gdf suez appendices - engie · appendices - contents business ... business case: peru ... ilo 21...

TRANSCRIPT

APPENDICESGDF SUEZ

2Investor Day GDF SUEZ – November 26, 2008

Appendices - Contents

Business Lines Appendices

- Energy Europe and International Business Line 4

- Benelux/Germany Energy Division 5

- Energy Europe Division 8

- Energy International Division 11

- Energy France Business Line 20

Pages

BUSINESS LINES APPENDICES

GDF SUEZ

BUSINESS LINES APPENDICES

GDF SUEZ

Energy Europeand InternationalBusiness Line

Benelux/GermanyEnergy Division

BUSINESS LINES APPENDICES

GDF SUEZ

6Investor Day GDF SUEZ – November 26, 2008

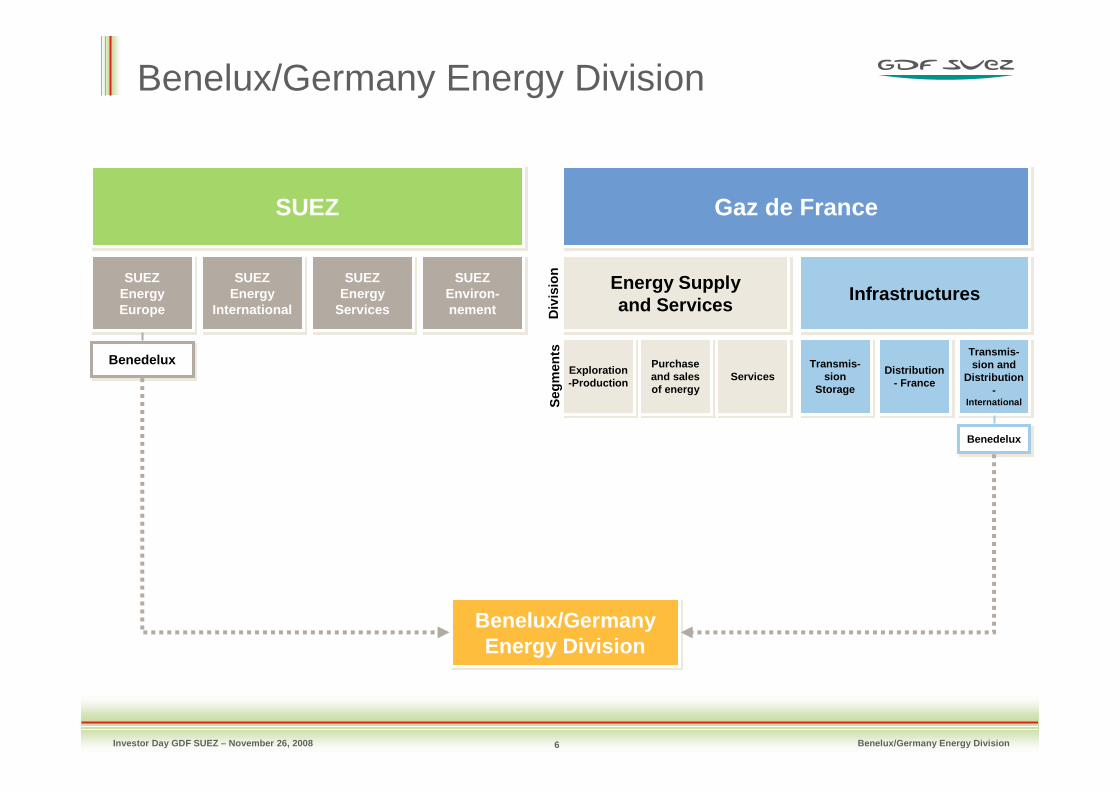

Benelux/Germany Energy Division

Gaz de FranceGaz de FranceSUEZSUEZ

Energy Supplyand Services

Energy Supplyand Services InfrastructuresInfrastructures

Benelux/Germany Energy Division

Benelux/Germany Energy Division

SUEZEnergy Europe

SUEZEnergy Europe

SUEZEnergy

International

SUEZEnergy

International

SUEZEnergy

Services

SUEZEnergy

Services

SUEZEnviron-nement

SUEZEnviron-nement

Exploration -ProductionExploration -Production

Purchase and sales of energy

Purchase and sales of energy

ServicesServicesTransmis-

sionStorage

Transmis-sion

Storage

Distribution- France

Distribution- France

Transmis-sion and

Distribution -

International

Transmis-sion and

Distribution -

International

BenedeluxBenedelux

BenedeluxBenedelux

Div

isio

nS

egm

ents

Benelux/Germany Energy Division

7Investor Day GDF SUEZ – November 26, 2008

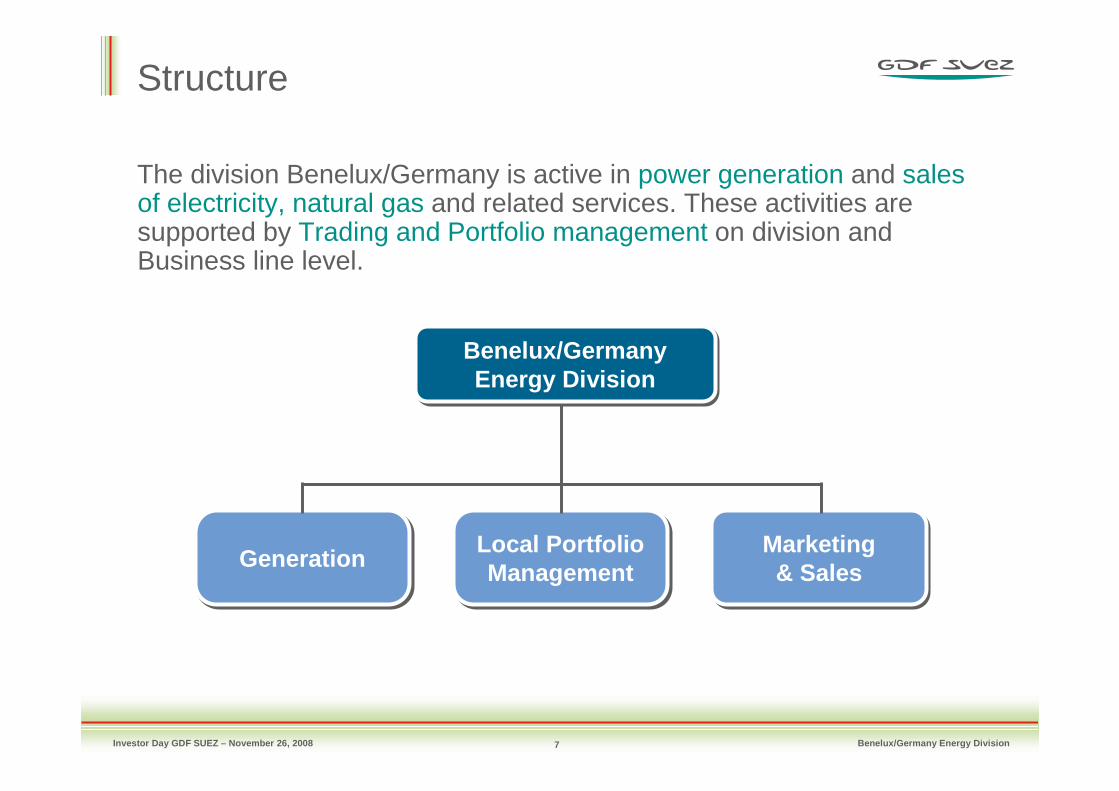

Structure

The division Benelux/Germany is active in power generation and sales of electricity, natural gas and related services. These activities are supported by Trading and Portfolio management on division and Business line level.

