generations and journeys - hsbc.com.sg · seeking retirement information from trusted sources and...

TRANSCRIPT

The Future of Retirement Generations and journeysSingapore Report

The Future of Retirement

Generations and journeys

The Future of Retirement Generations and journeys

Priorities and

feelings

Approaches to

finances

Practical steps

The researchPreparing for

the future

Foreword

Key findings

Finances in

retirement

The Future of Retirement Generations and journeys

ForewordOver the course of a lifetime, our needs and priorities will change but the

things we value in life often remain the same.

In our new global report Generations and journeys, the 13th in The Future of

Retirement series, we see that ensuring financial security for ourselves and

our families is a priority through all stages of life. So although retirement can

be a time to enjoy the fruits of our labour with those we hold dear, there are

also continuing financial responsibilities.

While there is much to learn from today’s retirees, younger generations must

navigate their own path through the big events in their lives and a changing

financial landscape. Starting to save early may no longer be enough to

ensure a comfortable retirement, and continuing to save through the ups and

downs of life is just as important.

Seeking retirement information from trusted sources and personalised

advice from professionals remain good ways to prepare for and help deal

with the unexpected financial bumps in the road.

I hope that the new insights and practical steps in this report will help

you on your journey into retirement.

Charlie Nunn

Group Head of Wealth Management, HSBC

The Future of Retirement Generations and journeys

Key findings

Read more

of people in their 40’s

are financially

supporting others

78% Pre-retirees expect to save

for retirement for

9 yearslonger than current retirees

did

of working age people

have not started saving

for their retirement

23% Of pre-retirees who

have started saving for

retirement,

38%have stopped or faced

difficulties

The Future of Retirement Generations and journeys

Key findings

of pre-retirees have

never received advice

or information about

retirement

26%of retirees wish they

had started saving

for retirement at an

earlier age

40%of people in their 60s and

over expect to move into

a retirement home

25%of retirees use cash

savings to help fund

their retirement

59%

The Future of Retirement Generations and journeys

The research identified five different types of approach to life and finances that affect people's attitudes and

behaviour to retirement planning:

Approaches to finances

20%31% 14% 12% 23%

Inclined to value

saving over

spending, but more

likely to face

struggles along the

way.

Tend to be older with

financial plans in

place. More able to

relax and enjoy time

with family and

friends.

Typically higher

earners who plan

early and

strategically. They

are more able to

enjoy the luxuries in

life as a result.

(27% globally) (21% globally) (20% globally) (16% globally) (17% globally)

Retirement findings particularly relevant to people with these approaches are included throughout the report

Have a more

pragmatic approach

to life and are more

likely to be cautious

in their planning and

spending.

More optimistic

about the future, and

more likely to have

the luxury of being

able to take risks

while having fun and

enjoying life.

Assured

Optimists

Committed

Savers

Comfortably

Affluent

Strategic

Planners

Concerned

Realists

The Future of Retirement Generations and journeysThe Future of Retirement Generations and journeys

Priorities and feelings

While priorities change at each stage

of life, family security and financial

security are the things people value

most throughout life. Retiring from

work is one of many priorities people

have in their lives, and on the whole

they feel positive about it.

The Future of Retirement Generations and journeys

63%family

security

Across generations,

financial security and

family security are the

things people

value most in life68%

financial

security

Q. Below is a list of things which

people value in life. Which three do

you value the most?

(Base: Pre-retirees and retirees)

Priorities and feelings

The Future of Retirement Generations and journeys

Values in life

Across generations, family security

and financial security are among the

things that people value most in life.

Over two thirds (68%) say financial

security is one of the things they

value most in life, and over three in

five (63%) say financial security is:

Nearly a third of women (32%) say

warm relationships with others is one

of the things they value most,

compared to just over a quarter

(27%) of men. Conversely, 28% of

men say self-fulfilment is something

they most value, compared to 22%

of women.

Some values differ by generation:

