– §651 – Deductions for Trusts Distributing Current Income Only

– §652 – Inclusion of Amounts in Gross Income of Beneficiaries of Trusts Distributing Current Income Only

© 2010-2020 Keebler Tax & Wealth Education, Inc. 13

Foundational concepts:Overview of Subchapter J of the Code

• Estates Which May Accumulate Income or Which Distribute Corpus §661 - §664

– §661 Deduction for Estates and Trusts Accumulating Income or Distributing Corpus

– §662 – Inclusion of Amounts in Gross Income of Beneficiaries of Estates and Trusts Accumulating Income or Distributing Corpus

– §663 – Special Rules Applicable to §661 and §662

– §664 – Charitable Remainder Trusts

© 2010-2020 Keebler Tax & Wealth Education, Inc. 14

Foundational ConceptsOverview of Subchapter J of the Code

• Treatment of Excess Distributions by Trusts §665 -§669

– §665 – Definitions Applicable to Subpart D

– §666 – Accumulation Distribution Allocated to Preceding Years

– §667 – Treatment of Amounts Deemed Distributed by Trusts in Preceding Years

– §668 – Interest Charge on Accumulation Distributions from foreign trusts

– §669 – This section was repealed

© 2010-2020 Keebler Tax & Wealth Education, Inc. 15

Foundational ConceptsOverview of Subchapter J Of The Code

• Grantors and Others treated as Substantial Owners §671 -§679– §671 – Trust Income, Deduction, and Credits Attributed to Grantors

and Others as Substantial Owners

– §672 – Definitions and Rules

– §673 – Reversionary Interests

– §674 – Power to Control Beneficial Enjoyment

– §675 – Administrative Powers

– §676 – Power to Revoke

– §677 – Income for Benefit of Grantor

– §678 – Person Other Than Grantor Treated as Substantial Owner

– §679 – Foreign Trusts Having One or More United States Beneficiaries

© 2010-2020 Keebler Tax & Wealth Education, Inc. 16

Foundational Concepts:Overview of Subchapter J of the Code

• Miscellaneous §681 - §685

– §681 – Limitation on Charitable Deduction

– §682 – Income of an Estate or Trust in Case of Divorce, etc.

– §683 – Use of Trust as an Exchange Fund

– §684 – Recognition of Gain on Certain Transfer to Certain Foreign Trusts and Estates

– §685 – Treatment of Funeral Trusts

© 2010-2020 Keebler Tax & Wealth Education, Inc. 17

Foundational concepts: general tax rules

• Trusts and estates are separate taxable entities

– Receive income and pay expenses

• Taxable income computed similar to individuals

– Exemption

• $100 complex trust

• $300 simple trust

• $600 estate

• Method of tax accounting

– Trusts – Calendar year (i.e. Jan. 1st – Dec. 31st)FM4117

© 2010-2020 Keebler Tax & Wealth Education, Inc. 18

Foundational concepts: general tax rules

• Income taxed to either the trust/estate or the beneficiary

– If income is accumulated, then the income is taxed to the trust/estate

– If income is distributed, then the trust/estate gets an income tax deduction and beneficiaries report taxable income

FM4118

© 2010-2020 Keebler Tax & Wealth Education, Inc. 19

Foundational concepts:2019 ordinary income tax rates for individuals

FM4119

© 2010-2020 Keebler Tax & Wealth Education, Inc. 20

Foundational concepts:2020 ordinary income tax rates for individuals

FM4120

© 2010-2020 Keebler Tax & Wealth Education, Inc. 21

Foundational concepts:2019 ordinary income tax rates for estates & trusts

FM4121

© 2010-2020 Keebler Tax & Wealth Education, Inc. 22

Foundational concepts:2020 ordinary income tax rates for estates & trusts

FM4122

© 2010-2020 Keebler Tax & Wealth Education, Inc. 23

Foundational concepts: tax asset classes

FM41 23

Interest

Income

Capital

Gain

Income

Roth IRA

and

Insurance

Real Estate

and

Oil & Gas

Pension

and

IRA Income

•Money market

•Corporate

bonds

•US Treasury

bonds

Attributes

•Annual

income tax on

interest

•Taxed at

highest

marginal rates

•Equity

Securities

Attributes

•Deferral until

sale

•Reduced

capital gains

rate

•Step-up

basis at

death

Real Estate

•Depreciation

tax shield

•1031

exchanges

•Deferral on

growth until

sale

•199A

Deduction

Oil & Gas

•Large up front

IDC

deductions

•Depletion

allowances

•199A

Deduction

•Pension plans

•Profit sharing

plans

•Annuities

Attributes

•Growth during

lifetime

•RMD for IRA

and qualified

plans

•No step-up

Dividend

Income

Tax Exempt

Interest

•Equity

Securities

Attributes

•Qualified

dividends at

LTCG rate

•Return of

capital

dividend

•Capital gain

dividends

•Bonds issued by

State and local

Governmental

entities

Attributes

•Federal tax

exempt

•State tax exempt

Roth IRA

•Tax-free growth

during lifetime

•No 70½ RMD

•Tax-free

distributions out

to beneficiaries

life expectancy

Life Insurance

•Tax-deferred

growth

•Tax-exempt

payout at death

© 2010-2020 Keebler Tax & Wealth Education, Inc. 24

Accounting in the year of death: partial checklist

• File final 1040 as due as usual for income received prior to death; account for income and deductions actually and constructively received

• Apply for an EIN for the estate & file 1041 for income received after death

• File Form 56, Notice Concerning Fiduciary Relationship

• Review “open” state & federal 1040s, 1041s, & 709s

• Review prior gift tax returns & begin marshaling other materials for filing 706

• Review prior RMDs for correctness and plan for future distributions

• Review IRAs for Prohibited Transactions

FM4124

© 2010-2020 Keebler Tax & Wealth Education, Inc. 25

Accounting in the year of death: allocating income 1040 v. 1041

• Allocated to Final 1040

– Decedents medical expenses (generally)

– Unused charitable contributions / other deductions

– Capital & net operating losses

• Allocated by date of receipt

– Wages/salary

– IRA distributions

– Installment sale payments

– Interest & dividendsFM4125

© 2010-2020 Keebler Tax & Wealth Education, Inc. 26

Accounting in the year of death: allocating income 1040 v. 1041

• Partnership – two allocation options

– Close books on date of death

– Pro-rate income already received for the whole tax year between the 1040 & 1041 according to the date of death

FM4126

© 2010-2020 Keebler Tax & Wealth Education, Inc. 27

Accounting in the year of death:1040 v. 1041 – special opportunities

• IRC §454 – Elect to recognize differed accounting income on Series E & EE bonds on the final personal income tax return (effective if decedent’s rate is low relative to beneficiaries or estate tax liability exists)

• IRC §754 – Elect to adjust the inside basis of a partnership to equal the outside basis (with numerous complications & exceptions)

FM4127

© 2010-2020 Keebler Tax & Wealth Education, Inc. 28

Accounting in the year of death:1040 v. 1041 – quarterly estimates

• Final 1040 – must continue to make timely quarterly payments in order to avoid penalties; however, the payments can be reduced based on the tax due on the prorated income

• 1041s – if election is made to be treated as an estate, as opposed to a trust, the requirement to make quarterly estimates in order to avoid penalties is waived for two years

FM4128

© 2010-2020 Keebler Tax & Wealth Education, Inc. 29

Accounting in the year of death:706 v. 1041 – administration expenses

• Administration expenses may be deductible on either Form 706 or Form 1041, but not both simultaneously

• However, the expenses can be strategically divided between the forms to the clients advantage

• If taken on form 1041, a waiver is required

• See 26 USC §642(g)

FM4129

© 2010-2020 Keebler Tax & Wealth Education, Inc. 30

Accounting in the year of death:706 v. 1041 – administration expenses

• Examples of Deductible Administration Expenses

– Executor’s management commissions

– Attorney’s fees

– Court costs

– Accountant’s fees

– Appraiser’s fees

– Expenses to preserve & distribute the estate

– Certain expenses to sell property if sale is necessary to pay decedent’s debts, administration expenses, taxes…

FM4130

© 2010-2020 Keebler Tax & Wealth Education, Inc. 31

Accounting in the year of death:706 v. 1041 – administration expenses

• Examples of Common Non-Deductible Expenses

– Funeral expenses (706 only)

– Certain improvements to property must be added to basis rather than expensed

FM4131

© 2010-2020 Keebler Tax & Wealth Education, Inc. 32

Accounting in the year of death:1041 – estate income tax return elections

• Fiscal year tax reporting (as opposed to calendar year)

• Combine revocable trust & estate onto one return

FM4132

© 2010-2020 Keebler Tax & Wealth Education, Inc. 33

Protecting the executor: forms to file

FM4133

Type of Tax Form Number“Protective”

FormStatute

Personal Income Tax

1040 4810§§ 6501(d),

6905(a)

FiduciaryIncome Tax

1041 4810§§ 6501(d),

6905(a)

Gift Tax 709 4810§§ 6501(d),

6905(a)

Estate Tax 706 5495 § 2204

© 2010-2020 Keebler Tax & Wealth Education, Inc. 34

Protecting the executor:request for prompt assessment using form 4810

• For income tax and gift tax

• Can request prompt assessment when filing or for a previously filed “open” return

• Shortens the Statue of limitations from three years to 18 months

• Reduces the risk of the executor receiving a notice of deficiency after the estate is distributed

• See IRC. §6501(d)FM4134

© 2010-2020 Keebler Tax & Wealth Education, Inc. 35

Protecting the executor:forms to file

FM4135

© 2010-2020 Keebler Tax & Wealth Education, Inc. 36

Protecting the executor:request for discharge from personal liability using form 5495

• For income, gift & estate tax

• Service has nine months from filing to inform the executor if any tax is due

• Doesn’t relieve the estate from liability or lien, but allows the executor to distribute the estate without taking on the risk of being held personally liable for decedent's unpaid taxes

• See Treas. Reg. §20.2002-1; IRC §§ 2204, 6905(a)FM4136

© 2010-2020 Keebler Tax & Wealth Education, Inc. 37

Protecting the executor: forms to file

FM4137

© 2010-2020 Keebler Tax & Wealth Education, Inc. 38

Foundational concepts: types of trusts

• Simple trusts

– Required to distribute accounting income annually

– Cannot make principal distributions

– Cannot make distributions to charity

• Complex trusts

– May accumulate income

– May make either discretionary or mandatory distributions of income and/or principal

– May make distributions to charity

• ESBT – Electing Small Businesses Trust

• QSST – Qualified Subchapter “S” Trust

FM4138

© 2010-2020 Keebler Tax & Wealth Education, Inc. 39

Foundational concepts: types of trusts

• Grantor trusts

– Trust and grantor treated as one taxpayer

– Income taxed to grantor

• Charitable trusts

– Split-interest trusts consisting of an income beneficiary and a remainder beneficiary