GenerationGeneration Local PortfolioManagement

Local PortfolioManagement

Marketing& Sales

Marketing& Sales

Benelux/GermanyEnergy Division

Benelux/GermanyEnergy Division

Benelux/Germany Energy Division

Energy EuropeDivision

BUSINESS LINES APPENDICES

GDF SUEZ

9Investor Day GDF SUEZ – November 26, 2008

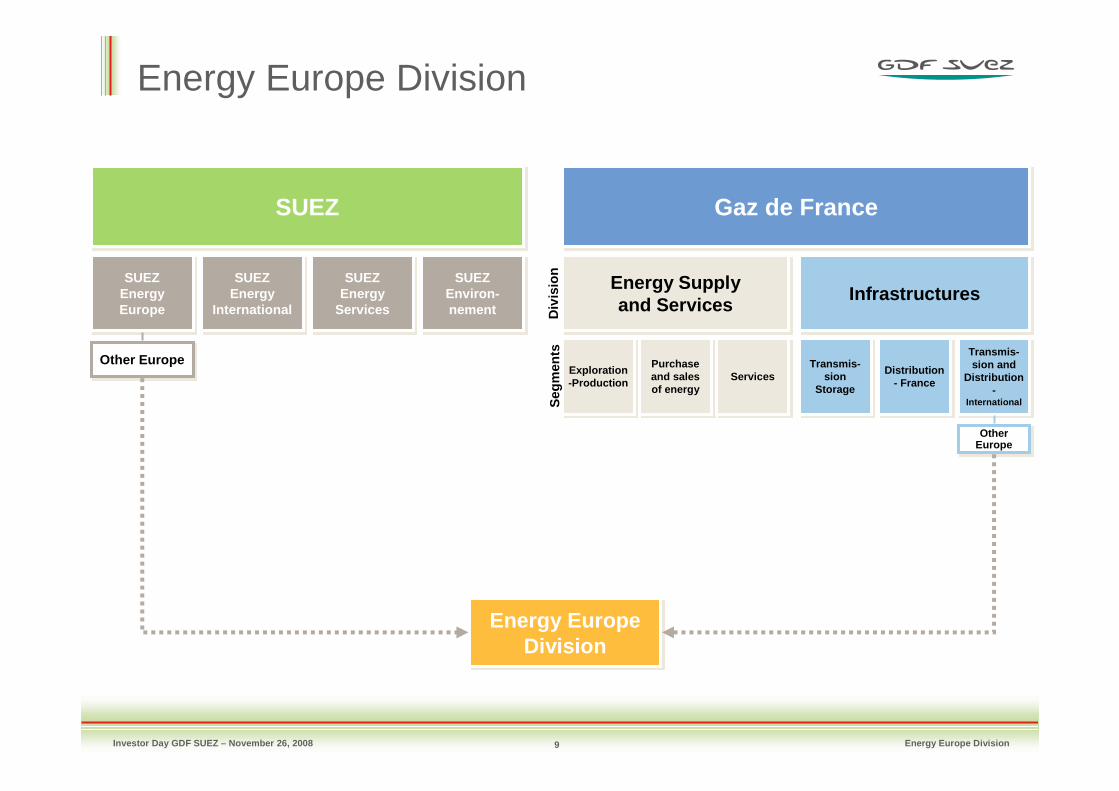

Energy Europe Division

Gaz de FranceGaz de FranceSUEZSUEZ

Energy Supplyand Services

Energy Supplyand Services InfrastructuresInfrastructures

Energy Europe Division

Energy Europe Division

SUEZEnergy Europe

SUEZEnergy Europe

SUEZEnergy

International

SUEZEnergy

International

SUEZEnergy

Services

SUEZEnergy

Services

SUEZEnviron-nement

SUEZEnviron-nement

Exploration -ProductionExploration -Production

Purchase and sales of energy

Purchase and sales of energy

ServicesServicesTransmis-

sionStorage

Transmis-sion

Storage

Distribution- France

Distribution- France

Transmis-sion and

Distribution -

International

Transmis-sion and

Distribution -

International

Other EuropeOther Europe

Other EuropeOther

Europe

Div

isio

n

Energy Europe Division

Seg

men

ts

10Investor Day GDF SUEZ – November 26, 2008

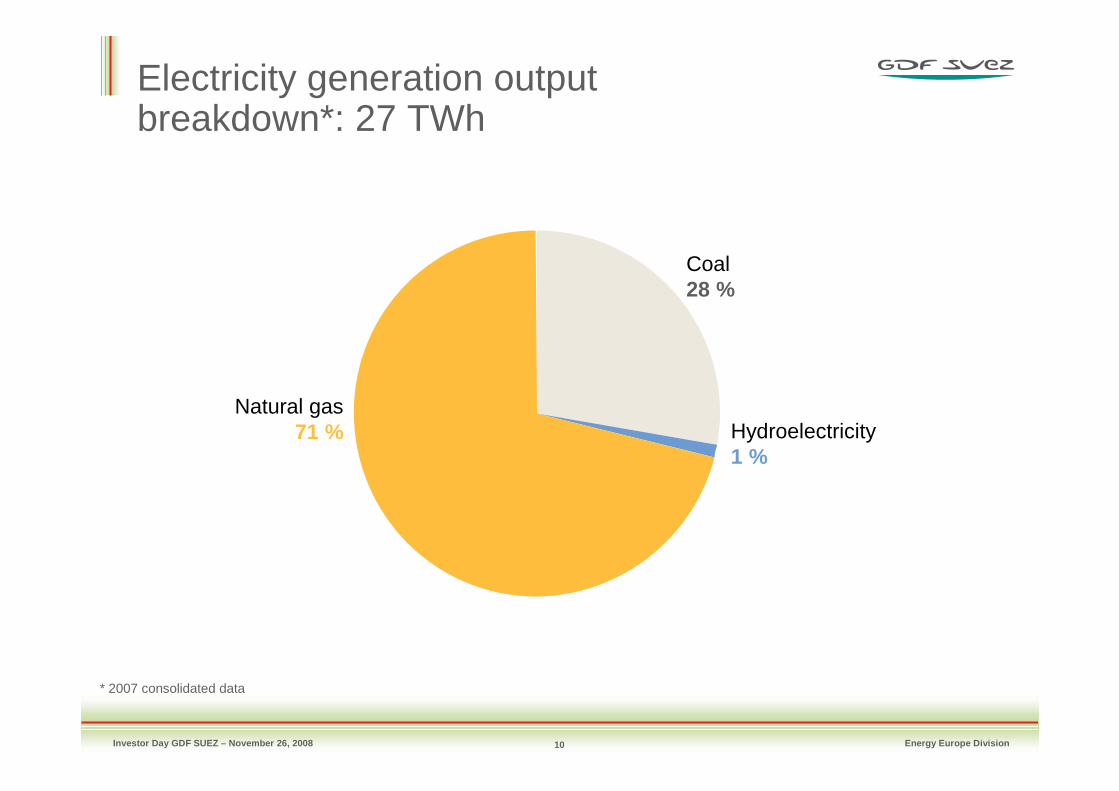

Electricity generation outputbreakdown*: 27 TWh

