taxation & trusts - expert pensions

TRANSCRIPT

Taxation & TrustsEssential Study Notes

Essential Study Notes

1Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Essential Study NotesTax Year 2018/19

Modules:

1. Income Tax2. National Insurance Contributions (NIC) and Capital Gains Tax (CGT)3. Inheritance Tax (IHT)4. Residence, Domicile, UK Tax Compliance and other Taxes5. Investment Taxation6. Trusts7. Power of Attorney and Bankruptcy8. Wills and Intestacy9. Taxation of Trusts

10. Financial Planning and Trusts

Essential Study Notes

2Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Income Tax .......................................................................................................................... 4Sources of Income............................................................................................................. 5Reliefs, Allowances, Reducers and Credits ....................................................................... 8Taxable Employee Benefits ............................................................................................. 13Calculating Income Tax and Income Tax Planning .......................................................... 16Income tax and Trusts ..................................................................................................... 19

National Insurance Contributions (NIC) and Capital Gains Tax (CGT ........................... 23NI for the Employed and their Employers ......................................................................... 24Company Directors and Multiple Employments ............................................................... 27NI for the Self-Employed and Others ............................................................................... 29Voluntary NI Contributions and Credits............................................................................ 31State Benefits .................................................................................................................. 32CGT - Exemptions, Losses and Reliefs ........................................................................... 34CGT Calculation, CGT Planning and Trusts .................................................................... 38Disposals subject to special CGT rules............................................................................ 42Principal Private Residence Relief................................................................................... 43

Inheritance Tax (IHT)......................................................................................................... 47IHT, the Transferable NRB and the Residence NRB ....................................................... 48PETs and CLTs ............................................................................................................... 53Reliefs ............................................................................................................................. 57Intestacy, Deed of Variation and Trusts ........................................................................... 59GWR, POAT and IHT Planning........................................................................................ 62

Residence, Domicile, UK Tax Compliance and Other Taxes ......................................... 64Residence and Domicile.................................................................................................. 65Domicile .......................................................................................................................... 66The Remittance Basis ..................................................................................................... 67Residency, Domicile and Income Tax.............................................................................. 69Residency, Domicile and Capital Gains Tax (CGT) ......................................................... 70

Investment Taxation ......................................................................................................... 87Cash and Fixed Interest Investments .............................................................................. 88Shares, Property and Pensions ....................................................................................... 91Individual Savings Accounts (ISAs) and Collectives ........................................................ 97Life Assurance-based Products..................................................................................... 100Indirect Property Investments, VCTs, EISs, SEISs and SITR ........................................ 106

Trusts............................................................................................................................... 110Overview of a Trust ....................................................................................................... 111More on Trustees .......................................................................................................... 114