• Charitable Lead Trust (CLT) – charity is the income beneficiary

• Charitable Remainder Trust (CRT) – charity is the remainder beneficiary

– Last for a term of years or lifeFM4139

© 2010-2020 Keebler Tax & Wealth Education, Inc. 40

Foundational concepts: types of “income”

• Fiduciary accounting income

– Governed by state law and the trust instrument

– Determines the amount that may or must pass to the trust’s or estate’s beneficiaries

• Tax accounting income

– Governed by the federal income tax law

– Determines who is taxed on the income

FM4140

© 2010-2020 Keebler Tax & Wealth Education, Inc. 41

Typical types of “income” under traditional fiduciary accounting

• Interest

– Taxable

– Tax-exempt

• Dividends

• Rents (net of expenses)

• Royalties

FM4141

© 2010-2020 Keebler Tax & Wealth Education, Inc. 42

Typical types of “principal” under traditional fiduciary accounting

• IRA value as of date of death

• Increases in asset value (i.e., growth)

• Realized long-term capital gain

• Realized short-term capital gain

• Proceeds from covered call writing

FM4142

© 2010-2020 Keebler Tax & Wealth Education, Inc. 43

Assume that a complex trust had the following sources of income and deductions during the current tax year:

Interest income $3,000

Tax-exempt interest income 1,000

Dividend income 6,000

Rental income 10,000

Royalty income 5,000

Long-term capital gains 15,000

Taxes 3,000

Trustee fees 3,000

Attorney/accountant fees 1,000All indirect expenses

Foundational concepts:fiduciary accounting vs. taxable income example

FM4143

© 2010-2020 Keebler Tax & Wealth Education, Inc. 44

Foundational concepts:fiduciary accounting vs. taxable income example

Fiduciary

Accounting

Income

Taxable

Income

Interest income 3,000$ 3,000$

Tax-exempt interest income 1,000 -

Dividend income 6,000 6,000

Rental income 10,000 10,000

Royalty income 5,000 5,000

Long-term capital gains - 15,000

Gross income 25,000$ 39,000$

Less: Taxes (1,875) (2,925)

Less: Trustee fees (1,875) (2,925)

Less: Attorney/accountant fees (625) (975)

Less: Exemption - (100)

Net Income 20,625$ 32,075$

FM4144

NOTE 1: Trust expenses (for fiduciary accounting purposes) were apportioned on a pro-rata basis between income and principal.

NOTE 2: Under IRC §265, the trust’s deductible expenses (for income tax purposes) must be reduced for the portion that are allocable to tax-exempt income.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 45

Foundational concepts: distributable net income (DNI)

• Determines the amount of the trust’s or estate’s income distribution deduction

• Determines how much the beneficiaries must report as income on their tax returns

• Determines the character (e.g., interest, dividends, etc.) of the taxable income in beneficiaries’ hands

FM4145

Beneficiaries

Trust

© 2010-2020 Keebler Tax & Wealth Education, Inc. 46

DNI

Trust/EstateDNI acts as a ceiling

for purposes of the allowable deduction

BeneficiaryDNI acts as a ceiling for the total amount of income the beneficiary must report on his/her tax return

Foundational concepts: distributable net income (DNI)

FM4146

© 2010-2020 Keebler Tax & Wealth Education, Inc. 47

Taxable income

+ Income distribution deduction

+ Exemption

+ Net tax-exempt income

+ Capital losses*

< Capital gains* >

< Extraordinary/stock dividends >

= Distributable Net Income (DNI)

* Except in the year of termination

Foundational concepts: computation of DNI

FM4147

© 2010-2020 Keebler Tax & Wealth Education, Inc. 48

Foundational concepts: distributable net income (DNI) – additional issues

• Normally, capital gains and losses are trapped at the trust or estate level

– However, in the year of termination, the capital gain/loss passes out to the beneficiaries

• Specific bequests do not carry out DNI to the beneficiaries

FM4148

© 2010-2020 Keebler Tax & Wealth Education, Inc. 49

Assume that a complex trust had the following sources of income and deductions during the current tax year:

Interest income $15,000

Dividend income 10,000

Rental income 5,000

Long-term capital gains 20,000

Taxes 2,500

Trustee fees 3,500

Attorney/accountant fees 2,000

Foundational concepts:distributable net income (DNI) example

FM4149

© 2010-2020 Keebler Tax & Wealth Education, Inc. 50

Foundational concepts:distributable net income (DNI) example

Interest income 15,000$

Dividend income 10,000

Rental income 5,000

Long-term capital gains 20,000

Total Income 50,000$

Less: Taxes (2,500)

Less: Trustee fees (3,500)

Less: Attorney/accountant fees (2,000)

Adjusted Gross Income (AGI) 42,000$

Less: Exemption (100)

Taxable Income 41,900$

Taxable Income 41,900$

Add-In: Exemption 100

Less: Long-term capital gains (20,000)

Distributable Net Income (DNI) 22,000$

FM4150

© 2010-2020 Keebler Tax & Wealth Education, Inc. 51

Foundational concepts: tier rules

• Apply to estates and complex trusts

• Two tiers

– First tier beneficiary

• Required distribution of income on a current basis

– Second tier beneficiary

• Receives any amount remaining (at the discretion of the trustee/executor)

FM4151

© 2010-2020 Keebler Tax & Wealth Education, Inc. 52

Mandatory

distributions

of income

Complex

Trust

First Tier

Beneficiary

DNI carries out to this

beneficiary only to the

extent that income

exceeds the distribution

made to the first tier

beneficiary

Second Tier

Beneficiary

Discretionary

distributions

of income and/or

principalDNI carries out to

this beneficiary first

Foundational concepts: tier rules

FM4152

© 2010-2020 Keebler Tax & Wealth Education, Inc. 53

Foundational concepts: separate share rule

• Applies to both estates and complex trusts

• Treats multiple beneficiaries of an estate or single trust as if each were the sole beneficiary

• Determines how DNI carries out to each beneficiary

– DNI is computed separately for each share

FM4153

© 2010-2020 Keebler Tax & Wealth Education, Inc. 54

Foundational concepts: separate share rule example

• Assumptions

– Complex trust

– Two equal beneficiaries (S & D)

– Distributable Net Income (DNI) in 2019 = $30,000

– Distributable Net Income (DNI) in 2020 = $10,000

– Trust distributes $20,000 to Son and $5,000 to Daughter in 2019

– Trust distributes $15,000 to Daughter in 2020

FM4154

© 2010-2020 Keebler Tax & Wealth Education, Inc. 55

Foundational concepts: separate share rule example

2019 Tax Year 2020 Tax Year

Son $15,000 $ 0

Daughter 5,000 5,000

Trust 10,000 5,000

Total $30,000 $10,000

FM4155

© 2010-2020 Keebler Tax & Wealth Education, Inc. 56

Foundational concepts:“65-day” rule (IRC §663(b))

• Applies to estates and complex trusts

• Allows fiduciary to treat distributions made within 65 days after year-end to be treated as if they were made as of December 31st of the prior year

– Limited to DNI (reduced by distributions made during the prior year)

• Election must be made by the due date of the tax return

– Election is irrevocable

– Annual election

FM4156

© 2010-2020 Keebler Tax & Wealth Education, Inc. 57

20202019

12/31

65 days

Distributions made during this period will be treated as having been made as of 12/31/2019 (if a timely

election is made)

Foundational concepts:“65-day” rule (IRC §663(b))

FM4157

© 2010-2020 Keebler Tax & Wealth Education, Inc. 58

Foundational concepts: specific bequests

• Do not carry out DNI

• Not taxable to trust/estate or beneficiaries

• Requirements

– Paid at once OR

– Paid in not more than three installments

• Examples

– “I leave my brother Randy $250,000.”

– “I leave my sister Mary my boat.”

FM4158

© 2010-2020 Keebler Tax & Wealth Education, Inc. 59

Foundational concepts: charitable deduction (IRC §642(c))

• Requirements

– Paid from gross income

– Paid pursuant to the governing document

• Must be actually be paid in the current year

– Exception – pre-1969 trusts

• Unlimited in amount

• Taken as a deduction in computing adjusted gross income (AGI)

FM4159

© 2010-2020 Keebler Tax & Wealth Education, Inc. 60

Foundational concepts: pecuniary bequests to charity CCA 200644020

• Pecuniary bequest to charitable beneficiary

• Acceleration of income on IRD

• No IRC §642(c) deduction – terms of trust did not direct or require that the trustee pay the pecuniary legacies from the trust's gross income

FM4160

© 2010-2020 Keebler Tax & Wealth Education, Inc. 61

Foundational concepts: income in respect of a decedent (IRD)

Income in respect of a decedent (IRD) – is all items of gross income in respect of a decedent which were not properly included as taxable income in a tax period falling on or before a taxpayer’s death and are payable to his/her estate and/or another beneficiary

FM4161

© 2010-2020 Keebler Tax & Wealth Education, Inc. 62

Foundational concepts: income in respect of a decedent (IRD)

• Specific types of IRD

– IRAs and other qualified retirement plans

– Unpaid salaries/wages at the time of death

– Dividends and interest earned, but not taxed, prior to death

– Unrecognized capital gain on an installment note at the time of the seller’s death

– Net Unrealized Appreciation (NUA) on employer securities

FM4162

© 2010-2020 Keebler Tax & Wealth Education, Inc. 63

Foundational concepts:IRC §691(c) deduction

• To the extent that a decedent’s taxable estate includes items of IRD and a federal estate tax is assessed, the estate and/or its beneficiaries are entitled to an income tax deduction for the estate tax attributable to IRD

– This deduction is a miscellaneous itemized deduction NOT subject to the 2% AGI limitation

– This deduction is subject to the 3% of AGI “Haircut”

FM4163

© 2010-2020 Keebler Tax & Wealth Education, Inc. 64

Foundational concepts:IRC §691(c) deduction

• The income tax deduction computation for estate taxed paid on IRD is determined on a “with and without” basis

– In essence, the total deduction allowed is the difference between: (a) the estate tax liability withall items of IRD included in the taxable estate and (b) the estate tax liability without the IRD included in the taxable estate

FM4164

© 2010-2020 Keebler Tax & Wealth Education, Inc. 65

Foundational concepts:IRC §691(c) deduction example

Non-IRD IRD

Cash & money market 15,000$ -$

Accrued interest - 100

Marketable securities (non-qualified) 750,000 -

Accrued interest & dividends - 9,900

IRA - 1,500,000

Primary Residence 350,000 -

Cottage 150,000 -

Personal property 50,000 -

TOTALS 1,315,000$ 1,510,000$

FM4165

On July 1, 2019, Jackie passed away leaving the following

assets:

