fy 2011 results analyst briefing - telekom … · this presentation may not be copied or otherwise...

TRANSCRIPT

FY 2011 RESULTS

ANALYST BRIEFING

24 February 2012

This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase, any securities

and neither this presentation nor anything contained in it shall form the basis of, or be relied on in connection with any contract or commitment or

investment decision.

This presentation has been prepared solely for use at this presentation. By your continued attendance at this presentation, you are deemed to

have agreed and confirmed to Telekom Malaysia Berhad (the “Company”) that: (a) you agree not to trade in any securities of the Company or its

respective affiliates until the public disclosure of the information contained herein; and (b) you agree to maintain absolute confidentiality

regarding the information disclosed in this presentation until the public disclosure of such information, or unless you have been otherwise

notified by the Company.

Reliance should not be placed on the information or opinions contained in this presentation or on its completeness. This presentation does not

take into consideration the investment objectives, financial situation or particular needs of any particular investor.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the

information, opinions and conclusions contained in this presentation. None of the Company and its affiliates and related bodies corporate, and

their respective officers, directors, employees and agents disclaim any liability (including, without limitation, any liability arising from fault or

negligence) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with it.

This presentation contains projections and “forward-looking statements” relating to the Company’s business and the sectors in which the

Company operates. These forward-looking statements include statements relating to the Company’s performance. These statements reflect the

current views of the Company with respect to future events and are subject to certain risks, uncertainties and assumptions. It is important to note

that actual results could differ materially from those anticipated in these forward looking statements. The Company does not undertake to inform

you of any matters or information which may come to light or be brought to the Company’s attention after the date hereof.

The forecasts and other forward-looking statements set out in this presentation are based on a number of estimates and assumptions that are

subject to business, economic and competitive uncertainties and contingencies, with respect to future business decisions, which are subject to

change and in many cases outside the control of the Company. The directors and officers of the Company believe that they have prepared the

forecasts with due care and attention and consider all best estimates and assumptions when taken as a whole to be reasonable at the time of

preparing the presentation. However, the Company’s forecasts presented in this presentation may vary from actual financial results, and these

variations may be material and, accordingly, neither the Company nor its directors or officers can give any assurance that the forecast

performance in the forecasts or any forward-looking statement contained in this presentation will be achieved. Details of the forecasts and the

assumptions on which they are based are set out in the presentation.

This presentation may not be copied or otherwise reproduced without the written consent of TM.

Disclaimer

Performance Overview

Financial review

Operating highlights

Concluding remarks

3

Key Highlights FY 2011 Achieved all Headline KPI’s for 2nd year

4

• Revenue growth of 4.1% vs. FY2010 to RM9.15bn

• Normalised EBITDA Margin at 33.5%

• Customer Satisfaction Measure 70

FY2011Headline KPI

FY2011 Achievement

2.5%

32%

4.1%

33.5%

>70

Broadband leadership continues:• Total customer base of over 1.9mn

•Over 230,000 Unifi customers activated, takeup rate >20%

• Internet & Multimedia Revenue grew >20% in FY2011• BAU Capex/Revenue improved to 12.4% compared to 12.8% last year

• Achieved 1.16mn premises passed with FY2011 HSBB Capex of RM1.4bn, lower than budgeted

• Final single-tier dividend of 9.8 sen per share•Proposed capital repayment of 30 sen per share via capital reduction

Key Operating Indicators

Key Highlights 4Q 2011

Financial Performance

Positive growth across the boardQoQ and YoY

4Q11 vs3Q11

5

Operating revenue grew by 5.4% QoQ and 5.5% YoY to RM2,447.2mn

- Revenue led by Internet & Multimedia, at 4.2% growth QoQ and

23.8% growth YoY

Normalised EBITDA up 0.6% QoQ and 1.5% YoY to RM808.1mn

Normalised PATAMI up 74.9% QoQ and 0.7% YoY to RM240.1mn

Broadband subscribership grew 2.8% QoQ and 12.3% YoY to 1.92mn customers.