Essential Study Notes

3Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

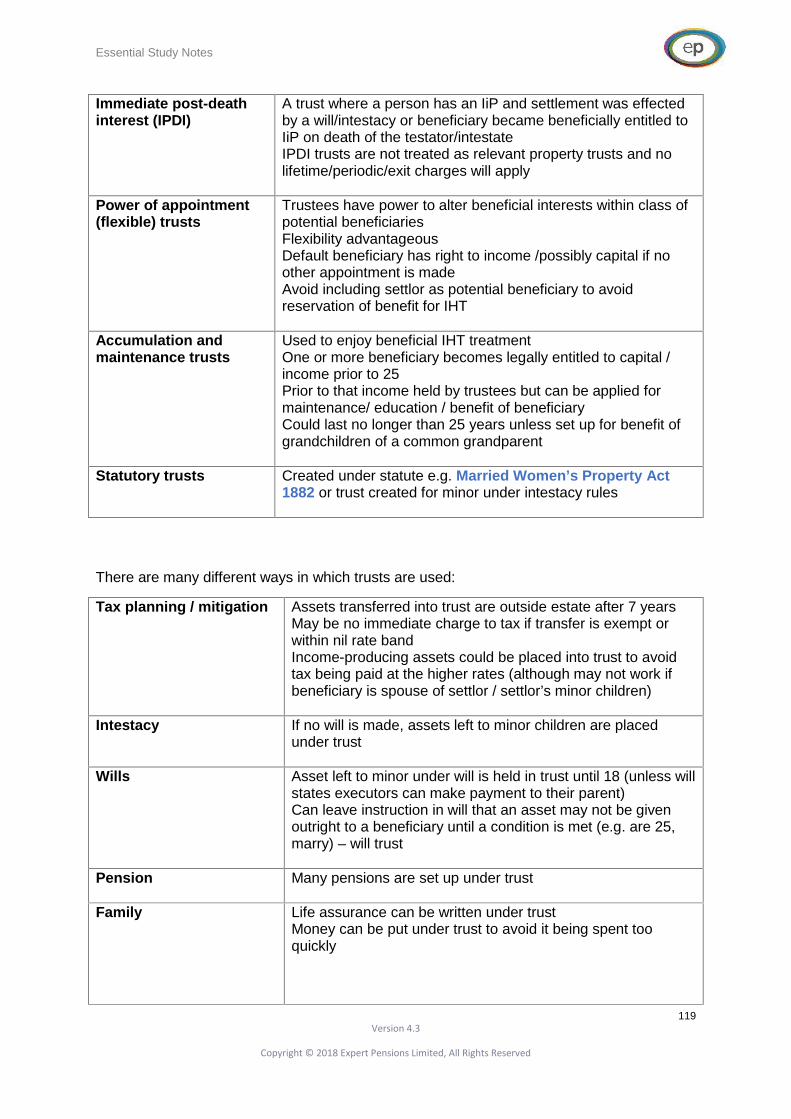

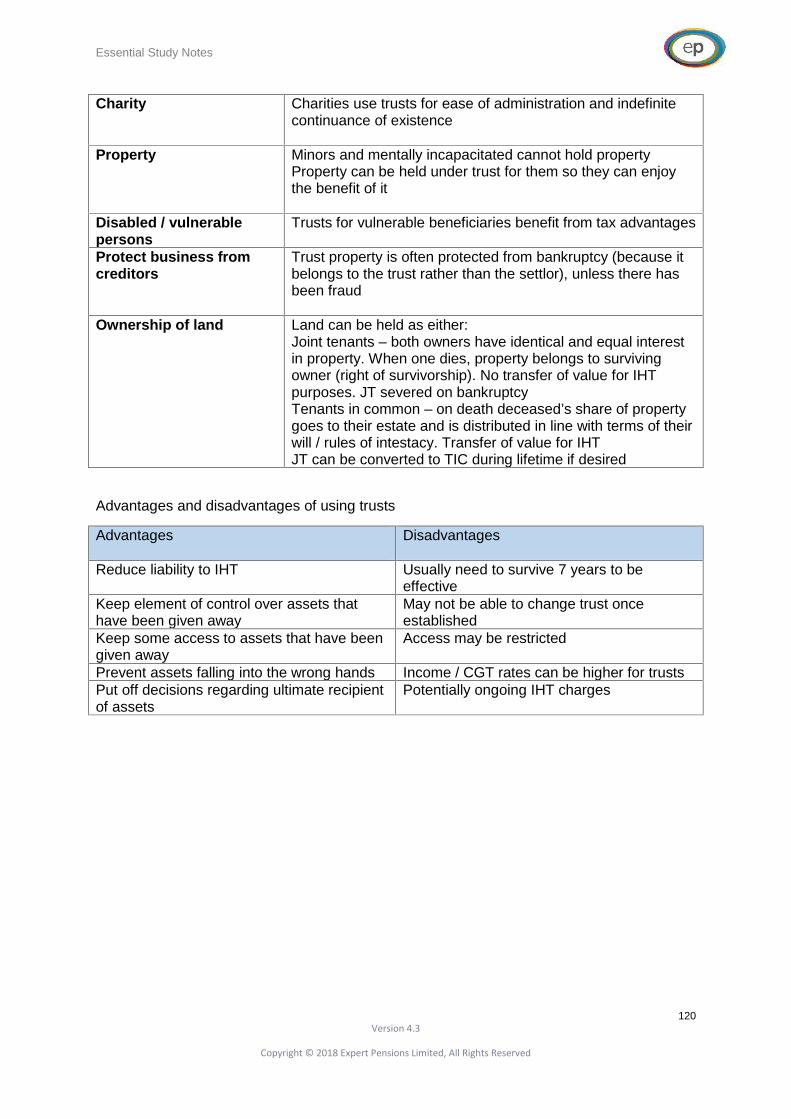

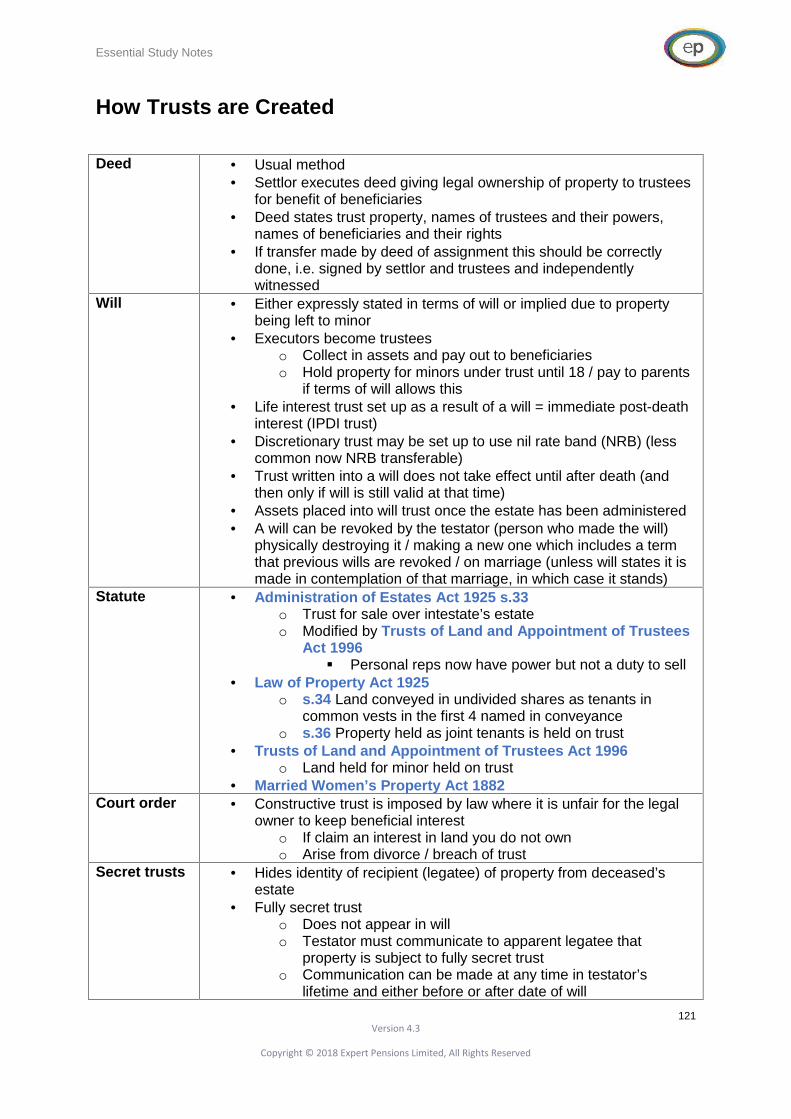

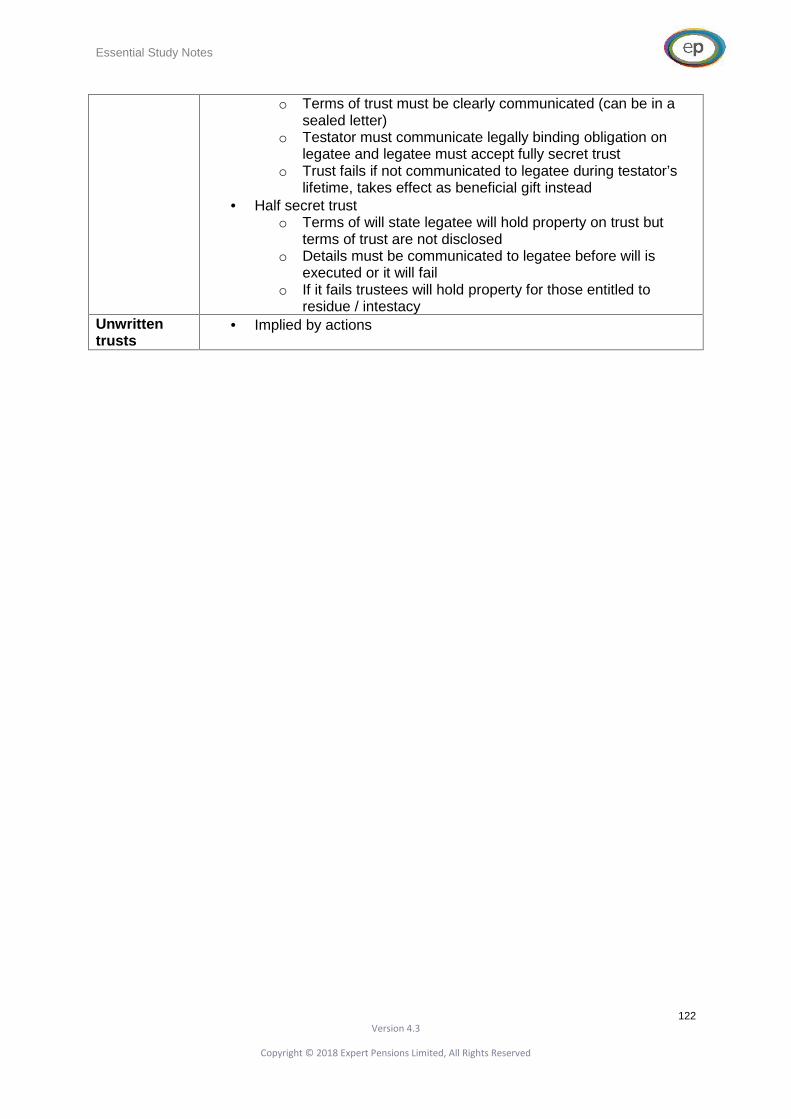

Types and Uses of Trusts.............................................................................................. 118How Trusts are Created ................................................................................................ 121Trust Rules.................................................................................................................... 123

Powers of Attorney and Bankruptcy ............................................................................. 127Powers of Attorney (POA) ............................................................................................. 128The Mental Health and Mental Capacity Acts ................................................................ 132The Process of Bankruptcy............................................................................................ 136The Effects of Bankruptcy on Investments, Life Assurance, Pensions and Trusts ......... 142Alternatives to Bankruptcy ............................................................................................. 144

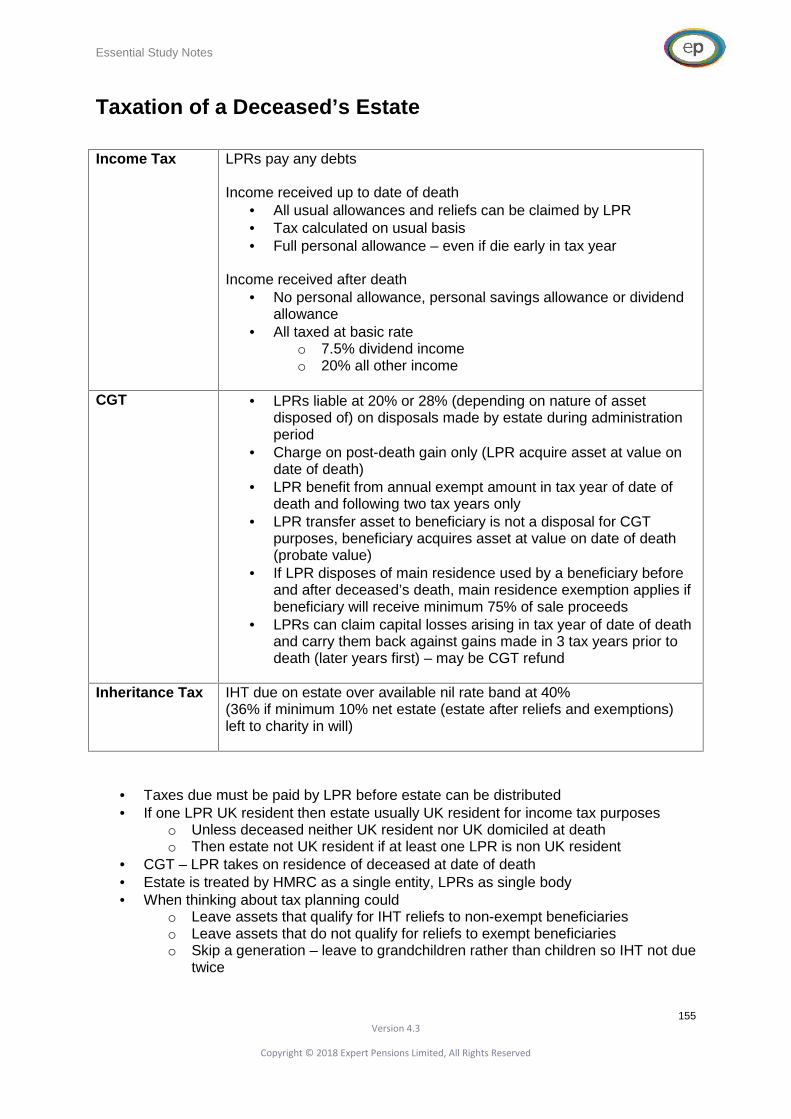

Wills and Intestacy.......................................................................................................... 146Wills, Deeds of Variation and Disclaimer ....................................................................... 147Intestacy........................................................................................................................ 150Transferable Nil Rate Band and Residence Nil Rate Band ............................................ 153Taxation of a Deceased’s Estate ................................................................................... 155

Taxation of Trusts........................................................................................................... 156Income Tax ................................................................................................................... 157Capital Gains Tax.......................................................................................................... 163Inheritance Tax.............................................................................................................. 165Collectives and Unit Trusts ............................................................................................ 168

Financial Planning and Trusts ....................................................................................... 169Life Assurance............................................................................................................... 170Pensions ....................................................................................................................... 178Transfers on Lifetime and on Death............................................................................... 180Reviewing trusts ............................................................................................................ 183IHT Planning Arrangements .......................................................................................... 186

Essential Study Notes

4Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Income Tax

If I had to pick one certainty in AF1 it is that you will get an income tax calculation for anindividual. There has been one in each of the past six AF1 papers, carrying an average of18 marks. The bare minimum to be included are earned (non-savings), savings anddividend income. There is bound to be at least one other issue such as a pensioncontribution, a benefit-in-kind like a company car, marriage allowance / married couple’sallowance or child benefit to add to the mix.

Within our income tax module we will work our way through each of the stages of an incometax calculation. We’ll start by examining the various sources of income an individual mayreceive and consider how they are treated for income tax purposes. We’ll then look at whatreliefs, allowances, reducers and credits are available to reduce the amount of tax anindividual pays. Most employee benefits are taxable so we’ll review how we arrive at theirtaxable value. We’ll then look at how to work out an individual’s tax bill before finallyexamining how the various types of trusts are taxed on the income they receive and pay out

TopicsSources of IncomeReliefs, Allowances, Reducers and CreditsEmployee BenefitsCalculating Income Tax and Income Tax PlanningIncome Tax and Trusts

Essential Study Notes

5Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Sources of Income

Non-savings income

Salary, bonuses and taxable benefits (employed) Fees, trading income/profits (self-employed) – expenses wholly and exclusively for

business purposes are allowable deductions Pension income (annuity, scheme pension or drawdown) Taxable State benefits Property income

Charged to tax at 20, 40 and 45% and taxed before savings and dividend income.

It is the duty of the employer to determine whether a worker is an employee or an employer.

Overlap relief

The self-employed are taxed on the income in their accounts ending in the tax year. Theyare free to choose their own trading year, it does not have to tie in with the tax year.

Special rules apply in the first and final years of a business:

Y1: The tax for the first year is based on the profits for that tax year. If the first yearends after the end of the first tax year, say in July or August, then only part of theseprofits are taxed in the first year.

Y2: The tax for the second year is based on the profits for the accounting periodending in the tax year. If that is not a full year, it is based on the first 12 months’profits. If it is longer than a year, assessment is usually based on the profits of the 12months ending on the accounting date.

Y3 onwards: Based on profits for the accounting period ending in the tax year.

NB In the final year, overlap relief is given for any profits taxed twice in years 1 and 2.

Example

Jack, a plumber, started his business on 1st of September 2017, his accounting period endson 31st of August 2018.

His profits for y/e 31st August 2018 are £100,000.

His profits for y/e 31st August 2019 are £120,000.

For the 2017/18 tax year, he will be assessed to tax on profits earned between 1stSeptember 2017 and 5th April 2018. The profits will be apportioned on a time basis:

i.e. £100,000 x 7/12 = £58,333.

For the 2018/19 tax year he will be assessed to tax on profits earned to the year ending 31st

August 2018:

i.e. £100,000

So, £58,333 of the £100,000 has been charged to tax twice. It is this amount that can beclaimed back as overlap relief in the final year of trading.

Essential Study Notes

6Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Employed or self-employed?

HMRC will look at the following indicators, but each case decided on individual basis,employer must determine and apply PAYE if in doubt:

Employed Self employedHigh control over worker Low controlContract of service Contract to provide / for servicesSet hours, set pay, holiday pay, overtime,supervision

Fee, commission, can refuse or sub contract

Long term, single employer Risks own money (own tools, correct work atown cost), profit from efficiency

Tax planning and the self employed

Choice of accounting date affects the timing of tax payments, change of date can enableoverlap relief from earlier years to be used, closing date / transfer to ltd company can makea difference to tax liability in final year.

Trading allowance

Trading income less than £1,000 (before expenses)o Exempt from taxo No need to be declared

Trading income greater than £1,000o Claim against income rather than deduct actual expenses

Property income

Income from property (accounts must be made up to 31st of March or 5th of April) –this includes payment from the tax-exempt element of a REIT – BUT those are paidnet of 20% tax

o If income before deducting expenses is £150k or less, accounts drawn up onsimplified cash basis (unless landlord opts out)

o Otherwise accruals basis used Ongoing expenses (but not enhancements) are allowable deductions, but relief on

mortgage interest is being gradually restricted to the basic rate since 6 April 2017.

Essential Study Notes

7Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

Jill has rental income of £25,000 and finance costs of £5,000.

In the 2018/19 tax year, £2,500 (50%) can still be deducted as an expense, £2,500 (50%)will be given as a basic tax deduction of £500 (£2,500 x 20%).

Assuming she has no other income her tax liability will look like this:

£

Rental income 25,000

Expenses (2,500)

Personal allowance (11,850)

Tax due on 10,650

All falls within basic rate therefore 10,650 @ 20% = 2,130

Less basic tax deduction of £500 to give total tax due of £1,630

Property allowance

Property income less than £1,000 (before expenses)o Exempt from taxo No need to be declared

Property income greater than £1,000o Claim against income rather than deduct actual expenses

Rent-a-room relief £7,500o Consultation currently taking place

For more details on taxation of property income go to our ‘Taxation of Investments’module

Savings income

Interest from:o Cash deposits – paid grosso Gilts – paid gross unless elect otherwiseo Permanent Interest Bearing Shares (PIBS) – paid grosso Directly held local authority bonds and corporate bonds – paid neto Interest distributing OEICs and unit trusts – paid grosso Purchased life annuity (PLA) – paid neto Interest from offshore reporting funds – paid gross

Basic rate tax payers (BRTs) have a Personal Savings Allowance (PSA) of £1,000 andhigher rate tax payers (HRTs) have a PSA of £500. Taxable savings income falling withinthese allowances will be charged to tax at 0%. Additional rate taxpayers (ARTs) do notbenefit from a PSA. These allowances should be applied to any savings income prior toapplying the relevant rate of tax (20% / 40% / 45%).

