fy 2005 results and comments - banpu · pdf filejiteng paper mill, mengniu milk, ln heat...

TRANSCRIPT

1

FY 2005 results and commentsINVESTOR & ANALYST UPDATE

24th February 2006

2

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Banpu plc. Nothing in this release should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

3

1. Introduction

2. Focus: China CHP acquisition

3. Operational review

4. Commercial review

5. Financial review

4

1. Introduction

Chanin VongkusolkitChief Executive Officer

5

Record net income at Bt 5,565 m (up 53%)

Trubaindo mine came on-stream, 5mt expected in 2006

Second investment in Chinese coal sector: 40% of Hebi(1 mtpa being expanded to 1.8 mtpa)

Non-core divestments: YBB (calcium carbonate), APBH (oil-fired power), RSA (insurance), ATC stake to 3.7%

Some frustrating delays and slippage in some key operational targets

Highlights of 2005

6

Acquisition of niche co-generation business in China

Other promising acquisition projects under evaluation

Trubaindo first full year of production

BLCP first unit completion

Banpu team is stronger and more focused than ever before

Brief look at the year ahead

OpportunitiesChallenges

Indonesian coal export tax ($1.5/t on FOB prices of $30/t or more) ? [Unfortunate, but now seems likely]

Impact of softer coal prices and short term earnings outlook

7

Banpu regional snapshot: 2006

Indominco-Bontang

Jorong Kitadin-Embalut

LP-2 CMMC

Daning

Trubaindo

Coal mining operation

Coal mining project

Barasentosa

Bharinto

Power plant operation

Power plant project

RatchBLCP

Hebi

CHINA

THAILAND

INDONESIA

Bengbu*

Luannan*

Zouping*Zhengding*

* Share Purchase Agreement signed on February 9, 2006

Newly acquired operation

8

A new cash flow structure is evolving …

Recent cashflowstructure

Cashflow structure by 2008 (existing assets*)

Coal represents c.90% of pre-capex cash flows, over 70% from Indonesia

Coal Indonesia

Coal Thailand

Power, other

CONCEPTUAL & ILLUSTRATIVE ONLY

Coal Indonesia

Coal China

China Power

Thai Power

Coal represents about 2/3 of cashflows going forward with China gradually replacing Thailand

Power represents about 1/3 of pre-capex cashflows

* Nb. New acquisitions and investments could alter this expectation

9

The Banpu jigsaw puzzle is gradually taking shape !

Thailand

Indonesia

China

Other ?

Coal Power

Banpu’s long term strategy envisages a matrix of diversified coal-based energy businesses spanning several Asian countries.

But Banpu is working towards its strategic goals opportunistically, seizing value-creating opportunities as they arise.

Non-core divestments

10

2. Focus: China CHP acquisition

Chanin VongkusolkitChief Executive Officer

11

Deal summary

Banpu has acquired a coal-fired co-generation business in China from AEC (a US utility group) for US$84.3 million in cash

Business consists of four plants with total power capacity of 279MW and steam capacity of 1,000 tph

Plants benefit from favorable regulation, captive steam markets and priority dispatch for electricity

Deal should provide platform for further growth for Banpu in the Chinese coal-based energy sector

12

Production capacities of plants acquired

Plant name

Zhengding

Luannan

Zouping

Bengbu

Shareholding

100%

100%

70%

64%

Power capacity Steam capacity

49 MW

100 MW

50 MW

80 MW 440 tph

160 tph

240 tph

160 tph

CHP: ‘Combined Heat & Power’ (co-generation)

13

Electricity power consumptions (billion kWh)

Xinjiang

Gansu

Heilongjiang

Jilin

Liaoning

Taiwan

Tibet

Sichuan

Yunnan

GuangxiGuangdong

Fujian

Shandong

Hubei

Hunan Jiangxi

Hainan

Inner Mongolia

Ningxia

Qinghai

Hebei

Shanxi

Henan Anhui

Zhejiang

JiangsuShaanxi

Guizhou

Beijing

Luannan: Jing Jin Tang Grid

Zhengding: Hebei South Grid

Zouping: Shandong Grid

Bengbu: Anhui Grid

Northwest Grid

Tibet Grid

South Grid

Middle Grid EastGrid

North Grid

Northeast Grid

2004 2005

75.2 85.2

138.9 160.5

163.9 191.1

51.5 58.2

%

13%

16%

17%

13%

14

Off-take arrangements

Plant name

Zhengding

Luannan

Zouping

Bengbu

Power

Off-takers

Steam

Off-takers

Off-take

(GWh)

Off-take

(Mt)

255 0.76Hebei Power

PPA to 2022

N. China Power

PPA to 2015

ZP Power

PPA to 2021

Anhui Power

PPA to 2021

Industrial,

residential,

ZD Heat

Jiteng Paper Mill,

Mengniu Milk, LN Heat

Bengbu H&P

SPA to 2020

Xiwang (sugar),

Sanxing (oil)

