genoteerd - loyens & loeffcdn.loyensloeff.com/media/4041/genoteerd_84_engels.pdf · in domestic...

TRANSCRIPT

2012 Dutch Tax Plan – impact on inbound investments

1. Introduction

On 21 December 2011 the 2012 Tax Plan1 was passed into law, and consequently a large number of tax statutes and regulations have been amended. This issue of Genoteerd sets out the principal changes in the area of inbound investments, i.e. investments by foreign investors in Dutch businesses. The changes relating to the tax liability of non-residents are discussed in paragraph 2. Paragraph 3 then considers the consequences of the introduction of a requirement for cooperative associations to withhold dividend tax. Finally, paragraph 4 discusses some attention points in practice.

2. Liability to corporation tax for non-residents

2.1. IntroductionNon-residents are only subject to corporation tax on income from certain Dutch sources, including taxable income from a substantial interest in a Netherlands resident company within the meaning of Chapter 4 of the Income Tax Act 2001 (‘ITA 2001’).2 Until 1 January 2012, an entity resident outside the Netherlands with a substantial interest in a Netherlands resident entity3 was subject to Dutch corporation tax on income from that substantial interest if the substantial interest did not form part of the foreign entity’s business assets (the ‘Foreign Substantial Interest rule’).

In domestic relationships, on the other hand, there is generally no liability to corporation tax because the participation exemption applies to interests of 5% or more. In principle the participation exemption also applies if the interest is held as an investment rather than as part of a business, provided that the asset test or subject to tax test is met.4

For this reason, on 30 September 2011 the European Commission formally requested the Netherlands to amend the non-resident taxation provision. The European Commission is of the opinion that this provision is not only in violation with EU law on the free movement of capital, but also with the EU Parent-Subsidiary Directive (the ‘Directive’).

1 Act of 22 December 2011 to amend several tax statutes and certain other statutes (Tax Plan 2012), Bulletin of Acts, Orders and Decrees 2011, 639.

2 In short, a substantial interest exists if the foreign entity holds an interest of 5% or more in the Dutch entity.

3 Not being an exempt investment institution within the meaning of article 6a Corporation Tax Act 1969.

4 This test will normally be met in domestic situations.

● Introduction● Liability to corporation tax

for non-residents● Requirement to withhold

dividend tax for cooperative associations

● Attention points in practice

Edition 84 ● March 2012

IN THIS EDITION

G e n o t e e r d1

liability of a third party whereby the foreign entity has no real function. The avoidance test is therefore split into two sub-tests: (i) does the interposition of the foreign entity result in a lower Dutch income tax or dividend withholding tax liability of a third party; and (ii) does the interposed foreign entity have a real function.

Re (i): does the interposition of the foreign entity result in a lower Dutch income tax or dividend withholding tax liability of a third party?

The application of the first sub-test requires a comparison to be made between the situation where the foreign entity holds the interest in the Netherlands resident entity and the situation that the parties directly or indirectly behind the foreign entity held the interest in the Netherlands resident entity directly. This appears to be a fairly mathematical test. If the situation without the interposition of the foreign entity does not result in a higher Dutch income tax or dividend withholding tax claim, then there is no avoidance of Dutch income tax or dividend withholding tax. This can be illustrated by a few simple examples:

Distributions by NL BV to EU Co are not subject to dividend withholding tax, by virtue of the Directive. Without EU Co, the distributions to the foreign individual would be subject to Dutch dividend withholding tax and income tax, assuming that the shares cannot be attributed to

Genoteerd Edition 84 ● March 2012 2

attorneys at law ● tax advisers ● civil law notaries

The Dutch cabinet considered the complete abolition of the Foreign Substantial Interest rule as undesirable, because in practice this rule plays an important role in combatting artificial structures aimed at tax avoidance. For this reason the legislator opted to formulate the anti-avoidance nature of the Foreign Substantial Interest rule more explicitly in the wording of the statutory provision.

2.2. The changes to the Foreign Substantial Interest rule

With effect from 1 January 2012, article 17 para. 3 of the Corporation Tax Act 1969 (‘CTA’) provides that a non-resident will be liable to tax in relation to a substantial interest in a Dutch entity if both of the following conditions are met:(i) the foreign entity holds the substantial interest for the

primary purpose, or one of the primary purposes, of avoiding a Dutch income or dividend withholding tax liability of a third party (the ‘Avoidance Motive’); and

(ii) the substantial interest does not form part of the assets of a business enterprise carried on by the foreign entity.