© 2010-2020 Keebler Tax & Wealth Education, Inc. 66

Foundational concepts:IRC §691(c) deduction example

With IRD Without IRD

Gross Estate 2,825,000$ 1,315,000$

Less: Exemption (2,000,000) (2,000,000)

Taxable Estate 825,000$ -$

Estate Tax 371,250$ -$

Gross IRC §691(c) Deduction 371,250$

(Difference between estate tax with and without IRD)

FM4166

Subsequent to her death, the personal representative

withdrew $50,000 from Jackie’s IRA. Accordingly, the IRC

§691(c) attributable to the $50,000 distribution would be

as follows:

© 2010-2020 Keebler Tax & Wealth Education, Inc. 67

Foundational concepts:IRC §691(c) deduction example

IRD

Allocable

IRC §691(c)

Deduction

Interest - Cash & money market 100$ 25$

Interest & dividends - Brokerage account 9,900 2,434

IRA 1,500,000 368,791

TOTAL 1,510,000$ 371,250$

Gross IRA distribution 50,000$

IRC §691(c) apportionment percentage (i.e. $368,791/$1,500,000) 24.586%

IRC §691(c) deduction 12,293$

FM4167

© 2010-2020 Keebler Tax & Wealth Education, Inc. 68

Foundational concepts:trust/estate termination

• In the year of termination, all Net Operating Losses (NOLs), capital losses and “excess deductions” pass to the beneficiaries

– Only applies in the year of termination

– NOLs subject to carryback/carryover rules that apply to individual taxpayers

– No time limit on beneficiaries to use capital loss carryovers

FM4168

© 2010-2020 Keebler Tax & Wealth Education, Inc. 69

Foundational concepts: “excess deductions”

• “Excess deductions” occur when trust/estate expenses exceed income in the year of termination

– Deduction passes to the beneficiaries

– Deductible as a “miscellaneous itemized deduction” (subject to the 2% AGI floor)

FM4169

© 2010-2020 Keebler Tax & Wealth Education, Inc. 70

APPLICATION OF THE 3.8% NET INVESTMENT INCOME TAX TO TRUSTS & ESTATES

© 2010-2020 Keebler Tax & Wealth Education, Inc. 71

3.8% NIIT – example

• In Year 1, Trust (T) has:

– Dividend income of $15,000

– Interest income of $10,000

– Capital gain of $5,000

– IRA distribution of $75,000

– No expenses

• T distributes $10,000 of its current year trust accounting income to A, a beneficiary of T

FM4171

See Reg. Section 1.1411-3(e)(5) Example 1

© 2010-2020 Keebler Tax & Wealth Education, Inc. 72

3.8% NIIT – example

• T’s DNI is $100,000 ($15,000 dividends + $10,000 interest + $75,000 IRA)

• $10,000 of DNI is distributed to A

• T’s deduction under §661 is $10,000

• Under §1.662(b)-1, the deduction reduces each class of income comprising DNI on a proportional basis.

– $10,000 distribution = 10% of DNI ($10,000/$100,000)

FM4172

See Reg. Section 1.1411-3(e)(5) Example 1

© 2010-2020 Keebler Tax & Wealth Education, Inc. 73

3.8% NIIT – example

• Therefore, the distribution consists of:

– $1,500 dividend

– $1,000 interest

– $7,500 IRA (ordinary income)

• Because the $5,000 of capital gain allocated to principal for trust accounting purposes did not enter into DNI, no portion of that amount is included in the $10,000 distribution, nor does it qualify for the deduction under §661

FM4173

See Reg. Section 1.1411-3(e)(5) Example 1

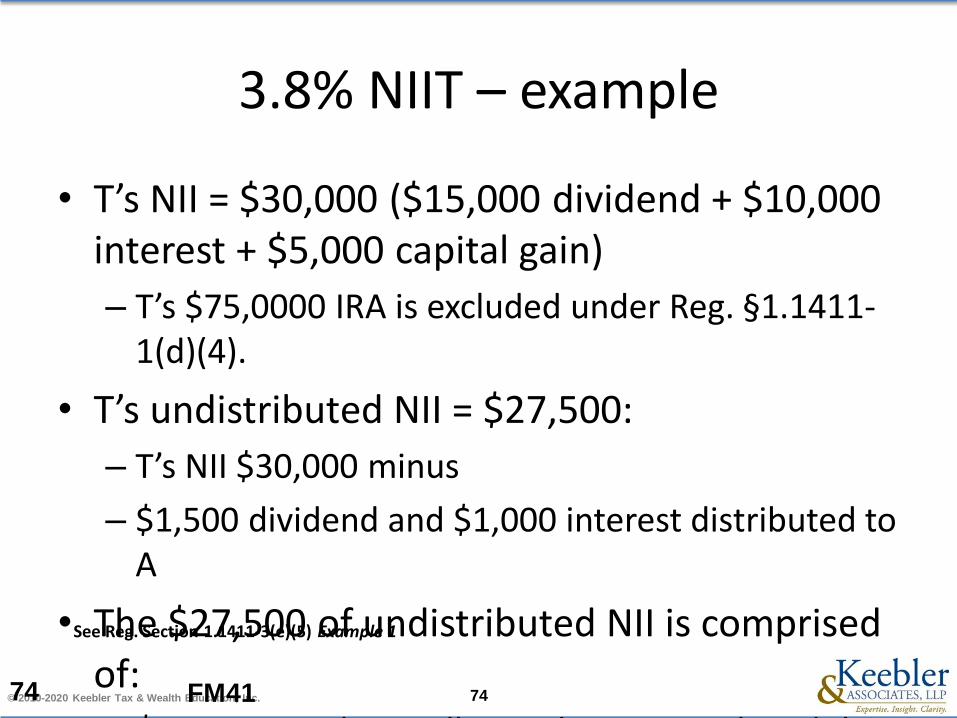

© 2010-2020 Keebler Tax & Wealth Education, Inc. 74

3.8% NIIT – example

• T’s NII = $30,000 ($15,000 dividend + $10,000 interest + $5,000 capital gain)

– T’s $75,0000 IRA is excluded under Reg. §1.1411-1(d)(4).

• T’s undistributed NII = $27,500:

– T’s NII $30,000 minus

– $1,500 dividend and $1,000 interest distributed to A

• The $27,500 of undistributed NII is comprised of:

– $5,000 capital gain allocated to principal, and the FM4174

See Reg. Section 1.1411-3(e)(5) Example 1

© 2010-2020 Keebler Tax & Wealth Education, Inc. 75

3.8% NIIT – example

• A’s NII includes:

– $1,500 of dividend income

– $1,000 of interest income

– Does NOT include $7,500 of ordinary income attributable to the IRA because it is excluded from NII under Reg. §1.1411-8

FM4175

See Reg. Section 1.1411-3(e)(5) Example 1

© 2010-2020 Keebler Tax & Wealth Education, Inc. 76

3.8% NIIT – exampleTrust

Income DNI

A’s share

of DNI

(10%)

Trust’s

total NII

A’s share

of NII

(10%)Trust’s UNII

Dividends $15,000 $15,000 $1,500 $15,000 $1,500 $13,500

Interest $10,000 $10,000 $1,000 $10,000 $3,000 $9,000

Capital gain $5,000 $5,000 $5,000

IRA $75,000 $75,000 $7,500

Total $105,000 $100,000 $10,000 $30,000 $2,500 $27,500

FM4176

Trust AGI:

Total income $ 105,000

Less: DNI ($10,000)

Less: exemption ( $100)

Trust AGI $94,900

Less: Threshold ($11,950)

$82,950

• 3.8% NIIT is $1,045

• NIIT applies to $27,500

Lesser of undistributed net investment income ($27,500) or AGI over $11,950 ($82,950)

is $27,500

*Thank you to Jeremiah W. Doyle, IV for preparing this slide.See Reg. Section 1.1411-3(e)(5) Example 1

© 2010-2020 Keebler Tax & Wealth Education, Inc. 77

3.8% NIIT – example:Form 8960 – part 1 & 2 (trust)

FM4177

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 78

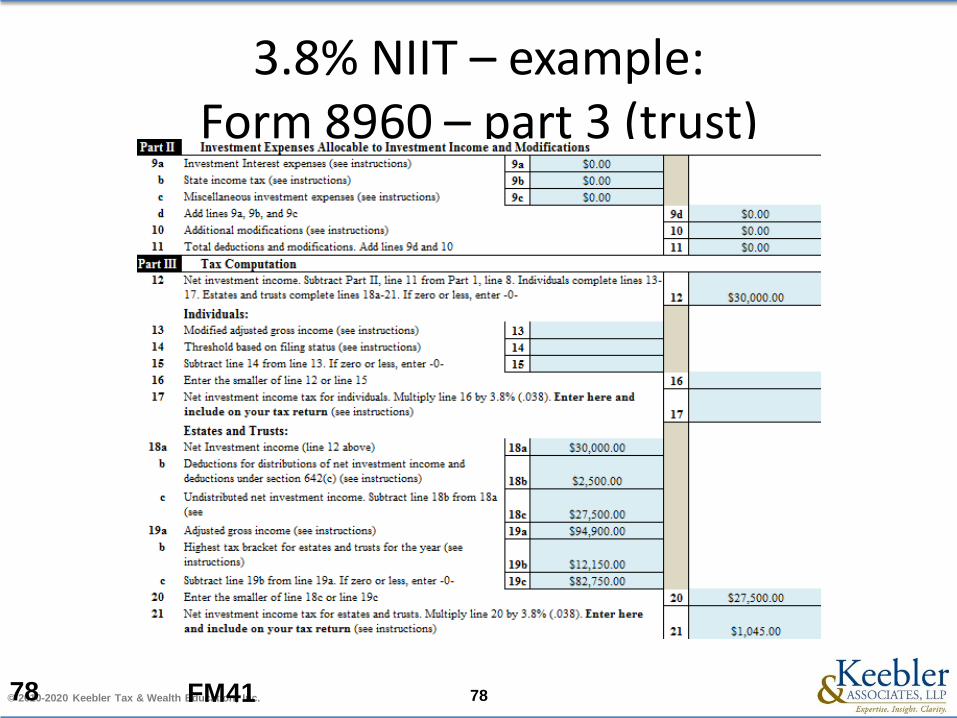

3.8% NIIT – example:Form 8960 – part 3 (trust)

FM4178

© 2010-2020 Keebler Tax & Wealth Education, Inc. 79

Example 20: Schedule K-1 (beneficiary)

FM4179

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 80

Example 20: Form 8960 – part 1 & 2 (beneficiary)