TM Wifi hotspot zones increased by 14.4% QoQ and 80.3% YoY, to 19,799 sites

4Q11 vs4Q10

1.1

4.2

12.4

60.1%

10.6%

1.11.21.4

Cash Balance (RM bn) 2.1 3.5 3.5

2008

Capital Expenditure, excluding HSBB(RM bn)

Our capital management approach is guided by two major principles :

Striving to optimize capital productivity and ROIC

Creating shareholder value with strong commitment to dividend policy

1 TRS: Source Bloomberg2 After interim dividend paid in September 2011 (RM351mn), and final gross dividend 2010 & capital distribution paid in June 2011 (RM1,037.4mn)3 Normalised EBIT / Total Revenue

16.7 14.1

2009 2010

12.8

Focus on Shareholder Value CreationGrowing enterprise value through improving return on capital

1Total Return to Shareholder (TRS)

7.7% 42.9% 24.0%

EBIT Margin 10.8%10.9% 10.6%3

Capex / Revenue ratio( %)

6

FY2011

2

Performance Overview

Financial review

Operating highlights

Concluding remarks

7

Note: EBITDA Margin is calculated as percentage of EBITDA against Revenue + Other Operating IncomeFor Normalised EBITDA and Normalised PATAMI refer Slides 10 & 11

•Excludes FX (Gain )/Loss

RMmn

ReportedComments

(FY11 vs FY10)4Q11 3Q11

% Change QoQ

4Q10% Change

YoYFY11 FY10

% ChangeFY11 vs

FY10

Revenue 2,447.2 2,321.7 +5.4 2,320.6 +5.5 9,150.7 8,791.0 +4.1Higher Internet & Multimedia and Others revenue

Other Operating Income

37.0 27.8 +33.1 52.7 -29.8 120.9 152.9 -20.9 -

EBITDA 796.1 812.5 -2.0 758.6 +4.9 3,086.4 2,924.3 +5.5Higher revenue and lower operating cost

EBITDA margin 32.0% 34.6% -2.6pp 32.0% 0.0pp 33.3% 32.7% +0.6pp -

Normalised EBITDA 808.1 803.3 +0.6 795.9 +1.5 3,108.4 2,958.5 +5.1 -

Normalised EBITDA Margin

32.5% 34.2% -1.7pp 33.5% -1.0pp 33.5% 33.1% +0.4pp -

Depn & Amort. 535.9 580.7 -7.7 565.7 -5.3 2,128.0 1,995.8 +6.6Higher asset base and provisionfor asset write-off

Other Gains 5.5 278.3 -98.0 215.4 -97.4 286.5 373.3 -23.3 -

Net Finance Cost* 50.6 50.9 -0.6 57.9 -12.6 185.2 245.2 -24.5Better yield income and lower interest expense

FX (Gain) / Loss (14.4) 122.5 +111.8 15.8 +191.1 58.6 (303.7) -119.3USD strengthened vs. RM by 3.5%

Profit Before Tax 229.6 337.2 -31.9 334.8 -31.4 1,001.2 1,360.2 -26.4 -

PATAMI 598.3 302.2 +98.0 400.7 +49.3 1,191.0 1,206.5 -1.3Unrealised forex loss on USD debts nett of last mile tax incentive

Normalised PATAMI 240.1 137.3 +74.9 238.4 +0.7 634.8 563.7 +12.6 -

Group Results 4Q11 & FY2011

8

In RM mn 4Q11 3Q11 4Q10 FY11 FY10

Reported EBITDA 796.1 812.5 758.6 3,086.4 2,924.3

Non Operational

ESOS (Income) - net - - - - (5.0)