In situations where the substantial interest forms part of the business enterprise of the foreign entity (see paragraph 2.4), nothing actually changes. Prior to 1 January 2012, these situations were not subject to non-resident taxation either.

If the interest does not form part of the foreign entity’s business assets, a tax liability will only arise if there is an Avoidance Motive.

2.3. The Avoidance MotiveWith effect from 1 January 2012, a further condition for non-resident tax liability has been added, i.e. that the substantial interest in the Dutch company is held for the primary purpose or one of the primary purposes of avoiding a Dutch income tax or dividend withholding tax

Individual

100%

100%

Eu-Co

NL BV

the business assets of the individual. In this example there is therefore both an income tax avoidance motive (‘IT avoidance motive’) and a dividend withholding tax avoidance motive (‘DWT avoidance motive’). The finding of the applicable avoidance motive is relevant for the establishment of the taxable basis for which EU Co as a non-resident should be subject to corporation tax (see paragraph 2.5 below).5

In the above example the question whether there is an Avoidance Motive was answered without taking into account the possible application of a tax treaty between the Netherlands and the country where the individual is resident. In the example below it is assumed that the individual is resident in Belgium.

Distributions by NL BV to EU Co are not subject to Dutch income tax and dividend withholding tax by virtue of the Directive. Without EU Co, distributions by NL BV would be subject to dividend withholding tax at 15%. If the interest in NL BV is not attributable to the business assets of the Belgian resident individual, the individual would also be subject to Dutch income tax because he has a substantial interest in a Dutch company. However, under the tax treaty between the Netherlands and Belgium the Netherlands is not permitted to tax capital gains of a Belgium resident and the right to tax dividends is restricted to 15% of the

Genoteerd Edition 84 ● March 2012 3

attorneys at law ● tax advisers ● civil law notaries

gross amount of the dividends distributed by NL BV to the Belgium resident.

Consequently there is never more income tax due than dividend withholding tax, since the income tax is calculated on a net basis, i.e. the costs attributable to the dividend income can be deducted. In view of the above, there cannot be an IT avoidance motive.6

There can also not be an IT avoidance motive if the individual’s (indirect) interest in NL BV would amount to less than 5%. The reason being that in such situation the individual would not have a substantial interest in a Dutch company. This would be the case if, for example, the individual only holds 4% of EU Co.

An Avoidance Motive also seems to be absent, if the interposed entity is held by a Netherlands resident individual, because such an individual would also be subject to Box II income tax even without the interposition of e.g. an EU Co. In addition, if the interest in NL BV was held directly, the dividend tax withheld from the individual would be fully offsettable against his liability to Dutch income tax.

Re (ii): Does the foreign entity have a real function?If it has been established on the basis of the comparison described above that more dividend withholding tax and/or income tax would be due without the interposition of the foreign resident entity, it is then necessary to assess whether the interposed entity has a real function. In order to answer this question, the parliamentary history indicates that reference has to be made to the European Court of Justice case law on the compatibility of anti-avoidance provisions with EU law which refers to ‘completely artificial arrangements’. According to the parliamentary history, in order to establish whether such arrangements exist, it is necessary to assess whether the economic reality

5 Under the rules that applied until 1 January 2012, EU Co was in principle subject to tax as a non-resident if the interest in NL BV was not attributable to the assets of a business enterprise. However, it could be derived from the Parliamentary history that under the Directive the Netherlands could not enforce its right to tax except in cases of abuse and fraud.

6 The analysis would be no different if the individual held the interest in EU Co indirectly via another company, since it is in principle necessary to look through the other company in determining the Avoidance Motive. This would only be different if the interposed entity fulfilled a real function.

Individual (Belgium)

100%

100%

Eu-Co

NL BV

Genoteerd Edition 84 ● March 2012 4

attorneys at law ● tax advisers ● civil law notaries

The first question that has to be answered is when something is a business enterprise. For this purpose it is not necessary for the foreign resident shareholder to be carrying on a business in a material sense.7 It should be enough for the foreign shareholder to have the intention to hold the interest other than as an investment. This is the case if the interest is not held with a view to obtaining a return which can be expected from normal asset management.