SPAs to 2021-2

169 0.6620042005

20042005

518617

0.540.53

407372

1.270.83

515464

1.121.28

2003131

537

352

439

2003 0.67

0.35

0.59

1.49

231 2006f

481

378

343

2006f 0.67

0.54

1.20

1.00

15

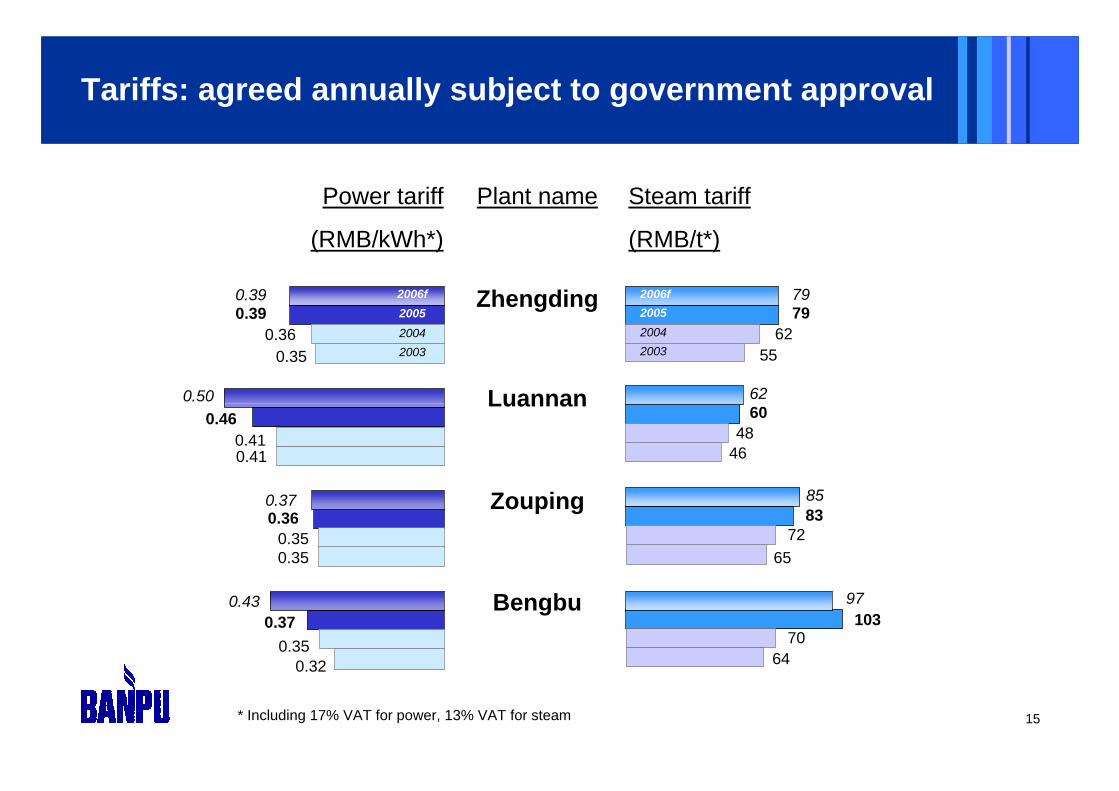

Tariffs: agreed annually subject to government approval

Plant name

Zhengding

Luannan

Zouping

Bengbu

Power tariff

(RMB/kWh*)

Steam tariff

(RMB/t*)

0.39

0.46

0.36

0.37

79

60

83

103

* Including 17% VAT for power, 13% VAT for steam

0.36

0.41

0.35

0.35

62

48

72

70

20042005

20042005

20030.35

0.41

0.35

0.32

2003 55

46

65

64

0.39 2006f

0.50

0.37

0.43

792006f

62

85

97

16

Coal sourcing and prices

ZhengdingShanxi Province

RMB 363 /t

Sources Prices 2005* CHP plant

LuannanHebei Province

RMB 441 /t

ZoupingShanxi Province

RMB 451 /t

BengbuAnhui Province

RMB 561 /t

70% of coal price changes** passed through to power and steam tariffs

** Subject to price movement of more than 5% in any 6m period; new regulations since May 2005* Average: mix of contract and spot price agreements; prices are for delivered coal, including transport costs to plants

Coal Consumption

2005* (Mt)

0.25

0.29

0.31

0.33

17

-

100

200

300

400

500

600

700

800

900

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

Comparison of average coal prices and power tariffs

2003 2004 2005 2006

Avg. coal price (RMB/t)

Avg. power tariff (RMB/kWh)