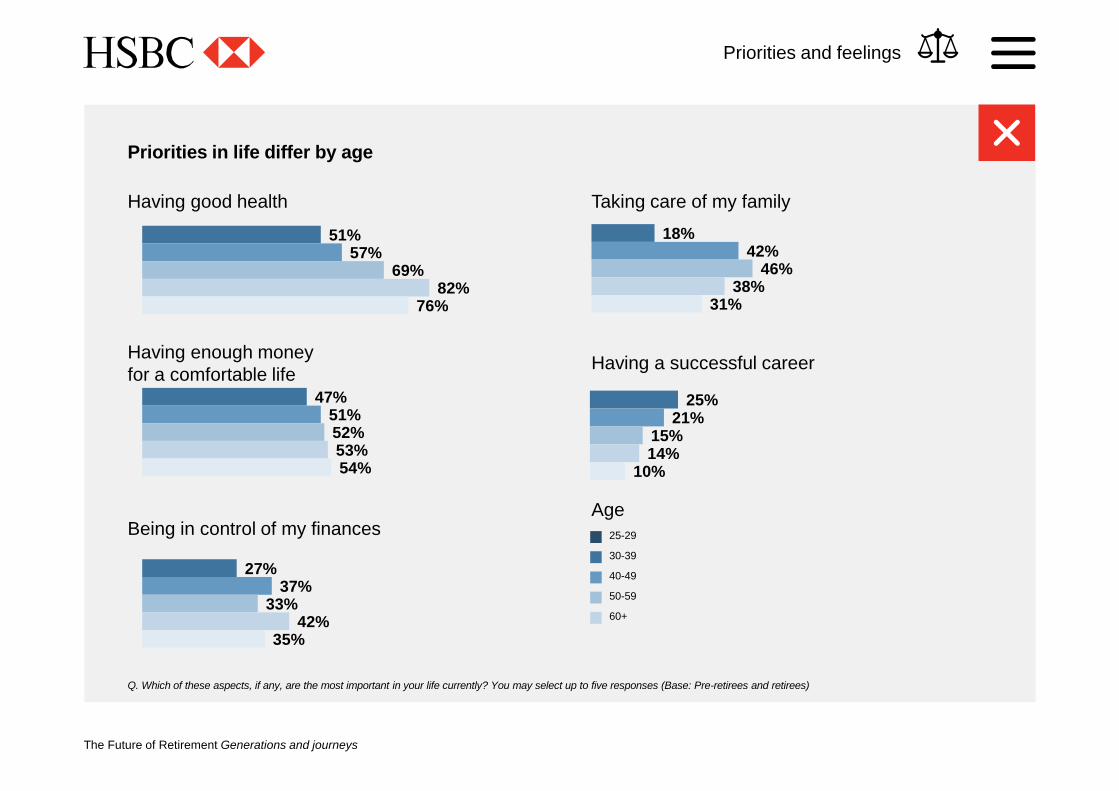

Priorities in life

Priorities differ by age, and while

having good health (68%) and

enough money for a comfortable

life (52%) rank highly for everyone,

these are more likely to be

important in life for older

generations:

AgeGood

health

Enough

money

25-29 51% 47%

30s 57% 51%

40s 69% 52%

50s 82% 53%

60+ 76% 54%

Pre-retirees Retirees

Financial security 67% 71%

Family security 63% 63%

Fun and enjoyment

in life34% 29%

Warm relationships

with others28% 36%

Self-fulfilment 25% 23%

Sense of

accomplishment20% 15%

Self-respect 17% 18%

Being well-

respected14% 20%

Sense of belonging 14% 13%

38% of people in their 30s rate

fun and enjoyment in life as

important, compared to 29%

of people in their 50s

23% of people in their 30s

value a sense of

accomplishment, compared to

13% of people aged 60 or over

Priorities and feelings

The Future of Retirement Generations and journeys

Priorities in life differ by age

18%42%

46%38%

31%

25%21%

15%14%

10%

25-29

30-39

40-49

50-59

60+

51%57%

69%82%

76%

Having good health

Having a successful career

27%37%

33%42%

35%

Being in control of my finances

47%51%52%53%54%

Having enough money

for a comfortable life

Taking care of my family

Age

Priorities and feelings

Q. Which of these aspects, if any, are the most important in your life currently? You may select up to five responses (Base: Pre-retirees and retirees)

The Future of Retirement Generations and journeys

Most people feel

positively about

retirement and this

increases the closer

they get

Q. Below are some words people

have used to describe their feelings in

retirement. To what extent does each

of these apply/ do you think each of

these will apply to you? A. Happy

(Base: Pre-retirees and retirees)Years to retirement

51%53%

55%

62%61%

50%

Retirement

Retired

Priorities and feelings

The Future of Retirement Generations and journeys

Happiness in

retirement

Pre-retirees are more likely to

expect they will feel happy rather

than anxious in retirement, and this

sentiment is shared by retirees. This

positivity increases in the lead up to

retirement, with those nearest to

retiring the most likely to say they

will feel happy in retirement.

Working age people who have not

started saving for retirement or have

not received any advice or

information about it, are less likely

to feel positive about their

retirement:

55% of working age people

who have started saving think

they will feel happy in

retirement, compared to 41%

who have not.

53% of working age people

who have received advice or

information think they will feel

happy in retirement, compared

to 35% who have not.

Working age people in their 60s or

over are more likely to think they will

feel happy in retirement. Over half

(55%) think they will feel happy

compared to 44% of those in their

40s.

Priorities and feelings

The Future of Retirement Generations and journeys

People are more likely to associate positive emotions with retirement

Q. Below are some words people have used to describe their feelings in retirement. To what extent does each of these apply / do you think each of these will apply to you?

A. Applies (Base: Pre-retirees and retirees)

Pre-retirees Retirees

48%

41%

40%

37%

36%

33%

33%

33%

28%

29%

50%

41%

46%

38%

40%

31%

35%

28%

25%

26%

Happy

Cautious

Calm

Hopeful

Optimistic

Excited

Confident

Motivated

Bored

Inspired

27%

26%

25%

21%

21%

21%

20%

19%

17%

10%

26%

21%

24%

27%

21%

20%

15%

15%

10%

9%

Creative

Lonely

Anxious

Wanted

Overwhelmed

Stressed

Isolated

Frustrated

Confused

Embarrassed

Priorities and feelings

The Future of Retirement Generations and journeysThe Future of Retirement Generations and journeys

Finances in retirement

Financial outgoings differ by age, as

does the way pre-retirees plan for their

retirement. Looking ahead, many

people expect to make significant

adjustments to their living

arrangements in later life.