The follow-up question is whether the interest in the Dutch entity is attributable to the business enterprise of the foreign entity. For example, a substantial interest is attributable to the business assets of the foreign shareholder if the business of the Dutch entity is an extension of the business of the foreign shareholder. Also if the foreign shareholder is a holding company which fulfils a genuine function in the conduct of the group’s business, it will not hold the interest as an investment. This applies both to a foreign top holding company and to a foreign sub-holding company which fulfils an intermediary function. As regards structures in which foreign private equity funds are involved, a practical framework has been developed in the ruling practice of the Dutch Tax Authorities. In this framework the deciding criterion for the question whether an interest is attributable to business assets is whether the management of the fund is actively involved with the management of the Dutch entity and its participations.

2.5. Tax baseThe tax base for the Foreign Substantial Interest Rule depends on the applicable Avoidance Motive. This is intended to achieve a greater link between corporation tax and the tax which is avoided.

If it has been established on the basis of the framework described above that there is an IT avoidance motive, then the Dutch income is set at the income from a substantial

is consistent with the legal form. The objective elements for assessing the economic reality include the place of effective management, the tangible presence of the place of business in the foreign country and the real risk incurred by the interposed foreign entity. The parliamentary history gives as clarification the example of a ‘pooling structure’ (bundelingsstructuur) where portfolio interests of foreign investors in Dutch companies are held via a single foreign entity in order to avoid Netherlands dividend withholding tax. Such a structure will be labelled as completely artificial if, for example, the foreign entity does not have enough qualified staff with sufficient powers in relation to the holding of the interest in the Dutch companies.

Qualified staff is an indication that there is a real function. Indications of a real function are for example also present if the foreign entity functions as an investment platform and does not only hold the interest in the Dutch entity, or if the foreign entity is used as a joint venture company.

According to the parliamentary history, however, the Avoidance Motive must not be applied too restrictively. The existence of some kind of (possibly incidental) non-tax motive in itself does not necessarily mean that there cannot be a completely artificial arrangement which is aimed at avoiding the tax which would normally be due. An incidental non-tax aspect of the pooling structure described above, for example, is that the shareholders of the interposed entity can combine their voting rights in the Dutch entity. It is, however, uncertain whether this would be considered as a sufficient non-tax motive.

2.4. Attributable to business assetsThe substantial interest will not be subject to tax if the interest is attributable to the business assets of the foreign resident shareholder. According to the parliamentary history, in answering this question similar criteria apply as in relation to the motive test for the purposes of the participation exemption.

7 A material business is present if there is an organisation of capital and labour which participates in economic life with the intention and reasonable expectation of realising a profit.

Genoteerd Edition 84 ● March 2012 5

attorneys at law ● tax advisers ● civil law notaries

2.7. Taxation of interest on substantial interest claims A foreign entity with a substantial interest in a Dutch resident company is also subject to tax on any receivable it has on that company. Until 1 January 2012 an exemption applied if the party entitled to the receivable was resident in another EU Member State and certain further conditions were met. As a result of the change to the substantial interest rules the legislator now assumes that there will only be a taxable substantial interest in certain cases of abuse. Consequently the legislator has abolished the above mentioned tax exemption whereby in case of abuse9, a tax will be levied on interest from receivables also from (certain) EU entities.

2.8. Burden of proofIn the parliamentary history the comment was made that the so-called free evidence rule (vrije bewijsleer) applies in relation to the Foreign Substantial Interest rule. In the first instance it is therefore up to the tax inspector to argue that the Foreign Substantial Interest rule applies. If the foreign entity sufficiently argues against this position, the inspector has to demonstrate that the interest is held for the primary purpose or one of the primary purposes of avoiding Dutch income tax or dividend withholding tax and that the interest does not form part of the assets of a business. Because the foreign entity is assumed to have access to the facts underlying this analysis, the entity cannot take a passive approach in this respect.

2.9. Implementation and transitionsThe amended legislation relating to the Foreign Substantial Interest Rule came into force on 1 January 2012. It does not include any transitional rules. This raises the question whether a foreign entity which was subject to tax under the old law but is no longer subject to tax under the new law is faced with a final tax levy as a result of this transition. This does not appear to be the case. However this does not necessarily means that the latent tax claim for the period up to the end of 2011 has disappeared. If a capital gain is realised after the enactment of the amendments, the tax

interest as referred to in chapter 4 of the ITA 2001. This covers both regular income (including dividends) and capital gains. It means this income is considered at a net basis, so any costs attributable to the income are in principle deductible.

If the substantial interest is held by the foreign entity to avoid dividend withholding tax, the corporation tax charge is set at 15% of the dividends8 within the meaning of the Dividend Withholding Tax Act 1965 (‘DWTA’). The 15% rate is achieved by only taking into account a proportionate part of the taxable income.