Loss on Sale of Assets 0.3 0.2 1.0 1.3 2.1

FX (Gain)/Loss on International trade Settlement

12.9 (9.4) 20.9 21.9 21.7

AFS Impairment/(Write back) – Receivables (1.2) - 15.4 (1.2) 15.4

Normalised EBITDA 808.1 803.3 795.9 3,108.4 2,958.5

Normalised EBITDA Margin 32.5% 34.2% 33.5% 33.5% 33.1%

Reported EBITDA Margin 32.0% 34.6% 32.0% 33.3% 32.7%

Normalised EBITDA

EBITDA is calculated as Total Revenue (Operating Revenue + Oth. Operating Income) less Operating Cost (Exc. Depreciation, Amortisation & Impairment).EBITDA Margin is calculated as percentage of EBITDA against Total Revenue

9

Improving margins due to higher operating revenue

In RM mn 4Q11 3Q11 4Q10 FY11 FY10

Reported PATAMI 598.3 302.2 400.7 1,191.0 1,206.5

Non Operational

ESOS (Income) - net - - - - (5.0)

FX (Gain)/Loss on International trade settlement

12.9 (9.4) 20.9 21.9 21.7

(Gain)/Loss on Sale of Assets and Investments* (5.2) (278.1) (214.4) (285.2) (371.2)

Unrealised FX (Gain)/Loss on Long Term loans (14.5) 122.6 15.8 58.5 (303.7)

Impairment of AFS receivables (1.2) - 15.4 (1.2) 15.4

Last Mile Tax Incentives for prior years (350.2) - - (350.2) -

Normalised PATAMI 240.1 137.3 238.4 634.8 563.7

Normalised PATAMI

* Comprise fair value (FV) changes of FVTPL (FV through P&L) investment and gain/loss on disposal for AFS (available for sale) investments, mainly due to disposal of Axiata shares (2010: Axiata & Measat)

10

22.3 23.0

20.4 18.0

18.9 19.8

11.6 11.3

5.6 6.3

5.7 6.1

4.3 4.40.7 0.8

FY10 FY11

Bad Debt

Marketing Expenses

Supplies & material

Maintenance Cost

Other operating cost

Manpower cost

Direct cost

Dep & Amortisation

Revenue = Operating Revenue + Other Operating Income

Cost % of Revenue1

Note: The classification of cost is as per financial reporting

(Please refer to Appendix for quarterly details & breakdown)

Cost/revenue ratios maintained YoY

1

11

RM mnRM mn

Total Cost / Revenue ( %)

RM8,015.4

89.6%

RM8,313.2

89.7%

FY 2011 vs. FY 2010•Higher Depreciation & Amortisationmainly due to higher asset base, provision for asset write-off nett of change of useful life impact

•Lower Direct Cost mainly due to lower domestic interconnect and international outpayment

•Higher Manpower cost mainly due to higher staff benefits

•Higher Maintenance Cost mainly due to NGN, new IP core maintenance contracts and equipment rental

•Higher Marketing Expenses mainly due to higher commissions in line with Unifi growth

% of Revenue

1,102 1,060

838 976

772 527

0

500

1,000

1,500

2,000

2,500

3,000

FY10 FY11

Access Core Network Support System*

511 401

308343

309 395

0

200

400

600

800

1000

1200

FY10 FY11Access Core Network Support System*

591 659

530633

463 132

0

200

400

600

800

1000

1200

1400

1600

1800

FY10 FY11

Access Core Network Support System*

Group Capital Expenditure

** Gross capex to be shared with Government equally1H2010 capex has been restated to include IPTV

Note: Government coinvestment treated as deferred income, to be amortisedprogressively to match against the depreciation of assets

*Include Application, Support System &Others (building, land improvement, moveable plants,application & other assets)

Capex/Revenue ratios continued to improve

12

Total Capex

HSBB Capex**

Note : BAU – Business As Usual

RM mn

2,712

1,584

30.8

BAU Capex

1,128

12.8

Capex / Revenue ( %)