* 2007 consolidated data

Natural gas71 %

Coal28 %

Hydroelectricity1 %

Energy Europe Division

Energy InternationalDivision

BUSINESS LINES APPENDICES

GDF SUEZ

12Investor Day GDF SUEZ – November 26, 2008

Energy International Division

Gaz de FranceGaz de FranceSUEZSUEZ

Energy Supplyand Services

Energy Supplyand Services InfrastructuresInfrastructures

Energy International Division

Energy International Division

SUEZEnergy Europe

SUEZEnergy Europe

SUEZEnergy

International

SUEZEnergy

International

SUEZEnergy

Services

SUEZEnergy

Services

SUEZEnviron-nement

SUEZEnviron-nement

Exploration -ProductionExploration -Production

Purchase and sales of energy

Purchase and sales of energy

ServicesServicesTransmis-

sionStorage

Transmis-sion

Storage

Distribution- France

Distribution- France

Transmis-sion and

Distribution -

International

Transmis-sion and

Distribution -

International

North America,

Latin America,

Middle-East-Asia

North America,

Latin America,

Middle-East-Asia InternationalInternational

Div

isio

n

Energy International Division

Seg

men

ts

13Investor Day GDF SUEZ – November 26, 2008

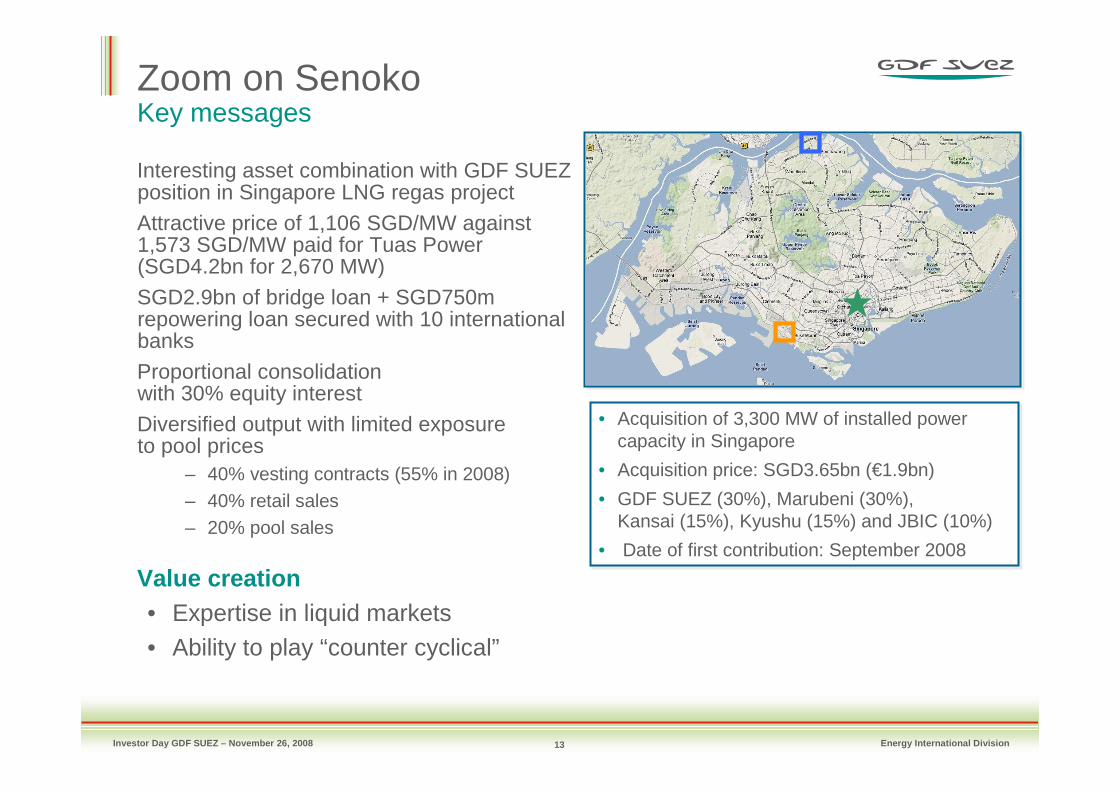

Zoom on SenokoKey messages

Interesting asset combination with GDF SUEZposition in Singapore LNG regas project