The Future of Retirement Generations and journeys

16%31%

57%63%

62%69%

Financially supporting others

Borrowing

25-29

30-39

40-49

50-59

60-69

70+

People in their 30s and

40s are most likely to be

financially supporting

others and borrowing

Q. What financial outgoings, if any,

do you currently have? (Base: Pre-

retirees and retirees)

43%44%

59%78%

36%40%

Age

Finances in retirement

The Future of Retirement Generations and journeys

Financial outgoings

in retirement

While household bills and leisure

and entertainment costs are always

likely to be financial outgoings,

other expenses including financially

supporting others and borrowing

vary more with age.

People in their 30s and 40s are the

most likely to be financially

stretched. The majority of people in

their 30s (69%) and 40s (78%) are

financially supporting others, and

are more likely to be borrowing

(62% and 59% respectively).

People aged 60 or over are less

likely to be borrowing or financially

supporting others, so have more

flexibility to spend their money on

other things:

Retirees continue to face regular

expenses once they stop work,

including household bills (60%) and

credit card repayments (22%).

Fewer pre-retirees are expecting to

face these financial outgoings. Less

than half (48%) expect to be paying

household bills, and just 12%

expect to be repaying credit card

bills in retirement.

12% of people age 60 or over

count charitable donations as

one of their financial outgoings,

compared to 5% of people

aged 25-29.

29% of people age 60 or over

identify general home and

garden maintenance as an

outgoing, compared to 16% of

25-29 year olds.

Finances in retirement

The Future of Retirement Generations and journeys

Pre-retirees expect fewer outgoings in retirement than current retirees have

Q. What financial outgoings, if any, do you expect to have in your retirement (Base: Pre-retirees)

Q. What financial outgoings, if any, do you currently have? (Base: Retirees)

23%

47%

33%

73%

55%

29%

68%

34%

88%

73%

Borrowing

General savings

Financially supporting others

Household/ personal living costs

Leisure/ entertainment

Pre-retirees predicted outgoings Retirees actual outgoings

Finances in retirement

The Future of Retirement Generations and journeys

The ways retirees

fund their retirement

differs from pre-

retirees’

expectations

Pre-retirees

Retirees

Q. Which of the following are likely to

help you fund / are currently helping

you fund your retirement?

(Base: Pre-retirees and retirees)

60% 59%

12% 11%

40%

19%

Personal pension

scheme

Cash savings/

deposit accounts

State pension/

social security

My own income

if I keep working to

some extent

11%

5%

Finances in retirement

The Future of Retirement Generations and journeys

Funding retirement

There are many methods of funding

retirement, and the expectations of

pre-retirees differ from the reality

experienced by retirees.

Nearly three in five (59%) retirees

use cash savings/deposit accounts

to help them fund their retirement.

Financial support from children

(34%) is also a popular funding

method for retirees, followed by:

Life insurance/

endowment savings

plan

34%

Stocks and shares 33%

Annuities 23%

For the next generations

of retirees, retirement funding

methods are likely to be different.

Fewer pre-retirees expect to have

financial support from children

(15%) or annuities (16%), than

current retirees do.

Instead, more pre-retirees expect to

use their own income (40%

compared to 19% of retirees), a

Defined Contribution employer

pension scheme (16% vs. 8%) and

income from renting out a property

(25% vs. 15%).

Despite their intentions, 17% of pre-

retirees who say they are likely to

help fund their retirement with cash

savings/ deposits are yet to start

saving for their retirement.

Finances in retirement

The Future of Retirement Generations and journeys

Retirees in Singapore are among the least likely be using state retirement funding

Q. Which of the following are currently helping you to fund your retirement? A. State pension/social security (Base: Retirees)

45%

64%62%

53% 53% 53%51%

48%44%

37%35%

30%26% 25%

11%9%

7%

Finances in retirement

The Future of Retirement Generations and journeys

Over one in five

working age people

expect to use

property to fund

their retirement

Q. Which of the following are likely to

help/are helping you fund your retirement?