1,424

1,139

12.4

2,563

28.0

15.618.0

30 June 11 31 Dec 10 30 June 11 31 Dec 10Return on Invested Capital 6.10% 6.03% Gross Debt to EBITDA 1.93 2.09

Return on Equity 8.65% 7.67% Net Debt/EBITDA 0.69 0.90

Return on Assets 4.65% 4.73% Gross Debt/ Equity 0.92 0.72

Current Ratio 1.65 1.62 Net Debt/ Equity 0.32 0.27

WACC 6.33% 6.58% Net Assets/Share (sen) 194.8 216.1

2

2 Based on Normalised PATAMI, comparative for Dec’10 is amended to be consistent with current year computation

31 Dec 11

Group Cash Flow & Key Financial Ratios

31 Dec 10

RM mn FY11 FY10

Cash & cash equivalent at start 3.488.0 3,490.2

Cashflows from operating activities 3,030.7 2,973.4

Cashflows from / (used-in) investing activities (1,338.0) (1,446.9)

Capex* 1,808.5 2,198.9

Cashflows from financing activities (962.5) (1,534.2)

Effect of exchange rate changes (5.6) 5.5

Cash & cash equivalent at end 4,212.6 3,488.0

Free cash-flow (EBITDA – Capex) 1,277.9 725.4

•net of HSBB grant received from Government (FY11 – RM754.5mn, FY10 - RM513.1mn)

Strong Balance Sheet to support futurebusiness requirements

1

Based on Normalised EBIT1

1

13

31 Dec 1031 Dec 11

Performance Overview

Financial review

Operating highlights

Concluding remarks

14

Voice41%

Data20%

Internet22%

Others17%

Voice44%

Data20%

Internet19%

Others17%

441 400506

1,521 1,597

4Q10 3Q11 4Q11 FY10 FY11

437519 541

1,653 2,001

4Q10 3Q11 4Q11 FY10 FY11

490 456 4831,754 1,819

4Q10 3Q11 4Q11 FY10 FY11

953 947 9173,863 3,734

4Q10 3Q11 4Q11 FY10 FY11

Group Total Revenue by Product

15

Data

RM mn

RM mn RM mn

Voice

Others

InternetFY11

FY10

RM mnRM mn

RM mn

RM9,151mn

RM8,791mn

-3.2%

-3.8% -3.3%

+4.2%

+23.8% +21.1%

+5.9%

-1.4% +3.7%

+26.5%

+14.7% +5.0%

Revenue growth driven by Internet, YoY growth >20%

Retail77%

Global10%

Wholesale9%

Others4%

115 98 93

338 343

4Q10 3Q11 4Q11 FY10 FY11

276215 256

915 845

4Q10 3Q11 4Q11 FY10 FY11

193 191 201

755 770

4Q10 3Q11 4Q11 FY10 FY11

585 629 639 2,264 2,459446 458 473

1,772 1,838358 370 368

1,4311,462

347 361 417

1,3161,433

4Q10 3Q11 4Q11 FY10 FY11

Consumer SME Enterprise Government

Retail79%

Global9%

Wholesale8%

Others4%

Group Total Revenue by Line of Business

16

FY11

FY10

RM9,151mn

RM8,791mn

* Others comprise revenue from Property Development, TM R&D, TMIM, UTSB and MKL

Retail Wholesale

RM mn

RM mnRM mn

RM mn

1,8971,8171,736

Note: Due to lower bandwidth sales

Global Others*

+19.1%

-7.2% -7.7%

6,7837,192

-5.1%

-19.1% +1.5%

+4.4%

+9.3% +6.0%

+5.2%

+4.1% +2.0%

Retail contribution to group revenue increases, led by Consumer & Govt

Net adds (in thousand)