An example to illustrate this: the income from the Dutch entity is 250, consisting of a dividend of 100 which qualifies as a profit within the meaning of the DWTA, a capital gain of 200 and costs attributable to the income of 50. On the assumption that there is only a DWT avoidance motive, only the dividend is subject to tax. Assuming a corporation tax rate of 25%, 60 (15/25 x 100) will be taken into account as income from a substantial interest. This 60 is taxed at 25%, which in this example results in a tax liability of 15 (so effectively 15% of the gross dividend of 100). Neither the capital gain nor the costs are therefore relevant for the taxation in this example. If the same substantial interest was held with an IT avoidance motive, a tax liability of 62.5 would arise (25% of 250).

2.6. Treaty application If it has been established that the non-resident is liable to tax, this does not automatically mean that tax will actually be levied, since the foreign entity may be able to invoke a tax treaty between the Netherlands and its country of residence. For example, in the majority of the Dutch tax treaties the right to tax capital gains on shares is allocated to the country of residence instead of the source country. For dividends, in a number of cases the Netherlands reduces its dividend withholding taxation rights for holdings of at least 25%. However, this varies from treaty to treaty.

8 I.e. not the income from a substantial interest within the meaning of chapter 4 ITA 2001.9 It is unclear whether interest on a substantial interest claim only gives rise to a tax charge where there is an IT avoidance motive, or also

where there is only a DWT avoidance motive. Technically the cleanest solution would be for tax only to be charged on interest relating to a substantial interest if there is an IT avoidance motive, since the DWT avoidance motive only relates to income which qualifies as a dividend.

Genoteerd Edition 84 ● March 2012 6

attorneys at law ● tax advisers ● civil law notaries

3.2.1. Interest in a foreign entityIf a cooperative association holds an interest11 in a foreign company, it will be required to withhold tax if both of the following criteria are met:(i) the cooperative association holds the interest in the

foreign company for the primary purpose or one of the primary purposes of avoiding the foreign tax liability of a third party and the cooperative association has no real function the ‘Avoidance Motive’); and

(ii) the membership right in the cooperative association does not form part of the assets of a business enterprise.

The Avoidance Motive for cooperative associations is also divided into two sub-tests. There must (a) be less foreign tax (or withholding tax) due with the interposition of the cooperative association, and (b) the cooperative association must not fulfil any real function.

Re (a): Is less foreign tax due as a result of the interposition of the cooperative association?

The first part of the Avoidance Motive can again be tested mathematically. If the members of a cooperative association would be liable to more foreign tax if they participated directly in the foreign entity, then the first part of the test is met. This can be clarified by an example:

authorities may still try to tax the capital gain by invoking the so called ‘compartimentalisation theory’.

The reverse situation, i.e. a becoming subject to non-resident taxation as a result of the amendments, is not very likely to arise, as in principle non-residents are less likely to be subject to Dutch corporate income tax after 1 January 2012.

If there is only a DWT avoidance motive, then in view of the absence of any transitional rules no distinction will be drawn between distributions from old or new profits when dividends are paid. These distributions will therefore be subject to tax at a rate of 15%.

3. Requirement to withhold dividend tax for cooperative associations

3.1. IntroductionUntil 1 January 2012 distributions made by a cooperative association without a capital divided into shares were not subject to dividend withholding tax. This is still the starting position after 1 January 2012. However, with effect from 1 January 2012 a cooperative association will be required to withhold dividend tax from distributions to certain members in situations involving abuse.

Unlike the position in relation to non-residents’ liability to tax, the percentage of the interest in the cooperative association held by a particular member is irrelevant. A requirement to withhold tax may therefore also arise in relation to distributions to members with an interest of less than 5%.

3.2. The Avoidance MotiveIn order to answer the question whether a situation exists which gives rise to a dividend withholding tax charge, a distinction has to be made between the situation where a cooperative association holds an interest in a foreign entity and the situation where a cooperative association holds an interest in a Dutch entity.10

10 This distinction is slightly different from the distinction made in the wording of the legislation, but effectively comes down to the same.11 This can be an interest in the form of shares, profit-sharing certificates or loans which function as equity for Dutch tax purposes.

10% 4%

Coop

BE BVBA

Eu-Co Tax Haven

Genoteerd Edition 84 ● March 2012 7

attorneys at law ● tax advisers ● civil law notaries

it serves as an active investment platform or has sufficient qualified staff.