ZD: Zhengding

LN: Luannan

ZP: Zouping

BB: Bengbu

ZD LN ZP BB ZD LN ZP BB ZD LN ZP BB ZD LN ZP BB

Power tariffs (RHS)

Coal prices (LHS)

18

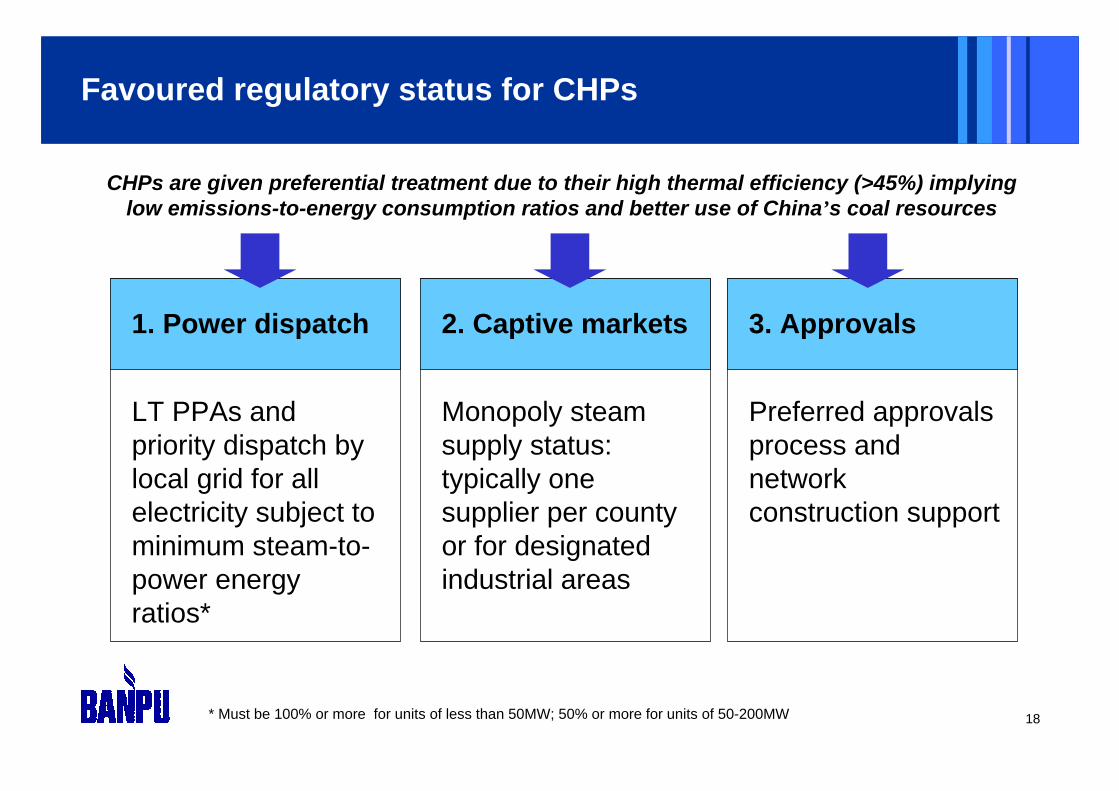

Favoured regulatory status for CHPs

1. Power dispatch

LT PPAs and priority dispatch by local grid for all electricity subject to minimum steam-to-power energy ratios*

CHPs are given preferential treatment due to their high thermal efficiency (>45%) implying low emissions-to-energy consumption ratios and better use of China’s coal resources

2. Captive markets

Monopoly steam supply status: typically one supplier per county or for designated industrial areas

3. Approvals

Preferred approvals process and network construction support

* Must be 100% or more for units of less than 50MW; 50% or more for units of 50-200MW

19

China CHP business: EBITDA summary (2005)

Zhengding100%

Luannan100%

Zouping70%

Bengbu64%

TotalOH

$5M

$10M

$15M

$20M

$25M

$3.7M

$10.2M

$7.0M

$2.9M

- $3.1M

$20.7M*

EBITDA

2005 ($M)

* Un-audited equity EBITDA figures

20

Integration of new management teams into Banpu (nb. existing management are highly qualified with extensive experience working to western professional standards)

Brownfield expansion of the existing plants (backed by high growth in new steam demand)

Improvement of plant operating efficiency

Refinancing opportunity

Work with local management to identify and secure further CHP acquisitions

Going forward …

Value

Creation

Plan

21

3. Operational review

Rawi CorsiriChief Operating Officer

22

Estimated 2006 production at 21m tonnes (exclud. China)

Indominco-Bontang8.2 mt

Jorong3.1 mt

Kitadin-Embalut1.6 mt

Thailand3.1 mt

Daning4 mt

(Banpu 12.5%)

Trubaindo5 mt

100% basis

Hebi1 mt(Banpu 40%)