1,212 1,261 1,311 1,393 1,417 1,425 1,393 1,374

273 280 285 287 291 296 314 3124 14 33 64 109 164 237

-

400

800

1,200

1,600

2,000

2,400

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

Residential Business UniFi

2,763 2,775 2,794 2,799 2,710 2,692 2,633 2,566

1,553 1,558 1,533 1,535 1,607 1,596 1,568 1,546

4 14 33 64 109 164 237

0

1,000

2,000

3,000

4,000

5,000

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11Residential Business UniFi

In thousand

In thousand

-0.4%

+12.3%

-0.4%

1,485

+2.8%

4,316

Physical Highlights

Broadband Customer Growth

Fixed Line Customer Growth

WiFi Hotspot Zones

+80.3%

+14.4%

*Call Usage Only ** Streamyx Gross ARPU only ^ Streamyx Net ARPU

1,545

+60

4,337 4,341

+65

1,610

+103

1,713

4,367

Note: inclusive of NBI initiative

17

Broadband growth driven by Unifi

+59

1,772

4,381

ARPU (RM) 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

Fixed Line (DEL)* 35 35 35 34 33 34 34 34

Streamyx Broadband** 82 81 77 78 77^ 77^ 78^ 78^

1,830

+58

4,397

1,871

+41

4,365 4,349

+52

1,923

2,245 2,533 2,432

10,982 13,251 16,111 17,313 19,799

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

3,60312,456

28,771 55,15693,107

139,896 201,842

448

1,445

4,1258,385

15,912

24,47934,659

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

Residential Business

UniFi – leading & shaping the future

18

UniFi update as at 22 February 2012

Delivered 1,179,000 premises passed covering 79 exchanges

HSBB ARPU as at 31 Dec 2011 is RM184

Unifi takeup continues to exceed expectations

Activated more than 283,000 customers - highest in Southeast Asia, Top 10 in Asia Pacific (source: FTTH Council Asia Pacific)

4,051

13,901

32,89663,541

+43.9%

+10

Net adds (in thousand)

109,019

+19 +31 +45

+618.9%

164,375

+55 +72

236,501

Signed HSBB Services Agreement with with 11 property developers to deploy HSBB network infrastructure and services to new housing developments

ARPU (RM) 1Q11 2Q11 3Q11 4Q11

Unifi (Blended) 188 186 184 184

Performance Overview

Financial review

Operating highlights

Concluding remarks

19

Key Takeaways

Financial Performance

Focus on Excellence

Shareholder Value

Broadband Champion

Customer-centricity

Achievement of all Headline KPIsRevenue growth of 4.1% vs. FY2010; KPI: 2.5% growthNormalised EBITDA margin of 33.5%; KPI: 32%• Internet & Multimedia revenue as main driver• Continuous focus on profitability and cost

Achievement of new Headline KPITRI*M index score of >70; KPI: 70• Strong commitment to delivering enhanced customer experience and quality improvement programmes

Continued operational improvementsHigher operating revenue, capex efficiency and better EBITDA marginHSBB rollout targets achieved – 1.16mn premises passed;

fastest rollout in region

Malaysia’s broadband champion1.92mn total broadband (Streamyx and Unifi) customersUnifi takeup rate at >20% (over 236,000 customers)• wider coverage, increased installation efficiencyHSBB a global success story

20

Commitment to create shareholder value• Total dividend payout of RM700mn (including interim dividend of RM350.6mn paid in September 2011)•Capital repayment of 30 sen per share by way of capital reduction totalling RM1.073bn