A. Income from downsizing or selling

property (Base: Pre-retirees and retirees)

21%of pre-retirees believe

that income from

downsizing or selling

a property is likely to

help them fund their

retirement

Income from

downsizing or selling

a property is helping

11%of retirees to fund

their retirement

Finances in retirement

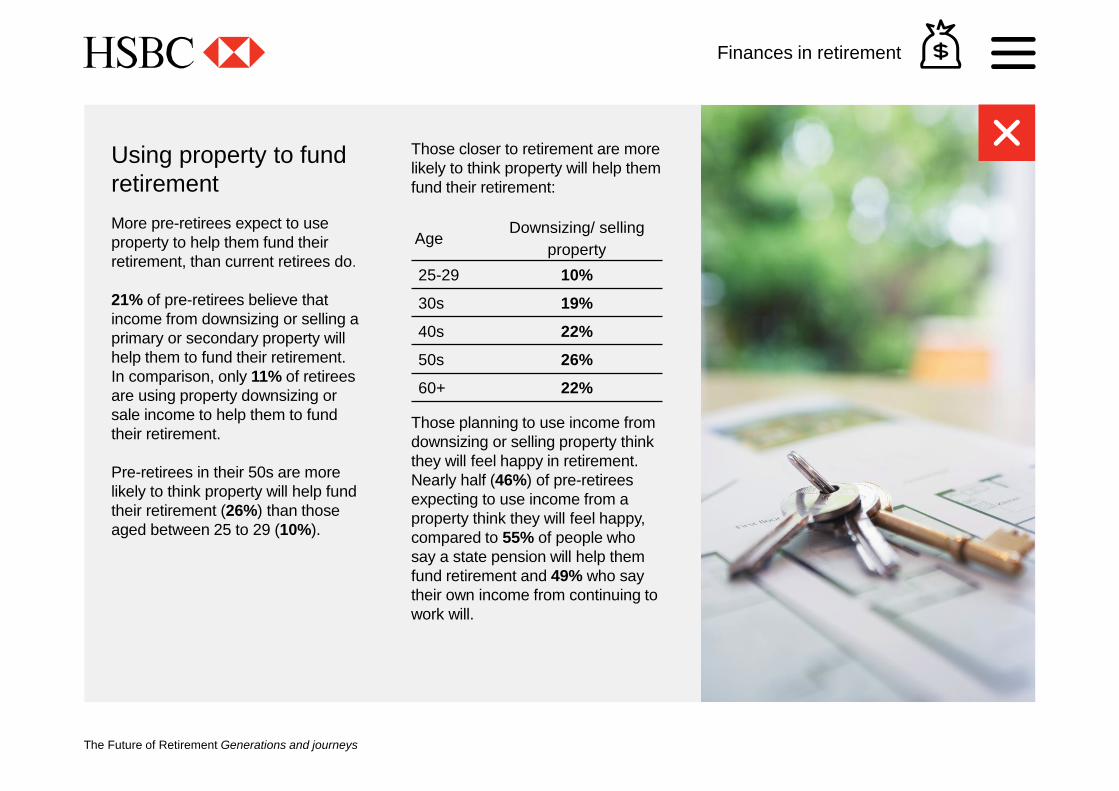

The Future of Retirement Generations and journeys

Using property to fund

retirement

More pre-retirees expect to use

property to help them fund their

retirement, than current retirees do.

21% of pre-retirees believe that

income from downsizing or selling a

primary or secondary property will

help them to fund their retirement.

In comparison, only 11% of retirees

are using property downsizing or

sale income to help them to fund

their retirement.

Pre-retirees in their 50s are more

likely to think property will help fund

their retirement (26%) than those

aged between 25 to 29 (10%).

Those closer to retirement are more

likely to think property will help them

fund their retirement:

AgeDownsizing/ selling

property

25-29 10%

30s 19%

40s 22%

50s 26%

60+ 22%

Those planning to use income from

downsizing or selling property think

they will feel happy in retirement.

Nearly half (46%) of pre-retirees

expecting to use income from a

property think they will feel happy,

compared to 55% of people who

say a state pension will help them

fund retirement and 49% who say

their own income from continuing to

work will.