If it has been established that there is an Avoidance Motive and the cooperative association has no real function, then dividend tax will have to be withheld unless the relevant member can attribute its membership rights to the assets of its business. We refer to paragraph 2.4 above for the question whether a membership right can be attributed to the assets of a business.

If the cooperative association is required to withhold tax in relation to a particular member, all distributions by the cooperative association to that member are subject to dividend withholding tax. In this respect, it is not relevant to which period the profits out of which the dividends are paid relate.

3.2.2. Interest in a Dutch entityIf a cooperative association holds an interest13 in a Netherlands resident company, a distinction has to be drawn between (a) the situation where the membership right is not attributable to business assets and (b) the situation where this is the case.

Re (a): Interest is not attributable to business assetsIn this situation dividend tax has to be withheld if the cooperative association holds the interest in the Dutch company for the primary purpose or one of the primary purposes of avoiding a Dutch dividend tax liability of a third party and the cooperative association does not fulfil any real function.

As regards the question whether there is an Avoidance Motive, a comparison again has to be made between the situation with the cooperative association and the situation without it. If more Dutch withholding tax is due without the interposition of the cooperative association, then the first part of the Avoidance Motive is met (see also the examples above).

Without the cooperative association, EU Co would hold an interest of 10% in the Belgian company and distributions by BE BVBA to EU Co would not be subject to Belgian dividend withholding tax by virtue of the Directive. To this extent EU Co therefore does not need the cooperative association and there is no Avoidance Motive.12 Distributions by the cooperative association to EU Co are therefore not subject to dividend withholding tax. Because it is necessary to assess for each member whether distributions by the cooperative association should be subject to dividend withholding tax, it is further necessary to assess whether Tax Haven is better off from a tax perspective with the cooperative association.

Without the cooperative association, Tax Haven would hold an interest of 4% in the Belgian company. Distributions by the Belgian company to Tax Haven would be subject to dividend withholding tax. However, distributions by the cooperation are – in principle – not subject to dividend withholding tax. Tax Haven is therefore better off as a result of the interposition of the cooperative association and consequently there is an Avoidance Motive to this extent. Distributions by the cooperative association to Tax Haven are therefore subject to dividend withholding tax unless (i) the cooperative association has a real function or (ii) the interest in the cooperative association is attributable to the business assets of Tax Haven.

Re (b): Does the cooperative association have a real function?

If it has been established that there is an Avoidance Motive, it is necessary to assess whether the cooperative association has a real function. The same test has to be applied for this question as described above in paragraph 2.3(ii) in relation to non-residents’ tax liability. Unlike the approach in relation to non-residents’ liability to tax, the test whether there is a real function is applied at the level of the cooperative association and not at the level of the foreign members of the cooperative association. It can be argued that a cooperative association has a real function if

12 However, a liability to Dutch corporation tax may arise (under the IT avoidance motive) if EU Co is held by 1 or 2 individuals whose (indirect) interest in Coop would amount to at least 5%.

13 This can be an interest via shares, profit-sharing certificates or loans which are treated as equity for Dutch tax purposes. The interest can be direct or indirect.

Genoteerd Edition 84 ● March 2012 8

attorneys at law ● tax advisers ● civil law notaries

However, it is not necessary to withhold dividend tax in the situation described above for all profits distributed by the cooperative association to the relevant member, but in short only to the extent that this is necessary to preserve the dividend withholding tax claim which would be avoided by the interposition of the cooperative association. This applies on a FIFO (first in first out) basis. The profits that are already present in the Dutch entity are therefore deemed to be distributed first by the cooperative association (i.e. they are taxable). The FIFO basis is limited to distributions by the cooperative association which are derived from profits reserves of Dutch entities to which a tax claim applies.

3.3. Tax liability and requirement to withhold tax achieved by various assimilations

As indicated above, the requirement to withhold dividend tax is determined per member of the cooperative association. It is therefore limited to distributions to specific members. The tax liability of the member and the requirement to withhold tax for the cooperative association are achieved by treating the membership right as equivalent to a share and the cooperative association as equivalent to a company with a capital divided into shares. This assimilation has the result that the capital contributed on the membership interests is taken into account in determining the profits which are subject to dividend tax. In summary, this means that dividend tax has to be withheld on all distributions which exceed the capital contributed on the membership rights. However, this assimilation does not go so far as to recognise a nominal value for the membership rights. It is therefore not possible for the capital contributed on the membership rights to be repaid tax-free by reducing the nominal value.