FM4180

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 81

Example 20: Form 8960 – part 3 (beneficiary)

FM4181

© 2010-2020 Keebler Tax & Wealth Education, Inc. 82

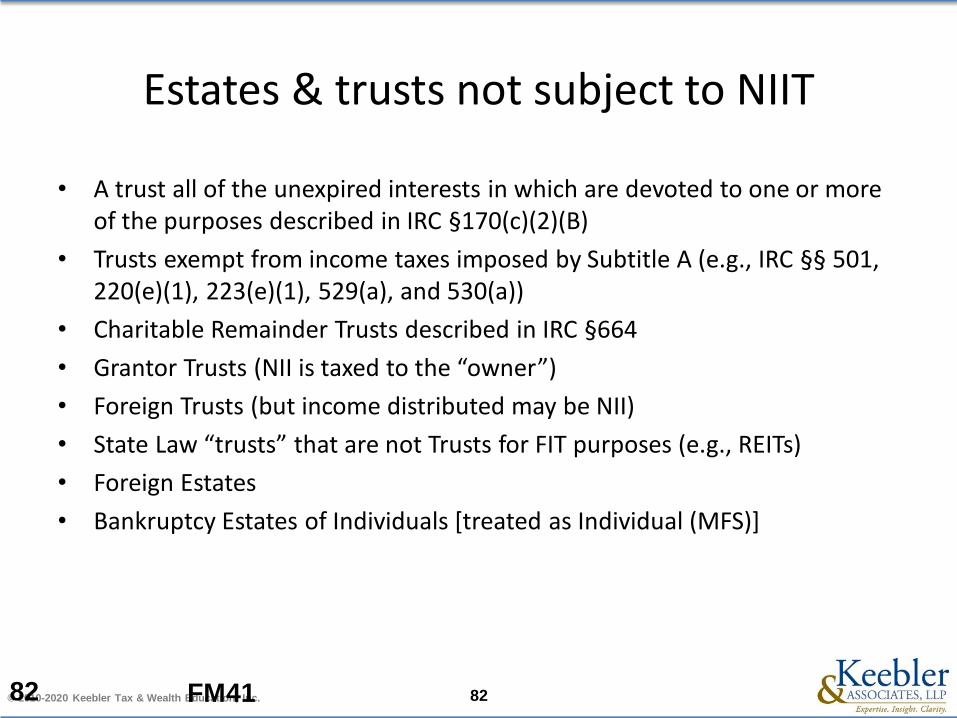

Estates & trusts not subject to NIIT

• A trust all of the unexpired interests in which are devoted to one or more of the purposes described in IRC §170(c)(2)(B)

• Trusts exempt from income taxes imposed by Subtitle A (e.g., IRC §§ 501, 220(e)(1), 223(e)(1), 529(a), and 530(a))

• Charitable Remainder Trusts described in IRC §664

• Grantor Trusts (NII is taxed to the “owner”)

• Foreign Trusts (but income distributed may be NII)

• State Law “trusts” that are not Trusts for FIT purposes (e.g., REITs)

• Foreign Estates

• Bankruptcy Estates of Individuals [treated as Individual (MFS)]

FM4182

© 2010-2020 Keebler Tax & Wealth Education, Inc. 83

Uncommon trusts subject to NIIT

• Section 1411 does apply to trusts subject to the provisions of part I of subchapter J, even though such trusts may have special computational rules within those provisions

• These trusts include:

– Pooled income funds [IRC §642(c)(5)],

– Cemetery perpetual care funds [IRC §642(i)],

– Qualified funeral trusts [IRC §685], and

– Alaska Native settlement trusts [IRC §646]

FM4183

© 2010-2020 Keebler Tax & Wealth Education, Inc. 84

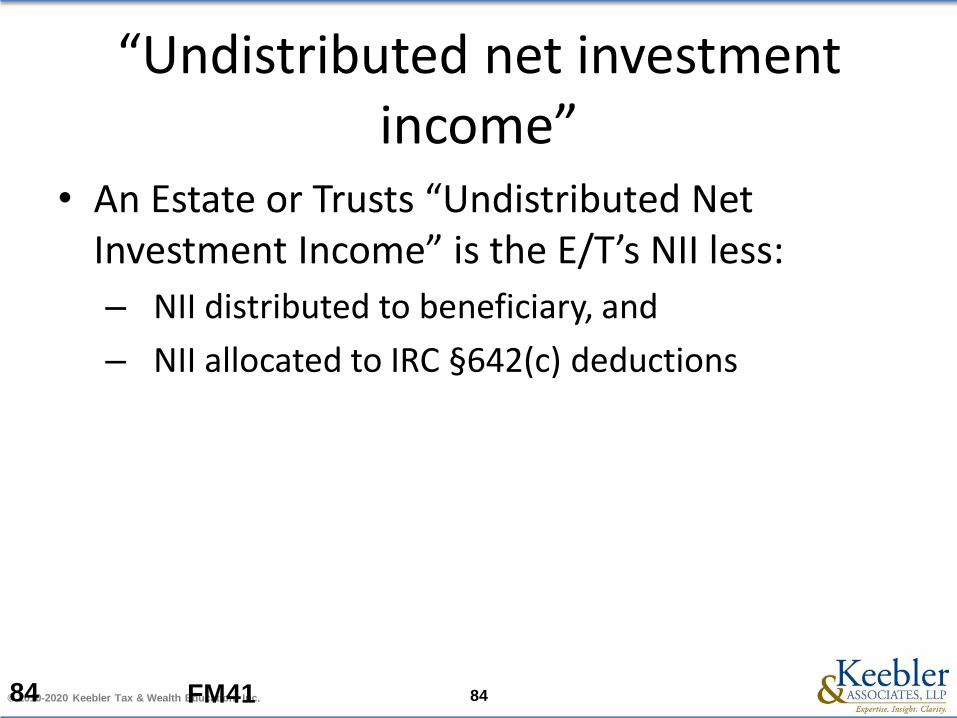

“Undistributed net investment income”

• An Estate or Trusts “Undistributed Net Investment Income” is the E/T’s NII less:

– NII distributed to beneficiary, and

– NII allocated to IRC §642(c) deductions

FM4184

© 2010-2020 Keebler Tax & Wealth Education, Inc. 85

“Undistributed net investment income”

• The NIIT rules were modeled after the rules in IRC 651-663

– The 651/661 Deduction may (or may not) be the same for NIIT as for Chapter 1 – it depends on the composition of the E/T’s income

– The total NII subject to tax is:

• E/T’s UNII, plus

• NII reportable by the beneficiary (from the Schedule K-1)

FM4185

© 2010-2020 Keebler Tax & Wealth Education, Inc. 86

GRANTOR TRUSTS

NOTE: A special thank you to Scott Schrader, Esq. of Miller & Schrader, P.A. for the use of the following slides regarding qualifying trusts for grantor status

© 2010-2020 Keebler Tax & Wealth Education, Inc. 87

Grantor trusts

• Grantor trusts were created to eliminate income tax abuses involving (then-lower) trusts brackets

• Grantor trust as to:

– Income

– Principal

– Both

• All trusts must be reviewed to determine grantor trust status

FM4187

© 2010-2020 Keebler Tax & Wealth Education, Inc. 88

Grantor trusts:benefits of utilizing a grantor trust

• Removal of highly-appreciating assets from taxable estate

• Payment of taxes on behalf of trust are not considered gifts for gift tax purposes

• Tax free distributions to trust beneficiaries

• Permissible transferee of life insurance policy outside of transfer for value rules

• Tax-free transfer of IRAs

FM4188

© 2010-2020 Keebler Tax & Wealth Education, Inc. 89

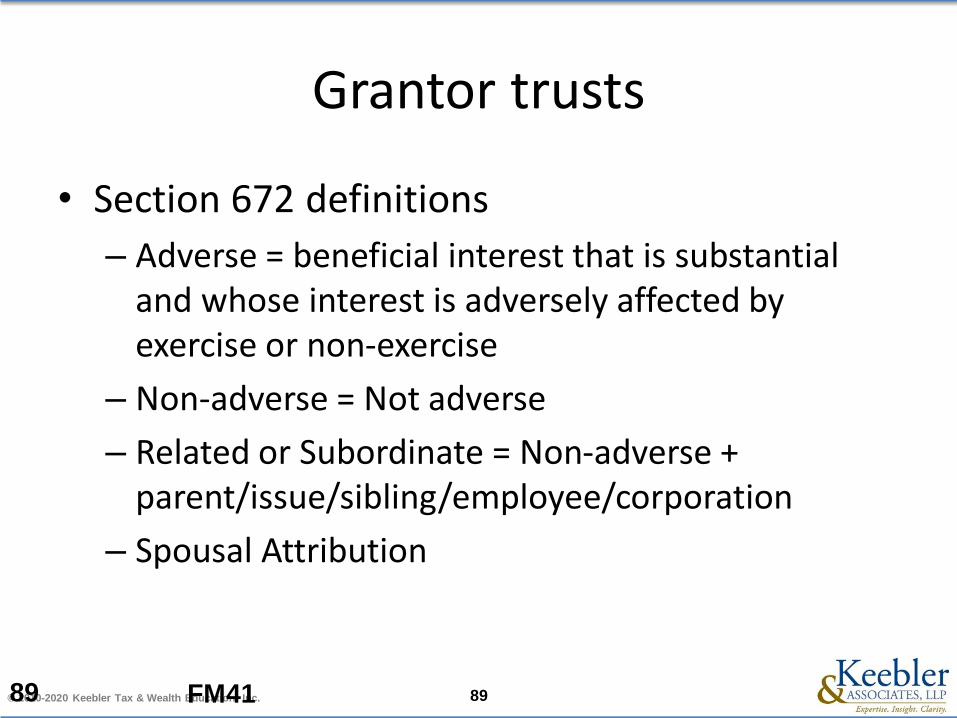

Grantor trusts

• Section 672 definitions

– Adverse = beneficial interest that is substantial and whose interest is adversely affected by exercise or non-exercise

– Non-adverse = Not adverse

– Related or Subordinate = Non-adverse + parent/issue/sibling/employee/corporation

– Spousal Attribution

FM4189

© 2010-2020 Keebler Tax & Wealth Education, Inc. 90

Grantor trusts

• Section 674 Power to Affect Beneficial Enjoyment

– Grantor is treated as owner of any portion of the trust over which grantor controls beneficial enjoyment or corpus or income, exercisable by grantor or non-adverse party or both, without the consent of any adverse party [674(a)]

– Powers found in 674(b) will never cause grantor trust status

– 674(c) – power to distribute income or principal, or to add beneficiariesFM4190

© 2010-2020 Keebler Tax & Wealth Education, Inc. 91

Grantor trusts

• Section 674 Power to Affect Beneficial Enjoyment

– 674(d) – Power to allocate income

• Power granted to someone other than grantor or “spouse living with grantor” to distribute, apportion or accumulate income to or for beneficiaries if limited by reasonably definite external standard

• Power creates grantor trust as to income only

• Possible to switch grantor trust status on and off merely by spouse moving out and back in?