Essential Study Notes

8Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Where savings income falls within the first £5,000 of taxable income (income in excess ofreliefs and allowances) it benefits from a starting rate band of 0%. This is in addition to thePSA (which is accounted for once the starting rate band is fully used).

Where savings income is paid net, 20% tax is deducted at source. This is reclaimable bynon-taxpayers, by those whose savings income falls within the starting rate band for savingsand by those whose PSA covers the income. This satisfies the liability for a BRT, but resultsin a further 20% liability for a HRT and a further 25% liability ART of the gross interest.

Example

Jane is an additional rate tax payer. She receives a net interest payment of £1,000.

To gross this up we divide by .8. £1,000 / .8 = £1,250.

Jane’s full tax liability is therefore £1,250 @ 45% = £562.50.

£250 was taken at source (£1,250 - £1,000) so this amount can be deducted from theamount Jane owes. £562.50 - £250 = £312.50.

Dividend income

Dividends from:o shares or investment trustso equity OEICs and unit trustso offshore reporting funds and offshore closed-ended investment companieso non-exempt element of a REIT

All dividends are paid gross.

All individuals currently benefit from a £2,000 dividend allowance. Taxable dividends fallingwithin the allowance are charged to tax at 0%. Thereafter, BRTs pay 7.5%, HRTs pay at32.5% and ARTs pay at the rate of 38.1%.

Essential Study Notes

9Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Reliefs, Allowances, Reducers and Credits

Qualifying Interest payments

Certain interest payments can be deducted from an individual’s tax bill. The deduction islimited to the higher of 25% of the individual’s adjusted total income or £50,000.

Adjusted total income = total income plus charitable donations made via payroll less anypension contributions.

Example

In 2018/19 James took out a loan to pay the IHT due on his father’s estate. Let’s assumeJames earned £60,000 and made gross pension contributions of £10,000. If he paid interestof £20,000 on the loan, how much can he deduct from his tax bill?

James’s adjusted total income is £50,000 (£60,000 - £10,000)

The cap is the higher of 25% of £50,000, i.e. £12,500, or £50,000

The entire interest payment can therefore be deducted from James’s tax bill

The cap applies to loans taken out for qualifying purposes which include:

- share purchase in the borrower’s company or loans to their company- partnership investment- purchase of plant and machinery for use in partnership- as well as payment of inheritance tax (relief restricted to a period of 1 year from

making the loan).

Extending the basic rate/higher rate tax band

Relief for gift aid payments and for pension contributions other than to an occupationalpension scheme (relief at source method) is given by extending the basic/higher rate taxbands. Payments are made into the pension/to the charity net of 20% basic rate tax. Thepension scheme/charity reclaims the 20% from HMRC.

There are conditions relating to reciprocal benefits and gift aid:

Gifts up to £100, reciprocal benefit must not exceed 25% Between £101 and £1,000 it is £25 Gifts over £1,000 it is 5% of the donation up to £2,500.

These limits are currently under review.

Higher and additional rate tax payers reclaim the additional relief due to them by having theirbasic/higher rate bands extended by the grossed-up contribution.

Essential Study Notes

10Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

Henry makes a personal pension contribution of £4,000. The contribution is grossed up(£4,000 / 0.8) = £5,000 and it is this amount that is added to the basic and higher rate taxbands.

Normally, the point at which Henry would become a higher rate tax payer would be once hisincome exceeds £46,350 (£11,850 (the personal allowance) plus £34,500* (the basic ratetax threshold)).

* NB The basic rate tax threshold for 2018/19 in the UK (excl. Scotland) is £34,500. Unlesswe state otherwise, please assume we are referring to the UK (excl. Scotland) figure.

However, with the gross pension contribution of £5,000, Henry benefits from a basic rate taxthreshold of £39,500 (£34,500 + £5,000) and therefore does not need to pay tax at thehigher rate until his income exceeds £51,350 (£11,850 + £39,500).

In a similar vein, the top of Henry’s higher rate tax threshold would increase from £150,000to £155,000.

If you get a scenario where there is a pension contribution made under the relief at sourcemethod/ a charitable contribution and a chargeable gain from an investment bond, you needto extend the basic rate tax band by the amount of the gross pension contribution first. Thewider the basic rate band the greater the chance the top sliced gain will fall within it andthere will therefore be no further tax to pay.

Note that the maximum an individual may pay into a pension and get tax relief is the higherof £3,600 or 100% of their relevant UK earnings. The lifetime allowance for 2018/19 is£1.03m.

Deductions from salary

Employee’s payments into occupational pension schemes are usually deducted from paybefore calculating tax so the employee does not have to claim tax relief on them – this isknown as the net pay arrangement.

Payroll giving allows the employer to deduct the payment from salary before calculating taxunder PAYE giving the employee tax relief at their highest rate.

Allowances

Personal allowance is £11,850.

Children have their own personal allowance. Care should be taken where an investment isheld in a child’s name, but the capital was provided by the parent. In this scenario, where theincome exceeds £100 it will be taxed as though it is the income of the parent rather than thechild. (Child = under 18 and unmarried/not in CP). Rule applies to cash ISA held by 16-17-year old, but not to junior ISA/CTF. Teenager could work for family business providingpayment reasonable to use up their allowance.

An individual’s personal allowance is reduced by £1 for every £2 that their adjusted netincome exceeds £100,000.

Adjusted net income is total net income – which is total income less deductions for loss reliefand interest payments - with the gross amount of personal pension and gift aid contributionsthen deducted.

Essential Study Notes

11Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

For the current tax year, income more than £123,700 reduces the personal allowance to £0leading to an effective rate of 60% (the personal allowance trap) tax for income between£100,000 and £123,700.

Example

An individual has earnings of £116,220. He makes a personal pension contribution of £6,000(net) and a gift-aid donation of £1,440 (net). How much personal allowance is he entitled to?

£116,220 less £7,500 (grossed up pension contribution (£6,000/.8)) less £1,800 (grossed upcharity aid donation £1,440/.8)) = adjusted net income of £106,920.

Reduced personal allowance:£106,920 – £100,000 = £6,920Reduced by £1 for every £2 over £100,000: £6,920/2 = £3,460£11,850 – £3,460 = £8,390

Tax reducers

Having calculated the tax due we then deduct any tax reducers and any tax deducted atsource (so that it is not paid twice). These include the married couple’s allowance, themarriage tax allowance, and investments into VCT, EIS or SEIS (at a maximum reduction of30% of the initial investment into VCTs / EISs and 50% into SEISs).

Married couple’s allowance

Available to married couples / civil partners, where one of the couple was born before 6 April1935. Income is relieved at the rate of 10%. The full allowance is £8,695, but this is reducedto £3,360 (minimum floor) by £1 for every £2 of income over £28,900. Reduction determinedby the income of the higher income and usually paid to them unless the couple elect to sharethe reduction. (Pre-Dec 2005 determined by husband’s income.)

Example

Gaynor is eligible for the married couple’s allowance and has total income of £29,700.

She has exceeded the £28,900 limit by £800.

£800 / 2 = £400.

Her allowance reduces from £8,695 to £8,295.

The reduction on her tax bill is 10% of £8,295 rather than 10% of £8,695, i.e. £829.50.

To reduce income below £28,900 consider withdrawing PCLS (tax-free), unconditionallyswapping investments between partners so neither has income above it and/or switching toinvestments that generate capital growth/tax-free income.

Marriage allowance

Transfer up to £1,190 of personal allowance to spouse/civil partner providing recipient notliable to income tax above basic rate. Potential saving of up to £238.

Essential Study Notes

12Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

Martha earns £42,350 a year, her husband Graham, £10,500. They elect to transfer £1,190of Graham’s allowance to Martha.

This has no impact on the tax Graham pays because his income is below his revisedpersonal allowance of £10,660 (£11,850 - £1,190).

Martha’s tax bill is initially £6,100 (£42,350 less £11,850 @ 20%).

From this we can then take off the personal allowance reduction of £238. £238 is 20% of theamount of allowance transferred.

Martha’s reduced tax bill is £6,100 - £238 = £5,862.

Tax credits

Child tax credit

Paid to parent of child under 16 (under 20 in approved education/training). Significant changes came into force for those with children born on or after 6 April

2017. Visit https://www.gov.uk/child-tax-credit/new-claim (Accessed 14 May 2018) formore detail.

Claimed from HMRC, can back-date 1 month (protective claim can be made ifincome falls in year because of, say, redundancy).

Reduced by 41p for every £1 income over £16,105. Couples must claim jointly and claim based on joint income. First £300 pension/investment/rental income excluded. Personal pension contributions reduce income. Having a low income, high childcare costs, several children or children with

disabilities can lead to additional credits. Income over basic rate threshold may stillget some credit.

Paid in arrears to account.

Working tax credit

Top up payment for working people on low income: over 16s with children / have adisability and work at least 16 hours, over 25s no children - work at least 30 hours.

Amount of credit varies depending on hours worked, single/joint applicant, income,disability, child-care (70% of eligible costs covered up to £175pw (1 child) £300 pw(2 + children) reduced for incomes over £16,105).

Paid by HMRC to employed & self-employed. Couple decides who receives joint credit. Reduced by 41p for every £1 income over £16,105. First £300 pension/investment/rental income excluded. Personal pension contributions reduce income.

Essential Study Notes

13Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Taxable Employee Benefits

Generally speaking, where benefits are provided to employees they are treated as if theywere earnings. This means they are usually taxable.

The employee is taxed on the cash equivalent value of the benefit they have received.The cash equivalent value is usually the cost to the employer of providing the benefit unlessother, more specific, rules apply, such as in the case of beneficial loans, accommodationand company cars.

Where an employee has use of an employer’s asset, there is a tax charge on the annualvalue of the asset. The charge is 20% the asset’s market value of the asset when it was firstgiven to the employee. Any employer expenses incurred in the upkeep of the asset areadded to this figure. If the asset is rented, the charge is the higher of the rent paid or theannual value.

For an asset given to an employee outright, the tax charge is based on the market value atthe time of the gift unless the asset is brand new in which case it will be based on the cost tothe employer of providing the asset. If the employee had use of the asset before it was giftedto them, the charge will be based on the higher of the market value at the time of the gift andthe market value when the asset was first made available to the employee. Any amount thathas already been subject to tax may be deducted.

Benefits provided ‘in-house’ are taxable at the marginal cost to the employer as determinedin Pepper v Hart.

Company cars

For cars with emissions more than 95g/km, a base charge of 20% increases by 1% for everycomplete 5g/km. For example, if emissions are 102g/km we round down to the nearest5g/km which is 100g/km giving a charge of 20% plus 1%. The maximum charge is 37% ofthe car’s list price.

Diesel cars not meeting RDE2 standard are subject to a 4% excess, although the maximumcharge is still 37%.

Additional accessories are added to the list price of the car.

Discounts are ignored.

If an employee contributes to the cost of the car, the maximum that can be deducted is£5,000.

If the employee makes a regular contribution to the running costs of the car, then thisamount can be deducted from the taxable value.

If the employer pays for private fuel use then there is a standard charge of £23,400multiplied by the same CO2% as used when calculating the taxable value of the car.

Where the employee only benefits from the car for say, six months of the year, the taxcharge is proportionate.

Essential Study Notes

14Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

In the 2018/19 tax year Joe was given a diesel car that did not meet the RDE2 standard. Thelist price was £25,000. CO2 emissions were 139g/km. Joe contributed £7,500 towards thecost of the car. What is the taxable value of the car?

Diesel cars with CO2 emissions of 139g/km have a relevant percentage charge of 32%, thisis the sum of:

20% = base charge

4% = diesel addition

8% = for every 5g in excess of 95g add 1%, 139 – 95 = 44, round down to 40 / 5 = 8

32% charged on £20,000 (can only deduct £5,000 of Joe’s £7,500 contribution)

£25,000 - £5,000 @ 32% = £6,400 taxable value.

The mileage rates that can be paid free of tax to employees who use their own car forbusiness mileage are 45p for the first 10,000 miles, 25p thereafter.