If it has been established that a cooperative association is required to withhold dividend tax, the association cannot invoke the exemptions from withholding tax under articles 4(1) and 4(2) DWTA. This reflects the legislator’s wish to be able to actually levy tax in abuse situations.

If a foreign shareholder contributes shares in a Dutch company which has profit reserves into a cooperative association owned by that shareholder, then, in addition to the application of the new legislation described above, this may also trigger certain anti-abuse provisions in relation to dividend stripping. This possible overkill was recognised in the parliamentary history and it was confirmed that if the dividend stripping rules have been applied there will no longer be an Avoidance Motive to that extent.

If it has been established that a particular member of the cooperative association has an Avoidance Motive, it will then have to be ascertained whether the cooperative association fulfils a real function (see above). If the cooperative association does not have a real function, distributions by the cooperative association to the relevant member will be subject to dividend withholding tax.

Re (b): Interest is attributable to business assets If the interest in the cooperative association is attributable to the assets of a business enterprise, the cooperative association will have to withhold dividend tax if both of the following conditions are met:(i) the cooperative association holds the interest in

the Dutch company for the primary purpose or one of the primary purposes of avoiding the Dutch dividend withholding tax liability of a third party and the cooperative association does not fulfil any real function; and

(ii) the Dutch company acquired by the cooperative association has freely distributable reserves at the time of its acquisition by the cooperative association.

The test whether an Avoidance Motive and a real function exist is the same as described above. For the question whether there is an Avoidance Motive, the dividend withholding tax position of the selling party also has to be reviewed, at least where the acquisition is from a third party. If there is no existing claim to Dutch dividend withholding tax, then no Dutch dividend withholding tax is avoided by interposing the cooperative association.14

14 Consider e.g. the situation where a BV with profit reserves was held by another BV which applied the participation exemption.

Genoteerd Edition 84 ● March 2012 9

attorneys at law ● tax advisers ● civil law notaries

new rules also apply to existing situations. This can be illustrated by the following example mentioned in the parliamentary history:

In 2007 a cooperative association acquires a Dutch company with retained profits of 100. In the years after 2007 the company pays an annual dividend of 20. As a result of the introduction of the requirement for cooperative associations to withhold dividend tax, with effect from 1 January 2012 distributions by the cooperative association which are derived from the Dutch company are subject to dividend withholding tax up to an amount of 100. This is despite the fact that the Dutch company has already distributed an amount equal to the reserves covered by the claim (albeit without dividend withholding tax) in the years 2007-2011.