21

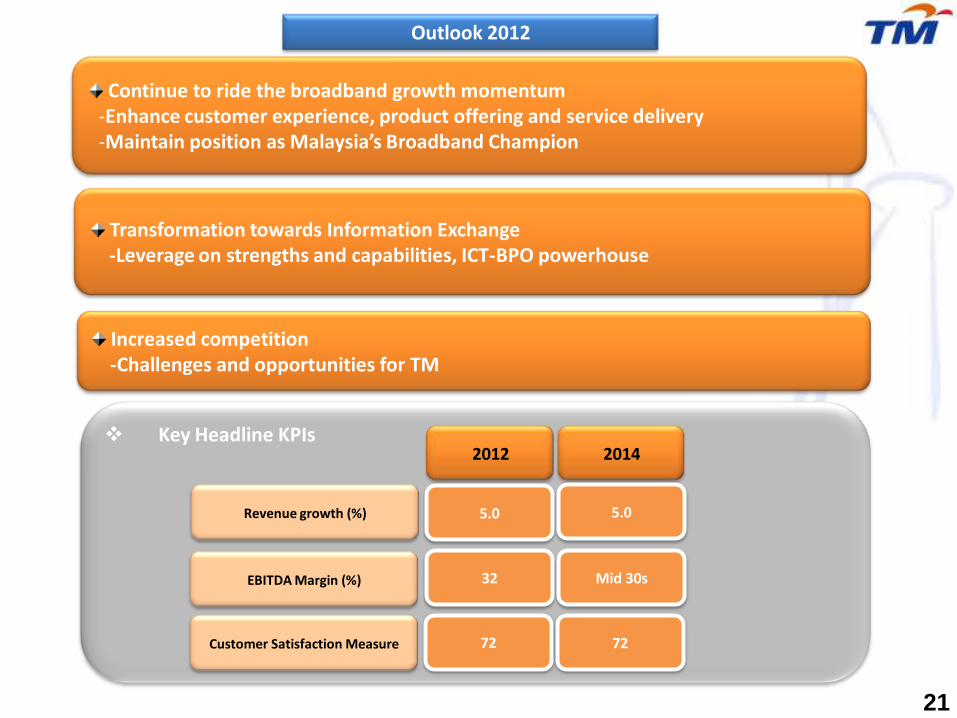

Increased competition-Challenges and opportunities for TM

Outlook 2012

Transformation towards Information Exchange-Leverage on strengths and capabilities, ICT-BPO powerhouse

Key Headline KPIs2012 2014

Revenue growth (%)

EBITDA Margin (%)

Customer Satisfaction Measure

5.0 5.0

32 Mid 30s

72 72

Continue to ride the broadband growth momentum-Enhance customer experience, product offering and service delivery-Maintain position as Malaysia’s Broadband Champion

Appendices

4Q11 3Q11 4Q10 FY11 FY10 FY11 vs FY10

Operating Revenue (RM mil) 2,447.2 2,321.7 2,320.6 9,150.7 8,791.0 -

Other Operating Income(RM mil)

37.0 27.8 52.7 120.9 152.9 -

Direct Costs % 16.8 18.0 19.4 18.0 20.4 Lower interconnect and international outpaymentRM mil. 417.3 423.4 460.1 1,665.9 1,825.4

Manpower % 19.1 19.5 20.9 19.8 18.9 Higher staff benefits, higher welfarefund paymentsRM mil. 475.4 458.3 497.2 1,838.4 1,692.9

Supplies & Materials % 6.7 5.9 7.4 6.1 5.7 Higher customer acquisition cost, customer projects and cable costRM mil. 165.9 139.5 176.0 570.1 514.1

Bad & Doubtful Debts % 0.8 0.3 0.8 0.8 0.7Higher trade bad debt at Consumer

RM mil. 19.8 6.8 18.3 72.8 66.9

Marketing Expenses % 5.2 4.7 3.7 4.4 4.3Higher commissions, lower A&P

RM mil. 129.7 109.7 87.8 407.7 385.7

Maintenance Cost % 7.4 6.9 5.1 6.3 5.6 Higher maintenance cost for NGN, new IP core maintance contracts, equipment rentalRM mil. 184.8 162.4 121.4 587.0 498.9

Other Operating Costs % 11.9 10.1 10.7 11.3 11.6

Lower building rentalRM mil. 295.2 236.9 253.9 1,043.3 1,035.7

Depreciation & Amortisation % 21.6 24.7 23.8 23.0 22.3 Higher asset base, new asset additions and asset impairmentRM mil. 535.9 580.7 565.7 2,128.0 1,995.8