Finances in retirement

The Future of Retirement Generations and journeys

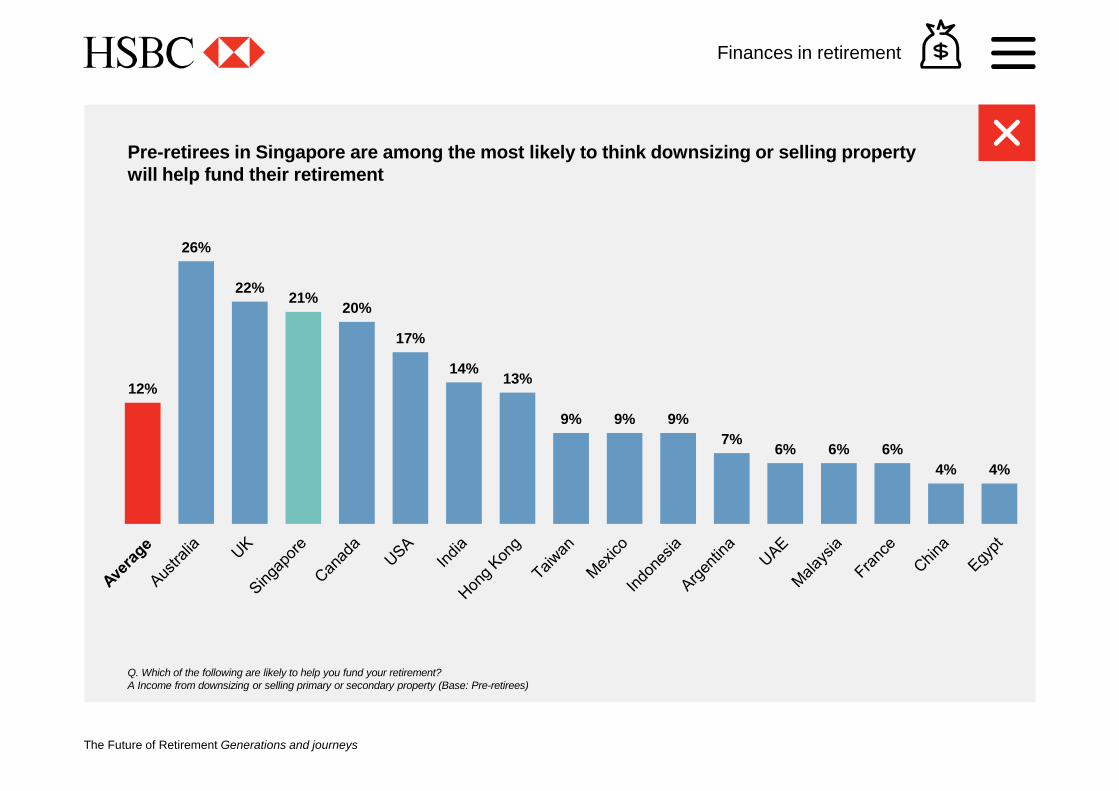

Pre-retirees in Singapore are among the most likely to think downsizing or selling property

will help fund their retirement

Q. Which of the following are likely to help you fund your retirement?

A Income from downsizing or selling primary or secondary property (Base: Pre-retirees)

12%

26%

22%21%

20%

17%

14%13%

9% 9% 9%

7%6% 6% 6%

4% 4%

Finances in retirement

The Future of Retirement Generations and journeys

Move to a bigger

home

Many people don’t

expect to stay in the

same home in their

later years

Q. Looking ahead [to your 40s or

beyond], when, if at all, do you expect

to make the following changes to your

living arrangements?

(Base: Pre-retirees and retirees)Move to

a smaller home

Move into

a retirement home

34%

56%

33%

32%

Move into

a care home

Finances in retirement

The Future of Retirement Generations and journeys

Future living

arrangements

Looking forward, working age

people and retirees of all ages have

plans to change their living

arrangements in the future. These

include moving to:

A smaller home 56%

Live closer to family

members/children39%

A bigger home 34%

A retirement home 33%

A care home 32%

Live with my children 30%

Another country 27%

Another city/ town in the

same country25%

57% of people in their 50s plan to

move to a smaller home in the

future compared to 52% of people

in their 60s and 24% of people 70 or

over.

Those who have received some

sort of retirement advice are also

more likely to think they will move to

a smaller home (60%) than those

who have received none (43%).

People who are Concerned

Realists are the most likely to think

they will move to a smaller home

(63%), while Assured Optimists

are the most likely to think they will

move to a bigger home (48%).

Finances in retirement

The Future of Retirement Generations and journeys

Over half of people in Singapore think they will move to a smaller home in the future

Q. Looking ahead [to your 40s or beyond], when, if at all, do you expect to make the following changes to your living arrangements? A. I will move to a smaller home (Base: Pre-retirees

and retirees)

39%

66%

59%56% 56% 54%

48%

39% 38%35% 34%

27% 25% 23%20%

17% 15%

Finances in retirement

The Future of Retirement Generations and journeysThe Future of Retirement Generations and journeys

Preparing for the future

Many working age people have not

yet started saving for retirement or

had any retirement advice. Among

pre-retirees who have started,

many have stopped or faced

difficulties saving for retirement.

Looking back, many wish they had

started saving for retirement

earlier.