23

Coal reserves increased to 260 million tonnes

218

2004Reserves

2005Reserves

2005production

Equity tonnes

Units: million tonnesBharinto:

+27

IMM E.Block: +17

Hebi: +14

260

(16)

Engineering studies

Acquisition

24

Coal production review and outlook

Indominco-BontangCV 6,500 kcal/kg

Lower output due to maintenance work at

Bontang port in 4Q051.9 1.8 1.8

1Q05 3Q05

SR 9.2:1 10.6:1

1Q 2Q 3Q

SR 9.5 7.2

.8

3Q

.8

1Q

SR 4.4

.8

2Q

3.7

Kitadin-EmbalutCV 6,000 kcal/kg

JorongCV 5,300 kcal/kg

LP-2 / CMMCCV 4,000 kcal/kg

2.2

4Q05

.3

4Q05

TrubaindoCV 6,950 kcal/kg

Slow production during the first year of operation

12.1:1

7.1

4.4

.9

4Q05Smooth production supported by strong

domestic sales

1Q

.1 .6

3Q

Strong output recovery during 2H05

Annual production was slightly better than plan

2Q

2Q05

.5 .4

1Q 2Q 3Q 4Q05

.4

4Q05

.5

.9.5 .7 .9

SR 5.5 6.2 6.7

SR 6.7

.5

2.2

1Q06F

.2

1Q06F

.7

1Q06F

.9

1Q06F

.9

1Q06F

11.2:1

8.0

5.4

2.8

8.5

25

CHINA

DANING

• Location: Shanxi province

• Investment: USD 32M (12.49% interest)

• Reserves : 75 Mt. Anthracite

• Production : 5 Mtpa

• Method : Underground longwall

• Market : Domestic power and fertilizerplants

• Logistics : Short – distance rail and truck

• Status : Operational

HEBI ZHONG TAI MINING CO. (HTZM)

• Location : Henan province

• Investment : USD 38M (40% interest)

• Reserves : 34Mt. Semi-anthracite

• Production : 1 Mtpa, expandable to 1.8 Mtpa by 2008

• Method : Underground longwall

• Market : Domestic power, steel mills,and fertilizer plants

• Status : Operational; Banpu to do equity account in 2Q06

China coal operations

26

China coal projects progress review

Daning - Longwall

Underground Mine

27

China coal projects progress review

Daning: Coal processing facilities

28

China coal projects progress review

Daning

29

China coal projects progress review

Hebi

30

BLCP plant progress view

• Location : Map Ta Put Industrial Estate

• Banpu % : 50%

• Capacity : 1,434 MW

• Fuel : Coal (approximately 3 mtpa)

• COD : Oct06 and Feb07(c. 700MW each unit)

Under constructionc. 93% completion*

Value

Development

Ship unloading facilities

9 Jan 06

Power plant

Stack

Boiler#1 Boiler#2

Coal stock yard

* As of January 31, 2006

31

Unloading port

32

Arrival of first coal shipment, cape size

11 February 2006

33

Unloading test

34

Unloading test

35

First coal pile on stockyard

36

4. Commercial review

Rawi CorsiriChief Operating Officer

37

10

20

30

40

50

60

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

e

BJI

Weighted avg

Indominco

Average Selling Prices (ASP)

ASP 2005 : $35.2 per tonne (+37% YoY)

ASP 2006e : $34 per tonne (-3% YoY)US$/Tonne

Contracted sales

2006

Unpriced

Priced

39%

61%

BJI*

Feb 23th: $47.0

Note: *Barlow Jonker Index (BJI) based on CV 6,700 kcal/kg GAD from Australia to JapanSource: Barlow Jonker