Attractive price of 1,106 SGD/MW against1,573 SGD/MW paid for Tuas Power(SGD4.2bn for 2,670 MW)

SGD2.9bn of bridge loan + SGD750m repowering loan secured with 10 internationalbanks

Proportional consolidation with 30% equity interest

Diversified output with limited exposureto pool prices

– 40% vesting contracts (55% in 2008)– 40% retail sales– 20% pool sales

Value creation• Expertise in liquid markets• Ability to play “counter cyclical”

• Acquisition of 3,300 MW of installed power capacity in Singapore

• Acquisition price: SGD3.65bn (€1.9bn)

• GDF SUEZ (30%), Marubeni (30%),Kansai (15%), Kyushu (15%) and JBIC (10%)

• Date of first contribution: September 2008

• Acquisition of 3,300 MW of installed power capacity in Singapore

• Acquisition price: SGD3.65bn (€1.9bn)

• GDF SUEZ (30%), Marubeni (30%),Kansai (15%), Kyushu (15%) and JBIC (10%)

• Date of first contribution: September 2008

Energy International Division

14Investor Day GDF SUEZ – November 26, 2008

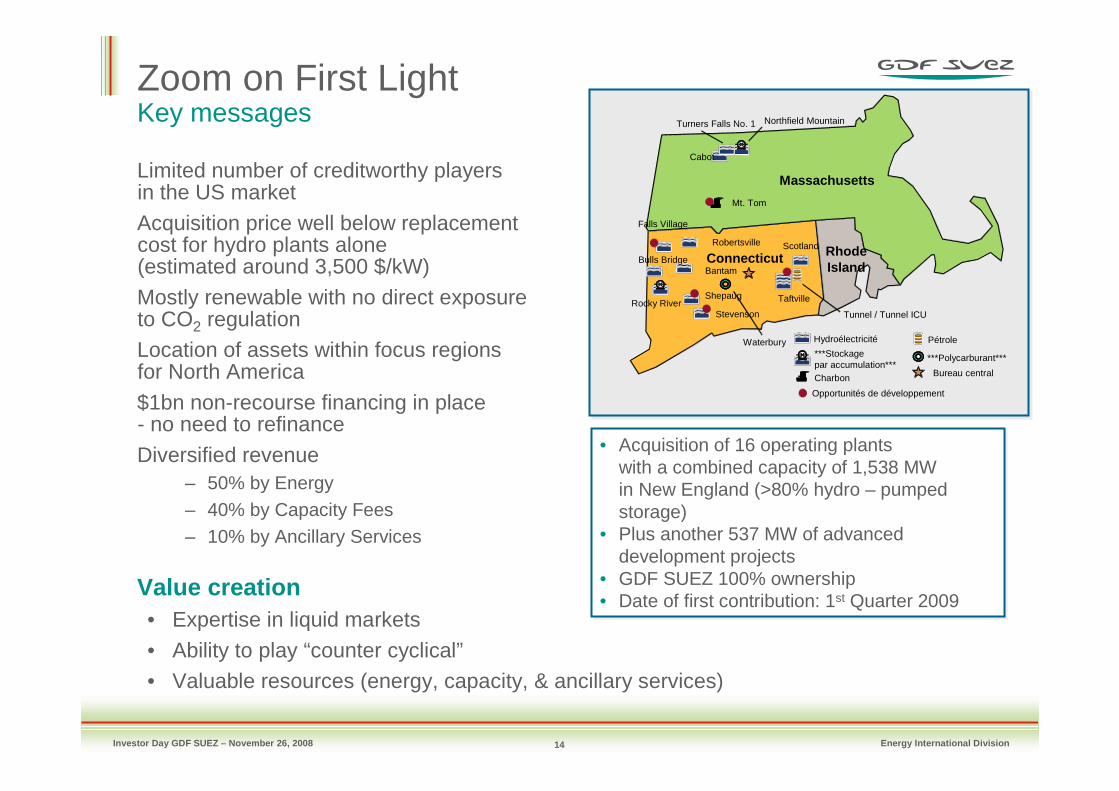

Zoom on First LightKey messages

Limited number of creditworthy playersin the US market

Acquisition price well below replacementcost for hydro plants alone(estimated around 3,500 $/kW)

Mostly renewable with no direct exposureto CO2 regulationLocation of assets within focus regionsfor North America

$1bn non-recourse financing in place- no need to refinance

Diversified revenue– 50% by Energy– 40% by Capacity Fees– 10% by Ancillary Services

Value creation• Expertise in liquid markets

• Ability to play “counter cyclical”• Valuable resources (energy, capacity, & ancillary services)

• Acquisition of 16 operating plantswith a combined capacity of 1,538 MWin New England (>80% hydro – pumped storage)

• Plus another 537 MW of advanceddevelopment projects

• GDF SUEZ 100% ownership• Date of first contribution: 1st Quarter 2009

• Acquisition of 16 operating plantswith a combined capacity of 1,538 MWin New England (>80% hydro – pumped storage)