There are detailed rules defining business & private travel - commuting to a normal place ofwork is defined as private travel, although travelling to a temporary workplace will normallyqualify as business travel.

Beneficial loans

The taxable value of beneficial loans in excess of £10,000 is based on the differencebetween the interest rate paid by the employee and the official rate (2.5% 2018/19).

Example

If an employee is offered a cheap loan of £15,000 at 0.75% then the taxable benefit is:

£15,000 x (2.5% – 0.75%) = £15,000 x 1.75% = £262.50.

Employee accommodation

Where an employee lives in rent-free or low-rent, accommodation provided by their employerthere will be a tax charge unless they are classified as having an exempt occupation.

An exempt occupation is one where the accommodation is deemed necessary for them toperform their duties, helps them perform their duties better or where there is a threat to theirsecurity.

Where a tax charge applies, it will be assessed on the benefit the employee receives byliving in their employer’s accommodation. This will usually be the annual rent.

Where the accommodation is owned by the employer and cost more than £75,000, there isan additional charge based on the excess of the cost of the property – plus the cost of anyimprovements – over £75,000. The charge is 2.5% of the excess (i.e. the official rate).

Essential Study Notes

15Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

The charge on a property worth £125,000 would be £1,250. We arrive at this figure byworking out the excess over £75,000. So, £125,000 - £75,000 equals £50,000 and thenmultiplying this by 2.5%.

Other taxable benefits

Cash and non-cash vouchers that can be exchanged for goods and services and credittokens, including company credit cards, are also taxable benefits.

Where an employer takes on an employee’s liability to meet costs, such as school fees, rentor professional fees the benefit is usually taxable in full.

Where an employer provides private medical insurance for an employee, this is also ataxable benefit.

Benefits wholly or largely exempt from tax

• Group Income Protection• Provision of meals (but not luncheon vouchers)• Long Service awards - £50/pa – min 20 years• Mobile phone – 1 per employee• Employer Sponsored Training• Suggestion Schemes - £25 or less, larger awards up to £5,000 subject to conditions• Relocation and removal expenses – up to £8,000• Home-working – up to £4 per week without evidence• Workplace nurseries• Liability insurance• Trivial benefits – under £50• Pension advice - £500

Essential Study Notes

16Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Calculating Income Tax and Income Tax Planning

To perform a full income tax calculation you need to:

1. Establish type of income: ADD earnings + pensions + rental income + any otherincome that isn’t savings or investment income = ‘Non-savings income’

2. TO deposit interest + any other savings income3. AND to dividends4. AND life policy chargeable gains5. DEDUCT reliefs or deductions which apply to any of the above income types (in the

same order)6. DEDUCT the personal allowance (watch out for restrictions on higher earners)7. EXTEND basic and higher rate bands for relievable payments (like non-occupational

pension contributions, gift aid)8. Then apply tax at the appropriate rates and don’t forget the starting rate band for

savings income/ the personal savings allowance/the dividend allowance (rememberto use the tax table provided)

9. DEDUCT tax reducers (EIS/SEIS/VCT/MCA/marriage tax allowance)10. AND any tax already deducted at source. This gives you the tax due for the

individual.

Not only is there a basic order in which you should deal with the calculation, but, for those ofyou who have progressed to AF1, the CII generally set out these calculations in exactly thesame way:

£ £ £ £Non-savings Savings Dividends Total

Employment income xx,xxxCompany pension xx,xxxBank interest xxxInvestment trust x,xxxTotals xx,xxx xxx x,xxx xx,xxx

See how the income is broken down into separate columns depending on whether it isearned (non-savings), savings or investment income? That makes it very clear for you tosee what needs to be taxed at what rate.

As you progress from R03 to AF1, clear explanations need to be given when detailing howthe taxable figures are arrived at. This is because the CII use ‘follow-through’ marks in theirwritten exams. This means that if you make a silly mistake in your calculation, likeincorrectly adding together two numbers, but go on to use the answer in the correct way, youwould only lose one mark for the silly mistake.

Essential Study Notes

17Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Income tax planning

Ensure client has enough money left to meet personal and business needs.

Tax efficient investments must also be a good match for the client in terms of risk, potentialreturns and costs.

Client should be aware of additional risks costs involved. Flexibility should be considered.

General rule: use allowances, reliefs and reduce income charged to tax at higher rates.

There are several income tax planning approaches that could be used to reduce tax,although most depend on the individual’s being married/in a civil partnership or owning theirown business. They include:

- non-taxpayers invest capital for income to maximise tax allowances, avoidinvestments where underlying funds are taxed and tax is not reclaimable (e.g.onshore bond)

- starting rate tax payers – make full use of 0% £5,000 starting rate tax band- higher/additional rate tax payers unconditionally transfer savings to spouse/partner or

into joint names to maximise use of both parties PSAs/DAs/starting rate/basic ratetax bands

- switch to investments that yield capital growth to minimise income/maximise use ofCGT annual exempt amount

- switch to investments on which income is tax-free (ISAs) or covered by the PSA/DA- defer tax by using offshore single premium bond – benefit from gross roll up- close deposit accounts/encash bonds/offshore non-reporting funds before/after 6

April to control year income is taxed in- make charitable donations that qualify as gift aid donations (because these are

deducted in working out adjusted net income)- make additional pension contributions (for same reason as above)- if feasible, meet ‘income’ requirements from 5% withdrawals from bond because

these are not added to taxable income in the year they are taken- where own business/self-employed could:

o reduce director’s remuneration if that’s an option, choose to take bonus ordividend before/after end of tax year if expect tax rate of one year to be morebeneficial than the other

o pay salary to spouse/partner (pay between £116 & £162 a week to qualify forstate benefit at 0% NIC, salary deducted from business profit)

o pay pension to employed spouse/partner (no tax /NIC on benefit foremployee, contribution deducted from business profit)

o Re: both the above amounts must be reasonable for the work carried out ormay not be deductible

o change to partnership – will not work if business consists of supplyingpersonal services (IR35 rules will apply) If IR35 rules apply, cannot save tax by paying dividends/employing a

partner. Need to pay sufficient salary to avoid being taxed on a‘deemed payment’. Company pension contributions allowable if pass‘wholly and exclusively’ test. Income from MSCs also employmentincome (cannot avoid IR35 this way).

o change to ltd company – IR35 will not apply. Self/partner become shareholderand receive dividends (not subject to NIC). DA available. Risky strategy ifprofits mostly generated by working partner who draws low salary. NB Dividends paid from after-tax profits, corporation tax 19%. Do not

count as earnings for pension purposes.

Essential Study Notes

18Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Where strategy involves married couple/civil partners transfers must be absolute andunconditional. Former owner cannot, for example, continue to receive an income from anasset given to their partner. Should consider possibility of divorce. If couple are notmarried/in a civil partnership transfer could lead to CGT/IHT liabilities

Example

Lillian earns £130,000 a year.

If she makes no charitable donations/pension contributions she will lose her entire personalallowance and, assuming she has no other income, her income tax liability will be £45,100:

£34,500 @ 20% = £6,900

£95,500 @ 40% = £38,200.

Let’s say she decides to make a pension contribution to regain her personal allowance. Sheneeds to reduce her net adjustable income to £100,000, i.e. by £30,000. This can beachieved by making a pension contribution of £24,000 (this would be the net amount,£24,000 / .8 = gross contribution of £30,000).

With net adjustable income of £100,000, Lillian is entitled to the full personal allowance. Herincome tax liability would therefore be £34,360:

£130,000 - £11,850 = £118,150 taxable income.

£64,500 (Lillian’s basic rate tax band would be extended by £30,000) @ 20% = £12,900

£53,650 @ 40% = £21,460.

£34,360 is a significant reduction on £45,100 and it is brought about in two ways – firstly thereinstatement of the personal allowance, and secondly the fact that her basic rate thresholdis extended by the gross amount of the pension contribution.

High income child benefit charge

The high-income child benefit charge can also be reduced/eliminated by using the abovestrategies. It is relevant where at least one partner has adjusted net income (total incomeless pension/charity donations) of £50,000 or more and is charged on the partner with thehighest income. It works by reducing the annual child benefit payment by 1% for each £100of excess adjusted net income over £50,000. Individuals never pay more in tax than the fullamount of child benefit available.

Example

Someone with two children will be entitled in 2018/19 to receive child benefit of (£20.70 +£13.70) x 52 = £1,788.80. If they earn £54,000, the tax charge will be £17.88 for every £100over £50,000, i.e. £4,000/100 x £17.88 = £715.20.

Essential Study Notes

19Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Income Tax and Trusts

Bare/absolute trust

Trustee

None.

Beneficiary

Taxed at beneficiary’s rates. Their personal allowance, personal savings allowanceand dividend allowance can be used to offset any tax.

Settlor

Parental settlement rules apply (where trust income exceeds £100 and settlor isparent it is taxed on the parent.)

Trusts for the vulnerable

Broadly speaking, a trustee’s tax liability under a trust for a vulnerable person is limited tothe tax liability that would have been suffered by the beneficiary were the trust not inexistence.

Interest in possession trust

Trustee

Charged at basic rate, i.e. 7.5% dividend income, 20% all other income. No allowances. No liability to higher rate tax. No relief for expenses of managing the trust, though these are deductible in arriving

at the beneficiary’s income. Complete R185 and pass to beneficiary.

Trustee expenses

Trustees not entitled to tax relief on expenses for managing trust. Trust expenses are deductible in arriving at beneficiaries’ income. Higher/additional rate tax due by beneficiary is paid on income received after

deduction of expenses.