FM4191

© 2010-2020 Keebler Tax & Wealth Education, Inc. 92

Grantor trusts

• Section 675 Administrative Powers

– 675(2) – Power given to nonadverse party to make loans to grantor without adequate interest or security

– N/A if trustee has authority to make loans to anyone without regard to interest or security

– Power alone will cause grantor trust status, even if no loan is made (PLR 199942017, 9645013)

FM4192

© 2010-2020 Keebler Tax & Wealth Education, Inc. 93

Grantor trusts

• Section 675 Administrative Powers

– 675(3) – Actual borrowing of funds

• Direct or indirect loan to grantor or grantor’s spouse which is unrepaid at the end of year

• N/A to loans with adequate interest and security

• Creates grantor trust to extent amounts are unrepaid at year end, but ...

• IRS has apparently ignored requirement that loan remain outstanding until year end

FM4193

© 2010-2020 Keebler Tax & Wealth Education, Inc. 94

Grantor trusts

• Section 675 Administrative Powers

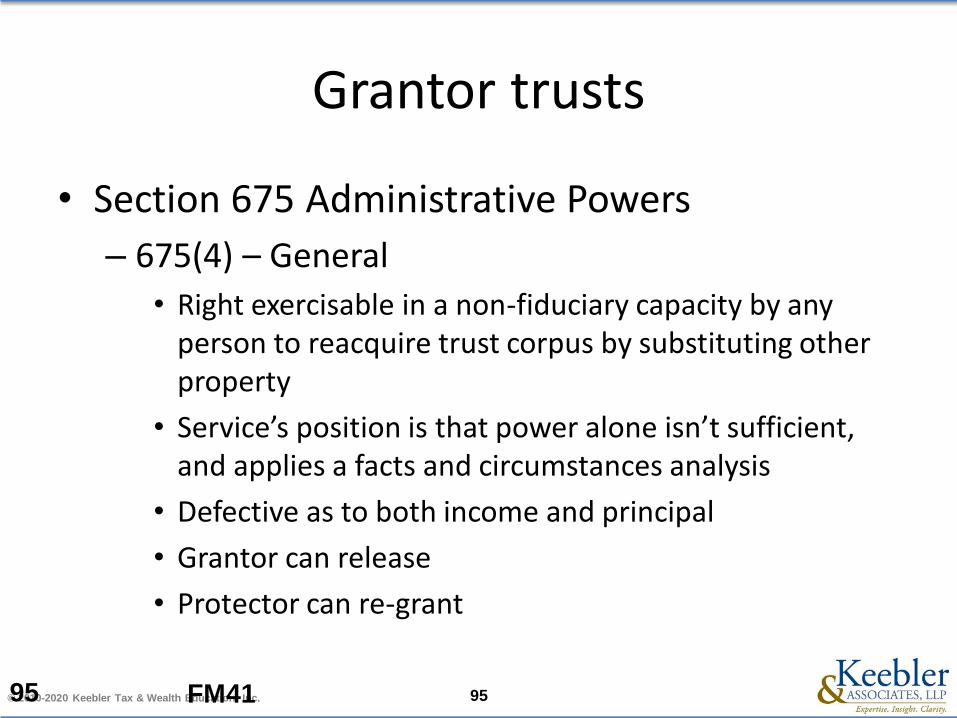

– 675(4) – General

• Right exercisable in a non-fiduciary capacity by any person to reacquire trust corpus by substituting other property

FM4194

© 2010-2020 Keebler Tax & Wealth Education, Inc. 95

Grantor trusts

• Section 675 Administrative Powers

– 675(4) – General

• Right exercisable in a non-fiduciary capacity by any person to reacquire trust corpus by substituting other property

• Service’s position is that power alone isn’t sufficient, and applies a facts and circumstances analysis

• Defective as to both income and principal

• Grantor can release

• Protector can re-grant

FM4195

© 2010-2020 Keebler Tax & Wealth Education, Inc. 96

Grantor trusts

• Section 677 Power to Use Income for Benefit of Grantor

– Grantor treated as owner of any portion of trust, whether or not under §674, the income of which, without the approval or consent of adverse party is, or in discretion of grantor or nonadverse party may be, distributed to or for benefit of grantor or spouse

– Or used to pay premiums on life insurance on the life of grantor or spouse

FM4196

© 2010-2020 Keebler Tax & Wealth Education, Inc. 97

Grantor trusts

• Section 677 Power to Use Income for Benefit of Grantor

– Trust should disallow use of income to satisfy obligation of support

– Discretionary power to pay income to grantor may cause inclusion under state law

– Some states have changed their laws to not cause inclusion (Alaska, Delaware, and others)

FM4197

© 2010-2020 Keebler Tax & Wealth Education, Inc. 98

Grantor trusts

• Section 678 Persons other than Grantor Treated as Owner

– Only code section attributing ownership to someone other than the actual grantor

– Power to vest corpus or income exercisable solely by that person

• Surviving spouse as sole trustee of bypass trust?

• Limitation to ascertainable standard (HEMS) prevents estate tax inclusion

• Switch on/off grantor trust status by appointing/firing co-trusteeFM4198

© 2010-2020 Keebler Tax & Wealth Education, Inc. 99

Grantor trusts

• Section 678 Persons other than Grantor Treated as Owner

– N/A with respect to power over “income” during any period actual grantor is treated as owner under §§617-677

– Service has interpreted §678(b) as applying to principal as well as income

• PLRs 9309023, 8701007, 8326074, 8308033, 8142061

FM4199

© 2010-2020 Keebler Tax & Wealth Education, Inc. 100

Grantor trusts

• Section 678 Persons other than Grantor Treated as Owner

– Power to distribute income or principal which is “partially released or otherwise modified” that would cause grantor trust status under 671-677

• 5/5 power holder, until released, modified, or allowed to lapse, is treated as grantor over portion of trust subject to power

• Upon lapse, power holder is treated as grantor of amount in excess of 5/5

• Rev. Rul. 67-241 and PLR 200022035

FM41100

© 2010-2020 Keebler Tax & Wealth Education, Inc. 101

Grantor trusts

• Section 678 Persons other than Grantor Treated as Owner

– Power to distribute income or principal which is “partially released or otherwise modified” that would cause grantor trust status under 671-677

FM41101

© 2010-2020 Keebler Tax & Wealth Education, Inc. 102

Grantor trusts

• Terminating grantor status

– Maintain flexibility

– Power to terminate grantor trust status should not be in hands of grantor

– Tax issues upon termination

FM41102

© 2010-2020 Keebler Tax & Wealth Education, Inc. 103

CHARITABLE REMAINDER TRUSTS (CRTS)

© 2010-2020 Keebler Tax & Wealth Education, Inc. 104

Charitable remainder trusts

A Charitable Remainder Trust (CRT) is a split interest trust consisting of an income interest and a remainder interest. During the term of the trust, the income interest is paid out to the beneficiaries which could be grantor, the grantor’s spouse and/or other individuals. At the end of the trust term, the remainder (whatever is left in the trust) is paid to the charity or charities the grantor has designated.

FM41104

© 2010-2020 Keebler Tax & Wealth Education, Inc. 105

Charitable remainder trusts:tax aspects – distributions

• The character of income received by the recipient is subject to and controlled by the tier rules of IRC §664(b)

– First, distributions are taxed as ordinary income

– Second, distributions are taxed as capital gains

– Third, distributions are taxed as tax-exempt income (e.g. municipal bond income)

– Finally, distributions are assumed to be the non-taxable return of principal

FM41105

© 2010-2020 Keebler Tax & Wealth Education, Inc. 106

OrdinaryIncome

Capital GainIncome

Tax-ExemptIncome Principal

Tier 1 Tier 2 Tier 3 Tier 4

STEP 1:

Current Ordinary Income

STEP 2:

Accumulated Ordinary Income

STEP 4:

Accumulated Capital Gains

STEP 3:

Current Capital Gains

STEP 5:

Current Tax-Exempt

Income

STEP 6:

Accumulated Tax-Exempt

Income

STEP 7:

Return of Capital

Charitable remainder trusts:tax aspects – distributions

FM41106

© 2010-2020 Keebler Tax & Wealth Education, Inc. 107

Charitable remainder trusts:example

Mr. & Mrs. Smith (both age 55) established a lifetime Charitable Remainder Unitrust (CRUT) in July 2019 by contributing $300,000 of XYZ Corp. stock (with a $100,000 basis). When the CRUT was funded, it was determined that it would have an annual payout percentage of 7% based on the balance of the trust assets at the beginning of each year.

FM41107

© 2010-2020 Keebler Tax & Wealth Education, Inc. 108

Charitable remainder trusts:example

As of the end of 2019, the trust the following sources of income:

Interest income – Current (Tier 1) $4,000

Interest income – Accumulated (Tier 1) 1,000

Capital gains – Current (Tier 2) 5,000

Capital gains – Accumulated (Tier 2) 185,000

FM41108

© 2010-2020 Keebler Tax & Wealth Education, Inc. 109

Assuming a $25,000 distribution for 2020, the CRUT distribution would comprise of the following sources of income:

Interest income – Current (Tier 1) $4,000

Interest income – Accumulated (Tier 1) 1,000

Capital gains – Current (Tier 2) 5,000

Capital gains – Accumulated (Tier 2) 15,000

TOTAL DISTRIBUTION $25,000

Charitable remainder trusts:example

FM41109

© 2010-2020 Keebler Tax & Wealth Education, Inc. 110

Charitable remainder trusts:example

FM41110

© 2010-2020 Keebler Tax & Wealth Education, Inc. 111

Charitable remainder trusts:example

FM41111

© 2010-2020 Keebler Tax & Wealth Education, Inc. 112

Shifting Income with Trust Distributions

© 2010-2020 Keebler Tax & Wealth Education, Inc. 113

Shifting income with trust distributions:

2019 ordinary income tax rates for individuals

FM41113

© 2010-2020 Keebler Tax & Wealth Education, Inc. 114

Shifting income with trust distributions:

2019 ordinary income tax rates for estates & trusts

FM41114

© 2010-2020 Keebler Tax & Wealth Education, Inc. 115

Foundational concepts:2020 ordinary income tax rates for individuals

FM41115

© 2010-2020 Keebler Tax & Wealth Education, Inc. 116

Foundational concepts:2020 ordinary income tax rates for estates & trusts

FM41116

© 2010-2020 Keebler Tax & Wealth Education, Inc. 117

Shifting capital gains to beneficiaries:IRC Section 643 regulations

• Generally, IRC § 643 excludes capital gains from DNI

• However, Reg. § 1.643(a)-3(b) provides that capital gains can be included in DNI pursuant to the trust document or state law

• Therefore, provided it is allowed by the trust document or state law, the tax advisor, with the consent of the trustee, can elect to include capital gains in DNI

FM41117

© 2010-2020 Keebler Tax & Wealth Education, Inc. 118

Shifting capital gains to beneficiaries:example of an effective shift

• A trust realizes $100,000 of capital gains

• If undistributed, the gain is subject to a marginal rate of 23.8%

• However, the marginal long-term capital gain rate of the sole beneficiary of the trust is 15%

• The trustee takes no issue with tax advisor’s suggestion to elect to treat the capital gains as DNI

• The trust distributes the gain, receives an income tax deduction of $100,000 and saves $23,800 in tax

FM41118

© 2010-2020 Keebler Tax & Wealth Education, Inc. 119

Shifting capital gains to beneficiaries:example of an ineffective shift

• A dynasty trust realizes $100,000 of capital gains

• If undistributed, the gain is subject to a marginal rate of 23.8%

• The marginal rate of the current beneficiary of the trust is 18.8%

• By distributing the gain, $5,000 in tax is saved

• However, the trust also has a contingent beneficiary in a younger generation

• Note that if the distribution increases the FM4111

9

© 2010-2020 Keebler Tax & Wealth Education, Inc. 120

Shifting capital gains to beneficiaries:IRC Section 643(e)

• IRC § 643(e) provides that property distributed in-kind from a trust to a beneficiary retains the trust’s cost basis

• Therefore, if the trust allows for the distribution of principal, the tax advisor with the consent of the trustee can distribute appreciated property to beneficiaries with low tax rates

FM41120

© 2010-2020 Keebler Tax & Wealth Education, Inc. 121

Shifting capital gains to beneficiaries:§643(e) example

• Trust makes an in-kind distribution of stock with a FMV of $100,000 and a cost basis of $40,000

• The beneficiary sells the stock upon receipt and recognizes the gain

• The same effect and benefit of characterizing capital gains as DNI is realized

• However, the trust’s income tax is not effected

FM41121

© 2010-2020 Keebler Tax & Wealth Education, Inc. 122

LIMIT ON MISCELLANEOUS DEDUCTIONS

© 2010-2020 Keebler Tax & Wealth Education, Inc. 123

Limit on miscellaneous deductions

• The Tax Cuts and Jobs Act suspended Miscellaneous Itemized Deductions. IRC §67(g)

• Deductions allowed under IRC §67(e) for trusts and estates remain available

FM41123

© 2010-2020 Keebler Tax & Wealth Education, Inc. 124

Limit on miscellaneous deductions

• AGI of a trust is adjusted for:

– “[T]he deductions for costs which are paid or incurred in connection with the administration of the estate or trust and which would not have been incurred if the property were not held in such trust or estate.” §67(e)(1):

– Personal exemption ($100, $300, or $600). §§67(e)(2), 642(b)

– Distributions to beneficiaries. §§ 67(e)(2), 651, 661

FM41124

© 2010-2020 Keebler Tax & Wealth Education, Inc. 125

Limit on miscellaneous deductions

• Section 67(e)(1): allows a direct reduction to a trust’s AGI for expenses not “commonly” or “customarily” incurred by an individual holding the same property

• Reg §1.67-4: applies to taxable years beginning after December 31st 2014, provides examples of such investment expenses

FM41125

© 2010-2020 Keebler Tax & Wealth Education, Inc. 126

Limit on miscellaneous deductions

Reg §1.67-4(3): 1041 preparation fees are not deductible; whereas 1040 or 709 preparation fees are not because such fees are typically incurred by individuals

FM41126

© 2010-2020 Keebler Tax & Wealth Education, Inc. 127

Limit on miscellaneous deductions

Reg §1.67-4(4): certain investment advisory fees beyond the amount normally chargeable to an individual, are deductible

FM41127

© 2010-2020 Keebler Tax & Wealth Education, Inc. 128

Limit on miscellaneous deductions

Reg §1.67-4(5): certain appraisal fees to determine the FMV of assets at death (or another valuation date), make distributions, or prepare tax returns

FM41128

© 2010-2020 Keebler Tax & Wealth Education, Inc. 129

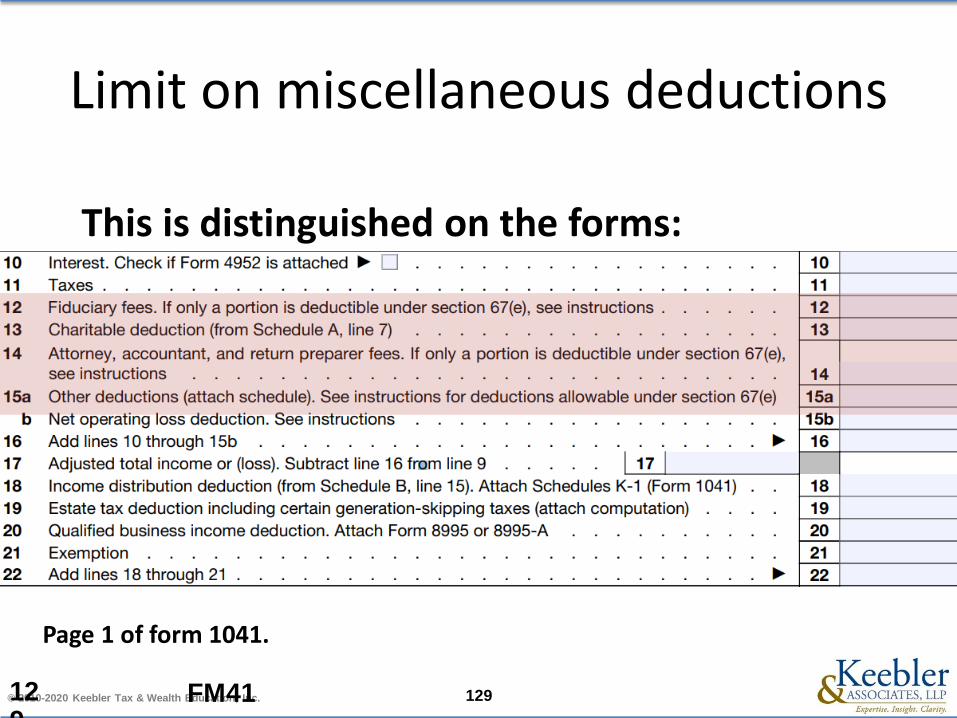

Limit on miscellaneous deductions

This is distinguished on the forms:

FM41129

Page 1 of form 1041.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 130

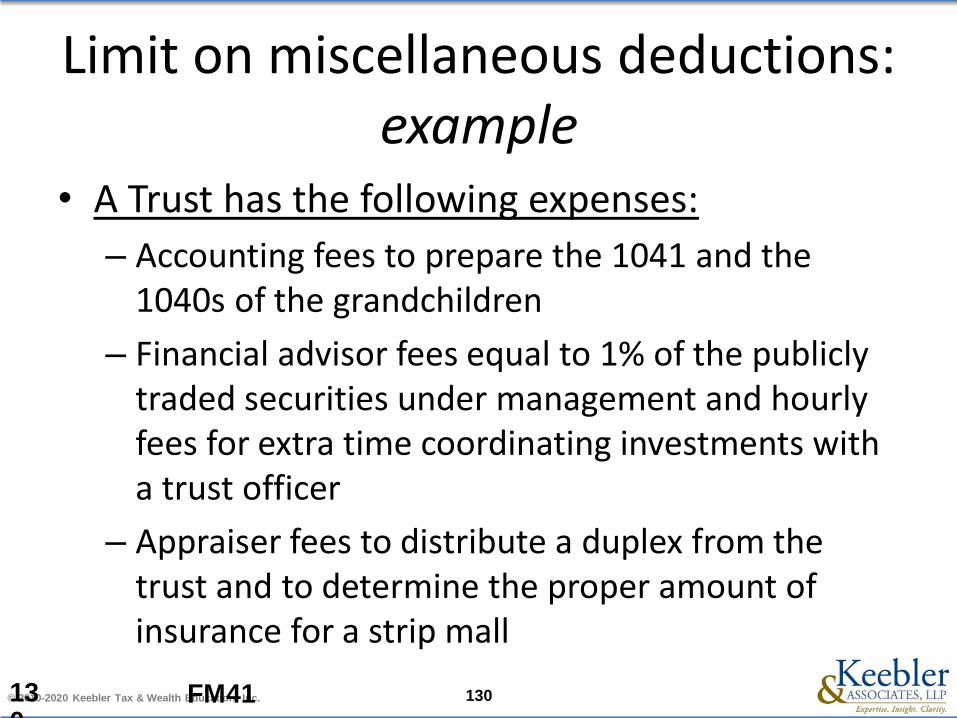

Limit on miscellaneous deductions: example

• A Trust has the following expenses:

– Accounting fees to prepare the 1041 and the 1040s of the grandchildren

– Financial advisor fees equal to 1% of the publicly traded securities under management and hourly fees for extra time coordinating investments with a trust officer

– Appraiser fees to distribute a duplex from the trust and to determine the proper amount of insurance for a strip mall

FM41130

© 2010-2020 Keebler Tax & Wealth Education, Inc. 131

Limit on miscellaneous deductions: example

• Accounting fees:

– The 1041 preparation fees are deductible by the trust

– The 1040 preparation fees are not deducible by the trust as an accounting fee

FM41131

© 2010-2020 Keebler Tax & Wealth Education, Inc. 132

Limit on miscellaneous deductions: example

• Financial advisor fees:

– The 1% fee is equal to the amount the advisor charges to individuals and therefore is generally not deductible

– The hourly fees to coordinate investments with the trust officer are fees which are not normally chargeable to an individual and therefore may be deductible

FM41132

© 2010-2020 Keebler Tax & Wealth Education, Inc. 133

Limit on miscellaneous deductions: example

• Real estate appraisal fees:

– The fees to appraise property in order to distribute it are deductible

– However, the fees to appraise property in order to insure it may not be

• The real estate appraisal fee distinction portion of the example was created by following an example in Internal Revenue Bulletin 2014-22

FM41133

© 2010-2020 Keebler Tax & Wealth Education, Inc. 134

Limit on miscellaneous deductions: investment expenses

• Investment expenses are a miscellaneous deduction, which in general was repealed by the Tax Cuts and Jobs Act

FM41134

© 2010-2020 Keebler Tax & Wealth Education, Inc. 135

Limit on miscellaneous deductions: investment expenses

• The term “investment expenses” means the deductions allowed under this chapter (other than for interest) which are directly connected with the production of investment income

• Section 163(d)(4)(C)

FM41135

© 2010-2020 Keebler Tax & Wealth Education, Inc. 136

Limit on miscellaneous deductions: investment expenses

• Are ordinary & necessary expenses to produce or collect income, or to manage property held for producing income

• Include: attorney/accounting fees, automatic reinvestment fees, clerical help & office rent, fees to collect income, fees to buy/sell, investment advisory services, etc.