38

Customer distribution

Philippines7%

Indonesia3%

Japan, Korea,

Taiwan, Hong Kong

53%

India5%

Italy12%

Thailand14%

Others6%

Coal sales by value: Bt 25bn in 2005

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Thai mines

Jorong

Kitadin-Embalut

Indominco-Bontang

Trubaindo

Japa

n,

Kor

ea,

Taiw

an, H

K

Thai

land

Indi

a

Phi

lippi

nes

Indo

nesi

a

Italy

Oth

ers

Coal sales by volume: 17 Mt in 2005Mt

38%

32%

8%6%

6%5%5%

39

Major coal customers in 2005

Customer

SCC

ENEL

SCCC

Chubu

EPDC

Kowepo

Adani

TCC

TPIPL

Hoping

Coal & Oil

TNB

PLN Paiton

NPC Pagbilao

PLN Asam Asam

Country

Thailand - c

Italy - p

Thailand - c

Japan - p

Japan - p

Korea - p

India - g

Thailand - p

Thailand - c

Taiwan - p

India - g

Malaysia - p

Indonesia - p

Philippines - p

Indonesia - p

Coal MT

1.4 mt

1.3 mt

1.0 mt

0.9 mt

0.8 mt

0.7 mt

0.7 mt

0.6 mt

0.6 mt

0.6 mt

0.5 mt

c. 0.5 mt

0.4 mt

0.4 mt

0.3 mt

Starting 2H06

40

5. Financial review

Somruedee SomphongChief Financial Officer

41

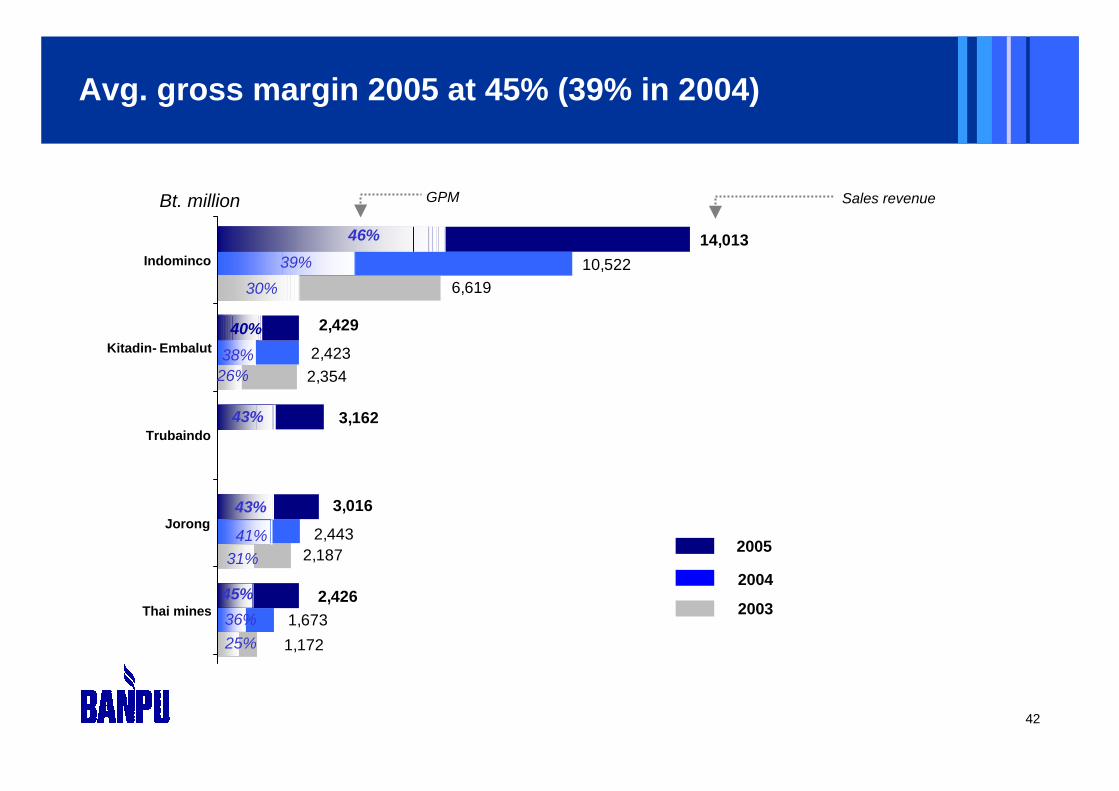

25,046

12,331

17,062

2003 2004 2005

Sales revenues: coal business

Note : Revenues from other businesses (e.g. industrial minerals) are not included

Units: Bt. million

• 9% increase in sale volume

• 37% increase in selling price

+47%

Y on Y

42

6,619

2,354

2,187

1,172

10,522

2,423

2,443

1,6732,426

3,016

3,162

2,429

14,013

Thai mines

Jorong

Trubaindo

Kitadin-Embalut

Indominco

Bt. million GPM Sales revenue

Thai mines

Jorong

Trubaindo

Kitadin- Embalut

Indominco

46%39%

30%

38%

43%

41%31%

45%36%25%

40%

26%

43%

2005

2004

2003

Avg. gross margin 2005 at 45% (39% in 2004)