Total (RM mil) 2,224.0 2,117.7 2,180.4 8,313.2 8,015.4 -

Total (%) 89.5 90.1 91.9 89.7 89.6 -

Cost % of Revenue

23

6,968.8

162.9

10,053.9

6,402.7

1,559.6

2,072.7

18.9

17,185.6

6,925.6

1,444.6

506.8

4,213.0

761.2

4,186.2

3,552.1

7.7

626.4

2,739.4

13,613.0

833.2

17,185.6

7,709.4

150.8

8,630.3

5,506.0

1,664.2

1,432.1

28.0

16,490.5

6,938.5

1,801.5

527.8

3,488.5

1,120.7

4,289.5

3,639.2

26.0

624.3

2,649.0

13,112.1

729.4

16,490.5

Shareholders’ Funds

Non-Controlling Interests

Deferred & Long Term Liabilities

Long Term Borrowings

Deferred Tax

Deferred Income

Derivative financial liabilities

Current Assets

Trade Receivables

Other Receivables

Cash & Bank Balances

Others

Current Liabilities

Trade and Other Payables

Short Term Borrowings

Others

Net Current Assets

Property Plant & Equipment

Other Non-Current Assets

RM MillionAs at 31 Dec 2011 As at 31 Dec 2010

Group Balance Sheet

24

3,177 3,081

871 982

1,637 1,982

1,4541,589

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY10 FY11

OthersInternetDataVoice

787 775 752

215 266 230

431514 535

394374 520

0

600

1200

1800

2400

4Q10 3Q11 4Q11

Others

Internet

Data

Voice

Consumer33%

SME26%

Enterprise21%

Government20%

Consumer34%

SME26%

Enterprise20%

Government20%

Total Revenue By Products

RM mn +4.4%

1,736

FY11

+9.3%

RETAIL

Revenue by ProductRevenue by Business Unit

FY10

Note: Total revenue is after inter-co elimination. Revenue of product is before inter-co elimination

RM mn

RM mn

RM7,192mn

RM6,783mn

25

RM mn +6.0%

6,7837,192

1,8171,897

256 224

566 597

65 85

0

200

400

600

800

1000

FY10 FY11

Others

Data

Voice

58 54 54

154 151 155

23 22 23

0

50

100

150

200

250

4Q10 3Q11 4Q11

Others

Data

Voice

ASP17%

MC83%

ASP16%

MC84%

MC : Malaysian CarrierASP : Application Service Provider

Others : Include internet

WHOLESALE

FY11

FY10

Note: Total revenue is after inter-co elimination. Revenue of product is before inter-co elimination 26

RM mn +2.0%

755 770

Revenue by ProductRevenue by Customer Segment

RM mn +5.2%

193

+4.1%

191 201

446 478

82 70

411 344

288

0

200

400

600

800

1000

1200

FY10 FY11

Others

Data

IRU Sales (Data)

Voice

111143 126

82 10 56

86

66

104

5

2

2

0

50

100

150

200

250

300

350

4Q10 3Q11 4Q11

Others

Data

IRU Sales (Data)

Voice

Africa & Middle East

6%America

13%

Europe10%

South Asia34%

North Asia17%

Oceania10%

Others10%

Africa & Middle East

9%

America7%

Europe11%

South Asia38%

North Asia14%

Oceania7%

Others14%

FY11

FY10

Others : Include internet

GLOBAL

Note: Total revenue is after inter-co elimination. Revenue of product is before inter-co elimination27

Revenue by RegionRevenue by Product

RM mn -7.7%

915845

RM mn +19.1%

276

-7.2%

215

256

THANK YOUAny queries please email to : [email protected]

•Investor Relations• Level 11 (South Wing)•Menara TM •JlnPantaiBharu •50672 Kuala Lumpur, Malaysia • Tel (603) 2240 4848/ 7366 / 7388