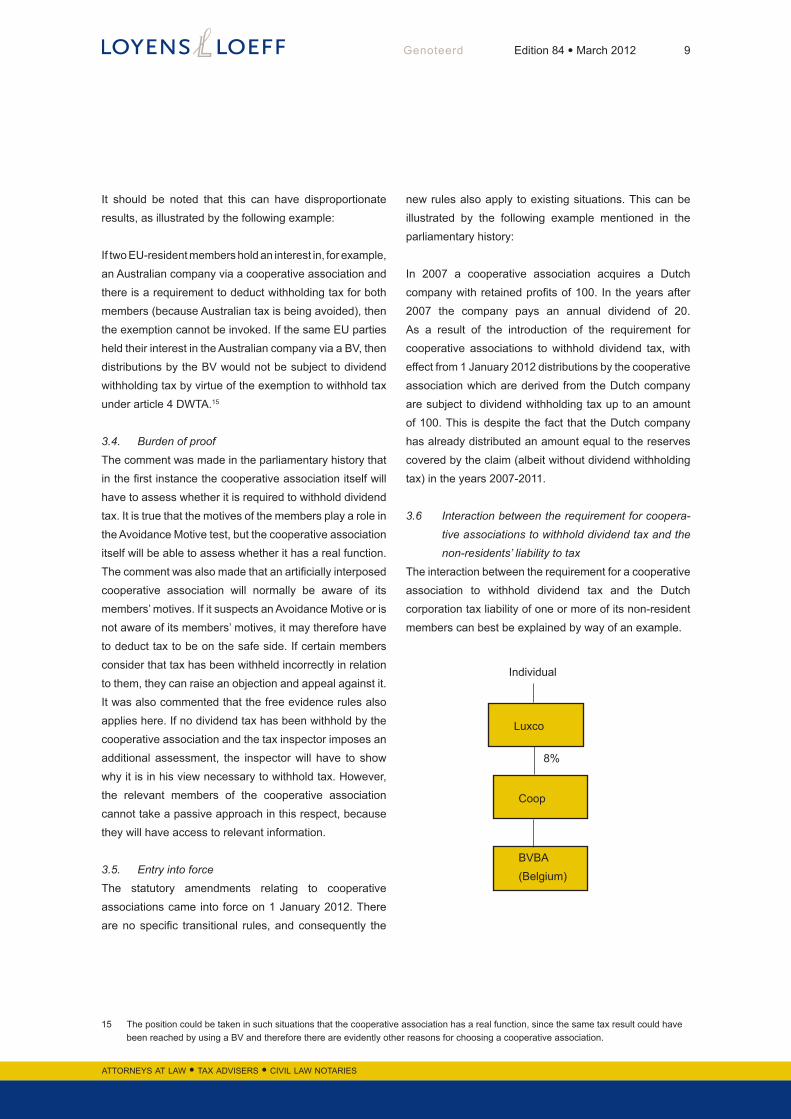

3.6 Interaction between the requirement for coopera-tive associations to withhold dividend tax and the non-residents’ liability to tax

The interaction between the requirement for a cooperative association to withhold dividend tax and the Dutch corporation tax liability of one or more of its non-resident members can best be explained by way of an example.

It should be noted that this can have disproportionate results, as illustrated by the following example:

If two EU-resident members hold an interest in, for example, an Australian company via a cooperative association and there is a requirement to deduct withholding tax for both members (because Australian tax is being avoided), then the exemption cannot be invoked. If the same EU parties held their interest in the Australian company via a BV, then distributions by the BV would not be subject to dividend withholding tax by virtue of the exemption to withhold tax under article 4 DWTA.15

3.4. Burden of proofThe comment was made in the parliamentary history that in the first instance the cooperative association itself will have to assess whether it is required to withhold dividend tax. It is true that the motives of the members play a role in the Avoidance Motive test, but the cooperative association itself will be able to assess whether it has a real function. The comment was also made that an artificially interposed cooperative association will normally be aware of its members’ motives. If it suspects an Avoidance Motive or is not aware of its members’ motives, it may therefore have to deduct tax to be on the safe side. If certain members consider that tax has been withheld incorrectly in relation to them, they can raise an objection and appeal against it. It was also commented that the free evidence rules also applies here. If no dividend tax has been withhold by the cooperative association and the tax inspector imposes an additional assessment, the inspector will have to show why it is in his view necessary to withhold tax. However, the relevant members of the cooperative association cannot take a passive approach in this respect, because they will have access to relevant information.

3.5. Entry into forceThe statutory amendments relating to cooperative associations came into force on 1 January 2012. There are no specific transitional rules, and consequently the

15 The position could be taken in such situations that the cooperative association has a real function, since the same tax result could have been reached by using a BV and therefore there are evidently other reasons for choosing a cooperative association.

8%

Coop

BVBA(Belgium)

Luxco

Individual

Genoteerd Edition 84 ● March 2012 10

attorneys at law ● tax advisers ● civil law notaries

4. Attention points in practice

In situations where a substantial interest forms part of the business assets of the foreign entity, the amendments to the legislation have not changed anything. To acknowledge this, it has been expressly confirmed a number of times in the parliamentary history that the new legislation is not intended to change the current (ruling) practice.

However, the new legislation may have consequences for settlement agreements which were concluded under the old ruling practice but can no longer be obtained under the current policy. Although such agreements will be respected for the term of the settlement agreement, according to the parliamentary history, such a situation is likely to result in a non-resident becoming liable to tax with effect from the expiry of the agreement.

As regards the changes relating to cooperative associations, the starting point remains that distributions are in principle not subject to dividend withholding tax. Because there was no requirement to deduct withholding tax before 1 January 2012, the potential tax liability under the new rules will have to be checked for all structures.

For members of cooperative associations for whom the membership right forms part of the assets of a business, which will be the case for many active funds, the change will not be relevant if only direct and indirect interests in foreign companies are held. For such members the change is only relevant if directly or indirectly held Dutch companies with existing profit reserves subject to a tax claim have been brought under the cooperative association. For members of cooperative associations for whom the membership right does not form part of the assets of a business, the change is relevant. However, it is doubtful

First of all it is necessary to assess whether the cooperative association is required to withhold dividend tax. In order to do this the cooperative association has to be disregarded. If the Luxembourg resident Luxco participated directly in BVBA, then Belgian dividend withholding tax would have been due on distributions by BVBA. This means that the first part of the Avoidance Motive applies. It is then necessary to assess the extent to which the cooperative association has a real function and the extent to which the membership right of LuxCo is attributable to the assets of a business. If there is no real function and the membership right is not attributable to the assets of a business, then the cooperative association is required to withhold dividend tax on the distributions at a rate of 15% (although this is reduced to 2.5% under the Netherlands – Luxembourg treaty). Further it is necessary to assess whether Luxco will be liable to Dutch tax as a non-resident. Without Luxco the individual would hold an interest of more than 5% in the cooperative association. There is therefore an IT avoidance motive.16 If Luxco has no real function (and the membership right is not attributable to the assets of a business), distributions by the cooperative association to Luxco will be subject to corporation tax.