43

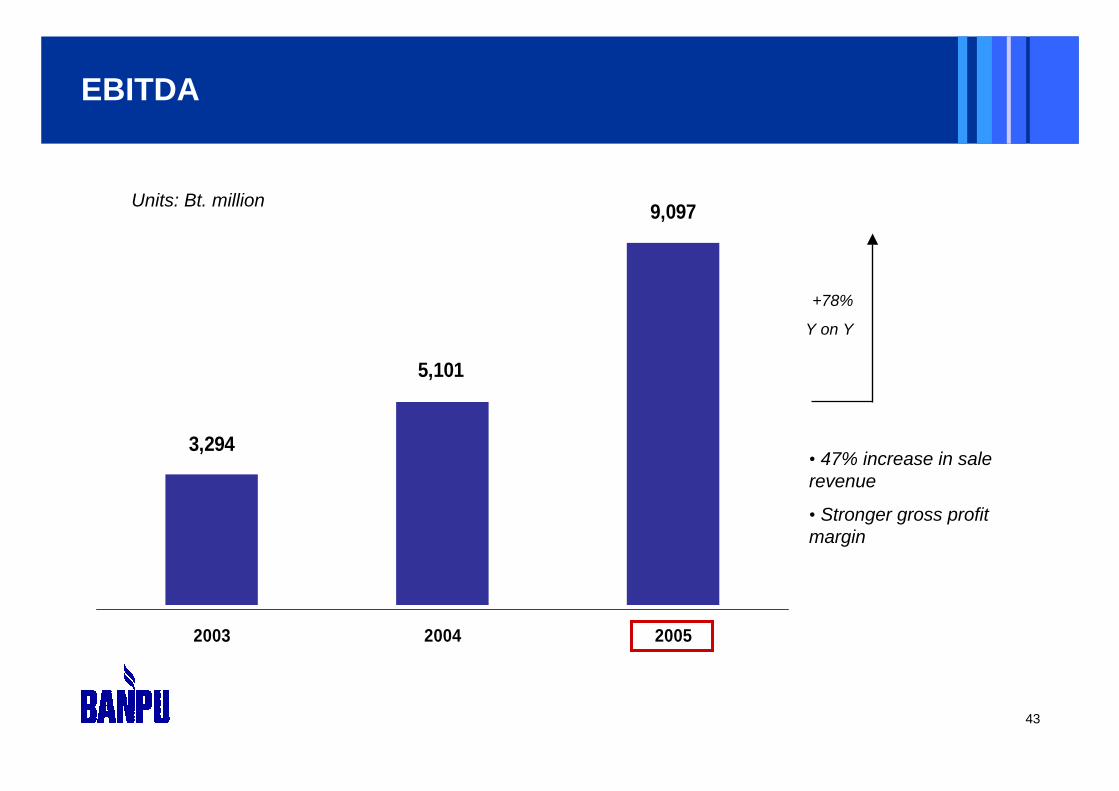

9,097

5,101

3,294

2003 2004 2005

Units: Bt. million

EBITDA

+78%

Y on Y

• 47% increase in sale revenue

• Stronger gross profit margin

44

Medium term (2005-08) CAPEX plans: $611million

Units: USD million

59

63

147

73

120

BLCPCoal ChinaCoal Indonesia

73

180

Committed Pre-feasibility ConceptualStatusCoal projects

Power projects

Indominco 12Trubaindo 47AACI 30Hebi 38

BLCP 147Peak 84

Bharinto 45Indominco 28

Indonesia 30China 120

China 30

The capital expenditure figures shown above are indicative only and do not include estimates for maintenance or sustaining capital expenditure. The figures shown in the ‘Conceptual’ column should be treated with extra caution and are likely to change as new projects are conceived, some are cancelled and as pre-feasibility analyses generate modified estimates of capital expenditure requirements.

Power China

84

358

Note: Spent in FY2005

30

30

45

0.34

0.250.240.230.24

0.56

2003 2004 1Q05 2Q05 3Q05 4Q05

Floating 9%

Fixed 91%

Strong balance sheet

Debt structureNet D/E (Times)

Net gearing (%)

As end of December 2005

36%

20% 20% 20% 20%25%

46

Dividend payments

55.54

2.6

3.5

4

2002 2003 2004 2005

Dividend per share (Bt)

(1H05)

(Special)

(2H05)

47

APPENDICES

48

China CHP business: ownership structure

Banpu Power Ltd

PPIC IEC

Zhengding Luannan Zouping Bengbu

100% 70%100%

90.9% 100%

64%

ShijiazhuangChengfeng Cogen Co.

Tangshan Peak Heat & Power Co Ltd

Zouping Peak Heat & Power Co Ltd

Anhui New Energy Heat & Power Co Ltd

Singapore co. China JV or WFOE co.

49

Zhengding - background

Zhengding CHP plant

49MW+160tph

Commenced operation 2000; expansion in 2004. Further expansion being studied

Ownership: 100%

WFOE* status

185 employees

Hebei Power accounts for 58% sales

Main industries in Zhengding County: tourism, furniture and food

Hebei Province facing power shortages in recent years. Shortages likely to remain.