• Pub. 550 (2013)

FM41136

© 2010-2020 Keebler Tax & Wealth Education, Inc. 137

STATE INCOME TAX PLANNING FOR TRUSTS AND BENEFICIARIES

© 2010-2020 Keebler Tax & Wealth Education, Inc. 138

Shifting income with trust situs:potential state tax savings

FM41138

2020 top individual marginal rate of each state.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 139

Types of trusts: in general

• Inter vivos

• Testamentary

• Trust under a revocable trust

FM41139

© 2010-2020 Keebler Tax & Wealth Education, Inc. 140

Types of trusts: for gift tax purposes

• Completed gifts

• Incomplete gifts

FM41140

© 2010-2020 Keebler Tax & Wealth Education, Inc. 141

ING trusts: overview

Taxpayers in high tax states should consider transferring assets to a trust in a state that does not tax trust income to avoid income tax in their home state

FM41141

Taxpayer(High Tax State)

Trust(No Tax State)

Transfer Assets

Tax Savings

© 2010-2020 Keebler Tax & Wealth Education, Inc. 142

ING trusts:strategy – 5 requirements

1. The trust must be created in a state that does not tax trust income

– Seven states don’t tax trust income: Alaska, Florida, Nevada, South Dakota, Texas, Washington and Wyoming

– Although there may be other states that won’t tax trust income, depending on their resident trust statutes, locating the trust in a no-tax state is the easiest and surest way to meet the first requirement

FM41142

© 2010-2020 Keebler Tax & Wealth Education, Inc. 143

ING trusts:strategy – 5 requirements

2. The income from the trust must not be taxable by the grantor’s home state

– Locating the trust in one of the states listed above doesn’t necessarily mean that the trust income will not be taxed by the grantor’s home state

– Most states tax all income of a resident trust but only the state source income of a non-resident trust

– The definition of a resident trust varies from state to state and could include trusts created in other states FM4114

3

© 2010-2020 Keebler Tax & Wealth Education, Inc. 144

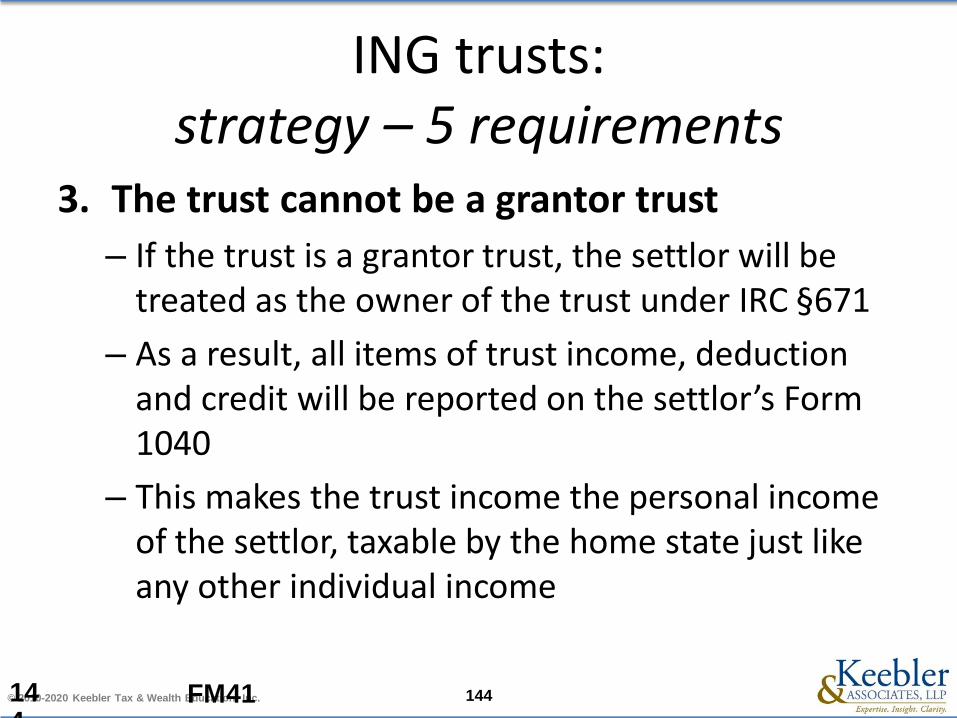

ING trusts:strategy – 5 requirements

3. The trust cannot be a grantor trust

– If the trust is a grantor trust, the settlor will be treated as the owner of the trust under IRC §671

– As a result, all items of trust income, deduction and credit will be reported on the settlor’s Form 1040

– This makes the trust income the personal income of the settlor, taxable by the home state just like any other individual income

FM41144

© 2010-2020 Keebler Tax & Wealth Education, Inc. 145

ING trusts:strategy – 5 requirements

4. The trust must allow discretionary distributions to the settlor

– Taxpayers are typically unwilling to make an outright transfer of their investment assets

– They either want income distributions or the possibility of reacquiring principal if they need it

– Thus, the trustee must be given the power to make discretionary distributions to the settlor

– However, this must be accomplished without making the trust a grantor trust

FM41145

© 2010-2020 Keebler Tax & Wealth Education, Inc. 146

ING trusts:strategy – 5 requirements

5. Transfers to the Trust must be Incomplete Gifts

– Finally, the settlor must retain enough control over the transferred assets to avoid making a completed gift that is subject to the gift tax

– This must also be done without making the trust a grantor trust

FM41146

© 2010-2020 Keebler Tax & Wealth Education, Inc. 147

ING trusts:income & gift tax liability

PLR 201310002 confirmed that a Nevada incomplete gift, non-grantor trust met all the requirements listed above for creating a trust that avoids state income tax, making it a great jurisdiction for setting up a state income tax saving trust, at least for the time being. Such trusts are referred to as Nevada Incomplete Gift, Non-Grantor Trusts, or NINGs.

FM41147

© 2010-2020 Keebler Tax & Wealth Education, Inc. 148

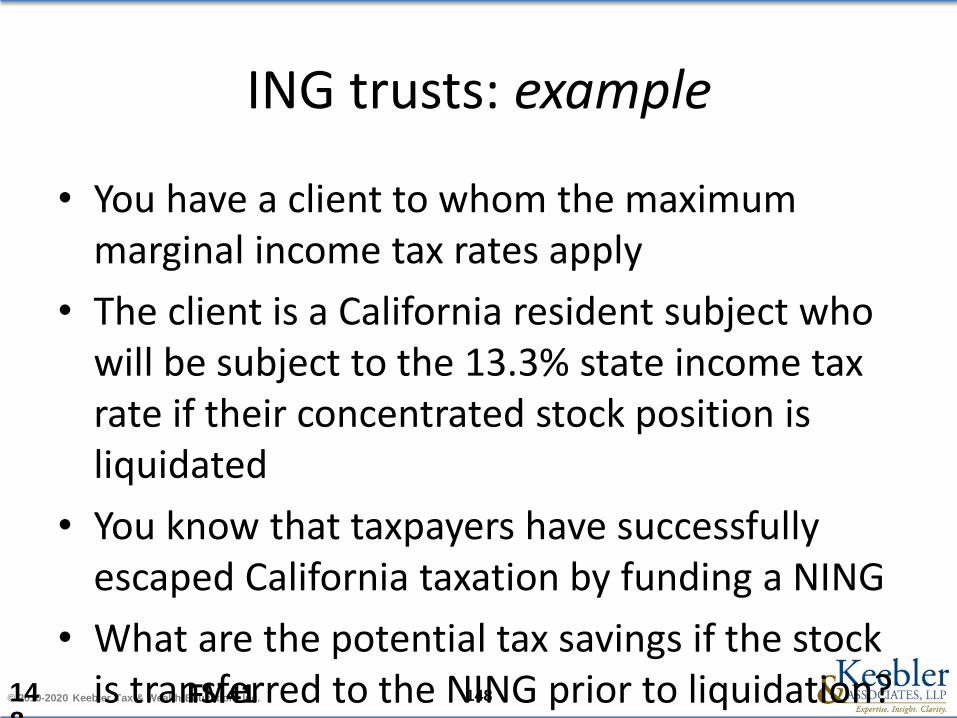

ING trusts: example

• You have a client to whom the maximum marginal income tax rates apply

• The client is a California resident subject who will be subject to the 13.3% state income tax rate if their concentrated stock position is liquidated

• You know that taxpayers have successfully escaped California taxation by funding a NING

• What are the potential tax savings if the stock is transferred to the NING prior to liquidation?FM4114

8

© 2010-2020 Keebler Tax & Wealth Education, Inc. 149

ING trusts: example

• The stock has the following tax characteristics:

– FMV = $4,000,000

– Basis = $ 0

• Following liquidation, the client wants to invest in a balanced portfolio:

– FMV = $4,000,000

– Basis = $ 0

FM41149

© 2010-2020 Keebler Tax & Wealth Education, Inc. 150

ING trusts: example

FM41150

© 2010-2020 Keebler Tax & Wealth Education, Inc. 151

States that do not impose income tax on trusts

FM41151

*

© 2010-2020 Keebler Tax & Wealth Education, Inc. 152

Inter vivos trust created by a resident

FM41152

States which tax such trusts

Map based on the 2013 work ofRichard W. Nenno of the

Wilmington Trust Company.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 153

Trust created by will of resident

FM41153

States which tax such trusts

Map based on the 2013 work ofRichard W. Nenno of the

Wilmington Trust Company.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 154

Trust administered in state

FM41154

States which tax such trusts

*

Map based on the 2013 work ofRichard W. Nenno of the

Wilmington Trust Company.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 155

Resident non-contingent beneficiary

FM41155

States which tax such trusts

Map based on the 2013 work ofRichard W. Nenno of the

Wilmington Trust Company.

© 2010-2020 Keebler Tax & Wealth Education, Inc. 156

Map based on the 2013 work ofRichard W. Nenno of the

Wilmington Trust Company.

FM41156

Resident trustee

States which tax such trusts

© 2010-2020 Keebler Tax & Wealth Education, Inc. 157

States that impose income tax BUT not on an inter vivos trust created by a resident

Clients from the states in blue might be able to fund a NING to avoid state income tax.