Essential Study Notes

20Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

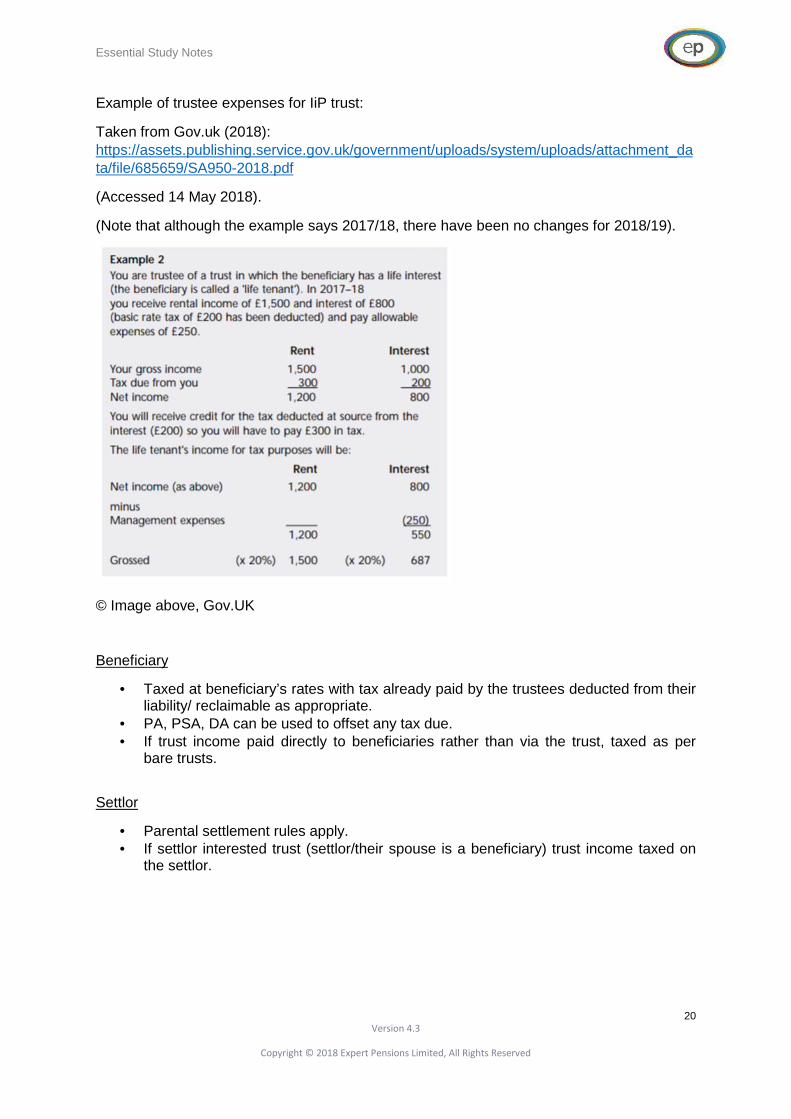

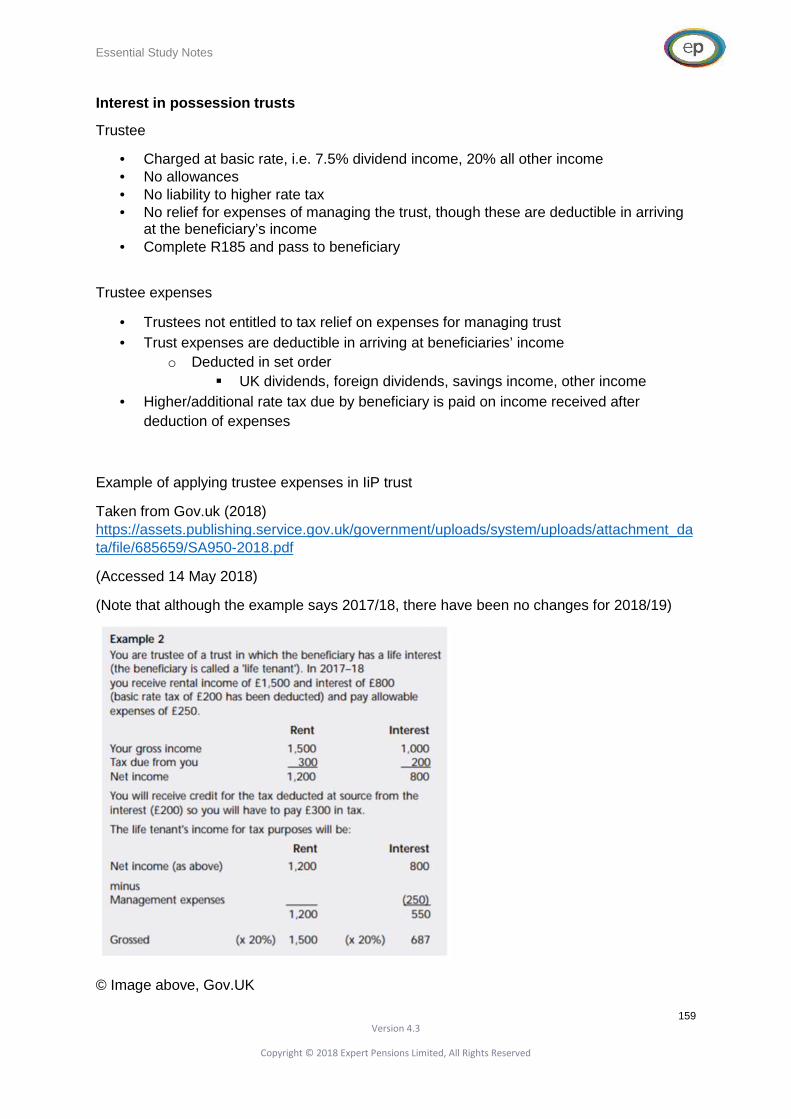

Example of trustee expenses for IiP trust:

Taken from Gov.uk (2018):https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/685659/SA950-2018.pdf

(Accessed 14 May 2018).

(Note that although the example says 2017/18, there have been no changes for 2018/19).

© Image above, Gov.UK

Beneficiary

Taxed at beneficiary’s rates with tax already paid by the trustees deducted from theirliability/ reclaimable as appropriate.

PA, PSA, DA can be used to offset any tax due. If trust income paid directly to beneficiaries rather than via the trust, taxed as per

bare trusts.

Settlor

Parental settlement rules apply. If settlor interested trust (settlor/their spouse is a beneficiary) trust income taxed on

the settlor.

Essential Study Notes

21Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

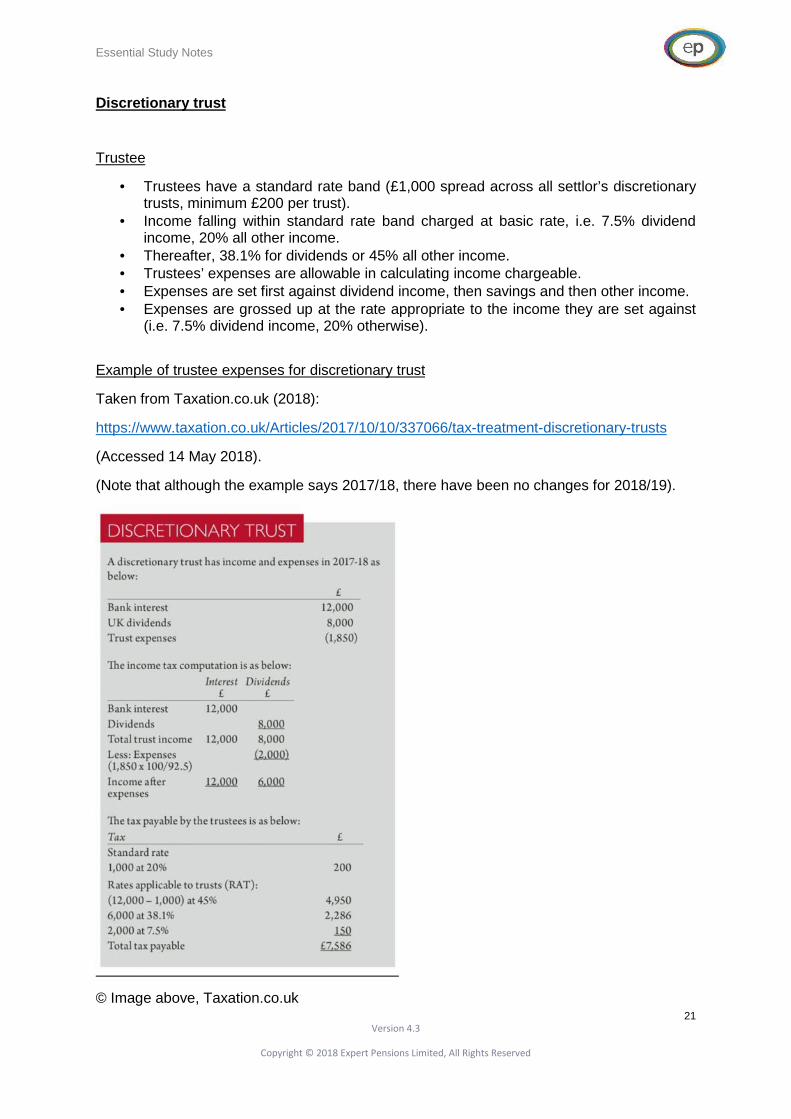

Discretionary trust

Trustee

Trustees have a standard rate band (£1,000 spread across all settlor’s discretionarytrusts, minimum £200 per trust).

Income falling within standard rate band charged at basic rate, i.e. 7.5% dividendincome, 20% all other income.

Thereafter, 38.1% for dividends or 45% all other income. Trustees’ expenses are allowable in calculating income chargeable. Expenses are set first against dividend income, then savings and then other income. Expenses are grossed up at the rate appropriate to the income they are set against

(i.e. 7.5% dividend income, 20% otherwise).

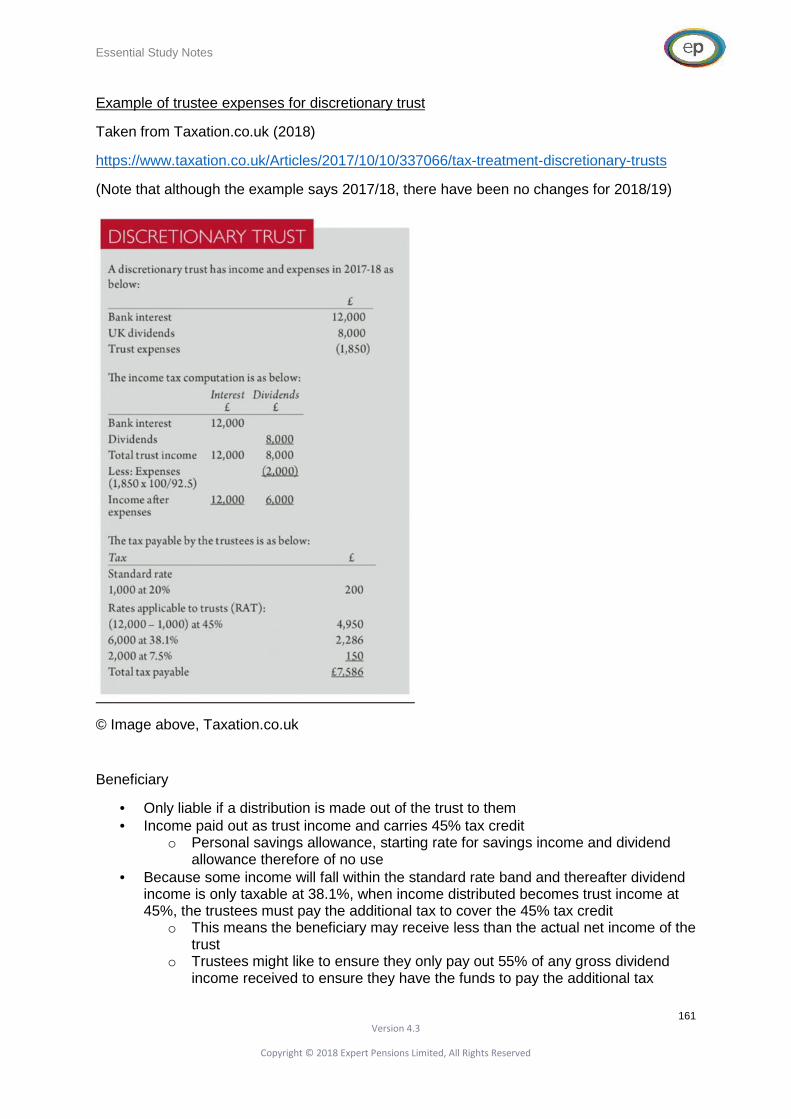

Example of trustee expenses for discretionary trust

Taken from Taxation.co.uk (2018):

https://www.taxation.co.uk/Articles/2017/10/10/337066/tax-treatment-discretionary-trusts

(Accessed 14 May 2018).

(Note that although the example says 2017/18, there have been no changes for 2018/19).

© Image above, Taxation.co.uk

Essential Study Notes

22Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Beneficiary

Income paid out as trust income and carries 45% tax credit. Non-taxpayer can reclaim the 45% tax paid. BRT can reclaim 25% tax and HRT 5%.

An ART has nothing more to pay but cannot reclaim anything. Any reclaim is made by completing form R40. Because dividend income is only taxable at 38.1%, but income distributed becomes

trust income at 45%, the trustees must pay the additional tax to cover the 45% taxcredit. Beneficiaries can only claim credit for tax paid by the trustees.

If the trustees decide to accumulate income rather than pay it out, the tax paid onthat income is carried forward in a ‘tax pool’. If that income is then distributed in lateryears the brought forward tax is available to ‘frank’ the 45% tax credit and thereforereduces any additional liability the trustees may have on distributions of dividendincome where the 45% tax credit exceeds the 38.1% tax the trustees must pay onthat income.

Settlor

Parental settlement and settlor interested trust rules apply.

Essential Study Notes

23Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

National Insurance Contributions (NIC) and Capital GainsTax (CGT

National Insurance (NI) is the third most popular topic in AF1, although it doesn’t alwaysappear as a calculation question. It can appear as a recommendation question applying tothe particular case study scenario given – for example recommending how someone couldimprove their NI contribution record, usually in order to qualify for the single-tier Statepension.