• Plus another 537 MW of advanceddevelopment projects

• GDF SUEZ 100% ownership• Date of first contribution: 1st Quarter 2009

Connecticut

Massachusetts

RhodeIsland

Shepaug

Stevenson

Falls Village

Bulls Bridge

Rocky River

Turners Falls No. 1 Northfield Mountain

Cabot

Robertsville

Mt. Tom

Waterbury

Tunnel / Tunnel ICU

Scotland

Taftville

Bantam

Charbon Bureau central

***Stockagepar accumulation***

***Polycarburant***

Hydroélectricité Pétrole

Opportunités de développement

Energy International Division

15Investor Day GDF SUEZ – November 26, 2008

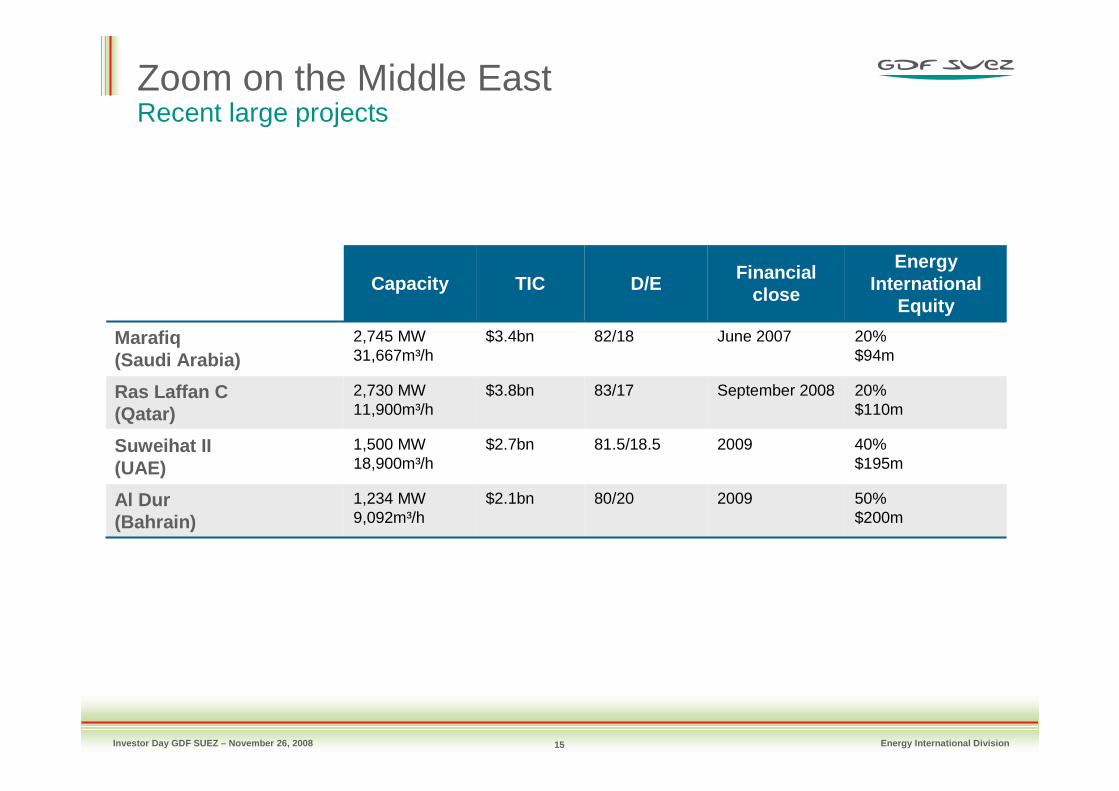

Zoom on the Middle EastRecent large projects

Energy International Division

Capacity TIC D/EFinancial

close

Energy International

Equity

Marafiq(Saudi Arabia)

2,745 MW31,667m³/h

$3.4bn 82/18 June 2007 20%$94m

Ras Laffan C(Qatar)

2,730 MW11,900m³/h

$3.8bn 83/17 September 2008 20%$110m

Suweihat II(UAE)

1,500 MW18,900m³/h

$2.7bn 81.5/18.5 2009 40%$195m

Al Dur(Bahrain)

1,234 MW9,092m³/h

$2.1bn 80/20 2009 50%$200m

16Investor Day GDF SUEZ – November 26, 2008

Zoom on Middle EastKey messages

All projects have secured fuel and offtakeagreements with creditworthy entities

Remuneration through equity return, development and management fees

Equity consolidation and equity exposure between 20 to 50%

Value creation

• Competitive advantages:

– Reputation from track record

– Local O&M synergies resulting from scale

– Synergies with SUEZ Environnement on desalination side

Energy International Division

17Investor Day GDF SUEZ – November 26, 2008

Business case: PeruFrom single client plant toward diversified customer portfolioand fuel mix

Lima

Ilo

Yuncan

Chilca 1997/8 2002 2004

2005

Acquisition of 245 MW capacity in ILO

Acquisition of 245 MW capacity in ILO

Step into gas business with 8% share in TGP (Camisea pipeline) + greenfield gas

distribution concession in Lima

Step into gas business with 8% share in TGP (Camisea pipeline) + greenfield gas

distribution concession in Lima

Acquisition of Yuncan130 MW hydro plant and

entry of local pension fundsEnersur capital (21%)

Acquisition of Yuncan130 MW hydro plant and

entry of local pension fundsEnersur capital (21%)

Start construction of ChilcaOne173 MW gas fired power plant and

IPO of 17% of Enersur capital

Start construction of ChilcaOne173 MW gas fired power plant and

IPO of 17% of Enersur capitalILO 21 new 135 MW coal plant enters in operation

ILO 21 new 135 MW coal plant enters in operation

2000

Enersur startsmulti-client

program

Enersur startsmulti-client

program

2003

Commissioning of second unit and construction of a third

unit Chilca

Commissioning of second unit and construction of a third

unit Chilca

Commissioning of ChilcaOnefirst unit and construction of

second unit

Commissioning of ChilcaOnefirst unit and construction of

second unit

2006

2007

Sale of Caliddagas distributionSale of Caliddagas distribution

Energy International Division

18Investor Day GDF SUEZ – November 26, 2008

• 5,152 MW installed power capacity

• 6 to 7% annual growth rate

• 5,152 MW installed power capacity

• 6 to 7% annual growth rate

245

850

1,028

0

200

400

600

800

1000

1200

1998 2008 2009

+347%

Business case: ENERSUR With proven value creation record

ENERSUR M$

Total acquisition cost in 1997/8 56.5

1998-2005 dividends 58.9

Proceeds from 11/2005 offering 77.5

Market value of 62% stake 289.6

Key market figures

Total shareholder return (*) 22.2 %

(*) Assuming full divestment at market price in Dec 2007.Source: GSELA AIFA: IRR3 in sale with taxes