However, by virtue of the treaty with Luxembourg the tax on these distributions is limited to 2.5% of the gross dividends distributed to Luxco. The dividend withholding tax withheld by the cooperative association is fully offsettable against the Dutch corporation tax due by Luxco. If the corporation tax due amounts to less than 2.5% of the gross dividend (e.g. because there are financing costs attributable to the dividend) then the excess dividend tax withheld will be refunded. For example, assuming a gross dividend of 100 and attributable costs of 92, the Netherlands will withhold dividend tax of 2.5 and a corporation tax liability of 2 (25% x (100 – 92)) will arise. Luxco will then be entitled to a refund of the excess dividend withholding tax of 0.5.

16 There is no DWT avoidance motive, as distributions by the cooperative association to Luxco are also subject to dividend withholding tax.

Genoteerd Edition 84 ● March 2012 11

attorneys at law ● tax advisers ● civil law notaries

whether many of such situations exist, because in most of such cases this structure was already not attractive because of the substantial interest tax liability to which such shareholders were also subject prior to the amendments (obviously except where treaty protection applied).

Members with an interest of less than 5% in a cooperative association are – as was the case under the legislation that applied until 1 January 2012 – not liable to corporation tax. These members will not have been deterred by a potential corporation tax liability and will not yet have considered their position (whether they are entrepreneurs or passive investors). Given that a requirement to withhold dividend tax can also arise for these members with effect from 1 January 2012, it is advisable to check the extent to which this is the case.

Genoteerd Edition 84 ● March 2012 12

AMSTERDAM • ARNHEM • BRUSSELS • EINDHOVEN • LUXEMBOURG • ROTTERDAM • ARUBA • CURAÇAODUBAI • FRANKFURT • GENEVA • HONG KONG • LONDON • NEW YORK • PARIS • SINGAPORE • TOKYO • ZURICH

Loyens & Loeff N.V. is an independent full service firm of civil lawyers, tax advisors and notaries, where civil law and tax services are provided on an integrated basis. The civil lawyers and notaries on the one hand and the tax advisors on the other hand have an equal position within the firm. This size and purpose make Loyens & Loeff N.V. unique in the Benelux countries.

The practice is primarily focused on the business sector (national and international) and the public sector. Loyens & Loeff N.V. is seen as a firm with extensive knowledge and experience in the area of, inter alia, tax law, corporate law, mergers and acquisitions, stock exchange listings, privatisations, banking and securities law, commercial real estate, employment law, administrative law, technology, media and procedural law, EU and competition, construction law, energy law, insolvency, environmental law, pensions law and spatial planning.

Over 1600 people work at Loyens & Loeff N.V., including over 900 civil lawyers, tax advisors and notaries. The firm has six offices in the Benelux countries and twelve in important financial centres of the world.

DisclaimerAlthough this publication has been compiled with great care, Loyens & Loeff N.V. and all other entities, partnerships, persons and practices trading under the name ‘Loyens & Loeff’, cannot accept any liability for the consequences of making use of this issue without their cooperation. The information provided is intended as general information and cannot be regarded as advice.

www.loyensloeff.com

GenoteerdGenoteerd is a periodical newsletter for contacts of Loyens & Loeff N.V. Genoteerd has been published since October 2001.

The authors of this issue are: M.M. Wierenga ([email protected]) and M. Kangarani ([email protected]).

This newsletter is also available in electronic form, in both Dutch and English. Orders/additional orders can be obtained via [email protected].

Editors:M.W. den BoogertE.H.J. HendrixA.N. Krol W.J. OostwouderA.J.A. StevensA.C.J. ViersenD.F.M.M. Zaman

You can of course also approach your own contact person within Loyens & Loeff N.V.

Please click here to unsubscribe from this mailing. Please click here to unsubscribe from all Loyens & Loeff electronic publications