FM41157

© 2010-2020 Keebler Tax & Wealth Education, Inc. 158

Form 1041 Examples

© 2010-2020 Keebler Tax & Wealth Education, Inc. 159

Example #1 – simple trust

• $5,000 interest income

• $10,000 dividend income (100% qualified dividends)

• $1,500 attorney and accountant fees

• Trust requires all income to be passed out to spouse no less than annually (i.e. a “simple trust”)

FM41159

© 2010-2020 Keebler Tax & Wealth Education, Inc. 160FM41160

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 161FM41161

© 2010-2020 Keebler Tax & Wealth Education, Inc. 162

Example #2 – complex trust

• $15,000 interest income

• $1,500 attorney and accountant fees

• Trustee is given discretion each year as to how much income and principal to

• pass to the trust beneficiaries (i.e. “complex trust”)

• Trustee distributes $5,000 each to two beneficiaries ($10,000 total distribution)

FM41162

© 2010-2020 Keebler Tax & Wealth Education, Inc. 163FM41163

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 164FM41164

© 2010-2020 Keebler Tax & Wealth Education, Inc. 165

Example #3 – complex trust with tax-exempt interest income

• $10,000 dividend income (100% qualified dividends)• $5,000 tax-exempt interest income• $1,500 attorney and accountant fees• Trustee is given discretion each year as to how much income and principal to pass

to the trust beneficiaries (i.e. “complex trust”)• No distributions

Tax-exempt interest income $5,000Dividend income (100% qualified) 10,000Total income $15,000

% Income Tax-Exempt 33.33%

Total attorney & accountant fees $1,500Less: Portion allocable to tax-exempt income - 500Deductible attorney & accountant fees $1,000

FM41165

© 2010-2020 Keebler Tax & Wealth Education, Inc. 166FM41166

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 167FM41167

© 2010-2020 Keebler Tax & Wealth Education, Inc. 168

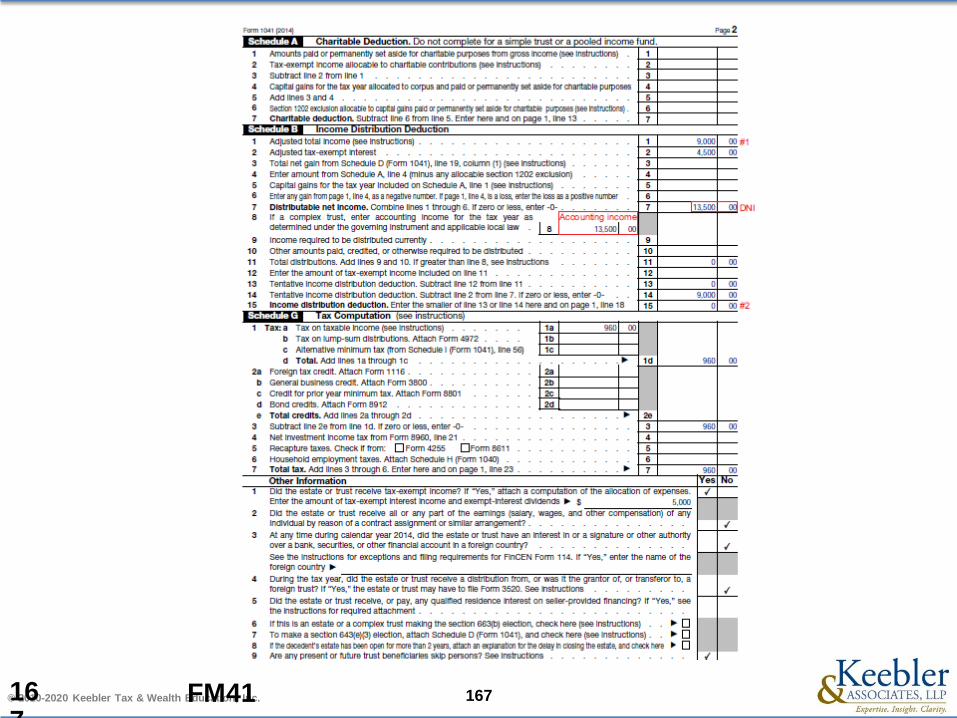

Example #4 – estate combined with revocable trust

• Decedent died on 2/3/2014• Estate electing fiscal year end (i.e. 1/31/2015)• Estate and decedent’s revocable living trust opt to file joint return

(i.e. IRC §645 election)• $5,000 interest income• $10,000 dividend income (100% qualified dividends)• $1,500 attorney and accountant fees• $1,000 executor fees• $2,500 other administrative expenses (not subject to 2% phase-out)• Expenses not being claimed on IRS Form 706 (i.e. IRC §642(g)

election)• $20,000 distribution to three beneficiaries

FM41168

© 2010-2020 Keebler Tax & Wealth Education, Inc. 169FM41169

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 170FM41170

© 2010-2020 Keebler Tax & Wealth Education, Inc. 171FM41171

© 2010-2020 Keebler Tax & Wealth Education, Inc. 172FM41172

© 2010-2020 Keebler Tax & Wealth Education, Inc. 173FM41173

© 2010-2020 Keebler Tax & Wealth Education, Inc. 174

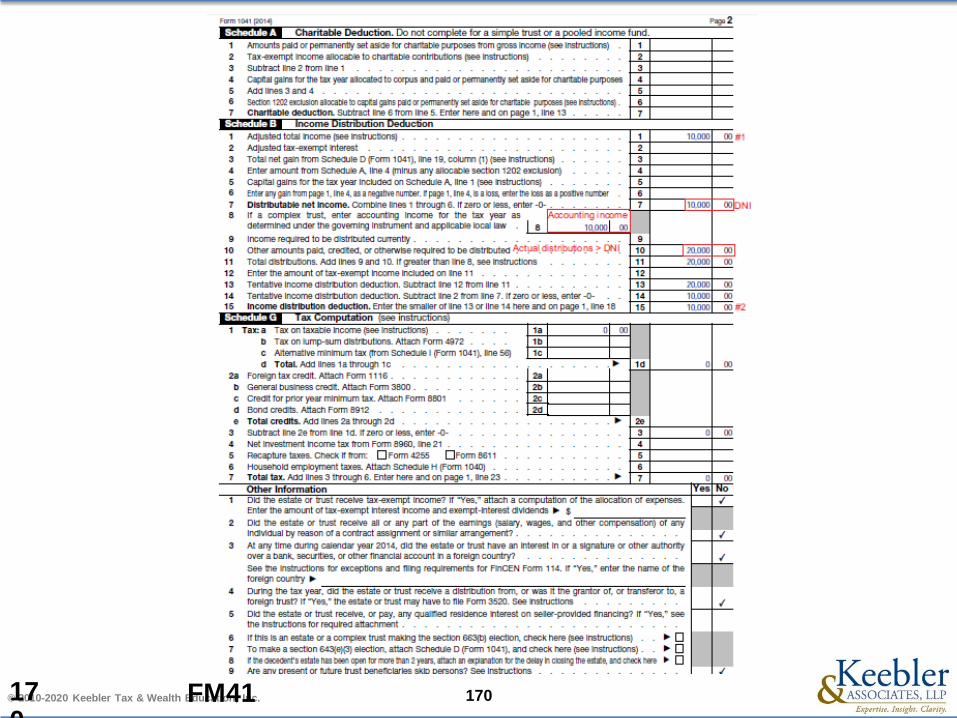

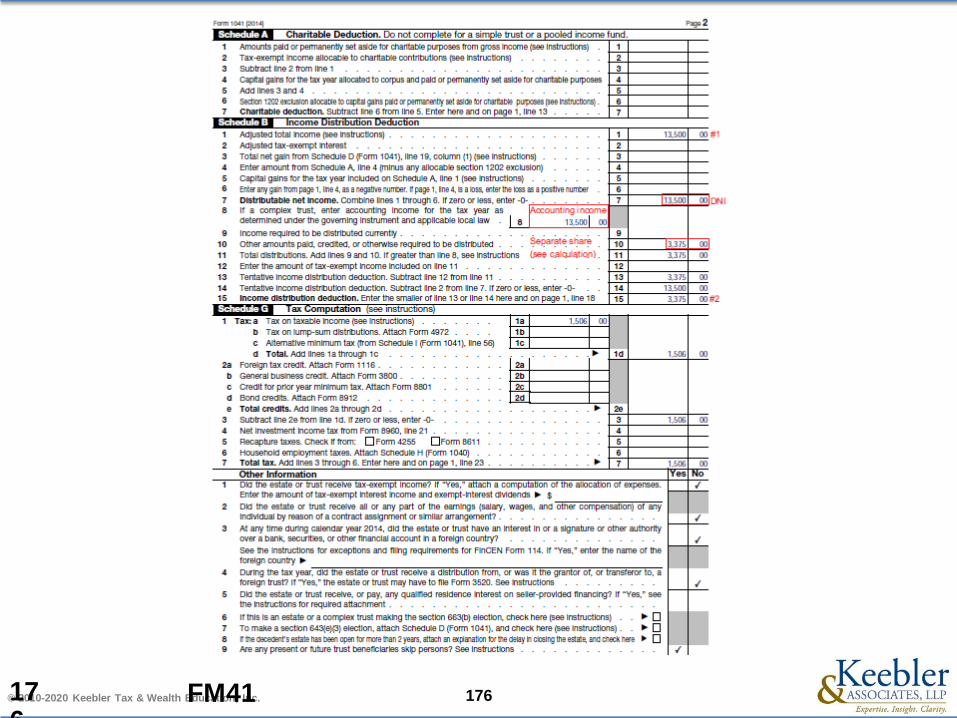

Example #5 – complex trust with separate shares

• $5,000 interest income• $10,000 dividend income (100% qualified dividends)• $1,500 attorney and accountant fees• Trustee is given discretion each year as to how much

income and principal to pass to the trust beneficiaries (i.e. “complex trust”)

• The trust instrument provides that each beneficiary’s share is to be held in a separate sub-trust (i.e. “separate share” treatment)

• Trustee makes a $10,000 distribution to one beneficiary, while the other three

• beneficiaries receive no distributions

FM41174

© 2010-2020 Keebler Tax & Wealth Education, Inc. 175FM41175

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 176FM41176

© 2010-2020 Keebler Tax & Wealth Education, Inc. 177FM41177

20XX

© 2010-2020 Keebler Tax & Wealth Education, Inc. 178

Q&A

We will now answer viewer questions that have come in during the webinar.

FM41178

© 2010-2020 Keebler Tax & Wealth Education, Inc. 179

Thank you!Individuals, CPE certificates will be available in your Surgent profile within 24 hours.

Groups, please scan and submit the attendance form to [email protected] for CPE certificates.