The Future of Retirement Generations and journeys

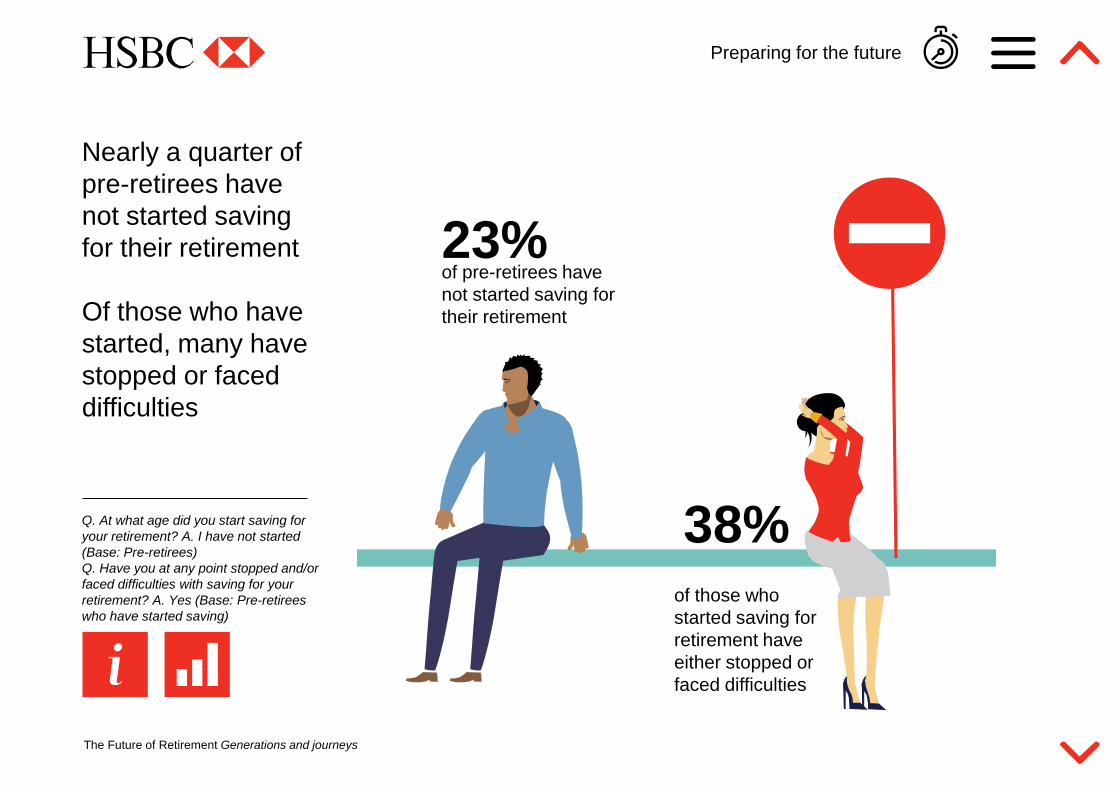

Nearly a quarter of

pre-retirees have

not started saving

for their retirement

Of those who have

started, many have

stopped or faced

difficulties

23%of pre-retirees have

not started saving for

their retirement

38%of those who

started saving for

retirement have

either stopped or

faced difficulties

Q. At what age did you start saving for

your retirement? A. I have not started

(Base: Pre-retirees)

Q. Have you at any point stopped and/or

faced difficulties with saving for your

retirement? A. Yes (Base: Pre-retirees

who have started saving)

Preparing for the future

The Future of Retirement Generations and journeys

Saving for retirement

Nearly a quarter (23%) of pre-retirees

have not started saving for their

retirement.

While those closer to retirement are

more likely to have started saving for

retirement, 18% of people in their 50s

and 10% of people aged 60 or over

have still not started saving.

Women are less likely to have started

saving. Over a quarter (26%) of

women have not started saving for

their retirement, compared to 20% of

men.

25% of pre-retirees who are

Comfortably Affluent have not

started saving for their retirement,

compared to 20% of Strategic

Planners.

While 73% of working age people

have started saving for retirement,

38% of them have stopped or faced

difficulties saving.

Pre-retirees who are Assured

Optimists are the most likely to

have stopped and/ or faced

difficulties with their retirement

saving (42%), while pre-retirees

that are Strategic Planners are the

least likely (32%).

Preparing for the future

The Future of Retirement Generations and journeys

Q. At what age did you start saving for your retirement? A. I have not started (Base: Pre-retirees)

Q. Have you at any point stopped and/or faced difficulties with saving for your retirement? A. Yes (Base: Pre-retirees who have started saving)

Over two in five pre-retirees in Singapore have either not started saving for retirement or

stopped /faced difficulties

46%

65%

54% 53% 52%48% 48% 47%

43% 42% 42% 41% 40% 39% 38% 37% 36%

Preparing for the future

The Future of Retirement Generations and journeys

26%of working age people

have never received

advice and/or

information about

retirement

Q. From which sources, if any, have

you received any advice and/or

information about retirement?

A. I have never received advice or

information about retirement

(Base: Pre-retirees)

Over a quarter of pre-

retirees have never

received advice or

information about

retirement

Preparing for the future

The Future of Retirement Generations and journeys

Receiving advice

Over a quarter (26%) of working

age people have never received

advice or information about

retirement. While they may seek

advice in future, some could be

leaving it too late.

Pre-retirees in their 50s are the

most likely to have received no

advice or information (30%), but

even among those aged 60 or over,

25% have not.

33% of pre-retirees and retirees

who are Committed Savers have

received no advice about

retirement, compared to 16% of

Assured Optimists and 24% of

Concerned Realists.

Friends and family are the most

common sources of retirement

advice or information. Nearly half

(49%) of pre-retirees and 56% of

retirees have received advice/

information from them. 21% of pre-

retirees and 34% of retirees only

consulted them.

Professionals including independent

financial advisers, government

agencies, insurance brokers/agents,

solicitors, accountants, healthcare

professionals and bank advisers are

also popular sources of advice or

information. Over two in five (41%)

retirees and around a third (32%) of

pre-retirees have received

retirement advice/information from

professionals.

Read more

Preparing for the future

The Future of Retirement Generations and journeys

Media, books and online sites also

play a role. Around a third (32%)

pre-retirees and over one in five

retirees (22%) found advice or

information about retirement from

sources including online financial

websites, blogs and discussion

forums, books, magazines and

direct marketing materials.