* Wholly-Owned Foreign Enterprise

50

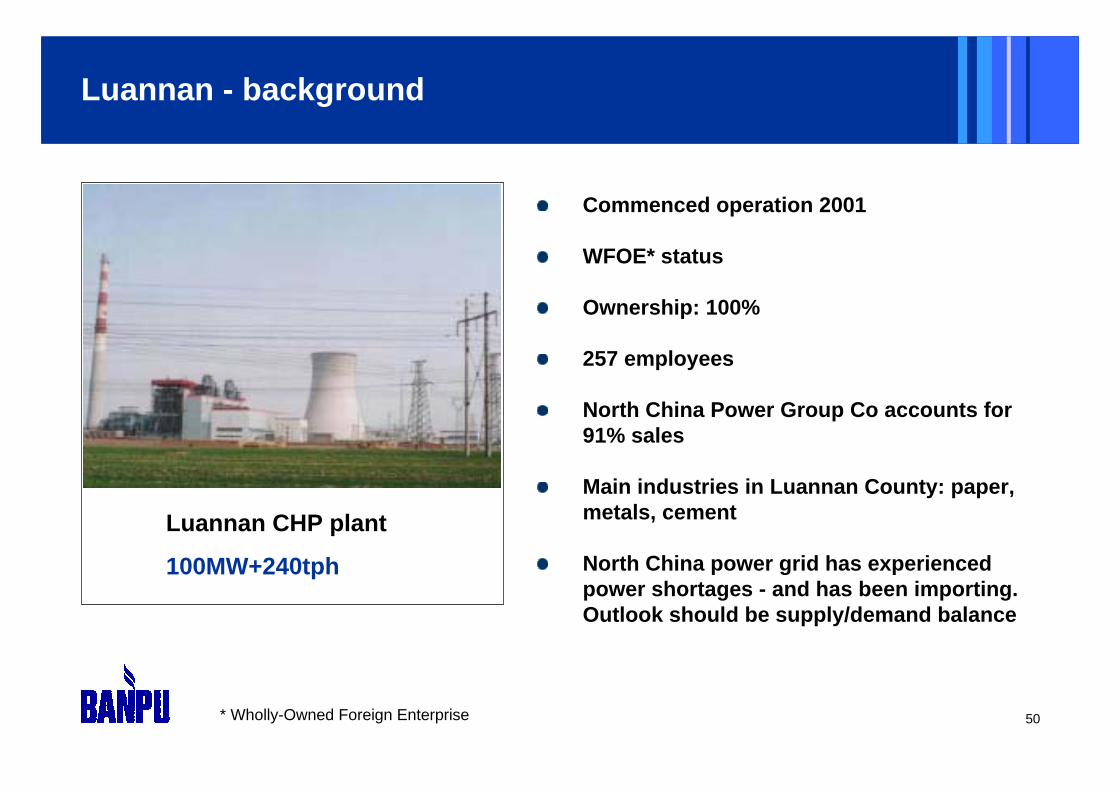

Luannan - background

Luannan CHP plant

100MW+240tph

Commenced operation 2001

WFOE* status

Ownership: 100%

257 employees

North China Power Group Co accounts for 91% sales

Main industries in Luannan County: paper, metals, cement

North China power grid has experienced power shortages - and has been importing. Outlook should be supply/demand balance

* Wholly-Owned Foreign Enterprise

51

Zouping - background

Zouping CHP plant

50MW+160tph

Commenced operation 2001. Expansion of 25MW currently under construction.

Ownership 70%

Company JV status; partner (30%) is Zouping County Power Co (‘ZP Power’)

253 employees

ZP Power accounts for 70% sales

Main industries in Zouping County: textiles (China’s No.1 textile area), agriculture

Power supply in Zouping County and Shandong Province is in surplus

52

Bengbu - background

Bengbu CHP plant

80MW+440tph

Commenced operation 1989. Expansion currently under consideration.

Ownership: 64%

Company JV: partners Bengbu H&P (30%), Transpacific Capital (6%)

707 employees

Anhui Power accounts for 64% sales

Main industries in Bengbu County: chemicals, agricultural product processing, glass, mechanical parts

Slight power shortage in Anhui Province

53

Bengbu - background

Bengbu CHP plant

Commenced operation 1989. Expansion currently under consideration.

Ownership: 64%

Company JV: partners Bengbu H&P (30%), Transpacific Capital (6%)

707 employees

Anhui Power accounts for 64% sales

Main industries in Bengbu County: chemicals, agricultural product processing, glass, mechanical parts

Slight power shortage in Anhui Province

54

China CHP business: financial summary (2005)

Plant name

Zhengding

Luannan

Zouping

Bengbu

Revenues

$ 16.8 M

$ 28.1 M

$ 26.9 M

$ 31.8 M

EBITDA

$ 3.7 M

$ 10.2 M

$ 7.0 M

$ 2.9 M

NPAT

$ 0.8 M

$ 6.1 M

$ 2.9 M

$ 0.2 M

External debt (YE)

$ 9.9 M

-

$ 3.7 M

$ 9.1 M

55

China CHP business: utilization hours (2005)