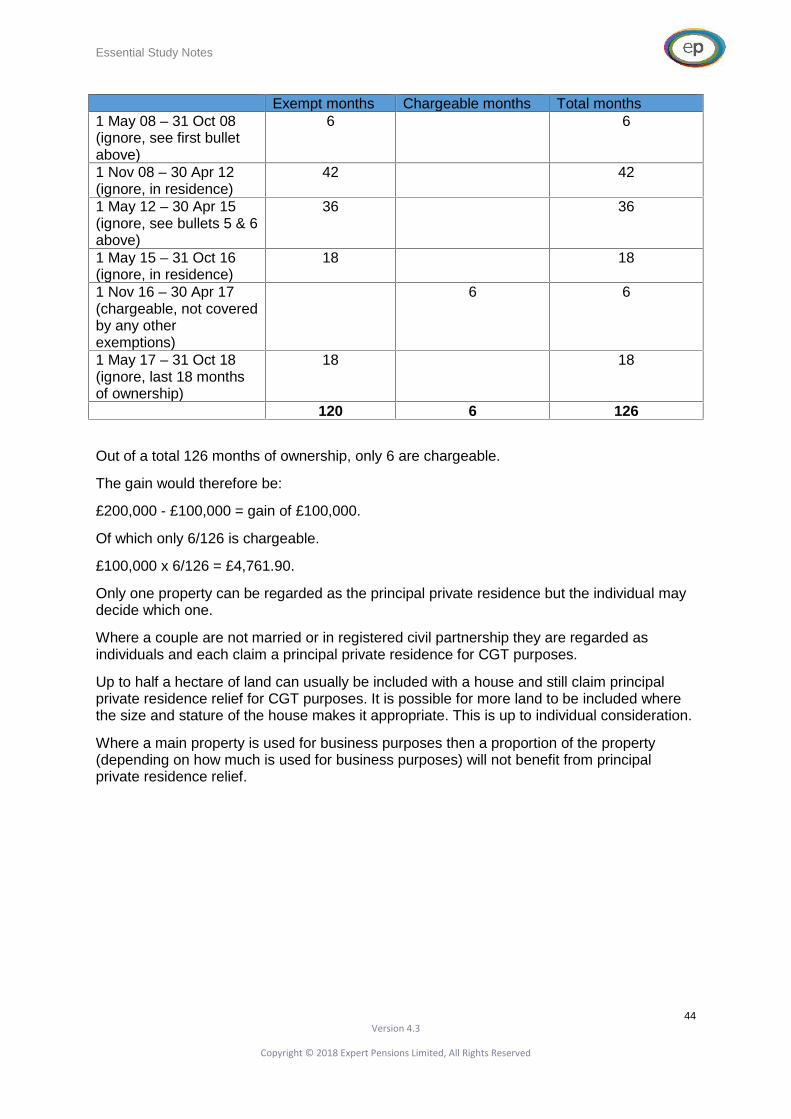

After income tax calculations, the next high certainty is a CGT calculation. Again, one ofthese has appeared in most recent exam papers, although sometimes the calculation isn’t astraightforward liability calculation, there have also been questions asking you to calculatethe % of a property gain that qualifies for PPR, so you need to think around the subject a bit.

TopicsNI for the Employed and their EmployersNI for the Self-Employed and OthersCGT - Exemptions, Losses and ReliefsCGT Calculation, CGT Planning and TrustsDisposals subject to special CGT Rules

Essential Study Notes

24Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

NI for the Employed and their Employers

NI for Employees and Employers

National Insurance contributions (NICs) are payable on earned income. The amount andwho pays them is determined by employment status, age, earnings and residence status.

They are administered through NICO – the National Insurance Contributions Office, a part ofHMRC. The chancellor will announce changes to rates in the budget but they take effectfrom the start of the tax year.

35 qualifying years required for single-tier State pension. State pension age (SPA)increasing - 65 men and women by Nov 2018, 66 by April 2020, 67 between 2026 and 2028,68 between 2037 and 2039. Reviews every 5 years linking SPA to longevity.

Contribution based benefits: State pension, contribution-based Job Seeker’s allowance(Class 1 only), bereavement benefits, contribution-based employment and supportallowance and maternity allowance.

Class 1

Payable on every type of earned income (including things like maternity pay, sick payand bonuses), lumps sums on joining/leaving an employer, payments to meet anemployee’s personal debts and payments in kind/assets that can easily be convertedinto cash.

Taxable employee benefits are usually liable for employer NI only (Class 1A, 13.8%).The first £55 a week of certain childcare benefits (closes to new entrants October2018) and trivial benefits costing £50 or less are free of NICs.

Two types – primary contributions paid by employees and secondary contributionspaid by employers. Employer contributions are deductible from taxable profits as anexpense.

Employee contributions paid at 12% between weekly primary contribution thresholdof £162 and upper earnings threshold of £892, thereafter the charge is 2%.

Employer contributions generally paid at 13.8% in excess of the secondarycontribution threshold of £162.

Employees potentially liable from age 16 to State Pension Age (SPA), but no upperage limit for employers.

Collected through PAYE (and therefore based on pay period). Taking dividends instead of salary / employer contributing to company pension

schemes by salary sacrifice are not liable to NI

Example

Alan, age 34, earns £800 a week. His weekly primary class 1 NIC liability is therefore:

£0 to £162 (the primary contribution threshold) @ 0% = £0.

£800 - £162 = £638. This is all taxed at the employee rate of 12%. £638 @ 12% = £76.56.

His total weekly liability is therefore £0 + £76.56 = £76.56.

Essential Study Notes

25Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Example

Alan gets a pay rise and is now earning £900 a week. His earnings therefore exceed theupper earnings limit of £892 so he will now pay:

£0 to £162 @ 0% = £0.

£892 - £162 @ 12% = £87.60.

£900 - £892 @ 2% = £0.16.

His total weekly liability is therefore now £0 + £87.60 + £0.16 = £87.76

Example

Let’s take a look at Alan’s employer’s NICs based on the two different sets of earnings. Notethat the secondary contribution threshold is the same as the primary contribution threshold,i.e. £162.

Firstly if weekly earnings are £800:

£0 to £162 @ 0% = £0.

£800 - £162 @ 13.8% = £88.04

His employer’s weekly liability is therefore £0 + £88.04 = £88.04.

After Alan’s pay rise (£900):

£0 to £162 @ 0% = £0.

£900 - £162 @ 13.8% = £101.84

His employer’s weekly liability is therefore £0 + £101.84 = £101.84.

Note that the employer does not benefit from a reduced rate once earnings exceed theupper earnings threshold. His employer’s weekly liability is therefore £101.84.

Example

Consider how the employer’s NICs would differ if Alan were either under 21 or an apprenticeaged under 25:

- If his earnings were £800 there would be no employer contributions to pay because a0% rate applies up to £892 a week (known as the upper secondary threshold (UST)/apprentice upper secondary threshold (AUST).

If his earnings were £900, then there would be employer contributions at the usual rate of13.8% on earnings in excess of £892.

Employee contributions are paid as normal.

Essential Study Notes

26Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Employer allowance

Most employers are entitled to an employment allowance of £3,000 a year and this isdeducted from their total secondary contributions. Businesses and charities can claim theallowance, as can individuals who employ a care or support worker. It is not available tocompanies where the director is the sole employee.

From April 2020, the allowance will be restricted to employers with an employer NIC billbelow £100,000 in the previous tax year.

Married women

Pre-6 April 1977 married women could pay reduced NIC (5.85% instead of 13.8%), someelections are still in force but are revoked on divorce/annulment/remarriage/ 2 consecutivetax years with no earnings above the LEL and no self-employed earnings/where normalcontributions are paid in error. Paying a reduced rate leads to reduced benefits.

Overseas employment

Members of EEA only pay towards social security benefits in one State – usually where theywork rather than were they live. Employer contributions will be paid in the same State.

Outside the EEA, NICO will collect NICs from employees who work regularly in the UK oncethey have been resident for 52 weeks. NICO will continue to collect NICs for 52 weeks forthose leaving the UK to work abroad for a UK employer.

Special categories of employment

Some workers are treated as employees for NIC purposes, even though for income taxpurposes they may not be including:

Domestic workers and office cleaners Agency workers Lecturers/instructors Ministers of religion Film/TV workers Labour-only subcontractors

Collection

Class 1 NICs are collected via PAYE with income tax. They are shown on P60.

Class 1A are due 22 July after end of tax year (19th if not paid electronically). Reported onP11D(b) which has to be submitted by 6 July after end of tax year.

Penalties for late payment Class 1:

No penalty for first offence unless more than 6 months late Then 1% of late amount increasing as number of late penalties increase 5% penalty where payments more than 6 months late, a further 5% after 12 months

Essential Study Notes

27Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Penalties for late payment Class 1A

5% if full payment not made within 30 days of being due 5% more than 6 months late 5% where more than 12 months late

Late payments charged interest daily.

Repayment

There is no automatic right to repayment where excess contributions are paid. Although theyare usually repaid, if contributions to another class should have been paid, HMRC willreallocate rather than repay.

Company Directors and Multiple Employments

As a general rule, you should always work out someone’s NI contribution on a weekly basisbefore multiplying it up to get the annual figure. Rounding means if you try and calculate onan annual basis your final answer isn’t quite right because NI is meant to be calculatedweekly.

There is ONE exception to this golden rule, and that is if the person is a company director.Because of the unpredictable pattern of director’s payments, their NI contributions arealways calculated annually.

Example

Nadine receives a director’s fee of £60,000. Her employee’s NIC are calculated not on thenormal weekly basis or monthly basis but using the annual limits as follows:

£0 to £8,424 @ 0% = £0

£46,350 - £8,424 @ 12% = £4,551.12

£60,000 - £46,350 @ 2% = £273

Her total Class 1 NICs on the fee are therefore £0 + £4,551.12 + £273 = £4,824.12

Remember: if directors draw funds as dividends rather than a salary/fee there is no NIC topay.

Essential Study Notes

28Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Associated employments

Earnings from linked employers will be aggregated for NI purposes.

Example

Simon works for a company which is a parent company with three subsidiaries. Simoncannot avoid NIC by arranging for each of the subsidiaries to pay him just under the primarycontribution threshold. In this instance, the earnings will be added together, and he will payNICs on the total amount in excess of the primary contribution threshold.

However, if Simon worked for three different companies who were in no way associated witheach other and each paid him under the primary contribution threshold then he would haveno NIC to pay as these earnings would not be aggregated.

Multiple employments

Maximum Class 1 NI contribution payable by an individual with more than one employment =£46,350 - £8,424 = £37,926 x 12% = £4,551.12 but no maximum at 2% rate which ispayable on combined earnings over £37,926 after taking off PCT for each.

Example

Jenny is a director of two unconnected companies. She earns £28,000 at both. Her totalearnings are therefore above the upper earnings level of £46,350, so she can apply fordeferment in respect of one set of earnings.

If she does so her NICs payable during 2018/19 will be:

£28,000 - £8,424 = £19,576 @ 12% = £2,349.12 plus

£28,000 - £8,424 = £19,576 @ 2% = £391.52.

Giving a total of £2,740.64.

At the end of the tax year Jenny’s earnings will be reviewed and she will have to pay thedifference between the annual maximum of £4,551.12 plus 2% of the combined earningsover £37,926 after taking off the PCT for each and the £2,740.64 she actually paid.

NICs at 2% (((£28,000 - £8,424) + (£28,000 - £8,424) - £37,926) x 2%) = £24.52

£4,551.12 + £24,52 - £2,740.64 = £1,835

If she had not applied for deferment she would have paid:

£28,000 - £8,424 = £19,576 @ 12% = £2,349.12 plus

£28,000 - £8,424 = £19,576 @ 12% = £2,349.12

Giving a total of £4,698.24 which is in excess of the annual maximum.

Essential Study Notes

29Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

NI for the Self-Employed and Others

NI and the Self-Employed

Class 2

Flat rate weekly amount (£2.95) paid by self-employed aged 16 to SPA whoseearnings exceed £6,205 pa (small profits threshold).