Those who have received

retirement advice and/or information

say it:

Gave them a more

realistic view of the

options available

49%

Gave them a better

understanding of the

financial implications of

their choices

43%

Informed them of

possibilities or options

that they hadn't

considered

41%

43% were prompted to get

retirement advice or information

because they thought it would be a

good thing to do, and the same

proportion (43%) because they

wanted to be prepared and/or take

control. A third (34%) were

prompted by seeing what happened

to their parents/other elderly people.

2% said there were no benefits.

Preparing for the future

The Future of Retirement Generations and journeys

People get retirement advice and/ or information from many different sources

Q: From which sources, if any, have you received any advice and/or information about retirement? (Base: Pre-retirees and retirees)

Pre-retirees Retirees

49%

21%

41%

9%

32%

5%

56%

34%

32%

6%

22%

3%

Friends or Family

Friends or Family only

Professionals

Professionals only

Media, Books or Online

Media, Books or Online only

Preparing for the future

The Future of Retirement Generations and journeys

Many retirees wish

they had started

saving earlier for

retirement

Q. Thinking about your current

retirement plans, what if anything

would you have done differently?

A. Started saving at an earlier age

(Base: Retirees)

Looking back,

40%of retirees would

have started saving

for retirement at an

earlier age

Preparing for the future

The Future of Retirement Generations and journeys

Looking back

Two in five (40%) retirees would have

started saving for retirement at an

earlier age, as would 41% of pre-

retirees, given the opportunity to do

something differently.

People who are Committed Savers

are the most likely to say they would

have started saving earlier (47%),

compared to 35% of Strategic

Planners.

Over two in five retirees (43%) and

35% of pre-retirees say they would

have taken better care of themselves

and their health.

Preparing for the future

The Future of Retirement Generations and journeys

41%

35%

33%

19%

17%

15%

13%

12%

2%

16%

40%

43%

32%

16%

16%

21%

11%

16%

2%

16%

Started saving at an earlier age

Taken better care of myself and my

health

Saved more by putting aside a larger

share of my income

Worried less

Chosen high/ higher return investments

Spent less on holidays/ cars

Chosen low/ lower risk savings

Obtained professional financial advice

Done something else

Not done anything differently

Looking back, pre-retirees and retirees would have done things differently in their retirement

planning

Q:Thinking about your current retirement plans, what if anything would you have done differently? (Base: Pre-retirees and retirees)

Pre-retirees Retirees

Preparing for the future

The Future of Retirement Generations and journeys

Working age people

expect to save for

retirement for nine

years longer than

current retirees did

20 years

29 years

Age retired/

expect to retire

Years saving

for retirement

Age started

saving for

retirement

Age

59

Age

61

Age

39

Age

32

9 year gap

Preparing for the future

Retirees

Pre-retirees

Q. At what age did you start saving for

your retirement?

(Base: Pre-retirees who have started

saving and retirees who have saved)

Q. At what age do you expect to stop

paid work completely / did you retire?

(Base: Pre-retirees who plan to retire

and retirees)

The Future of Retirement Generations and journeys

Retirement saving gap

On average, pre-retirees expect to

save for retirement for nine years

longer than current retirees did,

saving on average for 29 years,

compared to retirees who saved for

20 years. The average age retirees

started saving was 39 and they

stopped working at 59. Pre-retirees

who have begun saving started

when they were aged 32 and

expect to work until they are 61

years old.

While working age men and women

expect to save for a similar period

(31 and 29 years respectively),

retired men saved for longer (26

years) than retired women (15

years).

On average, retired men started

saving aged 37, while women

waited until they were 41. Men

retired when they were 63 years

old, and women when they were 55

years old.

Preparing for the future

The Future of Retirement Generations and journeys

Practical steps

Here are some important insights and practical actions drawn from the research findings, which may

help today’s retirement savers plan a better financial future for themselves.

Consider all your retirement expenses

1Start saving earlier for retirement

2Make sure your advice is professional

3Be prepared for financial ups and downs

4

The Future of Retirement Generations and journeys

Practical steps

Start saving earlier for retirement

2Make sure your advice is professional

3Be prepared for financial ups and downs

422% of retirees have credit

card repayments as one

of their outgoings, yet only

12% of pre-retirees

expect to be repaying

credit card bills in

retirement

When planning for

retirement, make sure to

list all your possible

retirement outgoings

Here are some important insights and practical actions drawn from the research findings, which may

help today’s retirement savers plan a better financial future for themselves.

The Future of Retirement Generations and journeys

Practical steps

Consider all your retirement expenses

1Make sure your advice is professional

3Be prepared for financial ups and downs

4Prepare for a longer and more active retirement

40% of retirees say they would

have started saving for

retirement at an earlier

age, if they could have

done anything differently

Plan to start saving for

retirement earlier, to help

build a bigger fund and

allow it to grow for longer

Here are some important insights and practical actions drawn from the research findings, which may

help today’s retirement savers plan a better financial future for themselves.

The Future of Retirement Generations and journeys

Practical steps

Consider all your retirement expenses

1Start saving earlier for retirement

2Be prepared for financial ups and downs

4Aim towards a healthier retirement

21% of pre-retirees and 34% of

retirees who received

retirement advice and/or

information got it only from

friends or family

Seek information from

many sources, but make

sure the advice you get is

professional

Here are some important insights and practical actions drawn from the research findings, which may

help today’s retirement savers plan a better financial future for themselves.