MW

Energy International Division

19Investor Day GDF SUEZ – November 26, 2008

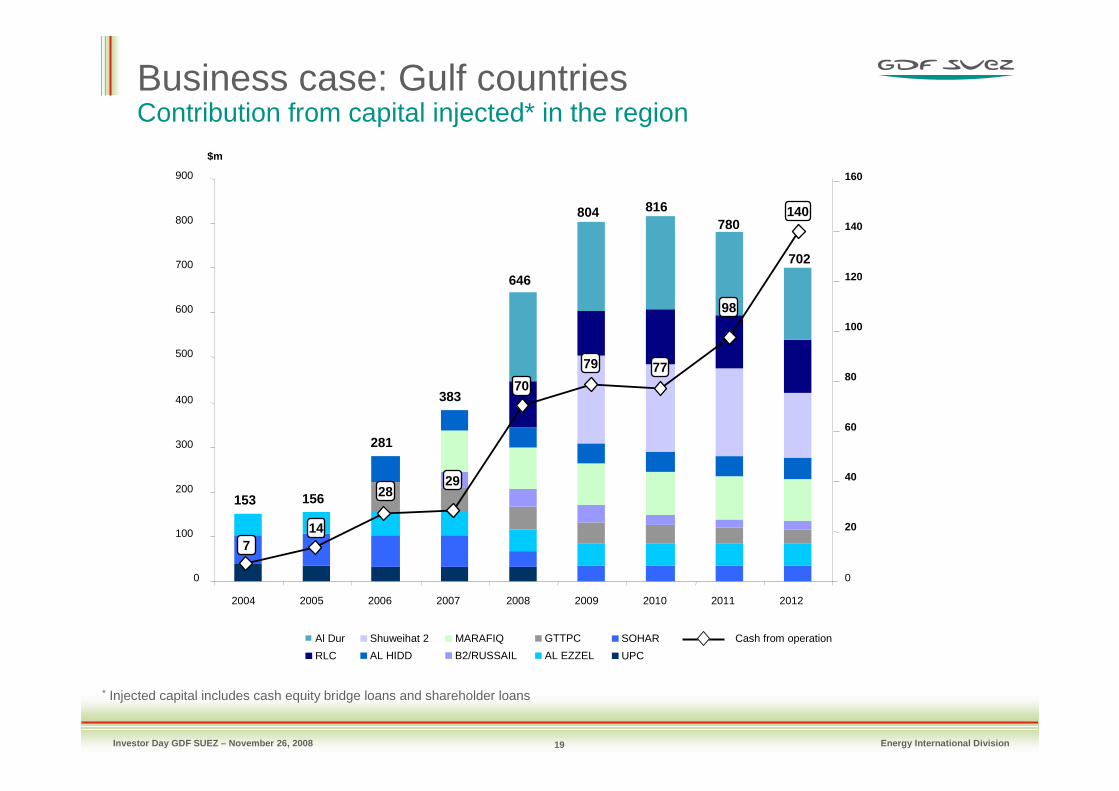

Business case: Gulf countriesContribution from capital injected* in the region

Energy International Division

* Injected capital includes cash equity bridge loans and shareholder loans

20

40

60

80

100

120

140

160

153 156

281

383

646

804 816780

702

0

100

200

300

400

500

600

700

800

900

2004 2005 2006 2007 2008 2009 2010 2011 2012

$m

0

714

2829

70

79 77

98

140

Al Dur

RLC

Shuweihat 2

AL HIDD

MARAFIQ

B2/RUSSAIL

GTTPC

AL EZZEL

SOHAR

UPC

Cash from operation

Energy FranceBusiness Line

BUSINESS LINES APPENDICES

GDF SUEZ

21Investor Day GDF SUEZ – November 26, 2008

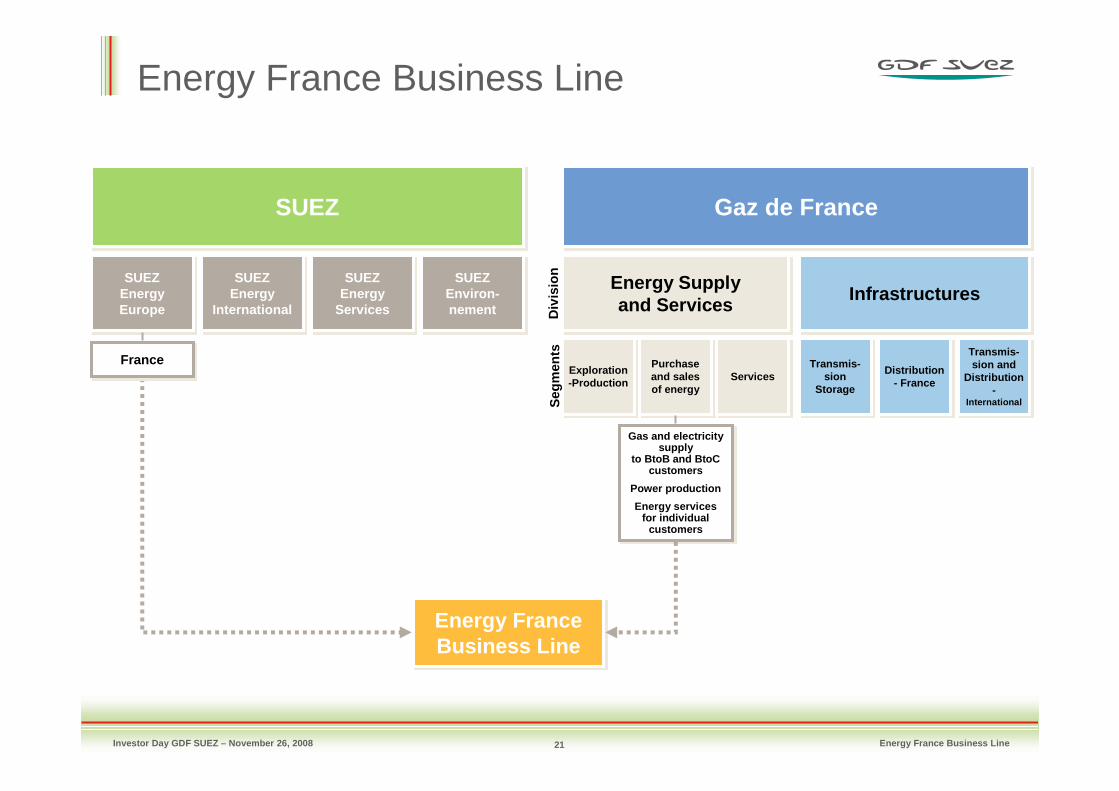

Energy France Business Line

Gaz de FranceGaz de FranceSUEZSUEZ

Energy Supplyand Services

Energy Supplyand Services InfrastructuresInfrastructures

Energy France Business LineEnergy France Business Line

SUEZEnergy Europe

SUEZEnergy Europe

SUEZEnergy

International

SUEZEnergy

International

SUEZEnergy

Services

SUEZEnergy

Services

SUEZEnviron-nement

SUEZEnviron-nement

Exploration -ProductionExploration -Production

Purchase and sales of energy

Purchase and sales of energy

ServicesServicesTransmis-

sionStorage

Transmis-sion

Storage

Distribution- France

Distribution- France

Transmis-sion and

Distribution -

International

Transmis-sion and

Distribution -

International

Gas and electricity supply

to BtoB and BtoCcustomers

Power production

Energy servicesfor individual

customers

Gas and electricity supply

to BtoB and BtoCcustomers

Power production

Energy servicesfor individual

customers

Div

isio

n

FranceFrance

Energy France Business Line

Seg

men

ts

22Investor Day GDF SUEZ – November 26, 2008

New segmentation

The Business line comprises:

• Entities that were formerly part of Gaz de France's Energy Purchases/Sales segment

– the Upstream Electricity Division, excluding electrical assets abroad (power plants in Teesside (938 MW) and Shotton (215 MW) in the UK and Cartagena (1,200 MW) in Spain)which were transfered to the Energy Europe and International Business Line - Europe Division

– the Sales Division

– the client services activities (Savelys, Solfea)

• Electrabel France and SUEZ Group's shareholdings in CNR (49.9%), SHEM (99.7%), La Compagnie du Vent (56.8%) and Great (100%)

It is now comprised of five business units:

• Electricity production

• Energy management - France

• Supply of BtoB customers

• Supply of BtoC customers

• Energy services for individual customers

Energy France Business Line

23Investor Day GDF SUEZ – November 26, 2008

Electricity Production BURoles and key figures

Targeting operational excellence in using the unit's current assetsand expanding production capacities to reach 10 GW by 2013