Class 2 NICs are calculated as part of the self-assessment process and paid in alump sum on the 31 January following the end of the tax year (i.e. at the same timeas the balancing payment)

NB credits are not given where earnings are below the threshold so may want tocontribute anyway to maintain contribution record (and because Class 2 are a lotcheaper than Class 3 voluntary which we look at in our next topic)

It is Class 2 contributions that build up entitlement to the single-tier state pension

Class 4

Paid by the self-employed aged 16 to SPA on a percentage of profits after adjustingfor capital allowances and trading losses brought forward. Higher NI rate of 9%based on band profits of £8,424 to £46,350 with 2% payable on all profits over£46,350. Paid with and at same time as income tax liability.

Does not contribute to state benefits

Overall the self-employed pay lower NI than the employer but receive fewer benefits. Theyrepresent a very small portion of NI contributions – 3% for Class 2 and 4 combined.

Example

Charlotte is self-employed, aged 40, and has taxable profits of £62,000 pa.

Her Class 2 and Class 4 NICs are therefore:

Class 2: £2.95 x 52 = £153.40

Class 4:(£46,350 - £8,424) = £37,926 @ 9% = £3,413.34(£62,000 - £46,350) = £15,650 @ 2% = £313.00

Total £3,879.74

Make use of the tax table you’re given in the exam – it saves you having to remember all thedifferent rates, limits and thresholds.

Essential Study Notes

30Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Employed or self-employed?

If an individual states they are self-employed and HMRC later find them to be employed, theemployer may be required to pay backdated employee and employer NICs.

HMRC has a set of ‘flags’ that indicate employment as opposed to self-employment:

A person is likely to be deemed to be employed if they have to complete the jobsthey are asked to do; if they can be told what to do, where to do it, when to do it byand how to do it; if they work for a specific number of hours each pay period in returnfor a regular wage and if other benefits associated with employment such asovertime or bonuses are available. (Contract of service)

A person is more likely to be deemed self-employed if they can sub-contract, if theyhave to supply their own tools, have their own money at risk, can chose what work totake on, where it has to take place, when it needs to be done by and how it should bedone. Working for a number of different firms and having to make right any errors attheir own cost are also indicators of self-employment. (Contract for services)

Employed and self employed

Special rules apply where an individual has both employed and self-employed earnings toprevent excessive NI payments.

The annual maxima are:

Class 1 plus class 2: £4,551.12

Class 2 plus class 4: £3,566.74

Class 1 plus class 2 plus class 4: Class 4 limited to maximum class 4 less main rate class 1paid

Special categories of self-employed earners

Special rules apply or share fisherman, who pay a higher rate of class 2 making themeligible for jobseeker’s allowance, sub-postmasters who have Class 1 NIC deducted fromtheir salary but are liable to pay Class 2 and Class 4 on any trading profit. Some are treatedas employees for income tax but self-employed for NIC paying a special Class 4 rate on theirearnings, e.g. examiners.

NB Class 2 NIC no longer expected to be abolished in the current Parliament.

Essential Study Notes

31Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Voluntary NI Contributions and Credits

Voluntary contributions

Class 3

Flat rate weekly amount for UK residents who have paid insufficient Class 1 or 2contributions during a tax year and wish to ensure they maintain/accrue entitlementto state benefits, particularly the single-tier State pension. If arrived in UK during taxyear, must have previously been liable for NI or UK resident for 26 weeks.

Cannot be paid in the same tax year in which you reach your state pension age orafter state pension age.

Can pay contributions going back six tax years but this will be at current rate (ratherthan the rate that applied at that time).

NI credits

Basically, this is a list you’re going to have to learn. You will be credited as if you had beenpaying sufficient National Insurance contributions in each of the following situations (fromhttps://www.gov.uk/national-insurance-credits/eligibility - Accessed 14 May 2018):

when unemployed, or unable to work because of ill health and claiming certain benefits if you are on an approved training course when you are doing jury service if you are getting Statutory Adoption Pay, Statutory Maternity Pay, Additional Statutory

Paternity Pay, Statutory Sick Pay, Maternity Allowance or Working Tax Credit if you have been wrongly put in prison if you are a man approaching age 65 (however, since 6 April 2010 these credits are

being phased out in line with the increase in women's State Pension age) if you are caring for a child or for someone who is sick or disabled if you are aged 16 or over and provided care for a child under 12, that you are related to

and you lived in the UK for the period(s) of care if your spouse or civil partner is a member of Her Majesty's forces and you are

accompanying them on an assignment outside the UK.

Credits are not given to the self-employed earning under the Class 2 threshold. In thesecircumstances, they might want to pay voluntarily pay Class 2 (as it will be cheaper thanClass 3 and will still maintain their record.)

Essential Study Notes

32Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

State Benefits

LEL = lower earnings threshold (£116pw or £6,032 pa) – the point at which entitlement to thesingle-tier State pension arises.

Here is a list of the main State benefits, together with a summary of whether they arecontribution-based or not, taxable or not, and significant points you should be aware of.

Application TaxableChild benefit Universal, though

subject to highincome charge

No

Child tax credits Means-tested NoMaternity allowance Contribution-based NoStatutory Maternity /Paternity/ Adoption Pay

Contribution-based Yes

Income support Means-tested NoJob seeker’s allowance Contribution-based YesWorking tax credits Means-tested NoAttendance allowance Not means-tested NoCarer’s allowance Means-tested YesDLA/PIP Eligibility criteria NoEmployment & SupportAllowance

Contribution-based YesMeans-tested No

Incapacity benefits Contribution-based After 28 weeksStatutory Sick Pay Contribution-based YesSingle-tier state pension

35 years’ cont/credit for fullpension, min 10 years anyentitlement at all

Contribution-based Yes

State pension credit

Savings element no longeravailable for majority ofthose reaching SPA on orafter 6 April 16

Means-tested No

State pension:

Forecast can be obtained online / use form BR19 to find out how many qualifyingyears have been recorded and whether voluntary contributions should be made.

Can be deferred – gain 1% for every 9 weeks of deferral (5.8% a year), no lump sum.Attractive if still work and pay tax at higher rates.

Can be paid outside of UK but increases only paid to those living in EEA / countrieswith a reciprocal arrangement with UK (not Australia, New Zealand, South Africa orCanada)

Essential Study Notes

33Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Universal credit:

To replace income support, income-based JSA, income related ESA, housingbenefit, child tax credit & working tax credit.

Paid monthly to claimants bank/building society account. Claimed online,administered by DWP.

5 elements on top of standard allowance: child/disabled child, childcare, carer, limitedcapability for work and housing.

Subject to benefit cap. Claimant commitment required from both those in and out of work. Deductions made based on earnings/relevant income. Taper rate 65% earned income net of income tax and NIC. Some earnings

disregarded (amount depends on personal circumstances). Unearned income all included and reduced £ for £. Capital in excess of £16,000, no credit. Below that figure capital that is not disregarded treated as if yield monthly income of

£4.35 for each £250 in excess of £6,000.o Capital disregarded include home, business assets, personal possessions,

personal injury/compensation payments, certain annuity payments andpension rights and the value of life insurance policy.

Self-employed deemed to earn minimum income floor (NMW over 35 hours lessnotional tax and NIC).

Long term care costs:

Means-testing capital disregard surrender value life insurance/annuity (incinvestment bond), personal possessions (unless bought to reduce capital/charge),own home if occupied by partner/former partner (unless estranged/divorced), loneparent (who is their estranged/divorced partner), relative 60+, child under 18 ofresident or incapacitated.

Care Act 2014o lifetime cap on care costs £72,000 (not including hotel costs which will be

capped at £12,000 a year).o £118,000 upper limit (currently £23,250), lower £17,000 (currently £14,250) –

sliding scale contribution between the two.o Due April 2020.

Essential Study Notes

34Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

CGT - Exemptions, Losses and Reliefs

General

CGT is payable on profits made on the transfer of ownership/disposal of a chargeable assetin excess of the annual exempt amount (£11,700 in current tax year).

Gains falling within the basic rate tax band are charged to CGT at 10% (18% for residentialproperty gains that aren’t covered by the principal private residence exemption/carriedinterest).

Gains falling above the basic rate tax band are charged to CGT at 20% (28% for residentialproperty gains that aren’t covered by the principal private residence exemption/carriedinterest).

The gain is added to an individual’s taxable income to establish which band it falls into.

If you don’t use your annual exempt amount you lose it. It can’t be carried forward or sharedwith a spouse.

The annual exempt amount should be used in the way that minimises the tax due.

Example

Joan, a higher rate tax payer, made a gain on a buy to let property and a gain on a portfolioof shares.

The annual exempt amount should be set against gain on the buy to let property becausethe tax on this will be charged at 28%, whereas the tax on shares will be charged at 20%.

Some assets are exempt including:

• Private residence• Private motor cars• Directly held Gilts / Qualifying Corporate Bonds• Pension funds• ISAs• Woodlands• National Savings Certificates• EIS (if held for 3 years) / VCT• Gains on gambling• Wasting assets

The main types of disposal include selling, giving away and destroying an asset or the rightto an asset.

Where a sale is made on a commercial basis, the sales proceeds are used for CGT.

If a disposal takes place ‘not at arm’s length’ (i.e. not on a commercial basis), the marketvalue rather than the sale proceeds is used.

Essential Study Notes

35Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

CGT arises on the date a contract for sale becomes binding – even if the money is receivedat a later date. This is known as deferred consideration.

Where there is an ascertainable value, i.e. a fixed amount will be paid at a latertime, that amount is charged to CGT when the sale becomes binding. HMRC willrefund if the sale does not go ahead or may agree to instalment payments if themoney is not expected within 18 months.

Where there is an unascertainable value, i.e. part of the sale price is not known atthe sale date, the market value is used to establish the CGT due with a furthercalculation made when the final payment takes place. If this leads to a loss, the losscan be treated as having been made at the time of the original sale.

The acquisition cost is usually the price at which the asset was bought.

If the asset was inherited, the acquisition cost is deemed to be the value at the date of theformer owner’s death. (CGT is not due on death).

If both income tax and CGT are owed on an asset (perhaps on the sale of a tradedendowment policy), the income tax due can be deducted from the sale proceeds reducingthe gain and, ultimately, the CGT payable.

Where it is not clear whether tax due is income or capital gains, HMRC has a set ofindicators to establish whether the person is trading (income tax) or not (CGT). Theseinclude the nature of the asset, how long it is held for, whether similar transactions haveoccurred, the quantity of the asset purchased, improvements made to the asset, whether theasset is sold in a way that suggests trading, reason for the sale and whether loans are usedto buy the asset which are then repaid from profit.

Transfers between spouses or civil partners are treated on a no gain/no loss basis; thereceiving spouse takes on the gifting spouse’s original acquisition cost rather than the valueat the time of the transfer.

Inter-spouse transfers are only treated this way if the spouses are living together at somepoint during the tax year.

Disposals between spouses after the tax year of separation but before divorce are taxable –the market value would be used rather than the proceeds as the transaction would betreated as not being at arms’ length.

Jointly held assets are taxed in accordance to how they are owned. HMRC assume a 50:50split unless informed otherwise.

Where an asset is of 'negligible value', the owner may claim a disposal for CGT purposeswithout actually disposing of the asset. This will usually result in a loss that can then beoffset against other gains. The deadline for claiming relief for assets becoming negligible in2018/19 is 5 April 2021.

In addition to the acquisition cost being deductible from the proceeds, any incidental costs ofpurchase and sale are also deductible – for example, legal costs, stockbroker fees, estateagent fees, auctioneer fees.

A deduction will also be given for any expenditure on an asset where the purpose of theexpenditure was to enhance its value.

Expenses which are usually claimed against income, such as repairs, are not allowed.

Essential Study Notes

36Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Where an asset was bought prior to the 31st of March 1982 then the acquisition cost will bethe market value at that date and any purchase or enhancement costs before that datecannot be taken into account.