Plant name

Zhengding

Luannan

Zouping

Bengbu

Utilization (Hours)

6,482

5,857

8,700

7,334

56

Chinese power sector: key statistics 2005

Indicator

Total installed capacity

Of which:

Thermal

Hydro

Nuclear

Power generation

Of which:

Thermal

Hydro

Nuclear

2005

508.4 GW

384.1 GW

116.5 GW

6.9 GW

2,475 bn kWh

2,018 bn kWh

395 bn kWh

52 bn kWh

% increase y-o-y

14.9%

16.6%

10.7%

0.1%

12.8%

11.5%

19.4%

3.7%

Source: China Electricity Council

57

Chinese power sector: key statistics 2005 (continued)

Indicator

Hours of operation *

Thermal

Hydro

Nuclear

Power supply

Transmission loss

Coal efficiency*

Coal consumption*

2005

5,411 hrs

5,876 hrs

3,642 hrs

7,554 hrs

2,158 bn kWh

7.18%

374g/kWh

984 Mt

Increase y-o-y

-44 hrs

-115 hrs

180 hrs

-51 hrs

14.2%

-0.4%

-2g

Source: China Electricity Council * Plants over 6MW

58

Operating profit

Units: Bt. million

Sales revenues 7,189 5,400 -4% 33%Cost of sales (4,400) (3,004)Gross profit 2,789 2,396 -22% 16%GPM 39% 44%SG&A (1,266) (682)Royalty (667) (545)Equity income - Power (30) 59Dividend income - Power - -Other income 16 83EBIT 842 1,311 -64% -36%EBITDA 1,860 1,665 -39% 12%

4Q05 4Q04 QoQ % YoY %

7,508(3,923)

3,58548%(645)(850)

0 217

322,3403,033

3Q05

59

Units: Bt. million

EBIT 842 2,340 1,311 -64% -36%Interest expenses (166) (149) (93)Financial expenses (57) (62) (36)Income tax (core business) (181) (548) (250)Minorities (26) (72) (27)Net profit before extra items 412 1,509 906 -73%Non-recurring items* 499 390 571Income tax (non-core business) (164) (152)Unrealized gain on coal swap contract (3) (3) 24Bond redemption premium - - -Mining property expense (17) (19) (15)Net profit 727 1,724 1,227 -58% -41%FX translations (2) (41)Net profit 725 1,683 1,148 -57% -37%EPS (Bt/share) 2.66 6.19 4.22

Note: * Income from non-core assets and other non-operating expenses

4Q04 YoY %4Q05 3Q05 QoQ %

Net profit

-33%

(258)

(80)

60

Operating profit

Units: Bt. million

Sales revenues 25,208 46%Cost of sales (13,933)Gross profit 11,275 68%GPM 45%SG&A (2,935)Royalty (2,548)Equity income - Power (126) Dividend income - Power 457Other income 208EBIT 6,332 75%EBITDA 9,097 78%

2005 YoY %

17,227(10,525)

6,70239%

(2,003)(1,700)

(22) 413219

3,6095,101

2004

61

Units: Bt. million

EBIT 6,332 3,609 75%Interest expenses (509) (412)Financial expenses (220) (141)Income tax (core business) (1,480) (823)Minorities (186) (67)Net profit before extra items 3,936 2,166Non-recurring items* 2,563 1,904Income tax (non-core business) (738) (381)Unrealized gain on coal swap contract (8) 24Bond redemption premium - -Mining property expense (72) (61)Net profit 5,682 3,651 56%FX translations (117) (6)Net profit 5,565 3,645 53%EPS (Bt/share) 20.48 13.42

Note: * Income from non-core assets and other non-operating expenses

YoY %2005 2004

Net profit

82%

62

Banpu’s Resources & Reserves statement (100% basis)

--34.4-34.473.5-73.540.00Hebi Zhongtai

75.0110.073.9-73.9107.335.072.312.49Daning No. 1

300.81,037.2363.675.2288.41,220.6375.3845.2Total

32.838.832.812.320.538.80.738.194.99Barasentosa

-85.928.56.322.2218.482.5135.994.04Bharinto

Project

2.22.41.6-1.61.8-1.8100.00Payao

7.27.94.2-4.24.6-4.6100.00Lampang

67.2307.465.830.035.8305.7134.7171.085.49Trubaindo

21.0155.919.25.114.2153.751.0102.794.98Kitadin

62.4283.972.916.156.8275.371.5203.894.98Indominco

33.145.030.20.829.441.6-41.695.00Jorong

Mine operation

Total Reserves

Total Resources

Total Reserves

Probable Reserves

Proved Reserves

Total Resources

Indicated Resources

Measured Resources

As at 31 December 2004

As at 31 December 2005Interest

(%)Mine operation and project