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2008 2009 2010 2011 2012 2013

Solar

Wind

Hydro

Thermal

Nuclear

Energy France Business Line

24Investor Day GDF SUEZ – November 26, 2008

Electricity Production BUA leading player in renewable energy in France

GDF SUEZ owns the largest installedfleet in France

• 337 MW in operation as at 30 Sept. 2008, i.e.market share of about 10%

• 395 MW in construction or for which a non recourse building permit has been obtained

GDF SUEZ owns a rich, diversified development portfolio

• over 8 GW in wind energy developmentallowing to reach 2 to 3 GW capacity by 2013

• about 150 MW in solar energy development

La Haute Lys (100%)

38 MW in operation

Nass & Wind (100%)

34 MW in operation(o/w 6 MW forNass & Wind)90 MW in construction

Great (100%)

10 MW in operation

Maia Eolis (49%)

78 MW in operation72 MW in construction

Erelia (95%)

68 MW in operation92 MW in construction

CNR (49.9%)

73 MW in operation53 MW in construction

La Compagnie du Vent (56%)

105 MW in operation125 MW in construction

Energy France Business Line

25Investor Day GDF SUEZ – November 26, 2008

Energy Management France BURoles and key figures

Optimize upstream electrical portfolio of the Group in France

Manage the supply of gas and electricity for the business line

Key figures (est. 2008)

• 300 TWh of gas supplied

• 30 TWh of electricity supplied (own production, contracts and market)

Outlook: contribute to the performance of the Energy France Business Line targeting operational excellence and valuing a diversified upstream portfolio

Energy France Business Line

26Investor Day GDF SUEZ – November 26, 2008

Supply of BtoB customers BURoles and key figures

Selling gas, electricity and services to business customersand local communities.

Key figures

• About 1,100 employees

• 150 TWh of gas sold to 260,000 different sites in 2007

• 9 TWh of electricity sold to 110,000 different sites in 2007

• Well-known brands including Provalys and Energies Communes

Outlook

• Sustain our leadership in the supply of natural gas

• Expand sales of electricity and energy-related services to meet customers’requirements

Energy France Business Line

27Investor Day GDF SUEZ – November 26, 2008

BtoC Sales BURoles and key figures

Selling energy and energy-related services to individualand professional customers

Key figures• About 2,500 employees • 139 TWh of gas sold to 10.7 million customers in 2007• As at 30 September 2008

– 10.1 million individual gas customers, 400,000 of which chose to pay market prices; 300,000 individual electricity customers

– 300,000 professional gas customers, 80,000 of which chose to pay market prices; 80,000 professional electricity customers

• A network of 3,500 partners

Outlook• Sustain our leadership in natural gas supply• Electricity market share: 20% in the medium term, depending on market