Losses

Must be set against gains in the same tax year even if it means the annual exemptamount is effectively lost

Losses in excess of gains can be carried forward indefinitely, but only need to beused to the extent that the annual exempt amount is fully used

Losses have to be claimed within four years of the end of the tax year in which theyarose

Example

Linda sells two valuable antiques, one of which makes a gain, the other a loss:

Vase: Sale proceeds £50,000, selling costs £5,000, acquisition costs £25,000

- gives a gain of £50,000 - £5,000 - £25,000 = £20,000

Art: Sale proceeds £60,000, selling costs £6,000, acquisition costs £90,000

- gives a loss of £60,000 - £6,000 - £90,000 = (£36,000)

Linda must offset her current year loss of £36,000 against her current year gain of £20,000.This gives her a net loss of £16,000 and she is not, therefore, able to benefit from her CGTannual exempt amount in the current tax year. The net loss of £16,000 can, however, becarried forward to the next tax year.

Had the loss occurred in the previous tax year Linda would only have needed to use enoughof it to reduce her gain for this tax year down to the CGT annual exempt amount, i.e.£20,000 - £11,700 = £8,300, which would mean carrying forward a larger loss to thefollowing tax year of £27,700, i.e. £36,000 - £8,300.

Essential Study Notes

37Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

Reliefs

Entrepreneurs’ relief (ER). Can be claimed on disposal of all or part of a businessafter 5 April 2008. Gains made after 6 April 2011 can be relieved up to £10 millionduring a person’s lifetime. Before then there were lower limits, so if someone hadalready claimed some ER this would need to be deducted from the new £10 millionlimit. Gains that qualify for ER are set against the BRT first, before any non-qualifying gains. The asset disposed of must have been owned for at least a yearbefore disposal in order to qualify (two years from 6 April 2019).

o NB From Oct 2018, if disposing of shares in a trading company where theindividual has a 5% shareholding and is an employee/director, the individualmust also be entitled to 5% of distributable profits and net assets of thecompany

o From 6 April 2019, relief will be available even if the 5% shareholding limit isno longer met on account of the company issuing new shares (i.e. it’s beendiluted)

Investors’ relief (IR) is available to external investors who are not employees/officersof the company whose shares they acquire. 10% rate applies and the limit is £10m(this is in addition to the £10m ER limit). Shares must be newly issued, issued after16.3.16, held for at least 3 years from 6.4.16 and held continually for 3 years untildisposal

Holdover relief – this applies to chargeable lifetime transfers for IHT providing thesettlor does not have an interest in the trust. If claimed, no CGT is payableimmediately but the donee’s acquisition cost is reduced by the amount of the held-over gain which increases the size of the gain when the donee eventually disposes ofthe asset and CGT becomes payable. Has to be claimed jointly by donor and donee.Also, available for gifts of business assets.

Business rollover relief – available where business assets are sold and the proceedsreinvested in other assets for the business. Must be a trading business and assetsused for trading purposes. New assets must have been purchased one year beforeor up to three years after disposal of old assets in order to qualify. Relief only defersgain until the sale of the new assets.

Incorporation relief is available when an unincorporated business is incorporated inexchange for new shares in the company. Any gain is deducted from the issue priceof the shares.

EIS reinvestment – CGT due on a disposal can be deferred if the gain is reinvestedinto EIS shares. Reinvestment must be made within 12 months before or up to threeyears after disposal. The gain is only deferred until the EIS shares are disposed of(unless the proceeds are reinvested into EIS) or the investor dies. Investor gets 30%income tax relief (as a tax reducer) and CGT relief at 10% or 20% as appropriate(18% or 28% if the original gain was residential property not exempt under PPR).

SEIS reinvestment – CGT due on a disposal can be exempted totally if the proceedsare reinvested into SEIS. This is restricted to a limit of 50% of the reinvested gain upto a maximum of £100,000 in the current tax year.

Essential Study Notes

38Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

CGT Calculation, CGT Planning and Trusts

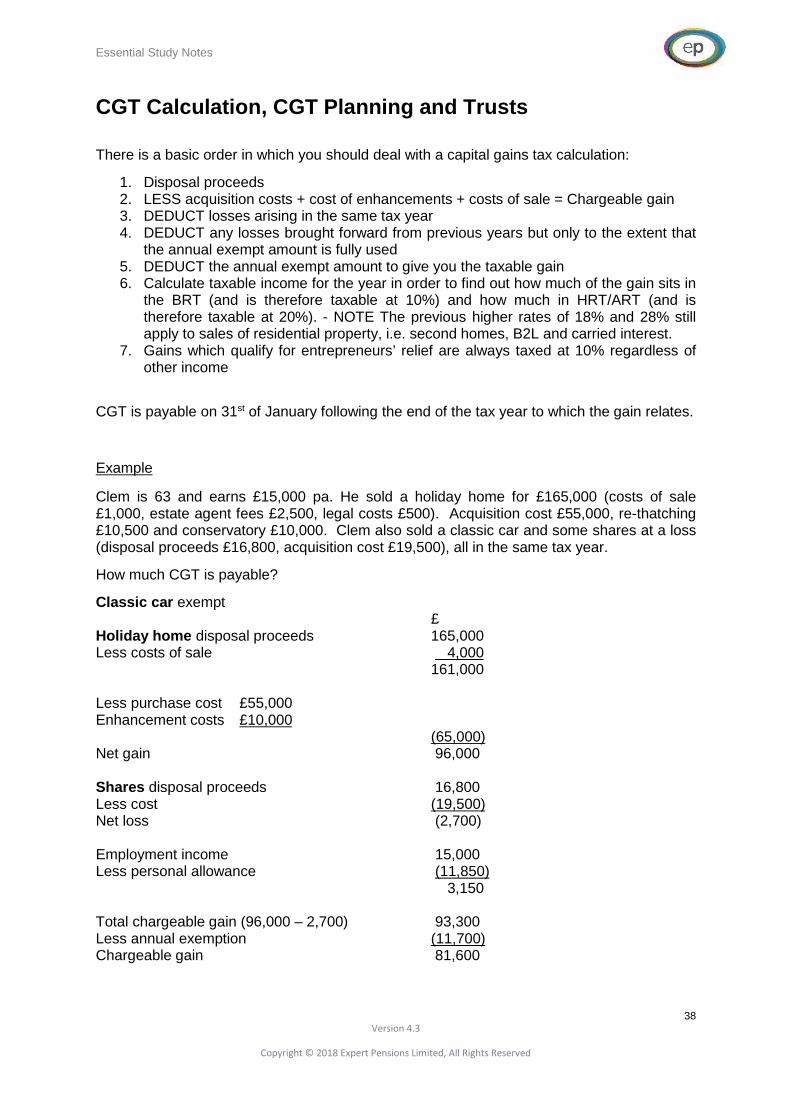

There is a basic order in which you should deal with a capital gains tax calculation:

1. Disposal proceeds2. LESS acquisition costs + cost of enhancements + costs of sale = Chargeable gain3. DEDUCT losses arising in the same tax year4. DEDUCT any losses brought forward from previous years but only to the extent that

the annual exempt amount is fully used5. DEDUCT the annual exempt amount to give you the taxable gain6. Calculate taxable income for the year in order to find out how much of the gain sits in

the BRT (and is therefore taxable at 10%) and how much in HRT/ART (and istherefore taxable at 20%). - NOTE The previous higher rates of 18% and 28% stillapply to sales of residential property, i.e. second homes, B2L and carried interest.

7. Gains which qualify for entrepreneurs’ relief are always taxed at 10% regardless ofother income

CGT is payable on 31st of January following the end of the tax year to which the gain relates.

Example

Clem is 63 and earns £15,000 pa. He sold a holiday home for £165,000 (costs of sale£1,000, estate agent fees £2,500, legal costs £500). Acquisition cost £55,000, re-thatching£10,500 and conservatory £10,000. Clem also sold a classic car and some shares at a loss(disposal proceeds £16,800, acquisition cost £19,500), all in the same tax year.

How much CGT is payable?

Classic car exempt£

Holiday home disposal proceeds 165,000Less costs of sale 4,000

161,000

Less purchase cost £55,000Enhancement costs £10,000

(65,000)Net gain 96,000

Shares disposal proceeds 16,800Less cost (19,500)Net loss (2,700)

Employment income 15,000Less personal allowance (11,850)

3,150

Total chargeable gain (96,000 – 2,700) 93,300Less annual exemption (11,700)Chargeable gain 81,600

Essential Study Notes

39Version 4.3

Copyright © 2018 Expert Pensions Limited, All Rights Reserved

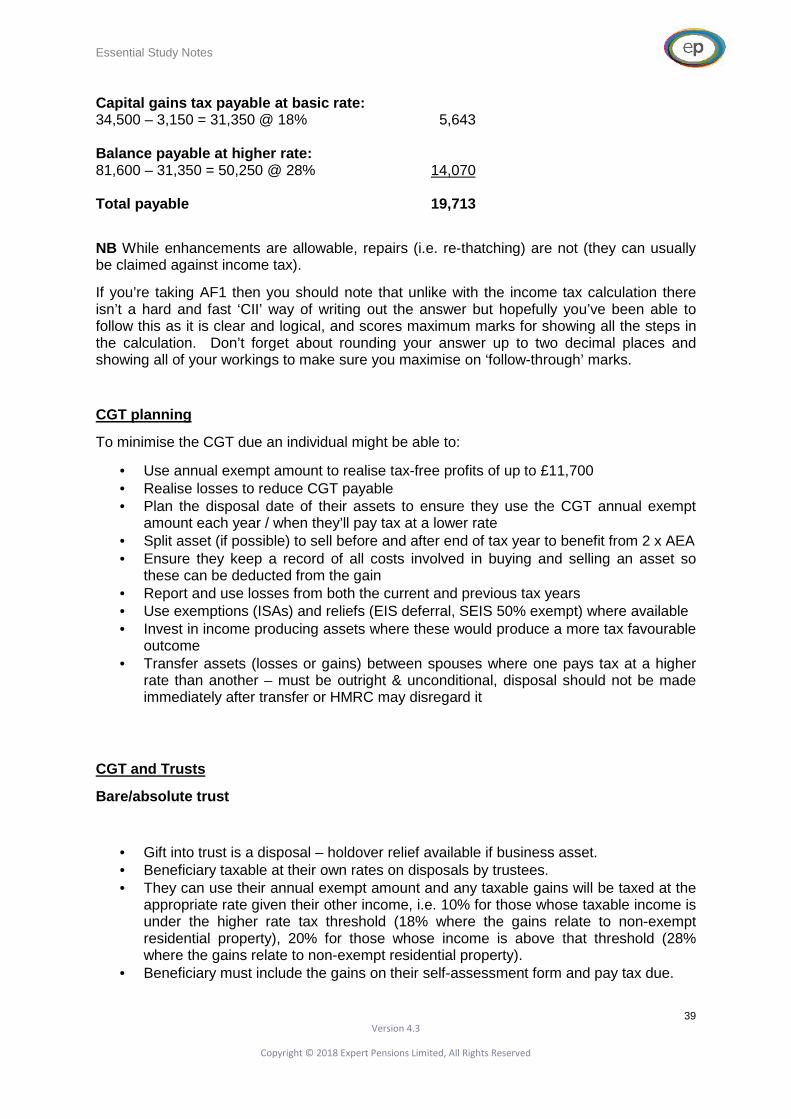

Capital gains tax payable at basic rate:34,500 – 3,150 = 31,350 @ 18% 5,643

Balance payable at higher rate:81,600 – 31,350 = 50,250 @ 28% 14,070

Total payable 19,713

NB While enhancements are allowable, repairs (i.e. re-thatching) are not (they can usuallybe claimed against income tax).

If you’re taking AF1 then you should note that unlike with the income tax calculation thereisn’t a hard and fast ‘CII’ way of writing out the answer but hopefully you’ve been able tofollow this as it is clear and logical, and scores maximum marks for showing all the steps inthe calculation. Don’t forget about rounding your answer up to two decimal places andshowing all of your workings to make sure you maximise on ‘follow-through’ marks.

CGT planning