The Future of Retirement Generations and journeys

Practical steps

Consider all your retirement expenses

1Start saving earlier for retirement

2Make sure your advice is professional

3Consider how your healthcare needs may change in retirement

38% of pre-retirees who started

saving for retirement have

either stopped and/or

faced difficulties saving

When saving for retirement

gets difficult, make sure to

review all your finances

and seek alternative ways

to help you continue

towards a comfortable

retirement

Here are some important insights and practical actions drawn from the research findings, which may

help today’s retirement savers plan a better financial future for themselves.

The Future of Retirement Generations and journeys

The research

The Future of Retirement is a world-

leading independent research study

into global retirement trends,

commissioned by HSBC. It provides

authoritative insights into the key

issues associated with ageing

populations and increasing life

expectancy around the world.

This report, Generations and

journeys, is the 13th in the series

and represents the views of 18,207

people in 17 countries and

territories.

Since The Future of Retirement

programme began in 2005, more

than 159,000 people have been

surveyed worldwide.

About HSBC LegalSurvey Copyright

The Future of Retirement Generations and journeys

The research The 17 countries and territories are:

Argentina

Australia

Brazil

Canada

China

Egypt

France

Hong Kong

India

Indonesia

Malaysia

Mexico

Singapore

Taiwan

United Arab

Emirates

United Kingdom

United States

The findings are based on a

nationally representative

survey of people of working

age (25+) and in retirement, in

each country or territory. The

research was conducted online

by Ipsos MORI in September

and October 2015, with

additional face-to-face

interviews in Egypt and the

UAE.

This country report represents the views of 1,008 people in Singapore.

All references to retirees refer to people who are semi or fully retired.

All references to pre-retirees refer to working age people who have yet to fully

or semi-retire.

Global figures are the average of all countries and territories surveyed.

All figures are global unless stated otherwise.

Figures have been rounded to the nearest whole number.

The Future of Retirement is a world-

leading independent research study

into global retirement trends,

commissioned by HSBC. It provides

authoritative insights into the key

issues associated with ageing

populations and increasing life

expectancy around the world.

This report, Generations and

journeys, is the 13th in the series

and represents the views of 18,207

people in 17 countries and

territories.

Since The Future of Retirement

programme began in 2005, more

than 159,000 people have been

surveyed worldwide.

Survey

The Future of Retirement Generations and journeys

HSBC Holdings plc, the parent

company of the HSBC Group, is

headquartered in London. The

Group serves customers worldwide

from around 6,000 offices in 71

countries and territories in Europe,

Asia, North and Latin America, and

the Middle East and North Africa.

With assets of US$2,596bn at 31

March 2016, HSBC is one of the

world’s largest banking and financial

services organisations.

The research

The Future of Retirement is a world-

leading independent research study

into global retirement trends,

commissioned by HSBC. It provides

authoritative insights into the key

issues associated with ageing

populations and increasing life

expectancy around the world.

This report, Generations and

journeys, is the 13th in the series

and represents the views of 18,207

people in 17 countries and

territories.

Since The Future of Retirement

programme began in 2005, more

than 159,000 people have been

surveyed worldwide.

About HSBC

The Future of Retirement Generations and journeys

The Future of Retirement is a world-

leading independent research study

into global retirement trends,

commissioned by HSBC. It provides

authoritative insights into the key

issues associated with ageing

populations and increasing life

expectancy around the world.

This report, Generations and

journeys, is the 13th in the series

and represents the views of 18,207

people in 17 countries and

territories.

Since The Future of Retirement

programme began in 2005, more

than 159,000 people have been

surveyed worldwide.

The research

Information and/or opinions

provided within this report

constitute research information

only and do not constitute an

offer to sell, or solicitation of an

offer to buy any financial

services and/or products, or

any advice or recommendation

with respect to such financial

services and/or products.

Legal

The Future of Retirement Generations and journeys

© HSBC Holdings plc 2016

All rights reserved.

Excerpts from this report may be used or quoted, provided

they are accompanied by the following attribution:

‘Reproduced with permission from The Future of Retirement

Generations and journeys, published in 2016 by HSBC

Holdings plc.’

HSBC is a trademark of HSBC Holdings plc and all rights in

and to HSBC vest in HSBC Holdings plc. Other than as

provided above, you may not use or reproduce the HSBC

trademark, logo or brand name.

Published by HSBC Holdings plc, London

www.hsbc.com > Retail Banking and Wealth Management

HSBC Holdings plc

8 Canada Square, London E14 5HQ

The research

The Future of Retirement is a world-

leading independent research study

into global retirement trends,

commissioned by HSBC. It provides

authoritative insights into the key

issues associated with ageing

populations and increasing life

expectancy around the world.

This report, Generations and

journeys, is the 13th in the series

and represents the views of 18,207

people in 17 countries and

territories.

Since The Future of Retirement

programme began in 2005, more

than 159,000 people have been

surveyed worldwide.

Copyright