conditions

Energy France Business Line

28Investor Day GDF SUEZ – November 26, 2008

Volumes sold

In TWh

Natural gas sales 2007 H1 2008Public Distribution 125 75Market offering 0 1

BtoC customers 125 76

Public Distribution 96 52Subscription tariff 24 13Market offering 44 25

BtoB customers 164* 90

Total 289 166

Energy France Business Line

* o/w 14 TWh sold by BtoC BU

Electricity sales 2007 H1 2008

Sales to customers 18 9

Market sales 13 10

Total 31 19

29Investor Day GDF SUEZ – November 26, 2008

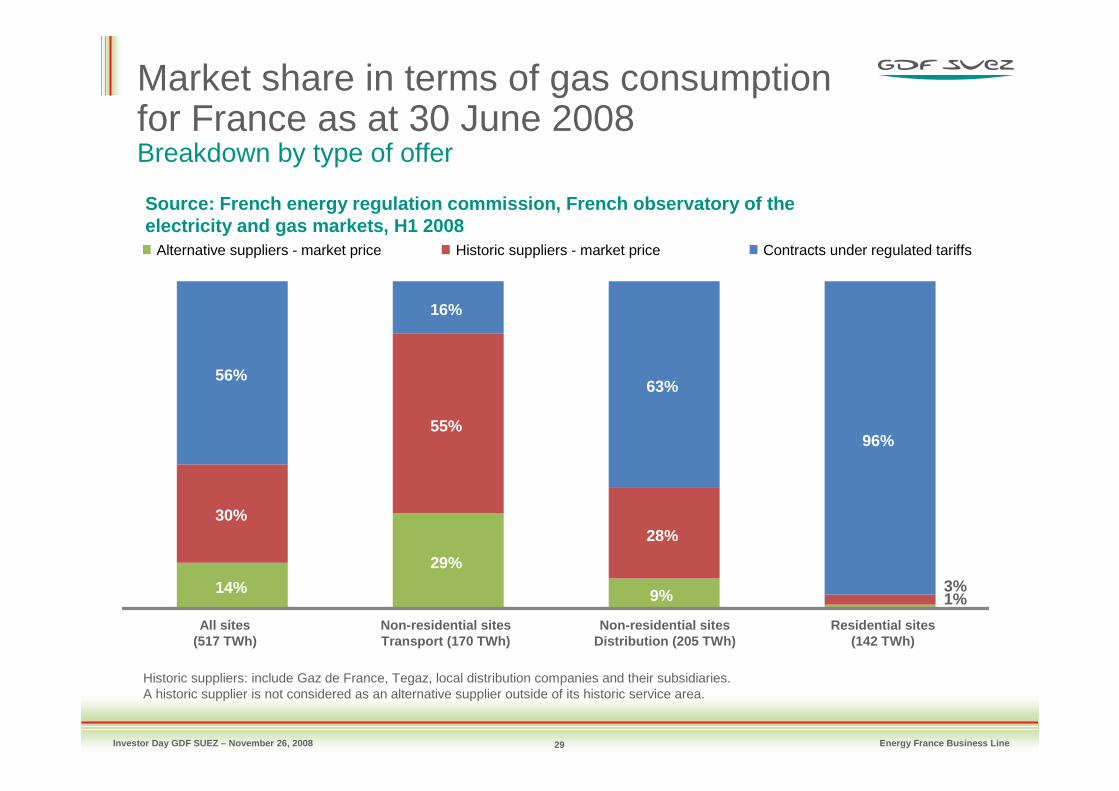

Market share in terms of gas consumptionfor France as at 30 June 2008Breakdown by type of offer

Source: French energy regulation commission, French observatory of the electricity and gas markets, H1 2008

Historic suppliers: include Gaz de France, Tegaz, local distribution companies and their subsidiaries.A historic supplier is not considered as an alternative supplier outside of its historic service area.

14%

29%

9% 1%

30%

55%

28%

3%

56%

16%

63%

96%

All sites(517 TWh)

Non-residential sitesTransport (170 TWh)

Non-residential sitesDistribution (205 TWh)

Residential sites(142 TWh)

Alternative suppliers - market price Historic suppliers - market price Contracts under regulated tariffs

Energy France Business Line

30Investor Day GDF SUEZ – November 26, 2008

A more favourable climate in Q3 2008than in Q3 2007Climate correction* in France

COLDER

WARMER

AVG. CLIMATE

* Distribution area: France

In TWh

Energy France Business Line

-25.3

H1 2007

10.7

H2 2007

H1 2008

-7.7

1.2

Q3 2008

31Investor Day GDF SUEZ – November 26, 2008

Energy services for individual customers BURoles and key figures

Providing individual customers with eco-comfort solutions in their homes, integrating Renewable Energy solutions, and carrying out works associated with the thermal renovation of developed areasKey figures• Solfea bank

– 15,000 partner companies (business providers) – 2/3 of loans issued are eco-loans for sustainable development or energy saving projects – 50,000 loan applications per year – 171,000 active clients – 76 employees

• Savelys– 1.5 million individual heating systems under contract – No. 1 in heating system maintenance/repairs in France; No. 2 in Europe – 4,200 employees – 250 branches and satellite centres– 90% residential, 10% service sector and merchants – Breakdown of clientele: 47% individual customers, 47% group customers (public and private sectors),

6% small group heating systems (public and private sectors) – 7 training centres to prepare 400 new heating system maintenance/repair professionals per year

• Climasave– Specializing in the renovation of energy systems based on renewable energies

(heat pumps, photovoltaic energy, solar thermal energy, etc.)

Energy France Business Line

32Investor Day GDF SUEZ – November 26, 2008

Consolidation scope: Subsidiaries (1/2)

Subsidiaries and drawing rights

• Electricity Production BU(1) and Energy Management France BU(2)

� DK6, 100%,Fully consolidated

� Cycofos, 100%,Fully consolidated

� Combigolfe, 100%,Fully consolidated

� SPEM, 100%,Fully consolidated

� Fraganlys, 100%,Fully consolidated

� CNR, 49.98%,Fully consolidated

� SHEM, 99.62%,Fully consolidated

� Maïa Eolis, 49%, Partially consolidated

� Erelia, 95%, Fully consolidated

� Nass&Wind, 100%, Fully consolidated

� Haute Lys, 100%, Fully consolidated

� LCV(3), 56.8%, Fully consolidated

� GREAT, 100%, Fully consolidated

� CN'AIR, 49.98%, Fully consolidated

� GDF Futures Energies, 100%,Fully consolidated

Thermal energy department Hydraulic energy dept Renewable Energies dept

Energy France Business Line

(1) in its capacity as fleet operator(2) in its capacity as optimiser of capacity output(3) La Compagnie du Vent(4) contractually guaranteed power: 377 MWe

� Chooz B, 650 MWe

� Tricastin, 458 MWe(4)

Drawing rights

33Investor Day GDF SUEZ – November 26, 2008

Consolidation scope: Subsidiaries (2/2)

Subsidiaries

� Electrabel France(1), 100%,Fully consolidated

� CNR(1), 49.98%,Fully consolidated

� Énergie du Rhône, 100%,Fully consolidated

� Savelys Group, 100%,Fully consolidated

� Banque Solféa, 54.72%,Partially consolidated

� Climasave Group, 100%,Fully consolidated

Consolidatedin H2 2008

Supply of BtoB customers BU

Energy services for individual customers BU

Energy France Business Line

(1) as regards their sales activities